UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10/A

(Amendment No. 2)

GENERAL FORM FOR REGISTRATION OF SECURITIES

Pursuant to Section 12(b) or 12(g) of the Securities Exchange Act of 1934

LEATT CORPORATION

(Exact name of registrant as specified in its charter)

| Nevada | 20-2819367 |

| (State or other jurisdiction | (I.R.S. Employer Identification No.) |

| of incorporation or organization) |

50 Kiepersol Drive, Atlas Gardens, Contermanskloof Road,

Durbanville, Western Cape, South Africa, 7441

(Address of Principal Executive Offices; Zip Code)

Registrant’s Telephone Number, Including Area Code: +(27) 21-557-7257

Securities to be registered under Section 12(b) of the Act:

| Title of each class | Name of each exchange on which each class is |

| to be so registered | to be registered |

| None | None |

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, par value 0.001

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definition for “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large Accelerated Filer [ ] | Accelerated Filer [ ] |

| Non-Accelerated Filer [ ] | Smaller Reporting Company [X] |

TABLE OF CONTENTS

| Number | Page | |

| Item 1. | Business | 4 |

| Item 1A. | Risk Factors | 22 |

| Item 2. | Financial Information | 28 |

| Item 3. | Properties | 33 |

| Item 4. | Security Ownership of Certain Beneficial Owners and Management | 33 |

| Item 5. | Directors and Executive Officers of the Registrant | 35 |

| Item 6. | Executive Compensation | 38 |

| Item 7. | Certain Relationships and Related Transactions | 40 |

| Item 8. | Legal Proceedings | 41 |

| Item 9 | Market Price of and Dividends on Common Equity and Related Stockholder Matters | 42 |

| Item 10. | Recent Sale of Unregistered Securities | 42 |

| Item 11. | Description of Securities to be Registered | 43 |

| Item 12. | Indemnification of Officers and Directors | 45 |

| Item 13. | Financial Statements and Supplementary Data | 46 |

| Item 14. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 46 |

| Item 15. | Exhibits and Financial Statement Schedules | 48 |

EXPLANATORY NOTE

On April 30, 2012, Leatt Corporation (the “Company”) filed a Registration Statement on Form 10-12G (the “Original Filing”) with the Securities and Exchange Commission (the “Commission”). The Company is filing this Registration Statement on Form 10-12G/A to (the “Amendment”) to amend the Original Filing in response to comments by the staff of the Commission (the “Staff”) in connection with its review of the Original Filing. Among other things, we provided additional disclosures regarding the Company’s business and operations.

SPECIAL NOTE REGARDING FORWARD LOOKING STATEMENTS

This registration statement contains forward-looking statements. The forward-looking statements are contained principally in the sections entitled “Our Business,” “Risk Factors,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” These statements involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from any future results, performances or achievements expressed or implied by the forward-looking statements. These risks and uncertainties include, but are not limited to, the factors described in the section captioned “Risk Factors” above.

In some cases, you can identify forward-looking statements by terms such as “anticipates,” “believes,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “projects,” “should,” “would” and similar expressions intended to identify forward-looking statements. Forward-looking statements reflect our current views with respect to future events and are based on assumptions and subject to risks and uncertainties. Given these uncertainties, you should not place undue reliance on these forward-looking statements. These forward-looking statements include, among other things, statements relating to:

our expectations regarding growth in the motor sports market;

our expectation regarding increasing demand for protective equipment used in the motor sports market;

our belief that we will be able to effectively compete with our competitors and increase our market share;

our expectations with respect to increased revenue growth and our ability to achieve profitability resulting from increases in our production volumes; and

our future business development, results of operations and financial condition.

Also, forward-looking statements represent our estimates and assumptions only as of the date of this prospectus. You should read this registration statement and the documents that we reference and filed as exhibits to the registration statement completely and with the understanding that our actual future results may be materially different from what we expect. Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, even if new information becomes available in the future.

Use of Certain Defined Terms

Except as otherwise indicated by the context, references in this registration statement to:

“Leatt,” “we,” “us,” “our,” the “Registrant” or the “Company” are to the combined business of Leatt Corporation, a Nevada corporation, its South African branch, Leatt SA, and its direct, wholly-owned subsidiaries, Two Eleven, Leatt New Zealand and Three Eleven;

“Leatt SA” are to the Company’s branch office known as ‘Leatt Corporation, Incorporated in the State of Nevada,’ incorporated under the laws of South Africa with registration number: 2007/032780/10;

“Leatt USA” are to Leatt USA, LLC, is a Nevada Limited Liability Company;

“Leatt New Zealand” are to Leatt New Zealand Limited, a New Zealand Company;

“NZD” are to the legal currency of New Zealand. For all NZD amounts reported, the dollar amount has been calculated on the basis that $1=NZD1.2914 for its December 31, 2011 audited balance sheet.

“PRC”, and “China” are to the People’s Republic of China;

“Two Eleven” refers to Two Eleven Distribution, LLC, a California limited liability company;

“Three Eleven” are to Three Eleven Distribution (Pty) Limited, a South African Company;

“Securities Act” are to the Securities Act of 1933, as amended, and to “Exchange Act” are to Securities Exchange Act of 1934, as amended;

“South Africa” are to the Republic of South Africa;

“U.S. dollar,” “$” and “US$” are to the legal currency of the United States. For all U.S. dollar amounts reported, the dollar amount has been calculated on the basis that $1 = ZAR8.1173 for its December 31, 2011 audited balance sheet;

3

“Xceed Holdings” refers to Xceed Holdings cc., a close corporation incorporated under the laws of South Africa, and wholly-owned by The Leatt Family Trust, of which Dr. Christopher J. Leatt, the Company’s chairman, is a Trustee and Beneficiary; and

“ZAR” refers to the South African Rand, the legal currency of South Africa.

OUR BUSINESS

We are an “emerging growth company” as defined in Title I of the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. An emerging growth company is defined as an issuer, including a foreign private issuer, with less than $1 billion of total annual gross revenues during its most recently completed fiscal year. The JOBS Act eases restrictions on the sale of securities, increases the number of shareholders a company must have before becoming subject to the U.S. Securities and Exchange Commission’s (“SEC’s”) reporting and disclosure rules, and exempts qualifying companies from certain financial disclosure and governance requirements for up to five years. For details on the JOBS Act and the Company’s status, see our disclosure under “Regulations – The 2012 JOBS Act” below.

Overview of Our Business

Leatt designs, develops, markets and distributes personal protective equipment for participants in all forms of motor sports and leisure activities, including riders of motorcycles, bicycles, snowmobiles and ATVs, as well as racing car drivers. The Company sells its products to customers worldwide through a global network of distributors and retailers. Leatt also acts as the original equipment manufacturer for neck braces sold by other international brands.

The Company’s flagship products are based on the Leatt-Brace® system, a patented injection molded neck protection system owned by Xceed Holdings, designed to prevent potentially devastating injuries to the cervical spine and neck. The Company has the exclusive global manufacturing, distribution, sale and use rights to the Leatt-Brace®, pursuant to a license agreement between the Company and Xceed Holdings, a company owned and controlled by the Company’s Chairman and founder, Dr. Christopher Leatt. The Company also has the right to use apparatus embodying, employing and containing the Leatt-Brace® technology and has designed, developed, marketed and distributed other personal protective equipment.

The Company’s research and development efforts are conducted at its research facilities, located at its executive headquarters in Cape Town, South Africa. The Company employs 6 full-time employees who are dedicated exclusively to research, development, and testing. The Company also utilizes consultants, academic institutions and engineering companies as independent contractors or consultants, from time to time, to assist it with its research and development efforts. Leatt products have been tested and reviewed internally and by external bodies. All Leatt products are compliant with applicable European Union directives, or CE certified, where appropriate. Certain products, such as the Moto R, have been certified by SFI Foundation (USA) and the Moto GPX was tested by BMW Motorrad (Germany) and reviewed by KTM (Austria). The Company is also in discussions with governing and racing bodies, such as the Fédération Internationale de l'Automobile (FIA), the Fédération Internationale de Motocyclisme (FIM) and the National Association for Stock Car Auto Racing (NASCAR), to have the Leatt-Brace® accredited by these bodies.

Our products are manufactured in China under outsource manufacturing arrangements with third-party manufacturers located there. The Company utilizes outside consultants and its own employees to ensure the quality of its products through regular on-site product inspections. Products purchased through international sales are usually shipped directly from our manufacturers’ warehouses or points of dispatch to customers or their import agents.

Leatt earns revenues through the sale of its products through approximately 60 distributors worldwide, who in turn sell its products to retailers. Leatt distributors are required to follow certain standard business terms and guidelines for the sale and distribution of Leatt products. Two Eleven and Leatt SA directly distribute Leatt products to retailers in the United States and South Africa, respectively. Our sales revenue for the fiscal years ended December 31, 2011 and 2010 were $17,878,727 and $14,330,072, respectively, and our net income (net loss) for the fiscal years ended December 31, 2011 and 2010 were $764,499 and ($208,562), respectively. For the years ended December 31, 2011 and 2010, annual revenues associated with international customers were $10,109,894 and $8,493,593, or 57% and 59% of total revenue, respectively.

Our Corporate History and Structure

We were incorporated in the State of Nevada on March 11, 2005 under the name Tradezone, Inc. Until March 2006, we were a shell company with little or no operations. Effective as of March 1, 2006, we acquired the exclusive global manufacturing, distribution, sale and use rights to the Leatt-Brace®, pursuant to a license agreement between the Company and Xceed Holdings, a company owned and controlled by the Company’s Chairman and founder, Dr. Christopher Leatt. On May 25, 2005, we changed our name to Leatt Corporation in connection with our anticipated acquisition of the Leatt-Brace® rights.

4

Leatt South Africa

The Company conducts business in South Africa as a foreign registered branch known as ‘Leatt Corporation, (Incorporated in the State of Nevada),’ registered under the laws of South Africa with registration number: 2007/032780/10. Based in Cape Town, South Africa, Leatt SA was formed on November 14, 2007, for conducting the Company’s business and operations in South Africa. Our corporate headquarters and our research and development efforts are based at Leatt SA.

Establishment of Two Eleven, Three Eleven and Leatt USA

On August 17, 2007, the Company established Two Eleven Distribution, a California limited liability company, as its wholly-owned subsidiary. Located in Santa Clarita, California, Two Eleven was formed to serve as the Company’s executive offices in the United States, as well as the exclusive distributor of Leatt® products in the United States.

Southern Palace Investments 409 (Proprietary) Limited, a South African company, was established on October 12, 2007, by the Company, to engage in the manufacturing and distribution of sporting goods and protective gear. The company was inactive until March 2009, when it acquired all intellectual property rights related to an invention entitled the Helmet® from Xceed Holdings, for an aggregate purchase price of ZAR 943,480 (approximately, $90,000) pursuant to a patent assignment agreement, effective as of January 1, 2009, between Xceed Holdings and Southern Palace, doing business as Three Eleven Distribution. On February 10, 2010, Southern Palace formally changed its name to Three Eleven Distribution to reflect its business purpose.

On June 26, 2010, the Company established Leatt USA, LLC, a Nevada Limited Liability Company, as our wholly-owned subsidiary and for the purpose of holding our California subsidiary, Two Eleven Distribution. However, as of the date of this registration statement the Company had not moved forward with its original plan and Leatt USA remains dormant.

Wind-up of Leatt New Zealand

On March 13, 2009, the Company established Leatt New Zealand Limited, a New Zealand company, as its wholly-owned subsidiary. Leatt New Zealand served as the exclusive distributor of Leatt-Brace® products in New Zealand, until the fourth quarter of 2011 when it ceased operations and became dormant. The Company has appointed an unrelated third party distributor to distribute its products in the New Zealand market.

Settlement Agreement

As consideration for their management and other services to the Company, we agreed to issue 20,000,000 shares of our common stock, and 19,200,000 shares of our preferred stock to Dr. Leatt, 5,000,000 shares of our common stock and 4,800,000 shares of our preferred stock to Jean-Pierre De Villiers, and 50,000 shares of our common stock to Ervian Jarrett. We issued the common stock to Dr. Leatt, Mr. De Villiers and Ms. Jarrett in accordance with the agreement, but we did not issue any preferred shares to Dr. Leatt or Mr. De Villiers. On September 25, 2008, in settlement of our obligation to issue Dr. Leatt and Mr. De Villiers shares of preferred stock, we entered into a Settlement Agreement with them, pursuant to which they agreed to release us from any and all liability arising out of or related to our failure to satisfy our prior obligation to them, and we issued 16,800,000 shares of our common stock and 2,400,000 shares of our Series A Preferred Stock to Dr. Leatt, and 4,200,000 shares of our common stock and 600,000 shares of our Series A Preferred Stock to Mr. De Villiers. The Series A Preferred Stock entitles Dr. Leatt and Mr. De Villiers to one hundred votes for each share of Series A Preferred Stock held (voting with the common stock as a single class). The Series A Preferred Stock converts into common stock, on a one-for-one basis, has a liquidation preference equal to $0.001 par value per share and is redeemable by us at $0.001 par value per share upon the occurrence of specified events, but it is not transferable and does not entitle Dr. Leatt and Mr. De Villiers to dividends.

5

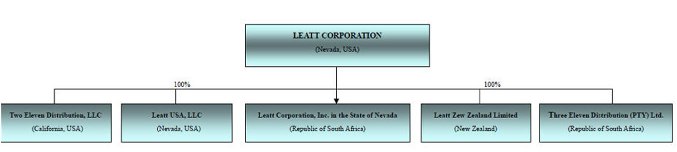

Our Corporate Structure

The following chart reflects our organizational structure as of the date of this registration statement.

Our corporate headquarters are located at 50 Kiepersol Drive, Atlas Gardens, Contermanskloof Road, Durbanville, Western Cape, South Africa, 7441. Our telephone number is +(27) 21-557-7257. We maintain a website at www.leatt.com that contains information about our Company, but that information is not incorporated into, or otherwise considered a part of, this registration statement.

Our Industry and Market Trends

Off-Road Motorcycle Market

| Our products have their roots in the off-road motorcycle market. Our revolutionary neck brace was invented by Dr. Leatt to protect from catastrophic neck injuries after he witnessed the death of a fellow off-road motorcycle rider the weekend after his son’s riding debut. As a result, our original products target participants in off-road cycling activities such as BMX racing and downhill racing. According to a RacerX magazine October 2011 reader survey, available at http://filterpubs.com/mediakit/Apparel/Apparel_PAGE2.html, approximately 45% of riders still do not wear a neck brace for protection. |

The same RacerX survey shows that, as at October 2011, we had an approximately 74% market share for neck braces and 2.9% of the market share for chest protectors in the U.S. market, which represents approximately 50% the world market. We believe that we have gained our market share, largely due to the innovation and quality of our products, the growth of the market, our increased marketing efforts and our steps to secure our international patents and protect our patents from infringement. |

Other Recreational Markets

We also design and sell neck braces for use by participants in other recreational sports such as ATV, go-kart and snowmobile users, race-car drivers and participants in other sports where a full face helmet should be worn. As a result, our overall performance in the market is also affected by the performance of these industries, especially in jurisdictions where the use of helmets are compulsory.

6

Our Products

The Company designs, develops, distributes and markets parts and accessories based on the Leatt-Brace®, a patented neck protection system for all helmeted sports.

The Leatt-Brace®

| The Leatt-Brace® is a prophylactic neck bracing system composed of various combinations of carbon fiber, glass fiber, polycarbonate or Glass Filled Nylon, which was designed to help prevent potentially devastating motor sport injuries to the cervical spine (neck). The first Leatt–Brace® was designed for motorcycle and ATV use, where there is little means of protecting the neck in the event of an accident, but the Leatt-Brace® has been designed in such a way as to offer neck protection to all who utilize a crash helmet as a form of protection, including soldiers, law enforcement officers and other professionals whose activities could result in cervical spine injury. The Company currently markets and sells four models of Leatt-Brace® products which bring the safety benefits of the Leatt-Brace® technology to a large group of sports participants: our GPX model for off- road motorcycle use; our DBX model, for downhill and BMX bicycle ranges; our SNX model for snowmobile use; and our STX model for street commuters. The GPX models include the GPX Club III, which is fully adjustable, the GPX Adventure III, which is less adjustable, and the GPX Pro, which is a full carbon brace. Our DBX models include the DBX Comp III, which is fully adjustable, the DBX Ride III, which is less adjustable, and the DBX Pro which is a full carbon brace. The SNX model includes the SNX Pilot, which is fully adjustable. The Company offers various versions and colors of these products to appeal to different clients and price points. The following table sets out the type of neck braces currently sold by the Company: |

| Product Category | Models | Description |

| NECK BRACES: | ||

| GPX | These neck braces are designed for off-road motorcycle riders. | |

| LEATT GPX Pro | The Pro brace features a fully ventilated carbon-fiber chassis with completely redesigned, open-cell padding and all aluminum hinges and bracket. It is the lightest brace in the range weighing 600g ±50g. | |

| LEATT GPX Club 3 | The Club 3 chassis is constructed with High Impact Polymer (LHIP) that improves its durability in a greater range of temperatures. It has a 5-way adjustability that allows for a wide range of body shapes and body sizes, creating a better, more comfortable fit. | |

| LEATT GPX Adventure 3 | The Adventure 3 is the entry-level brace in this category. Its 3-way adjustability allows it to fit different body shapes and sizes. The Adventure 3 lacks just the front and rear table height adjustments of its more expensive counterpart. | |

| DBX | These neck braces are for downhill and BMX riders. | |

| LEATT DBX Pro | The Pro brace features a fully ventilated carbon-fiber chassis with completely redesigned, open-cell padding and all aluminum hinges and bracket. It is the lightest brace in the range weighing 600g ±50g. | |

| LEATT DBX Comp 3 | The Comp 3 chassis is constructed of High Impact Polymer (LHIP) that improves its durability in a greater range of temperatures. The 5-way adjustability, including for the height of its front and rear tables, allows for a wide range of body shapes and body sizes, creating a better, more comfortable fit. | |

| LEATT DBX Ride 3 | The Ride 3 is the entry-level brace in this category. Its 3- way adjustability allows it to fit different body shapes and sizes. The Ride 3 lacks just the front and rear table height adjustments of its more expensive counterpart. | |

| STX | These neck braces are for street commuters. | |

| LEATT STX Jason Britton | This product is intended for use by all types of street riders. It features a quick and easy no- tool adjustable fit, with folding scapula wings that adapt to an outside back protector and hump, and a molded padding solution for an extra low profile. The folding scapula wings also permit easy storage. | |

| LEATT STX Road | This product is intended for use by all types of street riders. It features a quick and easy no- tool adjustable fit, with folding scapula wings that permit easy storage and adapt to an outside back protector and hump, and a molded padding solution for an extra low profile. | |

| SNX | These neck braces are for snowmobile riders. | |

| LEATT SNX Pilot | This neck brace features the AFC - Special low temperature resin material with a non- snow sticking padding. It includes a waterproof and breathable weather collar and sports fully adjustable front and rear tables. | |

| Kart | These neck braces are for go-kart riders. | |

| LEATT Kart | This neck brace features a special Kart angle for improved function and fit. It also has fully adjustable front and rear tables. | |

7

Leatt Protection Range

While we remain committed to the ongoing improvement and enhancement of the Leatt-Brace® and we are also focusing on the development of related and complimentary protection products. We now offer additional protection products, such as chest protectors, that can be worn with or without the Leatt-Brace®, as well as ancillary products such as clothing. Such products have a wider range of uses including in activities such as rugby, horseback riding, snowboarding, skiing and any activity where researched technology can be applied to help prevent injury.

In 2010 we launched the Leatt Protection Range with the introduction of the Leatt Adventure Chest Protector, a hard shell chest protector, and in 2011 we introduced junior protectors, body vests and full body protectors. All our protectors come standard with the Brace-On™ integration system that attaches the protector to the Leatt Brace yet permit independent movement of the brace and protector.

The Leatt Protection Range has also seen increasing sales since inception. Revenue derived from Leatt protection products in 2010 was 2% of total revenue, as compared to 8% of revenues to date in 2011.In November 2011, the Leatt Adventure Chest Protector was awarded a perfect sore (10/10) in a product evaluation done on Motocrossgear.com, an industry publication.

The following table sets out the type of protectors currently sold by the Company:

| Product Category | Models | Description |

| CHEST PROTECTORS: | ||

| LEATT Adventure Lite | This protector is designed to fit with the Leatt neck brace. t is made of tough HDPE plastic and washable bio-foam and includes a BraceOn® brace strap to improve fit. | |

| LEATT Adventure Jr | This protector is designed especially for children and is designed to fit with the Leatt neck brace. It is made of tough HDPE plastic and washable bio-foam and also includes a BraceOn® brace strap to improve fit. This product also has elbow/shoulder protection. | |

| LEATT Adventure Pro | This protector is designed to integrates perfectly with the Leatt neck brace. It has all the qualities of the Leatt Adventure Jr., but the back of protector is made with SaS-TeC impact absorbing material which meets the highest level of CE approval (EN 1621-2 level 2). | |

| LEATT Adventure | This Protector is designed to fit with the Leatt neck brace. It is made of tough HDPE plastic and washable bio-foam and includes a BraceOn® brace strap to improve fit. This product also has elbow/shoulder protection. | |

| BODY PROTECTORS: | ||

| Body Protector LEATT Adventure | This body protector is designed to be used with either an under or over shirt fitting of the Leatt neck brace . This product features zip off arms and height adjustable waist belt and the BraceOn® brace strap to improve fit. | |

| Body Vest LEATT Adventure | This body vest is designed to be used with either an under or over shirt fitting of the Leatt neck brace. This product features a height adjustable waist belt and the BraceOn® brace strap to improve fit. | |

| Body Vest LEATT Adventure Lite | This lighter version of the Body Vest Leatt Adventure is designed to be used with either an under or over shirt fitting of the Leatt neck brace. This product features a height adjustable waist belt and the BraceOn® brace strap to improve fit. | |

| Back Protector LEATT Adventure | This back protector is designed to be used with either an under or over shirt fitting of the Leatt neck brace. This product permits individual movement of body, brace and protector. | |

| Body Vest LEATT Adventure Lite Jr | This body vest is designed to be used with either an under or over shirt fitting of the Leatt neck brace. This product features the BraceOn® brace strap to improve fit and is sold in two Junior sizes. | |

| COMFORT WEAR: | ||

| Cooling Vest LEATT Coolit | This product is made from a patented HyperkewlTM cooling fabric that is designed to lower the body temperature. It fits snugly on the body under a body protector and is light weight. | |

| Cooling Tee LEATT Coolit | This product is also made from a patented HyperkewlTM cooling fabric that is designed to lower the body temperature. It fits snugly on the body under a body protector and is light weight. | |

8

Other Products, Parts and Accessories

The nature of our product is such that certain components collapse and fail in a controlled mode to help prevent further bodily injury. In light of this, we also provide aftermarket support for users of our products through our global distribution network. Specific parts of the product or the entire product may need to be replaced after a significant impact. Our aftermarket support primarily entails the replacement of worn or damaged parts, as well as sale of accessories, including hats, bags and hydration kits. We also sell clothing and outerwear.

Accolades

Leatt-Brace® products have attracted worldwide interest and we have corresponded with global motorsports governing bodies such as the FIM, Motorsport South Africa, NASCAR and the FIA, with motor racing teams such as the KTM Racing Team, with automotive and motorcycle manufacturers, and with global retailers and distributors of protective gear for motor and extreme sports. We are also in discussions with the FIM, NASCAR and the FIA, to have the Leatt-Brace® accredited.

Our Leatt-Brace® and chest protection products have acquired CE certification where necessary to distribute and sell products in the EU countries. The Leatt-Brace® products have won a series of awards and accolades since 2007, including the following:

Motocross Action: Leatt-Brace GPX awarded 5/5 Star Product Rating (2007) and Decade’s Most Significant Product (awarded by an industry magazine based on comfort, fit and safety)

Transworld MX: Editors Choice–Leatt Brace Adventure awarded Best New Product of Year (2009) (selected by editors of an industry magazine with no published criteria)

ISPO Brandnew Awards: Leatt-Brace DBX awarded Best Protection at Bike Expo (2010) (Bike Expo is an annual gathering of industry participants)

Transworld MX: Leatt GPX Pro Best Product of the Year (2011) (selected by editors of an industry magazine, based on comfort and safety)

Motocrossgear.com: Perfect Score to New 2012 Leatt-Brace Chest Protector Adventure Pro (selected by an industry website, based on looks, comfort and safety)

We believe that the quality of Leatt-Brace® products has resulted in increased sales since inception. We have sold in excess of 425,000 units of Leatt-Brace® products worldwide to date, with 79,977 units sold in 2010; 90,982 units sold in 2011 and 14,380 units sold in the first quarter of 2012, already representing a year on year increase in units sold. Approximately 9% of our 2010 unit sales were from our new DBX bicycle brace. This number has increased to 15% of unit sales in 2011 and 11% of unit sales in the first quarter of 2012. Our new STX street brace, which was introduced to the market in 2011, accounted for 6% of unit sales in 2011 and 4% of unit sales in the 2012 first quarter.

Manufacturing

Our products are manufactured in China in accordance with our manufacturing specifications, pursuant to outsource manufacturing arrangements with third- party manufacturers located there. Our third-party manufactures usually have the capacity to produce more than 120,000 braces per year and have the space to expand such capacity as required. We do not currently have written agreements with these entities but will include any such future written agreement with our periodic filings.

Upon internal determination of order quantities, we order from these third-party manufacturers by means of issuing a manufacturing purchase order. The purchase price for each such order is negotiated with the manufacturer and then a deposit of between 10 – 30% of the total purchase order value is made with the manufacturer upon receipt of the manufacturer’s invoice reflecting quantities ordered and negotiated price. The standard agreed on lead time from order date to ship-ready date is 70 days, and our usually agreed on shipping terms are FOB (Port). Products purchased through international sales are usually shipped directly from our manufacturers’ warehouses or points of dispatch to customers or their import agents.

During production, we measure the manufacturer’s on-time performance to determine whether to continue our outsource relationship. We utilize outside consultants and our own employees to ensure the quality of our products through regular on-site product inspections. Such quality inspections are conducted in conformance with ISO/IEC 17025 specifications at the manufacture’s premises and penalties are levied against a manufacturer if any delay in shipment to customers or customer rejection or non-acceptance is caused by quality issues. The balance of the open invoices is paid to the manufacturer six weeks after successful inspection.

Raw Materials and Suppliers

Our products are manufactured from generally available engineering materials, such as thermoset carbon fiber, glass fiber reinforced nylon, high impact polycarbonate resin. The cost of materials used in our products varies depending on the target market for, and the price of, our products. The prices of these raw materials are determined based upon prevailing market conditions and supply and demand and global conditions may impact the supply of these raw materials and adversely affect the supply of our products. We have not experienced any interruptions to our production due to shortage of our raw materials.

9

Our third-party manufacturers arrange for the purchase of most of the raw materials that are used to manufacture our products and they pay for the cost of such materials. However, we may directly source and pay for highly specialized protection materials, SaS-tec and WinBoss, for use in the production of our products, and that these protection materials are freely available. Furthermore, in the event that we need to maintain a specified production capacity, we may acquire raw materials on behalf of a third-party manufacturer to secure such production capacity. The expenses incurred for such materials for the years ended December 31, 2011 and 2010, were not material and we do not foresee these amounts being material in the near future.

We have implemented certain protocols to check the quality of raw materials used in the production process. Our third-party manufacturers are required to perform prescribed strength testing on critical parts of certain products. In addition, certain materials are tested by our research and development staff at Leatt SA and by independent material laboratories for compliance to manufacturing and material specification.

Our Customers

Leatt earns revenues through the sale of its products to customers worldwide through a global network of distributors and retailers. Leatt also acts as the original equipment manufacturer for neck braces sold by certain international brands. Leatt sells its products directly to distributors in South Africa (through Leatt SA), in the USA (through Two Eleven), and through a network of 60 third-party distributors worldwide. Our distributors are required to follow certain standard business terms and guidelines for the sale and distribution of our products. Two Eleven also sells our products directly to consumers through our online store available at www.leatt.com.

Products purchased through international sales are usually shipped directly from our manufacturers’ warehouses or points of dispatch to customers or their import agents. Revenue and related cost of revenue is recognized at the time of shipment from the manufacturer’s port when shipping terms are Free On Board (FOB) shipping point, Cost and Freight (CFR) or Cost and Insurance to named place (CIP) as legal title and risk of loss to the product pass to the customer.

We generate revenue both in the United States and internationally. For the years ended December 31, 2011 and 2010, annual revenues associated with international customers were $10,109,894 and $8,493,593, or 57% and 59% of total revenue, respectively.

We have derived a significant portion of our revenue from a limited number of customers, however none of our customers account for more than 10% of our consolidated revenues. For the years ended December 31, 2011 and 2010, our U.S. revenue was earned from five and six customers that accounted for approximately 36% and 36% of annual U.S. revenue, respectively, with our largest customer in the U.S. accounting for approximately 8% and 10% of our U.S. sales for those years, respectively. As of December 31, 2011 and 2010, $560,717, or 19%, and $329,505, or 14% of our accounts receivable, respectively, were due from these customers.

For the years ended December 31, 2011 and 2010, our international revenue (not including the U.S.) was earned from five customers that accounted for approximately 37% and 41% of our annual international revenue for the respective periods, with our largest international customers accounting for approximately 10% and 9% of international sales for respective periods. As of December 31, 2011 and 2010, $181,311, or 1%, and $928,274, or 32% of our accounts receivable, respectively, were due from these international customers.

Advertising and Marketing

We first gained market recognition through customer word-of-mouth and later through third-party articles and reviews of the Leatt-Brace® in motorcycle and racing magazines, and unsolicited and unpaid endorsements from current and former celebrity motocross (and other) riders, but we now advertise our products in various motorsport industry magazines and in related online media. We also enhance our image through the sponsorship of sporting events, teams and individuals.

We believe that, as a result of our marketing efforts, and based on our internal marketing estimates, we have approximately 2,451 distributors and dealers stock Leatt products in the U. S. and approximately 197 distributors and dealers in South Africa. We expect that the number of our distributors and dealers will also grow as the market segments that we sell to and our product offering grows but we cannot guarantee that this will be the case.

10

Our advertising and marketing expenses for the years ended December 31, 2011 and 2010 were $1,578,346 and $1,265,655, respectively, representing approximately 9% of our revenues for each period, and for the quarters ended March 31, 2012 and 2011 were $231,389 and $371,050, respectively, representing approximately 7% and 13% of our revenues for each period. The increase in advertising and marketing expenses during the fiscal year 2011 period was attributable to the introduction of our increased range of products to new global markets, while the decrease in such expenses during the first quarter of 2012 was attributable to the changed seasonality of our advertising and marketing expenditure.

Our Growth Strategy

We are committed to growing our business in the coming years. The key elements of our growth strategy are summarized below:

Regional Distributors. Our product range has attracted the interest of global retailers and distributors of protective gear for motor and extreme sports, as well as automotive and motorcycle manufacturers and racing teams like the KTM teams. The resultant interest and the expected demand for our products have prompted us to change our production and distribution strategy in order to cater to this demand. In November 2007, we established Two Eleven, our wholly owned California subsidiary, to manage and control the distribution of our products, particularly in the United States. We distribute products to international consumers through a network of international distributors who are selected by our management team based on their financial status and creditworthiness, their location in major geographic location, their marketing and media presence, their portfolio of leading motorcycle brands and accessories, and their reputation among industry players. We are also in discussions with various suppliers of motor sports protective gear in various regions throughout the world, including Europe, Asia, South America, Middle-East, in an effort to improve our network of distributors and dealers worldwide, with emphasis on emerging markets such as the Middle-East and South America. We believe that regional distributors will better promote our products in the designated regions and expand our global customer base.

OEM Manufacturer and Regional Distributors. We are seeking to expand our OEM services to other brands utilizing our Intellectual Property rights. With the launch of OEM agreements with other companies with their own established distribution networks, there are opportunities for us to greatly increase our regional distribution footprint globally.

Industry Accreditation and Endorsements. We are pursuing accreditation and endorsements of our products from global motor sports governing bodies and industry organizations. We are in discussions with governing racing bodies, such as the Commission Internationale de Karting, or CIK, the American Motorcyclist Association, or AMA, the FIM, the FIA, and NASCAR, to have the Leatt-Brace® accredited. We believe that these accreditations and endorsements will increase sales of our products and solidify our position as a leader in safety products. SFI testing is compulsory for neck protection used in automotive racing in the United States, therefore should neck protection be compulsory we believe that such accreditations and endorsements will additionally increase our sales.

Efforts to Promote Use of Our Products. We intend to promote the military use of our products to foreign governments worldwide, as well as promote the passage of standards and regulations prescribing the use of safety products such as ours by riders in South Africa as well as in other markets where we sell our products. We also intend to pursue large insurance carriers to mandate or incentivize their insured riders and/or drivers to wear safety products such as ours.

Expanding our Portfolio of Products. We are always looking for opportunities to introduce new products to reach a wider audience and penetrate new markets. This will include extending our product range to include both innovative protection products as well as peripheral or accessory products such as clothing. We expect that our sales of peripheral or accessory products will increase in line with brand awareness.

11

Our Research and Development Efforts

Our research and development efforts are headed by our Chairman and Founder, Dr. Christopher Leatt, and are conducted at our research facility, or Leatt Lab, located at our executive headquarters in Cape Town, South Africa. The facility houses a team of bio-medical engineers and designers who ensure products are scientifically and bio- medically sound. This facility features state of the art testing and prototyping equipment and sophisticated simulation models. Leatt also utilizes consultants, academic institutions and engineering companies from time to time to assist us with our research and development efforts.

We believe that the development of new products and new technology is critical to our success. We are continuously working to improve the quality, efficiency and cost-effectiveness of our existing products. All our products have achieved CE certification when necessary. We are working to develop technology to expand our range of products with further innovation, comfort, ergonomics and market appeal. We believe that our scientific and medical approach to product development gives our products a competitive edge.

Our research and development expenses for the fiscal years ended December 31, 2011 and 2010, amounted to $1,224,965 and $1,083,635, respectively. These expenses included salaries for research and development staff as well as other direct product development and research costs.

12

Competition

We compete with a small number of dominant competitors in the neck brace and body protection market, some of whom have substantially greater financial and other resources than we currently have. According to the October 2011 RacerX survey discussed elsewhere herein and available at http://filterpubs.com/mediakit/Apparel/Apparel_PAGE2.html, our major competitors in the neck brace market is Alpinestars S.p.A and EVS Sports, and our major competitors in the body protection market is Thor Motocross and Fox Racing.

Competition is based on quality, price reputation, industry endorsements and certifications, as well as, on product design, brand names, marketing support and distribution strategies. We believe that our products can be distinguished from the products offered by our competitors due to the fact that our products are innovative, safety tested, versatile, aesthetically appealing, priced competitively and comfortable without compromising quality and performance.

Our Competitive Strengths

We believe that our competitive strengths include the following:

Intellectual Property. Licensed patented technology allows us to provide a product that cannot easily be duplicated by our competitors. We have invested extensive resources to patent our products worldwide and have taken legal action to protect our intellectual property rights from infringement.

Diverse Multi-Cultural Skilled Management Team. Our management team is knowledgeable and experienced in the personal protective equipment industry, sports medicine and business development. Our executive corporate management team consists of Mr. Sean Macdonald, Dr. Christopher James Leatt, Mr. Erik Olsson and Mr. Philip Davy. Mr. Macdonald is our Chief Executive Officer, Chief Financial Officer, President and Director, and is a Chartered Accountant with 8 years’ experience in the financial and operational aspects of running sports orientated growth companies. Dr. Leatt is our Founder, Chairman and Head of Research and Development, who developed the Leatt-Brace® from his study of the benefits and viability of a neck protection system for helmet clad sport and recreational users. Mr. Davy is our Head of International Marketing and General Manager of our U.S. operations and has spent his entire professional life selling, envisioning, designing, developing and marketing protective equipment for motorcycle riders, racers and mechanics. Mr. Olsson is our General Manager and Head of International Distribution and has served as a Sales and Product Manager for various companies in the power sports industry for the past 15 years.

Outsourced Manufacturing. We outsource our manufacturing to third-party manufacturers in order to produce large volumes of our products. The manufacturing process remains subject to our strict quality control guidelines safeguarded by our employees and the third party inspectors who we hire as consultants to ensure that these guidelines are being implemented at the production point. While such manufacturing arrangements pose a risk to our ability to safeguard our property technologies and may lead to increased costs, as discussed under the “Risk Factors” heading in this registration statement, we expect that the increase in expected sales volumes will contribute to a lower production cost per unit and that this will translate to better margins for our distributors and retailers.

Research, Development, Certification and Marketing Capabilities. We have in-house know how in the areas of product development, testing and accreditation, particularly in the field of personal protective equipment. With the experience and capabilities developed and established in taking our product to market, we believe that we are well positioned to develop, manufacture and market additional products. With our medical and biomechanical expertise, demonstrated research and development capabilities, established outsource manufacturing capacity, established brand and our dedicated, loyal and enthusiastic distribution network, we believe that we have the components necessary to bring new successful products to market.

13

- Industry Accreditation, Testing Standards and Regulations. We are pursuing accreditation and endorsements of our products from global motor sports governing bodies and industry organizations. We have obtained homologations of our products from various global racing authorities where objective standards have been set and we are in discussions with governing racing bodies, such as the AMA, FIM, FIA, CIK, and NASCAR, to have the Leatt-Brace® accredited. SFI testing is compulsory for neck protection used in automotive racing in the U. S., therefore any of our competitors will also have to pass the certification testing. Should industry accreditation become compulsory, we would be ahead of our competitors in the market place.

Brand Recognition. A RacerX survey discussed elsewhere herein shows that, as at October 2011, Leatt had an approximately 74% market share for neck braces. We believe that public recognition of the Leatt® brand drives the sales of our products, regardless of the action of competitors and competitive products. We expect that the reputation of our brand in the market place, particularly our product testing and applicable CE certification, will continue to ensure market acceptance and facilitate market penetration of our new products. In order to bolster and grow the Leatt® brand, stringent quality control and assurance are our highest priority and our ongoing marketing, advertising and public relations efforts continue to stress the quality, safety and innovation of our products.

Our Intellectual Property

We believe that the continued success of our business is dependent on our intellectual property portfolio consisting of globally registered trademarks, design patents and utility patents related to the Leatt-Brace®. Most of these iniial intellectual property rights are held by Xceed Holdings, a corporation controlled by our Chairman, Dr. Christopher Leatt and the rest of these rights are held by the Company and Three Eleven Distribution, our South African subsidiary. We license most of our intellectual property from Xceed Holdings, pursuant to a patent and royalty license agreement, or Licensing Agreement, dated March 1, 2006, between the Company and Xceed Holdings. Under the terms of the Licensing Agreement, we are obligated to pay Xceed Holdings 4% of all our revenues from the Leatt-Brace®. In addition, pursuant to a separate license agreement between us and Mr. De Villiers, we are obligated to pay a royalty fee of 1% of all our billed and received sales revenue, in quarterly installments, based on sales of the previous quarter, to a trust that is beneficially owned and controlled by Mr. De Villiers. We also rely on nondisclosure agreements and other methods to protect our intellectual property rights. However, the steps we have taken may be inadequate to prevent the misappropriation of our technology.

The following table lists the patents and designs licensed from Xceed Holdings:

| Country | Application No | Patent No | Filing Date (year/month/day) | Invention Title | Status | Renewal Date |

| South Africa | 2006/05044 | 2006/05044 | 2006/06/20 | NECK BRACE | Granted | 2012/11/26 |

| Brazil | PI0416971-9 | 2006/05/26 | NECK BRACE | Pending | 2012/11/26 | |

| Canada | 2,547,855 | 2006/05/26 | NECK BRACE | Pending | 2012/11/26 | |

| China | 20048003507 2.4 | 2006/05/26 | NECK BRACE | Pending | ||

| Indonesia | W002006014 67 | 2006/06/19 | NECK BRACE | Accepted | ||

| Israel | 175931 | 2006/05/25 | NECK BRACE | Pending | ||

| Japan | 2006541524 | 4553903 | 2006/05/26 | NECK BRACE | Granted | 2013/07/23 |

| North Korea | 06-2007 | 46322 | 2006/05/26 | NECK BRACE | Lapsed | 2011/11/26 |

| South Korea | 10-2006- 7012173 | 10-0904041 | 2006/06/19 | NECK BRACE | Granted | 2012/06/15 |

| Morocco | PV29105 | 28229 | 2006/06/15 | NECK BRACE | Granted | 2014/11/26 |

| Mexico | JL/a/2006/000 026 | 2006/05/26 | NECK BRACE | Pending | ||

| Malaysia | PI 20062407 | 2006/05/25 | NECK BRACE | Accepted | ||

| Singapore | 200808773-6 | 2006/05/26 | NECK BRACE | Pending | ||

| USA | 11/440,576 | 7,993,293 | 2006/05/25 | NECK BRACE | Granted | 2015/02/09 |

| USA (Broad) | 11/690,412 | 8,002,723 | 2007/03/23 | NECK BRACE | Granted | 2015/02/23 |

| USA (Continuation) | 13/206,312 | 2011/08/09 | NECK BRACE | Pending | ||

| Eurasia | 200601049 | 10815 | 2006/06/26 | NECK BRACE | Granted | 2012/11/26 |

| Australia | 2004293118 | 2003/06/23 | NECK BRACE | Accepted - Opposed | 2012/11/26 |

14

| India | 2315/CHENP/ 2006 | 2006/06/26 | NECK BRACE | Pending | ||

| Norway | 20062971 | 327461 | 2006/06/26 | NECK BRACE | Granted | 2012/11/26 |

| New Zealand | 548068 | 548068 | 2006/06/22 | NECK BRACE | Granted | 2012/11/26 |

| Vietnam | 1-2006-01015 | 2006/06/26 | NECK BRACE | Pending | ||

| Europe | 04816084.0 | 1696842 | 2006/06/22 | NECK BRACE | Granted - Opposed | |

| Europe (Div) | 09165346.9 | 2113231 | 2009/07/13 | NECK BRACE | Granted | |

| Germany | 04816084.0 | 6020040259 75,6 | 2006/06/22 | NECK BRACE | Granted | 2012/11/26 |

| France | 04816084.0 | 1696842 | 2006/06/22 | NECK BRACE | Granted | 2012/11/26 |

| UK | 04816084.0 | 1696842 | 2006/06/22 | NECK BRACE | Granted | 2012/11/26 |

| Switzerland | 04816084.0 | 1696842 | 2006/06/22 | NECK BRACE | Granted | 2012/11/26 |

| Spain | 04816084.0 | 2342402 | 2006/06/22 | NECK BRACE | Granted | 2012/11/26 |

| Italy | 04816084.0 | 1696842 | 2006/06/22 | NECK BRACE | Granted | 2012/11/26 |

| Netherlands | 04816084.0 | 1696842 | 2006/06/22 | NECK BRACE | Granted | 2012/11/26 |

| Taiwan | 97109256 | 2008/03/17 | SSS BRACE | Accepted | ||

| South Africa | 2009/03522 | 2009/05/21 | 2009/05/21 | SSS BRACE | Granted | 2012/10/26 |

| Brazil | PI07180047 | 2009/04/27 | SSS BRACE | Pending | 2012/01/26 | |

| China | 2007 80047024.0 | 2009/06/19 | SSS BRACE | Pending | ||

| Japan | 2009-534037 | 2009/04/27 | SSS BRACE | Pending | ||

| USA | 12/447,452 | 2009/04/27 | SSS BRACE | Pending | ||

| Australia | 2007310441 | 2007310441 | 2009/05/20 | SSS BRACE (clip) | Granted | 2012/10/26 |

| Australia | 2011201521 | 2011/04/05 | SSS BRACE (tether) | Accepted | ||

| Europe | 07826882.8 | 2009/05/26 | SSS BRACE | Pending | 2012/10/26 | |

| New Zealand | 577131 | 577131 | 2009/05/21 | SSS BRACE (clip) | Granted | 2014/10/26 |

| New Zealand | 592116 | 592116 | 2009/05/21 | SSS BRACE (tether) | Granted | 2012/02/10 |

| USA | 12/532,409 | 2009/09/21 | TETHER PRE- TENSIONING | Pending | ||

| Europe | 08719762.0 | 2009/10/12 | TETHER PRE- TENSIONING | Accepted | 2012/03/19 | |

| Australia | 2008 227867 | 2009/10/19 | TETHER PRE- TENSIONING | Pending | ||

| USA | 12/812,596 | 2010/07/12 | MRX BRACE | Pending | ||

| Australia | 2009321240 | 2011/06/08 | MRX BRACE | Pending | 2014/11/26 | |

| Brazil | PI 0916012-4 | 2011/05/20 | MRX BRACE | Pending | 2012/02/25 | |

| China | 20098014755 8.X | 2011/05/26 | MRX BRACE | Pending | ||

| Europe | 09801554.8 | 2011/05/31 | MRX BRACE | Pending | 2012/11/30 | |

| Japan | 2011-537006 | 2011/05/19 | MRX BRACE | Pending | ||

| Switzerland | 09165346.9 | 2113231 | 2009/07/13 | NECK BRACE | Granted | 2012/11/26 |

| Germany | 09165346.9 | 2009/07/13 | NECK BRACE | Granted | 2012/11/26 | |

| Spain | 09165346.9 | 2009/07/13 | NECK BRACE | Granted | 2012/11/26 | |

| France | 09165346.9 | 2113231 | 2009/07/13 | NECK BRACE | Granted | 2012/11/26 |

| UK | 09165346.9 | 2113231 | 2009/07/13 | NECK BRACE | Granted | 2012/11/26 |

| Italy | 09165346.9 | 2113231 | 2009/07/13 | NECK BRACE | Granted | 2012/11/26 |

| Netherlands | 09165346.9 | 2113231 | 2009/07/13 | NECK BRACE | Granted | 2012/11/26 |

| South Africa | F2004/1128 | F2004/1128 | 2004/8/27 | MOTO-R BRACE | Registered | 2012/08/27 |

| Australia | 10790/2005 | 303171 | 2005/2/28 | MOTO-R BRACE | Registered | 2015/02/28 |

| China | 20053000447 5.X | 2005 3 0004475.X | 2005/2/28 | MOTO-R BRACE | Registered | 2013/03/16 |

| Europe | 000 304 225- 0001 | 000 304 225- 0001 | 2005/2/28 | MOTO-R BRACE | Registered | 2015/02/28 |

| New Zealand | 405910 | 405910 | 2005/2/28 | MOTO-R BRACE | Registered | 2014/08/27 |

| USA | 29/224,261 | D552,742 | 2005/2/28 | MOTO-R BRACE | Registered | |

| South Africa | F2004/1239 | F2004/1239 | 2004/9/17 | MOTO-GPX BRACE | Registered | 2012/09/17 |

| USA | 29/225,477 | D542,919 | 2005/3/17 | MOTO-GPX BRACE | Registered | |

| Europe | 000 312 061- 0001 | 000 312 061-0001 | 2005/3/17 | MOTO-GPX BRACE | Registered | 2015/03/17 |

| New Zealand | 405978 | 405978 | 2005/3/16 | MOTO-GPX BRACE | Registered | 2014/09/17 |

| China | 20053000910 0.2. | 2005 3 0009100.2 | 2005/3/16 | MOTO-GPX BRACE | Registered | 2013/03/16 |

| Australia | 11036/2005 | 305138 | 2005/3/15 | MOTO-GPX BRACE | Registered | 2015/03/15 |

| South Africa | F2006/01661 | F2006/0166 1 | 2006/10/26 | SSS BRACE | Registered | 2012/10/26 |

| USA | 29/279,249 | D631,167 | 2007/4/24 | SSS BRACE | Registered | |

| Europe | 000 711 130- 0001 | 000 711 130- 0001 | 2007/4/20 | SSS BRACE | Registered | 2017/04/20 |

| USA | 29/284,258 | D592,310 | 2007/9/4 | 2006 GPX- BRACE | Registered | |

| Europe | 000 785 373- 0001 | 000 785 373- 0001 | 2007/9/6 | 2006 GPX- BRACE | Registered | 2015/09/06 |

| USA | 29/325,870 | D633,623 | 2008/10/7 | DAMPER BRACE | Registered | |

| China | 20053000447 5.X | 2005 3 0004475.X | 2005/2/28 | MOTO-R BRACE | Registered | 2013/03/16 |

| Europe | 000 304 225- 0001 | 000 304 225- 0001 | 2005/2/28 | MOTO-R BRACE | Registered | 2015/02/28 |

| New Zealand | 405910 | 405910 | 2005/2/28 | MOTO-R BRACE | Registered | 2014/08/27 |

| USA | 29/224,261 | D552,742 | 2005/2/28 | MOTO-R BRACE | Registered | |

| South Africa | F2004/1239 | F2004/1239 | 2004/9/17 | MOTO-GPX BRACE | Registered | 2012/09/17 |

| USA | 29/225,477 | D542,919 | 2005/3/17 | MOTO-GPX BRACE | Registered | |

| Europe | 000 312 061- 0001 | 000 312 061-0001 | 2005/3/17 | MOTO-GPX BRACE | Registered | 2015/03/17 |

| New Zealand | 405978 | 405978 | 2005/3/16 | MOTO-GPX BRACE | Registered | 2014/09/17 |

| China | 20053000910 0.2. | 2005 3 0009100.2 | 2005/3/16 | MOTO-GPX BRACE | Registered | 2013/03/16 |

| Australia | 11036/2005 | 305138 | 2005/3/15 | MOTO-GPX BRACE | Registered | 2015/03/15 |

| South Africa | F2006/01661 | F2006/0166 1 | 2006/10/26 | SSS BRACE | Registered | 2012/10/26 |

| USA | 29/279,249 | D631,167 | 2007/4/24 | SSS BRACE | Registered | |

| Europe | 000 711 130- 0001 | 000 711 130- 0001 | 2007/4/20 | SSS BRACE | Registered | 2017/04/20 |

| USA | 29/284,258 | D592,310 | 2007/9/4 | 2006 GPX- BRACE | Registered | |

| Europe | 000 785 373- 0001 | 000 785 373- 0001 | 2007/9/6 | 2006 GPX- BRACE | Registered | 2015/09/06 |

| USA | 29/325,870 | D633,623 | 2008/10/7 | DAMPER BRACE | Registered |

15

The following table lists our own patents and designs:

| Country | Application No | Patent No | Filing date | Grant date | Invention Title | Status | Renewal Date |

| Held by Leatt Corporation | |||||||

| USA (CIP) | 11/778,840 | 7,846,117 | July 17, 2007 | December 7, 2010 | DAMPER BRACE | Granted | June 7, 2014 |

| Australia | 2008277318 | January 25, 2010 | DAMPER BRACE | Accepted | July 17, 2013 | ||

| Europe | 8789345.9 | January 15, 2010 | DAMPER BRACE | Abandoned | July 17, 2012 | ||

| USA (NAT PHASE) | 12/669,792 | January 19, 2010 | DAMPER BRACE | Pending | |||

| USA | 12/598,383 | October 30, 2009 | BACK PROTECTOR | Pending | |||

| Australia | 2,008,243,788 | November 9, 2009 | BACK PROTECTOR | Accepted | April 30, 2013 | ||

| Brazil | PI0810464-6 | October 21, 2009 | BACK PROTECTOR | Pending | July 30, 2012 | ||

| Europe | 8738037.4 | November 24, 2009 | BACK PROTECTOR | Pending | April 30, 2012 | ||

| PCT | PCT/IB2010/054 446 | October 1, 2010 | CHEST PROTECTOR | Pending | |||

| UK | 1119264.8 | November 8, 2011 | KNEE BRACE | Pending | |||

| UK | 1118611.1 | October 27, 2011 | CRS | Pending | |||

| USA | 29/297,349 | D609,815 | November 8, 2007 | February 9, 2010 | Leatt Sock Kit | Registered | |

| USA | 29/381,768 001 251 508- | D649,649 001 251 508- | December 22, 2010 | November 9, 2011 | STX Brace | Registered | |

| Europe | 0001 | 0001 | December 23, 2010 | January 7, 2011 | STX Brace | Registered | December 23, 2015 |

| Australia | 15733/2010 | 334789 | December 23, 2010 | January 24, 2011 | STX Brace | Registered | December 23, 2015 |

| Japan | 2010-031383 | 1422456 | December 28, 2010 | August 5, 2011 | STX Brace | Registered | August 6, 2012 |

| Held by Three Eleven Distribution (Pty) Ltd. | |||||||

| Brazil | PI0618410-3 | April 11, 2008 | HELMET | Pending | January 12, 2013 | ||

| China | 200680038079.0 | ZL2006800380 79.0 | April 14, 2008 | December 11, 2010 | HELMET | Granted | October 13, 2012 |

| Indonesia | W00200801199 1863/KOLNP/20 | May 28, 2008 | HELMET | Pending | |||

| India | 08 | May 8, 2008 | HELMET | Pending | |||

| USA | 12/280,105 | August 20, 2008 | HELMET | Pending | |||

| Hong Kong | 08112556.3 | HK 1120 708 | November 17, 2008 | August 27, 2010 | HELMET | Granted | October 13, 2013 |

| Germany | 06809017.4 | 60 2006 010 418.9-08 | March 31, 2008 | November 11, 2009 | HELMET | Granted | October 13, 2012 |

| France | 06809017.4 | 1933656 | March 31, 2008 | November 11, 2009 | HELMET | Granted | October 13, 2012 |

| UK | 06809017.4 | 1933656 | March 31, 2008 | November 11, 2009 | HELMET | Granted | October 13, 2012 |

| Italy | 67618/BE/2010 | 1933656 | March 31, 2008 | November 11, 2009 | HELMET | Granted | October 13, 2012 |

| Netherlands | 06809017.4 | 1933656 | March 31, 2008 | November 11, 2009 | HELMET | Granted | October 13, 2012 |

| Austria | 06809017.4 | AT-E 0447866 | March 31, 2008 | November 11, 2009 | HELMET | Granted | October 13, 2012 |

| Spain | 06809017.4 | 1933656 | March 31, 2008 | November 11, 2009 | HELMET | Granted | October 13, 2012 |

| Sweden | 06809017.4 | 1933656 | March 31, 2008 | November 11, 2009 | HELMET | Granted | October 13, 2012 |

____________________

* The Patent Cooperation Treaty, or PCT, is an international agreement for filing patent applications having effect in up to 117 countries. Under the PCT, an inventor can file a single international patent application in one language with one patent office in order to simultaneously seek protection for an invention in up to 117 countries throughout the world.

____________________

Patents applicable to specific products extend for varying periods according to the date of patent application filing or patent grant and the legal term of patents in the various countries where patent protection is obtained. The actual protection afforded by a patent, which can vary from country to country, depends upon the type of patent, the scope of its coverage and the availability of legal remedies in the country. Issued patents or patents based on pending patent applications or any future patent applications may not exclude competitors or may not provide a competitive advantage to us. In addition, patents issued or licensed to us may not be held valid if subsequently challenged and others may claim rights in or ownership of such patents. In addition, the validity and breadth of claims in protective gear technology patents involve complex legal and factual questions and, therefore, the extent of their enforceability and protection is highly uncertain.

16

The following table lists our licensed and/or registered and pending trademarks:

| Country | Trade Mark | Application No | Registration No | Filing Date | Renewal Date | Status |

| China | Leatt | 6287824 | 6287824 | September 21, 2007 | February 20, 2020 | Registered |

| China | The Helmet for your Neck Device | 6287823 | 6287823 | September 21, 2007 | February 20, 2020 | Registered |

| CTM* | Leatt-Brace | 006313993 | 006313993 | September 19, 2007 | September 19, 2017 | Registered |

| CTM | The Helmet for your neck | 006314009 | 006314009 | September 19, 2007 | September 19, 2017 | Registered |

| CTM | Leatt | 006314017 | 006314017 | September 19, 2007 | September 19, 2017 | Registered |

| CTM | Device (The Helmet for your neck) | 006314132 | 006314132 | September 19, 2007 | September 19, 2017 | Registered |

| USA | ALPT | 77/742,823 | 3,926,378 | May 22, 2009 | March 1, 2021 | Registered |

| USA | Alternative Load Path Technology | 77/742,826 | 3868833 | May 22, 2009 | October 26, 2020 | Registered |

| CTM | Alternative Load Path Technology | 008358046 | 008358046 | June 11, 2009 | June 11, 2019 | Registered |

| CTM | Alternative Load Path | 008358061 | 008358061 | June 11, 2009 | June 11, 2019 | Registered |

| CTM | ALPT | 008358079 | 008358079 | June 11, 2009 | June 11, 2019 | Registered |

| USA | Leatt Device | 77/765,739 | 3,861,760 | June 23, 2009 | October 12, 2019 | Registered |

| CTM | Leatt Device | 008444168 | July 23, 2009 | July 23, 2019 | Registered | |

| Australia | Leatt | 1372902 | July 16, 2010 | Response to Official Action filed. | ||

| Japan | Leatt | 2010- 056635 | 5432253 | July 16, 2010 | August 12, 2021 | Registered |

| Australia | Leatt | 1385227 | September 22, 2010 | Response to Official Action to be filed. | ||

| Japan | Leatt | 2010-74427 | 5403909 | September 22, 2010 | September 22, 2020 | Registered |

| CTM | Leatt | 009395997 | 009395997 | September 23, 2010 | September 23, 2020 | Registered |

| Brazil | Leatt Brace | 829468323 | 829468323 | March 11, 2010 | March 11, 2020 | Registered |

| Brazil | Leatt Brace (Special Script) | 829994920 | 829994920 | November 24, 2008 | February 8, 2021 | Registered |

| Brazil | Leatt Brace (Special Script) | 829994939 | 829994939 | November 24, 2008 | February 8, 2021 | Registered |

| Brazil | Leatt (Special Script) | 830409432 | November 5, 2009 | Advertised December 8 2009. Pending examination. | ||

| Brazil | Leatt and Device | 830409440 | November 5, 2009 | Advertised December 8 2009. Pending examination. |

17

| Brazil | Leatt and Device | 902094165 | November 5, 2009 | Advertised December 8 2009. Pending examination. | ||

| Brazil | Leatt and Device | 902094149 | November 5, 2009 | Advertised December 8 2009. Pending examination. | ||

| Brazil | Leatt (Special Script) | 902094238 | November 5, 2009 | Advertised December 8 2009. Pending examination. | ||

| Brazil | Leatt and Device | 902094190 | November 5, 2009 | Advertised December 8 2009. Pending examination. | ||

| Canada | LEATT | 1535498 | July 13, 2011 | Response to office action filed | ||

| USA | BraceOn | 85/429,145 | September 22, 2011 | Response to office action filed | ||

| Australia | BraceOn | 1450772 | September 23, 2011 | Pending | ||

| CTM | BraceOn | 010288405 | September 23, 2011 | Response to office action filed | ||

| New Zealand | Leatt | 829603 | September 9, 2010 | September 9, 2020 | Registered | |

| New Zealand | Leatt | 831034 | September 27, 2010 | September 27, 2020 | Registered | |

| New Zealand | Leatt | 831035 | September 27, 2010 | September 27, 2020 | Registered | |

| New Zealand | Leatt | 831036 | September 27, 2010 | 27/9/2020 | Registered | |

| South Africa | DEVICE (NEW LOGO) | 2009/11856 | 2009/11856 | June 26, 2009 | June 26, 2019 | Registered |

| South Africa | DEVICE (NEW LOGO) | 2009/11857 | 2009/11857 | June 26, 2009 | June 26, 2019 | Registered |

| South Africa | DEVICE (NEW LOGO) | 2009/11858 | June 26, 2009 | June 26, 2019 | Advertised October 2011 | |

| South Africa | Leatt-Brace (Special Script) | 2004/08584 | 2004/08584 | May 28, 2004 | May 28, 2014 | Registered |

| South Africa | Leatt | 2006/22761 | 2006/22761 | September 26, 2006 | September 26, 2016 | Registered |

| South Africa | The Helmet for your Neck | 2006/22760 | 2006/22760 | September 26, 2006 | September 26, 2016 | Registered |

| South Africa | Helmet for your Neck Device | 2007/15892 | 2007/15892 | July 19, 2007 | July 19, 2017 | Registered |

| South Africa | Helmet for your Neck Device | 2007/15893 | July 19, 2007 | July 19, 2017 | Accepted February 3 2012 | |

| South Africa | Adventure Leatt and Device | 2008/15403 | 2008/15403 | July 4, 2008 | July 4, 2018 | Registered |

18

| South Africa | Adventure Leatt and Device | 2008/15404 | 2008/15404 | July 4, 2008 | July 4, 2018 | Registered |

| South Africa | Adventure Leatt and Device | 2008/15405 | 2008/15405 | July 4, 2008 | July 4, 2018 | Registered |

| South Africa | Adventure Brace | 2008/28131 | 2008/28131 | December 1, 2008 | December 1, 2018 | Registered |

| South Africa | Adventure Brace | 2008/28132 | 2008/28132 | December 1, 2008 | December 1, 2018 | Registered |

| South Africa | Adventure Brace | 2008/28133 | 2008/28133 | December 1, 2008 | December 1, 2018 | Registered |

| USA | Leatt | 85135308 | September 22, 2010 | Accepted |

____________________

* A Community Trade Mark or CTM, is any trademark which is pending registration or has been registered in the European Union as a whole (rather than on a national level within the EU). The CTM system creates a unified trademark registration system in Europe, whereby one registration provides protection by being enforceable in all member states of the EU.

____________________

From time to time, we have had to enforce our intellectual property rights through litigation and we may be required to do so in the future. Reverse engineering, unauthorized copying or other misappropriation of our technologies could enable third parties to benefit from our technologies without paying us. We cannot assure you that our competitors have not developed or will not develop similar products, will not duplicate our products, or will not design around any patents issued to or licensed by us. We believe that a loss of these rights would harm or cause a material disruption to our business and, our corporate strategy is to aggressively take legal action against any violators of our intellectual property rights, regardless of where they may be.

Our Employees

As of March 31, 2012, we employed 42 full-time employees and no part-time employees. The following table sets forth the number of our full-time employees by function as of March 30, 2012.

| Employee Function | Number |

| Executive | 5 |

| Internet Technology | 2 |

| Product | 5 |

| Marketing and Distribution | 10 |

| Finance and Logistics | 10 |

| Research and Development | 6 |

| Legal and Compliance | 2 |

| Customer Service | 2 |

| Total | 42 |

We are required to pay UIF, or unemployment insurance, for each of our South African employees. We are also required to withhold income taxes for our South African and U.S. based employees. We generally provide health care benefits and other standard benefits to our employees. We do not have any pension or retirement plans for any of our employees.

We believe that we maintain a satisfactory working relationship with our employees and we have not experienced any significant labor disputes or any difficulty in recruiting staff for our operations.

19

Regulations

The 2012 JOBS Act

We qualify as an “emerging growth company,” as defined in Title I of the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). An emerging growth company is defined as an issuer, including a foreign private issuer, with less than $1 billion of total annual gross revenues during the most recently completed fiscal year. The SEC has interpreted “total annual gross revenues” to mean total revenues as presented on the income statement presentation under U.S. GAAP, which for the Company was $17.9 million for the fiscal year ended December 31, 2011. We will retain our status as an emerging growth company until the earlier of: (1) the fifth anniversary of the date we first sold securities pursuant to an IPO registration statement; (2) the last day of the fiscal year in which we first exceed $1 billion in annual gross revenues; (3) the time we become a large accelerated filer (an SEC registered company with a public float of at least $700 million); or (4) the date on which we have, within the previous three years, issued $1 billion of nonconvertible debt, whether issued in a registered or unregistered offering and whether or not it is still outstanding at the determination date.

The JOBS Act provides scaled disclosure provisions for us, including, among other things: (a) permitting us to include only two years of audited financial statements in a registration statement filed under the Securities Act of 1933 for an IPO of common equity securities; (b) allowing us to comply with the smaller reporting company version of Item 402 of Regulation S-K (Executive Compensation); and (c) removing the requirement that our independent registered public accounting firm attest to the effectiveness of our internal control over financial reporting in accordance with Section 404(b) of the Sarbanes-Oxley Act of 2002. The JOBS Act also exempts us from the following additional compensation-related disclosure provisions that were imposed on U.S. public companies pursuant to the Dodd-Frank Act: the advisory “say-on-pay” vote on executive compensation required under Section 14A(a) of the Exchange Act; the Section 14A(b) requirements relating to shareholder advisory votes on golden parachute compensation; the Section 14(i) requirements for disclosure relating to the relationship between executive compensation and financial performance of the issuer; and the requirement of Dodd-Frank Act Section 953(b)(1), which will require disclosure as to the relationship between CEO and median employee pay.

Under Section 102(b)(1) of the JOBS Act, "emerging growth companies" can also delay adopting new or revised accounting standards until such time as those standards apply to private companies. However, we have irrevocably elected not to avail ourselves of this extended transition period for compliance with new or revised accounting standards and, therefore, we will be subject to the same new or revised accounting standards as other public companies that are not "emerging growth companies.

European Union Certification

All our products are compliant with applicable European Union directives, or CE certified, where appropriate. European Economic Community, or EEC, directive 89/686/EEC imposes mandatory accreditation of all Personal Protective Equipment, or PPE, products offered for sale in the EEC, including the Company’s Leatt-Brace® and body protection products. This means that these products must comply with: the basic Health and Safety requirements of the directive; certain chemical innocuousness tests prescribed in EN 340:2003 - Protective clothing – General Requirements; and the requirements relating to usage, care, cleaning, sizing and other information supplied with the product. Accordingly, all Leatt-Braces®, chest protectors and body protection products are CE certified. Only our peripheral products such as jackets, clothing, and caps are not covered.

In addition to the minimum requirements the Company complies with certain European Standards, or EN, specific to certain categories of PPE. An EN is a standard that has been adopted by one of the three recognized European Standardisation Organisations (ESOs): CEN, CENELEC or ETSI. It is produced by all interested parties (including manufacturers, users, consumers and regulators of a particular material, product, process or service) through a transparent, open and consensus based process. In the Company’s case these are the EN standards: EN 14021 Stone Shields; EN 1621-1 Limb Protectors; EN 1621-2 Back Protectors; and EN 1621-3 Chest Protectors. These standards are more performance related and, among other things, measure the performance of PPE at various intensity levels and under different environmental conditions. They also prescribe product labeling, tests for user comfort and ease of use. Also, where no specific standards exist such as with the brace, the ESO may, at its discretion, require tests that it thinks are appropriate.

Our products are not required to obtain similar certification in the U.S. or to be approved by the United States Food and Drug Administration.

20

Other Accreditation

We have also sought certification for certain of our products, such as the Moto R neck brace, by the SFI Foundation (USA), or the SFI. To attain SFI certification, a safety device must, every five years, pass a series of impact sled tests with an instrumented crash test dummy at a SFI accredited test lab, as well as flammability tests on various parts of the safety device. These tests are done according to the SFI38.1 specification which can be found at http://www.sfifoundation.com. SFI 38.1 accreditation is mandatory for any safety device that is used by participants in SFI sanctioned events worldwide (except for V8 racing in Australia). We also voluntarily submitted our Moto GPX neck brace to be tested by the in-house engineers of BMW Motorrad (Germany) and to be reviewed by KTM (Austria). We believe that such testing, while not mandatory, provides validation for our product’s performance.