UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

Proxy Statement Pursuant to Section 14(a) of the

Securities Exchange Act of 1934

(Amendment No. )

Filed by the Registrant x Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| ¨ | Definitive Proxy Statement | |

| x | Definitive Additional Materials | |

| ¨ | Soliciting Material Pursuant to § 240.14a-12 | |

Hudson Pacific Properties, Inc.

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ¨ | Fee paid previously with preliminary materials: | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. | |||

| (1) | Amount previously paid:

| |||

| (2) | Form, Schedule or Registration Statement No.:

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

|

Supplemental Executive Compensation and Performance Summary

May 2014

|

Introduction

Explanatory Note

Hudson Pacific Properties, Inc. (the “Company”) is filing herewith certain supplementary materials that further demonstrate the strong link between pay and performance under the Company’s named executive officer 2013 compensation program, as originally described in the Company’s proxy statement filed with the Securities and Exchange Commission on March 28, 2014. The Company believes that certain shareholder advisory services have misinterpreted certain key components of this program and, accordingly, made unwarranted recommendations against our “say-on-pay” advisory vote. This supplemental disclosure clarifies the proper operation and quantification of relevant components of the Company’s 2013 compensation program. The Company encourages its stockholders to consider this additional information when casting their vote. This summary may be distributed in the future to certain of the Company’s stockholders or be used for other purposes.

Through this presentation, we are asking for your support at the Annual Meeting by voting in accordance with the recommendations of our Board of Directors on all proposals. In particular, we request your support on Proposal No. 3, Advisory Approval of Executive Compensation (“Say-On-Pay”).

ISS Proxy Advisory Services (“ISS”) and Glass Lewis have recently recommended that their clients vote against the Say-On-Pay proposal. We believe that both the ISS and Glass Lewis recommendations do not account for our performance relative to our peers and the pay-for-performance features imbedded in our executive compensation program, especially with respect to ISS as they relate to our 2013 Outperformance Plan (“2013 OPP”).

2

|

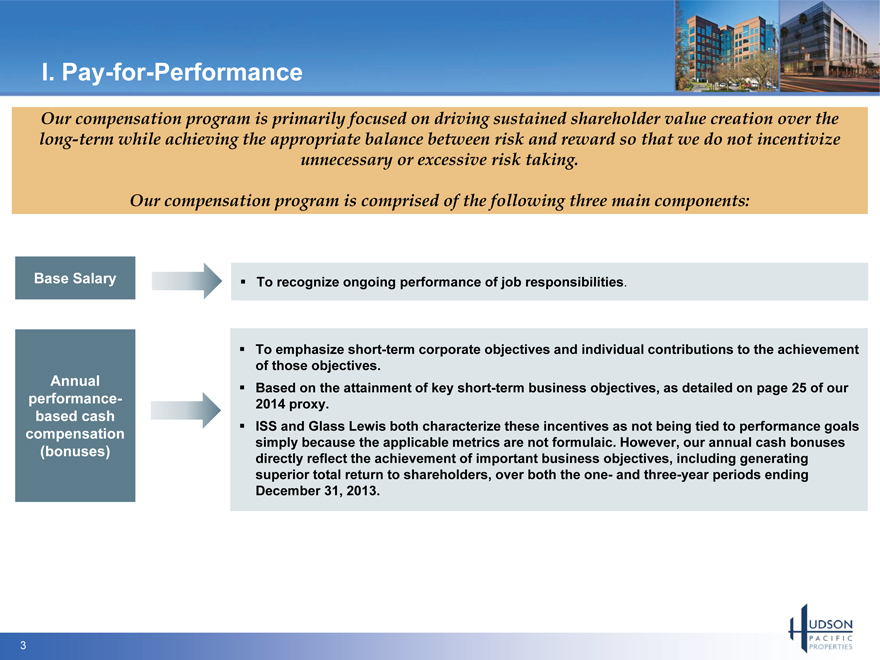

I. Pay-for-Performance

Our compensation program is primarily focused on driving sustained shareholder value creation over the long-term while achieving the appropriate balance between risk and reward so that we do not incentivize unnecessary or excessive risk taking.

Our compensation program is comprised of the following three main components:

Base Salary To recognize ongoing performance of job responsibilities.

To emphasize short-term corporate objectives and individual contributions to the achievement

of those objectives.

Annual Based on the attainment of key short-term business objectives, as detailed on page 25 of our

performance- 2014 proxy.

based cash

compensation ISS and Glass Lewis both characterize these incentives as not being tied to performance goals

simply because the applicable metrics are not formulaic. However, our annual cash bonuses

(bonuses) directly reflect the achievement of important business objectives, including generating

superior total return to shareholders, over both the one- and three-year periods ending

December 31, 2013.

3

|

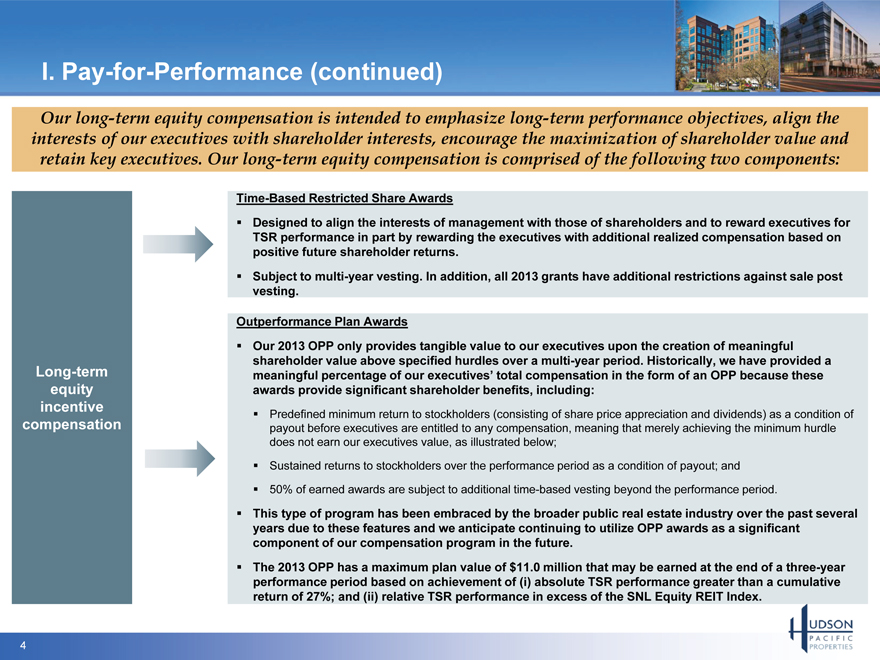

I. Pay-for-Performance (continued)

Our long-term equity compensation is intended to emphasize long-term performance objectives, align the interests of our executives with shareholder interests, encourage the maximization of shareholder value and retain key executives. Our long-term equity compensation is comprised of the following two components:

Time-Based Restricted Share Awards

Designed to align the interests of management with those of shareholders and to reward executives for

TSR performance in part by rewarding the executives with additional realized compensation based on

positive future shareholder returns.

Subject to multi-year vesting. In addition, all 2013 grants have additional restrictions against sale post

vesting.

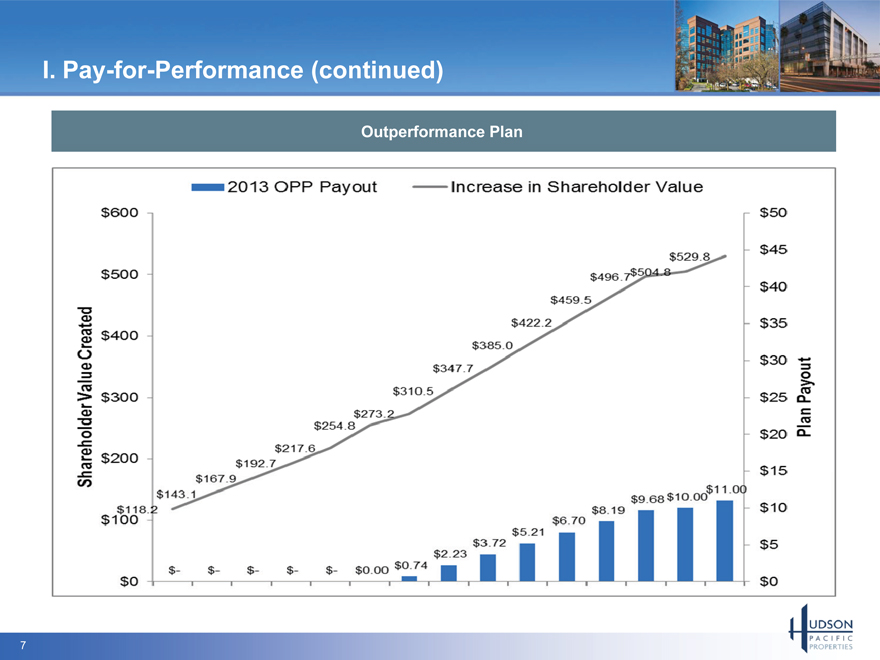

Outperformance Plan Awards

Our 2013 OPP only provides tangible value to our executives upon the creation of meaningful

shareholder value above specified hurdles over a multi-year period. Historically, we have provided a

Long-term meaningful percentage of our executives’ total compensation in the form of an OPP because these

equity awards provide significant shareholder benefits, including:

incentive Predefined minimum return to stockholders (consisting of share price appreciation and dividends) as a condition of

compensation payout before executives are entitled to any compensation, meaning that merely achieving the minimum hurdle

does not earn our executives value, as illustrated below;

Sustained returns to stockholders over the performance period as a condition of payout; and

50% of earned awards are subject to additional time-based vesting beyond the performance period.

This type of program has been embraced by the broader public real estate industry over the past several

years due to these features and we anticipate continuing to utilize OPP awards as a significant

component of our compensation program in the future.

The 2013 OPP has a maximum plan value of $11.0 million that may be earned at the end of a three-year

performance period based on achievement of (i) absolute TSR performance greater than a cumulative

return of 27%; and (ii) relative TSR performance in excess of the SNL Equity REIT Index.

4

|

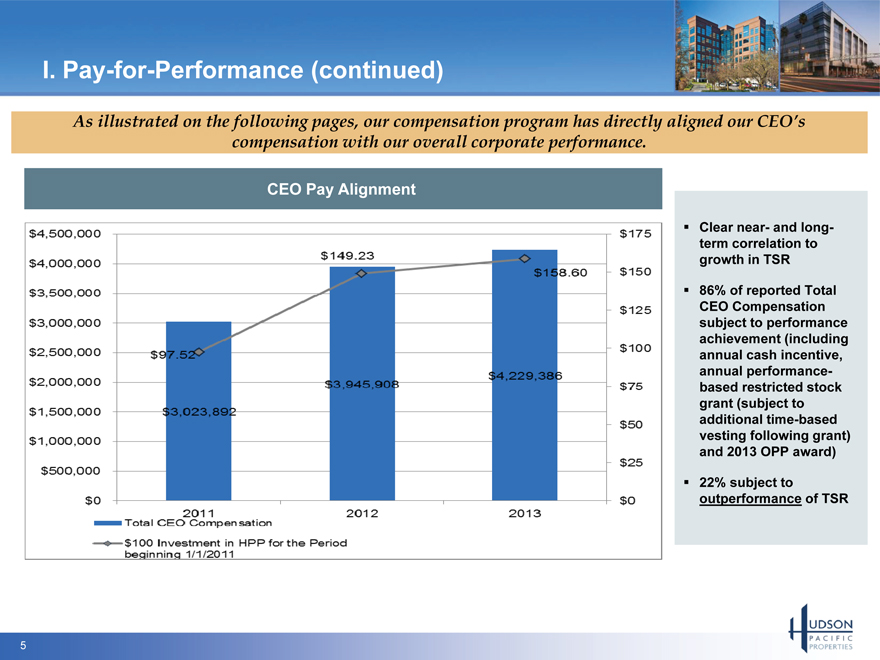

I. Pay-for-Performance (continued)

As illustrated on the following pages, our compensation program has directly aligned our CEO’s compensation with our overall corporate performance.

CEO Pay Alignment

Clear near- and long-term correlation to growth in TSR

86% of reported Total CEO Compensation subject to performance achievement (including annual cash incentive, annual performance-based restricted stock grant (subject to additional time-based vesting following grant) and 2013 OPP award)

22% subject to outperformance of TSR

5

|

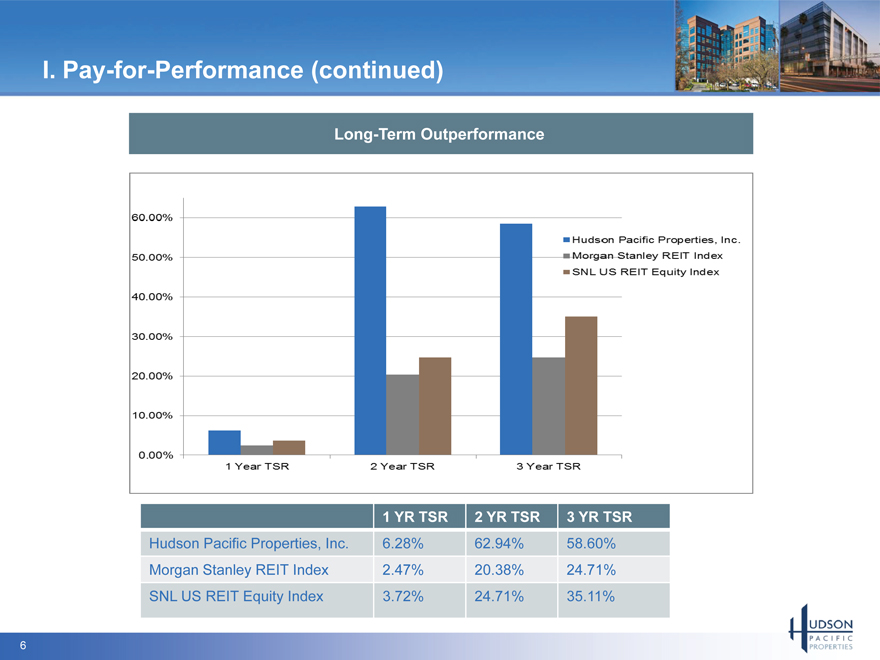

I. Pay-for-Performance (continued)

Long-Term Outperformance

1 YR TSR 2 YR TSR 3 YR TSR

Hudson Pacific Properties, Inc. 6.28% 62.94% 58.60%

Morgan Stanley REIT Index 2.47% 20.38% 24.71%

SNL US REIT Equity Index 3.72% 24.71% 35.11%

6

|

I. Pay-for-Performance (continued)

Outperformance Plan

7

|

II. Review of Third Party Proxy Reports

Comparison with ISS and Glass Lewis Evaluation of Annual Bonus Awards

Our annual cash incentives are based on the attainment of key short-term business objectives, as detailed on page 25 of our 2014 proxy.

ISS and Glass Lewis mischaracterize these incentives as not being tied to performance goals solely because the applicable metrics are not formulaic.

We believe this characterization is inaccurate – our annual cash bonuses directly reflect our Compensation Committee’s evaluation of the achievement of important business objectives, including the following:

Achieved total shareholder return performance for the three-year period ending December 31, 2013 at the 100th percentile of our performance-based executive compensation peer group and 70th percentile of our size-based peer group;

Successfully beat consensus FFO estimates for each quarter of 2013;

Successfully sourced and executed acquisitions with a gross purchase price of nearly $550.0 million and consisting of seven properties aggregating more than 1 million square feet of office space in the Company’s target markets and planned expansion into the Pacific Northwest;

Successfully disposed of 330,000 square-foot office property and completed 1031 tax-free exchange of proceeds;

Maintained a flexible capital structure demonstrated through (i) the raising of approximately $190 million of equity capital and (ii) the successful assumption or origination of nearly $550.0 million of corporate and project financing, including the replacement of our $200.0 million secured revolving credit facility with a $250.0 million unsecured revolving credit facility on improved terms;

Executed 58 new and renewal leases for more than 750,000 square feet; and

Demonstrated sound operating results that have led to a current stabilized office portfolio occupancy rate of 95.4% as of the end of 2013, nearly 200 basis points higher than the 93.5% occupancy rate as of the end of 2012.

We believe that our annual bonus awards have been a critical component of our overall compensation program that has directly aligned our CEO’s compensation with our overall corporate performance.

8

|

II. Review of Third Party Proxy Reports (continued)

Comparison with ISS Evaluation of CEO Pay

In its 2014 proxy report, ISS re-valued our CEO’s 2013 OPP award utilizing a valuation method that does not follow SEC disclosure requirements applicable to current year compensation disclosure or ISS’ stated valuation methodology.

ISS used a valuation method in which the 2013 OPP award was reflected at its maximum potential value, which we believe overstates the compensation value.

As a result, ISS valued our CEO’s 2013 OPP award at $2.5 million in 2013 as compared to the actual grant date fair value of $0.94 million, as disclosed in the Summary Compensation Table of our 2014 proxy (which reflects any reduction that is appropriate for the probability that the performance goals might not be met) – a 165% overstatement of the actual value.

ISS states they are using a “target” number, even though our program does not utilize a target approach. Instead, ISS actually based their calculation on the maximum possible payout assuming from “Day 1” the achievement of significant absolute and relative TSR hurdles.

The grant date fair value of the 2013 OPP award to our CEO was derived by an independent third party valuation expert and audited as part of the Company’s 2013 integrated audit by its independent auditor. The actual grant date fair value results directly from the application of meaningful performance hurdles that the Company must exceed before any of the award may be earned, and thus represents a more accurate portrayal of the current value of this award in light of the significant challenges inherent in exceeding such hurdles.

As a result, ISS overstated our CEO’s 2013 compensation at $5.8 million, as compared to his actual 2013 compensation of $4.2 million (as reported in our Summary Compensation Table in accordance with applicable disclosure rules).

9

|

II. Review of Third Party Proxy Reports (continued)

Comparison with ISS Evaluation of President Stern Consulting Agreement

In evaluating the payments made and awards granted to our former President in connection with his resignation and entering into a consulting agreement with the Company, ISS takes issue with both the magnitude and terms of the payments and awards.

These payments and awards were determined as the result of arm’s-length negotiations and, if considered in the context of the cash severance to which our former President would have been entitled under his employment agreement in connection with any termination without cause or for good reason, as disclosed on page 35 of our 2014 proxy, the approximately $2.8 million value of the negotiated consulting arrangement (consisting of the $2.5 million cash payment and 13,581 shares of Company restricted stock) is far less than the approximately $5.3 million of cash severance to which he would have been entitled in connection with a severance termination under his employment agreement.

Further, it is important to note that the amount Mr. Stern is receiving under his consulting agreement constitutes payment for services over the consulting period (one year) under the terms of his consulting arrangement. Had Mr. Stern been terminated without cause or for good reason, he would have been contractually entitled to cash payments equal to almost twice this amount, without any obligation for future performance on his part.

10

|

II. Review of Third Party Proxy Reports (continued)

Comparison with ISS Evaluation of Risk Mitigators

ISS misinterpreted our stockholding requirements and incorrectly factored into its pay-for-performance analysis the absence of applicable stockholding requirements. In fact, our named executive officers and directors are subject to significant stock ownership guidelines that we disclose on page 40 of our 2014 proxy.

Our named executive officers are required to hold Company common stock valued at 3x-5x their respective base salaries (depending on their position).

Our directors are required to hold Company stock valued at 2x their annual cash retainer.

Additionally, each restricted stock award granted to our Named Executive Officers in 2013 is subject to a two-year post-vesting holding period, which we believe further aligns their interests with those of our stockholders.

11

|

Conclusion

We urge stockholders to review our Proxy Statement, including the CD&A, and form their own opinions as to the reasonableness and appropriateness of our CEO’s compensation when evaluating our pay-for-performance. If you have any questions, comments or would like additional information, please contact Mark Lammas, our Chief Financial Officer, at (310) 445-5702.

Your vote is important. We urge you to vote FOR the advisory vote to approve the compensation to our named executive officers in 2013.

12

|