UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE

SECURITIES EXCHANGE ACT OF 1934

For the month of April, 2019

Commission File Number: 001-34476

BANCO SANTANDER (BRASIL) S.A.

(Exact name of registrant as specified in its charter)

Avenida Presidente Juscelino Kubitschek, 2041 and 2235

Bloco A – Vila Olimpia

São Paulo, SP 04543-011

Federative Republic of Brazil

Bloco A – Vila Olimpia

São Paulo, SP 04543-011

Federative Republic of Brazil

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:Form 20-F ___X___ Form 40-F _______

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes _______ No ___X____

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes _______ No ___X____

Indicate by check mark whether by furnishing the information contained in this Form, the Registrant is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934:

Yes _______ No ___X____

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): N/A

SUMMARY |

|

|

| Pages |

Performance Review | 1 | |

Financial Statements | ||

Balance Sheets | 19 | |

Income Statements | 23 | |

Statements of Changes in Stockholders' Equity – Bank | 24 | |

Statements of Changes in Stockholders' Equity - Consolidated | 27 | |

Cash Flows Statements | 30 | |

Statements of Value Added | 31 | |

Notes to the Financial Statements | ||

Provisions, Contingent Assets and Liabilities and Legal Obligations - Tax and Social Security | ||

| ||

Executive’s Report of Financial Statements | 113 | |

Executive’s Report of Independent Auditors' Report | 114 | |

Individual and Consolidated Financial Statements – March 31, 2019

(Free Translation into English from the Original Previously Issued in Portuguese) | |

| BANCO SANTANDER (BRASIL) S.A. AND SUBSIDIARIES |

PERFORMANCE REVIEW | |

In thousands of Brazilian Real - R$, unless otherwise stated | |

Dear Stockholders:

We present the Performance Review to Individual and Consolidated Financial Statements of Banco Santander (Brasil) S.A. (Banco Santander or Bank) related to the period ended March 31, 2019, prepared in accordance with accounting practices set by Brazilian Corporate Law, the standards of the National Monetary Council (CMN), the Central Bank of Brazil (Bacen) and document template provided by the Accounting National Financial System Institutions (Cosif) and the Brazilian Exchange Commission (CVM), that does not conflict with the rules issued by Bacen.

The Condensed Financial Statements in accordance with the International Accounting Standards Board (IASB) for the period ended March 31, 2019, will be disclosed simultaneously, on the website www.santander.com.br/ri.

1) Macroeconomic Environment

In general, prices of Brazilian financial assets ended the first quarter of 2019 at better levels than the ones registered at the end of 2018. The exception was the exchange rate, which weakened marginally versus the US dollar (approximately0.6%). However, it is important to notice that price dynamics of all assets followed a similar pattern during the period, as they reached levels that were more favorable in the beginning of first quarter than the ones in its end. That is, the year started with a generalized improvement trend in prices of Brazilian financial assets, which was followed by some profit-taking moves as months went by. In most cases – as stated before – the price correction was not enough to reverse the improvement observed in early 2019. Nonetheless, the performance of Brazilian financial asset prices could have been better than the one registered. Santander considers that both domestic and international factors influenced such a trajectory recorded by the Brazilian financial asset prices in the first three months of 2019.

From the international standpoint, the Bank understands that the aggravation of tensions derived from the so-called “Trade War” between China and the US played an important role in the reversal of Brazilian financial asset prices – as the imbroglio may bring collateral damage to all economies in the globe, including the Brazilian one. Besides, Santander remembers that additional evidences indicating that both Chinese and US economies may go through a more intense economic slowdown than previously anticipated by market participants raised concerns among international investors and increased their levels of risk aversion – a backdrop that put pressure over both the Brazilian exchange rate as well prices of its credit-default-swaps. The Bank also thinks it is important to highlight that two developments reinforced the general perception that world economy should face a protracted period of slow economic growth. Namely, a) the imbroglio related to the conclusion of the Brexit – the process of departure of United Kingdom from the European Union – and; b) signals conveyed by the European Central Bank that it would push forward the deadline for granting monetary stimulus to that economy. According to Santander’s appraisal, less auspicious perspectives for the world economy also contributed to the reversal of Brazilian financial asset prices.

As for the domestic environment, the beginning of 2019 was marked by the inauguration of a new federal administration, a factor that reinforced the process of recovery in confidence indicators – both entrepreneurs and consumer ones – which nurtured a climate of optimism among market participants regarding the approval of structural reforms the country needs. In the Bank’s view, these were the reasons behind the substantial improvement observed in the Brazilian financial asset prices in the beginning of the first quarter of 2019. However, as the complexity to get reforms in place became clearer and clearer – difficult negotiations with a very fragmented Congress, difficulties in the initial organization of the new Government, people’s anxiety with fast and concreted deeds, etc – the enthusiasm dwindled and was replaced by caution. In the wake of this mood change, Santander understands that the unfolding of a profit-taking process was something natural, but the Bank considers that the magnitude of price changes should not be considered as an indication of a critical situation.

On top of the on the political front observed, the Bank also verified a new round of frustration with regard to the performance of activity indicators, which provoked a wave of downward reviews in the forecasts for the GDP growth for 2019. Santander ended up recalculating its own projection for the performance of the Brazilian economy during this year and, instead of counting on a 3.0% expansion for the GDP in 2019, now the Bank considers that the most likely scenario is for a 2.3% growth this year. The maintenance of a gradual recovery reinforced favorable dynamics for price indices, with underlying inflation gauges signaling at plenty of room for the Brazilian Central Bank to meet the targets set by the National Monetary Council for the coming years. Consequently, the Bank believed it was created additional maneuvering-room for the Brazilian monetary authority to keep the base interest rate unchanged at the current level of 6.50% pa, without jeopardizing its duty of keeping inflation dynamics compatible with the convergence of current inflation toward targeted levels. As a result, Santander thinks the Selic target rate is likely to remain unchanged until the end of 2020 – previously the expectation was that the base interest rate would stay put until mid-2020.

These forecasts for economic growth, inflation and low interest rate that Santander works with are based upon the assumption that the country will continue to pursue an agenda of structural reforms, mainly on the fiscal front. The Santander restates that the willingness and commitment of the newly-instated administration in pursuing the improvement of the fiscal balance, as well as in keeping sustainable and sensible economic policy guidelines are going to be crucial for allowing the country to reach out social and economic development over time.

2) Performance

2.1) Corporate Net Income

Individual and Consolidated Financial Statements – March 31, 2019 1

CONSOLIDATED INCOME STATEMENTS |

|

|

| 1Q19 | 1Q18 | annual changes% |

Financial Income |

|

|

| 20,550.5 | 19,190.3 | 7.1 |

Financial Expenses |

|

|

| (12,556.6) | (11,932.5) | 5.2 |

Gross Profit From Financial Operations (a) |

|

|

| 7,993.9 | 7,257.8 | 10.1 |

Other Operating (Expenses) Income (b) |

|

|

| (2,642.4) | (2,416.1) | 9.4 |

Operating Income |

|

|

| 5,351.5 | 4,841.7 | 10.5 |

Non-Operating Income |

|

|

| 0.5 | 12.6 | -96.2 |

Income Before Taxes on Income and Profit Sharing |

|

|

| 5,352.0 | 4,854.2 | 10.3 |

Income Tax and Social Contribution (a) |

|

|

| (1,376.1) | (1,484.9) | -7.3 |

Profit Sharing |

|

|

| (468.4) | (466.3) | 0.5 |

Non-Controlling Interest |

|

|

| (92.0) | (83.3) | 10.5 |

Consolidated Net Income |

|

|

| 3,415.4 | 2,819.7 | 21.1 |

Excludes goodwill amortizations expenses |

|

|

| 69.8 | 69.4 | 0.6 |

Net Income Excluding Goodwill Amortization |

|

|

| 3,485.2 | 2,889.1 | 20.6 |

For a better understanding of the results in BRGAAP, below is the Gross Profit from Financial Operations, disregarding the hedge effect (according to item 1):

ADJUSTED GROSS PROFIT FROM FINANCIAL OPERATIONS |

|

|

| 1Q19 | 1Q18 | annual changes% |

Gross Profit From Financial Operations |

|

|

| 7,993.9 | 7,257.8 | 10.1 |

Income Tax and Social Contribution (hedge) |

|

|

| 152.8 | 150.5 | 1.6 |

Adjusted Gross Profit From Financial Operations |

|

|

| 8,146.7 | 7,408.3 | 10.0 |

INCOME TAX AND SOCIAL CONTRIBUITION |

|

|

| 1Q19 | 1Q18 | annual changes% |

Income Tax and Social Contribution |

|

|

| (1,376.1) | (1,484.9) | -7.3 |

Income Tax and Social Contribution (hedge) |

|

|

| (152.8) | (150.5) | 1.6 |

Adjusted Income Tax and Social Contribution |

|

|

| (1,528.9) | (1,635.4) | -6.5 |

a) Foreign Exchange Hedge of the Grand Cayman and Luxembourg Branches and the Subsidiary Santander Brasil EFC

Banco Santander operates branches in the Cayman Islands and Luxembourg and the subsidiary Santander Brasil Establecimiento Financiero de Credito, EFC, or “Santander Brasil EFC” which are used, mainly, to raise funds in the capital and financial foreign markets, providing credit lines that are extended to clients for trade-related financings and working capital. To protect the exposures to foreign exchange rate variations, the Bank uses derivatives. According to Brazilian tax rules, the gains or losses resulting from the impact of appreciation or depreciation of the local currency (Real) in foreign investments are nontaxable to PIS/Cofins/IR/CSLL, while gains or losses from derivatives used as hedges are taxable or deductible. The purpose of these derivatives is to protect the after-tax net income.

The different tax treatment of such foreign exchange rate differences results in a volatility on the operational earnings or losses and on the gross revenue tax expense (PIS/Cofins) and income taxes (IR/CSLL), as demonstrated below:

FOREIGN EXCHANGE HEDGE OF THE GRAND CAYMAN AND LUXEMBOURG BRANCHS |

|

|

| 1Q19 | 1Q18 | annual changes% |

Exchange Variation - Profit From Financial Operations |

|

|

| 225.5 | 183.9 | 22.6 |

Derivative Financial Instruments - Profit From Financial Operations |

|

|

| (396.8) | (350.7) | 13.1 |

Income Tax and Social Contribution |

|

|

| 152.8 | 150.5 | 1.6 |

PIS/Cofins - Tax Expenses |

|

|

| 18.4 | 16.3 | 13.1 |

b) Other Operating (Expenses) Income

Fees - The highlights are: (a) credit/debit card commission and Acquiring Services, with growth of 20.0% in relation to the same period of the previous year, mainly due to the increase in both card and acquirer services; (b) Current Account Services, an increase of 14.0% in relation to the same period of the previous year, influenced by the increase in the number of active account holders, which grew 43 consecutive months ; and (c) Insurance Commissions, with an increase of 11.6% in relation to the same period of the previous year, following the credit dynamics.

Individual and Consolidated Financial Statements – March 31, 2019 2

Fees |

|

|

| 1Q19 | 1Q18 | annual changes% |

Asset Management |

|

|

| 250.8 | 251.6 | -0.3 |

Checking Account Services |

|

|

| 909.5 | 797.6 | 14.0 |

Lending Operations and Income from Guarantees Provided |

|

|

| 324.3 | 385.5 | -15.9 |

Lending Operations |

|

|

| 189.6 | 229.0 | -17.2 |

Income Guarantees Provided |

|

|

| 134.7 | 156.5 | -13.9 |

Insurance Fees |

|

|

| 739.2 | 662.1 | 11.6 |

Cards (Debit and Credit) and Acquiring Services |

|

|

| 1,608.9 | 1,340.2 | 20.0 |

Collection |

|

|

| 375.4 | 373.4 | 0.5 |

Brokerage, Custody and Placement of Securities |

|

|

| 191.7 | 161.5 | 18.7 |

Others |

|

|

| 129.0 | 162.4 | -20.6 |

Total |

|

|

| 4,528.8 | 4,134.3 | 9.5 |

General Expenses - Total expenses, which include expenses with personnel, other administrative expenses and expenses with profit sharing, excluding the effects of goodwill amortization, increased by 6.2%, and personnel expenses and profit sharing, increased by 0.4% and other administrative expenses increased by 11.5%, all compared to same period of 2017. Changes in administrative expenses are mainly due to the increase in expenses with data processing, associated with greater transactionality and growth in the customer base and expenses with specialized technical services and third parties, mainly through the contracting of technology services.

General Expenses |

|

|

| 1Q19 | 1Q18 | annual changes% |

Personnel Expenses |

|

|

| (2,319.0) | (2,308.9) | 0.4 |

Other Administrative Expenses, excluding the effects of goodwill amortization |

|

|

| (2,783.1) | (2,496.5) | 11.5 |

General Expenses, excluding the effects of goodwill amortization |

|

|

| (5,102.1) | (4,805.4) | 6.2 |

2.2) Assets and Liabilities

CONSOLIDATED BALANCE SHEETS |

|

| Mar/19 | Dec/18 | mar/19 vs. dec/18 changes % |

Current and Long-Term Assets |

|

| 791,370.8 | 794,664.0 | -0.4 |

Permanent Assets |

|

| 12,308.3 | 11,155.3 | 10.3 |

TOTAL ASSETS |

|

| 803,679.2 | 805,819.3 | -0.3 |

Current and Long-Term Liabilities |

|

| 733,277.6 | 738,178.6 | -0.7 |

Deferred Income |

|

| 318.8 | 337.0 | -5.4 |

Non-Controlling Interest |

|

| 1,883.3 | 2,069.9 | -9.0 |

Stockholders' Equity |

|

| 68,199.5 | 65,233.7 | 4.5 |

TOTAL LIABILITIES AND STOCKHOLDERS' EQUITY |

|

| 803,679.2 | 805,819.3 | -0.3 |

Total assets are mainly represented:

(R$ Millions) |

|

| Mar/19 | Dec/18 | mar/19 vs. dec/18 changes % |

Loan Portfolio |

|

| 310,714.3 | 305,259.7 | 1.8 |

Securities and Derivative Financial Instruments (1) |

|

| 195,477.2 | 194,464.7 | 0.5 |

Interbank Investments |

|

| 33,631.7 | 56,812.2 | -40.8 |

Interbank Accounts |

|

| 91,670.8 | 92,442.6 | -0.8 |

(1) Given the provisions of Circular Bacen 3,068/2001, Banco Santander has the financial capacity and intention to hold to maturity, securities classified as held-to-maturity, in the amount of R$11,301.9 million onMarch 31, 2019 (12/31/2018 - R$11,256.3 million).

2.3) Loan Portfolio

MANAGEMENT DISCLOSURE OF LOAN PORTFOLIO BY SEGMENT |

|

| Mar/19 | Dec/18 | mar/19 vs. dec/18 changes % |

Individuals (1) |

|

| 136,555.8 | 132,564.9 | 3.0 |

Consumer Finance |

|

| 51,421.3 | 50,066.4 | 2.7 |

Individuals (1) |

|

| 45,263.8 | 43,785.4 | 3.4 |

Corporate |

|

| 6,157.5 | 6,281.0 | -2.0 |

Small and Medium-sized Entities |

|

| 35,839.1 | 35,770.0 | 0.2 |

Large-sized Entity |

|

| 86,898.1 | 86,858.4 | 0.0 |

Total Loan portfolio (gross) |

|

| 310,714.3 | 305,259.7 | 1.8 |

Other Operations with Credit Risk |

|

| 76,189.5 | 81,476.1 | -6.5 |

Total Extended Portfolio (gross) |

|

| 386,903.8 | 386,735.8 | 0.0 |

Allowance for Loan Losses (2) |

|

| (18,700.0) | (18,789.1) | -0.5 |

Total Loan portfolio (net) |

|

| 368,203.8 | 367,946.7 | 0.1 |

(1) Including the loans to individual in the consumer finance segment, the individual portfolio reached R$181,819.6 on March 31, 2019 (12/31/2018 – R$176,350.3).

(2) Includes debentures, FIDC, CRI, promissory notes, promissory notes for placement abroad, assets related to acquiring activities and sureties and sureties.

Individual and Consolidated Financial Statements – March 31, 2019 3

On March 31, 2019, the main highlights were the following segments: (a) "Individuals", which presented growth in both comparison periods, 3.0% compared to December 31, 2018, influenced mainly by the payroll growth, due to the good adherence of the digital channels by the customers and strong commercial dynamics of the network; (b) "Consumer Finance", also with growth in both periods, being 2.7% compared to December 2018; (c) “Small and Medium Companies”, with decrease of 4.5% compared to December 2018, relating to balance transfer onportfolio between the segments small and medium companies and large companies, according with the income adjustment of certain customers, and the seasonality period. The performance of this portfolio can be attributed in parts by platform + Business, focused on vehicles segment.

Delinquency

The over-90 delinquency ratio reached 3.1% of the total credit portfolio on March 31, 2019, remaining stable in relation to December 31, 2018 (3.1%). The ratio remains at a controlled level, as a result of the risk management and assertive models of Banco Santander.

Allowance for loan losses represents 6.0% of the loan portfolio on March 31, 2019, 6.2% on December 31, 2018.

The allowance for loan losses expenses, net of revenues with recovery of loans previously written off for the period ended on March 31, 2019 isR$2,567.7 million andR$2,738.7 million in 2018, increasing 6.2%.

2.4) Funding by Customers

FUNDING BY CUSTOMERS |

|

| Mar/19 | Dec/18 | mar/19 vs. dec/18 changes % |

Demand Deposits |

|

| 17,939.8 | 18,831.6 | -4.7 |

Saving Deposits |

|

| 46,211.2 | 46,068.3 | 0.3 |

Time Deposits |

|

| 185,095.9 | 184,098.3 | 0.5 |

Debentures/LCI/LCA/LIG (1) |

|

| 48,954.5 | 46,366.1 | 5.6 |

Treasury Bills/Structured Operations Certificates |

|

| 38,080.5 | 36,889.3 | 3.2 |

Total Funding |

|

| 336,281.9 | 332,253.7 | 1.2 |

(1) Debentures repurchase agreement, Real Estate Credit Notes (LCI), Agribusiness Credit Notes (LCA) and Guaranteed Real State Credit Notes (LIG).

The total funding resources increased 1.2%, compared toDecember 2018, with steady and more pronounced Time Deposit growth in Debentures.

2.5) Issuance of Debt Instruments Eligible to Compose Capital

On November 5, 2018, the Board of Directors approved the issuance of the equity instruments, which was held on November 8, 2018. Such issuance was in the form of Notes issued in US dollars, US$2,5 Billion, for payment in Tier I and Tier II of Reference Equity. The offer of these notes was made outside Brazil and the United States of America, for non-US Persons, based on Regulation S under the Securities Act, and was fully paid in by SantanderSpain, controlling shareholder of Banco Santander Brasil. On the same date, the Board of Directors approved the redemption of the Tier I and Tier II notes issued on January 29, 2014, in the total amount of U$ 2,5 billion.

The specific characteristics of Notes issued to make up Tier I are: (a) Principal: US$1,250 Billion (b) Interest Rate: 7.25% p.a; (c) no maturity (perpetual); (d) Periodicity of payment of interest: semiannually from May 8, 2019.

The specific characteristics of Notes issued to make up Tier II are: (a) Principal: US $ 1,250 Billion; (b) Interest Rate: 6.125% p.a.; (c) Maturity Term: on November 8, 2028; and (d) Periodicity of payment of interest: semiannually, as of May 8, 2019.

Notes have the following common characteristics:

(a) Unit value of at least US$150 thousand and in integral multiples of US$1 thousand in excess of such minimum value.

Individual and Consolidated Financial Statements – March 31, 2019 4

(b) The Notes may be repurchased or redeemed by Banco Santander after the fifth anniversary as of the date of issue of the Notes, at the sole discretion of the Company or as aresult of changes in the tax legislation applicable to the Notes; or at any time, due to the occurrence of certain regulatory events.

On December 18, 2018, the Bank issued an approval for the Notes to comprise Tier I and Tier II of Banco Santander's Referential Equity, as of that date, as well as the repurchase of the notes issued on January 29, 2014.

2.6) Stockholders’ Equity

On March 31, 2019, Banco Santander consolidated stockholders’ equity presented an increase of 4.5% compared to December, 2018.

The variation in the Stockholders' Equity balance between March 31, 2019 and 2018 was, mainly, due to the negative variation of the asset valuation adjustment (securities and derivative financial instruments) in the amount of R$648.3 million and the net income for the period in the amount of R$3,514.4 million and reduced, mainly, by the established of Interest on Capital in the amount of R$1 billion.

Treasury Shares

In the meeting held on November 1, 2018, the Bank’s Board of Directors approved, in continuation of the buyback program that expired on November 1, 2017, the buyback program of its Units and ADRs, by the Bank or its agency in Cayman, to be held in treasury or subsequently sold.

The Buyback Program will cover the acquisition up to 37,753,760 Units, representing 37,753,760 common shares and 37,753,760 preferred shares, or the ADRs, which, on December 31, 2018, corresponded to approximately 1% of the Bank’s share capital. On December 31, 2018, the Bank held 362,227,661 common shares and 390,032,076 preferred shares being traded.

The Buyback has the purpose to (1) maximize the value creation to stockholders by means of an efficient capital structure management; and (2) enable the payment of officers, management level employees and others Bank’s employees and companies under its control, according to the Long Term Incentive Plans. The term of the Buyback Program is 12 months counted from November 6, 2018, and will expire on November 5, 2019.

|

|

|

| Mar/19 | Dec/18 |

|

|

|

| Quantity | Quantity |

|

|

|

| Units | Units |

Treasury shares at beginning of the fiscal year |

|

|

| 13,317 | 1,773 |

Shares Acquisitions |

|

|

| 3,338 | 15,816 |

Payment - Share-based compensation |

|

|

| (3,026) | (4,272) |

Treasury shares at end of the fiscal year |

|

|

| 13,629 | 13,317 |

Subtotal - Treasury Shares in thousands of reais |

|

|

| R$ 520,267 | R$ 460,550 |

|

|

|

| R$ 2,410 | R$ 882 |

Balance of Treasury Shares in thousands of reais |

|

|

| R$ 522,677 | R$ 461,432 |

Cost/Share price |

|

|

| Units | Units |

Minimum cost |

|

|

| R$ 7.55 | R$ 7.55 |

Weighted average cost |

|

|

| R$ 30.69 | R$ 28.59 |

Maximum cost |

|

|

| R$ 49.55 | R$ 43.84 |

Share price |

|

|

| R$ 43.97 | R$ 42.70 |

In the period ended March 31, 2019 and 2018, there were highlights of Interest on Capital, as below:

DIVIDENDS AND INTEREST ON CAPITAL |

|

|

| Mar/19 | Mar/18 |

Interest on capital |

|

|

| 1,000.0 | 600.0 |

Total |

|

|

| 1,000.0 | 600.0 |

2.7) Basel Index

Financial institutions are required by Bacen to maintain Regulatory Capital (PR), Tier I and Principal Capital consistent with their risk activities, higher than the minimum requirement of the Regulatory Capital Requirement, represented by the sum of the partial credit risk, market risk and operational risk.

As required by Resolution CMN 4,193/2013, the requirement for PR in 2018 was 11.0%, composed of 8.625% of Reference Equity Minimum plus 1.875% of Capital Conservation Additional. Considering this additional, PR Level I increased to 8.375% and Minimum Principal Capital to 6.875%.

Individual and Consolidated Financial Statements – March 31, 2019 5

For the base year 2019, the PR requirement remains at 10.5%, including 8.0% of Minimum of Reference Equity and a further 2.5% of Capital Conservation Additional. The PR Level I reaches 8.5% and the Principal Capital Minimum 7.0%.

The Basel ratio is determined in accordance with the Financial Statements of the Prudential Conglomerate prepared in accordance with accounting practices adopted in Brazil, applicable to institutions authorized to operate by Bacen, as shown bellow:

BASEL INDEX % |

|

|

| Mar/19 | Dec/18 |

Tier I Regulatory Capital |

|

|

| 65,272.2 | 61,476.7 |

Principal Capital |

|

|

| 60,261.0 | 56,581.5 |

Supplementary Capital |

|

|

| 5,011.1 | 4,895.2 |

Tier II Regulatory Capital |

|

|

| 4,989.4 | 4,887.2 |

Regulatory Capital (Tier I and II) |

|

|

| 70,261.6 | 66,363.9 |

Credit Risk |

|

|

| 368,652.7 | 358,955.6 |

Market Risk |

|

|

| 40,200.4 | 39,231.8 |

Operational Risk |

|

|

| 46,527.0 | 42,375.6 |

Total RWA |

|

|

| 455,380.1 | 440,563.0 |

Basel I Ratio |

|

|

| 14.3 | 14.0 |

Basel Principal Capital |

|

|

| 13.2 | 12.8 |

Basel Regulatory Capital |

|

|

| 15.4 | 15.1 |

2.8) Main Subsidiaries

The table below presents the balances of total assets, net assets, net income and credit operations for the period ended March 31, 2019 for the main subsidiaries of Banco Santander portfolio:

SUBSIDIARIES | Total Assets | Stockholders' Equity | Net | Loan | Ownership / Interest (%) |

Aymoré Crédito, Financiamento e Investimento S.A. | 45,513.2 | 2,450.4 | 369.3 | 40,453.5 | 100.00% |

Getnet Adquirência e Serviços para Meios de Pagamento S.A. | 24,749.4 | 2,296.6 | 131.2 | 0.0 | 100.00% |

Santander Leasing S.A. Arrendamento Mercantil | 7,132.9 | 5,790.0 | 46.3 | 1,882.0 | 99.99% |

Banco Bandepe S.A. | 5,219.0 | 4,165.8 | 124.9 | 0.0 | 100.00% |

Santander Brasil, Establecimiento Financiero de Credito, S.A. | 3,597.3 | 3,432.3 | -0.5 | 1,570.5 | 100.00% |

Santander Corretora de Seguros, Investimento e Serviços S.A. | 2,830.9 | 2,665.7 | 107.9 | 0.0 | 100.00% |

Santander Corretora de Câmbio e Valores Mobiliários S.A. | 1,012.7 | 617.8 | 22.2 | 0.0 | 100.00% |

(1) Includes Leasing portfolio and other loans. ��

Balances reported above are in accordance with accounting practices established by Brazilian Corporate Law and standards established by the CMN, the Bacen and document template provided in the Accounting National Financial System Institutions (Cosif) and theCVM that does not conflict with the rules issued by Bacen, without disposal related party transactions.

3) Other Events

3.1) Post-employment Benefit Plan

On June 30, 2018, there was an increase in the cost contribution established in the Post-Employment Benefit Plan, which is calculated as a percentage of the total monthly compensation of members. The increase in the contribution resulted in a decrease in the past service cost, due to changes in the plan. The changes proposed in the Post-Employment Benefit imply a reduction in the present value of the obligations of the defined benefit plan, which is supported by actuarial valuations.

3.2) Recoverable Value Assessment

In the first half of 2018, Banco Santander recognized impairment losses in the amount of R$341 million on intangible assets in the acquisition and development of systems. The loss was recorded based on the performance of technical analysis, which demonstrated a significant reduction in expected future economic benefits on these assets.

3.3) Opening of the branch in Luxembourg

On June 9, 2017, Banco Santander obtained authorization from the Central Bank to set up an agency in Luxembourg with a capital of US $ 1 billion, with the objective of complementing the foreign trade strategy for corporate clients (large Brazilian companies and their operations abroad) and offer financial products and services through an offshore entity that is not established in a jurisdiction with favored taxation and that allows for the increase of funding capacity. The opening of the agency was authorized by the Luxembourg Minister of Finance on March 5, 2018. On April 3, 2018, after the reduction of the capital of the Cayman agency in the equivalent amount, the value of US$1 billion was allocated to capital of the Luxembourg branch.

Individual and Consolidated Financial Statements – March 31, 2019 6

3.4) Adhesion to Tax Debt Installment Programs

In October2017, the Bank also joined the Incentive Payment Programs and Installments issued by the cities Rio de Janeiro and São Paulo. Accessions to the programs include lawsuits and administrative proceedings related to ISS of the periods from 2005 to 2016, in the total amount of R$293 million. As a consequence were registered income of R$435 million.

Adherence to the program included administrative proceedings related to IRPJ, CSLL and Social Security Contributions referring to the base periods from 1999 to 2005, in the total of R$534 million, after the benefits of the installment program, ofwhich R$192 million was paid in August 2017 and R$300 million in January 2018.

3.5) Corporate Restructuring

Several social movements were implemented in order to reorganize the operations and activities of entities according to the business plan of the Conglomerate Santander.

a) Put option of equity interest in Banco Olé Bonsucesso Consignado S.A.

On March 14, 2019, the minority shareholder of Banco Olé Bonsucesso Consignado S.A. (Olé Consignado) formalized its interest to exercise the put option right provided in the Investment Agreement, executed on July 30, 2014, to sell its 40% equity interest in the capital stock of Olé Consignado to Aymoré CFI. The closing of the transaction is conditioned to implementation of the proceedings set forth in the Investment Agreement.

b) Acquisition of residual equity interest in Getnet S.A.

On December 19, 2018, Banco Santander and the Minority shareholders of Getnet S.A. executed an amendment to the Shares’ Sale and Purchase Agreement and Other Covenants of Getnet S.A., in which Banco Santander commits to acquire all of the Minority shareholders’ shares, corresponding to 11.5% of Getnet S.A. capital stock, per the amount of R$1,431,000. The acquisition was approved by Bacen on February 18, 2019 and closed on February 25, 2019, asa consequence, Santander Brasil has become the holder of 100% of the shares representatives of the capital stock of Getnet S.A.

c) Formation of Esfera Fidelidade S.A.

On August 14, 2018, Esfera Fidelidade was incorporated, with equity fully owned by Banco Santander. Esfera Fidelidade will act in the development and management of customer loyalty programs. On November 26, 2018, Esfera Fidelidade had its capital stock increased in the amount of R$10,000, amounting the full share capital of R$10,000, divided into 10,001,000 (ten million and one thousand) nominative common shares without par value, entirely held by Banco Santander. The company started its operation in November 2018.

d) Investment in Loop Gestão de Pátios S.A.

On June 26, 2018, Webmotors S.A., company with 70% interest indirectly owned by Banco Santander, signed an investment agreement with Allpark Empreendimentos, Participações e Serviços S.A. and Celta LA Participações S.A., in order to acquire an equity interest corresponding to 51% of the capital stock of Loop Gestão de Pátios S.A., through capital increase and issuance of new shares of Loop to be fully subscribed and paid-in by Webmotors. Loop operates in the segment of commercialization and physical and virtual auction of motor vehicles. On September 25, 2018, the transaction was completed with increase of the capital stock, in the amount of R$23,900, through issuance of shares representing 51% of equity interest in Loop, which were fully subscribed and paid-in by Webmotors.

e) Formation of BEN Benefícios e Serviços S.A.

On June 11, 2018,BEN Benefícios,with equity fully owned by Banco Santander,was incorporated, toact in the supply and administration of meal, food, transportation, cultural and similar vouchers, via printed or electronic and magnetic cards.

In the EGM held on August 1, 2018, BEN Benefícios had its capital increased in R$ 45,000, passing the capital stock to the amount of R$ 45,001, divided into 45,001,000 (forty-five million and one hundred thousand) registered common shares without par value, fully owned by Banco Santander.

In the EGM held on March 27, 2019, Santander Brasil approved the capital increase in the amount of R$44,999, totalizing R$90,000 of capital stock distributed into 90,000,000 (ninety million) common shares without par value, fully held by Santander Brasil.

BEN Benefícios started its activities in the first quarter of 2019.

f) Acquisition of Isban Brasil S.A. and Produban Serviços de Informática S.A.

On February 19 and 28, 2018, Banco Santander purchased, respectively, the totality of shares of Isban Brasil, formerly held by Ingeniería de Software Bancário, S.L., and of Produban Serviços de Informática, formerly held by Produban Servicios Informáticos Generales, S.L., for the amount of R$61,078 and R$42,731, respectively. The parties involved in the transactions had Banco Santander, S.A. (Santander Spain) as common indirect controller, being such transactions carried-out under market conditions. At the EGM held on February 19, 2018, was approved the capital increase of Isban Brasil in the amount of R$33,000, through the issuance of 11,783,900 (eleven million, seven hundred and eighty-three thousand and nine hundred) shares, without par value, entirely subscribed and paid in by Banco Santander. On February 28, 2018, the company Isban Brasil was merged into Produban Serviços de Informática S.A. and on the same date, Produban Serviços de Informática had its corporate name changed to Santander Brasil Tecnologia S.A. In continuity, on February 28, 2018, Produban Servicios Informáticos Generales, S.L. (currently named Santander Global Technology, S.L.) approved the merger of the spin-off share of Produban Serviços de Informática into Produban Brasil Tecnologia e Serviços de Informática Ltda. (currently named Santander Global Technology Brasil Ltda.).

Individual and Consolidated Financial Statements – March 31, 2019 7

g) Sale of equity interest in BW Guirapá I S.A.

On December 22, 2017, Santander Corretora de Seguros, Cia. de Ferro Ligas da Bahia - Ferbasa SA and Brazil Wind S.A. executed agreement for the sale of 100% of the shares issued by BW Guirapá I S.A. held by Santander Corretora de Seguros and Brazil Wind to Ferbasa. The basic price of the total sale was R$414,000, and an additional amount of up to R$35,000 may be paid if future targets stipulated in the Contract are met. As of January 1, 2018, this investment was written-off and, as a consequence, the assets and liabilities of BW Guirapá I and its subsidiaries were no longer consolidated by Banco Santander. On April 2, 2018, the transaction was concluded(Note 36).

h) Formation of Santander Auto S.A.

On December 20, 2017, Banco Santander and HDI Seguros S.A. (HDI Seguros), executed documents to form a partnership for the issuance, offering and sale of auto insurance, in a 100% digital way, through creation of a new insurance company - Santander Auto, to be held 50% by Sancap, a company controlled by Banco Santander, and 50% by HDI Seguros. On February 2, 2018 the partnership was approved by the Administrative Council of Economic Defense (Conselho Administrativo de Defesa Econômica – CADE), on April, 30, 2018, was approved by the Brazilian Central Bank and, on May, 15, 2018, SUSEP's prior approval was obtained. On October 9, 2018, through transformation of the corporate vehicle L.G.J.S.P.E. Investments and Participations S.A., Sancap and HDI Seguros formed Santander Auto S.A., with capital of R$15,000. On January 9, 2019, Susep granted to Santander Auto the authorization to operate insurance throughout national territory.

i) Formation of Gestora de Inteligência de Crédito S.A.

On April 14, 2017, the definitive documents necessary for the creation of a new credit bureau, Gestora de Inteligência de Crédito, were signed by the stockholders, whose control will be shared among the stockholders who will hold 20% of the its share capital each. In the EGM held on October 5, 2017, the capital increase of Gestora de Crédito was approved in the total amount of R$285,205, so that the capital stock increased from R$65,823 to R$351,028. The Company will develop a database with the objective of aggregating, reconciling and processing registration and credit information of individuals and legal entities, in accordance with the applicable standards, providing a significant improvement in the processes of granting, pricing and directing credit lines. The Bank estimates that the Company will be fully operational in 2019.

j) Formation of Banco Hyundai Capital Brasil S.A.

On April 28, 2016, Aymoré CFI and Banco Santander executed with Hyundai Capital Services, Inc. (Hyundai Capital) the necessary documents for the formation of Banco Hyundai and an insurance brokerage company with the purpose to provide, respectively, auto finance and financial and insurance brokerage services to clients and dealers of Hyundai in Brazil.

On April 11, 2018, the parties incorporated, with an equity interest of 50% held by Aymoré CFI and 50% held by Hyundai Capital, a non-operational entity named BHJV Assessoria e Consultoria em Gestão Empresarial Ltda. On May 8, 2018, Aymoré CFI and Hyundai Capital took resolution on the conversion of BHJV Assessoria into the non-operational joint-stock corporation named Banco Hyundai Capital Brasil S.A., as well as the capital stock increase in R$99,995, passing to the amount of R$100,000, divided into 100,000,000 (one hundred million) nominative common shares without par value. On December 13, 2018, the incorporation procedure of Banco Hyundai Capital Brasil S.A. was concluded.

In the EGM held on February 19, 2019, the shareholders of Banco Hyundai approved the capital increase in the amount of R$200,000, summing the total value of R$300,000 distributed into 300,000,000 (three hundred million) common shares without par value, held in the proportion of 50% by Aymoré CFI and 50% by Hyundai Capital.

On February 21, 2019, the authorization to operate granted by Bacen for the functioning of Banco Hyundai was published in the Federal Official Gazette. The expectation is that Banco Hyundai will start to operate in the first semester of 2019, being set that Aymoré CFI holds the effective operational control of this entity.

k) Creation of PI Distribuidora de Títulos e Valores Mobiliários S.A.

On May 3, 2018, Santander Finance Arrendamento Mercantil S.A., an indirectly controlled subsidiary of Banco Santander, was converted into a distribution company of bonds and securities and had its corporate name changed to SI Distribuidora de Títulos e Valores Mobiliários S.A. The conversion process of approved by Bacen on November 21, 2018. On December 17, 2018, SI Distribuidora de Títulos e Valores Mobiliários S.A. had its corporate name changed to PI Distribuidora de Títulos e Valores Mobiliários S.A., being the corporate name change process approved by Bacen on January 22, 2019. The company started its operations on March 14, 2019.

Individual and Consolidated Financial Statements – March 31, 2019 8

4) Strategy

Banco Santander Brasil is the only international bank with scale in the country. The Bank is convinced that the best way to grow in a profitable, recurring and sustainable manner is by providing excellent services to enhance customer satisfaction levels and attract more customers, making them more loyal. Our actions are based on establishing close and long-lasting relationships with customers, suppliers and shareholders. To accomplish that goal, our purpose is to help people and businesses prosper by being a Simple, Personal and Fair Bank, guided by the following strategic priorities:

· Increase customer preference and loyalty by offering targeted, simple, digital and innovative products and services through a multi-channel platform.

· Generate results in a sustainable and profitable manner, with greater revenue diversification, aiming to strike a balance between loans, funding and services, while maintaining a preemptive risk management approach and rigorous cost control.

· Be disciplined with capital and liquidity to preserve our solidity, face regulatory changes and seize growth opportunities.

· Achieve profitable market share gains through our robust portfolio, optimize the ecosystem and launch new ventures consistently improving the customer experience.

In the first quarter of 2019, the Bank was able to maintain recurring earnings generation, with outstanding profitability. The customer base continued to show steady growth, thanks to improved service to our customers, thereby allowing us to achieve profitable market share gains. At the same time, the Bank reached the highest level of engagement among our employees, which contributes to the sustainability of our business. These factors, allied to our strong capital and liquidity base, place us in a prime position to capture market opportunities.

People

The Bank continue to work on our strategic fronts, such as promoting collaboration, encouraging employee empowerment and horizontal management. The Bank highlight the following accomplishments in the past quarter:

The Bank reached the highest level of engagement, 92%, an increase of 4 p.p. compared to the previous year. In addition, 96% of employees feel proud to work at Santander.

Elected Company of the Year for Diversity by “Exame” magazine at the 2019 Diversity Forum, in partnership with the Ethos institute.

2nd place on LinkedIn’s Top Companies which ranks the most sought-after places to work for professionals in Brazil. The rise of 19 spots in the ranking over twelve months reflects the effectiveness of our talent attraction and retention strategies.

Our first blood donation campaign of 2019: The Bank hit 88% of the donation volume of the country's main blood bank, with the potential to save more than 33,000 lives.

My Place: internal mobility program with the purpose of encouraging employees to take charge of their careers and stimulating meritocracy. In its first year, the portal had more than 500,000 views.

Customer loyalty:

Our customers have acknowledged the enhancements in service and experience, which has led our NPS (Net Promoter Score) to remain on an upward trend, reaching 59 points this quarter, up 10 points YoY.

For the first time, the Bank was recognized by the EXAME/IBRC customer service ranking, reaching 1st place in customer service in the banking sector in 2018.

The customer base continues to enjoy solid expansion, highlighted by active account holders, who have been growing for the last 46 consecutive months.

Retail

Cards: our robust portfolio enables us to keep gaining market share in the loan portfolio, which reached 13.3%¹ in the quarter (+1.0 p.p. YoY - Source: Brazilian Central Bank, as of February/19), while our total card turnover expanded by 20% YoY. We launched Santander's credit plan for card customers, who can choose to make installment payments directly in the POS in as many as 36 installments, at competitive interest rates. The ability to purchase goods and services in installment payments aims to stimulate card turnover and foster customer loyalty. Santander Pass, our wristband for contactless payments using NFC technology, is now also available with the Visa brand and, in partnership with fashion retailer Osklen, we introduced Santander Pass Osklen. It is also worth mentioning that we have strengthened the Way app with: (i) the account opening functionality for single-product retailers; (ii) the possibility to pay the card bill in installments for current account holders; and (iii) the release of Santander ID for single-products retailers, thus reinforcing security.

Individual and Consolidated Financial Statements – March 31, 2019 9

Payroll Loans: our market share in the loan portfolio climbed by 10.2%, +1.4 p.p. YoY (Source: Brazilian Central Bank, as of February/19). Digital channels are one of our main credit origination vehicles. This quarter, the number of contracts generated via these channels saw a 27% QoQ rise.

Real Estate: the real estate portal provides more efficiency and agility. An example of that is the reduction in the average lead time for contracts by 43% compared to the previous year. This product remains one of the highlights in Retail, contributing to expand our loan portfolio.

Agro:our service model, with specialized Agro stores and managers exclusively dedicated to rural producers, has proven to be an important strategic component to maximize our role in the sector. This countryside expansion process is in line with our goal of being the best agribusiness bank in the country. Thanks to the increased number of account openings and loan portfolio growth, the Bank has experienced stronger results. In the issuance of agribusiness credit notes (“LCA”), our market share hit 8.5%, +2.8 p.p. YoY (Source: Brazilian Central Bank, as of February/19).

Getnet:The Bank continues with the strategy of offering physical and digital services, including for the e-commerce segment. This quarter, the Bank initiated an unprecedented offering for SuperGet, focused on individuals and individual microentrepreneurs, which includes payment of receivables in two business days and unification of debit and credit transaction fees. This innovative offering brings more transparency to our customer relationships and puts us in a competitive position to increase our presence in this dynamic market. It is worth noting that this product has the option of integrating with Superdigital, our digital account, to facilitate the payment of receivables. Our market share reached 12.3%² (+1.3 p.p. YoY), while total revenue climbed by 16% YoY in 1Q19, maintaining a double-digit growth rate. (Source: ABECS – “Monitor Bandeiras”, as of 4Q18).

SME:The Bank launched the “MEI” account for individual microentrepreneurs, a value offer that includes opening a business current account, access to credit, including the possibility of obtaining microcredit through Prospera, and acquisition of SuperGet at competitive prices. This is an example of integration and cross-selling between businesses that, together with other offers, places us in a good spot to capture opportunities in this segment. The market share in the loan portfolio reached 8.1%¹ (+ 0.3 p.p.), driven by customer base growth and greater loyalty.

Strengthening leading businesses

Consumer Finance: the Bank is the leaders in the sector, with a market share of 23.5%, +0.1 p.p. in twelve months (Source: Brazilian Central Bank, as of February/19. Total market share in vehicles (considering individuals and companies). The Bank attributes this performance to the innovations, partnerships and commercial service. As of this quarter, the Bank is also analyzing the financing documentation on weekends, with the possibility of clearing the vehicle on the same day, providing agile payment to dealerships.

Webmotors: The first phase of the Cockpit tool, which took place primarily in 2018, achieved good results, with high adherence of our dealership base. Now, our actions are focused on fine-tuning the tool and its integration with the bank. With this in mind, the Bank held the first edition of the “Mega Sale” promoted by Webmotors, in partnership with Santander Financiamentos, which generated 40% more leads for participating dealerships. Moreover, the Bank started the “autoguru” pilot, which already includes pricing in inventory acquisition, as well as quality rating alongside suggested sales prices.

Santander Corporate & Investment Banking (SCIB) – The Bank is still recognized as leaders:

Financial advisory for financing and concession auctions and finance structuring, according to Anbima (Financial Advisory – leadership since 2008, ANBIMA 2017) advisor in Americas and Project Finance (MLA) in LATAM according to Dealogic (Dealogic as of 2018).

In the foreign exchange market according to the Brazilian Central Bank (Cumulative figures from January to March 2019).

Innovations

Natura partnership:The Bank partnered with the country's first direct sales company to offer fully digital banking services to its sales consultants. In addition to traditional services, such as current account, cash transfer and withdrawal, it includes SuperGet with special conditions and access to the Prospera microcredit program via the app itself. This initiative is in line with our commitment to financial education, stimulating social transformation in the areas where the Bank operates through innovative solutions (SuperGet, Superdigital and Prospera Microcredit).

Santander Box: a new, more compact store model for high-flow locations, focusing primarily on potential customers in the Special segment. The objective is to offer fast financial solutions, such as account opening, card sales and SuperGet, among others. In this phase of the pilot program, the Bank inaugurated the first Santander Box in downtown Rio de Janeiro, with extended hours – and it is already showing significant results. This initiative contributes to increase our customer base in an innovative way.

Individual and Consolidated Financial Statements – March 31, 2019 10

New Ventures

Ben, which operates in the benefits industry, continued to make progress partnering with establishments. The proposal is to offer a better experience for end-customers, in addition to making partnerships with companies’ HR departments and commercial establishments. The Bank see potential synergies with the wholesale, SME and individuals segments, as well as with Getnet.

Pi, our digital investment platform, was made available to the general public this quarter, and the Bank expects to capture investors looking for more autonomy and practicality in the purchase of investment products.

Sustainability

The Bank continues to hold the leadership in microcredit through the the Prospera program, whose loan portfolio grew 63% YoY in March 2019 and reached R$ 730 million.

Volunteering financial guidance: on Saturdays, at our branches, the Bank will promote lectures and individual service for customers and non-customers, as the Bank believe that he can help people prosper. There will be no commercial activity in this action, and it will be executed through our network of volunteer employees.

In Higher Education, which is an important lever for our customer base, the Bank has, in addition to the financial offer, a non-financial offer based on training, employment and entrepreneurship. The Bank has already awarded over 14,200 scholarships in Brazil since 2015.

The Bank introduced the #Desplastify commitment to eliminate, still this year, tons of fast-use plastic across the Bank.

The Bank received AA rating in the MSCI ESG Ratings assessment.

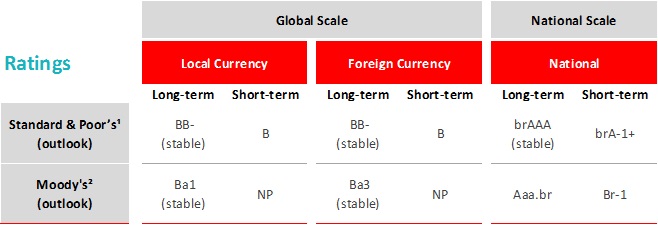

5) Rating Agencies

Banco Santander is rated by international ratings agencies and the ratings assigned reflect many factors including management quality, operating performance and financial strength, as well as other factors related to the financial sector and economic environment in which the Bank is inserted, having the long-term foreign currency rating limited to the sovereign rating. The table below presents the ratings assigned by the rating agencies Standard & Poor's and Moody's:

1) Last updated November 29, 2018.

2) Last updated February 18, 2019.

6) Corporate Governance

The Board of Directors of Banco Santander has met and resolved:

On April29, 2019, to approve the Individual and Consolidated Financial Statements of Banco Santander, prepared in accordance with accounting practices adopted in Brazil, applicable to institutions authorized to operate by Bacen and the Consolidated Financial Statements of Banco Santander, prepared in accordance with the International Financial Reporting Standards (IFRS), respect to the period ended March 31, 2019.

On March 27, 2019, to approve the proposal for declaration and payment of interest on equity, in the gross amount of R$1 billion, for payment as of April 29, 2019, without any indexation.

On March 27, 2019, to acknowledge the resignation of Mr. Fernando Carvalho Botelho de Miranda to the position of Officer without specific designation, as well as to approve the appointment of the following member to be part of the Board of Officers, as Officers without specific designation: Mr. Daniel Fantoni Assa; Mrs. Elita Vechin Pastorelo Ariaz; Mr. Franco Luigi Fasoli; Mr. Jran Paulo Kambourakis and Mr. Roberto Alexandre Borges Fischetti.

Individual and Consolidated Financial Statements – March 31, 2019 11

On March 20, 2019, to approve the 20-F Form of Banco Santander referred to the fiscal year ended December 31, 2018.

On February 25, 2019, to approve the Consolidated Financial Statements of Banco Santander referred to the fiscal year ended December 31, 2018, prepared in accordance with the International Financial Reporting Standards (IFRS).

On January 29, 2019, to approve the Individual and Consolidated Financial Statements of Banco Santander, prepared in accordance with accounting practices adopted in Brazil, applicable to institutions authorized to operate by Bacen, respect to the fiscal year ended December 31, 2018.

7) Risk Management

On February 23, 2017, Bacen published CMN Resolution 4,557, which provides for the risk and capital management structure (GIRC) and entered into force 180 days from the date of its publication. The resolution highlights the need to implement an integrated risk and capital management framework, definition of integrated stress testing program and Risk Appetite Statement (RAS), constitution of Risk Committee and appointment of director for management and director of capital. Banco Santander is continuously and progressively developing necessary actions aiming at adherence to the resolution. We haven´t identified relevant impacts resulting from this standard up to the date of publication of this note.

For further information, see explanatory note nº 35 of this publication.

Structure of Capital Management

Banco Santander’s structure of capital management has a robust governance framework that supports the process related to this theme and establishes the attributions of each teams involved. Furthermore, there is a clear definition that should be adopted to effective capital management. More details can be consult in “Structure Capital and Risk Management”, available on Investor Relations website.

Internal Audit

Internal Audit reports directly to the Board of Directors, whose activities are supervised by the Audit Committee.

Internal Audit is a permanent function, independent of any other functions or units, whose objective is to provide the Management Body and the senior management with independent assurance on the quality and effectiveness of internal control, risk management (current or emerging) and governance processes and systems, thereby helping to protect the company’s value, solvency and reputation. The Internal Audit has quality certificate issued by the Institute of Internal Auditors (IIA).

In order to perform its duties and reduce coverage risks inherent to Banco Santander's activities, the Internal Audit area has internally developed tools that are updated when necessary. These include the risk matrix, used as a planning tool, prioritizing each unit’s risk level, considering, among others, its inherent risks, the last audit rating, level of compliance with recommendations and their size. The work programs, which describe the audit tests to be performed, are reviewed periodically.

The Audit Committee and the Board of Directors favorably reviewed and approved the work plan of the Internal Audit for the year 2019

In the first quarter of 2019, internal control procedures and controls on the information systems of the selected units were evaluated according to the work plan for the year, considering the effectiveness of the design and its operation. The Internal Audit informed the Audit Committee and the Board of Directors about the conclusions of the works done during that period, according to its annual plan.

8) People

When the discussion is about the growth and development of Banco Santander, a force stands out: the People. Having a motivated and dedicated employees is a decisive factor in making the Bank in the best bank for clients and the best company for employees.

Employees are the strongest link between the Bank and clients and so, day after day, Banco Santander enhances their management practices because it knows that only with dedicated employees, well trained and with full professional development, the Bank will manage to get more and better clients, satisfied, proud to do business with Banco Santander and the Santander brand.

The daily performance of Banco Santander with clients, employees, stockholders and society is guided by the purpose of the Bank to contribute to people and businesses to prosper and their way of act.

Individual and Consolidated Financial Statements – March 31, 2019 12

The Bank has a talented team of 48,232 employees only in Brazil. The Bank seeks professionals who identified with the Corporate Culture, to be a Simple Bank (with uncomplicated and easy services to operate), Personal (with solutions and channels that meet client’s needs and preferences) and Fair (promoting business and relationships that are good for clients, stockholders, employees and society). In addition to identifying with the culture, the Banco Santander's employees act in their day to day aligned to it.

9) Sustainable Development

Santander’s Sustainability Strategy is based on three pillars: (i) Efficient and strategic use of Natural Capital, (ii) Potential Development and (iii) Resilient and Inclusive Economy. The Bank's vision of the future, through these pillars, is to support Brazilian society in its transformation to Brazil of the 21st Century, maintaining excellence and responsibility in internal management, with ethical values as the basis and technology at the service of people and business.

We remained for the ninth consecutive year in the portfolio of the Corporate Sustainability Index (ISE) of B³ and in 2019; the Guia EXAME of Diversity as the company of the year and the financial institution with the best practices of inclusion and diversity of the national market recognized us. Also in 2019, we received a rating of AA (on a scale of AAA-CCC) in the MSCI ESG Ratings assessment.

In Social and Environmental Business, we disbursed R$340,5 million in the first quarter of 2019. With Prospera Santander Microcredit we generated approximately R$396 million of production (69% more than the same period of 2018).

Through Santander Universities, we have awarded more than 440 study grants in the first quarter, from the Santander University-Business Program, where Banco Santander contributes a scholarship of R$700 to help the student in the payment of monthly fees and/or related costs, and of own programs, carried out directly with the University.

The Amigo de Valor Program allows Banco Santander, as well as our employees and clients, to direct part of the income tax due directly to the Funds for the Rights of Children and Adolescents. In 2018, this program raised funds totaling more than R$13 million, which were directed to 67 projects in Brazil.

We also launched the Plastic Free project whose initial goal is to reduce the consumption of single use plastic (cups and bottles) in our administrative buildings and until 2020 to impact all bank agencies.

We publish the Bank's Non-Financial Indicators Section that follows local and international guidelines, such as the Global Reporting Initiative (GRI), the International Integrated Reporting Council (IIRC) and the Brazilian Association of Public Held Companies (ABRASCA). The main purpose of the Section is to highlight our responsible internal management and the way in which we promote the transformation of society by the business.

10) Independent Audit

Banco Santander's policy of including its subsidiaries in contracting services not related to the external audit of its independent auditors is based on Brazilian and international auditing standards that preserve the auditor's independence. This reasoning provides as follows: (i) the auditor should not audit his own work, (ii) the auditor should not perform managerial duties on his client, (iii) the auditor should not promote the interests of his client, and (iv) need for approval of any services by the Bank's Audit Committee.

In compliance with the Instruction of the Securities Commission 381/2003, Banco Santander informs that in the period ended March 31, 2019, PricewaterhouseCoopers did not provide services not related to the independent audit of the Financial Statements of Banco Santander and subsidiaries above 5% of total fees related to independent auditing services.

In addition, the Bank confirms that PricewaterhouseCoopers has procedures, policies and controls to ensure its independence, which include an evaluation of the work performed, covering any service that is not independent of the Financial Statements of Banco Santander and its subsidiaries. This evaluation is based on the applicable regulations and accepted principles that preserve the independence of the auditor. The acceptance and provision of professional services not related to the external audit in the period ended March 31, 2019 did not affect the independence and objectivity in conducting the external audits carried out in Banco Santander and other entities of the Group, since the above principles were observed.

The Board of Directors

The Executive

(Authorized at the Meeting of the Board of April 29, 2019).

Individual and Consolidated Financial Statements – March 31, 2019 13

Independent auditor's report

To the Board of Directors and Stockholders

Banco Santander (Brasil) S.A.

Introduction

We have reviewed the interim balance sheets ofBanco Santander (Brasil) S.A.("Bank") as at March 31, 2019, and the related income statements, statements of changes in stockholders’ equity and cash flows statements for the quarter then ended, as well as the interim consolidated balance sheets ofBanco Santander (Brasil) S.A. and its subsidiaries ("Consolidated") as at March 31, 2019, and the related consolidated income statements, statements of changes in stockholders’ equity and cash flows statements for the quarter then ended, and a summary of significant accounting policies and other explanatory information.

Management is responsible for the preparation and fair presentation of these interim financial statements in accordance with accounting practices adopted in Brazil, applicable to institutions authorized to operate by the Brazilian Central Bank (BACEN).Our responsibility is to express a conclusion on these interim financial statements based on our review.

Scope of review

We conducted our review in accordance with Brazilian and International Standards on Reviews of Interim Financial Information (NBC TR 2410 – Review of Interim Financial Information Performed by the Independent Auditor of the Entity and ISRE 2410 – Review of Interim Financial Information Performed by the Independent Auditor of the Entity, respectively). A review of interim information consists of making inquiries, primarily of persons responsible for financial and accounting matters, and applying analytical and other review procedures. A review is substantially less in scope than an audit conducted in accordance with Brazilian and International Standards on Auditing and consequently does not enable us to obtain assurance that we would become aware of all significant matters that might be identified in an audit. Accordingly, we do not express an audit opinion.

Conclusion

Based on our review, nothing has come to our attention that causes us to believe that the accompanying interim financial statements referred to above do not present fairly, in all material respects, the financial position of Banco Santander (Brasil) S.A., and Banco Santander (Brasil) S.A. and its subsidiaries as at March 31, 2019, their financial performance and its cash flows for the quarter then ended, as well as their consolidated financial performance and its cash flows for the quarter then ended, in accordance with accounting practices adopted in Brazil, applicable to institutions authorized to operate by the Brazilian Central Bank (BACEN).

Other Matters

Statements of value added

We have also reviewed the parent company and consolidated statements of value added for the quarter ended March 31, 2019, prepared under the responsibility of the Management, whose presentation is required by Brazilian Corporate Law by publicly-held companies. These statements have been submitted to the same review procedures described above and, based on our review, nothing has come to our attention that causes us to believe that they have not been prepared, in all material respects, in a manner consistent with the interim financial statements taken as a whole.

São Paulo, April 29, 2019

PricewaterhouseCoopers

Auditores Independentes

CRC 2SP000160/O-5

Edison Arisa Pereira

Accountant CRC 1SP127241/O-0

PricewaterhouseCoopers, Av. Francisco Matarazzo 1400, Torre Torino, São Paulo, SP, Brasil 05001-903, Caixa Postal 61005 T: (11) 3674-2000, www.pwc.com/br

Individual and Consolidated Financial Statements – March 31, 2019 14

(Free Translation into English from the Original Previously Issued in Portuguese) | |

| BANCO SANTANDER (BRASIL) S.A. AND SUBSIDIARIES |

In thousands of Brazilian Real - R$, unless otherwise stated. | |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Bank |

| Consolidated | ||||

|

| Notes |

| 03/31/2019 |

| 12/31/2018 |

| 03/31/2019 |

| 12/31/2018 |

|

|

|

|

|

|

|

|

|

|

|

Current Assets |

|

|

| 487,967,086 |

| 495,071,546 |

| 515,322,355 |

| 523,287,889 |

Cash |

| 4 |

| 9,278,518 |

| 11,358,459 |

| 9,516,113 |

| 11,629,112 |

Interbank Investments |

| 5 |

| 62,238,480 |

| 86,464,685 |

| 33,195,821 |

| 56,375,289 |

Money Market Investments |

|

|

| 27,291,708 |

| 45,325,687 |

| 27,291,708 |

| 44,825,827 |

Interbank Deposits |

|

|

| 32,800,445 |

| 33,270,931 |

| 3,756,928 |

| 3,680,810 |

Foreign Currency Investments |

|

|

| 2,146,327 |

| 7,868,067 |

| 2,147,185 |

| 7,868,652 |

Securities and Derivative Financial Instruments |

| 6 |

| 72,086,326 |

| 77,244,185 |

| 86,864,883 |

| 90,103,130 |

Own Portfolio |

|

|

| 32,460,022 |

| 36,212,955 |

| 40,821,271 |

| 41,916,648 |

Subject to Repurchase Commitments |

|

|

| 33,946,676 |

| 36,382,807 |

| 28,459,466 |

| 32,252,210 |

Derivative Financial Instruments |

|

|

| 4,243,413 |

| 4,109,455 |

| 12,354,970 |

| 12,206,228 |

Deposited in the Central Bank |

|

|

| 4,665 |

| 5,071 |

| 4,665 |

| 103,604 |

Privatization Currencies |

|

|

| 586 |

| 667 |

| 586 |

| 667 |

Pledged in Guarantees |

|

|

| 1,430,964 |

| 533,230 |

| 5,223,925 |

| 3,623,773 |

Interbank Accounts |

| 7 |

| 82,395,760 |

| 79,563,879 |

| 91,389,482 |

| 92,161,239 |

Payments and Receipts Pending Settlement |

|

|

| 10,990,112 |

| 9,902,862 |

| 19,514,567 |

| 22,036,377 |

Restricted Deposits: |

|

|

| 71,372,600 |

| 69,625,970 |

| 71,853,739 |

| 70,103,002 |

Central Bank Deposits |

|

|

| 71,369,878 |

| 69,625,795 |

| 71,851,017 |

| 70,102,827 |

National Housing System (SFH) |

|

|

| 2,722 |

| 175 |

| 2,722 |

| 175 |

Interbank Transfers |

|

|

| 11,872 |

| 13,187 |

| - |

| - |

Correspondents |

|

|

| 21,176 |

| 21,860 |

| 21,176 |

| 21,860 |

Lending Operations |

| 8 |

| 81,251,086 |

| 74,689,851 |

| 107,077,421 |

| 100,432,401 |

Public Sector |

|

|

| 27,737 |

| 162 |

| 27,737 |

| 162 |

Private Sector |

|

|

| 84,798,595 |

| 78,890,129 |

| 111,588,448 |

| 105,386,559 |

Lending Operations Assignment |

|

|

| - |

| - |

| 13,972 |

| 17,912 |

(Allowance for Loan Losses) |

| 8.f |

| (3,575,246) |

| (4,200,440) |

| (4,552,736) |

| (4,972,232) |

Leasing Operations |

| 8 |

| - |

| - |

| 1,213,595 |

| 1,215,740 |

Private Sector |

|

|

| - |

| - |

| 1,237,673 |

| 1,239,421 |

(Allowance for Lease Losses) |

| 8.f |

| - |

| - |

| (24,078) |

| (23,681) |

Other Receivables |

|

|

| 179,040,871 |

| 164,105,338 |

| 183,902,218 |

| 169,226,857 |

Credits for Avals and Sureties Honored |

|

|

| 173,505 |

| 57,723 |

| 173,505 |

| 57,723 |

Foreign Exchange Portfolio |

| 9 |

| 123,463,842 |

| 105,683,300 |

| 123,463,842 |

| 105,683,300 |

Income Receivable |

|

|

| 2,454,777 |

| 2,112,919 |

| 2,147,333 |

| 1,927,635 |

Trading Account |

| 10 |

| 1,759,785 |

| 1,628,363 |

| 2,064,176 |

| 1,910,791 |

Deferred Taxes |

| 11 |

| 6,861,633 |

| 7,502,420 |

| 7,738,256 |

| 8,372,900 |

Others |

| 12 |

| 45,130,661 |

| 47,846,548 |

| 49,186,396 |

| 52,068,793 |

(Allowance for Other Receivables Losses) |

| 8.f |

| (803,332) |

| (725,935) |

| (871,290) |

| (794,285) |

Other Assets |

|

|

| 1,676,045 |

| 1,645,149 |

| 2,162,822 |

| 2,144,121 |

Other Assets |

|

|

| 1,226,809 |

| 1,235,921 |

| 1,582,593 |

| 1,601,986 |

(Allowance for Valuation) |

|

|

| (170,000) |

| (161,942) |

| (223,408) |

| (217,497) |

Prepaid Expenses |

|

|

| 619,236 |

| 571,170 |

| 803,637 |

| 759,632 |

The accompanying notes from Management are an integral part of these financial statements.

Individual and Consolidated Financial Statements – March 31, 2019 15

|

|

|

|

|

| Bank |

|

|

| Consolidated |

|

| Notes |

| 03/31/2019 |

| 12/31/2018 |

| 03/31/2019 |

| 12/31/2018 |

Long-Term Assets |

|

|

| 258,278,352 |

| 253,043,465 |

| 276,048,494 |

| 271,376,071 |

Interbank Investments |

| 5 |

| 27,538,067 |

| 28,031,980 |

| 435,845 |

| 436,942 |

Interbank Deposits |

|

|

| 27,538,067 |

| 28,031,980 |

| 435,845 |

| 436,942 |

Securities and Derivative Financial Instruments |

| 6 |

| 105,382,601 |

| 98,229,938 |

| 108,612,268 |

| 104,361,551 |

Own Portfolio |

|

|

| 27,840,113 |

| 22,599,399 |

| 29,052,181 |

| 26,253,702 |

Subject to Repurchase Commitments |

|

|

| 56,898,392 |

| 53,815,465 |

| 56,735,237 |

| 53,601,206 |

Derivative Financial Instruments |

|

|

| 6,891,850 |

| 5,782,175 |

| 6,925,818 |

| 5,820,767 |

Deposited with the Central Bank |

|

|

| 614,477 |

| 1,444,136 |

| 614,477 |

| 1,444,136 |

Privatization Currencies |

|

|

| 688 |

| 779 |

| 688 |

| 779 |

Pledged in Guarantees |

|

|

| 10,510,929 |

| 12,511,388 |

| 12,657,715 |

| 15,164,365 |

Securities Obtained from Commitments with Free Mover |

|

|

| 2,626,152 |

| 2,076,596 |

| 2,626,152 |

| 2,076,596 |

Interbank Accounts |

| 7 |

| 281,332 |

| 281,332 |

| 281,332 |

| 281,332 |

Restricted Deposits: |

|

|

| 281,332 |

| 281,332 |

| 281,332 |

| 281,332 |

National Housing System (SFH) |

|

|

| 281,332 |

| 281,332 |

| 281,332 |

| 281,332 |

Lending Operations |

| 8 |

| 94,943,351 |

| 94,654,519 |

| 129,256,089 |

| 127,327,245 |

Public Sector |

|

|

| 23,971 |

| 583,968 |

| 23,971 |

| 583,968 |

Private Sector |

|

|

| 106,686,537 |

| 105,266,028 |

| 141,867,556 |

| 138,961,203 |

Lending Operations Related to Assignment |

|

|

| - |

| - |

| - |

| 4,880 |

(Allowance for Loan Losses) |

| 8.f |

| (11,767,157) |

| (11,195,477) |

| (12,635,438) |

| (12,222,806) |

Leasing Operations |

| 8 |

| - |

| - |

| 1,366,200 |

| 1,287,060 |

Public Sector |

|

|

| - |

| - |

| 274 |

| 156 |

Private Sector |

|

|

| - |

| - |

| 1,412,049 |

| 1,333,502 |

(Allowance for Lease Losses) |

| 8.f |

| - |

| - |

| (46,123) |

| (46,598) |

Other Receivables |

|

|

| 29,901,360 |

| 31,426,963 |

| 35,735,962 |

| 37,146,216 |

Receivables for Guarantees Honored |

|

|

| 344,787 |

| 486,323 |

| 344,787 |

| 486,323 |

Foreign Exchange Portfolio |

| 9 |

| - |

| 1,690,088 |

| - |

| 1,690,088 |

Income Receivable |

|

|

| 117,446 |

| 146,813 |

| 117,446 |

| 146,813 |

Deferred Taxes |

| 11 |

| 16,489,059 |

| 16,945,139 |

| 18,932,033 |

| 19,291,180 |

Others |

| 12 |

| 13,409,972 |

| 12,770,902 |

| 16,911,998 |

| 16,261,333 |

(Allowance for Other Receivables Losses) |

| 8.f |

| (459,904) |

| (612,302) |

| (570,302) |

| (729,521) |

Other Assets |

|

|

| 231,641 |

| 418,733 |

| 360,798 |

| 535,725 |

Temporary Assets |

|

|

| 1,622 |

| 1,622 |

| 1,631 |

| 1,631 |

(Allowance for Losses) |

|

|

| (1,622) |

| (1,622) |

| (1,631) |

| (1,631) |

Prepaid Expenses |

|

|

| 231,641 |

| 418,733 |

| 360,798 |

| 535,725 |

|

|

|

|

|

|

|

|

|

|

|

Permanent Assets |

|

|

| 33,010,393 |

| 30,896,503 |

| 12,308,333 |

| 11,155,329 |

Investments |

|

|

| 23,595,551 |

| 21,491,544 |

| 348,941 |

| 337,589 |

Investments in Affiliates and Subsidiaries: |

| 14 |

| 23,574,784 |

| 21,470,777 |

| 328,104 |