No securities regulatory authority has expressed an opinion about these securities and it is an offence to claim otherwise. This short form prospectus constitutes a public offering of these securities only in those jurisdictions where they may be lawfully offered for sale and therein only by persons permitted to sell such securities. These securities have not been and will not be registered under the United States Securities Act of 1933, as amended (the “U.S. Securities Act”), or any state securities laws. Accordingly, these securities may not be offered or sold in the United States except in certain transactions exempt from the registration requirements of the U.S. Securities Act and applicable state securities laws. This short form prospectus does not constitute an offer to sell, or a solicitation of an offer to buy, any of these securities within the United States. See “Plan of Distribution”.

Information has been incorporated by reference in this prospectus from documents filed with the securities commissions or similar authorities in Canada. Copies of the documents incorporated herein by reference may be obtained on request without charge from the Secretary, Mala Noche Resources Corp., 1500 — 885 West Georgia Street, Vancouver, British Columbia, V6C 3E8 (Telephone (604) 895-7450), and are also available electronically at www.sedar.com.

SHORT FORM PROSPECTUS

| New Issue | July 9, 2010 |

MALA NOCHE RESOURCES CORP.

(To be renamed “PRIMERO MINING CORP.”)

$300,000,000

50,000,000 Subscription Receipts

This short form prospectus (the “Prospectus”) qualifies the distribution (the “Offering”) of 50,000,000 subscription receipts (“Subscription Receipts”) of Mala Noche Resources Corp. (“Mala Noche” or the “Company”) at a price of $6.00 per Subscription Receipt (the “Offering Price”) pursuant to the terms of an underwriting agreement dated July 9, 2010 (the “Underwriting Agreement”) among Canaccord Genuity Corp. (“Canaccord Genuity”), GMP Securities L.P., BMO Nesbitt Burns Inc., CIBC World Markets Inc., Scotia Capital Inc., TD Securities Inc., Merrill Lynch Canada Inc., Cormark Securities Inc., Dundee Securities Corporation, Mackie Research Capital Corporation, National Bank Financial Inc., Paradigm Capital Inc. and RBC Dominion Securities Inc. (the “Underwriters”) and the Company. The Offering Price of the Subscription Receipts was determined by negotiation between the Company and Canaccord Genuity on behalf of the Underwriters.

Each Subscription Receipt will entitle the holder thereof to receive, without payment of additional consideration, one unit of the Company (each, a “Unit”) upon closing of the acquisition (the “Acquisition”) by the Company of the San Dimas mines and related assets as described in more detail under “Acquisition of the San Dimas Mines”. The proceeds from the sale of the Subscription Receipts (the “Escrowed Funds”) will be held by Computershare Trust Company of Canada, as escrow agent (the “Escrow Agent”), and invested in short-term obligations of, or guaranteed by, the Government of Canada pending completion of the Acquisition. Upon the Acquisition being completed on or before the date that is 60 days from the date of completion of the Offering, the Escrowed Funds and the interest thereon will be released to the Company and each holder of Subscription Receipts will receive one Unit for each Subscription Receipt held. The Company will utilize the Escrowed Funds to pay the cash portion of the purchase price for the Acquisition, with the balance of the Escrowed Funds being applied to working capital.

Each Unit will consist of one post-consolidation common share of the Company (each, a “Common Share”) and 0.4 of one common share purchase warrant (each whole common share purchase warrant, a “Warrant”). Each Warrant will entitle the holder thereof to purchase one additional post-consolidation Common Share at a price of $8.00 per post-consolidation Common Share for a period of five years after the date of closing of the Offering. See “Details of the Offering — Warrants”. This Prospectus also qualifies the distribution of the Units, the underlying Common Shares and the Warrants.

The agreement governing the proposed Acquisition provides that the closing of the Acquisition is to be completed by July 30, 2010, subject to any extension agreed upon by the parties. If the closing of the Acquisition does not take place by the date that is 60 days from the date of completion of the Offering, if the Acquisition is terminated at any earlier time or if the Company has advised the Underwriters or announced to the public that it does not intend to proceed with the Acquisition (in each case, the “Termination Time”), holders of Subscription Receipts will be entitled to receive an amount equal to the full subscription price paid and to interest on such amount. The Escrowed Funds will be applied towards payment of such amount. See “Details of the Offering”.

Investing in the Subscription Receipts and other securities of the Company involves risk. Prospective investors should consider the risk factors described under “Risk Factors” and in the documents incorporated by reference into this Prospectus. In particular, prospective investors should be aware that the acquisition of the San Dimas mines and related assets is being completed on the understanding that the representations and warranties and indemnities to be provided by the San Dimas Vendors (as defined herein) in respect of the San Dimas mines and related assets will be limited. Consequently, the recourse the Company may have against the San Dimas Vendors will be limited.

__________________________________

Price $6.00 per Subscription Receipt

__________________________________

| Price to the | Underwriters’ | Net Proceeds to | |||

| Public | Fee(1) | the Company(2) | |||

| Per Subscription Receipt | $6.00 | $0.33 | $5.67 | ||

| Total(3) | $300,000,000 | $16,500,000 | $283,500,000 |

_______________

Notes:

| (1) | Pursuant to the terms of the Underwriting Agreement, the Underwriters will receive a fee (the “Underwriters’ Fee”) equal to 5.5% of the gross proceeds of the Offering (excluding proceeds not to exceed $20,000,000 in total from purchasers introduced to the Underwriters by the Company, see “Plan of Distribution — Underwriting Agreement” for which the Underwriters will only receive a fee in the amount of 2.75%) upon the satisfaction of the escrow release conditions set out under “Details of the Offering”. In addition, the Company has agreed to issue to the Underwriters at the closing of the Offering special warrants (the “Broker Special Warrants”) which will automatically convert into non- transferable common share purchase warrants (the “Broker Warrants”) upon the release from escrow of the Escrowed Funds. On a post-consolidation basis, the Broker Warrants will entitle the Underwriters to purchase up to 500,000 Common Shares (the “Broker Shares”) at a price of $6.00 per Broker Share until the date that is 18 months from the date of the closing of the Acquisition. |

| (2) | Before deducting the expenses of the Offering, estimated to be $3,650,000. |

| (3) | The Company has granted to the Underwriters an option (the “Over-Allotment Option”) to purchase up to an additional 7,500,000 Subscription Receipts at a price of $6.00 per Subscription Receipt on the same terms and conditions as the Offering, exercisable in whole or in part from time to time, not later than the earlier of (i) the 30th day following the closing of the Offering, and (ii) the Termination Time, for the purposes of covering the Underwriters’ over- allocation position, if any. If the Over-Allotment Option is exercised in whole or in part following the closing of the Acquisition, an equal number of Units will be issued in lieu of Subscription Receipts. If the Over-Allotment Option is exercised in full, the Purchase Price to the Public, Underwriters’ Fee and Net Proceeds to the Company (before deducting expenses of the Offering) will be $345,000,000, $18,975,000 and $326,025,000, respectively. This Prospectus also qualifies for distribution the grant of the Over-Allotment Option and the issuance of Subscription Receipts and Units pursuant to the exercise of the Over-Allotment Option. See “Plan of Distribution” and the table below. A person who acquires Subscription Receipts or Units forming part of the Underwriters’ over-allocation position, acquires such Subscription Receipts or Units under this Prospectus regardless of whether the over-allocation position is ultimately filled through the exercise of the Over-Allotment Option or secondary market purchases. |

The following table sets out the securities issuable to the Underwriters:

| Underwriters’ Position | Maximum Size or Number of Securities Available | Exercise Period or Acquisition Date | Exercise Price or Average Acquisition Price | ||

| Over-Allotment Option(1) | Option to acquire up to 7,500,000 Subscription Receipts | Exercisable for a period of 30 days after the closing of the Offering | $6.00 per Subscription Receipt | ||

| Broker Warrant(2) | Option to acquire up to 500,000 common shares | Exercisable for a period of 18 months after the closing of the Acquisition | $6.00 per common share | ||

| Any other option granted by Mala Noche or insiders of Mala Noche | Nil | n/a | n/a | ||

| Total securities under option issuable to Underwriters | 8,000,000 | — | — | ||

| Other compensation securities issuable to Underwriters | Nil | n/a | n/a |

_______________

Notes:

| (1) | If the Over-Allotment Option is exercised in whole or in part following the closing of the Acquisition, an equal number of Units will be issued in lieu of Subscription Receipts at the same Offering Price. |

| (2) | This Prospectus also qualifies the distribution of the Broker Special Warrants. See “Plan of Distribution”. |

The Underwriters, as principals, conditionally offer the Subscription Receipts, subject to prior sale, if, as and when issued by the Company and accepted by the Underwriters in accordance with the conditions contained in the Underwriting Agreement referred to under “Plan of Distribution” and subject to approval of certain legal matters relating to the Offering on behalf of the Company by Lang Michener LLP and on behalf of the Underwriters by Blake, Cassels & Graydon LLP.

ii

Immediately before the completion of the Acquisition the Company intends to consolidate its Common Shares on the basis of one new Common Share of the Company for every 20 pre-consolidation Common Shares (the “Consolidation”). The issued and outstanding Common Shares are listed on the TSX Venture Exchange (the “TSXV”) under the trading symbol “MLA”. On July 8, 2010, the closing price of the Common Shares on the TSXV was $0.235 ($4.70 assuming the completion of the Consolidation).

Canaccord Genuity acted as the Company’s financial advisor with respect to the acquisition of the San Dimas mines. Canaccord Genuity is entitled to receive a fee, payable in additional Common Shares, which is conditional on completion of the Acquisition. In addition to the success fee, Canaccord Genuity is also entitled to receive a fee which is not conditional upon the completion of the Acquisition, in connection with the delivery of an opinion to the board of directors of the Company as to whether the purchase price for the San Dimas mines and related assets is fair, from a financial point of view, to the current shareholders of the Company. Consequently, the Company may be considered to be a “connected issuer” of Canaccord Genuity within the meaning of National Instrument 33-105 —Underwriting Conflicts. See “Plan of Distribution” and “Relationship Between Issuer and Underwriter”.

There is no market through which the Subscription Receipts or Warrants may be sold and purchasers may not be able to resell Subscription Receipts or Warrants purchased under this Prospectus. This may affect the pricing of the Subscription Receipts and Warrants in the secondary market, the transparency and availability of trading prices, the liquidity of the Subscription Receipts and Warrants, and the extent of issuer regulation. See “Risk Factors”. The TSXV has conditionally approved the listing of the Subscription Receipts and the Common Shares forming part of the Units and the Common Shares issuable upon exercise of the Warrants forming part of the Units, subject to the Company fulfilling all of the requirements of the TSXV including distribution requirements. The Toronto Stock Exchange (the “TSX”) has conditionally approved the listing of the Common Shares and Warrants forming part of the Units and the Common Shares issuable upon exercise of the Warrants forming part of the Units, subject to the Company fulfilling all of the requirements of the TSX including the completion of the Acquisition.

This Prospectus also qualifies for distribution (a) the approximately 32,034,400 post-Consolidation Common Shares to be issued on the closing of the Acquisition to the vendors of the San Dimas mines and related assets and (b) the 2,000,000 post-Consolidation Common Shares to be issued to Alamos Gold Inc. in settlement of certain allegations raised in respect of an entitlement to an interest in the San Dimas mines. See “Acquisition of the San Dimas Mines”, “The Company — Recent Developments” and “Plan of Distribution”.

Subscriptions for Subscription Receipts will be received subject to rejection or allotment in whole or in part and the right is reserved to close the subscription books at any time without notice. It is expected that closing of the Offering will occur on or about July 20, 2010 or such other date not later than July 30, 2010 as the Company and the Underwriters may agree. The latest date that the Subscription Receipts will be taken up by the Underwriters, other than any Subscription Receipts that may be taken up upon the exercise of the Over-Allotment Option, is 42 days after the date that a receipt is obtained from the British Columbia Securities Commission, as principal regulator, with respect to this Prospectus. Except for certificates representing Subscription Receipts purchased in the United States pursuant to Rule 506 of Regulation D under the U.S. Securities Act, which will be issued to the purchasers thereof in definitive form, the Subscription Receipts will be represented by a global certificate issued in registered form to CDS Clearing and Depository Services Inc. (“CDS”) or its nominee under the book-based system administered by CDS. No certificates evidencing the Subscription Receipts will be issued to subscribers other than Rule 506 subscribers in the United States except in certain limited circumstances, and registration will be made in the depositary service of CDS. Subscribers for Subscription Receipts other than Rule 506 subscribers in the United States will receive only a customer confirmation from the Underwriters or other registered dealer who is a CDS participant and from or through whom a beneficial interest in the Subscription Receipts is purchased.

Subject to applicable laws and policies, the Underwriters may, in connection with the Offering, effect transactions that stabilize or maintain the market price of our common shares at levels other than those which might otherwise prevail in the open market. Such transactions, if commenced, may be discontinued at any time. The Underwriters may offer the Subscription Receipts at a price lower than the Offering Price. See “Plan of Distribution”.

The head office of the Company is located at Suite 1500, 885 West Georgia Street, Vancouver, British Columbia, V6C 3E8. The registered office of Company is located at Suite 1500, 1055 West Georgia Street, Vancouver, British Columbia, V6E 4N7.

iii

TABLE OF CONTENTS

_______________________________________

Unless the context requires otherwise, all references in this Prospectus to “we”, “Mala Noche”, or the “Company” refer to Mala Noche Resources Corp. and its subsidiaries.

iv

PROSPECTUS SUMMARY

The following is only a summary of the information in this Prospectus and should be read together with the more detailed information and financial data and statements contained elsewhere in this Prospectus.

The Company

Mala Noche Resources Corp. (“Mala Noche” or the “Company”) is a junior exploration company engaged in the business of acquiring, exploring, developing and seeking to achieve commercial production from resource properties. The Company currently has one mineral interest, an option on the Ventanas property in Durango Province, Mexico. In late 2008 the Company decided to defer undertaking further exploration work on this property and placed the property on care and maintenance. Since late 2008, the Company has been pursuing acquisition opportunities with a focus on acquiring producing, or near producing, precious metals properties.

On June 1, 2010, Mala Noche entered into a letter agreement (together with the amendment referred to below, the “Letter Agreement”) with Desarrollos Mineros San Luis, S.A. de C.V. (“DMSL”) and Goldcorp Silver (Barbados) Ltd. (“GSBL”) (together the “San Dimas Vendors”) to acquire the San Dimas mines, mill and related assets (the “Acquisition”). On July 7, 2010, Mala Noche entered into an amendment to the Letter Agreement pursuant to which the parties agreed to amend the consideration payable to the San Dimas Vendors. The Letter Agreement, as amended, is expected to be replaced by definitive asset and share purchase agreements. The completion of the Acquisition is subject to financing and other conditions. On the completion of the Acquisition, the board of directors intends to change the name of the Company to “Primero Mining Corp.” and to consolidate the Common Shares. At the annual and special meeting of shareholders held on June 28, 2010, shareholders of the Company approved resolutions authorizing (a) the creation of a new control person in connection with the Acquisition, and (b) the consolidation of the Common Shares.

On June 1, 2010, Mr. Joseph Conway was appointed the Company’s President and Chief Executive Officer. Mr. Conway was President and CEO of IAMGOLD Corporation from 2003 until his departure in January 2010. During this period, Mr. Conway led IAMGOLD Corporation through its transformation from a joint venture player to a leading mid-tier gold producer. Joining Mr. Conway as part of the senior management of the Company are Mr. Wade Nesmith, formerly Chief Executive Officer and now Executive Chairman, Mr. Eduardo Luna, formerly Chief Operating Officer and now Executive Vice President and President (Mexico), and Mr. David Blaiklock, Chief Financial Officer. Mr. Luna was formerly President of the company that currently operates the San Dimas mines. See “The Company”.

San Dimas Mines and Related Assets

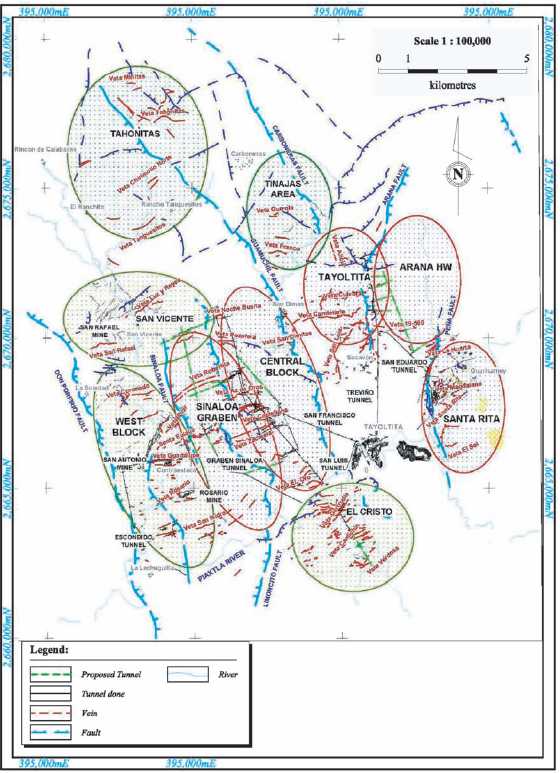

The San Dimas mines consist of the San Antonio (Central Block), Tayoltita and Santa Rita mines located in Mexico’s San Dimas district, on the border of Durango and Sinaloa states (together, the “San Dimas Mines”). An amount of refined silver equal to the payable silver produced from the San Dimas Mines is presently sold by Silver Trading (Barbados) Ltd. (“Silver Trading”), a subsidiary of GSBL, to Silver Wheaton (Caymans) Ltd. (“SW Caymans”), a subsidiary of Silver Wheaton Corp (“Silver Wheaton”) pursuant to a silver purchase agreement. In addition to the San Dimas Mines, as part of the Acquisition the Company will be acquiring all of the shares of Silver Trading as well as all rights to the Ventanas exploration property in which Mala Noche currently holds an interest pursuant to an option (together with the San Dimas Mines, the “San Dimas Assets”).

Unless otherwise indicated, the technical information in respect of the San Dimas Mines is based on the independent technical report entitled “Technical Report on the Tayoltita, San Rita and San Antonio Mines, Durango, Mexico for Goldcorp Inc. and Mala Noche Resources Corp.” dated June 1, 2010 prepared by Velasquez Spring, P.Eng. and Gordon Watts, P.Eng of Watts, Griffis and McOuat Limited, in accordance with NI 43-101. See “Technical Information” and “San Dimas Mines”.

In 2009, the San Dimas Mines produced 113,018 ounces of gold and 5,093,385 ounces of silver. The San Dimas Mines are located approximately 125 kilometres northeast of Mazatlan, Sinaloa or approximately 150 kilometres west of the city of Durango in the state of Durango, Mexico. The Santa Rita mine is located approximately three kilometres upstream from the Tayoltita mine while the San Antonio mine is seven kilometres west of Tayoltita.

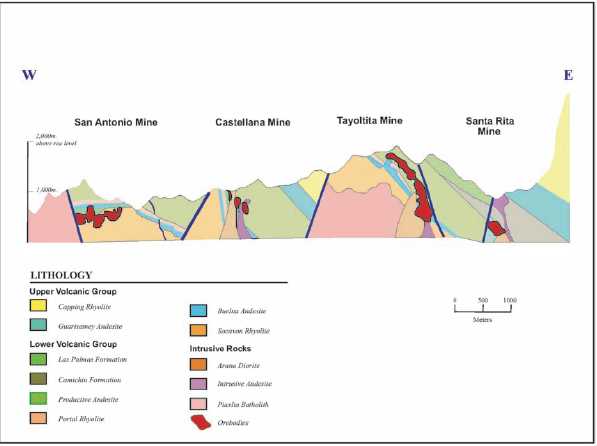

The San Dimas Mines are located in the San Dimas district. The San Dimas district is an area with a long mining history with production first reported in 1757. The San Dimas Mines, have been in production since 1975 and have been operated by Goldcorp Inc. (“Goldcorp”) since 2005. The typical mining operations employ mechanized cut-and-fill mining with primary access provided by adits and internal ramps from an extensive tunnel system through the steep mountainous terrain. All milling operations are now carried out at a central milling facility at Tayoltita that processes the production from the three active mining areas in San Dimas. The ore processing is by conventional cyanidation followed by zinc precipitation of the gold and silver followed by refining to doré. The mill currently has an installed capacity of 2,100 tonnes per day. In 2009, the mill averaged 1,934 tonnes per day.

1

Total proven and probable mineral reserves estimated as of December 31, 2009, for the San Dimas Mines are 5.589 million tonnes at a grade of 4.80 grams of gold per tonne and 339 grams of silver per tonne (860,000 ounces of gold and 61 million ounces of silver). The total inferred mineral resources, estimated as of December 31, 2009, for the San Dimas Mines, and not included in the mineral reserves stated above, are approximately 15.166 million tonnes at an approximate grade of 3.31 grams of gold per tonne and 317 grams of silver per tonne.

As of December 31, 2009, the total workforce at the San Dimas Mines, a combination of union and contracted workforce, was 1,071 personnel with 654 at Tayoltita (234 contracted) and 417 in the Central Block (267 contracted).

Summary information regarding production, reserves and resources, and operations at the San Dimas Mines is presented below. See “San Dimas Mines” for additional information, including the assumptions on which this information is based.

Mine Production

| Grade | Contained Ounces(1) | ||||||||||||||

| San Dimas Mines | Tonnes | g Au/t | g Ag/t | Au | Ag | ||||||||||

| 2003 | 423,673 | 5.20 | 428 | 70,831 | 5,824,513 | ||||||||||

| 2004 | 397,647 | 6.90 | 525 | 88,214 | 6,717,055 | ||||||||||

| 2005 | 507,529 | 7.40 | 497 | 120,749 | 8,114,662 | ||||||||||

| 2006 | 688,942 | 7.76 | 438 | 171,906 | 9,706,131 | ||||||||||

| 2007 | 685,162 | 6.27 | 341 | 138,163 | 7,500,695 | ||||||||||

| 2008 | 657,479 | 4.25 | 259 | 89,838 | 5,479,084 | ||||||||||

| 2009 | 673,311 | 5.35 | 247 | 115,748 | 5,355,786 | ||||||||||

_______________

Note:

| (1) | Represents gold and silver content in ore sent to milling operations. |

Summary of Reserves and Resources as at December 31, 2009

| Average Grade | Contained Ounces | ||||||||||||||

| Metric Tonnes | g Au/t | g Ag/t | Au | Ag | |||||||||||

| Total Proven Reserves | 2,013,582 | 5.68 | 371 | 367,477 | 24,019,101 | ||||||||||

| Total Probable Reserves | 1,575,134 | 4.67 | 340 | 236,336 | 17,209,099 | ||||||||||

| Total Proven and Probable Reserves | 3,588,716 | 5.23 | 357 | 603,813 | 41,288,200 | ||||||||||

| Total Probable Reserves by Diamond Drilling | 2,000,334 | 4.01 | 306 | 257,817 | 19,673,082 | ||||||||||

| Grand Total Proven and Probable Reserves | 5,589,050 | 4.80 | 339 | 861,630 | 60,901,283 | ||||||||||

| Total Inferred Resources | 15,166,000 | 3.31 | 317 | 1,612,000 | 154,629,000 | ||||||||||

2009 Performance of San Dimas Milling Operations

| Tonnes milled | 673,311 |

| Grade Au (g/t) | 5.36 |

| Grade Ag (g/t) | 248.7 |

| Recovery (Au) | 97.4% |

| Recovery (Ag) | 94.6% |

| Recovered Oz (Au) | 113,018 |

| Recovered Oz (Ag) | 5,093,385 |

Pro Forma Financial Information

T he following tables present selected unaudited pro forma consolidated financial information for Mala Noche that is based on the assumptions described in the notes to the Mala Noche unaudited pro forma consolidated financial statements included elsewhere in this Prospectus. The unaudited balance sheet as at March 31, 2010, and the unaudited consolidated statement of operations for the three months ended March 31, 2010 and for the year ended December 31, 2009, have been prepared based on the assumption, among other things, that the offering of Subscription Receipts (the “Offering”) and the Acquisition had occurred on the dates indicated. The unaudited pro forma consolidated financial statements are not necessarily indicative of Mala Noche’s consolidated financial position and results of Mala Noche that would have occurred if the events reflected had taken place on the dates indicated, nor do they purport to project Mala Noche’s consolidated financial position for any future period.

2

The pro forma consolidated financial statements are based on certain assumptions and adjustments, including that revenue from silver sales has been increased to reflect changes to the terms of the silver purchase agreement with SW Caymans which will come into effect on the completion of the Acquisition, interest expense in respect of indebtedness to be incurred as part of the Acquisition and the non-recurring expenses related to this Offering and the Acquisition. The selected unaudited pro forma consolidated financial information given below should be read in conjunction with the description of the Offering and the Acquisition in this Prospectus, the unaudited pro forma consolidated financial statements and the unaudited and audited financial statements of Mala Noche and carve out combined financial statements of the operations to be acquired by Mala Noche included elsewhere in this Prospectus.

Balance Sheet Data:

| Unaudited | |||

| Pro Forma as at | |||

| March 31, 2010 | |||

| (in thousands) | |||

| Cash | $ | 61,532 | |

| Mineral interests | 525,210 | ||

| Other assets | 84,012 | ||

| Total assets | $ | 670,754 | |

| Current liabilities | $ | 150,605 | |

| Long-term liabilities | 50,263 | ||

| Shareholders’ equity | 469,886 | ||

| Total liabilities and shareholders’ equity | $ | 670,754 |

Statements of Operations Data:

| Unaudited Pro Forma | ||||||

| Three months ended | Year ended | |||||

| March 31, 2010 | December 31, 2009 | |||||

| (in thousands) | ||||||

| Revenues | $ | 33,691 | $ | 151,809 | ||

| Cost of revenues | 24,758 | 109,001 | ||||

| Earnings from mining operations | 8,933 | 42,808 | ||||

| Expenses and other income | 14,274 | 48,570 | ||||

| Income taxes | 1,062 | 20,169 | ||||

| Net (loss) income | $ | (6,403 | ) | $ | (25,931 | ) |

Growth Strategy

Over the next several years, the Company intends to transition from being a single-asset gold producer to becoming an intermediate gold producer. The Company plans to achieve its goal of being an intermediate gold producer, with a target of 375,000 ounces of annual gold production by 2013, by increasing production at the San Dimas Mines and by making further acquisitions of precious metal properties in Latin America.

The San Dimas Mines are established assets with an operating history and a record of reserve replacement, resource conversion and exploration success. The Company believes that the San Dimas Mines provide, based on the current mine plan, a solid production base with immediate opportunities to optimize mine capacity and mill throughput. Cash flow from the San Dimas Mines is expected to provide the Company with an internal source of capital to fund mine development and exploration projects.

The Company estimates that gold production at the San Dimas Mines can average 107,000 ounces (157,000 gold equivalent ounces) annually over the next five years with, based on certain assumptions set out in the San Dimas Technical Report (see “Technical Information”), an average cash cost of US$60 per gold ounce on a by-product basis (US$337 per ounce on a gold equivalent basis). See “San Dimas Mines — Capital and Operating Costs” and “Management’s Discussion and Analysis of the San Dimas Operations — Outlook”. Total cash costs per ounce of gold on a by-product basis is a non-GAAP performance measure.

3

Acquisition of the San Dimas Mines

Mala Noche will be purchasing the San Dimas Assets for an aggregate purchase price of US$510 million (the “Purchase Price”) and will assume all liabilities associated with the San Dimas Mines, including environmental and labour liabilities. The Purchase Price will be payable as to (a) US$216 million in cash, (b) US$184 million in common shares of the Company (the “Acquisition Shares”), (c) US$50 million by way of a promissory note payable over a term of five years, and (d) a US$60 million principal amount convertible promissory note with a term of one year. The cash portion of the Purchase Price, the number of Acquisition Shares and the principal amount of the convertible promissory note are each subject to adjustment if the Over-Allotment Option is exercised before closing of the Acquisition. The convertible promissory note carries an annual interest rate of 3%, is convertible into Common Shares at the Offering Price at the option of the holder, and at maturity the convertible promissory note is repayable, at the Company’s option, in cash or Common Shares at a price equal to 90% of the volume weighted average trading price of the Common Shares for the five day period ending on the maturity date. See “Acquisition of the San Dimas Mines — Material Terms of the Letter Agreement — Purchase Price”. The Offering is being undertaken to finance the Acquisition and provide working capital.

The Letter Agreement provides that DMSL will sell the San Dimas Mines and related assets to a wholly-owned Mexican subsidiary of the Company. In addition, the Company will acquire from GSBL all of the shares of Silver Trading concurrent with the completion of the Acquisition. Silver Trading is a party to a silver purchase agreement with Silver Wheaton and SW Caymans. The silver purchase agreement, which will be amended and restated as part of the Acquisition, presently entitles SW Caymans to purchase an amount of refined silver equal to the payable silver produced from the San Dimas Mines. In consideration for up-front payments of cash and shares of Silver Wheaton paid to Silver Trading by SW Caymans, Silver Trading agreed that the price of refined silver would be at a fixed price. Presently, the fixed price is substantially below the current market price for silver.

Under the silver purchase agreement, the consent of SW Caymans is required in connection with any sale of the San Dimas Assets. Mala Noche has entered into a consent agreement dated June 1, 2010 with Silver Wheaton, Goldcorp and certain of their respective subsidiaries (the “Consent Agreement”) under which Silver Wheaton and SW Caymans have agreed to provide their consent to the Acquisition upon the satisfaction of certain conditions. The Consent Agreement includes the agreed-upon form of the amended and restated silver purchase agreements that will take effect upon closing of the Acquisition. See “Acquisition of the San Dimas Mines”.

Recent Developments

In addition to being a director of Mala Noche, Mr. Eduardo Luna is also a director of several other mining and exploration companies. One of those companies has alleged, in respect of Mala Noche’s proposed acquisition of the San Dimas mines, that Mr. Luna breached a duty owed to that company and that Mala Noche participated in and facilitated that breach. While the Company has denied liability for the claim, it has entered into a settlement agreement with this company in respect of these allegations. Under the terms of the settlement agreement, Mala Noche has agreed to pay $13.0 million to the company payable as to $1.0 million in cash and $12.0 million in post-Consolidation common shares issued at the same price as the Subscription Receipts. Payment of the settlement amount is conditional upon, and will occur at or immediately after, the closing of the Acquisition. See “The Company — Recent Developments” and “Risk Factors”.

Risk Factors

An investment in the Subscription Receipts and underlying common shares of the Company is subject to certain risks that should be considered by prospective investors and their advisors. See “Risk Factors”, San Dimas Mines and “Management’s Discussion and Analysis of San Dimas Operations”. The risks that should be considered include the following:

As the San Dimas Mines are being acquired on an “as is, where is” basis the representations and warranties to be provided to the Company by the San Dimas Vendors will be limited.

Unknown liabilities may be assumed by Mala Noche in connection with the Acquisition.

Mala Noche may not be able to successfully integrate and assume operations of the San Dimas Mines.

4

Operation of the San Dimas Mines will be subject to hazards and risks normally encountered in gold and silver mining operations.

The San Dimas Vendors will be significant shareholders.

Declines in the prices of gold and, to a limited extent, silver will adversely affect profitability.

Reserves and mineral resources are estimates only.

Inferred mineral resources are not mineral reserves and do not have demonstrated economic viability.

The historical record of converting inferred mineral resources into mineral reserves at the San Dimas Mines may not be continued.

Proven and probable mineral reserves must continually be replaced and expanded as gold and silver are produced.

Anticipated cash flows, operating costs and capital expenditures may not be realized.

Mala Noche’s indebtedness will limit cash flow available for other business opportunities.

Substantial additional financing may be required in order to expand the San Dimas mining operations and complete additional acquisitions.

Future cash flows from operations may not be sufficient to service debt and make necessary capital expenditures.

Mala Noche’s ability to incur additional indebtedness and to secure additional indebtedness will be limited under a silver purchase agreement.

Exchange rate fluctuations may affect the costs that Mala Noche incurs in its operations.

Mala Noche presently does not plan to hedge future gold or silver sales.

Title defects may exist which could adversely affect the San Dimas Mines.

Changes in government regulation in Mexico could adversely impact San Dimas mining operations and exploration activities.

All environmental liabilities associated with the San Dimas Mines will be assumed.

A failure in the tailings dams at the San Dimas Mines could result in significant liability.

The inability to maintain good relations with unions and employees could disrupt mining operations.

Insurance coverage is not available for all potential risks of mining operations.

Mala Noche will face strong competition from other mining companies for the acquisition of additional mining properties.

Acquisitions undertaken by Mala Noche may not be successful.

Adverse changes in governmental regulation or political stability in Mexico could adversely impact the operation of the San Dimas Mines.

Mexico’s status as a developing country may make it more difficult for Mala Noche to attract investors or obtain financing.

The loss of key executives may adversely affect Mala Noche’s business and future operations.

There exists the possibility for certain of Mala Noche’s directors and officers to be in a position of conflict.

The Ventanas property is on care and maintenance.

5

GLOSSARY OF TECHNICAL TERMS

In this Prospectus:

| g/t | means grams per tonne; |

| |

| Inferred Mineral Resource(1) | that part of a Mineral Resource for which quantity and grade or quality can be estimated on the basis of geological evidence and limited sampling and reasonably assumed, but not verified, geological and grade continuity. The estimate is based on limited information and sampling gathered through appropriate techniques from locations such as outcrops, trenches, pits, workings and drill holes; |

| |

| lb | means pound; |

| |

| m | means metre; |

| |

| Mineral Reserves(1) | Mineral Reserves are sub-divided in order of increasing confidence into Probable Mineral Reserves and Proven Mineral Reserves. A Mineral Reserve is the economically mineable part of a Measured or Indicated Mineral Resource demonstrated by at least a Preliminary Feasibility Study. This Study must include adequate information on mining, processing, metallurgical, economic and other relevant factors that demonstrate, at the time of reporting, that economic extraction can be justified. Mineral Reserves are those parts of Mineral Resources which, after the application of all mining factors, result in an estimated tonnage and grade which, in the opinion of the Qualified Person(s) making the estimates, is the basis of an economically viable project after taking account of all relevant processing, metallurgical, economic, marketing, legal, environment, socio-economic and government factors. The term ‘Mineral Reserve’ need not necessarily signify that extraction facilities are in place or operative or that all governmental approvals have been received; |

| |

| Mineral Resources(1) | a Mineral Resource is a concentration or occurrence of base and precious metals, natural solid inorganic material, or natural solid fossilized organic material including coal and diamonds in or on the Earth’s crust in such form and quantity and of such a grade or quality that it has reasonable prospects for economic extraction. Mineral Resources are sub-divided, in order of increasing geological confidence, into Inferred, Indicated and Measured categories. The location, quantity, grade, geological characteristics and continuity of a Mineral Resource are known, estimated or interpreted from specific geological evidence and knowledge. The term Mineral Resource covers mineralization and natural material of intrinsic economic interest which has been identified and estimated through exploration and sampling and within which Mineral Reserves may subsequently be defined by the consideration and application of technical, economic, legal, environmental, socio-economic and governmental factors. The phrase ‘reasonable prospects for economic extraction’ implies a judgement by the Qualified Person in respect of the technical and economic factors likely to influence the prospect of economic extraction. Mineral Resources that are not Mineral Reserves do not have demonstrated economic viability; |

| |

| NI 43-101 | means Canadian Securities Administrators’ National Instrument 43-101, Standards of Disclosure for Mineral Projects; |

| |

| ounce | means Troy ounce; |

| |

| San Dimas Technical Report | means the independent technical report entitled “Technical report on the Tayoltita, Santa Rita and San Antonio Mines, Durango, Mexico for Goldcorp Inc. and Mala Noche Resources Corp.” dated June 1, 2010 prepared by Velasquez Spring, P.Eng., Senior Geologist, and Gordon Watts, P.Eng., Senior Associate Mineral Economist, of Watts, Griffis and McOuat Limited, in accordance with NI 43-101; |

6

| ton | means 2,000 pounds; |

| tonne | means metric tonne, equalling 1,000 kilograms; and |

| tpd | means tonnes per day. |

_______________

Notes:

(1) See “Cautionary Note to United States Investors” below.

CAUTIONARY NOTE TO UNITED STATES INVESTORS

The disclosure in this Prospectus, including the documents incorporated by reference herein, uses terms that comply with reporting standards in Canada and certain estimates are made in accordance with Canadian National Instrument 43-101 Standards of Disclosure for Mineral Projects (“NI 43-101”). NI 43-101 is a rule developed by the Canadian Securities Administrators that establishes standards for all public disclosure an issuer makes of scientific and technical information concerning mineral projects. Unless otherwise indicated, all reserve and resource estimates contained in or incorporated by reference in this prospectus have been prepared in accordance with NI 43-101. These standards differ significantly from the requirements of the United States Securities and Exchange Commission (the “SEC”), and reserve and resource information contained herein and incorporated by reference herein may not be comparable to similar information disclosed by U.S. companies.

This Prospectus includes mineral reserve estimates that have been calculated in accordance with NI 43-101, as required by Canadian securities regulatory authorities. For United States reporting purposes, SEC Industry Guide 7 (under the United States Securities Exchange Act of 1934, as amended), as interpreted by Staff of the SEC, applies different standards in order to classify mineralization as a reserve. As a result, the definitions of proven and probable reserves used in NI 43-101 differ from the definitions in the SEC Industry Guide 7. Under SEC standards, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time the reserve determination is made. Among other things, all necessary permits would be required to be in hand or issued imminently in order to classify mineralized material as reserves under the SEC standards. Accordingly, mineral reserve estimates contained in this Prospectus may not qualify as “reserves” under SEC standards.

In addition, this Prospectus uses the terms “indicated mineral resources” and “inferred mineral resources” to comply with the reporting standards in Canada. We advise United States investors that while those terms are recognized and required by Canadian regulations, the SEC does not recognize them. United States investors are cautioned not to assume that any part or all of the mineral deposits in these categories will ever be converted into mineral reserves. These terms have a great amount of uncertainty as to their existence, and great uncertainty as to their economic and legal feasibility.

Further, “inferred resources” have a great amount of uncertainty as to their existence and as to whether they can be mined legally or economically. Therefore, United States investors are also cautioned not to assume that all or any part of the inferred resources exist. In accordance with Canadian rules, estimates of “inferred mineral resources” cannot form the basis of feasibility or other economic studies.

It cannot be assumed that all or any part of “measured mineral resources”, “indicated mineral resources”, or “inferred mineral resources” will ever be upgraded to a higher category. Investors are cautioned not to assume that any part of the reported “measured mineral resources”, “indicated mineral resources”, or “inferred mineral resources” in this prospectus is economically or legally mineable.

In addition, disclosure of resources using “contained ounces” is permitted under Canadian regulations; however, the SEC only permits issuers to report mineralization that does not qualify as a reserve as in place tonnage and grade without reference to unit measures.

For the above reasons, information contained in this prospectus and the documents incorporated by reference herein containing descriptions of our mineral deposits may not be comparable to similar information made public by U.S. companies subject to the reporting and disclosure requirements under the United States federal securities laws and the rules and regulations thereunder.

7

DOCUMENTS INCORPORATED BY REFERENCE

The following documents filed with the securities commission or similar regulatory authority in each of the provinces and territories of Canada, are specifically incorporated by reference into, and form an integral part of, this Prospectus:

the audited consolidated financial statements of the Company and the notes thereto for the year ended December 31, 2009, together with the auditors’ report thereon and management’s discussion and analysis of financial condition and results of operations for the fiscal year ended December 31, 2009;

the unaudited consolidated interim financial statements of the Company for the three months ended March 31, 2010 and 2009 and the notes thereto, and management’s discussion and analysis of financial condition and results of operations for the three months ended March 31, 2010;

the Annual Information Form of the Company for the fiscal year ended December 31, 2009 filed April 30, 2010;

the management information circular (the “Information Circular”) dated June 2, 2010 prepared in connection with the annual and special meeting of shareholders held on June 28, 2010, excluding the fairness opinion (the “Fairness Opinion”) of Canaccord Genuity;

the material change report dated June 4, 2010 related to the announcement of the binding letter agreement to acquire the San Dimas mines and related assets; and

the material change report dated July 8, 2010 related to the announcement of the amended terms of the Offering and the amendment to the binding letter agreement to acquire the San Dimas mines and related assets.

With respect to the exclusion of the Fairness Opinion, the Company has applied for, and is relying upon, relief from the mandatory incorporation by reference requirements in National Instrument 44-101 (the “Requested Relief”), which will be evidenced by the issuance of a receipt for this Prospectus. The Fairness Opinion was prepared by Canaccord Genuity pursuant to an engagement that is separate from their engagement as Underwriter. The Fairness Opinion was prepared with the limited scope of determining the fairness, from a financial perspective, to shareholders of the Company, and was provided to the board of directors of the Company in order to assist the board in determining whether to proceed with the Acquisition. The Fairness Opinion was not prepared for use in any public offering. For these reasons, and because the inclusion of the Fairness Opinion in this Prospectus may have the potential of exposing Canaccord Genuity to unintended liability to investors under the Prospectus, the Company applied for the Requested Relief. Prospective investors are cautioned not to rely upon the Fairness Opinion in making an investment decision and that as a result of the granting of the Requested Relief, Canaccord Genuity will not be liable to purchasers of Subscription Receipts for any misrepresentations contained in the Fairness Opinion.

Material change reports (other than confidential material change reports), business acquisition reports, interim financial statements and all other documents of the type referred to above and any other document of the type required by National Instrument 44-101 — Short Form Prospectus Distributions to be incorporated by reference in a short form prospectus, filed by the Company with a securities commission or similar regulatory authority in Canada after the date of this Prospectus and before termination of the distribution of securities being qualified hereunder, will be deemed to be incorporated by reference into this Prospectus.

Any statement contained in a document incorporated or deemed to be incorporated by reference herein will be deemed to be modified or superseded for the purposes of this Prospectus to the extent that a statement contained in this Prospectus or in any subsequently filed document that also is or is deemed to be incorporated by reference herein modifies or supersedes such statement. Any statement so modified or superseded will not constitute a part of this Prospectus, except as so modified or superseded. The modifying or superseding statement need not state that it has modified or superseded a prior statement or include any other information set forth in the document that it modifies or supersedes. The making of such a modifying or superseding statement will not be deemed an admission for any purpose that the modified or superseded statement, when made, constituted a misrepresentation, an untrue statement of a material fact or an omission to state a material fact that is required to be stated or that is necessary to make a statement not misleading in light of the circumstances in which it was made.

TECHNICAL INFORMATION

Technical information relating to the San Dimas Mines contained in this Prospectus is derived from, and in some instances is an extract from a technical report entitled “Technical Report on the Tayoltita, Santa Rita and San Antonio Mines, Durango, Mexico for Goldcorp Inc. and Mala Noche Resources Corp.” dated June 1, 2010, prepared by Velasquez Spring, P. Eng. and Gordon Watts, P. Eng. of Watts, Griffis and McOuat Limited, who are independent of the Company based on the definition of independence set out in National Instrument 43-101 Standards of Disclosure for Mineral Projects (the “San Dimas Technical Report”). The Company believes that for the purposes of National Instrument 43-101 after the closing of the Acquisition the San Dimas Mines will be the sole material properties of the Company. Reference should be made to the full text of the San Dimas Technical Report which has been filed with Canadian securities regulatory authorities pursuant to NI 43-101 and is available for review under the Company’s profile on SEDAR at www.sedar.com. Alternatively, a copy of the San Dimas Technical Report may be inspected until the day that is thirty days after the date hereof during normal business hours at the Company’s head office and at the offices of the Company’s legal counsel, Lang Michener LLP, #1500 — 1055 West Georgia Street, Vancouver, B.C. V6E 4N7.

8

For the meanings of certain technical terms used in this Prospectus, see “Glossary of Technical Terms”.

NON-GAAP MEASURES

The Company has included the following non-GAAP performance measures in this Prospectus: (a) total cash costs (by-product) per ounce gold, (b) total cash costs (co-product) per ounce gold, and (c) operating cash flows before working capital changes. These non-GAAP financial measures are common performance measures in the gold mining industry, but do not have any standardized meanings prescribed by GAAP. The Company believes that, in addition to conventional measures prepared in accordance with GAAP, certain investors may use this information to evaluate the operation of the San Dimas mines in order to evaluate performance and ability to generate cash flow. Accordingly, the non-GAAP performance measures are presented as additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with GAAP. For a reconciliation of each of these non-GAAP financial measures to the most directly comparable measure calculated in accordance with GAAP, see “Management’s Discussion and Analysis of San Dimas Operations — Non-GAAP Measures”.

ELIGIBILITY FOR INVESTMENT

In the opinion of Lang Michener LLP, counsel to the Company, and Blake, Cassels & Graydon LLP, counsel to the Underwriters, based on the provisions of the Income Tax Act (Canada) (the “Tax Act”) and the regulations thereto in force as of the date hereof, the Subscription Receipts, Common Shares and Warrants forming the Units and the Common Shares to be issued on the exercise of the Warrants (each as defined) will be “qualified investments” under the Tax Act and the regulations thereto for trusts governed by registered retirement savings plans, registered retirement income funds, registered education savings plans, deferred profit sharing plans, registered disability savings plans and tax free savings accounts (herein, collectively, “Registered Plans”) provided that (a) in the case of Subscription Receipts, the Common Shares and Warrants forming the Units are qualified investments as discussed in (b) and (c) below and the Company deals at arm’s length (for purposes of the Tax Act) with each person who is an annuitant, a beneficiary, an employer or a subscriber under, or a holder of, such Registered Plans. Subscription Receipts will also be qualified investments for Registered Plans if the Subscription Receipts are listed on a designated stock exchange (which currently includes the TSX Venture Exchange, Tiers 1 and 2) at the time the Subscription Receipts are acquired by the applicable Registered Plan, (b) in the case of Common Shares forming part of the Units or to be issued on exercise of the Warrants forming part of the Units, such Common shares are listed on a designated stock exchange, at the time the Common Shares are acquired by the applicable Registered Plan, (c) in the case of Warrants forming part of the Units, the Common Shares to be issued on the exercise of the Warrants are listed on a designated stock exchange at the time the Warrants are acquired by the applicable Registered Plan and that the Company deals at arm’s length (for purposes of the Tax Act) with each person who is an annuitant, a beneficiary, an employer or a subscriber under, or a holder of, such Registered Plans. Warrants will also be qualified investments for Registered Plans if the Warrants are listed on a designated stock exchange at the time the Warrants are acquired by the applicable Registered Plan.

Notwithstanding the foregoing, the holder of a tax-free savings account (“TFSA”) will be subject to a penalty tax where the TFSA holds a “prohibited investment” for purposes of the Tax Act. Generally, the Subscription Receipts, Common Shares and Warrants forming the Units and the Common Shares to be issued on the exercise of the Warrants should not be “prohibited investments” for a TFSA provided that the holder of the TFSA deals at “arm’s length” with the Company and does not have a “significant interest” in the Company or in any person or partnership with which the Company does not deal at “arm’s length”, all within the meaning of the Tax Act. Holders of TFSA s should consult their own tax advisors to ensure Subscription Receipts, Common Shares and Warrants forming the Units and the Common Shares to be issued on the exercise of the Warrants would not be prohibited investments in their particular circumstances.

9

FORWARD-LOOKING STATEMENTS

This Prospectus and the documents incorporated by reference herein contain “forward-looking statements” or “forward-looking information” within the meaning of Canadian securities legislation. These forward-looking statements are made as of the date of this Prospectus or, in the case of documents incorporated by reference herein, as of the date of such documents.

In certain cases, forward-looking statements can be identified by the use of words such as “believe”, “intend”, “may”, “will”, “should”, “plans”, “anticipates”, “believes”, “potential”, “intends”, “expects” and other similar expressions. Forward-looking statements reflect our current expectations and assumptions, and are subject to a number of known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any anticipated future results, performance or achievements expressed or implied by the forward-looking statements. Forward-looking statements, particularly as they relate to the completion of the acquisition of the San Dimas mines, the estimated offering price and consolidation ratio, the actual results of exploration activities, actual results of reclamation activities, the estimation or realization of Mineral Reserves and Resources, the timing and amount of estimated future production, capital expenditures, costs and timing of the development of new mineral deposits, requirements for additional capital, future prices of precious and base metals, possible variations in ore grade or recovery rates, failure of plant, equipment or processes to operate as anticipated, accidents, labour disputes, road blocks and other risks of the mining industry, delays in obtaining governmental approvals, permits or financing or in the completion of development or construction activities, currency fluctuations, title disputes or claims limitations on insurance coverage and the timing and possible outcome of pending litigation and the timing or magnitude of such events are inherently risky and uncertain.

Key assumptions upon which the Company’s forward-looking statements are based include the following:

the Company’s ability to complete the acquisition of the San Dimas mines;

the Company’s ability to successfully integrate and operate the San Dimas mines;

the prices for gold and, to a lesser extent, silver will not fall significantly;

the assumptions in the financial analysis in the San Dimas Technical Report are correct;

the Company will be able to secure new financing to continue its exploration, development and operational activities;

there being no significant adverse changes in currency exchange rates;

there being no significant changes in the ability of the Company to comply with environmental, safety and other regulatory requirements;

the Company is able to obtain regulatory approvals (including licenses and permits) in a timely manner;

the absence of any material adverse effects arising as a result of political instability, terrorism, sabotage, natural disasters, equipment failures or adverse changes in government legislation or the socio-economic conditions in the surrounding area to the Company’s operations;

the Company’s ability to achieve its growth strategy;

the Company’s operating costs will not increase significantly; and

key personnel will continue their employment with the Company and the Company will have access to all equipment necessary to operate the San Dimas mines.

Additional assumptions are included, among other places, in this Prospectus under the headings “The Company”, “Use of Proceeds”, “San Dimas Mines” and “Management’s Discussion and Analysis of the San Dimas Operations” and in each of the following documents that are incorporated by reference into this Prospectus:

in the Annual Information Form for the fiscal year ended December 31, 2009 under the headings “General Development of the Business” and “Description of Business”;

in the management’s discussion and analysis for the year ended December 31, 2009 under the headings “Overview”, “Results of Operations” and “Liquidity and Capital Resources”; and

in the management’s discussion and analysis for the three month period ended March 31, 2010 under the headings “Overview”, “Results of Operations” and “Liquidity and Capital Resources”.

10

These assumptions should be considered carefully by investors. Investors are cautioned not to place undue reliance on the forward-looking statements or the assumptions on which the Company’s forward-looking statements are based. Investors are advised to carefully review and consider the risk factors identified in this Prospectus under the heading “Risk Factors” and in the other documents incorporated by reference herein for a discussion of the factors that could cause the Company’s actual results, performance and achievements to be materially different from any anticipated future results, performance or achievements expressed or implied by the forward-looking statements. Investors are further cautioned that the foregoing list of assumptions is not exhaustive and it is recommended that prospective investors consult the more complete discussion of the Company’s business, financial condition and prospects that is included in this Prospectus, including the documents incorporated by reference herein. The forward-looking statements contained in this Prospectus are made as of the date hereof and, accordingly, are subject to change after such date.

Although the Company believes that the assumptions on which the forward-looking statements are made are reasonable, based on the information available to the Company on the date such statements were made, no assurances can be given as to whether these assumptions will prove to be correct. Accordingly, readers should not place undue reliance on forward-looking information. We do not undertake to update any forward-looking information, except as, and to the extent, required by applicable securities laws. The forward-looking statements contained in this Prospectus and the documents incorporated by reference herein are expressly qualified by this cautionary statement.

CURRENCY AND EXCHANGE RATE INFORMATION

Unless otherwise stated, references herein to “$” are to the Canadian dollar. References to “US$” are to the United States dollar. The following table reflects the low and high rates of exchange for one United States dollar, expressed in Canadian dollars, during the periods noted, the rates of exchange at the end of such periods and the average rates of exchange during such periods, based on the Bank of Canada noon spot rate of exchange.

| Year ended December 31, | Quarter ended | |||||||||||

| 2009 | 2008 | 2007 | June 30, 2010 | |||||||||

| Low for the period | $ | 1.3066 | $ | 1.3008 | $ | 1.1878 | $ | 1.0778 | ||||

| High for the period | 1.0251 | 1.0298 | 0.9066 | 0.9961 | ||||||||

| Rate at the end of the period | 1.0510 | 1.2180 | 0.9913 | 1.0606 | ||||||||

| Average noon spot rate for the period | 1.1420 | 1.0660 | 1.0747 | 1.0276 | ||||||||

On July 8, 2010 the Bank of Canada noon spot rate of exchange was US$1.00 - $1.0446.

11

THE COMPANY

Mala Noche is presently a junior exploration company engaged in the business of acquiring, exploring, developing and seeking to achieve commercial production from resource properties. Since late 2008, Mala Noche has been pursuing acquisition opportunities with a focus on acquiring producing, or near producing, precious metals properties. Executing on this strategy, Mala Noche has entered into an agreement to acquire the San Dimas mines, mill and related assets. The completion of the acquisition is subject to financing and other conditions. Before completion of the acquisition of the San Dimas mines, the board of directors intends to change the name of the Company to “Primero Mining Corp.” (or such other name as more appropriately reflects the change in status from an exploration company to a mine operator) and consolidate the common shares of the Company (see “Consolidated Capitalization — Share Consolidation”).

We currently have only one subsidiary, Mala Noche Resources, S.A. de C.V., a company incorporated under the laws of Mexico. The following is expected to be the principal operating subsidiaries of the Company after completion of the acquisition:

_______________

Notes:

| (1) | The Company will hold the San Dimas mines through a subsidiary and may incorporate a new company for this purpose. |

| (2) | Silver Trading (Barbados) Ltd. will be purchased by the Company as part of the acquisition of the San Dimas mines. It will be a party to silver purchase agreements that will be assumed as part of the acquisition. |

Recent Developments

Concurrent with the entering into of the agreement in respect of the acquisition of the San Dimas mines, Mr. Joseph Conway became the President and Chief Executive Officer of Mala Noche. Mr. Conway was President and CEO of IAMGOLD Corporation from 2003 until his departure in January 2010. During this period, Mr. Conway led IAMGOLD Corporation through its transformation from a joint venture player to a leading mid-tier gold producer. Joining Mr. Conway as part of the senior management of the Company are Mr. Wade Nesmith, formerly Chief Executive Officer and now Executive Chairman, Mr. Eduardo Luna, formerly Chief Operating Officer and now Executive Vice President and President (Mexico), and Mr. David Blaiklock, Chief Financial Officer. Mr. Luna was formerly President of the company that currently operates the San Dimas mines.

In addition to being a director of Mala Noche, Eduardo Luna is also a director of several other mining and exploration companies. One of those companies, Alamos Gold Inc. (“Alamos”), has alleged that, in respect of Mala Noche’s proposed acquisition of the San Dimas mines, Mr. Luna breached a fiduciary duty owed to Alamos and that Mala Noche participated in and facilitated that breach. While the Company has denied liability for the claim, it has reached a settlement with Alamos in respect of these allegations (the “Settlement Agreement”). Under the Settlement Agreement, in full settlement of the alleged claim and without admitting liability, the Company has agreed to pay $13.0 million to Alamos payable as to $1.0 million in cash and $12.0 million in post-Consolidation common shares issued at the same price as the Subscription Receipts. Payment of the settlement amount is conditional upon, and will occur at or immediately after, the closing of the Acquisition.

12

ACQUISITION OF THE SAN DIMAS MINES

Overview

On June 1, 2010, the Company entered into a letter agreement (together with the amendment referred to below, the “Letter Agreement”) with Desarrollos Mineros San Luis, S.A. de C.V. (“DMSL”) and Goldcorp Silver (Barbados) Ltd. (“GSBL”) (together the “San Dimas Vendors”) to acquire the San Dimas mines, mill and related assets (the “Acquisition”). Each of the San Dimas Vendors is an indirect, wholly-owned subsidiary of Goldcorp Inc. (“Goldcorp”). On July 7, 2010, Mala Noche entered into an amendment to the Letter Agreement pursuant to which the parties agreed to amend the consideration payable to the San Dimas Vendors. The Letter Agreement, as amended, is expected to be replaced by definitive asset and share purchase agreements prior to closing of the Acquisition.

The San Dimas mines consist of the San Antonio (Central Block), Tayoltita and Santa Rita mines located in Mexico’s San Dimas district, on the border of Durango and Sinaloa states (the “San Dimas Mines”). In addition to the San Dimas Mines, as part of the Acquisition the Company will also be acquiring (a) all rights to the Ventanas exploration property in which Mala Noche currently holds an interest pursuant to an option, and (b) all shares of Silver Trading (Barbados) Ltd. (“Silver Trading”), a subsidiary of GSBL (together with the San Dimas Mines, the “San Dimas Assets”). Silver Trading is a party to a silver purchase agreement with Silver Wheaton Corp. (“Silver Wheaton”) and Silver Wheaton (Caymans) Ltd. (“SW Caymans”), a subsidiary of Silver Wheaton.

The Letter Agreement provides that DMSL will sell the San Dimas Mines and related assets to a wholly-owned Mexican subsidiary of the Company, which is anticipated to be Mala Noche Resources, S.A. de C.V. (“Mala Noche Mexico”). In addition, the Company will acquire from GSBL all shares of Silver Trading concurrent with the completion of the acquisition of the San Dimas Mines. Silver Trading is a party to a silver purchase agreement with Silver Wheaton and SW Caymans. The silver purchase agreement, which will be amended and restated as part of the Acquisition, presently entitles SW Caymans to purchase an amount of refined silver equal to payable silver produced from the San Dimas Mines. In consideration for up-front payments comprised of cash and shares of Silver Wheaton previously paid to Silver Trading by SW Caymans, Silver Trading agreed that the price of refined silver would be at a fixed price. Presently, the fixed price is substantially below the current market price for silver.

Mala Noche will be purchasing the San Dimas Assets for an aggregate purchase price of US$510 million (the “Purchase Price”) and will assume all liabilities associated with the San Dimas Mines, including environmental and labour liabilities. The Purchase Price will be payable as to (a) US$216 million in cash, (b) US$184 million in common shares of the Company (the “Acquisition Shares”), (c) US$50 million by way of a promissory note payable over a term of five years, and (d) a US$60 million principal amount convertible promissory note with a term of one year. The cash portion of the Purchase Price, the number of Acquisition Shares and the principal amount of the convertible promissory note are each subject to adjustment if the Over-Allotment Option is exercised before closing of the Acquisition. See “— Material Terms of the Letter Agreement — Purchase Price”.

Mala Noche is undertaking this offering of Subscription Receipts to finance the Acquisition and provide working capital. Completion of the Acquisition is subject to a number of conditions, including completion of the financing and receipt of all government and regulatory approvals. Closing of the Acquisition is expected to occur on or before July 30, 2010. Subject to certain exceptions, including transfers to affiliates, the San Dimas Vendors will agree not to sell the Acquisition Shares for a period of three years following closing of the Acquisition.

The issue of the Acquisition Shares will result in the San Dimas Vendors owning approximately 38% of Mala Noche’s outstanding shares on closing of the Acquisition (potentially increasing if the convertible promissory note is converted by the holder in full into Common Shares at the Offering Price). Consequently, a new control person of the Company will be created upon closing of the Acquisition. In accordance with TSXV policies, the shareholders of Mala Noche have approved the creation of a new control person of the Company. The Acquisition is subject to the approval of the TSXV. The TSXV has conditionally approved the Acquisition subject to the satisfaction of customary conditions.

Under the silver purchase agreement with Silver Wheaton and SW Caymans, the consent of SW Caymans is required in connection with any sale of the San Dimas Assets. Mala Noche has entered into a consent agreement dated June 1, 2010 with Silver Wheaton, Goldcorp and certain of their respective subsidiaries (the “Consent Agreement”) under which Silver Wheaton and SW Caymans have agreed to provide their consent to the Acquisition upon the satisfaction of certain conditions. The Consent Agreement includes the agreed upon form of the amended and restated silver purchase agreement that will take effect upon closing of the Acquisition.

13

Mala Noche After the Acquisition

Following the completion of the Acquisition, the Company will be an established junior gold and silver producer. The Company intends to work to expand production at the San Dimas Mines and consider other acquisition opportunities to achieve its goal of becoming an intermediate gold producer. The following is a summary description of the San Dimas Mines (see “San Dimas Mines” for more information on the mines), the business strategy of the Company, and the material contracts the Company will be a party to with Goldcorp and Silver Wheaton after the Acquisition.

San Dimas Mines

The San Dimas Mines consist of three underground gold and silver mining operations at Tayoltita, San Antonio (Central Block) and Santa Rita. In 2009, the San Dimas Mines produced 113,018 ounces of gold and 5,093,385 ounces of silver. The San Dimas Mines are located approximately 125 kilometres northeast of Mazatlan, Sinaloa or approximately 150 kilometres west of the city of Durango in the state of Durango, Mexico. The Santa Rita mine is located approximately three kilometres upstream from the Tayoltita mine while the San Antonio mine is seven kilometres west of Tayoltita.

The San Dimas Mines are located in the San Dimas district. The San Dimas district is an area with a long mining history, with production first reported in 1757. The San Dimas Mines have been in production since 1975 and have been operated by Goldcorp since 2005. The typical mining operations employ mechanized cut-and-fill mining with primary access provided by adits and internal ramps from an extensive tunnel system through the steep mountainous terrain. All milling operations are now carried out at a central milling facility at Tayoltita that processes the production from the three active mining areas in San Dimas. The ore processing is by conventional cyanidation followed by zinc precipitation of the gold and silver followed by refining to doré. The mill currently has an installed capacity of 2,100 tonnes per day. In 2009, the mill averaged 1,934 tonnes per day.

Total proven and probable mineral reserves estimated as of December 31, 2009, for the San Dimas Mines are 5.589 million tonnes at a grade of 4.80 grams of gold per tonne and 339 grams of silver per tonne (860,000 ounces of gold and 61 million ounces of silver). The total inferred mineral resources, estimated as of December 31, 2009, for the San Dimas Mines, and not included in the mineral reserves stated above, are approximately 15.166 million tonnes at an approximate grade of 3.31 grams of gold per tonne and 317 grams of silver per tonne.

As of December 31, 2009, the total workforce at the San Dimas Mines, a combination of union and contracted workforce, was 1,071 with 654 personnel at Tayoltita (234 contracted) and 417 in the Central Block (267 contracted).

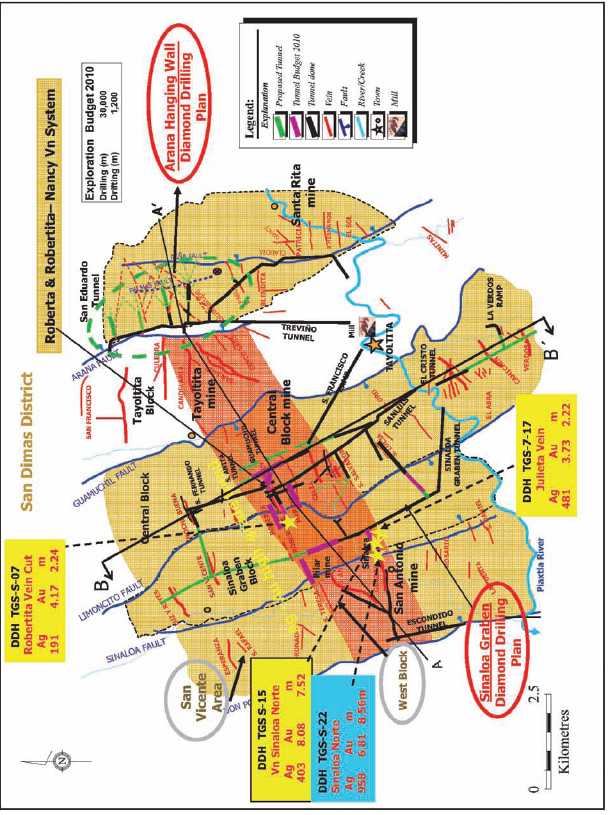

Recent Three-Year Operations

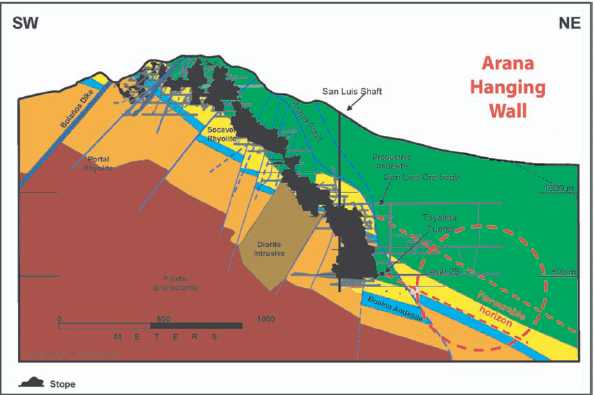

In the first trimester of 2010, diamond drilling and drifting showed additional Mineral Resources, in particular at the Sinola Graben structure. Positive exploration results were obtained including interceptions in the Roberta vein and in the North Sinaloa vein. This work followed-up exploration work conducted in 2009 that saw positive exploration results with three veins confirmed in the Sinaloa Graben Block (Julieta, North Sinaloa and Robertita). In 2008 and 2007, exploration was carried out in many veins in the district, in 2008 mainly in the Central Block area, the West Block and the Arana Hanging wall area.

The tunnels that serve as the main haulage levels for the Sinaloa Graben and Center Block areas were completed during the first quarter of 2010. The San Francisco ore pass was completed during the third quarter of 2009. The San Luis Bridge was completed during the fourth quarter of 2009 and is the first stage of the new waste rock dump. Management of the mine has continued to work to reduce operating costs by increasing the scale of operations as well as making improvements in the efficiency of operating methods. In February 2009, the San Dimas Mines began shipping doré bars to the Johnson Matthey refinery in Salt Lake City, Utah. See “San Dimas Mines — History” for information on historical mine production.

Significant portions of the remediation plan for up-grading the Tayoltita tailings dam to international standards were completed in 2007 and work has continued on improving this dam, with the most important work in 2009 being the construction of two basins in the back of the dam. The San Dimas Mines’ Las Truchas hydro power plant and line were completed in 2008 and began supplying approximately 76% of the current electrical power needs of the San Dimas Mines in June 2008.

Growth Strategy

Over the next several years, the Company intends to transition from being a single-asset gold producer to becoming an intermediate gold producer. The San Dimas Mines are established assets with an operating history and a record of reserve replacement, resource conversion and exploration success. The Company plans to achieve its goal of being an intermediate gold producer, with a target of 375,000 ounces of annual gold production by 2013, by increasing production at the San Dimas Mines and by considering and, if appropriate, making further acquisitions of precious metal properties in Latin America.

14

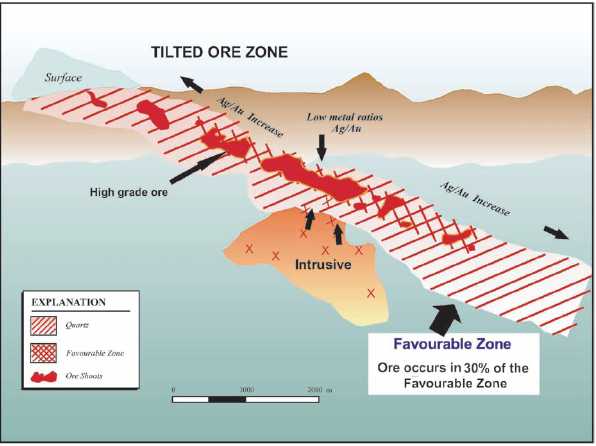

The Company believes that the San Dimas Mines provide, based on the current mine plan, a solid production base with immediate opportunities to optimize mine capacity and mill throughput. Drilling and development programs carried out over the last 10 years have resulted in discoveries that have significantly increased reserve and production estimates. The Company believes that it can continue to expand reserve capacity by focussing new drilling programs on areas of good exploration potential — principally the Sinaloa Graben Block and Arana Hanging Wall. See “San Dimas Mines —Exploration and Drilling”. Cash flow from the San Dimas Mines is expected to provide the Company with an internal source of capital to fund mine development and exploration projects.

The Company estimates that gold production at San Dimas can average 107,000 ounces (157,000 gold equivalent ounces) annually over the next five years with, based on certain assumptions set out in the San Dimas Technical Report, an average cash cost of US$60 per ounce on a by-product basis (US$337 per ounce on a gold equivalent basis). See “San Dimas Mines — Capital and Operating Costs” and “Management’s Discussion and Analysis of the San Dimas Operations — Outlook”. Total cash costs per ounce of gold on a by-product basis is a non-GAAP performance measure.

Ventanas Project

Under an option agreement dated May 8, 2007, as amended, the Company holds an option from an affiliate of Goldcorp to acquire a 70% interest in the Ventanas exploration property. As part of the Acquisition the Company will be acquiring all rights to this exploration property. Disclosure in respect of the Ventanas property is contained in the Annual Information Form of the Company dated April 28, 2010.

The Ventanas property lies within the Ventanas mining district in Durango State, Mexico. This exploration property is composed of 28 near-contiguous mining concessions covering approximately 3,470 hectares or 35 square kilometres. The Company last drilled on the property in 2008 and since then the property has been on care and maintenance. After completing the Acquisition, in the near-term the Company intends to conduct further exploration work as permitted by its corporate resources.

Area of Interest

The Company will covenant that it will not, directly or indirectly, acquire any interests or other rights to mineral properties, royalty interests, surface rights or water rights within specified areas (the “Goldcorp Area of Interest”) for a period of three years following the completion of the Acquisition. The Goldcorp Area of Interest will extend 20 kilometres from the external boundary of each mineral property in Mexico owned by Goldcorp and its affiliates.