Exhibit 99.1

NEWS RELEASE

Toronto, March 22, 2017

(in U.S. dollars unless otherwise noted)

Franco-Nevada Reports Strong Full-Year 2016 Results

Guidance exceeded and $110 million agreement to acquire second package of U.S. oil & gas royalties

Franco-Nevada’s CEO, David Harquail, commented: “Our diversified portfolio continues to perform very well. In 2016, we exceeded our recently increased guidance ranges for both Gold Equivalent Ounces1 (“GEOs”) and oil & gas revenues. The growth in 2016 is reflecting the contribution from acquisitions we made during the recent downturn and increased activity by many of the operators on our lands. Franco-Nevada has no debt and is growing its cash balances. We continue to see investment opportunities and Franco-Nevada has just agreed to acquire, for $110 million, oil & gas royalties on the Midland portion of the Permian Basin in Texas, U.S.”

2016 Q4 Financial Highlights

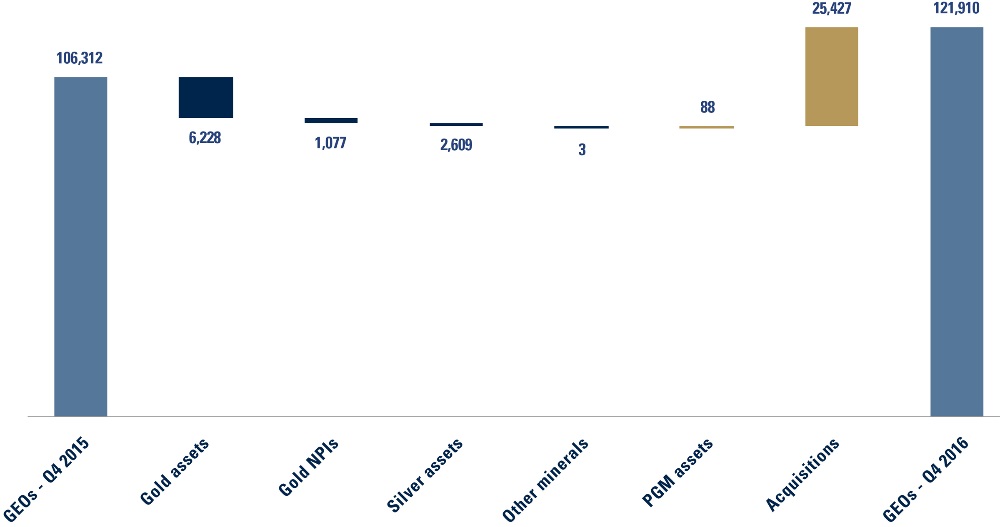

Record 129,036 GEOs delivered in the quarter, with 121,910 GEOs sold

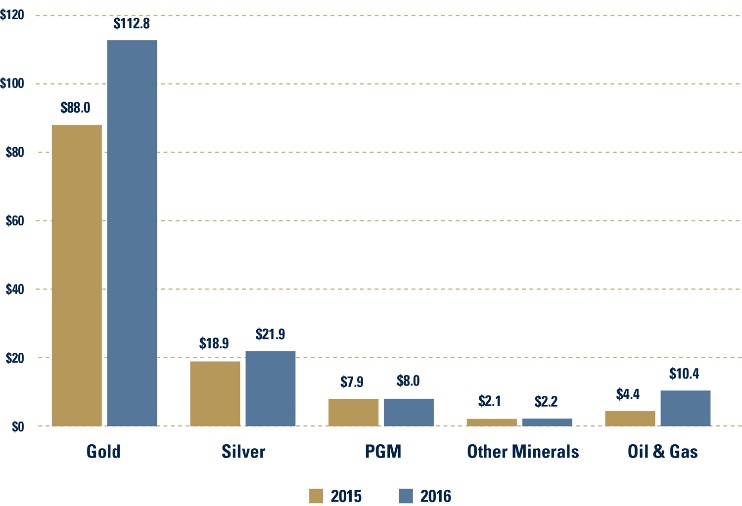

$155.3 million in revenue — a 28.0% increase over Q4/2015

$122.2 million of Adjusted EBITDA2 or $0.69 per share

$4.5 million of net loss, or $0.03 per share, reflecting impairment charges of $67.4 million on the Cooke 4 stream

$42.9 million of Adjusted Net Income3 or $0.24 per share

2016 Full Year Financial Highlights

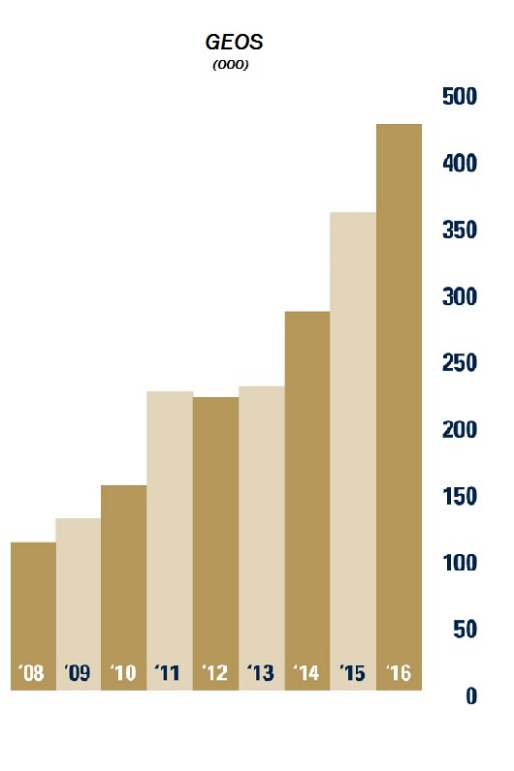

464,383 GEOs sold — a new record and a 29.0% increase year-over-year

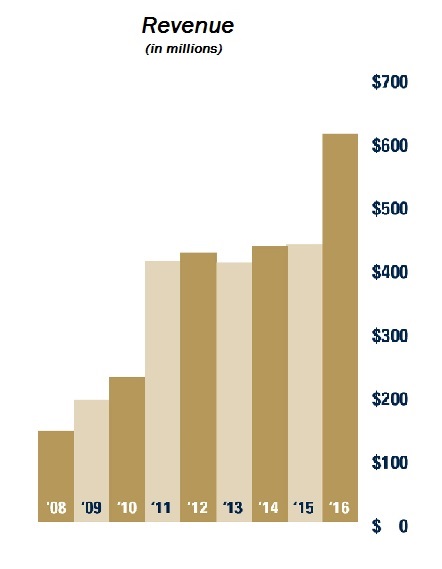

$610.2 million in revenue — a new record and a 37.6% increase year-over-year

$489.1 million of Adjusted EBITDA2 or $2.79 per share

$122.2 million of net income, or $0.70 per share

$164.4 million of Adjusted Net Income3 or $0.94 per share

$157.8 million of cash and DRIP dividends paid

$253.0 million in cash and cash equivalents at year-end and no debt

|

Revenue and GEOs by Asset Categories |

|

| Q4/2016 |

|

| Q4/2015 | ||||||

|

| Revenue |

| GEOs |

|

| Revenue |

| GEOs | ||

|

| (in millions) |

| # |

|

| (in millions) |

| # | ||

Precious Metals |

|

|

|

|

|

|

|

|

|

|

|

Gold |

| $ | 112.8 |

| 93,775 |

|

| $ | 88.0 |

| 79,800 |

Silver |

|

| 21.9 |

| 18,650 |

|

|

| 18.9 |

| 17,112 |

PGM |

|

| 8.0 |

| 7,611 |

|

|

| 7.9 |

| 7,523 |

Precious Metals - Total |

| $ | 142.7 |

| 120,036 |

|

| $ | 114.8 |

| 104,435 |

Other Minerals |

|

| 2.2 |

| 1,874 |

|

|

| 2.1 |

| 1,877 |

Oil & Gas |

|

| 10.4 |

| — |

|

|

| 4.4 |

| — |

|

| $ | 155.3 |

| 121,910 |

|

| $ | 121.3 |

| 106,312 |

2 | 2016 Annual Report | FNV TSX NYSE |

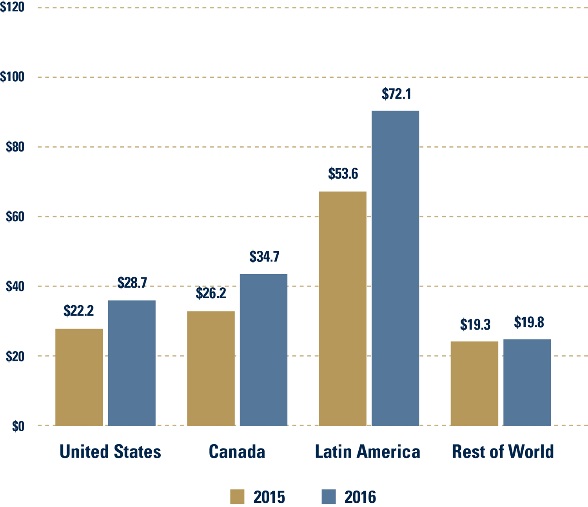

For Q4/2016, revenue was sourced 91.9% from precious metals (72.6% gold, 14.1% silver and 5.2% PGM) and 87.2% from the Americas (18.5% U.S., 22.3% Canada and 46.4% Latin America). Operating costs and expenses decreased slightly year-over-year, reflecting a realized gain of $14.1 million on the partial buy back of the Kirkland Lake NSR. Oil & gas revenue increased 136%, reflecting both higher prices and production levels year-over-year. Cash provided by operating activities was $121.9 million, an increase of 43.5% compared to Q4/2015.

Corporate Updates

Credit Facilities: On March 22, 2017, Franco-Nevada extended the term of its existing $1 billion credit facility from November 12, 2020 to March 22, 2022. In addition, on March 20, 2017, Franco-Nevada’s subsidiary, Franco-Nevada (Barbados) Corporation, entered into an unsecured revolving credit facility which provides for the availability of up to $100 million in borrowings.

Midland oil & gas royalties: On March 13, 2017, Franco-Nevada agreed to purchase a portfolio of oil & gas royalties in the Midland shale play of the Permian Basin of Texas for $110 million. Closing is expected in the second quarter of 2017.

STACK oil & gas royalties: On December 19, 2016, Franco-Nevada acquired a $100 million portfolio of oil & gas royalty rights in the Sooner Trend, Anadarko Basin, Canadian and Kingfisher counties (“STACK”) play in Oklahoma’s Anadarko basin.

Kirkland Lake royalty buy back: In October 2016, Kirkland Lake Gold exercised its option to buy back 1% of an overlying 2.5% net smelter return royalty for aggregate cash consideration of $30.3 million. Franco-Nevada recorded a gain on disposal of $14.1 million.

Cooke 4 stream impairment: In October 2016, Sibanye Gold Limited announced that it had ceased production at the Cooke 4 mine. Franco-Nevada recorded an impairment charge of $67.4 million.

Antapaccay stream: On February 26, 2016, Franco-Nevada acquired a $500 million precious metals stream from Glencore plc with reference to production from the Antapaccay mine located in Peru.

Equity financing: On February 19, 2016, Franco-Nevada completed a bought deal financing with a syndicate of underwriters for 19.2 million common shares at $47.85 per common share. Net proceeds were $884.3 million.

2017 Guidance

In 2017, Franco-Nevada expects attributable royalty and stream production to total 470,000 to 500,000 GEOs from its mineral assets and revenue of $35 million to $45 million from its oil & gas assets. Of the royalty and stream production, 335,000 to 345,000 GEOs are expected from Franco-Nevada’s various stream agreements. For 2017 guidance, silver, platinum and palladium metals have been converted to GEOs using assumed commodity prices of $1,200/oz Au, $17.50/oz Ag, $950/oz Pt and $750/oz Pd. The WTI oil price is assumed to average $50 per barrel with a $3.50 per barrel price differential between the Edmonton Light and realized prices for Canadian oil. The Company estimates depletion expense of $265 million to $295 million. 2017 guidance and 2021 outlook below is based on assumptions including the forecasted state of operations from our assets based on the public statements and other disclosures by the third-party owners and operators of the the underlying properties (subject to our assessment thereof).

2021 Outlook

Our outlook to 2021 further assumes that the Cobre Panama project will be ramping up production in 2019. At the same time, scheduled fixed ounce payments from Midas/Fire Creek, Karma and Sabodala are expected to step down to longer term royalty or stream payments. Using the same commodity price assumptions as were used for our 2017 guidance (see above) and assuming no other acquisitions, Franco-Nevada expects its existing portfolio to generate between 515,000 to 540,000 GEOs by 2021. Oil & gas revenues at the same $50 per barrel WTI oil price assumption are expected to range between $55 million and $65 million.

Q4/2016 Portfolio Updates

Precious Metals — U.S.: GEOs from U.S. precious metals assets increased by 14.5% year-over-year with decreases from Goldstrike being more than offset by payments received from the South Arturo mine. GEOs received from the U.S. precious metal assets were 22,971 GEOs.

South Arturo (4‑9% royalty) — This project, operated by Barrick and Premier Gold, poured its first gold in August. Q4/2016 payments represented 8,808 GEOs. The partners are looking at a second open pit (Dee) on the property and are advancing permitting for the El Nino underground opportunity below the current pit.

Goldstrike (2‑4% royalty & 2.4‑6% NPI) — Barrick is unitizing Goldstrike in an effort to reduce AISC by $100 per ounce which would benefit the profit royalty.

Bald Mountain (0.875‑5% royalty) — Kinross reported that it has doubled reserves at this project to 2.1 million gold ounces.

Stillwater (5% royalty) — Stillwater Mining now anticipates that the Blitz project will add between 270,000 and 330,000 PGM ounces of incremental production annually when fully ramped up by 2021‑2022.

The Gold Investment that WORKS | Franco-Nevada Corporation |

| 3 |

Precious Metals — Canada: GEOs from Canadian precious metals assets increased by approximately 8.6% to 20,849 GEOs compared with Q4/2015.

Hemlo (3% royalty & 50% NPI) — The main contributor to the increase in Canadian GEOs was the Hemlo NPI. Barrick has increased reserves at Hemlo including the Interlake and C-Zone Deep zones to which the royalties apply.

Hardrock (3% royalty) — Centerra Mining and Premier Gold presented a feasibility for a 14.5 year project with production averaging 300,000 gold ounces per year. A draft EA has been submitted.

Detour (2% royalty) — Detour Gold has had challenges in getting approvals for its West Detour pit and is expected to provide an alternative mine plan.

Holloway (sliding scale royalty) — In Q4, Kirkland Lake Gold announced its intention to put Holloway on care and maintenance. The Holloway royalty property encompasses the Holt mine property on which Franco-Nevada also receives royalties. Mining at Holt is expected to extend onto the Holloway property in the near term. At December 31, 2016, Franco-Nevada has recovered its initial investment in the Holloway mine.

Brucejack (1.2% royalty) — Pretium Resources expects to begin commissioning of the underground mine in mid‑2017.

Timmins West (2.25% royalty) — Tahoe Resources expects to provide a reserve estimate for the Gap 144 zone in Q3/2017.

Precious Metals — Latin America: GEOs from Latin American precious metals assets represented the largest year-over-year increase due to the addition of the Antapaccay stream. Precious metal GEOs earned from Latin America were 60,808 GEOs, an increase of 26.0% year-over-year.

Antapaccay (gold and silver stream) — Antapaccay delivered 22,927 GEOs in Q4/2016, for a total of 73,612 GEOs in 2016.

Antamina (22.5% silver stream) — Antamina delivered 10,619 GEOs during the quarter compared to 13,021 GEOs in Q4/2015, reflecting adjustments for final settlements of provisionally priced sales. For the full year 2016, Antamina delivered 60,273 GEOs.

Candelaria (gold and silver stream) — Candelaria earned 19,698 GEOs, compared to 21,846 GEOs in the prior year quarter, as expected according to its mine plan. Since acquisition, contained copper and gold in the reserves have increased by approximately 50% when mined depletion is included and the production profile has significantly improved.

Guadalupe (50% gold stream) — The 400,000 minimum ounce Palmarejo obligation was paid and fully met by Coeur Mining in Q3. That resulted in the original Palmarejo gold stream being terminated and the new Guadalupe stream commencing. During Q4, Franco-Nevada received 7,058 GEOs under the new Guadalupe agreement.

Cobre Panama (gold and silver stream) — During the quarter, Franco-Nevada contributed $46.6 million of its share of construction capital for the Cobre Panama project. Franco-Nevada at quarter-end has contributed $462.2 million of its total $1 billion commitment for the construction of Cobre Panama. First Quantum reported that the project was 46% complete as of year-end and that initial production in expected in late 2018 with ramping up through 2019. Franco-Nevada expects to contribute between $200‑$220 million to the project in 2017.

Precious Metals — Rest of World: GEOs from Rest of World precious metals assets were 15,408 GEOs during the quarter, a 9.0% decrease year-over-year. This reflected lower production at MWS and that a portion of ounces delivered from Karma and Sabodala had not been sold as at quarter-end.

Karma (fixed gold deliveries and stream) — 3,750 GEOs were delivered in the quarter of which 2,500 were sold in Q4/2016.

Sabodala (fixed gold deliveries and stream) — 5,625 GEOs were delivered in the quarter, of which 3,750 were sold in Q4/2016. Teranga Gold won the PDAC award for Environmental & Social Responsibility for its work around the Sabodala mine.

Edikan (1.5% royalty) — Perseus Mining completed an upgrade to the plant in October 2016 and is now reporting improved operating performance.

Sissingué (0.5% royalty) — Perseus Mining reports that this project has been in full scale development since July 2016 and expects first production in the March 2018 quarter. Perseus has also secured financing of $40 million to complete the development of the project.

Cerro Morro (2% royalty) — Yamana is targeting a Q2/2018 start-up.

Tasiast (2% royalty) — Kinross continues to advance development of the Tasiast Phase One expansion and expects to provide a feasibility for a possible Phase Two expansion in Q3/2017.

Subika (2% royalty) — Newmont Mining is expected to make a decision in the first half of 2017 regarding the underground development of Subika and expanding the Ahafo mill.

Agi Dagi (2% royalty) — Alamos Gold has tabled a positive feasibility for the project projecting annual production of 177,600 ounces of gold over 5 years. A positive PEA was also completed for the neighboring Camyurt project on which Franco-Nevada also holds a royalty.

Oil & Gas: Revenue from oil & gas assets increased to $10.4 million in Q4/2016 compared to $4.4 million in Q4/2015, reflecting both higher prices and production levels year-over-year.

4 | 2016 Annual Report | FNV TSX NYSE |

Acquisition of U.S. Oil & Gas Royalties — Midland Basin: On March 13, 2017, Franco-Nevada, through its wholly-owned U.S. subsidiary, agreed to purchase a package of royalty rights in the Midland Basin of West Texas for a price of $110 million. The Midland Basin forms the eastern portion of the broader Permian Basin and represents one of the most active and profitable oil plays in North America. The royalties consist of approximately 97% mineral title rights, along with some GORRs, which apply to approximately 908 acres (net after royalties) that, with pooling, provides exposure to an estimated gross acreage of 675,000 acres (a significant portion of the overall Midland Basin) at an estimated average royalty rate of 0.14%. The royalties are subject to a diverse operator base, which is anchored by Pioneer Natural Resources. Royalty revenue is expected to grow in future years as horizontal drilling activity in the area continues to ramp up. The transaction is expected to close in the second quarter of 2017.

Shareholder Information and 2017 Asset Handbook

The complete Consolidated Annual Financial Statements and Management’s Discussion and Analysis can be found today on Franco-Nevada’s website at www.franco-nevada.com, on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

Management will host a conference call tomorrow, Thursday, March 23, 2017 at 11:00 a.m. Eastern Time to review Franco-Nevada’s 2016 results, as well as discuss the 2017 and five-year outlook. In addition, Franco-Nevada will be releasing its 2017 Asset Handbook with updated disclosures on our assets and the number of gold ounces and royalty equivalent units associated with each asset.

Interested investors are invited to participate as follows:

Via Conference Call: Toll-Free: (888) 231‑8191; International: (647) 427‑7450

Conference Call Replay until March 30: Toll-Free (855) 859‑2056; Toronto (416) 849‑0833; Pass code 66380664

Webcast: A live audio webcast will be accessible at www.franco-nevada.com

Corporate Summary

Franco-Nevada Corporation is the leading gold-focused royalty and stream company with the largest and most diversified portfolio of cash-flow producing assets. Its business model provides investors with gold price and exploration optionality while limiting exposure to many of the risks of operating companies. Franco-Nevada is debt free and uses its free cash flow to expand its portfolio and pay dividends. It trades under the symbol FNV on both the Toronto and New York stock exchanges. Franco-Nevada is the gold investment that works.

For more information, please go to our website at www.franco-nevada.com or contact:

Stefan Axell |

| Sandip Rana |

Director, Corporate Affairs |

| Chief Financial Officer |

(416) 306‑6328 |

| (416) 306‑6303 |

info@franco-nevada.com |

|

|

NON-IFRS MEASURES: Adjusted Net Income and Adjusted EBITDA are intended to provide additional information only and do not have any standardized meaning prescribed under IFRS and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These measures are not necessarily indicative of operating profit or cash flow from operations as determined under IFRS. Other companies may calculate these measures differently. For a reconciliation of these measures to various IFRS measures, please refer to pages 37 to 39 of the Company’s current MD&A disclosure found in this Annual Report and on the Company’s website, on SEDAR and on EDGAR. Comparative information has been recalculated to conform to current presentation.

1GEOs include our gold, silver, platinum, palladium and other mineral assets. GEOs are estimated on a gross basis for NSR royalties and, in the case of stream ounces, before the payment of the per ounce contractual price paid by the Company. For NPI royalties, GEOs are calculated taking into account the NPI economics. Platinum, palladium, silver and other minerals are converted to GEOs by dividing associated revenue, which includes settlement adjustments, by the relevant gold price. The gold price used in the computation of GEOs earned from a particular asset varies depending on the royalty or stream agreement, which may make reference to the market price realized by the operator, or the average for the month, quarter, or year in which the mineral was produced or sold. For Q4/2016, the average commodity prices were as follows: $1,218 gold (2015 - $1,104), $17.18 silver (2015 - $14.76), $944 platinum (2015 - $908) and $684 palladium (2015 - $606).

2Adjusted EBITDA and Adjusted EBITDA per share are non-IFRS financial measures, which exclude the following from net income and EPS: income tax expense/recovery; finance expenses; finance income; depletion and depreciation; non-cash costs of sales; impairment charges related to royalty, stream and working interests and investments; gains/losses on sale of royalty interests; gains/losses on investments; and foreign exchange gains/losses and other income/expenses.

3Adjusted Net Income and Adjusted Net Income per share are non-IFRS financial measures, which exclude the following from net income and earnings per share (“EPS”): foreign exchange gains/losses and other income/expenses; impairment charges related to royalty, stream and working interests and investments; gains/losses on sale of royalty interests; gains/losses on investments; unusual non-recurring items; and the impact of income taxes on these items.

Please refer to Cautionary Statement on Forward-Looking Information on page 40 of this Annual Report.

The Gold Investment that WORKS | Franco-Nevada Corporation |

| 5 |

|

MANAGEMENT’S DISCUSSION AND ANALYSIS |

This Management’s Discussion and Analysis (“MD&A”) of financial position and results of operations of Franco-Nevada Corporation (“Franco-Nevada”, the “Company”, “we” or “our”) has been prepared based upon information available to Franco-Nevada as at March 22, 2017 and should be read in conjunction with Franco-Nevada’s audited consolidated financial statements and related notes as at and for the year ended December 31, 2016 and 2015. The audited consolidated financial statements and MD&A are presented in U.S. dollars and have been prepared in accordance with International Financial Reporting Standards (“IFRS”) as issued by the International Accounting Standards Board (“IASB”).

Readers are cautioned that the MD&A contains forward-looking statements and that actual events may vary from management’s expectations. Readers are encouraged to read the “Cautionary Statement on Forward-Looking Information” at the end of this MD&A and to consult Franco-Nevada’s audited consolidated financial statements for the years ended December 31, 2016 and 2015 and the corresponding notes to the financial statements which are available on our website at www.franco-nevada.com, on SEDAR at www.sedar.com and in our most recent Form 40‑F filed with the Securities and Exchange Commission on EDGAR at www.sec.gov.

Additional information related to Franco-Nevada, including our Annual Information Form, is available on SEDAR at www.sedar.com, and our Form 40‑F is available on EDGAR at www.sec.gov. These documents contain descriptions of certain of Franco-Nevada’s producing and advanced royalty and stream assets, as well as a description of risk factors affecting the Company. For additional information, our website can be found at www.franco-nevada.com.

TABLE OF CONTENTS

7 | |

8 | |

10 | |

11 | |

12 | |

13 | |

16 | |

23 | |

29 | |

30 | |

31 | |

34 | |

36 | |

36 | INTERNAL CONTROL OVER FINANCIAL REPORTING AND DISCLOSURE CONTROLS AND PROCEDURES |

37 | |

40 |

Abbreviations used in this report |

The following abbreviations may be used throughout this MD&A:

Abbreviated Definitions

Periods under review | Interest types | Measurement | |||

“Q4/2016” | The three-month period ended December 31, 2016 | “NSR” | Net smelter return royalty | “GEO” | Gold equivalent ounces |

“Q3/2016” | The three-month period ended September 30, 2016 | “GR” | Gross royalty | “oz” | Ounce |

“Q2/2016” | The three-month period ended June 30, 2016 | “ORR” | Overriding royalty | “oz Au” | Ounce of gold |

“Q1/2016” | The three-month period ended March 31, 2016 | “GORR” | Gross overriding royalty | “oz Ag” | Ounce of silver |

“Q4/2015” | The three-month period ended December 31, 2015 | “FH” | Freehold or lessor royalty | “oz Pt” | Ounce of platinum |

|

| “NPI” | Net profits interest | “oz Pd” | Ounce of palladium |

Places and currencies | “NRI” | Net royalty interest | “LBMA” | London Bullion Market Association | |

“U.S.” | United States | “WI” | Working interest | “bbl” | Barrel |

“$” or “USD” | United States dollars |

|

| “boe” | Barrels of oil equivalent |

“C$” or “CAD” | Canadian dollars |

|

| “WTI” | West Texas Intermediate |

6 | 2016 Annual Report | FNV TSX NYSE |

BUSINESS OVERVIEW AND STRATEGY

Franco-Nevada is the leading gold-focused royalty and stream company by both gold revenue and number of gold assets. The Company has the largest and most diversified portfolio of royalties and streams by commodity, geography, revenue type and stage of project. The portfolio is actively managed with the aim to maintain over 80% of revenue from precious metals (gold, silver & PGM).

Franco-Nevada Asset Count at March 22, 2017 |

|

| Precious Metals |

| Other Minerals |

| Oil & Gas |

| TOTAL |

Producing |

| 41 |

| 5 |

| 61 | (1) | 107 |

Advanced |

| 34 |

| 7 |

| — |

| 41 |

Exploration |

| 135 |

| 37 |

| 19 |

| 191 |

TOTAL |

| 210 |

| 49 |

| 80 |

| 339 |

(1)Includes acquisition of Midland Basin royalties expected to close in Q2/2017.

The Company does not operate mines, develop projects or conduct exploration. Franco-Nevada’s business model is focused on managing and growing its portfolio of royalties and streams. The advantages of this business model are:

Exposure to precious metals price optionality;

A perpetual discovery option over large areas of geologically prospective lands with no additional cost other than the initial investment;

Limited exposure to many of the risks associated with operating companies;

A free cash-flow business with limited cash calls;

A high-margin business that can generate cash through the entire commodity cycle;

A scalable and diversified business in which a large number of assets can be managed with a small stable overhead; and

A forward-looking business in which management focuses on growth opportunities rather than operational or development issues.

Franco-Nevada’s financial results in the short-term are primarily tied to the price of commodities and the amount of production from its portfolio of producing assets. Financial results have also been supplemented by acquisitions of new producing assets. Over the longer-term, results are impacted by the availability of exploration and development capital applied by other companies to expand or extend Franco-Nevada’s producing assets or to advance Franco-Nevada’s advanced and exploration assets into production.

Franco-Nevada has a long-term investment outlook and recognizes the cyclical nature of the industry. Franco-Nevada has historically operated by maintaining a strong balance sheet so that it can make investments during commodity cycle downturns.

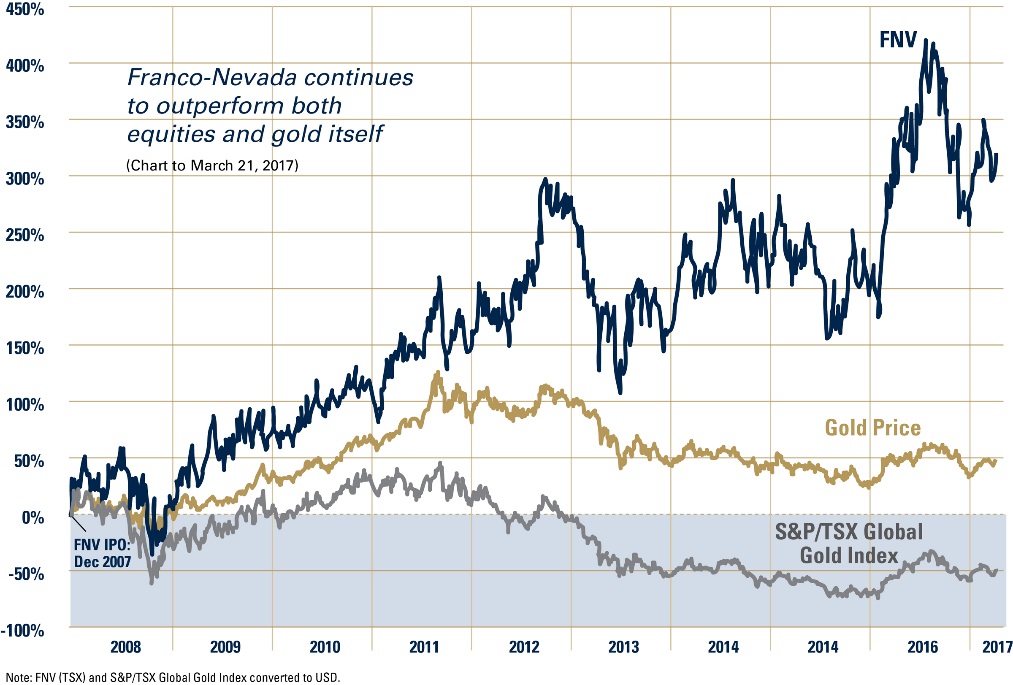

Franco-Nevada’s shares are listed on the Toronto and New York stock exchanges under the symbol FNV. An investment in Franco-Nevada’s shares is expected to provide investors with yield and exposure to gold price and exploration optionality while limiting exposure to many of the risks of operating companies. Since its Initial Public Offering (“IPO”) nine years ago, Franco-Nevada has increased its dividend annually and its share price has outperformed the gold price and all relevant gold equity benchmarks.

Franco-Nevada’s revenue is generated from various forms of agreements, ranging from net smelter return royalties, streams, net profits interests, net royalty interests, working interests and other. For definitions of the various types of agreements, please refer to our most recent Annual Information Form filed on SEDAR at www.sedar.com or our Form 40‑F filed on EDGAR at www.sec.gov.

The Gold Investment that WORKS | Franco-Nevada Corporation |

| 7 |

Franco-Nevada’s Relative Share Price Performance |

Financial Update — Q4/2016

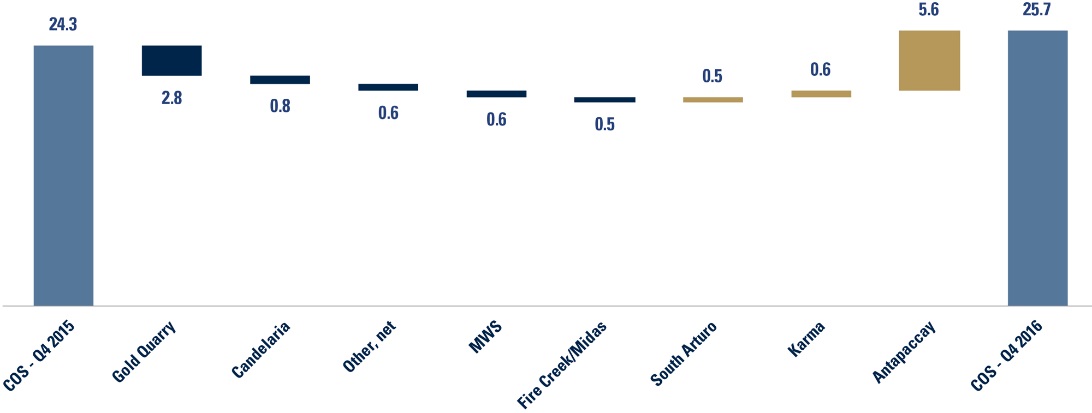

129,036 GEOs1 delivered in Q4/2016, an increase of 21.4% compared to 106,312 GEOs in Q4/2015.

121,910 GEOs recognized in revenue in Q4/2016, an increase of 14.7% from 106,312 GEOs in Q4/2015;

$155.3 million in revenue, an increase of 28.0% from revenue of $121.3 million in Q4/2015;

$122.2 million, or $0.69 per share, of Adjusted EBITDA2,3 in Q4/2016, an increase of 29.7% from $94.2 million or $0.60 per share, in Q4/2015;

78.7% in Margin2,3, compared to 77.7% in Q4/2015;

$4.5 million, or $0.03 per share, in net loss for Q4/2016, compared to a loss of $31.4 million, or $0.20 per share, in Q4/2015. The Q4/2016 net loss includes an impairment of $67.4 million on the Company’s Cooke 4 stream;

$42.9 million, or $0.24 per share, in Adjusted Net Income2,3 in Q4/2016, an increase of 81.0% compared to $23.7 million, or $0.15 per share, in Q4/2015;

$121.9 million in net cash provided by operating activities3 in Q4/2016, an increase of 43.5% compared to $84.9 million in Q4/2015;

$39.7 million in dividends paid in Q4/2016, of which $30.7 million was paid in cash and $9.0 million was paid in common shares issued under the Company’s Dividend Reinvestment Plan (“DRIP”), compared to $32.3 million in dividends paid in Q4/2015; and

$1.4 billion in available capital at December 31, 2016, comprising of $323.6 million of working capital, $114.6 million in marketable equity securities, and $1 billion available under the Company’s credit facility. Of this, $110.0 million will be used to fund the Company’s acquisition of the Midland Basin oil royalty interest which is expected to close in the second quarter of 2017.

1GEOs include our gold, silver, platinum, palladium and other mineral assets, and do not include Oil & Gas assets. GEOs are estimated on a gross basis for NSR royalties and, in the case of stream ounces, before the payment of the per ounce contractual price paid by the Company. For NPI royalties, GEOs are calculated taking into account the NPI economics. Silver, platinum, palladium and other minerals are converted to GEOs by dividing associated revenue, which includes settlement adjustments, by the relevant gold price. The gold price used in the computation of GEOs earned from a particular asset varies depending on the royalty or stream agreement, which may make reference to the market price realized by the operator, or the average for the month, quarter, or year in which the mineral was produced or sold. For illustrative purposes, please refer to average commodity price tables on pages 16 and 23 of this MD&A for indicative prices which may be used in the calculation of GEOs.

2Adjusted Net Income, Adjusted EBITDA and Margin are non-IFRS financial measures with no standardized meaning under IFRS. For further information and a detailed reconciliation, please see pages 37‑39 of this MD&A.

3In Q3/2016, the Company adopted a retrospective change in accounting policy with respect to its classification of proceeds from sales of gold bullion in its statement of cash flows and statement of income and comprehensive income (loss). For further information, refer to Note 2(b) of the consolidated financial statements for the year ended December 31, 2016. The Company’s non-IFRS measures, as defined in pages 37‑39 of this MD&A, were also adjusted accordingly to reflect gains/losses on sales of such gold bullion as an operating activity that is part of the Company’s underlying operating business. Comparative information has been adjusted to conform to current presentation.

8 | 2016 Annual Report | FNV TSX NYSE |

Financial Update — 2016

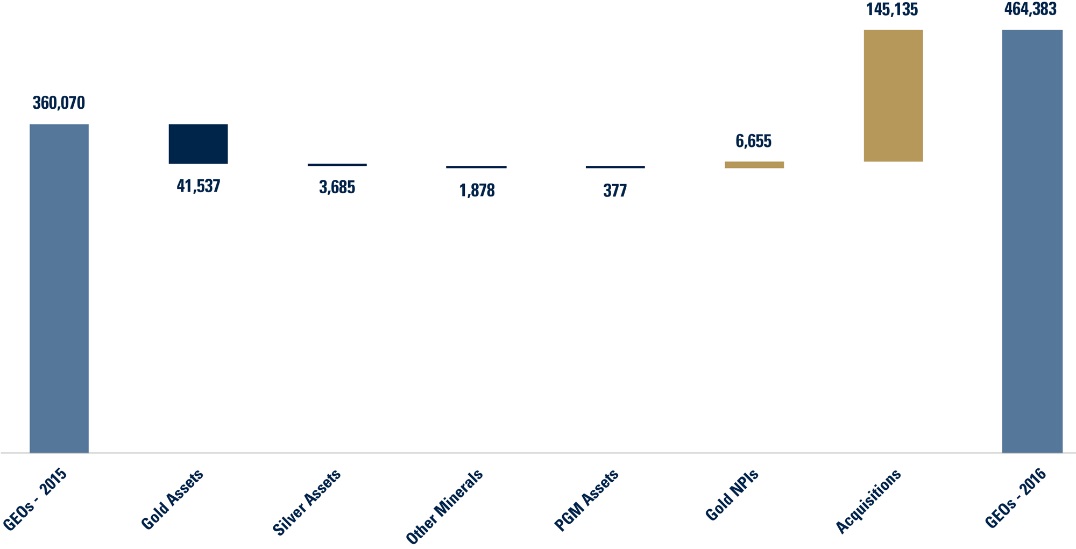

471,509 GEOs delivered in 2016, an increase of 30.9% from 360,070 GEOs delivered in 2015;

464,383 GEOs recognized in revenue in 2016, an increase of 29.0% from 360,070 GEOs in 2015;

$610.2 million in revenue in 2016, an increase of 37.6% from revenue of $443.6 million in 2015;

$489.1 million, or $2.79 per share, in Adjusted EBITDA in 2016, an increase of 45.1% from $337.1 million, or $2.16 per share, in 2015;

80.2% in Margin in 2016, compared to 76.0% in 2015;

$122.2 million, or $0.70 per share, in net income in 2016, an increase of 396.7% compared to net income of $24.6 million, or $0.16 per share, in 2015;

$164.4 million, or $0.94 per share, in Adjusted Net Income in 2016, an increase of 84.9% compared to $88.9 million, or $0.57 per share, in 2015;

$471.0 million in net cash provided by operating activities in 2016, compared to $314.3 million in 2015; and

$156.8 million in dividends paid in 2016, which included cash dividends of $118.1 million and $38.7 million in issued common shares under the Company’s DRIP, compared to $129.0 million in dividends paid in 2015.

Corporate Development

Acquisition of U.S. Oil & Gas Royalties — Midland Basin

On March 13, 2017, Franco-Nevada, through its wholly-owned U.S. subsidiary, agreed to purchase a package of royalty rights in the Midland Basin of West Texas for a price of $110.0 million. The Midland Basin forms the eastern portion of the broader Permian Basin and represents one of the most active and profitable oil plays in North America. The royalties consist of approximately 97% mineral title rights, along with some GORRs, which apply to approximately 908 acres (net after royalties) that, with pooling, provides exposure to an estimated gross acreage of 675,000 acres (a significant portion of the overall Midland Basin) at an estimated average royalty rate of 0.14%. The royalties are subject to a diverse operator base, which is anchored by Pioneer Natural Resources. Royalty revenue is expected to grow in future years as horizontal drilling activity in the area continues to ramp up. The transaction is expected to close in the second quarter of 2017.

Acquisition of U.S. Oil & Gas Royalties — STACK

On December 19, 2016, Franco-Nevada, through its wholly-owned U.S. subsidiary, acquired a package of royalty rights in the Sooner Trend, Anadarko Basin, Canadian and Kingfisher counties (“STACK”) shale play in Oklahoma’s Anadarko Basin for a price of $100.0 million. The two primary operators of the lands are Newfield Exploration Company and Devon Energy Corporation. Both companies have stated that STACK is a major focus of their capital spending, a portion of which is expected to be on the royalty lands. Full-field development is expected to begin in 2017 and is expected to grow royalty revenue in future years. The royalties consist of mineral title rights and GORRs which apply to approximately 1,200 acres (net after royalties) that, with pooling, provides exposure to an estimated gross acreage of 74,880 acres with an estimated average royalty rate of 1.61%.

Buy-Back of Kirkland Lake Gold Royalty

In October 2016, Kirkland Lake Gold (“Kirkland Lake”) exercised its option to buy back 1% of an overlying 2.5% NSR for aggregate cash consideration of $30.3 million ($36.0 million less royalty proceeds previously received attributable to the buy-back portion of the NSR). The Company recognized a gain on disposal of $14.1 million in the consolidated statement of income and comprehensive income (loss) for the year ended December 31, 2016.

Impairment of Cooke 4

On October 27, 2016, Sibanye Gold Limited (“Sibanye”) announced that it had ceased production at the Cooke 4 underground operation. Management assessed the cessation of operations as an indicator of impairment, and accordingly, performed an impairment assessment. The Company recorded an impairment charge of $67.4 million in its statement of income and comprehensive income (loss) for the year ended December 31, 2016.

Termination of Palmarejo Gold Stream and Commencement of Guadalupe Gold Stream

In October 2014, Franco-Nevada agreed with Coeur Mining Inc. (“Coeur”) to terminate the Palmarejo gold stream agreement following the completion of the 400,000 ounce minimum obligation in exchange for a cash payment of $2.0 million. In July 2016, Coeur met the minimum ounce obligation and the Palmarejo agreement was terminated. Deliveries of gold ounces from the Palmarejo project will start under a new agreement with Coeur, the Guadalupe gold stream agreement, pursuant to which Coeur will deliver 50% of its gold production from the Palmarejo project at an ongoing cost of $800 per ounce (no inflation adjustment). As part of the Guadalupe agreement, Franco-Nevada provided an upfront deposit of $22.0 million to partially fund the development of the Guadalupe underground mine.

Funding of Cobre Panama

The Company funded an additional $46.6 million towards the Cobre Panama precious metals stream in Q4/2016, for a total of $124.3 million in 2016. As at December 31, 2016, the Company has funded $462.2 million of its $1 billion commitment. First Quantum Minerals Ltd. (“First Quantum”) expects total capital expenditures of $1,060 million in 2017. According to First Quantum, the project was 46% complete as of year-end, total expected capital expenditure for the project is unchanged at $5.48 billion and development remains on track for a phased commissioning in late 2018 and continued ramp-up in 2019.

The Gold Investment that WORKS | Franco-Nevada Corporation |

| 9 |

Acquisition of Antapaccay Precious Metals Stream

On February 26, 2016, Franco-Nevada completed the acquisition of a $500.0 million precious metals stream from Glencore plc with reference to production from the Antapaccay mine located in Peru. Under the stream agreement, gold and silver deliveries are initially referenced to copper in concentrate shipped. The Company will receive 300 ounces of gold and 4,700 ounces of silver for each 1,000 tonnes of copper in concentrate shipped, until 630,000 ounces of gold and 10.0 million ounces of silver have been delivered. Thereafter, the Company will receive 30% of the gold and silver in concentrate shipped. The Company will pay an on-going price of 20% of the spot price of gold and silver until 750,000 ounces of refined gold and 12.8 million ounces of refined silver have been delivered. Thereafter, the on-going price will increase to 30% of the spot price of gold and silver.

Financing

On March 22, 2017, the Company extended the maturity term of its existing $1 billion credit facility, from November 12, 2020 to March 22, 2022.

On March 20, 2017, Franco-Nevada’s subsidiary, Franco-Nevada (Barbados) Corporation, entered into an unsecured revolving credit facility (the “FNBC Credit Facility”). The FNBC Credit Facility provides for the availability over a one-year period of up to $100.0 million in borrowings. Refer to “Liquidity and Capital Resources” for details.

On February 19, 2016, the Company completed a bought-deal financing with a syndicate of underwriters for 19.2 million common shares at $47.85 per common share. The net proceeds to the Company were $883.5 million after deducting share issue costs and expenses of $36.6 million.

The following contains forward-looking statements. Reference should be made to the “Cautionary Statement on Forward-Looking Information” section at the end of this MD&A. For a description of material factors that could cause our actual results to differ materially from the forward-looking statements below, please see the Cautionary Statement and the “Risk Factors” section of our most recent Annual Information Form filed with the Canadian securities regulatory authorities on www.sedar.com and our most recent Form 40‑F filed with the Securities and Exchange Commission on www.sec.gov. 2017 guidance is based on assumptions including the forecasted state of operations from our assets based on the public statements and other disclosures by the third-party owners and operators of the underlying properties (subject to our assessment thereof).

For 2017, the Company is pleased to provide the following guidance:

|

|

|

|

|

|

|

|

|

|

|

| 2017 Guidance |

| 2016 Actual |

| 2015 Actual | |||

Mineral assets - GEO production1, 2 |

|

| 470,000 - 500,000 GEOs |

|

| 464,383 GEOs |

|

| 360,070 GEOs |

Oil & Gas assets - Revenue3 |

|

| $35.0 million - $45.0 million |

|

| $30.1 million |

|

| $28.0 million |

1Of the 470,000 to 500,000 GEOs, Franco-Nevada expects to receive 335,000 to 345,000 GEOs under its various stream agreements, compared to 321,093 GEOs in 2016.

2In forecasting GEOs for 2017, gold, silver, platinum and palladium metals have been converted to GEOs using commodity prices of $1,200/oz Au, $17.50/oz Ag, $950/oz Pt and $750/oz Pd.

3In forecasting revenue from Oil & Gas assets for 2017, the WTI oil price is assumed to average $50 per barrel with a $3.50 per barrel price differential between the Edmonton Light and realized prices for Canadian oil.

More specifically, we expect the following with respect to our key asset categories for 2017:

Precious Metals — U.S.: GEOs from U.S. gold assets are expected to be slightly higher in 2017 compared to 2016. Higher production is expected at the Bald Mountain mine due to mine sequencing and a lag from ore previously placed on heap leach pads. This will be partly offset by lower production from South Arturo, as a result of a planned wind down of the Phase 2 pit.

Precious Metals — Canada: GEOs earned from Canadian assets in 2017 are expected to decrease, reflecting the Holloway mine being placed on care and maintenance in late 2016, as well as a reduction in our attributable ounces from Kirkland Lake following the 1% NSR buy-back in October 2016.

Precious Metals — Latin America: GEOs from Latin America are expected to increase, reflecting increased production from Candelaria due to an optimization of the open pit life-of-mine plan and inclusion of additional volumes of higher grade underground ore. This increase is expected to be partly offset by lower silver production from Antamina, which had exceptionally high production levels in 2016.

Precious Metals — Rest of World: GEOs from Rest of World assets are forecasted to increase compared to 2016, reflecting the first full-year of fixed ounce deliveries from Karma, and a full year of production at the Vivien and Wiluna mines. These increases will be partly offset by the cessation of production from the Cooke 4 operations.

Other Minerals: GEOs from other minerals are expected to be relatively similar to 2016.

Oil & Gas: Oil & gas revenues are expected to increase in 2017 compared to 2016, as a result of the additions of the STACK assets in Q4/2016 and Midland assets in 2017.

10 | 2016 Annual Report | FNV TSX NYSE |

We expect to fund approximately $200.0 million to $220.0 million towards the Cobre Panama precious metals stream in 2017. In 2016, the Company funded a total of $124.3 million, for a total of $462.2 million of its $1 billion commitment.

In addition, the Company estimates depletion and depreciation expense to be $265.0 million to $295.0 million for 2017.

Franco-Nevada strives to generate 80% of revenue from precious metals over a long-term horizon which includes gold, PGM and silver. In the short-term, we may diverge from the long-term target based on opportunities available. With 93.7% of revenue earned from precious metals in 2016, the Company has the flexibility to consider diversification opportunities outside of the precious metals space and increase its exposure to other commodities.

The prices of precious metals are the largest factors in determining profitability and cash-flow from operations for Franco-Nevada. Historically, the price of gold has been subject to volatile price movements and is affected by numerous macroeconomic and industry factors that are beyond the Company’s control. Major influences on the gold price include macroeconomic factors such as the level of interest rates, inflation expectations, currency exchange rate fluctuations including the relative strength of the U.S. dollar, and the supply of and demand for gold.

The gold price exhibited a positive rally in the first half of 2016 due to continuously low interest rates and uncertainty following the Brexit vote in June 2016, reaching a peak of $1,366/oz. However, these gains were somewhat reversed in the fourth quarter of 2016, following the U.S. Presidential election in November 2016 and an increase in interest rates by the U.S. Federal Reserve in December 2016. Volatility is expected to continue into 2017, as the implementation of economic policies by the new U.S. administration shifts international trade relations, further interest rate hikes are potentially enacted by the U.S. Federal Reserve, and a number of elections take place in Europe, adding to instability in the Eurozone.

Overall, the gold price ended the year 2016 at $1,146/oz approximately 8% higher than at the end of 2015. During Q4/2016, average gold prices traded between $1,126/oz and $1,313/oz with an average price of $1,218/oz. This compares to an average gold price of $1,104/oz for Q4/2015, an increase of 10.3%, and $1,335/oz for Q3/2016.

Silver prices averaged $17.18/oz in Q4/2016, compared to $14.76/oz in Q4/2015, an increase of 16.4%. Platinum and palladium prices averaged $944/oz and $684/oz, respectively, compared to $908/oz and $606/oz, respectively, for Q4/2015, increases of 4.0% and 12.9% year-over-year, respectively.

For the year 2016, average gold prices traded between $1,077/oz and $1,366/oz with an average price of $1,248/oz. This compares to an average gold price of $1,160/oz for the year ended December 31, 2015, an increase of 7.6%. Silver prices averaged $17.20/oz in 2016, compared to $15.68 in 2015, an increase of 9.7%. Platinum and palladium prices averaged $987/oz and $613/oz, respectively, compared to $1,054/oz and $691/oz, respectively, for 2015, decreases of 6.4% and 11.3% year-over-year, respectively.

Commodity price volatility also impacts the number of GEOs contributed by non-gold mineral assets when converting silver, platinum, palladium and other minerals to GEOs. Silver, platinum, palladium and other minerals are converted to GEOs by dividing associated revenue, which includes settlement adjustments, by the relevant gold price. The gold price used in the computation of GEOs earned from a particular asset varies depending on the royalty or stream agreement, which may make reference to the market price realized by the operator, or the average for the month, quarter, or year in which the mineral was produced or sold.

Despite the volatile commodity prices, the Company continued to deliver strong results and significant increases in GEOs compared to 2015, reflecting the performance of our mineral asset portfolio as well as accretion from recent acquisitions such as the Antamina and Antapaccay streams. One of the strengths of the Franco-Nevada business model is that our business is not impacted when producer costs increase as long as the producer continues to operate. Royalty and stream payments/deliveries are based on production levels of the underlying operations with no adjustments for the operator’s operating costs, with the exception of NPI and NRI royalties, which are based on the profit of the underlying mining operation. Profit-based royalties accounted for approximately 10.8% of total revenues in Q4/2016, and 7.5% for full year 2016.

The Gold Investment that WORKS | Franco-Nevada Corporation |

| 11 |

SELECTED FINANCIAL INFORMATION

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

(in millions, except Average Gold Price, |

|

|

| For the Three Months Ended December 31, |

|

|

| For the Year Ended December 31, |

| ||||||||

GEOs, Margin and per share amounts) |

|

| 2016 |

|

| 2015 |

|

| 2016 |

|

| 2015 |

| ||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Statistical Measures |

|

|

|

|

|

| |||||||||||

Average Gold Price |

|

| $ | 1,218 |

|

| $ | 1,104 |

|

| $ | 1,248 |

|

| $ | 1,160 |

|

GEOs1 |

|

|

| 121,910 |

|

|

| 106,312 |

|

|

| 464,383 |

|

|

| 360,070 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Statement of Income and Other Comprehensive Income (Loss) |

|

|

|

|

|

| |||||||||||

Revenue |

|

| $ | 155.3 |

|

| $ | 121.3 |

|

| $ | 610.2 |

|

| $ | 443.6 |

|

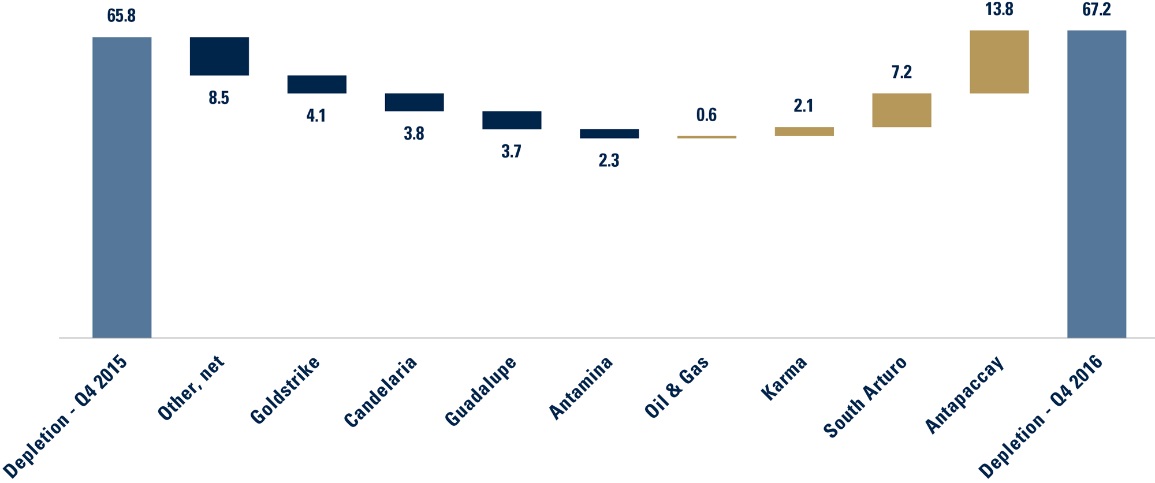

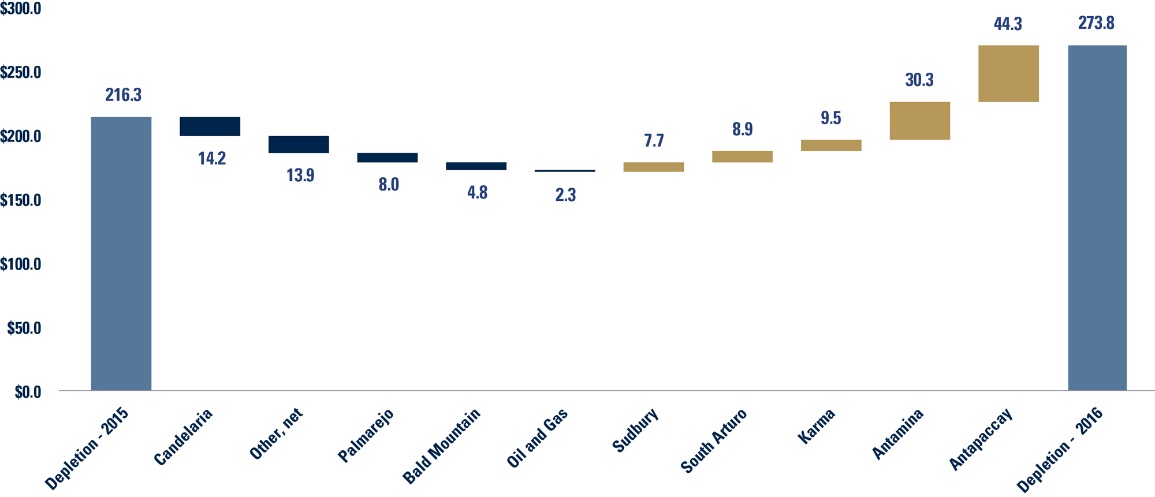

Depletion and depreciation |

|

|

| 67.2 |

|

|

| 65.8 |

|

|

| 273.8 |

|

|

| 216.3 |

|

Impairment charges |

|

|

| 67.5 |

|

|

| 62.9 |

|

|

| 67.5 |

|

|

| 64.9 |

|

Operating income (loss)2 |

|

|

| 0.4 |

|

|

| (36.1) |

|

|

| 155.4 |

|

|

| 51.3 |

|

Net (loss) income |

|

|

| (4.5) |

|

|

| (31.4) |

|

|

| 122.2 |

|

|

| 24.6 |

|

Basic (loss) earnings per share |

|

| $ | (0.03) |

|

| $ | (0.20) |

|

| $ | 0.70 |

|

| $ | 0.16 |

|

Diluted (loss) earnings per share |

|

| $ | (0.03) |

|

| $ | (0.20) |

|

| $ | 0.69 |

|

| $ | 0.16 |

|

Dividends declared per share |

|

| $ | 0.22 |

|

| $ | 0.21 |

|

| $ | 0.87 |

|

| $ | 0.83 |

|

Dividends declared (including DRIP) |

|

| $ | 39.7 |

|

| $ | 32.3 |

|

| $ | 156.8 |

|

| $ | 129.0 |

|

Weighted average shares outstanding |

|

|

| 178.3 |

|

|

| 156.8 |

|

|

| 175.2 |

|

|

| 156.9 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Non-IFRS Measures |

|

|

|

|

|

| |||||||||||

Adjusted EBITDA2,3 |

|

| $ | 122.2 |

|

| $ | 94.2 |

|

| $ | 489.1 |

|

| $ | 337.1 |

|

Adjusted EBITDA2,3 per share |

|

| $ | 0.69 |

|

| $ | 0.60 |

|

| $ | 2.79 |

|

| $ | 2.16 |

|

Margin2,3 |

|

|

| 78.7 | % |

|

| 77.7 | % |

|

| 80.2 | % |

|

| 76.0 % |

|

Adjusted Net Income2,3 |

|

| $ | 42.9 |

|

| $ | 23.7 |

|

| $ | 164.4 |

|

| $ | 88.9 |

|

Adjusted Net Income2,3 per share |

|

| $ | 0.24 |

|

| $ | 0.15 |

|

| $ | 0.94 |

|

| $ | 0.57 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Statement of Cash Flows |

|

|

|

|

|

| |||||||||||

Net cash provided by operating activities2 |

|

| $ | 121.9 |

|

| $ | 84.9 |

|

| $ | 471.0 |

|

| $ | 314.3 |

|

Net cash used in investing activities2 |

|

| $ | (113.3) |

|

| $ | (987.7) |

|

| $ | (689.8) |

|

| $ | (1,106.1) |

|

Net cash (used in) provided by financing activities |

|

| $ | (30.5) |

|

| $ | 445.2 |

|

| $ | 321.7 |

|

| $ | 374.1 |

|

|

|

|

|

|

|

|

|

| As at |

|

| As at |

| ||||

Statement of Financial Position |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and cash equivalents |

|

|

|

|

|

|

|

|

|

| $ | 253.0 |

|

| $ | 149.2 |

|

Short-term investments |

|

|

|

|

|

|

|

|

|

|

| — |

|

|

| 18.8 |

|

Total assets |

|

|

|

|

|

|

|

|

|

|

| 4,221.6 |

|

|

| 3,674.3 |

|

Debt |

|

|

|

|

|

|

|

|

|

|

| — |

|

|

| 457.3 |

|

Deferred income tax liabilities |

|

|

|

|

|

|

|

|

|

|

| 37.5 |

|

|

| 33.2 |

|

Total shareholders’ equity |

|

|

|

|

|

|

|

|

|

|

| 4,146.5 |

|

|

| 3,163.0 |

|

Working capital |

|

|

|

|

|

|

|

|

|

|

| 323.6 |

|

|

| 253.9 |

|

1Refer to Note 1 at the bottom of page 8 of this MD&A for the methodology for calculating GEOs, and, for illustrative purposes, to the average commodity price table on pages 16 and 23 of this MD&A for indicative prices which may be used in the calculations of GEOs.

2In Q3/2016, the Company adopted a retrospective change in accounting policy with respect to its classification of proceeds from sales of gold bullion in its statement of cash flows and statement of income and comprehensive income (loss). For further information, refer to Note 2(b) of the consolidated financial statements for the year ended December 31, 2016. The Company’s non-IFRS measures, as defined in pages 37‑39 of this MD&A, were also adjusted accordingly to reflect gains/losses on sales of such gold bullion as an operating activity that is part of the Company’s underlying business. Comparative information has been adjusted to conform to current presentation.

3Adjusted EBITDA, Margin and Adjusted Net Income are non-IFRS financial measures with no standardized meaning under IFRS. For further information and a detailed reconciliation, please see pages 37‑39 of this MD&A.

12 | 2016 Annual Report | FNV TSX NYSE |

Our portfolio is well-diversified with GEOs and revenue being earned from 46 mineral assets and 60 oil & gas interests in various jurisdictions. The following table details revenue earned from our various royalty, stream and working interests for the three months and year ended December 31, 2016 and 2015:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| For the three months ended |

|

|

| For the year ended |

| ||||||||

(expressed in millions) |

|

|

|

|

| December 31, |

|

|

| December 31, |

| ||||||||

Property |

| Interest |

|

| 2016 |

|

| 2015 |

|

| 2016 |

|

| 2015 |

| ||||

PRECIOUS METALS |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

United States |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Goldstrike |

| NSR 2‑4%, NPI 2.4‑6% |

|

| $ | 3.1 |

|

| $ | 9.5 |

|

| $ | 22.9 |

|

| $ | 23.4 |

|

Stillwater |

| NSR 5% |

|

|

| 3.8 |

|

|

| 3.2 |

|

|

| 14.6 |

|

|

| 15.6 |

|

Gold Quarry |

| NSR 7.29% |

|

|

| 3.6 |

|

|

| 2.4 |

|

|

| 14.0 |

|

|

| 13.1 |

|

Marigold |

| NSR 1.75‑5%, GR 0.5‑4% |

|

|

| 3.1 |

|

|

| 2.3 |

|

|

| 10.1 |

|

|

| 6.0 |

|

Fire Creek/Midas |

| Fixed to 2018 / NSR 2.5% |

|

|

| 1.5 |

|

|

| 2.1 |

|

|

| 9.2 |

|

|

| 8.7 |

|

Bald Mountain |

| NSR/GR 0.875‑5% |

|

|

| 1.3 |

|

|

| 1.8 |

|

|

| 3.9 |

|

|

| 8.2 |

|

South Arturo |

| GR 4‑9% |

|

|

| 10.7 |

|

|

| — |

|

|

| 13.8 |

|

|

| 0.2 |

|

Other |

|

|

|

|

| 0.7 |

|

|

| 0.8 |

|

|

| 2.5 |

|

|

| 2.3 |

|

Canada |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Sudbury |

| Stream 50% |

|

| $ | 6.0 |

|

|

| 6.4 |

|

|

| 30.4 |

|

| $ | 23.2 |

|

Detour Lake |

| NSR 2% |

|

|

| 3.8 |

|

|

| 3.3 |

|

|

| 13.3 |

|

|

| 11.7 |

|

Golden Highway |

| NSR 2‑15% |

|

|

| 2.7 |

|

|

| 2.2 |

|

|

| 10.7 |

|

|

| 10.1 |

|

Musselwhite |

| NPI 5% |

|

|

| 2.0 |

|

|

| 3.1 |

|

|

| 5.1 |

|

|

| 5.4 |

|

Hemlo |

| NSR 3%, NPI 50% |

|

|

| 7.2 |

|

|

| 3.3 |

|

|

| 12.7 |

|

|

| 5.0 |

|

Kirkland Lake1 |

| NSR 1.5‑5.5%, NPI 20% |

|

|

| 1.0 |

|

|

| 1.1 |

|

|

| 5.2 |

|

|

| 4.6 |

|

Timmins West |

| NSR 2.25% |

|

|

| 0.9 |

|

|

| 0.8 |

|

|

| 3.2 |

|

|

| 3.7 |

|

Canadian Malartic |

| GR 1.5% |

|

|

| 0.3 |

|

|

| 0.5 |

|

|

| 2.1 |

|

|

| 1.6 |

|

Other |

|

|

|

|

| 0.1 |

|

|

| — |

|

|

| 0.2 |

|

|

| 0.1 |

|

Latin America |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Antapaccay |

| Stream (indexed) |

|

| $ | 27.2 |

|

| $ | — |

|

| $ | 92.5 |

|

| $ | — |

|

Antamina |

| Stream 22.5% |

|

|

| 12.2 |

|

|

| 14.4 |

|

|

| 75.0 |

|

|

| 14.4 |

|

Candelaria |

| Stream 68% |

|

|

| 23.7 |

|

|

| 24.3 |

|

|

| 88.5 |

|

|

| 101.6 |

|

Guadalupe-Palmarejo2 |

| Stream 50% |

|

|

| 8.3 |

|

|

| 13.8 |

|

|

| 44.6 |

|

|

| 59.6 |

|

Other |

|

|

|

|

| 0.7 |

|

|

| 1.0 |

|

|

| 3.1 |

|

|

| 4.1 |

|

Rest of World |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

MWS |

| Stream 25% |

|

| $ | 5.5 |

|

| $ | 6.5 |

|

| $ | 27.1 |

|

| $ | 26.2 |

|

Sabodala |

| Stream 6%, Fixed to 2019 |

|

|

| 4.6 |

|

|

| 6.1 |

|

|

| 26.0 |

|

|

| 28.3 |

|

Subika |

| NSR 2% |

|

|

| 1.4 |

|

|

| 0.9 |

|

|

| 4.8 |

|

|

| 4.3 |

|

Tasiast |

| NSR 2% |

|

|

| 1.6 |

|

|

| 1.1 |

|

|

| 4.4 |

|

|

| 5.0 |

|

Karma |

| Stream 4.875%, Fixed to 75koz |

|

|

| 3.0 |

|

|

| — |

|

|

| 14.4 |

|

|

| — |

|

Duketon |

| NSR 2% |

|

|

| 1.8 |

|

|

| 1.6 |

|

|

| 7.2 |

|

|

| 6.7 |

|

Edikan |

| NSR 1.5% |

|

|

| 0.6 |

|

|

| 0.9 |

|

|

| 3.1 |

|

|

| 3.7 |

|

Other |

|

|

|

|

| 0.3 |

|

|

| 1.4 |

|

|

| 6.9 |

|

|

| 8.7 |

|

|

|

|

|

| $ | 142.7 |

|

| $ | 114.8 |

|

| $ | 571.5 |

|

| $ | 405.5 |

|

Other Minerals |

|

|

|

| $ | 2.2 |

|

| $ | 2.1 |

|

| $ | 8.6 |

|

| $ | 10.1 |

|

Oil & Gas |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Weyburn |

| NRI 11.71%, ORR 0.44%, WI 2.56% |

|

| $ | 7.9 |

|

| $ | 3.5 |

|

| $ | 23.6 |

|

| $ | 21.1 |

|

Midale |

| ORR 1.14%, WI 1.59% |

|

|

| 0.4 |

|

|

| 0.3 |

|

|

| 1.4 |

|

|

| 1.8 |

|

Edson |

| ORR 15% |

|

|

| 0.4 |

|

|

| 0.4 |

|

|

| 1.2 |

|

|

| 1.7 |

|

STACK |

| ORR & Mineral Title 7.15% |

|

|

| 0.9 |

|

|

| — |

|

|

| 0.9 |

|

|

| — |

|

Other |

|

|

|

|

| 0.8 |

|

|

| 0.2 |

|

|

| 3.0 |

|

|

| 3.4 |

|

|

|

|

|

| $ | 10.4 |

|

| $ | 4.4 |

|

| $ | 30.1 |

|

| $ | 28.0 |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue |

|

|

|

| $ | 155.3 |

|

| $ | 121.3 |

|

| $ | 610.2 |

|

| $ | 443.6 |

|

1In October 2016, the overlying NSR on the Kirkland Lake Gold properties was reduced from 2.5% to 1.5% pursuant to Kirkland Lake’s buy-back of 1% of the NSR.

2In July 2016, Coeur met its obligation to deliver 400,000 ounces under the Palmarejo agreement. Deliveries under the new Guadalupe agreement commenced in Q4/2016.

The Gold Investment that WORKS | Franco-Nevada Corporation |

| 13 |

Franco-Nevada realized record growth from its mineral assets in 2016, both in revenue and GEOs, reflecting the performance of our mineral asset portfolio as well as accretion from recent acquisitions.

Significant Mineral Interests

The most significant mineral assets which contributed to our 2016 performance included the following:

Antapaccay

The Company owns a gold and silver stream with reference to production from the Antapaccay mine, located in Peru. Under the stream agreement, gold and silver deliveries are initially referenced to copper in concentrate shipped. Franco-Nevada will receive 300 ounces of gold and 4,700 ounces of silver for each 1,000 tonnes of copper in concentrate shipped, until 630,000 ounces of gold and 10 million ounces of silver have been delivered. Thereafter, Franco-Nevada will receive 30% of the gold and silver in concentrate shipped. Franco-Nevada will initially pay an on-going price of 20% of the spot price of gold and silver until 750,000 ounces of refined gold and 12.8 million ounces of refined silver have been delivered. Thereafter, the on-going price will increase to 30% of the spot price of gold and silver. As at December 31, 2016, Antapaccay has delivered 60,470 ounces of gold, and 0.9 million ounces of silver since the stream was acquired in February 2016. These deliveries converted to 73,612 GEOs for 2016.

Candelaria

The Company owns a 68% gold and silver stream on Lundin Mining Corporation’s Candelaria mine in Chile. The stream will reduce to 40% after 720,000 ounces of gold and 12 million ounces of silver have been delivered to Franco-Nevada. Franco-Nevada will pay an ongoing price equal to the lesser of $400 per ounce of gold and $4.00 per ounce of silver or the then prevailing spot price for gold and silver for each ounce delivered under the stream. This price will escalate by 1% per annum following the third anniversary of the closing. As at December 31, 2016, Candelaria has delivered 145,864 ounces of gold and 2.5 million ounces of silver since the stream was acquired in November 2014. Deliveries received in 2016 converted to 73,410 GEOs, of which 71,378 GEOs were sold in 2016.

Antamina

The Company owns a silver stream on Teck Resources Limited’s 22.5% interest in the Antamina mine located in Peru, subject to a fixed silver payability of 90%. Franco-Nevada pays 5% of the spot silver price for each ounce of silver delivered under the stream. The stream will reduce by one-third after 86 million ounces have been delivered under the stream agreement. As at December 31, 2016, Antamina has delivered 5.4 million ounces of silver since the stream was acquired in October 2015. Deliveries in 2016 converted to 60,273 GEOs.

14 | 2016 Annual Report | FNV TSX NYSE |

Palmarejo-Guadalupe

Until July 2016, the Company owned a 50% gold stream on the Palmarejo silver and gold project. The Palmarejo stream covered 50% of the gold production from the Palmarejo project, included a monthly minimum of 4,167 ounces and was capped at 400,000 ounces. The Company paid Coeur the lesser of $400 per ounce, subject to an annual 1% inflation adjustment commencing in January 2013, and the prevailing spot price, for each ounce of gold delivered under the stream agreement. In July 2016, the 400,000 minimum ounce obligation was met at which point the Palmarejo stream was terminated and the Guadalupe stream became effective. Franco-Nevada believes the new agreement improves mine economics for Coeur and extends the mine life of the entire Palmarejo operation. The $22.0 million deposit provided by Franco-Nevada was used to partially fund the development of the Guadalupe underground mine on the Palmarejo property. Ongoing payments will be equal to the lesser of $800 per ounce (no inflation adjustment) and the then prevailing spot price for gold for each ounce delivered under the new stream agreement. In 2016, the Company received a combined 36,386 ounces of gold from the Palmarejo-Guadalupe streams, of which 7,058 GEOs were delivered as part of the Guadalupe agreement.

Sudbury Basin

The Company has an agreement to purchase 50% of the gold equivalent ounces of the gold, platinum and palladium contained in ore mined and shipped from the KGHM International Ltd. operations in Sudbury, Ontario. The Company will pay for each gold equivalent ounce delivered, a cash payment of the lesser of $400 per ounce (subject to a 1% annual inflationary adjustment starting in July 2011) or the then prevailing market price per ounce of gold. In 2016, the Company received 23,539 GEOs from its Sudbury Basin assets.

Significant Mineral Interests — 2015

The most significant mineral assets which contributed to our 2015 performance were our Candelaria stream (86,824 GEOs), Palmarejo stream (51,420 GEOs), Sabodala 6% gold stream (fixed to 22,500 ounces annually until 2019) (24,375 GEOs) and Mine Waste Solutions 25% gold stream (22,616 GEOs).

Significant Oil & Gas Interests

The most significant Oil & Gas asset which contributed to our 2016 performance was the following:

Weyburn

The Weyburn Unit is located in Saskatchewan, Canada and is operated by Cenovus Energy Inc. The Company holds an 11.71% net royalty interest (“NRI”), a 0.44% royalty interest and a 2.56% working interest in the Weyburn Unit. The Company takes product-in-kind for the working interest and NRI portions of this production and markets it through a third-party. An NRI is a royalty interest that is paid net of operating and capital costs. In 2016, the Company recognized $23.6 million in revenue from its Weyburn interest.

Significant Oil & Gas Interests — 2015

In 2015, the Weyburn interest was also our most significant Oil & Gas asset, contributing $21.1 million in revenue.

Significant Projects Under Development

The Company’s most significant mineral asset under development is the Cobre Panama gold and silver stream. Under its agreement with First Quantum, which owns 80% of the project, Franco-Nevada will provide a maximum of $1 billion in deposit pro-rata on a 1:3 ratio of First Quantum’s share of the capital costs. According to First Quantum, the project was 46% complete as of year-end, has an estimated capital cost of $5.48 billion, and is scheduled for a phased commissioning in late 2018 and continued ramp-up in 2019. At December 31, 2016, the Company has funded a total of $462.2 million of its $1 billion commitment.

Cash flows from the Company’s interest in the STACK shale play in Oklahoma’s Anadarko basin, which closed in Q4/2016, are expected to grow substantially as the top two operators of the lands, Newfield Exploration and Devon Energy, have announced the STACK assets would be a major focus of their capital spending.

The Gold Investment that WORKS | Franco-Nevada Corporation |

| 15 |

OVERVIEW OF FINANCIAL PERFORMANCE —Q4/2016 TO Q4/2015

The prices of precious metals, oil and gas and the actual production from mineral and oil & gas assets are the largest factors in determining profitability and cash flow from operations for Franco-Nevada. The following table summarizes average commodity prices and average exchange rate during the periods presented.

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| QOQ |

|

| YOY | |||

Quarterly average prices and rates |

|

|

|

| Q4/2016 |

|

| Q3/2016 |

| Q4/2015 |

| (Q4/16‑Q3/16) |

|

| (Q4/16‑Q4/15) | |||

Gold1 |

| ($/oz) |

|

| $ | 1,218 |

|

| $ | 1,335 |

| $ | 1,104 |

| (8.8%) |

|

| 10.3 % |

Silver2 |

| ($/oz) |

|

|

| 17.18 |

|

|

| 19.62 |

|

| 14.76 |

| (12.4%) |

|

| 16.4 % |

Platinum3 |

| ($/oz) |

|

|

| 944 |

|

|

| 1,084 |

|

| 908 |

| (12.9%) |

|

| 4.0 % |

Palladium3 |

| ($/oz) |

|

|

| 684 |

|

|

| 676 |

|

| 606 |

| 1.2% |

|

| 12.9 % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Edmonton Light |

| (C$/bbl) |

|

|

| 60.70 |

|

|

| 54.41 |

|

| 52.46 |

| 11.6% |

|

| 15.7 % |

Quality Differential |

| (C$/bbl) |

|

|

| (5.83) |

|

|

| (3.80) |

|

| (8.14) |

| 53.4 % |

|

| 28.4 % |

Realized oil price |

| (C$/bbl) |

|

|

| 54.87 |

|

|

| 50.61 |

|

| 44.32 |

| 8.4 % |

|

| 23.8 % |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

CAD/USD exchange rate4 |

|

|

|

|

| 0.7496 |

|

|

| 0.7663 |

|

| 0.7492 |

| (2.2%) |

|

| 0.1 % |

1Based on LBMA Gold Price PM Fix.

2Based on LBMA Silver Price.

3Based on London PM Fix.

4Based on Bank of Canada noon rates.

Revenue and Gold Equivalent Ounces

Revenue for Q4/2016 was $155.3 million compared with $121.3 million for Q4/2015, an increase of 28.0%. The increase year-over-year is due to the increase of GEOs sold of 121,910 GEOs in Q4/2016, an increase of 14.7% from 106,312 GEOs in Q4/2015, coupled with higher average precious metals prices. Of this $155.3 million in revenue, precious metals revenue comprised 91.9%, compared to 94.6% in Q4/2015, while revenue from the Americas was 87.2%, compared to 84.1% in Q4/2015.

Quarterly Revenue by Commodity and Geography |

(expressed in millions)

16 | 2016 Annual Report | FNV TSX NYSE |

The following table outlines GEOs and revenue attributable to Franco-Nevada for the three months ended December 31, 2016 and 2015 by commodity, geographical location and type of interest:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold Equivalent Ounces1 |

|

|

| Revenue (in millions) | ||||||||||||

For the three months ended December 31, |

|

| 2016 |

|

| 2015 |

| Variance |

|

| 2016 |

|

| 2015 |

| Variance | |||

Commodity |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Precious Metals |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Gold |

|

| 93,775 |

|

| 79,800 |

| 13,975 |

|

| $ | 112.8 |

|

| $ | 88.0 |

| $ | 24.8 |

Silver |

|

| 18,650 |

|

| 17,112 |

| 1,538 |

|

|

| 21.9 |

|

|

| 18.9 |

|

| 3.0 |

PGM |

|

| 7,611 |

|

| 7,523 |

| 88 |

|

|

| 8.0 |

|

|

| 7.9 |

|

| 0.1 |

Precious Metals – Total |

|

| 120,036 |

|

| 104,435 |

| 15,601 |

|

|

| 142.7 |

|

|

| 114.8 |

|

| 27.9 |

Other Minerals |

|

| 1,874 |

|

| 1,877 |

| (3) |

|

|

| 2.2 |

|

|

| 2.1 |

|

| 0.1 |

Oil & Gas |

|

| — |

|

| — |

| — |

|

|

| 10.4 |

|

|

| 4.4 |

|

| 6.0 |

|

|

| 121,910 |

|

| 106,312 |

| 15,598 |

|

| $ | 155.3 |

|

| $ | 121.3 |

| $ | 34.0 |

Geography |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

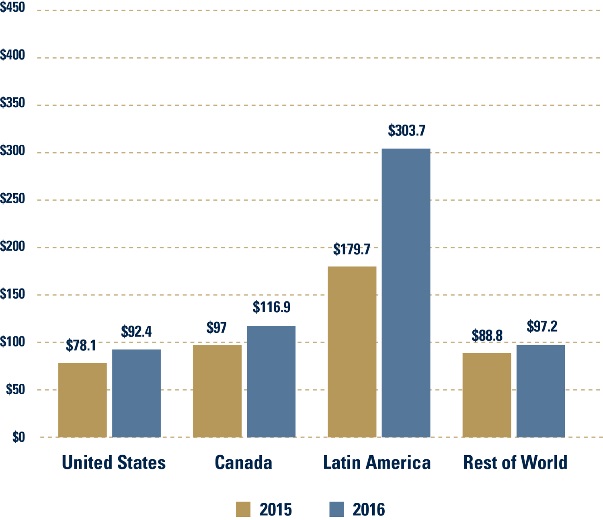

United States |

|

| 23,052 |

|

| 20,141 |

| 2,911 |

|

| $ | 28.7 |

|

| $ | 22.2 |

| $ | 6.5 |

Canada |

|

| 21,818 |

|

| 20,215 |

| 1,603 |

|

|

| 34.7 |

|

|

| 26.2 |

|

| 8.5 |

Latin America |

|

| 60,808 |

|

| 48,243 |

| 12,565 |

|

|

| 72.1 |

|

|

| 53.6 |

|

| 18.5 |

Rest of World |

|

| 16,232 |

|

| 17,713 |

| (1,481) |

|

|

| 19.8 |

|

|

| 19.3 |

|

| 0.5 |

|

|

| 121,910 |

|

| 106,312 |

| 15,598 |

|

| $ | 155.3 |

|

| $ | 121.3 |

| $ | 34.0 |

Type |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Revenue-based |

|

| 23,387 |

|

| 26,213 |

| (2,826) |

|

| $ | 31.0 |

|

| $ | 29.7 |

| $ | 1.3 |

Streams |

|

| 77,197 |

|

| 65,822 |

| 11,375 |

|

|

| 90.7 |

|

|

| 72.2 |

|

| 18.5 |

Profit-based |

|

| 9,628 |

|

| 10,705 |

| (1,077) |

|

|

| 16.8 |

|

|

| 13.0 |

|

| 3.8 |

Other |

|

| 11,698 |

|

| 3,572 |

| 8,126 |

|

|

| 16.8 |

|

|

| 6.4 |

|

| 10.4 |

|

|

| 121,910 |

|

| 106,312 |

| 15,598 |

|

| $ | 155.3 |

|

| $ | 121.3 |

| $ | 34.0 |

1Refer to Note 1 at the bottom of page 8 of this MD&A for the methodology for calculating GEOs, and, for illustrative purposes, to the average commodity price table on page 16 of this MD&A for indicative prices which may be used in the calculations of GEOs.

GEOs and revenue from precious metals were earned from the following geographical locations:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold Equivalent Ounces1 |

|

| Revenue (in millions) | |||||||||||||

For the three months ended December 31, |

| 2016 |

|

| 2015 |

| Variance |

|

| 2016 |

|

| 2015 |

| Variance | |||

Geography for Precious Metals |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Precious Metals |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

United States |

| 22,971 |

|

| 20,064 |

| 2,907 |

|

| $ | 27.8 |

|

| $ | 22.1 |

| $ | 5.7 |

Canada |

| 20,849 |

|

| 19,196 |

| 1,653 |

|

|

| 24.0 |

|

|

| 20.7 |

|

| 3.3 |

Latin America |

| 60,808 |

|

| 48,243 |

| 12,565 |

|

|

| 72.1 |

|

|

| 53.6 |

|

| 18.5 |

Rest of World |

| 15,408 |

|

| 16,932 |

| (1,524) |

|

|

| 18.8 |

|

|

| 18.4 |

|

| 0.4 |

Precious Metals - Total |

| 120,036 |

|

| 104,435 |

| 15,601 |

|

| $ | 142.7 |

|

| $ | 114.8 |

| $ | 27.9 |

Other Minerals |

| 1,874 |

|

| 1,877 |