Filed by Towers Watson & Co.

Pursuant to Rule 425 under the

Securities Act of 1933, as amended,

and deemed filed pursuant to Rule 14a-6(b)

of the Securities Exchange Act of 1934, as amended

Subject Company:

Towers Watson & Co. (Commission File No. 001-34594)

The following slide presentation was prepared by Towers Watson & Co. (“Towers Watson”) regarding the proposed merger of Towers Watson and Willis Group Holdings plc. Towers Watson first made these materials available on November 9, 2015.

1 Investor Presentation Update – Merger with Willis Group Holdings November 9, 2015 |

2 The benefits to Towers Watson shareholders are clear: This merger is the right deal with the right partner to drive significant shareholder value. The Towers Watson Board of Directors urges shareholders to vote FOR the transaction at our upcoming meeting on November 18, 2015 Unique opportunity to accelerate TW’s long-term growth strategy Right management team in place to execute on the integration and strategic plan Clear, compelling synergies Result of extensive evaluation and negotiation by an engaged, independent board Exchange ratio that is favorable to TW shareholders |

3 Unique Opportunity to Accelerate Long-Term Strategy Acceleration of TW’s existing long-term strategy » Increased penetration in growth / emerging markets » Higher percentage of products / solutions » Stronger platform for innovation Expanded direct access to Willis’ leading U.S. middle-market client base » Supports TW’s goal of capturing a 25% share of the growing active employee exchange market » Expanded client reach provides opportunity to realize growth across other areas, such as large market P&C brokerage and Global Health and Group Benefits Global platform across 120+ countries, expanding TW’s reach by 80+ countries » Leverages Willis’ strong relationships with large companies internationally Optimal mix of client offerings, with higher percentage of solutions » The transaction creates a comprehensive portfolio of advisory services, solutions and technology Brings together the top industry talent while enhancing our ability to invest in innovation “Towers Watson merger is an excellent strategic move by both companies. Willis’ has the country’s most extensive broker distribution network concentrating on small and mid-sized organizations in the country.” MKM Partners August 12, 2015 “[W]e believe the strategic rationale underpinning the proposed merger is sound. We believe the merger would enhance the overall competitive position of the companies, improve their ability to serve a broader range of clients, create an extensive offering of products and solutions and establish a stronger platform for growth and future investments.” Glass Lewis November 5, 2015 “[W]e recognize the strategic merit of the merger and the potential to achieve greater financial performance than either company could on its own in the long term.” Glass Lewis November 5, 2015 “[T]he potential long-term benefits of the deal appear compelling…” ISS November 5, 2015 “[I]ntegrating the [exchange] product with a powerful distribution system is more critical than a backward-looking analysis of growth rates can convey.” ISS November 5, 2015 “We believe the combination of the two firms will create strong long-term strategic value that outpaces what either firm on a standalone basis can achieve, including generation of material revenue, cost and tax synergies.” Piper Jaffray November 6, 2015 Analysts & Proxy Advisors Views (1) Permission to used quoted material was neither sought nor obtained; emphasis added. ( ¹ ) |

4 Projected to Generate Substantial Growth and Shareholder Value Merger expected to generate $4.7 billion in value from highly-achievable synergies Clearly identified cost, revenue and tax synergies » $375 - $675 million in revenue synergy opportunity » $100 - $125 million in clearly defined cost synergies » Maintain Irish domicile; achieve effective tax rate in mid-20 percent range vs. current mid- 30 percent range ($75 million estimated impact) Synergy estimates are a result of deep diligence by TW, Willis, and third-party consultants based on our detailed understanding of the businesses Substantially accretive to TW shareholders » Cash Net Income accretion expected to be >25% for CY 2016 and increase to 45% for CY 2018 “We believe the pending merger with Willis has the potential to unlock significant shareholder value, including an accelerated adoption curve for private exchange solutions leveraging channel synergies from Willis' middle market strength. Additionally, we identify strategic value from the combination in the form of enhanced TW international growth and expanded Willis U.S. P&C growth. We view the $125M in cost synergies and $75M in tax savings as highly achievable, and potentially conservative.” Piper Jaffray November 2, 2015 “Acquisition cost synergies are probably understated by $50M-$75M. Company is guiding to $100M-$125M in 2-3 years. We note that it achieved about $110M in synergies from the Towers Perrin acquisition – which was half the size of this deal.” Stifel July 1, 2015 “[W]e recognize the strategic merit of the merger and the potential to achieve greater financial performance than either company could on its own in the long term.” Glass Lewis November 6, 2015 “[A] combined entity would benefit from certain factors, including cost synergies and the potential revenue opportunity of better mating Towers' healthcare exchange with Willis' distribution network.” ISS November 6, 2015 “[W]e’re more focused at this point on the bigger prize. The material accretion associated with the WSH deal, where CY16 EPS of $8.25.” Citi August 12, 2015 Analysts & Proxy Advisors Views (1) Permission to used quoted material was neither sought nor obtained; emphasis added. ( ¹ ) |

5 Balanced Ownership Stake for TW Shareholders TW ownership split is favorable when viewed against historical trading and internal earnings projections. Source: Towers Watson and Willis Group standalone projections per S-4 filing and FactSet. Note: Market data from FactSet as of June 29, 2015. (1) Based on Pro Forma Fully Diluted Ownership. Towers Watson pro forma market capitalization adjusted for special one-time dividend of $337mm (2) Operational Improvement Spending of $124mm in 2016E, $128mm in 2017E and $0mm in 2018E per projections by Willis management. Willis standalone tax rate of 24.5% in 2016E, 24.0% in 2017E and 23.5% in 2018E. Implied TW Equity Ownership Implied WSH Equity Ownership Final Pro Forma Ownership - Higher/(Lower) Market Cap Basis Market Cap (60-day Average Ended 6/05/15) (1) 49.9% 50.1% - Market Cap (180-Day Average Ended 6/05/15) (1) 49.4% 50.6% + 0.5% Market Cap (1-year average Ended 6/05/15) (1) 48.9% 51.1% + 1.0% Market Cap (Based on 6/29/15) (1) 52.7% 47.3% (2.8)% Cash Net Income - Excluding Willis Operational Improvement Expense CY2016E Cash Net Income 43.5% 56.5% + 6.4% CY2017E Cash Net Income 41.5% 58.5% + 8.4% CY2018E Cash Net Income 40.7% 59.3% + 9.2% Cash Net Income - Including Willis Operational Improvement Expense (2) CY 2016E (2) 47.6% 52.4% + 2.3% CY 2017E (2) 45.1% 54.9% + 4.8% CY 2018E (2) 40.7% 59.3% + 9.2% Final Pro Forma Ownership 49.9% 50.1% - Contribution Analysis |

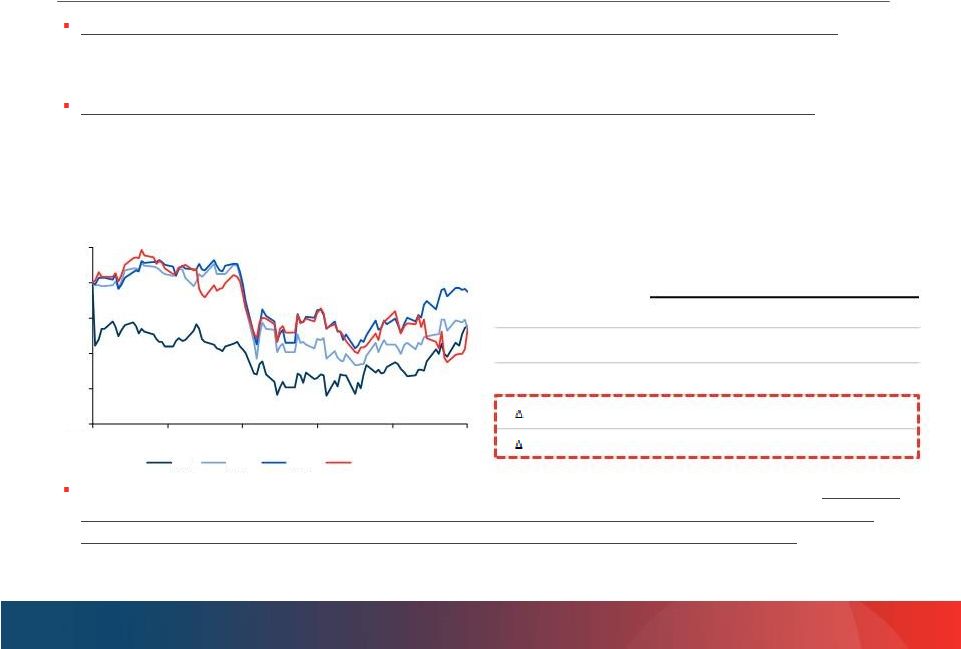

6 TW has Outperformed Industry Peers Since Announcement Purported underperformance relative to peers is driven solely by Marsh & McLennan Companies (MMC) – the broader peer group represents a more accurate benchmark for performance » MMC is significantly larger than Towers Watson and does not represent a pure-play comparable TW has actually outperformed peers ( ¹ ) since announcement – demonstrating investor support » TW management has spent significant time with its shareholders since announcement providing additional detail on the strategic fit and value creation potential of the transaction » We believe this engagement has generated significant shareholder support and driven recent outperformance relative to our peers In mergers, initial market reaction to a value-creating transaction may be negative – for instance, there was a ~8% decline in stock price on announcement of the 2009 Towers Perrin / Watson Wyatt transaction, although this transaction drove TW returns >20% in excess of peers post-transaction to date (1) Peers include Accenture, Advisory Board Company, Aon, The Corporate Executive Board, FTI, Huron Consulting, and MMC (2) Market data per FactSet; represents stock price performance from indicated start date through November 6, 2015 Indexed Share Price Performance (1) 80 85 90 95 100 105 6/29/15 7/25/15 8/20/15 9/15/15 10/11/15 11/6/15 TW AON MMC Peer Average Day Prior to Announcement (6/29 to Present) (2) Day of Announcement to Present (6/30 to Present) (2) Average TW Peers (1) (6.5%) (11.4%) Median TW Peers (1) (6.5%) (14.1%) Towers Watson (6.2%) (1.8%) vs. Peer Average 0.3% 9.6% vs. Median Average 0.3% 12.3% |

7 Proven Ability to Realize Benefits of the Merger Strong continuing management team increases the likelihood of successfully integrating and capturing synergies » The Chief Executive Officer, Chief Financial Officer, most of the business leaders and independent directors will continue to have important roles with the combined company TW has a proven record of delivering shareholder value in highly successful Towers Perrin/Watson Wyatt merger » Towers Watson shares up 214.4% since announcement » Achieved $110 million in pretax annual cost synergies – $30 million in excess of the initially anticipated amount Willis Towers Watson will benefit from the key elements that drove the success of the Watson Wyatt/Towers Perrin merger: » Transition of management team and Board members » Robust integration discipline » Properly aligned management incentives with shareholder’s interest Analysts & Proxy Advisors Views “[W]e also acknowledge that Towers Watson management has a track record of delivering shareholder value following a transformative transaction.” Glass Lewis November 5, 2015 “No one has questioned the wisdom of making Towers' CEO the head of the combined entity. In fact, several equity analysts have praised Haley's acquisition track record – noting that the market has at first underestimated certain transactions he has overseen.” ISS November 5, 2015 “Over the 15 years we have followed TW there have been a number of acquisitions that CEO John Haley has stewarded that were initially underappreciated -- including the key Towers Perrin merger and Extend Health acquisition to enter the private exchange space.” Baird Equity Research June 30, 2015 “Towers Watson management has an appropriate perspective on the value that will emerge at Willis as it executes on its Operational Improvement Program. The market clearly didn't see this in the immediate aftermath of the announcement, but it reflects good long-term thinking.” Keefe, Bruyette & Woods October 9, 2015 “The Willis merger represents a catalyst for upside in exchange revenue growth given increased penetration of the middle market channel. Additionally, we expect the deal to generate run-rate pre-tax cost synergies of $125M and tax synergies of $60M. Finally, we believe Towers’ management team can bring enhanced execution to Willis, driving a positive turnaround in the insurance business.” Piper Jaffray August 11, 2015 (1) Permission to used quoted material was neither sought nor obtained; emphasis added. (2) Source: FactSet dates from June 28, 2009 to November 6, 2015. ( ¹ ) (2) |

8 Transaction was a Result of a Thorough, Independent Process Extensive Evaluation by an Engaged, Independent Board Independent Directors played a significant role in evaluating the transaction and oversaw multiple meetings and executive sessions throughout the evaluation and negotiation process Board extensively reviewed the assumptions underlying the value-creation thesis of the Willis transaction, including internal and external perspectives on revenue, cost and tax synergies Board considered alternative transaction structures, but determined that the merger-of-equals structure was the optimal way to leverage the strengths of both businesses No market check was run due to Board, management and advisor judgment regarding lack of strategic interest, which has been validated post-announcement given that no other interested party has indicated interest or submitted a proposal Board concluded the potential value of the combined company is more compelling than standalone plan, since it provides a unique opportunity for TW to benefit from the upside created through broadened product offerings, client reach, and geographic scope “In our opinion, the proposed merger is the result of a thorough review of strategic alternatives. Towers Watson's evaluation of a potential combination with Willis involved various members of management, independent directors and external business, financial and legal advisors, all of whom assessed aspects of the potential value creation opportunities, the cultural compatibility and the strategic and financial implications of the proposed transaction.” - Glass Lewis, November 5, 2015 (1) Permission to used quoted material was neither sought nor obtained; emphasis added. ( ¹ ) |

9 The Towers Watson Board of Directors urges shareholders to vote FOR the transaction at our upcoming meeting on November 18, 2015 Compelling strategic rationale Significant value creation from clearly-identified cost, tax and revenue synergies Favorable MOE transaction structure Rigorous Board evaluation of merger Strong continuing leadership, with proven MOE execution and integration experience |

10 Where You Can Find Additional Information In connection with the proposed merger of Towers Watson and Willis Group, Willis Group filed a registration statement on Form S-4 with the Securities and Exchange Commission (the “Commission”) that contains a joint proxy statement/prospectus and other relevant documents concerning the proposed transaction. The registration statement on Form S-4 was declared effective by the SEC on October 13, 2015. Each of Towers Watson and Willis Group mailed the joint proxy statement/prospectus to its respective stockholders on or around October 13, 2015. YOU ARE URGED TO READ THE JOINT PROXY STATEMENT/PROSPECTUS AND THE OTHER RELEVANT DOCUMENTS THAT HAVE BEEN OR WILL BE FILED WITH THE COMMISSION AS THEY BECOME AVAILABLE BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION ABOUT TOWERS WATSON, WILLIS GROUP AND THE PROPOSED TRANSACTION. You may obtain the joint proxy statement/prospectus and the other documents filed with the Commission free of charge at the Commission’s website, www.sec.gov. In addition, you may obtain free copies of the joint proxy statement/prospectus and the other documents filed by Towers Watson and Willis Group with the Commission by requesting them in writing from Towers Watson, 901 N. Glebe Road, Arlington, VA 22203, Attention: Investor Relations, or by telephone at (703) 258-8000, or from Willis Group, Brookfield Place, 200 Liberty Street, 7th Floor, New York, NY 10281-1003, Attention: Matt Rohrman, Investor Relations, or by telephone at (212) 915-8084. |

11 Forward Looking Statements This document contains “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. You can identify these statements and other forward-looking statements in this document by words such as “may”, “will”, “would”, “expect”, “anticipate”, “believe”, “estimate”, “plan”, “intend”, “continue”, or similar words, expressions or the negative of such terms or other comparable terminology. These statements include, but are not limited to, the benefits of the business combination transaction involving Towers Watson and Willis Group, including the combined company’s future financial and operating results, plans, objectives, expectations and intentions and other statements that are not historical facts. Such statements are based upon the current beliefs and expectations of Towers Watson’s and Willis Group’s management and are subject to significant risks and uncertainties. Actual results may differ from those set forth in the forward-looking statements. The following factors, among others, could cause actual results to differ from those set forth in the forward-looking statements: the ability to obtain governmental approvals of the transaction on the proposed terms and schedule; the failure of Towers Watson stockholders and Willis Group shareholders to approve the transaction; the failure of the transaction to close for any reason; the risk that the businesses will not be integrated successfully; the risk that anticipated cost savings and any other synergies from the transaction may not be fully realized or may take longer to realize than expected; the potential impact of the announcement or consummation of the proposed transaction on relationships, including with employees, suppliers, customers and competitors; changes in general economic, business and political conditions, including changes in the financial markets; significant competition; compliance with extensive government regulation; the combined company’s ability to make acquisitions and its ability to integrate or manage such acquired businesses. Additional risks and factors are identified under “Risk Factors” in Towers Watson’s Annual Report on Form 10-K filed on August 14, 2015, which is on file with the Commission, and under “Risk Factors” in the joint proxy statement/prospectus. You should not rely upon forward-looking statements as predictions of future events because these statements are based on assumptions that may not come true and are speculative by their nature. Neither Towers Watson or Willis Group undertakes an obligation to update any of the forward-looking information included in this document, whether as a result of new information, future events, changed expectations or otherwise. |