| CUSIP NO. 143436400 | SCHEDULE 13D/A |

Exhibit A

Important Disclaimers This presentation is provided for informational purposes only. This presentation does not constitute a solicitation of a proxy from any person. Mittleman Brothers, LLC does not undertake any duty to update the information set forth herein. The information included in this presentation is based on information reasonably available to Mittleman Brothers, LLC as of the date hereof. Furthermore, the information included in this presentation has been obtained from sources that Mittleman Brothers, LLC believes to be reliable. However, these sources cannot be guaranteed as to their accuracy or completeness. No representation, warranty or undertaking, express or implied, is given as to the accuracy or completeness of the information contained herein, by Mittleman Brothers, LLC, its members or employees, and no liability is accepted by such persons for the accuracy or completeness of any such information.This presentation contains certain “forward-looking statements,” which may be identified by the use of such words as “believe,” “expect,” “anticipate,” “should,” “planned,” “estimated,” “potential,” “outlook,” “forecast,” “plan” and other similar terms. Examples of forward-looking statements include, without limitation, estimates with respect to financial condition, results of operations, and success or lack of success. All are subject to various factors, including, without limitation, general and local economic conditions, changing levels of competition within certain industries and markets, changes in interest rates, changes in legislation or regulation, and other economic, competitive, governmental, regulatory and technological factors, any or all of which could cause actual results to differ materially from projected results. The information set forth in this presentation does not constitute legal, tax, investment or other advice, or a recommendation to purchase or sell any particular security. 1

CKEC: why is the best performing theater chain, selling out at the worst valuation? 2 For nearly 9 years, Mittleman Brothers, LLC has been a shareholder of Carmike Cinemas (CKEC), since late 2007, and one of its largest shareholders since filing an initial 13G with the SEC in 2011. We currently control 9.5% of shares outstanding. On March 8, 2016 we changed our 13G to a 13D filing.Since 12/31/08, just before current CEO, David Passman, took that position in early 2009, Carmike has executed a remarkable turn-around and has out-performed the industry in terms of sales growth, EBITDA growth, and stock performance ever since.Despite its superior performance, at the $30 buy-out price today, CKEC is valued below the trading value of its peers, which trade at an ex-CKEC average of 9.7x EBITDA, with no control premium. So if CKEC, the best performing of the group, traded merely at the group average trading multiple of 9.7x EBITDA, the stock would be $40.70 per share (including $2.00 per share in est. value for Screenvision stake), a 36% premium to the $30 offered price. Sales CAGR Adj. EBITDA CAGR Stock total return CAGR EV/EBITDA (12/31/08 – 12/31/15): (12/31/08 – 12/31/15): (12/31/08 – 12/31/15): (EV at 6/08/16 closing prices /2015 EBITDA): Carmike Cinemas (CKEC): 7.9% 9.2% 30% 7.7x* AMC Entertainment (AMC): 3.3% 7.4% N/A (IPO'd 12/17/13) 8.5x Cinemark (CNK): 7.3% 8.7% 29% 8.2x Regal Entertainment (RGC): 1.8% 4.4% 19% 8.8x Cineplex (CGX CN): 7.1% 8.1% 25% 13.2x Industry-wide box office receipts (US & Canada): 2.1% *7.7x includes est. $50M value for Screenvision stake, at $0 value EV/EBITDA multiple is 8.1x

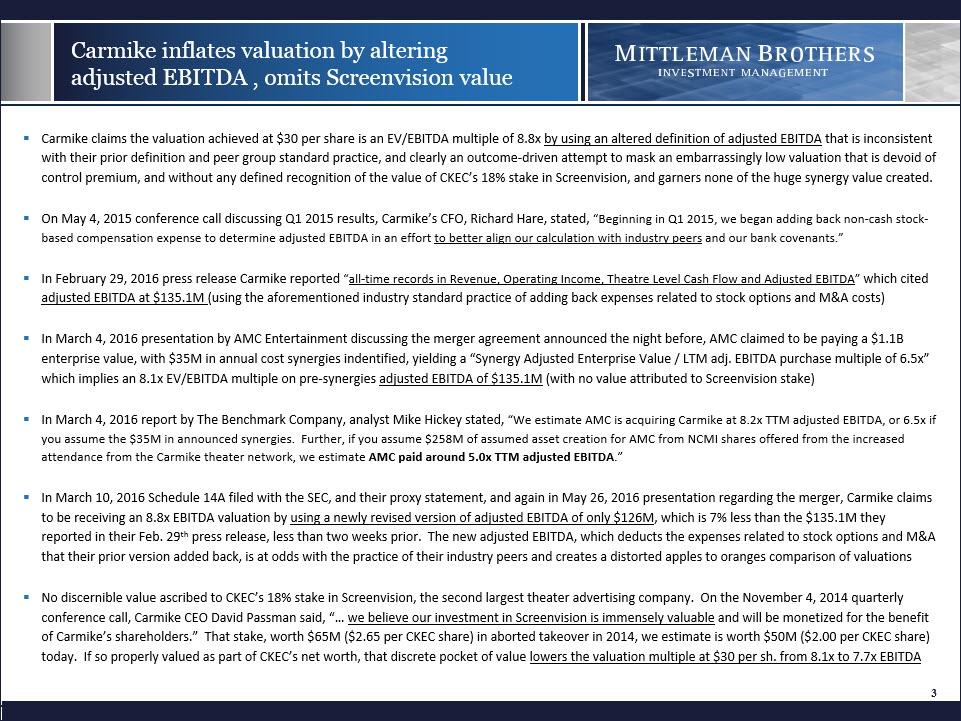

Carmike inflates valuation by altering adjusted EBITDA , omits Screenvision value Carmike claims the valuation achieved at $30 per share is an EV/EBITDA multiple of 8.8x by using an altered definition of adjusted EBITDA that is inconsistent with their prior definition and peer group standard practice, and clearly an outcome-driven attempt to mask an embarrassingly low valuation that is devoid of control premium, and without any defined recognition of the value of CKEC’s 18% stake in Screenvision, and garners none of the huge synergy value created.On May 4, 2015 conference call discussing Q1 2015 results, Carmike’s CFO, Richard Hare, stated, “Beginning in Q1 2015, we began adding back non-cash stock-based compensation expense to determine adjusted EBITDA in an effort to better align our calculation with industry peers and our bank covenants.”In February 29, 2016 press release Carmike reported “all-time records in Revenue, Operating Income, Theatre Level Cash Flow and Adjusted EBITDA” which cited adjusted EBITDA at $135.1M (using the aforementioned industry standard practice of adding back expenses related to stock options and M&A costs)In March 4, 2016 presentation by AMC Entertainment discussing the merger agreement announced the night before, AMC claimed to be paying a $1.1B enterprise value, with $35M in annual cost synergies indentified, yielding a “Synergy Adjusted Enterprise Value / LTM adj. EBITDA purchase multiple of 6.5x” which implies an 8.1x EV/EBITDA multiple on pre-synergies adjusted EBITDA of $135.1M (with no value attributed to Screenvision stake)In March 4, 2016 report by The Benchmark Company, analyst Mike Hickey stated, “We estimate AMC is acquiring Carmike at 8.2x TTM adjusted EBITDA, or 6.5x if you assume the $35M in announced synergies. Further, if you assume $258M of assumed asset creation for AMC from NCMI shares offered from the increased attendance from the Carmike theater network, we estimate AMC paid around 5.0x TTM adjusted EBITDA.”In March 10, 2016 Schedule 14A filed with the SEC, and their proxy statement, and again in May 26, 2016 presentation regarding the merger, Carmike claims to be receiving an 8.8x EBITDA valuation by using a newly revised version of adjusted EBITDA of only $126M, which is 7% less than the $135.1M they reported in their Feb. 29th press release, less than two weeks prior. The new adjusted EBITDA, which deducts the expenses related to stock options and M&A that their prior version added back, is at odds with the practice of their industry peers and creates a distorted apples to oranges comparison of valuationsNo discernible value ascribed to CKEC’s 18% stake in Screenvision, the second largest theater advertising company. On the November 4, 2014 quarterly conference call, Carmike CEO David Passman said, “… we believe our investment in Screenvision is immensely valuable and will be monetized for the benefit of Carmike’s shareholders.” That stake, worth $65M ($2.65 per CKEC share) in aborted takeover in 2014, we estimate is worth $50M ($2.00 per CKEC share) today. If so properly valued as part of CKEC’s net worth, that discrete pocket of value lowers the valuation multiple at $30 per sh. from 8.1x to 7.7x EBITDA 3

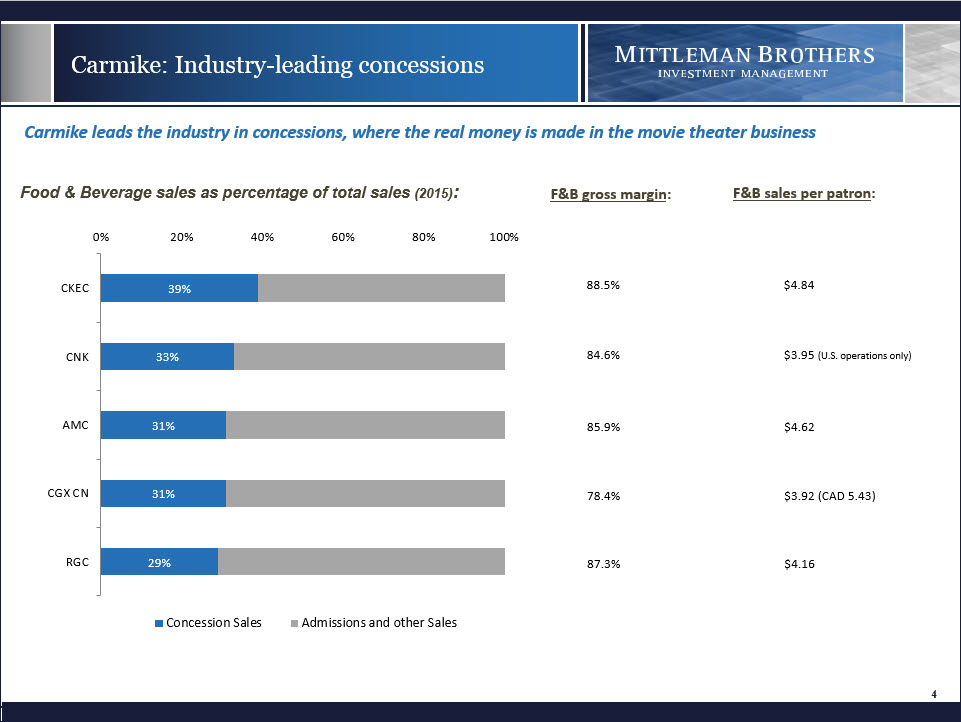

Carmike: Industry-leading concessions Food & Beverage sales as percentage of total sales (2015): 4 88.5% $4.84 F&B gross margin: F&B sales per patron: 84.6% $3.95 (U.S. operations only) 85.9% $4.62 78.4% $3.92 (CAD 5.43) 87.3% $4.16 Carmike leads the industry in concessions, where the real money is made in the movie theater business

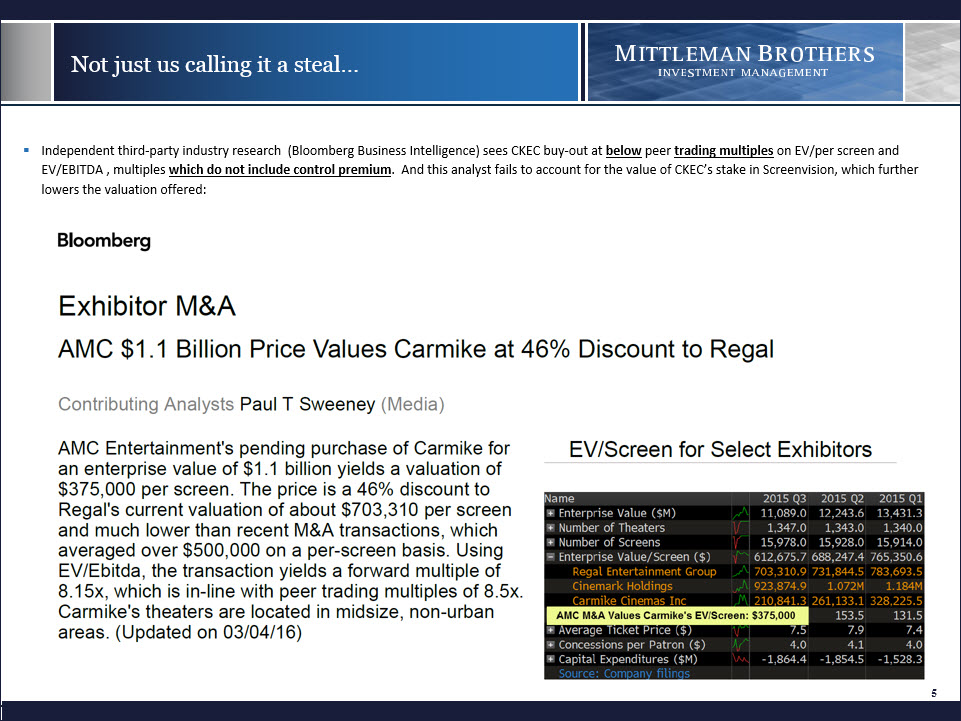

Not just us calling it a steal… 5 Independent third-party industry research (Bloomberg Business Intelligence) sees CKEC buy-out at below peer trading multiples on EV/per screen and EV/EBITDA , multiples which do not include control premium. And this analyst fails to account for the value of CKEC’s stake in Screenvision, which further lowers the valuation offered:

Deeply flawed sale process According to the proxy statement, AMC initially proposed merger talks in May 2014. CKEC’s stock price ranged from $28.99 to $34.63 during May 2014. CKEC’s adjusted EBITDA as reported for 2013 was $113.4M. Carmike declined to pursue a deal at that point due to their pending acquisition of Digital Cinema Destinations Corp. (“DCIN”). After the DCIN deal closed in August 2014, AMC approached CKEC again, signed a confidentiality agreement, and began negotiations. The Board then picked J.P. Morgan as its financial advisor, despite the fact that J.P. Morgan had been an owner of AMC from July 2004 to Sept. 2012. This is particularly disconcerting in light of the advice J.P. Morgan presumably gave Carmike to forgo shopping the company to private equity (ironic and hypocritical when J.P. Morgan and other private equity firms were the owners of AMC as recently as 2 years prior to their engagement with Carmike). The proxy makes no mention of any other investment banks having been considered. And despite the substantial merger-related compensation (golden parachute) ultimately negotiated for the CEO, the Board did not create a special committee to ensure the merger-related decision making was unconflicted.According to the proxy statement, sometime between October 2014 and December 2014, AMC offer $35 per share (50% cash / 50% AMC stock) to buy CKEC. CKEC reached out to other potential strategic buyers to canvass for interest. During that time period Carmike discussed with J.P. Morgan whether or not they should reach out to financial buyers (private equity firms) to gage their potential interest. They decided not to, explaining in the proxy that they deemed private equity buyers either uninterested due to the leverage required, or likely incapable of submitting a competitive bid due to lack of synergies and IRR hurdles. Given the very small number of potential strategic buyers in this situation, it seems ludicrous for CKEC and J.P. Morgan to have presumptively excluded the entire private equity industry from this sale process. In fact, private equity was responsible for one of the largest developed market movie theater deals in recent history, the $1.46B buyout of London-based Vue Entertainment Ltd (“Vue”), bought for 8.5x EBITDA of $171M in September 2013 by two Canadian private equity firms, OMERS Private Equity and Alberta Investment Management Corp., with no synergies to reduce their cost.During Q1 2015 AMC proposed to buy CKEC for $36 per share (50% cash / 50% AMC stock) and then ultimately $37 per share (60% cash / 40% stock). Carmike’s adjusted EBITDA as reported for 2014 was $98.3M. AMC withdrew from the process on April 10, 2015, citing a growing discomfort with the terms.AMC approached CKEC again in January 2016, via new CEO, Adam Aron. After initially offering $26 per share (in cash and stock), CKEC ultimately accepted $30 per share (cash only) on March 3, 2016, completely caving in to AMC’s unwillingness to issue its own shares at less than 8x EBITDA, roughly the same multiple AMC would pay for CKEC, just three days after CKEC reported all-time record adjusted EBITDA for 2015 of $135.1M on Feb. 29, 2016 So a process that began with an offer of $35 (50% cash/50% stock) near the end of 2014, a year in which CKEC produced $98.3M in adj. EBITDA, somehow ended with an accepted offer of $30 (all cash) just after the end of 2015, when CKEC produced $135.1M in adj. EBITDA. Seems not particularly shrewd… 6

Deeply flawed sale process (continued) The exclusion of all financial buyers from the pre-deal canvassing of interest is inexcusable and cannot be written off as merely the exercise of business judgment. The acquiescence to a much reduced price, in the face of much higher EBITDA production, and apparently no effort to capture any share of the huge synergies created by this merger by demanding a stock component, all speak to a bungled process. With no pressing need to sell, the company would clearly be better off on a stand-alone basis, rejecting anything other than a premium valuation that its track record and prospects so clearly warrant.The probable damage due to the lack of a comprehensive pre-signing market canvassing was compounded by the lack of a post-signing go-shop provision, along with a $30M break-up fee, which likely discouraged any post-announcement buying interest that might have developed otherwise. Massive value from cost synergies and the terms of AMC’s status as a founding member of NationalCinemedia (NCMI), are accruing entirely to the buyer. While earlier offers all contained a substantial AMC stock component ($35 per share offer in Q4 2014, 50% cash / 50% AMC stock… $36 per share offer in Q1 2015, 50% cash / 50% AMC stock… $37 per share offer in Q1 2015, 60% cash /40% AMC stock… $26 per share offer in January 2016, cash & stock in unspecified proportion) there is no evidence in the proxy statement that CKEC attempted to secure a stock component in the finally agreed upon deal. In the absence of a remotely fair value (not to mention any semblance of a control premium), securing a stock component to the deal consideration would be the last avenue for obtaining CKEC’s fair share of the synergy value created by the merger. The Board’s failure here is again, inexcusable.After gloating about the great bargain price at which he obtained CKEC for his shareholders, AMC’s new CEO, Adam Aron, on AMC’s March 4th conference call discussing the deal, indicated that he did not want to use AMC’s stock to purchase Carmike because “we think the synergy value is significant and we wanted that synergy value to accrue 100% to our shareholders” and because AMC’s stock price in the low $20s was just too cheap to issue. But on that day, 3/4/16, AMC’s stock was $27 and at about 8.1x EBITDA, at parity with the valuation of CKEC at $30 if one were to mark down Screenvision to $0, and more than the 7.7x multiple with Screenvision at $50M. So if AMC was unwilling to issue a non-controlling portion of it shares at 8x EBITDA to buy CKEC, why would CKEC, the better performing of the two over the past 7 years, sell complete control of itself to AMC for around that same 8x EBITDA valuation?The low valuation, the all cash consideration, and the restrictive ancillary terms reveal a deal so one-sided in favor of the buyer as to beg the question, who was J. P. Morgan and Carmike’s Board really looking out for? Because it does not appear that non-management shareholders were properly served here.Carmike’s shareholders are disillusioned. Recent director re-elections showed an average of only 55% of shares voting for directors, versus 76% last year. The Chair of the corporate governance committee received only 49% “for” votes, so while still re-electable under plurality voting rules, this shows the degree to which CKEC’s shareholders are disappointed in the corporate governance, or lack thereof, on display during this amateur-hour sale process. 7

Terrible timing, allowed AMC to take advantage of low CKEC price in market rout AMC appears to have set the timing of Carmike’s sale process, from the beginning. The proxy statement shows that AMC initiated the process, and that throughout, Carmike’s Board has been merely reactive to AMC’s initiatives. If the Board had determined it was the right time to sell, a proper auction, with private equity invited, would have likely produced a better outcome than negotiating with the sole interested strategic buyer, and on the buyer’s timing.AMC’s new CEO, Adam Aron, is highly experienced and became familiar with AMC prior to starting as CEO on Jan. 4, 2016 when he worked as a Senior Operating Partner for a major private equity fund, Apollo Management LP, from 2006 to 2015, which had co-owned AMC from 2004 to 2012 alongside Carmike’s chosen financial advisor, J.P. Morgan, who, we infer from the proxy statement, advised Carmike against entertaining offers from private equity.In communicating his planned strategy as AMC’s new CEO, Adam Aron emphasized that acquisitions would be a major focus of his game plan. He kept his word and eagerly began work on the Carmike acquisition only a few days after he started working at AMC, and was able to hurriedly get the deal done in a matter of about 6 weeks, during a small cap. stock bear market rout, with Carmike’s great assistance of course, in helping to rush it through.During negotiations in January and February of 2016, the stock market was generally falling. The Russell 2000 small cap index dropped 21.7% from 11/30/15 to 02/11/16, and Carmike’s stock had dropped from $26.48 on 11/04/15 to $18.52 on 02/11/16, a drop of 30%, bottoming out right around the time that AMC provided Carmike with a draft merger agreement for their $30.00 offer on 02/10/16 according to the proxy statement. In general, it’s probably not a good idea to attempt to sell your company into the throes of a significant market correction, especially if the business has proven itself recession-proof in the past. So why Carmike’s Board would acquiesce to sell during such a time of panic, especially as they prepared to report record results at the end of February, is a perplexing question indeed. AMC’s stock was also falling during this time, from $27.71 on 11/02/15 to $19.28 on 02/08/11, a 30% drop (same as CKEC). But AMC could no longer bear the concept of issuing their own stock at less than 8x EBITDA, so they changed the terms of their offer from a cash and stock offer, to cash only. Carmike accepted that change in terms, apparently unfazed that Carmike would be selling control to AMC, for a valuation that was less than the valuation at which AMC was unwilling to issue even a non-controlling stake in their own shares. Carmike’s Board should have been equally unwilling to part with our shares at such a putrid valuation, or at the very least should have demanded to receive AMC’s shares as part if not all of the deal value.CKEC reported record results on Feb. 29, 2016. The stock rose 15% the next day to just over $25. Analysts cheered the results. In a March 1, 2016 report by long-time Carmike analyst David W. Miller at Topeka Capital Markets, “… Carmike reported a record Q4 in virtually every metric on which exhibitors are measured – record revenues, record theater-level cash flow, and record adjusted EBITDA. The print is direct proof that, for the better part of the last year, the market has been under-appreciating Carmike’s margin potential, and hence, under-valuing the stock price, which is the least expensive of the four public exhibitors. We enthusiastically reiterate our rating of ‘Buy’ and price target of $36.00.” The $30 buy-out was signed on March 3rd, only three days after those record results were announced. This gave the market little time to fully adjust to the better than expected earnings report. We think the stock was headed to $30 on its own at that point. 8

Fatally flawed fairness opinion The “fairness” opinion provided by Carmike’s financial advisor, J.P. Morgan, with a substantial success fee hanging in the balance, is riddled with errors and omissions which we believe render it not just weak, but fatally flawed. Carmike’s Board had an obligation to vet this opinion before accepting it and using it as a basis to recommend the transaction to shareholders. Given the issues we point out below, we feel the Board failed in its duty of care here.Value of Carmike’s 18% Stake in Screenvision Ignored in Fairness Opinion - In May 2014 privately held Screenvision, the second largest (37% market share) provider of pre-show theater advertising, agreed to merge with its larger rival, publically traded NationalCineMedia, Inc. (“NCMI”) for an enterprise value of $375M, which valued Carmike’s 18% equity stake at $65M ($2.65 per CKEC share). The deal was cancelled in March 2015 after the FTC sued to block it over anti-trust concerns. On a November 4, 2014 quarterly conference call, Carmike’s CEO, David Passman, said “Regardless of the eventual outcome to the litigation, we believe our investment in Screenvision is immensely valuable and will be monitized for the benefit of Carmike’s shareholders.” According to Carmike’s 10-K for 2015, Screenvision’s sales grew 4.6% in 2015 to $165M from $158M in 2014 when the buyout of Screenvision was announced, and Screenvision’s shareholder equity increased from $67M to $86M in 2015. So we think it’s highly unlikely that Carmike’s 18% stake in Screenvision suddenly became worthless or of negligible value. We estimate Screenvision’s value at $275M, or approximately 17x the $16M in unlevered free cash flow that Screenvision produced in 2015, a reasonable multiple for such a large market share player in a unique and growing segment of the out-of-home advertising industry, where ads cannot be skipped by DVRs. Subtracting $20M in net debt from the $275M enterprise value provides an equity value of $255M, with Carmike’s 18% stake worth $46M which we round up to $50M, or just over $2.00 per share in value that is not reflected in the fairness opinion. J.P. Morgan either deliberately or accidentally chose to ignore this discrete pocket of significant value, and Carmike’s Board allowed them to ignore it. Carmike’s shareholders should not be forced to relinquish CKEC’s admittedly valuable stake in Screenvision for no apparent consideration. Our estimate of fair value for the Screenvision stake would add roughly $2.00 per share to the current $30 offered price, or 6.7%, which we view as a significant omission.Fairness Opinion Fails to Apply Control Premium to Valuations of Trading Comparables - Another fatal flaw in JP Morgan’s fairness opinion is the failure to add a control premium to the valuations of the four comparable companies they picked as the most relevant trading comparables. This is required because Carmike is selling control to AMC, and if those comparables were in the process of selling control they would likely be trading at substantially higher valuations. Carmike’s Chairman of the Board, Roland C. Smith, should have noticed this error given that as Chairman of the Board and CEO of Office Depot (his day job), the fairness opinion received from investment bank, Peter J. Solomon Company L.P., in their merger with Staples (since scuttled by the FTC), contained a section noting the trading comparables in that transaction, with a control premium applied. From the Office Depot / Staples proxy statement, PJSC’s fairness opinion: “PJSC also calculated a range of implied values per share of Office Depot common stock using the range of values from the selected publicly traded company analysis and applying to them a “control premium.” For these purposes, PJSC used a control premium of 35%, which reflects the mean control premium over the closing price thirty days prior to announcement in all announced transactions for U.S. based public targets involving mixed consideration of cash and stock with enterprise values ranging from $4 billion to $8 billion since 2012, excluding financial services and real estate companies.” The lack of a control premium applied to the trading comparables is a fatal flaw. 9

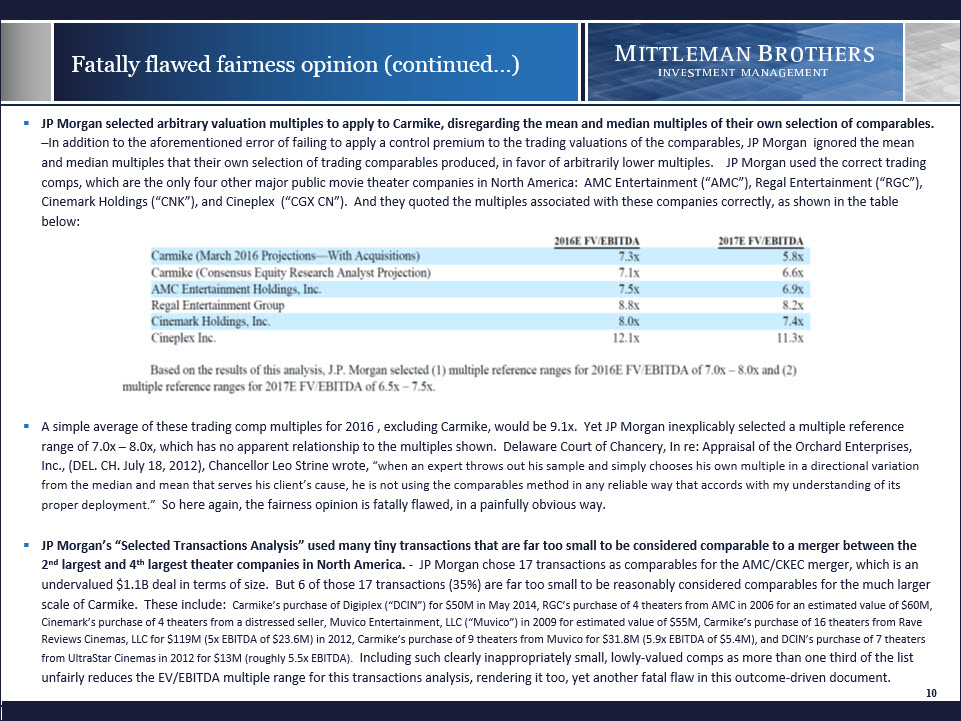

Fatally flawed fairness opinion (continued…) JP Morgan selected arbitrary valuation multiples to apply to Carmike, disregarding the mean and median multiples of their own selection of comparables. –In addition to the aforementioned error of failing to apply a control premium to the trading valuations of the comparables, JP Morgan ignored the mean and median multiples that their own selection of trading comparables produced, in favor of arbitrarily lower multiples. JP Morgan used the correct trading comps, which are the only four other major public movie theater companies in North America: AMC Entertainment (“AMC”), Regal Entertainment (“RGC”), Cinemark Holdings (“CNK”), and Cineplex (“CGX CN”). And they quoted the multiples associated with these companies correctly, as shown in the table below:A simple average of these trading comp multiples for 2016 , excluding Carmike, would be 9.1x. Yet JP Morgan inexplicably selected a multiple reference range of 7.0x – 8.0x, which has no apparent relationship to the multiples shown. Delaware Court of Chancery, In re: Appraisal of the Orchard Enterprises, Inc., (DEL. CH. July 18, 2012), Chancellor Leo Strine wrote, “when an expert throws out his sample and simply chooses his own multiple in a directional variation from the median and mean that serves his client’s cause, he is not using the comparables method in any reliable way that accords with my understanding of its proper deployment.” So here again, the fairness opinion is fatally flawed, in a painfully obvious way.JP Morgan’s “Selected Transactions Analysis” used many tiny transactions that are far too small to be considered comparable to a merger between the 2nd largest and 4th largest theater companies in North America. - JP Morgan chose 17 transactions as comparables for the AMC/CKEC merger, which is an undervalued $1.1B deal in terms of size. But 6 of those 17 transactions (35%) are far too small to be reasonably considered comparables for the much larger scale of Carmike. These include: Carmike’s purchase of Digiplex (“DCIN”) for $50M in May 2014, RGC’s purchase of 4 theaters from AMC in 2006 for an estimated value of $60M, Cinemark’s purchase of 4 theaters from a distressed seller, Muvico Entertainment, LLC (“Muvico”) in 2009 for estimated value of $55M, Carmike’s purchase of 16 theaters from Rave Reviews Cinemas, LLC for $119M (5x EBITDA of $23.6M) in 2012, Carmike’s purchase of 9 theaters from Muvico for $31.8M (5.9x EBITDA of $5.4M), and DCIN’s purchase of 7 theaters from UltraStar Cinemas in 2012 for $13M (roughly 5.5x EBITDA). Including such clearly inappropriately small, lowly-valued comps as more than one third of the list unfairly reduces the EV/EBITDA multiple range for this transactions analysis, rendering it too, yet another fatal flaw in this outcome-driven document. 10

Potential sand-bagging of projections Carmike’s proxy statement reveals that Carmike’s 2016 EBITDA estimate was down 4% vs. prior, despite a sales estimate up 7.6% December 2015 projections for 2016: Sales $800M, EBITDA $142M (with acquisitions)March 2016 projection for 2016: Sales $861M, EBITDA $136M (with acquisitions)The change in EBITDA projection from December to March is very difficult to comprehend. The December 2015 projection envisioned an EBITDA margin of 17.75%, while the March 2016 estimate implies an EBITDA margin of only 15.8%, a nearly 200 basis point decline. In the seven years that current management has been in control of Carmike, since early 2009, sales rose annually in five of those seven years, and in those five years when sales were up, adjusted EBITDA was up in four of those years. That one year in which EBITDA declined in concert with increased sales was 2014, when an initially dilutive acquisition of DCIN added significant costs after that deal closed in August 2014 just before a weak Q4 2014 industry-wide box office result. So, unless Carmike is planning another such awkwardly timed (and not particularly cheap) deal in 2016, then a higher sales estimate should bring forth a higher EBITDA estimate, as Carmike’s results over the past seven years have borne out 80% of the time. 11

What is Carmike Cinemas’ fair value? Peer group (RGC, AMC, CNK, CGX CN) trades at an average multiple of 9.7x EV/EBITDA for 2015, a trading multiple with no control-premium (see slide #2)CKEC has out-performed each member of the peer group in both sales and EBITDA growth over the past 7 years under current management. Growing sales at 7.9% and adjusted EBITDA at 9.2% annually from 12/31/08 to 12/31/15, versus annual growth in sales of 4.9% and adjusted EBITDA at 7.2% for the peer group average (see slide #2). So CKEC has grown sales at a rate that is 61% better than the peer group, and EBITDA growth rate that is 28% higher. A business that has proven itself to have grown faster than its peers over an extended time period should (all else being equal) be valued more highly than its peers if some semblance of that faster historical growth is likely to be perpetuated into the future. Because CKEC serves smaller rural markets in general, with a concentration in the Southeast which is demographically more favorable in terms of population growth, and the opportunities for consolidation are more plentiful in these smaller markets, with less competition from larger buyers for whom such small acquisitions would not move the needle, CKEC can continue to grow faster than its peers partially due to a deeper acquisition pipeline. Also, much of CKEC’s growth has been driven by their innovative and superior performance in growing concessions sales per patron, and attendance per screen at above the rate of the industry on average. But since some portion of their excess growth was due to acquisitions and may not be indicative of an inherently faster growing business (although the peer group also made substantial acquisitions), to be conservative we award CKEC only a slight 10% valuation premium in our estimate of fair value for their historical out-performance in terms of growth, as we believe that it will persist to a significant degree if CKEC were to remain a stand-alone entity.CKEC’s profitability is below the peer group average, with an adjusted EBITDA margin (for 2015) of 16.8%, which is 15.2% less than peer group average adjusted EBITDA margin of 19.8% (AMC: 18.2%, RGC: 19.4%, CNK 23.3%, CGX CN: 18.2%). Despite the structural disadvantage CKEC has in serving smaller markets with a lower number of screens per theater, the company nearly makes up for that with a much better sales mix in terms of ultra high-margin concessions versus admissions revenue, with CKEC reporting concessions (food & beverage) sales at 39% of total, versus 31% for the peer group on average. Also CKEC has been building larger theaters and buying chains with larger theaters so its average number of screens per theater, currently at 10.7, is trending higher towards the peer group average of 12.7 (AMC: 14.0, RGC: 12.9, CNK: 13.5, CGX CN: 10.2). Wall Street consensus estimates predict CKEC’s EBITDA margin will be 17.0% in 2016, and 17.5% in 2017. So for this lower level of profitability, we would discount CKEC’s valuation by 10%, effectively cancelling out the modest 10% premium we awarded them for their superior historical and prospective growth rate. We believe this is conservative as the significantly above average growth rate will overwhelm the effect of a modestly lower and narrowing profitability gap over time in a net present value calculation.CKEC’s 18% stake in Screenvision, which has been valued at $65M ($2.65 per CKEC share) as recently as 2014 in a takeover by NCMI that was scuttled by anti-trust concerns, we value at $50M ($2.00 per CKEC share) based on 17x unleveraged free cash flow for 2015 (Screenvision financial data in CKEC’s 10-K). 12

What is Carmike Cinemas’ fair value? (…continued) We believe that Carmike should trade in-line with the peer group average multiple of 9.7x EV/EBITDA for 2015, conservatively assuming that their above average growth is offset by a below average profit margin, this trading multiple (with no control-premium) yields a stand-alone equity price of $38.70. (9.7x $135.1M = $1,311M - $367.6M in net debt = $943.3M equity value / 24.376M shares outstanding (as of 05/18/16 as per proxy statement) = $38.70 )We believe that Carmike’s 18% stake in Screenvision, while not worth the $65M at which it was valued in 2014 since the scuttled NCMI merger, despite having grown in 2015, is worth about $50M (EV of $275M = 17x unlevered free cash flow of $16M, subtract Screenvision’s net debt of $20M = equity value of $255M, with Carmike’s 18% stake worth $46M which we round up to $50M, or roughly $2.00 per CKEC share. Screenvision is the number two player (37% market share) in a duopoly market for pre-show theater advertising, a growing part of the out-of-home advertising industry where DVR’s can’t skip over the ads shown to a captive audience. Private equity firm Shamrock Holdings has controlled privately-held Screenvision for nearly six years, and another exit attempt in the next few years seems likely. There is no mention of the value of CKEC’s 18% stake in Screenvision in the press release announcing the merger, nor in the proxy statement and the fairness opinion, so presumably CKEC and their financial advisory valued it at $0, which is at odds with Carmike’s CEO’s description of the asset as being “immensely valuable” in late 2014.$38.70 + $2.00 = $40.70 which is what CKEC is likely worth now on a STAND-ALONE BASIS. That is 36% more than the $30 per share in cash AMC is offering to pay to buy control of the company. As a reality check, $40.70 is an equity market value to free cash flow multiple of only 15.7x the $60M of free cash flow CKEC produced in 2015. That is an eminently reasonable and attainable valuation for the best-performing firm in the industry from a growth perspective.Adding a minimal 20% control premium to the stand-alone price of $38.70 takes it up to $46.44 in a cash-out take-over, plus $2.00 for Screenvision = $48.44. And while $48.44 would be an 11.1x EBITDA multiple on CKEC’s 2015 EBITDA of $135.1M, given the $35M in cost synergies AMC projects, the post-synergy multiple drops to 8.8x against $170.1M EBITDA + synergy (recall comparably sized London-based Vue Entertainment was bought out by private equity for 8.5x EBITDA with no synergy cost savings in 2013). Further, since AMC is entitled to an immediate award of additional shares in NCMI given its shareholder agreement with that firm in regards to its attendance and screen count, the increase expected from a 55% boost to screen count courtesy of the CKEC buyout is expected to add roughly $260M in value to AMC’s stake in NCMI, further reducing the effective multiple paid to 7.3x. So for AMC to pay CKEC $48.44 and become the #1 theater company in the world, the effective multiple is only 7.3x EBITDA for AMC, even though CKEC would be receiving 11.1x. Of course, if AMC was willing to make this an all-stock deal, instead of a cash-out, a lower initial price could be tolerated given the synergies and ancillary value created by the merger would be shared by both firms, instead of being hoarded by the acquirer as the currently offered cash-out deal proposes. 13

Carmike: a very bright future, no need to sell now for less than a well-deserved premium As we’ve pointed out in this presentation, and in our three 13D letters sent to Carmike’s Board since this deal was announced, Mittleman Brothers, LLC, one of Carmike’s largest and perhaps longest term shareholders, believes AMC’s $30 per share cash buyout offer severely undervalues Carmike’s stock, not just from a change of control / private market value perspective, but even merely relative to the current trading values of the peer group, this offer is woefully inadequate. And the process by which this low price and anti-competitive deal terms came to be accepted by Carmike’s Board, simply baffling…Carmike’s adjusted EBITDA as reported in 2015 was $135.1M. The mean estimate of adjusted EBITDA for 2016 is $141.6M (according to Bloomberg, tracking five analysts covering the stock), and $155.2M for 2017, a CAGR for EBITDA growth of 7.2%, which is less than CKEC’s 9.2% CAGR of EBITDA growth over the past seven years under current management, but in-line with the peer group’s average EBITDA CAGR of 7.2%. We think CKEC is likely to exceed those estimates for reasons previously discussed, but even if they only match them, clearly there should be no rush to sell here, again, unless we are getting some discernible premium over the peer group trading valuation for doing so.Carmike’s proven track record of superior performance in selling food and beverage items positions them very well to take full advantage of the roll-out of alcohol sales and dine-in theaters. Their geographic concentration, in the smaller towns and cities of the Southeast and rural areas around the country, where other entertainment options are more limited, should help them in this regard, too. The traditional date concept of dinner and a movie may soon become dinner at the movies.The acquisition pipeline remains rich, and more so for Carmike than for most of the larger players who require larger deals for the impact to be significant. Carmike is perhaps best positioned to continue to roll-up the smaller theater chains which still represent about 45% of the screens in the U.S. (with the big 4: RGC, AMC, CNK, & CKEC controlling the rest), a much more fragmented market than in Canada (where Cineplex controls 80% of the market), or in the U.K. where over 70% of the market is shared by the top three players.If AMC buys CKEC, they would increase their screen count by 55% in one fell swoop. Without buying Carmike, in order to acquire the same number of screens (2,954) in the U.S., AMC would have to buy the next 6 largest chains in the U.S., combined (Marcus Theatres: 681 screens, Harkin Theatres: 446, Southern Theatres: 445, B&B Theatres: 409, National Amusements: 409, and Bow Tie Cinemas: 388), and they’d still be 176 theaters short. Even if possible at reasonable prices, that would be a highly complex project, likely taking many years to complete. If AMC wants to avoid that torturous plan B, and get very big very fast, they should have to pay at least a fair price for the privilege. $30 per share in cash is not close to fair value. We see $40.70 as fair value on stand-alone basis, and $48.44 with a 20% control premium applied for a cash buy-out. Until a fair value is offered, we will vote “NO” to the merger and we urge other CKEC holders to do the same before the June 30th meeting. 14