UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-22298

Starboard Investment Trust

(Exact name of registrant as specified in charter)

116 South Franklin Street, Rocky Mount, North Carolina 27802

(Address of principal executive offices) (Zip code)

Paracorp Inc.

2140 South Dupont Hwy., Camden, DE 19934

(Name and address of agent for service)

Registrant's telephone number, including area code: 252-972-9922

Date of fiscal year end: May 31

Date of reporting period: May 31, 2024

Item 1. REPORTS TO STOCKHOLDERS.

Adaptive ETFs

ANNUAL REPORT

For the Fiscal Year Ended May 31, 2024

Adaptive Alpha Opportunities ETF

Adaptive Hedged Multi-Asset Income ETF

RH Tactical Outlook ETF

RH Tactical Rotation ETF

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Adaptive ETFs (the “ETFs”). The ETFs’ shares are not deposits or obligations of, or guaranteed by, any depository institution. The ETFs’ shares are not insured by the FDIC, Federal Reserve Board or any other agency, and are subject to investment risks, including possible loss of principal amount invested. Neither the ETFs nor the ETFs’ distributor is a bank.

The ETFs are distributed by Capital Investment Group, Inc., Member FINRA/SIPC, 100 E. Six Forks Road, Suite 200, Raleigh, NC, 27609. There is no affiliation between the ETFs, including their principals, and Capital Investment Group, Inc.

| Table of Contents | |

Letter to Shareholders | ……………………………………………………………………………… | 1 |

| Performance Update | ……………………………………………………………………………… | 3 |

| Schedule of Investments | ……………………………………………………………………………… | 7 |

| Statement of Assets and Liabilities | ……………………………………………………………………………… | 17 |

| Statement of Operations | ……………………………………………………………………………… | 18 |

| Statements of Changes in Net Assets | ……………………………………………………………………………… | 19 |

| Notes to Financial Statements | ……………………………………………………………………………… | 25 |

| Additional Information | ……………………………………………………………………………… | 46 |

Statements in this Annual Report that reflect projections or expectations of future financial or economic performance of the ETFs) and of the market in general and statements of the ETFs’ plans and objectives for future operations are forward-looking statements. No assurance can be given that actual results or events will not differ materially from those projected, estimated, assumed or anticipated in any such forward-looking statements. Important factors that could result in such differences, in addition to the other factors noted with such forward-looking statements, include, without limitation, general economic conditions such as inflation, recession and interest rates. Past performance is not a guarantee of future results. An investor should consider the investment objectives, risks, charges and expenses of the ETFs carefully before investing. The prospectus contains this and other information about the ETFs. A copy of the prospectus is available at https://docs.nottinghamco.com/Adaptive or by calling Shareholder Services at 800-773-3863. The prospectus should be read carefully before investing. |

For More Information on the Funds:

See Our Web site @ adaptivefunds.com

or

Call Our Shareholder Services Group at 800-773-3863.

(Unaudited)

Dear Investor,

We appreciate the opportunity to present the annual report for the fiscal year ended May 31, 2024.

Macro Commentary

As we reflect on the past year, we have seen a significant turnaround in global equity markets. On the strength of the S&P 500 closing at 4,769.81 on December 31, 2023, marking a significant recovery from the previous year, the first half of 2024 has shown resilience. We believe this resilience was attributed to declining inflationary pressures, positive global economic growth, low US unemployment rate, and the pause of an interest rate hiking cycle by the US Federal Reserve and other global central banks.

We feel the overall market sentiment has improved as investors anticipate the peak of inflationary levels. The US economy has remained robust, with consumer prices and inflationary trends slowing down1. The Federal Reserve has maintained the overnight federal funds target interest rate within a range of 5.25-5.50%; however, inflation remains well above the Fed’s long-term goal of 2.00%1. Despite the positive market sentiment, we foresee potential equity and fixed income market risks as investors forecast a soft-landing environment where the Federal Reserve may begin one or more of a series of Federal Fund interest rate cuts in 2024. However, we believe the path for the Federal Reserve reducing interest rates has become clouded as the solid job market and low unemployment rates in the first half of 2024 continue to act as a headwind for lower inflation1. Additionally, gross domestic product (GDP) remains positive and heavy fiscal deficits have offset much of the restrictive monetary policy, thus, creating challenges for the FOMC and path of lowering interest rates2.

Despite the solid job market and low unemployment rates, we believe that other leading economic data are pointing to a potential slowdown. We feel the largest headwinds, for the next several quarters, include the risk of Federal Reserve maintaining ‘higher for longer’ stance on interest rates with tighter lending standards by commercial banks and subsequent slowing leading economic data. Higher interest rates and an inverted yield curve have put pressure on banks’ net margins and lending capacity3. Additionally, higher interest rates have put pressure on the consumer with increasing credit card defaults and mortgage interest rates that remained elevated4. Geopolitical risks through the first half of 2024 have also reinforced persistent inflation pressures5. Ongoing tensions in the Gulf, particularly due to the Gaza war, have posed a high risk to disrupting supply chains and escalations between Israel and Iran could have global implications and US inflationary pressures5. So far in 2024 elevated interest rates, persistent inflation, and heightened geopolitical risks have been tempered. Our view is the US economy will end the first half of 2024 without entering a recession, and corporate earnings will remain strong; however, risks are elevated for the remainder of 2024.

Despite the complex landscape characterized by heightened risks and uncertainties, we remain steadfast in our commitment to navigating these challenges. By staying vigilant, maintaining discipline, and adapting to evolving market dynamics, we strive to fulfill our mission of delivering value and fostering long-term success for our investors.

Thank you for your continued trust and support.

Market and Fund Performance Recap

Recapping market performance, the US large-cap equity market, as measured by the S&P 500 Index, was up 28.19%, and the US fixed income market, as measured by the Bloomberg US Aggregate Bond Index, was up 1.31% for the one-year period ending May 31, 2024. US Small Cap equities, as measured by the Russell 2000 Index, underperformed Large Cap equities at 20.12%. Value, as measured by the S&P 500 Index, underperformed Growth, as measured by the Russell 1000 Growth Index, at 28.19% and 33.60%, respectively, during the same period. The Russell 1000 Growth Index was up 33.60% vs Russell 1000 Value index up 21.71% for the one-year period ending May 31, 2024. The International developed markets have been positive with the S&P Global BMI up 23.45% for the one-year period ending May 31, 2024.

The performance of each Adaptive Fund is shown below. Adaptive’s Risk Management Models have been indicating an environment favorable for higher equity market risk since Q3 2023, and portfolio performance generally reflects a more “risk on” environment. During the 12-month reporting period ended May 31, 2024, Adaptive Alpha Opportunities, Adaptive Hedged Multi Asset Income, and RH Tactical Rotation used put and call options for hedging and income purposes.

1 Minutes of the Federal Open Market Committee, March 19-20, 2024

2 International Monetary Fund, Executive Summary dated April 2024

3 2023 FDIC Risk Review

4 Bloomberg, May 31, 2024

5 BlackRock “Geopolitical risk dashboard”, April 25, 2024

All four Adaptive Funds had options exposure during the reporting period. Adaptive Alpha Opportunities held long and short calls and puts, both for leverage and hedging risk against common stock/ETF positions. Expressed as an approximate monthly average, Adaptive Alpha opportunities options activity impacted monthly performance an average of (0.21%). Adaptive Multi Asset Income held mostly covered calls against common positions for income generation. Expressed as an approximate monthly average, Adaptive Multi Asset Income options activity impacted monthly performance an average of (0.07%).

RH Tactical Rotation held a mixture of long and short calls and puts, as well as some covered call writing against common positions. These positions hedged risk as well as generated income. Expressed as an approximate monthly average, RH Tactical Rotation options activity impacted monthly performance an average of (1.07%).

RH Tactical Outlook had minimal options activity during the reporting period. Expressed as an approximate monthly average, RH Tactical Outlook options activity had an immaterial negative impact on monthly performance.

Adaptive Alpha Opportunities ETF

Adaptive Alpha Opportunities ETF outperformed the Morningstar Moderate Aggressive Target Return Index as the Fund maintained diversification across various US sectors, industries, and international ETFs. For the fiscal year ended May 31, 2024, in the Adaptive Alpha Opportunities ETF, the one-year return on the ETF was 20.01%. This compared to

17.14% for the Morningstar Moderate Aggressive Target Risk TR Index over the same period. The gross expense ratio, as of the Fund’s most recent prospectus dated October 1, 2023, is 1.54%.

Adaptive Hedged Multi-Asset Income ETF

Adaptive Hedged Multi-Asst Income ETF outperformed the iShares Core U.S. Aggregate Bond Index as allocations to covered calls and commodities supported total return. For the fiscal year ended May 31, 2024, in the Adaptive Hedged Multi-Asset Income ETF, the one-year return on the ETF was 9.01%. This compared to 1.31% for the iShares Core US Aggregate Bond Index over the same period. The gross expense ratio, as of the Fund’s most recent prospectus dated October 1, 2023, is 1.68%.

RH Tactical Outlook ETF

RH Tactical Outlook ETF positioned across Large cap, Mid cap, Small Cap, and allocations to Mid and Small caps resulted in slight outperformance vs. Morningstar Moderate Aggressive Target Return Index. For the fiscal year ended May 31, 2024, in the RH Tactical Outlook ETF, the one-year return on the ETF was 17.38%. This compared to 17.14% for the Morningstar Moderate Aggressive Target Risk TR Index over the same time period. The gross expense ratio, as of the Fund’s most recent prospectus dated October 1, 2023, is 1.91%.

RH Tactical Rotation ETF

RH Tactical Rotation ETF maintained a balance of growth and value. A tilt towards growth sectors enhanced performance vs. Morningstar Moderate Aggressive Target Return Index during the period. For the fiscal year ended May 31, 2024, in the RH Tactical Rotation ETF, the one-year return on the ETF was 24.95%. This compared to 17.14% for the Morningstar Moderate Aggressive Target Risk TR Index over the same time period. The gross expense ratio, as of the Fund’s most recent prospectus dated October 1, 2023, is 1.93%.

Thank you for the continued opportunity to serve you.

Greg Rutherford Adaptive Investments | Scott Wetherington Adaptive Investments |

RCADP0624001

| Adaptive Alpha Opportunities ETF |

Performance Update (unaudited) |

| For the period from May 31, 2014 through May 31, 2024 |

| The graph above assumes an initial $10,000 investment and the reinvestment of dividends and capital gains distributions. This graph depicts the performance of Adaptive Alpha Opportunities ETF versus the Morningstar Moderate Aggressive Target Risk TR Index. It is important to note that the ETF is a professionally managed exchange-traded fund while the index is not available for investment and is unmanaged. The comparison is shown for illustrative purposes only. |

| Average Annual Total Returns | |

| | As of | One | Five | Ten | |

| | May 31, 2024 | Year | Year | Year | |

| | Adaptive Alpha Opportunities ETF (a) | 20.01% | 13.46% | 9.88% | |

| | Morningstar Moderate Aggressive Target Risk TR Index | 17.14% | 8.55% | 6.99% | |

| | (a) NAV Return shown. | |

Performance quoted in the previous graph represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. The Advisor has entered into an Expense Limitation Agreement with the Fund under which it has agreed to waive or reduce its fees and assume other expenses of the Fund, if necessary, in an amount that limits the Fund’s annual operating expenses (exclusive of: (i) any front-end or contingent deferred loads; (ii) brokerage fees and commissions, (iii) fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including for example option and swap fees and expenses); (iv) borrowing costs (such as interest and dividend expense on securities sold short); (v) taxes; and (vii) extraordinary expenses, such as litigation expenses (which may include indemnification of Fund officers and Trustees and contractual indemnification of Fund service providers (other than the Advisor)) to not more than 1.39% of the average daily net assets of the Fund. The expense limitation agreement runs through September 30, 2024, and may be terminated by the Board at any time. Without the waiver, the expenses would be 1.54% per the Fund’s most recent prospectus dated October 1, 2023. An investor may obtain performance data, current to the most recent month-end, by visiting ncfunds.com.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Average annual total returns are historical in nature and measure net investment income and capital gain or loss from portfolio investments assuming reinvestment of distributions.

| Adaptive Hedged Multi-Asset Income ETF |

Performance Update (unaudited) |

| For the period from May 31, 2014 through May 31, 2024 |

| The graph above assumes an initial $10,000 investment and the reinvestment of dividends and capital gains distributions. This graph depicts the performance of Adaptive Hedged Multi-Asset Income ETF versus the Bloomberg Capital US Aggregate Bond Index. It is important to note that the ETF is a professionally managed exchange-traded fund while the index is not available for investment and is unmanaged. The comparison is shown for illustrative purposes only. | |

| |

| Average Annual Total Returns | |

| | As of | One | Five | Ten | |

| | May 31, 2024 | Year | Year | Year | |

| | Adaptive Hedged Multi-Asset Income ETF (a) | 9.01% | 0.39% | 1.93% | |

| | Bloomberg Capital US Aggregate Bond Index | 1.31% | (0.17)% | 1.26% | |

| | (a) NAV Return shown. | |

Performance quoted in the previous graph represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. The Advisor has entered into an Expense Limitation Agreement with the Fund under which it has agreed to waive or reduce its fees and assume other expenses of the Fund, if necessary, in an amount that limits the Fund’s annual operating expenses (exclusive of: (i) any front-end or contingent deferred loads; (ii) brokerage fees and commissions, (iii)fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including for example option and swap fees and expenses); (iv) borrowing costs (such as interest and dividend expense on securities sold short); (v) taxes; and (vi) extraordinary expenses, such as litigation expenses (which may include indemnification of Fund officers and Trustees and contractual indemnification of Fund service providers (other than the Advisor)) to not more than 1.29% of the average daily net assets of the Fund. The expense limitation agreement runs through September 30, 2024, and may be terminated by the Board at any time. Without the waiver, the expenses would be 1.68% per the Fund’s most recent prospectus dated October 1, 2023. An investor may obtain performance data, current to the most recent month-end, by visiting ncfunds.com.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Average annual total returns are historical in nature and measure net investment income and capital gain or loss from portfolio investments assuming reinvestment of distributions.

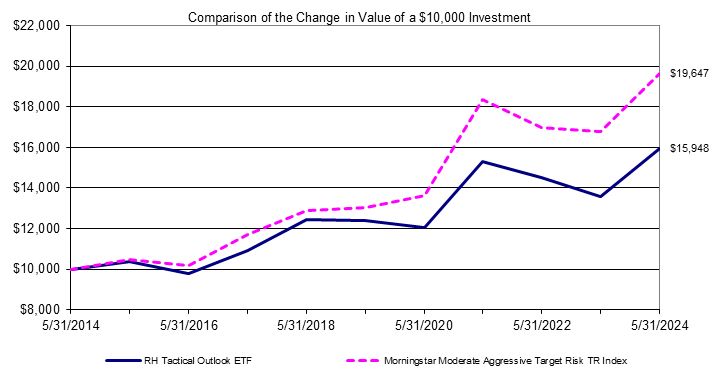

| RH Tactical Outlook ETF |

Performance Update (unaudited) |

| For the period from May 31, 2014 through May 31, 2024 |

The graph above assumes an initial $10,000 investment and the reinvestment of dividends and capital gains distributions. This graph depicts the performance of RH Tactical Outlook ETF versus the Morningstar Moderate Aggressive Target Risk TR Index. It is important to note that the ETF is a professionally managed exchange-traded fund while the index is not available for investment and is unmanaged. The comparison is shown for illustrative purposes only.

| |

| |

| Average Annual Total Returns | |

| | As of | One | Five | Ten | |

| | May 31, 2024 | Year | Year | Year | |

| | RH Tactical Outlook ETF (a) | 17.38% | 5.19% | 4.77% | |

| | Morningstar Moderate Aggressive Target Risk TR Index | 17.14% | 8.55% | 6.99% | |

| | (a) NAV Return shown. | |

Performance quoted in the previous graph represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. The Advisor has entered into an Expense Limitation Agreement with the Fund under which it has agreed to waive or reduce its fees and to assume other expenses of the Fund, if necessary, in an amount that limits the Fund's annual operating expenses (exclusive of (i) any front-end or contingent deferred loads; (ii) brokerage fees and commissions; (iii) acquired fund fees and expenses; (iv) fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including, for example, option and swap fees and expenses); (v) borrowing costs (such as interest and dividend expense on securities sold short); (vi) taxes and (vii) extraordinary expenses, such as litigation expenses (which may include indemnification of Fund officers and Trustees and contractual indemnification of Fund service providers) (other than the Advisor)) to not more than 1.25% of the average daily net assets of the Fund through September 30, 2024. The Expense Limitation Agreement may be terminated by the Board of Trustees of the Trust at any time. Without the waiver, the expenses would be 1.91% per the Fund’s most recent prospectus dated October 1, 2023. An investor may obtain performance data, current to the most recent month-end, by visiting ncfunds.com.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Average annual total returns are historical in nature and measure net investment income and capital gain or loss from portfolio investments assuming reinvestment of distributions.

|

Performance Update (unaudited) |

| For the period from May 31, 2014 through May 31, 2024 |

| The graph above assumes an initial $10,000 investment and the reinvestment of dividends and capital gains distributions. This graph depicts the performance of RH Tactical Rotation ETF versus the Morningstar Moderate Aggressive Target Risk TR Index. It is important to note that the ETF is a professionally managed exchange-traded fund while the index is not available for investment and is unmanaged. The comparison is shown for illustrative purposes only. | |

| |

| | |

| Average Annual Total Returns | |

| | As of | One | Five | Ten | |

| | May 31, 2024 | Year | Year | Year | |

| | RH Tactical Rotation ETF (a) | 24.95% | 5.83% | 5.00% | |

| | Morningstar Moderate Aggressive Target Risk TR Index | 17.14% | 8.55% | 6.99% | |

| | (a) NAV Return shown. | |

Performance quoted in the previous graph represents past performance, which is no guarantee of future results. Investment return and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. The Advisor has entered into an Expense Limitation Agreement with the Fund under which it has agreed to waive or reduce its fees and to assume other expenses of the Fund, if necessary, in an amount that limits the Fund's annual operating expenses (exclusive of (i) any front-end or contingent deferred loads; (ii) brokerage fees and commissions; (iii) acquired fund fees and expenses; (iv) fees and expenses associated with investments in other collective investment vehicles or derivative instruments (including, for example, option and swap fees and expenses); (v) borrowing costs (such as interest and dividend expense on securities sold short); (vi) taxes and (vii) extraordinary expenses, such as litigation expenses (which may include indemnification of Fund officers and Trustees and contractual indemnification of Fund service providers) (other than the Advisor)) to not more than 1.25% of the average daily net assets of the Fund through

September 30, 2024. The Expense Limitation Agreement may be terminated by the Board of Trustees of the Trust at any time. Without the waiver, the expenses would be 1.93% per the Fund’s most recent prospectus dated October 1, 2023. An investor may obtain performance data, current to the most recent month-end, by visiting ncfunds.com.

The graph and table do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Average annual total returns are historical in nature and measure net investment income and capital gain or loss from portfolio investments assuming reinvestment of distributions.

| Adaptive Alpha Opportunities ETF |

| Schedule of Investments |

| As of May 31, 2024 |

| | | | | | | | | | Shares | | Value

(Note 1) | |

| Common Stocks - 55.23% | | | | | |

| | Communications - 4.29% | | | | | |

| | | AT&T Inc | | | | | | | 110,184 | | $ 2,007,552 | |

| | | Booking Holdings Inc | | | | | | | 1,782 | | 6,729,456 | |

| | | Meta Platforms Inc | | | | | | | 6,002 | | 2,801,914 | |

| | | | | | | | | | | | 11,538,922 | |

| | Consumer Discretionary - 4.26% | | | | | | | | | | |

| | | Amazon.com Inc (a) | | | | | | | 20,000 | | 3,528,800 | |

| | | Copart Inc (a) | | | | | | | 46,030 | | 2,442,352 | |

| | | Deckers Outdoor Corp (a) | | | | | | | 3,283 | | 3,591,339 | |

| | | Green Brick Partners Inc (a) | | | | | | | 10,775 | | 588,315 | |

| | | Tri Pointe Homes Inc (a) | | | | | | | 18,850 | | 730,061 | |

| | | Winmark Corp | | | | | | | 1,611 | | 573,355 | |

| | | | | | | | | | | | 11,454,222 | |

| | Consumer Staples - 0.40% | | | | | | | | | | |

| | | elf Beauty Inc (a) | | | | | | | 5,738 | | 1,072,490 | |

| | | | | | | | | | | | | |

| | Energy - 0.03% | | | | | | | | | | |

| | | Exxon Mobil Corp | | | | | | | 410 | | 48,076 | |

| | | Marathon Petroleum Corp | | | | | | | 180 | | 31,790 | |

| | | | | | | | | | | | 79,866 | |

| | Financials - 3.28% | | | | | | | | | | |

| | | Ameriprise Financial Inc | | | | | | | 2,451 | | 1,070,131 | |

| | | Bank of America Corp | | | | | | | 16,074 | | 642,799 | |

| | | Cboe Global Markets Inc | | | | | | | 8,604 | | 1,488,406 | |

| | | Charles Schwab Corp/The | | | | | | | 9,090 | | 666,115 | |

| | | JPMorgan Chase & Co | | | | | | | 4,174 | | 845,778 | |

| | | Progressive Corp/The | | | | | | | 15,325 | | 3,236,333 | |

| | | Raymond James Financial Inc | | | | | | | 7,234 | | 887,974 | |

| | | | | | | | | | | | 8,837,536 | |

| | Health Care - 8.52% | | | | | | | | | | |

| | | Bio-Rad Laboratories Inc (a) | | | | | | | 3 | | 860 | |

| | | Boston Scientific Corp (a) | | | | | | | 66,446 | | 5,021,324 | |

| | | Eli Lilly & Co | | | | | | | 10,326 | | 8,470,831 | |

| | | Novo Nordisk A/S | | | | | | | 10,949 | | 1,481,181 | |

| | | Regeneron Pharmaceuticals Inc (a) | | | | | | | 4,825 | | 4,729,272 | |

| | | Sage Therapeutics Inc (a) | | | | | | | 11,007 | | 122,288 | |

| | | Vertex Pharmaceuticals Inc (a) | | | | | | | 6,799 | | 3,095,857 | |

| | | | | | | | | | | | 22,921,613 | |

| | Industrials - 9.34% | | | | | | | | | | |

| | | Badger Meter Inc | | | | | | | 11,958 | | 2,307,416 | |

| | | Eaton Corp PLC | | | | | | | 7,072 | | 2,353,915 | |

| | | Federal Signal Corp | | | | | | | 9,631 | | 886,244 | |

| | | General Electric Co | | | | | | | 20,000 | | 3,302,800 | |

| | | Howmet Aerospace Inc | | | | | | | 60,669 | | 5,135,631 | |

| | | Hubbell Inc | | | | | | | 1,765 | | 686,391 | |

| | | Ingersoll Rand Inc | | | | | | | 13,062 | | 1,215,419 | |

| | | Moog Inc | | | | | | | 5,525 | | 936,101 | |

| | | Quanta Services Inc | | | | | | | 1,217 | | 335,819 | |

| | | Terex Corp | | | | | | | 10,469 | | 624,685 | |

| | | TransDigm Group Inc | | | | | | | 1,823 | | 2,448,708 | |

| | | Vertiv Holdings Co | | | | | | | 20,228 | | 1,983,760 | |

See Notes to Financial Statements

| Adaptive Alpha Opportunities ETF |

Schedule of Investments (continued) |

| As of May 31, 2024 |

| | | | | | | | | | Shares | | Value

(Note 1) | |

| | Industrials (continued) | | | | | | | | | | |

| | | WESCO International Inc | | | | | | | 3,457 | | $ 620,497 | |

| | | WW Grainger Inc | | | | | | | 2,491 | | 2,295,357 | |

| | | | | | | | | | | | 25,132,743 | |

| | Materials - 0.29% | | | | | | | | | | |

| | | Ecolab Inc | | | | | | | 3,331 | | 773,458 | |

| | | | | | | | | | | | | |

| | Technology - 23.17% | | | | | | | | | | |

| | | Advanced Micro Devices Inc (a) | | | | | | | 32,147 | | 5,365,334 | |

| | | Analog Devices Inc | | | | | | | 121 | | 28,373 | |

| | | Appfolio Inc (a) | | | | | | | 10,649 | | 2,431,380 | |

| | | Apple Inc | | | | | | | 20,954 | | 4,028,407 | |

| | | Axcelis Technologies Inc (a) | | | | | | | 10,997 | | 1,237,053 | |

| | | Broadcom Inc | | | | | | | 1,668 | | 2,216,021 | |

| | | C3.ai Inc (a) | | | | | | | 31,572 | | 933,584 | |

| | | Cadence Design Systems Inc (a) | | | | | | | 4,991 | | 1,428,973 | |

| | | Fair Isaac Corp (a) | | | | | | | 1,499 | | 1,933,605 | |

| | | Manhattan Associates Inc (a) | | | | | | | 2,105 | | 462,132 | |

| | | Maximus Inc | | | | | | | 21,132 | | 1,819,465 | |

| | | Microsoft Corp | | | | | | | 15,959 | | 6,625,060 | |

| | | NVIDIA Corp | | | | | | | 16,461 | | 18,046,688 | |

| | | Oracle Corp | | | | | | | 161 | | 18,868 | |

| | | Salesforce Inc | | | | | | | 15,185 | | 3,559,971 | |

| | | Skyworks Solutions Inc | | | | | | | 6,458 | | 598,398 | |

| | | SPS Commerce Inc (a) | | | | | | | 9,926 | | 1,866,981 | |

| | | Super Micro Computer Inc (a) | | | | | | | 5,025 | | 3,942,163 | |

| | | Synopsys Inc (a) | | | | | | | 3,831 | | 2,148,425 | |

| | | Tyler Technologies Inc (a) | | | | | | | 1,449 | | 696,042 | |

| | | Verisk Analytics Inc | | | | | | | 11,649 | | 2,944,634 | |

| | | | | | | | | | | | 62,331,557 | |

| | Utilities - 1.65% | | | | | | | | | | |

| | | Constellation Energy Corp | | | | | | | 20,400 | | 4,431,900 | |

| | | | | | | | | | | | | |

| | | Total Common Stocks (Cost $124,923,612) | | | | 148,574,307 | |

| | | | | | | | | | | | | |

| Exchange-Traded Products - 35.59% | | | | | | | | | | |

| | Energy - 2.00% | | | | | | | | | | |

| | | Energy Select Sector SPDR Fund | | | | | | | 57,858 | | 5,392,366 | |

| | | | | | | | | | | | Spacer | |

| | Financials - 3.97% | | | | | | | | | | |

| | | Financial Select Sector SPDR Fund | | | | | | | 37,691 | | 1,569,453 | |

| | | iShares U.S. Broker-Dealers & Securities Exchanges ETF | | | | | | 1 | | 117 | |

| | | SPDR S&P Capital Markets ETF | | | | | | | 26,328 | | 2,926,936 | |

| | | SPDR S&P Regional Banking ETF | | | | | | | 216 | | 10,552 | |

| | | Vanguard Financials ETF | | | | | | | 61,000 | | 6,161,610 | |

| | | | | | | | | | | | 10,668,668 | |

| | Global - 0.48% | | | | | | | | | | |

| | | Global X MSCI Argentina ETF | | | | | | | 20,661 | | 1,296,684 | |

| | | | | | | | | | | | Spacer | |

| | Health Care - 0.01% | | | | | | | | | | |

| | | iShares U.S. Medical Devices ETF | | | | | | | 276 | | 15,326 | |

| | | | | | | | | | | | | |

See Notes to Financial Statements

| Adaptive Alpha Opportunities ETF |

Schedule of Investments (continued) |

| As of May 31, 2024 |

| | | | | | | | | | Shares | | Value

(Note 1) | |

Exchange-Traded Products (continued) | | | | | |

| | Industrials - 0.84% | | | | | | | | | | |

| | | Industrial Select Sector SPDR Fund | | | | | | | 2,164 | | $ 267,276 | |

| | | SPDR S&P Aerospace & Defense ETF | | | | | | | 13,804 | | 1,981,840 | |

| | | | | | | | | | | | 2,249,116 | |

| | Real Estate - 0.00% | | | | | | | | | | |

| | | SPDR S&P Homebuilders ETF | | | | | | | 100 | | 10,530 | |

| | | | | | | | | | | | | |

| | Technology - 28.29% | | | | | | | | | | |

| | | ALPS O'Shares Global Internet Giants ETF (a) | | | | | | | 318 | | 11,801 | |

| | | Invesco QQQ Trust Series 1 | | | | | | | 34,945 | | 15,750,061 | |

| | | Invesco S&P 500 Equal Weight Technology ETF | | | | | | | 152,430 | | 5,315,234 | |

| | | Technology Select Sector SPDR Fund | | | | | | | 113,359 | | 23,823,527 | |

| | | VanEck Semiconductor ETF (a) | | | | | | | 129,713 | | 31,193,382 | |

| | | | | | | | | | | | 76,094,005 | |

| | | Total Exchange-Traded Products (Cost $75,510,317) | | | | 95,726,695 | |

| | | | | | | | | | | | | |

| | | | Number of Contracts | | Exercise Price | | Exercise Date | | Notional Value | | | |

| Call Options Purchased - 10.63% | | | | | | | | | | |

| | | Advanced Micro Devices Inc | 100 | | $145 | | 6/21/2024 | | $ 1,450,000 | | 233,500 | |

| | | Advanced Micro Devices Inc | 100 | | 180 | | 6/21/2024 | | 1,800,000 | | 25,550 | |

| | | Apple Inc | 300 | | 170 | | 6/21/2024 | | 5,100,000 | | 702,750 | |

| | | Constellation Energy Corp | 600 | | 220 | | 6/21/2024 | | 13,200,000 | | 381,000 | |

| | | Eli Lilly & Co | 150 | | 815 | | 6/21/2024 | | 12,225,000 | | 333,852 | |

| | | Energy Select Sector SPDR Fund | 500 | | 98 | | 6/21/2024 | | 4,900,000 | | 10,500 | |

| | | Fair Isaac Corp | 50 | | 1,470 | | 6/21/2024 | | 7,350,000 | | 14,625 | |

| | | Howmet Aerospace Inc | 500 | | 85 | | 6/21/2024 | | 4,250,000 | | 83,750 | |

| | | Invesco QQQ Trust Series 1 | 200 | | 455 | | 6/21/2024 | | 9,100,000 | | 105,300 | |

| | | Invesco QQQ Trust Series 1 | 200 | | 460 | | 6/21/2024 | | 9,200,000 | | 61,900 | |

| | | Novo Nordisk A/S | 100 | | 130 | | 6/21/2024 | | 1,300,000 | | 73,000 | |

| | | NVIDIA Corp | 200 | | 940 | | 6/7/2024 | | 18,800,000 | | 3,155,000 | |

| | | NVIDIA Corp | 100 | | 1,105 | | 6/7/2024 | | 11,050,000 | | 257,000 | |

| | | NVIDIA Corp | 200 | | 1,120 | | 6/7/2024 | | 22,400,000 | | 398,500 | |

| | | NVIDIA Corp | 100 | | 945 | | 6/14/2024 | | 9,450,000 | | 1,569,250 | |

| | | NVIDIA Corp | 100 | | 850 | | 6/21/2024 | | 8,500,000 | | 2,508,500 | |

| | | NVIDIA Corp | 339 | | 900 | | 6/21/2024 | | 30,510,000 | | 6,860,513 | |

| | | NVIDIA Corp | 300 | | 930 | | 6/21/2024 | | 27,900,000 | | 5,229,000 | |

| | | NVIDIA Corp | 100 | | 1,060 | | 6/21/2024 | | 10,600,000 | | 714,750 | |

| | | NVIDIA Corp | 100 | | 1,120 | | 6/21/2024 | | 11,200,000 | | 390,250 | |

| | | NVIDIA Corp | 200 | | 1,135 | | 6/21/2024 | | 22,700,000 | | 704,500 | |

| | | NVIDIA Corp | 200 | | 1,140 | | 6/21/2024 | | 22,800,000 | | 668,500 | |

| | | NVIDIA Corp | 100 | | 1,130 | | 7/19/2024 | | 11,300,000 | | 594,000 | |

| | | Super Micro Computer Inc | 50 | | 775 | | 6/7/2024 | | 3,875,000 | | 154,365 | |

| | | Super Micro Computer Inc | 50 | | 825 | | 6/14/2024 | | 4,125,000 | | 134,500 | |

| | | Super Micro Computer Inc | 50 | | 760 | | 6/21/2024 | | 3,800,000 | | 270,391 | |

| | | Super Micro Computer Inc | 100 | | 880 | | 6/21/2024 | | 8,800,000 | | 195,000 | |

| | | Super Micro Computer Inc | 50 | | 905 | | 6/21/2024 | | 4,525,000 | | 75,000 | |

| | | Technology Select Sector SPDR Fund | 86 | | 195 | | 6/21/2024 | | 1,677,000 | | 138,030 | |

| | | Technology Select Sector SPDR Fund | 300 | | 210 | | 6/21/2024 | | 6,300,000 | | 116,250 | |

| | | Tesla Inc | 200 | | 150 | | 6/21/2024 | | 3,000,000 | | 585,000 | |

See Notes to Financial Statements

| Adaptive Alpha Opportunities ETF |

Schedule of Investments (continued) |

| As of May 31, 2024 |

| | | | Number of Contracts | | Exercise Price | | Exercise Date | | Notional Value | | Value

(Note 1) | |

Call Options Purchased (continued) | | | | | |

| | | VanEck Semiconductor ETF | 200 | | $ 225 | | 6/21/2024 | | $ 4,500,000 | | $ 348,000 | |

| | | VanEck Semiconductor ETF | 500 | | 235 | | 6/21/2024 | | 11,750,000 | | 497,500 | |

| | | VanEck Semiconductor ETF | 500 | | 240 | | 6/21/2024 | | 12,000,000 | | 345,000 | |

| | | VanEck Semiconductor ETF | 300 | | 245 | | 6/21/2024 | | 7,350,000 | | 135,000 | |

| | | Vertiv Holdings Co | 200 | | 95 | | 6/21/2024 | | 1,900,000 | | 96,800 | |

| | | Vistra Corp | 100 | | 88 | | 6/21/2024 | | 880,000 | | 117,000 | |

| | | Vistra Corp | 500 | | 95 | | 6/21/2024 | | 4,750,000 | | 300,000 | |

| | | Call Options Purchased (Premium Paid $18,161,822) | | | | 28,583,326 | |

| | | | | | | | | | | | | |

| Put Options Purchased - 3.07% | | | | | | | | | | |

| | | Advanced Micro Devices Inc | 200 | | 165 | | 6/21/2024 | | 3,300,000 | | 110,000 | |

| | | AT&T Inc | 500 | | 18 | | 6/21/2024 | | 900,000 | | 14,500 | |

| | | AT&T Inc | 500 | | 18 | | 7/19/2024 | | 900,000 | | 27,000 | |

| | | Booking Holdings Inc | 25 | | 3,420 | | 6/21/2024 | | 8,550,000 | | 9,250 | |

| | | Eli Lilly & Co | 150 | | 810 | | 6/21/2024 | | 12,150,000 | | 262,848 | |

| | | Howmet Aerospace Inc | 500 | | 65 | | 6/21/2024 | | 3,250,000 | | 53,750 | |

| | | Meta Platforms Inc | 100 | | 490 | | 6/21/2024 | | 4,900,000 | | 264,500 | |

| | | Novo Nordisk A/S | 100 | | 125 | | 6/21/2024 | | 1,250,000 | | 4,150 | |

| | | NVIDIA Corp | 500 | | 925 | | 6/7/2024 | | 46,250,000 | | 30,500 | |

| | | NVIDIA Corp | 100 | | 935 | | 6/7/2024 | | 9,350,000 | | 7,250 | |

| | | NVIDIA Corp | 300 | | 945 | | 6/7/2024 | | 28,350,000 | | 26,100 | |

| | | NVIDIA Corp | 200 | | 1,045 | | 6/7/2024 | | 20,900,000 | | 197,500 | |

| | | NVIDIA Corp | 400 | | 1,055 | | 6/7/2024 | | 42,200,000 | | 448,000 | |

| | | NVIDIA Corp | 200 | | 1,120 | | 6/7/2024 | | 22,400,000 | | 846,000 | |

| | | NVIDIA Corp | 300 | | 875 | | 6/21/2024 | | 26,250,000 | | 72,450 | |

| | | NVIDIA Corp | 200 | | 900 | | 6/21/2024 | | 18,000,000 | | 64,000 | |

| | | NVIDIA Corp | 600 | | 945 | | 6/21/2024 | | 56,700,000 | | 307,500 | |

| | | NVIDIA Corp | 300 | | 950 | | 6/21/2024 | | 28,500,000 | | 204,000 | |

| | | NVIDIA Corp | 100 | | 1,120 | | 6/21/2024 | | 11,200,000 | | 604,250 | |

| | | NVIDIA Corp | 300 | | 1,135 | | 6/21/2024 | | 34,050,000 | | 2,092,500 | |

| | | NVIDIA Corp | 100 | | 1,140 | | 6/21/2024 | | 11,400,000 | | 725,000 | |

| | | NVIDIA Corp | 100 | | 1,130 | | 7/19/2024 | | 11,300,000 | | 849,750 | |

| | | Regeneron Pharmaceuticals Inc | 25 | | 900 | | 6/21/2024 | | 2,250,000 | | 9,375 | |

| | | SPDR S&P 500 ETF Trust | 300 | | 500 | | 6/21/2024 | | 15,000,000 | | 19,800 | |

| | | SPDR S&P 500 ETF Trust | 500 | | 502 | | 6/21/2024 | | 25,100,000 | | 37,750 | |

| | | Super Micro Computer Inc | 50 | | 905 | | 6/21/2024 | | 4,525,000 | | 652,000 | |

| | | Technology Select Sector SPDR Fund | 200 | | 205 | | 6/21/2024 | | 4,100,000 | | 29,600 | |

| | | VanEck Semiconductor ETF | 200 | | 235 | | 6/7/2024 | | 4,700,000 | | 30,200 | |

| | | VanEck Semiconductor ETF | 100 | | 235 | | 6/21/2024 | | 2,350,000 | | 38,000 | |

| | | VanEck Semiconductor ETF | 200 | | 250 | | 6/21/2024 | | 5,000,000 | | 214,000 | |

| | | Vistra Corp | 100 | | 88 | | 6/21/2024 | | 880,000 | | 8,000 | |

| | | Total Put Options Purchased (Premiums Paid $19,167,365) | | | | 8,259,523 | |

| | | | | | | | | | | | | |

| Investments, at Value (Cost $237,763,116) - 104.52% | | | | $281,143,851 | |

| Options Written (Premiums Received $10,598,518) - (6.48)% | | | | (17,436,711) |

|

| Other Assets Less Liabilities - 1.96% | | | | 5,284,240 | |

| Net Assets - 100.00% | | | | $268,991,380 | |

| | | | | | | | | | | | | |

| (a) | Non-income producing investment |

See Notes to Financial Statements

| Adaptive Alpha Opportunities ETF |

| Schedule of Options Written |

| As of May 31, 2024 |

| | | Number of Contracts | | Exercise Price | | Exercise Date | | Notional Value | | Value

(Note 1) | |

| Call Options Written - (5.88)% | | | | | | | | | | |

| | Apple Inc | (300 | ) | $ 190 | | 6/21/2024 | | $ (5,700,000 | ) | $ (173,250 | ) |

| | Booking Holdings Inc | (25 | ) | 3,800 | | 6/21/2024 | | (9,500,000 | ) | (167,375 | ) |

| | Constellation Energy Corp | (300 | ) | 280 | | 8/16/2024 | | (8,400,000 | ) | (46,874 | ) |

| | Eli Lilly & Co | (100 | ) | 880 | | 7/19/2024 | | (8,800,000 | ) | (109,283 | ) |

| | Microsoft Corp | (100 | ) | 450 | | 6/21/2024 | | (4,500,000 | ) | (3,050 | ) |

| | NVIDIA Corp | (200 | ) | 1,050 | | 6/21/2024 | | (21,000,000 | ) | (1,532,000 | ) |

| | NVIDIA Corp | (400 | ) | 1,150 | | 6/21/2024 | | (46,000,000 | ) | (1,148,000 | ) |

| | NVIDIA Corp | (200 | ) | 1,170 | | 6/21/2024 | | (23,400,000 | ) | (460,500 | ) |

| | NVIDIA Corp | (500 | ) | 1,200 | | 6/21/2024 | | (60,000,000 | ) | (826,250 | ) |

| | NVIDIA Corp | (250 | ) | 1,100 | | 7/19/2024 | | (27,500,000 | ) | (1,867,500 | ) |

| | NVIDIA Corp | (600 | ) | 1,250 | | 7/19/2024 | | (75,000,000 | ) | (1,531,500 | ) |

| | NVIDIA Corp | (100 | ) | 1,300 | | 7/19/2024 | | (13,000,000 | ) | (168,000 | ) |

| | NVIDIA Corp | (100 | ) | 1,350 | | 7/19/2024 | | (13,500,000 | ) | (114,000 | ) |

| | Regeneron Pharmaceuticals Inc | (25 | ) | 980 | | 6/21/2024 | | (2,450,000 | ) | (52,625 | ) |

| | Super Micro Computer Inc | (50 | ) | 840 | | 6/21/2024 | | (4,200,000 | ) | (149,000 | ) |

| | Super Micro Computer Inc | (50 | ) | 900 | | 6/21/2024 | | (4,500,000 | ) | (73,555 | ) |

| | Super Micro Computer Inc | (150 | ) | 1,050 | | 6/21/2024 | | (15,750,000 | ) | (49,500 | ) |

| | Super Micro Computer Inc | (100 | ) | 1,100 | | 6/21/2024 | | (11,000,000 | ) | (21,500 | ) |

| | Super Micro Computer Inc | (50 | ) | 1,000 | | 6/28/2024 | | (5,000,000 | ) | (42,500 | ) |

| | Super Micro Computer Inc | (50 | ) | 1,000 | | 7/19/2024 | | (5,000,000 | ) | (96,788 | ) |

| | Technology Select Sector SPDR Fund | (100 | ) | 180 | | 6/21/2024 | | (1,800,000 | ) | (309,000 | ) |

| | Technology Select Sector SPDR Fund | (200 | ) | 200 | | 6/21/2024 | | (4,000,000 | ) | (232,500 | ) |

| | Tesla Inc | (200 | ) | 195 | | 6/21/2024 | | (3,900,000 | ) | (47,200 | ) |

| | VanEck Semiconductor ETF | (100 | ) | 160 | | 6/21/2024 | | (1,600,000 | ) | (785,500 | ) |

| | VanEck Semiconductor ETF | (400 | ) | 175 | | 6/21/2024 | | (7,000,000 | ) | (2,544,000 | ) |

| | VanEck Semiconductor ETF | (400 | ) | 180 | | 6/21/2024 | | (7,200,000 | ) | (2,346,000 | ) |

| | VanEck Semiconductor ETF | (200 | ) | 195 | | 6/21/2024 | | (3,900,000 | ) | (880,000 | ) |

| | Vertiv Holdings Co | (200 | ) | 110 | | 7/19/2024 | | (2,200,000 | ) | (49,199 | ) |

| | Call Options Written (Premium Received $6,262,643) | | | | (15,826,448 | ) |

| | | | | | | | | | | | |

| Put Options Written - (0.60)% | | | | | | | | | | |

| | Booking Holdings Inc | (25 | ) | 3,100 | | 6/21/2024 | | (7,750,000 | ) | (5,625 | ) |

| | Eli Lilly & Co | (100 | ) | 730 | | 7/19/2024 | | (7,300,000 | ) | (42,913 | ) |

| | Meta Platforms Inc | (100 | ) | 420 | | 6/21/2024 | | (4,200,000 | ) | (11,050 | ) |

| | NVIDIA Corp | (100 | ) | 650 | | 6/21/2024 | | (6,500,000 | ) | (3,250 | ) |

| | NVIDIA Corp | (100 | ) | 700 | | 6/21/2024 | | (7,000,000 | ) | (5,250 | ) |

| | NVIDIA Corp | (100 | ) | 720 | | 6/21/2024 | | (7,200,000 | ) | (6,150 | ) |

| | NVIDIA Corp | (100 | ) | 750 | | 6/21/2024 | | (7,500,000 | ) | (7,900 | ) |

| | NVIDIA Corp | (400 | ) | 780 | | 6/21/2024 | | (31,200,000 | ) | (41,000 | ) |

| | NVIDIA Corp | (100 | ) | 785 | | 6/21/2024 | | (7,850,000 | ) | (10,600 | ) |

| | NVIDIA Corp | (400 | ) | 790 | | 6/21/2024 | | (31,600,000 | ) | (44,600 | ) |

| | NVIDIA Corp | (400 | ) | 960 | | 6/21/2024 | | (38,400,000 | ) | (316,000 | ) |

| | NVIDIA Corp | (100 | ) | 1,060 | | 6/21/2024 | | (10,600,000 | ) | (320,000 | ) |

| | NVIDIA Corp | (250 | ) | 750 | | 7/19/2024 | | (18,750,000 | ) | (50,625 | ) |

| | NVIDIA Corp | (300 | ) | 900 | | 7/19/2024 | | (27,000,000 | ) | (295,500 | ) |

| | NVIDIA Corp | (100 | ) | 975 | | 7/19/2024 | | (9,750,000 | ) | (231,000 | ) |

| | Regeneron Pharmaceuticals Inc | (25 | ) | 840 | | 6/21/2024 | | (2,100,000 | ) | (6,000 | ) |

| | Super Micro Computer Inc | (100 | ) | 700 | | 6/21/2024 | | (7,000,000 | ) | (164,000 | ) |

| | VanEck Semiconductor ETF | (200 | ) | 230 | | 6/21/2024 | | (4,600,000 | ) | (48,800 | ) |

| | Put Options Written (Premium Received $4,335,875) | | | | (1,610,263 | ) |

| Total Options Written (Premiums Received $10,598,518) - (6.48)% | | $ (17,436,711 | ) |

See Notes to Financial Statements

| Adaptive Alpha Opportunities ETF |

| Summary of Investments by Sector |

| As of May 31, 2024 |

| | % of Net Assets | | Value | |

| Common Stocks: | | | | |

| Communications | 4.29% | | $ 11,538,922 | |

| Consumer Discretionary | 4.26% | | 11,454,222 | |

| Consumer Staples | 0.40% | | 1,072,490 | |

| Energy | 0.03% | | 79,866 | |

| Financials | 3.28% | | 8,837,536 | |

| Health Care | 8.52% | | 22,921,613 | |

| Industrials | 9.34% | | 25,132,743 | |

| Materials | 0.29% | | 773,458 | |

| Technology | 23.17% | | 62,331,557 | |

| Utilities | 1.65% | | 4,431,900 | |

| Exchange-Traded Products: | | | | |

| Energy Fund | 2.00% | | 5,392,366 | |

| Financials | 3.97% | | 10,668,668 | |

| Global | 0.48% | | 1,296,684 | |

| Health Care | 0.01% | | 15,326 | |

| Industrial | 0.84% | | 2,249,116 | |

| Real Estate | 0.00% | | 10,530 | |

| Technology | 28.29% | | 76,094,005 | |

| Call Options Purchased | 10.63% | | 28,583,326 | |

| Put Options Purchased | 3.07% | | 8,259,523 | |

| Options Written | (6.48)% | | (17,436,711 | ) |

| Other Assets Less Liabilities | 1.96% | | 5,284,240 | |

| Total Net Assets | 100.00% | | $268,991,380 | |

See Notes to Financial Statements

| Adaptive Hedged Multi-Asset Income ETF |

| Consolidated Schedule of Investments | |

| As of May 31, 2024 |

| | | | | | | | | | Shares | | Value

(Note 1) | |

| Exchange-Traded Products - 88.57% | | | | | | | | | | |

| | Commodity Funds - 25.30% | | | | | | | | | | |

| | | Credit Suisse X-Links Gold Shares Covered Call ETN | | | | | | | 26,487 | | $ 3,929,611 | |

| | | United States Oil Fund LP (a) | | | | | | | 11,664 | | 872,701 | |

| | | | | | | | | | | | 4,802,312 | |

| | Debt Funds - 18.75% | | | | | | | | | | |

| | | iShares 20+ Year Treasury Bond ETF | | | | | | | 39,352 | | 3,559,388 | |

| | | | | | | | | | | | | |

| | Large-Cap Funds - 40.01% | | | | | | | | | | |

| | | Invesco QQQ Trust Series 1 | | | | | | | 8,502 | | 3,831,937 | |

| | | SPDR S&P 500 ETF Trust | | | | | | | 7,136 | | 3,763,312 | |

| | | | | | | | | | | | 7,595,249 | |

| | Small-Cap Funds - 4.51% | | | | | | | | | | |

| | | iShares Russell 2000 ETF | | | | | | | 4,156 | | 855,180 | |

| | | Exchange-Traded Products (Cost $16,678,857) | | | | | | | | | 16,812,129 | |

| | | | | | | | | | | | | |

| | | | Number of Contracts | | Exercise Price | | Exercise Date | | Notional Value | | | |

| Call Options Purchased - 0.08% | | | | | | | | | | |

| | | SPDR S&P 500 ETF Trust | 71 | | $550 | | 7/31/2024 | | $3,905,000 | | 14,697 | |

| | | | | | | | | | | | | |

| Put Options Purchased - 0.28% | | | | | | | | | | |

| | | SPDR S&P 500 ETF Trust | 71 | | 525 | | 7/31/2024 | | 3,727,500 | | 53,428 | |

| | | | | | | | | | | | | |

| Collateralized Mortgage Obligations - 1.88% | | | Principal | | Interest Rate | | Maturity Date | | | |

| | | Alternative Loan Trust 2005-J11 | | | $88,704 | | 5.000% | | 11/25/2020 | | 67,937 | |

| | | Alternative Loan Trust 2006-28CB | | | 528,323 | | 6.500% | | 10/25/2036 | | 170,724 | |

| | | American Home Mortgage Investment Trust 2004-1 | | | 142,851 | | 7.737% | | 4/25/2044 | | 119,082 | |

| | | Total Collateralized Mortgage Obligations (Cost $452,582) | | | | | | | | 357,743 | |

| | | | | | | | | | | | | |

| Short-Term Investment - 0.59% | | | | | | | | | | |

| | | Fidelity Government Portfolio, 5.20% (b) | | | | | | | Shares | | | |

| | | (Cost $111,524) | | | | | | | 111,524 | | 111,524 | |

| | | | | | | | | | | | | |

| Investments, at Value (Cost $17,311,324) - 91.40% | | | | | | | | | $17,349,521 | |

| Options Written (Premiums Received $46,837) - (0.25)% | | | | | | | | | (47,429) |

|

| Other Assets Less Liabilities - 8.85% | | | | | | | | | 1,679,984 | |

| Net Assets - 100.00% | | | | | | | | | $18,982,076 | |

| | | | | | | | | | | | | |

| (a) | Non-income producing |

| (b) | Represents 7-day effective SEC yield as of November 30, 2023. |

See Notes to Financial Statements

| | Adaptive Hedged Multi-Asset Income ETF |

| | Consolidated Schedule of Options Written |

| | As of May 31, 2024 |

| | | | Number of Contracts | | Exercise Price | | Exercise Date | | Notional Value | | | Value

(Note 1) | |

| Call Options Written - (0.25)% | | | | | | | | | | | |

| | | Invesco QQQ Trust Series 1 | (85) |

| $462 | | 6/3/2024 | | $(3,927,000) |

| | $ (85 | ) |

| | | iShares 20+ Year Treasury Bond ETF | (390) |

| 90 | | 6/5/2024 | | (3,510,000) |

| | (23,985 | ) |

| | | SPDR S&P 500 ETF Trust | (71) |

| 545 | | 7/31/2024 | | (3,869,500) |

| | (23,359 | ) |

| | | Call Options Written (Premium Received $46,837) | | | | | $(47,429 | ) |

| Summary of Investments by Sector | % of Net Assets | | Value | |

| Exchange-Traded Products | | | | |

| Commodity Funds | 25.30% | | $ 4,802,312 | |

| Debt Fund | 18.75% | | 3,559,388 | |

| Large-Cap Funds | 40.01% | | 7,595,249 | |

| Small-Cap Fund | 4.51% | | 855,180 | |

| Call Options Purchased | 0.08% | | 14,697 | |

| Put Options Purchased | 0.28% | | 53,428 | |

| Collateralized Mortgage Obligations | 1.88% | | 357,743 | |

| Short-Term Investment | 0.59% | | 111,524 | |

| Options Written | (0.25)% | | (47,429 | ) |

| Other Assets Less Liabilities | 8.85% | | 1,679,984 | |

| Total Net Assets | 100.00% | | $18,982,076 | |

See Notes to Financial Statements

| RH Tactical Outlook ETF | |

| Schedule of Investments | |

| As of May 31, 2024 | |

| | | | | | | | | | Shares | | Value

(Note 1) | | |

| Exchange-Traded Products - 99.87% | | | | | | | | | | | |

| | Commodity Funds - 8.53% | | | | | | | | | | | |

| | | iShares Silver Trust (a) | | | | | | | 14,064 | | $ 390,417 | | |

| | | SPDR Gold Shares (a) | | | | | | | 1,966 | | 423,280 | | |

| | | | | | | | | | | | 813,697 | | |

| | Large-Cap Funds - 50.79% | | | | | | | | | | | |

| | | SPDR S&P 500 ETF Trust | | | | | | | 9,188 | | 4,845,475 | | |

| | | | | | | | | | | | | | |

| | Mid-Cap Funds - 30.22% | | | | | | | | | | | |

| | | SPDR Portfolio S&P 400 Mid Cap ETF | | | | | | | 55,052 | | 2,883,624 | | |

| | | | | | | | | | | | | | |

| | Small-Cap Funds - 10.33% | | | | | | | | | | | |

| | | iShares Russell 2000 ETF | | | | | | | 4,790 | | 985,638 | | |

| | | | | | | | | | | | | | |

| Investments, at Value (Cost $8,111,066) - 99.87% | | $9,528,434 | | |

| Other Assets Less Liabilities - 0.13% | | 12,221 | | |

| Net Assets - 100.00% | | $9,540,655 | | |

| (a) | Non-income producing |

| Summary of Investments by Sector | % of Net Assets | | Value | |

| Exchange-Traded Products | | | | |

| Commodity Funds | 8.53% | | $ 813,697 | |

| Large-Cap Funds | 50.79% | | 4,845,475 | |

| Mid-Cap Funds | 30.22% | | 2,883,624 | |

| Small-Cap Funds | 10.33% | | 985,638 | |

| Other Assets Less Liabilities | 0.13% | | 12,221 | |

| Total Net Assets | 100.00% | | $9,540,655 | |

See Notes to Financial Statements

| RH Tactical Rotation ETF |

| Schedule of Investments |

| As of May 31, 2024 |

| | | | | | | | | | Shares | | Value

(Note 1) | |

| Exchange-Traded Products - 100.59% | | | | | | | | | | |

| | Communications - 15.08% | | | | | | | | | | |

| | | Communication Services Select Sector SPDR Fund | | 26,020 | | $ 2,166,425 | |

| | | | | | | | | | | | | |

| | Large-Cap Funds - 49.82% | | | | | | | | | | |

| | | SPDR Portfolio S&P 500 Growth ETF | | 38,768 | | 2,907,988 | |

| | | SPDR S&P 500 ETF Trust | | 8,057 | | 4,249,020 | |

| | | | | | | | | | | | 7,157,008 | |

| | Technology - 35.69% | | | | | | | | | | |

| | | Technology Select Sector SPDR Fund | | 10,644 | | 2,236,943 | |

| | | VanEck Semiconductor ETF | | 12,022 | | 2,891,051 | |

| | | | | | | | | | | | 5,127,994 | |

| | | Total Exchange-Traded Products (Cost $12,072,075) | | | | 14,451,427 | |

| | | | Number of Contracts | | Exercise Price | | Exercise Date | | Notional Value | | | |

| Call Options Purchased - 0.11% | | | | | | | | | | |

| | | SPDR S&P 500 ETF Trust (Premiums Paid $20,660) | 80 | | $550 | | 7/31/2024 | | $4,400,000 | | 16,560 | |

| | | | | | | | | | | | | |

| Put Options Purchased - 0.42% | | | | | | | | | | |

| | | SPDR S&P 500 ETF Trust (Premiums Paid $56,366) | 80 | | 525 | | 7/31/2024 | | 4,200,000 | | 60,200 | |

| | | | | | | | | | | | | |

| Investments, at Value (Cost $12,149,100) - 101.12% | | $14,528,187 | |

| Options Written (Premiums Received $31,124) - (0.18)% | | (26,320) |

|

| Liabilities in Excess of Other Assets - (0.94)% | | (134,803) |

|

| Net Assets - 100.00% | | $14,367,064 | |

| | | | | | | | | | | | | |

| RH Tactical Rotation ETF |

| Schedule of Options Written |

| As of May 31, 2024 |

| | | | Number of Contracts | | Exercise Price | | Exercise Date | | Notional Value | | Value

(Note 1) | |

| Call Options Written - (0.18)% | | | | | | | | | | |

| | | SPDR S&P 500 ETF Trust (Premium Received $31,124) | (80) |

| $545 | | 7/31/2024 | | $(4,360,000) |

| $ (26,320 | ) | |

| Summary of Investments by Sector | % of Net Assets | | Value | |

| Exchange-Traded Products | | | | |

| Communications Fund | 15.08% | | $ 2,166,425 | |

| Large-Cap Fund | 49.82% | | 7,157,008 | |

| Technology Funds | 35.69% | | 5,127,994 | |

| Call Options Purchased | 0.11% | | 16,560 | |

| Put Options Purchased | 0.42% | | 60,200 | |

| Options Written | (0.18)% | | (26,320 | ) |

| Liabilities in Excess of Other Assets | (0.94%) | | (134,803 | ) |

| Total Net Assets | 100.00% | | $14,367,064 | |

See Notes to Financial Statements

|

| Statement of Assets and Liabilities |

| As of May 31, 2024 | | | | | | | | | | | | |

| | | | | Adaptive Alpha Opportunities ETF | | Adaptive Hedged Multi-Asset Income ETF (a) | | | RH Tactical Outlook ETF | | RH Tactical Rotation ETF |

| Assets: | | | | | | | | |

| | Investments, at value | | $281,143,851 | | | $17,349,521 | | | $ 9,528,434 | | | $14,528,187 | |

| | Cash | | - | | | 1,711,597 | | | 40,170 | | | - | |

| | Receivables: | | | | | | | | | | | | |

| | | Investment sold | | 101,679,258 | | | 996 | | | - | | | - | |

| | | Dividends | | 53,913 | | | - | | | - | | | - | |

| | | Interest | | 28,644 | | | 4,300 | | | - | | | - | |

| | | Due from Advisor | | - | | | 326 | | | 124 | | | - | |

| | | Prepaid expenses | | 5,215 | | | 3,600 | | | 3,117 | | | 3,104 | |

| | Total assets | | 382,910,881 | | | 19,070,340 | | | 9,571,845 | | | 14,531,291 | |

| Liabilities: | | | | | | | | | | | | |

| | Options written, at value | | 17,436,711 | | | 47,429 | | | - | | | 26,320 | |

| | | Due to custodian | | 6,232,695 | | | - | | | - | | | 96,492 | |

| | Payables: | | | | | | | | | | | | |

| | | Investments purchased | | 90,178,756 | | | - | | | - | | | - | |

| | Accrued expenses: | | | | | | | | | | | | |

| | | Advisory fees | | 14,787 | | | - | | | - | | | 255 | |

| | | Professional fees | | 20,508 | | | 21,237 | | | 17,446 | | | 18,352 | |

| | | Trustee fees and meeting expenses | | 2,007 | | | 2,225 | | | 2,097 | | | 2,069 | |

| | | Operational expenses | | 33,845 | | | 17,184 | | | 11,453 | | | 20,540 | |

| | | Other expenses | | 192 | | | 189 | | | 194 | | | 199 | |

| | Total liabilities | | 113,919,501 | | | 88,264 | | | 31,190 | | | 164,227 | |

| Total Net Assets | | $268,991,380 | | | $18,982,076 | | | $9,540,655 | | | $14,367,064 | |

| Net Assets Consist of: | | | | | | | | | | | | |

| | Paid in capital | | $250,346,138 | | | $27,742,481 | | | $12,567,135 | | | $19,387,538 | |

| | Accumulated earnings (deficit) | | 18,645,242 | | | (8,760,405 | ) | (3,026,480 | ) | (5,020,474 | ) |

| Total Net Assets | | $268,991,380 | | | $18,982,076 | | | $ 9,540,655 | | | $14,367,064 | |

| ETF Shares Outstanding, no par value | | | | | | | | | | | | |

| | (unlimited authorized shares) | | 10,173,738 | | | 2,400,546 | | | 633,586 | | | 967,274 | |

| Net Asset Value, Per Share | | $26.44 | | | $7.91 | | | $15.06 | | | $14.85 | |

| | Investments, at cost | | $237,763,116 | | | $17,311,324 | | | $ 8,111,066 | | | $12,149,100 | |

| | Options written, premiums received | | 10,598,518 | | | 46,837 | | | - | | | 31,124 | |

(a) Consolidated

See Notes to Financial Statements

|

| Statement of Operations |

| For the fiscal year ended May 31, 2024 | | | | | | | | | | | | |

| | | Adaptive Alpha Opportunities ETF | | Adaptive Hedged Multi-Asset Income ETF (a) | | RH Tactical Outlook ETF | | RH Tactical Rotation ETF |

| Investment Income: | | | | | | | | |

| | Dividends (net of withholding tax of $2,705, $0, $0, and $0) | | $ 2,555,706 | | | $ 779,738 | | | $ 192,466 | | | $ 187,993 | |

| | Interest | | 431,591 | | | 67,101 | | | 734 | | | - | |

| | Total Investment Income | | 2,987,297 | | | 846,839 | | | 193,200 | | | 187,993 | |

| Expenses: | | | | | | | | | | | | |

| | Advisory fees (note 2) | | 2,290,706 | | | 248,433 | | | 136,600 | | | 165,198 | |

| | Administration fees | | 227,024 | | | 45,342 | | | 24,523 | | | 26,800 | |

| | Professional fees | | 44,488 | | | 90,650 | | | 44,103 | | | 49,145 | |

| | Custody fees | | 58,515 | | | 21,071 | | | 11,500 | | | 10,865 | |

| | Distribution fees | | 21,302 | | | 23,688 | | | 21,594 | | | 21,078 | |

| | Compliance fees | | 42,515 | | | 12,662 | | | 9,531 | | | 11,729 | |

| | Fund Accounting Fee | | 18,820 | | | 18,764 | | | 18,824 | | | 18,824 | |

| | Transfer agent fees | | 24,042 | | | 16,579 | | | 12,761 | | | 12,904 | |

| | Shareholder fulfillment fees | | 33,712 | | | 9,790 | | | 4,174 | | | 2,920 | |

| | Trustee fees and meeting expenses (note 3) | | 8,280 | | | 8,488 | | | 8,362 | | | 8,362 | |

| | Security pricing fees | | 16,227 | | | 3,710 | | | 2,774 | | | 2,210 | |

| | Insurance fees | | 8,908 | | | 4,220 | | | 3,660 | | | 3,660 | |

| | Registration and filing expenses | | 4,806 | | | 3,294 | | | 1,098 | | | 1,404 | |

| | Other expenses | | 1,978 | | | 1,974 | | | 1,978 | | | 1,978 | |

| | | | | | | | | | | | | |

| | Total Expenses | | 2,801,323 | | | 508,665 | | | 301,482 | | | 337,077 | |

| | Fees waived by Advisor (note 2) | | - | | | (192,223 | ) | (130,732 | ) | (130,579 | ) |

| | Net Expenses | | 2,801,323 | | | 316,442 | | | 170,750 | | | 206,498 | |

| Net Investment Income (Loss) | | 185,974 | | | 530,397 | | | 22,450 | | | (18,505 | ) |

| Realized and Unrealized Gain (Loss) on Investments: | | | | | | | | | | | | |

| | Net realized gain (loss) from: | | | | | | | | | | | | |

| | | Investment transactions | | (9,072,550 | ) | (294,499 | ) | 17,325 | | | 255,209 | |

| | | Options written | | 5,470,057 | | | 900,266 | | | (133,666 | ) | (207,740 | ) |

| | | In-kind transactions | | 4,363,737 | | | 196,565 | | | 500,844 | | | 911,033 | |

| | Total realized gain (loss) | | 761,244 | | | 802,332 | | 384,503 | | | 958,502 | |

| | | | | | | | | | | | | |

| | Net change in unrealized appreciation (depreciation) on: | | | | | | | | | | | | |

| | | Investment transactions | | 48,856,426 | | | 665,377 | | | 1,371,685 | | | 2,401,566 | |

| | | Options written | | (7,009,017 | ) | | 48,609 | | | - | | | 35,972 | |

| | Total change in unrealized appreciation | | 41,847,409 | | | 713,986 | | | 1,371,685 | | | 2,437,538 | |

| Net Realized and Unrealized Gain (Loss) on Investments | | 42,608,653 | | | 1,516,318 | | 1,756,188 | | | 3,396,040 | |

| Net Increase in Net Assets Resulting from Operations | | $42,794,627 | | | $2,046,715 | | | $1,778,638 | | | $3,377,535 | |

(a) Consolidated

See Notes to Financial Statements

| | | | | | |

| Statements of Changes in Net Assets | | | | | | |

| For the fiscal years ended | | | | | | |

| | Adaptive Alpha Opportunities ETF | | |

| | May 31, 2024 | | | May 31, 2023 | | |

| Operations: | | | | | | |

| | Net investment income (loss) | $ 185,974 | | | $ 650,891 | | |

| | Net realized gain (loss) from investment transactions | (9,072,550 | ) | | (10,251,294 | ) |

| | Net realized gain (loss) from options written | 5,470,057 | | | 112,741 | | |

| | Net realized gain (loss) from in-kind transactions | 4,363,737 | | | 5,599,013 | | |

| | Capital gain distributions from underlying funds | - | | | 406,502 | | |

| | Net change in unrealized appreciation (depreciation) on investments | 41,847,409 | | | (205,584 | ) |

| Net Increase (Decrease) in Net Assets Resulting from Operations | 42,794,627 | | | (3,687,731 | ) |

| Distributions to Shareholders From: | | | | | | |

| | Distributable Earnings | (614,635 | ) | | (333,815 | ) |

| | Return of Capital | - | | | - | | |

| Net Decrease in Net Assets Resulting from Distributions | (614,635 | ) | | (333,815 | ) |

| Capital Share Transactions: | | | | | | |

| | Shares sold | 84,385,059 | | | 58,957,432 | | |

| | Shares repurchased | (53,128,852 | ) | | (71,230,077 | ) |

| Net Increase (Decrease) in Net Assets Resulting from Capital Share Transactions | 31,256,207 | | | (12,272,645 | ) |

| Net Increase (Decrease) in Net Assets | 73,436,199 | | | (16,294,191 | ) |

| Net Assets: | | | | | | |

| | Beginning of Year | 195,555,181 | | | 211,849,372 | | |

| | End of Year | $268,991,380 | | | $195,555,181 | | |

| Share Information: | | | | | | |

| | Shares sold | 3,550,000 | | | 2,760,000 | | |

| | Shares repurchased | (2,230,000 | ) | | (3,410,000 | ) |

| Net Increase (Decrease) in Capital Shares | 1,320,000 | | | (650,000 | ) |

(a) Consolidated

See Notes to Financial Statements

| Adaptive ETFs |

| Statements of Changes in Net Assets |

| For the fiscal years ended |

| | Adaptive Hedged Multi-Asset Income ETF | | | RH Tactical Outlook ETF | | | RH Tactical Rotation ETF | |

| | May 31, 2024 (a) | | | May 31, 2023 | | | May 31, 2024 | | | May 31, 2023 | | | May 31, 2024 | | | May 31, 2023 | |

| Operations: |

| | $ 530,397 | | | $ 1,684,618 | | | $ 22,450 | | | $ (55,466 | ) | $ (18,505 | ) | | $ 26,327 | |

| | (294,499 | ) | | (5,971,503 | ) | 17,325 | | | (2,027,942 | ) | 255,209 | | | (2,418,586 | ) |

| | 900,266 | | | 476,011 | | | (133,666 | ) | | - | | | (207,740 | ) | | 293,157 | |

| | 196,565 | | | (95,651 | ) | 500,844 | | | 334,357 | | | 911,033 | | | (30,876 | ) |

| | - | | | - | | | - | | | - | | | - | | | - | |

| | 713,986 | | | 3,311,468 | | | 1,371,685 | | | (95,741 | ) | 2,437,538 | | | 296,484 | |

| | 2,046,715 | | | (595,057 | ) | 1,778,638 | | | (1,844,792 | ) | 3,377,535 | | | (1,833,494 | ) |

| Distributions to Shareholders From: |

| | (527,681 | ) | | (1,552,215 | ) | - | | | - | | | - | | | - | |

| | (1,694,662 | ) | | (1,977,724 | ) | - | | | - | | | - | | | - | |

| | (2,222,343 | ) | | (3,529,939 | ) | - | | | - | | | - | | | - | |

| Capital Share Transactions: |

| | 14,758,931 | | | 12,243,981 | | | 817,232 | | | 4,586,940 | | | 10,311,601 | | | 1,542,248 | |

| | (43,581,321 | ) | | (8,850,005 | ) | (13,755,553 | ) | | (9,646,738 | | | (18,546,957 | ) | | (7,967,898 | |

| | (28,822,390 | ) | | 3,393,976 | | | (12,938,321 | ) | | (5,059,798 | ) | (8,235,356 | ) | | (6,425,650 | ) |

| | (28,998,018 | ) | | (731,020 | ) | (11,159,683 | ) | | (6,904,590 | ) | (4,857,821 | ) | | (8,259,144 | ) |

| Net Assets: |

| | 47,980,094 | | | 48,711,114 | | | 20,700,338 | | | 27,604,928 | | | 19,224,885 | | | 27,484,029 | |

| | $ 18,982,076 | | | $47,980,094 | | | $ 9,540,655 | | | $20,700,338 | | | $ 14,367,064 | | | $19,224,885 | |

| Share Information: |

| | 1,970,000 | | | 1,560,000 | | | 60,000 | | | 350,000 | | | 810,000 | | | 130,000 | |

| | (5,740,000 | ) | | (1,120,000 | ) | (1,040,000 | ) | | (750,000 | ) | (1,460,000 | ) | | (670,000 | ) |

| | (3,770,000 | ) | | 440,000 | | | (980,000 | ) | | (400,000 | ) | (650,000 | ) | | (540,000 | ) |

See Notes to Financial Statements

| Adaptive Alpha Opportunities ETF |

| Financial Highlights |

| | May 31, |

| For a share outstanding during each fiscal year ended | 2024 | | 2023 | | 2022 | | 2021 | | 2020 | |

| Net Asset Value, Beginning of Period | $22.09 | | $22.29 | | $25.77 | | $17.78 | | $15.55 | |

| | | | | | | | | | | | |

| Income (Loss) from Investment Operations: | | | | | | | | | | |

| | Net investment income (loss) (a) | 0.02 | | 0.08 | | (0.01) | | (0.17) | | 0.01 | |

| | Net realized and unrealized gain (loss) | | | | | | | | | | |

| | on investments | 4.40 | | (0.24) | | (1.85) | | 8.36 | | 2.69 | |

| | | | | | | | | | | | |

| Total from Investment Operations | 4.42 | | (0.16) | | (1.86) | | 8.19 | | 2.70 | |

| | | | | | | | | | | | |

| Less Distributions From: | | | | | | | | | | |

| | Net investment income | (0.07) | | (0.04) | | (0.05) | | (0.02) | | - | |

| | Net realized gains | - | | - | | (1.57) | | (0.18) | | (0.47) | |

| | | | | | | | | | | | |

| Total Distributions | (0.07) | | (0.04) | | (1.62) | | (0.20) | | (0.47) | |

| | | | | | | | | | | | |

| Net Asset Value, End of Period | $26.44 | | $22.09 | | $22.29 | | $25.77 | | $17.78 | |

| | | | | | | | | | | | |

| Total Return | 20.01% | | (0.71)% | | (8.05)% | | 46.18% | | 17.50% | |

| | | | | | | | | | | | |

| Net Assets, End of Period (in thousands) | $268,991 | | $195,555 | | $211,849 | | $153,188 | | $59,869 | |

| | | | | | | | | | | | |

| Ratios of: | | | | | | | | | | |

| Gross Expenses to Average Net Assets (b) | 1.22% | | 1.19% | | 1.18% | | 1.45% | (c) | 1.58% | (c) |

| Net Expenses to Average Net Assets (b) | 1.22% | | 1.19% | | 1.18% | | 1.26% | (c) | 1.26% | (c) |

| Net Investment Income (Loss) to Average Net Assets (b) | 0.08% | | 0.36% | | (0.02)% | | (0.75)% | | 0.07% | |

| Portfolio turnover rate | 368.05% | (d) | 22.32% | (d) | 25.74% | (d) | 94.33% | (d) | 319.85% | |

| (a) | Calculated using the average shares method. |

| (b) | Does not include expenses of the investment companies in which the Fund invests. |

| (c) | Includes interest expense of 0.01% for the fiscal years ended May 31, 2021 and 2020. |

| (d) | Excludes securities received or delivered in-kind. |

See Notes to Financial Statements

| Adaptive Hedged Multi-Asset Income ETF | |

| Financial Highlights | |

| | May 31, | |

| For a share outstanding during each fiscal year ended | 2024 (f) | | 2023 | | 2022 | | 2021 | | 2020 | |

| Net Asset Value, Beginning of Period | $7.78 | | $8.50 | | $9.83 | | $9.79 | | $10.29 | |

| | | | | | | | | | | | |

| Income (Loss) from Investment Operations: | | | | | | | | | | |

| | Net investment income (loss) (a) | 0.13 | | 0.62 | | 0.73 | | 0.26 | | 0.31 | |

| | Net realized and unrealized gain (loss) on investments | 0.54 | | (0.72) | | (1.38) | | 0.06 | | (0.47) | |

| | | | | | | | | | | | |

| Total from Investment Operations | 0.67 | | (0.10) | | (0.65) | | 0.32 | | (0.16) | |

| | | | | | | | | | | | |

| Less Distributions From: | | | | | | | | | | |

| | Net investment income | (0.13) | | (0.27) | | (0.68) | | (0.28) | | (0.34) | |

| | Return of Capital | (0.41) | | (0.35) | | - | | - | | - | |

| | | | | | | | | | | | |

| Total Distributions | (0.54) | | (0.62) | | (0.68) | | (0.28) | | (0.34) | |

| | | | | | | | | | | | |

| Net Asset Value, End of Period | $7.91 | | $7.78 | | $8.50 | | $9.83 | | $9.79 | |

| | | | | | | | | | | | |

| Total Return | 9.01% | | (1.06)% | | (6.98)% | (c) | 3.29% | | (1.62)% | |

| | | | | | | | | | | | |

| Net Assets, End of Period (in thousands) | $18,982 | | $47,980 | | $48,711 | | $18,911 | | $42,354 | |

| | | | | | | | | | | | |

| Ratios of: | | | | | | | | | | |

| Gross Expenses to Average Net Assets (b) | 1.64% | | 1.27% | | 2.29% | (d) | 1.86% | | 1.83% | |

| Net Expenses to Average Net Assets (b) | 1.02% | | 0.85% | | 1.74% | (d) | 1.25% | | 1.25% | |

| Net Investment Income to Average Net Assets (b) | 1.71% | | 7.88% | | 7.83% | (d) | 2.58% | | 3.04% | |

| Portfolio turnover rate | 596.01% | (e) | 155.15% | (e) | 225.13% | (e) | 148.62% | | 9.52% | |

| (a) | Calculated using the average shares method. | |

| (b) | Does not include expenses of the investment companies in which the Fund invests. | |

| (c) | The total return includes tax expenses. The impact on total returns was (0.44)% | |

| (d) | Gross expenses, net expenses, and net investment income include tax expenses. The impact on the ratios is 0.78%. | |

| (e) | Excludes securities received or delivered in-kind. | |

| (f) | Consolidated | |

See Notes to Financial Statements

| RH Tactical Outlook ETF |

| Financial Highlights |

| | May 31, |

| For a share outstanding during each fiscal year ended | 2024 | | 2023 | | 2022 | | 2021 | | 2020 | |

| Net Asset Value, Beginning of Period | $12.83 | | $13.71 | | $14.44 | | $11.36 | | $11.84 | |

| | | | | | | | | | | | |

| Income (Loss) from Investment Operations: | | | | | | | | | | |

| | Net investment income (loss) (a) | 0.02 | | (0.03) | | (0.03) | | 0.00 | (c) | 0.08 | |

| | Net realized and unrealized gain (loss) on investments | 2.21 | | (0.85) | | (0.70) | | 3.08 | | (0.39) | |

| Total from Investment Operations | 2.23 | | (0.88) | | (0.73) | | 3.08 | | (0.31) | |

| Less Distributions From: | | | | | | | | | | |

| | Net investment income | - | | - | | - | | - | | (0.17) | |

| Total Distributions | - | | - | | - | | - | | (0.17) | |

| | | | | | | | | | | | |

| Net Asset Value, End of Period | $15.06 | | $12.83 | | $13.71 | | $14.44 | | $11.36 | |

| | | | | | | | | | | | |

| Total Return | 17.38% | | (6.43)% | | (5.05)% | | 27.11% | | (2.84)% | |

| Net Assets, End of Period (in thousands) | $9,541 | | $20,700 | | $27,605 | | $10,816 | | $15,339 | |

| Ratios of: | | | | | | | | | | |

| Gross Expenses to Average Net Assets (b) | 2.21% | | 1.78% | | 2.01% | | 2.92% | | 2.50% | |

| Net Expenses to Average Net Assets (b) | 1.25% | | 1.25% | | 1.26% | | 1.25% | | 1.25% | |

| Net Investment Income (Loss) to Average Net Assets (b) | 0.16% | | (0.23)% | | (0.20)% | | (0.01)% | | 0.62% | |

| Portfolio turnover rate | 88.96% | (d) | 164.54% | (d) | 120.07% | (d) | 143.64% | | 141.55% | |

| (a) | Calculated using the average shares method. |

| (b) | Does not include expenses of the investment companies in which the Fund invests. |

| (c) | Less than $0.01 per share. |

| (d) | Excludes securities received or delivered in-kind. |

See Notes to Financial Statements

| RH Tactical Rotation ETF |

| Financial Highlights |

| | May 31, |

| For a share outstanding during each fiscal year ended | 2024 | | 2023 | | 2022 | | 2021 | | 2020 | |

| Net Asset Value, Beginning of Period | $11.89 | | $12.74 | | $13.36 | | $10.40 | | $11.61 | |

| Income (Loss) from Investment Operations: | | | | | | | | | | |

| | Net investment income (loss) (a) | (0.01) | | 0.01 | | (0.02) | | - | | 0.06 | |

| | Net realized and unrealized gain (loss) on investments | 2.97 | | (0.86) | | (0.60) | | 3.09 | | (0.94) | |

| Total from Investment Operations | 2.96 | | (0.85) | | (0.62) | | 3.09 | | (0.88) | |

| Less Distributions From: | | | | | | | | | | |

| | Net investment income | - | | - | | - | | (0.13) | | (0.33) | |

| Total Distributions | - | | - | | - | | (0.13) | | (0.33) | |

| | | | | | | | | | | | |

| Net Asset Value, End of Period | $14.85 | | $11.89 | | $12.74 | | $13.36 | | $10.40 | |

| | | | | | | | | | | | |

| Total Return | 24.95% | | (6.69)% | | (4.64)% | | 29.80% | | (7.98)% | |

| Net Assets, End of Period (in thousands) | $14,367 | | $19,225 | | $27,484 | | $19,021 | | $19,027 | |

| Ratios of: | | | | | | | | | | |

| Gross Expenses to Average Net Assets (b) | 2.04% | | 1.82% | | 1.74% | | 2.34% | | 1.80% | (c) |

| Net Expenses to Average Net Assets (b) | 1.25% | | 1.24% | | 1.25% | | 1.25% | | 1.25% | (c) |

| Net Investment Income (Loss) to Average Net Assets (b) | (0.11)% | | 0.11% | | (0.18)% | | 0.06% | | 0.49% | |

| Portfolio turnover rate | 243.76% | (d) | 78.83% | (d) | 293.36% | (d) | 529.41% | | 624.45% | |

| (a) | Calculated using the average shares method. |

| (b) | Does not include expenses of the investment companies in which the Fund invests. |

| (c) | Includes interest expense of less than 0.005% for the fiscal years ended May 31, 2020. |

| (d) | Excludes securities received or delivered in-kind. |

See Notes to Financial Statements

Adaptive ETFs

Notes to Financial Statements (consolidated with respect to the Adaptive Hedged Multi-Asset Income ETF)

As of May 31, 2024

| 1. | Organization and Significant Accounting Policies |

The Adaptive ETFs (the “Funds”) are each a series of the Starboard Investment Trust (“Trust”). The Trust is organized as a Delaware statutory trust and is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. Each Fund is a separate, diversified series of the Trust. Each Fund is actively managed and does not seek to replicate the performance of an index.

The Adaptive Alpha Opportunities ETF seeks to achieve its investment objective of capital appreciation by investing primarily in exchange-traded funds that are registered under the 1940 Act and not affiliated with the Fund (“Portfolio Funds”) that invest in equity securities of any market capitalization of issuers from a number of countries throughout the world, including emerging market countries. In addition to its indirect investments, the Adaptive Alpha Opportunities ETF may also invest directly in individual large cap equities and fixed income securities, as well as put and call options on index ETFs, individual equities, and cash and cash equivalents as part of its risk management strategy.

The Adaptive Hedged Multi-Asset Income ETF, previously the RH Hedged Multi-Asset Income ETF, seeks to achieve its investment objective of total return through a combination of capital appreciation and current income by investing in Portfolio Funds or by making direct investments. The Fund’s portfolio will consist of a mix of direct and indirect investments through Portfolio Funds and each may be all of the Fund’s portfolio or none of the Fund’s portfolio at any given time. In addition, the Fund may also invest directly in put and call options on index ETFs, sector ETFs, individual equities, and cash and cash equivalents as part of its risk management strategy. The Fund intends to invest up to 25% of its total assets in a wholly-owned and controlled subsidiary (the “Subsidiary”). The Subsidiary will invest its assets in ETNs and ETFs that provide exposure to commodities.

The RH Tactical Outlook ETF seeks to achieve its investment objective of total return through a combination of capital appreciation and current income, with a secondary goal of downside protection by investing in Portfolio Funds. In addition to its indirect investments, the Fund may also invest directly in put and call options on index ETFs, sector ETFs, individual equities, and cash and cash equivalents as part of its risk management strategy. The strategy will follow an asset allocation strategy under which the Advisor selects ETFs that invest in equity securities and fixed income securities.

The RH Tactical Rotation ETF seeks to achieve its investment objective of capital appreciation by investing in Portfolio Funds. In addition to its indirect investments, the Fund may also invest directly in put and call options on index ETFs, sector ETFs, individual equities, and cash and cash equivalents as part of its risk management strategy.

The Trust will issue and redeem shares at Net Asset Value (“NAV”) only in a large, specified number of shares called a “Creation Unit” or multiples thereof. A Creation Unit consists of 10,000 shares. Creation Unit transactions are typically conducted in exchange for the deposit or delivery of in-kind securities and/or cash. As a practical matter, only authorized participants may purchase or redeem these Creation Units. Except when aggregated in Creation Units, the shares are not redeemable securities of the Funds. The prices at which creations and redemptions occur are based on the next calculation of NAV after an order is received in proper form by Capital Investment Group, Inc. (the “Distributor”). Individual shares of the Funds may only be purchased and sold in secondary market transactions through brokers. Shares of the Funds are listed for trading on NYSE Arca under the trading symbols of each Fund listed in the table below, and because shares will trade at market prices rather than NAV, shares of the Funds may trade at a price greater than or less than NAV.

| Fund Name | Trading Symbol (Ticker) |

| Adaptive Alpha Opportunities ETF | AGOX |

| Adaptive Hedged Multi-Asset Income ETF | AMAX |

| RH Tactical Outlook ETF | RHTX |

| RH Tactical Rotation ETF | RHRX |

Transaction Fees