Exhibit 99.1

| PennyMac Mortgage Investment Trust September 10, 2012 Barclays Financial Services Conference |

| 2 This presentation contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, regarding management’s beliefs, estimates, projections and assumptions with respect to, among other things, the Company’s financial results, future operations, business plans and investment strategies, as well as industry and market conditions, all of which are subject to change. Words like “believe,” “expect,” “anticipate,” “promise,” “plan,” and other expressions or words of similar meanings, as well as future or conditional verbs such as “will,” “would,” “should,” “could,” or “may” are generally intended to identify forward-looking statements. Actual results and operations for any future period may vary materially from those projected herein, from past results discussed herein, or illustrative examples provided herein. Factors which could cause actual results to differ materially from historical results or those anticipated include, but are not limited to: changes in general business, economic, market and employment conditions from those expected; continued declines in residential real estate and disruption in the U.S. housing market; the availability of, and level of competition for, attractive risk-adjusted investment opportunities in residential mortgage loans and mortgage-related assets that satisfy our investment objectives and investment strategies; changes in our investment or operational objectives and strategies, including any new lines of business; the concentration of credit risks to which we are exposed; the availability, terms and deployment of short-term and long-term capital; unanticipated increases in financing and other costs, including a rise in interest rates; the performance, financial condition and liquidity of borrowers; increased rates of delinquency or decreased recovery rates on our investments; increased prepayments of the mortgage and other loans underlying our investments; changes in regulations or the occurrence of other events that impact the business, operation or prospects of government sponsored enterprises; changes in government support of homeownership; changes in governmental regulations, accounting treatment, tax rates and similar matters; and our ability to satisfy complex rules in order to qualify as a REIT for U.S. federal income tax purposes. You should not place undue reliance on any forward-looking statement and should consider all of the uncertainties and risks described above, as well as those more fully discussed in reports and other documents filed by the Company with the Securities and Exchange Commission from time to time. The Company undertakes no obligation to publicly update or revise any forward-looking statements or any other information contained herein, and the statements made in this presentation are current as of the date of this presentation only. Forward-Looking Statements Barclays Financial Services Conference |

| 3 Market Overview Home prices continue to show signs of stabilization Delinquencies are declining and home prices are firming (and in some cases, rising) Demand for foreclosure and REO properties continues to be strong Distressed whole loans available for purchase increased in 2Q12 and the flow of loans available for sale is likely to remain elevated into 2013 Transformation of the mortgage banking competitive landscape is still underway Banks continue to reduce their correspondent channel presence in favor of retail Represents a significant opportunity for non-bank aggregators with end-to-end fulfillment and servicing capabilities MSR returns remain attractive for both originated MSRs and bulk MSR acquisitions Newly produced MSRs have relatively low prepayment risk Opportunities to acquire bulk servicing will remain for the foreseeable future Barclays Financial Services Conference |

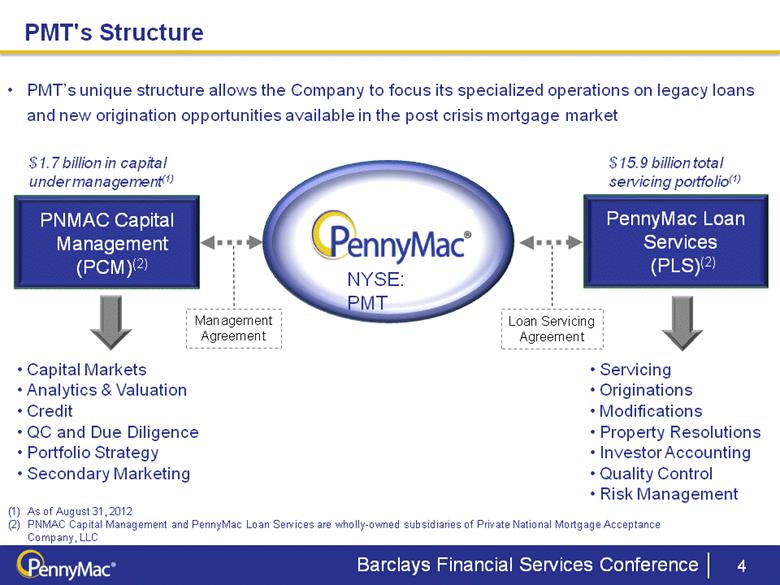

| 4 PMT's Structure NYSE: PMT PNMAC Capital Management (PCM)(2) PennyMac Loan Services (PLS)(2) Management Agreement Loan Servicing Agreement PMT’s unique structure allows the Company to focus its specialized operations on legacy loans and new origination opportunities available in the post crisis mortgage market Capital Markets Analytics & Valuation Credit QC and Due Diligence Portfolio Strategy Secondary Marketing Servicing Originations Modifications Property Resolutions Investor Accounting Quality Control Risk Management (1) As of August 31, 2012 (2) PNMAC Capital Management and PennyMac Loan Services are wholly-owned subsidiaries of Private National Mortgage Acceptance Company, LLC Barclays Financial Services Conference $1.7 billion in capital under management(1) $15.9 billion total servicing portfolio(1) |

| 5 Performance Highlights Second Quarter 2012 Earnings Net Income of $29.6 million on revenue of $64.4 million Diluted EPS of $0.79 per share; dividend of $0.55 per share; ROAE of 17% Correspondent purchase volume increased to $3.4 billion in UPB, an increase of 88% from 1Q12; conventional purchase volume reached $1.8 billion Purchased $402 million in unpaid principal balance (UPB) of distressed whole loan pools Third Quarter (Quarter-to-date) Highlights(1) Completed a common stock offering in excess of 17 million shares, with net proceeds totaling approximately $357 million Agreed to acquire a nonperforming whole loan pool totaling $452 million in UPB, which is anticipated to settle before quarter end(2) Correspondent purchase volume growth remains robust, with volume exceeding $3.9 billion in UPB through August; conventional loan purchase volume reached $2.3 billion (1) For the two months ended August 31, 2012 (2) This pending transaction is subject to continuing due diligence, customary closing conditions, and obtaining additional capital adequate to fund the acquisition. There can be no assurance that the committed amount will ultimately be acquired or that the transaction will be completed at all. Barclays Financial Services Conference |

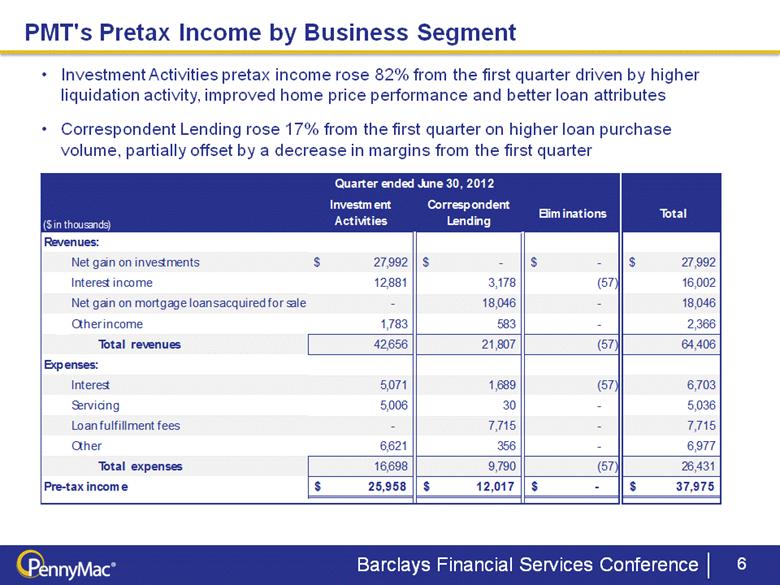

| ` PMT's Pretax Income by Business Segment 6 Barclays Financial Services Conference Investment Activities pretax income rose 82% from the first quarter driven by higher liquidation activity, improved home price performance and better loan attributes Correspondent Lending rose 17% from the first quarter on higher loan purchase volume, partially offset by a decrease in margins from the first quarter Quarter ended June 30, 2012 ($ in thousands) Investment Activities Correspondent Lending Eliminations Total Revenues: Net gain on investments 27,992 $ - $ - $ 27,992 $ Interest income 12,881 3,178 (57) 16,002 Net gain on mortgage loans acquired for sale - 18,046 - 18,046 Other income 1,783 583 - 2,366 Total revenues 42,656 21,807 (57) 64,406 Expenses: Interest 5,071 1,689 (57) 6,703 Servicing 5,006 30 - 5,036 Loan fulfillment fees - 7,715 - 7,715 Other 6,621 356 - 6,977 Total expenses 16,698 9,790 (57) 26,431 Pre-tax income 25,958 $ 12,017 $ - $ 37,975 $ |

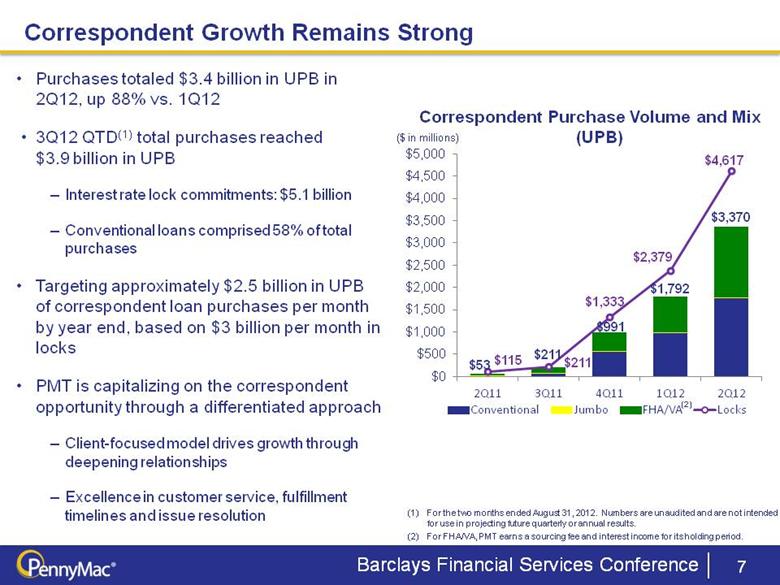

| Purchases totaled $3.4 billion in UPB in 2Q12, up 88% vs. 1Q12 3Q12 QTD(1) total purchases reached $3.9 billion in UPB Interest rate lock commitments: $5.1 billion Conventional loans comprised 58% of total purchases Targeting approximately $2.5 billion in UPB of correspondent loan purchases per month by year end, based on $3 billion per month in locks PMT is capitalizing on the correspondent opportunity through a differentiated approach Client-focused model drives growth through deepening relationships Excellence in customer service, fulfillment timelines and issue resolution Correspondent Purchase Volume and Mix (UPB) 7 Correspondent Growth Remains Strong For the two months ended August 31, 2012. Numbers are unaudited and are not intended for use in projecting future quarterly or annual results. For FHA/VA, PMT earns a sourcing fee and interest income for its holding period. ($ in millions) Barclays Financial Services Conference (2) Period Ended |

| Strong correspondent purchase activity drives the growth of PMT’s serviced for others portfolio MSRs are an attractive investment opportunity, particularly in the current environment where prepayment risk is lower Ability to organically grow PMT’s MSR asset is a key competitive advantage Actively pursuing accretive MSR acquisitions Scalable servicing infrastructure in place at PLS, with the capacity to support growth to many times the current volume of business Specialty servicing expertise of PLS helps drive future revenue opportunities for PMT Solid track record in driving modification and liquidations can be leveraged for additional opportunities 8 Servicing Portfolio Growth and Solid Performance Continues Barclays Financial Services Conference Serviced For Others Portfolio and MSR Asset ($ in millions) Modification and Liquidation Trends UPB |

| 9 Flow of Distressed Whole Loans for Sale Remains Strong Whole loan acquisitions totaled $402 million in UPB in 2Q12, comprised of both nonperforming and reperforming loans Nonperforming loans totaled $224 million (56%) and reperforming loans total $178 million (44%) in UPB Flow of distressed whole loan deals remains strong Recently agreed to acquire nonperforming whole loans totaling $452 million in UPB(1) Actively seeking additional whole loan purchases Additional purchases will likely include both nonperforming and reperforming whole loans We anticipate the pipeline of potential whole loan acquisitions to remain strong into 2Q13 and possibly longer Whole Loan Acquisitions (UPB) ($ in millions) Recent Portfolio Acquisition Summary Strats This pending transaction is subject to continuing due diligence, customary closing conditions, and obtaining additional capital adequate to fund the acquisition. There can be no assurance that the committed amount will ultimately be acquired or that the transaction will be completed at all. Barclays Financial Services Conference ($ in millions) As of 8/1/12 Outstanding Balance (UPB) 452.12 $ % Foreclosure 53% % 90+ days delinquent 47% WA delinquency (months) 23 Top states: Florida 18% California 16% Illinois 10% New York 8% New Jersey 6% |

| Portfolio Acquisitions Are Progressing in Line With Expectations 10 (1) Ratio of unpaid principal balance remaining to unpaid principal balance at acquisition Barclays Financial Services Conference Purchase 2Q12 Purchase 2Q12 Purchase 2Q12 Purchase 2Q12 Balance ($mm) 182.7 $ 85.2 Balance ($mm) 195.5 $ 82.9 Balance ($mm) 146.2 $ 65.8 Balance ($mm) 277.8 $ 176.4 Pool Factor (1) 1.00 0.47 Pool Factor (1) 1.00 0.42 Pool Factor (1) 1.00 0.45 Pool Factor (1) 1.00 0.63 Current 6.2% 26.9% Current 5.1% 29.3% Current 1.2% 23.2% Current 5.0% 29.6% 30 1.6% 6.9% 30 2.0% 4.4% 30 0.4% 4.3% 30 4.0% 6.7% 60 5.8% 5.8% 60 4.1% 3.5% 60 1.3% 4.4% 60 5.1% 3.7% 90+ 37.8% 11.2% 90+ 42.8% 9.8% 90+ 38.2% 13.7% 90+ 26.8% 10.0% FC 46.4% 41.1% FC 45.9% 40.7% FC 58.9% 39.7% FC 59.1% 41.4% REO 2.3% 8.1% REO 0.0% 12.2% REO 0.0% 14.7% REO 0.0% 8.6% Purchase 2Q12 Purchase 2Q12 Purchase 2Q12 Purchase 2Q12 Balance ($mm) 515.1 $ 379.7 Balance ($mm) 259.8 $ 209.7 Balance ($mm) 542.6 $ 381.7 Balance ($mm) 49.0 $ 46.0 Pool Factor (1) 1.00 0.74 Pool Factor (1) 1.00 0.81 Pool Factor (1) 1.00 0.70 Pool Factor (1) 1.00 0.94 Current 2.0% 24.9% Current 11.5% 28.4% Current 0.6% 8.2% Current 0.2% 1.4% 30 1.9% 4.1% 30 6.5% 5.6% 30 1.3% 2.2% 30 0.1% 0.1% 60 3.9% 1.9% 60 5.2% 3.7% 60 2.0% 1.5% 60 0.2% 0.1% 90+ 25.9% 11.5% 90+ 31.2% 11.8% 90+ 22.6% 13.6% 90+ 70.4% 54.5% FC 66.3% 46.5% FC 43.9% 40.1% FC 73.0% 61.5% FC 29.0% 42.0% REO 0.0% 11.1% REO 1.7% 10.4% REO 0.4% 12.9% REO 0.0% 1.9% 1Q10 2Q10 3Q10 4Q10 1Q11 2Q11 3Q11 4Q11 |

| 11 Illustrative Leveraged Gross Return(1) 20% - 26% 15% - 20% 27% - 39% (avg. holding period: 20 days) 25% - 32% Strategy and Outlook Investment Opportunities Seek to acquire ABS and MBS on an opportunistic basis Expect the population of potential distressed loan acquisitions to be $15-$20 billion over the next 12 months Agreed to acquire $452 million in UPB of whole loans thus far in 3Q12(2)(3) Executing on strategies prudently increase volume and expand the network of approved sellers Significant opportunities for growth Opportunities enabled by PennyMac Loan Services’ operational platform and seller/servicer approvals Transactions would be structured to optimize the qualification of some portion of the investments as REIT assets Illustrative gross returns including the effect of leverage before corporate operating and other administrative expenses For the two months ended August 31, 2012. The pending transaction s subject to continuing due diligence, customary closing conditions, and obtaining additional capital adequate to fund the acquisition. There can be no assurance that the committed amount will ultimately be acquired or that the transactions will be completed at all. Barclays Financial Services Conference |

| Key Takeaways 12 PMT’s business model and strong operational execution deliver solid results Significant opportunities exist in the current mortgage market Distressed Mortgage Assets Correspondent purchases Bulk MSR acquisitions Correspondent purchase volume continues to exceed targets, driven by client-focused model Servicing portfolio growth continues as investments in MSRs remains a key strategic focus Solid execution in liquidations and loan modifications drives higher portfolio returns PMT’s strong performance, growth, and strategic positioning ensure it is well positioned to capitalize on the growing opportunities across the mortgage market Barclays Financial Services Conference |

| 13 For questions or comments please contact us at: PennyMac Mortgage Investment Trust 6101 Condor Drive Moorpark, CA 93021 IR Contacts: Kevin Chamberlain Managing Director, Corporate Communications Christopher Oltmann Director, Investor Relations chris.oltmann@pnmac.com or InvestorRelations@pnmac.com Phone: 818-224-7442 Website: www.PennyMac-REIT.com Contact Us Barclays Financial Services Conference |

| PennyMac Mortgage Investment Trust September 10, 2012 Barclays Financial Services Conference |