As filed with the Securities and Exchange Commission on November 8, 2022

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-3

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

UNITED STATES COMMODITY INDEX FUNDS TRUST

(Exact Name of Registrant as Specified in Its Charter)

| | | |

| Delaware | 6770 | 27-1537655 |

(State or Other Jurisdiction of Incorporation or Organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

United States Commodity Funds LLC 1850 Mt. Diablo Boulevard, Suite 640 Walnut Creek, California 94596 510.522.9600 | Daphne G. Frydman 1850 Mt. Diablo Boulevard, Suite 640 Walnut Creek, California 94596 510.522.9600 |

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices) | (Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service) |

Copies to:

James M. Cain, Esq.

Owen J. Pinkerton, Esq.

Raymond A. Ramirez, Esq.

Eversheds Sutherland (US) LLP

700 Sixth Street, N.W., Suite 700

Washington, DC 20001-3980

202.383.0100

Approximate date of commencement of proposed sale to the public: As soon as practicable after this registration statement becomes effective.

If the only securities being registered on this form are being offered pursuant to dividend or interest reinvestment plans, check the following box. o

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, other than securities offered only in connection with dividend or interest reinvestment plans, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a registration statement pursuant to General Instruction I.D. or a post-effective amendment thereto that shall become effective upon filing with the Commission pursuant to Rule 462(e) under the Securities Act, check the following box. o

If this Form is a post-effective amendment to a registration statement filed pursuant to General Instruction I.D. filed to register additional securities or additional classes of securities pursuant to Rule 413(b) under the Securities Act, check the following box. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the 1934 Act:

| Large accelerated filer | o | | Accelerated filer | x |

| Non-accelerated filer | o | (Do not check if a smaller reporting company) | Smaller reporting company | o |

| | | | Emerging growth company | o |

| | | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. o

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Securities and Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated November 8, 2022

PRELIMINARY PROSPECTUS

United States Copper Index Fund*

Shares

*Principal U.S. Listing Exchange: NYSE Arca, Inc.

The United States Copper Index Fund (“CPER”), a series of the United States Commodity Index Funds Trust, is an exchange traded fund that issues shares that trade on the NYSE Arca stock exchange (“NYSE Arca”). CPER’s investment objective is for the daily changes in percentage terms of its shares’ net asset value (“NAV”) to reflect the daily changes in percentage terms of the SummerHaven Copper Index Total ReturnSM (the “SCI”), less CPER’s expenses. The SCI is designed to reflect the performance of the investment returns from a portfolio of copper futures contracts. The SCI is owned and maintained by SummerHaven Index Management, LLC (“SHIM”), and calculated and published by the NYSE Arca. CPER pays its sponsor, United States Commodity Funds LLC (“USCF”), a limited liability company, a management fee and incurs operating costs. CPER and USCF are located at 1850 Mt. Diablo Boulevard, Suite 640, Walnut Creek, California 94596. The telephone number for both CPER and USCF is 510.522.9600. Currently, USCF employs SummerHaven Investment Management, LLC (“SummerHaven”), a limited liability company, as a commodity trading advisor to CPER. SummerHaven is located at 1266 E. Main Street, Soundview Plaza, Fourth Floor, Stamford, CT 06902. SummerHaven’s telephone number is 203.352.2700. In order for a hypothetical investment in shares to break even over the next 12 months, assuming a selling price of $20.55 (the net asset value as of September 30, 2022), the investment would have to generate a 0.832% or $0.171 return, rounded to $0.17.

CPER is an exchange traded fund. This means that most investors who decide to buy or sell shares of CPER place their trade orders through their brokers and may incur customary brokerage commissions and charges. Shares trade on the NYSE Arca under the ticker symbol “CPER” and are bought and sold throughout the trading day at bid and ask prices like other publicly traded securities.

Shares trade on the NYSE Arca after they are initially purchased by “Authorized Participants,” institutional firms that purchase and redeem shares in blocks of 50,000 shares called “baskets” through CPER’s marketing agent, ALPS Distributors, Inc. (the “Marketing Agent”). The price of a basket is equal to the NAV of 50,000 shares on the day that the order to purchase the basket is accepted by the Marketing Agent. The NAV per share is calculated by taking the current market value of CPER’s total assets (after close of NYSE Arca) subtracting any liabilities and dividing that total by the total number of outstanding shares. The offering of CPER’s shares is a “best efforts” offering, which means that neither the Marketing Agent nor any Authorized Participant is required to purchase a specific number or dollar amount of shares. USCF pays the Marketing Agent a marketing fee consisting of a fixed annual amount plus an incentive fee based on the amount of shares sold. Authorized Participants will not receive from CPER, USCF or any of their affiliates, any fee or other compensation in connection with the sale of shares. Aggregate compensation paid to the Marketing Agent and any affiliate of USCF for distribution-related services in connection with this offering of shares will not exceed ten percent (10%) of the gross proceeds of the offering.

Investors who buy or sell shares during the day from their broker may do so at a premium or discount relative to the market value of the underlying copper futures contracts in which CPER invests due to supply and demand forces at work in the secondary trading market for shares that are closely related to, but not identical to, the same forces influencing the SCI that serves as CPER’s investment benchmark. INVESTING IN CPER INVOLVES RISKS SIMILAR TO THOSE INVOLVED WITH AN INVESTMENT DIRECTLY IN THE COPPER MARKET, BUT IT IS NOT A PROXY FOR TRADING DIRECTLY IN THE COPPER MARKET. Investing in CPER also involves the correlation risk described below and other significant risks. You should consider carefully the risks described below before making an investment decision. See “Risk Factors Involved with an Investment in CPER” beginning on page 8.

The offering of CPER’s shares is registered with the Securities and Exchange Commission (“SEC”) in accordance with the Securities Act of 1933 (the “1933 Act”). The offering is intended to be a continuous offering and is not expected to terminate until all of the registered shares have been sold or three years from the date of the original offering, whichever is earlier, unless extended as permitted under the rules under the 1933 Act, although the offering may be temporarily suspended if and when no suitable investments for CPER are available or practicable. CPER is not a mutual fund registered under the Investment Company Act of 1940 (“1940 Act”) and is not subject to regulation under the 1940 Act.

NEITHER THE SEC NOR ANY STATE SECURITIES COMMISSION HAS APPROVED OR DISAPPROVED OF THE SECURITIES OFFERED IN THIS PROSPECTUS, OR DETERMINED IF THIS PROSPECTUS IS TRUTHFUL OR COMPLETE. ANY REPRESENTATION TO THE CONTRARY IS A CRIMINAL OFFENSE.

CPER is a commodity pool and USCF is a commodity pool operator (“CPO”) subject to regulation by the Commodity Futures Trading Commission (“CFTC”) and the National Futures Association (“NFA”) under the Commodity Exchange Act (“CEA”).

THE COMMODITY FUTURES TRADING COMMISSION HAS NOT PASSED UPON THE MERITS OF PARTICIPATING IN THIS POOL NOR HAS THE COMMISSION PASSED ON THE ADEQUACY OR ACCURACY OF THIS DISCLOSURE DOCUMENT.

The date of this prospectus is [●], 2022.

COMMODITY FUTURES TRADING COMMISSION

RISK DISCLOSURE STATEMENT

YOU SHOULD CAREFULLY CONSIDER WHETHER YOUR FINANCIAL CONDITION PERMITS YOU TO PARTICIPATE IN A COMMODITY POOL. IN SO DOING, YOU SHOULD BE AWARE THAT COMMODITY INTEREST TRADING CAN QUICKLY LEAD TO LARGE LOSSES AS WELL AS GAINS. SUCH TRADING LOSSES CAN SHARPLY REDUCE THE NET ASSET VALUE OF THE POOL AND CONSEQUENTLY THE VALUE OF YOUR INTEREST IN THE POOL. IN ADDITION, RESTRICTIONS ON REDEMPTIONS MAY AFFECT YOUR ABILITY TO WITHDRAW YOUR PARTICIPATION IN THE POOL.

FURTHER, COMMODITY POOLS MAY BE SUBJECT TO SUBSTANTIAL CHARGES FOR MANAGEMENT, AND ADVISORY AND BROKERAGE FEES. IT MAY BE NECESSARY FOR THOSE POOLS THAT ARE SUBJECT TO THESE CHARGES TO MAKE SUBSTANTIAL TRADING PROFITS TO AVOID DEPLETION OR EXHAUSTION OF THEIR ASSETS. THIS DISCLOSURE DOCUMENT CONTAINS A COMPLETE DESCRIPTION OF EACH EXPENSE TO BE CHARGED THIS POOL AT PAGE 7 AND A STATEMENT OF THE PERCENTAGE RETURN NECESSARY TO BREAK EVEN, THAT IS, TO RECOVER THE AMOUNT OF YOUR INITIAL INVESTMENT, AT PAGE 45.

THIS BRIEF STATEMENT CANNOT DISCLOSE ALL THE RISKS AND OTHER FACTORS NECESSARY TO EVALUATE YOUR PARTICIPATION IN THIS COMMODITY POOL. THEREFORE, BEFORE YOU DECIDE TO PARTICIPATE IN THIS COMMODITY POOL, YOU SHOULD CAREFULLY STUDY THIS DISCLOSURE DOCUMENT, INCLUDING A DESCRIPTION OF THE PRINCIPAL RISK FACTORS OF THIS INVESTMENT, AT PAGE 8.

YOU SHOULD ALSO BE AWARE THAT THIS COMMODITY POOL MAY TRADE FOREIGN FUTURES OR OPTIONS CONTRACTS. TRANSACTIONS ON MARKETS LOCATED OUTSIDE THE UNITED STATES, INCLUDING MARKETS FORMALLY LINKED TO A UNITED STATES MARKET, MAY BE SUBJECT TO REGULATIONS WHICH OFFER DIFFERENT OR DIMINISHED PROTECTION TO THE POOL AND ITS PARTICIPANTS. FURTHER, UNITED STATES REGULATORY AUTHORITIES MAY BE UNABLE TO COMPEL THE ENFORCEMENT OF THE RULES OF REGULATORY AUTHORITIES OR MARKETS IN NON-UNITED STATES JURISDICTIONS WHERE TRANSACTIONS FOR THE POOL MAY BE EFFECTED.

SWAPS TRANSACTIONS, LIKE OTHER FINANCIAL TRANSACTIONS, INVOLVE A VARIETY OF SIGNIFICANT RISKS. THE SPECIFIC RISKS PRESENTED BY A PARTICULAR SWAP TRANSACTION NECESSARILY DEPEND UPON THE TERMS OF THE TRANSACTION AND YOUR CIRCUMSTANCES. IN GENERAL, HOWEVER, ALL SWAPS TRANSACTIONS INVOLVE SOME COMBINATION OF MARKET RISK, CREDIT RISK, COUNTERPARTY CREDIT RISK, FUNDING RISK, LIQUIDITY RISK, AND OPERATIONAL RISK.

HIGHLY CUSTOMIZED SWAPS TRANSACTIONS IN PARTICULAR MAY INCREASE LIQUIDITY RISK, WHICH MAY RESULT IN A SUSPENSION OF REDEMPTIONS. HIGHLY LEVERAGED TRANSACTIONS MAY EXPERIENCE SUBSTANTIAL GAINS OR LOSSES IN VALUE AS A RESULT OF RELATIVELY SMALL CHANGES IN THE VALUE OR LEVEL OF AN UNDERLYING OR RELATED MARKET FACTOR.

IN EVALUATING THE RISKS AND CONTRACTUAL OBLIGATIONS ASSOCIATED WITH A PARTICULAR SWAP TRANSACTION, IT IS IMPORTANT TO CONSIDER THAT A SWAP TRANSACTION MAY BE MODIFIED OR TERMINATED ONLY BY MUTUAL CONSENT OF THE ORIGINAL PARTIES AND SUBJECT TO AGREEMENT ON INDIVIDUALLY NEGOTIATED TERMS. THEREFORE, IT MAY NOT BE POSSIBLE FOR THE COMMODITY POOL OPERATOR TO MODIFY, TERMINATE, OR OFFSET THE POOL’S OBLIGATIONS OR THE POOL’S EXPOSURE TO THE RISKS ASSOCIATED WITH A TRANSACTION PRIOR TO ITS SCHEDULED TERMINATION DATE.

TABLE OF CONTENTS

PROSPECTUS SUMMARY

This is only a summary of the prospectus and, while it contains material information about CPER and its shares, it does not contain or summarize all of the information about CPER and the shares contained in this prospectus that is material and/or which may be important to you. You should read this entire prospectus, including “Risk Factors Involved with an Investment in CPER” beginning on page 8, before making an investment decision about the shares. For a glossary of defined terms, see Appendix A.

The Trust and CPER

The United States Commodity Index Funds Trust (the “Trust”) is a Delaware statutory trust formed on December 21, 2009. The Trust is a series trust formed pursuant to the Delaware Statutory Trust Act and is organized into three separate series (each series, a “Fund” and collectively, the “Funds”). The United States Copper Index Fund (“CPER”), formed on November 26, 2010, is a series of the Trust and is a commodity pool that continuously issues common shares of beneficial interest that may be purchased and sold on the NYSE Arca stock exchange (“NYSE Arca”). The Trust and CPER operate pursuant to the Trust’s Fourth Amended and Restated Declaration of Trust and Trust Agreement (the “Trust Agreement”), dated as of December 15, 2017. Wilmington Trust Company, a Delaware trust company, is the Delaware trustee of the Trust. The Trust and CPER are managed and controlled by United States Commodity Funds LLC (“USCF”), a limited liability company. USCF is registered as a CPO with the CFTC and is a member of the NFA.

Other series of the Trust include the United States Commodity Index Fund (“USCI”).

CPER’s Investment Objective and Strategy

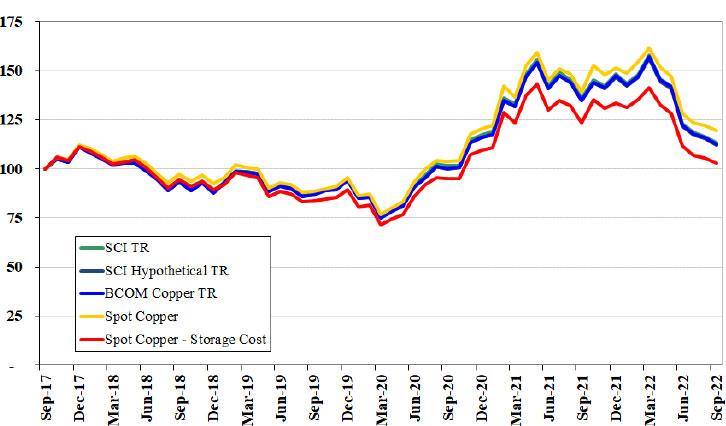

The investment objective of CPER is for the daily changes in percentage terms of its shares’ per share net asset value (“NAV”) to reflect the daily changes in percentage terms of the SummerHaven Copper Index Total ReturnSM (the “SCI”), less CPER’s expenses.

| What is the “SummerHaven Copper Index Total Return”? |

| |

| The SCI is designed to reflect the performance of the investment returns from a portfolio of copper futures contracts on the Commodity Exchange, Inc. exchange (“COMEX”). The SCI is owned and maintained by SummerHaven Index Management, LLC (“SHIM”) and is calculated and published by the NYSE Arca. The SCI is comprised of either one or three Eligible Copper Futures Contracts that are selected on a monthly basis based on quantitative formulas relating to the prices of the Eligible Copper Futures Contracts developed by SHIM. The Eligible Copper Futures Contracts that at any given time make up the SCI are referred to herein as “Benchmark Component Copper Futures Contracts.” |

| |

| As discussed further below, beginning with the first commodity selection process that occurred after December 31, 2020, the number of Futures Contracts that are Eligible Copper Futures Contracts was reduced and the SCI is comprised of one or three Eligible Copper Futures Contracts. |

| |

CPER seeks to achieve its investment objective by investing primarily in Benchmark Component Copper Futures Contracts. Then, if constrained by regulatory requirements, risk mitigation measures, liquidity requirements, or in view of market conditions, CPER will invest next in other Eligible Copper Futures Contracts based on the same copper as the futures contracts subject to such regulatory constraints or market conditions, and finally, to a lesser extent, in other exchange-traded futures contracts that are economically identical or substantially similar to the Benchmark Component Copper Futures Contracts if one or more other Eligible Copper Futures Contracts is not available. When CPER has invested to the fullest extent possible in exchange-traded futures contracts, CPER may then invest in other contracts and instruments based on the Benchmark Component Copper Futures Contracts, other Eligible Copper Futures Contracts or other items based on copper, such as cash-settled options, forward contracts, cleared swap contracts and swap contracts other than cleared swap contracts. Other exchange-traded futures contracts that are economically identical or substantially similar to the Benchmark Component Copper Futures Contracts and other contracts and instruments based on the Benchmark Component Copper Futures Contracts are collectively referred to as “Other Copper-Related Investments,” and together with Benchmark Component Copper Futures Contracts and other Eligible Copper Futures Contracts, “Copper Interests.”

In addition, USCF believes that market arbitrage opportunities will cause daily changes in CPER’s share price on the NYSE Arca on a percentage basis to closely track daily changes in CPER’s per share NAV on a percentage basis. USCF believes that the net effect of this expected relationship and the expected relationship described above between CPER’s per share NAV and the SCI will be that the daily changes in the price of CPER’s shares on the NYSE Arca on a percentage basis will closely track the daily changes in the SCI on a percentage basis, less CPER’s expenses. While CPER is composed of Benchmark Component Copper Futures Contracts and is therefore a measure of the prices of the corresponding commodities comprising the SCI for future delivery, there is nonetheless expected to be a reasonable degree of correlation between the SCI and the cash or spot prices of the commodities underlying the Benchmark Component Copper Futures Contracts.

Specifically, CPER seeks to achieve its investment objective by investing so that the average daily percentage change in CPER’s NAV for any period of 30 successive valuation days will be within plus/minus ten percent (10%) of the average daily percentage change in the price of the Benchmark Component Copper Futures Contracts over the same period.

Investors should be aware that CPER’s investment objective is not for its NAV or market price of shares to equal, in dollar terms, the spot prices of the commodities underlying the Benchmark Component Copper Futures Contracts or the prices of any particular group of futures contracts. CPER will not seek to achieve its stated investment objective over a period of time greater than one day. This is because natural market forces called contango and backwardation have impacted the total return on an investment in CPER’s shares during the past year relative to a hypothetical direct investment in the various commodities and, in the future, it is likely that the relationship between the market price of CPER’s shares and the changes in the spot prices of the underlying commodities will continue to be so impacted by contango and backwardation. (It is important to note that the disclosure above ignores the potential costs associated with physically owning and storing the commodities, which could be substantial.)

Principal Investment Risks of an Investment in CPER

An investment in CPER includes a degree of risk. Some of the risks you may face are summarized below. A more extensive discussion of these risks appears beginning on page 8.

Investment Risk

Investors may choose to use CPER as a means of investing indirectly in copper. INVESTING IN CPER INVOLVES RISKS SIMILAR TO THOSE INVOLVED WITH AN INVESTMENT DIRECTLY IN THE COPPER MARKET, BUT IT IS NOT A PROXY FOR TRADING DIRECTLY IN THE COPPER MARKET. You should carefully consider the risks described below before making an investment decision. Investing in CPER also involves the correlation risk described below and other significant risks. An investment in CPER involves the following investment risks:

| · | The NAV of CPER’s shares relates directly to the value of investments in Eligible Copper Futures Contracts and other assets held by CPER and fluctuations in the prices of these assets could materially adversely affect an investment in CPER’s shares. Past performance is not necessarily indicative of future results; all or substantially all of an investment in CPER could be lost. |

| · | The demand for commodities, in general, correlates closely with general economic growth rates. |

| · | Other factors that may affect the demand for certain commodities and therefore their price include technological improvements in energy efficiency; seasonal weather patterns, increased competitiveness of alternative metals changes in technology or consumer preferences that alter fuel choices, such as toward alternative, lighter, or more conducive metals and changes in consumer preference. |

| · | Copper prices also vary depending on a number of factors affecting supply and demand, including geopolitical risk associated with wars (such as the current war between Russia and Ukraine), terrorist attacks and tensions between countries. |

| · | The supply of and demand for copper and other commodities may also be impacted by changes in interest rates, inflation, and other local or regional market conditions, as well as by the development of alternative energy sources. |

| · | Price volatility may possibly cause the total loss of your investment. |

| · | Russia’s invasion of Ukraine, and sanctions brought by the United States and other countries against Russia and others, have caused disruptions in many business sectors, resulting in significant market disruptions that have led to increased volatility in the price of certain commodities, and may lead to volatility in CPER’s NAV or share price. |

| · | COVID-19 and other infectious disease outbreaks could negatively affect the valuation and performance of CPER’s investments. |

| · | Historical performance of CPER and the Benchmark Component Copper Futures Contract is not indicative of future performance. |

Correlation Risk

As further described below, an investment in CPER involves the following correlation risks:

| · | An investment in CPER may provide little or no diversification benefits. Thus, in a declining market, CPER may have no gains to offset losses from other investments, and an investor may suffer losses on an investment in CPER while incurring losses with respect to other asset classes. |

| · | The market price at which investors buy or sell shares may be significantly less or more than NAV. |

| · | Daily percentage changes in the price of the Benchmark Component Copper Futures Contract may not correlate with daily percentage changes in the spot price of the corresponding commodity. |

| · | An investment in CPER is not a proxy for investing in the copper markets, and the daily percentage changes in the price of the Benchmark Component Copper Futures Contract, or the NAV of CPER, may not correlate with daily percentage changes in the spot price of copper that underlie the SCI. |

| · | The price relationship between the SCI at any point in time and the Eligible Copper Futures Contracts that will become the Benchmark Component Copper Futures Contracts on the next rebalancing date will vary and may impact both CPER’s total return and the degree to which its total return tracks that of SCI. |

| · | Natural forces in the commodity futures market known as “backwardation” and “contango” may increase CPER’s tracking error and/or negatively impact total return. |

| · | Accountability levels, position limits, and daily price fluctuation limits set by the exchanges have the potential to cause tracking error, by limiting CPER’s investments, including its ability to fully invest in the Benchmark Component Copper Futures Contract, which could cause the price of shares to substantially vary from the price of the Benchmark Component Copper Futures Contract. |

| · | Risk mitigation measures that could be imposed by CPER’s futures commission merchants (“FCMs”) have the potential to cause tracking error by limiting CPER’s investments, including its ability to fully invest in the Benchmark Component Copper Futures Contract and other Futures Contracts, which could cause the price of CPER’s shares to substantially vary from the price of the Benchmark Component Copper Futures Contract. |

To the extent that investors use CPER as a means of indirectly investing in copper, there is the risk that the daily changes in the price of CPER’s shares on the NYSE Arca on a percentage basis will not closely track the daily changes in the spot prices of the commodities comprising the SCI on a percentage basis. This could happen if the price of shares traded on the NYSE Arca does not correlate closely with the value of CPER’s NAV; the changes in CPER’s NAV do not correlate closely with the changes in the price of the Benchmark Component Copper Futures Contracts; or the changes in the price of the Benchmark Component Copper Futures Contracts do not closely correlate with the changes in the cash or spot price of copper. This is a risk because if these correlations do not exist, then investors may not be able to use CPER as a cost-effective way to indirectly invest in copper or as a hedge against the risk of loss in copper-related transactions.

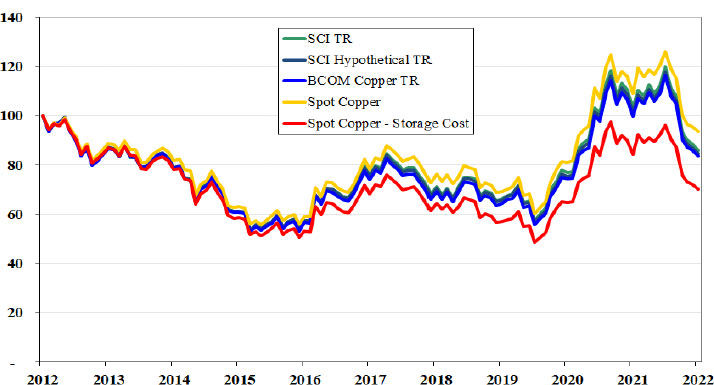

The design of the SCI is such that every month it is made up of different Benchmark Component Copper Futures Contracts and CPER’s investment must be rebalanced on an ongoing basis to reflect the changing composition of the SCI. In cases in which the near month contracts to expire trade at a higher price than next month contracts to expire, a situation referred to as “backwardation,” then absent the impact of the overall movement in commodity prices, the value of the SCI would tend to rise as it approaches expiration. As a result, CPER may benefit because it would be selling more expensive contracts and buying less expensive ones on an ongoing basis. Conversely, in the event of a commodity futures market where near month contracts trade at a lower price than next month contracts, a situation referred to as “contango,” then absent the impact of the overall movement in commodity prices, the value of the SCI would tend to decline as it approaches expiration. As a result, CPER’s total return may be lower than might otherwise be the case because it would be selling less expensive contracts and buying more expensive ones. The impact of backwardation and contango may cause the total return of CPER to vary significantly from the total return of other price references, such as the spot price of the commodities comprising the SCI. In the event of a prolonged period of contango, and absent the impact of rising or falling commodity prices, this could have a significant negative impact on CPER’s NAV and total return.

Tax Risk

The Trust is organized and operated as a Delaware statutory trust in accordance with the provisions of the Trust Agreement and applicable state law, but CPER is taxed as a partnership for U.S. federal income tax purposes, and therefore, has a more complex tax treatment than conventional mutual funds. An investment in CPER involves the following tax risks:

| · | An investor’s tax liability may exceed the amount of distributions, if any, on its shares. |

| · | An investor’s allocable share of taxable income or loss may differ from its economic income or loss on its shares. |

| · | Items of income, gain, deduction, loss and credit with respect to shares could be reallocated for U.S. federal income tax purposes, and CPER could be liable for U.S. federal income tax, if the U.S. Internal Revenue Service (“IRS”) does not accept the assumptions and conventions applied by CPER in allocating those items, with potential adverse consequences for an investor. |

| · | CPER could be treated as a corporation for U.S. federal income tax purposes, which may substantially reduce the value of the shares. |

| · | The Trust is organized as a Delaware statutory trust in accordance with the provisions of the Trust Agreement and applicable state law, but CPER is taxed as a partnership for U.S. federal income tax purposes, and therefore, CPER has a more complex tax treatment than traditional mutual funds. |

| · | If CPER is required to withhold tax with respect to any non-U.S. shareholders, the cost of such withholding may be borne by all shareholders. |

| · | The impact of changes in U.S federal income tax law and other proposed or future tax legislation or administrative guidance on CPER is uncertain. |

Over-the-Counter (“OTC”) Contract Risk

CPER may also invest in Other Copper-Related Investments, many of which are negotiated or “OTC” contracts that are not as liquid as Eligible Copper Futures Contracts and expose CPER to credit risk that its counterparty may not be able to satisfy its obligations to CPER. An investment in CPER involves the following OTC contract risks:

| · | CPER will be subject to credit risk with respect to counterparties to OTC contracts entered into by the Trust on behalf of CPER or held by special purpose or structured vehicles. |

| · | Valuing OTC derivatives may be less certain than actively traded financial instruments. |

Other Risks

CPER pays fees and expenses that are incurred regardless of whether CPER is profitable.

Unlike mutual funds, commodity pools or other investment pools that manage their investments in an attempt to realize income and gains and distribute such income and gains to their investors, CPER generally does not distribute cash to shareholders. You should not invest in CPER if you will need cash distributions from CPER to pay taxes on your share of income and gains of CPER, if any, or for any other reason.

You will have no rights to participate in the management of CPER and will have to rely on the duties and judgment of USCF to manage CPER.

CPER is subject to actual and potential inherent conflicts involving USCF, various commodity futures brokers and “Authorized Participants,” the institutional firms that directly purchase and redeem shares in baskets of 50,000 shares. USCF’s officers, directors and employees do not devote their time exclusively to CPER. USCF’s personnel are directors, officers or employees of other entities that may compete with CPER for their services, including other commodity pools (funds) that USCF manages. USCF could have a conflict between its responsibilities to CPER and to those other entities. As a result of these and other relationships, parties involved with CPER have a financial incentive to act in a manner other than in the best interest of CPER and the shareholders.

In addition, an investment in CPER involves the following other risks:

| · | CPER is not leveraged, but it could become leveraged if it had insufficient assets to completely meet its margin or collateral requirements relating to its investments. |

| · | CPER may temporarily limit the offering of Creation Baskets. |

| · | CPER pays fees and expenses that are incurred regardless of whether CPER is profitable. |

| · | You will have no rights to participate in the management of CPER and will have to rely on the duties and judgment of USCF to manage CPER. |

| · | Certain of CPER’s investments could be illiquid, which could cause large losses to investors at any time or from time to time. |

| · | CPER is not actively managed and its investment objective is for the daily changes in percentage terms of its shares’ per share NAV for any period of 30 successive valuation days to be within plus/minus ten percent (10%) of the average daily percentage change in the price of the Benchmark Component Copper Futures Contracts over the same period. |

| · | CPER may not meet the listing standards of NYSE Arca, which would adversely impact an investor’s ability to sell shares. |

| · | The NYSE Arca may halt trading in CPER’s shares, which would adversely impact an investor’s ability to sell shares. |

| · | The liquidity of CPER’s shares may also be affected by the withdrawal from participation of Authorized Participants, which could adversely affect the market price of the shares. |

| · | Shareholders that are not Authorized Participants may only purchase or sell their shares in secondary trading markets, and the conditions associated with trading in secondary markets may adversely affect investors’ investment in the shares. |

| · | The lack of an active trading market for CPER shares may result in losses on an investor’s investment in CPER at the time the investor sells the shares. |

| · | SummerHaven is leanly staffed and relies heavily on key personnel to manage advisory activities. |

| · | USCF’s LLC Agreement provides limited authority to the Non-Management Directors, and any Director of USCF may be removed by USCF’s parent company, which is wholly owned by The Marygold Companies, Inc., formerly Concierge Technologies, Inc., a controlled public company where the majority of shares are owned by Nicholas D. Gerber along with certain of his other family members and certain other shareholders. |

| · | There is a risk that CPER will not earn trading gains sufficient to compensate for the fees and expenses that it must pay and as such CPER may not earn any profit. |

| · | CPER is subject to extensive regulatory reporting and compliance. |

| · | Regulatory changes or actions, including the implementation of new legislation, is impossible to predict but may significantly and adversely affect CPER. |

| · | The Trust is not a registered investment company, so shareholders do not have the protections of the 1940 Act. |

| · | Trading in international markets could expose CPER to credit and regulatory risk. |

| · | CPER and USCF may have conflicts of interest, which may permit them to favor their own interests to the detriment of shareholders. |

| · | CPER, USCF and SummerHaven may have conflicts of interest, which may cause them to favor their own interests to the detriment of shareholders. |

| · | Shareholders have only very limited voting rights and have the power to replace USCF only under specific circumstances. Shareholders do not participate in the management of CPER and do not control USCF, so they do not have any influence over basic matters that affect CPER. |

| · | CPER could terminate at any time and cause the liquidation and potential loss of an investor’s investment and could upset the overall maturity and timing of an investor’s investment portfolio. |

| · | CPER does not expect to make cash distributions. |

| · | An unanticipated number of Redemption Basket requests during a short period of time could have an adverse effect on CPER’s NAV. |

| · | The suspension in the ability of Authorized Participants to purchase Creation Baskets could cause CPER’s NAV to differ materially from its trading price. |

| · | CPER may determine that, to allow it to reinvest the proceeds from sales of its Creation Baskets in currently permitted assets in a manner that meets its investment objective, it may limit its offers of Creation Baskets. |

| · | In a rising rate environment, CPER may not be able to fully invest at prevailing rates until any current investments in Treasury Bills mature in order to avoid selling those investments at a loss. |

| · | CPER may lose money by investing in government money market funds. |

| · | The failure or bankruptcy of a clearing broker or CPER’s Custodian could result in a substantial loss of CPER’s assets and could impair CPER in its ability to execute trades. |

| · | The failure or bankruptcy of CPER’s Custodian could result in a substantial loss of CPER’s assets. |

| · | The liability of SummerHaven is limited, and the value of the shares may be adversely affected if USCF and CPER are required to indemnify SummerHaven. |

| · | The liability of USCF and the Trustee are limited, and the value of the shares will be adversely affected if CPER is required to indemnify the Trustee or USCF. |

| · | Although the shares of CPER are limited liability investments, certain circumstances such as bankruptcy or indemnification of CPER by a shareholder will increase the shareholder’s liability. |

| · | Investors cannot be assured of the continuation of the agreement between SummerHaven and USCF for use of the SCI, and discontinuance of the SCI may be detrimental to CPER. |

| · | Investors cannot be assured of SummerHaven’s continued services, and discontinuance may be detrimental to CPER. |

| · | CPER is a series of the Trust and, as a result, a court could potentially conclude that the assets and liabilities of CPER are not segregated from those of another series of the Trust, thereby potentially exposing assets in CPER to the liabilities of another series of the Trust. |

| · | The Trust Agreement limits the forum in which claims may be brought against USCF, the Trust, the Trustee or their respective directors and officers. |

| · | USCF and the Trustee are not obligated to prosecute any action, suit or other proceeding in respect of any CPER property. |

| · | Third parties may infringe upon or otherwise violate intellectual property rights or assert that USCF has infringed or otherwise violated their intellectual property rights, which may result in significant costs and diverted attention. |

| · | Due to the increased use of technologies, intentional and unintentional cyber-attacks pose operational and information security risks. |

| · | CPER’s investment returns could be negatively affected by climate change and greenhouse gas restrictions. |

| · | USCF is the subject of class action, derivative, and other litigation. In light of the inherent uncertainties involved in litigation matters, an adverse outcome in this litigation could materially adversely affect USCF’s financial condition. |

CPER’s Fees and Expenses

This table describes the fees and expenses that you may pay if you buy and hold shares of CPER. You should note that you may pay brokerage commissions on purchases and sales of CPER’s shares, which are not reflected in the table. Authorized Participants will pay applicable creation and redemption fees. See “Creation and Redemption of Shares—Creation and Redemption Transaction Fee,” page 74.

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment)(1)

| Management Fees(2) | | | 0.65 | % |

| Distribution Fees | | | NONE | |

| Other Fund Expenses(1) | | | 0.23 | % |

| Total Annual Fund Operating Expenses | | | 0.88 | % |

| (1) | Based on amounts for the nine months ended September 30, 2022. The individual expense amounts in dollar terms are shown in the table below. As used in this table, (i) Professional Expenses include expenses for legal, audit, tax accounting and printing; and (ii) Independent Director and Officer Expenses include amounts paid to independent directors and for officers’ liability insurance. |

| Management Fees | | $ | 976,774 | |

| Brokerage Commissions | | $ | 41,446 | |

| Professional Expenses | | $ | 401,201 | |

| License Fees | | $ | 2,273 | |

| Independent Director and Officer Expenses | | $ | 58,708 | |

| Registration Fees | | $ | 24,092 | |

| | | | | |

These amounts are based on CPER’s average total net assets, which are the sum of daily total net assets of CPER divided by the number of calendar days in the year. For the nine months ended September 30, 2022, CPER’s average total net assets were $200,914,255.

| (2) | CPER is contractually obligated to pay USCF a management fee based on average daily net assets and paid monthly of 0.65% per annum on its average total net assets. |

RISK FACTORS INVOLVED WITH AN INVESTMENT IN CPER

You should consider carefully the risks described below before making an investment decision. You should also refer to the other information included in this prospectus, as well as information found in our periodic reports, which include the Trust’s and CPER’s financial statements and the related notes, that are incorporated by reference. See “Incorporation By Reference of Certain Information,” page 81.

CPER’s investment objective is for the daily changes in percentage terms of its shares’ per share NAV to reflect the daily changes in percentage terms of the SCI, less CPER’s expenses. CPER seeks to achieve its investment objective by investing so that the average daily percentage change in CPER’s NAV for any period of 30 successive valuation days will be within plus/minus ten percent (10%) of the average daily percentage change in the price of the Benchmark Component Copper Futures Contract over the same period. CPER’s investment strategy is designed to provide investors with a cost-effective way to invest indirectly in copper and to hedge against movements in the spot price of copper.

An investment in CPER involves investment risk similar to a direct investment in Eligible Copper Futures Contracts and Other Copper-Related Investments, but it is not a proxy for investing in copper market. Investing in CPER also involves correlation risk, or the risk that investors purchasing shares to hedge against movements in the price of copper will have an efficient hedge only if the price they pay for their shares closely correlates with the price of the copper. In addition to investment risk and correlation risk, an investment in CPER involves tax risks, OTC risks, and other risks.

Investment Risk

The NAV of CPER’s shares relates directly to the value of its assets invested in accordance with the SCI and other assets held by CPER and fluctuations in the prices of these assets could materially adversely affect an investment in CPER’s shares. Past performance is not necessarily indicative of future results; all or substantially all of an investment in CPER could be lost.

The net assets of CPER consist primarily of investments in Eligible Copper Futures Contracts and, to a lesser extent, in Other Copper-Related Investments. The NAV of CPER’s shares relates directly to the value of these assets (less liabilities, including accrued but unpaid expenses), which in turn relates to the market price of the commodities which comprise the SCI.

Economic conditions impacting copper. The demand for commodities, in general, correlates closely with general economic growth rates. The occurrence of recessions or other periods of low or negative economic growth will typically have a direct adverse impact on commodity demand and therefore, may have an adverse impact on commodity prices. Other factors that affect general economic conditions in the world or in a major region, such as changes in population growth rates, periods of civil unrest, military conflicts, war (such as the current war between Russia and Ukraine), pandemics (e.g. COVID-19), government austerity programs, or currency exchange rate fluctuations, can also impact the demand for commodities. Sovereign debt downgrades, defaults, inability to access debt markets due to credit or legal constraints, liquidity crises, the breakup or restructuring of fiscal, monetary, or political systems such as the European Union, and other events or conditions (e.g. pandemics such as COVID-19) that impair the functioning of financial markets and institutions also may adversely impact the demand for commodities.

Other copper demand-related factors. Other factors that may affect the demand for certain commodities and therefore their price include technological improvements in energy efficiency, seasonal weather patterns, increased competitiveness of alternative metals changes in technology or consumer preferences that alter fuel choices, such as toward alternative, lighter, or more conducive metals and changes in personal income levels.

Other copper supply-related factors. Copper prices also vary depending on a number of factors affecting supply, including geopolitical risk associated with wars (such as the current war between Russia and Ukraine), terrorist attacks and tensions between countries, including sanctions imposed as a result of the foregoing that can adversely affect commodity trade flows by limiting or disrupting trade between countries or regions. For example, increased supply from the development of alloys and technologies for efficient productions tends to reduce prices in such commodity to the extent such supply increases are not offset by commensurate growth in demand. Similarly, increases in industry manufacturing capacity may impact the supply of a particular metal. World supply levels can also be affected by factors that reduce available supplies, such as embargoes, the occurrence of geopolitical risk associated with wars, terrorist attacks and tensions between countries, including sanctions imposed as a result of the foregoing that can adversely affect commodity trade flows by limiting or disrupting trade between countries or regions, natural disasters, disruptions in competitors’ operations, or unexpected unavailability of distribution channels that may disrupt supplies. Technological change can also alter the relative costs for companies to produce, and process and distribute a commodity, which in turn, may affect the supply of and demand of such commodity.

Other factors impacting the copper market. The supply of and demand for copper and other commodities may also be impacted by changes in interest rates, inflation, and other local or regional market conditions, as well as by the development of alternative energy sources.

Price volatility may possibly cause the total loss of your investment.

Futures contracts have a high degree of price variability and are subject to occasional rapid and substantial changes. Consequently, you could lose all or substantially all of your investment in CPER.

Significant market volatility has recently occurred in the commodities markets. Such volatility is attributable in part to the COVID-19 pandemic, related supply chain disruptions, war, including the war between Russia and Ukraine, and continuing disputes among oil-producing countries. These and other events could cause continuing or increased volatility in the future, which may affect the value, pricing and liquidity of some investments or other assets, including those held by or invested in by CPER and the impact of which could limit CPER’s ability to have a substantial portion of its assets invested in the Benchmark Component Copper Futures Contracts. In such a circumstance, CPER could, if it determined it appropriate to do so in light of market conditions and regulatory requirements, invest in other Futures Contracts and/or Other Copper-Related Investments.

Russia’s invasion of Ukraine, and sanctions brought by the United States and other countries against Russia and others, have caused disruptions in many business sectors, resulting in significant market disruptions that have led to increased volatility in the price of certain commodities, and may lead to volatility in CPER’s NAV or share price.

On February 24, 2022, Russia launched a large-scale invasion of Ukraine. The extent and duration of the military action, and resulting sanctions, and future market or supply disruptions in the region, are impossible to predict, but could be significant and may have a severe adverse effect on the region.

The United States and other countries and certain international organizations have imposed broad-ranging economic sanctions on Russia and certain Russian individuals, banking entities and corporations as a response to Russia’s invasion of Ukraine, and additional sanctions may be imposed in the future. Such sanctions (and any future sanctions) will adversely impact the economies of Russia and Ukraine, and certain sectors of each country’s economy may be particularly affected, including but not limited to, financials, energy, metals and mining, engineering and defense and defense-related materials sectors. Among other things, the extent and duration of the military action, the responses of countries and political bodies to Russia’s actions, including sanctions, future market or supply disruptions, and Ukraine’s military response and the potential for wider conflict may increase financial market volatility generally, have severe adverse effects on regional and global economic markets, and cause volatility in the markets for commodities including the price of commodity futures, and the NAV or share price of CPER.

A resolution to the war in Ukraine also could impact the markets for certain commodities, and may have collateral impacts, including increased volatility, and cause disruptions to availability of certain commodities, commodity and futures prices and the supply chain globally. The longer-term impact on commodities and futures prices, including the spot price of copper and the price of the Benchmark Component Copper Futures Contract, is difficult to predict and depends on a number of factors that may have a negative impact on CPER in the future.

COVID-19 and other infectious disease outbreaks could negatively affect the valuation and performance of CPER’s investments.

An outbreak of infectious respiratory illness caused by a novel coronavirus known as COVID-19 was first detected in China in December 2019 and spread globally. In March 2020, the World Health Organization declared the COVID-19 outbreak a pandemic. COVID-19 has resulted in numerous deaths, travel restrictions, closed international borders, enhanced health screenings at ports of entry and elsewhere, disruption of and delays in healthcare service preparation and delivery, prolonged quarantines and the imposition of both local and more widespread “work from home” measures, cancellations, loss of employment, supply chain disruptions, and lower consumer and institutional demand for goods and services, as well as general concern and uncertainty. The ongoing spread of COVID-19 has had, and may continue to have, a material adverse impact on local economies in the affected jurisdictions and also on the global economy, as cross border commercial activity and market sentiment are impacted by the outbreak and government and other measures seeking to contain its spread. The impact of COVID-19, and other infectious disease outbreaks that may arise in the future, could adversely affect individual issuers and capital markets in ways that cannot necessarily be foreseen. In addition, actions taken by government and quasi-governmental authorities and regulators throughout the world in response to the COVID-19 outbreak, including significant fiscal and monetary policy changes, may affect the value, volatility, pricing and liquidity of some investments or other assets, including those held by or invested in by CPER. Public health crises caused by the COVID-19 outbreak may exacerbate other pre-existing political, social and economic risks in certain countries or globally. The duration of the COVID-19 outbreak and its ultimate impact on CPER and, on the global economy, cannot be determined with certainty.

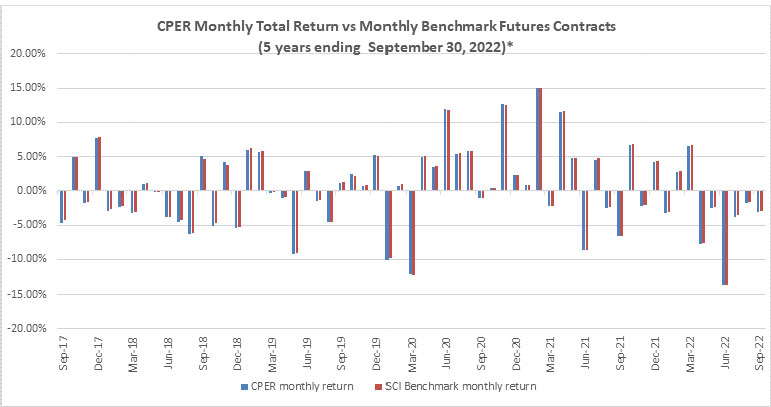

Historical performance of CPER and the Benchmark Component Copper Futures Contract is not indicative of future performance.

Past performance of CPER or the Benchmark Component Copper Futures Contract is not necessarily indicative of future results. Therefore, past performance of CPER or the Benchmark Component Copper Futures Contract should not be relied upon in deciding whether to buy shares of CPER.

Correlation Risk

An investment in CPER may provide little or no diversification benefits. Thus, in a declining market, CPER may have no gains to offset losses from other investments, and an investor may suffer losses on an investment in CPER while incurring losses with respect to other asset classes.

Investors purchasing shares to hedge against movements in the price of copper will have an efficient hedge only if the return from their shares closely correlates with the return from the SCI, which in turn, correlates with the price of the copper that comprises the SCI. Investing in CPER’s shares for hedging purposes includes the following risks:

| · | The market price at which the investor buys or sells shares may be significantly less or more than NAV. |

| · | Daily percentage changes in NAV may not closely correlate with daily percentage changes in the price of the SCI. |

| · | Daily percentage changes in the price of the Benchmark Component Copper Futures Contract may not closely correlate with daily percentage changes in the price of copper that comprises the SCI. |

Historically, Eligible Copper Futures Contracts and Other Copper-Related Investments have generally been non-correlated to the performance of other asset classes such as stocks and bonds. Non-correlation means that there is a low statistically valid relationship between the performance of futures and other commodity interest transactions, on the one hand, and stocks or bonds, on the other hand.

However, there can be no assurance that such non-correlation will continue during future periods. If, contrary to historic patterns, CPER’s performance were to move in the same general direction as the financial markets, investors will obtain little or no diversification benefits from an investment in CPER’s shares. In such a case, CPER may have no gains to offset losses from other investments, and investors may suffer losses on their investment in CPER at the same time they incur losses with respect to other investments.

Variables such as drought, floods, weather, military conflicts, pandemics (such as COVID-19), embargoes, tariffs and other political events may have a larger impact on commodity prices and commodity-linked instruments, including Eligible Copper Futures Contracts and Other Copper-Related Investments, than on traditional securities. These additional variables may create additional investment risks that subject CPER’s investments to greater volatility than investments in traditional securities.

Non-correlation should not be confused with negative correlation, where the performance of two asset classes would be opposite of each other. There is no historical evidence that the spot price of a commodity and prices of other financial assets, such as stocks and bonds, are negatively correlated. In the absence of negative correlation, CPER cannot be expected to be automatically profitable during unfavorable periods for the stock market, or vice versa.

The market price at which investors buy or sell shares may be significantly less or more than NAV.

CPER’s NAV per share will change throughout the day as fluctuations occur in the market value of CPER’s portfolio investments. The public trading price at which an investor buys or sells shares during the day from their broker may be different from the NAV of the shares, which is also the price shares can be redeemed with CPER by Authorized Participants in Redemption Baskets. Generally, price differences may relate to supply and demand forces at work in the secondary trading market for shares that are closely related to, but not identical to, the same forces influencing the prices of the Benchmark Component Copper Futures Contracts and the SCI at any point in time. USCF expects that exploitation of certain arbitrage opportunities by Authorized Participants and their clients will tend to cause the public trading price to track NAV per share closely over time, but there can be no assurance of that. For example, a shortage of CPER’s shares in the market and other factors could cause CPER’s shares to trade at a premium. Investors should be aware that such premiums can be transitory. To the extent an investor purchases shares that include a premium (e.g., because of a shortage of shares in the market due to the inability of Authorized Participants to purchase additional shares from CPER that could be resold into the market) and the cause of the premium no longer exists causing the premium to disappear (e.g., because more shares are available for purchase from CPER by Authorized Participants that could be resold into the market) such investor’s return on its investment would be adversely impacted due to the loss of the premium.

The NAV of CPER’s shares may also be influenced by non-concurrent trading hours between the NYSE Arca and the COMEX where the Benchmark Component Copper Futures Contract is traded.

Daily percentage changes in the price of the Benchmark Component Copper Futures Contract may not correlate with daily percentage changes in the spot price of the corresponding commodity.

The correlation between changes in prices of a Benchmark Component Copper Futures Contract and the spot price of the corresponding commodity may at times be only approximate. The degree of imperfection of correlation depends upon circumstances such as variations in the speculative commodities market, supply of and demand for Eligible Copper Futures Contracts (including the Benchmark Component Copper Futures Contracts) and Other Copper-Related Investments, and technical influences in futures trading.

In addition, CPER is not able to replicate exactly the changes in the price of the Benchmark Component Copper Futures Contracts and the SCI because the total return generated by CPER is reduced by expenses and transaction costs, including those incurred in connection with CPER’s trading activities, and increased by interest income from CPER’s holdings of Treasuries. Tracking the SCI requires trading of CPER’s portfolio with a view to tracking the SCI over time and is dependent upon the skills of USCF and its trading principals, among other factors.

An investment in CPER is not a proxy for investing in the copper markets, and the daily percentage changes in the price of the Benchmark Component Copper Futures Contract, or the NAV of CPER, may not correlate with daily percentage changes in the spot price of copper that underlie the SCI.

An investment in CPER is not a proxy for investing in the commodities markets. To the extent that investors use CPER as a means of indirectly investing in copper, there is the risk that the daily changes in the price of CPER’s shares on the NYSE Arca, on a percentage basis, will not closely track the daily changes in the spot price of copper on a percentage basis. This could happen if the price of shares traded on the NYSE Arca does not correlate closely with the value of CPER’s NAV; the changes in CPER’s NAV do not correlate closely with the changes in the price of the Benchmark Component Copper Futures Contract; or the changes in the price of the Benchmark Component Copper Futures Contract do not closely correlate with the changes in the cash or spot price of copper. This is a risk because if these correlations do not exist, then investors may not be able to use CPER as a cost-effective way to indirectly invest in copper or as a hedge against movements in the spot price of copper. The degree of correlation among CPER’s share price, the price of the Benchmark Component Copper Futures Contract and the spot price of copper depends upon circumstances such as variations in the speculative copper market, supply of and demand for Futures Contracts (including the Benchmark Component Copper Futures Contracts) and Other Copper-Related Investments, and technical influences on trading futures contracts. Investors who are not experienced in investing in futures contracts or the factors that influence that market or speculative trading in futures markets and may not have the background or ready access to the types of information that investors familiar with these markets may have and, as a result, may be at greater risk of incurring losses from trading in CPER shares than such other investors with such experience and resources.

The price relationship between the SCI at any point in time and the Eligible Copper Futures Contracts that will become the Benchmark Component Copper Futures Contracts on the next rebalancing date will vary and may impact both CPER’s total return and the degree to which its total return tracks that of SCI.

The design of SCI is such that every month it is made up of different Benchmark Component Copper Futures Contracts, and CPER’s investment must be rebalanced on an ongoing basis to reflect the changing composition of the SCI. In the event of a copper futures market where near month contracts to expire trade at a higher price than next month contracts to expire, a situation described as “backwardation” in the futures market, then absent the impact of the overall movement in copper prices, the value of the SCI would tend to rise as it approaches expiration. As a result, CPER may benefit because it would be selling more expensive contracts and buying less expensive ones on an ongoing basis. Conversely, in the event of a copper futures market where near month contracts trade at a lower price than next month contracts, a situation described as “contango” in the futures market, then absent the impact of the overall movement in copper prices, the value of the SCI would tend to decline as it approaches expiration. As a result, CPER’s total return may be lower than might otherwise be the case because it would be selling less expensive contracts and buying more expensive ones. The impact of backwardation and contango may cause the total return of CPER’s per share NAV to vary significantly from the total return of other price references, such as the spot price of the copper comprising the SCI. Moreover, absent the impact of rising or falling copper prices, a prolonged period of contango could have a significant negative impact on CPER’s per share NAV and total return and investors could lose part or all of their investment. See “Additional Information About CPER, its Investment Objective and Investments” for a discussion of the potential effects of contango and backwardation.

Accountability levels, position limits, and daily price fluctuation limits set by the exchanges have the potential to cause tracking error, by limiting CPER’s investments, including its ability to fully invest in the Benchmark Component Copper Futures Contract, which could cause the price of shares to substantially vary from the price of the Benchmark Component Copper Futures Contract.

Designated contract markets, such as the COMEX, have established accountability levels and position limits on the maximum net long or net short futures contracts in commodity interests that any person or group of persons under common trading control (other than as a hedge, which an investment by CPER is not) may hold, own or control. These levels and position limits apply to the futures contracts that CPER invests in to meet its investment objective. In addition to accountability levels and position limits, the COMEX also set daily price fluctuation limits on futures contracts. The daily price fluctuation limit establishes the maximum amount that the price of a futures contract may vary either up or down from the previous day’s settlement price. Once the daily price fluctuation limit has been reached in a particular futures contract, no trades may be made at a price beyond that limit.

On October 15, 2020, the CFTC approved a final rule that amended the existing federal position limits regime set forth in Part 150 of the CFTC’s regulations as well as the framework for exchange-set position limits and exemptions (such final rule, the “Position Limits Rule”). The Position Limits Rule establishes federal position limits for 25 core referenced futures contracts (comprised of agricultural, energy and metals futures contracts), futures and options linked to the core referenced futures contracts, and swaps that are economically equivalent to the core referenced futures contracts.

The Benchmark Component Copper Futures Contract is subject to position limits under the Position Limits Rule, and CPER’s trading does not qualify for an exemption therefrom. Accordingly, the Position Limits Rule could negatively impact the ability of CPER to meet its investment objectives by inhibiting USCF’s ability to effectively invest the proceeds from sales of Creation Baskets of CPER in particular amounts and types of its permitted investments.

These limits may potentially cause a tracking error between the price of CPER’s shares and the Benchmark Component Copper Futures Contract. This may in turn prevent investors from being able to effectively use CPER as a way to hedge against copper-related losses or as a way to indirectly invest in copper.

Risk mitigation measures that could be imposed by CPER’s futures commission merchants (“FCMs”) have the potential to cause tracking error by limiting CPER’s investments, including its ability to fully invest in the Benchmark Component Copper Futures Contract and other Futures Contracts, which could cause the price of CPER’s shares to substantially vary from the price of the Benchmark Component Copper Futures Contract.

CPER’s FCMs have discretion to impose limits on the positions that CPER may hold in the Benchmark Component Copper Futures Contract as well as certain other months. To date, CPER’s FCMs have not imposed any such limits. However, were CPER’s FCMs to impose limits, CPER’s ability to have a substantial portion of its assets invested in the Benchmark Component Copper Futures Contract and other Futures Contracts could be severely limited, which could lead CPER to invest in other Futures Contracts or, potentially, Other Copper-Related Investments. CPER could also have to more frequently rebalance and adjust the types of holdings in its portfolio than is currently the case. This could inhibit CPER from pursuing its investment objective in the same manner that it has historically and currently.

In addition, when offering Creation Baskets for purchase, limitations imposed by exchanges and/or any of CPER’s FCMs could limit CPER’s ability to invest the proceeds of the purchases of Creation Baskets in Benchmark Component Copper Futures Contracts and other Futures Contracts. If this were the case, CPER may invest in other permitted investments, including Other Copper-Related Investments, and may hold larger amounts of Treasuries, cash and cash equivalents, which could impair CPER’s ability to meet its investment objective.

Tax Risk

An investor’s tax liability may exceed the amount of distributions, if any, on its shares.

Cash or property will be distributed at the sole discretion of USCF. USCF has not and does not currently intend to make cash or other distributions with respect to shares. Investors will be required to pay U.S. federal income tax and, in some cases, state, local, or foreign income tax, on their allocable share of CPER’s taxable income, without regard to whether they receive distributions or the amount of any distributions. Therefore, the tax liability of an investor with respect to its shares may exceed the amount of cash or value of property (if any) distributed with respect to such shares.

An investor’s allocable share of taxable income or loss may differ from its economic income or loss on its shares.

Due to the application of the assumptions and conventions applied by CPER in making allocations for tax purposes and other factors, an investor’s allocable share of CPER’s income, gain, deduction, loss, or credit may be different than its economic profit or loss from its shares for a taxable year. This difference could be temporary or permanent and, if permanent, could result in it being taxed on amounts in excess of its economic income.

Items of income, gain, deduction, loss and credit with respect to shares could be reallocated for U.S. federal income tax purposes, and CPER could be liable for U.S. federal income tax, if the IRS does not accept the assumptions and conventions applied by CPER in allocating those items, with potential adverse consequences for an investor.

The U.S. federal income tax rules pertaining to entities treated as partnerships for U.S. federal income tax purposes are complex and their application to large, publicly traded entities, such as CPER, is in many respects uncertain. CPER applies certain assumptions and conventions in an attempt to comply with the intent of the applicable rules and to report taxable income, gains, deductions, losses and credits in a manner that properly reflects shareholders’ economic gains and losses. It is possible that the IRS could successfully challenge the application by CPER of these assumptions and conventions as not fully complying with all aspects of the Internal Revenue Code of 1986, as amended (the “Code”), and applicable Treasury Regulations, which would require CPER to reallocate items of income, gain, deduction, loss or credit in a manner that adversely affects investors. If this occurs, investors may be required to file an amended U.S. federal income tax return and to pay additional taxes, plus deficiency interest.

CPER may be liable for U.S. federal income tax on any “imputed understatement” resulting from an adjustment as a result of an IRS audit. The amount of the imputed understatement generally includes increases in allocations of items of income or gain to any investor and decreases in allocations of items of deduction, loss, or credit to any investor without any offset for corresponding reductions in allocations of items of income or gain to any investor or increases in allocations of items of deduction, loss, or credit to any investor. If CPER is required to pay any U.S. federal income taxes on any imputed understatement, the resulting tax liability would reduce the net assets of CPER and would likely have an adverse impact on the value of the shares. Under certain circumstances, CPER may be eligible to elect to cause the investors to take into account the amount of any imputed understatement, including any associated interest and penalties. The ability of a publicly traded partnership such as CPER to elect this treatment is uncertain. If the election is made, CPER would be required to provide investors who owned beneficial interests in the shares in the year to which the adjusted allocations relate with a statement setting forth their proportionate shares of the adjustment (“Adjusted K-1s”). The investors would be required to take the adjustment into account in the taxable year in which the Adjusted K-1s are issued.

CPER could be treated as a corporation for U.S. federal income tax purposes, which may substantially reduce the value of the shares.

The Trust, on behalf of CPER, has received an opinion of counsel that, under current U.S. federal income tax laws, CPER will be treated as a partnership that is not taxable as a corporation for U.S. federal income tax purposes, provided that (i) at least 90 percent of CPER’s annual gross income will be derived from (a) income and gains from commodities (not held as inventory) or futures, forwards, options, swaps and other notional principal contracts with respect to commodities, and (b) interest income; (ii) the Trust and CPER are organized and operated in accordance with their governing agreements and applicable law; and (iii) neither the Trust nor CPER elects to be taxed as a corporation for U.S. federal income tax purposes. Although USCF anticipates that CPER has satisfied and will continue to satisfy the “qualifying income” requirement for all taxable years, that result cannot be assured. CPER has not requested and will not request any ruling from the IRS with respect to its classification as a partnership taxable as a corporation for U.S. federal income tax purposes. If the IRS were to successfully assert that CPER is taxable as a corporation for U.S. federal income tax purposes in any taxable year, rather than passing through its income, gains, losses, deductions, and credits proportionately to its shareholders, CPER would be subject to U.S. federal income tax imposed at applicable corporate rates on its net income for the year. In addition, although USCF does not currently intend to make distributions with respect to its shares, if CPER were treated as a corporation for U.S. federal income tax purposes, any distributions made with respect to CPER shares would be taxable to shareholders as dividend income to the extent of CPER’s current and accumulated earnings and profits. Taxation of the Trust and CPER as corporations could materially reduce the after-tax return on an investment in shares and could substantially reduce the value of the shares.

The Trust is organized as a Delaware statutory trust in accordance with the provisions of the Trust Agreement and applicable state law, but CPER is taxed as a partnership for U.S. federal income tax purposes, and therefore, CPER has a more complex tax treatment than traditional mutual funds.

The Trust is organized as a Delaware statutory trust in accordance with the provisions of the Trust Agreement and applicable state law, but CPER is taxed as a partnership for U.S. federal income tax purposes. No U.S. federal income tax is paid by CPER on its income. Instead, CPER will furnish shareholders each year with tax information on IRS Schedules K-1, K-2, and/or K-3 (Form 1065) and each U.S. shareholder is required to report on its U.S. federal income tax return its allocable share of the income, gain, loss, deduction, and credit of CPER. This must be reported without regard to the amount (if any) of cash or property the shareholder receives as a distribution from CPER during the taxable year. A shareholder, therefore, may be allocated income or gain by CPER, but receive no cash distribution with which to pay the tax liability resulting from the allocation, or may receive a distribution that is insufficient to pay such liability.

In addition to U.S. federal income taxes, shareholders may be subject to other taxes, such as state and local income taxes, unincorporated business taxes, business franchise taxes and estate, inheritance or intangible taxes that may be imposed by the various jurisdictions in which CPER does business or owns property or where the shareholders reside. Although an analysis of those various taxes is not presented here, each prospective shareholder should consider their potential impact on its investment in CPER. It is each shareholder’s responsibility to file the appropriate U.S. federal, state, local, and foreign tax returns.

If CPER is required to withhold tax with respect to any non-U.S. shareholders, the cost of such withholding may be borne by all shareholders.

Under certain circumstances, CPER may be required to pay withholding tax with respect to allocations to non-U.S. shareholders. Although the Trust Agreement provides that any such withholding will be treated as being distributed to the non-U.S. shareholder, CPER may not be able to cause the economic cost of such withholding to be borne by the non-U.S. shareholder on whose behalf such amounts were withheld since it does not generally expect to make any distributions. Under such circumstances, the economic cost of the withholding may be borne by all shareholders, not just the shareholders on whose behalf such amounts were withheld. This could have a material impact on the value of the shares.

The impact of changes in U.S. federal income tax laws on CPER is uncertain.

In general, legislative or other actions relating to U.S. federal income taxes could have a negative effect on CPER or our investors. The rules dealing with U.S. federal income taxation are constantly under review by persons involved in the legislative process and by the IRS and the U.S. Treasury Department. On August 16, 2022, President Biden signed the Inflation Reduction Act (the “IRA”) into law. At this time, we cannot predict with certainty how the provisions of the IRA or any other proposed or future tax legislation might affect the Trust, CPER, our investors, or CPER’s investments. Investors are urged to consult with their tax advisor with respect to the status of legislative, regulatory or administrative developments and proposals and their potential effect on an investment in our shares.

OTC Contract Risk

CPER will be subject to credit risk with respect to counterparties to OTC contracts entered into by the Trust on behalf of CPER or held by special purpose or structured vehicles.

CPER faces the risk of non-performance by the counterparties to the OTC contracts. Unlike in futures contracts, the counterparty to these contracts is generally a single bank or other financial institution, rather than a clearing organization backed by a group of financial institutions. As a result, there will be greater counterparty credit risk in these transactions. A counterparty may not be able to meet its obligations to CPER, in which case CPER could suffer significant losses on these contracts.

If a counterparty becomes bankrupt or otherwise fails to perform its obligations due to financial difficulties, CPER may experience significant delays in obtaining any recovery in a bankruptcy or other reorganization proceeding. The Trust on behalf of CPER may obtain only limited recovery or may obtain no recovery in such circumstances.

Valuing OTC derivatives may be less certain than actively traded financial instruments.