Legal disclaimer CROSSFIRST BANKSHARES, INC. FORWARD

LOOKING STATEMENTS. The financial results

in this presentation reflect preliminary, unaudited results, which

are not final un

til the Company’s Quarterly Report on Form 10

Q is

filed. This presentation and oral statements made during this

meeting contain forward

looking statements. These forward

looking statements reflect our current views with respect to, among

other things, future events and our financial performance

. These sta

tements are often, but not always, made through the use of words

or phrases such as "may," "might," "should," "could," "predi

ct," "potential," "believe," "expect," "continue," "will," "anticipate,"

"seek," "estimate," "intend," "plan," "strive," "pro

jectio

n," "goal," "target," "outlook," "aim," "would," "annualized"

and "outlook," or the negative version of those words or other

comparable words or phrases of a future or forward

looking nature. These forward

looking statements are not historical facts, and a

re based on current expectations, estimates and projections about our

industry, management’s beliefs and certain assumptions

made by management, many of which, by their nature, are

inherently uncertain and beyond our control. Accordingly, we caution

you th

at any such forward

looking statements are not guarantees of future performance

and are subject to risks, assumptions, estimates and uncertaintie

s that are difficult to predict. Although we believe that the expectations

reflected in these forward

looking s

tatements are reasonable as of the date made, actual results

may prove to be materially different from the results expressed

or implied by the forward

looking statements. There are or will be important factors that could cause

our actual results to differ

materially from those indicated in these forward

looking statements, including, but not limited to, the following: risks relating

to the COVID

19 pandemic; risks

related to general business and economic conditions and any regulatory

responses to such condi

tions; our ability to effectively execute our growth strategy

and manage our growth, including identifying and consummating s

uitable mergers and acquisitions; the

geographic concentration of our markets; fluctuation of the fair value

of our investment secu

rities due to factors outside our control; our ability to successfully

manage our credit risk and the sufficiency of our allo

wance; regulatory restrictions on our ability to grow due

to our concentration in commercial real estate lending; our ability

to at

tract, hire and retain qualified management personnel; interest rate

fluctuations; our ability to raise or maintain sufficien

t capital; competition from banks, cr

edit unions and other financial services providers; the effectiveness

of our risk management f

ramework in mitigating risks and losses; our ability to maintain effective

internal control over financial reporting; our abi

lity to keep pace with technological changes; system failures and

interruptions, cyber

attacks and security breaches; employee erro

r, fraudulent activity by employees or clients and inaccurate

or incomplete information about our clients and counterparties;

our ability to maintain our reputation; costs and effects of litigation,

investigations or similar matters; risk exposure fro

m tra

nsactions with financial counterparties; severe weather,

acts of god, acts of war or terrorism; compliance with governmental

and regulatory requirements; changes in the laws, rules, regulations,

interpretations or policies relating to financial insti

tution

s, accounting, tax, trade, monetary and fiscal matters; compliance

with requirements associated with being a public company;

level of coverage of our business by

securities analysts; and future equity issuances.

Any forward

looking statement speaks only a

s of the date on which it is made, and we do not undertake

any obligation to update or

review any forwardlooking statement, whether as a result of new information,

future developments or otherwise, except as required by law.

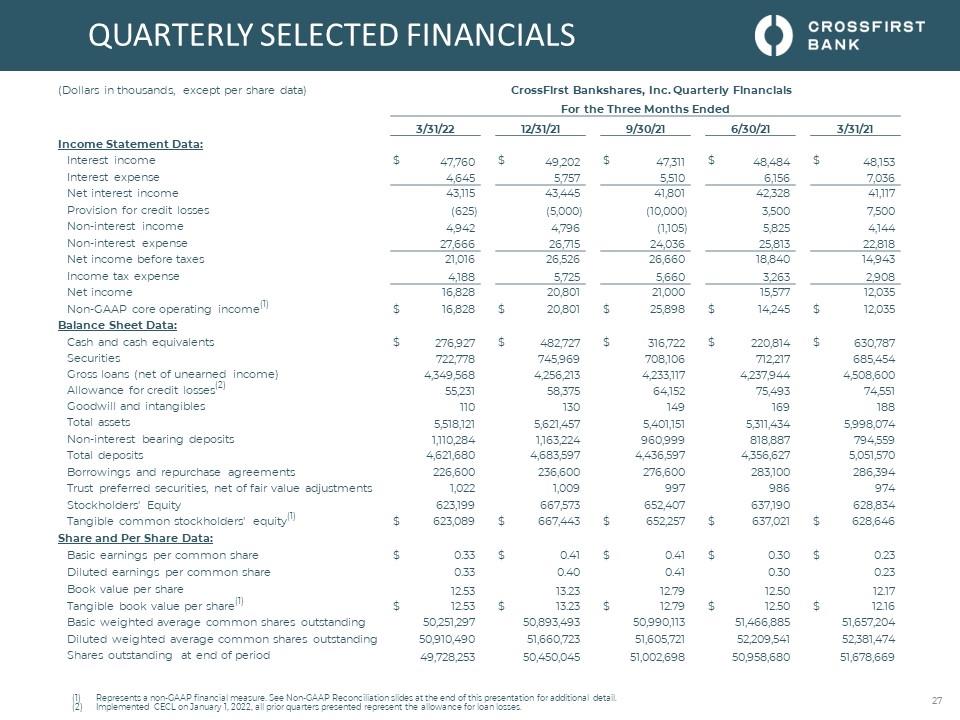

NONGAAP FINANCIAL INFORMATIO

N. This presentation contains certain nonGAAP

measures. These nonGAAP measures, as calculated

by CrossFirst, are not necessarily comparable to similarly titled

measures reported by other companies. Additionally, these non

GAAP measures are not measures of financial performance

or liquidity under GAAP and should not be considered alternatives to

the Company’s other financial information determined under

GAAP. The Company believes that the non-GAAP

financial measures presented reflect industry conventions, or standard

measures within the industry, and provide useful information

to the Company’s management, investors and other parties interested

in the Company’s operating performance. See reconciliations of

certain nonGAAP measures included at

the end of this presentation.

MARKET AND INDUSTRY DATA. This presentation

references certain market, industry and demographic data, foreca

sts and other statistical information. We have obtained this data,

forecasts and information from various independent, third party

industry sources and publications. Nothing in the data, forecasts

or information used or derived from third party sources should be construed

as advice. Some data and other information are also based on our

good faith estimates, which are derived from our review

of industry publications and surveys and independent sources. We

believe that these sources and estimates are reliablebut

have not independently verified them. Statements as to our

market position are based on market data currently available to us.

Although we are not aware of any misstatements regarding the

economic, employment, industry and other market data presented

herein, these estimates involve inherent risks and

uncertainties and are based on assumptions that are subject to change.

2