UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13a-16 OR 15d-16 UNDER THE

SECURITIES EXCHANGE ACT OF 1934

December 3, 2012

Commission File No.: 001-34830

D. MEDICAL INDUSTRIES LTD.

(Translation of registrant’s name into English)

Granot mobile post Hefer

Israel

(Address of principal executive offices)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F.

Form 20-F x Form 40-F o

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): _____.

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): _____.

Indicate by check mark whether by furnishing the information contained in this Form, the registrant is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Act of 1934.

Yes o No x

D. MEDICAL INDUSTRIES LTD.

Quarterly Report for the

Period Ended on September 30th, 2012

Date of the Balance Sheet: September 30th, 2012 Date of the Report: November 28th, 2012 |

Table of Contents

| · | Significant Transformations and Innovations that had Occurred in the Corporation’s Businesses; |

| · | The Board of Directors' Report regarding the Corporation's State of Affairs; |

| · | Condensed Consolidated Financial Statements; |

| · | Interim Separate Financial Data; |

| · | Goodwill impairment assessment. |

[Translated From Hebrew]

D. Medical Industries Ltd.

Significant Transformations and Innovations that had Occurred in the

Corporation’s Businesses in the Nine Months that had ended on September 30th,

20121

| 1. | The Company’s Activity and a Description of its Businesses’ Development |

| 1.1. | General |

D. Medical Industries Ltd. (hereinafter: the “Company”) has incorporated in Israel on September 22nd, 1992, as a limited liability private company according to the Companies Ordinance, 5743-1983. On August 29th, 1994, the Company became a public company, having its shares registered for trade in Tel Aviv’s Stock Exchange Ltd. (hereinafter: the “Stock Exchange”).

The Company was founded under the name Peer Maaliyot VeTaasiyot (92) Ltd. On January 1994, the Company changed its name to Ram Tzur Taasiyot Ltd. On January 2001, the Company changed its name to Arit Maarachot Ltd., and on January 2005, the Company changed its name to its current name.

On September 12th, 2011, the Company published a shelf prospectus. As of the date of this report, the Company has published four shelf offering reports according to the aforementioned prospectus.

Since August 2010, after an IPO in the USA, the Company's shares were also traded in the NASDAQ Stock Market. On July 26th, 2012, the trading of Company's shares in the NASDAQ Stock Market was suspended, since the Company did not meet the requirement according to which a Company should have a minimal equity capital of $2,500,000 or a market value of listed shares in a total of $35,000,000 or net income from current operation during the previous full fiscal year or during two out of the three previous full fiscal years in a total of $500,000. Afterwards, the Company turned to the American SEC in a request to remove its shares from listing and registration on the NASDAQ Stock Market. As of the date of this report, the Company's shares are traded in the Stock Exchange and in the OTC Bulletin Board (“Over the Counter”) or in the Pink Sheets.

| 1 | The update is in accordance with the provisions of regulation 39a to the Securities Regulations (Periodic and Immediate Statements), 5730-1970 and includes significant changes and innovations that had occurred in the corporation’s businesses during the nine months period that has ended on September 30th, 2012, and until the date on which this report is published. This report should be read in relation with the Company’s annual statement as of December 31st, 2011 (Form 20-F), that was published on April 30th, 2012. |

| 1.2. | The Company's Holdings |

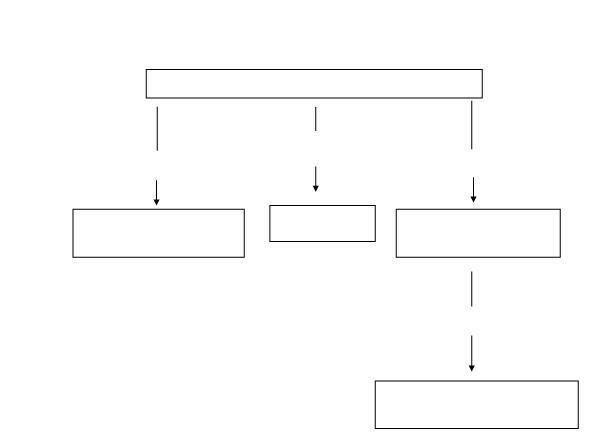

As of the date of this report, the Company holds the entire outstanding capital of Spring Health Solutions LTD. (hereinafter: “Spring Health”), a private company incorporated in Israel, that holds the entire outstanding capital of Spring Health Solutions INC (hereinafter: “Spring INC”), a private company incorporated in Delaware, USA; In addition, the Company holds the entire outstanding capital of G-Sense Ltd. (hereinafter: “G-Sense”)2, a private company incorporated in Israel; and the entire outstanding capital of Spring-Set Health Solutions Ltd. (hereinafter: “Spring-Set”), a private company incorporated in Israel (the Company, Spring Health, Spring INC, G-Sense and Spring-Set shall jointly be referred to hereinafter: the “Group”).

Below is a diagram of the Company’s holdings structure as of the date of this report:

D. Medical Industries Ltd.

G-Sense Ltd.

Spring-Set Health Solutions

Ltd.

Ltd.

Spring Health Solutions

Ltd.

Ltd.

100%

100%

100%

100%

Spring Health Solutions INC

2 | It should be noted that Mr. Avraham Shkalim (hereinafter: “Mr. Shkalim”), who was the CEO of G-Sense, holds stock warrants that may be exercised at any time to ordinary shares of G-Sense in a rate of 8% of G-Sense’s capital stock (in the event that G-Sense or its operation will be sold, Mr. Shkalim shall be entitled to exercise its stock warrants to ordinary shares of G-Sense in a rate of 15% of G-Sense's stock capital) (See Subsection 1.4.9 below). |

2

| 1.3. | Fields of Operation |

As of the date of this report, the Company, through its subsidiaries, holds intellectual property and know-how in the fields of treatment in diabetes and Drug Delivery. In addition, the Company has a little commercial operation in the field of sales of infusion sets to be used with insulin pumps that are manufactured by a sub-contractor in China.

The Company has commenced its operation in relation to medical equipment at the end of 2004. The Company mainly operates through its subsidiary Spring Health, that has developed the Group’s core tehcnology – the spring-based delivery mechanism. Spring Health operates in conjunction with Spring-Set and Spring INC on manufacturing and marketing of the infusion set known by the commercial name SpringTM Universal Infusion Set. G-Sense holds intellectual property and know-how in the field of continuos measurement of the concentration of glucose in the blood.

| 1.4. | Significant Acquisitions and Sales of Assets which are not in the Ordinary Course of Business |

| 1.4.1. | On December 21st, 2004 and February 2nd, 2005, the Company has entered into agreements with Spring Health, in accordance to which the Company acquired (by way of allocation) 72.99% of Spring Health’s outstanding capital stock on the same date (approximately 70% in full dilution, on the same date), in consideration for an investment of US$1,500 in Spring Health. The aforementioned consideration was paid in full. |

In the aforementioned agreement dated February 2nd, 2005, the shareholders of Spring Health who had held Spring Health's shares prior to signing the aforementioned agreement (hereinafter: the “First Shareholders of Spring Health”), were granted, according to their holdings' rate, the option to convert Spring Health’s shares, which were held by them, to the Company's shares, such that in exchange for each single share of Spring Health, the First Shareholders of Spring Health are entitled to receive 80 shares of the Company (2.5 shares after the Company’s capital consolidation). The aforementioned option was exersiced and the shares were converted as specified above.

In addition, it was set that the Company shall pay to the First Shareholders of Spring Health payments in a rate of 2% of the sales of the products of Spring Health and up to a total payment of US$3,000. It should be noted, that all of Spring Health's First Shareholders have exercised their right to convert Spring Health's shares to the Company’s shares, and by doing so, they have lost, in accordance with the aforementioned agreement, their right to receive for the aforementioned payment.

3

| 1.4.2. | On February 13th, 2007, the Company has engaged in an investment agreement with Spring Health, according to which on March 2007, the Company has invested in Spring Health a total sum of US$1,600, and in consideration, the Company’s holdings have been increased to 80.7% of Spring Health’s outstanding capital, in full dilution. |

| 1.4.3. | On Nobember 28th, 2007, the Company’s board of directors has decided to invest $US4,000 in Spring Health such that the Company’s holdings' rate in Spring Health will increase to 86.54% in full dilution. The aforementioned sum was transferred to Spring Health. |

| 1.4.4. | On October 24th, 2007, the Company offered the minority shareholders in Spring Health, who held on that time approximately 13% (not in full dilution) of Spring Health’s outstanding capital, to convert their shares to the Company’s shares in a rate of 60 shares (1.875 shares after the Company’s capital consolidation) for each share of Spring Health. Five of the said minority shareholders have accepted the Company's offer, and on July 2008, the Company has signed an agreement with the aforementioned shareholders, in accordance to which the Company has purchased 49,432 shares of Spring Health from the aforementioned shareholders in considertaion for an allocation of 2,965,920 shares of the Company (92,685 shares after the Company’s capital conslidation). The conversion was performed in its entirety. After performing the aforesaid conversion, the Company held approximately 92.2% of Spring Health’s share capital, in full dilution. |

| 1.4.5. | In accordance with the agreement dated February 6th, 2005, until December 31st, 2011, the remaining shares of Spring Health’s minority shareholders were converted and the options that had been granted to Spring Health's employees to convert their shares to the Company’s shares in a ratio of one Spring Health's share to 2.5 shares of the Company, were exercised. Following the performance of the aforesaid conversions, the Company held the entire share capital of Spring Health. |

4

| 1.4.6. | Loans to Spring Health |

On September 2009, a loan agreement was signed between the Company and Spring Health, in which the Company has granted Spring Health a loan in a sum of approximately 2,630 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On Feburary 2010, a loan agreement was signed between the Company and Spring Health, in which the Company has granted Spring Health a loan in a sum of approximately 5,500 thousand NIS for a year. The loan is index linked and bears an interest in a rate of 4%. The aforementioned loan had been repaid in full according to its terms.

On June 2010, a loan agreement was signed between the Company and Spring Health, in which the Company has granted Spring Health a loan in a sum of 500 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On October 2010, a loan agreement was signed between the Company and Spring Health, in which the Company has granted Spring Health a loan in a sum of approximately 16,000 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On Feburary 2011, a loan agreement was signed between The Company and Spring Health, in which the Company has granted Spring Health a loan in a sum of approximately 6,000 thosuand NIS for four years and eight months. The loan is index linked and bears an interest in a rate of 4%.

On May 2011, a loan agreement was signed between the Company and Spring Health, in which the Company has granted Spring Health a loan in a sum of approximately 10,000 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On December 2011, a loan agreement was signed between the Company and Spring Health, in which the Company exchanged all the loans to Spring Health, the balance of which in the day of the exchange was 44,224 thousand NIS, for a loan in a sum of approximately 44,224 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%. In the aforementioned date, Spring Health was granted an additional loan in a sum of 1,276 thousand NIS under the same terms.

On May 2012, a loan agreement was signed between the Company and Spring Health, in which the Company has granted Spring Health a loan in a sum of approximately 3,000 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

5

In July 2012, a loan agreement was signed between the Company and Spring Health, in which the Company granted Spring Health a loan in a sum of approximately 3,000 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

As of the date of this report, none of the loans which were granted on December 2011, May 2012 and July 2012, or any part hereof, has been repaid.

| 1.4.7. | In accordance with the resolution of the Company’s board of directors dated November 28th, 2007, the Company has engaged with Spring Health and Spring-Set (as a company in establishment) in an agreement regarding the establishment of Spring-Set. Upon the establishment of Spring-Set, the Company has held 90.1% of its outstanding capital. |

| It was agreed, that the Company shall grant Spring-Set a total of $700,000 as a loan to finance its operation. As of the date of this report, the loan (and any part hereof) was not yet repaid. |

| In addidtion, it was set that Spring Health will transfer to Spring-Set the intellectual property which relates to developing a perishable equipment for insulin pumps. It was also agreed, that Spring-Set will sell to Spring Health the products that Spring Health will order from it, in cost prices. In addition, Spring-Set shall pay to Spring Health royalties in a rate of 7% of Spring-Set’s total sales to third parties. |

According to an appended agreement to the aforementioned agreement, Mr. Shkalim, who was the CEO of Spring Health on that time, shall be entitled to an accumulative bonus of up to 1 million U.S. dollars, according to Spring-Set’s sales' rate as specified in the aforementioned appended agreement3. |

| On October 2011, it was agreed with Mr. Shkalim, in an agreement that was validated by the court, that in consideration for 9.9% of his holdings in Spring-Set, Mr. Shkalim shall receive 73,148 shares of the Company. As of the date of this report, the Company holds the entire share capital of Spring-Set. |

| 3 | It should be noted, that the Company is of the opinion that since the employer-employee relations between Spring Health and Mr. Shkalim have concluded, his entitlement to the aforesaid bonus has expired. |

6

| 1.4.8. | Loans to Spring-Set |

On Feburary 2008, the loan mentioned in Section 1.4.7 above was granted, in a sum of approximately 2,514 thousand NIS (which were equal to US$700 thousand) for five years. The loan is index linked and bears an interest in a rate of 4%.

On October 2008, a loan agreement was signed between the Company and Spring-Set, in which the Company has granted to Spring-Set a in a sum of approximately 1,874 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On March 2010, a loan agreement was signed between the Company and Spring-set, in which the Company has granted a loan to Spring-Set in a sum of approximately 2,500 thousand NIS for a year. The loan is index linked and bears an interest in a rate of 4%. On March 2011, the aforementioned loan was repaid.

On June 2010, a loan agreement was signed between the Company and Spring-Set, in which the Company has granted to Spring-Set a loan in a sum of approximately 3,000 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On October 2010, a loan agreement was signed between the Company and Spring-Set, in which the Company has granted to Spring-Set a loan in a sum of approximately 7,500 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On May 2011, a loan agreement was signed between the Company and Spring-set, in which the Company has granted to Spring-Set a loan in a sum of approximately 6,500 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On December 2011, a loan agreement was signed between the Company and Spring-Set, in which the Company has exchanged all of the loans, the balance of which on the date of the exchange was 23,752 thousand NIS, in a loan in a sum of approximately 23,752 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%. On the aforementioned date, Spring-Set was granted another loan in a sum of 1,748 thousand NIS under the same terms. As of the date of this report, the loans specified in this paragraph (and any part hereof) ware not yet repaid.

7

| 1.4.9. | On April 2005, an agreement was signed between the Company and G-Sense (as a company in establishment) and Spring Health, according to which Spring Health assigned and transferred to G-Sense all of its rights in relation to the development of a sensor for a continuous measurment of the glucose level in the blood and in relation to an application for a patent registration that was submitted by Spring Health in relation to the sensor. |

| It was agreed, that in consideration for assigning the rights in the sensor, Spring Health shall be entitled to receive royalties in a rate of 4% of any income that G-Sense will have in relation with the sensor, unlimitedly. |

| The Company has obligated to invest in G-Sense the sum of 2,500 thousand U.S. dollars in accordance with the milestones specified in the aforementioned agreement. As of the the date of this report, the Company has transferred to G-Sense 300 thousand dollars out of the aforementioned sum. |

| According to an appended agreement to the aforementioned agreement, Mr. Shkalim, who was the CEO of Spring Health on that time, shall be entitled, in consideration for his services to G-Sense, to options which may be immediately exercised to G-Sense's shares in an exercise price of 0 NIS per share and in a rate of 8% of the share capital, and in the event that the Company or its operation shall be sold, he shall be entitled to an exercise in a rate of 15% of the share capital. It was further set, that in the event that agreements with strategic partners shall be signed, the aforementioned employee will receive the sums of $100,000 or $200,000, in accordance with the rules set in the aforementioned agreement, or according to G-Sense’s resolution, options which may be exercised to 250,000 or 500,000 shares of the Company, respectively. |

8

| 1.4.10. | Loans to G-Sense |

On October 2006, a loan agreement was signed between the Company and G-Sense, in which the Company has granted to G-Sense a loan in a sum of approximately 330 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On Feburary 2007, a loan agreement was signed between the Company and G-Sense, in which the Company has granted to G-Sense a loan in a sum of approximately 2,982 thousand NIS for five years. The loan is index linked and an interest in a rate of 4%. On December 2007, a loan agreement was signed between the Company and G-Sense, in which the Company has granted to G-Sense a loan in a sum of approximately 2,000 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On September 2009, a loan agreement was signed between the Company and G-Sense, in which the Company has granted to G-Sense a loan in a sum of approximately 1,324 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On June 2010, a loan agreement was signed between the Company and G-Sense, in which the Company has granted to G-Sense a loan in a sum of approximately 1,750 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On September 2011, a loan agreement was signed between the Company and G-Sense, in which the Company has granted to G-Sense a loan in a sum of approximately 700 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

On December 2011, a loan agreement was signed between the Company and G-Sense, in which the Company exchanged all of the loans, the balance of which on the day of the exchange was approximately 11,541 thousand NIS, to a loan in a sum of approximately 11,541 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%. On the aforementioned date, G-Sense was granted an additional loan in a sum of 9 thousand NIS under the same terms.

On July 2012, a loan agreement was signed between the Company and G-Sense was signed, in which the Company granted G-Sense a loan in a sum of approximately 300 thousand NIS for five years. The loan is index linked and bears an interest in a rate of 4%.

As of the date of this report, none of the loans which were granted on December 2011 and July 2012 (or any part hereof), have been repaid.

9

| 1.4.11. | On April 29th, 2012, the Company’s board of directors has resolved that a merger between Spring Health and Spring-Set will be performed, by way of operation sale, effective as of July 1st, 2012. |

| 1.4.12. | On June 19th, 2012, the Company has announced that it is negotiating with an unrelated third party that is engaged in the field of medical equipment in relation to diabetes (hereinafter: the “Target Company”), regarding an execution of an acquisition transaction in which the Company or one of its subsidiaries shall purchase the entire outstanding capital of the Target Company, in considertion for cash and the Company’s and/or the Company’s subsidiary's shares. The aforementioned negotiation has not perfected into a transaction. |

| 1.4.13. | On November 8th, 2012, the Company has announced that it is negotiating with a foreign international company that is engaged in the development and manufacture of devices used for treatment of diabetes, for the purpose of selling the intellectual property which covers various aspects of Spring™ Universal Infusion Set, which is owned by Spring Health and Spring-Set. As of the date of this report, the entire of the aforesaid transaction's terms have not yet been agreed upon, and the said negotiation has not yet been perfected into a binding agreement. |

It is hereby clarified, that Spring™ Universal Infusion Set can be connected to all of the pumps that uses a universal luer lock. In addition, as aforementioned, the Company has additional products that are currently in different commercialization stages, among them a spring-based insulin pump, and that the intellectual property which relates to the aforesaid products shall remain the Company's property.

| 1.5. | Structural changes |

On March 2012, the Company has initiated a strategic reorganization in the Company, designed to significantly reduce the Company's ongoing operating expenses, including by means of a staff reduction and a voluntary reduction in the compensation of, among others, the chairman of the board, the chief executive officer, chief financial officer and the chief operating officer4. Following the resolution regarding the reorganization, the Company has dismissed most of its employees. As of the date of this report, the Company turns its efforts to continuing to support of its existing customer base and to receiving orders for SpringTM Universal Infusion Set, while the Company's efforts in relation to research and development, and some of its efforts in relation to regulatory and commercialization are currently on hold, until an addtional capital shall be raised for the purpose of these goals.

| 4 | It should be noted, that the chief executive officer, chief financial officer and the chief operating officer have cancelled the voluntary reduction about two months following their agreement to it. |

10

The Company has hired the services of Healthios Capital Markets, LLC (herein: “Healthios”), a Chicago-based leading consulting firm that focuses on providing services for companies engaged in health care products, as a financial advisor in relation to the aforementioned reorganization and in a purpose to support the Company in attaining strategic partnership (e.g. OEM, sale of the Company’s technology, in all or in part, or attaining licensing agreements to use the Company’s technology). As of November 28th, 2012, the Company has paid Healthios approximately 52 thousand U.S. dollars in consideration for the services which were provided to the Company by Healthios.

| 2. | Fields of Operation |

| See Section 1.3 above. |

| 3. | Investments in the Company’s Capital and Transactions in the Company's Shares |

Transactions in the Company’s shares

To the Company's best knowledge, during the period that has commenced on January 1st, 2011 and ended on the date of this report, the Company's stakeholder have not performed transactions outside of the stock market.

| 4. | Dividends distribution |

The Company has never declared and, as of the date of the report, the Company does not anticipate paying cash dividends on the Company's ordinary shares in the foreseeable future.

The Company's board of directors has the discretion to declare and pay dividends on the Company's ordinary shares, and it will make a determination to do so on a number of factors, including, among others, our earnings, financial condition and other business and economic factors that the Company's board of directors may deem relevant. The Company may pay dividends in any fiscal year only out of its “profits” (as defined by the Companies Law, 5759-1999), provided that the distribution is not reasonably expected to impair the Company's ability to fulfill its outstanding and expected obligations. In the event that the Company shall not pay dividends, the Company's ordinary shares may be less valuable because a return on the shareholders' investment will only occur if the trading price of the Company's ordinary shares appreciates.

11

| 5. | Financial Information regarding the Group’s Fields of Operation |

The following is a consolidated financial data regarding the Group’s fields of operation (in thousands NIS):

| The Nine Months that had ended on September 30th | |||

| 2011 | 2012 | ||

| Incomes from the operation field | From external | 1,145 | 609 |

| From other operation fields | - | - | |

| Total | 1,145 | 609 | |

| Costs attributed to the operation field | Costs which constitute incomes of another operation field | 8,402 | 2,761 |

| Other costs | - | - | |

| Total | 8,402 | 2,761 | |

| Costs attributed to the operation field | Fixed costs | 4,384 | 1,153 |

| Variable costs | 4,018 | 1,608 | |

| Total | 8,402 | 2,706 | |

| Profit (loss) from routine activities | From routine activities attributed to the owners | (28,884) | (12,584) |

| From routine activities attributed to rights which do not grant control | (3,504) | - | |

| Total | (32,388) | (12,584) | |

| Total assets | 29,454 | 8,743 | |

| Total liabilities | 10,977 | 7,724 | |

| 6. | General Environment and the Influence of external factors on the Group’s Operation |

The following is a description of the fundamental factors which, to the Group’s best knowledge, have or are expected to have a significant influence on the business results or developments of the Group, and their consequences:

| a. | Influence of the Global Crisis |

The year 2011 was characterized with an uneven financial development rate throughout the year, in both the international and local arenas: on the commencement of the year, there were forecasts for the continuation of the recovery of the global economy and the continuation of growth of the Israeli economy, a trend that was realized, among others, by increases of the prices of shares in the capital markets. However, toward the midyear of 2011, the European debt crisis worsened, where fears were growing stronger toward an insolvent Greece. The European crisis has worsened, when the concerns from Greece's lack of capability to perform repayments have become stronger. The European crisis has continued to become stronger and has additionally expanded to central countries in the continent such as Spain and Italy.

12

In the forth quarter of 2011, the European crisis has worsened, and as a result, the leaders of the European countries have decided to take several measures in order to deal with the debts. The transfer of large quantities of funds to the European bank system by the central bank has led, by the end of 2011 and on the commencement of 2012, to a reduction of the uncertainty, to stabilization and even to increases in the prices of the shares in the stocks and corporate bonds markets in the global financial markets. Nonetheless, the uncertainty in relation to all of the aforesaid regarding Spain’s debts and Greece’s political stability kept shaking the markets in 2012 as well.

The global changes influence the Company, especially in relation to the management of the balances of the liquid resources and the exposures to changes in the foreign currency rates. As of the date of this report, to the best knowledge of the Company’s board of directors, the aforesaid crisis has no direct influences on the Company’s operation and its current financial situation, except for the influence of the changes in the foreign currency rates.

The Company’s cash balances are deposited in short-term deposits in the Israeli currency and foreign currency in banks in Israel and the United States. The Company does not have positions in any derivatives.

Nonetheless, even though at this stage, the aforementioned global crisis does not have a direct influence on the Company, it may indirectly influence the Company in the future, such as an influence on the Company’s ability to raise additional funds in the capital market as well as from private investors for the purpose of continuation of its current operation, what might negatively influence its business results and marketing plans and its ability to expand to additional markets. Additionally, the financial crisis might influence the Company’s existing and potential clients, what might, under certain circumstances, indirectly influence on the Company’s operation and incomes. The crisis might bring about a decline in the extent of the financial activity in the markets in which the Company operates.

13

| b. | The State of the Israeli Hi-Tech Market and the Venture Capital Market |

According to an IVC5 survey for the year 2011, Israeli hi-tech companies raised $2.14 billion from local and foreign venture investors, the highest amount in the past 11 years, which constitutes nearly 70% above the amount raised in 2010 and 91% above the amount raised in 2009. |

| However, in the first half of 2012, the venture capital investments amount reached $936 million, an 11% less than the amount which was invested during the first half of 2011, but 62% more than the amount which was invested during the first half of 2010. |

| During the second quarter of 2012, Israeli hi-tech companies raised $453 million from local and foreign investors, which constitutes 6% less than the amount which was raised during the first quarter of 2012 and 20% less than the amount which was raised during the second quarter of 2011. |

| c. | Israel’s Security-Political State |

In times of tranquility in the security situation in Israel, an improvement occurs in the business environment of technological firms including the Company. The aforementioned is realized by the presence of foreign investors in Israel and by an improvement in the investments' atmosphere, which are performed by issuing of Israeli firms in markets in Israel and abroad as well as by mergers and acquisitions.

Deterioration in the security situation might cause a worsening in the market’s financial state, including in the business environment of technological firms, a concern of investors from Israel and abroad to conducting investment transactions in Israeli companies and a difficulty to perform “exits”.

| d. | Product Approval Policy of the Supervising Authorities |

The Group’s operation, mainly in the field of medical equipment, is influenced by the policies of the supervising authorities in the various countries for approving its products.

5 | Israel Venture Capital Research Center – A research center specializing in analyzing the Hi-Tech industry, and that observes the Israeli venture capital market, tendencies, statistics, transactions, etc. The organization is supported by Giza Venture Capital Fund and the IVA, which is Israel Venture Association. The IVC's survey is published on IVC's website www.ivc-online.com. The survey data is brought as is and were not examined by the Company or anyone on its behalf. |

14

The marketing of the Group’s products is conditional upon the receipt of an approval by the health authorities in each country in which the products will be marketed, including an FDA approval and a CE Mark since the Group's products are medical products, as detailed below:

| 1. | CE Mark |

To the Group's best knowledge, based on public publications, the CE Mark is a European standard for products, that constitutes a statement by a manufacturer according to which the product meets the standards of the European Union for health, safety and the environment. The standard ensures free trade between the countries of the European Union and the EFTA countries (Iceland, Liechtenstein and Norway), and permits the customs and enforcement authorities in the European countries to disapprove similar products which do not bear the CE Mark.

In accordance with the European Medical Device Directive regarding medical equipment (93/42/EEC), starting from June 14th, 1998, manufacturers of medical equipment must act according to the instructions of the European Medical Device Directive. Medical equipment is defined as any instrument, apparatus, appliance or material, which is used for medical treatment of human beings or required for the purpose of operation of a medical instrument or apparatus, whether used alone or in combination with additional instruments, including the software necessary for the medical device or which constitutes the product itself, and which is designated for diagnosis and treatment of disease, an injury or handicap, and which is not a medicine.

During the inspection of the medical equipment, the safety and technical features of the product as well as the quality management system of the manufacturer are tested by the European Notified Body, such that by the end of the process, the manufacturer receives the CE Mark as well as ISO13485 standard for the quality management process.

To obtain a CE Mark for the types of medical devices that are manufactured by the Group, the Group must implement a quality management system, or QMS, and create a Technical File demonstrating compliance with the requirements of the European Medical Devices Directive, as well as proving a contractual relationship with The European Authorized Representative. The QMS and the Technical File must be audited by a third-party assessing body, or a notified body, who, if the audit is successful, will issue an EC Certificate. The corporation must then draw up a Declaration of Conformity stating that its products conform to the type described in the EC Certificate and with the provisions of the European Medical Devices Directive, and must affix the CE Mark to all of its products marketed in the EEA.

The European Medical Devices Directive has been recently amended by Directive 2007/47/EC which has strengthened the EEA’s conformity assessment and post-marketing surveillance procedures. The European Commission is also currently reviewing the medical devices legislative framework with the aim of simplifying it and ensuring a more uniform application of the provisions contained in the Directives across the EEA.

15

As of the date of this report, Spring Health received a CE Mark for the first and second generation of the ADI pump and the Insulin delivery system SpringTM Zone, that replaces the second generation of the ADI pump. On September 1st, 2009, Spring Health received a CE Mark for the first version of Spring Hybrid Patch Pump.

On March 24th, 2009, the Company has announced that Spring-Set received a CE Mark for the advanced infusion kit “Lighty” (known by its new name - SpringTM Universal Infusion Set).

It should be noted, that in order to preserve the standards, a qualification exam of the European Qualification Body must be passed every year.

| 2. | U.S. Food and Drug Administration (“FDA”) |

To the Group's best knowledge, based on public publications, the FDA is a federal organization, that belongs to the American Department of Health and Human Services, whose aim is to protect the health of the American public by founding and enforcing a high product standard and by various regulatory demands, that will allow the safety and efficiency of products such as drugs meant to be used by human beings and veterinarian usage, as well as biological products and medical devices.

Foreign companies, that manufacture medical devices and are interested in exporting the devices to the USA, are committed to meeting the regulatory requirements of the FDA prior to exporting the medical devices and also afterwards, since the FDA does not recognize regulatory approvals given by the institutions of other countries. The FDA demands include, among others, manufacture of the medical devices according to a regulation of quality control, receipt of scientific reports regarding the medical devices, and providing an option to the FDA's representatives to oversee the manufacture procedures in the factory.

16

The FDA classifies medical devices into one of three classes. Devices deemed to pose lower risk are placed in either class I or II, which requires the manufacturer to submit to the FDA a premarket notification requesting permission for commercial distribution. This process is known as 510(k) clearance and is usually the shorter process. To obtain 510(k) clearance, the manufacturer must demonstrate that the proposed device is safe and efficient, and is substantially equivalent to other products which are legally marketed in the USA. Some low risk devices are exempt from this requirement. Devices deemed by the FDA to pose the greatest risk, such as life-sustaining, life-supporting or implantable devices, a device deemed to be not substantially equivalent to a previously cleared 510(k) device or a “pre amendment” class III device (in commercial distribution before May 28, 1976) for which premarket applications have not been called, are placed in class III. In general, a class III device cannot be marketed in the United States unless the FDA approves the device after submission of a premarket approval, or a PMA application. The FDA can also impose restrictions on the sale, distribution or use of devices at the time of their clearance or approval, or subsequent to marketing.

After a device receives a clearance or approval and is placed on the market, numerous regulatory requirements apply, including: establishment registration and device listing with the FDA; meeting the strict QSR requirements, which require manufacturers to follow quality assurance procedures during all aspects of the manufacturing process; labeling regulations; regulations regarding operations of marketing of the product; reporting regulations, which require that manufacturers report to the FDA if their device may have caused or contributed to a death or a serious injury or malfunctioned in a way that would likely cause or contribute to a death or a serious injury if the malfunction were to recur; regulations which require manufacturers to report to the FDA field corrections and product recalls or removals if undertaken to reduce a risk to health posed by the device; and post-market surveillance regulations.

Failure to comply with applicable regulatory requirements might result in enforcement actions by the FDA, which may include any of the following sanctions: civil or criminal penalties, recall or seizure of products, operating restrictions, partial suspension or total shutdown of production, refusing requests for 510(k) clearance or PMA approval of new products, and rescinding previously granted 510(k) clearances or withdrawing previously granted PMA approvals.

After obtaining the 510(K) clearance, the manufacturer is required to perform an establishment registration and listing procedure in the FDA’s database. Without performing the said procedure, products cannot be transferred through the customs for sale in the USA. The manufacturer is required for a yearly update of its registration and listing.

17

The ADI Insulin pump of the first generation and the SpringTM Universal Infusion Set were granted the FDA approval for marketing in the USA under the 510(K) procedure.

The Group estimates, based on consultation it has received, that its other products in the field of insulin dripping might require a 510(k) clearance procedure. Regarding the system for monitoring the glucose level, it is still unclear whether the aforesaid process will be sufficient. In the event that the Group shall be required to go through a procedure for obtaining a PMA approval, it will entail longer and more expensive procedures, costs and time.

It should be noted, that the Group’s estimation regarding the types of approvals required for its products as detailed above, the time tables and costs required in relation to obtaining of the above approvals, are anticipatory information, as defined in the Securities law, 5728-1968, that is based on the Company’s estimations of its development potential and preliminary documents that the Company received from relevant professional figures to the development plans detailed above. These estimations might not realize, in whole or in part, or realize in a different manner than as expected. The factors that might influence on the non-realization of the aforesaid estimations, in whole or in part, or on their realization in a different manner than expected, are compliance with the products' feasibility tests, the Group’s success in meeting the goals and dates detailed above, the costs involved in issuing the aforementioned approvals, the Group’s success in developing its products and/or realization of the risk factors that might bear a significant influence on the Group’s operation and business results.

| 3. | The Ministry of Health |

The Group’s operation in Israel will be subject to obtaining permits from the Ministry of Health, which relate to two levels: on the level of importing parts for the production and marketing of the Group’s products, the group is subject to the approval of the Medical Devices and Accessories Unit (“AMR”) in the Ministry of Health’s pharmaceutics department. On the R&D level, human testing will be performed by the group, which is subject to AMR’s and the Ethics Committee (“Helsinki Committee”) approval, as detailed below.

18

| 4. | Medical Devices and Accessories (“AMR”) |

AMR is defined as a device, an accessory, software, chemical material, biological or biotechnological product, that is used in a medical treatment, or is required for the operation of a device or accessory that is used for treatment and that is not designated principally to operate on the human body as medicine. The AMR unit in the Ministry of Health is the body in charge on AMR registration in the State of Israel, the issuance of documents that assist with the exportation of AMR, the grant of various importation permits to the AMR, monitoring the marketing of AMR in Israel and approving clinical experiments with the AMR.

As of the date of this report, the ADI pump of the first generation and the SpringTM Universal Infusion Set have received AMR approval and Free Sale Certificate approval.

| 5. | Public Health Regulations (Medical Experiments on Humans) 5741-1980 (hereinafter: the “Regulations”) and Procedure no. 14 of the Ministry of Health’s Pharmaceutics Department – Medical Experiments on Human Beings (hereinafter: the “procedure”) |

The regulations and procedure set the regularizations for approval of performance of a medical experiment and an experiment with medical equipment, that is defined as a special medical experiment on human beings. According to the procedure, every medical experiment is subject to the Regulations, to the Genetic Information law, 5761-2000, to the procedures’ directives, to the Harmonized Tripartite Guideline for Good Clinical Practice ICH-GCP (E6) and to the directives of ISO 14155-1, 14155-2 (2003): Clinical Investigation of Medical Devices for Human Subjects, as well as circulars and procedures of the Ministry of Health that are published from time to time.

19

The Regulations set that a medical experiment on a human being shall not be approved, unless the Ethics Committee “Helsinki Committee” (see herein) of the hospital intending to perform the experiment has approved its performance and notified the aforesaid in writing to the medical manager of the hospital in which the experiment is taking place and the hospital’s manager was convinced that the experiment does not contradict the “Helsinki Declaration” and is not contradictory to the regulations. In specific cases detailed in the Regulations, an expert opinion is additionally required from the supreme “Helsinki Committee” for medical experiments on human beings, in order to approve the performance of the experiment.

The Ethics Committee was established by virtue of the international convention (The Helsinki Convention) and the duty of which is to approve experiments on human beings aiming to prove the efficiency of instruments, only following their safety was proven on animals and the following conditions, among others, were tested: the latent advantages in the experiment for the participant and society as a whole, which justify the latent risk of the experiment and the inconvenience involved in its performance, and the existing medical and scientific information which justifies the performance of the experiment.

20

| 6. | The Encouragement of Industrial Research and Development Law 5744-1984 (hereinafter: the “R&D Law”) |

The R&D Law sets a series of demands, which must be met by the applicant for benefits for financing a research and development. Whoever was granted the benefits specified under the by the R&D Law should pay to the state’s treasury, royalties from any income derived from the product developed as part of or as a result of the program, including services that are additional or bound in the product. In addition, the R&D law requires that a product that shall be developed as a result of the research and development will be manufactured in Israel only, unless the research committee of the Industry, Trade and Labor Ministry has approved the assignment of manufacture rights of the product outside of Israel. Spring Health was granted grants by the Chief Scientist by virtue of the R&D Law.

On April 7th, 2005, amendment no. 3 to the R&D Law was published. The aforementioned amendment allows, among others, the extraction or sale of knowledge which its development was supported by the grants of the Chief Scientist to third parties outside of Israel, in consideration for a certain part (according to a defined formula) of the consideration that was received in connection with the transaction of the extraction or sale of the knowledge, or in consideration for receiving knowledge from third parties or cooperation in the operation of research and development. The amendment became affective on June 7th, 2005, two months after its publication, and it additionally applies to plans that were approved prior to the day in which the amendment became affective.

21

On January 6th, 2011, amendment no. 5 to the R&D Law was published. The aforesaid amendment sets that a transfer of manufacture abroad of products which were developed as part of one of the support plans of the Chief Scientist is conditional on the Chief Scientist's approval and, in addition, obligates the payment of increased royalties. In addition, the amendment narrows the existing incentive for extracting knowledge from Israel by selling the entire company and ceasing from operating in Israel, as opposed to extracting knowledge when the operation in Israel continues to be carried out, by changing the formula for calculating the sum of the payment to the Chief Scientist as compensation for the loss of knowledge (“The basic amount”). In addition, there were set amendments in the rules of reduction of the basic amount. The amendment came into effect on January 1st, 2011, except with regard to the change of the formula in relation to the calculation of the basic amount and the reduction rules of the basic amount (section 19b of the R&D Law), which shall become effective on the date in which regulations related to the aforesaid section will come into effect.

In this context, it should be noted that on May 14th, 2012, The Encouragement of Research and Development in the Industry Regulations (the Maximal Amount to be Paid in Consideration for Transfer of knowledge according to Sections 19B(b)(1) and (2) of the R&D Law), 5772-2012, were brought to the approval of the Knesset’s finance committee. The said regulations deal with the amount of the maximal payment to be paid by the grantee of the approval in consideration for selling knowledge of a company abroad, which company has been granted a grant from the Chief Scientist. The regulations set that the sale of knowledge only, shall entail a payment of up to 6 times of the total sum of the grants received by the seller according to the R&D Law, and in accordance with other support plans regarding that same knowledge. On the other hand, in the event that the sale of knowledge is performed as part of a transaction in which the seller of knowledge ceases from being a corporation incorporated in Israel, the payment shall not exceed a sum equal to 6 times the total sum of all the grants received according to the R&D Law and in accordance with other support plans regarding any knowledge whatsoever. In an event that the seller of the knowledge has obligated to keeping the research and development operation in Israel, the payment will not exceed 3 times the total of the grants received in relation to the same knowledge or the entire knowledge, according to the circumstances of the matter. According to the above regulations, keeping the research and development operation in Israel, means manning of not less than 75% of the R&D positions (directly or indirectly), based on a monthly average of the six months preceding the submission of the application, for a period of three years since the date of payment in consideration for selling the knowledge. The above regulations have not yet come into effect.

22

| 7. | Canadian Legislation |

The medical equipment field is regulated in Canada by the Federal Canadian Health Department. The Federal Canadian Health Department classifies medical equipment in accordance with the risk that is derived from medical equipment in accordance with the medical equipment classification rules detailed in appendix no. 1 of the Medical Devices Regulations to the Food and Drugs Act. There are four levels of classification in accordance with the level of invasiveness.

The Company is of the opinion, that in light of a review of The Health Canada guidance document Keyword Index to Assist Manufactures in Verifying Class of Medical Devices, that insulin pumps belong to the third classification category (the fourth classification category is the highest invasiveness category).

The Group received a license for the SpringTM Universal Infusion Set from the Canadian Health Department. Based on the aforementioned license, the said infusion set belongs to the second rating category.

In order to import and sell medical equipment in Canada, requirements regarding the equipment’s licensing and the “establishment licensing” must be followed. The significance of the aforesaid is that the equipment imported to Canada or sold within Canada must have a license, and that an entity importing or selling equipment as aforesaid must hold an establishment license (except in the event it is a retailer, a health treatment facility or a manufacturer).

The principal regulatory requirement is the demand for licensing the equipment. Thus, for instance, in order to receive a license for medical equipment that belongs in the third rating category, the manufacturer must submit the following documents to the Canadian Health Department: description of the equipment and the materials used for manufacture and packing the equipment; a description of the equipment characteristics that allow it to be used in medical situations, and the purposes and usages for which it is manufactured; a list of the countries in which the equipment is sold, the amount sold and a summary of problems reported and product returns; a list of standards according to which the equipment was designed and manufactured; in the event that the equipment needs to be sold in a sterile form, a description of the sterilization method; a summary of all the researches on which the manufacturer has based on in order to ensure that the equipment meets the demands for safety and effectiveness, and the conclusions derived from these researches by the manufacturer; a copy of the equipment’s label; in the event of a near patient in vitro diagnostic device, a summary of investigational testing conducted on the device using human subjects under conditions similar to the conditions of use; references of all the reports published that regard the usage, safety and effectiveness of the equipment; and a copy of the quality management system certificate that testifies that the quality management system according to the rules of which the equipment is designed and manufactured, fulfills Canada’s national standards – CAN/CSA-ISO 13485:03, Medical devices – Quality management systems – Requirements for regulatory purposes.

23

The Canadian regulation imposes many obligations on manufacturers, including obligations to follow the Canadian distribution records, treatment of complaints and requirements for reporting on problems.

Failure to conform with the Canadian regulatory regime might result in: (i) notice from Health Canada requiring conformity; (ii) suspension of the device license; (iii) an order for seizure and destruction of non-conforming products; and/or (iii) prosecution for an offence, with penalties including fines of up to $5,000.

The company is performing regulatory registration processes in China and in Mexico – files were submitted to the Mexican authorities and to the consultation company responsible for registering the product in China.

| 7. | A Description of the Corporate's Business according to Fields of Operation |

| a. | The Structure of Competition in the Field of Operation of the Company and the Changes that Occur in it |

Below is a description of several companies engaged in the business:

| 1. | Insulet Corporation (hereinafter: "Insulet") – Insulet is a medical device supplier that develops, manufactures and markets insulin infusion systems for insulin dependent diabetics. Insulet's insulin management system, OmniPod (OmniPod system), includes the OmniPod disposable infusion device as well as personal mobile diabetes manager that operates wirelessly. The FDA approved the sale of the OmniPod system in the USA. |

| 2. | Medtronic Inc. (hereinafter: "Medtronic") – Medtronic is a global company operating in the medical technology arena. It operates through seven divisions that manufacture and sell medical treatments based on devices: heart rhythm management, spine, cardiovascular, neuro-modulation, surgical technologies and Physio-control. Medtronic develops, manufactures and markets its medical devices in over 120 countries. Its major products include solutions for cardiac arrhythmia, cardiovascular diseases, neurological problems, spinal problems, skeletal and muscular system traumas, urological problems and gastric problems, diabetes as well as nose, ear and throat disorders. The Medtronic diabetes division produces external insulin pumps, continuous glucose monitoring devices, Carelink treatment management software and blood glucose meters. |

24

| 3. | Animas Corporation (hereinafter: "Animas") – Animas develops pager-sized automated insulin pumps, "worn" by diabetic patients, providing the body with continuous fast acting insulin. The infusion pumps, connected to a pipe with a needle inserted under the skin, replace the use of periodic insulin injections. Additionally, Animas sells diabetes management software and various pump accessories. It markets its products around the world through a combination of direct sales representatives and distributors. Animas is a Johnson & Johnson subsidiary, subordinated to its LifeScan division. |

| 4. | I-Flow Corporation (hereinafter: "I-Flow") – I-Flow designs, develops and markets drug delivery systems and surgical products for alleviating post surgical pains and treatment of the operated area. I-Flow products are used in hospitals, independent surgical centers, homes etc. The group deals mainly in design, development, production and marketing of advanced, cost-effective ambulatory infusion systems. It operates through a single operation channel; I-Flow has identified two product lines: local anesthetics and intravenous infusion treatment. It produces compact, mobile infusion pumps, catheters and pain kits that enable delivery of local anesthetics, chemotherapy, nutritious additives and other medications. Group customers include hospitals and alternative sites. It markets its products through distributors in the United States, Canada, Europe, Asia, Mexico, Brazil, Australia, New Zealand and the Middle East. |

The leading supplier is Medtronic, which held in 2009 58% of the market. Medtronic's MiniMed Paradigm product sells well: it is the first insulin pump integrated with the company's continuous glucose monitoring system (CGM), providing closer monitoring of glucose levels along with higher quality of living.

Roche, with a 12% market share, is the following leading supplier. Its Accucheck insulin pump is characterized by steady growth due to properties such as three operating menus, four bolus options, five basal profiles and smaller dimensions.

MiniMed (Medtronics) and Disetronic Medical Systems (Roche) were the market leaders in this segment until 2000. Following that year, a market fragmentation began due to the entrance of companies such as Animas Corporation with the R1000 insulin pump, and Eltec with the Cozmo insulin pump. The acquisition of MiniMed, which was considered the leading insulin pump manufacturer in the USA, by Medtronic, and acquisition of Disetronic, one of Europe's leading insulin pump manufacturers by Roche, helped these companies to regain the market share and to obtain control in the global market of the insulin pumps.

25

Currently, Animas holds a global market share of 11% and preserves close competition with Insulet, which has a market share of 10%. Because, as of the date of this report, Insulet is the only company that supplies disposable insulin pumps, it has managed to increase its market share rapidly since entering the arena in 2005.

Hereinafter is a chart detailing the shares of the competitors at the global market of insulin pumps (based on the revenue):

26

| b. | Developments in the Markets of the Segment of Operations, or Changes in Its Clients' Characteristics |

The diabetes treatments market includes drug treatments and treatments through medical devices. The pharmaceutical aspect includes insulin and orally administered anti-diabetes drugs. The devices segment comprises of diagnosis and monitoring devices and a variety of devices for the delivery of insulin. Some of these devices contain pre-loaded insulin doses, and they can be treated both as medical devices and pharmaceutical products. The leading segments of the diabetes products market are as follows:

Insulin, blood glucose meters and related biodegradable materials (e.g. needles, test strips), insulin pumps, insulin delivery devices (e.g. syringes, pens) and anti-diabetes drugs.

In 2010, the global diabetes management market totaled $40 billion and is expected to reach a total of around $114 billion, following an annual growth rate (CAGR) of 13.5%. Insulin, test strips and anti-diabetes drugs are the products that generate the highest revenue in this market.

The anti-diabetic drug market, which is one of the major segments of the global diabetes market, was estimated in 2010 at around $28 billion, with oral drugs being 38% of the segment and injected drugs being over 55% of the segment. The additional major segment of the global diabetes market – the devices sector – was estimated at $16 billion in 2010.

27

The value of the global insulin pump market was estimated at $724.3 million in 2010 and is expected to grow in an annual growth rate (CAGR) of 7.9% and reach $1.2 billion in 2017. According to the market reports and studies, the market is expected to be driven by a fast increase in diabetes prevalence, availability of the monetary refund, positive clinical results in studies related to the insulin pumps usage and the advantages that the insulin pumps provide to the groups of "niche" patients. USA continues to be the largest insulin pump market, driven by a high penetration rate of pumps to the market and the availability of the monetary refunds.

In 2010, the value of the American insulin pump market was estimated at $518.5 million and is expected to be characterized by 8.5% CAGR and reach the value of $915.4 million by 2017. Market growth is expected to be driven by several factors, such as an increase in prevalence of diabetes among people of all ages, higher penetration of insulin pumps to the market and the availability of the monetary refunds.

The global diabetes product market in 2010 (in $ millions) is described below:

Often, coping with diabetes is frustrating and difficult for the patients, since the blood glucose levels are influenced by hydrocarbon content of the meals, physical activity, pressure, existing or developing diseases, hormonal fluctuations, insulin absorption fluctuations and changes in the known influence of insulin on the body. Diabetics with insulin dependent diabetes, and particularly those with type 1 diabetes, require the following treatments:

| 1. | Constant monitoring and daily intake of insulin, as well as increased carbohydrate intake during the day to retain normal blood glucose levels; |

| 2. | Constant insulin supply, known as basal insulin, to address the background metabolic needs. |

28

In addition to the basal insulin, insulin-dependent diabetics require an additional insulin dosage known as "bolus", to compensate for the carbohydrates consumed during meals or as snacks or in order to offset the high doses of glucose in the blood. Diabetics who try to closely control blood glucose levels for preventing long-term complications related to the fluctuations in such levels are at high risk of "over correction" that sometimes causes hypoglycemia. Therefore, the time dedicated to the diabetes management, blood glucose level fluctuations and apprehension of hypoglycemia all contribute to the huge burden carried by patients and their family members.

| c. | Critical Success Factors in the Group’s Operation |

There are several critical success factors relating to the Group’s field of operation, which influence on the Group’s functioning and position in the market:

| 1. | A successful final development of the Group’s products. |

| 2. | Obtaining regulatory approvals in Israel, United States (FDA) and Europe (CE Mark) for all of the Group’s products, for usage and marketing in the aforementioned markets. |

| 3. | The Group’s success in marketing and selling its products in the future on a commercial basis in significant volumes whether directly or through strategic partnerships. |

| d. | The Main Entrance and Exit Barriers of the Field of Operation and the Changes that Occur to Them |

The entrance barriers of the field of operation are mainly the obtaining of regulatory approvals as detailed in Section 6(d) above, intellectual property protections and the ability to set up appropriate distribution channels in the target markets. To the Company's best knowledge, there are no exit barriers from the field of operation.

| e. | Segmentation of Income and Profitability from Products |

As of the date of this report, the Company sells only one product – SpringTM Universal Infusion Set. This sales of the aforementioned infusion set during the third quarter of 2012 constitute the entire sales for the said quarter.

| f. | New products |

As aforementioned, after the performance of the reorganization in the Company, as described in section 1.5 above, the Company has suspended its operation in the fields of research and development until additional funds will be raised for this purpose. The Company may engage in research and development in the future, but there is no assurance that it will do so.

29

| g. | Customers |

The Company does not depend on a single customer or in a small number of customers, the loss of which will significantly influence the Company’s field of operation.

The Company’s main activity is performed in Europe, USA and Canada. The volume of sales does not justify a distribution of the customers according to geographical and socio-economic characteristics.

| h. | Marketing and Distribution |

As specified above, Spring Health, Spring-Set and Spring INC operate in the fields of manufacture and marketing of SpringTM Universal Infusion Set. The said infusion set can be connected to all of the insulin pumps that use a luer lock connector, and fulfilling beyond the minimum requirements of subcutaneous drug delivery, the set includes features such as a hidden auto-retractable needle, a 360 degrees connector and a small and compact needle inserter. The core of the set is based on a mechanism of detecting detachment from the user’s body, that upon the aforesaid detachment activates a mechanism that creates a block of the infusion tube, which causes an alert. The aforementioned infusion set was recommended by a consumer guide of the American Diabetes Association.

On May 24th, 2011, the Company has announced that it has entered into an agreement with a Polish distributer in relation to the distribution of the Company's Spring™ Universal Infusion Sets in Poland. On September 28th, 2012, the Company has announced that a dispute has erupted between the Company and the Polish distributer, who has announced the Company that due to malfunctions that have been revealed, as claimed by distributer, in the infusion set, it is not willing to pay in consideration for the products that have been supplied to it, and has requested to return the products to the Company. The sum of the debt owed by the distributer for the products that have been supplied to it is approximately ˆ38,000. The Company is inspecting its rights in relation to the aforesaid difference of opinion with the assistance of its legal counsels. At this stage, the Company is not proceeding with supplying products to the said distributer.

30

On January 17th, 2012 and January 25th, 2012, the Company has announced that Spring INC has entered into non-exclusive agreements with Better Living Now Inc. and Solora Medical Supplies Inc., respectively, for the distribution of the aforementioned infusion sets in the USA. The agreements were signed for a preliminary period of two years, which is to commence upon the first order of the above companies, and after the aforementioned preliminary period, the agreements will be renewed for periods of one year. Each party can terminate the agreements upon a delivery of a prior 3 months' notice. As of the date of this report, the agreement with Soloara has not been realized.

On February 14th, 2012, the Company has announced that Spring Health and Spring-Set have entered into an exclusive distribution agreement with Nordiclnfu Care AB, a Swedish company, for the distribution of the aforementioned infusion set in the Nordic countries. The abovementioned agreement replaced a previous distribution agreement in relation to the Swedish territory and has expanded the distribution network to the entire Nordic area. The agreement was signed for a preliminary period of three years, which is to commence upon the first order of the above company, and after the aforementioned preliminary period, the agreement will be renewed for periods of one year. Each party may terminate the agreement without a cause upon a delivery of a six months' prior notice. It was also agreed that the parties will set annual sale goals.

On February 14th, 2012, the Company has announced that a distribution agreement with EXXE s.r.l, an Italian company, was terminated by the company, effective as of August 15th, 2012.

On May 14th, 2012, the Company has announced that Spring Health and Spring-Set have entered into an original equipment manufacturer (OEM) agreement with Twobiens Ltd., a leading South Korea based supplier of diabetes treatment and drug delivery products, for the worldwide distribution of the said infusion set under Twobiens' private label. The Agreement is for a term of three years and contains annual sales targets and minimum order quantities estimated at a total of US$5 Million. It was also agreed, that Twobiens shall be responsible for all costs and expenses incurred by it in the performance of its duties and responsibilities under the agreement. In addition, the Company and Spring Health retain all of their proprietary and intellectual property rights. On day June 4th, 2012, the Company has announced that the first payment according to the aforementioned agreement has been received, which payment constitutes a third of the adjustment cost for the necessities of the aforementioned supplier, as detailed in the agreement. As of the date of the report, additional payments have not yet been received from the aforementioned supplier.

31

On June 6th, 2012, the Company announced that Spring INC has signed a non-exclusive agreement with a confidential figure, for the distribution of the aforementioned set in the USA. The agreement was signed for a preliminary period of two years, and it shall be automatically renewed for periods of one year, unless it shall be terminated by either party. Each party may terminate the agreement upon a delivery of three months' prior notice.

Further to the Company's filing dated July 5th, 2011, regarding the engagement of Spring Health with Dex Medical Inc., a Canadian distributer, in a letter of intent for the exclusive distribution of the said infusion set in Canada, the Company has announced on November 15th and November 20th, 2012, that the aforementioned distributer has announced the Company it has decided to cease from serving as the exclusive distributer of the said infusion set in Canada, due to a few reasons. The distributer has indicated, that in the event that a new version of the said infusion set will be developed, it will examine it and consider distributing it in Canada. It should be noted, that the volume of sales to the said distributer has been relatively small since its appointment as the Company's distributer.

| i. | Order Backlog |

| As of the date of the financial statements and as of the date of this report, the Company has no order backlog. |

| For the purpose of this subsection, an “order backlog” shall mean obligating orders that have not yet been realized as incomes in the financial statements. |

| j. | Competition |

| 1. | Insulet Corporation |

Insulet is a U.S. company founded in 2000, which manufactures insulin injection systems for diabetics in the U.S. The company manufactures compact systems designed to be carried and used by the diabetics and enabling control of the disease by injecting insulin and monitoring blood sugar levels. The company was founded in 2000 and its headquarters are in Bedford, Massachusetts.

| 2. | Medtronic Inc. |

Medtronic is engaged in manufacturing and supplying medical equipment, surgical devices and medical products for treatment of patients suffering from various chronic diseases. The company's operation is organized in five business divisions, one of which provided products for treating urological disorders, diabetes, gastroenterology and various neurological disorders. The company was established in 1949 and its headquarters are in Minneapolis, Minnesota. Medtronic manufactures insulin infusion systems for diabetics in the U.S.

| 3. | Vascular Solutions Inc. |

Vascular develops solutions for cardiologists and radiologists throughout the world. The company's products include anti-bleeding bandages, compound for prevention of bleeding under the skin, catheter system for removing arterial blood clots, laser kit for treating varicose veins, etc. Additionally, the company provides access products, including a wire for inter-venous access. The company was established in 1996 and is headquartered in Minneapolis, Minnesota.

32

| 4. | Retractable Technologies Inc. |

The company develops, manufactures and markets safety syringes and other medical safety products. The company's products include insulin syringes, antigen syringes, safety syringes for prevention of infection and protection from wounds, etc. The company was established in 1994 and is headquartered in Texas.

| 5. | Kensey Nash Corporation |

The company develops, manufactures and markets technologies, products, equipment, biological substances and medical solutions for the health care industry. Its flagship product is used to seal open perforations in the vascular system during surgical treatments. The company has additional products including: tissue fusion kits and other biometric products for treating orthopedic injuries etc. The company was established in 1984 and its headquarters are in Pennsylvania, USA.

The following table displays the data of the comparison companies which served for tests of the reasonability of the rate of the gross profit, the R&D and operational profit in 2010-2011 and in the first nine months of 2012 (if published):

| Company | Gross profit | R&D cost rate | Operational profit |

| Insulet | 44.2% | 14.5% | (29.1)% |

| Medtronic | 76.3% | 9.3% | 25.0% |

| Vascular | 66.6% | 11.9% | 16.7% |

| Retractable | 35.6% | 2.4% | (12.8)% |

| Kensey Nash | 67.2% | 24.0% | 22.0% |

| Average | 58.0% | 12.4% | 4.3% |

| Median | 66.6% | 11.9% | 16.7% |

The Company's revenue forecast is based on the Company's multi-annual business plan, with the review of its reasonableness according to the public information with respect to the market in which the Company operates, and the discussions of the Company's management.

The Company's forecast revenue is based on its expected sales in the following product lines:

| 1. | SpringTM Zone pump; |

| 2. | Dedicated infusion set for SpringTM Zone pump; |

| 3. | Hybrid patch pump SpringTM Zone; |

| 4. | Dedicated infusion set for the hybrid pump. |

33

Below is the detailed description of the foregoing:

SpringTM Zone pump

The multi-use insulin pump SpringTM Zone is used as the improved next generation for the Company's "Adi" pump. To the Company's best knowledge, SpringTM Zone pump is the only insulin pump that implements the insulin delivery technology known as IntellispringTM. This technology, backed by a continuous monitoring safety system Total Line ControlTM (TLC), is innovative in the areas of continuous monitoring and control of insulin delivery.

In the beginning of 2012, the Company obtained CE standard for marketing of the pump in Europe, however, due to lack of financing sources, the commercialization operations were frozen. The estimation of the Company's management is that the launch of the product to the distributors will commence during the fourth quarter of 2014.

Dedicated Infusion set for SpringTM Zone pump

Along with the SpringTM Zone pump sales, the Company intends to sell to its distributors also the dedicated disposable infusion set which was developed for the pump.

SpringTM Zone Hybrid Patch Pump

As of the date of this report, the Company is at final stages of developing the SpringTM Zone hybrid patch pump. The system is hybrid since it can be carried as patch pump directly on the body or in a traditional manner by connecting it to the body with the infusion set. The hybrid pump offers, in addition to its small dimensions, also a price tag which is cheaper in comparison to the similar products. The Company intends to use this advantage for future penetration into developing markets, such as BRIC countries, with a low rate of medical insurance and sensitivity for products prices.

The first version of the pump received the CE standard. The Company's management expects that it will finalize the development and design of the pump, including receiving regulatory permission in Europe and the U.S. towards the end of 2014. The Company's forecast does not include the sales of the pump in the BRIC countries due to the high uncertainty involved in penetrating these developing markets.

Dedicated Infusion Set for SpringTM Zone Hybrid Patch Pump

Along with the SpringTM Zone hybrid patch pump sales, the Company intends to sell to its distributors the dedicated infusion set developed for the pump.

34

| k. | Production Capacity |