Use these links to rapidly review the document

TABLE OF CONTENTS

GIBSON ENERGY HOLDING ULC

Table of Contents

As filed with the Securities and Exchange Commission on February 12, 2010

Registration No. 333-

FORM F-4

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

| | |

Gibson Energy ULC

(Exact name of registrant

as specified in its charter) | | GEP Midstream Finance Corp.

(Exact name of registrant guarantor

as specified in its charter) |

| | | | |

Alberta

(State or other jurisdiction

of incorporation) | | 1389

(Primary Standard Industrial

Classification Code Number) | | 98-0615355

(I.R.S. Employer

Identification Number) |

SEE TABLE OF ADDITIONAL REGISTRANT GUARANTORS

1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000

(Address, including zip code, and telephone number, including area code, of registrants' principal executive offices)

C T Corporation System

111 Eighth Avenue

New York, NY 10011

Tel: +1. 212.894.8641

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With a copy to:

Marc D. Jaffe, Esq.

Patrick H. Shannon, Esq.

Latham & Watkins LLP

885 Third Avenue

New York, NY 10022-4834

Tel: +1.212.906.1200

Approximate date of commencement of proposed exchange offer:

As soon as practicable after this Registration Statement is declared effective.

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act of 1933, as amended (the "Securities Act"), check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer). o

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer). o

Calculation of Registration Fee

| | | | | | | | |

| | | | | | | | |

| |

Title of Each Class of Securities

to be Registered

| | Amount to be

Registered

| | Proposed Maximum

Offering Price Per

Note

| | Proposed Maximum

Aggregate Offering

Price(2)

| | Amount of

Registration Fee

|

|---|

| |

11.75% First Lien Senior Secured Notes due 2014 | | U.S.$560,000,000 | | 100% | | U.S.$560,000,000 | | $39,928(2) |

| |

Guarantees of 11.75% First Lien Senior Secured Notes due 2014(3) | | N/A(4) | | (4) | | (4) | | (4) |

| |

10.00% Senior Notes due 2018 | | U.S.$200,000,000 | | 100% | | U.S.$200,000,000 | | 14,260(2) |

| |

Guarantees of 10.00% Senior Notes due 2018(3) | | N/A(4) | | (4) | | (4) | | (4) |

| |

Total | | U.S.$760,000,000 | | 100% | | U.S.$760,000,000 | | $54,188 |

|

- (1)

- Estimated solely for the purpose of calculating the registration fee under Rule 457(f) of the Securities Act.

- (2)

- The registration fee for the securities offered hereby was calculated under Rule 457(f)(2) of the Securities Act.

- (3)

- See inside facing page for additional guarantors.

- (4)

- Pursuant to Rule 457(n) under the Securities Act, no separate filing fee is required for the guarantees.

The Registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

TABLE OF ADDITIONAL REGISTRANT GUARANTORS

| | | | | | | | | |

Exact Name as

Specified in its Charter | | State or Other

Jurisdiction of

Incorporation or

Organization | | Primary

Standard

Industrial

Classification

Number | | I.R.S. Employer

Identification

Number | | Address, Including Zip Code and

Telephone Number,

Including Area Code, of Principal

Executive Offices |

|---|

Gibson Energy (U.S.) Inc. | | Delaware | | | 1389 | | 71-1012012 | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Link Petroleum, Inc. | | Washington | | |

1389 | | 98-0156853 | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Gibson Energy Holding ULC | | Alberta | | |

1389 | | 98-0630747 | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Moose Jaw Refinery Partnership | | Alberta | | |

1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Moose Jaw Refinery ULC | | Alberta | | |

1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Canwest Propane Partnership | | Alberta | | |

1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Canwest Propane ULC | | Alberta | | |

1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

MP Energy Partnership | | Alberta | | |

1389 | | 98-0569218 | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

MP Energy ULC | | Alberta | | |

1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Gibson Energy Partnership | | Alberta | | |

1389 | | 98-0615168 | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Table of Contents

| | | | | | | | | |

Exact Name as

Specified in its Charter | | State or Other

Jurisdiction of

Incorporation or

Organization | | Primary

Standard

Industrial

Classification

Number | | I.R.S. Employer

Identification

Number | | Address, Including Zip Code and

Telephone Number,

Including Area Code, of Principal

Executive Offices |

|---|

GEP ULC | | Alberta | | | 1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Link Petroleum Services Ltd. | | British Columbia | | |

1389 | | 98-0151585 | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Chief Hauling Contractors ULC | | Alberta | | |

1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Gibson GCC Inc. | | Alberta | | |

1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Battle River Terminal LP | | Alberta | | |

1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Battle River Terminal GP Inc. | | Alberta | | |

1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Bridge Creek Trucking Ltd. | | Saskatchewan | | |

1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Johnstone Tank Trucking Ltd. | | Saskatchewan | | |

1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Aarcam Propane & Construction Heat Ltd. | | Alberta | | |

1389 | | Not applicable | | 1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Tel: +1.403.206.4000 |

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED FEBRUARY 12, 2010

PRELIMINARY PROSPECTUS

Gibson Energy ULC

GEP Midstream Finance Corp.

OFFER TO EXCHANGE

Up to U.S.$560,000,000 aggregate principal amount of 11.75% First Lien Senior Secured Notes due 2014 issued by Gibson Energy ULC and GEP Midstream Finance Corp., as co-issuer, which have been registered under the Securities Act of 1933, for any and all outstanding 11.75% First Lien Senior Secured Notes due 2014 (CUSIP Nos. 374826AA3 and C39288AA0) issued by Gibson Energy ULC and GEP Midstream Finance Corp., as co-issuer.

Up to U.S.$200,000,000 aggregate principal amount of 10.00% Senior Notes due 2018 issued by Gibson Energy ULC and GEP Midstream Finance Corp., as co-issuer, which have been registered under the Securities Act of 1933, for any and all outstanding 10.00% Senior Notes due 2018 (CUSIP Nos. 374826AB1 and C39288AB8) issued by Gibson Energy ULC and GEP Midstream Finance Corp., as co-issuer.

The exchange notes will be fully and unconditionally guaranteed on an unsecured basis by our parent company, Gibson Energy Holding ULC, and certain of our domestic and foreign subsidiaries.

We are conducting the exchange offer in order to provide you with an opportunity to exchange your unregistered notes for freely tradable notes that have been registered under the Securities Act.

Terms of the Exchange Offer:

- •

- We will exchange all initial notes that are validly tendered and not validly withdrawn for an equal principal amount of exchange notes that are freely tradable.

- •

- You may withdraw tenders of initial notes at any time prior to the expiration date of the exchange offer.

- •

- The exchange offer expires at 5:00 p.m., New York City time, on , 2010, unless extended.

- •

- We will not receive any proceeds from the exchange offer.

- •

- We believe that the exchange of initial notes for exchange notes in the exchange offer will not be a taxable event for U.S. federal income tax purposes. Non-residents of Canada will generally not be subject to Canadian federal income tax on a disposition of the initial notes. Accordingly, even if the exchange of the initial notes for exchange notes were a taxable event, Canadian federal income tax would not generally apply. See "Certain Canadian and United States Tax Considerations," which describes when a non-resident will be exempt from Canadian federal income tax with respect to the notes.

- •

- The terms of the exchange notes are substantially identical to the unregistered notes, except that the exchange notes have been registered under the Securities Act, and transfer restrictions and registration rights relating to the unregistered notes do not apply to the exchange notes.

All untendered initial notes will continue to be subject to the restrictions on transfer set forth in the initial notes and in the applicable indentures. In general, the initial notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, we do not currently anticipate that we will register the initial notes under the Securities Act.

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The Letter of Transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an "underwriter" within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for the initial notes where such initial notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, starting on the expiration date of the exchange offer and ending on the close of business one year after the expiration date, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See "Plan of Distribution."

See "Risk Factors" beginning on page 25 for a discussion of certain risks that you should consider before participating in the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the exchange notes to be issued in the exchange offer or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. If you receive any other information, you should not rely on it. We are not making an offer of these securities in any state where the offer is not permitted.

The date of this prospectus is , 2010.

Table of Contents

TABLE OF CONTENTS

| | |

IMPORTANT INFORMATION ABOUT THIS PROSPECTUS | | i |

ENFORCEMENT OF FOREIGN JUDGMENTS AND SERVICE OF PROCESS | |

i |

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS | |

i |

PRESENTATION OF INFORMATION | |

ii |

CURRENCY PRESENTATION AND EXCHANGE RATE INFORMATION | |

iv |

MARKET AND INDUSTRY DATA | |

iv |

WHERE YOU CAN OBTAIN MORE INFORMATION | |

v |

SUMMARY | |

1 |

RISK FACTORS | |

25 |

USE OF PROCEEDS | |

50 |

CAPITALIZATION | |

51 |

THE TRANSACTIONS | |

52 |

UNAUDITED PRO FORMA CONDENSED CONSOLIDATED FINANCIAL INFORMATION | |

54 |

SELECTED HISTORICAL CONSOLIDATED FINANCIAL DATA | |

63 |

RATIO OF EARNINGS TO FIXED CHARGES | |

65 |

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | |

66 |

INDUSTRY | |

110 |

BUSINESS | |

112 |

REGULATION | |

127 |

PRINCIPAL SHAREHOLDERS | |

135 |

MANAGEMENT | |

136 |

CERTAIN RELATIONSHIPS AND RELATED-PARTY TRANSACTIONS | |

142 |

DESCRIPTION OF CERTAIN INDEBTEDNESS | |

144 |

THE EXCHANGE OFFER | |

146 |

DESCRIPTION OF THE SENIOR SECURED NOTES | |

156 |

DESCRIPTION OF THE SENIOR NOTES | |

222 |

BOOK-ENTRY, DELIVERY AND FORM OF SECURITIES | |

276 |

CERTAIN CANADIAN AND UNITED STATES TAX CONSIDERATIONS | |

278 |

ERISA CONSIDERATIONS | |

284 |

PLAN OF DISTRIBUTION | |

285 |

LEGAL MATTERS | |

286 |

EXPERTS | |

286 |

GLOSSARY OF TERMS | |

A-1 |

INDEX TO THE CONSOLIDATED FINANCIAL STATEMENTS | |

F-1 |

Table of Contents

We have not authorized any dealer, salesperson or other person to give any information or represent anything to you other than the information contained in this prospectus. You must not rely on unauthorized information or representations.

This prospectus does not offer to sell nor ask for offers to buy any of the securities in any jurisdiction where it is unlawful, where the person making the offer is not qualified to do so, or to any person who cannot legally be offered the securities. The information in this prospectus is current only as of the date on its cover, and may change after that date.

Following the date of this prospectus, we will be subject to reporting obligations and any filings we make will be available via the website of the United States Securities and Exchange Commission, or SEC, atwww.sec.gov. You can also obtain any filed documents regarding us without charge by written or oral request to:

Gibson Energy ULC

1700, 440-2nd Ave S.W.

Calgary, Alberta T2P 5E9

Canada

Attn. Mr. T. Murray Carey

General Counsel

Tel: +1.403.206.4000

Please note that copies of documents provided to you will not include exhibits.

In order to receive timely delivery of requested documents in advance of the expiration date of the exchange offer, you should make your request no later than , 2010, which is five business days before you must make a decision regarding the exchange offer.

Table of Contents

IMPORTANT INFORMATION ABOUT THIS PROSPECTUS

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell or a solicitation of an offer to buy any of these securities to any person in any jurisdiction where it is unlawful to make this type of an offer or solicitation.

ENFORCEMENT OF FOREIGN JUDGMENTS AND SERVICE OF PROCESS

We and most of the guarantors are organized under the laws of Canadian jurisdictions. The majority of our and the guarantors' directors and officers named in this prospectus reside outside the United States. Because most of these persons may be located outside the United States, it may not be possible for you to effect service of process within the United States on these persons. Furthermore, it may not be possible for you to enforce against us or them, in the United States, judgments obtained in United States courts, because all or a substantial portion of our assets and the assets of these persons are located outside the United States. We have been advised by Bennett Jones LLP, our Canadian counsel, that there is doubt as to the enforceability, in original actions in Canadian courts, of liabilities based upon the United States federal securities laws and as to the enforceability in Canadian courts of judgments of United States courts obtained in actions based upon the civil liability provisions of the United States federal securities laws. Therefore, it may not be possible to enforce those actions against us or our directors and officers named in this prospectus.

DISCLOSURE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements within the meaning of Section 27A of the Securities Act and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"). You can generally identify forward-looking statements by our use of forward-looking terminology such as "anticipate," "believe," "continue," "could," "estimate," "expect," "intend," "may," "might," "plan," "potential," "predict," "seek," "should," or "will" or the negative thereof or other variations thereon or comparable terminology. In particular, statements about (1) general market conditions, competition and pricing; and (2) our expectations, beliefs, plans, strategies, objectives, prospects, assumptions or future events or performance contained in this prospectus under the headings "Summary," "Risk Factors," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Business" are forward-looking statements.

We have based these forward-looking statements on our current expectations, assumptions, estimates and projections. While we believe these expectations, assumptions, estimates and projections are reasonable, such forward-looking statements are only predictions and involve known and unknown risks and uncertainties, many of which are beyond our control. These and other important factors, including those discussed in this prospectus under the headings "Summary," "Risk Factors," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Business," may cause our actual results, performance or achievements to differ materially from any future results, performance or achievements expressed or implied by these forward-looking statements. Some of the factors that could cause actual results to differ materially from those expressed or implied by the forward-looking statements include:

- •

- certain risks are amplified by the current economic environment;

- •

- potential future acquisitions or investments in other companies may have a negative impact on our business;

- •

- we may not be successful in making acquisitions to grow our truck transportation and propane marketing and distribution segments;

i

Table of Contents

- •

- our marketing activities expose us to price and market risks which could adversely impact our financial condition;

- •

- access to credit from our suppliers could be restricted;

- •

- we may not successfully balance our purchases and sales of natural gas, propane, crude oil and condensate, which would increase our exposure to commodity price risks;

- •

- our financial results depend on the demand for the petroleum products that we transport, store, sell and distribute;

- •

- some of our business segments are dependent on certain major customers, and a loss of one or more major customers could have a material adverse effect on segment profitability;

- •

- our expansion projects may not immediately produce operating cash flows and may exceed our cost estimates;

- •

- we face intense competition in all areas of our business and may not be able to successfully compete with our competitors, which could lead to lower levels of profits and reduce the amount of cash we generate;

- •

- we experience a high level of competition in our propane marketing and distribution segment from other propane retailers and from alternative energy sources and energy efficiency and technological advances;

- •

- our success depends on our ability to retain the current members of our senior management team and other key personnel;

- •

- a material decrease in the production of crude oil for oil fields served by our pipelines and terminals could materially reduce our revenues;

- •

- an impairment in the carrying value of goodwill or other assets could negatively affect our consolidated results of operations; and

- •

- other risks and uncertainties, including those listed under the caption "Risk Factors."

Given these risks and uncertainties, you are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements included in this prospectus are made only as of the date hereof. Readers are cautioned that the foregoing list of risk factors is not exhaustive and that the forward-looking statements contained in this prospectus are expressly qualified by this cautionary statement. We do not undertake and specifically decline any obligation to update any such statements or to publicly announce the results of any revisions to any of such statements to reflect future events or developments.

PRESENTATION OF INFORMATION

Corporate Organization

- •

- The term "issuers" refers to Gibson Energy ULC, an Alberta unlimited liability corporation, and GEP Midstream Finance Corp., an Alberta corporation;

- •

- the term "Parent" refers to Gibson Energy Holding ULC, an Alberta unlimited liability corporation and the parent of the issuers, which is also a guarantor of the notes offered hereby, and its consolidated subsidiaries;

- •

- the terms "Gibson," "the Company," "we," "our," "us," or like terms refer to Gibson Energy Holding ULC and its subsidiaries;

ii

Table of Contents

- •

- the term "Predecessor" refers to Gibson Energy Holdings Inc. for periods prior to the Acquisition on December 12, 2008; and

- •

- the term "Successor" refers to Gibson Energy Holding ULC for periods subsequent to the Acquisition at the close of business on December 12, 2008.

Financial and Other Information

Predecessor results for periods prior to the Acquisition on December 12, 2008 ("Predecessor") have been presented separately from Successor results subsequent to the Acquisition ("Successor"). To facilitate a discussion of certain results of operations across periods, we have combined certain Predecessor results with Successor results for the year ended December 31, 2008. The combined information does not comply with Canadian generally accepted accounting principles ("Canadian GAAP") or accounting principles generally accepted in the United States of America ("U.S. GAAP") and does not include the pro forma effects of the Transactions as if they had occurred on January 1, 2008. For information regarding the pro forma effects of the Transactions, see "Unaudited Pro Forma Condensed Consolidated Financial Information."

The financial statements included in this prospectus are presented in Canadian dollars. In this prospectus, references to $ and "dollars" are to Canadian dollars and references to "U.S.$" and "U.S. dollars" are to United States dollars. See "—Currency Presentation and Exchange Rate Information."

Our consolidated financial statements have been prepared in accordance with Canadian GAAP, which differs in certain respects from U.S. GAAP. For a discussion of the principal differences between Canadian GAAP and U.S. GAAP as they pertain to us, see note 26 to our audited consolidated financial statements and note 18 to our unaudited condensed consolidated financial statements.

This prospectus includes certain financial measures that do not comply with Canadian GAAP or U.S. GAAP, such as EBITDA, Pro Forma EBITDA and Pro Forma Adjusted EBITDA. As used in the prospectus, EBITDA represents net income before deduction of amounts for interest, taxes, depreciation and amortization. Pro Forma Adjusted EBITDA is presented because certain covenants in the indentures governing the notes offered hereby include a ratio based on this measure. Pro Forma Adjusted EBITDA differs from the term "EBITDA" as it is commonly used. Pro Forma Adjusted EBITDA is defined under the indentures as consolidated net income before net interest, taxes, depreciation, amortization and accretion; other non-cash expenses and charges deducted in determining consolidated net income, including movement in the unrealized gains and losses on derivatives used in connection with commodity price risk management activities; stock based compensation; expenses associated with the Hunting employee stock option program and long-term incentive plan that will not recur in post-closing periods; and non-cash inventory writedowns. It also takes into account, among other things, the impact of the Transactions, the Refinancing and the 2010 Offering on our historical financial performance, the impact of realized and unrealized foreign exchange movements in our U.S. dollar denominated long-term debt, certain management fees which will be paid to our Sponsor, the pro forma effect of certain acquisitions that took place subsequent to September 30, 2008 and other adjustments that are considered extraordinary or non-recurring in nature, based on definitions included in the indentures governing our notes. EBITDA, Pro Forma EBITDA and Pro Forma Adjusted EBITDA are not measures of operating performance or liquidity under Canadian GAAP or U.S. GAAP. EBITDA, as used in this prospectus, is not necessarily comparable with similarly titled measures used by other companies. Management believes that EBITDA may be useful for potential purchasers of the notes in assessing our operating performance and as an indicator of our ability to service or incur indebtedness, make capital expenditures and finance working capital requirements. Pro Forma Adjusted EBITDA may not be comparable to such calculations used in debt covenants applicable to other companies. Refer to pages 22, 23 and 24 for a reconciliation of net income to EBITDA, Pro Forma EBITDA and Pro Forma Adjusted EBITDA. The items excluded in determining

iii

Table of Contents

EBITDA are significant in assessing our operating results and liquidity. Therefore, EBITDA should not be considered in isolation or as an alternative to cash from operating activities or other income or cash flow data prepared in accordance with Canadian GAAP or U.S. GAAP. See note 2 under "Summary—Summary Financial Data" and "Unaudited Pro Forma Condensed Consolidated Financial Information."

CURRENCY PRESENTATION AND EXCHANGE RATE INFORMATION

The following chart shows for the period from January 1, 2005 through January 29, 2010, the period end, average, high and low noon buying rates in the City of New York for cable transfers of Canadian dollars as certified for customs purposes by the Federal Reserve Bank of New York expressed as U.S. dollars per $1.00.

| | | | | | | | | | | | | | |

| | U.S. dollars per $1.00 | |

|---|

Period | | High | | Low | | Period

average | | Period

end | |

|---|

2005 | | | 0.8690 | | | 0.7872 | | | 0.8282 | | | 0.8579 | |

2006 | | | 0.9100 | | | 0.8528 | | | 0.8847 | | | 0.8582 | |

2007 | | | 1.0908 | | | 0.8374 | | | 0.9419 | | | 1.0120 | |

2008 | | | 1.0162 | | | 0.7727 | | | 0.9399 | | | 0.8170 | |

2009 | | | 0.9719 | | | 0.7695 | | | 0.8834 | | | 0.9559 | |

| | Nine months ended September 30, 2009 | | | 0.9421 | | | 0.7695 | | | 0.8634 | | | 0.9329 | |

| | August | | | 0.9390 | | | 0.9011 | | | 0.9199 | | | 0.9118 | |

| | September | | | 0.9421 | | | 0.9042 | | | 0.9246 | | | 0.9329 | |

| | October | | | 0.9719 | | | 0.9223 | | | 0.9484 | | | 0.9288 | |

| | November | | | 0.9562 | | | 0.9309 | | | 0.9441 | | | 0.9461 | |

| | December | | | 0.9615 | | | 0.9334 | | | 0.9491 | | | 0.9559 | |

2010 | | | | | | | | | | | | | |

| | January | | | 0.9747 | | | 0.9373 | | | 0.9582 | | | 0.9388 | |

The above rates may differ from the actual rates used in the preparation of the financial statements and other financial data appearing in this prospectus. Our inclusion of these exchange rates is not meant to suggest that the Canadian dollar amounts actually represent such U.S. dollar amounts or that such amounts could have been converted into U.S. dollars at any particular rate, if at all.

Unless otherwise indicated, throughout this prospectus U.S. dollar amounts have been translated into Canadian dollar amounts based on the noon buying rate in the City of New York for cable transfers of Canadian dollars on September 30, 2009 of U.S.$0.9327 = $1.00, as published by the Federal Reserve Bank of New York. On January 29, 2010 the noon buying rate was U.S.$0.9388 = $1.00.

Canada has no system of exchange controls. There are no Canadian exchange restrictions affecting the remittance of dividends, interest, royalties or similar payments to non-resident holders of our securities.

MARKET AND INDUSTRY DATA

Market data and other statistical information used throughout this prospectus are based on independent industry publications, government publications, reports by market research firms or other published independent sources, including the Energy Information Administration of the U.S. Department of Energy, the National Energy Board, Standard & Poor's, the Canadian Association of Petroleum Producers and the Oil and Gas Journal. Some data are also based on our good faith estimates, which are derived from our review of internal data and information, as well as the independent sources listed above. Although we believe these sources are reliable, we have not independently verified the information and cannot guarantee its accuracy and completeness.

iv

Table of Contents

WHERE YOU CAN OBTAIN MORE INFORMATION

We have filed with the SEC a registration statement on Form F-4 under the Securities Act with respect to the exchange notes being offered in this prospectus. This prospectus, which forms a part of the registration statement, does not contain all of the information set forth in the registration statement. For further information with respect to us and the exchange notes, reference is made to the registration statement. Statements contained in this prospectus as to the contents of any contract or other document are not necessarily complete, and, where such contract or other document is an exhibit to the registration statement, each such statement is qualified by the provisions in such exhibit to which reference is hereby made.

We are not currently, and prior to the effectiveness under the Securities Act of a registration statement for an exchange offer for the unregistered notes, are not expected to be, required to file reports with the SEC for the unregistered notes or to deliver an annual report to holders of the unregistered notes under the Exchange Act. However, we will be subject to the disclosure obligations described in "Description of the Senior Secured Notes—Certain Covenants—Reports" and in "Description of the Senior Notes—Certain Covenants—Reports." Under these obligations, as long as the notes are outstanding, we will furnish you with certain annual and quarterly financial information and, for as long as the notes are "restricted securities" within the meaning of Rule 144(a)(3) under the Securities Act, we will furnish you, or any prospective purchaser of the exchange notes you designate, with the information required to be delivered by Rule 144A(d)(4) under the Securities Act when we receive a written request to do so from you. Written requests for the information should be addressed to Gibson Energy ULC, 1700, 440-2nd Ave S.W., Calgary, Alberta T2P 5E9, Canada, Attn. Mr. T. Murray Carey, General Counsel.

As a result of the offering of the exchange notes, we will become subject to the informational requirements of the Exchange Act applicable to foreign private issuers and, in accordance therewith, will file reports and other information with the SEC. As a foreign private issuer, we are not subject to the proxy rules under Section 14 or the short-swing insider profit disclosure rules under Section 16 of the Exchange Act. The registration statement and other information can be inspected and copied at the Public Reference Room of the SEC located at Room 1580, 100 F Street, N.E., Washington D.C. 20549. Copies of such materials, including copies of all or any portion of the registration statement, can be obtained from the Public Reference Room of the SEC at prescribed rates. You can call the SEC at 1-800-SEC-0330 to obtain information on the operation of the Public Reference Room. Such materials may also be accessed electronically by means of the SEC's home page on the Internet (http://www.sec.gov).

v

Table of Contents

SUMMARY

This summary highlights information contained elsewhere in this prospectus. You should read the entire prospectus carefully, including the risks discussed in the "Risk Factors" section and the historical financial statements and the notes thereto before making an investment decision. This summary may not contain all of the information that may be important to you. If you are not familiar with some of the oil and gas industry terms used in this memorandum, please refer to the "Glossary of Terms" included as Appendix A to this prospectus. On December 12, 2008, Gibson Acquisition ULC, an Alberta unlimited liability corporation ("Gibson AcquisitionCo"), an indirect wholly owned subsidiary of R/C Guitar Coöperatief U.A., a Dutch co-op ("Co-op") owned by investment funds affiliated with Riverstone Holdings LLC ("Riverstone" or the "Sponsor"), acquired all of the issued and outstanding Class A Common Shares and Class B Common Shares (the "Acquisition") of Gibson Energy Holdings Inc. Following the Acquisition, Gibson Energy Holdings Inc. was converted into an unlimited liability corporation and through several amalgamations, was amalgamated with Gibson AcquisitionCo to form the surviving amalgamated unlimited liability corporation, Gibson Energy ULC, a wholly owned subsidiary of Gibson Energy Holding ULC. See "The Transactions." Average daily volumes referenced throughout the prospectus are reflective of the twelve months ended September 30, 2009 (the "LTM Period"), unless stated otherwise.

Gibson Energy

We are one of the largest independent midstream energy companies in Canada and are engaged in the transportation, storage, blending, processing, marketing and distribution of crude oil, condensate, NGLs such as propane and butane, refined products and natural gas. This business is typically referred to as the midstream energy business. Through our extensive network of integrated assets in western Canada and the northern United States, we move hydrocarbon products to market utilizing our terminals, pipelines, tank storage and truck transportation fleet, which, in concert with processing, blending and marketing capabilities, provide valuable services to both producers and consumers. We participate across the full midstream energy value chain, from the producing regions in western Canada, through our strategically located terminals in Hardisty and Edmonton, to the refineries of North America via major pipelines serving the region. Having provided market access to the energy industry in western Canada over the last 55 years, we believe we are a critical component to the future development of the substantial resources in the Western Canadian Sedimentary Basin (the "WCSB"), one of the most hydrocarbon-rich regions in the world.

Since 1953, we have consistently been a leader in the western Canadian midstream energy market, developing and maintaining strong relationships with the leading industry participants. Since that time, our business has grown by expanding both geographically and by diversifying our service offerings to meet new customer needs. From our inception until the Acquisition, we were controlled by Hunting Plc, a UK-based energy services company publicly listed on the London Stock Exchange. On December 12, 2008, we were acquired by investment funds controlled by Riverstone, an energy-focused private equity firm, for $1.3 billion.

Our operations are primarily concentrated in the provinces of Alberta, British Columbia and Saskatchewan, as well as parts of the northern United States and are segmented into five different business units:

- •

- Terminals and Pipelines: We provide tariff-based pipeline services and fee-based storage and terminalling services for crude oil, condensate and refined products, moving an average of over 290,000 barrels per day over the past five fiscal years. We own and operate 245 miles of pipeline, two major storage terminals strategically located at Edmonton and Hardisty, which are the principal hubs for moving oil products out of the WCSB, a fractionation plant at Hardisty and 11 custom blending terminals (of which seven have custom blending activities including the

1

Table of Contents

Through our strategically located asset network, specialized midstream energy capabilities and deep knowledge of the market, we have historically generated stable cash flows. For the year ended December 31, 2008, combined revenues and total segment profit were $4.8 billion and $168.4 million, respectively.

Our Market

We operate in the WCSB, one of the most hydrocarbon-rich basins in the world. Estimates indicate that the total reserve potential in western Canada is equivalent to 175.4 billion barrels, providing Canada with the second largest single country reserve in the world after Saudi Arabia. According to the Canadian Association of Petroleum Producers, crude oil production from the WCSB is due to increase from 2.4 million barrels per day in 2008 to 3.2 million barrels per day in 2015, driven by increased production and activity in the oil sands regions. As a leading provider of midstream energy services to the region, we believe that we will be a key component to this development, assisting producers in getting their product to market. As production from this region increases, we believe there will be a substantial opportunity to grow our asset footprint and increase the volume of barrels flowing through our system.

Our Operations

Terminals and Pipelines

Our terminals and pipelines segment owns and operates over 245 miles of pipeline, two major storage terminals, a fractionation plant at Hardisty and 11 custom blending terminals, located throughout Alberta and Saskatchewan, which is the heart of the growing Canadian energy industry. We provide tariff-based pipeline services with over 80,000 barrels per day of capacity and fee-based storage and terminalling services with an aggregate storage capacity exceeding 2.0 million barrels, with daily throughput of approximately 283,000 barrels per day. In addition, our custom terminals business generates profits by purchasing lower quality crude and condensate from producers at the wellhead and blending it to create higher quality product that can be sold at a premium.

2

Table of Contents

The following table contains information regarding our terminals and pipelines segment as of September 30, 2009:

| | |

| Asset | | Key attributes |

|---|

Hardisty Terminal | | • 1.6 million barrels of storage, 184,000 barrels per day of throughput |

| | • Truck loading and offloading, crude blending and cooling, storage and receipt and delivery services into Keystone, Enbridge, Express and Bow River southbound pipelines |

Edmonton South Terminal | | • Approximately 440,000 barrels of storage connected to the major export pipelines operated by Enbridge and Kinder Morgan |

| | • Handles diesel fuel, LPGs, wellsite fluids and crude oil |

| | • Serviced by Canadian Pacific and Canadian National rail systems, four pipeline connections, truck loading and offloading |

Custom Terminals | | • 11 strategically located terminals throughout Alberta and Saskatchewan, Canada |

| | • Typically blend smaller batches of crude grades which are transported to the terminals by truck transportation and injected into pipeline systems |

Provost Pipeline | | • 175 miles of pipe extending east of Hardisty Terminal, with 50,000 barrels per day capacity |

| | • Handles two stream types that are sent in batches down the pipeline to Hardisty Terminal |

| | • Diluent injection points along the line ensure efficient crude transport |

Bellshill Lake Pipeline | | • Approximately 70 miles of pipe extending west of Hardisty Terminal with 30,000 barrels per day capacity |

| | • Handles two stream types that are sent in batches down the pipeline to Hardisty Terminal |

Fractionation Plant | | • Capable of processing approximately 5,800 barrels per day of NGL into butane, propane, condensate and other by-products |

Battle River Terminal (25% equity interest) | | • Approximately 1.2 million barrels of storage connected to the Hardisty Terminal |

Our significant terminals and pipelines' customers include Suncor, Husky Energy, Trafigura Canada and Cenovus. For the year ended December 31, 2008, combined revenues and combined segment profit were $890.0 million and $49.3 million, respectively.

3

Table of Contents

Truck Transportation

Our truck transportation segment is one of the largest truck haulers of crude, condensate, propane, butane, asphalt, methanol, sulfur, petroleum coke, gypsum and drilling fluids in western Canada, moving over 228,000 boe per day. The large scale and strategic position of our fleet operations allow us to carry out logistically complex and high margin jobs, regardless of the volume or destination. The segment's unique integration within the broader Gibson network positions it to optimize the Company's assets to drive strong profitability and cash flows. For the year ended December 31, 2008, approximately 12% of our truck transportation segment's sales were intra-company with our other business segments.

We own approximately 1,480 trailers and have access to approximately 660 tractors through a combination of company-owned tractors and contractual arrangements with over 290 owner-operators. This enables us to consistently provide timely, safe delivery of petroleum feedstocks and products to a multitude of customers through over ten base locations situated throughout western Canada. Truck transportation's significant customers include Canadian Natural Resources, Husky Energy, Suncor, Japan Canada Oil Sands and Bonavista Petroleum. For the year ended December 31, 2008, combined revenues and combined segment profit were $301.4 million and $48.7 million, respectively.

Propane Marketing and Distribution

Our propane marketing and distribution segment operates in both the retail and wholesale propane markets. Our branded Canwest business distributes propane to retail customers throughout western Canada. In the LTM Period, Canwest's retail operations distributed in excess of 61 million gallons to residential and commercial/industrial customers. Over 70% of these LTM Period volumes were derived from oil field related and commercial/industrial volumes, which are somewhat insulated from weather risk. We lease the majority of our tanks to our customers, providing us with a steady source of income and creating a dependable customer base. Over the last 20 years we have established our presence in the market as the second largest retail propane distributor in Canada.

In addition, we have grown our presence in the North American wholesale propane market with the acquisition of MP Energy in October 2007 and the acquisition of certain propane terminal facilities from Superior Propane LLC ("Superior Propane") in November 2009. The wholesale distribution business is served by four owned and operated propane storage facilities with combined storage of 660,000 gallons located in Ontario, British Columbia, South Dakota and Montana and third party storage locations. Our wholesale division sold over 196 million gallons of propane in the LTM Period.

Through our propane marketing and distribution segment, we have established a consistent reputation as a dependable, customer service-oriented propane supplier, consistently honoring our service and supply commitments to our customers, while maintaining industry-leading health, safety and environmental standards, as evidenced by our long-standing relationships with leading industry participants.

For the year ended December 31, 2008, combined revenues and combined segment profit were $452.8 million and $27.0 million, respectively.

Processing and Wellsite Fluids

Our processing and wellsite fluids segment, located at Moose Jaw, utilizes our refinery with a capacity of approximately 16,000 barrels per day to process heavy crude into asphaltic and lighter distillate products, including road asphalt, roofing flux, tops and wellsite fluids. Our products are then shipped by truck, rail and pipeline from Saskatchewan to high demand markets in the U.S. and western Canada. Currently, Moose Jaw processes heavy crude oil received from two independent pipelines. Our refinery is both interconnected and strategically positioned to be in close proximity with the critical

4

Table of Contents

Enbridge and South Saskatchewan pipelines located between the Canadian oil producing markets and the Canadian/U.S. product consuming markets. By synchronizing with our other segments, namely truck transportation and marketing, we enjoy the benefits of having ready access to both heavy crude oil supply and a solid downstream customer base.

Until the fall of 2005, the refinery at Moose Jaw operated seven months a year, producing asphalt in the summer months when there was sufficient demand. Recognizing a significant market opportunity to capture attractive economics by operating year round, we have invested over $43.8 million in capital projects since 2002 to upgrade the facility and grow the business. These expenditures included the addition of asphalt storage facilities, an efficient boiler system, increased rail loading facilities, pipeline and plant upgrades and winterization. We process an average of approximately 13,700 barrels per day of heavy crude into an average of approximately 6,300 barrels per day of asphaltic products and approximately 7,400 barrels per day of wellsite fluids or refinery feedstock. Our plant facilities have 1.0 million barrels of storage capacity, 32 miles of pipelines, truck, and rail loading facilities and approximately 545 leased rail cars.

For the year ended December 31, 2008, combined revenues and combined segment profit were $540.4 million and $29.1 million, respectively.

Marketing

Our marketing segment focuses on enhancing the overall profitability of our assets by partnering with our customers and leveraging our extensive infrastructure and asset network to take advantage of specific location, quality or time-based arbitrage opportunities. We purchase, sell, store and blend approximately 175,000 boe per day of crude oil, condensate, natural gas and NGLs. The marketing segment is also responsible for managing our physical commodity positions, based on the needs of each operating segment.

We have a board-approved policy to maintain a total company-wide Value at Risk ("VAR") of no more than $7.0 million. The marketing segment manages our VAR amongst the various operating units and product lines, with each individual commodity having a sublimit of no more than $2.5 million. For the year ended December 31, 2008, our company-wide daily VAR did not exceed $3.9 million. The $7.0 million VAR limit is split amongst the following books: Wellsite Fluids, Crude Oil and Diluent, Natural Gas, Retail Propane, Wholesale Propane, NGL Marketing, Moose Jaw, Electricity, Producer Hedges and Foreign Exchange. Our marketing segment also manages the 310,000 barrel capacity Edmonton North Terminal, which is fully dedicated to the segment and manages our 25% ownership interest in the 1.2 million barrel Battle River Terminal, which is also fully dedicated to the segment.

For the year ended December 31, 2008, combined revenues and combined segment profit were $4.1 billion and $14.3 million, respectively.

Competitive Strengths

We believe that we are well-positioned to execute our primary business objectives and strategies because of the following competitive strengths:

- •

- Key service provider to one of the fastest growing and hydrocarbon-rich basins in the world. Our operations are focused on the WCSB, one of the most hydrocarbon-rich basins in the world. In order to meet growing worldwide demand for energy, crude oil production from the WCSB is expected to increase from 2.4 million barrels per day in 2008 to 3.2 million barrels per day in 2015. As production from this region increases, we believe there will be substantial opportunity to add assets to our business, increase the volume of barrels flowing through our systems and expand our service offerings.

5

Table of Contents

- •

- Services provide fundamental economic value. On any given day, a barrel of crude oil that is produced from the wellhead is worth fundamentally less than a barrel delivered to the refinery gate, with the differential in value depending on the quality of the crude produced at the wellhead, the distance and route the barrel needs to travel before it reaches its final destination and the spot price for crude on the open market. Because we provide the gathering, blending, terminalling and transportation services between the wellhead and the ultimate market, we are in a position to capture a significant portion of this value differential as revenue.

- •

- Diversified, high-value fixed asset base. Our asset base includes two pipelines with a combined capacity of 80,000 barrels per day, 13 terminals capable of storing approximately 2.7 million barrels, approximately 1,480 trailers hauling over 228,000 barrels per day of crude or NGLs and related products, a refinery with approximately 16,000 barrels per day and 1.0 million barrels of storage capacity, 48 retail propane distribution branches and a fractionation plant capable of processing 5,800 barrels per day of NGLs. Operated as an integrated network, these assets have provided a diversified stream of cash flows. As a participant across the midstream energy value chain, we often "touch" a barrel several times between the wellhead and the refinery, and have experienced synergistically balanced profits amongst our business segments, depending on market conditions and the competitive environment.

- •

- Valuable footholds in strategic markets. Our terminals in Hardisty and Edmonton are at the hub of the energy industry in western Canada, linking producers in the region to the rest of North America. Hardisty is a 1.6 million barrel storage facility with approximately 184,000 barrels per day of average throughput for the LTM Period. The Edmonton South Terminal is comprised of a storage facility of approximately 440,000 barrels with approximately 45,000 barrels per day of average throughput for the LTM Period. Together, our Hardisty and Edmonton South terminals give our customers access to all of the major pipelines moving crude to export markets from the WCSB, including connections to the Enbridge, Express, Trans Mountain, Bow River and Keystone pipelines. These footholds not only offer us stable fee-based cash flow, but also give us insight into the operations and service needs of major participants in the Western Canadian energy market, which enhances our ability to meet their changing requirements.

- •

- Leading health, safety and environmental record. Throughout our long history, we have continually focused on having "best in class" operations with respect to health, safety and environmental compliance. We have been recognized by the Province of Alberta for excellence in these areas, which we believe gives us a competitive advantage versus smaller competitors lacking either the historical knowledge or the resources to match our performance. Several of our customers are large, multinational oil companies that have very strict guidelines on the standards to which their service providers must adhere. Our record on health, safety and environmental matters allows us to do business with the most discriminating market participants.

- •

- Conservative risk management policies consistent with past practices. We have a long history of conservatively managing our exposure to commodity prices. Because some of our service offerings entail taking title to the products that we transport, store, process or blend, we are exposed to market price fluctuations. Our marketing segment works with our other operating segments to balance our physical commodity positions, and our board-approved policy is to have no more than $7.0 million of VAR at any one time, with each individual commodity having a sublimit of no more than $2.5 million. For the year ended December 31, 2008, our company-wide daily VAR did not exceed $3.9 million per day. During the past 15 years, we have not suffered an annual net loss in our marketing segment.

- •

- Management with a long track record of profitable operations and strong industry reputation. Our senior management team members have an average tenure at our company of approximately 8.5 years. See "Management." During this period, our management team has demonstrated a

6

Table of Contents

Business Strategies

Our primary objective is to generate stable and growing cash flows for our stakeholders. As we move energy products through our facilities utilizing our terminals, pipelines, tank storage and truck transportation fleet in concert with our marketing, processing and blending capabilities, we look to create value through our synergistic service offerings for producers and consumers of hydrocarbon products across western Canada and the northern United States.

- •

- Utilize integrated asset base to capture inter-division synergies within the hydrocarbon value chain. Our existing asset base has been constructed to participate in the full hydrocarbon value chain, generating profits on the commodities we touch all the way from the wellhead to the refinery. By spanning the entire value chain, we are able to provide efficient, reliable service to both producers and end-users while deriving revenue and cost synergies through our integrated network of terminals, pipelines, processing facilities, truck transportation and distribution network. For example, we believe the margins in the processing and wellsite fluids segment are higher and more stable as a result of its source of supply, heavy crude oil purchased by our marketing segment, and its ability to interface with our truck transportation and our terminals and pipelines segments. By processing heavy crude oil, we receive a competitive cost advantage, as most of our competitors are processing higher-cost light sweet crude and condensate. In addition, our ability to transport via internal truck and rail to our own interim storage allows us to minimize transportation costs and to service our customer base with just-in-time delivery.

- •

- Expand our network of assets by pursuing numerous growth opportunities. Given the anticipated long-term growth in the WCSB region and our existing asset network there, we believe we are well-positioned to capitalize on the numerous organic growth opportunities in the region. From 2006 we have invested in growth capital, which has meaningfully expanded our asset platform and positioned us to take advantage of future industry activity through our increased and available capacity. Furthermore, we believe there still remain a significant number of promising organic expansion opportunities.

- •

- Enhance margins by focusing on quality of volumes, not quantity. We have historically been able to add value throughout the midstream energy value chain, which has provided us with a competitive advantage. As such, we feel that our greatest opportunity for organic growth lies in providing additional, value-adding services along the chain. One of our objectives is to provide as many complementary services as possible on every barrel, rather than simply increasing the volume of barrels we process or transport. By aiming to increase the number of services we provide, we feel we will continue to grow both our profit potential and our efficiency.

- •

- Continue to conservatively manage the risks affecting our business. We have a long history of conservatively managing the risks faced by our business and intend to continue with this practice going forward. We aim to minimize our exposure to commodity prices by continually hedging our physical commodity inventory using both physical and financial contracts. Our board-approved policy is to have no more than $7.0 million of VAR at any one time, with each individual commodity having a sublimit of no more than $2.5 million. For the year ended

7

Table of Contents

December 31, 2008, our company-wide daily VAR did not exceed $3.9 million. By conservatively managing our commodity exposure, our marketing segment has remained consistently profitable over the past 15 years. Similarly, as we conduct our business of moving hydrocarbons to market, we are exposed to a number of health, safety and environmental risks. Proactively managing these risks is critical to maintaining the high standards expected by our customers, creating an attractive work environment for our employees and complying with government regulations. We have been recognized for having leading health, safety and environmental practices in the past, and are committed to continued high standards in the future.

- •

- Continuously improve processes, products and services through investing in new equipment, technology, facilities and personnel. We plan to continue our historical practice of deploying capital in a disciplined manner to grow our business and improve upon our existing operations. Historically, we have focused on investing capital in both our physical assets and our personnel, and we plan on continuing this practice. We expect to make capital investment decisions principally by analyzing the projected return on capital employed, whether this involves equipment, technology or facilities.

- •

- Pursue acquisition opportunities consistent with past practices. We have a long track record of pursuing acquisitions that we feel will benefit our business, either by expanding our reach in existing markets or by providing platforms with which to enter new markets. We will continue to seek acquisitions which we feel will allow us to successfully expand our business, both in existing markets and in new markets.

Our Equity Sponsor

As part of the Transactions (as defined below), Riverstone/Carlyle Global Energy & Power Fund IV (Cayman), L.P. ("R/C Fund IV") invested approximately $537.7 million of cash equity in us through certain wholly controlled subsidiaries. R/C Fund IV is sponsored by Riverstone. See "—The Transactions."

Riverstone, an energy- and power-focused private equity firm founded in 2000, has approximately U.S.$17 billion of assets under management across six investment funds. Riverstone conducts buyout and growth capital investments in the midstream, exploration and production, oilfield service, power and renewable sectors of the energy industry. With offices in New York, London and Houston, the firm has committed approximately U.S.$12.4 billion to 64 investments in North America, Latin America, Europe and Asia.

The Transactions

On August 5, 2008, Hunting Plc, Hunting Energy Holdings Limited (together with Hunting Plc, "Hunting") and Gibson AcquisitionCo entered into a Sale and Purchase Agreement pursuant to which, among other things, Gibson AcquisitionCo acquired all of the issued and outstanding Class A Common Shares and Class B Common Shares of Gibson Energy Holdings Inc. for $1.3 billion.

In connection with the Acquisition, we entered into the following financing transactions:

- •

- R/C Fund IV capitalized Gibson AcquisitionCo with an aggregate equity contribution of approximately $537.7 million through certain wholly controlled subsidiaries;

- •

- we entered into a U.S.$230.0 million first lien senior secured interim credit agreement and a U.S.$315.0 million second lien senior secured interim credit agreement (together, the "Bridge Loans");

- •

- we entered into our liquidity facility providing for U.S.$65.0 million of total borrowing capacity, prior to giving effect to an estimated $2.0 million of issued but undrawn letters of credit, and no

8

Table of Contents

Following the consummation of the Acquisition, Gibson Energy Holdings Inc. was converted into an unlimited liability corporation and through several amalgamations was amalgamated with Gibson AcquisitionCo to form the continuing amalgamated unlimited liability corporation, Gibson Energy ULC, a wholly owned subsidiary of Gibson Energy Holding ULC.

We refer to the Acquisition, the equity contribution to Gibson AcquisitionCo, the borrowings under our Bridge Loans, our new liquidity facility and the other transactions described above as the "Transactions." For more information regarding the Transactions, see "—The Transactions."

The Refinancing

On May 27, 2009, we issued our 11.75% First Lien Senior Secured Notes due 2014 in an aggregate principal amount of U.S.$560.0 million, the proceeds of which were used to repay in full all amounts outstanding under our Bridge Loans and to pay fees and expenses related thereto (the "Refinancing").

The 2010 Offering

On January 19, 2010, we issued our 10.00% Senior Notes due 2018 in an aggregate principal amount of U.S.$200.0 million (the "2010 Offering"), some of the proceeds of which were used to fund the acquisition of Johnstone Tank Trucking Ltd ("Johnstone") and Aarcam Propane & Construction Heat Ltd. ("Aarcam") acquisitions, and will be used to fund the potential acquisition of the remaining equity interests in certain tankage assets connected to our Hardisty Terminal, to fund identified and approved capital expenditures expected to be undertaken in the next 12 to 18 months and to fund other future acquisitions and capital expenditures and general corporate purposes. On January 19, 2010 we entered into an amendment to our liquidity facility to allow for the 2010 Offering and to increase total borrowing capacity for revolving loans and letters of credit in an aggregate principal amount of up to U.S.$150.0 million.

Recent Developments

On January 31, 2010, we completed the acquisition of Johnstone for approximately $20.0 million. Johnstone provides fluid hauling, acid hauling, vacuum service and pressure trucking for the oil and gas industry across southern Saskatchewan. This acquisition will further expand our market presence in southern Saskatchewan and provide access to activity related to the Bakken oil fields. In addition, on February 1, 2010 we completed the acquisition of Aarcam, a propane retailer in Calgary, for approximately $3.2 million.

Issuer and Co-issuer Information

Our principal executive offices are located at 1700, 440-2nd Ave S.W., Calgary, Alberta T2P 5E9, Canada. Our telephone number at this address is +1.403.206.4000. Our corporate website address ishttp://gibsons.com. Our website and the information contained on our website do not constitute a part of this prospectus and is not incorporated by reference herein.

9

Table of Contents

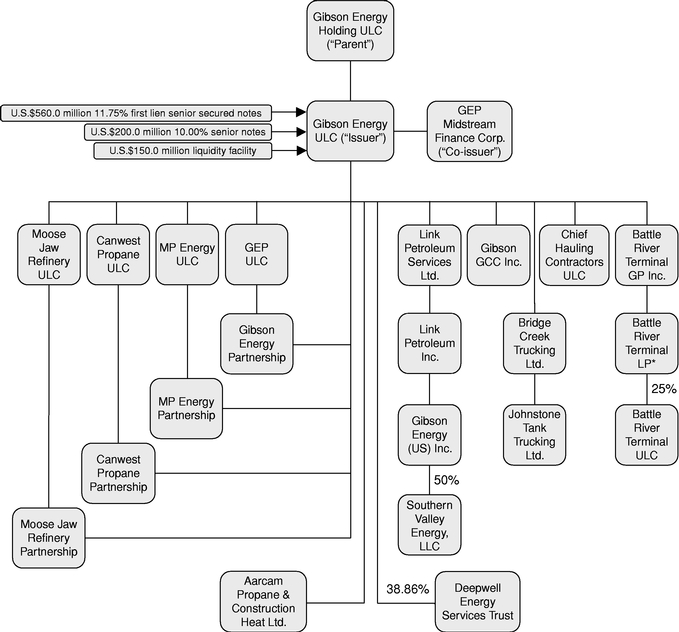

Our corporate structure is as follows:

- *

- Battle River Terminal LP is a Limited Partnership formed between Battle River Terminal GP Inc., as General Partner, and Gibson Energy ULC as Limited Partner.

10

Table of Contents

THE EXCHANGE OFFER

The following summary contains basic information about the exchange offer and the exchange notes. It does not contain all the information that is important to you. For a more complete understanding of the exchange notes, please refer to the sections of this prospectus entitled "The Exchange Offer," "Description of the Senior Secured Notes," and "Description of the Senior Notes."

On May 27, 2009, the issuers issued an aggregate of U.S.$560.0 million principal amount of 11.75% First Lien Senior Secured Notes due May 27, 2014 (the "initial senior secured notes") and on January 19, 2010, the issuers issued an aggregate of U.S.$200.0 million principal amount of 10.00% Senior Notes due January 15, 2018 (the "initial senior notes") (collectively, the "initial notes") to a group of initial purchasers in reliance on exemptions from, or in transactions not subject to, the registration requirements of the Securities Act and applicable state securities laws. The initial senior secured notes are unconditionally guaranteed on a senior secured basis by the guarantors, and the initial senior notes are unconditionally guaranteed on a senior basis by the guarantors.

| | |

The Exchange Offer | | The issuers are offering to exchange up to: |

| | • U.S.$560.0 million aggregate principal amount of 11.75% exchange senior secured notes due 2014, which have been registered under the Securities Act (the "exchange senior secured notes"), for any and all outstanding 11.75% initial senior secured notes due 2014; and |

| | • U.S.$200.0 million aggregate principal amount of 10.00% exchange senior notes due 2018, which have been registered under the Securities Act (the "exchange senior notes"), for any and all outstanding 10.00% initial senior notes due 2018. |

| | The "exchange senior secured notes" and the "exchange senior notes" are collectively referred to as the "exchange notes," and the term "notes" refers to both the initial notes and the exchange notes. The term "senior secured notes" refers to both the initial senior secured notes and the exchange senior secured notes, and the term "senior notes" refers to both the initial senior notes and the exchange senior notes. |

| | To exchange your initial notes, you must properly tender them, and the issuers must accept them. You may tender outstanding initial notes only in denominations of the principal amount of $2,000 and integral multiples of $1,000 in excess thereof. The issuers will exchange all initial notes that you validly tender and do not validly withdraw prior to the withdrawal of the exchange offer. The issuers will issue registered exchange notes promptly after the expiration of the exchange offer. |

11

Table of Contents

| | |

| | The form and terms of the exchange notes will be substantially identical to those of the initial notes except that the exchange notes will have been registered under the Securities Act. Therefore, the exchange notes will not be subject to certain contractual transfer restrictions, registration rights and certain additional interest provisions applicable to the initial notes prior to consummation of the exchange offer. |

| | Upon completion of the exchange offer, there may not be a market for the initial notes and you may have difficulty selling them. |

Resale of Exchange notes | | We believe that, if you are not a broker-dealer, you may offer exchange notes (together with the guarantees thereof) for resale, resell and otherwise transfer the exchange notes (and the related guarantees) without complying with the registration and prospectus delivery requirements of the Securities Act if you: |

| | • acquired the exchange notes in the ordinary course of business; |

| | • are not engaged in, do not intend to engage in and have no arrangement or understanding with any person to participate in a "distribution" (as defined under the Securities Act) of the exchange notes; and |

| | • are not an "affiliate" (as defined under Rule 405 of the Securities Act) of the issuers or any guarantor. |

| | If any of these conditions are not satisfied, you must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale transaction. Our belief that transfers of exchange notes would be permitted without registration or prospectus delivery under the conditions described above is based on the interpretations of the SEC given to other, unrelated issuers in transactions similar to the exchange offer. We cannot assure you that the SEC would take the same position with respect to the exchange offer. |

Broker-Dealers | | Each broker-dealer that receives exchange notes for its own account in exchange for initial notes, where the initial notes were acquired by it as a result of market-making activities or other trading activities, may be deemed to be an "underwriter" within the meaning of the Securities Act and must acknowledge that it will deliver a prospectus that meets the requirements of the Securities Act in connection with any resale of the exchange notes. However, by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an "underwriter" within the meaning of the Securities Act. See "Plan of Distribution." |

Expiration Date | | The exchange offer will expire at 5:00 p.m., New York City time, on , 2010, unless we extend it. |

12

Table of Contents

| | |

Withdrawal | | You may withdraw your tender of initial notes under the exchange offer at any time prior to the expiration date of the exchange offer. We will return to you any of your initial notes that are not accepted for any reason for exchange, without expense to you, promptly after the expiration or termination of the exchange offer. Any withdrawal must be in accordance with the procedures described in "The Exchange Offer—Withdrawal Rights." |

Conditions to the Exchange Offer | | The exchange offer is subject to customary conditions which we may assert or waive. The exchange offer is not conditioned upon any minimum principal amount of initial notes being tendered for exchange. See "The Exchange Offer—Conditions to the Exchange Offer." |

Procedures for Tendering Initial Notes | | Each holder of initial notes that wishes to tender initial notes for exchange notes pursuant to the exchange offer must, before the exchange offer expires, either: |

| | • transmit a properly completed and duly executed letter of transmittal, together with all other documents required by the letter of transmittal, including the initial notes, to the exchange agent; or |

| | • if initial notes are tendered in accordance with book-entry procedures, arrange with The Depository Trust Company ("DTC"), to cause to be transmitted to the exchange agent an agent's message indicating, among other things, the holder's agreement to be bound by the letter of transmittal, |

| | or comply with the procedures described below under "—Guaranteed Delivery." |

| | A holder of initial notes that tenders initial notes in the exchange offer must represent, among other things, that: |

| | • the holder is not an "affiliate" of the issuers or any guarantor as defined under Rule 405 of the Securities Act; |

| | • the holder is acquiring the exchange notes in its ordinary course of business; |

| | • the holder is not engaged in, does not intend to engage in and has no arrangement or understanding with any person to participate in a distribution of the exchange notes within the meaning of the Securities Act; |

| | • if the holder is a broker-dealer that will receive exchange notes for its own account in exchange for initial notes that were acquired as a result of market-making or other trading activities, then the holder will deliver a prospectus in connection with any resale of the exchange notes; and |

13

Table of Contents

| | |

| | • the holder is not acting on behalf of any person who could not truthfully make the foregoing representations. |

| | Do not send letters of transmittal, certificates representing initial notes or other documents to us or DTC. Send these documents only to the exchange agent at the address given in this prospectus and in the letter of transmittal. |

Special Procedures for Tenders by Beneficial Owners of Initial Notes | | If: |

| | • you beneficially own initial notes; |

| | • those initial notes are registered in the name of a broker, dealer, commercial bank, trust company or other nominee or custodian; and |

| | • you wish to tender your initial notes in the exchange offer, |

| | you should contact the registered holder as soon as possible and instruct it to tender the initial notes on your behalf and comply with the instructions set forth in this prospectus and the letter of transmittal. |

Guaranteed Delivery | | If you hold initial notes in certificated form or if you own initial notes in the form of a book-entry interest in a global note deposited with the trustee, as custodian for DTC, and you wish to tender those initial notes but |

| | • the certificates for your initial notes are not immediately available or all required documents are unlikely to reach the exchange agent before the exchange offer expires; or |

| | • you cannot complete the procedure for book-entry transfer prior to the expiration date, |

| | you may tender your initial notes in accordance with the procedures described in "The Exchange Offer—Procedures for Tendering Initial Notes—Guaranteed Delivery." |

Consequences of Not Exchanging Initial Notes | | If you do not tender your initial notes or we reject your tender, your initial notes will remain outstanding and will continue to be subject to the provisions in the indentures regarding the transfer and exchange of the initial notes and the existing restrictions on transfer set forth in the legends on the initial notes. In general, the initial notes may not be offered or sold unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Holders of initial notes will not be entitled to any further registration rights under the registration rights agreement. We do not currently plan to register the initial notes under the Securities Act. |

14

Table of Contents

| | |

| | You do not have any appraisal or dissenters' rights in connection with the exchange offer. |

| | To the extent that initial notes are tendered and accepted in the exchange offer, the trading market for initial notes that remain outstanding after the exchange offer could be adversely affected. |

Registration Rights Agreement | | You are entitled to exchange your initial notes for exchange notes with substantially identical terms. This exchange offer satisfies this right. After the exchange offer is completed, you will no longer be entitled to any exchange or registration rights with respect to your initial notes. |

Certain Canadian and United States Tax Considerations | | Your exchange of initial notes for exchange notes will not be treated as a taxable exchange for United States income tax purposes. |

| | If you are a non-resident of Canada who does not use or hold the initial notes in carrying on business in Canada, deals at arm's length with the issuers and does not carry on certain insurance businesses, you will not generally be subject to Canadian federal income tax on disposition of the initial notes. Accordingly, even if the exchange of the initial notes for exchange notes were a taxable event for Canadian federal income tax purposes, Canadian federal income tax would not generally apply to you. See "Certain Canadian and United States Tax Considerations." |

Use of Proceeds | | We will not receive any cash proceeds from the exchange offer. |