Exhibit 99.1 INVESTOR DAY June 2021Exhibit 99.1 INVESTOR DAY June 2021

FORWARD-LOOKING STATEMENTS This presentation contains information from PennyMac Financial Services, Inc.’s (“PFSI”) and PennyMac Mortgage Investment Trust’s (“PMT”) joint investor day held on June 17, 2021 (collectively, “PennyMac,” “our” or “we”) and contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, regarding PFSI’s and PMT’s beliefs, estimates, projections and assumptions with respect to, among other things, financial results, operations, business plans and investment strategies, as well as industry and market conditions, all of which are subject to change. Words like “believe,” “expect,” “anticipate,” “promise,” “project,” “plan,” and other expressions or words of similar meanings, as well as future or conditional verbs such as “will,” “would,” “should,” “could,” or “may” are generally intended to identify forward-looking statements. Actual results and operations for any future period may vary materially from those projected herein and from past results discussed herein. These forward-looking statements include, but are not limited to, statements regarding the future impact of COVID-19 on our business and financial operations, loan originations and servicing, production, loan delinquencies and forbearances, servicing advances requirements and other business and financial expectations. Factors which could cause actual results to differ materially from historical results or those anticipated include, but are not limited to: our exposure to risks of loss and disruptions in operations resulting from adverse weather conditions, man-made or natural disasters, climate change and pandemics such as COVID-19; the continually changing federal, state and local laws and regulations applicable to the highly regulated industry in which we operate; lawsuits or governmental actions that may result from any noncompliance with the laws and regulations applicable to our businesses; the mortgage lending and servicing-related regulations promulgated by the Consumer Financial Protection Bureau and other regulatory bodies; our dependence on U.S. government-sponsored entities and changes in their current roles or their guarantees or guidelines; volatility in the debt or equity markets, the general economy or the real estate finance and real estate markets; changes in general business, economic, market, employment and domestic and international political conditions, or in consumer confidence and spending habits from those expected; the concentration of credit risk; the degree and nature of competition; the degree to which our hedging strategies may or may not protect against interest rate volatility; the effect of the accuracy of or changes in the estimates made about uncertainties, contingencies and asset and liability valuations when measuring and reporting upon our financial condition and results of operations; changes to government mortgage modification programs; licensing and operational regulatory requirements applicable to our business, to which bank competitors are not subject; foreclosure delays and changes in foreclosure practices; difficulties inherent in growing loan production volume; difficulties inherent in adjusting the size of our operations to reflect changes in business levels; purchase opportunities for mortgage servicing rights and our success in winning bids; our substantial amount of indebtedness; expected discontinuation of LIBOR; increases in loan delinquencies and defaults; maintaining sufficient capital and liquidity including compliance with financial covenants; unanticipated increases or volatility in financing and other costs, including changes in interest rates; our obligation to indemnify third-party purchasers or repurchase loans if loans that we originate, acquire, service or assist in the fulfillment of, fail to meet certain criteria or characteristics or under other circumstances; decreases in management and incentive fees; conflicts of interest in allocating our services and business opportunities between PFSI and PMT and their affiliates; limitations imposed on PMT’s ability to satisfy complex rules for it to qualify as a REIT for U.S. federal income tax purposes and qualify for an exclusion from the Investment Company Act of 1940 and the ability of certain of PMT’s subsidiaries to qualify as REITs or as taxable REIT subsidiaries for U.S. federal income tax purposes; the effect of public opinion on our reputation; our ability to effectively identify, manage, monitor and mitigate financial risks; our initiation or expansion of new business and investment activities or strategies; our ability to detect misconduct and fraud; our ability to maintain appropriate internal control over financial reporting; our ability to mitigate cybersecurity risks and cyber incidents; our ability to pay dividends; and our organizational structure and certain requirements in our charter documents. You should not place undue reliance on any forward-looking statement and should consider all of the uncertainties and risks described above, as well as those more fully discussed in reports and other documents filed by PFSI and PMT with the Securities and Exchange Commission from time to time. PFSI and PMT undertake no obligation to publicly update or revise any forward-looking statements or any other information contained herein, and the statements made in this presentation are current as of the date of this presentation. This presentation also contains financial information calculated other than in accordance with U.S. generally accepted accounting principles (“GAAP”), such as pretax income excluding valuation items that provide a meaningful perspective on PFSI’s business results since it utilizes this information to evaluate and manage the business. Non-GAAP disclosure has limitations as an analytical tool and should not be viewed as a substitute for financial information determined in accordance with GAAP. 2FORWARD-LOOKING STATEMENTS This presentation contains information from PennyMac Financial Services, Inc.’s (“PFSI”) and PennyMac Mortgage Investment Trust’s (“PMT”) joint investor day held on June 17, 2021 (collectively, “PennyMac,” “our” or “we”) and contains forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, regarding PFSI’s and PMT’s beliefs, estimates, projections and assumptions with respect to, among other things, financial results, operations, business plans and investment strategies, as well as industry and market conditions, all of which are subject to change. Words like “believe,” “expect,” “anticipate,” “promise,” “project,” “plan,” and other expressions or words of similar meanings, as well as future or conditional verbs such as “will,” “would,” “should,” “could,” or “may” are generally intended to identify forward-looking statements. Actual results and operations for any future period may vary materially from those projected herein and from past results discussed herein. These forward-looking statements include, but are not limited to, statements regarding the future impact of COVID-19 on our business and financial operations, loan originations and servicing, production, loan delinquencies and forbearances, servicing advances requirements and other business and financial expectations. Factors which could cause actual results to differ materially from historical results or those anticipated include, but are not limited to: our exposure to risks of loss and disruptions in operations resulting from adverse weather conditions, man-made or natural disasters, climate change and pandemics such as COVID-19; the continually changing federal, state and local laws and regulations applicable to the highly regulated industry in which we operate; lawsuits or governmental actions that may result from any noncompliance with the laws and regulations applicable to our businesses; the mortgage lending and servicing-related regulations promulgated by the Consumer Financial Protection Bureau and other regulatory bodies; our dependence on U.S. government-sponsored entities and changes in their current roles or their guarantees or guidelines; volatility in the debt or equity markets, the general economy or the real estate finance and real estate markets; changes in general business, economic, market, employment and domestic and international political conditions, or in consumer confidence and spending habits from those expected; the concentration of credit risk; the degree and nature of competition; the degree to which our hedging strategies may or may not protect against interest rate volatility; the effect of the accuracy of or changes in the estimates made about uncertainties, contingencies and asset and liability valuations when measuring and reporting upon our financial condition and results of operations; changes to government mortgage modification programs; licensing and operational regulatory requirements applicable to our business, to which bank competitors are not subject; foreclosure delays and changes in foreclosure practices; difficulties inherent in growing loan production volume; difficulties inherent in adjusting the size of our operations to reflect changes in business levels; purchase opportunities for mortgage servicing rights and our success in winning bids; our substantial amount of indebtedness; expected discontinuation of LIBOR; increases in loan delinquencies and defaults; maintaining sufficient capital and liquidity including compliance with financial covenants; unanticipated increases or volatility in financing and other costs, including changes in interest rates; our obligation to indemnify third-party purchasers or repurchase loans if loans that we originate, acquire, service or assist in the fulfillment of, fail to meet certain criteria or characteristics or under other circumstances; decreases in management and incentive fees; conflicts of interest in allocating our services and business opportunities between PFSI and PMT and their affiliates; limitations imposed on PMT’s ability to satisfy complex rules for it to qualify as a REIT for U.S. federal income tax purposes and qualify for an exclusion from the Investment Company Act of 1940 and the ability of certain of PMT’s subsidiaries to qualify as REITs or as taxable REIT subsidiaries for U.S. federal income tax purposes; the effect of public opinion on our reputation; our ability to effectively identify, manage, monitor and mitigate financial risks; our initiation or expansion of new business and investment activities or strategies; our ability to detect misconduct and fraud; our ability to maintain appropriate internal control over financial reporting; our ability to mitigate cybersecurity risks and cyber incidents; our ability to pay dividends; and our organizational structure and certain requirements in our charter documents. You should not place undue reliance on any forward-looking statement and should consider all of the uncertainties and risks described above, as well as those more fully discussed in reports and other documents filed by PFSI and PMT with the Securities and Exchange Commission from time to time. PFSI and PMT undertake no obligation to publicly update or revise any forward-looking statements or any other information contained herein, and the statements made in this presentation are current as of the date of this presentation. This presentation also contains financial information calculated other than in accordance with U.S. generally accepted accounting principles (“GAAP”), such as pretax income excluding valuation items that provide a meaningful perspective on PFSI’s business results since it utilizes this information to evaluate and manage the business. Non-GAAP disclosure has limitations as an analytical tool and should not be viewed as a substitute for financial information determined in accordance with GAAP. 2

AGENDA 1. Overview – David Spector, Andy Chang 2. Mortgage Banking Overview – Doug Jones 3. Consumer Direct Lending – Scott Bridges 4. Broker Direct Lending – Kim Nichols 5. Correspondent Production – Abbie Tidmore 6. Mortgage Fulfillment – Jim Follette 7. Loan Servicing – Steve Bailey 8. PMT – Vandy Fartaj, Will Chang 9. Capital Management & Financial Outlook – Pam Marsh, Dan Perotti 3AGENDA 1. Overview – David Spector, Andy Chang 2. Mortgage Banking Overview – Doug Jones 3. Consumer Direct Lending – Scott Bridges 4. Broker Direct Lending – Kim Nichols 5. Correspondent Production – Abbie Tidmore 6. Mortgage Fulfillment – Jim Follette 7. Loan Servicing – Steve Bailey 8. PMT – Vandy Fartaj, Will Chang 9. Capital Management & Financial Outlook – Pam Marsh, Dan Perotti 3

OVERVIEW DAVID SPECTOR Chairman and Chief Executive Officer ANDY CHANG Senior Managing Director Chief Operating OfficerOVERVIEW DAVID SPECTOR Chairman and Chief Executive Officer ANDY CHANG Senior Managing Director Chief Operating Officer

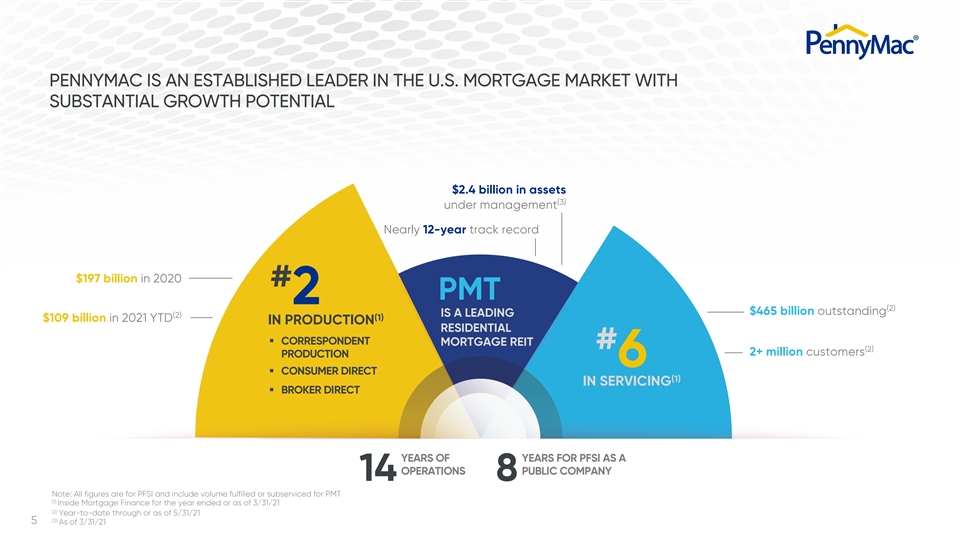

PENNYMAC IS AN ESTABLISHED LEADER IN THE U.S. MORTGAGE MARKET WITH SUBSTANTIAL GROWTH POTENTIAL $2.4 billion in assets (3) under management Nearly 12-year track record $197 billion in 2020 # PMT 2 (2) $465 billion outstanding IS A LEADING (2) (1) $109 billion in 2021 YTD IN PRODUCTION RESIDENTIAL § CORRESPONDENT MORTGAGE REIT # (2) 2+ million customers PRODUCTION 6 § CONSUMER DIRECT (1) IN SERVICING § BROKER DIRECT YEARS OF YEARS FOR PFSI AS A OPERATIONS PUBLIC COMPANY 14 8 Note: All figures are for PFSI and include volume fulfilled or subserviced for PMT (1) Inside Mortgage Finance for the year ended or as of 3/31/21 (2) Year-to-date through or as of 5/31/21 (3) 5 As of 3/31/21PENNYMAC IS AN ESTABLISHED LEADER IN THE U.S. MORTGAGE MARKET WITH SUBSTANTIAL GROWTH POTENTIAL $2.4 billion in assets (3) under management Nearly 12-year track record $197 billion in 2020 # PMT 2 (2) $465 billion outstanding IS A LEADING (2) (1) $109 billion in 2021 YTD IN PRODUCTION RESIDENTIAL § CORRESPONDENT MORTGAGE REIT # (2) 2+ million customers PRODUCTION 6 § CONSUMER DIRECT (1) IN SERVICING § BROKER DIRECT YEARS OF YEARS FOR PFSI AS A OPERATIONS PUBLIC COMPANY 14 8 Note: All figures are for PFSI and include volume fulfilled or subserviced for PMT (1) Inside Mortgage Finance for the year ended or as of 3/31/21 (2) Year-to-date through or as of 5/31/21 (3) 5 As of 3/31/21

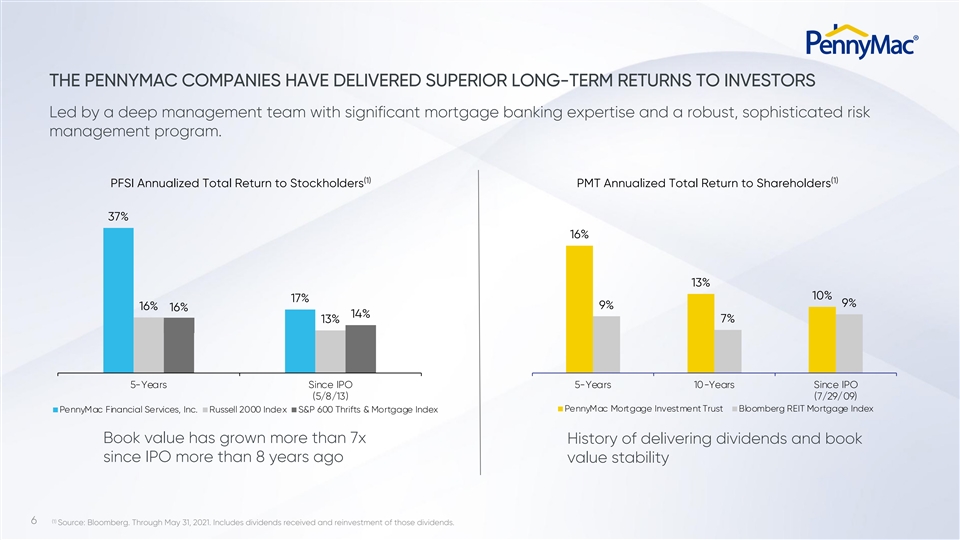

THE PENNYMAC COMPANIES HAVE DELIVERED SUPERIOR LONG-TERM RETURNS TO INVESTORS Led by a deep management team with significant mortgage banking expertise and a robust, sophisticated risk management program. (1) (1) PFSI Annualized Total Return to Stockholders PMT Annualized Total Return to Shareholders 37% 16% 13% 10% 17% 9% 9% 16% 16% 14% 13% 7% 5-Years Since IPO 5-Years 10-Years Since IPO (5/8/13) (7/29/09) PennyMac Mortgage Investment Trust Bloomberg REIT Mortgage Index PennyMac Financial Services, Inc. Russell 2000 Index S&P 600 Thrifts & Mortgage Index Book value has grown more than 7x History of delivering dividends and book since IPO more than 8 years ago value stability (1) 6 Source: Bloomberg. Through May 31, 2021. Includes dividends received and reinvestment of those dividends.THE PENNYMAC COMPANIES HAVE DELIVERED SUPERIOR LONG-TERM RETURNS TO INVESTORS Led by a deep management team with significant mortgage banking expertise and a robust, sophisticated risk management program. (1) (1) PFSI Annualized Total Return to Stockholders PMT Annualized Total Return to Shareholders 37% 16% 13% 10% 17% 9% 9% 16% 16% 14% 13% 7% 5-Years Since IPO 5-Years 10-Years Since IPO (5/8/13) (7/29/09) PennyMac Mortgage Investment Trust Bloomberg REIT Mortgage Index PennyMac Financial Services, Inc. Russell 2000 Index S&P 600 Thrifts & Mortgage Index Book value has grown more than 7x History of delivering dividends and book since IPO more than 8 years ago value stability (1) 6 Source: Bloomberg. Through May 31, 2021. Includes dividends received and reinvestment of those dividends.

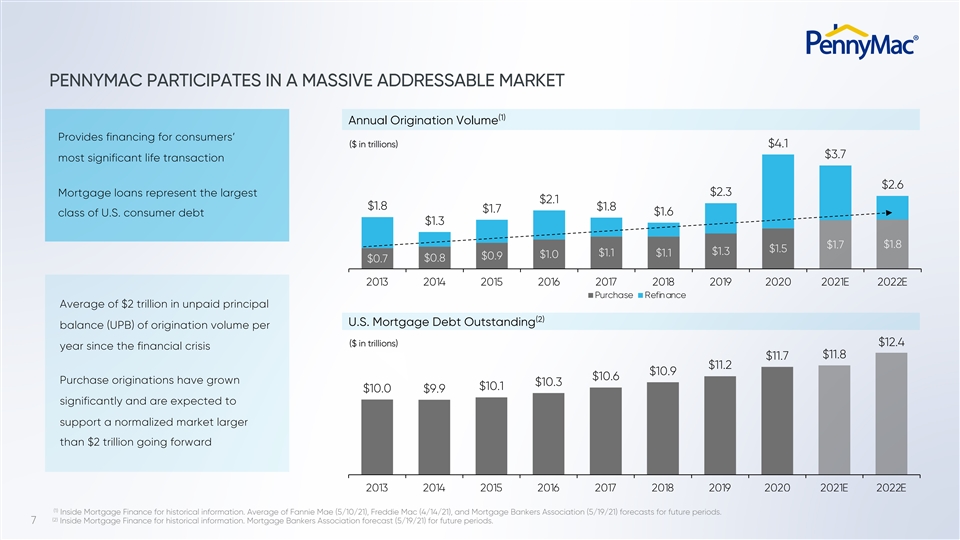

PENNYMAC PARTICIPATES IN A MASSIVE ADDRESSABLE MARKET (1) Annual Origination Volume Provides financing for consumers’ ($ in trillions) $4.1 $3.7 most significant life transaction $2.6 $2.3 Mortgage loans represent the largest $2.1 $1.8 $1.8 $1.7 class of U.S. consumer debt $1.6 $1.3 $1.7 $1.8 $1.5 $1.3 $1.1 $1.1 $1.0 $0.9 $0.7 $0.8 2013 2014 2015 2016 2017 2018 2019 2020 2021E 2022E Purchase Refinance Average of $2 trillion in unpaid principal (2) U.S. Mortgage Debt Outstanding balance (UPB) of origination volume per $12.4 ($ in trillions) year since the financial crisis $11.8 $11.7 $11.2 $10.9 $10.6 Purchase originations have grown $10.3 $10.1 $10.0 $9.9 significantly and are expected to support a normalized market larger than $2 trillion going forward 2013 2014 2015 2016 2017 2018 2019 2020 2021E 2022E (1) Inside Mortgage Finance for historical information. Average of Fannie Mae (5/10/21), Freddie Mac (4/14/21), and Mortgage Bankers Association (5/19/21) forecasts for future periods. (2) Inside Mortgage Finance for historical information. Mortgage Bankers Association forecast (5/19/21) for future periods. 7PENNYMAC PARTICIPATES IN A MASSIVE ADDRESSABLE MARKET (1) Annual Origination Volume Provides financing for consumers’ ($ in trillions) $4.1 $3.7 most significant life transaction $2.6 $2.3 Mortgage loans represent the largest $2.1 $1.8 $1.8 $1.7 class of U.S. consumer debt $1.6 $1.3 $1.7 $1.8 $1.5 $1.3 $1.1 $1.1 $1.0 $0.9 $0.7 $0.8 2013 2014 2015 2016 2017 2018 2019 2020 2021E 2022E Purchase Refinance Average of $2 trillion in unpaid principal (2) U.S. Mortgage Debt Outstanding balance (UPB) of origination volume per $12.4 ($ in trillions) year since the financial crisis $11.8 $11.7 $11.2 $10.9 $10.6 Purchase originations have grown $10.3 $10.1 $10.0 $9.9 significantly and are expected to support a normalized market larger than $2 trillion going forward 2013 2014 2015 2016 2017 2018 2019 2020 2021E 2022E (1) Inside Mortgage Finance for historical information. Average of Fannie Mae (5/10/21), Freddie Mac (4/14/21), and Mortgage Bankers Association (5/19/21) forecasts for future periods. (2) Inside Mortgage Finance for historical information. Mortgage Bankers Association forecast (5/19/21) for future periods. 7

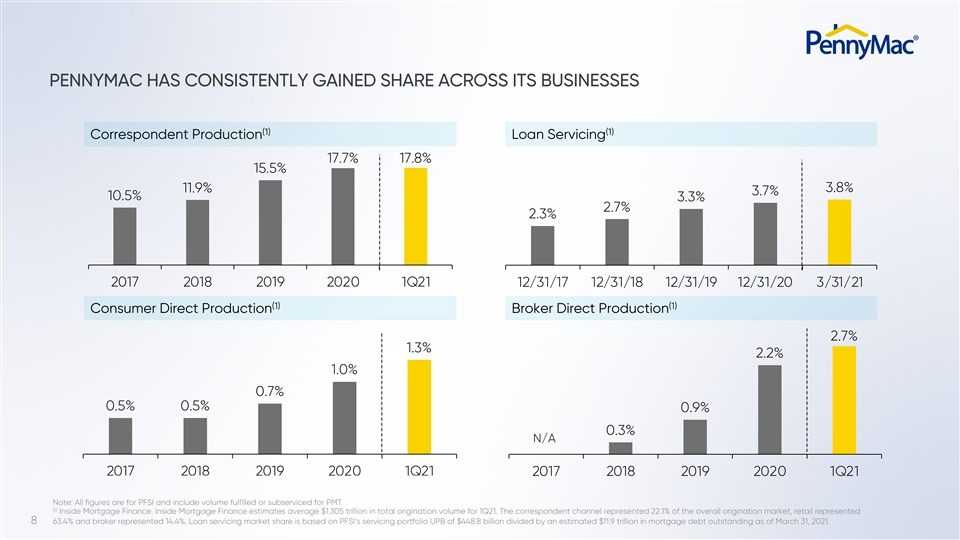

PENNYMAC HAS CONSISTENTLY GAINED SHARE ACROSS ITS BUSINESSES (1) (1) Correspondent Production Loan Servicing 17.7% 17.8% 15.5% 11.9% 3.8% 3.7% 10.5% 3.3% 2.7% 2.3% 2017 2018 2019 2020 1Q21 12/31/17 12/31/18 12/31/19 12/31/20 3/31/21 (1) (1) Consumer Direct Production Broker Direct Production 2.7% 1.3% 2.2% 1.0% 0.7% 0.5% 0.5% 0.9% 0.3% N/A 2017 2018 2019 2020 1Q21 2017 2018 2019 2020 1Q21 Note: All figures are for PFSI and include volume fulfilled or subserviced for PMT (1) Inside Mortgage Finance. Inside Mortgage Finance estimates average $1.305 trillion in total origination volume for 1Q21. The correspondent channel represented 22.1% of the overall origination market, retail represented 8 63.4% and broker represented 14.4%. Loan servicing market share is based on PFSI’s servicing portfolio UPB of $448.8 billion divided by an estimated $11.9 trillion in mortgage debt outstanding as of March 31, 2021.PENNYMAC HAS CONSISTENTLY GAINED SHARE ACROSS ITS BUSINESSES (1) (1) Correspondent Production Loan Servicing 17.7% 17.8% 15.5% 11.9% 3.8% 3.7% 10.5% 3.3% 2.7% 2.3% 2017 2018 2019 2020 1Q21 12/31/17 12/31/18 12/31/19 12/31/20 3/31/21 (1) (1) Consumer Direct Production Broker Direct Production 2.7% 1.3% 2.2% 1.0% 0.7% 0.5% 0.5% 0.9% 0.3% N/A 2017 2018 2019 2020 1Q21 2017 2018 2019 2020 1Q21 Note: All figures are for PFSI and include volume fulfilled or subserviced for PMT (1) Inside Mortgage Finance. Inside Mortgage Finance estimates average $1.305 trillion in total origination volume for 1Q21. The correspondent channel represented 22.1% of the overall origination market, retail represented 8 63.4% and broker represented 14.4%. Loan servicing market share is based on PFSI’s servicing portfolio UPB of $448.8 billion divided by an estimated $11.9 trillion in mortgage debt outstanding as of March 31, 2021.

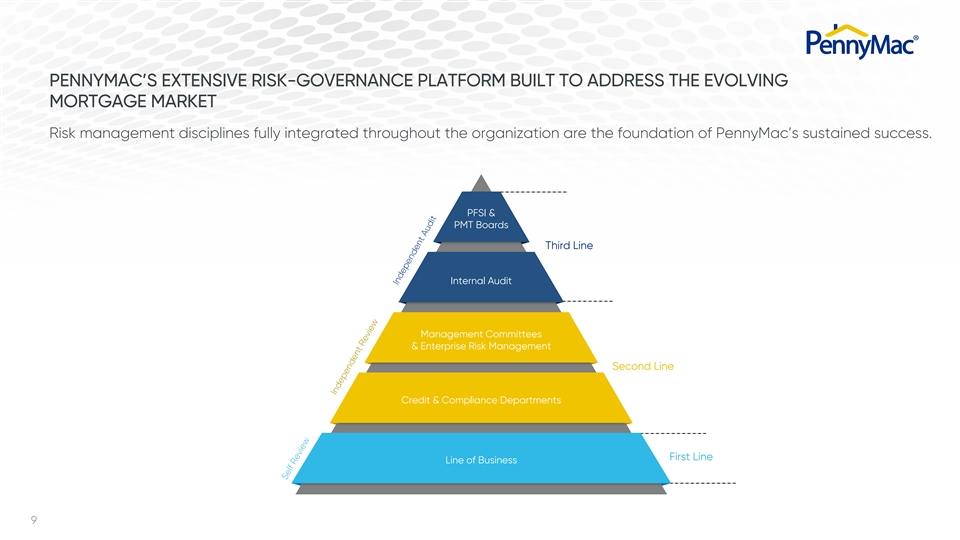

PENNYMAC’S EXTENSIVE RISK-GOVERNANCE PLATFORM BUILT TO ADDRESS THE EVOLVING MORTGAGE MARKET Risk management disciplines fully integrated throughout the organization are the foundation of PennyMac’s sustained success. PFSI & PMT Boards Third Line Internal Audit Management Committees & Enterprise Risk Management Second Line Credit & Compliance Departments First Line Line of Business 9 Independent Audit Self Review Independent ReviewPENNYMAC’S EXTENSIVE RISK-GOVERNANCE PLATFORM BUILT TO ADDRESS THE EVOLVING MORTGAGE MARKET Risk management disciplines fully integrated throughout the organization are the foundation of PennyMac’s sustained success. PFSI & PMT Boards Third Line Internal Audit Management Committees & Enterprise Risk Management Second Line Credit & Compliance Departments First Line Line of Business 9 Independent Audit Self Review Independent Review

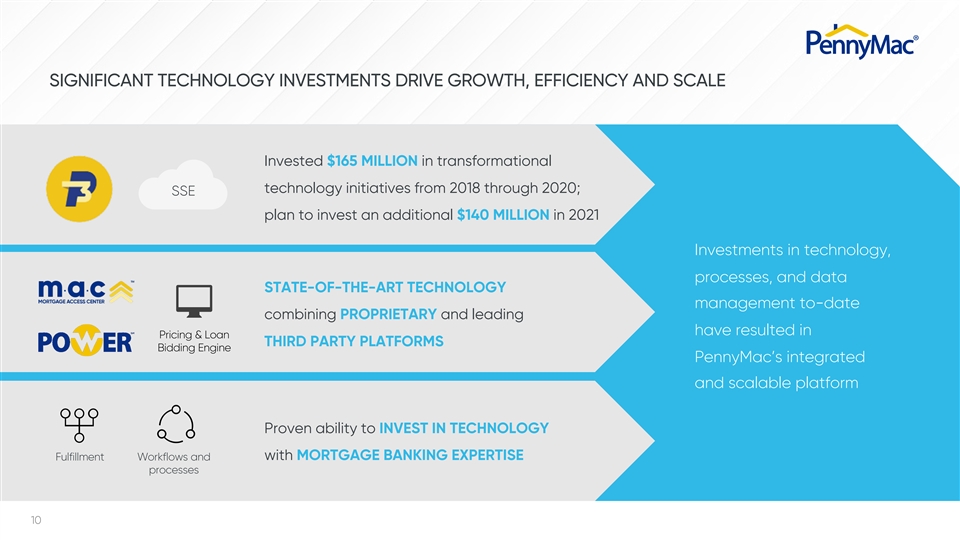

SIGNIFICANT TECHNOLOGY INVESTMENTS DRIVE GROWTH, EFFICIENCY AND SCALE Invested $165 MILLION in transformational technology initiatives from 2018 through 2020; SSE plan to invest an additional $140 MILLION in 2021 Investments in technology, processes, and data STATE-OF-THE-ART TECHNOLOGY management to-date combining PROPRIETARY and leading have resulted in Pricing & Loan THIRD PARTY PLATFORMS Bidding Engine PennyMac’s integrated and scalable platform Proven ability to INVEST IN TECHNOLOGY with MORTGAGE BANKING EXPERTISE Fulfillment Workflows and processes 10SIGNIFICANT TECHNOLOGY INVESTMENTS DRIVE GROWTH, EFFICIENCY AND SCALE Invested $165 MILLION in transformational technology initiatives from 2018 through 2020; SSE plan to invest an additional $140 MILLION in 2021 Investments in technology, processes, and data STATE-OF-THE-ART TECHNOLOGY management to-date combining PROPRIETARY and leading have resulted in Pricing & Loan THIRD PARTY PLATFORMS Bidding Engine PennyMac’s integrated and scalable platform Proven ability to INVEST IN TECHNOLOGY with MORTGAGE BANKING EXPERTISE Fulfillment Workflows and processes 10

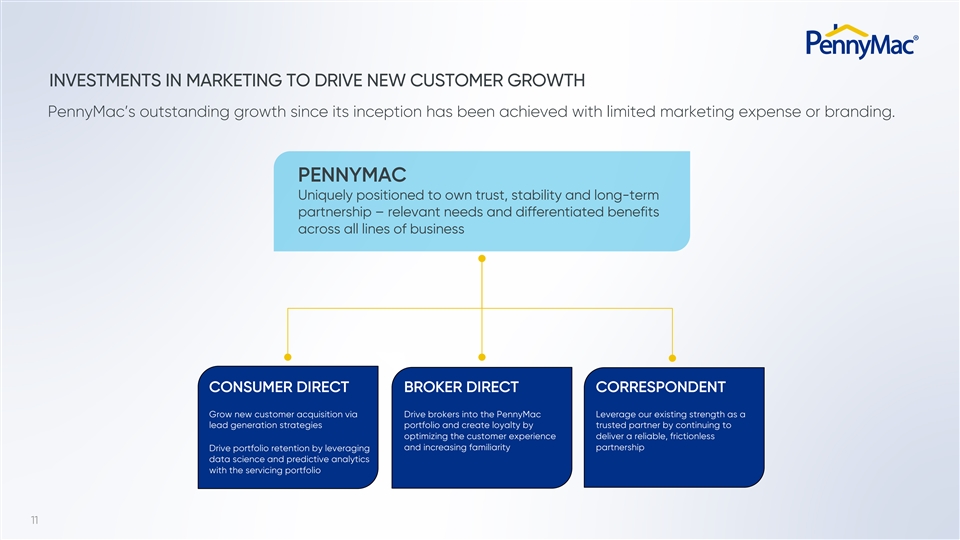

INVESTMENTS IN MARKETING TO DRIVE NEW CUSTOMER GROWTH PennyMac’s outstanding growth since its inception has been achieved with limited marketing expense or branding. PENNYMAC Uniquely positioned to own trust, stability and long-term partnership – relevant needs and differentiated benefits across all lines of business CONSUMER DIRECT BROKER DIRECT CORRESPONDENT Grow new customer acquisition via Drive brokers into the PennyMac Leverage our existing strength as a lead generation strategies portfolio and create loyalty by trusted partner by continuing to optimizing the customer experience deliver a reliable, frictionless and increasing familiarity partnership Drive portfolio retention by leveraging data science and predictive analytics with the servicing portfolio 11INVESTMENTS IN MARKETING TO DRIVE NEW CUSTOMER GROWTH PennyMac’s outstanding growth since its inception has been achieved with limited marketing expense or branding. PENNYMAC Uniquely positioned to own trust, stability and long-term partnership – relevant needs and differentiated benefits across all lines of business CONSUMER DIRECT BROKER DIRECT CORRESPONDENT Grow new customer acquisition via Drive brokers into the PennyMac Leverage our existing strength as a lead generation strategies portfolio and create loyalty by trusted partner by continuing to optimizing the customer experience deliver a reliable, frictionless and increasing familiarity partnership Drive portfolio retention by leveraging data science and predictive analytics with the servicing portfolio 11

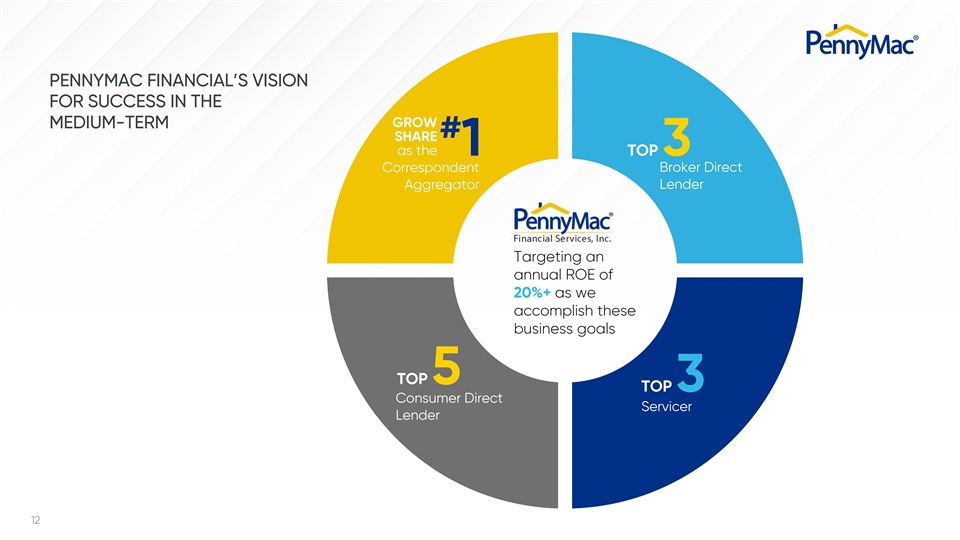

PENNYMAC FINANCIAL’S VISION FOR SUCCESS IN THE GROW MEDIUM-TERM # SHARE as the 1 TOP 3 Correspondent Broker Direct Aggregator Lender Targeting an annual ROE of 20%+ as we accomplish these business goals TOP5 TOP3 Consumer Direct Servicer Lender 12PENNYMAC FINANCIAL’S VISION FOR SUCCESS IN THE GROW MEDIUM-TERM # SHARE as the 1 TOP 3 Correspondent Broker Direct Aggregator Lender Targeting an annual ROE of 20%+ as we accomplish these business goals TOP5 TOP3 Consumer Direct Servicer Lender 12

PENNYMAC IS WELL-POSITIONED FOR LONG-TERM SUCCESS EFFECTIVE INNOVATIVE AND MULTI-CHANNEL PROPRIETARY STRATEGY TECHNOLOGY BALANCED DEEP AND STRONG AND PRODUCTION AND EXPERIENCED SOPHISTICATED SERVICING BUSINESS MANAGEMENT CAPITAL MODEL TEAM STRUCTURE LARGE-SCALE SCALABLE RISK MANAGEMENT AND EFFICIENT AND HEDGING PLATFORM EXPERTISE 13PENNYMAC IS WELL-POSITIONED FOR LONG-TERM SUCCESS EFFECTIVE INNOVATIVE AND MULTI-CHANNEL PROPRIETARY STRATEGY TECHNOLOGY BALANCED DEEP AND STRONG AND PRODUCTION AND EXPERIENCED SOPHISTICATED SERVICING BUSINESS MANAGEMENT CAPITAL MODEL TEAM STRUCTURE LARGE-SCALE SCALABLE RISK MANAGEMENT AND EFFICIENT AND HEDGING PLATFORM EXPERTISE 13

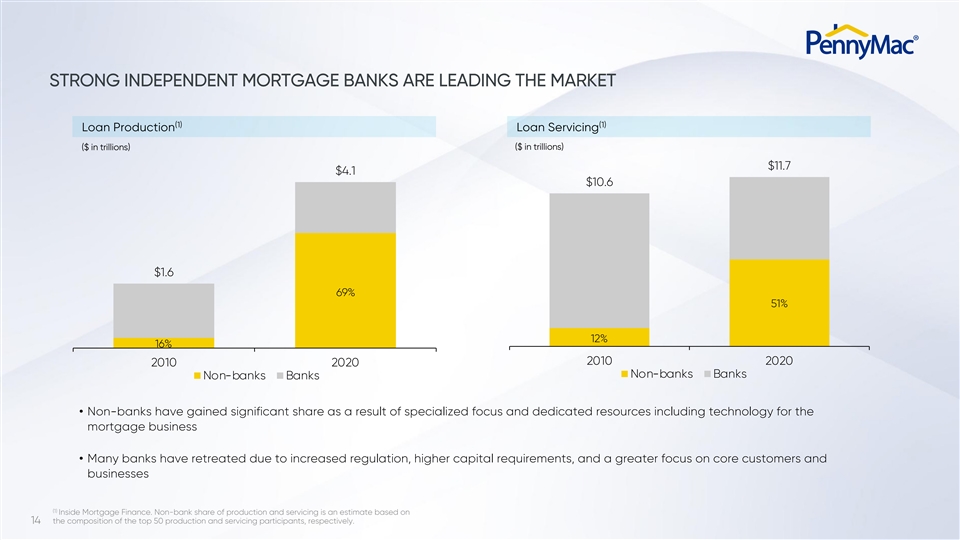

STRONG INDEPENDENT MORTGAGE BANKS ARE LEADING THE MARKET (1) (1) Loan Production Loan Servicing ($ in trillions) ($ in trillions) $11.7 $4.1 $10.6 $1.6 69% 51% 12% 16% 2010 2020 2010 2020 Non-banks Banks Non-banks Banks • Non-banks have gained significant share as a result of specialized focus and dedicated resources including technology for the mortgage business • Many banks have retreated due to increased regulation, higher capital requirements, and a greater focus on core customers and businesses (1) Inside Mortgage Finance. Non-bank share of production and servicing is an estimate based on 14 the composition of the top 50 production and servicing participants, respectively.STRONG INDEPENDENT MORTGAGE BANKS ARE LEADING THE MARKET (1) (1) Loan Production Loan Servicing ($ in trillions) ($ in trillions) $11.7 $4.1 $10.6 $1.6 69% 51% 12% 16% 2010 2020 2010 2020 Non-banks Banks Non-banks Banks • Non-banks have gained significant share as a result of specialized focus and dedicated resources including technology for the mortgage business • Many banks have retreated due to increased regulation, higher capital requirements, and a greater focus on core customers and businesses (1) Inside Mortgage Finance. Non-bank share of production and servicing is an estimate based on 14 the composition of the top 50 production and servicing participants, respectively.

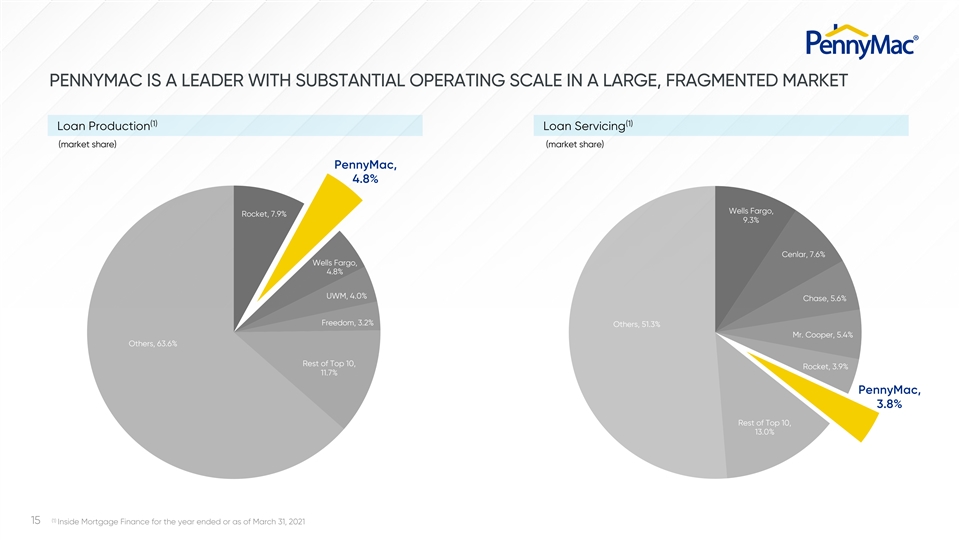

PENNYMAC IS A LEADER WITH SUBSTANTIAL OPERATING SCALE IN A LARGE, FRAGMENTED MARKET (1) (1) Loan Production Loan Servicing (market share) (market share) PennyMac, 4.8% Wells Fargo, Rocket, 7.9% 9.3% Cenlar, 7.6% Wells Fargo, 4.8% UWM, 4.0% Chase, 5.6% Freedom, 3.2% Others, 51.3% Mr. Cooper, 5.4% Others, 63.6% Rest of Top 10, Rocket, 3.9% 11.7% PennyMac, 3.8% Rest of Top 10, 13.0% (1) 15 Inside Mortgage Finance for the year ended or as of March 31, 2021PENNYMAC IS A LEADER WITH SUBSTANTIAL OPERATING SCALE IN A LARGE, FRAGMENTED MARKET (1) (1) Loan Production Loan Servicing (market share) (market share) PennyMac, 4.8% Wells Fargo, Rocket, 7.9% 9.3% Cenlar, 7.6% Wells Fargo, 4.8% UWM, 4.0% Chase, 5.6% Freedom, 3.2% Others, 51.3% Mr. Cooper, 5.4% Others, 63.6% Rest of Top 10, Rocket, 3.9% 11.7% PennyMac, 3.8% Rest of Top 10, 13.0% (1) 15 Inside Mortgage Finance for the year ended or as of March 31, 2021

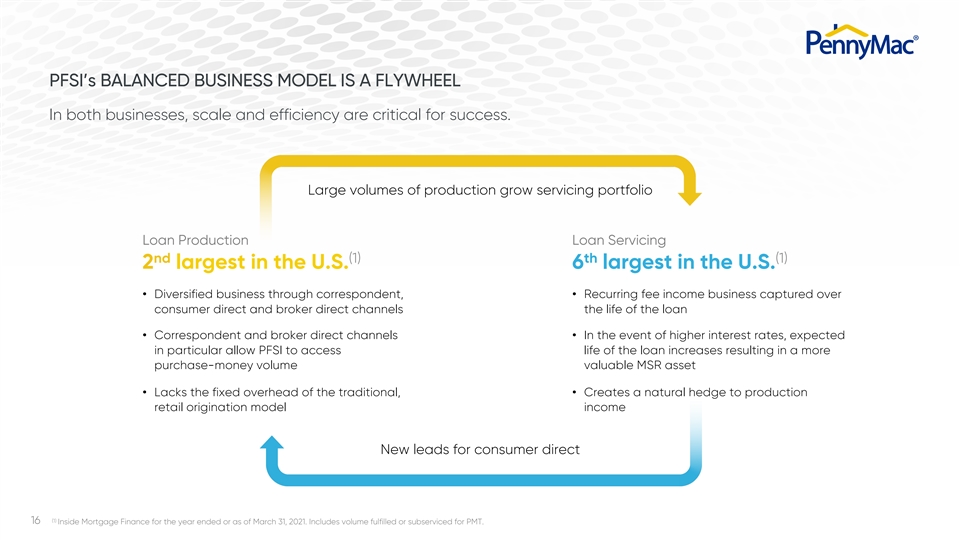

PFSI’s BALANCED BUSINESS MODEL IS A FLYWHEEL In both businesses, scale and efficiency are critical for success. Large volumes of production grow servicing portfolio Loan Production Loan Servicing nd (1) th (1) 2 largest in the U.S. 6 largest in the U.S. • Diversified business through correspondent, • Recurring fee income business captured over consumer direct and broker direct channels the life of the loan • Correspondent and broker direct channels • In the event of higher interest rates, expected in particular allow PFSI to access life of the loan increases resulting in a more purchase-money volume valuable MSR asset • Lacks the fixed overhead of the traditional, • Creates a natural hedge to production retail origination model income New leads for consumer direct (1) 16 Inside Mortgage Finance for the year ended or as of March 31, 2021. Includes volume fulfilled or subserviced for PMT.PFSI’s BALANCED BUSINESS MODEL IS A FLYWHEEL In both businesses, scale and efficiency are critical for success. Large volumes of production grow servicing portfolio Loan Production Loan Servicing nd (1) th (1) 2 largest in the U.S. 6 largest in the U.S. • Diversified business through correspondent, • Recurring fee income business captured over consumer direct and broker direct channels the life of the loan • Correspondent and broker direct channels • In the event of higher interest rates, expected in particular allow PFSI to access life of the loan increases resulting in a more purchase-money volume valuable MSR asset • Lacks the fixed overhead of the traditional, • Creates a natural hedge to production retail origination model income New leads for consumer direct (1) 16 Inside Mortgage Finance for the year ended or as of March 31, 2021. Includes volume fulfilled or subserviced for PMT.

SYNERGISTIC RELATIONSHIP PROVIDES A COMPETITIVE ADVANTAGE FOR BOTH COMPANIES Mortgage company with industry-leading operations Management Services: and technology PFSI is the external manager of PMT Fulfillment Services: Fee for service Oversight from Offers PFSI access to a PFSI performs fulfillment in arrangements for PMT independent PFSI low-cost balance sheet creates cost efficient connection with the acquisition, designed to make directors and structure with limited long-term investments PMT trustees packaging and sale of loans for operational risk in mortgage assets PMT’s correspondent production Loan Servicing: PFSI is the subservicer for PMT’s MSR portfolio Tax-efficient vehicle with long track record of success investing in residential mortgage assets 17SYNERGISTIC RELATIONSHIP PROVIDES A COMPETITIVE ADVANTAGE FOR BOTH COMPANIES Mortgage company with industry-leading operations Management Services: and technology PFSI is the external manager of PMT Fulfillment Services: Fee for service Oversight from Offers PFSI access to a PFSI performs fulfillment in arrangements for PMT independent PFSI low-cost balance sheet creates cost efficient connection with the acquisition, designed to make directors and structure with limited long-term investments PMT trustees packaging and sale of loans for operational risk in mortgage assets PMT’s correspondent production Loan Servicing: PFSI is the subservicer for PMT’s MSR portfolio Tax-efficient vehicle with long track record of success investing in residential mortgage assets 17

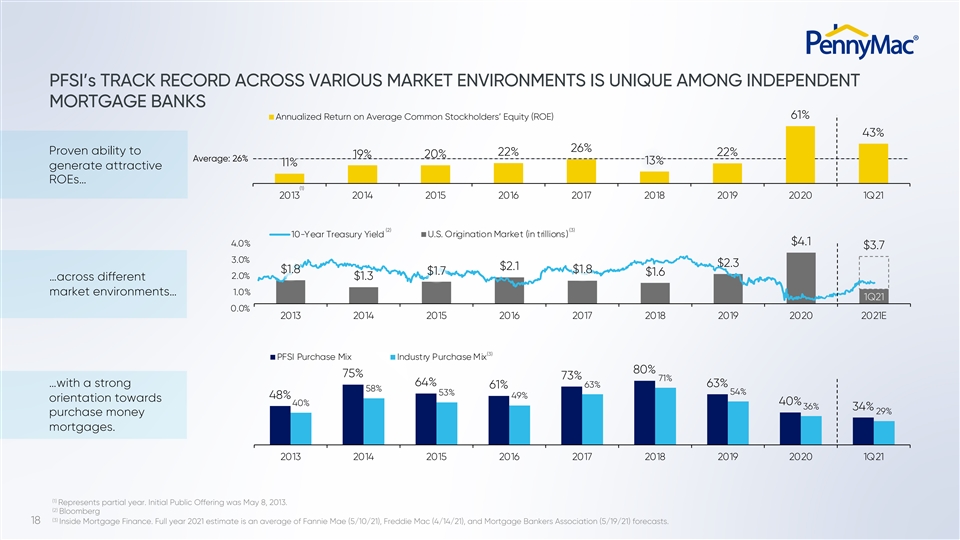

PFSI’s TRACK RECORD ACROSS VARIOUS MARKET ENVIRONMENTS IS UNIQUE AMONG INDEPENDENT MORTGAGE BANKS 61% Annualized Return on Average Common Stockholders’ Equity (ROE) 43% 26% Proven ability to 22% 22% 19% 20% Average: 26% 13% 11% generate attractive ROEs… (1) 2013 2014 2015 2016 2017 2018 2019 2020 1Q21 (2) (3) 10-Year Treasury Yield U.S. Origination Market (in trillions) $4.1 4.0% $3.7 3.0% $2.3 $2.1 $1.8 $1.8 $1.7 $1.6 2.0% $1.3 …across different market environments… 1.0% 1Q21 0.0% 2013 2014 2015 2016 2017 2018 2019 2020 2021E (3) PFSI Purchase Mix Industry Purchase Mix 80% 75% 73% 71% 64% …with a strong 63% 63% 61% 58% 54% 53% 48% 49% orientation towards 40% 40% 36% 34% 29% purchase money mortgages. 2013 2014 2015 2016 2017 2018 2019 2020 1Q21 (1) Represents partial year. Initial Public Offering was May 8, 2013. (2) Bloomberg (3) 18 Inside Mortgage Finance. Full year 2021 estimate is an average of Fannie Mae (5/10/21), Freddie Mac (4/14/21), and Mortgage Bankers Association (5/19/21) forecasts.PFSI’s TRACK RECORD ACROSS VARIOUS MARKET ENVIRONMENTS IS UNIQUE AMONG INDEPENDENT MORTGAGE BANKS 61% Annualized Return on Average Common Stockholders’ Equity (ROE) 43% 26% Proven ability to 22% 22% 19% 20% Average: 26% 13% 11% generate attractive ROEs… (1) 2013 2014 2015 2016 2017 2018 2019 2020 1Q21 (2) (3) 10-Year Treasury Yield U.S. Origination Market (in trillions) $4.1 4.0% $3.7 3.0% $2.3 $2.1 $1.8 $1.8 $1.7 $1.6 2.0% $1.3 …across different market environments… 1.0% 1Q21 0.0% 2013 2014 2015 2016 2017 2018 2019 2020 2021E (3) PFSI Purchase Mix Industry Purchase Mix 80% 75% 73% 71% 64% …with a strong 63% 63% 61% 58% 54% 53% 48% 49% orientation towards 40% 40% 36% 34% 29% purchase money mortgages. 2013 2014 2015 2016 2017 2018 2019 2020 1Q21 (1) Represents partial year. Initial Public Offering was May 8, 2013. (2) Bloomberg (3) 18 Inside Mortgage Finance. Full year 2021 estimate is an average of Fannie Mae (5/10/21), Freddie Mac (4/14/21), and Mortgage Bankers Association (5/19/21) forecasts.

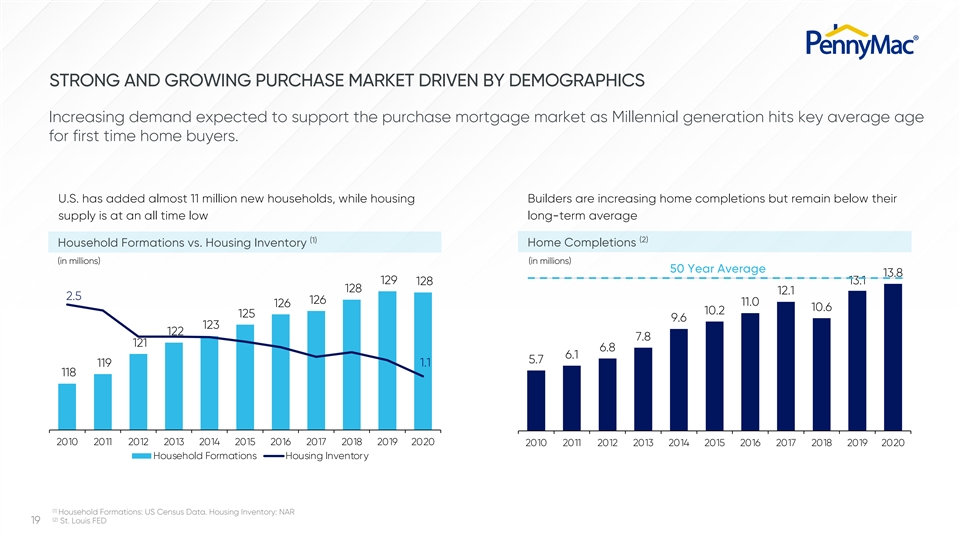

STRONG AND GROWING PURCHASE MARKET DRIVEN BY DEMOGRAPHICS Increasing demand expected to support the purchase mortgage market as Millennial generation hits key average age for first time home buyers. U.S. has added almost 11 million new households, while housing Builders are increasing home completions but remain below their supply is at an all time low long-term average (2) (1) Home Completions Household Formations vs. Housing Inventory (in millions) (in millions) 50 Year Average 13.8 3.0 130 129 13.1 128 128 12.1 128 2.5 126 2.5 11.0 126 10.6 126 10.2 125 9.6 123 2.0 124 122 7.8 121 122 6.8 1.5 6.1 5.7 120 119 1.1 118 1.0 118 116 0.5 114 - 112 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Household Formations Housing Inventory (1) Household Formations: US Census Data. Housing Inventory: NAR (2) St. Louis FED 19STRONG AND GROWING PURCHASE MARKET DRIVEN BY DEMOGRAPHICS Increasing demand expected to support the purchase mortgage market as Millennial generation hits key average age for first time home buyers. U.S. has added almost 11 million new households, while housing Builders are increasing home completions but remain below their supply is at an all time low long-term average (2) (1) Home Completions Household Formations vs. Housing Inventory (in millions) (in millions) 50 Year Average 13.8 3.0 130 129 13.1 128 128 12.1 128 2.5 126 2.5 11.0 126 10.6 126 10.2 125 9.6 123 2.0 124 122 7.8 121 122 6.8 1.5 6.1 5.7 120 119 1.1 118 1.0 118 116 0.5 114 - 112 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 2020 Household Formations Housing Inventory (1) Household Formations: US Census Data. Housing Inventory: NAR (2) St. Louis FED 19

PENNYMAC IS POSITIONED TO SUCCEED REGARDLESS OF FUTURE TRENDS INCREASED HOME CHANGING ROLE OF INCREASED PURCHASES DRIVING GSES / GOVERNMENT RELEVANCE OF THE ORIGINATION SUPPORT FOR THE NON-AGENCY MARKET MORTGAGE MARKET PRODUCTS CONTINUED INDUSTRY HIGHER ADVANCEMENTS IN CONSOLIDATION MORTGAGE RATES TECHNOLOGY AND AND GROWING OVER TIME AND HOW AMERICANS IMPORTANCE OF INCREASED VALUE BUY AND FINANCE SCALE IN SERVICING HOMES 20PENNYMAC IS POSITIONED TO SUCCEED REGARDLESS OF FUTURE TRENDS INCREASED HOME CHANGING ROLE OF INCREASED PURCHASES DRIVING GSES / GOVERNMENT RELEVANCE OF THE ORIGINATION SUPPORT FOR THE NON-AGENCY MARKET MORTGAGE MARKET PRODUCTS CONTINUED INDUSTRY HIGHER ADVANCEMENTS IN CONSOLIDATION MORTGAGE RATES TECHNOLOGY AND AND GROWING OVER TIME AND HOW AMERICANS IMPORTANCE OF INCREASED VALUE BUY AND FINANCE SCALE IN SERVICING HOMES 20

MORTGAGE BANKING OVERVIEW DOUG JONES President and Chief Mortgage Banking OfficerMORTGAGE BANKING OVERVIEW DOUG JONES President and Chief Mortgage Banking Officer

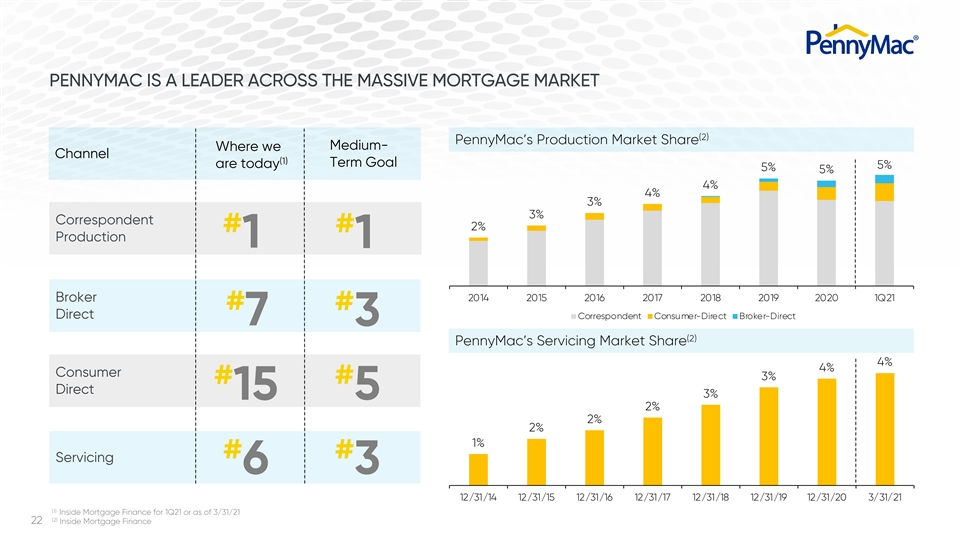

PENNYMAC IS A LEADER ACROSS THE MASSIVE MORTGAGE MARKET (2) PennyMac’s Production Market Share Medium- Where we Channel (1) Term Goal are today 5% 5% 5% 4% 4% 3% 3% Correspondent 2% # # Production 1 1 2014 2015 2016 2017 2018 2019 2020 1Q21 Broker # # Direct Correspondent Consumer-Direct Broker-Direct 7 3 (2) PennyMac’s Servicing Market Share 4% 4% Consumer 3% # # Direct 3% 15 5 2% 2% 2% 1% # # Servicing 6 3 12/31/14 12/31/15 12/31/16 12/31/17 12/31/18 12/31/19 12/31/20 3/31/21 (1) Inside Mortgage Finance for 1Q21 or as of 3/31/21 (2) 22 Inside Mortgage FinancePENNYMAC IS A LEADER ACROSS THE MASSIVE MORTGAGE MARKET (2) PennyMac’s Production Market Share Medium- Where we Channel (1) Term Goal are today 5% 5% 5% 4% 4% 3% 3% Correspondent 2% # # Production 1 1 2014 2015 2016 2017 2018 2019 2020 1Q21 Broker # # Direct Correspondent Consumer-Direct Broker-Direct 7 3 (2) PennyMac’s Servicing Market Share 4% 4% Consumer 3% # # Direct 3% 15 5 2% 2% 2% 1% # # Servicing 6 3 12/31/14 12/31/15 12/31/16 12/31/17 12/31/18 12/31/19 12/31/20 3/31/21 (1) Inside Mortgage Finance for 1Q21 or as of 3/31/21 (2) 22 Inside Mortgage Finance

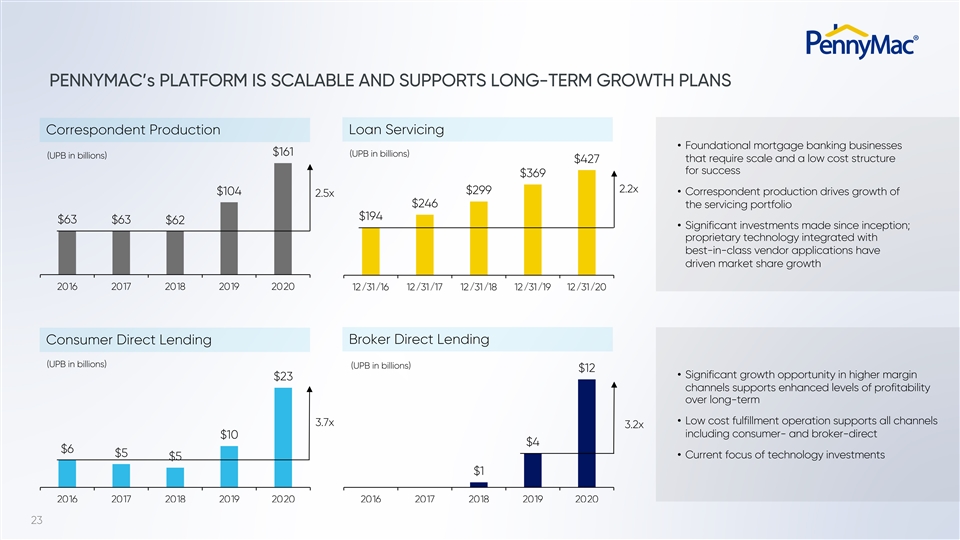

PENNYMAC’s PLATFORM IS SCALABLE AND SUPPORTS LONG-TERM GROWTH PLANS Correspondent Production Loan Servicing • Foundational mortgage banking businesses $161 (UPB in billions) (UPB in billions) that require scale and a low cost structure $427 for success $369 2.2x $299 $104 • Correspondent production drives growth of 2.5x $246 the servicing portfolio $194 $63 $63 $62 • Significant investments made since inception; proprietary technology integrated with best-in-class vendor applications have driven market share growth 2016 2017 2018 2019 2020 12/31/16 12/31/17 12/31/18 12/31/19 12/31/20 Consumer Direct Lending Broker Direct Lending (UPB in billions) (UPB in billions) $12 • Significant growth opportunity in higher margin $23 channels supports enhanced levels of profitability over long-term • Low cost fulfillment operation supports all channels 3.7x 3.2x including consumer- and broker-direct $10 $4 $6 $5 • Current focus of technology investments $5 $1 2016 2017 2018 2019 2020 2016 2017 2018 2019 2020 23PENNYMAC’s PLATFORM IS SCALABLE AND SUPPORTS LONG-TERM GROWTH PLANS Correspondent Production Loan Servicing • Foundational mortgage banking businesses $161 (UPB in billions) (UPB in billions) that require scale and a low cost structure $427 for success $369 2.2x $299 $104 • Correspondent production drives growth of 2.5x $246 the servicing portfolio $194 $63 $63 $62 • Significant investments made since inception; proprietary technology integrated with best-in-class vendor applications have driven market share growth 2016 2017 2018 2019 2020 12/31/16 12/31/17 12/31/18 12/31/19 12/31/20 Consumer Direct Lending Broker Direct Lending (UPB in billions) (UPB in billions) $12 • Significant growth opportunity in higher margin $23 channels supports enhanced levels of profitability over long-term • Low cost fulfillment operation supports all channels 3.7x 3.2x including consumer- and broker-direct $10 $4 $6 $5 • Current focus of technology investments $5 $1 2016 2017 2018 2019 2020 2016 2017 2018 2019 2020 23

PENNYMAC’s PARTICIPATION ACROSS ALL THREE ORIGINATION CHANNELS IS A STRATEGIC ADVANTAGE All three channels supported by best-in-class risk management and centralized fulfillment platforms. Correspondent Production Consumer Direct Broker Direct • Operational consistency and • Internet and call-center based • Excellence in correspondent low cost structure model enables low cost structure provides foundation for B2B success • Independent mortgage banks, • Digital marketing and branding community banks and initiatives to drive new customer • Access to a growing channel of the credit unions growth origination market that has historically performed well in • Access to the growing purchase • Sophisticated data analysis to purchase markets market via branch offices and loan drive growth in purchase and officers with local relationships portfolio recapture • Brokers have meaningful, local relationships in their communities • Drives servicing portfolio growth 24PENNYMAC’s PARTICIPATION ACROSS ALL THREE ORIGINATION CHANNELS IS A STRATEGIC ADVANTAGE All three channels supported by best-in-class risk management and centralized fulfillment platforms. Correspondent Production Consumer Direct Broker Direct • Operational consistency and • Internet and call-center based • Excellence in correspondent low cost structure model enables low cost structure provides foundation for B2B success • Independent mortgage banks, • Digital marketing and branding community banks and initiatives to drive new customer • Access to a growing channel of the credit unions growth origination market that has historically performed well in • Access to the growing purchase • Sophisticated data analysis to purchase markets market via branch offices and loan drive growth in purchase and officers with local relationships portfolio recapture • Brokers have meaningful, local relationships in their communities • Drives servicing portfolio growth 24

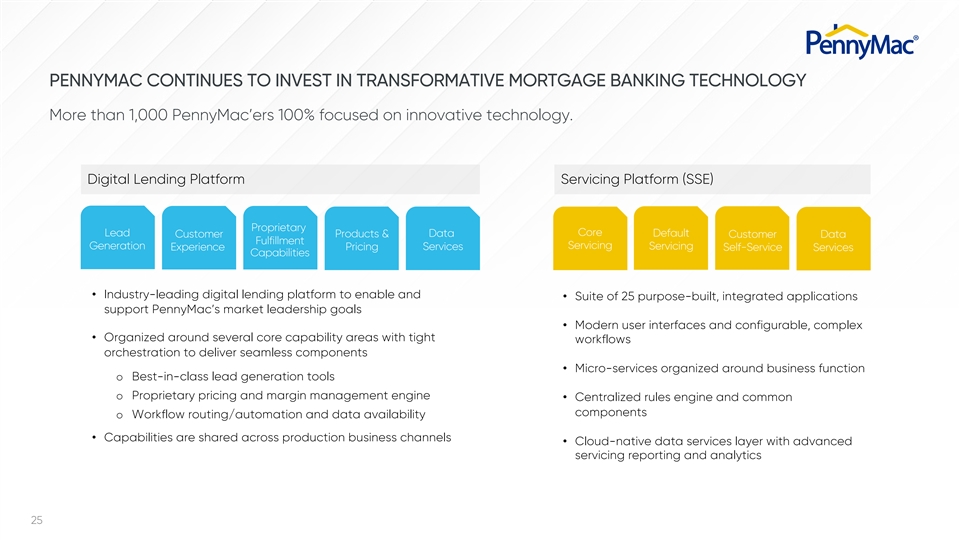

PENNYMAC CONTINUES TO INVEST IN TRANSFORMATIVE MORTGAGE BANKING TECHNOLOGY More than 1,000 PennyMac’ers 100% focused on innovative technology. Digital Lending Platform Servicing Platform (SSE) Proprietary Lead Core Products & Data Default Customer Customer Data Fulfillment Generation Servicing Pricing Services Servicing Experience Self-Service Services Capabilities • Industry-leading digital lending platform to enable and • Suite of 25 purpose-built, integrated applications support PennyMac’s market leadership goals • Modern user interfaces and configurable, complex • Organized around several core capability areas with tight workflows orchestration to deliver seamless components • Micro-services organized around business function o Best-in-class lead generation tools o Proprietary pricing and margin management engine • Centralized rules engine and common components o Workflow routing/automation and data availability • Capabilities are shared across production business channels • Cloud-native data services layer with advanced servicing reporting and analytics 25PENNYMAC CONTINUES TO INVEST IN TRANSFORMATIVE MORTGAGE BANKING TECHNOLOGY More than 1,000 PennyMac’ers 100% focused on innovative technology. Digital Lending Platform Servicing Platform (SSE) Proprietary Lead Core Products & Data Default Customer Customer Data Fulfillment Generation Servicing Pricing Services Servicing Experience Self-Service Services Capabilities • Industry-leading digital lending platform to enable and • Suite of 25 purpose-built, integrated applications support PennyMac’s market leadership goals • Modern user interfaces and configurable, complex • Organized around several core capability areas with tight workflows orchestration to deliver seamless components • Micro-services organized around business function o Best-in-class lead generation tools o Proprietary pricing and margin management engine • Centralized rules engine and common components o Workflow routing/automation and data availability • Capabilities are shared across production business channels • Cloud-native data services layer with advanced servicing reporting and analytics 25

CONSUMER DIRECT LENDING SCOTT BRIDGES Managing Director Consumer Direct LendingCONSUMER DIRECT LENDING SCOTT BRIDGES Managing Director Consumer Direct Lending

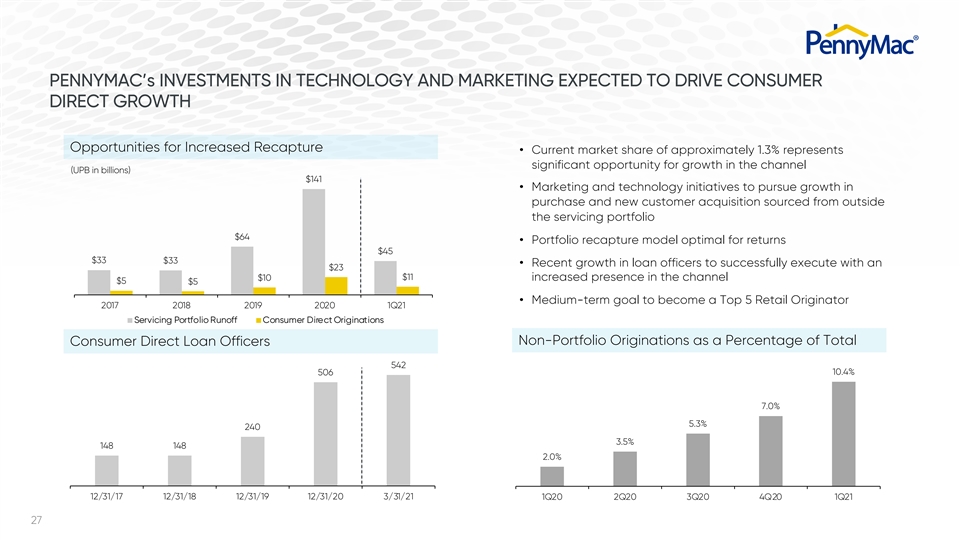

PENNYMAC’s INVESTMENTS IN TECHNOLOGY AND MARKETING EXPECTED TO DRIVE CONSUMER DIRECT GROWTH Opportunities for Increased Recapture • Current market share of approximately 1.3% represents significant opportunity for growth in the channel (UPB in billions) $141 • Marketing and technology initiatives to pursue growth in purchase and new customer acquisition sourced from outside the servicing portfolio $64 • Portfolio recapture model optimal for returns $45 $33 $33 • Recent growth in loan officers to successfully execute with an $23 $11 $10 increased presence in the channel $5 $5 • Medium-term goal to become a Top 5 Retail Originator 2017 2018 2019 2020 1Q21 Servicing Portfolio Runoff Consumer Direct Originations Non-Portfolio Originations as a Percentage of Total Consumer Direct Loan Officers 542 506 10.4% 7.0% 5.3% 240 3.5% 148 148 2.0% 12/31/17 12/31/18 12/31/19 12/31/20 3/31/21 1Q20 2Q20 3Q20 4Q20 1Q21 27PENNYMAC’s INVESTMENTS IN TECHNOLOGY AND MARKETING EXPECTED TO DRIVE CONSUMER DIRECT GROWTH Opportunities for Increased Recapture • Current market share of approximately 1.3% represents significant opportunity for growth in the channel (UPB in billions) $141 • Marketing and technology initiatives to pursue growth in purchase and new customer acquisition sourced from outside the servicing portfolio $64 • Portfolio recapture model optimal for returns $45 $33 $33 • Recent growth in loan officers to successfully execute with an $23 $11 $10 increased presence in the channel $5 $5 • Medium-term goal to become a Top 5 Retail Originator 2017 2018 2019 2020 1Q21 Servicing Portfolio Runoff Consumer Direct Originations Non-Portfolio Originations as a Percentage of Total Consumer Direct Loan Officers 542 506 10.4% 7.0% 5.3% 240 3.5% 148 148 2.0% 12/31/17 12/31/18 12/31/19 12/31/20 3/31/21 1Q20 2Q20 3Q20 4Q20 1Q21 27

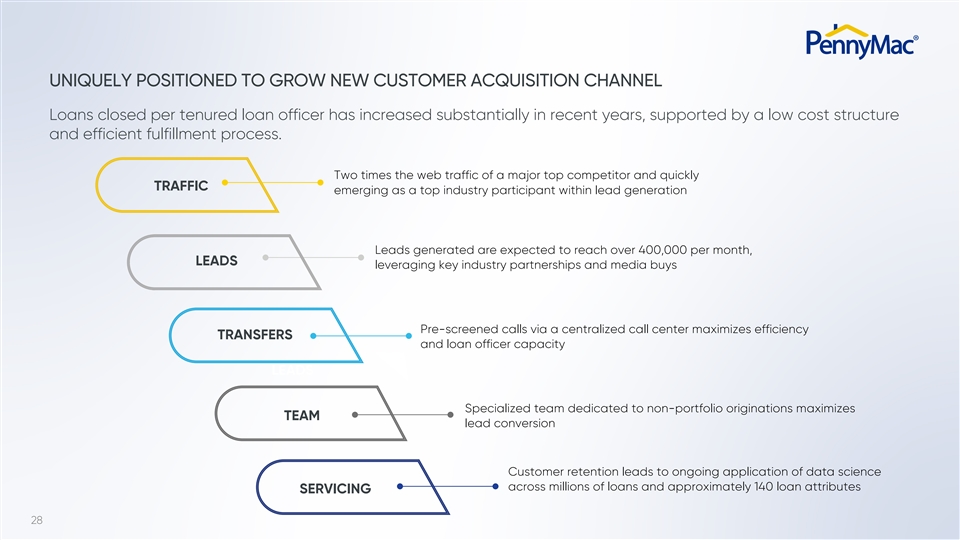

UNIQUELY POSITIONED TO GROW NEW CUSTOMER ACQUISITION CHANNEL Loans closed per tenured loan officer has increased substantially in recent years, supported by a low cost structure and efficient fulfillment process. Two times the web traffic of a major top competitor and quickly TRAFFIC emerging as a top industry participant within lead generation Leads generated are expected to reach over 400,000 per month, LEADS leveraging key industry partnerships and media buys Pre-screened calls via a centralized call center maximizes efficiency TRANSFERS and loan officer capacity LEADS Specialized team dedicated to non-portfolio originations maximizes TEAM lead conversion Customer retention leads to ongoing application of data science across millions of loans and approximately 140 loan attributes SERVICING 28UNIQUELY POSITIONED TO GROW NEW CUSTOMER ACQUISITION CHANNEL Loans closed per tenured loan officer has increased substantially in recent years, supported by a low cost structure and efficient fulfillment process. Two times the web traffic of a major top competitor and quickly TRAFFIC emerging as a top industry participant within lead generation Leads generated are expected to reach over 400,000 per month, LEADS leveraging key industry partnerships and media buys Pre-screened calls via a centralized call center maximizes efficiency TRANSFERS and loan officer capacity LEADS Specialized team dedicated to non-portfolio originations maximizes TEAM lead conversion Customer retention leads to ongoing application of data science across millions of loans and approximately 140 loan attributes SERVICING 28

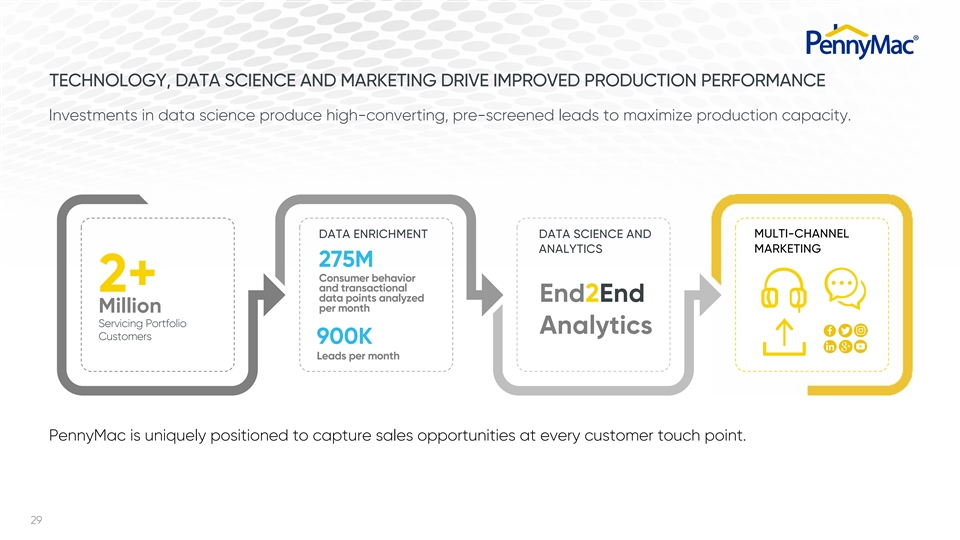

TECHNOLOGY, DATA SCIENCE AND MARKETING DRIVE IMPROVED PRODUCTION PERFORMANCE Investments in data science produce high-converting, pre-screened leads to maximize production capacity. DATA ENRICHMENT DATA SCIENCE AND MULTI-CHANNEL ANALYTICS MARKETING 275M Consumer behavior 2+ and transactional data points analyzed End2End per month Million Servicing Portfolio Analytics Customers 900K Leads per month PennyMac is uniquely positioned to capture sales opportunities at every customer touch point. 29TECHNOLOGY, DATA SCIENCE AND MARKETING DRIVE IMPROVED PRODUCTION PERFORMANCE Investments in data science produce high-converting, pre-screened leads to maximize production capacity. DATA ENRICHMENT DATA SCIENCE AND MULTI-CHANNEL ANALYTICS MARKETING 275M Consumer behavior 2+ and transactional data points analyzed End2End per month Million Servicing Portfolio Analytics Customers 900K Leads per month PennyMac is uniquely positioned to capture sales opportunities at every customer touch point. 29

DATA AND ANALYTICS DRIVE PATH TO GROWTH IN PURCHASE ORIGINATIONS • Disciplined workflow focused on growth in pre-approvals to build down stream productivity • Advanced data science payoff prediction model • Dedicated sales and operations staff for purchase loans • Operational discipline in purchase loans Advanced data Marketing to Aggressive Communication Dedicated Best-in-class analytics to consumers in pre-approval strategies to keep operations staff execution to anticipate home consideration strategy to all parties informed to ensure a ensure customers buying activity phase, far in maximize smooth close on time advance of opportunity transaction decision making 30DATA AND ANALYTICS DRIVE PATH TO GROWTH IN PURCHASE ORIGINATIONS • Disciplined workflow focused on growth in pre-approvals to build down stream productivity • Advanced data science payoff prediction model • Dedicated sales and operations staff for purchase loans • Operational discipline in purchase loans Advanced data Marketing to Aggressive Communication Dedicated Best-in-class analytics to consumers in pre-approval strategies to keep operations staff execution to anticipate home consideration strategy to all parties informed to ensure a ensure customers buying activity phase, far in maximize smooth close on time advance of opportunity transaction decision making 30

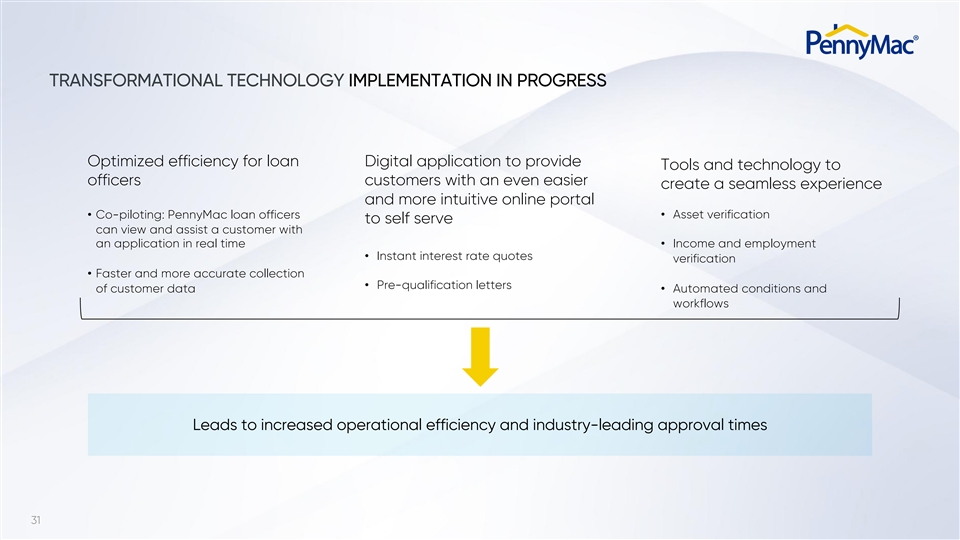

TRANSFORMATIONAL TECHNOLOGY IMPLEMENTATION IN PROGRESS Optimized efficiency for loan Digital application to provide Tools and technology to officers customers with an even easier create a seamless experience and more intuitive online portal • Asset verification • Co-piloting: PennyMac loan officers to self serve can view and assist a customer with an application in real time • Income and employment • Instant interest rate quotes verification • Faster and more accurate collection • Pre-qualification letters of customer data • Automated conditions and workflows Leads to increased operational efficiency and industry-leading approval times 31TRANSFORMATIONAL TECHNOLOGY IMPLEMENTATION IN PROGRESS Optimized efficiency for loan Digital application to provide Tools and technology to officers customers with an even easier create a seamless experience and more intuitive online portal • Asset verification • Co-piloting: PennyMac loan officers to self serve can view and assist a customer with an application in real time • Income and employment • Instant interest rate quotes verification • Faster and more accurate collection • Pre-qualification letters of customer data • Automated conditions and workflows Leads to increased operational efficiency and industry-leading approval times 31

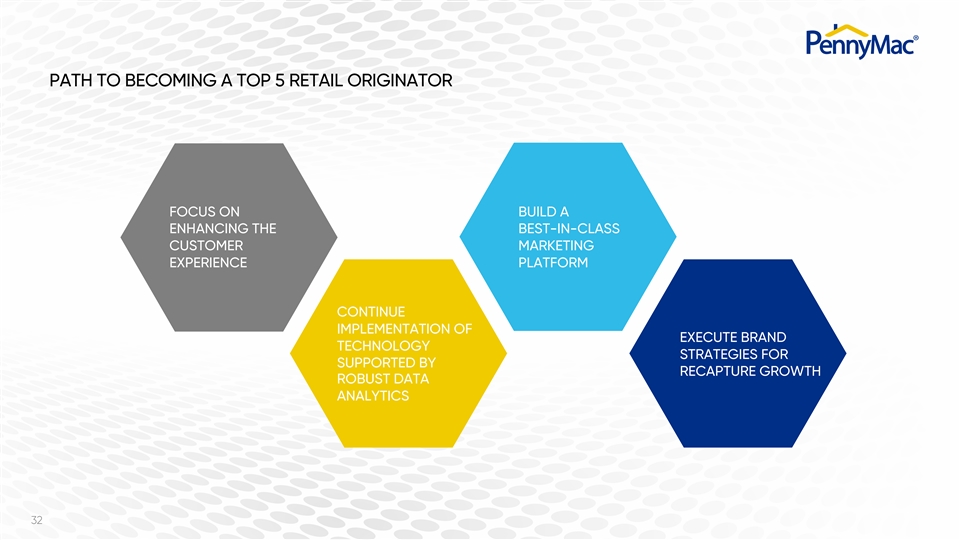

PATH TO BECOMING A TOP 5 RETAIL ORIGINATOR FOCUS ON BUILD A ENHANCING THE BEST-IN-CLASS CUSTOMER MARKETING EXPERIENCE PLATFORM CONTINUE IMPLEMENTATION OF EXECUTE BRAND TECHNOLOGY STRATEGIES FOR SUPPORTED BY RECAPTURE GROWTH ROBUST DATA ANALYTICS 32PATH TO BECOMING A TOP 5 RETAIL ORIGINATOR FOCUS ON BUILD A ENHANCING THE BEST-IN-CLASS CUSTOMER MARKETING EXPERIENCE PLATFORM CONTINUE IMPLEMENTATION OF EXECUTE BRAND TECHNOLOGY STRATEGIES FOR SUPPORTED BY RECAPTURE GROWTH ROBUST DATA ANALYTICS 32

BROKER DIRECT LENDING KIM NICHOLS Senior Managing Director Broker Direct LendingBROKER DIRECT LENDING KIM NICHOLS Senior Managing Director Broker Direct Lending

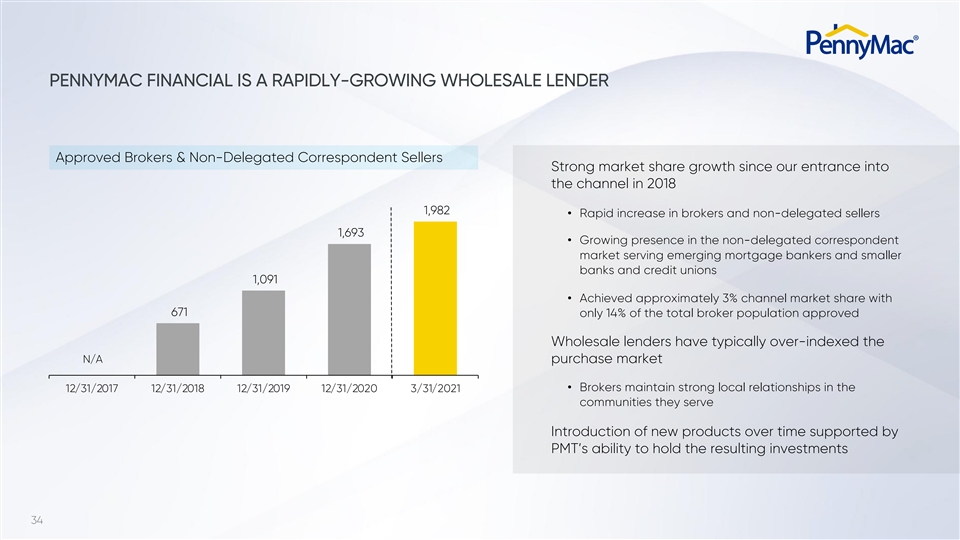

PENNYMAC FINANCIAL IS A RAPIDLY-GROWING WHOLESALE LENDER Approved Brokers & Non-Delegated Correspondent Sellers Strong market share growth since our entrance into the channel in 2018 1,982 • Rapid increase in brokers and non-delegated sellers 1,693 • Growing presence in the non-delegated correspondent market serving emerging mortgage bankers and smaller banks and credit unions 1,091 • Achieved approximately 3% channel market share with 671 only 14% of the total broker population approved Wholesale lenders have typically over-indexed the N/A purchase market • Brokers maintain strong local relationships in the 12/31/2017 12/31/2018 12/31/2019 12/31/2020 3/31/2021 communities they serve Introduction of new products over time supported by PMT’s ability to hold the resulting investments 34PENNYMAC FINANCIAL IS A RAPIDLY-GROWING WHOLESALE LENDER Approved Brokers & Non-Delegated Correspondent Sellers Strong market share growth since our entrance into the channel in 2018 1,982 • Rapid increase in brokers and non-delegated sellers 1,693 • Growing presence in the non-delegated correspondent market serving emerging mortgage bankers and smaller banks and credit unions 1,091 • Achieved approximately 3% channel market share with 671 only 14% of the total broker population approved Wholesale lenders have typically over-indexed the N/A purchase market • Brokers maintain strong local relationships in the 12/31/2017 12/31/2018 12/31/2019 12/31/2020 3/31/2021 communities they serve Introduction of new products over time supported by PMT’s ability to hold the resulting investments 34

PROPRIETARY TECHNOLOGY AND TOOLS DISTINGUISH PENNYMAC • Perfect Rate: Uses PennyMac’s industry- • PennyMac’s POWER portal provides leading, proprietary pricing engine to fine brokers with full transparency and access 146 months tune the interest rate to the thousandth for to their pipelines and loan data to customers 2.124% transact around the clock 287 months • Perfect Term: Provides brokers with • Extends best-in-class tools and solutions capabilities to get the perfect term for to brokers with ease of use via a single, their clients’ situation to the exact month digital platform • A POWERful tool that searches through all • Because we retain the servicing on 100% of the loans we originate, customers have our negotiated provider options to extract the best possible mortgage insurance rate a seamless loan lifecycle experience, from for each loan start to finish • PennyMac’s reduced mortgage insurance • Every broker we approve is assigned their rates are among the most competitive in own experienced PennyMac Broker the industry and provide a competitive Operations Manager (BOM) to serve as a advantage for brokers dedicated point of contact, assuring loans stay on track and on time 35 3.088% 312 monthsPROPRIETARY TECHNOLOGY AND TOOLS DISTINGUISH PENNYMAC • Perfect Rate: Uses PennyMac’s industry- • PennyMac’s POWER portal provides leading, proprietary pricing engine to fine brokers with full transparency and access 146 months tune the interest rate to the thousandth for to their pipelines and loan data to customers 2.124% transact around the clock 287 months • Perfect Term: Provides brokers with • Extends best-in-class tools and solutions capabilities to get the perfect term for to brokers with ease of use via a single, their clients’ situation to the exact month digital platform • A POWERful tool that searches through all • Because we retain the servicing on 100% of the loans we originate, customers have our negotiated provider options to extract the best possible mortgage insurance rate a seamless loan lifecycle experience, from for each loan start to finish • PennyMac’s reduced mortgage insurance • Every broker we approve is assigned their rates are among the most competitive in own experienced PennyMac Broker the industry and provide a competitive Operations Manager (BOM) to serve as a advantage for brokers dedicated point of contact, assuring loans stay on track and on time 35 3.088% 312 months

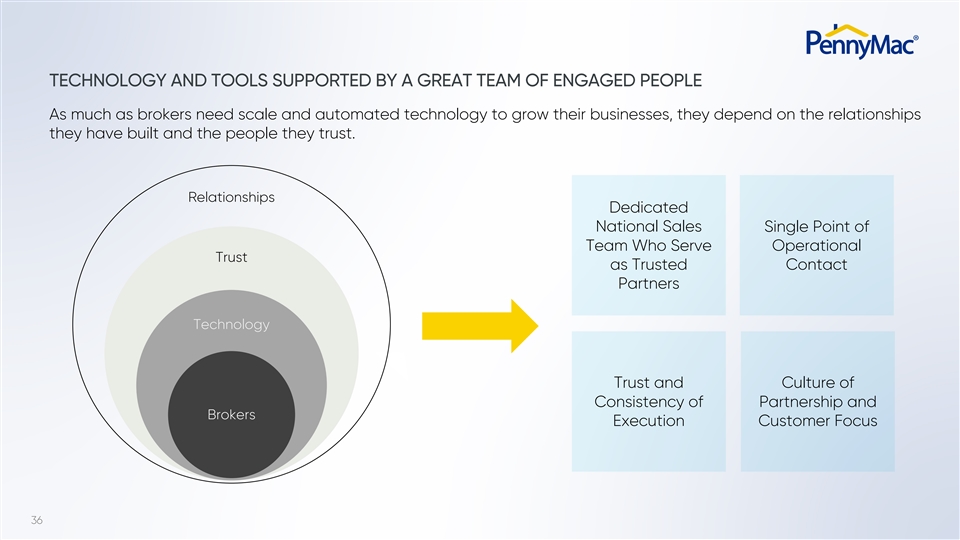

TECHNOLOGY AND TOOLS SUPPORTED BY A GREAT TEAM OF ENGAGED PEOPLE As much as brokers need scale and automated technology to grow their businesses, they depend on the relationships they have built and the people they trust. Relationships Dedicated National Sales Single Point of Team Who Serve Operational Trust as Trusted Contact Partners Technology Trust and Culture of Consistency of Partnership and Brokers Execution Customer Focus 36TECHNOLOGY AND TOOLS SUPPORTED BY A GREAT TEAM OF ENGAGED PEOPLE As much as brokers need scale and automated technology to grow their businesses, they depend on the relationships they have built and the people they trust. Relationships Dedicated National Sales Single Point of Team Who Serve Operational Trust as Trusted Contact Partners Technology Trust and Culture of Consistency of Partnership and Brokers Execution Customer Focus 36

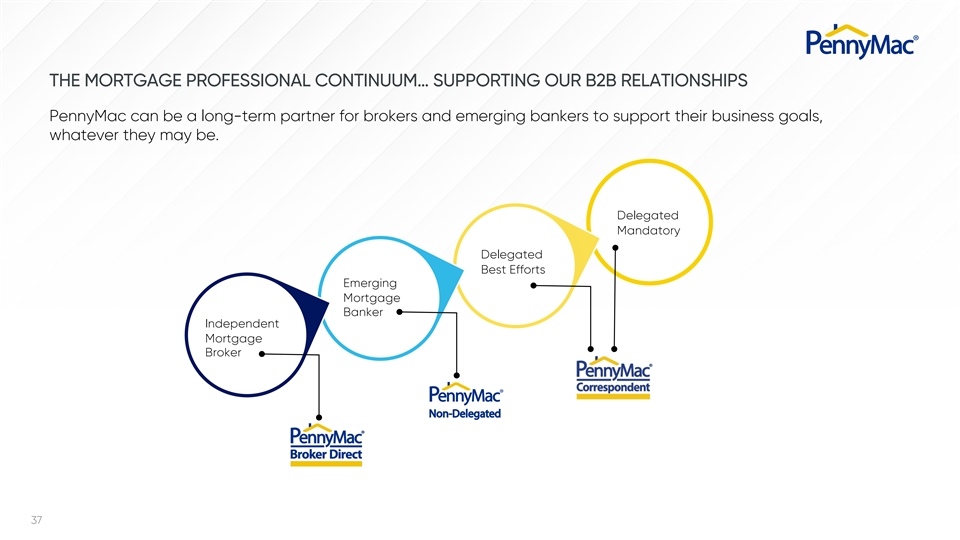

THE MORTGAGE PROFESSIONAL CONTINUUM… SUPPORTING OUR B2B RELATIONSHIPS PennyMac can be a long-term partner for brokers and emerging bankers to support their business goals, whatever they may be. Delegated Mandatory Delegated Best Efforts Emerging Mortgage Banker Independent Mortgage Broker Non-Delegated 37THE MORTGAGE PROFESSIONAL CONTINUUM… SUPPORTING OUR B2B RELATIONSHIPS PennyMac can be a long-term partner for brokers and emerging bankers to support their business goals, whatever they may be. Delegated Mandatory Delegated Best Efforts Emerging Mortgage Banker Independent Mortgage Broker Non-Delegated 37

PATH TO BECOMING A TOP 3 WHOLESALE ORIGINATOR GROW OUR BASE FOCUS ON OF BROKERS AND THE CLIENT NON-DELEGATED EXPERIENCE AND SELLERS RELATIONSHIPS CONTINUE EXPAND INVESTMENT IN NON-DELEGATED TECHNOLOGY TO SERVICE OFFERING HELP BUSINESS PARTNERS GROW 38PATH TO BECOMING A TOP 3 WHOLESALE ORIGINATOR GROW OUR BASE FOCUS ON OF BROKERS AND THE CLIENT NON-DELEGATED EXPERIENCE AND SELLERS RELATIONSHIPS CONTINUE EXPAND INVESTMENT IN NON-DELEGATED TECHNOLOGY TO SERVICE OFFERING HELP BUSINESS PARTNERS GROW 38

CORRESPONDENT PRODUCTION ABBIE TIDMORE Senior Managing Director Correspondent ProductionCORRESPONDENT PRODUCTION ABBIE TIDMORE Senior Managing Director Correspondent Production

PENNYMAC IS THE LEADER IN CORRESPONDENT PRODUCTION PennyMac has become the largest correspondent aggregator in the U.S. with a transparent business model well-aligned with customer and shareholder desires. 700+ 10+ Active clients across Years of operational Innovative the U.S. excellence technology • Community banks and • Consistent execution • Seamless integration credit unions with proprietary loan • Relationship-based bidding systems • Well-established, model independent mortgage • Process consistency • Strong capital base originators and efficiency • Unmatched • Builder-owned commitment mortgage companies 40PENNYMAC IS THE LEADER IN CORRESPONDENT PRODUCTION PennyMac has become the largest correspondent aggregator in the U.S. with a transparent business model well-aligned with customer and shareholder desires. 700+ 10+ Active clients across Years of operational Innovative the U.S. excellence technology • Community banks and • Consistent execution • Seamless integration credit unions with proprietary loan • Relationship-based bidding systems • Well-established, model independent mortgage • Process consistency • Strong capital base originators and efficiency • Unmatched • Builder-owned commitment mortgage companies 40

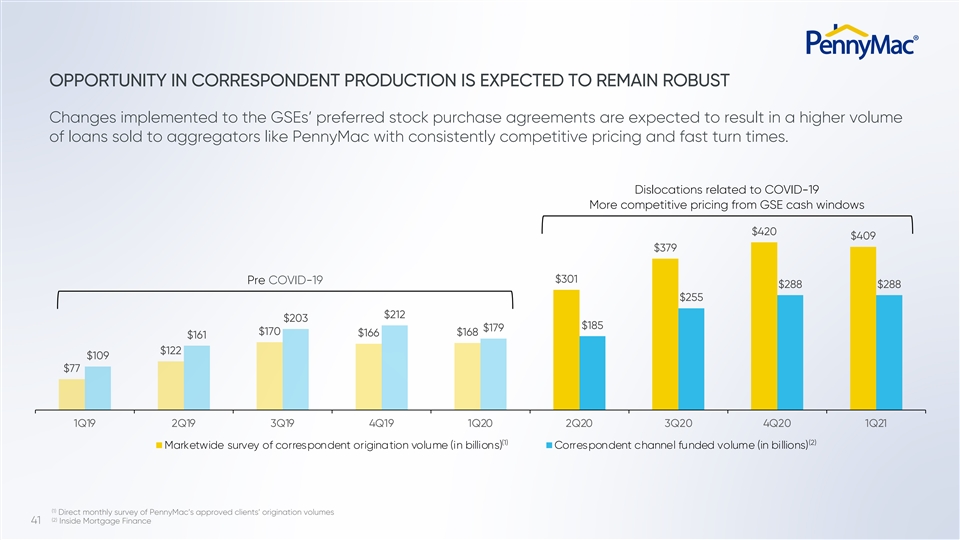

OPPORTUNITY IN CORRESPONDENT PRODUCTION IS EXPECTED TO REMAIN ROBUST Changes implemented to the GSEs’ preferred stock purchase agreements are expected to result in a higher volume of loans sold to aggregators like PennyMac with consistently competitive pricing and fast turn times. Dislocations related to COVID-19 More competitive pricing from GSE cash windows $420 $409 $379 $301 Pre COVID-19 $288 $288 $255 $212 $203 $185 $179 $170 $168 $166 $161 $122 $109 $77 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 (1) (2) Marketwide survey of correspondent origination volume (in billions) Correspondent channel funded volume (in billions) (1) Direct monthly survey of PennyMac’s approved clients’ origination volumes (2) 41 Inside Mortgage FinanceOPPORTUNITY IN CORRESPONDENT PRODUCTION IS EXPECTED TO REMAIN ROBUST Changes implemented to the GSEs’ preferred stock purchase agreements are expected to result in a higher volume of loans sold to aggregators like PennyMac with consistently competitive pricing and fast turn times. Dislocations related to COVID-19 More competitive pricing from GSE cash windows $420 $409 $379 $301 Pre COVID-19 $288 $288 $255 $212 $203 $185 $179 $170 $168 $166 $161 $122 $109 $77 1Q19 2Q19 3Q19 4Q19 1Q20 2Q20 3Q20 4Q20 1Q21 (1) (2) Marketwide survey of correspondent origination volume (in billions) Correspondent channel funded volume (in billions) (1) Direct monthly survey of PennyMac’s approved clients’ origination volumes (2) 41 Inside Mortgage Finance

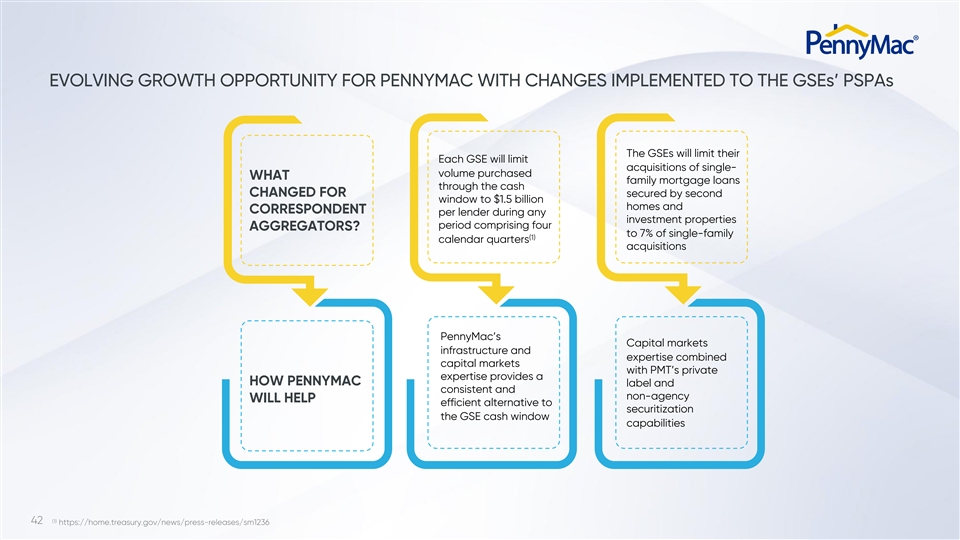

EVOLVING GROWTH OPPORTUNITY FOR PENNYMAC WITH CHANGES IMPLEMENTED TO THE GSEs’ PSPAs The GSEs will limit their Each GSE will limit acquisitions of single- volume purchased WHAT family mortgage loans through the cash CHANGED FOR secured by second window to $1.5 billion homes and CORRESPONDENT per lender during any investment properties period comprising four AGGREGATORS? to 7% of single-family (1) calendar quarters acquisitions PennyMac’s Capital markets infrastructure and expertise combined capital markets with PMT’s private expertise provides a HOW PENNYMAC label and consistent and non-agency WILL HELP efficient alternative to securitization the GSE cash window capabilities (1) 42 https://home.treasury.gov/news/press-releases/sm1236EVOLVING GROWTH OPPORTUNITY FOR PENNYMAC WITH CHANGES IMPLEMENTED TO THE GSEs’ PSPAs The GSEs will limit their Each GSE will limit acquisitions of single- volume purchased WHAT family mortgage loans through the cash CHANGED FOR secured by second window to $1.5 billion homes and CORRESPONDENT per lender during any investment properties period comprising four AGGREGATORS? to 7% of single-family (1) calendar quarters acquisitions PennyMac’s Capital markets infrastructure and expertise combined capital markets with PMT’s private expertise provides a HOW PENNYMAC label and consistent and non-agency WILL HELP efficient alternative to securitization the GSE cash window capabilities (1) 42 https://home.treasury.gov/news/press-releases/sm1236

SUSTAINING PENNYMAC’S LEADERSHIP POSITION IN CORRESPONDENT PRODUCTION EXPAND THE CONTINUE TO INCREASE ALREADY ROBUST SUITE OF PRODUCTS SHARE OF EXISTING AND SERVICES CLIENT PRODUCTION OFFERED PROVIDE INNOVATIVE CONTINUE TO SOLUTIONS FOR DELIVER AN UNMATCHED CORRESPONDENTS CUSTOMER EXPERIENCE CURRENTLY DELIVERING WITH CONSISTENTLY TO THE GSE CASH COMPETITIVE BIDS WINDOW AND FAST TURNS TIMES 43SUSTAINING PENNYMAC’S LEADERSHIP POSITION IN CORRESPONDENT PRODUCTION EXPAND THE CONTINUE TO INCREASE ALREADY ROBUST SUITE OF PRODUCTS SHARE OF EXISTING AND SERVICES CLIENT PRODUCTION OFFERED PROVIDE INNOVATIVE CONTINUE TO SOLUTIONS FOR DELIVER AN UNMATCHED CORRESPONDENTS CUSTOMER EXPERIENCE CURRENTLY DELIVERING WITH CONSISTENTLY TO THE GSE CASH COMPETITIVE BIDS WINDOW AND FAST TURNS TIMES 43

MORTGAGE FULFILLMENT JIM FOLLETTE Senior Managing Director Chief Mortgage Fulfillment OfficerMORTGAGE FULFILLMENT JIM FOLLETTE Senior Managing Director Chief Mortgage Fulfillment Officer

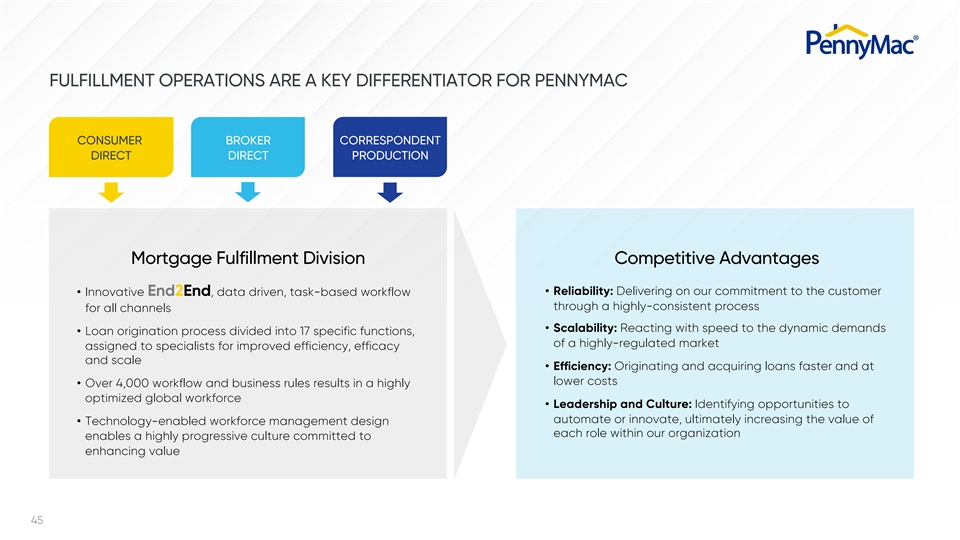

FULFILLMENT OPERATIONS ARE A KEY DIFFERENTIATOR FOR PENNYMAC CONSUMER BROKER CORRESPONDENT DIRECT DIRECT PRODUCTION Mortgage Fulfillment Division Competitive Advantages • Reliability: Delivering on our commitment to the customer • Innovative End2End, data driven, task-based workflow through a highly-consistent process for all channels • Scalability: Reacting with speed to the dynamic demands • Loan origination process divided into 17 specific functions, of a highly-regulated market assigned to specialists for improved efficiency, efficacy and scale • Efficiency: Originating and acquiring loans faster and at lower costs • Over 4,000 workflow and business rules results in a highly optimized global workforce • Leadership and Culture: Identifying opportunities to automate or innovate, ultimately increasing the value of • Technology-enabled workforce management design each role within our organization enables a highly progressive culture committed to enhancing value 45FULFILLMENT OPERATIONS ARE A KEY DIFFERENTIATOR FOR PENNYMAC CONSUMER BROKER CORRESPONDENT DIRECT DIRECT PRODUCTION Mortgage Fulfillment Division Competitive Advantages • Reliability: Delivering on our commitment to the customer • Innovative End2End, data driven, task-based workflow through a highly-consistent process for all channels • Scalability: Reacting with speed to the dynamic demands • Loan origination process divided into 17 specific functions, of a highly-regulated market assigned to specialists for improved efficiency, efficacy and scale • Efficiency: Originating and acquiring loans faster and at lower costs • Over 4,000 workflow and business rules results in a highly optimized global workforce • Leadership and Culture: Identifying opportunities to automate or innovate, ultimately increasing the value of • Technology-enabled workforce management design each role within our organization enables a highly progressive culture committed to enhancing value 45

SUPPORTING PENNYMAC’s PRODUCTION GOALS FOR THE LONG TERM SUPPORT THE LEVERAGE VAST DATA PLANNED GROWTH OF SETS TO FURTHER ALL THREE PRODUCTION ENHANCE CHANNELS WITH A WORKFLOWS AND SCALABLE AND EFFICIENT PROCESSES FULFILLMENT PROCESS DEVELOP TECHNOLOGY WITH A COMMITMENT CONTINUE TO AND FOCUS ON FOCUS ON SOLVING OMNI-CHANNEL FOR THE CUSTOMER SOLUTIONS 46SUPPORTING PENNYMAC’s PRODUCTION GOALS FOR THE LONG TERM SUPPORT THE LEVERAGE VAST DATA PLANNED GROWTH OF SETS TO FURTHER ALL THREE PRODUCTION ENHANCE CHANNELS WITH A WORKFLOWS AND SCALABLE AND EFFICIENT PROCESSES FULFILLMENT PROCESS DEVELOP TECHNOLOGY WITH A COMMITMENT CONTINUE TO AND FOCUS ON FOCUS ON SOLVING OMNI-CHANNEL FOR THE CUSTOMER SOLUTIONS 46

LOAN SERVICING STEVE BAILEY Senior Managing Director Chief Servicing OfficerLOAN SERVICING STEVE BAILEY Senior Managing Director Chief Servicing Officer

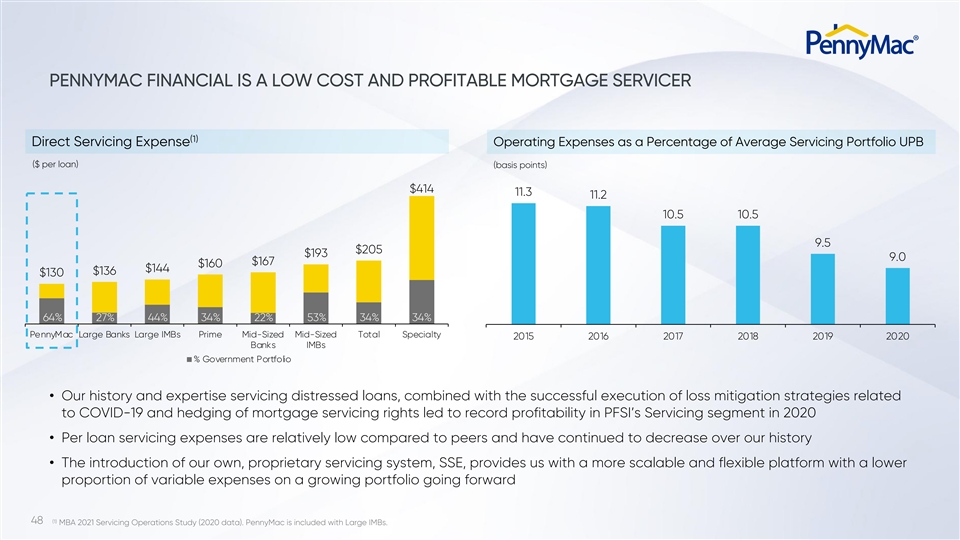

PENNYMAC FINANCIAL IS A LOW COST AND PROFITABLE MORTGAGE SERVICER (1) Direct Servicing Expense Operating Expenses as a Percentage of Average Servicing Portfolio UPB ($ per loan) (basis points) $414 11.3 11.2 10.5 10.5 9.5 $205 $193 9.0 $167 $160 $144 $136 $130 64% 27% 44% 34% 22% 53% 34% 34% PennyMac Large Banks Large IMBs Prime Mid-Sized Mid-Sized Total Specialty 2015 2016 2017 2018 2019 2020 Banks IMBs % Government Portfolio • Our history and expertise servicing distressed loans, combined with the successful execution of loss mitigation strategies related to COVID-19 and hedging of mortgage servicing rights led to record profitability in PFSI’s Servicing segment in 2020 • Per loan servicing expenses are relatively low compared to peers and have continued to decrease over our history • The introduction of our own, proprietary servicing system, SSE, provides us with a more scalable and flexible platform with a lower proportion of variable expenses on a growing portfolio going forward (1) 48 MBA 2021 Servicing Operations Study (2020 data). PennyMac is included with Large IMBs.PENNYMAC FINANCIAL IS A LOW COST AND PROFITABLE MORTGAGE SERVICER (1) Direct Servicing Expense Operating Expenses as a Percentage of Average Servicing Portfolio UPB ($ per loan) (basis points) $414 11.3 11.2 10.5 10.5 9.5 $205 $193 9.0 $167 $160 $144 $136 $130 64% 27% 44% 34% 22% 53% 34% 34% PennyMac Large Banks Large IMBs Prime Mid-Sized Mid-Sized Total Specialty 2015 2016 2017 2018 2019 2020 Banks IMBs % Government Portfolio • Our history and expertise servicing distressed loans, combined with the successful execution of loss mitigation strategies related to COVID-19 and hedging of mortgage servicing rights led to record profitability in PFSI’s Servicing segment in 2020 • Per loan servicing expenses are relatively low compared to peers and have continued to decrease over our history • The introduction of our own, proprietary servicing system, SSE, provides us with a more scalable and flexible platform with a lower proportion of variable expenses on a growing portfolio going forward (1) 48 MBA 2021 Servicing Operations Study (2020 data). PennyMac is included with Large IMBs.

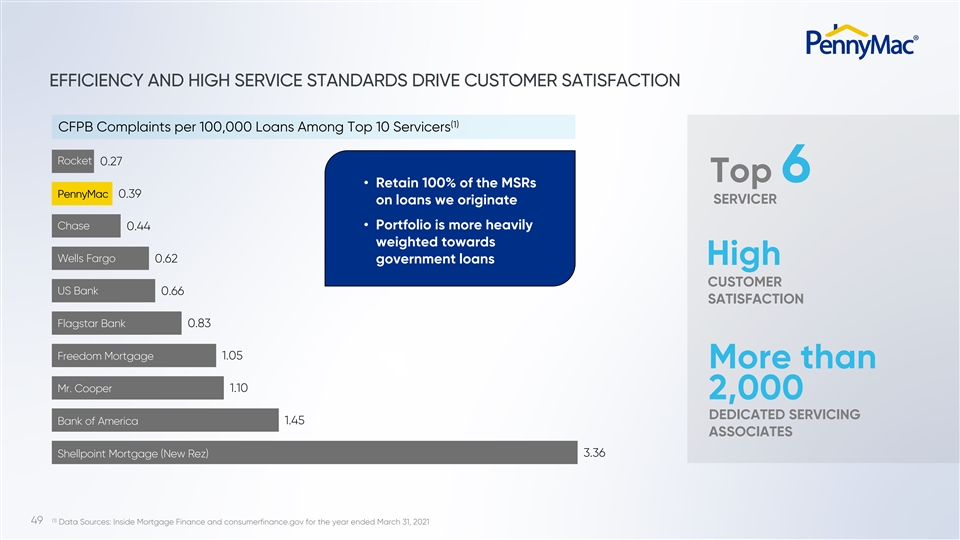

EFFICIENCY AND HIGH SERVICE STANDARDS DRIVE CUSTOMER SATISFACTION (1) CFPB Complaints per 100,000 Loans Among Top 10 Servicers Rocket 0.27 Top6 • Retain 100% of the MSRs PennyMac 0.39 on loans we originate SERVICER Chase • Portfolio is more heavily 0.44 weighted towards Wells Fargo 0.62 government loans High CUSTOMER US Bank 0.66 SATISFACTION Flagstar Bank 0.83 Freedom Mortgage 1.05 More than Mr. Cooper 1.10 2,000 DEDICATED SERVICING 1.45 Bank of America ASSOCIATES Shellpoint Mortgage (New Rez) 3.36 (1) 49 Data Sources: Inside Mortgage Finance and consumerfinance.gov for the year ended March 31, 2021EFFICIENCY AND HIGH SERVICE STANDARDS DRIVE CUSTOMER SATISFACTION (1) CFPB Complaints per 100,000 Loans Among Top 10 Servicers Rocket 0.27 Top6 • Retain 100% of the MSRs PennyMac 0.39 on loans we originate SERVICER Chase • Portfolio is more heavily 0.44 weighted towards Wells Fargo 0.62 government loans High CUSTOMER US Bank 0.66 SATISFACTION Flagstar Bank 0.83 Freedom Mortgage 1.05 More than Mr. Cooper 1.10 2,000 DEDICATED SERVICING 1.45 Bank of America ASSOCIATES Shellpoint Mortgage (New Rez) 3.36 (1) 49 Data Sources: Inside Mortgage Finance and consumerfinance.gov for the year ended March 31, 2021

PROPRIETARY SERVICING PLATFORM (SSE) DRIVES COMPETITIVE ADVANTAGE SSE is a suite of proprietary PennyMac applications and processes integrated with key partners’ applications and PennyMac’s data warehouse for increased efficiency in servicing, tracking and reporting. PRIME SERVICING Loan administration & boarding Fees & disbursements SPECIAL SERVICING Investor reporting Loss mitigation Escrow management Modifications Document & correspondence Default reporting management Claims DATA AND CUSTOMER FACING VENDOR SOFTWARE ANALYTICS Call IVR Web Mobile Center App 50PROPRIETARY SERVICING PLATFORM (SSE) DRIVES COMPETITIVE ADVANTAGE SSE is a suite of proprietary PennyMac applications and processes integrated with key partners’ applications and PennyMac’s data warehouse for increased efficiency in servicing, tracking and reporting. PRIME SERVICING Loan administration & boarding Fees & disbursements SPECIAL SERVICING Investor reporting Loss mitigation Escrow management Modifications Document & correspondence Default reporting management Claims DATA AND CUSTOMER FACING VENDOR SOFTWARE ANALYTICS Call IVR Web Mobile Center App 50

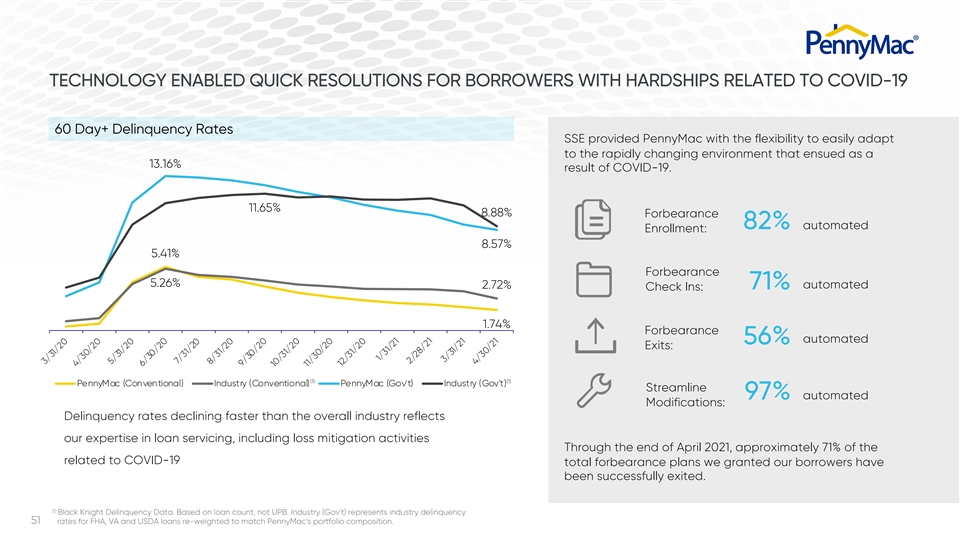

TECHNOLOGY ENABLED QUICK RESOLUTIONS FOR BORROWERS WITH HARDSHIPS RELATED TO COVID-19 60 Day+ Delinquency Rates SSE provided PennyMac with the flexibility to easily adapt to the rapidly changing environment that ensued as a 13.16% result of COVID-19. 11.65% 8.88% Forbearance 82% automated Enrollment: 8.57% 5.41% Forbearance 5.26% 2.72% 71% automated Check Ins: 1.74% Forbearance automated 56% Exits: (1) (1) PennyMac (Conventional) Industry (Conventional) PennyMac (Gov't) Industry (Gov't) Streamline automated 97% Modifications: Delinquency rates declining faster than the overall industry reflects our expertise in loan servicing, including loss mitigation activities Through the end of April 2021, approximately 71% of the related to COVID-19 total forbearance plans we granted our borrowers have been successfully exited. (1) Black Knight Delinquency Data. Based on loan count, not UPB. Industry (Gov't) represents industry delinquency 51 rates for FHA, VA and USDA loans re-weighted to match PennyMac's portfolio composition. 3/31/20 4/30/20 5/31/20 6/30/20 7/31/20 8/31/20 9/30/20 10/31/20 11/30/20 12/31/20 1/31/21 2/28/21 3/31/21 4/30/21TECHNOLOGY ENABLED QUICK RESOLUTIONS FOR BORROWERS WITH HARDSHIPS RELATED TO COVID-19 60 Day+ Delinquency Rates SSE provided PennyMac with the flexibility to easily adapt to the rapidly changing environment that ensued as a 13.16% result of COVID-19. 11.65% 8.88% Forbearance 82% automated Enrollment: 8.57% 5.41% Forbearance 5.26% 2.72% 71% automated Check Ins: 1.74% Forbearance automated 56% Exits: (1) (1) PennyMac (Conventional) Industry (Conventional) PennyMac (Gov't) Industry (Gov't) Streamline automated 97% Modifications: Delinquency rates declining faster than the overall industry reflects our expertise in loan servicing, including loss mitigation activities Through the end of April 2021, approximately 71% of the related to COVID-19 total forbearance plans we granted our borrowers have been successfully exited. (1) Black Knight Delinquency Data. Based on loan count, not UPB. Industry (Gov't) represents industry delinquency 51 rates for FHA, VA and USDA loans re-weighted to match PennyMac's portfolio composition. 3/31/20 4/30/20 5/31/20 6/30/20 7/31/20 8/31/20 9/30/20 10/31/20 11/30/20 12/31/20 1/31/21 2/28/21 3/31/21 4/30/21

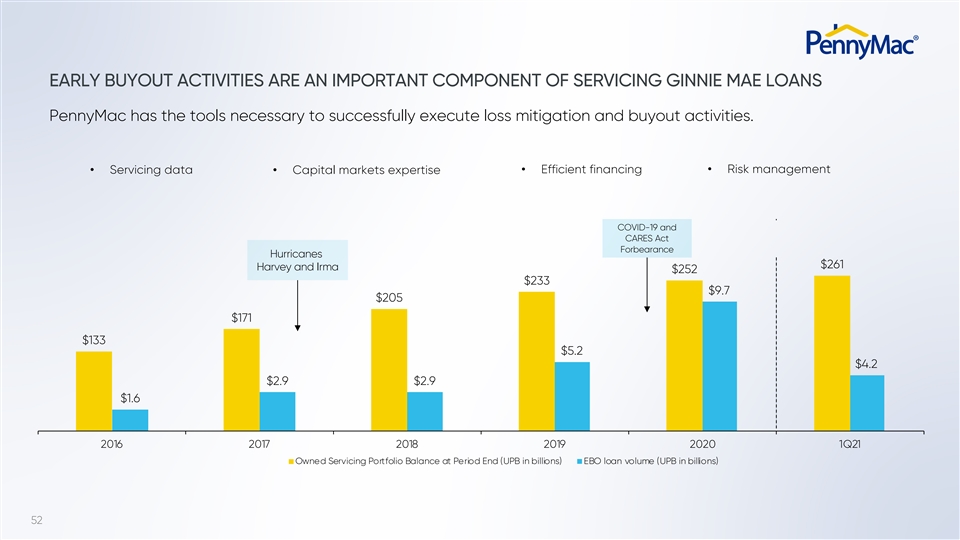

EARLY BUYOUT ACTIVITIES ARE AN IMPORTANT COMPONENT OF SERVICING GINNIE MAE LOANS PennyMac has the tools necessary to successfully execute loss mitigation and buyout activities. • Efficient financing • Risk management • Servicing data • Capital markets expertise COVID-19 and CARES Act Forbearance Hurricanes $261 Harvey and Irma $252 $233 $9.7 $205 $171 $133 $5.2 $4.2 $2.9 $2.9 $1.6 2016 2017 2018 2019 2020 1Q21 Owned Servicing Portfolio Balance at Period End (UPB in billions) EBO loan volume (UPB in billions) 52EARLY BUYOUT ACTIVITIES ARE AN IMPORTANT COMPONENT OF SERVICING GINNIE MAE LOANS PennyMac has the tools necessary to successfully execute loss mitigation and buyout activities. • Efficient financing • Risk management • Servicing data • Capital markets expertise COVID-19 and CARES Act Forbearance Hurricanes $261 Harvey and Irma $252 $233 $9.7 $205 $171 $133 $5.2 $4.2 $2.9 $2.9 $1.6 2016 2017 2018 2019 2020 1Q21 Owned Servicing Portfolio Balance at Period End (UPB in billions) EBO loan volume (UPB in billions) 52

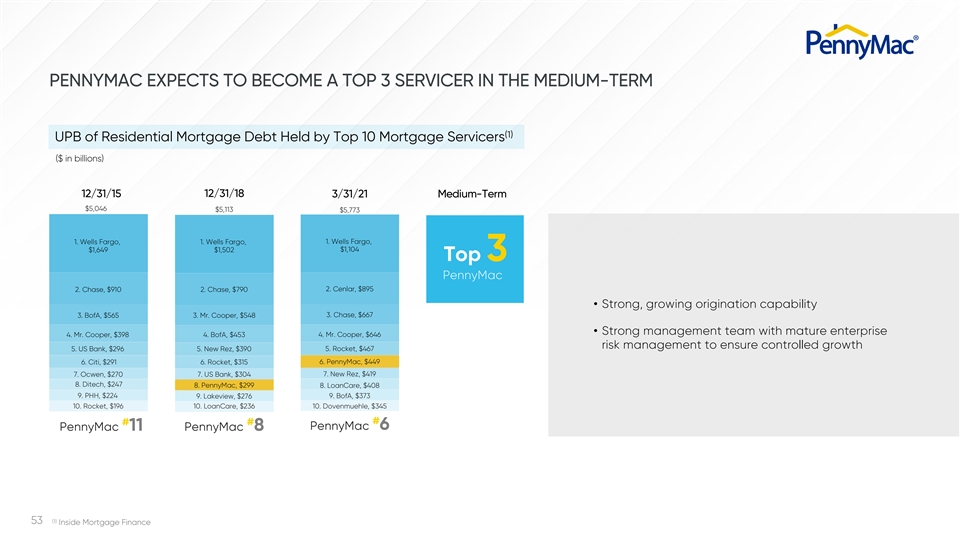

PENNYMAC EXPECTS TO BECOME A TOP 3 SERVICER IN THE MEDIUM-TERM (1) UPB of Residential Mortgage Debt Held by Top 10 Mortgage Servicers ($ in billions) 12/31/15 12/31/18 3/31/21 Medium-Term $5,046 $5,113 $5,773 1. Wells Fargo, 1. Wells Fargo, 1. Wells Fargo, $1,649 $1,502 $1,104 Top3 PennyMac 2. Cenlar, $895 2. Chase, $910 2. Chase, $790 • Strong, growing origination capability 3. Chase, $667 3. BofA, $565 3. Mr. Cooper, $548 • Strong management team with mature enterprise 4. Mr. Cooper, $398 4. BofA, $453 4. Mr. Cooper, $646 risk management to ensure controlled growth 5. US Bank, $296 5. New Rez, $390 5. Rocket, $467 6. PennyMac, $449 6. Citi, $291 6. Rocket, $315 7. New Rez, $419 7. Ocwen, $270 7. US Bank, $304 8. Ditech, $247 8. PennyMac, $299 8. LoanCare, $408 9. PHH, $224 9. BofA, $373 9. Lakeview, $276 10. Rocket, $196 10. LoanCare, $236 10. Dovenmuehle, $345 # # # PennyMac 6 PennyMac 11 PennyMac 8 (1) 53 Inside Mortgage FinancePENNYMAC EXPECTS TO BECOME A TOP 3 SERVICER IN THE MEDIUM-TERM (1) UPB of Residential Mortgage Debt Held by Top 10 Mortgage Servicers ($ in billions) 12/31/15 12/31/18 3/31/21 Medium-Term $5,046 $5,113 $5,773 1. Wells Fargo, 1. Wells Fargo, 1. Wells Fargo, $1,649 $1,502 $1,104 Top3 PennyMac 2. Cenlar, $895 2. Chase, $910 2. Chase, $790 • Strong, growing origination capability 3. Chase, $667 3. BofA, $565 3. Mr. Cooper, $548 • Strong management team with mature enterprise 4. Mr. Cooper, $398 4. BofA, $453 4. Mr. Cooper, $646 risk management to ensure controlled growth 5. US Bank, $296 5. New Rez, $390 5. Rocket, $467 6. PennyMac, $449 6. Citi, $291 6. Rocket, $315 7. New Rez, $419 7. Ocwen, $270 7. US Bank, $304 8. Ditech, $247 8. PennyMac, $299 8. LoanCare, $408 9. PHH, $224 9. BofA, $373 9. Lakeview, $276 10. Rocket, $196 10. LoanCare, $236 10. Dovenmuehle, $345 # # # PennyMac 6 PennyMac 11 PennyMac 8 (1) 53 Inside Mortgage Finance

LARGE SERVICING BUSINESS IS A KEY COMPONENT OF PENNYMAC’S BALANCED BUSINESS MODEL HIGH-QUALITY SUCCESSFUL EXECUTION SERVICING PORTFOLIO OF LOSS MITIGATION REPRESENTS A GROWING ACTIVITIES KEEPS STREAM OF RECURRING BORROWERS IN THEIR EARNINGS AND HOMES AND ENHANCES CASH FLOW LIFETIME RELATIONSHIPS DRIVER OF LOW- SERVES AS A NATURAL COST, HIGH-QUALITY HEDGE TO PRODUCTION LEADS FOR OUR CONSUMER-DIRECT INCOME AS RATES RISE LENDING BUSINESS 54LARGE SERVICING BUSINESS IS A KEY COMPONENT OF PENNYMAC’S BALANCED BUSINESS MODEL HIGH-QUALITY SUCCESSFUL EXECUTION SERVICING PORTFOLIO OF LOSS MITIGATION REPRESENTS A GROWING ACTIVITIES KEEPS STREAM OF RECURRING BORROWERS IN THEIR EARNINGS AND HOMES AND ENHANCES CASH FLOW LIFETIME RELATIONSHIPS DRIVER OF LOW- SERVES AS A NATURAL COST, HIGH-QUALITY HEDGE TO PRODUCTION LEADS FOR OUR CONSUMER-DIRECT INCOME AS RATES RISE LENDING BUSINESS 54

PMT VANDY FARTAJ Senior Managing Director Chief Investment Officer WILL CHANG Senior Managing Director Deputy Chief Investment OfficerPMT VANDY FARTAJ Senior Managing Director Chief Investment Officer WILL CHANG Senior Managing Director Deputy Chief Investment Officer

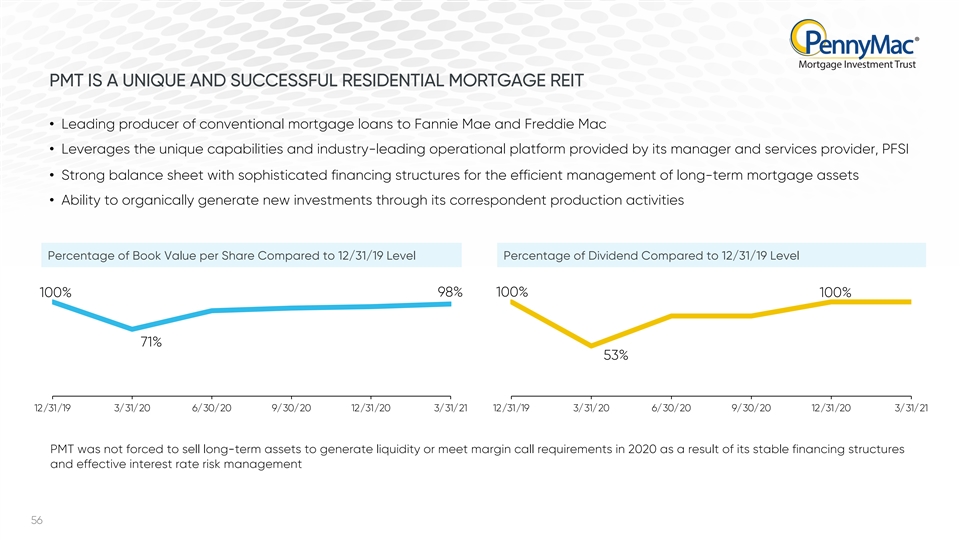

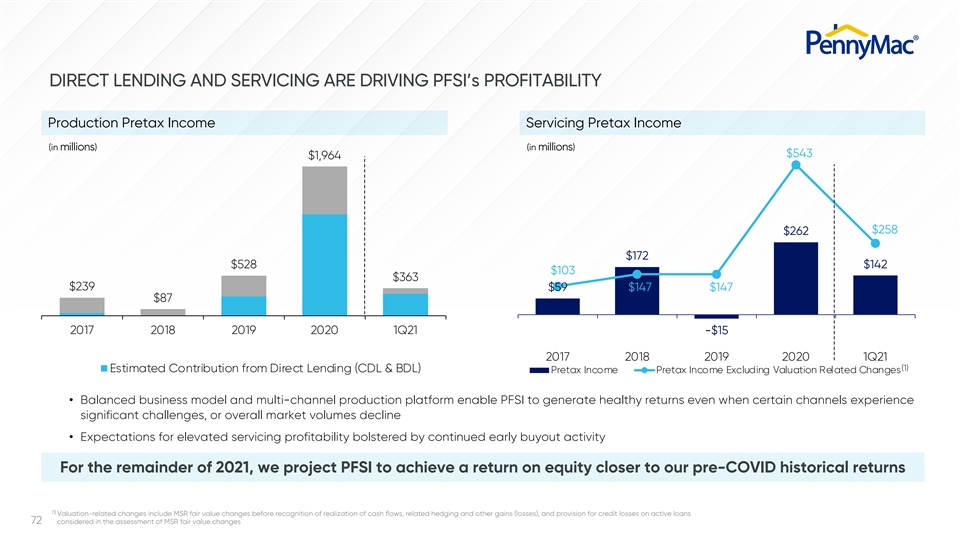

PMT IS A UNIQUE AND SUCCESSFUL RESIDENTIAL MORTGAGE REIT • Leading producer of conventional mortgage loans to Fannie Mae and Freddie Mac • Leverages the unique capabilities and industry-leading operational platform provided by its manager and services provider, PFSI • Strong balance sheet with sophisticated financing structures for the efficient management of long-term mortgage assets • Ability to organically generate new investments through its correspondent production activities Percentage of Book Value per Share Compared to 12/31/19 Level Percentage of Dividend Compared to 12/31/19 Level 100% 98% 100% 100% 71% 53% 12/31/19 3/31/20 6/30/20 9/30/20 12/31/20 3/31/21 12/31/19 3/31/20 6/30/20 9/30/20 12/31/20 3/31/21 PMT was not forced to sell long-term assets to generate liquidity or meet margin call requirements in 2020 as a result of its stable financing structures and effective interest rate risk management 56PMT IS A UNIQUE AND SUCCESSFUL RESIDENTIAL MORTGAGE REIT • Leading producer of conventional mortgage loans to Fannie Mae and Freddie Mac • Leverages the unique capabilities and industry-leading operational platform provided by its manager and services provider, PFSI • Strong balance sheet with sophisticated financing structures for the efficient management of long-term mortgage assets • Ability to organically generate new investments through its correspondent production activities Percentage of Book Value per Share Compared to 12/31/19 Level Percentage of Dividend Compared to 12/31/19 Level 100% 98% 100% 100% 71% 53% 12/31/19 3/31/20 6/30/20 9/30/20 12/31/20 3/31/21 12/31/19 3/31/20 6/30/20 9/30/20 12/31/20 3/31/21 PMT was not forced to sell long-term assets to generate liquidity or meet margin call requirements in 2020 as a result of its stable financing structures and effective interest rate risk management 56