Table of Contents

Filed Pursuant to Rule No. 424(b)(5)

Registration No. 333-166103

CALCULATION OF REGISTRATION FEE

Class of Securities Registered | Proposed Aggregate Offering Price | Amount of Registration Fee(1) | ||

8 1/4% Senior Notes due 2018 | $300,000,000 | $21,390 | ||

Subsidiary Guarantees of 8 1/4% Senior Notes due 2018 | (2) | (2) |

| (1) | The registration fee is being paid on a deferred basis in reliance upon Rules 456(b) and 457(r) and includes $39,060 that is being offset pursuant to Rule 457(p) for fees paid with respect to the $700,000,000 aggregate initial offering price of securities that were previously registered pursuant to Registration Statement No. 333-162118, initially filed on September 24, 2009. Pursuant to Rule 457(p) under the Securities Act, such unutilized filing fee may be applied to the filing fee payable in connection with the filing of this prospectus supplement pursuant to Rule 424(b). |

| (2) | In accordance with Rule 457(n), no separate fee is payable with respect to the Subsidiary Guarantees. |

Table of Contents

PROSPECTUS SUPPLEMENT

(to Prospectus dated April 16, 2010)

Penn Virginia Resource Partners, L.P.

Penn Virginia Resource Finance Corporation

$300,000,000

8 1/4% Senior Notes due 2018

We are offering $300,000,000 of our 8 1/4% Senior Notes due 2018. Interest on the notes will accrue from April 27, 2010 and will be payable semiannually on April 15 and October 15 of each year, beginning on October 15, 2010. The notes will mature on April 15, 2018.

We may redeem the notes at any time on or after April 15, 2014 at the redemption prices set forth in this prospectus supplement. We may redeem the notes prior to April 15, 2014 at the “make-whole” redemption price set forth in this prospectus supplement. In addition, we may redeem up to 35% of the notes until April 15, 2013 with the proceeds of certain equity offerings at the redemption price set forth in this prospectus supplement. If we sell certain of our assets or experience specific kinds of changes of control, we must offer to purchase the notes at prices set forth in this prospectus supplement plus accrued and unpaid interest.

The notes are senior unsecured obligations of Penn Virginia Resource Partners, L.P. and Penn Virginia Resource Finance Corporation, our wholly owned subsidiary that has no material assets. The notes will be fully and unconditionally guaranteed on a senior unsecured basis by our existing and future domestic restricted subsidiaries, subject to certain exceptions. The notes and the guarantees will rank equally with our existing and future senior unsecured indebtedness and will be effectively subordinated to all of our and the guarantors’ existing and future secured indebtedness (to the extent of the assets securing such indebtedness), including indebtedness under our revolving credit facility, and senior in right of payment to all existing and future subordinated debt.

Investing in the notes involves risks. Please read “Risk Factors” beginning on page S-17 of this prospectus supplement.

| Per Note | Total | |||||

Price to public1 | 100 | % | $ | 300,000,000 | ||

Underwriting discounts and commissions | 2.50 | % | $ | 7,500,000 | ||

Estimated proceeds, before expenses, to Penn Virginia Resource Partners, L.P. | 97.50 | % | $ | 292,500,000 | ||

1Plus accrued interest, if any, from April 27, 2010, if settlement occurs after that date.

None of the Securities and Exchange Commission, any state securities commission or any other regulatory body has approved or disapproved of these securities or determined if this prospectus supplement or the accompanying prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

We expect delivery of the notes will be made to investors in book-entry form through The Depository Trust Company on or about April 27, 2010.

Joint Book-Running Managers

| Wells Fargo Securities | BofA Merrill Lynch | J.P. Morgan | RBC Capital Markets |

Senior Co-Managers

| BB&T Capital Markets | BNP PARIBAS | Mitsubishi UFJ Securities | PNC Capital Markets LLC |

Co-Managers

| Barclays Capital | BMO Capital Markets | Capital One Southcoast | Comerica Securities | Credit Suisse |

| SOCIETE GENERALE | TD Securities | UBS Investment Bank | US Bancorp |

The date of this prospectus supplement is April 22, 2010.

Table of Contents

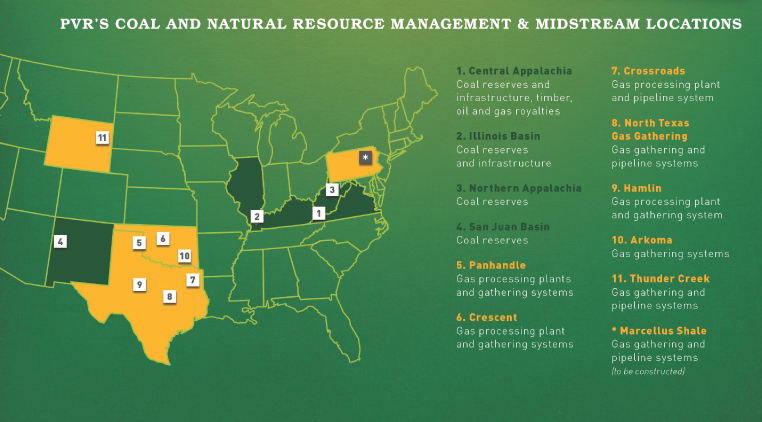

The map below shows the general locations of our coal reserves and related infrastructure investments and our natural gas gathering and processing systems as of December 31, 2009, as well as the natural gas gathering and pipeline systems we have agreed to construct in the Marcellus Shale formation of north central Pennsylvania.

Table of Contents

Prospectus Supplement

| Page | ||

| S-ii | ||

| S-iii | ||

| S-iv | ||

| S-1 | ||

| S-17 | ||

| S-38 | ||

| S-39 | ||

| S-40 | ||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | S-44 | |

| S-70 | ||

| S-104 | ||

| S-107 | ||

| S-110 | ||

| S-111 | ||

Certain United States Federal Income and Estate Tax Considerations | S-161 | |

| S-166 | ||

| S-170 | ||

| S-170 | ||

| S-170 | ||

| S-170 | ||

| F-1 |

Prospectus

| Page | ||

| 1 | ||

| 1 | ||

| 1 | ||

| 2 | ||

| 2 | ||

| 3 | ||

| 4 | ||

| 5 | ||

| 5 | ||

| 14 | ||

| 18 | ||

| 21 | ||

| 31 | ||

| 50 | ||

| 51 | ||

| 51 |

S-i

Table of Contents

ABOUT THIS PROSPECTUS SUPPLEMENT

This document is in two parts. The first part is this prospectus supplement, which describes the specific terms of the notes we are offering and certain other matters. The second part, the base prospectus dated April 16, 2010, provides more general information about the various securities that we may offer from time to time, some of which information may not apply to the notes we are offering hereby. Generally when we refer to this prospectus, we are referring to both this prospectus supplement and the base prospectus combined. You should read this prospectus supplement along with the accompanying base prospectus, the documents incorporated by reference herein and therein, as well as any free writing prospectus that is filed. If any of the information in this prospectus supplement is inconsistent with any of the information in the base prospectus or the documents incorporated by reference herein or therein, you should rely on the information in this prospectus supplement.

You should rely only on the information contained in this prospectus supplement, the accompanying base prospectus and the documents incorporated by reference herein and therein or that is contained in any free writing prospectus relating to the notes. We have not, and the underwriters have not, authorized anyone to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not making an offer of the notes in any jurisdiction where their offer or sale is not permitted. The information in this prospectus supplement, the base prospectus and the documents incorporated herein and therein by reference may only be accurate as of their respective dates. Our business, financial condition, results of operations and prospects may have changed since those dates.

S-ii

Table of Contents

TERMS USED IN THIS PROSPECTUS SUPPLEMENT

Unless the context requires otherwise, references in this prospectus supplement to the term:

| • | “Penn Virginia Resource Partners” or “PVR” refer to Penn Virginia Resource Partners, L.P., a Delaware limited partnership; |

| • | “the Partnership,” “we,” “us” or “our” refer to Penn Virginia Resource Partners and its subsidiaries, except in “Prospectus Supplement Summary—The Offering” and “Description of Notes”; |

| • | “Finance Co.” refers to Penn Virginia Resource Finance Corporation, a Delaware corporation and a wholly owned subsidiary of Penn Virginia Resource Partners; |

| • | “Issuers” refer to Penn Virginia Resource Partners and Finance Co.; |

| • | “PVR GP” or “our general partner” refers to Penn Virginia Resource GP LLC, a Delaware limited liability company; |

| • | “Penn Virginia” or “PVA” refers to Penn Virginia Corporation, a Virginia corporation; |

| • | “PVOG” refers to Penn Virginia Oil & Gas Corporation, a Virginia corporation, and its subsidiaries; |

| • | “PVG” refers to Penn Virginia GP Holdings, L.P., a Delaware limited partnership; and |

| • | “PVG GP” means PVG GP, LLC, a Delaware limited liability company and the general partner of PVG. |

The following are certain abbreviations and terms commonly used in the coal and oil and gas industries that are used in this prospectus supplement:

| • | “Bbl” refers to a standard barrel of 42 U.S. gallons liquid volume; |

| • | “Bcf” refers to one billion cubic feet; |

| • | “Bcfe” refers to one billion cubic feet equivalent with one barrel of oil or condensate converted to six thousand cubic feet of natural gas based on the estimated relative energy content; |

| • | “BTU” refers to British thermal unit; |

| • | “Mbf” refers to one thousand board feet; |

| • | “Mcf” refers to one thousand cubic feet; |

| • | “MMBtu” refers to one million British thermal units; |

| • | “MMcf” refers to one million cubic feet; |

| • | “MMcfd” refers to one million cubic feet per day; |

| • | “NGLs” refers to natural gas liquids, such as ethane, propane, normal butane, isobutane and natural gasoline; |

S-iii

Table of Contents

| • | “probable coal reserves” refers to those reserves for which quantity and grade and/or quality are computed from information similar to that used for proven reserves, but the sites for inspection, sampling and measurement are farther apart or are otherwise less adequately spaced. The degree of assurance, although lower than that for proven coal reserves, is high enough to assume continuity between points of observation; and |

| • | “proven coal reserves” refers to those reserves for which: (a) quantity is computed from dimensions revealed in outcrops, trenches, workings or drill holes; grade and/or quality are computed from the results of detailed sampling; and (b) the sites for inspection, sampling and measurement are spaced so closely, and the geologic character is so well defined, that the size, shape, depth and mineral content of reserves are well-established. |

Some of the information included in this prospectus supplement and the documents we incorporate by reference contains forward-looking statements. These statements use forward-looking words such as “may,” “will,” “should,” “could,” “achievable,” “anticipate,” “believe,” “expect,” “estimate,” “project” or other words and phrases of similar meaning. These statements discuss goals, intentions and expectations as to future trends, plans, events, results of operations or financial condition or state other “forward-looking” information. A forward-looking statement may include a statement of the assumptions or bases underlying the forward-looking statements. We believe we have chosen these assumptions or bases in good faith and that they are reasonable. However, we caution you that assumed facts or bases almost always vary from actual results, and the differences between assumed facts or bases and actual results can be material, depending on the circumstances. When considering forward-looking statements, you should keep in mind the cautionary statements in this prospectus and the documents we have incorporated by reference. These statements reflect our current views with respect to future events and are subject to various risks, uncertainties and assumptions, including, but not limited to, the following:

| • | the volatility of commodity prices for natural gas, NGLs and coal; |

| • | our ability to access external sources of capital; |

| • | any impairment writedowns of our assets; |

| • | the relationship between natural gas, NGL and coal prices; |

| • | the projected demand for and supply of natural gas, NGLs and coal; |

| • | competition among producers in the coal industry generally and among natural gas midstream companies; |

| • | the extent to which the amount and quality of actual production of our coal differs from estimated recoverable coal reserves; |

| • | our ability to generate sufficient cash from our businesses to maintain and pay the quarterly distribution to our general partner and our unitholders; |

| • | the experience and financial condition of our coal lessees and natural gas midstream customers, including our lessees’ ability to satisfy their royalty, environmental, reclamation and other obligations to us and others; |

S-iv

Table of Contents

| • | operating risks, including unanticipated geological problems, incidental to our coal and natural resource management or natural gas midstream business; |

| • | our ability to acquire new coal reserves or natural gas midstream assets and new sources of natural gas supply and connections to third-party pipelines on satisfactory terms; |

| • | our ability to retain existing or acquire new coal lessees and natural gas midstream customers; |

| • | the ability of our lessees to produce sufficient quantities of coal on an economic basis from our reserves and obtain favorable contracts for such production; |

| • | the occurrence of unusual weather or operating conditions including force majeure events; |

| • | delays in anticipated start-up dates of our lessees’ mining operations and related coal infrastructure projects and new processing plants in our natural gas midstream business; |

| • | environmental risks affecting the mining of coal reserves or the production, gathering and processing of natural gas; |

| • | the timing of receipt and availability of necessary governmental permits by us or our lessees; |

| • | hedging results; |

| • | accidents; |

| • | changes in governmental regulation or enforcement practices, especially with respect to environmental, health and safety matters, including with respect to emissions levels applicable to coal-burning power generators and permissible levels of mining runoff; |

| • | uncertainties relating to the outcome of current and future litigation regarding mine permitting and the effects of recent regulatory guidance on permitting under the Clean Water Act; |

| • | uncertainties regarding Penn Virginia Corporation’s continued equity interest in the holding company of our general partner and its future business relationship with us; |

| • | risks and uncertainties relating to general domestic and international economic (including inflation, interest rates and financial and credit markets) and political conditions (including the impact of potential terrorist attacks); |

| • | risks set forth in our Annual Report on Form 10-K for the fiscal year ended December 31, 2009 and in other reports we file with the Securities and Exchange Commission, or the SEC, that are incorporated by reference in this prospectus supplement; and |

| • | other risks set forth in “Risk Factors.” |

All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements in this paragraph and elsewhere in this prospectus supplement and in the documents incorporated by reference herein. When considering forward-looking statements, you should keep in mind the risk factors and other cautionary statements in this prospectus, including those described in the “Risk Factors” section of this prospectus. We will not update these statements unless the securities laws require us to do so.

S-v

Table of Contents

This summary highlights information contained elsewhere in this prospectus supplement and the accompanying base prospectus. It does not contain all of the information that you should consider before making an investment decision. You should carefully read this entire prospectus supplement, the accompanying base prospectus and the documents incorporated by reference to understand fully the terms of the notes. You should also read “Risk Factors” contained in this prospectus supplement for more information about important risks that you should consider before buying notes in this offering.

The notes will be jointly issued by Penn Virginia Resource Partners and Finance Co., a wholly owned subsidiary of Penn Virginia Resource Partners. Finance Co. has no material assets and was formed for the sole purpose of being a co-issuer of the notes.

Penn Virginia Resource Partners, L.P.

Penn Virginia Resource Partners, L.P. (NYSE: PVR) is a publicly traded Delaware limited partnership formed in 2001 by Penn Virginia Corporation (NYSE: PVA), or Penn Virginia, that is principally engaged in the management of coal and natural resource properties and the gathering and processing of natural gas in the United States. Both in our current limited partnership form and in our previous corporate form, we have managed coal properties since 1882. We currently conduct operations in two business segments: (i) coal and natural resource management and (ii) natural gas midstream. In the year ended December 31, 2009, we generated operating income of $108.3 million and Adjusted EBITDA of $184.8 million. Please read “—Non-GAAP Financial Measures” for a reconciliation of Adjusted EBITDA to net income and cash flows from operating activities. In the year ended December 31, 2009, our coal and natural resource management segment contributed $87.5 million, or 81%, to operating income, and our natural gas midstream segment contributed $20.8 million, or 19%, to operating income.

Coal and Natural Resource Management Segment

Our coal and natural resource management segment primarily involves the management and leasing of coal properties and the subsequent collection of royalties. We do not operate any mines, and therefore, we do not have direct exposure to mine operating costs or risks or mine reclamation costs. Coal royalties accounted for 83% of our coal and natural resource management segment revenues in the year ended December 31, 2009. We also earn revenues from other land management activities, such as selling standing timber, leasing fee-based coal-related infrastructure facilities to certain lessees and end-user industrial plants, collecting oil and gas royalties and from coal transportation, or wheelage, fees, which accounted for 17% of our coal and natural resource management segment revenues for the year ended December 31, 2009. We have relatively low maintenance capital expenditure requirements that are associated with our coal and natural resource management activities.

S-1

Table of Contents

As of December 31, 2009, we owned or controlled approximately 829 million tons of proven and probable coal reserves in Central and Northern Appalachia, the Illinois Basin and the San Juan Basin. The following table sets forth reserve information with respect to each of our regions:

| Proven and Probable Coal Reserves as of December 31, 2009 | ||||||||||||

Region | Underground | Surface | Total | Steam | Metallurgical | Total | ||||||

| (tons in millions) | ||||||||||||

Central Appalachia | 443.6 | 160.3 | 603.9 | 514.7 | 89.2 | 603.9 | ||||||

Northern Appalachia | 23.4 | — | 23.4 | 23.4 | — | 23.4 | ||||||

Illinois Basin | 154.2 | 9.7 | 163.9 | 163.9 | — | 163.9 | ||||||

San Juan Basin | — | 37.4 | 37.4 | 37.4 | — | 37.4 | ||||||

Total | 621.2 | 207.4 | 828.6 | 739.4 | 89.2 | 828.6 | ||||||

In the year ended December 31, 2009, our lessees produced 34.3 million tons of coal from our properties and paid us coal royalties revenues of $120.4 million, for an average royalty per ton of $3.51 ($3.34 per ton net of coal royalties expense). The following table sets forth production data with respect to each of our regions:

| Production for the Year Ended December 31, | ||||||

Region | 2009 | 2008 | 2007 | |||

| (tons in millions) | ||||||

Central Appalachia | 18.3 | 19.6 | 18.8 | |||

Northern Appalachia | 3.8 | 3.6 | 4.2 | |||

Illinois Basin | 4.7 | 4.6 | 3.8 | |||

San Juan Basin | 7.5 | 5.9 | 5.7 | |||

Total | 34.3 | 33.7 | 32.5 | |||

Approximately 82% of our coal royalties revenues in 2009 were derived from coal mined on our properties under leases containing royalty rates based on the higher of a fixed base price or a percentage of the gross sales price. However, because our lessees generally sell their coal under long-term contracts (one to five years), payments from these operators are not directly subject to short-term fluctuations in commodity prices. The balance of our coal royalties revenues in 2009 was derived from coal mined on our properties under leases containing fixed royalty rates that escalate annually.

Natural Gas Midstream Segment

Our natural gas midstream segment is engaged in providing natural gas processing, gathering and other related services. As of December 31, 2009, we owned and operated natural gas midstream assets located in Oklahoma and Texas, including six natural gas processing facilities having 400 MMcfd of total capacity and approximately 4,118 miles of natural gas gathering pipelines. Our natural gas midstream operations currently include four natural gas gathering and processing systems and two stand-alone natural gas gathering systems, including: (i) the Panhandle gathering and processing facilities in the Texas/Oklahoma panhandle area; (ii) the Crossroads gathering and processing facilities in east Texas; (iii) the Crescent gathering and processing facilities in central Oklahoma; (iv) the Arkoma gathering system in eastern Oklahoma; (v) the North Texas gathering and pipeline facilities in the Fort Worth Basin; and (vi) the Hamlin gathering and processing facilities in

S-2

Table of Contents

west-central Texas. In addition, we own a 25% member interest in Thunder Creek Gas Services, LLC, or Thunder Creek, a joint venture that gathers and transports coalbed methane in Wyoming’s Powder River Basin.

The following table sets forth information regarding our natural gas midstream assets at and for the year ended December 31, 2009:

Asset | Type | Approximate Length (Miles) | Current Processing Capacity (MMcfd) | Average System Throughput (MMcfd) | |||||

Panhandle System | Gathering pipelines and processing facilities | 1,681 | 260 | 224 | (1) | ||||

Crossroads System | Gathering pipelines and processing facility | 8 | 80 | 47 | |||||

Crescent System | Gathering pipelines and processing facility | 1,701 | 40 | 22 | |||||

Hamlin System | Gathering pipelines and processing facility | 516 | 20 | 8 | |||||

Arkoma System | Gathering pipelines | 78 | — | 13 | |||||

North Texas Gas Gathering System | Gathering pipelines | 134 | — | 18 | |||||

Total | 4,118 | 400 | 332 | ||||||

| (1) | Includes gas processed at other systems connected to the Panhandle System. |

In addition, the Thunder Creek joint venture had gathering pipelines of approximately 558 miles in length and 375 MMcfd of average system throughput at and for the year ended December 31, 2009.

We have recently entered into an agreement with a subsidiary of Range Resources Corporation, or Range, to construct and operate gas gathering and pipeline compression facilities servicing Range’s Marcellus Shale natural gas production located primarily in Lycoming County, Pennsylvania. Our total capital investment in this system is anticipated to range from $170 to $200 million through 2015. We expect that the initial phase of gathering and compression facilities will become operational in the fourth quarter of 2010. Revenues from this contract will be 100% fee-based. Please read “—Recent Developments—PVR Midstream Agreement with Range Resources.”

Our natural gas midstream business earns revenues primarily from gas processing contracts with natural gas producers and from fees charged for gathering natural gas volumes and providing other related services. We also own a natural gas marketing business, which aggregates third-party volumes and sells those volumes into intrastate pipeline systems and at market hubs accessed by various interstate pipelines.

Business Strategies

We intend to pursue the following business strategies:

| • | Expand our natural gas midstream operations by adding new production to existing systems and acquiring or building new gathering and processing assets. We continually |

S-3

Table of Contents

seek new supplies of natural gas both to offset the natural declines in production from the wells currently connected to our systems and to increase system throughput volumes. New natural gas supplies are obtained for all of our systems by contracting for production from new wells, connecting new wells drilled on dedicated acreage and by contracting for natural gas that has been released from competitors’ systems. During 2009, we acquired a 60 MMcfd processing plant and residue pipeline facilities in western Oklahoma. Additionally, we completed a 40 MMcfd processing plant expansion in our Panhandle system. In March 2010, we entered into an agreement with a subsidiary of Range to construct and operate gas gathering and compression facilities servicing Range’s gas production in the Marcellus Shale formation. Please read “—Recent Developments—PVR Midstream Agreement with Range Resources.” |

| • | Continue to grow coal reserve holdings through acquisitions and investments in our existing market areas. We expect to continue to add to our coal reserve holdings in Central Appalachia and the Illinois Basin in the future, but may consider the acquisition of reserves outside of these basins if the market and quality of the reserves satisfy our criteria. We have historically operated in Central Appalachia, our largest area of coal reserves, but we view the Illinois Basin as a growth area, both because of its proximity to power plants and because we expect future environmental regulations will require the scrubbing of most coals, and not just the higher sulfur coal that is typically found in this basin. We will consider acquisitions of coal reserves that are long-lived and that are of sufficient size to yield significant production or serve as a platform for complementary acquisitions. |

| • | Mitigate commodity price exposure in our natural gas midstream segment. Our natural gas midstream operations consist of a mix of fee-based and margin-based services that, together with our hedging activities, are expected to generate relatively stable cash flows. During the quarter ended December 31, 2009, approximately 19% of the system throughput volumes in our natural gas midstream segment were gathered or processed under fee-based contracts. Our Marcellus Shale project with Range, when operational, will generate fee-based revenues from a combination of firm reservation charges and additional fees based on delivered volumes. Under fee-based contracts, we are not exposed directly to commodity price risk. The remainder of our system throughput volumes were gathered or processed under gas purchase/keep-whole arrangements and percentage-of-proceeds arrangements that are subject to commodity price risk. However, we expect to manage our exposure to commodity price risk by entering into hedging transactions. Based upon volumes as of December 31, 2009 and after giving effect to additional hedging agreements we entered into on March 29, 2010, we have entered into hedging agreements covering approximately58% and 56% of our commodity price-sensitive volumes in 2010 and 2011. We generally target hedging 50% to 60% of our commodity price-sensitive volumes covering a two-year period. |

| • | Expand in areas that complement our coal royalty business. Coal infrastructure and timber projects typically involve long-lived, fee-based assets that generally produce predictable cash flows. We own a number of coal infrastructure facilities. We also have an equity interest in a coal handling joint venture, which is expected to provide development opportunities for coal-related infrastructure projects. We also own or control approximately 243,000 acres of forestlands in Appalachia, which primarily produce various hardwoods. |

S-4

Table of Contents

Competitive Strengths

We believe we are well positioned to execute our business strategies successfully because of the following competitive strengths:

| • | Strategically located natural gas midstream assets. Our natural gas midstream assets are primarily located in Oklahoma and the panhandle of Texas, where natural gas reserves are generally characterized as being moderately declining and long-lived, and east Texas, where we believe natural gas exploration, development and production activities present significant opportunities to generate additional system throughput volumes. We expect that in the fourth quarter of 2010, we will put into operation the initial phase of gathering and compression facilities in the Marcellus Shale formation. Please read “—Recent Developments—PVR Midstream Agreement with Range Resources.” We believe that the Marcellus Shale is one of the most prolific natural gas formations in the United States and that our facilities in Lycoming County, Pennsylvania, once fully operational, will have substantial throughput volumes. We believe that our presence in these regions provides us with a competitive advantage in capturing new supplies of natural gas. |

| • | High quality, diverse and strategically located coal reserves. Our coal reserves cover a range of sulfur and heat content and consist of both steam coal and metallurgical coal that are marketable to a diverse customer base. We believe that our higher sulfur Illinois Basin and Northern Appalachian coal will benefit from the ongoing installation of scrubbers at the power plants supplied by our coal. Our Appalachian coal reserves also include metallurgical grade coal, which commands a market premium compared to other grades of coal. In addition, our coal reserves are primarily located on or near major coal hauling railroads and inland waterways that serve Central Appalachia and the Illinois Basin. We believe that this geographic location of our coal reserves gives our lessees a transportation cost advantage to their domestic customers. We also believe that our Appalachian coal reserves are well situated to capitalize on the current favorable export market given their geographical proximity to East Coast ports, which provide access to transoceanic shipments. |

| • | Coal royalty structure that maintains stable and predictable coal-related cash flows and limits exposure to coal mining operational and regulatory costs. Our coal leases, which are generally 10 to 15 years in duration, provide either for royalty rates equal to the higher of a fixed minimum rate or a percentage of the gross sales price received by our lessees for the coal they produce from our reserves or for a fixed royalty rate. This structure allows our earnings and cash flow to be stable and predictable in periods of low coal prices, while enabling us to benefit during periods of high coal prices. We also indirectly benefit from the long-term fixed price coal sales contracts our lessees have with their end users, which we believe are typically one to five years in duration, because the royalty rates our lessees pay to us will be fixed during the terms of those contracts. In addition, because we do not operate any mines, we do not directly bear any operational or regulatory costs, such as environmental or occupational health and safety costs and liabilities. |

| • | Broad range of services and long-term contracts and relationships with active natural gas producers. Our natural gas supply strategy for our natural gas midstream segment is to establish long-term, integrated and comprehensive midstream services to our natural gas producers. We provide natural gas gathering, compression, dehydration, treating, processing and marketing and NGL fractionation services to natural gas producers. We |

S-5

Table of Contents

believe our ability to provide this broad range of services gives us an advantage in competing for new supplies of natural gas because we can provide all of the services producers require to connect their natural gas quickly and efficiently. We have long-term contracts with many of the most active producers in the areas served by our natural gas midstream assets. |

| • | Experienced coal mine operator lessees that have long-term relationships with a diverse group of major customers. We lease our coal reserves principally to lessees that we believe have substantial experience as coal mine operators, established reputations in the industry and strong relationships with a diverse group of major electric utilities, independent power producers and other commercial and industrial customers. |

| • | Well positioned to pursue acquisition and expansion opportunities. We have a proven track record of successfully growing our business through organic growth projects and acquisitions of coal and natural resource properties and natural gas midstream assets. Since our initial public offering in October 2001, we have completed numerous accretive acquisitions with an aggregate purchase price of approximately $1.1 billion and expended approximately $188.9 million on expansion projects. We intend to use all of the net proceeds from this offering to repay a portion of the borrowings outstanding under our revolving credit facility, or Revolver, which will increase our borrowing capacity and provide us with greater flexibility to fund organic growth projects and pursue potential acquisitions as they arise. |

| • | Senior management team with substantial industry experience. In connection with Penn Virginia’s ongoing reduction of its limited partner interest in PVG, our general partner has a new chief executive officer and chief financial officer who are not officers of Penn Virginia. William H. Shea, Jr., our new Chief Executive Officer, and Robert B. Wallace, our new Executive Vice President and Chief Financial Officer, bring to their new positions substantial industry experience, including from their prior service in such roles at Buckeye GP LLC, the general partner of a major midstream publicly traded partnership, Buckeye Partners, L.P. (NYSE: BPL). Please read “Management—Our Executive Officers and Directors.” At the same time, our operational management remains unchanged to provide continuity. Our Co-Presidents and Chief Operating Officers of our coal and midstream business segments will continue to operate their respective businesses. Members of our executive management team and the heads of our principal business segments have, on average, 30 years of experience in the industries in which we operate. |

Recent Developments

Certain Estimated Unaudited Financial Measures for the Three Months Ended March 31, 2010

Our consolidated financial statements for the three months ended March 31, 2010 are not yet available. Based on preliminary information, we currently estimate that for the three months ended March 31, 2010, our operating income will be between $26.5 million and $28.5 million and our depreciation, depletion and amortization will be between $17.5 million and $18.0 million. The foregoing estimates are based on preliminary information relating to the first quarter of 2010. We caution that we have not completed our normal quarter-end closing and review processes for the first quarter of 2010, and that actual results could differ materially from the foregoing estimates.

S-6

Table of Contents

PVR Midstream Agreement with Range Resources

On March 10, 2010, a subsidiary of the operating company for our natural gas midstream segment, PVR Midstream LLC, or PVR Midstream, entered into an agreement with a subsidiary of Range to construct and operate gas gathering pipelines and compression facilities servicing Range’s Marcellus Shale natural gas production primarily in Lycoming County, Pennsylvania.

PVR Midstream and Range have agreed to an area of mutual interest, or AMI, that covers parts of Lycoming, Tioga and Bradford Counties in north central Pennsylvania, in which Range currently holds a substantial acreage position. Within this AMI, PVR Midstream will construct approximately 16 miles of 24- and 30-inch gathering trunklines, smaller-diameter field gathering lines and compression facilities required to gather Range’s production from the AMI. The gathering system is expected to have over 700 MMcfd of throughput capacity, and the initial phase is expected to become operational in the fourth quarter of 2010. The agreement provides Range significant firm gathering capacity in the system, and PVR Midstream will be compensated for the gathering and compression services provided to Range through a combination of firm reservation charges and additional fees based on delivered volumes, with no direct commodity exposure. Excess capacity on the system and the location within a core area of Marcellus Shale development may provide opportunities for PVR Midstream to develop additional revenues by providing gathering and compression services to other third-party producers in the area.

PVR Midstream’s total capital investment in this system is anticipated to range from $170 to $200 million and is expected to be expended between 2010 and 2015, with $35 to $40 million planned for 2010.

PVR Midstream Agreement to Construct Gas Gathering and Compression Facilities

On March 1, 2010, PVR Midstream entered into an agreement to construct and operate gas gathering pipelines and compression facilities servicing a private firm’s Marcellus Shale natural gas production in Wyoming County, Pennsylvania. Pursuant to the terms of the agreement, PVR Midstream will construct a 12-inch gathering pipeline and compression facilities with 25 MMcfd of throughput capacity and the potential for additional system extensions. PVR Midstream’s 2010 capital investment in this system is anticipated to range from $6 to $7 million, with potential future system extensions costing up to $10 million.

Sale by Penn Virginia of PVG Limited Partner Interests

On March 31, 2010, a subsidiary of Penn Virginia sold 10,000,000 common units of PVG that it beneficially owned in an underwritten public offering. PVG is the sole member of Penn Virginia Resource GP, LLC, our general partner, or PVR GP. As a result of this sale, Penn Virginia, which previously had beneficially owned 51.4% of the outstanding common units of PVG, now beneficially owns25.8% of PVG’s outstanding common units. This sale followed an earlier offering by a subsidiary of Penn Virginia in the third quarter of 2009, that reduced Penn Virginia’s beneficial ownership in PVG’s common units from 77.0% to 51.4%.

Changes in Our Governance

In connection with Penn Virginia’s reduction of its limited partner interest in PVG, we implemented certain changes in our partnership’s governance as a result of which the right to elect half the members of our general partner’s board of directors was given to our unaffiliated limited

S-7

Table of Contents

partners. On March 31, 2010, PVG and the Partnership entered into the Fifth Amended and Restated Limited Liability Company Agreement of PVR GP (as so amended, the “PVR GP LLC Agreement”), and PVR GP entered into Amendment No. 2 to the Third Amended and Restated Agreement of Limited Partnership of PVR (as amended, the “PVR Partnership Agreement”). Pursuant to the PVR GP LLC Agreement, the number of directors constituting the board of directors of PVR GP is six, consisting of three Class A directors and three Class B directors. The limited partners of PVR, other than PVG GP, PVG and their respective affiliates have the right to nominate and vote in the election of the three Class A directors to the board of directors of PVR GP. PVG has a right to appoint the three Class B directors to the board of directors of PVR GP. In the event of a tie vote, the board of directors of PVR GP has delegated to Penn Virginia the right to break the tie. This right is subject to termination under certain circumstances.

Changes in Our Management

In connection with Penn Virginia’s reduction of its limited partner interest in PVG, we implemented certain changes in management, as a result of which certain executive officers of Penn Virginia resigned as executive officers and directors of our general partner and were replaced in such positions by persons who are not executive officers of Penn Virginia. On March 8, 2010, A. James Dearlove resigned from his position as Chief Executive Officer of PVR GP, and on March 9, 2010, he resigned from his position as President and Chief Executive Officer of PVG GP. On March 8, 2010, the board of directors of PVR GP appointed William H. Shea, Jr. to the position of Chief Executive Officer of PVR GP, and on March 9, 2010 the board of directors of PVG GP appointed Mr. Shea to the positions of President and Chief Executive Officer of the PVG GP. Please read “Management—Our Executive Officers and Directors” for biographical information regarding Mr. Shea. On March 23, 2010, Frank A. Pici resigned from his position as Vice President and Chief Financial Officer of PVR GP, and his position as Vice President and Chief Financial Officer of PVG GP. On March 23, 2010, the board of directors of PVR GP appointed Robert B. Wallace to the position of Executive Vice President and Chief Financial Officer of PVR GP, and the board of directors of PVG appointed Mr. Wallace to the position of Executive Vice President and Chief Financial Officer of PVG GP. Please read “Management—Our Executive Officers and Directors” for biographical information regarding Mr. Wallace. On March 31, 2010, A. James Dearlove, Frank A. Pici and Nancy M. Snyder each resigned from their positions as directors on the board of directors of PVR GP. On March 31, 2010, Mr. Shea was appointed as a director on the board of directors of PVR GP and on the board of directors of PVG GP.

Prospective Matters

From time to time we engage in discussions with potential sellers regarding the possible purchase of coal or other natural resources properties or natural gas midstream assets. These potential acquisition opportunities consist of smaller acquisitions as well as larger acquisitions that could have a material impact on our capital structure and operating results. We cannot predict the likelihood of completing, or the timing of, any such acquisition.

Principal Executive Offices

Our principal executive offices are located at Four Radnor Corporate Center, Suite 200, 100 Matsonford Road, Radnor, Pennsylvania 19087. Our telephone number is (610) 687-8900.

S-8

Table of Contents

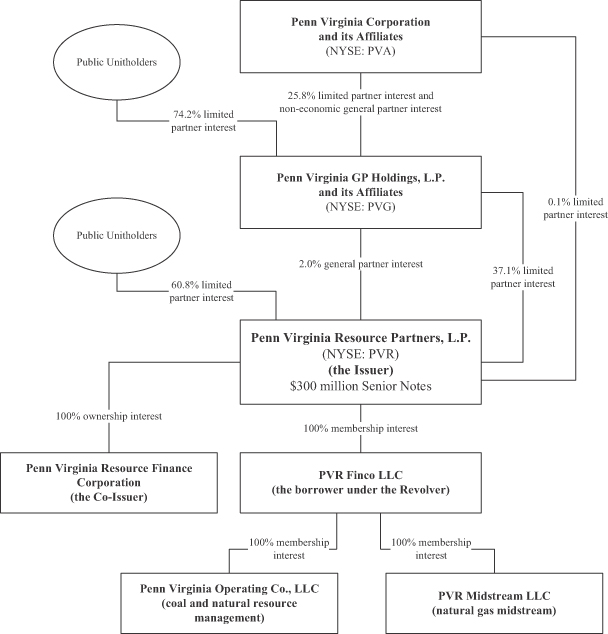

Summary Partnership Structure

Our general partner is Penn Virginia Resource GP, LLC, which is a wholly owned subsidiary of PVG. Penn Virginia beneficially owns an approximate 25.8% limited partner interest in PVG, as well as the non-economic general partner interest in PVG. PVG owns an approximate 37.1% limited partner interest in us, as well as 100% of our general partner, which owns a 2% general partner interest in us and all of our incentive distribution rights.

Our operations are conducted through, and our operating assets are owned by, our subsidiaries. We own our subsidiaries through PVR Finco LLC, which is the borrower under our Revolver. The following diagram depicts our and our affiliates’ simplified organizational and ownership structure as of April 12, 2010:

S-9

Table of Contents

The Offering

The following summary contains basic information about the notes and is not intended to be complete. For a more complete understanding of the notes, please refer to the section entitled “Description of Notes” beginning on pageS-111 in this prospectus supplement.

Issuers | Penn Virginia Resource Partners, L.P. and Penn Virginia Resource Finance Corporation. |

Penn Virginia Resource Finance Corporation is our wholly owned direct subsidiary that was incorporated in Delaware for the purpose of serving as a co-issuer of the notes. Penn Virginia Resource Finance Corporation has no material assets and does not conduct any operations. As a result, you should not expect Penn Virginia Resource Finance Corporation to participate in servicing the interest and principal obligations on the notes.

Securities Offered | $300,000,000 aggregate principal amount of 8 1/4% Senior Notes due 2018. |

Maturity | April 15, 2018. |

Interest | Interest on the notes will accrue at a rate per annum equal to 8 1/4%. |

Interest Payment Dates | April 15 and October 15 of each year, beginning October 15, 2010. |

Guarantees | The notes will be fully and unconditionally guaranteed on a senior basis by our existing and future domestic restricted subsidiaries, subject to certain exceptions. |

Ranking | The notes and the related guarantees will be the unsecured senior obligations of us, Penn Virginia Resource Finance Corporation and the guarantors. Accordingly, they will rank: |

| • | effectively subordinated to all of our, Penn Virginia Resource Finance Corporation’s and the guarantors’ existing and future secured debt, including debt under our Revolver, to the extent of the value of the assets securing such debt; |

| • | structurally subordinated to all existing and future indebtedness and obligations of any of our present and future subsidiaries that do not guarantee the notes; |

| • | equal in right of payment with our, Penn Virginia Resource Finance Corporation’s and the guarantors’ existing and future unsecured senior debt; and |

S-10

Table of Contents

| • | senior to all of our, Penn Virginia Resource Finance Corporation’s and the guarantors’ existing and future debt that expressly provides that it is subordinated to the notes or the respective guarantees. |

As of December 31, 2009, after giving effect to this offering and the application of the net proceeds therefrom, we would have had $628.1 million of debt outstanding, $328.1 million of which would have been secured indebtedness, and we would have had $470.3 million of remaining borrowing capacity under our Revolver (net of $1.6 million of outstanding letters of credit). As of December 31, 2009, our non-guarantor subsidiaries had no indebtedness outstanding. Please read “Capitalization.”

Optional Redemption | Beginning on April 15, 2014, we may redeem some or all of the notes at the redemption prices listed under “Description of Notes—Optional Redemption” plus accrued and unpaid interest on the notes to the date of redemption. |

Before April 15, 2014, we may redeem some or all of the notes at the “make-whole” redemption price set forth under “Description of Notes—Optional Redemption” plus accrued and unpaid interest on the notes to the date of redemption.

At any time prior to April 15, 2013 we may redeem up to 35% of the notes from the proceeds of certain sales of our equity securities at 108.250% of the principal amount, plus accrued and unpaid interest, if any, to the date of redemption. We may make that redemption only if, after the redemption, at least 65% of the aggregate principal amount of the notes remains outstanding and the redemption occurs within 60 days of the closing of the equity offering. Please read “Description of Notes—Optional Redemption.”

Change of Control | Upon the occurrence of a change of control (as described under “Description of Notes—Repurchase at the Option of Holders—Change of Control”), we must offer to repurchase the notes at 101% of the principal amount of the notes, plus accrued and unpaid interest to the date of repurchase. |

Covenants | The indenture governing the notes contains certain covenants limiting our ability and the ability of our restricted subsidiaries to, under certain circumstances: |

| • | prepay subordinated indebtedness, pay distributions, redeem stock or make certain other restricted payments; |

| • | make certain restricted investments; |

| • | incur indebtedness; |

| • | create liens on our assets to secure debt; |

S-11

Table of Contents

| • | restrict dividends, distributions or other payments from subsidiaries to us; |

| • | enter into transactions with affiliates; |

| • | designate subsidiaries as unrestricted subsidiaries; |

| • | sell or otherwise transfer or dispose of assets, including equity interests of restricted subsidiaries; |

| • | use the proceeds of permitted sales of assets; |

| • | effect a consolidation or merger; and |

| • | change our line of business. |

These covenants are subject to important exceptions and qualifications as described in this prospectus supplement under the caption “Description of Notes—Certain Covenants.” In addition, certain of the covenants listed above will terminate before the notes mature if both of the specified rating agencies assign the notes an investment grade rating in the future and no events of default exist under the indenture. Any covenants that cease to apply to us as a result of achieving investment grade ratings will not be restored, even if the credit ratings assigned to the notes later fall below investment grade.

Use of Proceeds | We will use all of the net proceeds of this offering to reduce outstanding indebtedness under our Revolver. Please read “Use of Proceeds” and “Underwriting—Conflicts of Interest.” |

Risk Factors | Please read “Risk Factors” beginning on pageS-17 and the other information in this prospectus supplement, the base prospectus and the documents incorporated by reference herein and therein for a discussion of factors you should carefully consider before making an investment in the notes. |

Conflicts of Interest | Affiliates of each of the underwriters, excluding Credit Suisse Securities (USA) LLC, are lenders or agents under our Revolver. As a result, this offering is being conducted in accordance with the applicable requirements of Financial Industry Regulatory Authority, or FINRA, Rule 5110 regarding the underwriting of securities of a company with a member that has a conflict of interest within the meaning of those rules. Credit Suisse Securities (USA) LLC has agreed to act as the qualified independent underwriter with respect to this offering. See “Underwriting — Conflicts of Interest.” |

S-12

Table of Contents

Summary Historical Financial and Operating Data

The following tables present historical financial and operating data for the periods and the dates indicated. Our summary historical financial data as of and for the years ended December 31, 2009, 2008 and 2007 have been derived from our audited consolidated financial statements and the notes thereto.

The following tables should be read together with, and are qualified in their entirety by reference to, our historical financial statements and the accompanying notes included elsewhere in this prospectus supplement. The tables should also be read together with “Selected Historical Financial and Operating Data” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

| Year Ended December 31, | ||||||||||||

| 2009 | 2008 | 2007 | ||||||||||

(in thousands, except per unit data) | ||||||||||||

Income Statement Data: | ||||||||||||

Revenues: | ||||||||||||

Natural gas midstream | $ | 504,789 | $ | 720,002 | $ | 433,174 | ||||||

Coal royalties | 120,435 | 122,834 | 94,140 | |||||||||

Coal services | 7,332 | 7,355 | 7,252 | |||||||||

Other | 24,148 | 31,389 | 14,879 | |||||||||

Total revenues | 656,704 | 881,580 | 549,445 | |||||||||

Expenses: | ||||||||||||

Cost of midstream gas purchased | 406,583 | 612,530 | 343,293 | |||||||||

Operating | 35,111 | 32,677 | 20,964 | |||||||||

Taxes other than income | 4,794 | 4,258 | 3,036 | |||||||||

General and administrative | 30,168 | 26,906 | 22,915 | |||||||||

Impairments | 1,511 | 31,801 | — | |||||||||

Depreciation, depletion and amortization | 70,235 | 58,166 | 41,512 | |||||||||

Total expenses | 548,402 | 766,338 | 431,720 | |||||||||

Operating income | 108,302 | 115,242 | 117,725 | |||||||||

Other income (expense): | ||||||||||||

Interest expense | (24,653 | ) | (24,672 | ) | (17,338 | ) | ||||||

Other gain/(loss) | 1,280 | (2,907 | ) | 1,804 | ||||||||

Derivatives gain/(loss) | (19,714 | ) | 16,837 | (45,568 | ) | |||||||

Net income | $ | 65,215 | $ | 104,500 | $ | 56,623 | ||||||

General partner’s interest in net income | $ | 24,962 | $ | 23,715 | $ | 14,224 | ||||||

Limited partners’ interest in net income | $ | 40,253 | $ | 80,785 | $ | 42,399 | ||||||

Basic and diluted net income per limited partner unit | $ | 0.76 | $ | 1.63 | $ | 0.92 | ||||||

Weighted average number of units outstanding, basic and diluted | 51,799 | 49,495 | 46,103 | |||||||||

S-13

Table of Contents

| Year Ended December 31, | ||||||||||||

| 2009 | 2008 | 2007 | ||||||||||

| (in thousands, except ratios and operating data) | ||||||||||||

Balance Sheet Data (at period-end): | ||||||||||||

Net property, plant and equipment | $ | 900,844 | $ | 895,119 | $ | 731,282 | ||||||

Total assets | 1,208,060 | 1,218,819 | 931,279 | |||||||||

Total debt | 620,100 | 568,100 | 411,714 | |||||||||

Total liabilities | 731,553 | 688,137 | 560,003 | |||||||||

Partners’ capital | 476,507 | 530,682 | 371,276 | |||||||||

Cash Flow Data: | ||||||||||||

Net cash provided by (used in): | ||||||||||||

Operating activities | $ | 159,972 | $ | 139,176 | $ | 127,824 | ||||||

Investing activities | (79,530 | ) | (331,030 | ) | (224,182 | ) | ||||||

Financing activities | (81,267 | ) | 181,808 | 104,448 | ||||||||

Distributions paid per limited partner unit | $ | 1.880 | $ | 1.820 | $ | 1.660 | ||||||

Other Financial Data: | ||||||||||||

Adjusted EBITDA(1) | $ | 184,777 | $ | 169,092 | $ | 147,572 | ||||||

Ratio of total debt to adjusted EBITDA(1) | 3.4x | 3.4x | 2.8x | |||||||||

Ratio of earnings to fixed charges(2) | 3.3x | 4.9x | 3.8x | |||||||||

Expansion capital expenditures | $ | 36,863 | $ | 59,385 | $ | 38,771 | ||||||

Other capital expenditures | 8,584 | 14,700 | 9,851 | |||||||||

Acquisitions | 29,581 | 286,492 | 176,918 | |||||||||

Operating Data: | ||||||||||||

System throughput volumes (MMcfd) | 332 | 270 | 186 | |||||||||

Gross processing margin ($/Mcf) | $ | 0.81 | $ | 1.09 | $ | 1.33 | ||||||

Coal owned or controlled (millions of tons) | 829 | 827 | 818 | |||||||||

Coal produced by lessees (millions of tons) | 34.3 | 33.7 | 32.5 | |||||||||

Average royalty revenues per ton ($/ton) | $ | 3.51 | $ | 3.65 | $ | 2.89 | ||||||

Average royalty revenues per ton by area ($/ton): | ||||||||||||

Central Appalachia | $ | 4.65 | $ | 4.78 | $ | 3.66 | ||||||

Northern Appalachia | $ | 1.83 | $ | 1.84 | $ | 1.53 | ||||||

Illinois Basin | $ | 2.63 | $ | 2.28 | $ | 1.97 | ||||||

San Juan Basin | $ | 2.12 | $ | 2.06 | $ | 2.00 | ||||||

| (1) | Adjusted EBITDA is a non-GAAP financial measure. Please see “—Non-GAAP Financial Measures” for a reconciliation of Adjusted EBITDA to net income and cash flows from operating activities. |

| (2) | For purposes of determining the ratio of earnings to fixed charges, earnings are defined as the aggregate of income from continuing operations (before adjustment for equity earnings), fixed charges and distributions from equity investment, less capitalized interest. Fixed charges consist of interest expense (including amounts capitalized), amortization of debt costs and the portion of rental expense representing the interest factor. After giving effect to the issuance and sale of the notes in this offering and the application of the net proceeds therefrom to repay a portion of the borrowings outstanding under our Revolver as described under “Use of Proceeds,” our ratio of earnings to fixed charges would have been 2.1x for the year ended December 31, 2009. |

S-14

Table of Contents

Non-GAAP Financial Measures

We include in this prospectus supplement the non-GAAP financial measures EBITDA and Adjusted EBITDA and provide reconciliations of these non-GAAP financial measures to their most directly comparable financial measures calculated and presented in accordance with GAAP.

We define EBITDA as net income plus interest expense, provision for income taxes and depreciation, depletion and amortization, or DD&A, expenses. Adjusted EBITDA represents EBITDA plus impairments, plus an adjustment for equity earnings, net of distributions received, plus derivative losses (gains) included in net income, plus cash settlements of derivatives.

EBITDA and Adjusted EBITDA are used as supplemental financial measures by our management and by external users of our financial statements such as investors, commercial banks, research analysts and others to assess:

| • | the financial performance of our assets without regard to financing methods, capital structure, historical cost basis or the non-cash effects of derivative transactions; |

| • | the ability of our assets to generate cash sufficient to pay interest costs and support our indebtedness, including the notes; |

| • | our operating performance and return on capital as compared to those of other companies, without regard to financing methods or capital structure; and |

| • | the viability of acquisitions and capital expenditure projects and the overall rates of return on alternative investment opportunities. |

EBITDA and Adjusted EBITDA are also financial measurements that are reported to our banks and are used to compute our financial covenants under our Revolver. We have calculated Adjusted EBITDA herein in the same manner as the measure in such financial covenants in our Revolver defined as “EBITDA.” See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Financial Condition—Covenant Compliance.” EBITDA and Adjusted EBITDA should not be considered alternatives to net income, operating income, cash flows from operating activities or any other measure of financial performance presented in accordance with GAAP. Our EBITDA and Adjusted EBITDA may not be comparable to EBITDA, Adjusted EBITDA or similarly titled measures of other entities, as other entities may not calculate EBITDA and Adjusted EBITDA in the same manner as we do. EBITDA and Adjusted EBITDA have limitations as analytical tools, and you should not consider them in isolation from, or as a substitute for analysis of, our financial information prepared in accordance with GAAP. Some of these limitations are:

| • | they do not reflect cash outlays for capital expenditures or future contractual commitments; |

| • | they do not reflect changes in, or cash requirements for, working capital; |

| • | they do not reflect interest expense or the cash requirements necessary to service interest, or principal payments, on indebtedness; |

| • | they do not reflect income tax expense or the cash necessary to pay income taxes; |

S-15

Table of Contents

| • | they do not reflect available liquidity to Penn Virginia Resource Partners; and |

| • | other entities, including entities in our industry, may not use such measures or may calculate such measures differently than as presented in this prospectus supplement, limiting their usefulness as comparative measures. |

The following table presents a reconciliation of the non-GAAP financial measures of EBITDA and Adjusted EBITDA to the GAAP financial measures of net income and cash flows from operating activities on a historical basis for each of the periods indicated.

| Year Ended December 31, | ||||||||||||

| 2009 | 2008 | 2007 | ||||||||||

| (in thousands) | ||||||||||||

Reconciliation of net income to Adjusted EBITDA: | ||||||||||||

Net income | $ | 65,215 | $ | 104,500 | $ | 56,623 | ||||||

Depreciation, depletion and amortization | 70,235 | 58,166 | 41,512 | |||||||||

Interest expense | 24,653 | 24,672 | 17,338 | |||||||||

EBITDA | 160,103 | 187,338 | 115,473 | |||||||||

Impairments | 1,511 | 31,801 | — | |||||||||

Equity earnings, net of distributions received | (2,537 | ) | (224 | ) | (285 | ) | ||||||

Derivative losses (gains) | 22,700 | (11,357 | ) | 50,163 | ||||||||

Cash settlements of derivatives | 3,000 | (38,466 | ) | (17,779 | ) | |||||||

Adjusted EBITDA | $ | 184,777 | $ | 169,092 | $ | 147,572 | ||||||

Reconciliation of cash flows from operating activities to Adjusted EBITDA: | ||||||||||||

Cash flows from operating activities | $ | 159,972 | $ | 139,176 | $ | 127,824 | ||||||

Changes in operating assets and liabilities | 5,308 | 6,529 | 2,243 | |||||||||

Non-cash interest expense | (4,391 | ) | (2,693 | ) | (678 | ) | ||||||

Interest expense | 24,653 | 24,672 | 17,338 | |||||||||

Equity earnings, net of distributions received | 2,537 | 224 | 285 | |||||||||

Derivative gains (losses) | (22,700 | ) | 11,357 | (50,163 | ) | |||||||

Cash settlements of derivatives | (3,000 | ) | 38,466 | 17,779 | ||||||||

Impairments | (1,511 | ) | (31,801 | ) | — | |||||||

Other | (765 | ) | 1,408 | 845 | ||||||||

EBITDA | 160,103 | 187,338 | 115,473 | |||||||||

Impairments | 1,511 | 31,801 | — | |||||||||

Equity earnings, net of distributions received | (2,537 | ) | (224 | ) | (285 | ) | ||||||

Derivative losses (gains) | 22,700 | (11,357 | ) | 50,163 | ||||||||

Cash settlements of derivatives | 3,000 | (38,466 | ) | (17,779 | ) | |||||||

Adjusted EBITDA | $ | 184,777 | $ | 169,092 | $ | 147,572 | ||||||

S-16

Table of Contents

This offering involves a high degree of risk. Before deciding to invest in the notes, you should consider carefully the risks and uncertainties described below with all of the other information included or incorporated by reference in this prospectus supplement, including the risk factors contained in Item 1A of our Annual Report on Form 10-K for the year ended December 31, 2009. While these are the risks and uncertainties we believe are most important for you to consider, you should know that they are not the only risks or uncertainties facing us or which may adversely affect our business. If any of these risks actually occur, our business, financial condition or results of operations could be materially adversely affected.

Risks Related to Our Coal and Natural Resource Management Business

If our lessees do not manage their operations well or experience financial difficulties, their production volumes and our coal royalties revenues could decrease.

We depend on our lessees to effectively manage their operations on our properties. Our lessees make their own business decisions with respect to their operations, including decisions relating to:

| • | the method of mining; |

| • | credit review of their customers; |

| • | marketing of the coal mined; |

| • | coal transportation arrangements; |

| • | negotiations with unions; |

| • | employee hiring and firing; |

| • | employee wages, benefits and other compensation; |

| • | permitting; |

| • | surety bonding; and |

| • | mine closure and reclamation. |

If our lessees do not manage their operations well, or if they experience financial difficulties, their production could be reduced, which would result in lower coal royalties revenues to us and could have a material adverse effect on our business, results of operations or financial condition.

The coal mining operations of our lessees are subject to numerous operational risks that could result in lower coal royalties revenues.

Our coal royalties revenues are largely dependent on the level of production from our coal reserves achieved by our lessees. The level of our lessees’ production is subject to operating conditions or events that may increase our lessees’ cost of mining and delay or halt production at particular mines for varying lengths of time and that are beyond their or our control, including:

| • | the inability to acquire necessary permits; |

S-17

Table of Contents

| • | changes or variations in geologic conditions, such as the thickness of the coal deposits and the amount of rock embedded in or overlying the coal deposit; |

| • | changes in governmental regulation of the coal industry; |

| • | mining and processing equipment failures and unexpected maintenance problems; |

| • | adverse claims to title or existing defects of title; |

| • | interruptions due to power outages; |

| • | adverse weather and natural disasters, such as heavy rains and flooding; |

| • | labor-related interruptions; |

| • | employee injuries or fatalities; and |

| • | fires and explosions. |

Any interruptions to the production of coal from our reserves could reduce our coal royalties revenues and could have a material adverse effect on our business, results of operations or financial condition. In addition, our coal royalties revenues are based upon sales of coal by our lessees to their customers. If our lessees do not receive payments for delivered coal on a timely basis from their customers, their cash flow would be adversely affected, which could cause our cash flow to be adversely affected and could have a material adverse effect on our business, results of operations or financial condition.

A substantial or extended decline in coal prices could reduce our coal royalties revenues and the value of our coal reserves.

A substantial or extended decline in coal prices from recent levels could have a material adverse effect on our lessees’ operations (including mine closures) and on the quantities of coal that may be economically produced from our properties. In addition, because a majority of our coal royalties are derived from coal mined on our properties under leases containing royalty rates based on the higher of a fixed base price or a percentage of the gross sales price, our coal royalties revenues could be reduced by such a decline. Such a decline could also reduce our coal services revenues and the value of our coal reserves. Additionally, volatility in coal prices could make it difficult to estimate with precision the value of our coal reserves and any coal reserves that we may consider for acquisition. The future state of the global economy, including financial and credit markets and its impact on coal production levels and prices is uncertain. Depending on the longevity and ultimate severity of this downturn, demand for coal may decline, which could adversely affect production and pricing for coal mined by our lessees, and, consequently, adversely effect the royalty income received by us.

We depend on a limited number of primary operators for a significant portion of our coal royalties revenues and the loss of or reduction in production from any of our major lessees would reduce our coal royalties revenues.

We depend on a limited number of primary operators for a significant portion of our coal royalties revenues. In the year ended December 31, 2009, five primary operators, each with multiple leases, accounted for 61% of our coal royalties revenues and 11% of our total consolidated revenues. If any of these operators enters bankruptcy, decides to cease operations or significantly reduces its production, our coal royalties revenues would be reduced.

S-18

Table of Contents

A failure on the part of our lessees to make coal royalty payments could give us the right to terminate the lease, repossess the property or obtain liquidation damages and/or enforce payment obligations under the lease. If we repossessed any of our properties, we would seek to find a replacement lessee. We may not be able to find a replacement lessee and, if we find a replacement lessee, we may not be able to enter into a new lease on favorable terms within a reasonable period of time. In addition, the outgoing lessee could be subject to bankruptcy proceedings that could further delay the execution of a new lease or the assignment of the existing lease to another operator. If we enter into a new lease, the replacement operator might not achieve the same levels of production or sell coal at the same price as the lessee it replaced. In addition, it may be difficult for us to secure new or replacement lessees for small or isolated coal reserves, since industry trends toward consolidation favor larger-scale, higher technology mining operations to increase productivity rates.

Our coal business will be adversely affected if we are unable to replace or increase our coal reserves through acquisitions.

Because our reserves decline as our lessees mine our coal, our future success and growth depends, in part, upon our ability to acquire additional coal reserves that are economically recoverable. The current state of the global economy, including financial markets, and the consequential adverse effect on credit availability is adversely impacting our access to new capital and credit availability. Depending on the longevity and ultimate severity of this downturn, our ability to make acquisitions may be significantly adversely affected. If we are unable to negotiate purchase contracts to replace or increase our coal reserves on acceptable terms, our coal royalties revenues will decline as our coal reserves are depleted and we could, therefore, experience a material adverse effect on our business, results of operations or financial condition. If we are able to acquire additional coal reserves, there is a possibility that any acquisition could be dilutive to earnings and reduce our ability to make distributions to unitholders or to pay interest on, or the principal of, our debt obligations. Any debt we incur to finance an acquisition may similarly affect our ability to make distributions to unitholders or to pay interest on, or the principal of, our debt obligations. Our ability to make acquisitions in the future also could be limited by restrictions under our existing or future debt agreements, competition from other coal companies for attractive properties or the lack of suitable acquisition candidates.

Our lessees could satisfy obligations to their customers with coal from properties other than ours, depriving us of the ability to receive amounts in excess of the minimum coal royalties payments.

We do not control our lessees’ business operations. Our lessees’ customer supply contracts do not generally require our lessees to satisfy their obligations to their customers with coal mined from our reserves. Several factors may influence a lessee’s decision to supply its customers with coal mined from properties we do not own or lease, including the royalty rates under the lessee’s lease with us, mining conditions, transportation costs and availability and customer coal quality specifications. If a lessee satisfies its obligations to its customers with coal from properties we do not own or lease, production under our lease will decrease, and we will receive lower coal royalties revenues.

Fluctuations in transportation costs and the availability or reliability of transportation could reduce the production of coal mined from our properties.

Transportation costs represent a significant portion of the total cost of coal for the customers of our lessees. Increases in transportation costs could make coal a less competitive source of energy or could make coal produced by some or all of our lessees less competitive than coal produced from other sources. On the other hand, significant decreases in transportation costs could result in increased competition for our lessees from coal producers in other parts of the country or increased imports from offshore producers.

S-19

Table of Contents

Our lessees depend upon rail, barge, trucking, overland conveyor and other systems to deliver coal to their customers. Disruption of these transportation services due to weather-related problems, strikes, lockouts, bottlenecks, mechanical failures and other events could temporarily impair the ability of our lessees to supply coal to their customers. Our lessees’ transportation providers may face difficulties in the future and impair the ability of our lessees to supply coal to their customers, thereby resulting in decreased coal royalties revenues to us.

Our lessees’ workforces could become increasingly unionized in the future, which could adversely affect their productivity and thereby reduce our coal royalties revenues.

One of our lessees has one mine operated by unionized employees. This mine was our third largest mine on the basis of coal production for the year ended December 31, 2009. All of our lessees could become increasingly unionized in the future. If some or all of our lessees’ non-unionized operations were to become unionized, it could adversely affect their productivity and increase the risk of work stoppages. In addition, our lessees’ operations may be adversely affected by work stoppages at unionized companies, particularly if union workers were to orchestrate boycotts against our lessees’ operations. Any further unionization of our lessees’ employees could adversely affect the stability of production from our coal reserves and reduce our coal royalties revenues.

Our coal reserve estimates depend on many assumptions that may be inaccurate, which could materially adversely affect the quantities and value of our coal reserves.

Our estimates of our coal reserves may vary substantially from the actual amounts of coal our lessees may be able to economically recover. There are numerous uncertainties inherent in estimating quantities of reserves, including many factors beyond our control. Estimates of coal reserves necessarily depend upon a number of variables and assumptions, any one of which may, if incorrect, result in an estimate that varies considerably from actual results. These factors and assumptions relate to:

| • | geological and mining conditions, which may not be fully identified by available exploration data; |

| • | the amount of ultimately recoverable coal in the ground; |

| • | the effects of regulation by governmental agencies; and |

| • | future coal prices, operating costs, capital expenditures, severance and excise taxes and development and reclamation costs. |

Actual production, revenues and expenditures with respect to our coal reserves will likely vary from estimates, and these variations may be material. As a result, you should not place undue reliance on the coal reserve data provided by us.

Any change in fuel consumption patterns by electric power generators away from the use of coal could affect the ability of our lessees to sell the coal they produce and thereby reduce our coal royalties revenues.

According to the U.S. Department of Energy, domestic electric power generation accounted for approximately 89% of domestic coal consumption in 2008. The amount of coal consumed for domestic electric power generation is affected primarily by the overall demand for electricity, the price and availability of competing fuels for power plants such as nuclear, natural gas, fuel oil and hydroelectric power and environmental and other governmental regulations. We believe that most

S-20

Table of Contents

new power plants will be built to produce electricity during peak periods of demand. Many of these new power plants will likely be fired by natural gas because of lower construction costs compared to coal-fired plants and because natural gas is a cleaner burning fuel. The increasingly stringent requirements of the Clean Air Act, or the CAA, may result in more electric power generators shifting from coal to natural gas-fired power plants. Please read “Business—Government Regulation and Environmental Matters—Coal and Natural Resource Management Segment—Air Emissions.”

Extensive environmental laws and regulations affecting electric power generators could have corresponding effects on the ability of our lessees to sell the coal they produce and thereby reduce our coal royalties revenues.

Federal, state and local laws and regulations extensively regulate the amount of sulfur dioxide, particulate matter, nitrogen oxides, mercury and other compounds emitted into the air from electric power plants, which are the ultimate consumers of the coal our lessees produce. These laws and regulations can require significant emission control expenditures for many coal-fired power plants, and various new and proposed laws and regulations may require further emission reductions and associated emission control expenditures. As a result of these current and proposed laws, regulations and trends, electricity generators may elect to switch to other fuels that generate less of these emissions, possibly further reducing demand for the coal that our lessees produce and thereby reducing our coal royalties revenues. Please read “Business—Government Regulation and Environmental Matters—Coal and Natural Resource Management Segment—Air Emissions.”

Concerns about the environmental impacts of fossil-fuel emissions, including perceived impacts on global climate change, are resulting in increased regulation of emissions of greenhouse gases in many jurisdictions and increased interest in and the likelihood of further regulation, which could significantly affect our coal royalties revenues.