As filed with the Securities and Exchange Commission on July 1, 2011

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form S-11

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Industrial Income Trust Inc.

(Exact name of registrant as specified in governing instruments)

518 Seventeenth Street, 17th Floor

Denver, Colorado 80202

Telephone (303) 228-2200

(Address of principal executive offices)

Dwight L. Merriman

Chief Executive Officer

518 Seventeenth Street, 17th Floor

Denver, Colorado 80202

Telephone (303) 228-2200

(Name, address and telephone number of agent for service)

copies to:

Judith D. Fryer, Esq.

Alice L. Connaughton, Esq.

Greenberg Traurig, LLP

200 Park Avenue

New York, New York 10166

(212) 801-9200

Approximate date of commencement of proposed sale to the public:as soon as practicable after this registration statement becomes effective.

If any of the Securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: x

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of theearlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | |

| Large accelerated filer | | ¨ | | Accelerated filer | | ¨ |

| | | |

| Non-accelerated filer | | x (Do not check if a smaller reporting company) | | Smaller reporting company | | ¨ |

CALCULATION OF REGISTRATION FEE

| | | | | | | | |

| |

Title of each class of

securities to be registered | | Amount to

be registered (1) | | Proposed maximum

offering price

per share | | Proposed maximum

aggregate

offering price(1) | | Amount of

registration fee |

Primary Offering, Common Stock, $0.01 par value per share | | | | $ | | $1,500,000,000 | | |

Distribution Reinvestment Plan, Common Stock, $0.01 par value per share | | | | $ | | $500,000,000 | | |

Total, Common Stock, $0.01 par value per share | | | | | | $2,000,000,000 | | $232,200 |

| |

| |

| (1) | Represents number of shares to be offered by the Registrant at a price to be determined by the Registrant prior to the effective date of this Registration Statement, with an aggregate offering amount of $1,500,000,000, and number of shares to be issued under the Registrant’s distribution reinvestment plan at a price to be determined by the Registrant prior to the effective date of this Registration Statement, with an aggregate offering amount of $500,000,000. The Registrant reserves the right to reallocate the shares of common stock being offered between the primary offering and the distribution reinvestment plan. Estimated solely for the purpose of determining the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is declared effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, Dated July 1, 2011

$2,000,000,000 Maximum Offering

$2,000 Minimum Purchase

Industrial Income Trust Inc. principally makes equity and debt investments in income producing real estate assets consisting primarily of high-quality distribution warehouses and other industrial properties that are leased to creditworthy corporate customers. We are externally managed by Industrial Income Advisors LLC, or the “Advisor,” an affiliate of ours. We believe we have operated in such a manner as to qualify, and we intend to elect to be treated, as a real estate investment trust, or “REIT”, for U.S. federal income tax purposes, commencing with our taxable year ended December 31, 2010. This is a best efforts offering, which means that Dividend Capital Securities LLC, or the “Dealer Manager,” our affiliate and the underwriter of this offering, will use its best efforts but is not required to sell any specific amount of shares. This is a continuous offering that will end no later than a date which is two years after the effective date of this offering, unless extended for up to an additional one year period. We are offering up to $2,000,000,000 in shares, 75% of which will be offered at a price of $ per share, and 25% of which will be offered pursuant to our distribution reinvestment plan at a price of $ per share. We reserve the right to reallocate the shares between the primary offering and our distribution reinvestment plan. Subject to certain exceptions, you must initially invest at least $2,000 in shares of our common stock. As of June 24, 2011, we had raised gross proceeds of $361.3 million from the sale of 36.5 million of our common shares in our initial public offering, including $2.9 million from the sale of approximately 306,000 of our common shares issued through our distribution reinvestment plan. Shares are issued in book entry form only.

Investing in shares of our common stock involves a high degree of risk. You should purchase shares only if you can afford a complete loss of your investment. See “Risk Factors” beginning on page 21. These risks include, among others:

| | • | | We have a limited prior operating history and there is no assurance that we will be able to achieve our investment objectives; |

| | • | | Because there is no public trading market for shares of our common stock and there are limits on the ownership, transferability and redemption of shares of our common stock, which will significantly limit the liquidity of your investment, you must be prepared to hold your shares for an indefinite length of time; |

| | • | | We have not identified any specific assets to acquire or investments to make with all of the proceeds of this offering. You will not have the opportunity to evaluate all of the investments we will make with the proceeds of this offering prior to purchasing shares of our common stock; |

| | • | | This is a “best efforts” offering and if we are unable to raise substantial funds, then we will be more limited in our investments; |

| | • | | Distributions have been paid from sources other than cash flows from operations, such as cash flows from financing activities, which include net proceeds of our initial public offering and borrowings (including borrowings secured by our assets). Some or all of our future distributions may be paid from borrowings as well as from the sales of assets, cash resulting from a waiver or deferral of fees, and interest income from our cash balances. There is no limit on distributions that may be made from these sources; however, proceeds from this offering will not be used. To the extent we pay distributions from sources other than our cash flows from operations, we may have less funds available for the acquisition of properties, and your overall return may be reduced. |

| | • | | We are subject to various risks related to owning real estate, including changes in economic, demographic and real estate market conditions, as well as the current severe dislocations in the U.S. and global capital and real estate markets; |

| | • | | The Advisor and other affiliates face conflicts of interest as a result of compensation arrangements, time constraints, competition for investments and for tenants and the fact that we do not have arm’s length agreements with our Advisor, Dividend Capital Property Management LLC, or the “Property Manager,” or any other affiliates of Industrial Income Advisors Group LLC, the parent of the Advisor and the sponsor of this offering, or the “Sponsor,” all of which could result in actions that are not in your best interests; and |

| | • | | If we fail to qualify as a REIT, it would adversely affect our operations and our ability to make distributions to our stockholders. |

Neither the Securities and Exchange Commission nor any state securities regulator has approved or disapproved of these securities or determined if this prospectus is truthful or complete. In addition, the Attorney General of the State of New York has not passed on or endorsed the merits of this offering. Any representation to the contrary is unlawful.

The use of forecasts in this offering is prohibited. Any representation to the contrary and any predictions, written or oral, as to the amount or certainty of any present or future cash benefit or tax consequence which may flow from an investment in our common stock is not permitted.

| | | | | | | | | | | | |

| | | PRICE TO

PUBLIC (1) | | | COMMISSIONS (1)(2) | | | PROCEEDS

TO

COMPANY

BEFORE

EXPENSES (1)(3) | |

Primary Offering Per Share of Common Stock | | $ | | | | $ | | | | $ | | |

Total Maximum | | $ | 1,500,000,000 | | | $ | 142,500,000 | | | $ | 1,357,500,000 | |

Distribution Reinvestment Plan Offering Per Share of Common Stock | | $ | | | | $ | 0.00 | | | $ | | |

Total Maximum | | $ | 500,000,000 | | | $ | 0.00 | | | $ | 500,000,000 | |

Total Maximum Offering (Primary and Distribution Reinvestment Plan) | | $ | 2,000,000,000 | | | $ | 142,500,000 | | | $ | 1,857,500,000 | |

| | | | | | | | | | | | |

| (1) | Assumes we sell $1,500,000,000 in the primary offering and $500,000,000 pursuant to our distribution reinvestment plan. |

| (2) | Includes a 7.0% sales commission and a 2.5% dealer manager fee. See “Plan of Distribution” beginning on page 184. |

| (3) | Proceeds are calculated before reimbursing the Advisor for paying other distribution-related costs and cumulative organization and offering expenses in the amount of up to $35,000,000, or 1.75% of aggregate gross offering proceeds from the sale of shares in the primary offering and the distribution reinvestment plan. |

The date of this prospectus is , 2011.

HOW TO SUBSCRIBE

Investors who meet the suitability standards described herein may purchase shares of our common stock. See “Suitability Standards” and “Plan of Distribution” below for the suitability standards. Investors seeking to purchase shares of our common stock should proceed as follows:

| | • | | Read this entire prospectus and any appendices and supplements accompanying this prospectus. |

| | • | | Complete the execution copy of the subscription agreement. A specimen copy of the subscription agreement, including instructions for completing it, is included in this prospectus as Appendix B. The subscription agreement includes representations covering, among other things, suitability. |

| | • | | Deliver a check or submit a wire transfer for the full purchase price of the shares of our common stock being subscribed for along with the completed subscription agreement to the soliciting broker dealer. Your check should be made payable, or wire transfer directed, to “Industrial Income Trust Inc.,” and the completed subscription agreement, along with the check or wire transfer, should be delivered to Industrial Income Trust Inc., PO Box 8353, Boston, Massachusetts 02266-8353 or sent overnight to Industrial Income Trust Inc., c/o Boston Financial Data Services, Inc., 30 Dan Road, Canton, Massachusetts 02021-2809. After you have satisfied the applicable minimum purchase requirement of $2,000, additional purchases must be in increments of $100, except for purchases made pursuant to our distribution reinvestment plan. |

Subscriptions will be effective only upon our acceptance, and we reserve the right to reject any subscription in whole or in part. Subscriptions will be accepted or rejected within 30 days of receipt by us and, if rejected, all funds shall be returned to subscribers with interest and without deduction for any expenses within 10 business days from the date the subscription is rejected, or as soon thereafter as practicable. We are not permitted to accept a subscription for shares of our common stock until at least five business days after the date you receive the final prospectus, as declared effective by the Securities and Exchange Commission, which we refer to as the “SEC,” as supplemented and amended. If we accept your subscription, our transfer agent will mail you a confirmation.

An approved trustee must process and forward to us subscriptions made through individual retirement accounts, or “IRAs,” Keogh plans and 401(k) plans. In the case of investments through IRAs, Keogh plans and 401(k) plans, we will send the confirmation and notice of our acceptance to the trustee.

i

SUITABILITY STANDARDS

The shares of common stock we are offering are suitable only for a person of adequate financial means, who desires a long-term investment and who will not need immediate liquidity from their investment. We do not expect to have a public market for shares of our common stock, which means that it may be difficult for you to sell your shares. On a limited basis, you may be able to have your shares redeemed through our share redemption program, and in the future we may also consider various forms of additional liquidity. You should not buy shares of our common stock if you need to sell them immediately or if you will need to sell them quickly in the future.

Our Sponsor and each participating broker dealer shall make every reasonable effort to determine that the purchase of shares of our common stock is a suitable and appropriate investment for each investor based on information concerning the investor’s financial situation and investment objectives. In consideration of these factors, we have established suitability standards for initial stockholders and subsequent transferees. These suitability standards require that a purchaser of shares of our common stock have either:

| | • | | A net worth (excluding the value of an investor’s home, furnishings and automobiles) of at least $250,000; or |

| | • | | A gross annual income of at least $70,000 and a net worth (excluding the value of an investor’s home, furnishings and automobiles) of at least $70,000. |

The minimum purchase amount is $2,000, except in certain states as described below. In order to satisfy the minimum purchase requirements for retirement plans, unless otherwise prohibited by state law, a husband and wife may jointly contribute funds from their separate IRAs, provided that each such contribution is made in increments of $100. You should note that an investment in shares of our common stock will not, in itself, create a retirement plan and that, in order to create a retirement plan, you must comply with all applicable provisions of the Internal Revenue Code of 1986, as amended, which we refer to as the “Code.”

The minimum purchase for Minnesota and New York residents is $2,500, except for IRAs which must purchase a minimum of $2,000. The minimum purchase for Tennessee residents is $2,500.

Purchases of shares of our common stock pursuant to our distribution reinvestment plan may be in amounts less than set forth above and are not required to be made in increments of $100.

Several states have established suitability standards different from those we have outlined above. Shares of our common stock will be sold only to investors in these states who meet the special suitability standards set forth below.

Kentucky, Michigan, Missouri, Oregon and Pennsylvania—In addition to our suitability requirements, investors must have a net worth of at least 10 times their investment in us.

Alabama—In addition to our suitability requirements, an Alabama investor must have a liquid net worth of at least 10 times such Alabama resident’s investment in us and other similar programs.

Iowa—In addition to our suitability requirements, an Iowa investor’s maximum investment in us and our publicly offered affiliates with similar investment objectives may not exceed 10% of such investor’s net worth.

Kansas and Massachusetts—In addition to our suitability requirements, it is recommended that investors limit their total investment in us and in the securities of similar programs to not more than 10% of their liquid net worth. For this purpose, “liquid net worth” is that portion of net worth (total assets minus total liabilities) which consists of cash, cash equivalents and readily marketable securities.

ii

Nebraska—A Nebraska investor must have either (i) a minimum net worth of $100,000 (exclusive of home, auto and furnishings) and an annual income of $70,000, or (ii) a minimum net worth of $350,000. In addition, a Nebraska investor’s maximum investment in us may not exceed 10% of such investor’s net worth (exclusive of home, auto and furnishings).

Ohio—In addition to our suitability requirements, an Ohio investor must have a net worth of at least 10 times such Ohio resident’s investment in us and other real estate programs sponsored by our affiliates.

Tennessee—Tennessee residents’ investment must not exceed 10% of their liquid net worth.

In the case of sales to fiduciary accounts, these suitability standards must be met by the fiduciary account, by the person who directly or indirectly supplied the funds for the purchase of the shares of our common stock or by the beneficiary of the account. These suitability standards are intended to help ensure that, given the long-term nature of an investment in shares of our common stock, our investment objectives and the relative illiquidity of shares of our common stock, shares of our common stock are an appropriate investment for those of you who become stockholders. Each participating broker dealer must make every reasonable effort to determine that the purchase of shares of our common stock is a suitable and appropriate investment for each stockholder based on information provided by the stockholder. Each participating broker dealer is required to maintain for six years records of the information used to determine that an investment in shares of our common stock is suitable and appropriate for a stockholder.

Determination of Suitability

In determining suitability, participating broker dealers who sell shares on our behalf may rely on, among other things, relevant information provided by the prospective investors. Each prospective investor should be aware that participating broker dealers are responsible for determining suitability and will be relying on the information provided by prospective investors in making this determination. In making this determination, participating broker dealers have a responsibility to ascertain that each prospective investor:

| | • | | meets the minimum income and net worth standards set forth under the “Suitability Standards” section of this prospectus; |

| | • | | can reasonably benefit from an investment in our shares based on the prospective investor’s investment objectives and overall portfolio structure; |

| | • | | is able to bear the economic risk of the investment based on the prospective investor’s net worth and overall financial situation; and |

| | • | | has apparent understanding of: |

| | • | | the fundamental risks of an investment in the shares; |

| | • | | the risk that the prospective investor may lose his or her entire investment; |

| | • | | the lack of liquidity of the shares; |

| | • | | the restrictions on transferability of the shares; and |

| | • | | the tax consequences of an investment in the shares. |

Participating broker dealers are responsible for making the determinations set forth above based upon information relating to each prospective investor concerning his age, investment objectives, investment experience, income, net worth, financial situation and other investments of the prospective investor, as well as other pertinent factors. Each participating broker dealer is required to maintain records of the information used to determine that an investment in shares is suitable and appropriate for an investor. These records are required to be maintained for a period of at least six years.

iii

TABLE OF CONTENTS

iv

PROSPECTUS SUMMARY

This prospectus summary summarizes information contained elsewhere in this prospectus. Because it is a summary, it may not contain all the information that is important to you. To fully understand this offering, you should carefully read this entire prospectus, including the “Risk Factors.” References in this prospectus to “us,” “we,” “our” or “the Company” refer to Industrial Income Trust Inc.

Industrial Income Trust Inc.

We make equity and debt investments in income producing real estate assets consisting primarily of high-quality distribution warehouses and other industrial properties that are leased to creditworthy corporate customers throughout the U.S. Prior to giving effect to our initial public offering, our sole investors were the Sponsor and the Advisor, which currently own 200 shares and 20,000 shares of our common stock, respectively. The Sponsor contributed $1,000 to Industrial Income Operating Partnership LP, or the “Operating Partnership,” in connection with our formation. The Sponsor, which owns the Advisor, is presently directly or indirectly majority owned by John A. Blumberg, James R. Mulvihill and Evan H. Zucker and/or their affiliates and the Sponsor and the Advisor are jointly controlled by Messrs. Blumberg, Mulvihill and Zucker and/or their affiliates. Messrs. Blumberg, Mulvihill and Zucker are a part of the Advisor’s management team.

We were formed as a Maryland corporation on May 19, 2009. We believe we have operated in such a manner as to qualify, and we intend to elect to be treated, as a REIT for U.S. federal income tax purposes, commencing with our taxable year ended December 31, 2010. Our office is located at 518 Seventeenth Street, 17th Floor, Denver, Colorado 80202, and our main telephone number is (303) 228-2200.

Investment Strategy and Objectives

Investment Objectives

Our primary investment objectives include the following:

| | • | | Preserving and protecting our stockholders’ capital contributions; |

| | • | | Providing current income to our stockholders in the form of regular cash distributions; and |

| | • | | Realizing capital appreciation through the potential sale of our assets or other Liquidity Event (as defined below). |

We cannot assure you that we will attain our investment objectives. Our charter places numerous limitations on us with respect to the manner in which we may invest our funds. These limitations cannot be changed unless our charter is amended, which requires the approval of our stockholders.

We will supplement this prospectus during the offering period in connection with the acquisition of any material investments.

Investment Strategy

As of June 30, 2011, we have acquired properties with an aggregate purchase price of $655.1 million, comprised of 63 buildings in 11 markets that total approximately 11.6 million square feet. Our operating portfolio, which excludes five value-add buildings owned by us, included 58 buildings with 136 tenants, an occupancy rate of 95%, and an aggregate average remaining lease term (based on square feet) of 6.5 years. The estimated aggregate weighted-average purchase

1

price capitalization rate of the operating portfolio is approximately 7.3% (calculated as the aggregate projected net operating income from in-place leases for the 12 months from the date of the respective acquisition, including any contractual rent increases contained in such leases for those 12 months, divided by the aggregate purchase price, exclusive of transfer taxes, due diligence expenses, and other closing costs including acquisition costs and fees paid to our Advisor or its affiliates).

We intend to continue to focus our investment activities on, and use the proceeds of this offering principally to build a national industrial platform, which includes the acquisition, development and/or financing of income producing real estate assets consisting primarily of high-quality distribution warehouses and other industrial properties that are leased to creditworthy corporate tenants. In general, our investment strategy adheres to the following core principles:

| | • | | Careful selection of target markets and submarkets, with an intent to overweight locations with high barriers to entry, close proximity to large demographic bases and/or access to major distribution hubs; |

| | • | | Primary focus on highly functional generic bulk distribution and light industrial facilities; |

| | • | | Achievement of portfolio diversification in terms of markets, tenants, industry exposure and lease rollovers; and |

| | • | | Emphasis on a mix of creditworthy national, regional and local tenants. |

Although our investment activities are currently focused primarily on distribution warehouses and other industrial properties, our charter and bylaws do not preclude us from investing in other types of commercial property or real estate-related debt. Our investment in any distribution warehouse, other industrial property, or other property type will be based upon the best interests of our Company and our stockholders as determined by the Advisor and our board of directors. Real estate assets in which we may invest may be acquired either directly by us or through joint ventures or other co-ownership arrangements with affiliated or unaffiliated third parties, and may include (i) equity investments in commercial real property, (ii) mortgage, mezzanine, construction, bridge and other loans related to real estate and (iii) investments in other real estate-related entities, including REITs, private real estate funds, real estate management companies, real estate development companies and debt funds, both foreign and domestic.

We may finance a portion of the purchase price of any real estate asset that we acquire with borrowings on an interim or permanent basis from banks, institutional investors and other lenders. Such borrowings may be secured by a mortgage or other security interest in some, or all, of our assets.

Our charter limits the aggregate amount we may borrow to an amount not to exceed 300% of our net assets, unless our board determines that a higher level is appropriate. For these purposes, net assets are defined to be our total assets (other than intangibles), valued at cost prior to deducting depreciation, reserves for bad debts and other non-cash reserves, less total liabilities.

There is no public trading market for our shares of common stock. On a limited basis, you may be able to have your shares redeemed through our share redemption program. However, in the future we may also consider various forms of additional liquidity, each of which we refer to as a “Liquidity Event,” including but not limited to (i) a listing of our common stock on a national securities exchange (or the receipt by our stockholders of securities that are listed on a national securities exchange in exchange for our common stock); (ii) our sale, merger or other transaction in which our stockholders either receive, or have the option to receive, cash, securities redeemable for cash, and/or securities of a publicly traded company; and (iii) the sale of all or substantially all of our assets where our stockholders either receive, or have the option to receive, cash or other consideration. We presently intend to consider alternatives for effecting a Liquidity Event for our stockholders beginning generally after seven years following the investment of substantially all of the net proceeds from all offerings made by us. Although our intention is to seek a Liquidity Event generally within seven to 10 years

2

following the investment of substantially all of the net proceeds from all offerings made by us, there can be no assurance that a suitable transaction will be available or that market conditions for a transaction will be favorable during that timeframe. Alternatively, we may seek to complete a Liquidity Event earlier than seven years following the investment of substantially all of the net proceeds from all offerings made by us. For purposes of the time frame for seeking a Liquidity Event, investment of “substantially all” of the net proceeds means the equity investment of 90% or more of the net proceeds from all offerings made by us.

Summary Risk Factors

An investment in shares of our common stock involves significant risks. See “Risk Factors” beginning on page 21. These risks include, among others:

| | • | | We have a limited prior operating history and there is no assurance that we will be able to achieve our investment objectives; |

| | • | | Because there is no public trading market for shares of our common stock and there are limits on the ownership, transferability and redemption of shares of our common stock, which will significantly limit the liquidity of your investment, you must be prepared to hold your shares for an indefinite length of time; |

| | • | | We have not identified any specific assets to acquire or investments to make with all of the proceeds of this offering. You will not have the opportunity to evaluate all of the investments we will make with the proceeds of this offering prior to purchasing shares of our common stock; |

| | • | | This is a “best efforts” offering and if we are unable to raise substantial funds, then we will be more limited in our investments; |

| | • | | We are subject to various risks related to owning real estate, including changes in economic, demographic and real estate market conditions, as well as the current severe dislocations in the U.S. and global capital and real estate markets; |

| | • | | Distributions have been paid from sources other than cash flows from operations, such as cash flows from financing activities, which include net proceeds of our initial public offering and borrowings (including borrowings secured by our assets). Some or all of our future distributions may be paid from borrowings as well as from the sales of assets, cash resulting from a waiver or deferral of fees, and interest income from our cash balances. There is no limit on distributions that may be made from these sources; however, proceeds from this offering will not be used. To the extent we pay distributions from sources other than our cash flows from operations, we may have less funds available for the acquisition of properties, and your overall return may be reduced; |

| | • | | The Advisor and other affiliates face conflicts of interest as a result of compensation arrangements, time constraints, competition for investments and for tenants, and the fact that we do not have arm’s length agreements with our Advisor, Property Manager, or any other affiliates of our Sponsor, all of which could result in actions that are not in your best interests; |

| | • | | If we fail to qualify as a REIT, it would adversely affect our operations and our ability to make distributions to our stockholders; |

| | • | | Our use of leverage, such as mortgage indebtedness and other borrowings, increases the risk of loss on our investments; |

| | • | | Continued and prolonged disruptions in the U.S. and global credit markets could adversely affect our ability to finance or refinance investments and the ability of our tenants to meet their obligations, which could affect our ability to meet our financial objectives and make distributions; |

3

| | • | | Our charter does not require us to have a finite date for a Liquidity Event and does not ensure that a Liquidity Event will occur. If we do not effect a Liquidity Event, it will be very difficult for you to have liquidity with respect to your investment in shares of our common stock; |

| | • | | We will not be a registered investment company, and we will not be subject to the provisions of the Investment Company Act of 1940, or the “Investment Company Act.” If we become subject to the Investment Company Act, it could significantly impair the operation of our business; and |

| | • | | The global economic downturn negatively impacted the commercial real estate market in the U.S., including the industrial warehouse and property sector, and if these adverse trends were to continue, our revenues could decline and our ability to pay distributions may be adversely affected. |

Compensation to the Advisor and Affiliates

The Advisor and other affiliates receive compensation and fees for services related to this offering and for the investment and management of our assets, subject to review and approval of a majority of our board of directors, including a majority of the independent directors. In addition, the Sponsor has been issued partnership units in the Operating Partnership constituting a separate series of partnership interests with special distribution rights, which we refer to as the “Special Units.” Set forth below is a summary of the fees and expenses we expect to pay these entities. The maximum amount that we may pay with respect to such fees and expenses is also set forth below.

See “Management Compensation” for a more detailed explanation of the fees and expenses payable to the Advisor and its affiliates and for a more detailed description of the Special Units. Subject to limitations in our charter, the fees, compensation, income, expense reimbursements, interests and other payments payable by us may increase or decrease during this offering or future offerings from those described below if such revision is approved by a majority of our board of directors, including a majority of the independent directors.

| | | | |

Type of Fee and Recipient | | Description and Method of Computation | | Estimated Maximum Dollar Amount |

| Organization and Offering Stage | | | | |

| | |

| Sales Commission—the Dealer Manager | | Up to 7.0% of the gross offering proceeds from the sale of shares in the primary offering (all or a portion of which may be reallowed to participating broker dealers). | | $105,000,000 |

| | |

| Dealer Manager Fee—the Dealer Manager | | Up to 2.5% of the gross offering proceeds from the sale of shares in the primary offering. | | $37,500,000 |

| | |

| Organization and Offering Expense Reimbursement—the Advisor or its affiliates, including the Dealer Manager | | Up to 1.75% of the aggregate gross offering proceeds from the sale of shares in the primary offering and the distribution reinvestment plan to reimburse the Advisor for paying certain cumulative organization and offering expenses and certain distribution-related expenses of the Dealer Manager and participating broker dealers. | | $35,000,000 |

4

| | | | |

Type of Fee and Recipient | | Description and Method of Computation | | Estimated Maximum Dollar Amount |

| Acquisition Stage | | | | |

| | |

| Acquisition Fees—the Advisor | | Acquisition of Real Properties Acquisition fees are payable to the Advisor in connection with the acquisition, development or construction of real properties and will vary depending on whether the asset acquired is in the operational, development or construction stage. For each real property acquired in the operational stage, the acquisition fee is an amount equal to 1.0% of the total purchase price of the properties acquired (or our proportional interest therein), including in all instances real property held in joint ventures or co-ownership arrangements. For each real property acquired prior to or during the development or construction stage, the acquisition fee will equal up to 4.0% of total project cost (including debt, whether borrowed or assumed); provided, however, that we will only pay such a fee to our Advisor if the Advisor provides, directly or indirectly, the development services. | | Operational Stage: $18,225,000 (assuming no debt financing to purchase assets). $72,900,000 (assuming debt financing equal to 75% of the aggregate value of our assets). Development or Construction Stage: $72,900,000 (assuming no debt financing to purchase assets). $291,600,000 (assuming debt financing equal to 75% of the aggregate value of our assets). |

| | |

| | Acquisition of Interest in Real Estate-Related Entities The Advisor is also entitled to receive acquisition fees of (i) 1.0% of our proportionate share of the purchase price of the property owned by any real estate-related entity in which we acquire a majority economic interest or that we consolidate for financial reporting purposes in accordance with generally accepted accounting principles in the U.S., or “GAAP,” and (ii) 1.0% of the purchase price in connection with the acquisition of an interest in any other real estate-related entity. | | Amount will depend on our proportional share and cannot be determined at the present time. |

| | |

| | Acquisition of Debt and Other Investments The Advisor is entitled to receive an acquisition fee of 1.0% of the purchase price, including any third-party | | $18,225,000 (assuming no debt financing to purchase assets or third party expenses, which cannot be determined at the present time). |

5

| | | | |

Type of Fee and Recipient | | Description and Method of Computation | | Estimated Maximum Dollar Amount |

| | expenses related to such investment, in connection with the acquisition or origination of any type of debt investment or other investment. | | |

| | |

| | For purposes of calculating fees in this prospectus, “purchase price” includes debt, whether borrowed or assumed. | | $72,900,000 (assuming debt financing equal to 75% of the aggregate value of our assets but no third party expenses, which cannot be determined at the present time). |

| | |

| Operational Stage | | | | |

| | |

| Asset Management Fees—the Advisor | | For all assets acquired, the asset management fee will consist of (i) a monthly fee of one-twelfth of 0.80% of the aggregate cost (including debt, whether borrowed or assumed) (before non-cash reserves and depreciation) of each real property asset within our portfolio (or our proportional interest therein with respect to real property held in joint ventures, co-ownership arrangements or real estate-related entities in which we own a majority economic interest or that we consolidate for financial reporting purposes in accordance with GAAP); provided, that the monthly asset management fee with respect to each real property asset located outside the U.S. that we own, directly or indirectly, will be one-twelfth of 1.20% of the aggregate cost (including debt, whether borrowed or assumed) (before non-cash reserves and depreciation) of such real property asset, (ii) a monthly fee of one-twelfth of 0.80% of the aggregate cost or investment (before non-cash reserves and depreciation, as applicable) of any interest in any other real estate-related entity or any type of debt investment or other investment, and (iii) a fee of 2.0% of the sales price of each asset upon disposition. | | Actual amounts are dependent upon aggregate cost of assets, the sales price of assets, the location of assets and the amount of leverage and therefore cannot be determined at the present time. |

| | |

| Property Management and Leasing Fees—the Property Manager | | Property management fees may be paid to the Property Manager in an amount equal to a market based percentage of the annual gross revenues of each real property owned by us and managed by the Property Manager. Such fee is | | Actual amounts are dependent upon gross revenues of specific properties and actual property management and leasing fees and therefore cannot be determined at the present time. |

6

| | | | |

Type of Fee and Recipient | | Description and Method of Computation | | Estimated Maximum Dollar Amount |

| | expected to range from 2% to 5% of annual gross revenues. In addition, we may pay the Property Manager a separate fee for initially leasing-up our real properties, for leasing vacant space in our real properties and for renewing or extending current leases on our real properties. Such leasing fee will be in an amount that is usual and customary for comparable services rendered to similar assets in the geographic market of the asset (generally expected to range from 2% to 8% of the projected first year’s annual gross revenues of the property); provided, however, that we will only pay a leasing fee to the Property Manager if the Property Manager provides leasing services, directly or indirectly. | | |

| | |

| Liquidity Stage | | | | |

| | |

| Real Estate Sales Commission—the Advisor or its affiliates | | Up to 50.0% of the reasonable, customary and competitive commission paid for the sale of a comparable real property, provided that the Advisor provides a substantial amount of services in connection with the sale and that such amount shall not exceed 3.0% of the contract price of the property sold and, when added to all other real estate commissions paid to unaffiliated parties in connection with the sale, may not exceed the lesser of a competitive real estate commission or 6.0% of the sales price of the property. If our Advisor receives a real estate commission, it will be in addition to the 2.0% asset disposition fee that will be payable to our Advisor, as described under the heading “Operational Stage—Asset Management Fees—the Advisor” in this table. | | Actual amounts are dependent upon the sales price of specific properties and therefore cannot be determined at the present time. |

| | |

| Special Units—Industrial Income Advisors Group LLC, the parent of the Advisor | | In general, the holder of the Special Units will be entitled to receive 15% of net sales proceeds on dispositions of the Operating Partnership’s assets after stockholders have received, in the aggregate, cumulative distributions from all sources equal to their capital contributions plus a 6.5% cumulative | | Actual amounts are dependent on net sales proceeds and therefore cannot be determined at the present time. |

7

| | | | |

Type of Fee and Recipient | | Description and Method of Computation | | Estimated Maximum Dollar Amount |

| | non-compounded annual pre-tax return on their net contributions. The Special Units will be redeemed for a specified amount upon the earliest of: (i) the occurrence of certain events that result in the termination or non-renewal of the Advisory Agreement defined below in “—The Advisor”, or (ii) the listing of our common stock on a national securities exchange, or other Liquidity Event. | | |

| | |

| | Notwithstanding anything herein to the contrary, no redemption of the Special Units will be permitted unless and until the stockholders have received (or are deemed to have received), in the aggregate, cumulative distributions from operating income, sales proceeds and other sources in an amount equal to their capital contributions plus a 6.5% cumulative non-compounded annual pre-tax return thereon. See “The Operating Agreement—Redemption Rights of Special Units.” | | |

The table below provides information regarding fees paid to the Dealer Manager, the Advisor and their affiliates in connection with our operations and our initial public offering. The table includes amounts incurred for the three months ended March 31, 2011 and for the year ended December 31, 2010, as well as amounts payable as of March 31, 2011 and December 31, 2010.

| | | | | | | | | | | | | | | | |

Type and Recipient | | Incurred for the

Three Months Ended

March 31,

2011 | | | Incurred and

Unpaid as of

March 31,

2011 | | | Incurred for the

Year Ended

December 31,

2010 | | | Incurred and

Unpaid as of

December 31,

2010 | |

| | | (in thousands) | |

Sales Commissions—the Dealer Manager | | $ | 6,277 | | | $ | 397 | | | $ | 9,906 | | | $ | 291 | |

Dealer Manager Fee—the Dealer Manager | | | 2,664 | | | | 153 | | | | 3,903 | | | | 126 | |

Organization and Offering Expense Reimbursement—the Advisor or its affiliates, including the Dealer Manager | | | 1,844 | | | | 107 | | | | 2,725 | | | | 96 | |

Acquisition Fees—the Advisor | | | 3,163 | | | | — | | | | 4,527 | | | | 322 | |

Asset Management Fees—the Advisor | | | 667 | | | | — | | | | 428 | | | | 151 | |

Other (repayments) expenses —the Advisor (1) | | | (1,767 | ) | | | 20 | | | | 437 | | | | 70 | |

| | | | | | | | | | | | | | | | |

Subtotal(2) | | | 12,888 | | | | 677 | | | | 21,926 | | | | 1,056 | |

Incurred Organization and Offering Expense Reimbursement—not payable until additional gross proceeds of the offering are received (2) | | | 2,734 | | | | 5,705 | | | | 2,971 | | | | 5,796 | |

| | | | | | | | | | | | | | | | |

Due to Affiliates | | $ | 15,622 | | | $ | 6,382 | | | $ | 24,897 | | | $ | 6,852 | |

| | | | | | | | | | | | | | | | |

8

| (1) | Includes reimbursement for expenses incurred on our behalf in connection with the services provided to us under the Advisory Agreement. |

| (2) | We reimburse the Advisor for certain organization and offering expenses up to 1.75% of the gross offering proceeds. The Advisor or an affiliate of the Advisor is responsible for the payment of our cumulative organization and offering expenses to the extent the total of such cumulative expenses exceed the 1.75% organization and offering expense reimbursement, without recourse against or reimbursement by us. A portion of the organization and offering expenses for the year ended December 31, 2010 and for the three months ended March 31, 2011, represents an accrual based on the estimated gross offering proceeds to be raised in the future. |

Conflicts of Interest

The Advisor and certain of our other affiliates are subject to conflicts of interest in connection with the management of our business affairs, including the following:

| | • | | The managers, directors, officers and other employees of the Advisor, its affiliates and related parties, must allocate their time between advising us and managing various other real estate programs and projects and business activities in which they may be involved, which may be numerous and may change as programs are closed or new programs are formed; |

| | • | | The compensation payable by us to the Advisor and other affiliates may not be on terms that would result from arm’s length negotiations between unaffiliated parties; |

| | • | | We may purchase assets from, sell assets to, or enter into business combinations involving certain affiliates of the Advisor (if approved by a majority of our board of directors, including a majority of the independent directors, not otherwise interested in the transaction, as being fair and reasonable to us); |

| | • | | We cannot guarantee that the terms of any joint venture entered into with affiliated entities proposed by the Advisor will be equally beneficial to us as those that would result from arm’s length negotiations between unaffiliated parties; |

| | • | | We expect to compete with certain affiliates of direct or indirect owners of our Sponsor for investments, including Dividend Capital Total Realty Trust Inc. (which we refer to herein as “Total Realty Trust”), Fundcore Institutional Income Trust Inc. and one or more additional debt funds that an affiliate of the Sponsor and Fundcore Finance Group LLC, may form and/or advise, the primary purpose of which will be to originate debt secured by commercial real estate (which, together with Fundcore Institutional Income Trust Inc., we refer to herein collectively as the “Fundcore Funds”), subjecting the Advisor and its affiliates to certain conflicts of interest in evaluating the suitability of investment opportunities and making or recommending acquisitions on our behalf; |

| | • | | Regardless of the quality of the assets acquired, the services provided to us or whether we make distributions to our stockholders, the Advisor and its affiliates will receive certain fees in connection with transactions involving the purchase, management and sale of our investments; |

| | • | | Our Advisor has incentives to recommend that we purchase properties using debt financing since the acquisition fees and asset management fees that we pay to the Advisor will increase if we use debt financing to acquire properties; and |

| | • | | The Property Manager and the Dealer Manager are affiliates of ours. As a result, (i) we may not always have the benefit of independent property management, (ii) we do not have the benefit of an independent dealer manager, and (iii) you do not have the benefit of an independent third party review of this offering to the same extent as if we and the Dealer Manager were unaffiliated. |

9

For a more detailed discussion of these conflicts of interest, see “Conflicts of Interest” beginning on page 125 of this prospectus.

Our UPREIT Structure

An Umbrella Partnership Real Estate Investment Trust, which we refer to as “UPREIT,” is a REIT that holds all or substantially all of its assets through a partnership in which the REIT holds an interest. We use this structure because, among other reasons, a sale of property directly to the REIT in exchange for cash or REIT shares, or a combination of cash and REIT shares, is generally a taxable transaction to the selling property owner. In an UPREIT structure, a seller of a property who desires to defer the taxable gain on the disposition of his property may transfer the property to the partnership in exchange for units in the partnership and defer taxation of gain until the seller later sells the units in the partnership or exchanges them, normally on a one-for-one basis, for REIT shares. If the REIT shares are publicly traded, the former property owner will achieve liquidity for his investment. We believe that using an UPREIT structure gives us an advantage in acquiring desired properties from persons who may not otherwise sell their properties because of unfavorable tax results.

Our Operating Partnership

We intend to own all of our assets directly or indirectly through our Operating Partnership or its subsidiaries. As the sole general partner of the Operating Partnership, we have invested $2,000 in the Operating Partnership in exchange for 200 partnership units in the Operating Partnership, or “OP Units,” and we intend that the proceeds of the offering will be provided to the Operating Partnership for investment and operational purposes. The initial limited partner of the Operating Partnership is the Sponsor. The Advisor invested $200,000 in the Operating Partnership in exchange for 20,000 OP Units, which were subsequently exchanged for 20,000 shares of our common stock, and the Sponsor has invested $1,000 in the Operating Partnership and has been issued a separate class of OP Units which constitute the Special Units. The holders of OP Units (other than us and the holder of the Special Units) generally have the right to cause the Operating Partnership to redeem all or a portion of their OP Units for, at our sole discretion, shares of our common stock, cash, or a combination of both.

Our Board of Directors

We operate under the direction of our board of directors, the members of which are accountable to us and our stockholders as fiduciaries. Our board of directors is responsible for the management and control of our affairs. We currently have five members on our board of directors, three of whom are independent of us. Our directors are elected annually by the stockholders. Our board of directors has established an Audit Committee, an Investment Committee, a Nominating and Corporate Governance Committee and an IIT - TRT Conflicts Resolution Committee. Our board of directors may also establish a Compensation Committee. The names and biographical information of our directors and officers are contained under “Management—Directors and Executive Officers.”

The Advisor

Our Advisor was formed as a Delaware limited liability company on May 12, 2009. We have contracted with the Advisor pursuant to an amended and restated advisory agreement, dated May 14, 2010, as amended, which we refer to as the “Advisory Agreement,” to manage our day-to-day operating and acquisition activities and to implement our investment strategy. Under the Advisory Agreement, the Advisor must use reasonable efforts, subject to the oversight, review and approval of our board of directors, to, among other things, research, identify, review and make investments in and dispositions of investments on our behalf consistent with our investment policies and objectives. The Advisor performs its duties and responsibilities under the Advisory Agreement as a fiduciary of ours and our stockholders. The term of the Advisory Agreement is for one year, subject to renewals by our board of directors for an unlimited number of successive one-year periods. The

10

Advisory Agreement was renewed through December 16, 2011, pursuant to approval by our independent directors on December 9, 2010. Our officers and our affiliated directors are all employees of the Advisor.

The Sponsor

Our Sponsor was formed as a Delaware limited liability company on May 12, 2009. The Sponsor currently owns 200 shares of our common stock, which were originally purchased by Blue Mesa Capital LLC, an affiliate of one of the owners of the Sponsor, and subsequently transferred to the Sponsor. The Sponsor also contributed $1,000 to the Operating Partnership in connection with its formation. The Sponsor, which owns the Advisor, is presently directly or indirectly owned by John A. Blumberg, James R. Mulvihill and Evan H. Zucker and/or their affiliates and the Sponsor is jointly controlled by Messrs. Blumberg, Mulvihill and Zucker and/or their affiliates.

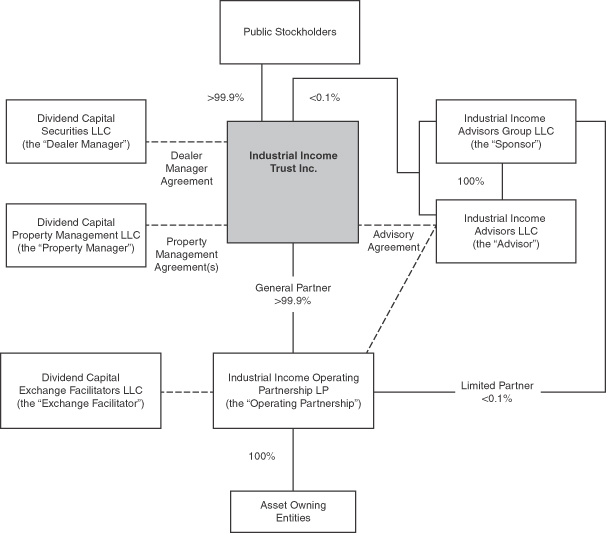

Our Affiliates

Various affiliates of ours are involved in this offering and our operations. The Dealer Manager will provide dealer manager services to us in this offering. The Property Manager may perform certain property management services for us and the Operating Partnership. Dividend Capital Exchange Facilitators LLC, which we refer to as the “Exchange Facilitator,” may assist in effecting transactions related to potential private placements by the Operating Partnership of tenancy-in-common interests in real properties, Delaware statutory trust interests, and similar private placements. Furthermore, we expect that we may enter into, and the Advisor expects that it may enter into, contractual arrangements with other affiliated entities. We refer to the Advisor, the Dealer Manager, the Property Manager, the Exchange Facilitator and other of our affiliates, each as a “Sponsor affiliated entity” and collectively as “Sponsor affiliated entities.”

11

Structure Chart

The chart below shows the relationships among various Sponsor affiliated entities. The Sponsor, which owns the Advisor, is presently directly or indirectly majority owned by John A. Blumberg, James R. Mulvihill and Evan H. Zucker and/or their affiliates and the Sponsor and the Advisor are jointly controlled by Messrs. Blumberg, Mulvihill and Zucker and/or their affiliates. The Dealer Manager, the Property Manager and the Exchange Facilitator are presently each directly or indirectly majority owned, controlled and/or managed by Messrs. Blumberg, Mulvihill and/or Zucker and/or their affiliates. As of the date of this prospectus, the Sponsor has not issued, but expects in the future to issue, equity or profits interests or derivatives thereof to certain of its employees, affiliated or other unaffiliated individuals, consultants or other parties. However, none of such transactions is expected to result in a change in control of the Sponsor.

12

Terms of the Offering

We are offering up to $2.0 billion in shares of our common stock, 75% of which are being offered to the public at a price of $ per share, and 25% of which are being offered pursuant to our distribution reinvestment plan at a price of $ per share. We reserve the right to reallocate the shares of common stock we are offering between the primary offering and our distribution reinvestment plan.

As of June 24, 2011, we had raised gross proceeds of $361.3 million from the sale of 36.5 million of our common shares in our initial public offering, including $2.9 million from the sale of approximately 306,000 of our common shares issued through our distribution reinvestment plan. As of that date, 166.2 million shares remained available for sale pursuant to our initial public offering, including 52.3 million shares available for sale through our distribution reinvestment plan.

We expect to commence this offering after the termination of our initial public offering. We will offer shares of our common stock on a continuous basis until this offering terminates on or before , 2013, a date which is two years after the effective date of this offering, unless extended for up to an additional one year period. We reserve the right to terminate this offering at any time. The net offering proceeds will be available for investment as soon as we accept your subscription agreement. We generally intend to admit stockholders on a daily basis.

Estimated Use of Proceeds

Our management team expects to invest approximately 87.0% to 90.0% of the gross offering proceeds to acquire real property, debt and other investments as described above. The actual percentage of offering proceeds used to make investments will depend on the number of primary shares sold and the number of shares sold pursuant to our distribution reinvestment plan.

Distributions

We believe we have operated in such a manner as to qualify, and we intend to elect to be treated, as a REIT for U.S. federal income tax purposes, commencing with our taxable year ended December 31, 2010. In order to qualify as a REIT, we are generally required to distribute at least 90% of our annual REIT taxable income to our stockholders. We intend to continue to accrue and make distributions on a quarterly basis. Until the net proceeds from this offering are fully invested and from time to time thereafter, we may not generate sufficient company-defined funds from operations to fully cover distributions. See “Selected Financial Data” for a reconciliation of Funds from Operations (“FFO”) and Company-Defined FFO to our GAAP net loss, and “Description of Capital Stock—Distributions” for a discussion of distributions declared as compared to FFO for the year ended December 31, 2010 and the three months ended March 31, 2011. Distributions have been paid from sources other than cash flows from operations, such as cash flows from financing activities, which include net proceeds of our initial public offering and borrowings (including borrowings secured by our assets). Some or all of our future distributions may be paid from sources such as cash flows from financing activities, which include borrowings (including borrowings secured by our assets) and sales of assets, cash resulting from a waiver or deferral of fees otherwise payable to the Advisor or its affiliates, and interest income from our cash balances. We have not established a cap on the amount of our distributions that may be paid from any of these sources. Distributions will be authorized at the discretion of our board of directors, and will depend on, among other things, current and projected cash requirements, tax considerations and other factors deemed relevant by our board.

Our board of directors authorized cash distributions at a quarterly rate of $0.15625 per share of common stock for each quarter of 2010, and for the first, second and third quarters of 2011. We calculate individual payments of distributions to each stockholder based upon daily record dates during each quarter so that investors

13

are eligible to earn distributions immediately upon purchasing shares of our common stock. The distributions are calculated based on common stockholders of record as of the close of business each day in the period. Accordingly, assuming we declare daily distributions during the period in which you own shares of our common stock, your distributions will begin to accrue on the date we accept your subscription for shares of our common stock, which is subject to, among other things, your meeting the applicable suitability requirements for this offering. All cash distributions for 2010 and the three months ended March 31, 2011 were from sources other than cash flows from operations on a GAAP basis.

Our long-term goal is to have company-defined funds from operations meet or exceed the payment of quarterly distributions to investors. There can be no assurances that we will achieve this goal or that the current distribution rate will be maintained. In the near-term, we expect to continue to be dependent on cash flows from financing activities to pay distributions, which if insufficient could negatively impact our ability to pay distributions or may erode the net asset value. We intend to pay distributions for the second quarter of 2011 on or around July 15, 2011.

The following table outlines distributions declared for the second, third, and fourth quarters of 2010 and the three months ended March 31, 2011 and the sources of funds used to pay cash distributions:

| | | | | | | | | | | | | | | | |

| | | Three Months Ended | |

| | | June 30,

2010 | | | September 30,

2010 | | | December 31,

2010 | | | March 31,

2011 | |

Distributions: | | | | | | | | | | | | | | | | |

Paid in cash | | $ | 120,865 | | | $ | 400,584 | | | $ | 941,979 | | | $ | 1,818,654 | |

Reinvested in shares | | | 179,420 | | | | 449,762 | | | | 843,861 | | | | 1,435,880 | |

| | | | | | | | | | | | | | | | |

Total distributions | | $ | 300,285 | | | $ | 850,346 | | | $ | 1,785,840 | | | $ | 3,254.534 | |

| | | | | | | | | | | | | | | | |

Source of distributions paid in cash: | | | | | | | | | | | | | | | | |

Provided by financing activities(1) | | $ | 120,865 | | | $ | 400,584 | | | $ | 941,979 | | | $ | 1,818,654 | |

Provided by operating activities | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | |

Total distributions paid in cash | | $ | 120,865 | | | $ | 400,584 | | | $ | 941,979 | | | $ | 1,818,654 | |

| | | | | | | | | | | | | | | | |

| (1) | For the three months ended June 30, 2010, all cash distributions provided by financing activities were funded through offering proceeds. For the three months ended September 30, 2010, December 31, 2010 and March 31, 2011, all cash distributions provided by financing activities were funded through proceeds from our debt financings. |

Distribution Reinvestment Plan

You may participate in our distribution reinvestment plan and elect to have the cash distributions you receive reinvested in shares of our common stock at $ per share. Our board of directors may amend or terminate the distribution reinvestment plan at its discretion at any time; provided, however, that if our board of directors materially amends or terminates the distribution reinvestment plan, such material amendment or termination, as applicable, will only be effective upon 10 days’ written notice to you. Following any termination of the distribution reinvestment plan, all subsequent distributions to stockholders would be made in cash.

Share Redemption Program

After you have held your shares of common stock for a minimum of one year, our share redemption program may provide a limited opportunity for you to have your shares of common stock redeemed, subject to certain restrictions and limitations, at a price equal to or at a discount from the purchase price you paid for the

14

shares being redeemed. The discount will vary based upon the length of time that you have held the shares of our common stock subject to redemption, as described in the following table, which has been posted on our website at www.industrialincome.com.

| | |

Share Purchase Anniversary | | Redemption Price

as a Percentage

of Purchase Price |

Less than one year | | No Redemption Allowed |

One year | | 92.5% |

Two years | | 95.0% |

Three years | | 97.5% |

Four years and longer | | 100.0% |

We are not obligated to redeem shares of our common stock under the share redemption program. We presently intend to limit the number of shares to be redeemed during any calendar quarter to the “Quarterly Redemption Cap” which will equal the lesser of: (i) one-quarter of five percent of the number of shares of common stock outstanding as of the date that is 12 months prior to the end of the current quarter, and (ii) the aggregate number of shares sold pursuant to our distribution reinvestment plan in the immediately preceding quarter, which amount may be less than the Aggregate Redemption Cap described below. Our board of directors retains the right, but is not obligated to, redeem additional shares if, in its sole discretion, it determines that it is in our best interest to do so, provided that we will not redeem during any consecutive 12-month period more than five percent of the number of shares of common stock outstanding at the beginning of such 12-month period (referred to herein as the “Aggregate Redemption Cap”), unless permitted to do so by applicable regulatory authorities. Although we presently intend to redeem shares pursuant to the above-referenced methodology, to the extent that the aggregate proceeds received from the sale of shares pursuant to our distribution reinvestment plan in any quarter are not sufficient to fund redemption requests, our board of directors may, in its sole discretion, choose to use other sources of funds to redeem shares of our common stock, up to the Aggregate Redemption Cap. Such sources of funds could include cash on hand, cash available from borrowings, cash from the sale of our shares pursuant to our distribution reinvestment plan in other quarters, and cash from liquidations of securities investments, to the extent that such funds are not otherwise dedicated to a particular use, such as working capital, cash distributions to stockholders, debt repayment, purchases of real property, debt related or other investments, or redemptions of OP Units. Our board of directors has no obligation to use other sources to redeem shares of our common stock under any circumstances.

Our board of directors may, in its sole discretion, amend, suspend, or terminate the share redemption program at any time if it determines that the funds available to fund the share redemption program are needed for other business or operational purposes or that amendment, suspension or termination of the share redemption program is in the best interests of our stockholders. You will have no right to request redemption of your shares of our common stock if the shares of our common stock are listed on a national securities exchange. For the three months ended March 31, 2011, we received one eligible redemption request related to 9,300 shares of our common stock, which we redeemed in full for $93,000 in April 2011 using proceeds from the sale of shares pursuant to our distribution reinvestment plan. The redemption request was due to the death of a stockholder.

Investment Company Act of 1940 Exemption

We intend to conduct the operations of the Company and its subsidiaries so that they will not be required to register as an investment company under the Investment Company Act.

Section 3(a)(1)(A) of the Investment Company Act defines an investment company as any issuer that is or holds itself out as being engaged primarily in the business of investing, reinvesting or trading in securities. Section 3(a)(1)(C) of the Investment Company Act defines an investment company as any issuer that is engaged or proposes to engage in the business of investing, reinvesting, owning, holding or trading in securities and owns

15

or proposes to acquire investment securities having a value exceeding 40% of the value of the issuer’s total assets (exclusive of U.S. Government securities and cash items) on an unconsolidated basis, which we refer to as the 40% test. Excluded from the term “investment securities,” among other things, are U.S. Government securities and securities issued by majority-owned subsidiaries that are not themselves investment companies and are not relying on the exception from the definition of investment company set forth in Section 3(c)(1) or Section 3(c)(7) of the Investment Company Act.

We will conduct our businesses primarily through our majority owned Operating Partnership and expect to establish other direct or indirect subsidiaries to carry out specific activities. We expect the focus of our business will involve investments in real estate, buildings, and other assets that can be referred to as “sticks and bricks.” We also may invest in other real estate investments such as real estate-related securities. Both we and the Operating Partnership intend to conduct our operations so that they comply with the limit imposed by the 40% test and neither will be primarily engaged in or hold ourselves out as being engaged primarily in the business of investing, reinvesting or trading in securities. Therefore, we expect that we and the Operating Partnership will not be subject to registration under the Investment Company Act. The securities issued to the Operating Partnership by its wholly owned or majority-owned subsidiaries that are not investment companies or companies exempt under Sections 3(c)(1) or 3(c)(7) of the Investment Company Act, as well as any securities of any of our direct subsidiaries that are not investment companies or companies exempt under Sections 3(c)(1) or 3(c)(7) of the Investment Company Act, are not investment securities for the purpose of the 40% test.

We will monitor our holdings and those of our subsidiaries to ensure continuing and ongoing compliance with these tests, and we will be responsible for making the determinations and calculations required to confirm our compliance with these tests. If the SEC does not agree with our determinations, we may be required to adjust our activities, those of the Operating Partnership, or other subsidiaries.

One or more of our subsidiaries or subsidiaries of the Operating Partnership may seek to qualify for an exemption from registration as an investment company under the Investment Company Act pursuant to other provisions of the Investment Company Act, such as Section 3(c)(5)(C) which is available for entities “primarily engaged in the business of purchasing or otherwise acquiring mortgages and other liens on and interests in real estate.” This exemption generally requires that at least 55% of such a subsidiary’s portfolios be comprised of qualifying assets, and at least 80% of the total asset portfolio must be comprised of qualifying assets and real estate-related assets (and no more than 20% comprised of miscellaneous assets that are not real estate-related assets). To qualify for this exemption, the subsidiary would be required to comply with interpretations issued by the staff of the SEC that govern this activity.

Qualification for these exemptions could affect our ability to acquire or hold investments, or could require us to dispose of investments that we might prefer to retain in order to remain qualified for such exemptions. Changes in current policies by the SEC and its staff could also require that we alter our business activities for this purpose. See “Risk Factors” for a discussion of certain risks associated with the Investment Company Act.

Information About This Prospectus

This prospectus is part of a registration statement that we filed with the SEC using a continuous offering process. Periodically, as we make material investments and in certain other instances, we will provide a prospectus supplement that may add, update or change information contained in this prospectus. Any statement that we make in this prospectus will be modified or superseded by any inconsistent statement made by us in a subsequent prospectus supplement. The registration statement we filed with the SEC includes exhibits that provide more detailed descriptions of the matters discussed in this prospectus. You should read this prospectus and the related exhibits filed with the SEC and any prospectus supplement, together with additional information described herein under “Additional Information.” In this prospectus, we use the term “day” to refer to a calendar day, and we use the term “business day” to refer to any day other than Saturday, Sunday, a legal holiday or a day on which banks in New York City are authorized or required to close.

16

QUESTIONS AND ANSWERS ABOUT THIS OFFERING

Set forth below are some of the more frequently asked questions and answers relating to our structure, our management, our business and an offering of this type.

Questions and Answers Relating to our Structure, Management and Business

Q: WHAT IS A “REIT”?

A: In general, a REIT is a company that:

| | • | | Offers the benefits of a diversified real estate portfolio under professional management; |

| | • | | Is required to make distributions to investors of at least 90% of its taxable income for each year; |

| | • | | Prevents the federal “double taxation” treatment of income that generally results from investments in a corporation because a REIT is not generally subject to federal corporate income taxes on the portion of its net income that is distributed to the REIT’s stockholders; and |

| | • | | Combines the capital of many investors to acquire or provide financing for real estate assets. |

Q: WHAT IS THE EXPERIENCE OF THE ADVISOR’S MANAGEMENT TEAM?

A: The key members of the Advisor’s management team include, in alphabetical order, John Blumberg, Anne DeMarco, David Fazekas, Andrea Karp, Thomas McGonagle, Dwight Merriman III, Lainie Minnick, James Mulvihill, Scott Recknor, Gary Reiff, Randy Resley, Peter Vanderburg, J.R. Wetzel, Joshua Widoff, and Evan Zucker. The Advisor’s management team collectively has substantial experience in various aspects of acquiring, owning, managing, financing and operating commercial real estate across diverse property types, as well as significant experience in the asset allocation and investment management of real estate, debt and other investments.

Certain affiliates of the Sponsor, directly or indirectly through affiliated entities, have sponsored three public REITs including Keystone Property Trust (New York Stock Exchange (“NYSE”): KTR), (formerly known as American Real Estate Investment Corp.), which was acquired by ProLogis Trust (NYSE: PLD) in August 2004, DCT Industrial Trust Inc. (formerly known as Dividend Capital Trust Inc. and which we refer to herein as “DCT Industrial”) (NYSE: DCT) and Total Realty Trust. Owners of the Sponsor, directly or indirectly through affiliated entities, have also sponsored numerous private entities.

Collectively, as of December 31, 2010, the public and private real estate programs sponsored by certain direct and/ or indirect owners of the Sponsor, together with their affiliates and others, had raised approximately $5.8 billion of equity capital and equity capital commitments and had purchased interests in real properties having combined acquisition and development costs of approximately $7.7 billion.

Q: WHO WILL CHOOSE WHICH INVESTMENTS TO MAKE?

A: The Advisor will choose which real property, debt and other investments to make based on specific investment objectives and criteria, including preserving and protecting our stockholders’ capital contributions, providing current income to our stockholders in the form of regular cash distributions and realizing capital appreciation upon the potential sale of our assets, and subject to the direction, oversight and approval of our board of directors, and under certain circumstances our Investment Committee. If we are considering purchasing an investment from an affiliate, a majority of our board of directors (including a majority of our independent directors) will need to approve such investment.

17

Q: WHY DO YOU PLAN ON FOCUSING YOUR INVESTMENTS ON INDUSTRIAL PROPERTIES?

A: We believe that ownership of industrial properties may have certain potential advantages relative to ownership of other classes of real estate, including but not limited to the following:

| | • | | We believe that industrial properties generally exhibit lower rent volatility than other types of commercial real estate, resulting in greater revenue stability; |

| | • | | We believe that, because industrial properties are typically leased on a net basis, meaning the lessee undertakes to pay all the expenses of maintaining the leased property, such as insurance, taxes, utilities and repairs, the owner has limited cost responsibilities; |

| | • | | We believe that operating costs and capital improvement costs are generally lower for industrial properties; |