Exhibit 99.2

Management’s Discussion and Analysis

For the PERIOD ended June 30, 2019

This Management’s Discussion and Analysis (“MD&A”) for Cenovus Energy Inc. (which includes references to “we”, “our”, “us”, “its”, the “Company”, or “Cenovus”, and means Cenovus Energy Inc., the subsidiaries of, and partnership interests held by, Cenovus Energy Inc. and its subsidiaries) dated July 24, 2019, should be read in conjunction with our June 30, 2019 unaudited interim Consolidated Financial Statements and accompanying notes (“interim Consolidated Financial Statements”), the December 31, 2018 audited Consolidated Financial Statements and accompanying notes (“Consolidated Financial Statements”) and the December 31, 2018 MD&A (“annual MD&A”). All of the information and statements contained in this MD&A are made as of July 24, 2019, unless otherwise indicated. This MD&A provides an update to our annual MD&A and contains forward-looking information about our current expectations, estimates, projections and assumptions. See the Advisory for information on the risk factors that could cause actual results to differ materially and the assumptions underlying our forward-looking information. Cenovus management (“Management”) prepared the MD&A. The interim MD&As are approved by the Audit Committee of the Cenovus Board of Directors (the “Board”) and the annual MD&A is reviewed by the Audit Committee and recommended for approval by the Board. Additional information about Cenovus, including our quarterly and annual reports, the Annual Information Form (“AIF”) and Form 40-F, is available on SEDAR at sedar.com, on EDGAR at sec.gov, and on our website at cenovus.com. Information on or connected to our website, even if referred to in this MD&A, does not constitute part of this MD&A.

Basis of Presentation

This MD&A and the interim Consolidated Financial Statements and comparative information have been prepared in Canadian dollars, (which includes references to “dollar” or “$”), except where another currency has been indicated, and in accordance with International Financial Reporting Standards (“IFRS” or “GAAP”) as issued by the International Accounting Standards Board (“IASB”). Production volumes are presented on a before royalties basis. We adopted IFRS 16, “Leases” (“IFRS 16”), effective January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section of this MD&A for further information.

Non-GAAP Measures and Additional Subtotals

Certain financial measures in this document do not have a standardized meaning as prescribed by IFRS, such as Netbacks, Adjusted Funds Flow, Operating Earnings, Free Funds Flow, Debt, Net Debt, Capitalization and Adjusted Earnings Before Interest, Taxes, Depreciation and Amortization (“Adjusted EBITDA”) and therefore are considered non-GAAP measures. In addition, Operating Margin is considered an additional subtotal found in Notes 1 and 7 of our interim Consolidated Financial Statements. These measures may not be comparable to similar measures presented by other issuers. These measures have been described and presented in order to provide shareholders and potential investors with additional measures for analyzing our ability to generate funds to finance our operations and information regarding our liquidity. This additional information should not be considered in isolation or as a substitute for measures prepared in accordance with IFRS.

The definition and reconciliation, if applicable, of each non-GAAP measure or additional subtotal is presented in the Operating Results, Financial Results, Liquidity and Capital Resources, or Advisory sections of this MD&A.

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 1 |

| | |

OVERVIEW OF CENOVUS

We are a Canadian integrated oil company headquartered in Calgary, Alberta, with our shares listed on the Toronto and New York stock exchanges. On June 30, 2019, we had an enterprise value of approximately $22 billion. Operations include oil sands projects in northeast Alberta and established crude oil, natural gas liquids (“NGLs”) and natural gas production in Alberta and British Columbia. Total production from our upstream assets averaged approximately 443,000 BOE per day for the three months ended June 30, 2019. We also conduct marketing activities and have ownership interest in refining operations in the United States (“U.S.”). The refineries processed an average of 474,000 gross barrels per day of crude oil feedstock into an average of 501,000 gross barrels per day of refined products in the three months ended June 30, 2019.

Our strategy is focused on maximizing shareholder value through cost leadership and realizing the best margins for our products. We believe that maintaining a strong balance sheet will help Cenovus navigate through commodity price volatility and give us the flexibility to proceed with opportunities at all points in the price cycle. We aim to evaluate disciplined investment in our portfolio against dividend increases, share repurchases and maintaining the optimal debt level while retaining investment grade status. Our investment focus will be on areas where we believe we have the greatest competitive advantage. We plan to achieve our strategy by leveraging our strategic focus areas including oil sands, conventional oil and natural gas assets, marketing, transportation and refining portfolio, and our people.

For a description of our operations, refer to the Reportable Segments section of this MD&A.

QUARTERLY HIGHLIGHTS

Cenovus delivered solid operating and financial results in the second quarter of 2019 and made significant progress on further deleveraging the balance sheet. We repurchased US$814 million of our unsecured notes during the quarter and US$1.3 billion since the beginning of the year.

Our upstream operational performance was solid during the quarter with production averaging 443,318 BOE per day, restricted by the Government of Alberta’s mandatory production curtailment program and the planned turnaround completed at Christina Lake.

Refining and Marketing operations were solid with improved crude oil runs in second quarter of 2019 compared with 2018, despite unplanned outages at both the Wood River and Borger refineries (“the Refineries”). Our Refining and Marketing segment generated operating margin of $198 million down from the second quarter of 2018, due to lower crude advantage and higher operating costs, partially offset by higher crack spreads.

With market access constraints for Canadian crude oil production continuing to be a challenge, we have made good progress on our strategy to maintain firm transportation through a combination of pipelines, rail and marine access. In the second quarter of 2019, we received approximately one-third of the railcars under the agreements signed in late 2018. Delivery will continue through 2019, in line with our expected ramp up to 100,000 barrels per day shipped by rail. We have also secured additional storage capacity in the U.S. Gulf Coast to support the ramp up of our crude-by-rail activity.

Average Brent and West Texas Intermediate (“WTI”) benchmark prices were lower than the second quarter of 2018. At the same time, the differential between WTI and Western Canadian Select ("WCS") benchmark prices narrowed 45 percent, supported by the Government of Alberta’s mandatory production curtailment program. As a result, WCS benchmark crude oil prices remained relatively flat, averaging US$49.18 per barrel in the second quarter of 2019 compared with US$48.61 per barrel in the same period of 2018. Our realized crude oil sales price rose to $62.75 per barrel as a result of the higher WCS price along with lower cost of condensate due to lower condensate benchmark prices compared with the second quarter of 2018.

In the second quarter of 2019, we:

• | Achieved Cash from Operating Activities of $1,275 million and Adjusted Funds Flow of $1,082 million, a significant increase from the second quarter of 2018; |

• | Repurchased US$814 million of our unsecured notes, reducing total debt to US$5.5 billion ($7.2 billion), driven by Free Funds Flow of $834 million; |

• | Achieved Net Debt of $7.1 billion; |

• | Recorded Net Earnings from continuing operations of $1,784 million (2018 – Net Loss of $410 million) including one-time deferred tax recoveries related to the Alberta corporate tax rate change and a tax basis increase related to our refining assets and realized risk management losses of $52 million compared with $697 million in 2018; |

• | Used our fleet of leased railcars to transport an average of 34,519 barrels per day by rail to sales locations outside of Alberta, allowing us to capture higher market prices; |

• | Earned an average companywide Netback from continuing operations of $32.14 per BOE, before realized hedging; |

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 2 |

| | |

• | Increased rail loading activity at our Bruderheim crude-by-rail terminal averaging 53,539 barrels per day, which partially cleared pipeline constrained barrels in Alberta; and |

• | Invested $248 million on sustaining capital, yield enhancement, rail initiatives and infrastructure, office space and information technology. |

OPERATING RESULTS

Upstream Production Volumes

| Three Months Ended June 30, | | | Six Months Ended June 30, | |

| 2019 | | | Percent Change | | | 2018 | | | 2019 | | | Percent Change | | | 2018 | |

Continuing Operations | | | | | | | | | | | | | | | | | | | | | | | |

Liquids (barrels per day) | | | | | | | | | | | | | | | | | | | | | | | |

Oil Sands | | | | | | | | | | | | | | | | | | | | | | | |

Foster Creek | | 165,953 | | | | (3 | ) | | | 171,079 | | | | 160,087 | | | | (3 | ) | | | 164,273 | |

Christina Lake | | 179,020 | | | | (18 | ) | | | 218,299 | | | | 183,895 | | | | (13 | ) | | | 210,332 | |

| | 344,973 | | | | (11 | ) | | | 389,378 | | | | 343,982 | | | | (8 | ) | | | 374,605 | |

Deep Basin | | | | | | | | | | | | | | | | | | | | | | | |

Crude Oil | | 4,904 | | | | (22 | ) | | | 6,263 | | | | 4,862 | | | | (24 | ) | | | 6,389 | |

NGLs | | 21,513 | | | | (23 | ) | | | 27,778 | | | | 22,344 | | | | (21 | ) | | | 28,367 | |

| | 26,417 | | | | (22 | ) | | | 34,041 | | | | 27,206 | | | | (22 | ) | | | 34,756 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Liquids Production (barrels per day) | | 371,390 | | | | (12 | ) | | | 423,419 | | | | 371,188 | | | | (9 | ) | | | 409,361 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Natural Gas (MMcf per day) | | | | | | | | | | | | | | | | | | | | | | | |

Oil Sands | | - | | | | (100 | ) | | | 1 | | | | - | | | | (100 | ) | | | 2 | |

Deep Basin (1) | | 432 | | | | (24 | ) | | | 570 | | | | 445 | | | | (21 | ) | | | 560 | |

| | 432 | | | | (24 | ) | | | 571 | | | | 445 | | | | (21 | ) | | | 562 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Production From Continuing Operations (BOE per day) | | 443,318 | | | | (15 | ) | | | 518,530 | | | | 445,283 | | | | (11 | ) | | | 503,083 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Production From Discontinued Operations (Conventional) (BOE per day) | | - | | | | (100 | ) | | | 79 | | | | - | | | | (100 | ) | | | 585 | |

| | | | | | | | | | | | | | | | | | | | | | | |

Total Production (BOE per day) | | 443,318 | | | | (15 | ) | | | 518,609 | | | | 445,283 | | | | (12 | ) | | | 503,668 | |

(1) | Includes production used for internal consumption by the Oil Sands segment of 319 MMcf per day, for both the three and six months ended June 30, 2019 (2018 – 300 MMcf per day and 311 MMcf per day, respectively). |

Overall, production for the three and six months ended June 30, 2019 was in line with production limits set by the Government of Alberta. Oil Sands production for the three and six months ended June 30, 2019 was limited due to mandatory production curtailments and a planned turnaround at Christina Lake. During the quarter, production decreased by 7,665 barrels per day due to the turnaround, minimized by additional plant capacity from the Christina Lake phase G facility and production capability from Foster Creek. In 2018, Oil Sands production was impacted by our decision to reduce producing well rates in the first quarter due to pipeline capacity constraints and discounted heavy oil prices and the subsequent ramp up of production in the second quarter as differentials narrowed.

Deep Basin production for the three months ended June 30, 2019 averaged 98,345 BOE per day compared with 129,066 BOE per day in the second quarter of 2018 due to lower sustaining capital investment, the divestiture of Cenovus Pipestone Partnership (“CPP”) on September 6, 2018, natural declines and a temporary shut-in to manage low gas prices. This was partially offset by less downtime in the second quarter of 2019 compared with 2018. Deep Basin production for the six months ended June 30, 2019 decreased by 21 percent to 101,301 BOE per day compared with 2018 due to lower sustaining capital investment, the divestiture of CPP and natural declines, partially offset by less downtime.

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 3 |

| | |

Netbacks From Continuing Operations

Netback is a non-GAAP measure commonly used in the oil and gas industry to assist in measuring operating performance on a per-unit basis, and is defined in the Canadian Oil and Gas Evaluation Handbook. Netbacks reflect our margin on a per-barrel of oil equivalent basis. Netback is defined as gross sales less royalties, transportation and blending, operating expenses and production and mineral taxes divided by sales volumes. Netbacks do not reflect the non-cash writedowns of product inventory until the product is sold. The sales price, transportation and blending costs, and sales volumes exclude the impact of purchased condensate. Condensate is blended with the heavy oil to reduce its thickness in order to transport it to market. Our Netback calculation is aligned with the definition found in the Canadian Oil and Gas Evaluation Handbook. For a reconciliation of our Netbacks see the Advisory section of this MD&A.

| Three Months Ended June 30, | | | Six Months Ended June 30, | |

($/BOE) | 2019 | | | 2018 (2) | | | 2019 | | | 2018 (2) | |

Sales Price | | 58.22 | | | | 46.87 | | | | 52.50 | | | | 40.30 | |

Royalties | | 9.24 | | | | 4.55 | | | | 7.42 | | | | 3.49 | |

Transportation and Blending | | 7.76 | | | | 5.59 | | | | 7.10 | | | | 5.86 | |

Operating Expenses | | 9.07 | | | | 7.66 | | | | 8.55 | | | | 7.77 | |

Production and Mineral Taxes | | 0.01 | | | | 0.01 | | | | 0.01 | | | | 0.01 | |

Netback Excluding Realized Risk Management (1) | | 32.14 | | | | 29.06 | | | | 29.42 | | | | 23.17 | |

Realized Risk Management Gain (Loss) | | (1.62 | ) | | | (16.27 | ) | | | (0.65 | ) | | | (14.07 | ) |

Netback Including Realized Risk Management (1) | | 30.52 | | | | 12.79 | | | | 28.77 | | | | 9.10 | |

(1) | Excludes results from our Conventional segment, which has been classified as a discontinued operation. Excludes intersegment sales. |

(2) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section in this MD&A. |

Our average Netback, excluding realized risk management gains and losses, increased in the second quarter of 2019 and on a year-to-date basis, compared with 2018, primarily due to higher realized sales prices and lower transportation and blending costs, partially offset by higher royalties, higher per-unit operating costs and lower sales volumes. Higher royalties were driven by higher prices and our Christina Lake property achieving payout in the third quarter of 2018. On a quarterly and year-to-date basis, the weakening of the Canadian dollar relative to the U.S. dollar compared with 2018 had a positive impact on our reported sales price of approximately $2.03 per BOE and $2.21 per BOE, respectively.

Refining and Marketing

In the second quarter of 2019, both refineries demonstrated good operational performance with crude utilization rates averaging 98 percent. Wood River was impacted by pipeline outages and flooding on the Mississippi River, which resulted in the reduction of throughput to manage finished product inventories. On a year-to-date basis, crude oil runs and refined product output increased as planned and unplanned maintenance in 2019, including a fire in a crude unit at Wood River in the first quarter of 2019, had less of an impact than major planned turnarounds completed at both Refineries in the first quarter of 2018.

| Three Months Ended June 30, | | | Six Months Ended June 30, | |

| 2019 | | | Percent Change | | | 2018 | | | 2019 | | | Percent Change | | | 2018 | |

Crude Oil Capacity (Mbbls/d) | | 482 | | | | 5 | | | | 460 | | | | 482 | | | | 5 | | | | 460 | |

Crude Oil Runs (1) (Mbbls/d) | | 474 | | | | 2 | | | | 464 | | | | 425 | | | | 4 | | | | 407 | |

Heavy Crude Oil (1) | | 194 | | | | (4 | ) | | | 203 | | | | 168 | | | | (8 | ) | | | 183 | |

Refined Product (1) (Mbbls/d) | | 501 | | | | 2 | | | | 490 | | | | 451 | | | | 5 | | | | 430 | |

Crude Utilization (1) (percent) | | 98 | | | | (3 | ) | | | 101 | | | | 88 | | | | - | | | | 88 | |

Operating Margin (2) ($ millions) | | 198 | | | | (45 | ) | | | 357 | | | | 502 | | | | 62 | | | | 309 | |

(1) | Represents 100 percent of the Wood River and Borger refinery operations. Cenovus’s interest is 50 percent. |

(2) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section of this MD&A. |

We continue to increase total rail volumes loaded at our Bruderheim crude-by-rail terminal. In the three months ended June 30, 2019, we loaded an average of 53,539 barrels per day at our Bruderheim crude-by-rail terminal compared with an average of 21,756 barrels per day in the second quarter of 2018.

Operating Margin from the Refining and Marketing segment in the three and six months ended June 30, 2019 was $198 million and $502 million, respectively (2018 – $357 million and $309 million, respectively). Our Operating Margin in the second quarter of 2019 decreased compared with 2018 due to lower crude advantage from narrowing heavy and medium sour crude oil differentials, and higher operating costs related to labour and unplanned maintenance at both Refineries. Operating margin improved significantly year-over-year, primarily due to lower operating expenses as a result of major planned turnarounds at both Refineries in the first quarter of 2018, higher

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 4 |

| | |

market crack spreads, higher margins on fixed priced products due to a lower benchmark WTI, and a reduction in the cost of Renewable Identification Numbers (“RINs”), partially offset by a reduced crude advantage from narrowing heavy and medium sour crude oil differentials.

Further information on the changes in our production volumes and other items included in our Netbacks, and refining results can be found in the Reportable Segments section of this MD&A. Further information on our risk management activities can be found in the Risk Management and Risk Factors section of this MD&A and in the notes to the interim Consolidated Financial Statements.

COMMODITY PRICES UNDERLYING OUR FINANCIAL RESULTS

Key performance drivers for our financial results include commodity prices, price differentials, refining crack spreads as well as the U.S./Canadian dollar exchange rate. The following table shows selected market benchmark prices and the U.S./Canadian dollar average exchange rates to assist in understanding our financial results.

Selected Benchmark Prices and Exchange Rates (1)

| Six Months Ended June 30, | | | | | | | | | | | | | |

(US$/bbl, unless otherwise indicated) | 2019 | | | Percent Change | | | 2018 | | | Q2 2019 | | | Q1 2019 | | | Q2 2018 | |

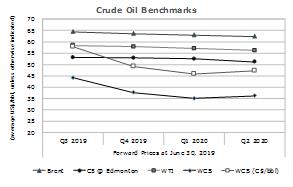

Brent | | | | | | | | | | | | | | | | | | | | | | | |

Average | | 66.13 | | | | (7 | ) | | | 71.04 | | | | 68.34 | | | | 63.88 | | | | 74.91 | |

End of Period | | 66.55 | | | | (16 | ) | | | 79.44 | | | | 66.55 | | | | 68.39 | | | | 79.44 | |

WTI | | | | | | | | | | | | | | | | | | | | | | | |

Average | | 57.38 | | | | (12 | ) | | | 65.37 | | | | 59.83 | | | | 54.90 | | | | 67.88 | |

End of Period | | 58.47 | | | | (21 | ) | | | 74.15 | | | | 58.47 | | | | 60.14 | | | | 74.15 | |

Average Differential Brent-WTI | | 8.75 | | | | 54 | | | | 5.67 | | | | 8.51 | | | | 8.98 | | | | 7.03 | |

WCS | | | | | | | | | | | | | | | | | | | | | | | |

Average | | 45.87 | | | | 5 | | | | 43.60 | | | | 49.18 | | | | 42.53 | | | | 48.61 | |

Average (C$/bbl) | | 61.22 | | | | 10 | | | | 55.70 | | | | 65.80 | | | | 56.58 | | | | 62.75 | |

End of Period | | 45.48 | | | | (11 | ) | | | 51.32 | | | | 45.48 | | | | 50.97 | | | | 51.32 | |

Average Differential WTI-WCS | | 11.51 | | | | (47 | ) | | | 21.77 | | | | 10.65 | | | | 12.37 | | | | 19.27 | |

West Texas Sour (“WTS”) | | | | | | | | | | | | | | | | | | | | | | | |

Average | | 55.96 | | | | (8 | ) | | | 60.55 | | | | 58.18 | | | | 53.71 | | | | 59.64 | |

End of Period | | 58.37 | | | | (6 | ) | | | 62.05 | | | | 58.37 | | | | 61.09 | | | | 62.05 | |

Average Differential WTI-WTS | | 1.42 | | | | (71 | ) | | | 4.82 | | | | 1.65 | | | | 1.19 | | | | 8.24 | |

Condensate (C5 @ Edmonton) | | | | | | | | | | | | | | | | | | | | | | | |

Average | | 53.20 | | | | (19 | ) | | | 65.93 | | | | 55.87 | | | | 50.50 | | | | 68.83 | |

Average (C$/bbl) | | 70.96 | | | | (16 | ) | | | 84.20 | | | | 74.74 | | | | 67.15 | | | | 88.81 | |

Average Differential WTI-Condensate (Premium)/Discount | | 4.18 | | | | (846 | ) | | | (0.56 | ) | | | 3.96 | | | | 4.40 | | | | (0.95 | ) |

Average Differential WCS-Condensate (Premium)/Discount | | (7.33 | ) | | | (67 | ) | | | (22.33 | ) | | | (6.69 | ) | | | (7.97 | ) | | | (20.22 | ) |

Mixed Sweet Blend (“MSW” @ Edmonton) | | | | | | | | | | | | | | | | | | | | | | | |

Average | | 52.61 | | | | (12 | ) | | | 59.70 | | | | 55.21 | | | | 49.99 | | | | 62.42 | |

Average (C$/bbl) | | 70.19 | | | | (8 | ) | | | 76.25 | | | | 73.87 | | | | 66.48 | | | | 80.54 | |

End of Period | | 52.48 | | | | (18 | ) | | | 64.32 | | | | 52.48 | | | | 55.52 | | | | 64.32 | |

Average Refined Product Prices | | | | | | | | | | | | | | | | | | | | | | | |

Chicago Regular Unleaded Gasoline (“RUL”) | | 72.72 | | | | (8 | ) | | | 79.04 | | | | 81.23 | | | | 64.15 | | | | 85.00 | |

Chicago Ultra-low Sulphur Diesel (“ULSD”) | | 79.19 | | | | (7 | ) | | | 85.21 | | | | 81.29 | | | | 77.10 | | | | 89.07 | |

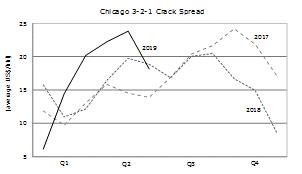

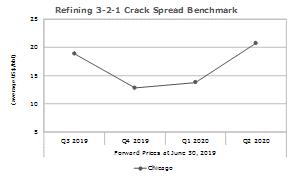

Refining Margin: Average 3-2-1 Crack Spreads (2) | | | | | | | | | | | | | | | | | | | | | | | |

Chicago | | 17.52 | | | | 12 | | | | 15.66 | | | | 21.44 | | | | 13.57 | | | | 18.36 | |

Group 3 | | 17.41 | | | | 3 | | | | 16.85 | | | | 19.99 | | | | 14.80 | | | | 18.04 | |

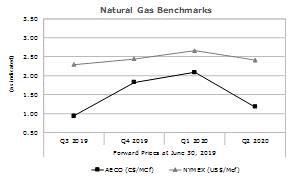

Average Natural Gas Prices | | | | | | | | | | | | | | | | | | | | | | | |

AECO (3) (C$/Mcf) | | 1.55 | | | | 8 | | | | 1.44 | | | | 1.17 | | | | 1.94 | | | | 1.03 | |

NYMEX (US$/Mcf) | | 2.89 | | | | - | | | | 2.90 | | | | 2.64 | | | | 3.15 | | | | 2.80 | |

Basis Differential NYMEX-AECO (US$/Mcf) | | 1.73 | | | | (2 | ) | | | 1.76 | | | | 1.76 | | | | 1.69 | | | | 2.00 | |

Foreign Exchange Rate (US$ per C$1) | | | | | | | | | | | | | | | | | | | | | | | |

Average | | 0.750 | | | | (4 | ) | | | 0.783 | | | | 0.748 | | | | 0.752 | | | | 0.775 | |

End of Period | | 0.764 | | | | 1 | | | | 0.759 | | | | 0.764 | | | | 0.748 | | | | 0.759 | |

(1) | These benchmark prices are not our realized sales prices. For our average realized sales prices and realized risk management results, refer to the Netbacks tables in the Operating Results and Reportable Segments sections of this MD&A. |

(2) | The average 3-2-1 Crack Spread is an indicator of the refining margin and is valued on a last in, first out accounting basis. |

(3) | Alberta Energy Company (“AECO”) natural gas monthly index. |

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 5 |

| | |

Crude Oil Benchmarks

The average Brent and WTI crude oil benchmark prices were lower compared with the second quarter of 2018. Continued uncertainty from oversupply and decreased demand for crude oil due to U.S.-China trade tensions lowered crude oil benchmark pricing. Global prices continued to be supported by the Organization of the Petroleum Exporting Countries (“OPEC”) led production cuts over the first six months of 2019 compared with the same period of 2018. Crude oil prices were further supported by turmoil in Venezuela that reduced the country’s crude oil supply. The decrease of crude oil supply from Venezuela coupled with OPEC cuts, which are predominately medium and heavy weighted crudes, reduced heavy crude supply globally causing WCS prices in the U.S. Gulf Coast to strengthen from the first quarter of 2019.

WTI is an important benchmark for Canadian crude oil since it reflects inland North American crude oil prices and the Canadian dollar equivalent is the basis for determining royalty rates for a number of our crude oil properties. In the second quarter of 2019, the Brent-WTI differential increased compared with 2018 as a result of increasing U.S. supply and inventory builds exceeding pipeline takeaway capacity at Cushing, Oklahoma.

WCS is blended heavy oil which consists of both conventional heavy oil and unconventional diluted bitumen. The average WTI-WCS differential narrowed in the second quarter of 2019 and on a year-to-date basis compared with 2018. Heavy oil differentials have narrowed in 2019 in response to production curtailments mandated by the Government of Alberta to address record high differentials in the fourth quarter of 2018 and high levels of crude oil in storage. Decreased production due to mandatory curtailments continues to support Alberta benchmark prices.

WTS is an important North American crude oil benchmark, representing the heavier, more sour counterpart to WTI crude oil, and is a primary component of the input feedstock at the Borger refinery. The differential between WTI and WTS benchmark prices narrowed in 2019 compared with 2018, due to additional pipeline capacity coming online, helping to debottleneck the Permian Basin.

Blending condensate with bitumen enables our production to be transported through pipelines. Our blending ratios, diluent volumes as a percentage of total blended volumes, range from approximately 25 percent to 33 percent. The WCS-Condensate differential is an important benchmark as a narrower differential generally results in an increase in the recovery of condensate costs when selling a barrel of blended crude oil. When the supply of condensate in Alberta does not meet the demand, Edmonton condensate prices may be driven by U.S. Gulf Coast condensate prices plus the cost to transport the condensate to Edmonton.

Average condensate benchmark prices were discounted relative to WTI in the second quarter of 2019 and on a year-to-date basis compared with a premium in the same periods of 2018 due to increasing domestic supply and lower demand as production curtailments were implemented.

MSW is an Alberta based light sweet crude oil benchmark that is representative of Canadian conventional production, comparable to the crude oil produced by our Deep Basin assets. The average MSW benchmark price declined in the second quarter of 2019 compared with 2018, consistent with the general decrease in average crude oil prices.

Refining Benchmarks

The Chicago Regular Unleaded Gasoline (“RUL”) and Chicago Ultra-low Sulphur Diesel (“ULSD”) benchmark prices are representative of inland refined product prices and are used to derive the Chicago 3-2-1 market crack spread. The 3‑2‑1 market crack spread is an indicator of the refining margin generated by converting three barrels of crude oil into two barrels of regular unleaded gasoline and one barrel of ultra-low sulphur diesel using current month WTI‑based crude oil feedstock prices and valued on a last in, first out accounting basis.

Average Chicago refined product prices decreased on a year-to-date basis in 2019 compared with the same period of 2018 primarily due to lower global crude oil prices. As North American refining crack spreads are expressed on a WTI basis, while refined products are set by international prices, the strength of refining crack spreads in the U.S. Midwest and Midcontinent will reflect the differential between Brent and WTI benchmark prices. The widening of the

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 6 |

| | |

Chicago 3-2-1 and Group 3 crack spreads in 2019 can be primarily attributed to the widening of the Brent-WTI differential, as discussed above.

Our realized crack spreads are affected by many other factors such as the variety of crude oil feedstock, refinery configuration and product output, the time lag between the purchase and delivery of crude oil feedstock, and the cost of feedstock which is valued on a first in, first out (“FIFO”) accounting basis.

Natural Gas Benchmarks

Average AECO prices strengthened during the three and six months ended June 30, 2019 compared with 2018 due to strong weather induced demand and flat natural gas supply in Alberta. Average NYMEX prices were comparable with 2018 due to supply continuing to be high from the development of U.S. shale gas and natural gas associated with crude oil plays.

Foreign Exchange Benchmark

Our revenues are subject to foreign exchange exposure as the sales prices of our crude oil, NGLs, natural gas and refined products are determined by reference to U.S. benchmark prices. An increase in the value of the Canadian dollar compared with the U.S. dollar has a negative impact on our reported results. Likewise, as the Canadian dollar weakens, there is a positive impact on our reported results. In addition to our revenues being denominated in U.S. dollars, our long‑term debt is also U.S. dollar denominated. In periods of a strengthening Canadian dollar, our U.S. dollar debt gives rise to unrealized foreign exchange gains when translated to Canadian dollars.

The average Canadian dollar weakened relative to the U.S. dollar in 2019, compared with 2018, resulting in a positive impact of approximately $445 million on our revenues in the first half of the year. The strengthening of the Canadian dollar relative to the U.S. dollar as at June 30, 2019 compared with December 31, 2018, and the derecognition of unrealized foreign exchange losses, which were realized due to the repurchase of our unsecured notes, resulted in $628 million of unrealized foreign exchange gains on the translation of our U.S. dollar debt.

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 7 |

| | |

FINANCIAL RESULTS

Selected Consolidated Financial Results

In 2019, the impact of mandatory production curtailments, rising crude oil prices, higher refining throughput, and lower blending costs were the primary drivers of our financial results. The following key performance measures are discussed in more detail within this MD&A.

($ millions, except per share | Six Months Ended June 30, | | 2019 | | 2018 (5) | | 2017 (5) | |

amounts) | 2019 | | 2018 (5) | | Q2 | | Q1 | | Q4 | | Q3 | | Q2 | | Q1 | | Q4 | | Q3 | | Q2 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Revenues | | 10,607 | | | 10,442 | | | 5,603 | | | 5,004 | | | 4,545 | | | 5,857 | | | 5,832 | | | 4,610 | | | 5,079 | | | 4,386 | | | 4,037 | |

Operating Margin (1) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

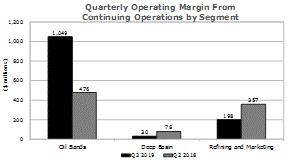

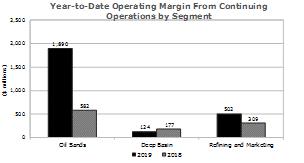

From Continuing Operations | | 2,516 | | | 1,068 | | | 1,277 | | | 1,239 | | | 135 | | | 1,191 | | | 911 | | | 157 | | | 1,018 | | | 1,097 | | | 572 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Operating Margin | | 2,516 | | | 1,107 | | | 1,277 | | | 1,239 | | | 132 | | | 1,192 | | | 938 | | | 169 | | | 1,088 | | | 1,214 | | | 731 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cash From Operating Activities | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

From Continuing Operations | | 1,711 | | | 372 | | | 1,275 | | | 436 | | | 488 | | | 1,258 | | | 506 | | | (134 | ) | | 833 | | | 481 | | | 1,102 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Cash From Operating Activities | | 1,711 | | | 410 | | | 1,275 | | | 436 | | | 485 | | | 1,259 | | | 533 | | | (123 | ) | | 900 | | | 592 | | | 1,239 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Adjusted Funds Flow (2) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

From Continuing Operations | | 2,130 | | | 694 | | | 1,082 | | | 1,048 | | | (33 | ) | | 976 | | | 747 | | | (53 | ) | | 796 | | | 865 | | | 603 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Adjusted Funds Flow | | 2,130 | | | 733 | | | 1,082 | | | 1,048 | | | (36 | ) | | 977 | | | 774 | | | (41 | ) | | 866 | | | 980 | | | 745 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating Earnings (Loss) (2) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

From Continuing Operations | | 336 | | | (1,044 | ) | | 267 | | | 69 | | | (1,670 | ) | | (41 | ) | | (292 | ) | | (752 | ) | | (533 | ) | | 240 | | | 298 | |

Per Share ($) (3) | | 0.27 | | | (0.85 | ) | | 0.22 | | | 0.06 | | | (1.36 | ) | | (0.03 | ) | | (0.24 | ) | | (0.61 | ) | | (0.43 | ) | | 0.20 | | | 0.27 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Operating Earnings (Loss) | | 336 | | | (1,015 | ) | | 267 | | | 69 | | | (1,672 | ) | | (42 | ) | | (272 | ) | | (743 | ) | | (514 | ) | | 327 | | | 352 | |

Per Share ($) (3) | | 0.27 | | | (0.83 | ) | | 0.22 | | | 0.06 | | | (1.36 | ) | | (0.03 | ) | | (0.22 | ) | | (0.60 | ) | | (0.42 | ) | | 0.27 | | | 0.32 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net Earnings (Loss) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

From Continuing Operations | | 1,894 | | | (1,324 | ) | | 1,784 | | | 110 | | | (1,350 | ) | | (242 | ) | | (410 | ) | | (914 | ) | | (776 | ) | | 275 | | | 2,558 | |

Per Share ($) (3) | | 1.54 | | | (1.08 | ) | | 1.45 | | | 0.09 | | | (1.10 | ) | | (0.20 | ) | | (0.33 | ) | | (0.74 | ) | | (0.63 | ) | | 0.22 | | | 2.30 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Net Earnings (Loss) | | 1,894 | | | (1,072 | ) | | 1,784 | | | 110 | | | (1,356 | ) | | (241 | ) | | (418 | ) | | (654 | ) | | 620 | | | (82 | ) | | 2,617 | |

Per Share ($) (3) | | 1.54 | | | (0.87 | ) | | 1.45 | | | 0.09 | | | (1.10 | ) | | (0.20 | ) | | (0.34 | ) | | (0.53 | ) | | 0.50 | | | (0.07 | ) | | 2.35 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Capital Investment (4) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

From Continuing Operations | | 565 | | | 816 | | | 248 | | | 317 | | | 276 | | | 271 | | | 294 | | | 522 | | | 557 | | | 396 | | | 277 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Capital Investment | | 565 | | | 816 | | | 248 | | | 317 | | | 276 | | | 271 | | | 292 | | | 524 | | | 583 | | | 438 | | | 327 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends | | 123 | | | 122 | | | 62 | | | 61 | | | 62 | | | 61 | | | 62 | | | 60 | | | 61 | | | 62 | | | 61 | |

Per Share ($) | | 0.10 | | | 0.10 | | | 0.05 | | | 0.05 | | | 0.05 | | | 0.05 | | | 0.05 | | | 0.05 | | | 0.05 | | | 0.05 | | | 0.05 | |

(1) | Additional subtotal found in Notes 1 and 7 of the interim Consolidated Financial Statements and defined in this MD&A. |

(2) | Non-GAAP measure defined in this MD&A. |

(3) | Represented on a basic and diluted per share basis. |

(4) | Includes expenditures on property, plant and equipment (“PP&E”), Exploration and Evaluation (“E&E”) assets and assets held for sale. |

(5) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section in this MD&A. |

Revenues

($ millions) | Three Months Ended | | | Six Months Ended | |

Revenues for the Periods Ended June 30, 2018 | | 5,832 | | | | 10,442 | |

Increase (Decrease) due to: | | | | | | | |

Oil Sands | | (353 | ) | | | (451 | ) |

Deep Basin | | (85 | ) | | | (103 | ) |

Refining and Marketing | | 72 | | | | 529 | |

Corporate and Eliminations | | 137 | | | | 190 | |

Revenues for the Periods Ended June 30, 2019 | | 5,603 | | | | 10,607 | |

Upstream revenues decreased in 2019 compared with 2018 due to lower sales volumes and higher royalties, partially offset by higher realized pricing.

Refining and Marketing revenues rose three percent in the second quarter of 2019 compared with 2018 and increased 11 percent on a year-to-date basis. Refining revenues increased due to higher refined product output partially offset by lower refined product pricing. Revenues from third-party crude oil and natural gas sales

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 8 |

| | |

undertaken by our marketing group increased on a quarterly and year-to-date basis in 2019 compared with 2018 due to an increase in crude oil and natural gas volumes partially offset by lower prices.

Corporate and Eliminations revenues relate to sales of natural gas or crude oil and operating revenue between segments and are recorded at transfer prices based on current market prices.

Further information regarding our revenues can be found in the Reportable Segments section of this MD&A.

Operating Margin

Operating Margin is an additional subtotal found in Notes 1 and 7 of the interim Consolidated Financial Statements and is used to provide a consistent measure of the cash generating performance of our assets for comparability of our underlying financial performance between periods. Operating Margin is defined as revenues less purchased product, transportation and blending, operating expenses, production and mineral taxes, plus realized gains less realized losses on risk management activities. Items within the Corporate and Eliminations segment are excluded from the calculation of Operating Margin.

| Three Months Ended June 30, | | | Six Months Ended June 30, | |

($ millions) | 2019 | | | 2018 (1) | | | 2019 | | | 2018 (1) | |

Revenues | | 5,705 | | | | 6,071 | | | | 10,850 | | | | 10,875 | |

(Add) Deduct: | | | | | | | | | | | | | | | |

Purchased Product | | 2,441 | | | | 2,224 | | | | 4,604 | | | | 4,181 | |

Transportation and Blending | | 1,363 | | | | 1,669 | | | | 2,529 | | | | 3,186 | |

Operating Expenses | | 571 | | | | 569 | | | | 1,167 | | | | 1,274 | |

Production and Mineral Taxes | | - | | | | 1 | | | | - | | | | 1 | |

Realized (Gain) Loss on Risk Management Activities | | 53 | | | | 697 | | | | 34 | | | | 1,165 | |

Operating Margin From Continuing Operations | | 1,277 | | | | 911 | | | | 2,516 | | | | 1,068 | |

Conventional (Discontinued Operations) | | - | | | | 27 | | | | - | | | | 39 | |

Total Operating Margin | | 1,277 | | | | 938 | | | | 2,516 | | | | 1,107 | |

(1) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section in this MD&A. |

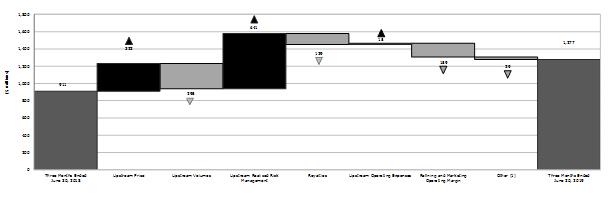

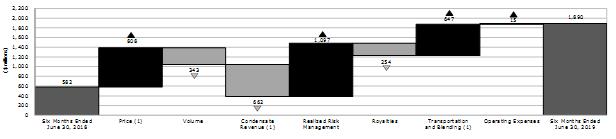

Three Months Ended June 30, 2019 Compared With June 30, 2018

Operating Margin from continuing operations increased primarily due to: |

|

• | An increase in our average liquids sales prices; |

• | A decrease in our transportation and blending costs due to a decrease in condensate volumes required for blending and lower condensate prices, partially offset by an increase in rail transportation costs and pipeline tariffs due to higher volumes shipped to the U.S.; |

• | A decrease in upstream operating expenses; and |

• | Realized risk management losses of $53 million (2018 – losses of $697 million). |

These increases in Operating Margin were partially |

offset by: |

• | Lower sales volumes; |

• | Higher royalties; and |

• | Lower Operating Margin from our Refining and Marketing segment due to lower crude advantage and higher operating expenses partially offset by higher market crack spreads. |

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 9 |

| | |

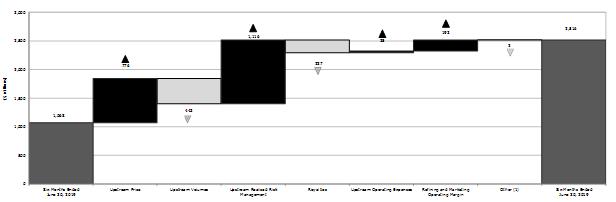

Operating Margin From Continuing Operations Variance

| (1) | Other includes the value of condensate sold as heavy oil blend recorded in revenues and condensate costs recorded in transportation and blending expense. The crude oil price excludes the impact of condensate purchases. |

Six Months Ended June 30, 2019 Compared With June 30, 2018

Operating Margin from continuing operations increased in 2019 compared with 2018 primarily due to: |

|

• | An increase in our average liquids and natural gas sales prices; |

• | A decrease in transportation and blending expenses due to a reduction in condensate volumes required for blending and lower condensate prices, partially offset by increased rail transportation costs and pipeline tariffs due to higher volumes shipped to the U.S.; |

• | Higher Operating Margin from our Refining and Marketing segment due to lower operating |

| expenses, higher market crack spreads, and higher margins on fixed priced products, partially offset by lower crude advantage; |

• | Lower upstream operating expenses; and |

• | Realized risk management losses of $34 million (2018 – losses of $1,165 million). |

These increases in Operating Margin were partially offset by lower volumes, and higher royalties primarily due to Christina Lake achieving payout in August 2018. |

Operating Margin From Continuing Operations Variance

| (1) | Other includes the value of condensate sold as heavy oil blend recorded in revenues and condensate costs recorded in transportation and blending expense. The crude oil price excludes the impact of condensate purchases. |

Additional details explaining the changes in Operating Margin from continuing operations can be found in the Reportable Segments section of this MD&A.

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 10 |

| | |

Cash From Operating Activities and Adjusted Funds Flow

Adjusted Funds Flow is a non-GAAP measure commonly used in the oil and gas industry to assist in measuring a company’s ability to finance its capital programs and meet its financial obligations. Adjusted Funds Flow is defined as cash from operating activities excluding net change in other assets and liabilities and net change in non-cash working capital. Non-cash working capital is composed of accounts receivable, inventories, income tax receivable, accounts payable and income tax payable. Net change in other assets and liabilities is composed of site restoration costs and pension funding.

Total Cash From Operating Activities and Adjusted Funds Flow

| Three Months Ended June 30, | | | Six Months Ended June 30, | |

($ millions) | 2019 | | | 2018 (2) | | | 2019 | | | 2018 (2) | |

Cash From Operating Activities (1) | | 1,275 | | | | 533 | | | | 1,711 | | | | 410 | |

(Add) Deduct: | | | | | | | | | | | | | | | |

Net Change in Other Assets and Liabilities | | (13 | ) | | | (17 | ) | | | (34 | ) | | | (35 | ) |

Net Change in Non-Cash Working Capital | | 206 | | | | (224 | ) | | | (385 | ) | | | (288 | ) |

Adjusted Funds Flow (1) | | 1,082 | | | | 774 | | | | 2,130 | | | | 733 | |

(1) | Includes results from our Conventional segment, which has been classified as a discontinued operation. |

(2) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section in this MD&A. |

Cash From Operating Activities and Adjusted Funds Flow were higher in the second quarter of 2019 compared with 2018 due to higher Operating Margin, as discussed above, lower general and administrative costs, and lower finance costs, partially offset by an increase in current income tax expense. The change in non-cash working capital in the second quarter of 2019 was due to a decrease in accounts receivable and lower income tax receivable, partially offset by a decrease in accounts payable and an increase in inventories. For the three months ended June 30, 2018, the change in non-cash working capital was primarily due to an increase in accounts receivable, partially offset by a rise in accounts payable.

Cash From Operating Activities and Adjusted Funds Flow were higher on a year-to-date basis compared with 2018 due to higher Operating Margin, lower general and administrative costs due to $47 million severance costs in 2018 and lower finance costs, partially offset by an increase in current income tax expense. The change in non-cash working capital for the six months ended June 30, 2019 was primarily due to an increase in accounts receivable and increase in inventories, partially offset by a decrease in income tax receivable and an increase in accounts payable. For the first six months of 2018, the change in non-cash working capital was primarily due to an increase in accounts receivable and a decline in income tax payable, partially offset by an increase in accounts payable.

Operating Earnings (Loss)

| Three Months Ended June 30, | | | Six Months Ended June 30, | |

($ millions) | 2019 | | | 2018 (3) | | | 2019 | | | 2018 | |

Earnings (Loss) From Continuing Operations, Before Income Tax | | 918 | | | | (390 | ) | | | 1,075 | | | | (1,462 | ) |

Add (Deduct): | | | | | | | | | | | | | | | |

Unrealized Risk Management (Gain) Loss (1) | | (88 | ) | | | (122 | ) | | | 148 | | | | (261 | ) |

Non-Operating Unrealized Foreign Exchange (Gain) Loss (2) | | (407 | ) | | | 205 | | | | (616 | ) | | | 469 | |

(Gain) Loss on Divestiture of Assets | | (1 | ) | | | (1 | ) | | | 4 | | | | (1 | ) |

Other | | - | | | | 1 | | | | - | | | | - | |

Operating Earnings (Loss) From Continuing Operations, Before Income Tax | | 422 | | | | (307 | ) | | | 611 | | | | (1,255 | ) |

Income Tax Expense (Recovery) | | 155 | | | | (15 | ) | | | 275 | | | | (211 | ) |

Operating Earnings (Loss) From Continuing Operations | | 267 | | | | (292 | ) | | | 336 | | | | (1,044 | ) |

Operating Earnings (Loss) From Discontinued Operations | | - | | | | 20 | | | | - | | | | 29 | |

Total Operating Earnings (Loss) | | 267 | | | | (272 | ) | | | 336 | | | | (1,015 | ) |

(1) | Includes the reversal of unrealized (gains) losses recorded in prior periods. |

(2) | Includes unrealized foreign exchange (gains) losses on translation of U.S. dollar denominated notes issued from Canada and foreign exchange (gains) losses on settlement of intercompany transactions. |

(3) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section in this MD&A. |

Operating Earnings (Loss) is a non-GAAP measure used to provide a consistent measure of the comparability of our underlying financial performance between periods by removing non-operating items. Operating Earnings (Loss) is defined as Earnings (Loss) Before Income Tax excluding gain (loss) on discontinuance, unrealized risk management gains (losses) on derivative instruments, unrealized foreign exchange gains (losses) on translation of U.S. dollar denominated notes issued from Canada, foreign exchange gains (losses) on settlement of intercompany

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 11 |

| | |

transactions, gains (losses) on divestiture of assets, less income taxes on Operating Earnings (Loss) before tax, excluding the effect of changes in statutory income tax rates and the recognition of an increase in U.S. tax basis.

Operating Earnings from continuing operations increased in the second quarter of 2019 compared with 2018 primarily due to a re-measurement gain of $109 million on the contingent payment compared with a loss of $377 million in 2018 and higher Cash From Operating Activities and Adjusted Funds Flow, as discussed above, partially offset by realized foreign exchange losses of $256 million on the repurchase of our unsecured notes compared with losses of $14 million in 2018.

For the six months ended June 30, 2019, Operating Earnings from continuing operations increased relative to 2018 primarily due to higher Cash From Operating Activities and Adjusted Funds Flow, as discussed above, a re‑measurement loss of $154 million on the contingent payment compared with a loss of $494 million in 2018, lower depreciation, depletion and amortization (“DD&A”), and a lower provision for onerous contracts. The increase in our Operating Earnings for the six months ended June 30, 2019 was partially offset by realized foreign exchange losses of $279 million on the repurchase of our unsecured notes, compared with losses of $14 million in 2018.

Net Earnings (Loss)

($ millions) | Three Months Ended | | | Six Months Ended | |

Net Earnings (Loss) From Continuing Operations, for the Periods Ended June 30, 2018 (1) | | (410 | ) | | | (1,324 | ) |

Increase (Decrease) due to: | | | | | | | |

Operating Margin From Continuing Operations | | 366 | | | | 1,448 | |

Corporate and Eliminations: | | | | | | | |

Unrealized Risk Management Gain (Loss) | | (34 | ) | | | (409 | ) |

Unrealized Foreign Exchange Gain (Loss) | | 632 | | | | 1,143 | |

Re-measurement of Contingent Payment | | 486 | | | | 340 | |

Gain (Loss) on Divestiture of Assets | | - | | | | (5 | ) |

Expenses (2) | | (157 | ) | | | (61 | ) |

DD&A | | 15 | | | | 84 | |

Exploration Expense | | - | | | | (3 | ) |

Income Tax Recovery (Expense) | | 886 | | | | 681 | |

Net Earnings (Loss) From Continuing Operations, for the Periods Ended June 30, 2019 | | 1,784 | | | | 1,894 | |

(1) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section in this MD&A. |

(2) | Includes Corporate and Eliminations realized risk management (gains) losses, general and administrative, onerous contract provisions, finance costs, interest income, realized foreign exchange (gains) losses, transaction costs, research costs, other (income) loss, net and Corporate and Eliminations revenues, purchased product, transportation and blending, and operating expenses. |

Net Earnings of $1,784 million from continuing operations in the second quarter of 2019 increased compared with 2018 primarily due to:

• | A deferred income tax recovery of $877 million compared with a deferred tax expense of $55 million in 2018 primarily due to a four percent reduction in the Alberta corporate tax rate over the next four years and a step‑up in the tax basis of our refining assets; |

• | Non-operating unrealized foreign exchange gains of $407 million compared with losses of $205 million in 2018; and |

• | Higher Operating Earnings, as discussed above. |

These increases to our Net Earnings from continuing operations in 2019 were partially offset by unrealized risk management gains of $88 million compared with unrealized gains of $122 million in 2018.

On a year-to-date basis, Net Earnings of $1,894 million from continuing operations increased from the first half of 2018 due to higher Operating Earnings, as discussed above, non-operating unrealized foreign exchange gains of $616 million compared with losses of $469 million in 2018, and a deferred income tax recovery of $836 million compared with $49 million in 2018. These increases to our Net Earnings were partially offset by unrealized risk management losses of $148 million compared with gains of $261 million in 2018.

For the three months ended June 30, 2018, we incurred a Net Loss from discontinued operations of $8 million. Net Earnings from discontinued operations for the six months ended June 30, 2018 was $252 million and includes an after-tax gain of $223 million on the divestiture of the Suffield assets in the first quarter of 2018.

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 12 |

| | |

Total Capital Investment

| Three Months Ended June 30, | | | Six Months Ended June 30, | |

($ millions) | 2019 | | | 2018 (2) | | | 2019 | | | 2018 (2) | |

Oil Sands | | 136 | | | | 224 | | | | 350 | | | | 542 | |

Deep Basin | | 8 | | | | 26 | | | | 22 | | | | 171 | |

Refining and Marketing | | 72 | | | | 35 | | | | 127 | | | | 88 | |

Corporate and Eliminations | | 32 | | | | 9 | | | | 66 | | | | 15 | |

Capital Investment - Continuing Operations | | 248 | | | | 294 | | | | 565 | | | | 816 | |

Conventional (Discontinued Operations) | | - | | | | (2 | ) | | | - | | | | - | |

Total Capital Investment (1) | | 248 | | | | 292 | | | | 565 | | | | 816 | |

(1) | Includes expenditures on PP&E, E&E assets and assets held for sale. |

(2) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section of this MD&A. |

Capital investment in 2019 decreased compared with 2018, reflecting our reduced capital investment program, lower Christina Lake phase G spend as the project was completed in March 2019, and a smaller sustaining well program. Oil Sands focused capital spending on sustaining capital related to existing production and stratigraphic test wells to determine pad placement for sustaining wells. Capital investment in the Deep Basin focused spending on pad and well equipping and tie-ins, as well as capital maintenance activities.

Refining and Marketing capital investment increased on a year-to-date basis due to higher spending on yield enhancements and capital maintenance projects at Borger, as well as higher spending on strategic rail initiatives and infrastructure.

Further information regarding our capital investment can be found in the Reportable Segments section of this MD&A.

Capital Investment Decisions

Our interim Net Debt target of $7.0 billion has largely been achieved. Ensuring balance sheet strength will continue to be a priority and we plan to direct the vast majority of our Free Funds Flow towards debt reduction until we reach our longer-term Net Debt target of $5.0 billion. This level of Net Debt aligns with a Net Debt to EBITDA ratio of two times at bottom of the cycle commodity prices. As we progress towards $5.0 billion, we will also consider opportunities for shareholder returns in the form of dividends and share repurchases.

Once we have achieved our long-term Net Debt target, our capital allocation priorities are:

• | First, to sustaining and maintenance capital for our existing business operations; |

• | Second, to paying our dividend and providing a stable and predictable shareholder return; and |

• | Third, consider incremental returns to shareholders, further deleveraging, and disciplined investment in growth. |

Our approach to capital allocation includes evaluating all opportunities using specific rigorous criteria with the objective of maintaining a prudent and flexible capital structure and strong balance sheet metrics, which positions us to be financially resilient in times of lower cash flows. In addition, we continue to evaluate other corporate and financial opportunities, including generating cash from our existing portfolio. Refer to the Liquidity and Capital Resources section of this MD&A for further information.

| Three Months Ended June 30, | | | Six Months Ended June 30, | |

($ millions) | 2019 | | | 2018 (3) | | | 2019 | | | 2018 (3) | |

Adjusted Funds Flow (1) | | 1,082 | | | | 774 | | | | 2,130 | | | | 733 | |

Total Capital Investment (1) | | 248 | | | | 292 | | | | 565 | | | | 816 | |

Free Funds Flow (1) (2) | | 834 | | | | 482 | | | | 1,565 | | | | (83 | ) |

Cash Dividends | | 62 | | | | 62 | | | | 123 | | | | 122 | |

| | 772 | | | | 420 | | | | 1,442 | | | | (205 | ) |

(1) | Includes our Conventional segment, which has been classified as a discontinued operation. |

(2) | Free Funds Flow is a non-GAAP measure defined as Adjusted Funds Flow less capital investment. |

(3) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section in this MD&A. |

We expect our capital investment and cash dividends for 2019 to be funded from our internally generated cash flows and our cash balance on hand.

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 13 |

| | |

REPORTABLE SEGMENTS

Our reportable segments are as follows:

Oil Sands, which includes the development and production of bitumen in northeast Alberta. Cenovus’s bitumen assets include Foster Creek, Christina Lake and Narrows Lake as well as other projects in the early stages of development.

Deep Basin, which includes approximately 2.8 million net acres of land primarily in the Elmworth-Wapiti, Kaybob‑Edson, and Clearwater operating areas, rich in natural gas and NGLs. The assets reside in Alberta and British Columbia and include interests in numerous natural gas processing facilities.

Refining and Marketing, which is responsible for transporting, selling and refining crude oil into petroleum and chemical products. Cenovus jointly owns two refineries in the U.S. with the operator Phillips 66, an unrelated U.S. public company. In addition, Cenovus owns and operates a crude‑by‑rail terminal in Alberta. This segment coordinates Cenovus’s marketing and transportation initiatives to optimize product mix, delivery points, transportation commitments and customer diversification. The marketing of crude oil and natural gas sourced from Canada, including physical product sales that settle in the U.S., is considered to be undertaken by a Canadian business. U.S. sourced crude oil and natural gas purchases and sales are attributed to the U.S.

Corporate and Eliminations, which primarily includes unrealized gains and losses recorded on derivative financial instruments, gains and losses on divestiture of assets, as well as other Cenovus-wide costs for general and administrative, financing activities and research costs. As financial instruments are settled, the realized gains and losses are recorded in the reportable segment to which the derivative instrument relates. Eliminations include adjustments for internal usage of natural gas production between segments, transloading services provided to the Oil Sands segment by the Company’s rail terminal, crude oil production used as feedstock by the Refining and Marketing segment, and unrealized intersegment profits in inventory. Eliminations are recorded at transfer prices based on current market prices.

As at January 5, 2018, all of the Conventional segment assets were sold. Refer to the Discontinued Operations section of this MD&A for more information.

Revenues by Reportable Segment

| Three Months Ended June 30, | | | Six Months Ended June 30, | |

($ millions) | 2019 | | | 2018 | | | 2019 | | | 2018 | |

Oil Sands | | 2,716 | | | | 3,069 | | | | 4,966 | | | | 5,417 | |

Deep Basin | | 140 | | | | 225 | | | | 346 | | | | 449 | |

Refining and Marketing | | 2,849 | | | | 2,777 | | | | 5,538 | | | | 5,009 | |

Corporate and Eliminations | | (102 | ) | | | (239 | ) | | | (243 | ) | | | (433 | ) |

| | 5,603 | | | | 5,832 | | | | 10,607 | | | | 10,442 | |

OIL SANDS

In the second quarter of 2019 we:

• | Successfully completed a planned turnaround at Christina Lake; |

• | Managed total production to mandated curtailment requirements; |

• | Generated Operating Margin of $1,049 million, an increase of $573 million due to higher average realized sales prices, decreased transportation and blending costs, and realized risk management losses of $57 million compared with losses of $688 million in 2018, partially offset by lower sales volumes and higher royalties; |

• | Earned crude oil Netbacks of $35.78 per barrel, excluding realized risk management activities, a 10 percent increase compared with 2018; |

• | Received delivery of approximately one-third of our railcars under the agreements signed in late 2018. Delivery will continue through 2019, in line with our expected ramp up to 100,000 barrels per day shipped by rail; |

• | Used our fleet of leased railcars to transport 34,519 barrels per day by rail to sales locations outside of Alberta, allowing us to capture higher market prices; and |

• | On July 10, 2019, we reached one billion barrels of cumulative production from our Foster Creek and Christina Lake oil sands facilities in northern Alberta. |

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 14 |

| | |

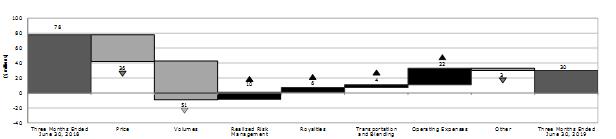

Three Months Ended June 30, 2019 Compared With June 30, 2018

Financial Results

| Three Months Ended June 30, | |

($ millions) | 2019 | | | 2018 (1) | |

Gross Sales | | 3,030 | | | | 3,248 | |

Less: Royalties | | 314 | | | | 179 | |

Revenues | | 2,716 | | | | 3,069 | |

Expenses | | | | | | | |

Transportation and Blending | | 1,340 | | | | 1,642 | |

Operating | | 270 | | | | 263 | |

(Gain) Loss on Risk Management | | 57 | | | | 688 | |

Operating Margin | | 1,049 | | | | 476 | |

Capital Investment | | 136 | | | | 224 | |

Operating Margin Net of Related Capital Investment | | 913 | | | | 252 | |

(1) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section in this MD&A. |

Operating Margin Variance

(1) | Revenues include the value of condensate sold as heavy oil blend. Condensate costs are recorded in transportation and blending expense. The crude oil price excludes the impact of condensate purchases. |

Revenues

Price

In the second quarter of 2019, our average realized crude oil sales price increased to $62.68 per barrel (2018 – $51.07 per barrel). While WTI decreased, the narrowing of the heavy oil differentials increased our realized crude oil sales price. The WTI-WCS differential narrowed to a discount of US$10.65 per barrel (2018 – US$19.27 per barrel) and the WCS-Christina Dilbit Blend (“CDB”) differential narrowed to a discount of US$1.25 per barrel (2018 – US$2.95 per barrel).

Our realized crude oil sales price is influenced by the cost of condensate used in blending. Our blending ratios range between 25 percent and 33 percent. As the cost of condensate decreases relative to the price of blended crude oil, our bitumen sales price increases. Due to high demand for condensate at Edmonton, we also purchase condensate from U.S. markets and deliver it to the Edmonton hub. As such, our average cost of condensate is generally higher than the Edmonton benchmark price due to transportation between market hubs and transportation to field locations. In addition, up to three months may elapse from when we purchase condensate to when we sell our blended production. In a rising crude oil price environment, we expect to see a positive impact on our bitumen sales price as we are using condensate purchased at a lower price earlier in the year.

Production Volumes

| Three Months Ended June 30, | |

(barrels per day) | 2019 | | | Percent Change | | | 2018 | |

Foster Creek | | 165,953 | | | | (3 | ) | | | 171,079 | |

Christina Lake | | 179,020 | | | | (18 | ) | | | 218,299 | |

| | 344,973 | | | | (11 | ) | | | 389,378 | |

Production levels in the second quarter of 2019 were limited by the government curtailment program and a planned turnaround at Christina Lake. In the three months ended June 30, 2019, the impact of the planned turnaround was approximately 7,665 barrels per day, minimized by the use of the Christina Lake phase G facility and production capability from Foster Creek. In the second quarter of 2018, we benefited from ramping up production and producing the majority of barrels that were stored in our oil sands reservoirs due to the decision to reduce producing well rates in the first quarter of 2018.

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 15 |

| | |

Condensate

The bitumen currently produced by Cenovus must be blended with condensate to reduce its thickness in order to transport it to market through pipelines or by rail. Revenues represent the total value of blended crude oil sold and include the value of condensate. Consistent with the narrowing of the WCS-Condensate differential in the second quarter of 2019, the proportion of the cost of condensate recovered increased. The total amount of condensate used decreased as a result of lower sales volumes.

Royalties

Royalty calculations for our oil sands projects are based on government prescribed pre- and post-payout royalty rates which are determined on a sliding scale using the Canadian dollar equivalent WTI benchmark price.

Royalties for a pre-payout project are based on a monthly calculation that applies a royalty rate (ranging from one to nine percent, based on the Canadian dollar equivalent WTI benchmark price) to the gross revenues from the project.

Project payout is achieved when the cumulative project revenue exceeds the cumulative project allowable costs. Royalties for a post-payout project are based on an annualized calculation which uses the greater of: (1) the gross revenues multiplied by the applicable royalty rate (one to nine percent, based on the Canadian dollar equivalent WTI benchmark price); or (2) the net profits of the project multiplied by the applicable royalty rate (25 to 40 percent, based on the Canadian dollar equivalent WTI benchmark price). Gross revenues are a function of sales revenues less diluent costs and transportation costs. Net profits are a function of sales revenues less diluent costs, transportation costs, and allowed operating and capital costs.

Foster Creek and Christina Lake are post-payout projects with our Christina Lake property achieving payout in the third quarter of 2018.

Effective Royalty Rates

| Three Months Ended June 30, | |

(percent) | 2019 | | | 2018 | |

Foster Creek | | 18.2 | | | | 19.6 | |

Christina Lake | | 19.7 | | | | 4.2 | |

Royalties increased $135 million in the second quarter of 2019 compared with 2018. Royalties increased primarily due to Christina Lake achieving project payout in August 2018 and higher realized sales prices, partially offset by lower annual average WTI benchmark pricing (which determines the royalty rate).

Expenses

Transportation and Blending

Transportation and blending costs decreased $302 million from the second quarter of 2018. Blending costs decreased primarily from reduced condensate volumes required for our decreased production and lower priced condensate in the second quarter of 2019 compared with 2018. Transportation costs increased primarily due to higher rail costs from additional volumes shipped by rail. In the three months ended June 30, 2019, we shipped 34,519 barrels per day by rail to locations outside of Alberta (2018 – nil).

Per-unit Transportation Expenses

At Foster Creek, transportation costs increased $2.06 per barrel due to higher rail transportation costs as a result of more railcars shipping our volumes and higher pipeline tariffs from increased U.S. sales, and decreased sales volumes. Christina Lake transportation costs of $6.69 per barrel were 35 percent higher relative to 2018 due to a higher volume of product shipped by rail and higher pipeline tariff rates due to increased U.S. sales, and decreased sales volumes. Transporting our volumes to U.S. destinations, either by pipeline or rail, allows us to achieve better market prices.

Operating

Primary drivers of our operating expenses in the second quarter of 2019 were workforce, fuel, repairs and maintenance, and chemical costs. Total operating expenses increased $7 million primarily due to higher repairs and maintenance costs, and waste handling and trucking costs due to the planned turnaround at Christina Lake, partially offset by lower chemical costs due to lower emulsion and less sulphur treating.

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 16 |

| | |

Per-unit Operating Expenses

| Three Months Ended June 30, | |

($/bbl) | 2019 | | | Percent Change | | | 2018 (1) | |

Foster Creek | | | | | | | | | | | |

Fuel | | 2.17 | | | | 14 | | | | 1.91 | |

Non-fuel | | 6.72 | | | | (2 | ) | | | 6.84 | |

Total | | 8.89 | | | | 2 | | | | 8.75 | |

Christina Lake | | | | | | | | | | | |

Fuel | | 1.79 | | | | 1 | | | | 1.77 | |

Non-fuel | | 6.75 | | | | 52 | | | | 4.45 | |

Total | | 8.54 | | | | 37 | | | | 6.22 | |

Total | | 8.70 | | | | 19 | | | | 7.32 | |

| (1) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section in this MD&A. |

At Foster Creek, per barrel fuel costs increased in the second quarter of 2019 primarily due to lower sales volumes and higher consumption. At Christina Lake, per barrel fuel costs were relatively flat due to lower sales volumes offset by less consumption. Foster Creek per-barrel non-fuel operating expenses decreased compared with 2018, due to lower greenhouse gas costs and lower chemical costs, partially offset by lower sales volumes. At Christina Lake, per-barrel non-fuel operating expenses increased 52 percent compared with 2018, due to lower sales volumes, higher repairs and maintenance costs, and fluid, waste handling and trucking costs due to a planned turnaround, partially offset by lower chemical costs.

Netbacks (1)

| Foster Creek | | | Christina Lake | |

| Three Months Ended June 30, | |

($/bbl) | 2019 | | | 2018 (2) | | | 2019 | | | 2018 (2) | |

Sales Price | | 65.90 | | | | 54.08 | | | | 59.78 | | | | 48.74 | |

Royalties | | 10.02 | | | | 9.14 | | | | 10.24 | | | | 1.84 | |

Transportation and Blending | | 9.60 | | | | 7.54 | | | | 6.69 | | | | 4.95 | |

Operating Expenses | | 8.89 | | | | 8.75 | | | | 8.54 | | | | 6.22 | |

Netback Excluding Realized Risk Management | | 37.39 | | | | 28.65 | | | | 34.31 | | | | 35.73 | |

Realized Risk Management Gain (Loss) | | (1.55 | ) | | | (19.54 | ) | | | (2.08 | ) | | | (19.08 | ) |

Netback Including Realized Risk Management | | 35.84 | | | | 9.11 | | | | 32.23 | | | | 16.65 | |

(1) | Netbacks reflect our operating margin on a per-barrel basis of unblended crude oil. |

(2) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section in this MD&A. |

Risk Management

Risk management positions in the second quarter of 2019 resulted in realized losses of $57 million (2018 – realized losses of $688 million), consistent with average benchmark prices exceeding our contract prices.

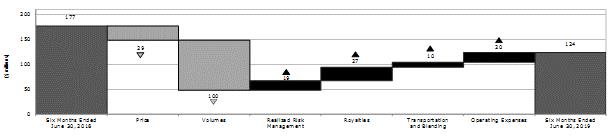

Six Months Ended June 30, 2019 Compared With June 30, 2018

Financial Results

| Six Months Ended June 30, | |

($ millions) | 2019 | | | 2018 (1) | |

Gross Sales | | 5,457 | | | | 5,654 | |

Less: Royalties | | 491 | | | | 237 | |

Revenues | | 4,966 | | | | 5,417 | |

Expenses | | | | | | | |

Transportation and Blending | | 2,487 | | | | 3,134 | |

Operating | | 544 | | | | 559 | |

(Gain) Loss on Risk Management | | 45 | | | | 1,142 | |

Operating Margin | | 1,890 | | | | 582 | |

Capital Investment | | 350 | | | | 542 | |

Operating Margin Net of Related Capital Investment | | 1,540 | | | | 40 | |

(1) | IFRS 16 was adopted January 1, 2019 using the modified retrospective approach; therefore, comparative information has not been restated. Refer to the Critical Accounting Judgments, Estimation Uncertainties and Accounting Policies section in this MD&A. |

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 17 |

| | |

Operating Margin Variance

(1) | Revenues include the value of condensate sold as heavy oil blend. Condensate costs are recorded in transportation and blending expense. The crude oil price excludes the impact of condensate purchases. |

Revenues

Price

In the six months ended June 30, 2019, our realized crude oil sales price increased to $56.30 per barrel compared with $43.00 per barrel in the first half of 2018. In the first half of 2018, WCS prices were more volatile ranging from $34.93 per barrel to $51.32 per barrel. The increase in our crude oil price reflects the rise in WCS prices, narrower WCS-Condensate and WCS-CDB differentials. While WTI benchmark prices decreased, the narrowing of the differential increased our realized sales price. The WTI-WCS differential narrowed to a discount of US$11.51 per barrel (2018 – discount of US$21.77 per barrel) and the WCS-CDB differential narrowed to a discount of US$1.51 per barrel (2018 – US$2.81 per barrel).

Production Volumes

| Six Months Ended June 30, | |

(barrels per day) | 2019 | | | Percent Change | | | 2018 | |

Foster Creek | | 160,087 | | | | (3 | ) | | | 164,273 | |

Christina Lake | | 183,895 | | | | (13 | ) | | | 210,332 | |

| | 343,982 | | | | (8 | ) | | | 374,605 | |

Production at both Foster Creek and Christina Lake was lower compared with 2018 primarily due to the mandated production curtailments. The planned turnaround at Christina Lake reduced production by approximately 3,854 barrels per day in 2019, which was minimized by using the Christina Lake phase G facility and production capabilities from Foster Creek.

Royalties

Effective Royalty Rates

| Six Months Ended June 30, | |

(percent) | 2019 | | | 2018 | |

Foster Creek | | 15.2 | | | | 16.1 | |

Christina Lake | | 18.7 | | | | 3.5 | |

On a year-to-date basis, royalties increased $254 million compared with 2018. Royalties increased primarily due to Christina Lake achieving project payout in August 2018 and higher realized sales prices, partially offset by lower annual average WTI benchmark pricing (which determines the royalty rate).

Expenses

Transportation and Blending

Transportation and blending costs decreased $647 million. Blending costs decreased due to a decline in condensate volumes required for our lower production and lower condensate prices. Our condensate costs were higher than the average Edmonton benchmark price primarily due to the transportation expense associated with moving the condensate between market hubs and to our oil sands projects.

Transportation costs increased primarily due to an increase in volumes shipped by rail. In the first half of 2019, using our railcars we shipped 23,712 barrels per day to locations outside of Alberta (2018 – nil). Transporting our volumes to U.S. destinations, either by pipeline or rail, allows us to achieve better market prices.

Cenovus Energy Inc. – Q2 2019 Management’s Discussion and Analysis | | 18 |

| | |

Per-unit Transportation Expenses

Foster Creek per-barrel transportation costs increased $1.28 per barrel due to higher rail transportation costs, from an increase in our volumes shipped by rail, and increased pipeline tariff costs due to higher volumes shipped to the U.S., and decreased sales volumes. Christina Lake transportation costs increased $0.72 per barrel as a result of a higher volume of product shipped by rail and decreased sales volumes relative to 2018.

Operating

Primary drivers of our operating expenses in the first half of 2019 were workforce, fuel, repairs and maintenance, and chemical costs. While total operating costs decreased $15 million, per-barrel operating expenses increased 11 percent primarily due to the lower sales volumes.

Per-unit Operating Expenses

| Six Months Ended June 30, | |

($/bbl) | 2019 | | | Percent Change | | | 2018 | |

Foster Creek | | | | | | | | | | | |

Fuel | | 2.64 | | | | 14 | | | | 2.32 | |

Non-fuel | | 7.00 | | | | (4 | ) | | | 7.29 | |

Total | | 9.64 | | | | - | | | | 9.61 | |

Christina Lake | | | | | | | | | | | |

Fuel | | 2.29 | | | | 12 | | | | 2.04 | |

Non-fuel | | 5.91 | | | | 25 | | | | 4.73 | |

Total | | 8.20 | | | | 21 | | | | 6.77 | |

Total | | 8.88 | | | | 11 | | | | 8.02 | |