Table of Contents

Exhibit 99.1

Part II

| ITEM 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Unless the context otherwise requires, references in this report to the “Partnership,” “we,” “our,” “us” or like terms, when used in a historical context, refer to the financial results of Chesapeake Midstream Partners, L.L.C. through the closing date of our initial public offering (“IPO”) on August 3, 2010 and to Access Midstream Partners, L.P. (NYSE: ACMP) and its subsidiaries thereafter. The “GIP I Entities” refers to, collectively, GIP-A Holding (CHK), L.P., GIP-B Holding (CHK), L.P. and GIP-C Holding (CHK), L.P., the “GIP II Entities” refers to certain entities affiliated with Global Infrastructure Investors II, LLC, and “GIP” refers to the GIP I Entities and their affiliates and the GIP II Entities, collectively. “Williams” refers to The Williams Companies, Inc. (NYSE: WMB). “Chesapeake” refers to Chesapeake Energy Corporation (NYSE: CHK). “Total,” when discussing the upstream joint venture with Chesapeake, refers to Total E&P USA, Inc., a wholly owned subsidiary of Total S.A. (NYSE: TOT, FP: FP), and when discussing our gas gathering agreement and related matters, refers to Total E&P USA, Inc. and Total Gas & Power North America, Inc., a wholly owned subsidiary of Total S.A.

Overview

We are a growth-oriented publicly traded Delaware limited partnership formed in 2010 to own, operate, develop and acquire natural gas, natural gas liquids (“NGLs”) and oil gathering systems and other midstream energy assets. We are principally focused on natural gas and NGL gathering, the first segment of midstream energy infrastructure that connects natural gas and NGLs produced at the wellhead to third-party takeaway pipelines.

We provide our midstream services to Chesapeake, Total, Mitsui & Co. (“Mitsui”), Anadarko Petroleum Corporation (“Anadarko”), Statoil ASA (“Statoil”) and other leading producers under long-term, fixed-fee contracts. We operate assets in our Barnett Shale region in north-central Texas; our Eagle Ford Shale region in South Texas; our Haynesville Shale region in northwest Louisiana; our Marcellus Shale region primarily in Pennsylvania and West Virginia; our Niobrara Shale region in eastern Wyoming; our Utica Shale region in eastern Ohio; and our Mid-Continent region which includes the Anadarko, Arkoma, Delaware and Permian Basins.

Acquisitions

Our CMO Acquisition and Williams’ Acquisition of 50 Percent of Our General Partner

On December 20, 2012, we acquired from Chesapeake Midstream Development, L.P. (“CMD”), a wholly owned subsidiary of Chesapeake, and certain of CMD’s affiliates, 100 percent of the issued and outstanding equity interests in Chesapeake Midstream Operating, L.L.C. (“CMO”) for total consideration of $2.16 billion (the “CMO Acquisition”). As a result of the CMO Acquisition, the Partnership now owns certain midstream assets in the Eagle Ford, Utica and Niobrara regions. The CMO Acquisition also extended our assets and operations in the Haynesville, Marcellus and Mid-Continent regions. The acquired assets included, in the aggregate, approximately 1,675 miles of pipeline and 4.3 million (gross) dedicated acres as of the date of the acquisition. We also assumed various gas gathering and processing agreements associated with the assets that have terms ranging from 10 to 20 years and that, in certain cases, include cost of service or fee redetermination mechanisms.

The results of operations presented and discussed in this annual report include results of operations from the CMO assets for the twelve-day period from closing of the CMO Acquisition on December 20, 2012 through December 31, 2012.

Concurrently with the CMO Acquisition, the GIP I Entities sold to Williams 34,538,061 of our subordinated units and 50 percent of the outstanding equity interests in Access Midstream Ventures, L.L.C., the sole member of our general partner (“Access Midstream Ventures”), for cash consideration of approximately $1.82 billion (the “Williams Acquisition”). As a result of the closing of the Williams Acquisition, the GIP II Entities and Williams together own and control our general partner and the GIP I Entities no longer have any ownership interest in the Partnership or our general partner.

Our Marcellus Acquisition

On December 29, 2011, we acquired from CMD all of the issued and outstanding common units of Appalachia Midstream Services, L.L.C. (“Appalachia Midstream”) for total consideration of $879.3 million, consisting of 9,791,605 common units and $600.0 million in cash. Through Appalachia Midstream, we currently operate 100 percent of and own an approximate average 47 percent interest in 10 gas gathering systems that consist of approximately 549 miles

Table of Contents

of gas gathering pipeline in the Marcellus Shale. The remaining 53 percent interest in these assets is owned primarily by Statoil, Anadarko and Mitsui. Appalachia Midstream operates the assets under 15-year, 100 percent fixed fee gathering agreements that include significant acreage dedications and cost of service mechanisms. In addition, CMD committed to pay us quarterly for any shortfall between the actual EBITDA generated by these gas gathering systems and specified quarterly targets totaling $100 million in 2012 and $150 million in 2013. EBITDA generated by these gas gathering systems exceeded the specified EBITDA commitment in 2012.

The results of operations presented and discussed in this annual report include results of operations from Appalachia Midstream for the full year of operations in 2012 and the two-day period from closing of the acquisition on December 29, 2011, through December 31, 2011.

We acquired additional assets in the Marcellus Shale region through the acquisition of CMO in December 2012.

Our Haynesville Springridge Acquisition

On December 21, 2010, we acquired the Springridge gathering system and related facilities located in Caddo and De Soto Parishes, Louisiana from CMD for $500.0 million. In connection with the acquisition, we entered into a 10-year, 100 percent fixed-fee gas gathering agreement with Chesapeake that includes a significant acreage dedication, an annual fee redetermination and a three-year minimum volume commitment.

Our Operations

We operate assets in the Barnett Shale region in north-central Texas, the Eagle Ford Shale region in southwest Texas, the Haynesville Shale region in northwest Louisiana, the Marcellus Shale region primarily in Pennsylvania and West Virginia, the Niobrara Shale region in Wyoming, the Utica Shale region in northeast Ohio, and our Mid-Continent region, which includes the Anadarko, Arkoma, Delaware and Permian Basins.

We generated approximately 54 percent of our fees from our gathering systems in the Barnett Shale region, approximately 19 percent of our fees from our gathering systems in the Marcellus Shale region, approximately 18 percent of our fees from our gathering systems in our Mid-Continent region and approximately 9 percent of our fees from our gathering systems in the Haynesville Shale region for the year ended December 31, 2012. The CMO assets contributed to our income during the 12-day period from closing of the acquisition to December 31, 2012, but the impact was immaterial to our results.

The results of our operations are primarily driven by the volumes of natural gas and liquids we gather, treat, compress and process across our gathering systems. We currently provide all of our midstream services pursuant to fixed fee contracts, which limit our direct commodity price exposure, and we generally do not take title to the natural gas or NGLs we gather. We have entered into long-term gas gathering and processing agreements with Chesapeake, Total, Statoil, Anadarko, Mitsui, and other producers. Pursuant to our commercial agreements, our producer customers have agreed to dedicate extensive acreage in our operating regions.

Our Commercial Agreements with Producers

We generate substantially all of our revenues through long-term, fixed-fee natural gas gathering, treating and compression contracts, and increasingly through processing contracts, all of which limit our direct commodity price exposure.

Future revenues under our commercial agreements with producers will be derived pursuant to terms that will vary depending on the applicable operating region. The following outlines the key economic provisions of our commercial agreements by region.

Barnett Shale Region.Under our gas gathering agreements with Chesapeake and Total, we have agreed to provide the following services in our Barnett Shale region for the fees and obligations outlined below:

| • | Gathering, Treating and Compression Services. We gather, treat and compress natural gas for Chesapeake and Total within the Barnett Shale region in exchange for specified fees per thousand cubic feet (“Mcf”) for natural gas gathered on our gathering systems that are based on the pressure at the various points where our gathering systems received our customers’ natural gas. We refer to these fees collectively as the Barnett Shale fee. Our Barnett Shale fee is subject to an annual rate escalation of two percent at the beginning of each year. |

2

Table of Contents

| • | Acreage Dedication. Pursuant to our gas gathering agreements, subject to certain exceptions, each of Chesapeake and Total has agreed to dedicate all of the natural gas owned or controlled by it and produced from or attributable to existing and future wells located on natural gas and oil leases covering lands within an acreage dedication in our Barnett Shale region. |

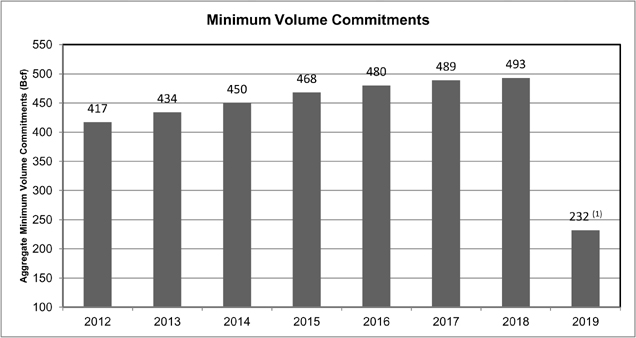

| • | Minimum Volume Commitments. Pursuant to our gas gathering agreements, Chesapeake and Total have agreed to minimum volume commitments for each year through December 31, 2018 and for the six-month period ending June 30, 2019. Approximately 75 percent of the aggregate minimum volume commitment is attributed to Chesapeake, and approximately 25 percent is attributed to Total. The minimum volume commitments increase, on average, approximately 3 percent per year. The following table outlines the approximate aggregate minimum volume commitments for each year during the minimum volume commitment period: |

| (1) | Indicated volumes relate to the six months ending June 30, 2019. |

If either Chesapeake or Total does not meet its minimum volume commitment to us, as adjusted in certain instances, for any annual period (or six-month period in the case of the six months ending June 30, 2019) during the minimum volume commitment period, Chesapeake or Total, as applicable, will be obligated to pay us a fee equal to the Barnett Shale fee for each Mcf by which the applicable party’s minimum volume commitment for the year (or six-month period) exceeds the actual volumes gathered on our systems attributable to the applicable party’s production. To the extent natural gas gathered on our systems from Chesapeake or Total, as applicable, during any annual period (or six-month period) exceeds such party’s minimum volume commitment for the period, Chesapeake or Total, as applicable, will be obligated to pay us the Barnett Shale fee for all volumes gathered, and the excess volumes will be credited first against the minimum volume commitments for the six months ending June 30, 2019, and then against the minimum volume commitments of each preceding year. If the minimum volume commitment for any period is credited in full, the minimum volume commitment period will be shortened to end on the final day of the immediately preceding period.

| • | Fee Redetermination.In May 2012, we entered into an agreement with Chesapeake and Total relating to the initial redetermination period. The agreement called for an upward adjustment of the Barnett Shale fee and was effective July 1, 2012. We and each of Chesapeake and Total, as applicable, have the right to request an additional redetermination of the Barnett Shale fee during a two-year period beginning on September 30, 2014. The fee redetermination mechanism is intended to support a return on our invested capital. If a fee redetermination is requested, we will determine an adjustment (upward or downward) to our Barnett Shale fee with Chesapeake and Total based on the factors specified in our gas gathering agreements, including, but not limited to: (i) differences between our actual capital expenditures, compression expenses and revenues as of the redetermination date and the scheduled estimates of these amounts for the minimum volume commitment period made as of September 30, 2009 and (ii) differences between the revised estimates of our capital expenditures, compression expenses and revenues for the remainder of the minimum volume commitment period forecast as of the redetermination date and |

3

Table of Contents

scheduled estimates thereof for the minimum volume commitment period made as of September 30, 2009. The cumulative upward or downward adjustment for the Barnett Shale region is capped at 27.5 percent of the initial weighted average Barnett Shale fee (as escalated) as specified in the gas gathering agreement. If we and Chesapeake or Total, as applicable, do not agree upon a redetermination of the Barnett Shale fee within 30 days of receipt of the request for the redetermination, an industry expert will be selected to determine adjustments to the Barnett Shale fee. |

| • | Well Connection Requirement. Subject to required notice by Chesapeake and Total and certain exceptions, we have generally agreed to connect new operated drilling pads and new operated wells within our Barnett Shale region acreage dedications as requested by Chesapeake and Total during the minimum volume commitment period. During the minimum volume period, if we fail to complete a connection in the acreage dedication by the required date, Chesapeake and Total, as their sole remedy for such delayed connection, are entitled to a delay in the minimum volume obligations for gas volumes that would have been produced from the delayed connection. |

| • | Fuel and Lost and Unaccounted For Gas. We have agreed with Chesapeake and Total on caps on fuel and lost and unaccounted for gas on our systems, both on an individual basis and an aggregate basis, with respect to Chesapeake’s and Total’s volumes. These caps do not apply to certain of our gathering systems due to their historic performance relative to the caps. These systems will be reviewed annually to determine whether changes have occurred that would make them suitable for inclusion. If we exceed a permitted cap in any covered period, we may incur significant expenses to replace the natural gas used as fuel and lost or unaccounted for in excess of such cap based on then current natural gas prices. Accordingly, this replacement obligation will subject us to direct commodity price risk. |

Eagle Ford Shale Region. Under our gas gathering agreement that we entered into with our producer customer, as part of the CMO Acquisition, we have agreed to provide the following services in our Eagle Ford Shale region for the fees and obligations outlined below:

| • | Gathering, Compression, Dehydration and Treating Services. We will gather, compress, dehydrate and treat natural gas and liquids for the producers within the Eagle Ford Shale region in exchange for a cost of service based fee for natural gas and liquids gathered and treated on our gathering systems. The cost of service components will include revenue, compression expense, deemed general and administrative expense, capital expenditures, fixed and variable operating expenses and other metrics. We refer to these fees collectively as the Eagle Ford fee. |

| • | Acreage Dedication. Subject to certain exceptions, our producer customer has agreed to dedicate all of the natural gas and liquids owned or controlled by it and produced from the Eagle Ford Shale formation through existing and future wells with a surface location within the dedicated area in the Eagle Ford Shale region. |

| • | Fee Redetermination. During 2013 and 2014, the Eagle Ford fee is determined by a fee tiering mechanism that calculates the Eagle Ford fee on a monthly basis according to the quantity of gas delivered to us by our producer customer relative to its scheduled deliveries. Effective on January 1, 2015 and January 1 of each year thereafter for a period of 20 years from July 1, 2012, the Eagle Ford fee will be redetermined based on a cost of service calculation that targets a specified pre-income tax rate of return on invested capital. There is no cap on these adjustments. |

| • | Well Connection Requirement. Subject to required notice by our producer customer, we will have the option to connect new operated wells within our Eagle Ford Shale region acreage dedications as requested by the producer customer. If we elect not to connect a new operated well, the producer will be provided alternative forms of release. Subject to certain conditions specified in the applicable gas gathering agreement, if we elect to connect a new well to our gathering systems, we are generally required to connect the new wells within specified timelines subject to penalties for delayed connections, up to a specified cap, and the potential for a well pad release from the producer customer’s acreage dedication in certain circumstances. |

| • | Fuel and Lost and Unaccounted For Gas. We have agreed with the producer customer to a cap on fuel and lost and unaccounted for gas on our systems with respect to the producer customer’s volumes. The cap is based on a percentage per deemed compression stage and a percentage for lost and unaccounted for gas. If we exceed a permitted cap in any covered period and do not respond in a timely manner with a proposed solution, we may incur significant expenses to replace the natural gas used as fuel or lost and unaccounted for in excess of such cap based on then-current natural gas prices. Accordingly, this replacement obligation may subject us to direct commodity price risk. |

4

Table of Contents

Haynesville Shale Region.Under our gas gathering agreement that we entered into with our producer customer, we have agreed to provide the following services in our Haynesville Shale region for the fees and obligations outlined below:

Springridge Gathering System

| • | Gathering, Treating and Compression Services.We gather, treat and compress natural gas in exchange for fees per Mcf for natural gas gathered and per Mcf for natural gas compressed, which we refer to as the Springridge fees. The Springridge fees for these systems are subject to an annual specified rate escalation at the beginning of each year. |

| • | Minimum Volume Commitments. Pursuant to our gas gathering agreement, our producer customer has agreed to minimum volume commitments for each year through December 31, 2013. In the event our producer customer does not meet its minimum volume commitment to us, as adjusted in certain instances, for any annual period during the minimum volume commitment period, it will be obligated to pay us a fee equal to the Springridge fee for each Mcf by which the minimum volume commitment for the year exceeds the actual volumes gathered on our systems attributable to its production. To the extent natural gas gathered on our systems from our producer customer during any annual period exceeds its minimum volume commitment for the period, it will be obligated to pay us the Springridge fee for all volumes gathered, and the excess volumes will be credited first against the minimum volume commitments for the year 2013, and then against the minimum volume commitments of each preceding year. In the event that the minimum volume commitment for any period is credited in full, the minimum volume commitment period will be shortened to end on the final day of the immediately preceding period. |

| • | Acreage Dedication. Pursuant to our gas gathering agreement, subject to certain exceptions, our producer customer has agreed to dedicate all of the natural gas owned or controlled by them and produced from or attributable to existing and future wells located on oil, natural gas and mineral leases within the Springridge acreage dedication. |

| • | Fee Redetermination. The Springridge fees are subject to a redetermination mechanism. The first redetermination period will extend from December 1, 2010 through December 31, 2012, and subsequent redetermination periods will be the calendar years 2013 through 2020. We will determine an adjustment to fees for the gathering systems in the region with our producer customer based on the factors specified in the gas gathering agreement, including, but not limited to, differences between our actual capital expenditures, compression expenses and revenues as of the redetermination date and the scheduled estimates of these amounts for the period ending December 31, 2020, referred to as the redetermination period, made as of November 30, 2010. The annual upward or downward fee adjustment for the Springridge region is capped at 15 percent of the then-current fees at the time of redetermination. |

5

Table of Contents

| • | Well Connection Requirement. We have certain connection obligations for new operated drilling pads and operated wells of our producer customer in the acreage dedications. Our producer customer is required to provide us notice of new drilling pads and wells operated by our producer customer in the acreage dedications. Subject to certain conditions specified in the gas gathering agreement, we are generally required to connect new operated drilling pads in the acreage dedication by the later of 30 days after the date the wells commence production and six months after the date of the connection notice. During the minimum volume period, if we fail to complete a connection in the Springridge acreage dedication by the required date, our producer customer, as its sole remedy for such delayed connection, is entitled to a delay in the minimum volume obligations for gas volumes that would have been produced from the delayed connection. After the minimum volume period, we are subject to a daily penalty for such delayed connections, up to a specified cap per delayed connection. Our producer customer also is required to notify us of its wells drilled in the acreage dedications that are operated by other parties and we have the option, but not the obligation, to connect non-operated wells to our gathering systems. If we decline to make a connection to a non-operated well, our producer customer has certain rights to have the well released from the dedication under the gas gathering agreement. |

| • | Fuel and Lost and Unaccounted For Gas.We have agreed with our producer customer on caps on fuel and lost and unaccounted for gas on our systems with respect to our producer customer’s volumes. These caps do not apply to one of our compressor stations due to its historical performance relative to the caps. This station will be reviewed periodically to determine whether changes have occurred that would make it suitable for inclusion. If we exceed a permitted cap in any covered period, we may incur significant expenses to replace the natural gas used as fuel or lost and unaccounted for in excess of such cap based on then current natural gas prices. Accordingly, this replacement obligation may subject us to direct commodity price risk. |

Mansfield Gathering System

| • | Gathering, Dehydration, Compression and Treating Services. We will gather, dehydrate, compress and to the extent provided, treat natural gas in exchange for a fixed fee per MMBtu for natural gas gathered. We refer to this fee as the Mansfield fee. The Mansfield fee is subject to an annual 2.5 percent rate escalation at the beginning of each year. |

| • | Acreage Dedication. Subject to certain exceptions, our producer customer has agreed to dedicate all of the natural gas owned or controlled by it and produced from the Bossier and Haynesville formations through existing and future wells with a surface location within the dedicated area in the Mansfield acreage dedication. |

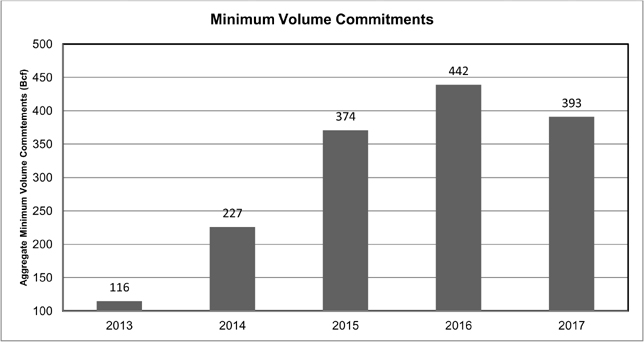

| • | Minimum Volume Commitments. Pursuant to our gas gathering agreement, our producer customer has agreed to minimum volume commitments for each year through December 31, 2017. If our producer customer does not meet its minimum volume commitments to us, as adjusted in certain instances, for any annual period during the minimum volume commitment period, it will be obligated to pay us the difference between the minimum volume commitment and the volume of gas delivered from its wells. |

6

Table of Contents

| • | Fixed Fee/Tiered Fees. During the minimum volume commitment period, the Mansfield fee is a fixed fee on all monthly volumes. Subsequent to that period, our producer customer will pay a tiered fee that calculates the Mansfield fee on a monthly basis according to the quantity of gas delivered to us from our producer customer’s wells relative to its scheduled deliveries. |

| • | Well Connection Requirement. We have certain connection obligations for new operated wells of our producer customer in the acreage dedications. Our producer customer is required to provide us notice of new wells that it operates in the acreage dedications. Subject to certain conditions specified in the applicable gas gathering agreement, we are generally required to connect new wells within specified timelines subject to minimum volume commitment delays for volumes that would have been received from the new wells during the minimum volume commitment period and penalties up to a specified cap after the minimum volume commitment period. |

| • | Fuel and Lost and Unaccounted For Gas. We have agreed with our producer customer on percentage-based caps on fuel and lost and unaccounted for gas on our systems with respect to our producer customer’s volumes. If we exceed a permitted cap in any covered period, we may incur significant expenses to replace the natural gas used as fuel or lost and unaccounted for in excess of such cap based on then current natural gas prices. Accordingly, this replacement obligation may subject us to direct commodity price risk. |

Marcellus Shale Region.Under our gas gathering agreements with certain subsidiaries of Chesapeake, Statoil, Anadarko, Epsilon, Mitsui and Chief, we have agreed to provide the following services in our Marcellus Shale region for our proportionate share (based on our ownership interest in the applicable systems) of the fees and obligations outlined below:

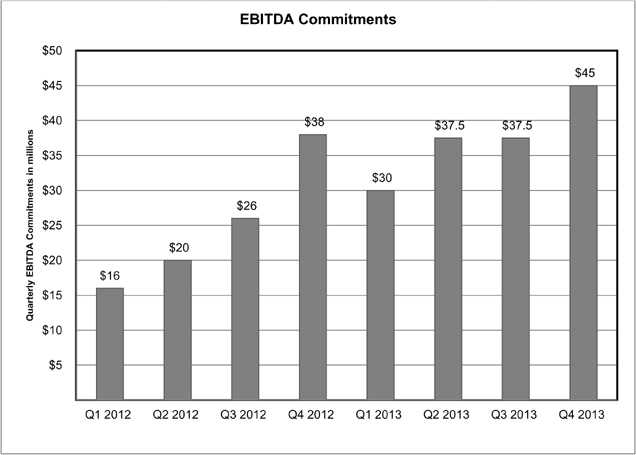

| • | Gathering and Compression Services.In systems operated by Appalachia Midstream, we gather and compress natural gas in exchange for fees per million British thermal units (“MMBtu”) of natural gas gathered and per MMBtu of natural gas compressed. The gathering fees are redetermined annually based on a cost of service mechanism, as described below. The compression fees escalate on January 1 of each year based on the consumer price index. In addition, CMD has committed to pay us quarterly any shortfall between the actual EBITDA generated by these assets and specified quarterly targets totaling $100 million in 2012 and $150 million in 2013. EBITDA generated by these assets exceeded the $100 million target for 2012 and no additional revenue related to the commitment was recognized. The target for 2013 represents the minimum amount of EBITDA we will recognize with the potential that throughput for these systems will generate EBITDA in excess of the guaranteed amounts. The following table below outlines the EBITDA commitments for each quarter during the commitment period. In the systems acquired as part of the CMO Acquisition, we gather and compress natural gas in exchange for a gathering fee per MMBtu, which is redetermined annually based on a cost of service mechanism. |

7

Table of Contents

| • | Acreage Dedication.Pursuant to our gas gathering agreements, subject to certain exceptions, the shippers and producers have agreed to dedicate all of the natural gas owned or controlled by them and produced from or attributable to existing and future wells with a surface location within the designated dedicated areas. |

| • | Fee Redetermination.Each January 1, gathering fees for each gathering system under the gas gathering agreements with Chesapeake, Statoil, Anadarko, Epsilon and Mitsui will be redetermined based on a cost of service calculation that targets a specified pre-income tax rate of return on invested capital. There is no cap on these fee adjustments. Each January 1, gathering fees for each gathering system under the gas gathering agreement with Chief are adjusted based on the applicable producer price index. The change in the amount of the gathering fees under the Chief agreement is not to exceed 3 percent in any one year. |

| • | Well Connections.We have the option to connect to new wells within the dedicated acreage. If we elect not to connect to any new well within the dedicated acreage, the shipper for such well may elect to have such well, and any subsequent wells within a two-mile radius (in the case of Chesapeake, Statoil, Anadarko, Epsilon and Mitsui) or a one-mile radius (in the case of Chief) of the surface location of such well, permanently released from the dedication area, or the shipper may elect to construct, at the shipper’s expense, a gathering system to connect to such well (and wells within a one-mile radius of such well in the case of Chesapeake, Statoil, Anadarko, Epsilon and Mitsui), in which case the shipper would pay us a reduced gathering fee for natural gas we receive through the shipper-installed asset. Alternatively, the shipper may require us to enter into an agreement pursuant to which we would construct the gathering system to connect to the well in exchange for a reimbursement by the shipper of the costs we incur in connection therewith. The shipper may elect to connect wells outside the dedicated area at its sole expense and pay us a reduced gathering fee for natural gas we receive from such wells, but gas from such outside wells will not be afforded the same priority as gas produced from wells located within the dedicated area. In the systems acquired as part of the CMO Acquisition, subject to certain conditions specified in the applicable gas gathering agreement, if we elect to connect a new well to our gathering systems, we are generally required to connect the new wells within specified timelines subject to penalties for delayed connections, up to a specified cap, and the potential for a well pad release from the producer’s acreage dedication in certain circumstances. |

8

Table of Contents

| • | Fuel and Lost and Unaccounted For Gas. Under our gas gathering agreements with Chesapeake, Statoil, Anadarko, Epsilon and Mitsui, we have agreed on caps on fuel and lost and unaccounted for gas on the systems. If we exceed the permitted cap, we must provide a cost estimate for a remedy that is reasonably expected to prevent exceeding the permitted cap in the future. At the election of the shippers we may pay such costs (which costs would then be included in the gathering fee redetermination) or the shippers may pay the costs. If we exceed the permitted cap and do not provide a proposal to the shippers to prevent exceeding the cap in the future within the required time period, we may incur our proportionate share (based on our ownership interest in the applicable system) of significant expenses in connection with the natural gas used as fuel or lost and unaccounted for in excess of such cap based on then current natural gas prices. Accordingly, this may subject us to direct commodity price risk. |

Under gas gathering agreements between Appalachia Midstream and certain subsidiaries of Chief, the shipper on each system is to furnish to us, at the shipper’s sole cost and expense, all necessary fuel gas to operate the system. Gas volumes lost solely due to our actions or inactions constituting gross negligence or willful misconduct are our sole responsibility. Additionally, we will bear the cost of natural gas lost in excess of one percent due to our failure to maintain adequate corrosion protection. If we lose natural gas due to our gross negligence or willful misconduct or our failure to maintain an adequate corrosion protection system, we may incur significant expenses in connection with the cost of the lost natural gas. Our responsibility for the cost of the lost gas may subject us to direct commodity price risk.

Niobrara Shale Region. Under our gas gathering and processing agreement that we entered into with our producer customer, as part of the CMO Acquisition, we have agreed to provide the following services in our Niobrara Shale region for the fees and obligations outlined below:

| • | Gathering, Compression, Dehydration and Processing Services. We will gather, compress, dehydrate and process natural gas and liquids within the Niobrara region in exchange for a cost of service based fee for natural gas and liquids gathered on our gathering systems and for natural gas and liquids processed at our proposed processing facility. The cost of service components will include revenues, compression expense, deemed general and administrative expense, capital expenditures, fixed and variable operating expenses and other metrics. We refer to these fees collectively as the Niobrara fee. |

| • | Acreage Dedication. Subject to certain exceptions, our producer customer has agreed to dedicate all of the natural gas and liquids owned or controlled by them and produced from the Frontier Sand and the Niobrara Shale through existing and future wells with a surface location within the dedicated areas in the Niobrara Shale region. |

| • | Fee Redetermination. Effective on January 1, 2014 and January 1st of each year thereafter for a period of 20 years from July 1, 2012, the Niobrara fee will be redetermined based on a cost of service calculation that targets a specified pre-income tax rate of return on invested capital. There is no cap on these fee adjustments. |

| • | Well Connections. Subject to required notice by our producer customer, we will have the option to connect new operated wells within our Niobrara region acreage dedications as requested by such producer customer. If we elect not to connect a new operated well, the producer customer will be provided alternative forms of release. Subject to certain conditions specified in the gas gathering agreement, if we elect to connect a new well to our gathering systems, we are generally required to connect the new wells within specified timelines subject to penalties for delayed connections up to a specified cap, and the potential for a well pad release from the producer customer’s acreage dedication in certain circumstances. |

| • | Fuel and Lost and Unaccounted For Gas. We have agreed with our producer customer to a cap on fuel and lost and unaccounted for gas on our systems with respect to the producer customer’s volumes. The cap is based on a percentage per deemed compression stage and a percentage for lost and unaccounted for gas. If we exceed a permitted cap in any covered period and do not respond in a timely manner with a proposed solution, we may incur significant expenses to replace the natural gas used as fuel or lost and unaccounted for in excess of such cap based on then current natural gas prices. Accordingly, this replacement obligation may subject us to direct commodity price risk. |

Utica Shale Region. Under our commercial agreements that we entered into with Chesapeake, Total and Enervest, acquired as part of the CMO Acquisition, we have agreed to provide the following services in our Utica Shale region to our producer customers for the fees and obligations of our producer customers outlined below:

| • | Gathering, Compression, Dehydration, Processing and Fractionation Services. We will gather, compress and dehydrate natural gas and liquids in exchange for a cost of service based fee for natural gas and liquids gathered on our gathering systems. The cost of service components (i) for our 66 percent operating interest in a joint venture that owns five wet gas gathering systems (the “Cardinal JV”), and (ii) in the area covered |

9

Table of Contents

by our 100 percent ownership interest in four dry gas gathering systems (the “Utica Dry”) will include revenues, compression expense (in the case of the Utica Dry only), deemed general and administrative expense, capital expenditures, fixed and variable operating expenses and other metrics. We also will process and fractionate natural gas and liquids through our 49 percent non-operating interest in a joint venture that is currently constructing four 200 MMcf/d processing trains, a 120,000 barrel per day fractionation facility, approximately 870,000 barrels of NGL storage capacity and other ancillary assets (the “UEO JV”) for a fixed fee that escalates annually within a specified range. The Partnership refers to these fees collectively as the Utica fee. |

| • | Acreage Dedication. Subject to certain exceptions, our producer customers have agreed to dedicate all of the natural gas and liquids owned or controlled by them and produced from the Utica Shale formation through existing and future wells with a surface location within the dedicated areas in the Utica Shale region. The UEO JV has a processing and fractionation dedication with a designated dedication area from Chesapeake, Total and Enervest for 800 MMcf/d. |

| • | Fee Redetermination. Beginning on October 1, 2013 for the Cardinal JV and January 1, 2014 for Utica Dry and annually thereafter, for a period of 20.75 years from January 1, 2012 (Cardinal JV) and 15 years from July 1, 2012 (Utica Dry), the gathering fee portion of the Utica fee will be redetermined based on a cost of service calculation that targets a specified pre-income tax rate of return on invested capital. There is no cap on these fee adjustments. |

| • | Well Connections. In the Cardinal JV, we are generally required to connect new wells within specified timelines subject to penalties for delayed connections in the form of a temporary reduction in the gathering fee for the new well. In Utica Dry, subject to required notice by the producer customer, we will have the option to connect new operated wells within our dedicated acreage as requested by the producer customer. If we elect not to connect a new operated well, the producer customer will be provided alternative forms of release. Subject to certain conditions specified in the gas gathering agreement, if we elect to connect a new well to our gathering systems, we are generally required to connect the new wells within specified timelines subject to penalties for delayed connections, up to a specified cap, and the potential for a well pad release from the producer’s acreage dedication in certain circumstances. |

| • | Processing and Fractionation Performance Standards. We have agreed with our producer customers to certain performance standards for the UEO JV, including guaranteed in-service dates, minimum facility run-time standards, minimum propane recovery standards, and fuel caps. If the UEO JV fails to achieve any of these performance standards as specified, the fees associated with these services will be temporarily reduced. |

| • | Fuel and Lost and Unaccounted For Gas. We have agreed with the producer customers to a cap on fuel and lost and unaccounted for gas on our systems with respect to each producer’s volumes. The cap is based on a percentage per deemed compression stage and a percentage for lost and unaccounted for gas. If we exceed a permitted cap in any covered period, we may incur significant expenses to replace the natural gas used as fuel or lost and unaccounted for in excess of such cap based on then current natural gas prices. Accordingly, this replacement obligation may subject us to direct commodity price risk. In Utica Dry, exceeding the permitted cap does not result in a reimbursement to the Utica producers if we respond in a timely manner with a proposed solution. |

Mid-Continent Region.Under our gas gathering agreement with producer customers, we have agreed to provide the following services in our Mid-Continent region to our producer customers for the fees and obligations of our producer customers outlined below:

| • | Gathering, Treating and Compression and Processing Services.We gather, treat, compress and process natural gas and NGLs in exchange for system-based services fees per Mcf for natural gas gathered and per Mcf for natural gas compressed. We refer to the fees collectively as the Mid-Continent fee. The Mid-Continent fees for these systems are subject to an annual two and a half percent rate escalation at the beginning of each year. |

| • | Acreage Dedication.Pursuant to our gas gathering agreement, subject to certain exceptions, our producer customers have agreed to dedicate all of the natural gas and liquids owned or controlled by them and produced from or attributable to existing and future wells located on oil, natural gas and mineral leases covering lands within the acreage dedication. |

10

Table of Contents

| • | Fee Redetermination. The Mid-Continent fees are redetermined at the beginning of each year through 2019. We and our producer customers will determine an adjustment to fees for the gathering systems in the region with our producer customers based on the factors specified in the gas gathering agreement, including, but not limited to, differences between our actual capital expenditures, compression expenses and revenues as of the redetermination date and the scheduled estimates of these amounts for the period ending June 30, 2019, referred to as the redetermination period, made as of September 30, 2009. The annual upward or downward fee adjustment for the Mid-Continent region is capped at 15 percent of the then current fees at the time of redetermination. |

| • | Well Connection Requirement.Subject to required notice by our producer customers and certain exceptions, we have generally agreed to use our commercially reasonable efforts to connect new operated drilling pads and new operated wells in our Mid-Continent region acreage dedications as requested by our producer customers through June 30, 2019. |

| • | Fuel and Lost and Unaccounted For Gas.We have agreed with our producer customers on caps on fuel and lost and unaccounted for gas on our systems, both on an individual basis and an aggregate basis, with respect to our producer customers volumes. These caps do not apply to certain of our gathering systems due to their historic performance relative to the caps. These systems will be reviewed annually to determine whether changes have occurred that would make them suitable for inclusion. If we exceed a permitted cap in any covered period, we may incur significant expenses to replace the natural gas used as fuel or lost or unaccounted for in excess of such cap based on then current natural gas prices. Accordingly, this replacement obligation will subject us to direct commodity price risk. |

As part of the CMO Acquisition, we acquired a 33% equity interest in Ranch Westex JV, LLC, which we own jointly with Regency Energy Partners, LP and Anadarko Pecos Midstream LLC. Under a gas processing agreement with Chesapeake and Anadarko, Ranch Westex JV, LLC provides gas processing services under a cost of service fee arrangement.

All Regions. If one of the counterparties to the gas gathering agreements sells, transfers or otherwise disposes of to a third party properties within the our acreage dedications, it does so subject to the terms of the gas gathering agreement, including our dedication, and it will be required to cause the third party to acknowledge and take assignment of the counterparty’s obligations under the existing gas gathering agreement with the Partnership, subject to our consent. Our producer customers’ dedication of the gas produced from applicable properties under our gas gathering agreements will run with the land in order to bind successors to the producer customers’ interest, as well as any interests in the dedicated properties subsequently acquired by the producer customer.

Other Arrangements

Services Arrangements.Under our services agreement with Chesapeake, Chesapeake has agreed to provide us with certain general and administrative services and any additional services we may request. We reimburse Chesapeake for such general and administrative services in any given month subject to a cap equal to $0.0310 per Mcf multiplied by the volume (measured in Mcf) of natural gas and liquids that we gather, treat or compress. The fee is calculated as the lesser of $0.0310 per Mcf gathered or actual corporate overhead costs, excluding those overhead costs that are billed directly to the Partnership. The $0.0310 per Mcf cap is subject to an annual upward adjustment on October 1 of each year equal to 50 percent of any increase in the Consumer Price Index, and, subject to receipt of requisite approvals, such cap may be further adjusted to reflect changes in general and administrative services provided by Chesapeake relating to new laws or accounting rules that are implemented. The cap contained in the services agreement does not apply to our direct general and administrative expenses.

Additionally, pursuant to an employee secondment agreement, specified employees of Chesapeake were seconded to our general partner to provide operating, routine maintenance and other services with respect to our business under the direction, supervision and control of our general partner. Our general partner, subject to specified exceptions and limitations, reimbursed Chesapeake on a monthly basis for substantially all costs and expenses it incurred relating to such seconded employees.

On June 15, 2012, in connection with the closing of the first portion of the acquisition by the GIP II Entities of Chesapeake’s ownership interest in the Partnership (the “GIP Acquisition”), we entered into a letter agreement with Chesapeake regarding the terms on which Chesapeake will provide certain transition services to the Partnership and our general partner following the GIP Acquisition by the GIP II Entities. Among other things, the letter agreement provides for the continuation of our services agreement and secondment agreement with Chesapeake until December 31, 2013. On June 29, 2012, we entered into an amendment to the letter agreement amending certain terms relating to the insurance coverage to be provided under our services agreement and altering the workers’ compensation insurance endorsements for our general partner under our secondment agreement. On December 20, 2012 in connection with the CMO Acquisition, we entered into another amendment to the letter agreement amending certain terms relating primarily to the extension of transition services for technology related services through March 2014 and through June 2014 for certain field communication support services. The secondment agreement and employee transfer agreement each terminated on January 1, 2013.

11

Table of Contents

How We Evaluate Our Operations

Our management relies on certain financial and operational metrics to analyze our performance. These metrics are significant factors in assessing our operating results and profitability and include (i) throughput volumes, (ii) revenues, (iii) operating expenses, (iv) Adjusted EBITDA, (v) distributable cash flow and (vi) segment operating income.

Throughput Volumes

Our management analyzes our performance based on the aggregate amount of throughput volumes on our gathering systems in our operating regions in order to maintain or increase throughput volumes on our gathering systems as a whole. Our success in connecting additional wells is impacted by successful drilling activity on the acreage dedicated to our systems, our ability to secure volumes from new wells drilled on non-dedicated acreage, our ability to attract natural gas and liquids volumes currently gathered by our competitors and our ability to cost-effectively construct new infrastructure to connect new wells.

Revenues

Our revenues are driven primarily by our contractual terms with our customers and the actual volumes of natural gas we gather, treat and compress, and increasingly by the actual volumes of natural gas we process. Our revenues will be supported by the minimum volume commitments contained in our gas gathering agreements with Chesapeake and Total in the case of our Barnett Shale and Chesapeake in the case of our Haynesville Shale as well as fee redetermination and cost of service provisions in our other regions. We contract with producers to gather natural gas or liquids from individual wells located near our gathering systems. We connect wells to gathering pipelines through which natural gas is compressed and may be delivered to a treating facility, processing plant or an intrastate or interstate pipeline for delivery to market. We treat natural gas and liquids that we gather to the extent necessary to meet required specifications of third-party takeaway pipelines. For the years ended December 31, 2012, 2011 and 2010, Chesapeake accounted for approximately 81 percent, 84 percent and 81 percent, respectively, of the natural gas volumes on our gathering systems and 81 percent, 83 percent and 82 percent, respectively, of our revenues. Across all operating regions, we earned approximately 75.3 percent of our fees from Chesapeake and 24.7 percent from other producer customers for the year ended December 31, 2012.

Our revenues are also impacted by other aspects of our contractual agreements, including rate redetermination, cost of service and other contractual provisions and our management constantly evaluates capital spending and its impact on future revenue generation.

Operating Expenses

Our management seeks to maximize the profitability of our operations by minimizing operating expenses without compromising environmental protection and employee safety. Operating expenses are comprised primarily of field operating costs (which include labor, treating and chemicals, and measurements services among other items), compression expense, ad valorem and taxes and other operating costs, some of which are independent of the volumes that flow through our systems but fluctuate depending on the scale of our operations during a specific period.

Adjusted EBITDA and Distributable Cash Flow

We define Adjusted EBITDA as net income (loss) before income tax expense (benefit), interest expense, depreciation and amortization expense and certain other items management believes effect the comparability of operating results.

We define distributable cash flow as Adjusted EBITDA, plus interest income, less cash paid for interest expense, maintenance capital expenditures and income taxes. Distributable cash flow does not reflect changes in working capital balances. Distributable cash flow and Adjusted EBITDA are not presentations made in accordance with generally accepted accounting principles (“GAAP”).

We did not utilize a distributable cash flow measure prior to becoming a publicly traded partnership in 2010 and, as such, did not differentiate between maintenance and capital expenditures prior to 2010 and do not report distributable cash flow for periods prior to 2010.

12

Table of Contents

Adjusted EBITDA and distributable cash flow are non-GAAP supplemental financial measures that management and external users of our consolidated financial statements, such as industry analysts, investors, lenders and rating agencies, may use to assess:

| • | our operating performance as compared to other publicly traded partnerships in the midstream energy industry, without regard to historical cost basis, or in the case of Adjusted EBITDA, financing methods; |

| • | our ability to incur and service debt and fund capital expenditures; |

| • | the ability of our assets to generate sufficient cash flow to make distributions to our unitholders; and |

| • | the viability of acquisitions and other capital expenditure projects and the returns on investment of various investment opportunities. |

Segment Operating Income

Prior to the CMO Acquisition, our operations were organized into a single business segment. As a result of the CMO Acquisition, we added assets in three new operating regions. Effective January 1, 2013, our chief operating decision maker began to analyze and make operating decisions based on geographic segments. Our operations are divided into eight operating segments: Barnett Shale, Eagle Ford Shale, Haynesville Shale, Marcellus Shale, Niobrara Shale, Utica Shale, Mid-Continent region and Corporate.

Reconciliation to GAAP measures

We believe that the presentation of Adjusted EBITDA and distributable cash flow provides useful information to investors in assessing our financial condition and results of operations. Adjusted EBITDA and distributable cash flow are presented because they are helpful to management, industry analysts, investors, lenders and rating agencies and may be used to assess the financial performance and operating results of our fundamental business activities. The GAAP measures most directly comparable to Adjusted EBITDA and distributable cash flow are net income and net cash provided by operating activities. Our non-GAAP financial measures of Adjusted EBITDA and distributable cash flow should not be considered as an alternative to GAAP net income or net cash provided by operating activities. Each of Adjusted EBITDA and distributable cash flow has important limitations as an analytical tool because it excludes some but not all items that affect net income and net cash provided by operating activities. You should not consider either Adjusted EBITDA or distributable cash flow in isolation or as a substitute for analysis of our results as reported under GAAP. Because Adjusted EBITDA and distributable cash flow may be defined differently by other companies in our industry, our definitions of Adjusted EBITDA and distributable cash flow may not be comparable to similarly titled measures of other companies, thereby diminishing their utility.

The following table presents a reconciliation of the non-GAAP financial measures of Adjusted EBITDA and distributable cash flow to the GAAP financial measures of net income and net cash provided by operating activities:

| Year Ended December 31, 2012 | Year Ended December 31, 2011 | Year Ended December 31, 2010 | ||||||||||

| ($ in thousands) | ||||||||||||

Reconciliation of Adjusted EBITDA and Distributable cash flow to net income: | ||||||||||||

Net income attributable to Access Midstream Partners, L.P. | $ | 178,455 | $ | 194,337 | $ | 195,227 | ||||||

Interest expense | 64,739 | 14,884 | 7,426 | |||||||||

Income tax expense | 3,214 | 3,289 | 2,431 | |||||||||

Depreciation and amortization expense | 165,517 | 136,169 | 88,601 | |||||||||

Other | (820 | ) | 739 | 285 | ||||||||

Income from unconsolidated affiliates | (67,542 | ) | (433 | ) | — | |||||||

EBITDA from unconsolidated affiliates | 116,887 | 488 | — | |||||||||

Acquisition transaction costs | 17,432 | — | — | |||||||||

|

|

|

|

|

| |||||||

Adjusted EBITDA | $ | 477,882 | $ | 349,473 | $ | 293,970 | ||||||

|

|

|

|

|

| |||||||

Maintenance capital expenditures | (75,184 | ) | (74,000 | ) | (70,000 | ) | ||||||

Cash portion of interest expense | (59,411 | ) | (10,224 | ) | (2,550 | ) | ||||||

Income tax expense | (3,214 | ) | (3,289 | ) | (2,431 | ) | ||||||

|

|

|

|

|

| |||||||

Distributable cash flow | $ | 340,073 | $ | 261,960 | $ | 218,989 | ||||||

|

|

|

|

|

| |||||||

13

Table of Contents

| Year Ended December 31, 2012 | Year Ended December 31, 2011 | Year Ended December 31, 2010 | ||||||||||

| ($ in thousands) | ||||||||||||

Reconciliation of Adjusted EBITDA and Distributable cash flow to net cash provided by operating activities: | ||||||||||||

Net cash provided by operating activities | $ | 318,130 | $ | 399,016 | $ | 317,091 | ||||||

Changes in assets and liabilities | (33,472 | ) | (62,457 | ) | (28,002 | ) | ||||||

Interest expense | 64,739 | 14,884 | 7,426 | |||||||||

Current income tax expense | 3,214 | 3,289 | 2,431 | |||||||||

Other non-cash items | (9,048 | ) | (5,747 | ) | (4,976 | ) | ||||||

Acquisition transaction costs | 17,432 | — | — | |||||||||

EBITDA from unconsolidated affiliates | 116,887 | 488 | — | |||||||||

|

|

|

|

|

| |||||||

Adjusted EBITDA | $ | 477,882 | $ | 349,473 | $ | 293,970 | ||||||

|

|

|

|

|

| |||||||

Maintenance capital expenditures | (75,184 | ) | (74,000 | ) | (70,000 | ) | ||||||

Cash portion of interest expense | (59,411 | ) | (10,224 | ) | (2,550 | ) | ||||||

Income tax expense | (3,214 | ) | (3,289 | ) | (2,431 | ) | ||||||

|

|

|

|

|

| |||||||

Distributable cash flow | $ | 340,073 | 261,960 | 218,989 | ||||||||

|

|

|

|

|

| |||||||

Results of Operations

We have provided a detailed comparison for the years ended December 31, 2012, 2011 and 2010 in the chart and discussion below. The following table and discussion present a summary of our financial results of operations for the periods described above:

| Year Ended December 31, 2012 | Year Ended December 31, 2011 | Year Ended December 31, 2010 | ||||||||||

| ($ in thousands, except per unit data) | ||||||||||||

Revenues, including revenue from Affiliates(1) | $ | 608,447 | $ | 565,929 | $ | 459,153 | ||||||

Operating expenses, including expenses from affiliates | 197,639 | 176,851 | 133,293 | |||||||||

Depreciation and amortization expense | 165,517 | 136,169 | 88,601 | |||||||||

General and administrative expense, including expenses from affiliates | 67,579 | 40,380 | 31,992 | |||||||||

Other operating (income) expense | (766 | ) | 739 | 285 | ||||||||

|

|

|

|

|

| |||||||

Total operating expenses | 429,969 | 354,139 | 254,171 | |||||||||

|

|

|

|

|

| |||||||

Operating income | 178,478 | 211,790 | 204,982 | |||||||||

Income from unconsolidated affiliates | 67,542 | 433 | — | |||||||||

Interest expense | (64,739 | ) | (14,884 | ) | (7,426 | ) | ||||||

Other income | 320 | 287 | 102 | |||||||||

|

|

|

|

|

| |||||||

Income before income tax expense | 181,601 | 197,626 | 197,658 | |||||||||

Income tax expense | 3,214 | 3,289 | 2,431 | |||||||||

|

|

|

|

|

| |||||||

Net income | 178,387 | 194,337 | 195,227 | |||||||||

Net loss attributable to noncontrolling interest | (68 | ) | — | — | ||||||||

|

|

|

|

|

| |||||||

Net income attributable to Access Midstream Partners, L.P. | $ | 178,455 | $ | 194,337 | $ | 195,227 | ||||||

|

|

|

|

|

| |||||||

Operating Data: | ||||||||||||

Throughput, Bcf/d(2) | 2.819 | 2.176 | 1.595 | |||||||||

| (1) | If either Chesapeake or Total does not meet its minimum volume commitment to the Partnership in the Barnett Shale region or Chesapeake does not meet its minimum volume commitment in the Haynesville Shale region under the applicable gas gathering agreement for specified annual periods, Chesapeake or Total is obligated to pay the Partnership a fee equal to the applicable fee for each Mcf by which the applicable party’s minimum volume commitment for the year exceeds the actual volumes gathered on the Partnership’s systems. The Partnership recognizes any associated revenue in the fourth quarter. For the years ended December 31, 2011 and 2010, we recognized revenue related to volume shortfall of $17.4 million and $56.8 million, respectively, because throughput in our Barnett Shale region was below contractual minimum volume commitment levels. |

| (2) | Excludes production from CMO assets acquired on December 20, 2012. |

Segment Reporting

We present information in this Management’s Discussion and Analysis of Financial Condition and Results of Operations by segment. The segment information appearing in Note 14 of the accompanying Notes to the Condensed Consolidated Financial Statements is presented on a basis consistent with our internal management reporting. Beginning on January 1, 2013, we conduct our operations in the following segments: Barnett Shale, Eagle Ford Shale, Haynesville Shale, Marcellus Shale, Niobrara Shale, Utica Shale, Mid-Continent region and Corporate.

14

Table of Contents

Year Ended December 31, 2012 vs. Year Ended December 31, 2011

The following tables reflect the Partnership’s revenues, throughput, operating expenses and operating expenses per Mcf of throughput by segment for the years ended December 31, 2012 and 2011 (please note that revenue, throughput and operating expenses related to our equity investments (primarily in the Marcellus Shale) are excluded from the tables below as the financial results for our equity investments are reported separately. Please read “Income from Unconsolidated Affiliates” in this Results of Operations section of Management’s Discussion and Analysis of Financial Condition and Results of Operations):

| Years Ended December 31, | ||||||||||||||

| 2012 | 2011 | % Change(1) | ||||||||||||

| (In thousands, except percentages and throughput data) | ||||||||||||||

Revenue: | ||||||||||||||

Barnett Shale | $ | 395,467 | $ | 361,843 | 9.3 | % | ||||||||

Eagle Ford Shale(2) | 7,232 | — | N.M. | |||||||||||

Haynesville Shale(2) | 68,184 | 93,107 | (26.8 | ) | ||||||||||

Marcellus Shale(2) | 783 | — | N.M. | |||||||||||

Niobrara Shale(2) | 116 | — | N.M. | |||||||||||

Utica Shale(2) | 353 | — | N.M. | |||||||||||

Mid-Continent | 136,312 | 110,979 | 22.8 | |||||||||||

|

|

|

| |||||||||||

| $ | 608,447 | $ | 565,929 | 7.5 | % | |||||||||

|

|

|

| |||||||||||

Throughput (Bcf): | ||||||||||||||

Barnett Shale | 437.3 | 395.4 | 10.6 | % | ||||||||||

Eagle Ford Shale | 2.2 | — | N.M. | |||||||||||

Haynesville Shale | 138.4 | 197.5 | (30.0 | ) | ||||||||||

Marcellus Shale | 0.3 | — | N.M. | |||||||||||

Niobrara Shale | 0.1 | — | N.M. | |||||||||||

Utica Shale | 0.8 | — | N.M. | |||||||||||

Mid-Continent | 206.5 | 201.4 | 2.5 | |||||||||||

|

|

|

| |||||||||||

| 785.6 | 794.3 | (1.1 | )% | |||||||||||

|

|

|

| |||||||||||

| (1) | N.M.—not meaningful |

| (2) | Reflective of revenue after completion of the CMO Acquisition on December 20, 2012. |

| Years Ended December 31, | ||||||||||||

| 2012 | 2011 | % Change(1) | ||||||||||

| (In thousands, except percentages and per Mcf data) | ||||||||||||

Operating Expenses: | ||||||||||||

Barnett Shale | $ | 101,703 | $ | 94,009 | 8.2 | % | ||||||

Eagle Ford Shale(2) | 1,604 | — | N.M. | |||||||||

Haynesville Shale(2) | 15,642 | 18,057 | (13.4 | ) | ||||||||

Marcellus Shale(2) | 188 | — | N.M. | |||||||||

Niobrara Shale(2) | 85 | — | N.M. | |||||||||

Utica Shale(2) | 159 | — | N.M. | |||||||||

Mid-Continent | 52,979 | 47,749 | 11.0 | |||||||||

Corporate | 25,279 | 17,036 | 48.4 | |||||||||

|

|

|

| |||||||||

| $ | 197,639 | $ | 176,851 | 11.8 | % | |||||||

|

|

|

| |||||||||

Expenses ($ per Mcf): | ||||||||||||

Barnett Shale | $ | 0.23 | $ | 0.24 | (4.2 | )% | ||||||

Eagle Ford Shale | 0.73 | — | N.M. | |||||||||

Haynesville Shale | 0.11 | 0.09 | 22.2 | |||||||||

Marcellus Shale | 0.63 | — | N.M. | |||||||||

Niobrara Shale | 0.85 | — | N.M. | |||||||||

Utica Shale | 0.20 | — | N.M. | |||||||||

Mid-Continent | 0.26 | 0.24 | 8.3 | |||||||||

|

|

|

| |||||||||

| $ | 0.25 | $ | 0.22 | 13.6 | % | |||||||

|

|

|

| |||||||||

| (1) | N.M.—not meaningful |

| (2) | Reflective of operating expenses after completion of the CMO Acquisition on December 20, 2012. |

15

Table of Contents

Barnett Shale

Revenues. For the years ended December 31, 2012 and 2011, revenues were $395.5 million and $361.8 million, respectively. The increase was primarily the result of increased throughput of 10.6 percent due to additional wells connected in 2011 and the first half of 2012. Additionally, the Barnett Shale fees increased five cents per mcf effective July 1, 2012, as a result of fee redetermination.

We have contractual minimum volume commitments from Chesapeake and Total in the Barnett Shale. Throughput in the Barnett Shale during the current year was above the minimum volume commitment level. Because throughput in the Barnett Shale during 2011 was below contractual minimum volume commitment levels, we recognized revenue related to the volume shortfall of $17.4 million for the year ended December 31, 2011.

Operating Expenses. For the years ended December 31, 2012 and 2011, operating expenses were $101.7 million and $94.0 million, respectively. As throughput increased, operating expenses have increased in order to support the additional throughput. Operating expenses per Mcf decreased slightly from 2011 to 2012.

Depreciation and Amortization Expenses. For the years ended December 31, 2012 and 2011, depreciation expenses were $93.3 million and $77.0 million. The increase was due to capital expenditures made in this region during 2011 and 2012.

Eagle Ford Shale

We acquired the Eagle Ford Shale assets in December 2012. For the twelve-day period from closing the CMO Acquisition on December 20, 2012 through December 31, 2012, revenues and operating expenses were $7.2 million and $1.6 million, respectively.

Haynesville Shale

Revenues. For the years ended December 31, 2012 and 2011, revenues were $68.2 million and $93.1 million, respectively. Revenues were down 26.8 percent due to a volume decrease on the Springridge gathering system, offset partially by a 2.5 percent annual fee escalation and additional production from the Mansfield gathering system acquired in December 2012. Additionally, we have contractual minimum volume commitment from Chesapeake in the Haynesville Shale. Throughput during the current year was above the minimum volume commitment levels.

Operating Expenses. For the years ended December 31, 2012 and 2011, operating expenses were $15.6 million and $18.1 million, respectively. We have reduced operating expense in the Haynesville Shale in response to the reduction in throughput in this region; however, in the first half of 2012 we had fixed costs in this area which caused the expense per Mcf to increase temporarily.

Marcellus Shale

Revenues and expenses in the Marcellus Shale reflect only the results of the Marcellus gathering systems acquired in December 2012. For the twelve-day period from closing the CMO Acquisition on December 20, 2012 through December 31, 2012, revenues and expenses were $0.8 million and $0.2 million, respectively. The majority of our assets in the Marcellus Shale are accounted for as equity investments and included in Income from Unconsolidated Affiliates. See further discussion below under “Income from Unconsolidated Affiliates” in this section of Marcellus Shale results of operations.

16

Table of Contents

Income from unconsolidated affiliates.On December 29, 2011, we acquired all of the issued and outstanding common units of Appalachia Midstream, which owns an approximate average 47 percent interest in 10 gas gathering systems in the Marcellus Shale in Pennsylvania and West Virginia. The remaining 53 percent interest in these assets are owned primarily by Statoil, Anadarko, Epsilon and Mitsui. Income from unconsolidated affiliates was $67.6 million and $0.4 million reflecting activity for the year ended December 31, 2012 and the last two days of December 2011, respectively. The following table summarizes the results of the Appalachia Midstream assets (net to our interest) for the year ended December 31, 2012.

| Year Ended December 31, 2012 | ||||

Revenues ($ in thousands) | $ | 140,541 | ||

Throughput (Bcf) | 256.7 | |||

Operating expenses ($ in thousands) | $ | 15,782 | ||

Expenses ($ per Mcf) | 0.06 | |||

Niobrara Shale

We acquired 50 percent of the Niobrara Shale assets in December 2012. Because we operate the assets and have contractual discretion to make operating decisions for the assets, we are deemed to control the assets and thus, we consolidated 100 percent of the assets and results of operation in our financial results. We present the noncontrolling interest for these assets in Noncontrolling Interests on the condensed consolidated balance sheet and in Net Income Attributable to Noncontrolling Interests on the condensed consolidated statement of operations. For the twelve-day period from closing the CMO Acquisition on December 20, 2012 through December 31, 2012, revenues and operating expenses in the Niobrara Shale were $0.1 million and $0.1 million, respectively.

Utica Shale

In the CMO Acquisition, we acquired a 100 percent ownership interest in four natural gas gathering systems, a 66 percent operating interest in the Cardinal Joint Venture and a 49 percent interest in the UEO Joint Venture. Because we operate the four wholly-owned natural gas gathering systems and Cardinal Joint Venture and have contractual discretion to make operating decisions for the Cardinal Joint Venture, we are deemed to control the assets and thus, we consolidated 100 percent of the assets and results of operations in our financial results and reflect the ownership of the other interest owners through a noncontrolling interest in the income and equity of the investment. The UEO Joint Venture is accounted for as an equity investment because the power to direct the activities which are most significant to the UEO Joint Venture’s economic performance is shared between us and the other equity holders. For the twelve-day period from closing the CMO Acquisition on December 20, 2012 through December 31, 2012, revenues and operating expenses in the Utica Shale were $0.4 million and $0.2 million, respectively.

Mid-Continent

Revenues. For the years ended December 31, 2012 and 2011, revenues were $136.3 million and $111.0 million, respectively. This increase was due to increased throughput of 2.5 percent as drilling activity increased in this liquids-rich region, a 2.5 percent annual fee escalation and a 15 percent fee increase due to annual contractual fee redetermination.

Operating Expenses. For the years ended December 31, 2012 and 2011, operating expenses were $53.0 million and $47.7 million, respectively. Operating expenses increased due to added compression to support additional throughput.

Corporate

Operating Expenses. For the years ended December 31, 2012 and 2011, operating expenses were $25.3 million and $17.0 million, respectively. The increase in operating expenses resulted from additional technical resources to support the assets acquired in 2011.

General and Administrative Expense.For the years ended December 31, 2012 and 2011, general and administrative expenses were $67.6 million and $40.4 million, respectively, representing an increase of 67.3 percent. This increase is primarily attributable to additional overhead expenses resulting from the increased scale of the Partnership’s operations, additional expense from equity-based, long-term incentive compensation influenced by the recent increase in the Partnership’s unit price, one-time transition costs as the Partnership develops an independent back office infrastructure and $15.0 million of transaction costs related to the CMO Acquisition.

17

Table of Contents

Interest Expense.Interest expense for the year ended December 31, 2012 was $64.7 million, which was net of $14.6 million of capitalized interest. Interest expense was $14.9 million for the year ended December 31, 2011, which was net of $9.5 million of capitalized interest. The increase is related to interest expense on the $750 million of senior notes issued in January 2012 and $1.4 billion of senior notes issued in December 2012. We incurred interest expenses on borrowings under our revolving credit facility and our senior notes issued in April 2011. Interest expense also includes commitment fees on the unused portion of our credit facility and amortization of debt issuance costs.

Income Tax Expense.Income tax expense for the years ended December 31, 2012 and 2011 was $3.2 million and $3.3 million, respectively, and was attributable to franchise taxes in the state of Texas. The Partnership and its subsidiaries are pass-through entities for federal income tax purposes. For these entities, all income, expenses, gains, losses and tax credits generated flow through to their owners and, accordingly, do not result in a provision for income taxes in the financial statements, other than Texas Franchise Tax.

Year Ended December 31, 2011 vs. Year Ended December 31, 2010

The following tables reflect the Partnership’s revenues, throughput, operating expenses and operating expenses per Mcf of throughput by segment for the years ended December 31, 2011 and 2010 (please note that revenue, throughput and operating expenses related to our equity investments (primarily in the Marcellus Shale) are excluded from the tables below as the financial results for our equity investments are reported separately. Please read “Income from Unconsolidated Affiliates” in this Results of Operations section of Management’s Discussion and Analysis of Financial Condition and Results of Operations):

| Years Ended December 31, | ||||||||||||

| 2011 | 2010 | % Change(1) | ||||||||||

| (In thousands, except percentages and throughput data) | ||||||||||||

Revenue: | ||||||||||||

Barnett Shale | $ | 361,843 | $ | 358,821 | 0.8 | % | ||||||

Haynesville Shale – Springridge gathering system | 93,107 | 2,082 | N.M. | |||||||||

Mid-Continent | 110,979 | 98,250 | 13.0 | |||||||||

|

|

|

| |||||||||

| $ | 565,929 | $ | 459,153 | 23.3 | % | |||||||

|

|

|

| |||||||||

Throughput (Bcf): | ||||||||||||

Barnett Shale | 395.4 | 374.0 | 5.7 | % | ||||||||

Haynesville Shale – Springridge gathering system | 197.5 | 4.9 | N.M. | |||||||||

Mid-Continent | 201.4 | 203.4 | (1.0 | ) | ||||||||

|

|

|

| |||||||||

| 794.3 | 582.3 | 36.4 | % | |||||||||

|

|

|

| |||||||||

| (1) | N.M.—not meaningful |

| Years Ended December 31, | ||||||||||||

| 2011 | 2010 | % Change(1) | ||||||||||

| (In thousands, except percentages and per Mcf data) | ||||||||||||

Operating Expenses: | ||||||||||||

Barnett Shale | $ | 94,009 | $ | 81,304 | 15.6 | % | ||||||

Haynesville Shale – Springridge gathering system | 18,057 | 508 | N.M. | |||||||||

Mid-Continent | 47,749 | 42,521 | 12.3 | |||||||||

Corporate | 17,036 | 8,960 | 90.1 | |||||||||

|

|

|

| |||||||||

| $ | 176,851 | $ | 133,293 | 32.7 | % | |||||||

|

|

|

| |||||||||

Expenses ($ per Mcf): | ||||||||||||

Barnett Shale | $ | 0.24 | $ | 0.22 | 9.1 | % | ||||||

Haynesville Shale – Springridge gathering system | 0.09 | 0.10 | (10.0 | ) | ||||||||

Mid-Continent | 0.24 | 0.21 | 14.3 | |||||||||

|

|

|

| |||||||||

| $ | 0.22 | $ | 0.23 | (4.3 | )% | |||||||

|

|

|

| |||||||||

| (1) | N.M.—not meaningful |

Barnett

Revenues. For the years ended December 31, 2011 and 2010, Barnett Shale throughput was 1.1 Bcf per day and 1.0 Bcf per day, respectively. Revenues were $361.8 million and $358.8 million, respectively, an increase of 0.8 percent. Gathering rates increased two percent as a result of annual contractual rate increases. We also benefited from added compression revenues during 2011.

18

Table of Contents

Because throughput in the Barnett Shale during 2011 and 2010 was below contractual minimum volume commitment levels, we recognized revenue related to volume shortfall of $17.4 million and $56.8 million for the years ended December 31, 2011 and 2010, respectively. The amount recognized in 2010 included a one-time carry forward from 2009 of $17.2 million. The minimum volume commitment is measured annually and recognized in the fourth quarter of each year.

Operating Expenses. Operating expenses were $0.24 per Mcf for the year ended December 31, 2011 compared to $0.22 per Mcf for the year ended December 31, 2010. The increase in the Barnett Shale region was due to additional compression expense to support increased throughput. We have also incurred increased expenses for additional field personnel and other personnel related costs resulting from Partnership growth.

Depreciation and Amortization Expense. For the years ended December 31, 2011 and 2010, depreciation and amortization expense was $77.0 million and 62.6 million, respectively. The increase in depreciation and amortization is a result of capital expenditures made in 2010 and early 2011.

Haynesville Shale

Revenues. For the years ended December 31, 2011 and 2010, revenues totaled $93.1 million and $2.1 million, respectively. The increase in our revenue was due to the acquisition of the Springridge gathering system at the end of 2010.

Operating Expenses. Operating expenses were $18.1 million for the year ended December 31, 2011 compared to $0.5 million for the year ended December 31, 2010. The increase in operating expenses resulted from the acquisition of the Springridge gathering system at the end of 2010.

Depreciation and Amortization Expense. Depreciation and amortization expense for the year ended December 31, 2011 and 2010 was $29.1 million from $0.4 million, respectively. The increase in depreciation and amortization is a result of the acquisition of the Springridge gathering system at the end of 2010.

Marcellus Shale