As filed with the Securities and Exchange Commission on February 12, 2024.

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

AMERICAN BATTERY MATERIALS, INC.

(Exact name of registrant as specified in its charter)

| Delaware | | 1000 | | 22-395644 |

(State or other jurisdiction of

incorporation or organization) | | (Primary Standard Industrial

Classification Code No.) | | (IRS Employer

Identification No.) |

American Battery Materials, Inc.

500 West Putnam Avenue, Suite 400

Greenwich, Connecticut 06830

(800) 998-7962

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Sebastian Lux and David Graber

Co-Chief Executive Officers

American Battery Materials, Inc.

500 West Putnam Avenue, Suite 400

Greenwich, Connecticut 06830

(800) 998-7962

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copy to:

| | | Spencer G. Feldman, Esq.

Olshan Frome Wolosky LLP

1325 Avenue of the Americas, 15th Floor

New York, New York 10019

(212) 451-2300 | | |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended, check the following box. ☐

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer | | ☐ | | Accelerated Filer | | ☐ |

| Non-Accelerated Filer | | ☒ | | Smaller Reporting Company | | ☒ |

| | | | | Emerging Growth Company | | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided to Section 7(a)(2)(B) of the Securities Act. ☐

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. These securities may not be sold until the Registration Statement filed with the Securities and Exchange Commission becomes effective. This preliminary prospectus is not an offer to sell nor does it seek an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | | SUBJECT TO COMPLETION DATED FEBRUARY 12, 2024 |

__________ Shares

AMERICAN BATTERY MATERIALS, INC.

Common Stock

This is a public offering of common stock of American Battery Materials, Inc. We are offering ________ shares. Our common stock is quoted on the OTC Pink Open Market, operated by the OTC Markets Group Inc., under the symbol “BLTH.” On February 9, 2024, our common stock closed at $0.50 per share. We intend to apply for the listing of our common stock for trading on the NYSE American and expect such listing to occur concurrently with this offering. A NYSE American listing, however, is not a condition to completing this offering.

Investing in our common stock involves a high degree of risk. See the section titled “Risk Factors” beginning on page 14 of this prospectus to read about factors you should consider before purchasing shares of our common stock.

| | | Per Share | | | Total | |

| Public offering price | | $ | | | | $ | | |

| Underwriting discounts and commissions(1) | | $ | | | | $ | | |

| Proceeds to us, before expenses | | $ | | | | $ | | |

| (1) | Please see the section of this prospectus entitled “Underwriting’’ for additional information regarding compensation payable to the underwriters. |

We have granted a 30-day option to the underwriters to purchase up to ______ additional shares of our common stock, solely to cover over-allotments, if any, at the public offering price less underwriting discounts and commissions.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of our common stock to purchasers on or about _____, 2024.

The date of this prospectus is __________, 2024

American battery materials, INC.

Table of Contents

About this Prospectus

Neither we nor the underwriters have authorized anyone to provide any information or to make any representations other than those contained in this prospectus. We and the underwriters take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the securities offered hereby and only under circumstances and in jurisdictions where it is lawful to do so. No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus. You should assume that the information appearing in this prospectus is accurate only as of the date on the front of this prospectus only, regardless of the time of delivery of this prospectus, or any sale of a security. Our business, financial condition, results of operations and prospects may have changed since those dates.

We are not, and the underwriters are not, offering to sell or seeking offers to purchase these securities in any jurisdiction where the offer or sale is not permitted. We and the underwriters have not done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the securities as to distribution of the prospectus outside of the United States.

The industry and market data and certain other statistical information used throughout this prospectus are from our own research, surveys or studies conducted by third parties and industry or general publications. Industry publications and third-party research, surveys and studies generally indicate that their information has been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. We are responsible for all of the disclosure contained in this prospectus, and we believe that these sources are reliable; however, we have not independently verified the information contained in such publications. While we are not aware of any misstatements regarding any third-party information presented in this prospectus, their estimates, in particular, as they relate to projections, involve numerous assumptions, are subject to risks and uncertainties, and are subject to change based on various factors, including those discussed under the section entitled “Risk Factors” and elsewhere in this prospectus. Some data are also based on our good faith estimates.

PROSPECTUS SUMMARY

This summary highlights information contained in greater detail elsewhere in this prospectus. This summary is incomplete and does not contain all the information you should consider in making your investment decision. You should read the entire prospectus carefully before investing in our common stock. You should carefully consider, among other things, our financial statements and the related notes and the sections entitled “Risk Factors,” “Summary Consolidated Financial Information,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this prospectus. Unless otherwise indicated or the context otherwise requires, the terms “we,” “us,” “our,” and “our company” refer to American Battery Materials, Inc., a Delaware corporation.

Our Company

We operate as a U.S. based renewable energy company focused on the extraction, refinement and distribution of technical minerals in an environmentally responsible manner. In November 2021, we found ourselves with the unique opportunity to acquire mining claims that historically reported high levels of lithium and other technical minerals. We hired and affiliated ourselves with industry veterans that bring decades of experience, credibility and relationships.

On November 5, 2021, we acquired the rights to 102 federal mining claims located in the Lisbon Valley of Utah for $100,000 plus the future payment of royalties based on a percentage of the net revenue from the sale of lithium produced from a portion of the mining property. The acquisition was driven by historical mineral data from seven existing wells with brine aquifer access. We have not yet commenced any mining operations, and we are an exploration stage issuer, as defined in SEC Regulation S-K Item 1300 (“Regulation S-K 1300”). An independent third-party technical report indicated that further investment and development in the claims was warranted, although no determination has been made whether we have any reserves of minerals. Similarly, no determination has been made whether mineralization could be economically and legally produced or extracted. We have no mineral reserves as defined by Regulation S-K 1300 and we have had no mining revenue to date.

In July 2023, we acquired and staked additional lithium mining claims adjacent to our Lisbon Valley Project in Utah. The new claims have been registered with the Bureau of Land Management (BLM). We now own a total of 743 placer claims over 14,320 acres, comprised of the 102 original claims held and the 641 new claims.

Our Growth Strategy

Our strategic goal is to become a producer of lithium in the United States. We believe that a strategy of employing advanced brine extractive technology methodologies for selective mineral extraction is the most cost-effective and environmentally friendly approach currently available. We believe that this approach is environmentally friendly because we would not deconstruct land structures which leave dirty tailings, but rather we would extract the desired minerals and metals from subsurface brines that re-inject the brines back down into the aquafer to maintain pressure after lithium extraction. We plan, as part of our sustainability goals within our overall environmental, social and governance (“ESG”) strategy, to develop sustainable production operations. Our plan is to develop our projects and strategic equity investments on a measured timeline to provide the potential for both near-term cash flow and long-term value maximization.

We have been executing the necessary steps to determine analytical results from our technical report, which should provide current results, analytical, geotech modeling, aquifer modeling, recharge, flows and depth. We have engaged RESPEC Company LLC as our geotech, engineering and resource management partner to assist in the exploration of the Lisbon Valley brine extraction project. Leveraging its expertise, we will focus on several initiatives, which include the following:

| ● | advancement of geotech, engineering, geology and fieldwork to complete technical reports on the Lisbon Project; |

| ● | understanding Lisbon Valley brines, on and around owned leases; |

| ● | develop a well plan to re-enter, sample and test the “Superior Well,” that has a historical lithium concentration of 340 ppm (parts per million); |

| ● | enter other prospective plugged and abandoned wells, taking brine samples and performing hydrological testing at each identified high potential zone to evaluate the properties of the clastic formation; |

| ● | as information is advanced, prepare technical reports following the Regulation S-K 1300 Standards of Disclosure for Mineral Projects, initially a Preliminary Economic Assessment (PEA) and longer term, a Preliminary Feasibility Study (PFS); |

| ● | test the collected brines for lithium, but also for previously identified high value elements such as cobalt, manganese, magnesium, and suites of metals in the alkaline earth metals, transition metals, and halogens group; and |

| ● | based on the results of the Superior well, develop area resource estimates. |

The Lisbon Valley of Utah also provides many added benefits:

| ● | historically rich industrial and natural resource extraction area; |

| ● | a developed infrastructure including high voltage electrical, proximity to major roadways and rail spurs; and |

| ● | state and local agency support through the Utah Division of Oil, Gas and Mining (UDOGM) and the Trust Land Administration (SITLA). |

We will also look to expand our holdings in the Lisbon Valley area with the acquisition of additional mineral claims and joint venture opportunities. We continue to explore and evaluate opportunities to further expand our resource base and production capacity through the possible acquisition of properties and projects in other areas of the United States, as well as in South America, particularly Argentina.

As part of our strategy for growth, our projects and strategic investments will be developed on a measured timeline, and we will evaluate all opportunities to further expand our resource base and production capacity. We understand that our timelines are subject to a variety of risks and variables, including, without limitation, obtaining permits, approvals and funding. We are also focused on the implementation of direct lithium extraction (DLE) technologies, which we believe have the potential to significantly increase the supply of lithium from our brine projects, similar to the impact which shale did for oil.

To achieve our goal of becoming a producer of lithium, we will rely on our competitive strengths and experienced management team to explore and consider all opportunities to generate revenue and increase our projects, properties and assets, as well as all potential funding options. Some opportunities for growth may be in the form of (i) strategic partnerships, (ii) off-take agreements, (iii) diversification of projects and properties, (iv) acquisitions of companies and technologies, and (v) participation in related commercial development activities.

The Lithium Market

Lithium is on the list of the 35 minerals considered critical to the economic and national security of the United States, as first published by the U.S. Department of the Interior on May 18, 2018. In June 2021, the U.S. Department of Energy published a report titled “National Blueprint for Lithium Batteries 2021-2030” (the “NBLB Report”) which was developed by the Federal Consortium for Advanced Batteries (“FCAB”), a collaboration by the U.S. Departments of Energy, Defense, Commerce, and State. According to the Report, one of the main goals of this U.S. government effort is to “secure U.S. access to raw materials for lithium batteries.” In the NBLB Report, Jennifer M. Granholm, the U.S. Secretary of Energy, states: “Lithium-based batteries power our daily lives from consumer electronics to national defense. They enable electrification of the transportation sector and provide stationary grid storage, critical to developing the clean-energy economy.”

The NBLB Report summarizes the U.S. government’s views on the need for lithium and the expected growth of the lithium battery market as follows:

| ● | “A robust, secure, domestic industrial base for lithium-based batteries requires access to a reliable supply of raw, refined, and processed material inputs…” |

| ● | “The worldwide lithium battery market is expected to grow by a factor of 5 to 10 in the next decade.” |

The growth in electric vehicles (“EVs”) will provide the greatest needs for lithium-based batteries. The NBLB Report states: “Bloomberg projects worldwide sales of 56 million passenger electric vehicles in 2040, of which 17% (about 9.6 million EVs) will be in the U.S. market.” Source: NBLB Report (defined above). Original Source: Bloomberg NEF Long-Term Electric Vehicle Outlook 2019.

In a February 2021 report, Canalys, a global technology market analyst firm, states that global sales of EVs in 2020 increased by 39% year on year to 3.1 million units. This compares with a sales decline of 14% of the total passenger car market in 2020. Canalys forecasts that the number of EVs sold will rise to 30 million in 2028 and EVs will represent nearly half of all passenger cars sold globally by 2030.

Bloomberg’s Long-Term Electric Vehicle Outlook 2021 report states: “The outlook for EV adoption is getting much brighter, due to a combination of more policy support, further improvements in battery density and cost, more charging infrastructure being built, and rising commitments from automakers. Passenger EV sales are set to increase sharply in the next few years, rising from 3.1 million in 2020 to 14 million in 2025. Globally, this represents around 16% of passenger vehicle sales in 2025, but some countries achieve much higher shares. In Germany, for example, EVs represent nearly 40% of total sales by 2025, while China — the world’s largest auto market — hits 25%.”

Regarding the lithium battery growth derived from grid storage demands, the NBLB Report states: “In addition to the EV market, grid storage uses of advanced batteries are also anticipated to grow, with Bloomberg projecting total global deployment to reach over 1,095 GW by 2040, growing substantially from 9 GW in 2018;” and “Bloomberg forecasts 3.2 million EV sales in the U.S. for 2028, and over 200 GW of lithium-ion battery-based grid storage deployed globally by 2028. With an average EV battery capacity of 100 kWh, 320 GWh of domestic lithium-ion battery production capacity will be needed just to meet passenger EV demand.

On August 25, 2022, the Washington Post published an article titled “Did California just kill the gas-powered car?” and with the sub-heading “California’s decision to ban the sales of combustion engine cars is the latest victory in the transition to electric vehicles.” A particularly relevant passage from this article reads as follows:

“…the transition from gas-powered, internal combustion engine vehicles to electric vehicles no longer feels niche, or speculative. It feels inevitable. And this week, another profound development: California, which already leads the nation with 18 percent of new cars sold electric, is expected to approve a regulation to ban the sales of new gas-only powered vehicles by 2035. In addition to EVs, only a limited number of plug-in hybrids will be allowed to be sold. This is a big deal: California’s car market is only slightly smaller than those of France, Italy and Britain — and while many countries have promised to phase out sales of gas cars by such-and-such date, few have concrete regulations like California. Sixteen states have traditionally followed California’s lead in setting its own independent fuel standards — they could soon follow.”

Although no assurance can be given, these recent developments, if left unchallenged, may potentially increase demand for lithium in the United States, as well as globally. Benchmark Mineral Intelligence, a global consulting firm specializing in the battery supply chain market, in a September 6, 2022 report, predicted that:

| ● | demand for lithium-ion batteries is set to grow six-fold by 2032 as global automakers scale up production of EVs; and |

| ● | to meet the world’s lithium requirements would require 74 new lithium mines with an average size of 45,000 tonnes by 2035. |

While these figures are robust relative to historical data, there can be no guarantee that ultimate consumer adoption for EVs and plug-in-hybrid vehicles (PHEV) will drive lithium demand as predicted.

Lithium Brine Deposits and Direct Lithium Extraction

Lithium is mined from three different deposit types: lithium brine deposits, pegmatite lithium deposits (also referred to as “hard rock”), and sedimentary lithium deposits (also referred to as clay deposits). Brine deposits are the most common, accounting for more than half of the world’s known lithium reserves. All our projects are in brine deposits.

As described by the U.S. Geological Survey, lithium brine deposits are accumulations of saline groundwater that are enriched in dissolved lithium. All producing lithium brine deposits share a number of first-order characteristics: (1) arid climate, (2) closed basin containing a playa or salar, (3) tectonically driving subsidence, (4) associated igneous or geothermal activity, (5) suitable lithium source-rocks, and (6) one or more adequate aquifers. South American countries Chile and Argentina are where the majority of the lithium produced from brines originates, as well as Nevada to a much smaller extent.

It is anticipated that we will use a direct lithium extraction (“DLE”), and reinjection of the processed brine back into the subsurface, rather than using evaporation ponds to recover the lithium and other potential mineral from brines, as the project advances to the production stage. This method has been gaining favor in the lithium industry over the last several years because it does not involve the use of evaporation ponds. DLE uses a much smaller footprint than evaporation ponds and is therefore more acceptable from an environmental standpoint. As yet, we have not done any testing for the possibility of using DLE and will not be able to do any testing until samples of brine are acquired from the target formations. See “Risk Factors – Our success as a company producing lithium and related products depends to a great extent on our research and development capabilities for direct lithium extraction and our ability to secure capital for the implementation of brine processing plants.”

DLE technologies precipitate lithium out of brine using filters, membranes, ceramic beads or other equipment, which is often housed in a small warehouse, significantly shrinking the environmental footprint of evaporation ponds used to produce commercial quantities of lithium traditionally. In a DLE operation, brine is pumped to a processing unit where an adsorption, resin or membrane material is used to extract only the lithium from the brine, while spent brine can be reinjected into the basin aquifers. The more rapid production time frame and possible brine reinjection into the aquifer is a key environmental differentiator between the DLE process and traditional lithium process that uses evaporation ponds.

While there may still be challenges around scalability, water consumption, and the possible dilutive effects of brine reinjection, over the past decade many DLE technologies have arisen to separate lithium from brine. DLE has the potential to significantly impact the lithium industry, with implementation on the extraction of lithium brines potentially having a dramatic positive impact on production, capacity, timing, and environmental impact. Similar to the impact shale exploration had on the oil industry, DLE has the potential to significantly increase the supply of lithium from brine projects, nearly doubling lithium production/yield (taking recoveries from 40-60% to 70-90%+) and improving project returns. DLE should also offer lower perceived environmental risk and yield significant environmental benefits when compared to traditional brine ponds, offering sustainability benefits and ESG credentials. It is estimated that approximately 12% of the world’s lithium supply in 2019 was produced using DLE technology. DLE technologies are broadly grouped into three main categories: adsorption, ion exchange and solvent extraction.

| ● | Adsorption physically absorbs lithium chloride (LiCl) molecules onto the surface of a sorbent from a lithium loaded solution. The lithium is then stripped from the surface of the sorbent with water. |

| ● | Ion exchange takes lithium ions from the solution and replaces them with a different positively charged cation that is contained in the sorbent material. An acidic (or basic) solution is required to strip the lithium from the material and regenerate the sorbent material. |

| ● | Solvent extraction removes lithium ions from solution by contacting the solution with an immiscible fluid (i.e., oil or kerosene) that contains an extractant that attaches to lithium ions and brings them into the immiscible fluid. The lithium is then stripped from the fluid with water or chemical treatment. |

Our identification as an “environmentally friendly” business is evidenced by our commitment to deploy direct lithium extraction rather than the typical extraction techniques of hard-rock mining or underground brine water. Unlike those traditional methods for producing lithium, DLE uses filters, membranes, or resin materials to extract the mineral from brine water, resulting in:

| ● | recycling of the majority of the brine water used; |

| ● | consumption of less fossil fuels; |

| ● | reduction in the need for additional processing and alternative mining sources; and |

| ● | leaving a smaller environmental footprint. |

Traditionally, lithium produced from brine water is stored in evaporation ponds. As the water evaporates, the other elements of the brine such as magnesium or calcium precipitate out, leaving the brine more concentrated to produce lithium carbonate. The evaporation process can take from 9 to 18 months depending on the type of project and weather conditions. With DLE, that process can be shortened to days or even hours. DLE also reduces the amount of land required for the pond evaporation process, while the potential to reinject the remaining brine water after the process further reduces the environmental impact.

Our Market Opportunity

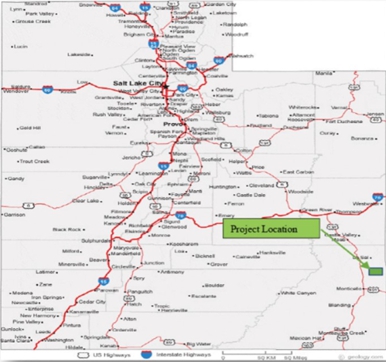

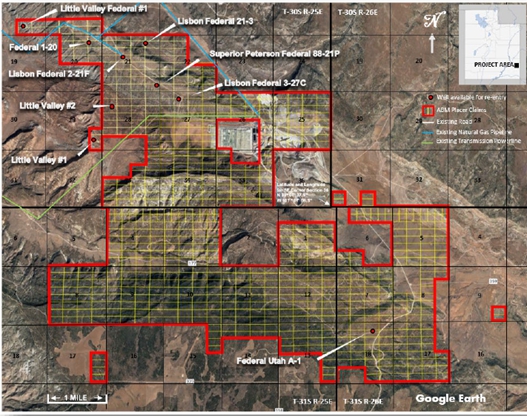

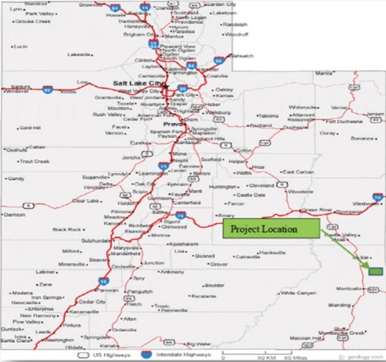

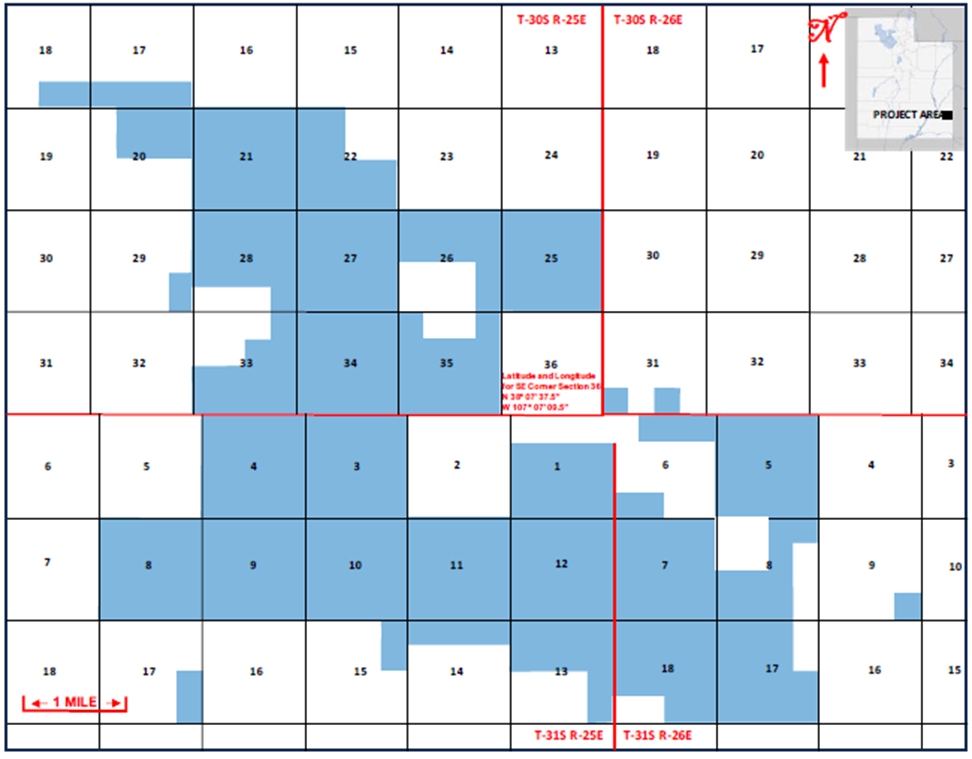

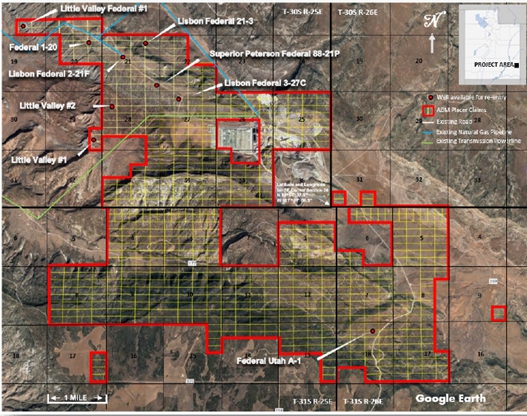

Our Lisbon Valley Lithium Project is located in San Juan County, Utah, approximately 35 miles southeast of the city of Moab, part of an area known as the Paradox Basin. The Project consists of 743 placer mining claims staked on U.S. government land administered by the BLM covering 14,300 acres, part of a semi-contiguous group named the LVL Group. The map below shows the approximate location of our claims:

Our original 102 placer claims were staked by Plateau Ventures LLC and sold to us have been assigned to our wholly owned subsidiary, Mountain Sage Minerals, LLC. Our additional 641 placer claims are registered or filed in the name of Mountain Sage Mineral, LLC. All such claims have been registered currently in good standing according to BLM records. All 743 Claims have been staked, recorded and are in good standing with BLM until next year’s maintenance fee renewal on September 1, 2024. No other mineral, land or water rights have been applied, granted or permitted to or by Mountain Sage Minerals LLC on the subject property. The following diagram is an overview of our claims which comprise our Lisbon Valley Lithium Project:

The maps above are referenced with Professional Land Survey System (PLSS) and a latitude/longitude reference coordinate, accurate to 50 feet.

Our placer claims are plotted on the figures above, which is a Public Land Survey System (PLSS) map using Salt Lake City Prime Meridian. The claims are located in Southeast Utah in sections 17-18, 20-22, 25-29, 33-35 of Township 30 South and Range 25 East; sections 1, 3, 4, 8-15 of Township 31 South and Range 25 East; sections 31 of Township 30 South and Range 26 East and sections 5-9, 17 and 18 of Township 31 South and Range 26 East. The latitude and longitude of the southeast corner of Section 36, Township 30 South, 25 East is noted on the figure is accurate to +/- 50 feet.

There is a network of dirt and paved roads within the claims area, which service the oil and gas wells and the Lisbon Valley Copper Mine. Two existing natural gas pipelines traverse the claims. Power is supplied to the copper mine, also within the claim area, for use in their electrowinning copper recovery process. Nine wellbores (8 oil and gas and 1 potash) are available for re-entry and nearby water rights and private land are available for sale or lease.

Moab, Utah, the nearest population center to the property, is a city of 5,336 persons (2020 Census). It is located in a relatively remote portion of Utah but is easily accessed by U. S. Highway 191. Highway 191 intersects with Interstate 70 about 30 miles (48 kilometers) north of Moab, at Crescent Junction. Moab is a tourist destination and has numerous motels and restaurants. Moab would also be the nearest source of labor in the region.

The region has a history of mining, primarily uranium and vanadium that dates back as far as 1881. The Lisbon Valley Copper Mine is in the heart of the Lisbon Valley and is currently producing copper cathode. An all-weather road and electric power supply the mine. A few gravel roads cross the property. Oil and gas drilling and production, along with ranching have made the area relatively accessible.

There has been no exploration or drilling conducted on the property by us or our predecessors other than the gathering and assimilation of data from all available sources. It will be necessary for us to re-enter an oil and gas well or to drill a new well to obtain brine samples for analysis and metallurgical testing. Permits for such operations will be required from the BLM and the UDOGM. We are in the process of permitting two appraisal wells.

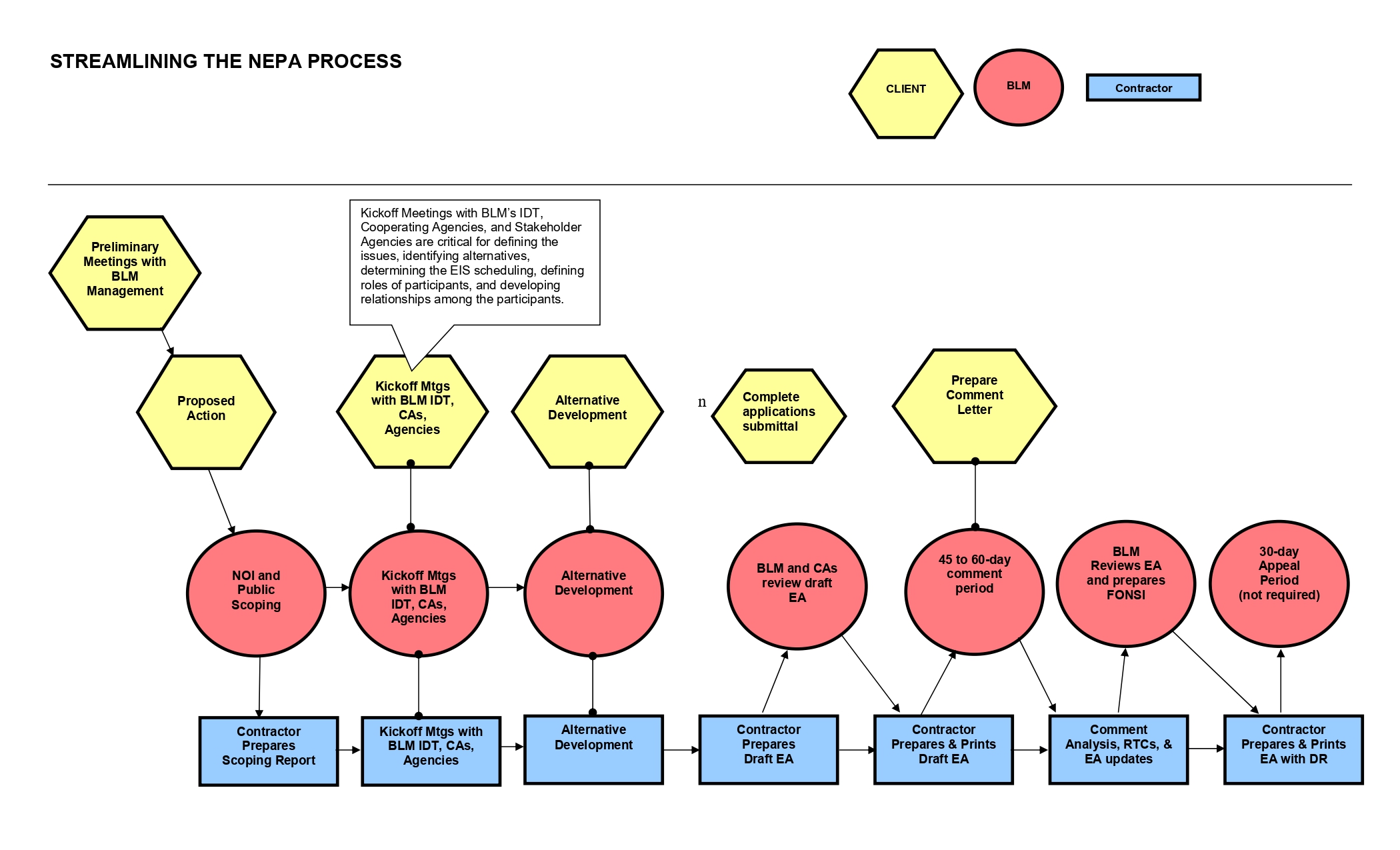

The BLM Permit Process

The flow charts below outline the permit process for exploration of minerals (lithium well drilling) which is regulated by the UDOGM and the BLM. It is anticipated that it will take 300-360 days for approval to drill once the initial application is filed and under review by each agency.

We believe there is abundant evidence from oil, gas and potash wells drilled in the Paradox Basin indicating a probability of identifying and producing super saturated brines from beneath the Project. The geology of the area of the Project and of the Paradox Basin as a whole is complex, although zones have been targeted and proven and they are mappable within and beyond the claims area. It is not likely that the same zones vary significantly in terms of reservoir quality and thickness as evidenced by log analysis; however, these parameters have not been confirmed by actual testing by us.

We have not calculated mineral and resource estimation and has no revenue being generated from the subject property. The only way to determine if the lithium enriched brines exist and can be economically produced from the target zones is to drill exploration wells to produce and test brine from the targeted zones. We through our wholly owned operating company Mountain Sage Minerals, LLC intends to drill two appraisal wells on the subject property to evaluate reservoir properties (porosity, permeability and pressure), flow rates and in situ mineral concentrations. Information from the two wells will be used to assess the resource potential and devise a detailed development plan. The subsurface data collected from the two wells will be used to refine our proprietary subsurface model. The development model will include a proprietary 3D seismic survey to refine the subsurface model and delineate reservoir(s) continuity below the subject property and allow the team to select optimal spacing of future well locations and the network of production and injection wells required to fully develop potential mineral (brine) resources. Based on a substantial number of studies with lithium analyses from the Paradox Basin, we believe there is a substantial indication that lithium mineralization in brines occurs beneath the Project.

We have retained a third-party consulting firm to assist with drilling, completion and review of test results for the two appraisal wells. Any extracted brines should be tested to determine lithium and other important mineral concentrations and to prove the economic viability of a pilot and permanent production program. We have identified an appraisal and development program that is proprietary. This information will be disclosed in an advanced technical report after the appraisal wells are drilled and individual zones are identified and fully evaluated. Cost estimates and authority for expenditures for both well tests and the 3D Survey are currently in process.

The Technical Report Summary on the Project prepared by Bradley C. Peek, MSc. of CPG Peek Consulting, Inc., in accordance with Regulation S-K 1300, is included as an exhibit to this registration statement, of which this prospectus forms a part. The effective date of the report is October 31, 2023.

Selected Risks Associated with Our Business

An investment in our common stock involves a high degree of risk. Our ability to execute on our growth strategies is also subject to certain risks. The risks described under the heading “Risk Factors” immediately following this prospectus summary may have an adverse effect on our business, cash flows, financial condition, and results of operations or may cause us to be unable to execute all or part of these strategies successfully. Below are the principal factors that make an investment in our company speculative or risky:

| ● | Our future performance is difficult to evaluate because we have a limited operating history in the lithium industry. |

| ● | We have a history of losses and expect to continue to incur losses in the future. |

| ● | There is substantial doubt about our ability to continue as a going concern. |

| ● | We are an exploration stage issuer and there is no guarantee that our development will result in the commercial extraction of mineral deposits. |

| ● | We face numerous risks related to exploration, construction and extraction of mineral deposits. |

| ● | The mineral and chemical processing industry is intensely competitive. |

| ● | Our long-term success will depend ultimately on our ability to generate revenues, achieve and maintain profitability, and develop positive cash flows from their lithium activities. |

| ● | Our growth strategy depends on their ability to successfully access the capital and financial markets. Any inability to access the capital or financial markets may limit their ability to meet our liquidity needs and long-term commitments, fund their ongoing operations, execute their business plan or pursue investments that we may rely on for future growth. |

| ● | We are dependent upon key management employees. |

| ● | Our ability to manage growth will have an impact on our business, financial condition, and results of operations. |

| ● | Lawsuits may be filed against us and an adverse ruling in any such lawsuit may adversely affect our business, financial condition or liquidity or the market price of our common stock. |

| ● | Our success as a company producing lithium and related products depends to a great extent on our research and development capabilities for direct lithium extraction and our ability to secure capital for the implementation of brine processing plants. |

| ● | The development of non-lithium battery technologies could adversely affect our company. |

| ● | Our business is subject to cybersecurity risks. |

| ● | Our operations may be further disrupted, and our financial results may be adversely affected by the novel coronavirus pandemic. |

| ● | An escalation of the current war in Ukraine, conflict in the Middle East, or the emergence of conflict elsewhere, may adversely affect our business. |

| ● | We will be required to obtain governmental permits and approvals in order to conduct development and extraction operations, a process that is often costly and time-consuming. There is no certainty that all necessary permits and approvals for our planned operations will be granted. |

| ● | Our operations face substantial regulation of health and safety. |

| ● | Compliance with environmental regulations and litigation based on environmental regulations could require significant expenditures. |

| ● | Lithium prices are subject to unpredictable fluctuations. |

| ● | Changes in technology or other developments could adversely affect demand for lithium compounds or result in preferences for substitute products. |

Corporate and Background Information

We are a Delaware corporation. Our corporate office is located at 500 West Putnam Avenue, Suite 400, Greenwich, Connecticut 06830. Our telephone number is (800) 998-7962. We maintain one active website, www.americanbatterymaterials.com, which serves as our corporate website and contains information about us and our business. Information contained on our website is not a part of this prospectus.

We were originally incorporated in the State of Delaware on March 26, 2007 under the name Internet Media Services, Inc. On April 9, 2010, we filed Form S-1 with the SEC in order to become an SEC reporting company. On January 7, 2014, we entered into an Exchange of Securities Agreement with U-Vend Canada, Inc., and our shareholders under which we acquired all issued and outstanding shares of U-Vend in exchange for shares of our common stock. While the transaction did not result in a change of control of our company, it did result in a new line of business for us. On April 15, 2014, we filed a Certificate of Amendment to change the name of our company to U-Vend Inc. On February 26, 2018, we filed a Certificate of Amendment to change the name of our company to BoxScore Brands, Inc. On October 20, 2022, we filed an amendment to our certificate of incorporation to, among other things, change the name of our company from BoxScore Brands, Inc. to American Battery Materials, Inc. The name change was processed by FINRA, and declared the name change effective as of May 1, 2023.

Channels for Disclosure of Information

Investors and others should note that we use social media to communicate about our company, services, new business developments, and other matters with the public. Any information we consider to be material to an evaluation of our company will be included in filings on the SEC website, http://www.sec.gov, and may also be disseminated using our investor relations website, which can be found at http://www.americanbatterymaterials.com, and press releases. However, we encourage investors, the media, and others interested in our company also to review our social media channels.

The information contained on, or that can be accessed through, our website is not incorporated by reference into this prospectus, and you should not consider any information contained on, or that can be accessed through, our website as part of this prospectus or in deciding whether to purchase our common stock.

Summary of the Offering

Common stock offered | | __________ shares (_______ shares if the underwriters exercise their option to purchase additional shares in full). |

| Common stock outstanding immediately before this offering | | __________ shares. |

| Common stock to be outstanding immediately after this offering | | __________ shares (_______ shares if the underwriters’ option to purchase additional shares is exercised in full). |

| Underwriters’ option to purchase additional shares | |

We have granted a 30-day option to the underwriters to purchase up to an aggregate of _______ additional shares of common stock from us at the public offering price, less underwriting discounts and commissions, on the same terms as set forth in this prospectus. |

| Use of proceeds | | We estimate that our net proceeds from the sale of shares of our common stock in this offering will be approximately $________, or $_______ if the underwriters’ option to purchase additional shares is exercised in full, based on the public offering price of $___ per share, and after deducting underwriting discounts and commissions and estimated offering expenses payable by us. We intend to use a significant portion of the net proceeds from this offering to fund the development and operation of our Lisbon Valley Project, including the drilling, permitting and geological work on the 14,260-acre land position. We may also use a portion of the net proceeds to expand our mineral rights through acquisitions of land and claims, and joint venture opportunities. The remainder of the net proceeds will be used for working capital and other general corporate purposes. See the section titled “Use of Proceeds” for additional information. |

| Risk Factors | | You should carefully read the “Risk Factors” section of this prospectus for a discussion of factors that you should consider before deciding to invest in our common stock. |

| OTC Pink Open Market symbol | | BLTH We intend to apply for the listing of our common stock for trading on the NYSE American and expect such listing to occur concurrently with this offering. A NYSE American listing, however, is not a condition to completing this offering. |

Unless otherwise indicated, all information contained in this prospectus assumes that the underwriters will not exercise their over-allotment option to purchase additional shares of our common stock.

All shares and per share information in this prospectus reflects, and where appropriate, is restated for, a 1-for-300 reverse stock split of our outstanding shares of common stock, effective December 8, 2023.

SUMMARY CONSOLIDATED FINANCIAL DATA

Our consolidated balance sheet data as of December 31, 2022 and December 31, 2021, consolidated statement of operations data and consolidated statement of cash flow data for the years ended December 31, 2022 and December 31, 2021 are derived from our audited financial statements, included elsewhere in this prospectus. Our summary historical interim financial information as of September 30, 2023 and September 30, 2022 and for the nine months ended September 30, 2023 and 2022 are derived from the our unaudited condensed consolidated interim financial statements included elsewhere in this prospectus. Our historical results are not necessarily indicative of the results that may be expected in the future. Per share data and shares outstanding reflect an adjustment for the effect of the 1-for-300 reverse stock split of our outstanding shares of common stock, which became effective on December 8, 2023. This summary of historical financial data should be read together with the financial statements and the related notes, as well as “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” appearing elsewhere in this prospectus.

| | | Nine Months Ended September 30, 2023 (unaudited) | | | Nine Months Ended September 30, 2022 (unaudited) | | | Year Ended December 31, 2022 | | | Year Ended December 31, 2021 | |

| Income Statement Data | | | | | | | | | | | | | | | | |

| Revenue | | $ | - | | | | - | | | | - | | | | - | |

| Loss from operations | | $ | (2,462,799 | ) | | | (1,148,588 | ) | | | (1,135,088 | ) | | $ | (393,376 | ) |

| Net income (loss) | | $ | (2,462,799 | ) | | | (1,148,588 | ) | | | (1,486,848 | ) | | $ | 1,762,466 | |

| Loss per share, basic | | $ | (0.00 | ) | | | (0.00 | ) | | | (0.00 | ) | | $ | 0.01 | |

| Loss per share, diluted | | $ | (0.00 | ) | | | (0.00 | ) | | | (0.00 | ) | | $ | (0.00 | ) |

| Weighted average common shares outstanding, basic | | | 3,324,638,012 | | | | 382,019,948 | | | | 335,778,778 | | | | 210,477,658 | |

| Weighted average common shares outstanding, diluted | | | 3,324,638,012 | | | | 382,019,948 | | | | 335,778,778 | | | | 374,389,986 | |

| | | As of September 30,

2022 (unaudited) | | | As of December 31,

2022 | | | As Adjusted (1) | |

| Balance Sheet Data | | | | | | | | | |

| Cash | | $ | 338,982 | | | | 42,582 | | | | | |

| Working capital | | $ | (3,165,242 | ) | | | (1,400,412 | ) | | | | |

| Total assets | | $ | 625,550 | | | | 205,299 | | | | | |

| Total liabilities | | $ | 3,584,792 | | | | 1,505,711 | | | | | |

| Total stockholders’ equity (deficit) | | $ | (2,959,242 | ) | | | (1,300,412 | ) | | | | |

| (1) | Reflects our sale of ________ shares of common stock offered by this prospectus at an assumed public offering price of $___ per share, after deducting the underwriting discount and the estimated offering expenses that we will pay. |

RISK FACTORS

You should carefully review and consider the risk factors described below and the other information contained in this prospectus, including the financial statements and notes to the financial statements and matters addressed in the section entitled “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” The occurrence of one or more of the events or circumstances described in these risk factors, alone or in combination with other events or circumstances, may have an adverse effect on our business, cash flows, financial condition, and results of operations. We may face additional risks and uncertainties that are not presently known to us, or, or that we currently deem immaterial, which may also harm our business, financial condition, results of operations, and prospects.

Risks Related to Our Business

Our future performance is difficult to evaluate because we have a limited operating history in the lithium industry.

We entered the lithium industry in November 2021. We have not realized any revenues to date from the sale of lithium, and our operating cash flow needs have been financed primarily through issuances of debt and equity securities, and not through cash flows derived from our operations. As a result, we have little historical financial and operating information from our lithium business to help you evaluate our performance.

We have a history of losses and expect to continue to incur losses in the future.

We have an accumulated deficit of approximately $17,854,837 as of December 31, 2022, which increased to $20,317,636 as of September 30, 2023. We expect to continue to incur losses unless and until such time as our projects or one of our future acquired properties enters into commercial production and generates sufficient revenues to fund continuing operations and we are able to develop at least one economic deposit. We recognize that if we are unable to generate cash flows from our operations, we will not be able to earn profits or continue operations. At this early stage of our lithium operations, we also expect to face the risks, uncertainties, expenses and difficulties encountered by companies at the mineral exploration stage. We cannot be sure that we will be successful in addressing these risks and uncertainties and our failure to do so could have a materially adverse effect on our financial condition.

There is uncertainty regarding our ability to implement our business plan and to grow our operations with our existing financial resources without additional financing. Our ability to implement our business plan is dependent on us generating cash from operations, the sale of our stock and/or obtaining debt financing. Historically, we have funded our operations primarily through the issuance of debt and equity securities. Management’s plan to fund our capital requirements and ongoing operations includes the generation of revenue from our lithium operations and projects. Management’s secondary plan to cover any shortfall is selling our equity securities and obtaining debt financing. There is no assurance that we will be successful in implementing our business plan or that we will be able to generate sufficient cash from operations, sell securities or borrow funds on favorable terms or at all. Our inability to generate significant revenue or obtain additional financing could have a material adverse effect on our ability to fully implement our business plan and grow our business to a greater extent than we can with our existing financial resources.

There is substantial doubt about our ability to continue as a going concern.

Our independent registered public accounting firm has included an explanatory paragraph in their report in our audited financial statements for the year ended December 31, 2022 to the effect that our recurring losses since inception and failure to achieve profitable operations raise substantial doubt about our ability to continue as a going concern. Our financial statements do not include any adjustments that might be necessary should we be unable to continue as a going concern within one year after the date that the financial statements are issued. We may be required to cease operations which could result in our stockholders losing all or almost all of their investment.

We are an exploration stage issuer and there is no guarantee that our development will result in the commercial extraction of mineral deposits.

As defined under Regulation S-K Item 1300, we are an exploration stage issuer as we have no known mineral reserves, and we have not yet conducted any mining operations. Accordingly, we cannot assure you that we will ever realize any profits. Any profitability in the future from our business will be dependent upon the development of an economic deposit of minerals and further exploration and development of other economic deposits of minerals, each of which is subject to numerous risk factors. Further, we cannot assure you that any of our property interests can be commercially mined or that any exploration programs will result in profitable commercial mining operations. The exploration and development of mineral deposits involves a high degree of financial risk over a significant period of time, which may or may not be reduced or eliminated through a combination of careful evaluation, experience, and skilled management. While discovery of additional ore-bearing deposits may result in substantial rewards, few properties that are explored are ultimately developed into producing mines. Major expenses may be required to construct processing facilities and to establish reserves.

Our exploration prospects may not contain any reserves and any funds spent on evaluation and exploration may be lost. We do not know with certainty that economically recoverable lithium exists on our properties. In addition, the quantity of any reserves may vary depending on commodity prices. Any material change in the quantity or grade of reserves may affect the economic viability of our properties.

Exploration and development projects like ours have no operating history upon which to base estimates of future operating costs and capital requirements. Actual operating costs and economic returns of any and all exploration projects may materially differ from the costs and returns estimated, and accordingly, our financial condition, results of operations, and cash flows may be negatively affected.

We face numerous risks related to exploration, construction, and extraction of mineral deposits.

Our level of profitability, if any, in future years will depend to a great degree on lithium prices and whether our properties can be brought into production. Exploration and development of lithium resources are highly speculative in nature, and it is impossible to ensure that any of our existing properties will establish reserves. Whether it will be economically feasible to extract lithium depends on a number of factors, including, but not limited to: (i) the particular attributes of the deposit, such as size, grade, and proximity to infrastructure; (ii) lithium prices; (iii) extraction, processing, and transportation costs; (iv) the willingness of lenders and investors to provide project financing; (v) labor costs and possible labor strikes; (vi) non-issuance of permits; and (vii) governmental regulations, including, without limitation, regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting materials, foreign exchange, environmental protection, employment, worker safety, transportation, and reclamation and closure obligations.

We are also subject to the risks normally encountered in the lithium industry, which include, without limitation:

| ● | the discovery of unusual or unexpected geological formations; |

| ● | accidental fires, floods, earthquakes, severe weather, seismic activity, or other natural disasters; |

| ● | unplanned power outages and water shortages; |

| ● | construction delays and higher than expected capital costs due to, among other things, supply chain disruptions, higher transportation costs, and inflation; |

| ● | the ability to obtain suitable or adequate machinery, equipment, or labor; |

| ● | shortages in materials or equipment and energy and electrical power supply interruptions or rationing; |

| ● | environmental liability; and |

| ● | other unknown risks involved in the conduct of lithium exploration and operations. |

The nature of these risks is such that liabilities could exceed any applicable insurance policy limits or could be excluded from coverage. There are also risks against which we cannot insure or against which we may elect not to insure. The potential costs, which could be associated with any liabilities not covered by insurance or in excess of insurance coverage, or compliance with applicable laws and regulations may cause substantial delays and require significant capital outlays, adversely affecting our future earnings, competitive position, and potentially our financial viability.

The mineral and chemical processing industry is intensely competitive.

The mineral and chemical processing industry is intensely competitive. We may be at a competitive disadvantage because we must compete with other individuals and companies, many of which have greater financial resources, operational experience and technical capabilities than we do. Increased competition could adversely affect our ability to attract necessary capital funding or acquire suitable exploration properties. We may also encounter increasing competition from other mineral and chemical processing companies in our efforts to locate acquisition targets, hire experienced mining professionals and acquire exploration resources.

Our quarterly and annual operating and financial results and our revenue are likely to fluctuate significantly in future periods.

Our quarterly and annual operating and financial results are difficult to predict and may fluctuate significantly from period to period. Our revenues, net income and results of operations may fluctuate as a result of a variety of factors that are outside our control including, but not limited to, lack of sufficient working capital, equipment malfunction and breakdowns, inability to timely find spare machines or parts to fix the broken equipment, regulatory or licensing delays and severe weather phenomena.

Our long-term success will depend ultimately on our ability to generate revenues, achieve and maintain profitability, and develop positive cash flows from our lithium activities.

Our ability to (i) acquire additional lithium projects; and (ii) initiate and continue exploration, development, commissioning of lithium ultimately depends on our ability to generate revenues, achieve and maintain profitability, and generate positive cash flow from our operations. The economic viability of our future extraction activities has many risks and uncertainties including, but not limited to:

| ● | significant, prolonged decrease in the market price of lithium; |

| ● | significantly higher than expected construction and extraction costs; |

| ● | significantly lower than expected lithium extraction; |

| ● | significant delays, reductions, or stoppages in lithium extraction activities; |

| ● | significant shortages of adequate and skilled labor or a significant increase in labor costs; |

| ● | significantly more stringent regulatory laws and regulations; and |

| ● | significant difficulty in marketing and/or selling lithium or lithium hydroxide. |

It is common for a new lithium extraction operation to experience unexpected costs, problems, and delays during construction, commissioning and start-up. Most similar projects suffer delays during these periods due to numerous factors, including the factors listed above. Any of these factors could result in changes to economic returns or cash flow estimates of the project or have other negative impacts on our financial position. There is no assurance that our projects will commence commercial production on schedule, or at all, or will result in profitable operations. If we are unable to develop our projects into a commercial operating mine, our business and financial condition will be materially adversely affected. Moreover, even if a feasibility study supports a commercially viable project, there are many additional factors that could impact the project’s development, including terms and availability of financing, cost overruns, litigation or administrative appeals concerning the project, delays in development, and any permitting changes, among other factors.

Our future lithium extraction activities may change as a result of any one or more of these risks and uncertainties. We cannot assure you that any of our activities will result in achieving and maintaining profitability and developing positive cash flows.

We depend on our ability to successfully access the capital and financial markets. Any inability to access the capital or financial markets may limit our ability to meet our liquidity needs and long-term commitments, fund our ongoing operations, execute our business plan or pursue investments that we may rely on for future growth.

Until commercial production is achieved from our planned projects, we will continue to incur operating and investing net cash outflows associated with including, but not limited to, maintaining and acquiring exploration properties, undertaking exploration activities, and the development of our planned projects. As a result, we rely on access to capital markets as a source of funding for our capital and operating requirements. We require additional capital to meet our liquidity needs related to expenses for our various corporate activities, including the costs related to our status as a publicly traded company, fund our ongoing operations, explore and define lithium mineralization, and establish any future lithium operations. We cannot assure you that such additional funding will be available to us on satisfactory terms, or at all.

To finance our future ongoing operations, and future capital needs, we may require additional funds through the issuance of additional equity or debt securities. Depending on the type and terms of any financing we pursue, stockholders’ rights and the value of their investment in our common stock could be reduced. Any additional equity financing will dilute shareholdings. If the issuance of new securities results in diminished rights to holders of our common stock, the market price of our common stock could be negatively impacted. New or additional debt financing, if available, may involve restrictions on financing and operating activities. In addition, if we issue secured debt securities, the holders of the debt would have a claim to our assets that would be prior to the rights of stockholders until the debt is paid. Interest on such debt securities would increase costs and negatively impact operating results.

If we are unable to obtain additional financing, as needed, at competitive rates, our ability to fund our current operations and implement our business plan and strategy will be affected. These circumstances may require us to reduce the scope of our operations and scale back our exploration, development and extraction programs. There is, however, no guarantee that we will be able to secure any additional funding or be able to secure funding to provide us with sufficient funds to meet our objectives, which may adversely affect our business and financial position.

We are dependent upon key management employees.

The responsibility of overseeing the day to day operations and the strategic management of our business depends substantially on our senior management. Loss of any such personnel may have an adverse effect on our performance. The success of our operations will depend upon numerous factors, many of which, in part, are beyond our control, including our ability to attract and retain additional key personnel in sales, marketing, technical support, and finance. Certain areas in which we operate are highly competitive and competition for qualified personnel is significant. We may be unable to hire suitable field personnel for our technical team or there may be periods of time where a particular position remains vacant while a suitable replacement is identified and appointed. We may not be successful in attracting and retaining the personnel required to grow and operate our business profitably.

Our ability to manage growth will have an impact on our business, financial condition, and results of operations.

Future growth may place strains on our financial, technical, operational, and administrative resources and cause us to rely more on project partners and independent contractors, thus, potentially adversely affecting our financial position and results of operations. Our ability to grow will depend on a number of factors, including, but not limited to:

| ● | our ability to develop existing prospects; |

| ● | our ability to identify and acquire or lease new exploratory prospects; |

| ● | our ability to maintain or enter into new relationships with project partners and independent contractors; |

| ● | our ability to continue to retain and attract skilled personnel; |

| ● | the market price for lithium products; and |

| ● | our ability to enter into agreements for the sale of lithium products. |

Lawsuits may be filed against us and an adverse ruling in any such lawsuit may adversely affect our business, financial condition or liquidity or the market price of our common stock.

We may become involved in, named as a party to, or be the subject of, various legal proceedings, including regulatory proceedings, tax proceedings, and legal actions relating to personal injuries, property damage, property taxes, land rights, the environment, and contract disputes. For additional information, refer to “Legal Proceedings”.

The outcome of future legal proceedings cannot be predicted with certainty and may be determined adversely to us and as a result, could have a material adverse effect on our assets, liabilities, business, financial condition, or results of operations. Even if we prevail in any such legal proceeding, the proceedings could be costly, time-consuming, and may divert the attention of management and key personnel from our business operations, which could adversely affect our financial condition.

Our success as a company producing lithium and related products depends to a great extent on our research and development capabilities for direct lithium extraction and our ability to secure capital for the implementation of brine processing plants.

Our success as a producer of lithium and related products is dependent on our ability to develop and implement more efficient production capabilities based on mineral rich brine and implementation of direct lithium extraction (DLE) technologies, which while having the potential to significantly increase the supply of lithium from brine projects, the technology for DLE remains subject to many questions. A number of DLE technologies are emerging and being tested at scale, with a handful of projects already in commercial construction. However, there remain challenges around scalability and water consumption/ brine reinjection. We expect to make significant investment in research and development of the DLE process, and we will need to continue to invest heavily to scale our manufacturing to ultimately producing sufficient amounts of lithium. We cannot assure you that our future product research and development projects and financing efforts will be successful or be completed within the anticipated time frame or budget. There is no guarantee we will achieve anticipated sales target or in a profitable manner. In addition, we cannot assure you that our existing or potential competitors will not develop products which are similar or superior to our products or are more competitively priced. As it is often difficult to project the time frame for developing new products and the duration of market window for these products, there is a substantial risk that we may have to abandon a potential product that is no longer commercially viable, even after we have invested significant resources in the development of such product and our facilities. If we fail in our product launching efforts, our business, prospects, financial condition and results of operations may be materially and adversely affected.

The development of non-lithium battery technologies could adversely affect us.

The development and adoption of new battery technologies that rely on inputs other than lithium compounds could significantly impact our prospects and future revenues. Current and next generation high energy density batteries for use in electric vehicles rely on lithium compounds as a critical input. Alternative materials and technologies are being researched with the goal of making batteries lighter, more efficient, faster charging and less expensive, and some of these could be less reliant on lithium compounds. We cannot predict which new technologies may ultimately prove to be commercially viable and on what time horizon. Commercialized battery technologies that use no, or significantly less, lithium could materially and adversely impact our prospects and future revenues.

Our business is subject to cybersecurity risks.

Our operations depend on effective and secure information technology systems. Threats to information technology systems, such as cyberattacks and cyber incidents, continue to increase. Cybersecurity risks include, but are not limited to, malicious software, attempts to gain unauthorized access to our data and the unauthorized release, corruption or loss of our data and personal information, as well as interruptions in communication and operations. It is possible that our business, financial, and other systems could be compromised, which could go unnoticed for a prolonged period of time. We have not experienced a material breach of our information technologies. Nevertheless, we continue to take steps to mitigate these risks by employing a variety of measures, including employee training, technical security controls, and maintenance of backup and protective systems. Despite these mitigation efforts, cybersecurity attacks and other threats exist and continue to increase, any of which could have a material adverse effect on our business, results of operations, financial condition, and cash flows.

Risks Related to Regulation

We will be required to obtain governmental permits and approvals in order to conduct development and extraction operations, a process that is often costly and time-consuming. There is no certainty that all necessary permits and approvals for our planned operations will be granted.

We are required to obtain and renew governmental permits and approvals for our exploration and development activities and, prior to extracting any mineralization we discover, we will be required to obtain additional governmental permits and approvals that we do not currently possess. Obtaining and renewing any of these governmental permits is a complex, time consuming and uncertain process involving numerous jurisdictions, public hearings, and possibly costly undertakings. The timeliness and success of permitting efforts are contingent upon many variables not within our control, including the interpretation of approval requirements administered by the applicable governmental authority.

We may not be able to obtain or renew permits or approvals that are necessary to our planned operations, or we may discover that the cost and time required to obtain or renew such permits and approvals exceeds our expectations. Any unexpected delays, costs or conditions associated with the governmental approval process could delay our planned exploration, development and extraction operations, which in turn could materially adversely affect our prospects, revenues, and profitability. In addition, our prospects may be adversely affected by the revocation or suspension of permits or by changes in the scope or conditions to use of any permits obtained.

Private parties, such as environmental activist organizations, frequently attempt to intervene in the permitting process to persuade regulators to deny necessary permits or seek to overturn permits that have been issued. These third-party actions can materially increase the costs, cause delays in the permitting process, and could cause us to not proceed with the development or operation of a property. In addition, our ability to successfully obtain key permits and approvals to explore for, develop, operate, and expand operations will likely depend on our ability to undertake such activities in a manner consistent with the creation of social and economic benefits in the surrounding communities, which may or may not be required by law. Our ability to obtain permits and approvals and to successfully operate in particular communities may be adversely affected by real or perceived detrimental events associated with our activities.

Our operations face substantial regulation of health and safety.

Our operations are subject to extensive and complex laws and regulations governing worker health and safety across our operating regions and our failure to comply with applicable legal requirements can result in substantial penalties. Future changes in applicable laws, regulations, permits and approvals or changes in their enforcement or regulatory interpretation could substantially increase costs to achieve compliance, lead to the revocation of existing or future exploration or mining rights or otherwise have an adverse impact on our results of operations and financial position.

Our mining claims are inspected on a regular basis by government regulators who may issue citations and orders when they believe a violation has occurred under local mining regulations. If inspections result in an alleged violation, we may be subject to fines, penalties or sanctions and our mining operations could be subject to temporary or extended closures.

In addition to potential government restrictions and regulatory fines, penalties or sanctions, our ability to operate (including the effect of any impact on our workforce) and thus, our results of operations and our financial position (including because of potential related fines and sanctions), could be adversely affected by accidents, injuries, fatalities or events detrimental (or perceived to be detrimental) to the health and safety of our employees, the environment or the communities in which we operate.

Compliance with environmental regulations and litigation based on environmental regulations could require significant expenditures.

Environmental regulations mandate, among other things, the maintenance of air and water quality standards, land development, and land reclamation, and set forth limitations on the generation, transportation, storage, and disposal of solid and hazardous waste. Environmental legislation is evolving in a manner that may require stricter standards and enforcement, increased fines and penalties for non-compliance, more stringent environmental assessments of proposed projects, and a heightened degree of responsibility for mining companies and their officers, directors, and employees. We may incur environmental costs that could have a material adverse effect on financial condition and results of operations. Any failure to remedy an environmental problem could require us to suspend operations or enter into interim compliance measures pending completion of the required remedy.

Moreover, governmental authorities and private parties may bring lawsuits based upon damage to property and injury to persons resulting from the environmental, health, and safety impacts of prior and current operations. These lawsuits could lead to the imposition of substantial fines, remediation costs, penalties, and other civil and criminal sanctions, as well as reputational harm, including damage to our relationships with customers, suppliers, investors, governments or other stakeholders. Such laws, regulations, enforcement, or private claims may have a material adverse effect on our financial condition, results of operations, or cash flows.

Lithium prices are subject to unpredictable fluctuations.

We expect to derive revenues, if any, from the extraction and sale of lithium. The prices of lithium may fluctuate widely and are affected by numerous factors beyond our control, including international, economic, and political trends, expectations of inflation, currency exchange fluctuations, interest rates, global or regional consumptive patterns, speculative activities, increased production due to new extraction developments and improved extraction and production methods and technological changes in the markets for the end products. The effect of these factors on the prices of lithium and lithium byproducts, and therefore the economic viability of any of our exploration properties, cannot accurately be predicted.

Changes in technology or other developments could adversely affect demand for lithium compounds or result in preferences for substitute products.

Lithium and its derivatives are preferred raw materials for certain industrial applications, such as rechargeable batteries. For example, current and future high energy density batteries for use in electric vehicles will rely on lithium compounds as a critical input. The pace of advancements in current battery technologies, development and adoption of new battery technologies that rely on inputs other than lithium compounds, or a delay in the development and adoption of future high nickel battery technologies that utilize lithium could significantly impact our prospects and future revenues. Many materials and technologies are being researched and developed with the goal of making batteries lighter, more efficient, faster charging, and less expensive, some of which could be less reliant on lithium or other lithium compounds. Some of these technologies, such as commercialized battery technologies that use no, or significantly less, lithium compounds, could be successful and could adversely affect demand for lithium batteries in personal electronics, electric and hybrid vehicles, and other applications. We cannot predict which new technologies may ultimately prove to be commercially viable and on what time horizon. In addition, alternatives to industrial applications dependent on lithium compounds may become more economically attractive as global commodity prices shift. Any of these events could adversely affect demand for and market prices of lithium, thereby resulting in a material adverse effect on the economic feasibility of extracting any mineralization we discover and reducing or eliminating any reserves we identify.

Risks Related to this Offering and Ownership of Our Common Stock

An active trading market for our common stock may not develop, and you may be unable to resell your shares at or above the public offering price.

Our common stock trading over the counter has not been historically active. Although we intend to apply for listing our common stock for trading on the NYSE American, an active trading market for our shares may never develop or be sustained following this offering. No assurance can be given that our common stock will be accepted to trade on the NYSE American. The public offering price of our common stock will be determined through negotiations between us and the underwriters. This public offering price may not be indicative of the market price of our common stock after the offering. In the absence of an active trading market for our common stock, investors may not be able to sell their common stock at or above the public offering price or at the time that they would like to sell.

Our stock price may be volatile, and the market price of our common stock after this offering may drop below the price you pay due to a variety of factors, many of which are beyond our control.

The market price of our common stock could be subject to significant fluctuations after this offering, and it may decline below the public offering price. Market prices for securities of early-stage companies have historically been particularly volatile. As a result of this volatility, you may not be able to sell your common stock at or above the public offering price. Some of the factors that may cause the market price of our common stock to fluctuate include:

| ● | fluctuations in our quarterly financial results or the quarterly financial results of companies perceived to be similar to our company; |

| ● | changes in estimates of our financial results or recommendations by securities analysts; |