J.P. MORGAN EXCHANGE-TRADED FUND TRUST

270 PARK AVENUE

NEW YORK, NEW YORK 10017

VIA EDGAR

November 8 , 2016

Alison White

Securities and Exchange Commission

100 F Street, NE

Washington, DC 20549

Re: J.P. Morgan Exchange-Traded Fund Trust (the “Trust”);

File Nos. 333-191837; 811-22903

Post-Effective Amendment No. 77

Dear Ms. White:

This letter is in response to the comments you provided with respect to Post-Effective Amendment No. 77 which was filed on behalf of the JPMorgan Diversified Return U.S. Small Cap Equity ETF (the “Fund”). Our responses to your comments are set forth below. Except as otherwise noted below, we will incorporate the changes referenced below into the Trust’s Registration Statement in a filing made pursuant to Rule 485(b) of the Securities Act of 1933, which will become automatically effective on or about November 14, 2016. Capitalized terms used but not defined in this letter have the meanings given to them in the Fund’s registration statement

| 1. | Comment: Please include a “Tandy” representation in your response letter. |

Response: As announced by the staff of the U.S. Securities and Exchange Commission on October 5, 2016, “Tandy” representations are no longer required. Therefore, no Tandy representation is included with this letter.

PROSPECTUS COMMENTS

| 2. | Comment: Please update the series and class information with the Fund’s ticker. |

Response: The update will be made prior to the launch of the Fund.

| 3. | Comment: Please provide supplementally the rules-based methodology for the Russell 2000 Diversified Factor Index, the Fund’s underlying index (the “Underlying Index”), and confirm whether the Underlying Index will be operational by the commencement of operations of the Fund. |

1

Response: Attached to this letter as Appendix A is the rules-based methodology for the Underlying Index. The Underlying Index was launched as of September 30, 2016.

| 4. | Comment: In order to comply with the requirements of Rule 35d-1 under the Investment Company Act of 1940 (“Rule 35d-1”), please include in the prospectus a representation that the Fund will invest at least 80% of its assets in U.S. small cap equity securities. |

Response: In accordance with the requirements of the exemptive relief on which the Fund will rely to operate as an exchange-traded fund, the Fund has adopted a policy to invest at least 80% of its Assets in securities included in the Underlying Index (the “80% Policy”). The Fund must provide shareholders with at least 60 days’ notice prior to any change in the 80% Policy. Because the Underlying Index consists solely of securities suggested by the Fund’s name (i.e., U.S. small capitalization equity securities), the Fund believes it complies with Rule 35d-1 through adoption of the 80% Policy. The Fund notes that this approach is consistent with industry practice for index-based ETFs whose names implicate the provisions of Rule 35d-1.

| 5. | Comment: Please advise how derivatives will be valued for purposes of determining the Fund’s compliance with its 80% Policy. |

Response: Derivatives are not included in the numerator for purposes of determining the Fund’s compliance with its 80% Policy.

| 6. | Comment: The disclosure states that “Holdings in the Underlying Index are selected by the Index Providerprimarily from the constituents of the Russell 2000 Index . . . .” If holdings are not selected from the constituents of the Russell 2000 Index, please explain the other sources from which they could be selected. |

Response: There may be infrequent instances when a security could be a component of the Underlying Index, but no longer a component of the Russell 2000 Index. This may occur when a security was originally in the Russell 2000 Index, had been removed from the Russell 2000 Index, but still qualifies for the Underlying Index based on its methodology.

| 7. | Comment: Since preferred stock may be included in the Underlying Index, please consider whether specific risk disclosure for preferred stock should be included. |

Response: We have reviewed the anticipated amount that preferred stock will represent in the Underlying Index and, based on that amount, we do not believe the additional risk disclosure is necessary in the Risk/Return Summary. We have included preferred stock risk as an additional risk in the “More About the Fund” section of the prospectus.

| 8. | Comment: Because the Fund’s strategy disclosure only identifies the use of exchange-traded futures, and not other types of derivatives, as a principal strategy, please consider revising the “Derivatives Risk” section to focus on the risks related to such futures. |

2

Response: The Fund has reviewed the current “Derivatives Risk” disclosure and believe it appropriately identifies the main risks associated with its use of the derivatives and complies with the requirements of Form N-1A and the guidance with respect to derivatives provided by the staff of the SEC to the Investment Company Institute in a letter dated July 30, 2010.

| 9. | Comment: Please provide supplementally the number of authorized participants (“APs”) that the Fund will have when it commences operations. |

Response: The Fund is expected to have four APs when it begins operations.

Statement of Additional Information

| 10. | Comment: Please confirm whether the Fund will invest in other exchange-traded funds. |

Response: The Fund retains the flexibility to invest in other exchange-traded funds. It is anticipated that any investment would not exceed the limits of Section 12(d)(1)(A) of the Investment Company Act of 1940.

We hope that the Staff finds this letter responsive to the Staff’s comments. Should members of the Staff have any questions or comments concerning this letter, please call the undersigned at (614) 213-4020.

Sincerely,

/s/ Elizabeth A. Davin

Elizabeth A. Davin

Assistant Secretary

3

Appendix A

Ground Rules |  |

Russell 2000 Diversified

Factor Index

v1.0

|

| 1.0 | Introduction | 3 | ||||

| 2.0 | Management Responsibilities | 5 | ||||

| 3.0 | Queries and Complaints | 6 | ||||

| 4.0 | Eligible Securities | 7 | ||||

| 5.0 | Factor Definitions | 8 | ||||

| 6.0 | Custom Sector Indexes and Target Weights | 10 | ||||

| 7.0 | Periodic Review of Constituents | 12 | ||||

| 8.0 | Changes to Constituent Companies | 14 | ||||

| 9.0 | Corporate Actions and Events | 15 | ||||

| 10.0 | Indexes Algorithm and Calculation Method | 16 | ||||

| 18 | ||||||

| 19 | ||||||

| 20 | ||||||

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 2 of 20 |

|

Section 1

Introduction

| 1.0 | Introduction |

| 1.1 | This document sets out the Ground Rules for the construction and management of the Russell 2000 Diversified Factor Index. Copies of the Ground Rules are available fromwww.ftserussell.com. |

| 1.2 | The Russell 2000 Diversified Factor Index is designed to reflect the performance of US securities representing a diversified set of factor characteristics. Constituents are selected from the Russell 2000® Index universe based on a composite factor score. The composite factor spans Value, Price Momentum and Quality characteristics. |

| 1.3 | These Ground Rules should be read in conjunction with the FTSE Global Equity Index Series Ground Rules which are available atwww.ftserussell.com and Russell U.S. Equity Indexes Construction and Methodology which is available at http://www.ftse.com/products/indices/Russell-US. Unless stated in these Ground Rules, the Russell 2000 Diversified Factor Index will follow the same process as the FTSE Global Equity Index Series. |

| 1.4 | A Price Index, Total Return Index and Net of Tax Index will be calculated in real-time and published in US dollars. The Total Return and Net of Tax indexes include income based on ex dividend adjustments. |

| 1.5 | The Net of Tax Total Return Index is calculated based on the maximum withholding tax rates applicable to dividends received by institutional investors who are not resident in the same country as the remitting company and who do not benefit from double taxation treaties. |

| 1.6 | FTSE Russell |

FTSE Russell is a trading name of FTSE International Limited (FTSE), Frank Russell Company (Russell), FTSE TMX Global Debt Capital Markets Inc. and FTSE TMX Global Debt Capital Markets Limited (together, “FTSE TMX”) and MTSNext Limited. FTSE, Russell and FTSE TMX are each benchmark administrators of indexes. References to FTSE Russell should be interpreted as a reference to the relevant benchmark administrator for the relevant index.

| 1.7 | Statement of Principles for FTSE Russell Non Market Capitalisation Weighted Equity Indexes (the Statement of Principles) |

Indexes need to keep abreast of changing markets and the Ground Rules cannot anticipate every eventuality. Where the Ground Rules do not fully cover a specific event or development, FTSE Russell will determine the appropriate treatment by reference to the Statement of Principles which summarises the ethos underlying FTSE Russell’s approach to index construction. The Statement of Principles is reviewed annually and any changes proposed by FTSE Russell are presented to the FTSE Russell Policy Advisory Board for discussion before approval by FTSE Russell’s Governance Board.

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 3 of 20 |

The Statement of Principles can be accessed using the following link:

Statement of Principles Non-Market Cap Equity Indexes.pdf

| 1.8 | FTSE Russell hereby notifies users of the index that it is possible that circumstances, including external events beyond the control of FTSE Russell, may necessitate changes to, or the cessation of, the index and therefore, any financial contracts or other financial instruments that reference the index should be able to withstand, or otherwise address the possibility of changes to, or cessation of, the index. |

| 1.9 | Index users who choose to follow this index or to buy products that claim to follow this index should assess the merits of the index’s rules-based methodology and take independent investment advice before investing their own or client funds. No liability whether as a result of negligence or otherwise is accepted by FTSE Russell (or any person concerned with the preparation or publication of these Ground Rules) for any losses, damages, claims and expenses suffered by any person as a result of: |

| • | any reliance on these Ground Rules, and/or |

| • | any errors or inaccuracies in these Ground Rules, and/or |

| • | any non-application or misapplication of the policies or procedures described in these Ground Rules, and/or |

| • | any errors or inaccuracies in the compilation of the index or any constituent data. |

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 4 of 20 |

|

Section 2

Management Responsibilities

| 2.0 | Management Responsibilities |

| 2.1 | FTSE International Limited (FTSE) |

| 2.1.1 | FTSE is the benchmark administrator. |

| 2.1.2 | FTSE is responsible for the daily calculation, production and operation of the index and will: |

| • | maintain records of the index weightings of all constituents; |

| • | make changes to the constituents and their weightings in accordance with the Ground Rules; |

| • | carry out the periodic index reviews of the index and apply the changes resulting from the reviews as required by the Ground Rules; |

| • | publicise changes to the constituent weightings resulting from their ongoing maintenance and the periodic reviews; |

| • | disseminate the index. |

| 2.1.3 | FTSE is responsible for monitoring the performance of the Russell 2000 Diversified Factor Index throughout the day and will determine whether the status of the Index should be Firm, Closed, Indicative or Held (see Appendix B). |

| 2.1.4 | These Ground Rules set out the methodology and provide information about the publication of the Russell 2000 Diversified Factor Index. |

| 2.2 | Amendments to these Ground Rules |

| 2.2.1 | These Ground Rules shall be subject to regular review by FTSE Russell to ensure that they continue to meet the current and future requirements of investors and other index users. Any proposals for significant amendments to these Ground Rules will be subject to consultation with FTSE Russell advisory committees and other stakeholders if appropriate. The feedback from these consultations will be considered by the FTSE Russell Governance Board before approval is granted. |

| 2.2.2 | As provided for in Rule 1.7, where FTSE Russell determines that the Ground Rules are silent or do not specifically and unambiguously apply to the subject matter of any decision, any decision shall be based as far as practical on the Statement of Principles. After making any such determination, FTSE Russell shall advise the market of its decision at the earliest opportunity. Any such treatment will not be considered as an exception or change to the Ground Rules, or to set a precedent for future action, but FTSE Russell will consider whether the Ground Rules should subsequently be updated to provide greater clarity. |

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 5 of 20 |

|

Section 3

Queries and Complaints

| 3.0 | Queries and Complaints |

FTSE Russell’s complaints procedure can be accessed using the following link:

Queries and Complaints Policy.pdf

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 6 of 20 |

|

Section 4

Eligible Securities

| 4.0 | Eligible Securities |

| 4.1 | All securities of the Russell 2000 Index on the last business day of each review month are eligible for inclusion in the Russell 2000 Diversified Factor Index. |

| 4.1.1 | All existing constituents of the Russell 2000 Diversified Factor Index are eligible for inclusion in the subsequent review of the Russell 2000 Diversified Factor Index. |

| 4.1.2 | New corporate entities arising from corporate actions that are effective between the data cut-off date and the index review effective date, for which price data is unavailable are not eligible for inclusion. |

| 4.2 | Sector Classification |

All securities in the Russell 2000 Index and Russell Custom Sector Indexes are allocated to one of eight custom sector classifications. Each custom sector classification consists of combinations of Industry Classification Benchmark (ICB) Industries:

| • | Energy/Materials (ICB 0001 Oil & Gas and ICB 1000 Basic Materials) |

| • | Industrials (ICB 2000 Industrials) |

| • | Consumer Goods (ICB 3000 Consumer Goods) |

| • | Health Care (ICB 4000 Health Care) |

| • | Consumer services (ICB 5000 Consumer Services) |

| • | Telecom/Utilities (ICB 6000 Telecommunications and ICB 7000 Utilities) |

| • | Financials (ICB 8000 Financials) |

| • | Technology (ICB 9000 Technology) |

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 7 of 20 |

|

Section 5

Factor Definitions

| 5.0 | Factor Definitions |

The data cut-off date for the determination of all security level factor data is the close of business on the last trading day of the month prior to the review month. Multiple lines of the same company are treated as separate securities.

| 5.1 | Ranking Mechanism |

Securities with missing factor data are temporarily removed from the Eligible Universe and the remaining securities are ranked in ascending order and partitioned into 100 groups. A group consists of securities ranked on the factor of interest with the most attractive group being ranked 100 and the least attractive group being ranked 1.

If N is the number of stocks in the Eligible Universe with valid data, then the group number of a stock with valid data is the value resulting from rounding 100 x stock ranking / N up to the nearest integer. The rank of stocks with same factor value is the average of their positions.

Securities with missing factor data are assigned to a group with rank 50.5.

| 5.2 | Book to Price Ratio |

Latest Book Value | * | 100 | ||

| Market Capitalisation |

Book value is the latest common equity sourced from Thomson Reuters Worldscope as of the data cut-off date. Market capitalisation is the full market capitalisation as of the data cut-off date.

| 5.3 | Return on Equity |

Latest12 month Net Income | * | 100 | ||

| Average Shareholders’ Equity |

Net income is the trailing 12 month net income as of the data cut-off date. Net income is earnings from continuing operations before preferred dividends and excluding discontinued operations and extraordinary items sourced from Thomson Reuters Worldscope. Shareholders’ equity is the average of the most recent and previous fiscal year’s total shareholders’ equity as of the data cut-off date.

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 8 of 20 |

| 5.4 | Momentum |

Momentum is calculated as the 12 month total return in local currency divided by the annualized standard deviation of daily local returns over one year.

12 Month Total Return | * | 100 | ||

| Standard Deviation of Daily Total Return * sqrt(252) |

If a security has a trading history of less than one year, it is allocated a neutral score of 50.5. A minimum of 200 daily price observations are required to constitute a full year.

| 5.5 | Dividend Yield |

Latest 12 month Trailing Dividend | * | 100 | ||

| Market Capitalisation |

Latest 12 month trailing dividend is the sum of ordinary and extra dividends from Thomson Reuters Worldscope as of the data cut-off date. Market Capitalisation is the full market capitalisation as of the data cut-off date.

| 5.6 | Index Back-Histories |

| 5.6.1 | In order to simulate the availability of factor data prior to June 2016 when the Russell diversified factor data is available, all index reviews prior to this date utilise 3 month lagged reported fundamental data except dividend data. |

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 9 of 20 |

|

Section 6

Custom Sector Indexes and Target Weights

| 6.0 | Custom Sector Indexes and Target Weights |

| 6.1 | Custom Sector Indexes |

| 6.1.1 | Only constituents of Russell 2000 Index at each quarterly review are eligible for inclusion in the first year custom sector indexes. |

| 6.1.2 | The composite factor score of each sector in the first year is the rank of the aggregate individual factor ranks of 0.5 * Book to price ratio + 0.5 * Dividend Yield + Return on equity + Momentum within each custom sector. |

| 6.1.3 | The top 70% of stocks by composite factor within each custom sector (See Rule 4.2) form the constituents of the custom sector indexes in the first year. |

| 6.1.4 | The constituents of each custom sector index in the first year are weighted by the normalised reciprocal of stock volatility (see Rule 6.1.5) such that stock weights within each sector sum to 100%. |

| 6.1.5 | Stock volatility is calculated as the standard deviation of the past 252 daily USD total returns as of the data cut-off date. If a stock has less than 200 daily prices available or volatility that is higher than the 99th percentile of the Russell 2000 constituents excluding stocks without volatility data, the volatility measure is set at the 99th percentile. |

| 6.1.6 | Custom sector indexes in consequent years consist of all the constituents in Russell 2000 Diversified Factor Index within same custom sectors, and the custom sector index weights are the headline index weights with same custom sector rescaled to sum to 100%. |

| 6.1.7 | All aspects of the maintenance and calculation of the custom sector indexes follow the FTSE Global Equity Index Series Ground Rules which are available atwww.ftserussell.com. |

| 6.2 | Target Weights |

| 6.2.1 | The composite factor score of each stock is the rank of the aggregated individual factor ranks of 0.5 * Book to price ratio + 0.5 * Dividend Yield + Return on equity + Momentum in the Russell 2000 universe. |

| 6.2.2 | The smoothed composite factor score is the 7 month arithmetic average of the composite factor score. If a security has less than 7 months composite factor score history, the smoothed average score is formed over the available months of data. |

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 10 of 20 |

| 6.2.3 | The top 70% of stocks by smoothed composite factor score within each custom sector universe classification form the Russell 2000 Diversified Factor Index constituents. |

| 6.2.4 | All stocks selected by Rule 6.2.3 are weighted by the reciprocal of stock volatility. Stock weights are rescaled in proportion to the custom sector risk weights as defined in Rules 6.2.5-6.2.6, such that stock weights within a sector sum to the sector risk weight. |

| 6.2.5 | Custom sector risk weights are the normalised reciprocal of sector volatility such that sector risk weights sum to 100%. |

| 6.2.6 | The volatility of each custom sector is calculated as the standard deviation of daily total USD returns over the 252 business days prior to the data cut-off date. |

| 6.2.7 | The target weights are adjusted based on the maximum permitted constituent weight. The maximum permitted constituent weight: |

MIN (50 bps, 5 * ADV/ hypothetical AUM)

| • | ADV = close price as of the data cut-off date x average daily trading volume over the previous 252 trading days. If a stock has ADV that is lower than the 1st percentile of the Russell 2000 constituents excluding stocks without liquidity data, ADV is set to the 1st percentile ADV. If a stock has a price history that is shorter than 200 days or ADV is missing, ADV is set to the 10th percentile ADV. |

| • | The hypothetical AUM is 50 bps of the total market cap of the Russell 2000 as of the data cut-off date. |

| 6.2.8 | Constituents of the Russell 2000 Diversified Factor Index have their weights set to 95% of the maximum permitted weight if their weight exceeds the maximum permitted weight. Excess stock weight is distributed pro-rata across all stocks in the same sector. |

| 6.2.9 | The adjustment process is iterated 10 times or until no position breaches the maximum permitted weight. |

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 11 of 20 |

|

Section 7

Periodic Review of Constituents

| 7.0 | Periodic Review of Constituents |

| 7.1 | Review Dates |

| 7.1.1 | The Russell 2000 Diversified Factor Index and custom sector indexes will be reviewed quarterly in March, June, September and December, based on data at the close of business on the last trading day of the month prior to review, using constituents as of the Monday following the third Friday of the review month for the March, September and December reviews, and using constituents as of the Russell 2000 review implementation date for the June review. |

| 7.1.2 | Changes arising from the March, September and December reviews are announced after the close on the Wednesday following the first Friday of each review month, seven trading days prior to the implementation of the Russell 2000 Diversified Factor Index review. The review will be implemented after the close of business on the third Friday of each review month. |

| 7.1.3 | Changes arising from the June review are announced seven trading days prior to the implementation of the Russell 2000 Diversified Factor Index review. The review will be implemented on the same date as the Russell 2000 annual reconstitution. For details of the implementation dates of Russell 2000, please refer to the Russell U.S. Equity Indexes Construction and Methodology available atRussell-US. |

| 7.2 | Index Membership |

| 7.2.1 | Constituents of the Russell 2000 Diversified Factor Index and the custom sector indexes are determined by the application of the ranking procedure detailed in Rules 6.1 & 6.2 at each quarterly review. |

| 7.3 | Custom Sector Indexes |

| 7.3.1 | Stock weights in custom sector indexes are defined in Rule 6.1. |

| 7.4 | Initial Russell 2000 Diversified Factor Index |

| 7.4.1 | The initial Russell 2000 Diversified Factor Index uses the target weights (see Rule 6.2) at the initial review. |

| 7.5 | Subsequent Russell 2000 Diversified Factor Index |

| 7.5.1 | The weights of Russell 2000 Diversified Factor Index are determined by assessing the weight changes between the pre-rebalance index and target weights (see Rule 6.2). If an existing index constituent has not been assigned a target weight, it is considered to have a target weight of zero. |

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 12 of 20 |

| 7.5.2 | Maximum constituent weights are implemented as defined in Rules 6.2.7-6.2.9. |

| 7.5.3 | The minimum permitted weight change of a stock that has non-zero target weight: |

| 0.5 * target weight * MIN (1, 1/(100*(sector weight in pre-rebalance index – target sector weight))^2) |

| 7.5.4 | The maximum permitted change is stock weight is MIN (25 bps, 0.50 * ADV / hypothetical AUM) |

| 7.5.5 | A new constituent with non-zero target weight ranked in the bottom 40% within the custom sector by smoothed composite factor score will have zero weight. |

| 7.5.6 | An existing constituent of Russell 2000 Diversified Factor Index with zero target weight ranked in the top 80% within the custom sector by smoothed composite factor score will have no weight change. |

| 7.5.7 | Weight changes in excess of the maximum permitted are set to the maximum permitted weight change. |

| 7.5.8 | Weights are normalised such that they sum to one. |

| 7.5.9 | Constituents of the Russell 2000 Diversified Factor Index with weights in excess of the maximum permitted, have weights set to 95% of the maximum permitted weight. The excess weight is distributed pro-rata across all stocks. |

| 7.5.10 | Russell 2000 Diversified Factor Index constituents that are also Russell 2000 Index constituents with weight changes between 0.1 bps and 5 bps have weights set to the pre-rebalance weights. Stock weights are normalised such that they sum to one. This adjustment process is iterated 10 times or until no Russell 2000 Diversified Factor Index constituents that are also Russell 2000 Index constituents have weight changes between 0.1 bps and 5 bps. |

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 13 of 20 |

|

Section 8

Changes to Constituent Companies

| 8.0 | Changes to Constituent Companies |

| 8.1 | Intra-review Additions |

| 8.1.1 | Additions to the Russell 2000 Index will be considered for inclusion in the Russell 2000 Diversified Factor Index and custom sector indexes at the next quarterly review. |

| 8.2 | Intra-review Deletions |

| 8.2.1 | A stock that is removed from the Russell 2000 Index will be removed from Russell 2000 Diversified Factor Index and custom sector indexes. A minimum of two days notice will be provided and its weight will be distributed pro-rata amongst the remaining constituents in the relevant index. |

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 14 of 20 |

|

Section 9

Corporate Actions and Events

| 9.0 | Corporate Actions and Events |

| 9.1 | If a constituent has a stock split, stock consolidation, capital repayment, rights issue, bonus issue, a change in the number of shares in issue or a change in free float, the constituent’s weighting in the Russell 2000 Diversified Factor Index will remain unchanged pre and post such an event. |

| 9.2 | Full details of changes to constituent companies due to corporate actions and events can be accessed in the Corporate Actions and Events Guide for Non Market Capitalisation Weighted Indexes using the following link: |

| Corporate Actions and Events Guide for Non Market Cap Weighted Indexes.pdf |

| A Corporate ‘Action’ is an action on shareholders with a prescribed ex date. The share price will be subject to an adjustment on the ex date. These include the following: |

| • | Capital Repayments |

| • | Rights Issues/Entitlement Offers |

| • | Stock Conversion |

| • | Splits (sub-division) / Reverse splits (consolidation) |

| • | Scrip issues (Capitalisation or Bonus Issue) |

A Corporate ‘Event’ is a reaction to company news (event) that may impact the index depending on the index rules. For example, a company announces a strategic shareholder is offering to sell their shares (secondary share offer) – this could result in a free float weighting change in the index. Where an index adjustment is required FTSE Russell will provide notice advising of the timing of the change.

| 9.3 | Suspension of Dealing |

Suspension of Dealing rules can be found within the Corporate Actions and Events Guide for Non Market Capitalisation Weighted Indexes.

| 9.4 | Takeovers, Mergers and Demergers |

The treatment of takeovers, mergers and demergers can be found within the Corporate Actions and Events Guide for Non Market Capitalisation Weighted Indexes.

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 15 of 20 |

|

Section 10

Indexes Algorithm and Calculation Method

| 10.0 | Indexes Algorithm and Calculation Method |

| 10.1 | Prices |

| 10.1.1 | The Russell 2000 Diversified Factor Index uses official closing mid-market or last trade prices, where available, for securities with local market quotations. Further details can be accessed using the following link: |

Closing Prices Used For Index Calculation.pdf

| 10.1.2 | Thomson Reuters real time exchange rates are used in the index calculations which are disseminated in real-time. Exchange rates used in the End of Day calculations are WM/Reuters Closing Spot Rates™, collected at 16:00 London time (further information on The WM/Reuters Closing Spot Rates service is available from The WM Company). |

| 10.2 | Calculation Frequency |

| 10.2.1 | The Russell 2000 Diversified Factor Index will be calculated on a real-time basis. |

| 10.3 | Index Calculation |

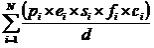

| 10.3.1 | The Russell 2000 Diversified Factor Index is calculated using the algorithm described below: |

Where,

| • | i = 1,2,...,N |

| • | N is the number of securities in the index. |

| • | S the latest trade price of the component security (or the price at the close of the index on the previous day). |

| • | ei is the exchange rate required to convert the security’s currency into the index’s base currency. |

| • | Si is the number of shares in issue used by FTSE Russell for the security, as defined in these Ground Rules. |

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 16 of 20 |

| • | fi is the Investability Weighting Factor to be applied to a security to allow amendments to its weighting, expressed as a number between 0 and 1, where 1 represents a 100% free float. This factor is published by FTSE Russell for each security in the underlying index. |

| • | ci is the Weighting Factor to be applied to a security to correctly weight that security in the index. This factor maps the investable market capitalisation of each stock to a notional market capitalisation for inclusion in the index. |

| • | d is the divisor, a figure that represents the total issued share Capital of the index at the base date. The divisor can be adjusted to allow changes in the issued share Capital of individual securities to be made without distorting the index. |

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 17 of 20 |

|

Appendix A: Index Opening and Closing Hours

Index | Open | Close | ||||||

Russell 2000 Diversified Factor Index | ||||||||

Monday to Friday | 9:30 | 16:10 | ||||||

Notes:

| 1 | Closing prices are downloaded from Thomson Reuters at 16:30. Since the New York Stock Exchange, NYSE Arca and NASDAQ do not release official closing prices until several hours later, the price used in the index may not match this official close. If the downloaded closing price is subsequently overwritten by the official closing price, the downloaded closing price is retained in the index calculation. |

| 2 | The indexes will be calculated during normal trading hours of the New York Stock Exchange, NYSE Arca and NASDAQ will be closed on US holidays. |

| 3 | Timings are based on Eastern Standard Time (EST). |

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 18 of 20 |

|

A Price Index, Total Return Index and Net of Tax Index will be calculated on a real-time basis in US Dollars. The Russell 2000 Diversified Factor Index may exist in the following states.

| A) | Firm |

The Index is being calculated during Official Market Hours (see Appendix A). No message will be displayed against the Index value.

| B) | Closed |

The Index has ceased all calculations for the day. The message ‘CLOSE’ will be displayed against the Index value calculated by FTSE Russell.

| C) | Held |

During Official Market Hours, an Index has exceeded pre-set operating parameters and the calculation has been suspended pending resolution of the problem. The message ‘HELD’ will be displayed against the last Index value calculated by FTSE Russell.

| D) | Indicative |

If there is a system problem or situation in the market that is judged to affect the quality of the constituent prices at any time when the Index is being calculated, the Index will be declared indicative (e.g. normally where a ‘fast market’ exists in the equity market). The message ‘IND’ will be displayed against the Index value calculated by FTSE Russell.

The official opening and closing hours of the Russell 2000 Diversified Factor Index are set out in Appendix A. Variations to the official hours of the Index will be published by FTSE Russell.

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 19 of 20 |

|

Appendix C: Further Information

A Glossary of Terms used in FTSE Russell’s Ground Rule documents can be found using the following link:

Glossary.pdf

Further information on the Russell 2000 Diversified Factor Index is available from FTSE Russell.

For contact details please visit the FTSE Russell website or contact FTSE Russell client services atinfo@ftserussell.com.

Website:www.ftserussell.com

© 2016 London Stock Exchange Group plc and its applicable group undertakings (the “LSE Group”). The LSE Group includes (1) FTSE International Limited (“FTSE”), (2) Frank Russell Company (“Russell”), (3) FTSE TMX Global Debt Capital Markets Inc. and FTSE TMX Global Debt Capital Markets Limited (together, “FTSE TMX”) and (4) MTSNext Limited (“MTSNext”). All rights reserved.

The Russell 2000 Diversified Factor Index is calculated by FTSE or its agent. All rights in the Index vest in FTSE.

FTSE Russell® is a trading name of FTSE, Russell, FTSE TMX and MTS Next Limited. “FTSE®”, “Russell®”, “FTSE Russell®” “MTS®”, “FTSE TMX®”, “FTSE4Good®” and “ICB®” and all other trademarks and service marks used herein (whether registered or unregistered) are trade marks and/or service marks owned or licensed by the applicable member of the LSE Group or their respective licensors and are owned, or used under licence, by FTSE, Russell, MTSNext, or FTSE TMX.

All information is provided for information purposes only. Every effort is made to ensure that all information given in this publication is accurate, but no responsibility or liability can be accepted by any member of the LSE Group nor their respective directors, officers, employees, partners or licensors for any errors or for any loss from use of this publication or any of the information or data contained herein.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any claim, prediction, warranty or representation whatsoever, expressly or impliedly, either as to the results to be obtained from the use of the Russell 2000 Diversified Factor Index or the fitness or suitability of the Index for any particular purpose to which it might be put.

No member of the LSE Group nor their respective directors, officers, employees, partners or licensors provide investment advice and nothing in this document should be taken as constituting financial or investment advice. No member of the LSE Group nor their respective directors, officers, employees, partners or licensors make any representation regarding the advisability of investing in any asset. A decision to invest in any such asset should not be made in reliance on any information herein. Indexes cannot be invested in directly. Inclusion of an asset in an index is not a recommendation to buy, sell or hold that asset. The general information contained in this publication should not be acted upon without obtaining specific legal, tax, and investment advice from a licensed professional.

No part of this information may be reproduced, stored in a retrieval system or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without prior written permission of the applicable member of the LSE Group. Use and distribution of the LSE Group index data and the use of their data to create financial products require a licence with FTSE, Russell, FTSE TMX, MTSNext and/or their respective licensors.

FTSE Russell | Russell 2000 Diversified Factor Index, v1.0, September 2016 | 20 of 20 |