Exhibit 99.2

MANAGEMENT’S DISCUSSION AND ANALYSIS

FOR THE YEAR ENDED DECEMBER 31, 2017

This Management’s Discussion and Analysis (“MD&A”) for Cenovus Energy Inc. (which includes references to “we”, “our”, “us”, “its”, the “Company”, or “Cenovus”, mean Cenovus Energy Inc., the subsidiaries of, and partnership interests held by, Cenovus Energy Inc. and its subsidiaries) dated February 14, 2018, should be read in conjunction with December 31, 2017 audited Consolidated Financial Statements and accompanying notes (“Consolidated Financial Statements”). All of the information and statements contained in this MD&A are made as of February 14, 2018, unless otherwise indicated. This MD&A contains forward-looking information about our current expectations, estimates, projections and assumptions. The information in this MD&A, as it relates to our operations for 2017, reflects the closing of the Acquisition (as defined in this MD&A) on May 17, 2017. See the Advisory for information on the risk factors that could cause actual results to differ materially and the assumptions underlying our forward-looking information. Cenovus management (“Management”) prepared the MD&A. The Audit Committee of the Cenovus Board of Directors (the “Board”) reviewed and recommended the MD&A for approval by the Board, which occurred on February 14, 2018. Additional information about Cenovus, including our quarterly and annual reports, the Annual Information Form (“AIF”) and Form40-F, is available on SEDAR at sedar.com, on EDGAR at sec.gov, and on our website at cenovus.com. Information on or connected to our website, even if referred to in this MD&A, does not constitute part of this MD&A.

Basis of Presentation

This MD&A and the Consolidated Financial Statements and comparative information have been prepared in Canadian dollars, except where another currency has been indicated, and in accordance with International Financial Reporting Standards (“IFRS” or “GAAP”) as issued by the International Accounting Standards Board (“IASB”). Production volumes are presented on a before royalties basis.

Non-GAAP Measures and Additional Subtotals

Certain financial measures in this document do not have a standardized meaning as prescribed by IFRS, such as Netbacks, Adjusted Funds Flow, Operating Earnings, Free Funds Flow, Debt, Net Debt, Capitalization and Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization (“Adjusted EBITDA”) and therefore are considerednon-GAAP measures. In addition, Operating Margin is considered an additional subtotal found in Notes 1 and 11 of our Consolidated Financial Statements. These measures may not be comparable to similar measures presented by other issuers. These measures have been described and presented in order to provide shareholders and potential investors with additional measures for analyzing our ability to generate funds to finance our operations and information regarding our liquidity. This additional information should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS.

The definition and reconciliation, if applicable, of eachnon-GAAP measure or additional subtotal is presented in the Operating Results, Financial Results, Liquidity and Capital Resources, or Advisory sections of this MD&A.

| | |

| Cenovus Energy Inc. | | 1 2017 Management’s Discussion and Analysis |

OVERVIEW OF CENOVUS

We are a Canadian integrated oil company headquartered in Calgary, Alberta, with our shares listed on the Toronto and New York stock exchanges. On December 31, 2017, we had an enterprise value of approximately $24 billion. We are in the business of developing, producing and marketing crude oil, natural gas liquids (“NGLs”) and natural gas in Western Canada. We also conduct marketing activities and have refining operations in the United States (“U.S.”). Our average crude oil and NGLs (collectively, “liquids”) production in 2017 was 360,704 barrels per day, our average natural gas production was 659 MMcf per day, and our total production was 470,490 BOE per day. The refining operations processed an average of 442,000 gross barrels per day of crude oil feedstock into an average of 470,000 gross barrels per day of refined products.

Year in Review

2017 was a year of significant change for Cenovus, where we gained full ownership of our oil sands assets, acquired an additional core operating area in the Deep Basin and divested the majority of our legacy Conventional assets. On May 17, 2017, we acquired from ConocoPhillips Company and certain of its subsidiaries (collectively, “ConocoPhillips”) their 50 percent interest in the FCCL Partnership (“FCCL”), and the majority of ConocoPhillips’ western Canadian conventional assets in the Deep Basin in Alberta and British Columbia for total consideration of $17.9 billion (“the Acquisition”).

The Acquisition effectively doubled our oil sands production and proved bitumen reserves. In addition, we acquired more than three million net acres of land, exploration and production assets, and related infrastructure in Alberta and British Columbia (collectively, the “Deep Basin Assets”). The Deep Basin Assets are expected to provide short-cycle development opportunities with high-return potential that complement our long-cycle oil sands investments.

The purchase consideration included US$10.6 billion in cash, before adjustments, and 208 million Cenovus common shares. The cash portion of the consideration was funded through a combination of cash on hand, a draw on our existing committed credit facility, an offering of senior unsecured notes (US$2.9 billion), a committed asset-sale bridge credit facility ($3.6 billion) (“Bridge Facility”), and a bought-deal common share offering ($3.0 billion).

In the second half of 2017, we sold the majority of our legacy Conventional crude oil and natural gas assets for aggregate gross cash proceeds of approximately $3.2 billion. The net proceeds and cash on hand were used to fully repay and retire the Bridge Facility. The sale of Suffield, our remaining legacy Conventional segment asset, closed on January 5, 2018 for gross proceeds of $512 million. In aggregate, gross proceeds for all legacy Conventional crude oil and natural gas assets divested was $3.7 billion, before closing adjustments, and resulted in abefore-tax gain on discontinuance of approximately $1.6 billion, of which $1.3 billion was recorded in 2017.

In December 2017, we also commenced marketing for sale certainnon-core assets located in the East and West Clearwater areas of the Deep Basin, representing approximately 15,000 BOE per day of production, to further streamline our portfolio and deleverage our balance sheet.

Over the course of 2017, Cenovus has transitioned its asset base and strategy to support focused development in the oil sands and Deep Basin, providing opportunities for disciplined growth and long-term cash flow generation. At the same time, investor concern about the Acquisition, volatile commodity prices and a number of other factors contributed to a more than 40 percent decline in our share price. Over the last few months, Cenovus has made considerable progress in reducing debt and is taking steps toright-size the Company for the current environment. Effective November 6, 2017, Alex Pourbaix was appointed Cenovus’s President and Chief Executive Officer, and he subsequently announced changes to the senior leadership team in December 2017.

Cenovus’s 2018 budget was announced in December, with total capital expenditures expected to be between $1.5 billion and $1.7 billion. This budget reflects Cenovus’s focus on capital discipline, cost reductions and deleveraging.

Our Strategy

Our strategy is to increase cash flows through disciplined production growth from our industry leading portfolio of oil sands and Deep Basin natural gas and liquids assets in Western Canada. We are focused on increasing our current share price and maximizing shareholder value through cost leadership and realizing the best margins for our products to help us maintain financial resilience and deliver sustainable dividend growth. We plan to achieve our strategy by drawing on the expertise of our people and leveraging our strategic differentiators: premium asset quality, executional excellence, value-added integration, focused innovation and trusted reputation.

Our Key Strategic Differentiators

Premium Asset Quality

Cenovus has a deep portfolio of premium-quality oil sands, natural gas and NGLs assets that we believe provide us with significant cost and environmental performance advantages. Ourin-situ oil sands projects and Deep Basin Assets in Western Canada offer long and short-cycle opportunities that provide the capital investment flexibility to position us to deliver value growth at various points of the price cycle. In addition to our exploration and production assets, we have complementary interests in refineries and product transportation infrastructure.

| | |

| Cenovus Energy Inc. | | 2 2017 Management’s Discussion and Analysis |

Executional Excellence

Our team is committed to delivering on our business plan in a safe, disciplined and responsible manner and continuously improving our performance to help manage risk and optimize returns. We use a manufacturing approach to support consistent performance and enhance reliability. This involves applying standardized and repeatable designs and processes to the construction and operation of our facilities to reduce costs and improve efficiencies at all project stages. We strive to execute our work in an agile manner with a focus on using our resources effectively.

Value-Added Integration

Our integrated business approach helps provide stability to our cash flows and maximize value for the oil and natural gas we produce. Having ownership in oil refineries positions us to capture the full value chain from production to high-quality end products like transportation fuels. In addition, our pipeline commitments,crude-by-rail loading facility and product marketing activities assist us to obtain global pricing for our oil. As a consumer of natural gas at our oil sands facilities and refineries, our natural gas production acts as an economic hedge to help manage price volatility. In addition, our cogeneration plants efficiently provide power for our oil sands facilities with the added value of excess electricity being sold to the Alberta electricity grid.

Focused Innovation

We focus our innovation efforts on accelerating the adoption of technology solutions and methods of operating to enhance safety, reduce costs, improve margins and lower emissions. We expect innovation at Cenovus to mean significant improvements and game-changing developments that are implemented to generate value. We aim to complement our internal technology development efforts with external collaboration that will leverage our technology spend.

Trusted Reputation

We are a responsible, progressive company that is committed to providing a safe and healthy workplace, building strong external relationships, minimizing our environmental footprint and being a part of a lower carbon future. Our actions are intended to support our trusted reputation and enable us to attract and retaintop-quality staff and to engage with and be respected by our stakeholders: investors, the communities in which we operate, environmental groups, governments, Aboriginal people, media, project partners and the general public.

We measure our performance through a scorecard that reflects our financial, operational, safety, environmental and organizational health goals.

Our Operations

Oil Sands

Our oil sands assets include steam-assisted gravity drainage (“SAGD”) oil sands projects in northern Alberta, including Foster Creek, Christina Lake, Narrows Lake and other emerging projects. Foster Creek and Christina Lake are producing, while Narrows Lake is in the initial stages of development. These three projects are located in the Athabasca region of northeastern Alberta, and our project at Telephone Lake is located within the Borealis region of northeastern Alberta. The Oil Sands segment also includes the Athabasca natural gas property, from which a portion of the natural gas production is used as fuel at the adjacent Foster Creek operations.

| | | | | | | | | | |

| | | 2017 | |

| ($ millions) | | Crude Oil | | | | | Natural Gas | |

Operating Margin | | | 2,231 | | | | | | 1 | |

Capital Investment | | | 969 | | | | | | 4 | |

| | | | | | | | | | |

Operating Margin Net of Related Capital Investment | | | 1,262 | | | | | | (3 | ) |

| | | | | | | | | | |

Deep Basin

Our Deep Basin Assets include approximately three million net acres of land rich in natural gas, condensate and other NGLs, and light and medium oil. The assets are located primarily in the Elmworth-Wapiti, Kaybob-Edson, and Clearwater operating areas of British Columbia and Alberta, and include interests in numerous natural gas processing facilities. The Deep Basin Assets are expected to provide short-cycle development opportunities with high return potential that complement our long-term oil sands development and provide an economic hedge for the natural gas required as a fuel source at both our oil sands and refining operations.

| | | | |

| ($ millions) | | May 17 – December 31,

2017 | |

Operating Margin | | | 207 | |

Capital Investment | | | 225 | |

| | | | |

Operating Margin Net of Related Capital Investment | | | (18 | ) |

| | | | |

| | |

| Cenovus Energy Inc. | | 3 2017 Management’s Discussion and Analysis |

Conventional

All references to our legacy Conventional segment are accounted for as a discontinued operation.

In late 2017, we sold the majority of our legacy Conventional crude oil and natural gas assets for gross cash proceeds totaling approximately $3.2 billion, resulting in a netbefore-tax gain on discontinuance of approximately $1.3 billion. The sale of our remaining Conventional segment asset, Suffield, closed on January 5, 2018 for gross proceeds of $512 million and resulted in abefore-tax gain on sale of approximately $350 million.

The Conventional segment produced crude oil, NGLs and natural gas in Alberta and Saskatchewan, including the heavy oil assets at Pelican Lake, the carbon dioxide (“CO2”)enhanced oil recovery project at Weyburn and tight oil opportunities in the Palliser block in southern Alberta.

| | | | | | | | | | |

| | | 2017 | |

| ($ millions) | | Liquids | | | | | Natural Gas | |

Operating Margin | | | 360 | | | | | | 124 | |

Capital Investment | | | 195 | | | | | | 11 | |

| | | | | | | | | | |

Operating Margin Net of Related Capital Investment | | | 165 | | | | | | 113 | |

| | | | | | | | | | |

Refining and Marketing

Our operations include two refineries located in Illinois and Texas that are jointly owned with (50 percent interest) and operated by Phillips 66, an unrelated U.S. public company. The gross crude oil capacity at the Wood River and Borger refineries (the “Refineries”) is approximately 314,000 barrels per day and 146,000 barrels per day, respectively. This includes processing capability of up to 255,000 gross barrels per day of blended heavy crude oil. The refining operations allow us to capture the value from crude oil production through to refined products, such as diesel, gasoline and jet fuel, to partially mitigate volatility associated with regional North American light/heavy crude oil price differential fluctuations.

This segment also includes ourcrude-by-rail terminal operations, located in Bruderheim, Alberta, and the marketing of third-party purchases and sales of product undertaken to provide operational flexibility for transportation commitments, product quality, delivery points and customer diversification.

| | |

| ($ millions) | | 2017 |

| |

Operating Margin | | 598 |

Capital Investment | | 180 |

| | |

Operating Margin Net of Related Capital Investment | | 418 |

| | |

2017 HIGHLIGHTS

In 2017, we completed the Acquisition which gave us full ownership of our oil sands operations and provided an additional core operating area with the Deep Basin Assets.

Including the Suffield divestiture which closed on January 5, 2018, all of our legacy Conventional oil and gas assets have been sold for combined gross cash proceeds of $3.7 billion. Gross proceeds received prior to December 31, 2017 of $3.2 billion, combined with cash on hand, were used to fully repay and retire the $3.6 billion Bridge Facility that was drawn to help fund the Acquisition.

Crude oil prices continued to be volatile throughout the year. West Texas Intermediate (“WTI”) benchmark crude price ranged from a high of US$60.42 per barrel to a low of US$42.53 per barrel and averaged 18 percent higher compared with 2016. Western Canadian Select (“WCS”), a blended heavy oil benchmark, ranged from a high of US$44.79 per barrel to a low of US$29.56 per barrel, while averaging 32 percent higher in 2017 compared to 2016. In addition, natural gas prices were very volatile, ranging from a high of $3.75 per Mcf to a low of $1.07 per Mcf; however, still averaging 16 percent higher than 2016.

In 2017, we:

| ● | | Produced 470,490 BOE per day, a 73 percent increase from 2016; |

| ● | | Earned an average companywide Netback from continuing operations of $20.89 per BOE, before realized hedging, an increase of 78 percent from 2016; |

| ● | | Generated upstream operating margin, excluding the Conventional segment, of $2,394 million compared with $877 million in 2016 primarily due to the Acquisition, a rise in sales volumes and higher liquids sales prices; |

| ● | | Achieved cash from operating activities and Adjusted Funds Flow of $3,059 million and $2,914 million, respectively, increasing significantly from 2016; |

| ● | | Recorded a $275 million tax recovery as a result of the U.S. federal corporate income tax rate change announced in 2017; |

| ● | | Recorded Net Earnings from continuing operations of $2,268 million (2016 – Net Loss from continuing operations of $459 million); |

| ● | | Invested $1,661 million in capital which allowed us to generate Free Funds Flow of $1,253 million, a threefold increase from $397 million in 2016; |

| | |

| Cenovus Energy Inc. | | 4 2017 Management’s Discussion and Analysis |

| · | | Divested of the majority of our legacy Conventional crude oil and natural gas assets, recognizing abefore-tax gain of $1.3 billion in discontinued operations; |

| · | | Announced the appointment of Alex Pourbaix as President and Chief Executive Officer in November, and announced changes to the senior leadership team in December; |

| · | | Re-evaluated our oil sands Exploration & Evaluation (“E&E”) projects in line with our current business plans. As a result, we wrote off $887 million in the fourth quarter as exploration expense; and |

| · | | Announced our 2018 budget in December, focusing on capital discipline, cost reductions and deleveraging. |

OPERATING RESULTS

Our upstream assets continued to perform well in 2017. Total production increased primarily due to the Acquisition, slightly offset by the disposition of legacy Conventional assets late in the year.

Production Volumes

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | 2017 | | | | |

| Percent

Change |

| | | | | 2016 | | | | |

| Percent

Change |

| | | | | 2015 | |

| | | | | | | | | |

Continuing Operations | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Liquids(barrels per day) | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Oil Sands | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Foster Creek | | | 124,752 | | | | | | 78% | | | | | | 70,244 | | | | | | 7% | | | | | | 65,345 | |

Christina Lake | | | 167,727 | | | | | | 111% | | | | | | 79,449 | | | | | | 6% | | | | | | 74,975 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 292,479 | | | | | | 95% | | | | | | 149,693 | | | | | | 7% | | | | | | 140,320 | |

| | | | | | | | | |

Deep Basin | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Light and Medium Oil | | | 3,922 | | | | | | -% | | | | | | - | | | | | | -% | | | | | | - | |

NGLs | | | 16,928 | | | | | | -% | | | | | | - | | | | | | -% | | | | | | - | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 20,850 | | | | | | -% | | | | | | - | | | | | | -% | | | | | | - | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Liquids Production(barrels per day) | | | 313,329 | | | | | | 109% | | | | | | 149,693 | | | | | | 7% | | | | | | 140,320 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Natural Gas(MMcf per day) | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Oil Sands | | | 10 | | | | | | (41)% | | | | | | 17 | | | | | | (11)% | | | | | | 19 | |

Deep Basin | | | 316 | | | | | | -% | | | | | | - | | | | | | -% | | | | | | - | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 326 | | | | | | 1,818% | | | | | | 17 | | | | | | (11)% | | | | | | 19 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Conventional Production(BOE per day) | | | - | | | | | | -% | | | | | | - | | | | | | -% | | | | | | 4,163 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Production From Continuing Operations(BOE per day) | | | 367,635 | | | | | | 141% | | | | | | 152,527 | | | | | | 3% | | | | | | 147,701 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Discontinued Operations (Conventional) | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Liquids(barrels per day) | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Heavy Oil | | | 21,478 | | | | | | (26)% | | | | | | 29,185 | | | | | | (15)% | | | | | | 34,256 | |

Light and Medium Oil | | | 24,824 | | | | | | (4)% | | | | | | 25,915 | | | | | | (10)% | | | | | | 28,675 | |

NGLs | | | 1,073 | | | | | | 1% | | | | | | 1,065 | | | | | | (7)% | | | | | | 1,149 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 47,375 | | | | | | (16)% | | | | | | 56,165 | | | | | | (12)% | | | | | | 64,080 | |

Natural Gas(MMcf per day) | | | 333 | | | | | | (12)% | | | | | | 377 | | | | | | (8)% | | | | | | 412 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Production From Discontinued Operations(BOE per day) | | | 102,855 | | | | | | (14)% | | | | | | 118,998 | | | | | | (10)% | | | | | | 132,746 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | |

Total Production(BOE per day) | | | 470,490 | | | | | | 73% | | | | | | 271,525 | | | | | | (3)% | | | | | | 280,447 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

In 2017, Oil Sands production increased primarily as a result of the Acquisition. Incremental production at Foster Creek and Christina Lake from May 17, 2017, the closing date of the Acquisition, until December 31, 2017 was 76,748 barrels per day and 102,945 barrels per day, respectively. Foster Creek also had incremental production volumes related to the phase G expansion, partially offset by reduced volumes as a result of temporary treating issues and a20-day planned plant turnaround. The phase F expansion at Christina Lake contributed incremental production volumes.

Total production in the Deep Basin averaged 117,138 BOE per day for the period of May 17, 2017 to December 31, 2017. Incremental volumes due to the drilling and completion of horizontal production wells in the second half of the year was partially offset by downtime associated with third party pipeline and facility outages.

Prior to the dispositions, our Conventional liquids production was lower than in 2016 primarily due to expected natural declines partially offset by new production from our tight oil drilling program in the first half of 2017 before growth capital was reduced as a result of the decision to divest the Palliser asset. Our Conventional natural gas production decreased in 2017, relative to the same period in 2016 due to expected natural declines.

| | |

| Cenovus Energy Inc. | | 5 2017 Management’s Discussion and Analysis |

Oil and Gas Reserves

Based on our reserves report prepared by independent qualified reserves evaluators (“IQREs”), our proved bitumen reserves increased 103 percent to approximately 4.75 billion barrels and our proved plus probable bitumen reserves increased 92 percent to approximately 6.38 billion barrels. Our Deep Basin proved reserves were 410 MMBOE and our proved plus probable reserves were 660 MMBOE.

Additional information about our reserves is included in the Oil and Gas Reserves section of this MD&A.

Netbacks From Continuing Operations

Netback is anon-GAAP measure commonly used in the oil and gas industry to assist in measuring operating performance on aper-unit basis, and is defined in the Canadian Oil and Gas Evaluation Handbook. Netbacks reflect our margin on aper-barrel of oil equivalent basis. Netback is defined as gross sales less royalties, transportation and blending, operating expenses and production and mineral taxes divided by sales volumes. Netbacks do not reflect thenon-cash write-downs of product inventory until the product is sold. The sales price, transportation and blending costs, and sales volumes exclude the impact of purchased condensate. Condensate is blended with the heavy oil to reduce its thickness in order to transport it to market. Our Netback calculation is aligned with the definition found in the Canadian Oil and Gas Evaluation Handbook. For a reconciliation of our Netbacks see the Advisory section of this MD&A.

| | | | | | | | | | | | | | | | |

| ($/BOE) | | 2017 | | | | 2016 | | | | 2015 |

Sales Price | | | 36.86 | | | | | | 27.37 | | | | | | 30.81 | |

Royalties | | | 2.07 | | | | | | 0.17 | | | | | | 0.56 | |

Transportation and Blending | | | 5.43 | | | | | | 6.51 | | | | | | 6.34 | |

Operating Expenses | | | 8.46 | | | | | | 8.94 | | | | | | 9.94 | |

Production and Mineral Taxes | | | 0.01 | | | | | | - | | | | | | 0.03 | |

| | | | | | | | | | | | | | | | |

Netback Excluding Realized Risk Management(1) | | | 20.89 | | | | | | 11.75 | | | | | | 13.94 | |

Realized Risk Management Gain (Loss) | | | (2.35 | ) | | | | | 3.22 | | | | | | 7.60 | |

| | | | | | | | | | | | | | | | |

Netback Including Realized Risk Management(1) | | | 18.54 | | | | | | 14.97 | | | | | | 21.54 | |

| | | | | | | | | | | | | | | | |

| (1) | Excludes results from our Conventional segment, which has been classified as a discontinued operation. |

Our average Netback improved primarily due to higher liquids sales prices, partially offset by increased royalties and the strengthening of the Canadian dollar relative to the U.S. dollar. The strengthening of the Canadian dollar compared with 2016 had a negative impact on our sales price of approximately $0.78 per BOE.

Refining and Marketing

Crude oil runs and refined product output in 2017 remained consistent compared with 2016. The planned and unplanned maintenance at both Refineries in 2017 had a similar impact on crude oil runs and refined product output as the planned and unplanned maintenance in 2016.

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | 2017 | | | | Percent Change | | 2016 | | Percent Change | | 2015 |

Crude Oil Runs(1)(Mbbls/d) | | | 442 | | | | | | | | -% | | | | 444 | | | | 6% | | | | 419 | |

Heavy Crude Oil(1) | | | 202 | | | | | | | | (13)% | | | | 233 | | | | 17% | | | | 200 | |

Refined Product(1)(Mbbls/d) | | | 470 | | | | | | | | -% | | | | 471 | | | | 6% | | | | 444 | |

Crude Utilization(1)(percent) | | | 96 | | | | | | | | (1)% | | | | 97 | | | | 6% | | | | 91 | |

| (1) | Represents 100 percent of the Wood River and Borger refinery operations. |

In 2017, Operating Margin from our Refining and Marketing segment increased 73 percent compared with 2016 due to higher average market crack spreads and increased margins on the sale of our secondary products due to higher realized pricing. These increases were partially offset by narrowing heavy crude oil differentials, which increase crude input costs to the refinery, and the strengthening of the Canadian dollar relative to the U.S. dollar.

Further information on the changes in our production volumes, items included in our Netbacks and refining results can be found in the Reportable Segments section of this MD&A. Further information on our risk management activities can be found in the Risk Management and Risk Factors section of this MD&A and in the notes to the Consolidated Financial Statements.

| | |

| Cenovus Energy Inc. | | 6 2017 Management’s Discussion and Analysis |

COMMODITY PRICES UNDERLYING OUR FINANCIAL RESULTS

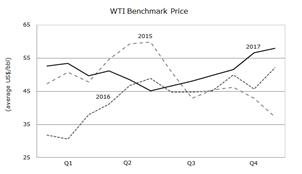

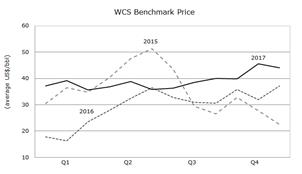

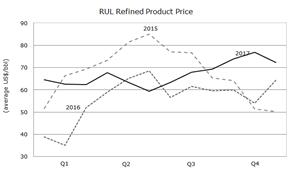

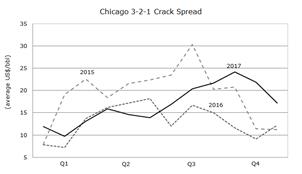

Key performance drivers for our financial results include commodity prices, price differentials, refining crack spreads as well as the U.S./Canadian dollar exchange rate. The following table shows selected market benchmark prices and the U.S./Canadian dollar average exchange rates to assist in understanding our financial results.

Selected Benchmark Prices and Exchange Rates(1)

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| (US$/bbl, unless otherwise indicated) | | Q4 2017 | | Q4 2016 | | 2017 | | | | Percent Change | | 2016 | | 2015 |

Crude Oil Prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

Brent | | | | | | | | | | | | | | | | | | | | | | | | | | |

Average | | | 61.54 | | | | 51.13 | | | | 54.82 | | | | | | 22% | | | | 45.04 | | | | 53.64 | |

End of Period | | | 66.87 | | | | 56.82 | | | | 66.87 | | | | | | 18% | | | | 56.82 | | | | 37.28 | |

WTI | | | | | | | | | | | | | | | | | | | | | | | | | | |

Average | | | 55.40 | | | | 49.29 | | | | 50.95 | | | | | | 18% | | | | 43.32 | | | | 48.80 | |

End of Period | | | 60.42 | | | | 53.72 | | | | 60.42 | | | | | | 12% | | | | 53.72 | | | | 37.04 | |

Average DifferentialBrent-WTI | | | 6.14 | | | | 1.84 | | | | 3.87 | | | | | | 125% | | | | 1.72 | | | | 4.84 | |

WCS | | | | | | | | | | | | | | | | | | | | | | | | | | |

Average | | | 43.14 | | | | 34.97 | | | | 38.97 | | | | | | 32% | | | | 29.48 | | | | 35.28 | |

Average(C$/bbl) | | | 54.84 | | | | 46.63 | | | | 50.56 | | | | | | 29% | | | | 39.05 | | | | 45.12 | |

End of Period | | | 34.93 | | | | 38.81 | | | | 34.93 | | | | | | (10)% | | | | 38.81 | | | | 24.98 | |

Average DifferentialWTI-WCS | | | 12.26 | | | | 14.32 | | | | 11.98 | | | | | | (13)% | | | | 13.84 | | | | 13.52 | |

Condensate (C5 @ Edmonton) | | | | | | | | | | | | | | | | | | | | | | | | | | |

Average(2) | | | 57.97 | | | | 48.33 | | | | 51.57 | | | | | | 21% | | | | 42.47 | | | | 47.36 | |

Average DifferentialWTI-Condensate (Premium)/Discount | | | (2.57 | ) | | | 0.96 | | | | (0.62 | ) | | | | | (173)% | | | | 0.85 | | | | 1.44 | |

Average DifferentialWCS-Condensate (Premium)/Discount | | | (14.83 | ) | | | (13.36 | ) | | | (12.60 | ) | | | | | (3)% | | | | (12.99 | ) | | | (12.08 | ) |

Mixed Sweet Blend (“MSW” @ Edmonton) | | | | | | | | | | | | | | | | | | | | | | | | | | |

Average(3) | | | 54.26 | | | | 46.18 | | | | 48.49 | | | | | | 21% | | | | 40.11 | | | | 45.32 | |

End of Period | | | 53.03 | | | | 51.26 | | | | 53.03 | | | | | | 3% | | | | 51.26 | | | | 34.98 | |

Average Refined Product Prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

Chicago Regular Unleaded Gasoline (“RUL”) | | | 74.36 | | | | 59.46 | | | | 66.95 | | | | | | 19% | | | | 56.24 | | | | 67.68 | |

ChicagoUltra-low Sulphur Diesel (“ULSD”) | | | 80.58 | | | | 61.50 | | | | 69.09 | | | | | | 23% | | | | 56.33 | | | | 68.12 | |

Refining Margin: Average3-2-1 Crack

Spreads(4) | | | | | | | | | | | | | | | | | | | | | | | | | | |

Chicago | | | 21.09 | | | | 10.96 | | | | 16.77 | | | | | | 28% | | | | 13.07 | | | | 19.11 | |

Average Natural Gas Prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

AECO(C$/Mcf)(5) | | | 1.96 | | | | 2.81 | | | | 2.43 | | | | | | 16% | | | | 2.09 | | | | 2.77 | |

NYMEX(US$/Mcf) | | | 2.93 | | | | 2.98 | | | | 3.11 | | | | | | 26% | | | | 2.46 | | | | 2.66 | |

Basis Differential NYMEX-AECO(US$/Mcf) | | | 1.40 | | | | 0.86 | | | | 1.26 | | | | | | 42% | | | | 0.89 | | | | 0.49 | |

Foreign Exchange Rate(US$ per C$1) | | | | | | | | | | | | | | | | | | | | | | | | | | |

Average | | | 0.787 | | | | 0.750 | | | | 0.771 | | | | | | 2% | | | | 0.755 | | | | 0.782 | |

| (1) | These benchmark prices are not our realized sales prices. For our average realized sales prices and realized risk management results, refer to the Netbacks tables in the Operating Results, Reportable Segments and Discontinued Operations sections of this MD&A. |

| (2) | The average Canadian dollar condensate benchmark price for 2017 was $66.89 per barrel (2016 – $56.25 per barrel; 2015 – $60.56 per barrel); fourth quarter average condensate benchmark price was $73.66 per barrel (2016 – $64.44 per barrel). |

| (3) | The average Canadian dollar MSW benchmark price for 2017 was $62.89 per barrel (2016 – $53.13 per barrel; 2015 – $57.95 per barrel); fourth quarter average Canadian dollar MSW benchmark price was $68.95 per barrel (2016 – $61.57 per barrel). |

| (4) | The average3-2-1 Crack Spread is an indicator of the refining margin and is valued on a last in, first out accounting basis. |

| (5) | Alberta Energy Company (“AECO”) natural gas. |

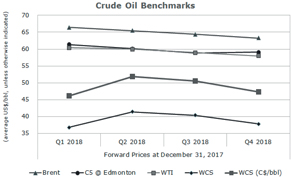

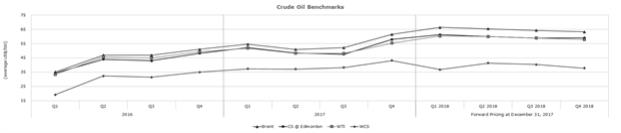

Crude Oil Benchmarks

The average Brent, WTI and WCS benchmark prices improved in 2017. Compliance with the production cuts outlined in the fourth quarter of 2016 by the Organization of Petroleum Exporting Countries (“OPEC”) led to widespread market expectations of an accelerated return to normal inventory levels. However, without supporting supply and demand drivers, prices continued to be volatile in 2017 as growing supply from the U.S., unstable supply from Libya and Nigeria, severe weather related incidents, and strong global demand resulted in varying expectations on the pace of crude oil and refined product inventory draws.

WTI is an important benchmark for Canadian crude oil since it reflects inland North American crude oil prices and its Canadian dollar equivalent is the basis for determining royalties for a number of our crude oil properties. In 2017, WTI benchmark prices weakened relative to Brent compared with 2016 due to growing U.S. crude oil supply and refinery disruptions from hurricanes in the U.S. Gulf Coast resulting in increased crude oil inventories.

WCS is blended heavy oil which consists of both conventional heavy oil and unconventional diluted bitumen. The averageWTI-WCS differential narrowed in 2017 compared with 2016. WCS strengthened relative to WTI due to a temporary decrease in supply of blended heavy oil in Alberta and OPEC’s compliance with production cuts reducing global heavy oil supply.

| | |

| Cenovus Energy Inc. | | 7 2017 Management’s Discussion and Analysis |

Blending condensate with bitumen and heavy oil enables our production to be transported through pipelines. Our blending ratios in 2017 ranged from approximately 10 percent to 33 percent. TheWCS-Condensate differential is an important benchmark as a narrower differential generally results in an increase in the recovery of condensate costs when selling a barrel of blended crude oil. When the supply of condensate in Alberta does not meet the demand, Edmonton condensate prices may be driven by U.S. Gulf Coast condensate prices plus the cost to transport the condensate to Edmonton.

The averageWTI-Condensate differential changed by US$1.47 per barrel, with condensate being sold at a premium to WTI in 2017 as compared with being sold at a discount in 2016. This change in benchmark pricing resulted from incremental demand for diluent due to a rise in Alberta heavy oil production, and minimal spare capacity on pipelines which increased the cost of transporting condensate to Edmonton.

MSW is an Alberta based light sweet crude oil benchmark that is representative of Canadian conventional production, comparable to the crude oil produced by our Deep Basin Assets. The average MSW benchmark price improved in 2017 compared with 2016, consistent with the general increase in average crude oil benchmark prices.

Refining Benchmarks

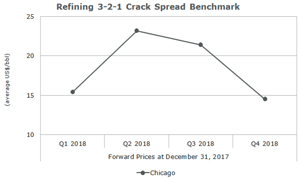

The Chicago Regular Unleaded Gasoline (“RUL”) and ChicagoUltra-low Sulphur Diesel (“ULSD”) benchmark prices are representative of inland refined product prices and are used to derive the Chicago3-2-1 crack spread. The3-2-1 crack spread is an indicator of the refining margin generated by converting three barrels of crude oil into two barrels of regular unleaded gasoline and one barrel ofultra-low sulphur diesel using current monthWTI-based crude oil feedstock prices and valued on a last in, first out accounting basis.

Average Chicago refined product prices increased in 2017 primarily due to strong refined product demand and severe weather related events that impacted the refined product supply output of U.S. Gulf Coast refineries. Average Chicago3-2-1 crack spreads rose in 2017 compared with 2016 due to the widerBrent-WTI differential reflecting product prices trending with global crude oil prices, significant regional refinery maintenance causing product shortages and strong refined product demand. Our realized crack spreads are affected by many other factors such as the variety of crude oil feedstock, refinery configuration and product output, the time lag between the purchase and delivery of crude oil feedstock, and the cost of feedstock which is valued on a first in, first out (“FIFO”) accounting basis.

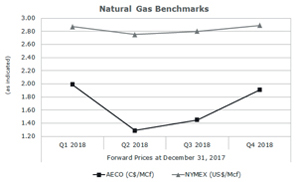

Natural Gas Benchmarks

Average AECO and NYMEX natural gas prices rose compared with 2016. Natural gas prices strengthened as North American inventory levels declined due to lower production and stronger demand. Production decreased as a result of reduced drilling programs while demand increased from additional capacity to export North American natural gas to foreign markets. In addition, natural gas prices in 2016 were negatively impacted by an exceptionally warm winter that resulted in poor heating demand and record-high seasonal North American natural gas storage levels.

| | |

| Cenovus Energy Inc. | | 8 2017 Management’s Discussion and Analysis |

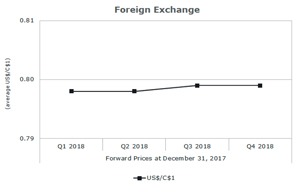

Foreign Exchange Benchmark

Our revenues are subject to foreign exchange exposure as the sales prices of our crude oil, natural gas and refined products are determined by reference to U.S. benchmark prices. An increase in the value of the Canadian dollar compared with the U.S. dollar has a negative impact on our reported results. Likewise, as the Canadian dollar weakens, our reported results are higher. In addition to our revenues being denominated in U.S. dollars, our long-term debt is also U.S. dollar denominated. In periods of a strengthening Canadian dollar, our U.S. dollar debt gives rise to unrealized foreign exchange gains when translated to Canadian dollars.

In 2017, the Canadian dollar strengthened relative to the U.S. dollar, which had a negative impact of approximately $360 million on our revenues, excluding our Conventional segment. The Canadian dollar as at December 31, 2017 compared with December 31, 2016 was stronger relative to the U.S. dollar, resulting in $665 million of unrealized foreign exchange gains on the translation of our U.S. dollar debt.

FINANCIAL RESULTS

Selected Consolidated Financial Results

The Acquisition and improvements in commodity prices, as referred to above, were the primary drivers of our financial results in 2017. The following key performance measures are discussed in more detail within this MD&A.

| | | | | | | | | | | | | | | | | | | | | | |

| ($ millions, except per share amounts) | | 2017 | | | | Percent Change | | 2016 | | | Percent Change | | | 2015 | |

Revenues | | | 17,043 | | | | | | 55% | | | | 11,006 | | | | (5)% | | | | 11,529 | |

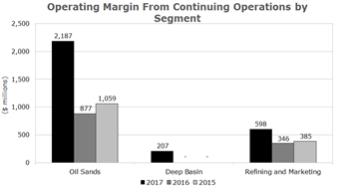

Operating Margin(1) | | | | | | | | | | | | | | | | | | | | | | |

From Continuing Operations | | | 2,992 | | | | | | 145% | | | | 1,223 | | | | (18)% | | | | 1,499 | |

Total Operating Margin | | | 3,483 | | | | | | 97% | | | | 1,767 | | | | (28)% | | | | 2,439 | |

Cash From Operating Activities | | | | | | | | | | | | | | | | | | | | | | |

From Continuing Operations | | | 2,611 | | | | | | 513% | | | | 426 | | | | (39)% | | | | 696 | |

Total Cash From Operating Activities | | | 3,059 | | | | | | 255% | | | | 861 | | | | (42)% | | | | 1,474 | |

Adjusted Funds Flow(2) | | | | | | | | | | | | | | | | | | | | | | |

From Continuing Operations | | | 2,447 | | | | | | 154% | | | | 965 | | | | 8% | | | | 896 | |

Total Adjusted Funds Flow | | | 2,914 | | | | | | 105% | | | | 1,423 | | | | (16)% | | | | 1,691 | |

Operating Earnings (Loss)(2) | | | | | | | | | | | | | | | | | | | | | | |

From Continuing Operations | | | (34) | | | | | | 88% | | | | (291) | | | | (172)% | | | | (107) | |

Per Share – Diluted ($) | | | (0.03) | | | | | | 91% | | | | (0.35) | | | | (169)% | | | | (0.13) | |

Total Operating Earnings (Loss) | | | 126 | | | | | | (133)% | | | | (377) | | | | 6% | | | | (403) | |

Per Share – Diluted ($) | | | 0.11 | | | | | | (124)% | | | | (0.45) | | | | 8% | | | | (0.49) | |

Net Earnings (Loss) | | | | | | | | | | | | | | | | | | | | | | |

From Continuing Operations | | | 2,268 | | | | | | (594)% | | | | (459) | | | | (150)% | | | | 914 | |

Per Share – Basic and Diluted ($) | | | 2.06 | | | | | | (475)% | | | | (0.55) | | | | (149)% | | | | 1.12 | |

Total Net Earnings (Loss) | | | 3,366 | | | | | | (718)% | | | | (545) | | | | (188)% | | | | 618 | |

Per Share – Basic and Diluted ($) | | | 3.05 | | | | | | (569)% | | | | (0.65) | | | | (187)% | | | | 0.75 | |

| | | | | | |

Total Assets | | | 40,933 | | | | | | 62% | | | | 25,258 | | | | (2)% | | | | 25,791 | |

Total Long-Term Financial Liabilities (3) | | | 9,717 | | | | | | 52% | | | | 6,373 | | | | (2)% | | | | 6,552 | |

| | | | | | |

Capital Investment(4) | | | | | | | | | | | | | | | | | | | | | | |

From Continuing Operations | | | 1,455 | | | | | | 70% | | | | 855 | | | | (42)% | | | | 1,470 | |

Total Capital Investment | | | 1,661 | | | | | | 62% | | | | 1,026 | | | | (40)% | | | | 1,714 | |

Dividends(5) | | | | | | | | | | | | | | | | | | | | | | |

Cash Dividends | | | 225 | | | | | | 36% | | | | 166 | | | | (69)% | | | | 528 | |

Per Share ($) | | | 0.20 | | | | | | -% | | | | 0.20 | | | | (77)% | | | | 0.8524 | |

| (1) | Additional subtotal found in Notes 1 and 11 of the Consolidated Financial Statements and defined in this MD&A. |

| (2) | Non-GAAP measure defined in this MD&A. |

| (3) | Includes Long-Term Debt, Risk Management, Contingent Payment Liabilities and other financial liabilities included within Other Liabilities on the Consolidated Balance Sheets. |

| (4) | Includes expenditures on Property, Plant and Equipment (“PP&E”), E&E assets, and assets held for sale. |

| (5) | Dividends issued in shares from treasury for 2017 were $nil (2016 – $nil; 2015 – $182 million). |

| | |

| Cenovus Energy Inc. | | 9 2017 Management’s Discussion and Analysis |

Revenues

| | | | | | |

| ($ millions) | | 2017 vs. 2016 | | | | 2016 vs. 2015 |

Revenues, Comparative Year | | 11,006 | | | | 11,529 |

Increase (Decrease) due to: | | | | | | |

Oil Sands | | 4,212 | | | | (81) |

Deep Basin | | 514 | | | | - |

Refining and Marketing | | 1,413 | | | | (366) |

Corporate and Eliminations | | (102) | | | | (76) |

| | | | | | |

Revenues, End of Year | | 17,043 | | | | 11,006 |

| | | | | | |

Upstream revenues from continuing operations increased significantly in 2017 compared with 2016. The rise was primarily related to the Acquisition, incremental sales volumes from our oil sands expansion phases, and higher commodity prices. These increases were partially offset by the strengthening of the Canadian dollar relative to the U.S. dollar and higher royalties.

In 2017, Refining and Marketing revenues increased 17 percent compared with 2016. Refining revenues increased primarily due to higher refined product pricing, consistent with the rise in average Chicago refined product benchmark prices, partially offset by the strengthening of the Canadian dollar relative to the U.S. dollar. Revenues fromthird-party crude oil and natural gas sales undertaken by our marketing group increased slightly in 2017 compared with 2016 due to higher crude oil prices and natural gas volumes sold, partially offset by a decline in crude oil volumes and natural gas prices.

Corporate and Eliminations revenues relate to sales and operating revenues between segments and are recorded at transfer prices based on current market prices.

Further information regarding our revenues can be found in the Reportable Segments section of this MD&A.

Operating Margin

Operating Margin is an additional subtotal found in Notes 1 and 11 of the Consolidated Financial Statements and is used to provide a consistent measure of the cash generating performance of our assets for comparability of our underlying financial performance between periods. Operating Margin is defined as revenues less purchased product, transportation and blending, operating expenses, production and mineral taxes plus realized gains less realized losses on risk management activities. Items within the Corporate and Eliminations segment are excluded from the calculation of Operating Margin.

| | | | | | | | | | | | | | | | |

| ($ millions) | | 2017 | | | | | 2016 | | | | | 2015 (1) | |

Revenues | | | 17,498 | | | | | | 11,359 | | | | | | 11,866 | |

(Add) Deduct: | | | | | | | | | | | | | | | | |

Purchased Product | | | 8,476 | | | | | | 7,325 | | | | | | 7,709 | |

Transportation and Blending | | | 3,760 | | | | | | 1,721 | | | | | | 1,816 | |

Operating Expenses | | | 1,956 | | | | | | 1,243 | | | | | | 1,288 | |

Production and Mineral Taxes | | | 1 | | | | | | - | | | | | | 1 | |

Realized (Gain) Loss on Risk Management Activities | | | 313 | | | | | | (153 | ) | | | | | (447 | ) |

| | | | | | | | | | | | | | | | |

Operating Margin From Continuing Operations | | | 2,992 | | | | | | 1,223 | | | | | | 1,499 | |

Conventional (Discontinued Operations) | | | 491 | | | | | | 544 | | | | | | 940 | |

| | | | | | | | | | | | | | | | |

Total Operating Margin | | | 3,483 | | | | | | 1,767 | | | | | | 2,439 | |

| | | | | | | | | | | | | | | | |

| (1) | 2015 Operating Margin From Continuing Operations includes $55 million related to certain legacy Conventional royalty interest assets which were sold in 2015 and has been included in the Corporate and Eliminations Segment. |

| | |

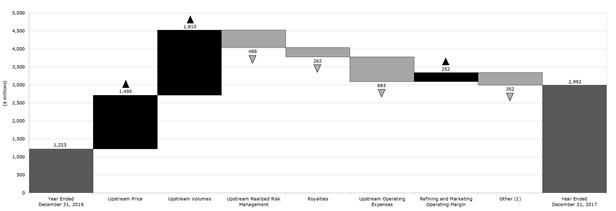

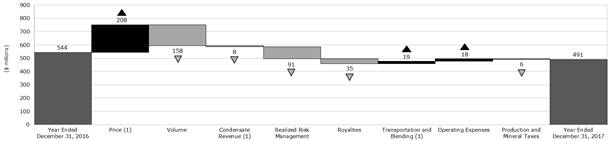

Operating Margin from continuing operations increased significantly in 2017 compared with 2016 primarily due to: • Increased sales volumes; • Higher average liquids sales prices; and • A higher Operating Margin from Refining and Marketing. | |  |

| | |

| Cenovus Energy Inc. | | 10 2017 Management’s Discussion and Analysis |

These increases in Operating Margin from continuing operations were partially offset by:

| · | | A rise in transportation and blending expenses primarily due to higher condensate prices along with an increase in condensate volumes required for blending our increased oil sands production; |

| · | | An increase in upstream operating expenses primarily due to the Acquisition and higher fuel costs related to the increase in natural gas consumption; |

| · | | Realized risk management losses of $307 million, compared with gains of $179 million in 2016; and |

| · | | Higher royalties primarily due to an increase in the WTI benchmark price (which determines the royalty rate), a rise in our liquids sales price and additional sales volumes. |

Operating Margin From Continuing Operations Variance

| (1) | Other includes the value of condensate sold as heavy oil blend recorded in revenues and condensate costs recorded in transportation and blending expense. The crude oil price excludes the impact of condensate purchases. |

Additional details explaining the changes in Operating Margin from continuing operations can be found in the Reportable Segments section of this MD&A.

Cash From Operating Activities and Adjusted Funds Flow

Adjusted Funds Flow is anon-GAAP measure commonly used in the oil and gas industry to assist in measuring a company’s ability to finance its capital programs and meet its financial obligations. Adjusted Funds Flow is defined as cash from operating activities excluding net change in other assets and liabilities and net change innon-cash working capital.Non-cash working capital is composed of current assets and current liabilities, excluding cash and cash equivalents, risk management, the contingent payment, assets held for sale and liabilities related to assets held for sale. Net change in other assets and liabilities is composed of site restoration costs and pension funding.

Total Cash From Operating Activities and Adjusted Funds Flow

| | | | | | | | | | | | | | | | |

| ($ millions) | | 2017 | | | | | 2016 | | | | | 2015 | |

Cash From Operating Activities(1) | | | 3,059 | | | | | | 861 | | | | | | 1,474 | |

(Add) Deduct: | | | | | | | | | | | | | | | | |

Net Change in Other Assets and Liabilities | | | (107 | ) | | | | | (91 | ) | | | | | (107 | ) |

Net Change inNon-Cash Working Capital | | | 252 | | | | | | (471 | ) | | | | | (110 | ) |

| | | | | | | | | | | | | | | | |

Adjusted Funds Flow(1) | | | 2,914 | | | | | | 1,423 | | | | | | 1,691 | |

| | | | | | | | | | | | | | | | |

| (1) | Includes results from our Conventional segment, which has been classified as a discontinued operation. |

Cash From Operating Activities and Adjusted Funds Flow increased compared with 2016 due to a higher Operating Margin, as discussed above, and a realized risk management gain on foreign exchange contracts due to hedging activity undertaken to support the Acquisition. These increases were partially offset by a rise in finance costs primarily associated with additional debt incurred to finance the Acquisition and an increase in realized foreign exchange losses on working capital items.

The change innon-cash working capital in 2017 was primarily due to a decrease in accounts receivable and inventory, partially offset by higher income tax receivable and a decrease in accounts payable. For 2016, the change innon-cash working capital was primarily due to an increase in accounts receivable and a rise in inventory, partially offset by an increase in accounts payable.

| | |

| Cenovus Energy Inc. | | 11 2017 Management’s Discussion and Analysis |

Operating Earnings (Loss)

Operating Earnings (Loss) is anon-GAAP measure used to provide a consistent measure of the comparability of our underlying financial performance between periods by removingnon-operating items. Operating Earnings (Loss) is defined as Earnings (Loss) Before Income Tax excluding gain (loss) on discontinuance, revaluation gain, gain on bargain purchase, unrealized risk management gains (losses) on derivative instruments, unrealized foreign exchange gains (losses) on translation of U.S. dollar denominated notes issued from Canada, foreign exchange gains (losses) on settlement of intercompany transactions, gains (losses) on divestiture of assets, less income taxes on Operating Earnings (Loss) before tax, excluding the effect of changes in statutory income tax rates and the recognition of an increase in U.S. tax basis.

| | | | | | | | | | | | | | | | |

| ($ millions) | | 2017 | | | | | 2016 | | | | | 2015 | |

Earnings (Loss) From Continuing Operations, Before Income Tax | | | 2,216 | | | | | | (802 | ) | | | | | 890 | |

Add (Deduct): | | | | | | | | | | | | | | | | |

Unrealized Risk Management (Gain) Loss(1) | | | 729 | | | | | | 554 | | | | | | 195 | |

Non-Operating Unrealized Foreign Exchange (Gain) Loss(2) | | | (651 | ) | | | | | (196 | ) | | | | | 1,064 | |

Revaluation (Gain) | | | (2,555 | ) | | | | | - | | | | | | - | |

(Gain) Loss on Divestiture of Assets | | | 1 | | | | | | 6 | | | | | | (2,392 | ) |

| | | | | | | | | | | | | | | | |

| | | | | |

Operating Earnings (Loss) From Continuing Operations,Before Income Tax | | | (260 | ) | | | | | (438 | ) | | | | | (243 | ) |

Income Tax Expense (Recovery) | | | (226 | ) | | | | | (147 | ) | | | | | (136 | ) |

| | | | | | | | | | | | | | | | |

Operating Earnings (Loss) From Continuing Operations | | | (34 | ) | | | | | (291 | ) | | | | | (107 | ) |

Operating Earnings (Loss) From Discontinued Operations | | | 160 | | | | | | (86 | ) | | | | | (296 | ) |

| | | | | | | | | | | | | | | | |

Total Operating Earnings (Loss) | | | 126 | | | | | | (377 | ) | | | | | (403 | ) |

| | | | | | | | | | | | | | | | |

| (1) | Includes the reversal of unrealized (gains) losses recorded in prior periods. |

| (2) | Includes unrealized foreign exchange (gains) losses on translation of U.S. dollar denominated notes issued from Canada and foreign exchange (gains) losses on settlement of intercompany transactions. |

Operating Earnings from continuing operations increased in 2017 compared with 2016 primarily due to higher cash from operating activities and Adjusted Funds Flow, as discussed above, greater unrealized foreign exchange gains on operating items compared with losses in 2016, and there-measurement of the contingent payment, partially offset by an increase in depreciation, depletion and amortization (“DD&A”) and exploration expense due to asset writedowns.

Net Earnings (Loss)

| | | | | | | | | | |

| ($ millions) | | 2017 vs. 2016 | | | | | 2016 vs. 2015 | |

Net Earnings (Loss) From Continuing Operations, Comparative Year | | | (459 | ) | | | | | 914 | |

Increase (Decrease) due to: | | | | | | | | | | |

Operating Margin From Continuing Operations | | | 1,769 | | | | | | (276 | ) |

Corporate and Eliminations: | | | | | | | | | | |

Unrealized Risk Management Gain (Loss) | | | (175 | ) | | | | | (359 | ) |

Unrealized Foreign Exchange Gain (Loss) | | | 668 | | | | | | 1,286 | |

Revaluation Gain | | | 2,555 | | | | | | - | |

Re-measurement of Contingent Payment | | | 138 | | | | | | - | |

Gain (Loss) on Divestiture of Assets | | | 5 | | | | | | (2,398 | ) |

Expenses(1) | | | (149 | ) | | | | | (72 | ) |

DD&A | | | (907 | ) | | | | | 62 | |

Exploration Expense | | | (886 | ) | | | | | 65 | |

Income Tax Recovery (Expense) | | | (291 | ) | | | | | 319 | |

| | | | | | | | | | |

Net Earnings (Loss) From Continuing Operations | | | 2,268 | | | | | | (459 | ) |

| | | | | | | | | | |

| (1) | Includes realized risk management (gains) losses, general and administrative, finance costs, interest income, realized foreign exchange (gains) losses, transaction costs, research costs, other (income) loss, net and Corporate and Eliminations revenues, purchased product, transportation and blending, and operating expenses. |

Net Earnings from continuing operations in 2017 increased due to:

| · | | The revaluation gain of $2,555 million related to the deemed disposition of ourpre-existing interest in FCCL; |

| · | | Non-operating unrealized foreign exchange gains of $651 million compared with $196 million in 2016; and |

| · | | Higher Operating Earnings, as discussed above. |

These increases were partially offset by a deferred income tax expense in 2017. The gain on the revaluation of ourpre-existing interest in FCCL resulted in a deferred tax expense, which was partially offset by a recovery due to the reduction of the U.S. federal corporate income tax rate. In 2016, a deferred tax recovery was recorded largely due to risk management losses and the recognition of operating losses.

Net Earnings from discontinued operations in 2017 was $1,098 million, including anafter-tax gain of $938 million on the divestiture of the Conventional segment assets. In 2016, discontinued operations generated a net loss of $86 million.

| | |

| Cenovus Energy Inc. | | 12 2017 Management’s Discussion and Analysis |

Net Capital Investment

| | | | | | | | | | | | | | | | |

| ($ millions) | | 2017 | | | | | 2016 | | | | | 2015 | |

Oil Sands | | | 973 | | | | | | 604 | | | | | | 1,185 | |

Deep Basin | | | 225 | | | | | | - | | | | | | - | |

Refining and Marketing | | | 180 | | | | | | 220 | | | | | | 248 | |

Corporate and Eliminations | | | 77 | | | | | | 31 | | | | | | 37 | |

| | | | | | | | | | | | | | | | |

Capital Investment – Continuing Operations | | | 1,455 | | | | | | 855 | | | | | | 1,470 | |

Conventional (Discontinued Operations) | | | 206 | | | | | | 171 | | | | | | 244 | |

| | | | | | | | | | | | | | | | |

Total Capital Investment | | | 1,661 | | | | | | 1,026 | | | | | | 1,714 | |

Acquisitions(1) | | | 18,388 | | | | | | 11 | | | | | | 87 | |

Divestitures(1) | | | (3,210 | ) | | | | | (8 | ) | | | | | (3,344 | ) |

| | | | | | | | | | | | | | | | |

Net Capital Investment(2) | | | 16,839 | | | | | | 1,029 | | | | | | (1,543 | ) |

| | | | | | | | | | | | | | | | |

| (1) | In connection with the Acquisition that was completed in the second quarter of 2017, Cenovus was deemed to have disposed of itspre-existing interest in FCCL and reacquired it at fair value as required by IFRS 3 “Business Combinations” (“IFRS 3”), which is not reflected in the table above. The carrying value of thepre-existing interest was $9,081 million and the estimated fair value was $11,605 million as at May 17, 2017. |

| (2) | Includes expenditures on PP&E, E&E assets and assets held for sale. |

Capital investment in continuing operations in 2017 increased $600 million compared with 2016, reflecting our increased ownership in FCCL through the Acquisition. Oil Sands capital investment focused on sustaining capital related to existing production; Christina Lake expansion phase G; and stratigraphic test wells to determine pad placement for sustaining wells, near-term expansion phases, and progression of certain emerging assets. Deep Basin capital investment related to asset development planning and our horizontal drilling and completion program targeting liquids-rich natural gas within the Deep Basin corridor.

Further information regarding our capital investment can be found in the Reportable Segments section of this MD&A.

Capital Investment Decisions

We have now completed the divestiture of our legacy Conventional assets. However, we continue to focus on deleveraging our balance sheet and are currently marketing for sale certainnon-core Deep Basin Assets in order to further streamline our portfolio. In addition to our commitment to continue reducing our debt, we are actively identifying further cost reduction opportunities.

Once our balance sheet leverage is more in line with our target debt metric, our disciplined approach to capital allocation includes prioritizing our uses of cash in the following manner:

| · | | First, to sustaining and maintenance capital for our existing business operations; |

| · | | Second, to paying our current dividend as part of providing strong total shareholder return; and |

| · | | Third, for growth or discretionary capital. |

Our approach to capital allocation includes evaluating all opportunities using specific rigorous criteria with the objective of maintaining a prudent and flexible capital structure and strong balance sheet metrics, which position us to be financially resilient in times of lower cash flows. In addition, we continue to evaluate other corporate and financial opportunities, including generating cash from our existing portfolio. Refer to the Liquidity and Capital Resources section of this MD&A for further information.

| | | | | | | | | | | | | | | | |

| ($ millions) | | 2017 | | | | | 2016 | | | | | 2015 | |

Adjusted Funds Flow(1) | | | 2,914 | | | | | | 1,423 | | | | | | 1,691 | |

Total Capital Investment(1) | | | 1,661 | | | | | | 1,026 | | | | | | 1,714 | |

| | | | | | | | | | | | | | | | |

Free Funds Flow(1) (2) | | | 1,253 | | | | | | 397 | | | | | | (23 | ) |

Cash Dividends | | | 225 | | | | | | 166 | | | | | | 528 | |

| | | | | | | | | | | | | | | | |

| | | 1,028 | | | | | | 231 | | | | | | (551 | ) |

| | | | | | | | | | | | | | | | |

| (1) | Includes our Conventional segment, which has been classified as a discontinued operation. |

| (2) | Free Funds Flow is anon-GAAP measure defined as Adjusted Funds Flow less capital investment. |

We expect our capital investment and cash dividends for 2018 to be funded from our internally generated cash flows and our cash balance on hand.

| | |

| Cenovus Energy Inc. | | 13 2017 Management’s Discussion and Analysis |

REPORTABLE SEGMENTS

| | |

Our reportable segments are as follows: Oil Sands,which includes the development and production of bitumen and natural gas in northeast Alberta. Cenovus’s bitumen assets include Foster Creek, Christina Lake and Narrows Lake as well as other projects in the early stages of development. Our interest in certain of our operated oil sands properties, notably Foster Creek, Christina Lake and Narrows Lake increased from 50 percent to 100 percent on May 17, 2017. Deep Basin,which includes approximately three million net acres of land primarily in the Elmworth-Wapiti, Kaybob-Edson, and Clearwater operating areas, rich in natural gas and natural gas liquids. The assets reside in Alberta and British Columbia and include interests in numerous natural gas processing facilities. The Deep Basin Assets were acquired on May 17, 2017. Refining and Marketing, which is responsible for transporting, selling and refining crude oil into petroleum and chemical products. Cenovus jointly owns two refineries in the U.S. with the operator Phillips 66, an unrelated U.S. public company. In addition, Cenovus owns and operates acrude-by-rail terminal in Alberta. This segment coordinates Cenovus’s marketing and transportation initiatives to optimize product mix, delivery points, transportation commitments and customer diversification. Corporate and Eliminations, which primarily includes unrealized gains and losses recorded on derivative financial instruments, gains and losses on divestiture of assets, as well as other Cenovus-wide costs for general and administrative, financing activities and research costs. As financial instruments are settled, the realized gains and losses are recorded in the reportable segment to which the derivative instrument relates. Eliminations relate to sales and operating revenues, and purchased product between segments, recorded at transfer prices based on current market prices, and to unrealized intersegment profits in inventory. | |

|

In 2017, Cenovus divested the majority of the crude oil and natural gas assets in the Company’s Conventional segment. As such, the results of operations have been presented as a discontinued operation and all prior periods restated. This segment included the production of conventional crude oil, NGLs and natural gas in Alberta and Saskatchewan, including the heavy oil assets at Pelican Lake, the CO2 enhanced oil recovery project at Weyburn and emerging tight oil opportunities. As at December 31, 2017, all Conventional assets were sold, except for the Company’s Suffield operations. The sale of the Suffield assets closed on January 5, 2018. Refer to the Discontinued Operations section of this MD&A for more information.

Revenues by Reportable Segment

| | | | | | | | | | | | | | |

| ($ millions) | | 2017 | | | | 2016 | | | | | 2015 | |

Oil Sands(1) | | 7,132 | | | | | 2,920 | | | | | | 3,001 | |

Deep Basin(2) | | 514 | | | | | - | | | | | | - | |

Refining and Marketing | | 9,852 | | | | | 8,439 | | | | | | 8,805 | |

Corporate and Eliminations | | (455) | | | | | (353) | | | | | | (277) | |

| | | | | | | | | | | | | | |

| | 17,043 | | | | | 11,006 | | | | | | 11,529 | |

| | | | | | | | | | | | | | |

| (1) | Our 2017 results include 229 days of FCCL operations at 100 percent. See the Oil Sands segment section of this MD&A for more details. |

| (2) | Our 2017 results include 229 days of operations from the Deep Basin Assets. See the Deep Basin segment section of this MD&A for more details. |

| | |

| Cenovus Energy Inc. | | 14 2017 Management’s Discussion and Analysis |

OIL SANDS

In northeastern Alberta, we own 100 percent of the Foster Creek, Christina Lake and Narrows Lake oil sands projects following the completion of the Acquisition. In addition, we have several emerging projects in the early stages of development. The Oil Sands segment includes the Athabasca natural gas property, from which a portion of the natural gas production is used as fuel at the adjacent Foster Creek operations.

Significant developments in our Oil Sands segment in 2017 compared with 2016 include:

| · | | Increasing our crude oil production by 95 percent primarily due to the Acquisition and incremental production volumes from Christina Lake phase F and Foster Creek phase G, both of which started up in the second half of 2016; |

| · | | Crude oil netbacks, excluding realized risk management activities, of $24.54 per barrel (2016 – $11.94 per barrel); and |

| · | | Generating Operating Margin net of capital investment of $1,214 million, an increase of $941 million. |

Oil Sands – Crude Oil

Financial Results

| | | | | | | | | | | | | | | | | | | | |

| ($ millions) | | 2017 | | | | | 2016 | | | | 2015 |

| | | | | |

Gross Sales | | | 7,340 | | | | | | | | 2,911 | | | | | | | | 3,000 | |

Less: Royalties | | | 230 | | | | | | | | 9 | | | | | | | | 29 | |

| | | | | | | | | | | | | | | | | | | | |

Revenues | | | 7,110 | | | | | | | | 2,902 | | | | | | | | 2,971 | |

Expenses | | | | | | | | | | | | | | | | | | | | |

Transportation and Blending | | | 3,704 | | | | | | | | 1,720 | | | | | | | | 1,814 | |

Operating | | | 868 | | | | | | | | 486 | | | | | | | | 511 | |

(Gain) Loss on Risk Management | | | 307 | | | | | | | | (179) | | | | | | | | (400) | |

| | | | | | | | | | | | | | | | | | | | |

Operating Margin | | | 2,231 | | | | | | | | 875 | | | | | | | | 1,046 | |

Capital Investment | | | 969 | | | | | | | | 601 | | | | | | | | 1,184 | |

| | | | | | | | | | | | | | | | | | | | |

Operating Margin Net of Related Capital Investment | | | 1,262 | | | | | | | | 274 | | | | | | | | (138) | |

| | | | | | | | | | | | | | | | | | | | |

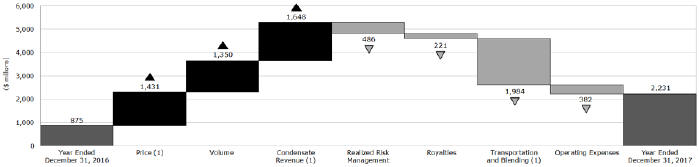

Operating Margin Variance

| (1) | Revenues include the value of condensate sold as heavy oil blend. Condensate costs are recorded in transportation and blending expense. The crude oil price excludes the impact of condensate purchases. |

Revenues

Price

In 2017, our average crude oil sales price increased to $41.49 per barrel (2016 – $27.64 per barrel). The rise in our crude oil price was consistent with the increase in the WCS and Christina Dilbit Blend (“CDB”) benchmark prices and the narrowing of theWCS-Condensate differential, partially offset by the strengthening of the Canadian dollar relative to the U.S. dollar. TheWCS-CDB differential narrowed to a discount of US$1.67 per barrel (2016 – discount of US$2.05 per barrel).

Our crude oil sales price is influenced by the cost of condensate used in blending. Our blending ratios range between 25 percent and 33 percent. As the cost of condensate increases relative to the price of blended crude oil, our bitumen sales price decreases. Due to high demand for condensate at Edmonton, we also purchase condensate from U.S. markets. As such, our average cost of condensate is generally higher than the Edmonton benchmark price due to transportation between market hubs and transportation to field locations. In addition, up to three months may elapse from when we purchase condensate to when we blend it with our production. In a rising price environment, we expect to see some benefit in our bitumen sales price as we are using condensate purchased at a lower price earlier in the year.

| | |

| Cenovus Energy Inc. | | 15 2017 Management’s Discussion and Analysis |

Production Volumes

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (barrels per day) | | 2017 | | | | | Percent Change | | | | | 2016 | | | | | | Percent Change | | | | | | 2015 | |

| | | | | | | | | |

Foster Creek | | | 124,752 | | | | | | 78% | | | | | | 70,244 | | | | | | | | 7% | | | | | | | | 65,345 | |

Christina Lake | | | 167,727 | | | | | | 111% | | | | | | 79,449 | | | | | | | | 6% | | | | | | | | 74,975 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | 292,479 | | | | | | 95% | | | | | | 149,693 | | | | | | | | 7% | | | | | | | | 140,320 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

In 2017, production increased primarily due to incremental volumes at Foster Creek and Christina Lake of 48,080 barrels per day and 64,437 barrels per day, respectively, as a result of the Acquisition. The phase G expansion at Foster Creek and the phase F expansion at Christina Lake also contributed to higher volumes. Production at Foster Creek was reduced as a result of temporary treating issues and a20-day planned turnaround completed in 2017.

Condensate

The bitumen currently produced by Cenovus must be blended with condensate to reduce its thickness in order to transport it to market through pipelines. Revenues represent the total value of blended crude oil sold and include the value of condensate. Consistent with the narrowing of theWCS-Condensate differential during 2017, the proportion of the cost of condensate recovered increased. The total amount of condensate used increased as a result of higher production volumes.

Royalties

Royalty calculations for our oil sands projects are based on government prescribedpre- and post-payout royalty rates which are determined on a sliding scale using the Canadian dollar equivalent WTI benchmark price. Royalty calculations differ between properties.

Royalties at Foster Creek, a post-payout project, are based on an annualized calculation which uses the greater of: (1) the gross revenues multiplied by the applicable royalty rate (one to nine percent, based on the Canadian dollar equivalent WTI benchmark price); or (2) the net profits of the project multiplied by the applicable royalty rate (25 to 40 percent, based on the Canadian dollar equivalent WTI benchmark price). Gross revenues are a function of sales volumes and sales prices. Net profits are a function of sales volumes, sales prices and allowed operating and capital costs.

Royalties at Christina Lake, apre-payout project, are based on a monthly calculation that applies a royalty rate (ranging from one to nine percent, based on the Canadian dollar equivalent WTI benchmark price) to the gross revenues from the project.

Effective Royalty Rates

| | | | | | | | | | | | |

| (percent) | | 2017 | | | 2016 | | | 2015 | |

| | | |

Foster Creek | | | 11.4 | | | | - | | | | 1.9 | |

Christina Lake | | | 2.5 | | | | 1.6 | | | | 2.8 | |

Royalties increased $221 million in 2017 compared with 2016. Royalties at Foster Creek increased primarily due to a higher WTI benchmark price (which determines the royalty rate). The royalty calculation was based on net profits as compared with a calculation based on gross revenues for 2016, resulting in a significant increase in the royalty rate. In 2016, the low royalty rate was primarily due to low crude oil sales prices, a decline in the WTI benchmark price and atrue-up of the 2015 royalty calculation.

Christina Lake royalties increased in 2017 primarily as a result of a rise in the WTI benchmark price (which determines the royalty rate) and higher crude oil sales prices.

Expenses

Transportation and Blending

Transportation and blending costs increased $1,984 million. Blending costs increased due to a rise in condensate volumes required for our increased production as well as higher condensate prices. Our condensate costs were higher than the average Edmonton benchmark price, primarily due to the transportation expense associated with moving the condensate between market hubs and to our oil sands projects.

Transportation costs increased primarily due to incremental sales volumes as a result of the Acquisition and expansion phases. In addition, rail costs rose as a result of moving higher volumes by rail over longer distances to U.S. markets. We transported an average of 9,743 barrels per day of crude oil by rail (2016 – 4,906 barrels per day).

| | |

| Cenovus Energy Inc. | | 16 2017 Management’s Discussion and Analysis |

Per-unit Transportation Expenses

At both Foster Creek and Christina Lake,per-barrel transportation costs declined primarily due to lower pipeline tariffs from an increase in the proportion of Canadian sales in 2017. Foster Creekper-barrel transportation costs were partially offset by higher rail costs from additional volumes shipped to the U.S. by unit trains.

Operating

Primary drivers of our operating expenses in 2017 were workforce costs, fuel, repairs and maintenance, chemical costs and workovers. While unit operating costs decreased six percent, total operating expenses increased $382 million primarily due to the Acquisition, higher fuel costs due to increased fuel consumption, additional repairs and maintenance, as well as increased chemical and workforce costs associated with the phase F expansion at Christina Lake. In addition, repairs and maintenance costs, as well as fluid, waste handling and trucking costs increased in 2017 due to the20-day turnaround at Foster Creek.

Per-unit Operating Expenses

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| ($/bbl) | | 2017 | | | | Percent Change | | | | | 2016 | | | | Percent Change | | | | 2015 |

Foster Creek | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Fuel | | | 2.44 | | | | | | (1)% | | | | | | 2.46 | | | | | | (12)% | | | | | | 2.80 | |

Non-fuel | | | 8.02 | | | | | | (1)% | | | | | | 8.09 | | | | | | (17)% | | | | | | 9.80 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total | | | 10.46 | | | | | | (1)% | | | | | | 10.55 | | | | | | (16)% | | | | | | 12.60 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Christina Lake | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Fuel | | | 2.06 | | | | | | (1)% | | | | | | 2.08 | | | | | | (5)% | | | | | | 2.20 | |

Non-fuel | | | 4.78 | | | | | | (11)% | | | | | | 5.40 | | | | | | (7)% | | | | | | 5.81 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total | | | 6.84 | | | | | | (9)% | | | | | | 7.48 | | | | | | (7)% | | | | | | 8.01 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total | | | 8.40 | | | | | | (6)% | | | | | | 8.91 | | | | | | (12)% | | | | | | 10.13 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

At Foster Creek,per-barrel fuel costs decreased slightly due to lower natural gas prices, partially offset by increased consumption.Per-barrelnon-fuel operating expenses declined in 2017 primarily due to higher production, partially offset by higher repairs and maintenance, an increase in workover costs due to increased pump changes, higher chemical costs, as well as increased fluid, waste handling and trucking costs due to the20-day planned turnaround in the second quarter. This represents the largest scale turnaround executed to date and it was completed under budget.

At Christina Lake, fuel costs declined on aper-barrel basis due to lower natural gas prices, partially offset by increased consumption.Per-barrelnon-fuel operating expenses decreased primarily due to higher production, partially offset by increased workforce and chemical costs associated with the phase F expansion, as well as higher repairs and maintenance activities.

Netbacks(1)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Foster Creek | | | | | Christina Lake | |

($/bbl) | | 2017 | | | | | 2016 | | | | | 2015 | | | | | 2017 | | | | | 2016 | | | | | 2015 | |

| | | | | | | | | | | |

Sales Price | | | 43.75 | | | | | | 30.32 | | | | | | 33.65 | | | | | | 39.78 | | | | | | 25.30 | | | | | | 28.45 | |

Royalties | | | 4.00 | | | | | | (0.01) | | | | | | 0.47 | | | | | | 0.87 | | | | | | 0.33 | | | | | | 0.67 | |

Transportation and Blending | | | 8.73 | | | | | | 8.84 | | | | | | 8.84 | | | | | | 4.52 | | | | | | 4.68 | | | | | | 4.72 | |

Operating Expenses | | | 10.46 | | | | | | 10.55 | | | | | | 12.60 | | | | | | 6.84 | | | | | | 7.48 | | | | | | 8.01 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Netback Excluding Realized Risk Management | | | 20.56 | | | | | | 10.94 | | | | | | 11.74 | | | | | | 27.55 | | | | | | 12.81 | | | | | | 15.05 | |

Realized Risk Management Gain (Loss) | | | (2.95) | | | | | | 3.51 | | | | | | 8.60 | | | | | | (2.99) | | | | | | 3.08 | | | | | | 7.33 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Netback Including Realized Risk Management | | | 17.61 | | | | | | 14.45 | | | | | | 20.34 | | | | | | 24.56 | | | | | | 15.89 | | | | | | 22.38 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | Netbacks reflect our margin on aper-barrel basis of unblended crude oil. |

Risk Management