This report and the financial statements contained herein are submitted for the general information of the shareholders of the Sector Rotation Fund (the “Fund”). The Fund’s shares are not deposits or obligations of, or guaranteed by, any depository institution. The Fund’s shares are not insured by the FDIC, Federal Reserve Board or any other agency, and are subject to investment risks, including possible loss of principal amount invested. Neither the Fund nor the Fund’s distributor is a bank.

The Sector Rotation Fund is distributed by Capital Investment Group, Inc., Member FINRA/SIPC, 100 E. Six Forks Road, Suite 200, Raleigh, NC, 27609. There is no affiliation between the Sector Rotation Fund, including its principals, and Capital Investment Group, Inc.

Letter to Investors

(Unaudited)

“Don’t be afraid to see what you see.” President Ronald Reagan

These days, it seems like people don’t always mean what they say or say what they mean — and I’m here to set the record straight. You might not like it but changing the facts to fit our feelings leads us down a dangerous path.

So, let’s get straight to it.

Historically, economists have defined a recession as two consecutive quarters of significant economic decline, which is represented by declining real gross domestic product (“GDP”), which is a measurement of the total goods and services produced by the U.S. economy as reported on a quarterly basis. It’s been that way for as long as I can remember, and I’ve been on this earth quite a few years.

And according to that definition, we’re in a recession. On an annualized basis, U.S. GDP fell 1.6% in first quarter 2022 and 0.9% in the second quarter.

So why aren’t the headlines screaming that we’re in a recession and telling the stories of the working-class families who can’t make ends meet? Surely, you remember those stories (and images) from the last time we had a recession.

If you don’t recall, there was a small recession in early 2020, in the wake of COVID lockdowns. With that recession, the tales of woe were all over the news. Mom and pop standing outside their neighborhood store with a “closed” sign behind them; grandpa coming out of retirement to get a job at Home Depot.

We believe that one reason no one wants to admit we’re in a recession is that they’re bad for business — the business being the stable operation of the U.S. government. No one wants a recession before elections.

So, you don’t hear much talk of a recession in the news, and news pundits (and even some economists) are being a little wiggly with their words.

The Fed printed massive amounts of money during the pandemic and again more recently to provide aid to Ukraine. Just to be clear, “printing” money doesn’t just refer to physical cash. It can also refer to the money supply the Fed creates via a computer — i.e., the non-paper money it injects into the financial system.

Increasing the money supply in this way inevitably leads to inflation. When the government prints money, consumers have more cash to spend. If the amount of goods stays the same (or falls due to supply chain disruptions, cough cough), that extra cash drives up prices. As Milton Friedman said, “Inflation is caused by too much money chasing after too few goods.”

So here we are. I could break down the components for you, but I’m sure you already know what I’d say. You feel inflation when you fill up your gas tank; you feel inflation when you go to the grocery store. Wait until it’s time to pay your heating bills this winter. In some countries — like the United Kingdom — the situation is dire.

Last year, government officials called the increase in inflation “transitory” as opposed to systematic. Labor disruptions were limiting supply, they said, which increases demand and, thus, prices. Remember what I wrote about that in this letter a year ago?

“I say (mostly) hogwash to that. The government has good reason to pay the ‘transitory’ card: It created this mess! All of those bailout packages increased the money supply and diluted the value of each dollar in circulation.”

Hogwash it is, and here we are.

Now, to curtail the inflation it created, the government is raising interest rates. That’s really hurting homebuyers. Buying a home in 2021 — assuming you put 20% down — would give you a monthly payment of around $1,204, thanks to a 30-year fixed interest rate of about 3%. Today, that payment would be $1,997. And it’s only going to worsen. Some of us remember the early 1980s, when mortgage rates creeped close to 20%.

I hope some of you listened last year when I wrote, “We will have inflation to contend with. A lot of inflation, in my opinion — so best to get those fixed-rate loans now.”

So, where are we headed? Well, the same pundits and economists who said inflation was transitory are now saying the housing market is strong.

Excuse me?

Once again, people don’t always mean what they say or say what they mean, and I’m going to set the record straight: The housing market is going to slow down significantly if not totally crash. It’s common sense, not economic tomfoolery. As interest rates rise, homes will become less affordable, and people will stop buying homes.

This could potentially lead to general economic mayhem, because at the same time, people with variable-rate mortgages will see their monthly costs increase. At first, they may stop buying unnecessary goods. Eventually, though, we believe many people will default on their mortgages.

It all sounds eerily familiar, doesn’t it? Well, at least there are no “too-big-to-fail” financial institutions on the brink of collapse.

Oh.

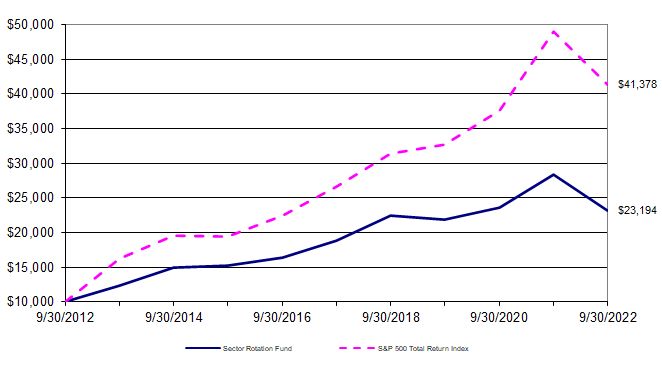

The Fund had a negative net return of 18.20% for the one-year period through September 30, 2022. This compares with its benchmark index, S&P 500 Total Return Index, which dropped 15.47% during the same period. There were several sectors such as Information Technology (VGT) and Consumer Discretionary (VCR) that had a relative performance below the Fund and benchmark index. However, the Fund plans to maintain a position in both sectors due to the historical performance both sectors have when an economy is coming out of a recession. The consumer staples (VDC) and health care sectors (VHT) both outperformed the markets (although down) and had a very positive impact on the Fund.

So, what are we in for in 2023 and beyond?

You heard it here first:

I predict a top issue for the 2024 U.S. Presidential election will be the massive wealth gap in the country. Why? Two reasons: First, because Uncle Sam spent trillions of dollars in 2020-2022 during the Covid-19 pandemic. Where did that money go? Yes, money flows up, very little of it trickles down. Second, inflation and higher interest rates pull money from the bottom and deliver it easily to the top.

Well, we can take COVID out of the equation. It appears to be finished. Yes, there will be new variants, and new calls for masking and lockdowns and vaccinations, but the American people have, for the most part, said “enough.”

But just as consumers began resuming activity in previously shut-down sectors — spending their pent-up savings on entertainment and travel — inflation took off. And now interest rates are rising. And people are worrying. I don’t know about you, but I’m hunkering down — more hamburgers, fewer steaks. More walks in the park, fewer movies.

In terms of investing, be careful. These are perhaps the most troubling times I’ve seen in recent years. The investments that satisfied investors over the past one to five years likely won’t satisfy investors over the next one to five years. That’s why I’m always looking at the economy and markets from five miles up. This broad view helps me identify sectors that show the strongest signs of growth over the next three to 12 months at any point in time.

As always, I appreciate the trust you have placed in me. I will continue to work hard every day to maintain that trust.

Mark Anthony Grimaldi,

Portfolio Manager and Author

RCSEC1022001

1. Organization and Significant Accounting Policies

The Sector Rotation Fund (“Fund”) is a series of the Starboard Investment Trust (“Trust”). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended (“1940 Act”), as an open-end management investment company. The Fund is a separate, non-diversified series of the Trust.

The Fund commenced operations on December 31, 2009 as a series of the World Funds Trust (“WFT”). Shareholders approved the reorganization of the Fund as a series of the Trust at a special meeting on June 22, 2011. The reorganization occurred on June 27, 2011. Effective November 29, 2010, the Fund changed its name from the Navigator Fund to the Sector Rotation Fund.

The investment objective of the Fund is to seek to achieve capital appreciation. The Fund utilizes a sector rotation strategy which evaluates the relative strength and momentum of different sectors of the economy in order to identify short-term investment opportunities. Under normal circumstances, the Fund invests in exchange-traded funds (“ETFs”). An ETF is an open-end investment company that holds a portfolio of investments designed to track a particular market segment or underlying index.

The following is a summary of significant accounting policies consistently followed by the Fund. The policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”). The Fund follows the accounting and reporting guidance in the Financial Accounting Standards Board (“FASB”) Accounting Standards Codification 946 “Financial Services – Investment Companies,” and Financial Accounting Standards Update (“ASU”) 2013-08.

Investment Valuation

The Fund’s investments in securities are carried at fair value. Securities listed on an exchange or quoted on a national market system are valued at the last sales price as of 4:00 p.m. Eastern Time. Securities traded in the NASDAQ over-the-counter market are generally valued at the NASDAQ Official Closing Price. Other securities traded in the over-the-counter market and listed securities for which no sale was reported on that date are valued at the most recent bid price. Instruments with maturities of 60 days or less are valued at amortized cost, which approximates market value. Securities and assets for which representative market quotations are not readily available (e.g., (i) an exchange-traded portfolio security is so thinly traded that there have been no transactions for that security over an extended period of time or the validity of a market quotation received is questionable; (ii) the exchange on which the portfolio security is principally traded closes early; or (iii) trading of the portfolio security is halted during the day and does not resume prior to the Fund’s NAV calculation) or which cannot be accurately valued using the Fund’s normal pricing procedures are valued at fair value as determined in good faith under policies approved by the Trustees. A security’s “fair value” price may differ from the price next available for that security using the Fund’s normal pricing procedures.

Fair Value Measurement

Various inputs are used in determining the value of the Fund's investments. These inputs are summarized in the three broad levels listed below:

Level 1: quoted prices in active markets for identical securities

Level 2: other significant observable inputs (including quoted prices for similar securities, interest rates, credit risk, etc.)

Level 3: significant unobservable inputs (including the Fund’s own assumptions in determining fair value of investments)

The availability of observable inputs can vary from security to security and is affected by a wide variety of factors, including, for example, the type of security, whether the security is new and not yet established in the marketplace, the liquidity of markets, and other characteristics particular to the security. To the extent that valuation is based on models or inputs that are less observable or unobservable in the market, the determination of fair value requires more judgment. Accordingly, the degree of judgment exercised in determining fair value is greatest for instruments categorized in Level 3.

The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety, is determined based on the lowest level input that is significant to the fair value measurement in its entirety.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

| Sector Rotation Fund |

|

| Notes to Financial Statements |

| |

As of September 30, 2022

|

The following table summarizes the inputs as of September 30, 2022, for the Fund’s assets measured at fair value:

| Sector Rotation Fund | | |

| Investments in Securities (a) | | Total | | Level 1 | | Level 2 | | Level 3 |

| Assets | | | | | | | | |

| Exchange-Traded Funds* | $ | 22,004,430 | $ | 22,004,430 | $ | - | $ | - |

| Short-Term Investment | | 4,145,048 | | 4,145,048 | | - | | - |

| Total | $ | 26,149,478 | $ | 26,149,478 | $ | - | $ | - |

| | | | | | | | | |

| (a) | The Fund had no Level 3 holdings during the fiscal year ended September 30, 2022. |

*Refer to Schedule of Investments for breakdown by Industry.

Investment Transactions and Investment Income

Investment transactions are accounted for as of the date purchased or sold (trade date). Dividend income is recorded on the ex-dividend date. Certain dividends from foreign securities will be recorded as soon as the Fund is informed of the dividend if such information is obtained subsequent to the ex-dividend date. Interest income is recorded on the accrual basis and includes accretion of discounts and amortization of premiums using the effective interest method. Gains and losses are determined on the identified cost basis, which is the same basis used for federal income tax purposes.

Expenses

The Fund is responsible for all expenses incurred specifically on its behalf as well as a portion of Trust level expenses, which are allocated according to methods reviewed annually by the Trustees.

Distributions

The Fund may declare and distribute dividends from net investment income (if any) annually. Distributions from capital gains (if any) are generally declared and distributed annually. Dividends and distributions to shareholders are recorded on ex-date.

Estimates

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and the disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in the net assets from operations during the reported period. Actual results could differ from those estimates.

Federal Income Taxes

No provision for income taxes is included in the accompanying financial statements, as the Fund intends to distribute to shareholders all taxable investment income and realized gains and otherwise comply with Subchapter M of the Internal Revenue Code applicable to regulated investment companies.

| 2. | Transactions with Related Parties and Service Providers |

Advisor

The Fund pays a monthly fee to Grimaldi Portfolio Solutions, Inc. (the “Advisor”) calculated at the annual rate of 1.00% of the Fund’s average daily net assets.

The Advisor has entered into a contractual agreement (the “Expense Limitation Agreement”) with the Trust, on behalf of the Fund, under which it has agreed to waive or reduce its fees and to assume other expenses of the Fund, if necessary, in amounts that limit the Fund’s total operating expenses (exclusive of (i) any front-end or contingent deferred loads; (ii) brokerage fees and commissions; (iii) acquired fund fees and expenses; (iv) fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including, for example, option and swap fees and expenses); (v) borrowing costs (such as interest and dividend expense on securities sold short); (vi) taxes and (vii) extraordinary expenses, such as litigation expenses (which may include indemnification of Fund officers and Trustees and contractual indemnification of Fund service providers (other than the Advisor)) to not more than 2.14%. The Expense Limitation Agreement runs through January 31, 2023 and may be terminated by the Board at any time. The Advisor cannot recoup from the Fund any amounts paid by the Advisor under the Expense Limitation Agreement.

For the fiscal year ended September 30, 2022, $307,401 in advisory fees were incurred, and no fees were waived by the Advisor.

| Sector Rotation Fund |

|

| Notes to Financial Statements |

| |

As of September 30, 2022

|

Administrator

The Fund pays a monthly fee to The Nottingham Company (the “Administrator”) based upon the average daily net assets of the Fund and calculated at the annual rates shown in the schedule below subject to a minimum of $2,000 per month. The Administrator also receives a fee as to procure and pay the Fund’s custodian, as additional compensation for fund accounting and recordkeeping services, and additional compensation for certain costs involved with the daily valuation of securities and as reimbursement for out-of-pocket expenses. The Administrator also receives a miscellaneous compensation fee for peer group, comparative analysis, and compliance support totaling $350 per month. As of September 30, 2022, the Administrator received $4,201 in miscellaneous reporting expenses.

A breakdown of the fees is provided in the following table:

| Administration Fees* | Custody Fees* | Fund Accounting Fees (minimum monthly) | Fund Accounting Fees (asset- based fee) | Blue Sky Administration Fees (annual) |

Average Net Assets | Annual Rate |

Average Net Assets | Annual Rate |

| First $250 million | 0.100% | First $200 million | 0.020% | $2,250 | 0.01% | $150 per state |

| Next $250 million | 0.080% | Over $200 million | 0.009% | | | |

| Next $250 million | 0.060% | | | | | |

| Next $250 million | 0.050% | *Minimum monthly fees of $2,000 and $417 for Administration and Custody, respectively. |

| Next $1 billion | 0.040% |

| Over $2 billion | 0.035% |

The Fund incurred $38,255 in administration fees, $9,803 in custody fees, and $30,084 in fund accounting fees for the fiscal year ended September 30, 2022.

Compliance Services

The Nottingham Company, Inc. provides services as the Trust’s Chief Compliance Officer. The Nottingham Company, Inc. is entitled to receive customary fees from the Fund for its services pursuant to the Compliance Services Agreement with the Fund.

Transfer Agent

Nottingham Shareholder Services, LLC (“Transfer Agent”) serves as transfer, dividend paying, and shareholder servicing agent for the Fund. For its services, the Transfer Agent is entitled to receive compensation from the Fund pursuant to the Transfer Agent’s fee arrangements with the Fund.

Distributor

Capital Investment Group, Inc. (the “Distributor”) serves as the Fund’s principal underwriter and distributor.

The Distributor receives $6,500 per year paid in monthly installments for services provided and expenses assumed. Additional expenses may be incurred for processing fees during the year. This expense is included in the shareholder fulfillment expenses on the Statement of Operations.

3. Trustees and Officers

The Trust is governed by the Board of Trustees, which is responsible for the management and supervision of the Fund. The Trustees meet periodically throughout the year to review contractual agreements with companies that furnish services to the Fund; review performance of the Advisor and the Fund; and oversee activities of the Fund. Officers of the Trust and Trustees who are interested persons of the Trust or the Advisor will receive no salary or fees from the Trust. Each Trustee who is not an “interested person” of the Trust or the Advisor within the meaning of the Investment Company Act of 1940, as amended (the “Independent Trustee”) receives $2,000 per series per year, $200 per meeting attended, and $500 per series per special meeting related to contract renewal issues. The Trust reimburses each Trustee and officer of the Trust for his or her travel and other expenses related to attendance of Board meetings. Additional fees were incurred during the year as special meetings were necessary in addition to the regularly scheduled meetings of the Board of Trustees.

Certain officers of the Trust may also be officers of the Administrator.

| Sector Rotation Fund |

|

| Notes to Financial Statements |

| |

As of September 30, 2022

|

4. Distribution and Service Fees

The Trustees, including a majority of the Trustees who are not “interested persons” of the Trust as defined in the 1940 Act and who have no direct or indirect financial interest in such plan or in any agreement related to such plan, adopted a distribution plan pursuant to Rule 12b-1 of the 1940 Act (the “Plan”). The 1940 Act regulates the manner in which a regulated investment company may assume expenses of distributing and promoting the sales of its shares and servicing of its shareholder accounts. The Plan provides that the Fund may incur certain expenses, which may not exceed 0.25% per annum of the average daily net assets of the Fund for each year elapsed subsequent to adoption of the Plan, for payment to the Distributor and others for items such as advertising expenses, selling expenses, commissions, travel or other expenses reasonably intended to result in sales of shares of the Fund or support servicing of shareholder accounts. For the fiscal year ended September 30, 2022, $76,850 in distribution and service fees were incurred by the Fund.

5. Purchases and Sales of Investment Securities

For the fiscal year ended September 30, 2022, the aggregate cost of purchases and proceeds from sales of investment securities (excluding short-term securities) were as follows:

| Purchases of Securities | Proceeds from Sales of Securities |

| $117,290,675 | $116,248,630 |

There were no long-term purchases or sales of U.S Government Obligations during the fiscal year ended September 30, 2022.

6. Risks

Cybersecurity Risk. As part of its business, the Advisor processes, stores and transmits large amounts of electronic information, including information relating to the transactions of the Fund. The Advisor and the Fund are therefore susceptible to cybersecurity risk. Cyber-attacks include, among other behaviors, stealing or corrupting data maintained online or digitally, denial of service attacks on websites, the unauthorized release of confidential information and causing operational disruption. Successful cyber-attacks against, or security breakdowns of, the Fund or its advisor, custodians, fund accountant, fund administrator, transfer agent, pricing vendors and/or other third-party service providers may adversely impact the Fund and its shareholders. For instance, cyber-attacks may interfere with the processing of shareholder transactions, impact the Fund’s ability to calculate its NAV, cause the release of private shareholder information or confidential Fund information, impede trading, cause reputational damage, and subject the Fund to regulatory fines, penalties or financial losses, reimbursement or other compensation costs, and/or additional compliance costs. The Fund also may incur substantial costs for cybersecurity risk management in order to guard against any cyber incidents in the future. The Fund and its shareholders could be negatively impacted as a result.

COVID-19 Risk. The outbreak of an infectious respiratory illness caused by a novel coronavirus known as COVID-19 has resulted in travel restrictions, closed international borders, enhanced health screenings at ports of entry and elsewhere, disruption of and delays in healthcare service preparation and delivery, prolonged quarantines, cancellations, supply chain disruptions, and lower consumer demand, as well as general concern and uncertainty. The impact of COVID-19, and other infectious illness outbreaks that may arise in the future, could adversely affect the economies of many countries or the entire global economy, individual issuers and capital markets in ways that cannot necessarily be foreseen. In addition, the impact of infectious illnesses in emerging market countries may be greater due to generally less established healthcare systems. Public health crises caused by the COVID-19 outbreak may exacerbate other pre-existing political, social and economic risks in certain countries or globally. As such, issuers of debt securities with operations, productions, offices, and/or personnel in (or other exposure to) areas affected with the virus may experience significant disruptions to their business and/or holdings. The potential impact on the credit markets may include market illiquidity, defaults and bankruptcies, among other consequences, particularly on issuers in the airline, travel and leisure and retail sectors. The extent to which COVID-19 will affect the Fund, the Fund’s service providers’ and/or issuer’s operations and results will depend on future developments, which are highly uncertain and cannot be predicted, including new information that may emerge concerning the severity of COVID-19 and the actions taken to contain COVID-19. Economies and financial markets throughout the world are becoming increasingly interconnected. As a result, whether or not the Fund invests in securities of issuers located in or with significant exposure to countries experiencing economic, political and/or financial difficulties, the value and liquidity of the Fund’s investments may be negatively affected by such events. If there is a significant decline in the value of the Fund’s portfolio, this may impact the Fund’s asset coverage levels for certain kinds of derivatives and other portfolio transactions. The duration of the COVID-19 outbreak and its impact on the global economy cannot be determined with certainty.

| Sector Rotation Fund |

|

| Notes to Financial Statements |

| |

As of September 30, 2022

|

Foreign Securities Risk. The ETFs held by the Fund may have significant investments in foreign securities. Foreign securities involve investment risks different from those associated with domestic securities. Changes in foreign economies and political climates are more likely to affect the Fund than a mutual fund that invests exclusively in domestic securities. The value of foreign currency denominated securities or foreign currency contracts is affected by the value of the local currency relative to the U.S. dollar. There may be less government supervision of foreign markets, resulting in non-uniform accounting practices and less publicly available information about issuers of foreign currency denominated securities. The value of foreign investments may be affected by changes in exchange control regulations, application of foreign tax laws (including withholding tax), changes in governmental administration or economic or monetary policy (in this country or abroad) or changed circumstances in dealings between nations. In addition, foreign brokerage commissions, custody fees, and other costs of investing in foreign securities are generally higher than in the United States. Investments in foreign issues could be affected by other factors not present in the United States, including expropriation, armed conflict, confiscatory taxation, and potential difficulties in enforcing contractual obligations.

Investments in ETFs. Since the Fund invests in ETFs, the Fund will be subject to substantially the same risks as those associated with the direct ownership of the securities comprising the index on which the ETF is based, and the value of the Fund’s investment will fluctuate in response to the performance of the underlying index. ETFs typically incur fees that are separate from those of the Fund. Accordingly, the Fund’s investments in ETFs will result in the layering of expenses such that shareholders will indirectly bear a proportionate share of the ETFs’ operating expenses, in addition to paying Fund expenses. ETFs are subject to the following risks that do not apply to traditional mutual funds: (i) an ETF’s shares may trade at a market price that is above or below its NAV; (ii) an active trading market for an ETF’s shares may not develop or be maintained; (iii) the ETF may employ an investment strategy that utilizes high leverage ratios; or (iv) trading of an ETF’s shares may be halted if the listing exchange’s officials deem such action appropriate, the shares are de-listed from the exchange, or the activation of market-wide “circuit breakers” (which are tied to large decreases in stock prices) halts stock trading generally.

Leveraged or Inverse ETFs. The Fund may invest in leveraged and/or inverse ETFs, including multiple inverse (or ultra-short) ETFs. These ETFs are subject to additional risk not generally associated with traditional ETFs. Leveraged ETFs seek to multiply the performance of the particular benchmark that is tracked (which may be an index, a currency or other benchmark). Inverse ETFs seek to negatively correlate to the performance of the benchmark. These ETFs seek to achieve their returns by using various forms of derivative transactions, including by short-selling the underlying index. Ultra-short ETFs seek to multiply the negative return of the tracked index (e.g., twice the inverse return). As a result, an investment in an inverse ETF will decrease in value when the value of the underlying index rises. For example, an inverse ETF tracking the S&P 500 Index will gain 1% when the S&P falls 1% (if it is an ultra-short ETF that seeks twice the inverse return, it will gain 2%), and will lose 1% if the S&P 500 gains 1% (if an ultra-short ETF that seeks twice the inverse return, it would lose 2%). By investing in ultra-short ETFs and gaining magnified short exposure to a particular index, the Fund can commit less assets to the investment in the securities represented on the index than would otherwise be required.

Manager Risk. The Advisor’s ability to choose suitable investments has a significant impact on the ability of the Fund to achieve its investment objectives.

Market Risk. Market risk refers to the possibility that the value of securities held by the Fund may decline due to daily fluctuations in the securities markets. Stock prices change daily as a result of many factors, including developments affecting the condition of both individual companies and the market in general. The price of a stock may even be affected by factors unrelated to the value or condition of its issuer, such as changes in interest rates, national and international economic and/or political conditions and general equity market conditions. In a declining stock market, prices for all companies (including those in the Fund’s portfolio) may decline regardless of their long-term prospects. The Fund’s performance per share will change daily in response to such factors.

Portfolio Turnover Risk. The Advisor may sell portfolio securities without regard to the length of time they have been held in order to take advantage of new investment opportunities or changing market conditions. As portfolio turnover may involve paying brokerage commissions and other transaction costs, there could be additional expenses for the Fund. High rates of portfolio turnover may also result in the realization of short-term capital gains and losses. The payment of taxes on gains could adversely affect the Fund’s performance. Any distributions resulting from such gains will be considered ordinary income for federal income tax purposes.

| Sector Rotation Fund |

|

| Notes to Financial Statements |

| |

As of September 30, 2022

|

Sector Focus Risk. Because the Fund’s investments may, from time to time, be more heavily invested in particular sectors, the value of its shares may be especially sensitive to factors and economic risks that specifically affect those sectors. As a result, the Fund’s share price may fluctuate more widely than the value of shares of a mutual fund that invests in a broader range of industries. The specific risks for each of the sectors in which the Fund may focus its investments include the additional risks described below:

| • | Consumer Discretionary. Companies in this sector may be adversely affected by negative changes in the domestic and international economies, interest rates, competition, consumer confidence, disposable household income, and consumer spending. These companies are also subject to severe competition and changes in demographics and consumer tastes, which may have an adverse effect on the performance of these companies. |

| • | Consumer Staples. Companies in this sector may be adversely affected by negative changes in the domestic and international economies, interest rates, competition, consumer confidence, and consumer spending. These companies also are subject to the risk that government regulation could affect the permissibility of using various production methods and food additives, which regulations could affect company profitability. The success of food, household, and personal product companies may be strongly affected by consumer tastes, marketing campaigns, and other factors affecting supply and demand. |

| • | Industrials. Companies in this sector are affected by supply and demand both for their specific product or service and for industrial sector products in general. Government regulation, world events, and economic conditions will affect the performance of these companies. These companies can also be cyclical, subject to sharp price movements, and significantly affected by government spending policies. |

| • | Information Technology. The performance of companies in this sector may be adversely affected by intense competition both domestically and internationally; limited product lines, markets, financial resources, or personnel; rapid product obsolescence and frequent new product introduction; dramatic and unpredictable changes in growth rates; and dependence on patent and intellectual property rights. |

Small-Cap and Mid-Cap Securities Risk. The Fund or ETFs held by the Fund may invest in securities of small-cap and mid-cap companies, which involve greater volatility than investing in larger and more established companies. Small-cap and mid-cap companies can be subject to more abrupt or erratic share price changes than larger, more established companies. Securities of these types of companies have limited market liquidity, and their prices may be more volatile. You should expect that the value of the Fund’s shares will be more volatile than a fund that invests exclusively in large-capitalization companies.

7. Federal Income Tax

Distributions are determined in accordance with Federal income tax regulations, which differ from GAAP, and, therefore, may differ significantly in amount or character from net investment income and realized gains for financial reporting purposes. Financial reporting records are adjusted for permanent book/tax differences to reflect tax character but are not adjusted for temporary differences.

Management reviewed the Fund’s tax positions taken or to be taken on federal income tax returns for the open tax years of September 30, 2019, through September 30, 2022, and determined that the Fund does not have a liability for uncertain tax positions. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as income tax expense in the Statement of Operations. During the year, the Fund did not incur any interest or penalties.

Distributions during the fiscal years ended were characterized for tax purposes as follows:

| | September 30, 2022 | September 30, 2021 |

| Net Investment Income | $ 906,061 | $ - |

| Long-Term Capital Gain | $ 774,440 | $ 320,001 |

Reclassifications relate primarily to differing book/tax treatment of ordinary net investment losses and have no impact on the net assets of the Funds.

| Sector Rotation Fund |

|

| Notes to Financial Statements |

| |

As of September 30, 2022

|

For the year ended September 30, 2022, the following reclassifications were necessary:

Distributable Earnings | | | $ 54,652 |

| Paid in Capital | | | $ (54,652) |

As of September 30, 2022, the tax-basis cost of investments and components of distributable earnings were as follows:

| Cost of Investments | $ | 24,492,170 |

| | | |

| Unrealized Appreciation | | 1,812,383 |

| Unrealized Depreciation | | (155,075) |

| Net Unrealized Appreciation | $ | 1,657,308 |

| | | |

| Late Year Losses | | (150,470) |

| Accumulated Capital Gains – Long-Term | | 1,863,887 |

| | | |

| Distributable Earnings | $ | 3,370,725 |

| | | |

| | | | | | |

Realized losses reflected in the accompanying financial statements include net capital losses realized between January 1 and the Fund’s fiscal year-end that have not been recognized for tax purposes (Late Year Losses) totaling $150,470.

8. Beneficial Ownership

The beneficial ownership, either directly or indirectly, of 25% or more of the voting securities of a fund creates a presumption of control of a fund, under Section 2(a)(9) of the Investment Company Act of 1940. As September 30, 2022, Charles Schwab held 87.63% of the Fund. The Fund has no knowledge as to whether all or any portion of the shares owned of record by Charles Schwab are also owned beneficially.

9. Commitments and Contingencies

Under the Trust’s organizational documents, its officers and Trustees are indemnified against certain liabilities arising out of the performance of their duties to the Fund. In addition, in the normal course of business, the Trust entered into contracts with its service providers, on behalf of the Fund, and others that provide for general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund. The Fund expects risk of loss to be remote.

10. Subsequent Events

In accordance with GAAP, management has evaluated the need for disclosures and/or adjustments resulting from subsequent events through the date of issuance of these financial statements. Management has concluded there are no additional matters, other than those noted above, requiring recognition or disclosure.

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Board of Trustees of Starboard Investment Trust

and the Shareholders of Sector Rotation Fund

Opinion on the Financial Statements

We have audited the accompanying statement of assets and liabilities of Sector Rotation Fund, a series of shares of beneficial interest in Starboard Investment Trust (the “Fund”), including the schedule of investments, as of September 30, 2022, and the related statement of operations for the year then ended, the statements of changes in net assets for each of the years in the two-year period then ended, the financial highlights for each of the years in the five-year period then ended, and the related notes (collectively referred to as the “financial statements”). In our opinion, the financial statements present fairly, in all material respects, the financial position of the Fund as of September 30, 2022, and the results of its operations for the year then ended, the changes in its net assets for each of the years in the two-year period then ended and its financial highlights for each of the years in the five-year period then ended, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements are the responsibility of the Fund’s management. Our responsibility is to express an opinion on the Fund's financial statements based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (“PCAOB”) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities law and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audits to obtain reasonable assurance about whether the financial statements are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risk of material misstatement of the financial statements, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements. Our procedures included confirmation of securities owned as of September 30, 2022 by correspondence with the custodian and broker. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements. We believe that our audits provide a reasonable basis for our opinion.

BBD, LLP

We have served as the auditor of one or more of the Funds in the Starboard Investment Trust since 2012.

Philadelphia, Pennsylvania

November 21, 2022

| Sector Rotation Fund |

|

Additional Information (Unaudited) |

| |

As of September 30, 2022

|

| 1. | Proxy Voting Policies and Voting Record |

A copy of the Advisor’s Proxy and Corporate Action Voting Policies and Procedures is included as Appendix B to the Fund’s Statement of Additional Information and is available, without charge, upon request, by calling 800-773-3863, and on the website of the Securities and Exchange Commission (“SEC”) at http://www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30, is available (1) without charge, upon request, by calling the Fund at the number above and (2) on the SEC’s website at http://www.sec.gov.

| 2. | Quarterly Portfolio Holdings |

The Fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-PORT. The Fund’s Form N-PORT is available on the SEC’s website at http://www.sec.gov. You may also obtain copies without charge, upon request, by calling the Fund at 800-773-3863.

We are required to advise you within 60 days of the Fund’s fiscal year-end regarding the federal tax status of certain distributions received by shareholders during each fiscal year. The following information is provided for the Fund’s fiscal year ended September 30, 2022.

During the fiscal year, $906,500 in income distributions were paid from the Fund, and $774,001 in long-term capital gain distributions were paid from the Fund.

Dividend and distributions received by retirement plans such as IRAs, Keogh-type plans, and 403(b) plans need not be reported as taxable income. However, many retirement plans may need this information for their annual information meeting.

| 4. | Schedule of Shareholder Expenses |

As a shareholder of the Fund, you incur ongoing costs, including management fees; distribution and/or service (12b-1) fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period from April 1, 2022, through September 30, 2022.

Actual Expenses – The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (e.g., an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during this period.

Hypothetical Example for Comparison Purposes – The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as sales charges (loads), redemption fees, or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

| Sector Rotation Fund |

|

Additional Information (Unaudited) |

| |

As of September 30, 2022

|

| Sector Rotation Fund | Beginning Account Value April 1, 2022 | Ending Account Value September 30, 2022 |

Expenses Paid During Period* |

Actual Hypothetical (5% annual return before expenses) | | | |

| $1,000.00 | $ 811.90 | $8.95 |

| $1,000.00 | $1,015.19 | $9.95 |

*Expenses are equal to the average account value over the period multiplied by the Fund’s annualized expense ratio of 1.97%, multiplied by 183/365 (to reflect the one-half year period).

5. Approval of Investment Advisory Agreement

In connection with the regular Board meeting held on March 10, 2022, the Board, including a majority of the Independent Trustees, discussed the approval of a management agreement between the Trust and the Advisor, with respect to the Fund (the "Investment Advisory Agreement"). The Trustees were assisted by legal counsel throughout the review process. The Trustees relied upon the advice of legal counsel and their own business judgment in determining the material factors to be considered in evaluating the Investment Advisory Agreement and the weight to be given to each factor considered. The conclusions reached by the Trustees were based on a comprehensive evaluation of all of the information provided and were not the result of any one factor. Moreover, each Trustee may have afforded different weight to the various factors in reaching his conclusions with respect to the approval of the Investment Advisory Agreement. In connection with their deliberations regarding approval of the Investment Advisory Agreement, the Trustees reviewed materials prepared by the Advisor.

In deciding on whether to approve the renewal of the Investment Advisory Agreement, the Trustees considered numerous factors, including:

| (i) | Nature, Extent, and Quality of Services. The Trustees considered the responsibilities of the Advisor under the Investment Advisory Agreement. The Trustees reviewed the services being provided by the Advisor to the Fund including, without limitation, the quality of its investment advisory services since the Advisor began managing the Fund (including research and recommendations with respect to portfolio securities); its procedures for formulating investment recommendations and assuring compliance with the Fund’s investment objectives, policies and limitations; its coordination of services for the Fund among the Fund’s service providers; and its efforts to promote the Fund, grow the Fund’s assets, and assist in the distribution of Fund shares (although no portion of the investment advisory fee was targeted to pay distribution expenses). The Trustees evaluated the Advisor’s staffing, personnel, and methods of operating; the education and experience of the Advisor’s personnel; compliance program; and the financial condition of the Advisor. It was noted that there had been no change in personnel. After reviewing the foregoing information and further information in the memorandum from the Advisor (e.g., descriptions of the Advisor’s business, compliance program, and Form ADV), the Board concluded that the nature, extent, and quality of the services provided by the Advisor were satisfactory and adequate for the Fund. |

| (ii) | Performance. The Trustees compared the performance of the Fund with the performance of comparable funds with similar strategies managed by other investment advisers, and applicable peer group data (e.g., Morningstar/Lipper peer group average). The Trustees also considered the consistency of the Advisor’s management of the Fund with its investment objective, policies, and limitations. It was noted that the Fund outperformed the peer group and the category for the 1-year, 5-year, and 10-year periods, but slightly underperformed the category for the since inception period. The Trustees noted that the Fund underperformed its benchmark index for all periods. The Trustees noted that the Advisor had indicated that the Fund was not designed to outperform an index. After reviewing the investment performance of the Fund, the Advisor’s experience managing the Fund, the historical investment performance, and other factors, the Board concluded that the investment performance of the Fund and the Advisor was satisfactory. |

| (iii) | Fees and Expenses. The Trustees noted the management fees for the Fund under the Investment Advisory Agreement. The Trustees then compared the advisory fee and expense ratio of the Fund to other comparable funds, noting that the management fee and the expense ratio were higher than the average of the peer group and category. The Board noted however, that the Fund’s performance commands a higher management fee. |

| Sector Rotation Fund |

|

Additional Information (Unaudited) |

| |

As of September 30, 2022

|

Following this comparison, and upon further consideration and discussion of the foregoing, the Board concluded that the fees to be paid to the Advisor were not unreasonable in relation to the nature and quality of the services provided by the Advisor and that they reflected charges that were within a range of what could have been negotiated at arm’s length.

| (iv) | Profitability. The Board reviewed the Advisor’s profitability analysis in connection with its management of the Fund over the past twelve months. The Board noted that the Advisor realized a profit for the prior twelve months of operations. The Board considered the quality of the Advisor’s service to the Fund, and after further discussion, concluded that the Advisor’s level of profitability was not excessive. |

| (v) | Economies of Scale. In this regard, the Trustees reviewed the Fund’s operational history and noted that the size of the Fund has not provided an opportunity to realize economies of scale. The Trustees then reviewed the Fund’s fee arrangements for breakpoints or other provisions that would allow the Fund’s shareholders to benefit from economies of scale in the future as the Fund grows. The Trustees determined that the maximum management fee would stay the same regardless of the Fund’s asset levels but noted the Advisor’s willingness to consider the breakpoints in the future as assets grow. |

Conclusion. Having reviewed and discussed in depth such information from the Advisor as the Trustees believed to be reasonably necessary to evaluate the terms of the Investment Advisory Agreement and as assisted by the advice of legal counsel, the Trustees concluded that renewal of the Investment Advisory Agreement was fair and reasonable and in the best interest of the shareholders of the Fund.

6. Information about Trustees and Officers

The business and affairs of the Fund and the Trust are managed under the direction of the Board of Trustees of the Trust. Information concerning the Trustees and officers of the Trust and Fund is set forth below. Generally, each Trustee and officer serves an indefinite term or until certain circumstances such as their resignation, death, or otherwise as specified in the Trust’s organizational documents. Any Trustee may be removed at a meeting of shareholders by a vote meeting the requirements of the Trust’s organizational documents. The Statement of Additional Information of the Fund includes additional information about the Trustees and officers and is available, without charge, upon request by calling the Fund toll-free at 1-800-773-3863. The address of each Trustee and officer, unless otherwise indicated below, is 116 South Franklin Street, Rocky Mount, North Carolina 27804. The Independent Trustees received aggregate compensation of $8,649 during the fiscal year ended September 30, 2022, for their services to the Fund and Trust.

| Sector Rotation Fund |

|

Additional Information (Unaudited) |

| |

As of September 30, 2022

|

Name and

Date of Birth | Position

held with

Funds or Trust | Length

of Time Served | Principal Occupation

During Past 5 Years | Number of Portfolios in Fund Complex Overseen by Trustee | Other Directorships

Held by Trustee

During Past 5 Years |

| Independent Trustees |

James H. Speed, Jr.

(06/1953) | Chairman and Independent Trustee | Trustee since 7/09, Chair since 5/12 | Retired Executive/Private Investor | 14 | Independent Trustee of the Brown Capital Management Mutual Funds for all its series from 2011 to present, Centaur Mutual Funds Trust for all its series from 2013 to present, WST Investment Trust for all its series from 2013 to present, and Chesapeake Investment Trust for all its series from 2016 to present (all registered investment companies). Member of Board of Directors of Communities in Schools of N.C. from 2001 to present. Member of Board of Directors of Investors Title Company from 2010 to present. Member of Board of Directors of AAA Carolinas from 2011 to present. Previously, Independent Trustee of the Hillman Capital Management Trust from 2009 to 2021. Previously, Independent Trustee of the Leeward Investment Trust from 2018 to 2020. Previously, member of Board of Directors of M&F Bancorp Mechanics & Farmers Bank from 2009 to 2019. |

Theo H. Pitt, Jr.

(04/1936) | Independent Trustee | Since 9/10 | Senior Partner, Community Financial Institutions Consulting (financial consulting) since 1999. | 14 | Independent Trustee of World Funds Trust for all its series from 2013 to present, ETF Opportunities Trust for all its series from 2019 to present, and Chesapeake Investment Trust for all its series from 2002 to present (all registered investment companies). Senior Partner of Community Financial Institutions Consulting from 1997 to present. Previously, Independent Trustee of the Hillman Capital Management Investment Trust from 2000 to 2021. Previously, Independent Trustee of the Leeward Investment Trust from 2011 to 2021. Previously, Partner at Pikar Properties from 2001 to 2017. |

Michael G. Mosley

(01/1953) | Independent Trustee | Since 7/10 | Owner of Commercial Realty Services (real estate) since 2004. | 14 | None. |

J. Buckley Strandberg

(03/1960) | Independent Trustee | Since 7/09 | President of Standard Insurance and Realty since 1982. | 14 | None. |

Name and

Date of Birth | Position held with

Funds or Trust | Length

of Time Served | Principal Occupation

During Past 5 Years |

| Officers |

Katherine M. Honey

(09/1973) | President and Principal Executive Officer | Since 05/15 | President of The Nottingham Company since 2018. EVP of The Nottingham Company from 2008 to 2018.

|

Ashley H. Lanham (03/1984) | Treasurer, Assistant Secretary, Principal Accounting Officer, and Principal Financial Officer | Since 05/15 | Director of Fund Administration, The Nottingham Company since 2008. |

Tracie A. Coop

(12/1976) | Secretary | Since 12/19 | General Counsel, The Nottingham Company since 2019. Formerly, Vice President and Managing Counsel, State Street Bank and Trust Company from 2015 to 2019. |

| Sector Rotation Fund |

|

Additional Information (Unaudited) |

| |

As of September 30, 2022

|

Name and

Date of Birth | Position held with

Funds or Trust | Length

of Time Served | Principal Occupation

During Past 5 Years |

Andrea M. Knoth

(09/1983) | Chief Compliance Officer | Since 06/2022 | Director of Compliance, The Nottingham Company since 2022. Formerly, Senior Fund Compliance Administrator, Ultimus Fund Solutions from 2019 to 2022. Formerly, Associate Director of Operational Compliance, Barings from 2018 to 2019. Formerly, Senior Fund Compliance Administrator, Gemini Fund Services from 2012 to 2018. |