| OMB APPROVAL |

OMB Number: 3235-0570

Expires: August 31, 2020

Estimated average burden hours per response: 20.6 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| Investment Company Act file number | 811-22359 |

| Papp Investment Trust |

| (Exact name of registrant as specified in charter) |

| 2201 E. Camelback Road, Suite 227B Phoenix, Arizona | 85016 |

| (Address of principal executive offices) | (Zip code) |

Benjamin V. Mollozzi, Esq.

| Ultimus Fund Solutions, LLC 225 Pictoria Drive, Suite 450 Cincinnati, Ohio 45246 |

| (Name and address of agent for service) |

| Registrant's telephone number, including area code: | (602) 956-0980 |

| Date of fiscal year end: | November 30 | |

| Date of reporting period: | May 31, 2019 |

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget ("OMB") control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to the Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

| Item 1. | Reports to Stockholders. |

Papp Investment Trust

Papp Small & Mid-Cap Growth Fund

Semi-Annual Report

May 31, 2019

(Unaudited)

Investment Adviser

L. Roy Papp & Associates, LLP

Phoenix, AZ

Beginning on January 1, 2021, as permitted by regulations adopted by the U.S. Securities and Exchange Commission, paper copies of the Fund’s shareholder reports like this one will no longer be sent by mail, unless you specifically request paper copies of the reports from the Fund or from your financial intermediary, such as a broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from the Fund electronically by contacting the Fund at 1-877-370-7277 or, if you own these shares through a financial intermediary, by contacting your financial intermediary.

You may elect to receive all future reports in paper free of charge. You can inform the Fund that you wish to continue receiving paper copies of your shareholder reports by contacting the Fund at 1-877-370-7277. If you own shares through a financial intermediary, you may contact your financial intermediary or follow instructions included with this document to elect to continue to receive paper copies of your shareholder reports. Your election to receive reports in paper will apply to all Funds held with the Fund complex or at your financial intermediary.

PAPP SMALL & MID-CAP GROWTH FUND | |

LETTER TO SHAREHOLDERS | June 30, 2019 |

Dear Fellow Shareholder,

We are writing to report on the performance results of the Papp Small & Mid-Cap Growth Fund (the “Fund”) for the six months ended May 31, 2019. As we mentioned in our December 31, 2018 report to Shareholders, markets here in the U.S. and all around the world were down sharply in December of 2018. As we told you, we believe that the markets were pricing in the start of a recession in 2019 based on fears that the Federal Reserve had over done it with four quarter-point rate increases during 2018 along with projections for additional rate increases in 2019. We believe oil and other commodity prices dropped sharply based on these fears.

A lot has changed during the first half of 2019. Most importantly, the Federal Reserve has changed their guidance on interest rates completely. The Fed is projecting no rate increase in 2019 and the possibility of one or more interest rate cuts. As of this writing, the markets are pricing in nearly a 100% probability of a quarter-point rate cut in July and a strong likelihood of one or two more cuts later on in 2019 or 2020. President Trump has been a very vocal critic of Fed Chairman Powell and has called for a reduction in the Fed Fund’s rate by a full percentage point. Markets have responded strongly to the prospects of a much more accommodative Federal Reserve. The markets have experienced volatility with President Trump’s on-again, off-again tariff threats primarily with China, but more recently with Mexico. The President is quite unpredictable, but one aspect of his Presidency that we think is predictable is his desire to be re-elected in 2020. We continue to believe that the President needs a strong economy and a trade resolution with China well in advance of November 2020, in order to win re-election.

Long-term, we still believe that for all of its unfair trade practices, censorship issues and authoritarian government, China remains an important global growth driver over the next several decades. Accordingly, we continue to own some companies where the growth of the Chinese economy is an important driver of results.

During the six months ended May 31, 2019, the Fund produced a total return of 5.00% as compared to the Russel MidCap® Growth Index (the “Benchmark”), which earned 7.12%. Interestingly, over the same period, the Standard & Poor’s 500 was up a mere 0.74%. While we are happy that the Fund returned 5% in six months, we trailed our Benchmark this period as it enjoyed solid returns driven primarily by technology companies and other very high valuation companies that we normally avoid. Given the strength of the Fund’s performance relative to its Benchmark for the last few years, we are happy with these results. Since inception, on March 8, 2010 through May 31, 2019, the Fund has produced an annualized total return of 11.41% compared to 13.19% for the Benchmark.

As of May 31, 2019, the net assets of the Fund were approximately $35 million. The Fund remains substantially fully invested with approximately 97.1% of its assets invested in stocks, which is consistent with our normal strategy. Though the Fund

1

mandate is to include small and mid-cap stocks, we remain heavily focused on the mid-cap portion of the market where we continue to find the most attractive values. The Fund is reasonably diversified with 30 holdings. During the past six months, the Fund’s sector weightings detracted from relative performance as Information Technology and Consumer Discretionary were the Benchmark’s best performing sectors and the Fund is significantly underweight in both sectors due to valuation and quality considerations.

Looking at individual holdings, the Fund experienced strong performance from Pegasystems, Inc., which produces leading-edge customer relationship software. CoStar Group, Inc., our software provider that services the real estate industry, also enjoyed strong growth. Finally, Worldpay, Inc., which is in the rapid growth financial tech sector, agreed to be acquired by Fidelity National Information Services which led to a significant advance during this period.

Individual companies that detracted from performance include, PRA Health Sciences, Inc., which is a contract research organization providing outsourced drug trials to biotech and pharmaceutical companies, saw a slow start to their new year. Westinghouse Air Brake Technologies Corporation, which supplies equipment and technology to the railroad industry, saw weakness due to its acquisition of General Electric’s (“GE”) transportation division. It is probably too early to see how that acquisition is developing, but the market fears that GE may sell its significant stake in the combined company and this has pressured the stock. Finally, our oil and lubricant company, Valvoline, Inc., experienced pricing pressure in the North American lubricant business which caused us to exit the position.

Looking forward, we continue to expect reasonable GDP and corporate earnings growth here in the U.S. in the coming quarters particularly as President Trump needs to cut back on his disruptive statements and tweets which cause uncertainty as we get closer to the 2020 elections. At this point, the Federal Reserve may well cut rates in July or perhaps later this year. While we continue to think that is a long-term mistake, it is unlikely to do dramatic damage to the economy or the markets in the short-term if the Fed decides cuts are necessary. The Fund’s performance suffered last December in the face of a possible global recession. Since the first of the year, the performance has come roaring back and for calendar year 2019, we are enjoying very strong returns. This aligns with our goal of participating in strong markets and striving to reduce downside risk in tough markets.

Here at L. Roy Papp & Associates, the Fund Manager, our firm promoted 2 Associates to full Partners which now brings our total to 11 Partners, 8 of which are Chartered Financial Analysts.

We appreciate your continued confidence in the Fund and as always, we would be happy to answer any questions that you may have about the Fund or other investment issues. We invite you to call any of us at 1-800-421-0131.

2

Warmest regards,

|

|

Rosellen C. Papp, CFA | Harry Papp, CFA |

Co-Portfolio Manager | President |

June 30, 2019 | June 30, 2019 |

|

|

Brian Riordan, CFA | Greg Smith, CFA |

Co-Portfolio Manager | Assistant Portfolio Manager |

June 30, 2019 | June 30, 2019 |

Past performance is not predictive of future performance. Investment results and principal value will fluctuate so that shares, when redeemed, may be worth more or less than their original cost. Current performance may be higher or lower than the performance data quoted. Performance current through the most recent month end is available by calling 1-877-370-7277.

An investor should consider the investment objectives, risks, charges and expenses of the Fund carefully before investing. The Fund’s prospectus contains this and other important information. To obtain a copy of the Fund’s prospectus please call 1-877-370-7277 and a copy will be sent to you free of charge. Please read the prospectus carefully before you invest. The Fund is distributed by Ultimus Fund Distributors, LLC.

The Letter to Shareholders seeks to describe some of the Adviser’s current opinions and views of the financial markets. Although the Adviser believes it has a reasonable basis for any opinions or views expressed, actual results may differ, sometimes significantly so, from those expected or expressed.

3

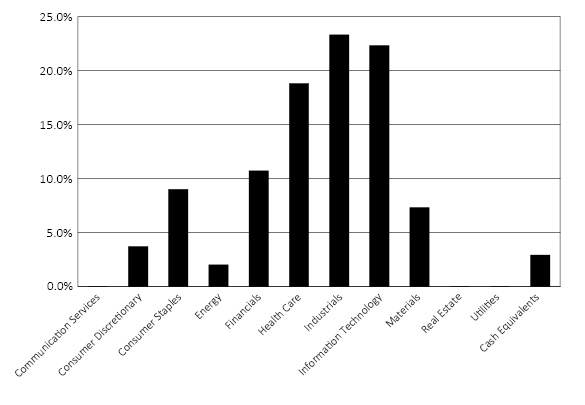

PAPP SMALL & MID-CAP GROWTH FUND

PORTFOLIO INFORMATION

May 31, 2019 (Unaudited)

Sector Diversification (% of Net Assets)

Top 10 Equity Holdings

Security Description | % of |

Mettler-Toledo International, Inc. | 5.6% |

Ecolab, Inc. | 5.3% |

Pegasystems, Inc. | 4.8% |

IDEX Corporation | 4.8% |

AMETEK, Inc. | 4.7% |

Expeditors International of Washington, Inc. | 4.6% |

ANSYS, Inc. | 4.6% |

CoStar Group, Inc. | 4.2% |

FactSet Research Systems, Inc. | 4.1% |

McCormick & Company, Inc. | 3.9% |

4

PAPP SMALL & MID-CAP GROWTH FUND | ||||||||

COMMON STOCKS — 94.1% | Shares | Value | ||||||

Consumer Discretionary — 3.7% | ||||||||

Specialty Retail — 3.7% | ||||||||

O’Reilly Automotive, Inc. (a) | 3,500 | $ | 1,299,795 | |||||

Consumer Staples — 9.0% | ||||||||

Food Products — 3.9% | ||||||||

McCormick & Company, Inc. | 8,700 | 1,357,548 | ||||||

Household Products — 5.1% | ||||||||

Church & Dwight Company, Inc. | 17,000 | 1,264,970 | ||||||

Clorox Company (The) | 3,500 | 520,835 | ||||||

| 1,785,805 | ||||||||

Energy — 2.0% | ||||||||

Oil, Gas & Consumable Fuels — 2.0% | ||||||||

Pioneer Natural Resources Company | 4,950 | 702,702 | ||||||

Financials — 10.7% | ||||||||

Banks — 1.4% | ||||||||

UMB Financial Corporation | 8,000 | 493,920 | ||||||

Capital Markets — 9.3% | ||||||||

FactSet Research Systems, Inc. | 5,100 | 1,418,820 | ||||||

SEI Investments Company | 13,400 | 673,350 | ||||||

T. Rowe Price Group, Inc. | 11,200 | 1,132,768 | ||||||

| 3,224,938 | ||||||||

Health Care — 15.8% | ||||||||

Health Care Equipment & Supplies — 6.9% | ||||||||

ResMed, Inc. | 5,300 | 604,836 | ||||||

Teleflex, Inc. | 3,100 | 893,730 | ||||||

Varian Medical Systems, Inc. (a) | 7,300 | 921,698 | ||||||

| 2,420,264 | ||||||||

Life Sciences Tools & Services — 8.9% | ||||||||

Mettler-Toledo International, Inc. (a) | 2,700 | 1,952,343 | ||||||

PRA Health Sciences, Inc. (a) | 13,200 | 1,144,836 | ||||||

| 3,097,179 | ||||||||

5

PAPP SMALL & MID-CAP GROWTH FUND | ||||||||

COMMON STOCKS — 94.1% (Continued) | Shares | Value | ||||||

Industrials — 23.3% | ||||||||

Air Freight & Logistics — 4.6% | ||||||||

Expeditors International of Washington, Inc. | 23,000 | $ | 1,600,570 | |||||

Electrical Equipment — 4.7% | ||||||||

AMETEK, Inc. | 20,100 | 1,645,989 | ||||||

Machinery — 9.8% | ||||||||

IDEX Corporation | 11,000 | 1,679,810 | ||||||

RBC Bearings, Inc. (a) | 6,750 | 960,525 | ||||||

Westinghouse Air Brake Technologies Corporation | 12,200 | 761,036 | ||||||

| 3,401,371 | ||||||||

Professional Services — 4.2% | ||||||||

CoStar Group, Inc. (a) | 2,900 | 1,477,956 | ||||||

Information Technology — 22.3% | ||||||||

Electronic Equipment, Instruments & Components — 2.9% | ||||||||

Trimble, Inc. (a) | 25,500 | 1,017,450 | ||||||

IT Services — 3.4% | ||||||||

Worldpay, Inc. - Class A (a) | 9,800 | 1,192,072 | ||||||

Semiconductors & Semiconductor Equipment — 6.6% | ||||||||

Analog Devices, Inc. | 11,200 | 1,082,144 | ||||||

NXP Semiconductors N.V. | 6,000 | 528,960 | ||||||

Silicon Laboratories, Inc. (a) | 7,100 | 664,347 | ||||||

| 2,275,451 | ||||||||

Software — 9.4% | ||||||||

ANSYS, Inc. (a) | 8,900 | 1,597,550 | ||||||

Pegasystems, Inc. | 23,400 | 1,688,076 | ||||||

| 3,285,626 | ||||||||

Materials — 7.3% | ||||||||

Chemicals — 7.3% | ||||||||

Ecolab, Inc. | 10,000 | 1,840,900 | ||||||

Scotts Miracle-Gro Company (The) | 7,600 | 680,428 | ||||||

| 2,521,328 | ||||||||

Total Common Stocks (Cost $16,325,344) | $ | 32,799,964 | ||||||

6

PAPP SMALL & MID-CAP GROWTH FUND | ||||||||

EXCHANGE-TRADED FUNDS — 3.0% | Shares | Value | ||||||

Health Care — 3.0% | ||||||||

Biotechnology — 3.0% | ||||||||

SPDR® S&P® Biotech ETF (Cost $827,662) | 13,300 | $ | 1,056,552 | |||||

| ||||||||

MONEY MARKET FUNDS — 2.8% | Shares | Value | ||||||

Fidelity Institutional Money Market Government Portfolio - Class I, 2.27% (b) (Cost $959,330) | 959,330 | $ | 959,330 | |||||

Total Investments at Value — 99.9% (Cost $18,112,336) | $ | 34,815,846 | ||||||

Other Assets in Excess of Liabilities — 0.1% | 37,489 | |||||||

Net Assets — 100.0% | $ | 34,853,335 | ||||||

(a) | Non-income producing security. |

(b) | The rate shown is the 7-day effective yield as of May 31, 2019. |

See accompanying notes to financial statements. | |

7

PAPP SMALL & MID-CAP GROWTH FUND | ||||

ASSETS | ||||

Investments in securities: | ||||

At cost | $ | 18,112,336 | ||

At value (Note 2) | $ | 34,815,846 | ||

Dividends receivable | 34,082 | |||

Other assets | 32,047 | |||

TOTAL ASSETS | 34,881,975 | |||

LIABILITIES | ||||

Payable for capital shares redeemed | 10,063 | |||

Payable to Adviser (Note 4) | 6,092 | |||

Payable to administrator (Note 4) | 7,080 | |||

Other accrued expenses | 5,405 | |||

TOTAL LIABILITIES | 28,640 | |||

NET ASSETS | $ | 34,853,335 | ||

NET ASSETS CONSIST OF: | ||||

Paid-in capital | $ | 17,879,147 | ||

Accumulated earnings | 16,974,188 | |||

NET ASSETS | $ | 34,853,335 | ||

Shares of beneficial interest outstanding (unlimited number of shares authorized, no par value) | 1,521,864 | |||

Net asset value, offering price and redemption price per share (Note 2) | $ | 22.90 | ||

See accompanying notes to financial statements. |

8

PAPP SMALL & MID-CAP GROWTH FUND | ||||

INVESTMENT INCOME | ||||

Dividend income (Net of foreign tax of $450) | $ | 138,677 | ||

EXPENSES | ||||

Investment advisory fees (Note 4) | 165,788 | |||

Professional fees | 34,058 | |||

Registration and filing fees | 17,994 | |||

Fund accounting fees (Note 4) | 16,658 | |||

Administration fees (Note 4) | 16,601 | |||

Transfer agent fees (Note 4) | 7,500 | |||

Insurance expense | 5,102 | |||

Custody and bank service fees | 5,004 | |||

Trustees’ fees (Note 4) | 3,400 | |||

Postage and supplies | 3,321 | |||

Printing of shareholder reports | 2,652 | |||

Other fees | 3,992 | |||

TOTAL EXPENSES | 282,070 | |||

Less fee reductions by the Adviser (Note 4) | (74,834 | ) | ||

NET EXPENSES | 207,236 | |||

NET INVESTMENT LOSS | (68,559 | ) | ||

REALIZED AND UNREALIZED GAINS ON INVESTMENTS | ||||

Net realized gains on investment transactions | 479,849 | |||

Net change in unrealized appreciation (depreciation) on investments | 1,232,525 | |||

NET REALIZED AND UNREALIZED GAINS ON INVESTMENTS | 1,712,374 | |||

NET INCREASE IN NET ASSETS FROM OPERATIONS | $ | 1,643,815 | ||

See accompanying notes to financial statements. |

9

PAPP SMALL & MID-CAP GROWTH FUND | ||||||||

| Six Months | Year | ||||||

FROM OPERATIONS | ||||||||

Net investment loss | $ | (68,559 | ) | $ | (148,419 | ) | ||

Net realized gains from investment transactions | 479,849 | 860,985 | ||||||

Net change in unrealized appreciation (depreciation) on investments | 1,232,525 | 1,916,393 | ||||||

Net increase in net assets from operations | 1,643,815 | 2,628,959 | ||||||

DISTRIBUTIONS TO SHAREHOLDERS (Note 2) | (861,010 | ) | (2,380,121 | ) | ||||

CAPITAL SHARE TRANSACTIONS | ||||||||

Proceeds from shares sold | 1,001,721 | 1,065,518 | ||||||

Net asset value of shares issued in reinvestment of distributions to shareholders | 795,660 | 2,149,398 | ||||||

Payments for shares redeemed | (662,276 | ) | (1,410,977 | ) | ||||

Net increase in net assets from capital share transactions | 1,135,105 | 1,803,939 | ||||||

TOTAL INCREASE IN NET ASSETS | 1,917,910 | 2,052,777 | ||||||

NET ASSETS | ||||||||

Beginning of period | 32,935,425 | 30,882,648 | ||||||

End of period | $ | 34,853,335 | $ | 32,935,425 | ||||

CAPITAL SHARE ACTIVITY | ||||||||

Shares sold | 46,197 | 48,029 | ||||||

Shares reinvested | 40,699 | 103,436 | ||||||

Shares redeemed | (30,981 | ) | (65,871 | ) | ||||

Net increase in shares outstanding | 55,915 | 85,594 | ||||||

Shares outstanding at beginning of period | 1,465,949 | 1,380,355 | ||||||

Shares outstanding at end of period | 1,521,864 | 1,465,949 | ||||||

See accompanying notes to financial statements. |

10

PAPP SMALL & MID-CAP GROWTH FUND | ||||||||||||||||||||||||

Per Share Data for a Share Outstanding Throughout Each Period: | ||||||||||||||||||||||||

| Six Months | Year | Year | Year | Year | Year | ||||||||||||||||||

Net asset value at beginning of period | $ | 22.47 | $ | 22.37 | $ | 17.73 | $ | 18.14 | $ | 17.92 | $ | 16.48 | ||||||||||||

Income (loss) from investment operations: | ||||||||||||||||||||||||

Net investment loss | (0.04 | ) | (0.10 | ) | (0.09 | ) | (0.04 | ) | (0.05 | ) | (0.07 | ) | ||||||||||||

Net realized and unrealized gains on investments | 1.06 | 1.93 | 4.73 | 0.05 | 0.82 | 1.58 | ||||||||||||||||||

Total from investment operations | 1.02 | 1.83 | 4.64 | 0.01 | 0.77 | 1.51 | ||||||||||||||||||

Less distributions: | ||||||||||||||||||||||||

From net realized gains from investment transactions | (0.59 | ) | (1.73 | ) | — | (0.42 | ) | (0.55 | ) | (0.07 | ) | |||||||||||||

Net asset value at end of period | $ | 22.90 | $ | 22.47 | $ | 22.37 | $ | 17.73 | $ | 18.14 | $ | 17.92 | ||||||||||||

Total return (a) | 5.00 | %(b) | 8.81 | % | 26.17 | % | 0.14 | % | 4.41 | % | 9.17 | % | ||||||||||||

Net assets at end of period (000’s) | $ | 34,853 | $ | 32,935 | $ | 30,883 | $ | 25,067 | $ | 26,648 | $ | 25,342 | ||||||||||||

Ratios/supplementary data: | ||||||||||||||||||||||||

Ratio of total expenses to average net assets (c) | 1.70 | %(f) | 1.61 | % | 1.73 | % | 1.73 | % | 1.70 | % | 1.79 | % | ||||||||||||

Ratio of net expenses to average net assets (c)(d) | 1.25 | %(f) | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | 1.25 | % | ||||||||||||

Ratio of net investment loss to average net assets (d)(e) | (0.41 | %)(f) | (0.46 | %) | (0.47 | %) | (0.19 | %) | (0.29 | %) | (0.42 | %) | ||||||||||||

Portfolio turnover rate | 4 | %(b) | 5 | % | 19 | % | 14 | % | 18 | % | 14 | % | ||||||||||||

(a) | Total return is a measure of the change in value of an investment in the Fund over the periods covered. The returns shown do not reflect the deduction of taxes a shareholder would pay on Fund distributions, if any, or the redemption of Fund shares. Had the Adviser not reduced its fees, total returns would have been lower. |

(b) | Not annualized. |

(c) | The ratios of expenses to average net assets do not reflect the Fund’s proportionate share of expenses of the underlying investment companies in which the Fund invests. |

(d) | Ratio was determined after advisory fee reductions (Note 4). |

(e) | Recognition of net investment loss by the Fund is affected by the timing of the declaration of dividends by the underlying investment companies in which the Fund invests. |

(f) | Annualized. |

See accompanying notes to financial statements. | |

11

PAPP SMALL & MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS

May 31, 2019 (Unaudited)

1. Organization

Papp Small & Mid-Cap Growth Fund (the “Fund”) is a diversified series of Papp Investment Trust (the “Trust”), an open-end investment company established as an Ohio business trust under a Declaration of Trust dated November 12, 2009.

The investment objective of the Fund is long-term capital growth.

2. Significant Accounting Policies

The Fund follows accounting and reporting guidance under Financial Accounting Standards Board Accounting Standards Codification Topic 946, “Financial Services – Investment Companies.” The following is a summary of the Fund’s significant accounting policies used in preparation of its financial statements. These policies are in conformity with accounting principles generally accepted in the United States of America (“GAAP”).

Securities valuation – The Fund’s portfolio securities are valued at market value as of the close of regular trading on the New York Stock Exchange (the “NYSE”) (normally 4:00 p.m. Eastern time) on each business day the NYSE is open. Securities, including common stocks and exchange-traded funds (“ETFs”), listed on the NYSE or other exchanges are valued on the basis of their last sale price on the exchanges on which they are primarily traded. If there are no sales on that day, the securities are valued at the closing bid price on the NYSE or other primary exchange for that day. NASDAQ listed securities are valued at the NASDAQ Official Closing Price. If there are no sales on that day, the securities are valued at the last bid price as reported by NASDAQ. Securities traded in the over-the-counter market are valued at the last reported sale price, if available, otherwise at the most recently quoted bid price. To the extent the Fund is invested in money market funds and other open-end investment companies, except for ETFs, that are registered under the Investment Company Act of 1940, as amended (the “1940 Act”), the Fund’s net asset value per share (“NAV”) is calculated based upon the NAVs reported by such registered open-end companies, and the prospectuses for these companies explain the circumstances under which they will use fair value pricing and the effects of using fair value pricing. When using a quoted price and when the market is considered active, the security will be classified as Level 1 within the fair value hierarchy (see below). In the event that market quotations are not readily available or are considered unreliable due to market or other events, securities and other assets are valued at fair value as determined in good faith in accordance with procedures adopted by the Board of Trustees and will be classified as Level 2 or 3 within the fair value hierarchy, depending on the inputs used. Factors for determining when portfolio investments are subject to fair value determination include, but are not limited to, the following: the spread between bid and asked prices is substantial; infrequency of sales; thinness of market;

12

PAPP SMALL & MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

the size of reported trades; a temporary lapse in the provision of prices by any reliable pricing source; and actions of the securities or future markets, such as the suspension or limitation of trading.

GAAP establishes a single authoritative definition of fair value, sets out a framework for measuring fair value and requires additional disclosures about fair value measurements.

Various inputs are used in determining the value of the Fund’s investments. These inputs are summarized in the three broad levels listed below:

● | Level 1 – quoted prices in active markets for identical securities |

● | Level 2 – other significant observable inputs |

● | Level 3 – significant unobservable inputs |

The inputs or methodology used for valuing securities are not necessarily an indication of the risks associated with investing in those securities. The inputs used to measure fair value may fall into different levels of the fair value hierarchy. In such cases, for disclosure purposes, the level in the fair value hierarchy within which the fair value measurement falls in its entirety is determined based on the lowest level input that is significant to the fair value measurement.

The following is a summary of the inputs used to value the Fund’s investments as of May 31, 2019:

| Level 1 | Level 2 | Level 3 | Total | ||||||||||||

Common Stocks | $ | 32,799,964 | $ | — | $ | — | $ | 32,799,964 | ||||||||

Exhange-Traded Funds | 1,056,552 | — | — | 1,056,552 | ||||||||||||

Money Market Funds | 959,330 | — | — | 959,330 | ||||||||||||

Total | $ | 34,815,846 | $ | — | $ | — | $ | 34,815,846 | ||||||||

Refer to the Fund’s Schedule of Investments for a listing of the common stocks by industry type. The Fund did not hold derivative instruments or any assets or liabilities that were measured at fair value on a recurring basis using significant unobservable inputs (Level 3) as of or during the six months ended May 31, 2019.

Share valuation – The NAV of the Fund is calculated daily by dividing the total value of the Fund’s assets, less liabilities, by the number of shares outstanding. The offering price and redemption price per share of the Fund is equal to the NAV.

13

PAPP SMALL & MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

Investment income – Dividend income is recorded on the ex-dividend date. Interest income is accrued as earned. Withholding taxes on foreign dividends have been recorded in accordance with the Fund’s understanding of the applicable country’s tax rules and rates.

Investment transactions – Investment transactions are accounted for on the trade date. Realized gains and losses on investments sold are determined on a specific identification basis.

Distributions to shareholders – Distributions arising from net investment income and net realized capital gains, if any, are paid to shareholders at least once each year. The amount of distributions from net investment income and net realized capital gains are determined in accordance with federal income tax regulations, which may differ from GAAP. Dividends and distributions to shareholders are recorded on the ex-dividend date. For the periods ended May 31, 2019 and November 30, 2018, the tax character of all distributions paid to shareholders was long-term capital gains.

Estimates – The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Federal income tax – The Fund has qualified and intends to continue to qualify each year as a “regulated investment company” under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”). By so qualifying, the Fund will not be subject to federal income taxes to the extent that it distributes its net investment income and any net realized capital gains in accordance with the Code.

In order to avoid imposition of the excise tax applicable to regulated investment companies, it is also the Fund’s intention to declare as dividends in each calendar year at least 98% of its net investment income (earned during the calendar year) and 98.2% of its net realized capital gains (earned during the twelve months ended November 30) plus undistributed amounts from prior years.

The following information is computed on a tax basis for each item as of May 31, 2019:

Tax cost of portfolio investments | $ | 18,112,339 | ||

Gross unrealized appreciation | $ | 17,176,890 | ||

Gross unrealized depreciation | (473,383 | ) | ||

Net unrealized appreciation | 16,703,507 | |||

Accumulated capital and other gains | 270,681 | |||

Accumulated earnings | $ | 16,974,188 |

14

PAPP SMALL & MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

The difference between the federal income tax cost of portfolio investments and the financial statement cost of portfolio investments is due to certain timing differences in the recognition of capital gains or losses under income tax regulations and GAAP. These “book/tax” differences are temporary in nature and are primarily due to the tax deferral of losses on wash sales.

The Fund recognizes the tax benefits or expenses of uncertain tax positions only when the position is “more likely than not” to be sustained assuming examination by tax authorities. Management has reviewed the Fund’s tax positions taken on federal income tax returns for the current and all open tax years (generally, three years) and has concluded that no provision for unrecognized tax benefits or expenses is required in these financial statements and does not expect this to change over the next twelve months. The Fund identifies its major tax jurisdiction as U.S. Federal.

3. Investment Transactions

During the six months ended May 31, 2019, cost of purchases and proceeds from sales of investment securities, other than short-term investments, were $1,281,236 and $1,516,970, respectively.

4. Transactions with Related Parties

Certain Trustees and officers of the Trust are directors and officers of L. Roy Papp & Associates, LLP (the “Adviser”) or of Ultimus Fund Solutions, LLC (“Ultimus”), the Fund’s administrator, transfer agent and fund accounting agent, and Ultimus Fund Distributors, LLC (the “Distributor”), the Fund’s principal underwriter. These Trustees and officers are not compensated by the Fund for their services as Trustees and officers of the Trust.

INVESTMENT ADVISORY AGREEMENT

The Fund’s investments are managed by the Adviser pursuant to the terms of an Investment Advisory Agreement. For its services, the Fund pays the Adviser an advisory fee, computed daily and paid monthly, at the annual rate of 1.00% of its average daily net assets.

The Adviser has contractually agreed to reduce its advisory fees and to reimburse the Fund’s operating expenses to the extent necessary so that the Fund’s annual ordinary operating expenses (excluding brokerage costs, taxes, interest, acquired fund fees and expenses and extraordinary expenses, if any) do not exceed an amount equal to 1.25% of its average daily net assets. This Expense Limitation Agreement (“ELA”) remains in effect until at least April 1, 2020. Accordingly, the Adviser reduced its advisory fees by $74,834 during the six months ended May 31, 2019.

15

PAPP SMALL & MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

The ELA permits the Adviser to recover fee reductions and expense reimbursements made on behalf of the Fund, but only for a period of three years after such reductions or reimbursements were incurred and only if such recovery will not cause the Fund’s expense ratio to exceed the annual rate of 1.25%. As of May 31, 2019, the Adviser may in the future recover fee reductions and expense reimbursements totaling $387,471. The Adviser may recover a portion of this amount no later than the dates as stated below:

November 30, 2019 | $ | 61,503 | ||

November 30, 2020 | 134,731 | |||

November 30, 2021 | 116,403 | |||

May 31, 2022 | 74,834 | |||

| $ | 387,471 |

OTHER SERVICE PROVIDERS

Ultimus provides administration, fund accounting and transfer agency services to the Fund. The Fund pays Ultimus fees in accordance with the agreements for such services. In addition, the Fund pays out-of-pocket expenses including but not limited to, postage, supplies and costs of pricing the Fund’s portfolio securities. The Distributor is a wholly-owned subsidiary of Ultimus. The Distributor is compensated by the Adviser (not the Fund) for acting as principal underwriter.

PLAN OF DISTRIBUTION

The Trust has adopted a plan of distribution (the “Plan”) pursuant to Rule 12b-1 under the 1940 Act. Under the Plan, the Fund may incur certain expenses related to the distribution of its shares. The annual limitation of payment of expenses pursuant to the Plan is 0.25% of the Fund’s average daily net assets. The Board of Trustees has not authorized the payment of any fees pursuant to the Plan until at least April 1, 2020.

TRUSTEE COMPENSATION

Each Trustee who is not an interested person of the Trust (“Independent Trustee”) receives from the Fund a fee of $500 for each Board meeting attended, except that the Chair of the Committee of Independent Trustees receives a fee of $700 for each Board meeting attended.

16

PAPP SMALL & MID-CAP GROWTH FUND

NOTES TO FINANCIAL STATEMENTS (Continued)

PRINCIPAL HOLDER OF FUND SHARES

As of May 31, 2019, the following shareholder owned of record 25% or more of the outstanding shares of the Fund:

NAME OF RECORD OWNER | % Ownership |

Charles Schwab & Company, Inc. (for the benefit of its customers) | 59% |

A beneficial owner of 25% or more of the Fund’s outstanding shares may be considered a controlling person. That shareholder’s vote could have a more significant effect on matters presented at a shareholders’ meeting.

5. Contingencies and Commitments

The Fund indemnifies the Trust’s officers and Trustees for certain liabilities that might arise from their performance of their duties to the Fund. Additionally, in the normal course of business the Fund enters into contracts that contain a variety of representations and warranties and which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would involve future claims that may be made against the Fund that have not yet occurred. However, based on experience, the Fund expects the risk of loss to be remote.

6. Subsequent Events

The Fund is required to recognize in the financial statements the effects of all subsequent events that provide additional evidence about conditions that existed as of the date of the Statement of Assets and Liabilities. For non-recognized subsequent events that must be disclosed to keep the financial statements from being misleading, the Fund is required to disclose the nature of the event as well as an estimate of its financial effect, or a statement that such an estimate cannot be made. Management has evaluated subsequent events through the issuance of these financial statements and has noted no such events.

17

PAPP SMALL & MID-CAP GROWTH FUND |

We believe it is important for you to understand the impact of costs on your investment. As a shareholder of the Fund, you incur ongoing costs, including management fees and other operating expenses. The following examples are intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

A mutual fund’s ongoing costs are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The expenses in the table below are based on an investment of $1,000 made at the beginning of the most recent period (December 1, 2018) and held until the end of the period (May 31, 2019).

The table below illustrates the Fund’s ongoing costs in two ways:

Actual fund return – This section helps you to estimate the actual expenses that you paid over the period. The “Ending Account Value” shown is derived from the Fund’s actual return, and the third column shows the dollar amount of operating expenses that would have been paid by an investor who started with $1,000 in the Fund. You may use the information here, together with the amount you invested, to estimate the expenses that you paid over the period.

To do so, simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number given for the Fund under the heading “Expenses Paid During Period.”

Hypothetical 5% return – This section is intended to help you compare the Fund’s ongoing costs with those of other mutual funds. It assumes that the Fund had an annual return of 5% before expenses during the period shown, but that the expense ratio is unchanged. In this case, because the return used is not the Fund’s actual return, the results do not apply to your investment. The example is useful in making comparisons because the U.S. Securities and Exchange Commission (the “SEC”) requires all mutual funds to calculate expenses based on a 5% return. You can assess the Fund’s ongoing costs by comparing this hypothetical example with the hypothetical examples that appear in shareholder reports of other funds.

Note that expenses shown in the table are meant to highlight and help you compare ongoing costs only. The Fund does not charge transaction fees, such as purchase or redemption fees, nor does it carry a “sales load.”

The calculations assume no shares were bought or sold during the period. Your actual costs may have been higher or lower, depending on the amount of your investment and the timing of any purchases or redemptions.

18

PAPP SMALL & MID-CAP GROWTH FUND

ABOUT YOUR FUND’S EXPENSES (Unaudited) (Continued)

More information about the Fund’s expenses, including historical annual expense ratios, can be found in this report. For additional information on operating expenses and other shareholder costs, please refer to the Fund’s prospectus.

| Beginning | Ending | Expenses |

Based on Actual Fund Return | $1,000.00 | $1,050.00 | $6.39 |

Based on Hypothetical 5% Return (before expenses) | $1,000.00 | $1,018.70 | $6.29 |

* | Expenses are equal to the Fund’s annualized net expense ratio of 1.25% for the period, multiplied by the average account value over the period, multiplied by 182/365 (to reflect the one-half year period). |

19

PAPP SMALL & MID-CAP GROWTH FUND |

A description of the policies and procedures that the Fund uses to vote proxies relating to portfolio securities is available without charge upon request by calling toll-free 1-877-370-7277, or on the SEC’s website at https://www.sec.gov. Information regarding how the Fund voted proxies relating to portfolio securities during the most recent 12-month period ended June 30 is available without charge upon request by calling toll-free 1-877-370-7277, or on the SEC’s website at https://www.sec.gov.

The Trust files a complete listing of portfolio holdings for the Fund with the SEC as of the end of the first and third quarters of each fiscal year on Form N-Q. These filings are available upon request by calling 1-877-370-7277. Furthermore, you may obtain a copy of the filings on the SEC’s website at https://www.sec.gov.

20

PAPP SMALL & MID-CAP GROWTH FUND

APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited)

L. Roy Papp & Associates, LLP (the “Adviser”), 2201 E. Camelback Road, Suite 227B, Phoenix, Arizona 85016, serves as the investment adviser to the Papp Small & Mid-Cap Growth Fund (the “Fund”). The Adviser provides the Fund with a continuous program of investing the Fund’s assets and determining the composition of the Fund’s portfolio. In addition to serving as the investment adviser to the Fund, the Adviser provides investment advisory services to individuals, trusts, retirement plans, endowments, and foundations.

The Adviser is subject to the oversight of the Fund and the Fund’s board of trustees (the “Board”). The Adviser serves as investment adviser to the Fund pursuant to a written investment management agreement between the Adviser and the Fund dated May 1, 2012 (the “Advisory Agreement”). The Advisory Agreement provides that the Adviser shall not be liable for any loss suffered by the Fund or its shareholders, except by reason of its own willful misfeasance, bad faith or gross negligence, or from its reckless disregard of its obligations and duties under the Advisory Agreement. The Advisory Agreement is terminable by the Fund at any time, without penalty, either by action of the Board or upon a vote of the holders of a majority of the outstanding voting securities of the Fund upon 60 days’ prior written notice to the Adviser. The Advisory Agreement is also terminable by the Adviser with 60 days’ prior written notice to the Fund, and will terminate automatically in the event of its “assignment,” as defined in the Investment Company Act of 1940 (the “1940 Act”), including in the event of a change of control or sale of the Adviser. The Advisory Agreement’s initial two-year term ended May 1, 2014, after which it may be continued from year to year thereafter only as long as such continuance is approved annually by (a) the vote of a majority of the Board, including a majority of the Trustees who are not “interested persons,” as defined by the 1940 Act, of the Trust (the “Independent Trustees”), or (b) the vote of a majority of the Fund’s outstanding voting securities (as defined in the 1940 Act).

The Board, including the Fund’s Independent Trustees voting separately, reviewed and approved the continuance of the Advisory Agreement for an additional term of one year at an in-person meeting held on April 23, 2019, at which all of the Trustees were present. In the course of their deliberations, the Independent Trustees were advised by their independent legal counsel of their obligations in determining to approve the Advisory Agreement. The Board received and reviewed a substantial amount of information provided by the Adviser in response to requests of the Board and counsel.

In considering whether to approve the Advisory Agreement, the Board, including the Independent Trustees, did not identify any single factor as determinative, and each Trustee weighed the various factors independently as he or she deemed appropriate. The Board considered the following matters, among other things, in connection with its approval of the Advisory Agreement.

21

PAPP SMALL & MID-CAP GROWTH FUND

APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited) (Continued)

Nature, Extent and Quality of Services

The Board received and considered various information, which it had previously requested from the Adviser, regarding the nature, extent and quality of services provided to the Fund by the Adviser. The Board specifically reviewed the qualifications, backgrounds and responsibilities of the key personnel that oversee the investment management and day-to-day operations of the Fund, including the support resources available for investment research. The Board noted that Ms. Papp, Mr. Riordan, and Mr. Smith are responsible for the day-to-day management of the Fund. The Board noted that the Adviser had previously served as the investment adviser and investment sub-adviser to other open-end registered investment companies with substantially similar investment objectives and strategies. The Board considered that the Adviser has a staff of skilled investment professionals who provide research, trading and compliance support services to the Fund and determined that the Adviser possesses adequate resources to manage the Fund. The Board also considered the Adviser’s compliance program and noted the resources it has dedicated towards compliance, including providing a seasoned compliance officer to oversee its compliance program. The Board also considered the overall investment management capabilities of the Adviser and its ongoing financial commitment to the Fund. The Board considered the Adviser’s responsibilities with regards to brokerage selection and best execution and noted that the Adviser has never entered into any “soft dollar” arrangements.

Investment Performance of the Fund

The Fund’s returns were compared to the returns of the Index, comparable private accounts managed by the Adviser, and other domestic equity funds of similar size with similar investment styles. In reviewing the comparative performance, the Board considered that the Fund’s average annual total return was higher than the average and median returns of “Mid Cap Growth Funds Under $50 Million” as derived from Morningstar, Inc. for the one-year period ended March 31, 2019, and higher than the average and median returns for the three-year and five-year periods ended March 31, 2019. The Board then reviewed the Fund’s performance as compared to the performance of funds in a peer group of five funds selected by the Adviser. The Board considered the Adviser’s explanation of the reasons for selecting the particular funds presented, noting that the selected funds had a strategy and risk profile that were similar to those of the Fund. The Board noted that the Fund generally performed well as compared to this peer group for the one- and five-year periods ended March 31, 2019. The Board also considered that the Fund’s average annual total return was higher than the return of the Index for the one-year period, but lower for the five-year and since inception periods ended March 31, 2019. The Board noted the consistency of the Adviser’s management of the Fund in accordance with the Fund’s investment objective and policies and considered that the Adviser believes the Fund’s performance

22

PAPP SMALL & MID-CAP GROWTH FUND

APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited) (Continued)

to be consistent with its strategy. The Board further noted that the Adviser has been managing the Fund, predecessor funds and private accounts using this same investment philosophy for more than 18 years and that the Adviser’s investment process and long-term performance record over a full market cycle were important factors in the Board’s evaluation of the quality of services to be provided by the Adviser under the Advisory Agreement.

Expenses

The Board considered statistical information regarding the Fund’s expense ratio and its various components, including the contractual advisory fee and fee reductions and/or expense reimbursements. It also considered a comparison of these fees and expenses to the expense information for other domestic equity funds of similar size with similar investment styles. The Fund’s overall expense ratio, after contractual fee reductions, was compared to funds within its relevant Morningstar peer group, as defined above. The Board noted that the overall expense ratio of the Fund, after fee reductions, was higher than the average and median expense ratios for the peer group presented. The Board also observed that, under the expense cap arrangement agreed to by the Adviser, this expense ratio will be maintained until at least April 1, 2020.

Investment Advisory Fee Rates

The Board reviewed and considered the proposed contractual investment advisory fee rate payable by the Fund to the Adviser for investment advisory services. Additionally, the Board received and considered information comparing the Fund’s advisory fee rate with those of the other funds in its relevant Morningstar peer group, as defined above, and private accounts managed by the Adviser with a comparable investment strategy. The Board noted that the advisory fee rate for the Fund was higher than the median and average rates for the peer group presented. The Board then discussed the differences in the Fund’s advisory fee rate and the advisory fee rate charged to private accounts managed by the Adviser with a comparable investment strategy. The Adviser discussed the reasons for lower fees for the private accounts in some instances, noting that the applicable accounts have lower operational and compliance costs relative to the Fund.

The Board reviewed the Adviser’s financial statements and discussed its financial condition. The Board noted that the Adviser is operating at a loss in providing services to the Fund because of the fee reductions and expense reimbursements it has incurred since the Fund’s inception. The Board discussed the level of Fund assets necessary for the Adviser to break even, the projected profits of the Adviser and the other ancillary benefits that the Adviser may receive with regard to providing advisory services to the Fund. The Board noted that, in light of the Fund’s asset level, these were not primary factors at this time. The Board further considered the Adviser’s commitment to grow the

23

PAPP SMALL & MID-CAP GROWTH FUND

APPROVAL OF INVESTMENT ADVISORY AGREEMENT (Unaudited) (Continued)

Fund’s assets and the Adviser’s representation that it has adequate financial reserves to cover its anticipated losses from providing advisory services to the Fund for several years.

Economies of Scale

The Board noted that the investment advisory fee schedule for the Fund does not contain breakpoints, but further noted that the fee reduction and expense reimbursement arrangement creates a single expense ratio and that shareholders have benefited from the lower expense ratios that resulted from the fee reductions and expense reimbursements. The Board noted that the Fund’s assets have grown, but not to an extent that permits it to realize any meaningful economies of scale. The Board observed that as the Fund grows further in assets, this factor will become more relevant to its consideration process.

Conclusion

After full consideration of the above factors as well as other factors, the Board, including all of the Independent Trustees, unanimously concluded that approval of the continuance of the Advisory Agreement was in the best interest of the Fund and its shareholders.

24

Privacy Notice | ||

FACTS | WHAT DOES PAPP INVESTMENT TRUST DO WITH YOUR PERSONAL INFORMATION? | |

Why? | Financial companies choose how they share your personal information. Federal law gives consumers the right to limit some but not all sharing. Federal law also requires us to tell you how we collect, share, and protect your personal information. Please read this notice carefully to understand what we do. | |

What? | The types of personal information we collect and share depend on the product or service you have with us. This information can include: ■ Social Security number ■ account balances and account transactions ■ account transactions, transaction or loss history and purchase history ■ checking account information and wire transfer instructions When you are no longer our customer, we continue to share your information as described in this notice. | |

How? | All financial companies need to share customers’ personal information to run their everyday business. In the section below, we list the reasons financial companies can share their customers’ personal information; the reasons Papp Investment Trust chooses to share; and whether you can limit this sharing. | |

Reasons we can share your personal information | Does the Papp Investment share? | |

For our everyday business purposes – | Yes | |

For our marketing purposes – | No | |

For joint marketing with other financial companies | No | |

For our affiliates’ everyday business purposes – | No | |

For our affiliates’ everyday business purposes – | No | |

For nonaffiliates to market to you | No | |

Questions? | Call 1-877-370-7277. | |

25

Page 2 |

Who we are | |

Who is providing this notice? | Papp Investment Trust Ultimus Fund Distributors, LLC |

What we do | |

How does Papp Investment Trust protect my personal information? | To protect your personal information from unauthorized access and use, we use security measures that comply with federal law. These measures include computer safeguards and secured files and buildings. |

How does Papp Investment Trust collect my personal information? | We collect your personal information, for example, when you ■ open an account or deposit money ■ buy securities from us or sell securities to us ■ make deposits or withdrawals from your account provide account information ■ give us your account information ■ make a wire transfer ■ tell us who receives the money ■ tell us where to send the money ■ show your government-issued ID ■ show your driver’s license |

Why can’t I limit all sharing? | Federal law gives you the right to limit only ■ sharing for affiliates’ everyday business purposes – information about your creditworthiness ■ affiliates from using your information to market to you ■ sharing for nonaffiliates to market to you State laws and individual companies may give you additional rights to limit sharing. |

Definitions | |

Affiliates | Companies related by common ownership or control. They can be financial and nonfinancial companies. ■ L. Roy Papp & Associates, LLP could be deemed to be an affiliate. |

Nonaffiliates | Companies not related by common ownership or control. They can be financial and nonfinancial companies ■ Papp Investment Trust does not share your personal information with nonaffiliates so they can market to you. |

Joint marketing | A formal agreement between nonaffiliated financial companies that together market financial products or services to you. ■ Papp Investment Trust doesn’t jointly market financial products or services to you. |

26

| Item 2. | Code of Ethics. |

Not required

| Item 3. | Audit Committee Financial Expert. |

Not required

| Item 4. | Principal Accountant Fees and Services. |

Not required

| Item 5. | Audit Committee of Listed Registrants. |

Not applicable

| Item 6. | Schedule of Investments. |

| (a) | Not applicable [schedule filed with Item 1] |

| (b) | Not applicable |

| Item 7. | Disclosure of Proxy Voting Policies and Procedures for Closed-End Management Investment Companies. |

Not applicable

| Item 8. | Portfolio Managers of Closed-End Management Investment Companies. |

Not applicable

| Item 9. | Purchases of Equity Securities by Closed-End Management Investment Company and Affiliated Purchasers. |

Not applicable

| Item 10. | Submission of Matters to a Vote of Security Holders. |

The registrant’s Committee of Independent Trustees shall review shareholder recommendations to fill vacancies on the registrant’s board of trustees if such recommendations are submitted in writing, addressed to the Committee at the registrant’s offices and meet any minimum qualifications adopted by the Committee. The Committee may adopt, by resolution, a policy regarding its procedures for considering candidates for the board of trustees, including any recommended by shareholders.

| Item 11. | Controls and Procedures. |

(a) Based on their evaluation of the registrant’s disclosure controls and procedures (as defined in Rule 30a-3(c) under the Investment Company Act of 1940) as of a date within 90 days of the filing date of this report, the registrant’s principal executive officer and principal financial officer have concluded that such disclosure controls and procedures are reasonably designed and are operating effectively to ensure that material information relating to the registrant, including its consolidated subsidiaries, is made known to them by others within those entities, particularly during the period in which this report is being prepared, and that the information required in filings on Form N-CSR is recorded, processed, summarized, and reported on a timely basis.

(b) There were no changes in the registrant’s internal control over financial reporting (as defined in Rule 30a-3(d) under the Investment Company Act of 1940) that occurred during the second fiscal quarter of the period covered by this report that have materially affected, or are reasonably likely to materially affect, the registrant’s internal control over financial reporting.

| Item 12. | Disclosure of Securities Lending Activities for Closed-End Management Investment Companies. |

Not applicable

| Item 13. | Exhibits. |

File the exhibits listed below as part of this Form. Letter or number the exhibits in the sequence indicated.

(a)(1) Any code of ethics, or amendment thereto, that is the subject of the disclosure required by Item 2, to the extent that the registrant intends to satisfy the Item 2 requirements through filing of an exhibit: Not required

(a)(2) A separate certification for each principal executive officer and principal financial officer of the registrant as required by Rule 30a-2(a) under the Act (17 CFR 270.30a-2(a)): Attached hereto

(a)(3) Any written solicitation to purchase securities under Rule 23c-1 under the Act (17 CFR 270.23c-1) sent or given during the period covered by the report by or on behalf of the registrant to 10 or more persons: Not applicable

(a)(4) Change in the registrant’s independent public accountants: Not applicable

(b) Certifications required by Rule 30a-2(b) under the Act (17 CFR 270.30a-2(b)): Attached hereto

| Exhibit 99.CERT | Certifications required by Rule 30a-2(a) under the Act |

| Exhibit 99.906CERT | Certifications required by Rule 30a-2(b) under the Act |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| (Registrant) | Papp Investment Trust | ||

| By (Signature and Title)* | /s/ Harry A. Papp | ||

| Harry A. Papp, President | |||

| Date | July 31, 2019 | ||

| Pursuant to the requirements of the Securities Exchange Act of 1934 and the Investment Company Act of 1940, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated. | |||

| By (Signature and Title)* | /s/ Harry A. Papp | ||

| Harry A. Papp, President | |||

| Date | July 31, 2019 | ||

| By (Signature and Title)* | /s/ Theresa M. Bridge | ||

| Theresa M. Bridge, Treasurer and Principal Financial Officer | |||

| Date | July 31, 2019 | ||

| * | Print the name and title of each signing officer under his or her signature. |