UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2020

Commission File Number: 000-54191

SINO AGRO FOOD, INC.

(Exact Name of Registrant as Specified in its Charter)

| Nevada | 33-1219070 |

| | |

| (State or Other Jurisdiction ofIncorporation) | (IRS Employer Identification Number) |

Room 3520, Block A, China Shine Plaza

No. 9 Lin He Xi Road

Tianhe District, Guangzhou City, P.R.C. 510610

(Address of principal executive offices, including zip code)

Registrant’s Telephone Number, including area code: (+86)-20-22116293

Securities registered pursuant to Section 12(b) of the Exchange Act: None

Securities registered pursuant to Section 12(g) of the Exchange Act: Common Stock, $0.001 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this annual report or any amendment to this annual report. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,”“accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer ¨ | Accelerated Filer ¨ |

| Non-Accelerated Filer o | Smaller Reporting Company x |

| | Emerging growth company x |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

The aggregate market value of the voting stock held by non-affiliates of the issuer on June 16th 2021, based upon the $0.086 per share closing price of such stock on that date, was in round figure of $5,118,413.00.

There were 60,356,776 shares of our common stock issued and outstanding consisting 59,516,423 free trading shares and 840,353

Documents incorporated by reference: None

FORWARD-LOOKING STATEMENTS

This Annual Report contains “forward-looking statements,” within the meaning of the Private Securities Litigation Reform Act of 1995 and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The Company intends such forward-looking statements to be covered by the safe harbor provisions for forward-looking statements contained in Section 21E of the Exchange Act. Forward-looking statements can be identified by the use of forward-looking terminology, such as “estimates,” “projects,” “plans,” “believes,” “expects,” “anticipates,” “intends,” or the negative thereof or other variations thereon, or by discussions of strategy that involve risks and uncertainties These statements reflect management’s current beliefs and are based on information now available to it. Accordingly, these statements are subject to certain risks, uncertainties and contingencies that could cause the Company’s actual results, performance or achievements in 2017 and beyond to differ materially from those expressed in, or implied by, such statements. Such statements, include, but are not limited to, statements contained in this Annual Report relating to the Company’s business, financial performance, business strategy, recently announced transactions and capital outlook. Important factors that could cause actual results to differ materially from those in the forward-looking statements include: a continued decline in general economic conditions nationally and internationally; decreased demand for our products and services; market acceptance of our products; the impact of any litigation or infringement actions brought against us; competition from other providers and products; the inability to raise capital to fund continuing operations; changes in government regulation; the ability to complete customer transactions, and other factors relating to our industry, our operations and results of operations and any businesses that may be acquired by us. Should one or more of these risks or uncertainties materialize, or should the underlying assumptions prove incorrect, actual results may differ significantly from those anticipated, believed, estimated, expected, intended or planned. The Company has been severely impacted by the effects of COVID-19 “Pandemic 2020”, which effects continue to this day as such presently the Company do not have the ability to control the exact timing of progresses in moving forward of its business plans tangibly except best effort basis. Readers of this Annual Report should not place undue reliance on any forward-looking statements. Except as required by federal securities laws, the Company undertakes no obligation to update or revise these forward-looking statements to reflect new events or uncertainties.

You should read the following discussion and analysis of the financial condition and results of operations of the Company together with the financial statements and the related notes presented herein.

In this Annual Report, unless the context requires otherwise, references to the “Company,” “Sino Agro,” “SIAF,” “we,” “our company” and “us” refer to Sino Agro Food, Inc., a Nevada corporation together with its subsidiaries.

Part 1 Business

Back Ground:

Sino Agro Food, Inc.

SIAF is an agriculture technology and natural food holding company with principal operations in the People’s Republic of China. The Company acquires and maintains equity stakes in a cohesive portfolio of companies that SIAF forms according to its core mission to produce, distribute, market and sell natural, sustainable protein food and produce, primarily seafood and cattle, to the rapidly growing middle class in China. SIAF provides financial oversight and strategic direction for each company, and for the interoperation between companies, stressing vertical integration between the levels of the Company’s subsidiary food chain. The Company owns or licenses patents, proprietary methods, and other intellectual properties in its areas of expertise. SIAF provides technology consulting and services to joint venture partners to construct and operate food businesses, primarily producing wholesale fish and cattle. Further joint ventures market and distribute the wholesale products as part of an overall “farm to plate” concept and business strategy.

The Company (SIAF) has been established since 2007 with major activities in agriculture industry producing food produces and products (as primary producer) using modern technologies introduced and transferred mainly from Australia. SIAF became a SEC fully reporting company since 2010. The Company employs a strategy of vertical integration from primary production through processing, distribution and marketing of high quality, organic food products in the food value chain. China’s fast growing middle class is creating rapidly rising demand for gourmet and high-quality protein food.

The Company’s operations and strategy are executed through a number of subsidiaries located in China, and the Company contributes financial oversight and strategic direction to otherwise independent management teams which employ the Company’s intellectual property and proprietary methods.

The Company has been severely impacted by the effects of COVID-19 “Pandemic 2020”, which effects continue to this day as such presently the Company is no longer a fully reporting company and has dropped from quoting on OTCQX to OTC Pink sheet from September 2020 onward due primarily to the Company’s auditors, which are located in Hong Kong, have been unable to do on-site inspections of the Company’s operations in China due to COVID-19 restrictions to complete the audit of 2019 and 2020. So Basically SIAF is delinquent in its Form 10-Ks for fiscal year end 2019 and 2020, Form 10-Qs for periods ended March 31, 2020, June 30, 2020, September 30, 2020, and March 31, 2021. It will need to amend and restate filings going back to December 31, 2019 to be able to apply to become a fully reporting company.

The aggregate market value of the voting stock held by non-affiliates of the issuer on June 16th 2021, based upon the $0.086 per share closing price of such stock on that date, was in round figure of $5,118,413.00.

There were 60,356,776 shares of our common stock issued and outstanding consisting 59,516,423 free trading shares and 840,353 restricted shares as at June 16th 2021.

In Fiscal year ended 31.12.2020 the Company’s strategy is to manage and operate its businesses under three (3) business divisions or units on a standalone basis and to generate revenues and incomes from the consolidated results of operations as follows:

Business (1): The Fishery Division is operating under Capital Award Inc. (CA), a fully owned subsidiary of the Company, with major activity in providing engineering consulting and services and technology, fishery developments global (excluding China) and agriculture developments global.

Business (2): The Corporate and Other Division is operation under the corporation’s business operational teams consisting staff members from CA as well as from SIAF’s Guangzhou office, with major activity in trading (importing) of agriculture food commodities and frozen food products that are marketed and sold in China and the (exporting from China) of agricultural plants and equipment to South Africa.

Business (3): The Leasing and Sub-contracting Division of the following operations:

(a). The fertilizer manufacturing and piggery operation of HSA (Hunan Shenghua A Power Agriculture Development Co. Ltd.)

(b). The plantation operation of JHST (Jiangmen City Heng Sheng Tai Agriculture Development Co., Ltd)

(C). The cattle (Asian Yellow Cattle) of MEIJI (Macau Eiji Company Limited) and JHMC (Jiangmen City Hang Mei Cattle Farm Development Co., Ltd.)

In Fiscal year ended 31.12.2020 the Company’s strategy is to derive from investment incomes generated from two (2) investees’ unconsolidated results of operations as follows:

(i). Cattle, Beef, Fertilizer & Livestock’ and Feed operations of SJAP

(ii). Fishery Development (China) and operations of TWL (or Twi-way) (Tri-way Industries Limited HK)

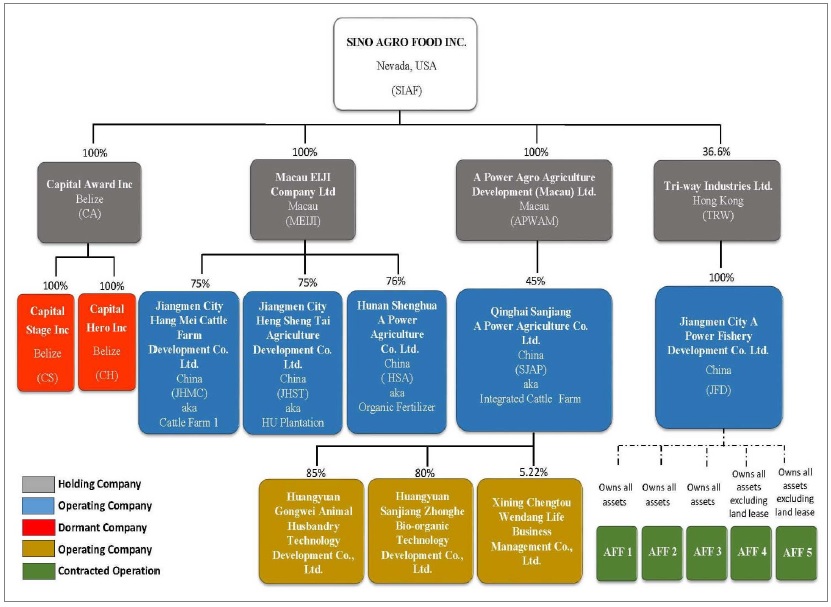

Please find our company’s legal structure chart listed below;

A summary of each business division and operations is described below:

| | · | Fishery Division refers to the operations of Capital Award Inc. (“Capital Award” or “CA”) covering its engineering, technology and consulting service management of fishery farms, technology transfers and seafood sales and marketing, fishery developments global (excluding China) and agriculture developments global where; |

Capital Award generates revenues from providing engineering consulting services as turnkey contractors to owners and developers of fishery and agriculture projects that are being designed and engineered into turnkey contracts by Capital Award globally (excluding China) using its A Power Module Technology Systems (“APM”) for fishery projects’ developments and using other agricultural technologies, knowhow and patents expanded from the development of SJAP for agriculture development projects globally as follows:

(A). Engineering and Technology Services; via Consulting and Service Contracts (“CSC’s”) for the development, construction, and supply of plant and equipment, and management of fishery (and prawn or shrimp) farms and related business operations. From January 2020 up to the date of this annual report CA has not been able to do any fishery project or fishery project development due to the effects of the Pandemic COVID-19 as such, there was no revenue generated from January 2020 to May 31st 2021. However, the Company and CA have been exploring other possible business opportunities during the period and SIAF became the joint venture partner of the China Africa Joint Chamber of Commerce and Industries (CAJCCI) which is a non-profit organization established in November 2016 by the China and Africa Governments to plan and to implement agriculture projects and related developments in Africa through development fund of US$60 Billion every three years provided by and granted by the China Government to Africa Nations in Agriculture industry projects and developments etc. In March 2021, development project papers in (i). Development of Trading of exporting dried cassavas to China and exporting of plant and equipment from China to Madagascar and developments of cassavas plantations and related value added processing and drying of cassavas on 100,000 acres of land in Madagascar and (ii). Development of goat farms and related value added processing in Madagascar were submitted to CAJCCI and Government of Madagascar; by early May 2021, both CAJCCI and the Government of Madagascar gave consents to both projects such that we have obtained official invitation to go to Madagascar to initiate the Projects subjecting to the Pandemic COVID-19 situation and conditions will be improved and controlled, we shall have our team members (including various professionals and professionals from CAJCCI) to assist our current Madagascar management teams of two members in Madagascar to start up the Projects.

(B). Seafood Sales from CA’s projected farms; became a discontinued segment of operations from October 5, 2016 when Tri-way was disposed to other third parties in term Tri-way was reclassified as an unconsolidated equity investee on same date.

| l | Corporate & Others Division refers to the trading segment of business operations of the Group named internally under corporate division of Sino Agro Food, Inc., including import/export business and consulting and service operations provided to projects that are not included in the above categories, and not limited to corporate affairs. Over the years up until end of fiscal year 2019 the corporate division imported mainly live seafood from South Africa countries, Vietnam, Thailand, Russian and other nearby countries and frozen beef from Australia and South America countries; however it is due to the interruptions and adverse impacts caused by the Pandemic COVID-19 made it impossible and unprofitable to continue the imports of live seafood, and the poor political relationship between China and Australia in 2020 induced high risks on the imports of Australian beef. The Corporate’s trading division based on standalone figures ended up with a loss of over $1.6 million as at 31.12 2020. However, over the years the Company has built up a strong base of connections and customers in China that provides an unique opportunity to the Company to develop an additional Trading Platform aiming to generate additional revenues, profits and most importantly positive cash flows, so from July 2020 onward, the corporate division started to explore the opportunities of importing some of the China markets’ niche products and managed to start to import from March 2021, frozen chicken (that China imports millions of metric tons annually) and pork products (that China has been in shortage since the pandemic of European Swine Diseases occurred in 2018 disrupted the domestic supply of pork estimated until year 2026), from Brazil, USA, Argentina and other South America countries and (ii). Dried agriculture products (i.e. Dried Cassavas that has vast industrial and consumable food processing applications, that China has an annual short fall of over 4 million MT; peanuts, cashew-nuts, Soybeans that China imports multiples of millions of MT annually, etc.) from South Africa Countries (i.e. Madagascar, Ghana, Nigeria and Cote D’lovire etc.) and Brazil. Although in so far the Company achieved minimal financial impacts, (please refer to a standalone Q1 2021 income statement of the Trading division attached in the later Chapter named Subsequent events). During months of venturing into this trading activity, we experienced many teething problems and obstacles especially with the supplies of the said commodities affected mainly by the said Pandemic situations causing much stringent and constant changes of importation regulations requiring much tougher importation and cargoes release conditions and procedures, précised timely and orderly documentary presentation with the China custom authority and extremely tight controls domestically disorientated all arrangements with domestic cold storages and logistic operations etc. resulting in inconstancy of the supplies and untimely deliveries etc. Disregarding all of these difficult consequences and hardship, the Company feels that persistence, tolerance and with time, the trading division will prevailed leading the Company into a positive cash path targeting encourage performances to show starting from the early quarter 1 of fiscal year 2022. ’ |

Leasing and subcontracting Division:

Over the years, there has been significant capital expenditures (CPE) and working capital (WC) required for and employed on the developments, expansion and operations of the minor operational activities that we managed to fund while our two core businesses (in the Cattle and beef of SJAP and the Fishery of CA) were generating sufficient cash flows and incomes, however after the collapse of the SJAP’s business from 2016 and the poor performances of the Mega farms from 2017 (“Crises”) for reasons mentioned in the earlier chapters and the previous Ks and Qs reports, the Company is no longer in the position to support and to finance the growth of these minor operational businesses in the way as they were before the Crises, therefore in order that capital spending could be kept within an affordable level, the Company decided to lease and sub-contract the following operations to their respective operational managements from 1st October 2019 as such there are no sales revenue and income derived from these operations but leasing and sub-contracting revenues and incomes thereon.

| l | The operation of Hunan Shenghua A Power Agriculture Co. Ltd. (“HSA”) is in manufacturing and sales of organic fertilizer. From 1st October 2019 the Company contracted out its manufacturing and sales of organic fertilizer to its operational management; as such income of HSA is derived mainly from said management contract. Historically, HSA was developed to enhance more sales and profits of SJAP’s fertilizer due to the availability of a direct cargo train service between Xining and Hunan having a station within close proximity to HSA’s operation site and Hunan is a strong agricultural province producing big quantity of rice, tobaccos, tea and multiple varieties of produces that requires large quantity of fertilizer (especially in organic fertilizer due to the Government’s direction to phase out the application of chemical fertilizer in China). During the period of developing HSA’s business it was discovered that Hunan is big in aquaculture having many and large areas in natural fresh water lakes where aquaculture of fresh water fish is a dominated industry, as such HSA developed a water soluble organic fertilizer specially applied for and by the lake fishery farms to provide nutrients to the water plants and micro-organism for the sea animals etc. Although it was an excellent product but aging receivables were always a big problems to HSA with the fishery operators, the constant up-keeps and replacements of new production plants & equipment and the forever requirement of expending working areas and buildings to keep up with the productivity and the long (i.e. over 60 days) period of fermentation of raw materials required huge capital funds (both in CPE and WC) that the Company was not able to supply consistently and that was why HSA hasn’t reached its ultimate potential of becoming a multiple millions MT per year producer. However HSA has a block of leased hilly land of 450 Chinese Mu, in which HSA developed 50 Mu originally for a cattle station that was changed into a piggery (with the capacity to hold 4,000 pigs at a time and producing 10,000 heads of pigs per year) in 2017 after the collapse of the local cattle industry. It was necessary to cut half of the hill in the said 50 Mu to get enough leveled land to build the said piggery, then it was discovered that the 450 Mu land consisting many fine sand hills. From 2018 onward the China Government stopped most of the sand mining operations in the country so all of a sudden fine construction sand became a valuable commodity with 2019’s averaged prices (of RMB245 / cubic meter or m3) jumped more than 12 times of 2017’s averaged prices. As such HSA is sitting on a block of valuable property. But sand mining is restricted by the China Government Regulation so it is impossible to obtain any sand mining permits. By September of 2020 the Company strategically designed a business plan for HSA to expand its piggery to produce 200,000 head of pigs per annual using and developing the whole of said 450 Mu that will be financed ultimately by the fine sand recovered from said development’s leveling activities. In this aspect, the related Project’s business plan (including all feasibility, viability and environmental studies) have been prepared with approaches and dialogues have been made with a number of China owned entities aiming to attract enough investors to finance the Project as soon as possible. Although currently the Pandemic effects hinder many businesses’ decisions making it difficult to predict any tangible schedule for this Hunan Project, however, our management team members are working diligently on it hoping that soon a clearer road will be opened to allow them to pick up momentum on the Project. |

| l | Plantation Division refers to the operations of Jiangmen City Heng Sheng Tai Agriculture Development Co. Ltd. (“JHST”) in the HU Plantation business where dragon fruit flowers (dried and fresh), crops of vegetables and immortal vegetables (dried) are sold to wholesale and retail markets. JHST’s financial statements are consolidated into the financial statements of Macau EIJI Company Ltd. (“MEIJI”) as one entity. From 1st October 2019 the Company contracted out its plantation operation to its operational management; as such income of JHST is derived mainly from said management contract. Over the years, the Company has tried many means to increase the performances of the plantation (of 1,250 Chinese Mu) but failed due mainly to the plantation is situated in an area subjecting to heavy rainfalls yearly that induced root diseases to the dragon fruit plants stopping the yield of flowers. 1,250 Mu plantation is too small for growing of other selective fruit plants except for the growing of cash crops (i.e. seasonal vegetables etc.), however growing of cash crops is labor intensive, so with the forever increases of labor and operation costs in China and the seasonal unpredictable sales prices of cash crops, managements of the Company has yet to find a suitable solution for JHST but keep on trying hoping that eventually a perfect solution will surface to revitalize JHST. In the meantime leasing and contracting JHST ‘s operation to its existing operational management will limit the Company’s financing exposure in both CPE and WC requirements from JHST. |

| l | Cattle Farm Division refers to the operations of Cattle Farm 1 under Jiangmen City Hang Mei Cattle Farm Development Co. Ltd (“JHMC”) where cattle are sold live to third party livestock wholesalers who sell them mainly to Guangzhou and Beijing livestock wholesale markets. The financial statements of JHMC are consolidated into MEIJI as one entity along with MEIJI’s operation in the consulting and service for development of other cattle farms (e.g., Cattle Farm 2) or related projects. From 1st October 2019 the Company contracted out its cattle operation to its operational management; as such incomes of JHMC are derived mainly from said management contract. JHMC’s business strategy in 2018 of changing into fattening of the Asian Yellow Cattle instead of the fattening of conventional breed of cattle (i.e. Angus and Simantals etc.) proven to be a good strategic change increasing revenues and incomes each year ever since. However this cattle operation is too small (with. Cattle Farm 1 and 2 operate on 500 Chinese Mu) coupling with the increasing of land and development costs making it extremely difficult for the Company to finance its expansion plan at the moment as such by leasing and contracting JHMC’s cattle operation to its existing operational management will provide the Company with a small but steady incomes each year and will limit capital funding to JHMC until such time the Company is in a better financial position to consider JHMC’s expansion plan. |

SJAP: Qinghai Sanjiang A Power Agriculture Co., Ltd

| l | A fully integrated cattle and beef business was developed from 2008 under SJAP, (a joint venture company incorporated in China whereby SIAF has an equity interest of 45% and the management controlling interest allowing the VIT arrangement with consolidated financial as a subsidiary of SIAF until Q3 2019 when Mr. Solomon Lee resigned the Chairmanship from SJAP), and starting business (or income generated) operation from 2010 (consisting of fertilizer manufacturing, pasture farms, farmers’ corporative, cattle rearing and growing, abattoirs or slaughter operation, value added beef processing and packaging, primary livestock feed producing, industrial concentrated livestock feed manufacturing, marketing networks with retails as well as wholesaling operation etc.); as such by 2016 this cattle and beef segmental business was producing, processing and marketing over 20,000 heads of cattle per year managing more than 2,000 corporative farmers, 50,000 Chinese Mu (equivalent to 8,500 acres) of pasteurized farm land, over 50,000 (square meter, m2)of operational buildings developed on over 400 Chinese Mu (equivalent to about 70 acres) of Industrial and / or commercial zoned land in Huangyuen district of Xining City. In November 2015 the China Government announced a Macro Economic Policy to allow the imports of cattle and beef from many developing and developed countries that impacted adversely and directly to its local cattle and beef industry, all of a sudden the local cattle and beef industry was transformed from a protected industry to a non-protected industry, as such SJAP was on a decline financially since 2016 that took SJAP 3 full years to stop the bleeding capped the losses totaling to S$ 12 million as shown in SIAF’s 10K 31.12 2019 report. On September 30th 2019, Mr. Solomon Lee resigned as the Chairman of SJAP resulting in categorization of SJAP as an Investor in Associate from a subsidiary status, and SJAP contracted out its business operations to its existing management. However the adverse impacts of the COVID-19 Pandemic, SJAP again suffered badly with further losses of $1.28 million that was saved by a Government Grant of $1.48 million netting incomes of $200,000 for 2020. It is because SJAP became an investee of SIAF since 01102019 such that its 2020 financial is not detailed in SIAF’s annual report 2020 financial report but under Others and Subsequent events of SIAF’s annual report 2020 a separated information memorandum shows SJAP’s 2020 Income Statement. |

TWL (or Tri-way) Tri-way Industries Limited: l A fully integrated live fish, shrimps and seafood business from 2010 starting operation with one small in door and on land farm in Enping District Enping City and by 2015 the Company developed and started operations of 4 small to medium sized indoor as well as open land farms in Enping districts Enping City and Zhongzhen Districts Zhingzhen City that we called Aqua-Fish Farm (or AFF) 1, 2, 3a and 3 b producing and marketing over 5,000 (Metric Tons, MT) of live fish, shrimps and seafood per annual under its developed brood stock stations, nursery farms, grow-out farms, R & D stations, wholesale centers, restaurants and marketing net-works etc. and providing aquaculture engineering services to and activating trading relationship with 8 corporative farmers and their related farms. Apart from AFF 1 that the Corporation had 75% equity interest whereas the rest of the aqua-farms (AF2, 3a and 3b) were operated by different China incorporated entities (in accordance with the China Company regulation that operational companies must be registered in the districts where their core-operation are based) and owned by unrelated third parties consisting of various farm developers, suppliers, core farms’ operators, workers and farms’ investors etc. Whereby the Corporation has an executive marketing and sales Contract with all AFFS to market, purchase and sales all of their respective productions derived into one of the Corporation’s main sources of incomes. At the same time in 2015, the Corporation accepted the Zhongshan Government’s invitation to developed aquaculture fish and shrimps farms in a block of leased land measuring over 3,700 Chinese Mu (equivalent to about 650 acres) that was leased from a company owned by the Zhongshen Government whereas the land lease agreement was executed and secured by a newly formed company incorporated at Zhongshen City namely Zhongshen City A Power Agriculture Development Limited Co. (ZSAPADL); whereas the ZSAPADL is the operational company of the Zhongshen Project and owned by a local company and a Hong Kong Company (that are ultimately owned by various third parties consisting of investors, developers and farm operators etc) and SIAF’s fully owned subsidiary CA is its development’s turnkey contractor, engineering services provider, sole marketing and sales agent with the option to purchase and to sell its developed farms’ productions. In the land lease agreement, the land was allocated gradually ZSAPADL as and when respective earlier lease holds to other farmers are expired such that there was a total of 1,350 Chinese Mu (equivalent to about 225 acres) available for Phase (1) of the Project’s developments as of year 2015, however during 2018 and 2019, 250 Chinese Mu were given back to the local Government by ZSAPADL for the constructions of highways and a Wet-Land Project involving part of the Project land netting about 1,100 Chinese acres (or the equivalent of less than 200 acres of the Project land available for project developments currently). This particular project’s developments are planned over 10 years in multiple phases and subsequent stages etc. with construction to start in 2015 and operation incomes to be generated from sometimes in 2017 aiming annual production over 100,000 MT by end of year 2025. By the mid-year 2017, we completed almost 85% of the development of two indoor APRAS farms (APM farms) each measuring 9,000 m2 totaling to 18,000m2 of building areas on a block of land of 60 Chinese Mu (equivalent to 10 acres) and 165 open APRAS dams (ODRAS) on about 990 Chinese Mu (equivalent to about 165 acres) of land (Phase 1 stage 1 development) that we called the “Mega Farm” or Aqua-farm 4 & 5 (AFF 4 & 5). In 2016 The Company’s carve-out of Tri-way resulting in categorization of Tri-way as an Investor in Associate from a subsidiary status. As such, the Company’s fully owned subsidiary namely, Capital Award Inc. a company incorporated in Belize City, Belize (CA), retained its main business activity in the sector of technology and engineering consulting and related services and Tri-way Industries Limited, a private company incorporated in Hong Kong (Tri-way) has assumed all activity regarding aquaculture operations and the sale of all live fish and seafood products produced by all developed APM farms as well as ODRAS Dams. Therefore as from October 1, 2016, all future fishery project development in China using APM-RAS or ODRAS will be developed by Tri-way. CA has been hired by Tri-way as the Company’s turnkey contractor for its fishery developments in China and to provide consultation respective of Tri-way’s operations. CA’s aim, in addition to providing quality service to Tri-way in China, is expecting to expand its reach to introduce and help implement its APM-RAS and ODRAS plant and equipment and services, worldwide. To complete the transformation of Tri-way From October 5th 2016 we brought out the remaining 25% equity interest in “Jiangmen City A Power Fishery Development Co. Ltd, China” (“JFD”) and sold the 100% equity interest in JFD to Tri-way (inclusive all original assets of its one farm namely Aqua-Fish Farm 1(AFF 1) with other additional assets transferred from work in progress etc.) and converted JFD into a Wholly Owned Foreign Entity (WOFE) such that Tri-way is holding 100% equity interest in JFD for $51.226 million; at the same time Triway acquired a Master License from CA for the rights of future development and operation of our APRAS farms in China for $30 million and simultaneously (on October 5th 2016) JFD completed the acquisition: of the assets and operation from owners and investors of four other aquaculture farms (namely Aqua-farm 2, 3 and 4) for $215.56 Million such that the total transformation and acquisition cost of Tri-way at $340 million (in round figure) that were satisfied by 100 million Tri-way shares at unit price of $3.40 / share capitalizing into fully paid-up capital of $340 million (or HK$2.635 billion). Our corporation SIAF was to receive 36.6 million Tri-ways shares (or 36.6% of equity) for the sales of JFD and Master license for 23.89 million (or 23.89% equity) plus the conversion of the amount due from unconsolidated equity investee into equity interest during the fourth quarter of 2017, which resulted in equity interest in Tri-way from 23.89% to 36.60%. |

We announced our (good will) intension with the approval of Tri-way’s management of distributing 18.3% of Tri-way equity interest (about half of SAIF’s holding) from our 36.6% equity interest to our shareholders and prepared a F1 for filing to SEC accordingly sometimes in 2018 . However complication of USA taxation was one of the major issues that have not been resolved and at that time period Mr. Dan Ritchey was our CFO responsible for the said distribution of Tri-way shares but he passed away on December 1st 2018 as such we were searching for a new CFO and consequently, Mr. Solomon Lee (I) serves as the Company’s interim CFO that enhanced the delay in processing said distribution of Tri-way shares to SIAF’s shareholders. Also 2019 was a traumatic year for the Corporation having lost the services of our most brilliant CFO, our long time independent directors namely Mr. Nils Erik Sandberg and Mr. Anthony Soh who have been serving our Corporation since 2010, the recruitment and reappointment of new directors and audit committee members in Mr. Colanukuduru Ravindran and Mr. Muson Cheung, the reorganization of the Corporation’s other segmental operations; The Corporation’s common stocks were delisted from the Merkur Market (OSLO) from September 10th 2019, On September 30th 2019, the Company contracted out the following businesses’ operations to the existing management of the corresponding operations: (i). SJAP’s integrated cattle activity to Mr. Zhao Y L, the legal representative and MD of SJAP, (ii). HSA’s manufacturing of fertilizer to Mr. Lee Ping the existing manager of HSA and (iii). JHST’s plantation operation and MEIJI’s cattle operations to Mr. Fang Zhi Jun, the existing manager of both operations, On September 30th 2019, Mr. Solomon Lee resigned as the Chairman of SJAP resulting in categorization of SJAP as an Investor in Associate from a subsidiary status, the preparation of S1 and S4 for the IPO exercise of 2 million G Series Preferred Shares of the Corporation to be listed on the OTCQX Market and the Derivative Complaint of Heng Ren and Co. etc. that involved lots of extra costs in time, money and human resources of the Corporation such that it was not practically possible to carry out said distribution of Tri-way shares in 2019. Year 2020 is another disaster year for the Corporation due to the COVID-19 Pandemic incurring losses in excessive of $100 million (which is an earlier estimate subjecting to final derivation of the segmental accounting departments)

Similarly Tri-way experienced extremely poor operational performances from its Mega Farm (AFF 4 & 5) and its incomes in 2017 to 2019 were generated mainly from the operations of AFF 1, 2 , 3a & 3b and other sub-contracted farms:

In fact, the operation of the Mega Farms (AF4 and AF5 and the ODRAS dams) had a poor start and performed badly in 2017 and by the first half of 2018 and the end of 2018, their operations (under their operation company ZSAPADL) incurred debts over $4.5 million and $4 million respectively, due primarily to i). Unsuccessful management coordination resulting in low productivity and sales of products, (ii). Over spending on capital expenditure on Phase (1) Stage (1) of the Mega Farm Project which exceeded the original budget of $50 million by more than 60%, as a result, it limited available cash-flow to support the needs of working capital that affected the overall production and sales leading to, there were not enough funds to complete some of the supporting facilities needed by the APM farms (i.e., the external filtration systems, lighting, electrical wiring, external drainages for waste water and connection and fitting for the supply of fresh water etc.), supporting external water dams and waste water treatment dams, the heating facility and part of the internal filtration systems that made it difficult for the farms to carry out their production efficiently, (iii). The production operation of the Mega Farms started prematurely before all the completion of their construction & development works, (iv) The two APM farms are the biggest indoor farms that we have ever built, and we didn't have enough experienced personnel to support their operation, (v). Guangzhou experienced a very hot summary in 2017 that killed and retarded many stocks in the open dams (ODRAS dams) and one of the big typhoons during August 2017 caused flooding that washed away hundreds of tons of fish and prawns in the open dams that would have been ready for harvest in September & October of 2017. Also, the extremely strong Typhoon in September 2018 caused power stoppage that killed hundreds of tons of stock including some valuable brood stock.

However, by August 2019, efforts of the Company and Tri-way trying to revitalize Aqua-farm 4 and 5 failed due primarily to the lack of capital funding to continue to support farms’ developments and the necessity in adding new talents into the existing management teams to carry out the revitalization works, the Company and Tri-way finally decided to cease operation of Aqua-farm 4 and 5 during September 2019. Again the COVID-19 Pandemic of 2020 is a complete write-off for AFF 1, 2,and 3 as well as to Tri-way’s sub-contracted farms incurring losses over $77 million for the year (subjecting to final figures of their respective accounting departments) due completely to the impacts of the pandemic causing all farms to stop work for over 7 months without sufficient workers, feed, supplementary, medications, transportation and maintenances etc. to keep the live stocks going and they all died during the period calculating to multiple million pieces (equivalent to multiple of thousand metric tons). It will cost over $80 million and a minimum of two years to replace said live stocks. As such Tri-way’s current operations are concentrating on rebuilding of brood stocks, the production of fingerling and nursery stocks and repairing the damages etc. It is anticipating that under current conditions, the Triway’s fishery operation recovery will be a tall order and will take a long period before recovery.

This section discusses the industry in which the Company operates. Certain of the information in this section relating to market environment, market developments, growth rates, market trends, industry trends, competition and similar information are estimates based on data compiled by professional organizations, consultants and analysts, in addition to market data from other external and publicly available sources.

Economic outlook in China

China’s economy is at present second only to that of the United States. Due to the impact of the COVID19 pandemic, China's GDP growth was only 2.3%, the slowest pace in more than four decades. Growth has slowed significantly following the COVID19 outbreak in early 2020. Based on the World Bank’s classification, China has had a remarkable period of rapid growth shifting from a centrally planned to a market based economy. Today, China is an upper middle-income country that has complex needs for all kinds of consumer goods, including food.

Agriculture in China

Agriculture is a vital industry in China, employing over 300 million farmers. China ranks first in worldwide farm output, primarily producing rice, wheat, potatoes, tomato, sorghum, peanuts, tea, millet, barley, cotton, oilseed and soybeans and also the largest consumer of many agricultural products, such as pork, rice and soybeans. Although accounting for only 10 percent of arable land worldwide, it produces food for 20 percent of the world's population. While China generally has been successful in meeting its rapidly rising demand for food and grains by increasing domestic production, it has emerged as a leading global importer of several agricultural commodities, including cotton, soybeans, vegetable oils, and animal hides. As its domestic agricultural production has grown, China has also become the largest exporter in global markets for several horticultural products, including mandarin oranges, apples, apple juice, garlic and other vegetables.

China’s increasingly important position in global agricultural markets followed decades of gradual growth in domestic food production and consumption. After the introduction of market-based reforms in 1978 that included the elimination of the collective production system and relaxation of government direction over certain farmer production and marketing decisions, Chinese agricultural output grew significantly. Between 1978 and 2008, China almost doubled its production of grains (rice, wheat and corn) and quadrupled its production of meats; the production of fruit and milk was about 30 times greater in 2008 than in 1978. During these three decades, population growth of about 1 percent annually, coupled with annual per capita income growth of eight percent, fueled a large increase in demand for more and higher-value agricultural products, especially by China’s large and growing middle class. China’s rapid growth in food consumption was largely met by domestic production growth, enabling it to remain self-sufficient in most major commodities. However, China is also now the world's largest agricultural importer, surpassing both the European Union (EU) and the United States in 2019 with imports totaling $133.1 billion.

China’s support for agriculture

China’s government support for agriculture is low compared to that of developed countries, such as the United States and European Union, but in line with that of other rapidly growing economies, according to USITC. As measured by the OECD’s PSE1, the amount of support provided to Chinese farmers was low (and sometimes negative) during the 1990’s, but gradually rose during the period 2008-2010. Compared with other countries at a similar level of development, including Brazil, Mexico, Russia, and South Africa, China’s support for farmers falls in the middle of the range. China’s PSE reflects changes in the central government’s policy priorities from grain self-sufficiency and low consumer prices toward a stronger focus on raising farm household incomes, according to USITC. Government support to China’s agricultural sector indicates that Chinese policymakers are placing a renewed emphasis on the rural economy. Indirect support, in the form of general services, is very high relative to similar support programs in other countries, due largely to investments in agricultural infrastructure. General services include modern research and extension services, food safety agencies, and agricultural price information services, most of which provide benefits to producers and consumers throughout the economy. Compared with direct payments to farmers, general services support is less production-distorting to the sector.

Agricultural consumption

China is a major global consumer of agricultural products. It consumes one-third of the world’s rice, one-fourth of all corn, and half of all pork and cotton, and it is the largest consumer of oilseeds and most edible oils. The traditional Chinese diet centers around staple foods (mainly grains and starches), which account for nearly half of the daily caloric intake. Average Chinese per capita consumption recently stabilized at approximately 3,000 calories per day, one of the highest levels among Asian countries.

Chinese food consumption is influenced by factors such as population size and demographics, income, food prices, and general preferences. Per capita income growth and urbanization are the two factors most responsible for altering recent consumption patterns in China. Rising income translates into higher per capita food consumption, while increasing urbanization is driving diversification of food choices because of greater availability and choice offered through increasingly diverse sales outlets.

Chinese consumers generally fall into one of three categories: rural consumers; urban low-income consumers; or urban high-income consumers. Although urban high-income consumers can afford to buy more and better-quality food, the ubiquity of food outlets in cities means that nearly every urban resident, regardless of income, has available an increasingly diverse food selection. Compared to rural diets, urban diets contain less grain and more non-staple items, including processed and convenience foods. Rural migrants to cities tend to adopt the urban diet.

Expenditure on food

Food is the largest class of household expenditure for all Chinese income groups; even housing takes a smaller share of average household income, according to USITC. As income rises, the absolute amount of food expenditure increases, although the share of income spent on food falls. Urban residents spend substantially more on food than their rural counterparts, according to USITC. Higher incomes lead to an increase in both the quantity and quality of food demanded. However, while demand for higher quantities of food appears to level off in the top income households, demand for higher-quality foods continues to rise with income.

The market for aquatic products and aquaculture in China

The information in this section regarding aquatic and aquaculture, including graphs, is taken from the USDA’s GAIN Report Number: CH12073 per 12/28/2012 unless otherwise stated.2

1OECD: PSE is defined as the estimated monetary value of transfers from consumers and taxpayers to farmers, expressed as a percentage of gross farm receipts (defined as the value of total farm production at farmgate prices), plus budgetary support.

2Definition of terms: China’s definition of aquatic products includes both cultured (farm-raised) and wild caught products; aquatic products include fish, shrimp/prawn/crab, shellfish, algae, and other. Aquatic catch production is total volume of both fresh and seawater wild caught aquatic products; Aquaculture production is the total volume of both fresh and seawater cultured (farmed) aquatic products. This report will use Chinese terminology to maintain consistency between Chinese statistics and product categories. Total aquatic trade statistics below do not include fishmeal.

Total Aquatic Products Production

China has the world’s largest aquatic production and its market share of the world’s fish production has risen from 7 percent in 1961 to 37 percent by 2012. China alone accounted for 62.5 percent of the aquaculture production in the world by volume in 2015. Aquaculture represents more than 71.9 percent of the total fish production in China. Total 2015 aquatic production in China increased 4.38 percent to reach 47.9 million tons, compared to the 45.8 million tons in 2014, per the FAO.

Fish production accounts for 59 percent of the total aquatic production, followed by shellfish and crustaceans at 22.6 percent and 10 percent, respectively. Fish production is, according to the USDA, expected to continue its upward growth trend to reach 34.5 million tons in 2012, up from 33 million tons in 2011 and 31.3 million tons in 2010.

In 2011, Shandong, Guangdong, Fujian and Zhejiang provinces profited from favorable coastal locations and abundant freshwater resources/facilities to rank as the top four aquatic production areas. In terms of freshwater cultured production, Hubei, Guangdong, and Jiangsu provinces are the largest producers.

According to @2020 undercurrent news, China’s seafood imports increased by 39% to $15bn in 2018. China has the largest aquaculture industry in the world, accounting for approximately two-thirds of total cultivated aquatic products worldwide. In 2020, output of the Marin culture segment in China is estimated to total 22.3 million tons, up 4.7% from 2019.

The market for meat in China

China is by far the world’s largest producer and consumer of meat which includes pork, poultry and beef. Historically, this situation did not have a large impact on the rest of the world, as China, for the most part, maintained self-sufficiency in meat. However, since 2007 the situation has changed dramatically. China has gradually turned into a net importer of meats. In 2019, China consumed around 28% of the global meat supply.

World meat production was 340 million tons in 2017.3 Global trade in meat is projected to be 20% higher in 2027, representing a slowing down of meat trade growth to an annual average of 1.5% compared to 2.9% during the previous decade.4 Meat imports into Asia account for 56% of global trade, and poultry will constitute more than half of this additional import demand. China’s meat production reached 86.60 million tons in 2018, where total meat production in the United States amounted to 47.06 million tons in 2018.

With strong economic growth and the improvement of living standards, the demand for beef in China is rising.5 China’s animal feed market is projected to grow at a CAGR of over 16% till 2019.6

3Review of Recirculation Aquaculture System Technologies and their Commercial Application, Stirling Aquaculture, Institute of Aquaculture.

4 Food Outlook, FAO, November 2018

5 Research Report on Beef Import in China, 2019-2023

6 China Animal Feed Market Forecast and Opportunities, 2019

There are several other specific market drivers which underpin the increase in demand for red meat. One driver is the improved living standard in China which stimulates the growth of beef markets since beef often sells at a much higher price and traditionally has been more expensive than what most people can afford. Another is the fact that Chinese people’s dietary structure is becoming more diversified and reasonable, bringing larger amount of beef consumption since beef has nutritional benefits. Lastly, a gradual lowering of import taxes is likely to support sufficient supply of cattle.

Feed grain prices are projected to remain low during 2018-2027. The year 2017 was affected by numerous outbreaks of Avian Influenza (AI) around the world which resulted in a slower increase in world output. China, the second largest producer after the United States, was particularly affected by several outbreaks over the last years. Thus, China can expect a return to historical trend growth in poultry production from 2018 onwards. Globally, the share of meat output traded is expected to remain constant at around 10%, with most of the increase in volume coming from poultry meat. The projected production growth in developing countries remains insufficient to satisfy demand grown, particularly in Asia and Africa. As a result, import demand is expected to remain strong.7

Market drivers

The improvement of living standard stimulates the growth of beef markets:

Traditionally, Chinese people eat pork and chicken to satisfy their desire for meat. This is largely due to the much higher price of beef which goes beyond normal people’s affordable level. With the improvement of living standards, Chinese people have begun the upgrade of their consumption of meat, and began to eat more beef.

Chinese people’s dietary structure becomes more diversified and reasonable, bringing larger amount of beef consumption:

At present, Chinese people are changing their diet patterns to higher and richer nutrition. From a nutritional perspective, beef not only contains high unsaturated fatty acids and high protein, it also has low fat and lots of nutrition, which makes it perfect for the healthy diet. Thus, in the future, beef is expected to replace some parts of the market shares in pork, chicken and other meats.8

The market for fertilizer in China

Sales of fertilizers are expected to be supported by healthy expansion of agricultural activities as the amount of sown areas continues to grow and rural income levels rise. Farmers will continue to register steadily increasing incomes, the result of growing crop prices and government subsidies designed to supplement their revenues and reduce their material costs. Subsidies aimed directly at cutting the cost of fertilizers is expected to encourage additional use. In addition, rising crop prices have encouraged farmers to invest in fertilizers to further boost crop yields. Advances will also be driven by increases in the acreage of sown land dedicated to growing cash crops. However, increasing demand for organic food and improved understanding of the correct application of fertilizers is expected to prevent demand from rising at a faster pace.

7 Meat - OECD-FAO Agricultural Outlook 2018-2027

8 Frost & Sullivan: China’s beef market has great growth potential

In value terms, fertilizer demand is expected to grow from over $195 billion in 2016 to over $245 billion in 2020.9 Faster value growth will be driven by strong demand for higher value multi-nutrient fertilizers. In addition, advances will be supported by continued growth in fertilizer prices as the cost of natural gas, oil, coal, and other raw materials continues to increase.

Demand for fertilizer nutrients in China is projected to grow 4.4 percent annually through 2015 to 98.1 million metric tons. Nutrient demand will be stimulated by increasing use of higher nutrient level products as income levels grow in rural areas in China. In addition, government efforts to promote multi-nutrient fertilizers will also support gains in fertilizer nutrient demand. Accounting for more than three-fourths of total fertilizer demand in 2010, single-nutrient fertilizers will remain the larger product type through 2015, despite a relatively low growth rate of 2.1 percent per year. Sales of single nutrient fertilizers will continue to be supported by their relatively low prices.

The size, growth and composition of fertilizer demand in the six regions that make up China vary considerably. The Central-South and Central-East will remain the two largest regional fertilizer markets. Due to the comparatively high income levels in the Central-South and Central-East ¨¨which enable residents to afford more expensive food items ¨ demand for cash crops such as fruits and vegetables will rise in these regions, which in turn will fuel demand for fertilizer. Sales in the Northeast and Northwest regions will outpace the average through 2015, benefiting from the Great Western Development Strategy, the Northeast Revitalization Policy, and increasing income levels for farmers.10

In 2006, the central government started a program intended to partially compensate farmers for price increases in fuel, fertilizer and other agricultural inputs. In the case of fertilizers, government support is part of several separate programs targeting fertilizer producers, with cost reductions being passed along to farmers purchasing the input.

Fish production accounts for 59 percent of the total aquatic production, followed by shellfish and crustaceans at 22.6 percent and 10 percent, respectively. Fish production is, according to the USDA, expected to continue its upward growth trend to reach 34.5 million tons in 2012, up from 33 million tons in 2011 and 31.3 million tons in 2010.

In 2011, Shandong, Guangdong, Fujian and Zhejiang provinces profited from favorable coastal locations and abundant freshwater resources/facilities to rank as the top four aquatic production areas. In terms of freshwater cultured production, Hubei, Guangdong, and Jiangsu provinces are the largest producers.

According to @2019 undercurrent news, China’s seafood imports increased by 44% to $12bn in 2018. In the twelve months to the end of December 2018, China imported CNY 787bn worth of seafood, according to Chinese customs data.

The market for meat in China

China is by far the world’s largest producer and consumer of meat which includes pork, poultry and beef. Historically, this situation did not have a large impact on the rest of the world, as China, for the most part, maintained self-sufficiency in meat. However, since 2007 the situation has changed dramatically. China has gradually turned into a net importer of meats.

World meat production was 323 million tons in 2017.11 Global trade in meat is projected to be 20% higher in 2027, representing a slowing down of meat trade growth to an annual average of 1.5% compared to 2.9% during the previous decade.12 Meat imports into Asia account for 56% of global trade, and poultry will constitute more than half of this additional import demand. China’s meat production reached 86.60 million tons in 2018, where total meat production in the United States amounted to 47.06 million tons in 2018.

9 Fertilizer Market Global Report 2017, Business Research Company

10 Fertilizers in China, Industry Study with Forecasts for 2015 & 2020, Freedonia Group; June 2012

11 Review of Recirculation Aquaculture System Technologies and their Commercial Application, Stirling Aquaculture, Institute of Aquaculture.

12 Food Outlook, FAO, November 2018

With strong economic growth and the improvement of living standards, the demand for beef in China is rising.13 China’s animal feed market is projected to grow at a CAGR of over 16% till 2019.14

There are several other specific market drivers which underpin the increase in demand for red meat. One driver is the improved living standard in China which stimulates the growth of beef markets since beef often sells at a much higher price and traditionally has been more expensive than what most people can afford. Another is the fact that Chinese people’s dietary structure is becoming more diversified and reasonable, bringing larger amount of beef consumption since beef has nutritional benefits. Lastly, a gradual lowering of import taxes is likely to support sufficient supply of cattle.

Feed grain prices are projected to remain low during 2018-2027. The year 2017 was affected by numerous outbreaks of Avian Influenza (AI) around the world which resulted in a slower increase in world output. China, the second largest producer after the United States, was particularly affected by several outbreaks over the last years. Thus, China can expect a return to historical trend growth in poultry production from 2018 onwards. Globally, the share of meat output traded is expected to remain constant at around 10%, with most of the increase in volume coming from poultry meat. The projected production growth in developing countries remains insufficient to satisfy demand grown, particularly in Asia and Africa. As a result, import demand is expected to remain strong.15

Market drivers

The improvement of living standard stimulates the growth of beef markets:

Traditionally, Chinese people eat pork and chicken to satisfy their desire for meat. This is largely due to the much higher price of beef which goes beyond normal people’s affordable level. With the improvement of living standards, Chinese people have begun the upgrade of their consumption of meat, and began to eat more beef.

Chinese people’s dietary structure becomes more diversified and reasonable, bringing larger amount of beef consumption:

At present, Chinese people are changing their diet patterns to higher and richer nutrition. From a nutritional perspective, beef not only contains high unsaturated fatty acids and high protein, it also has low fat and lots of nutrition, which makes it perfect for the healthy diet. Thus, in the future, beef is expected to replace some parts of the market shares in pork, chicken and other meats.16

13 Research Report on Beef Import in China, 2019-2023

14 China Animal Feed Market Forecast and Opportunities, 2019

15 Meat - OECD-FAO Agricultural Outlook 2018-2027

16 Frost & Sullivan: China’s beef market has great growth potential

The market for fertilizer in China

Sales of fertilizers are expected to be supported by healthy expansion of agricultural activities as the amount of sown areas continues to grow and rural income levels rise. Farmers will continue to register steadily increasing incomes, the result of growing crop prices and government subsidies designed to supplement their revenues and reduce their material costs. Subsidies aimed directly at cutting the cost of fertilizers is expected to encourage additional use. In addition, rising crop prices have encouraged farmers to invest in fertilizers to further boost crop yields. Advances will also be driven by increases in the acreage of sown land dedicated to growing cash crops. However, increasing demand for organic food and improved understanding of the correct application of fertilizers is expected to prevent demand from rising at a faster pace.

In value terms, fertilizer demand is expected to grow from over $195 billion in 2016 to over $245 billion in 2020.17 Faster value growth will be driven by strong demand for higher value multi-nutrient fertilizers. In addition, advances will be supported by continued growth in fertilizer prices as the cost of natural gas, oil, coal, and other raw materials continues to increase.

Demand for fertilizer nutrients in China is projected to grow 4.4 percent annually through 2015 to 98.1 million metric tons. Nutrient demand will be stimulated by increasing use of higher nutrient level products as income levels grow in rural areas in China. In addition, government efforts to promote multi-nutrient fertilizers will also support gains in fertilizer nutrient demand. Accounting for more than three-fourths of total fertilizer demand in 2010, single-nutrient fertilizers will remain the larger product type through 2015, despite a relatively low growth rate of 2.1 percent per year. Sales of single nutrient fertilizers will continue to be supported by their relatively low prices.

The size, growth and composition of fertilizer demand in the six regions that make up China vary considerably. The Central-South and Central-East will remain the two largest regional fertilizer markets. Due to the comparatively high income levels in the Central-South and Central-East ¨¨which enable residents to afford more expensive food items ¨ demand for cash crops such as fruits and vegetables will rise in these regions, which in turn will fuel demand for fertilizer. Sales in the Northeast and Northwest regions will outpace the average through 2015, benefiting from the Great Western Development Strategy, the Northeast Revitalization Policy, and increasing income levels for farmers.18

17 Fertilizer Market Global Report 2017, Business Research Company

18 Fertilizers in China, Industry Study with Forecasts for 2015 & 2020, Freedonia Group; June 2012

4.Material Agreements

Joint Venture Agreements

The Company has two types of SFJVCs established under Chinese law:

| | · | Contractual Joint Ventures (“CJV”); and |

| | · | Equity Joint Ventures (“EJV”). |

Of the five Chinese joint venture project companies which are CJVs or EJVs, four are CJVs (JFD, JHMC, JHST and SJAP) and one is an EJV (HSA).19

The main difference between an EJV and a CJV is that in a CJV, the obligation of capital contribution shall be determined by the contractual parties themselves. The proportions of capital contribution do not have to be fixed between the Chinese and foreign parties. Profit distribution and risk sharing ratio shall also be determined by the contracting parties themselves which do not have to be the same proportions as the parties’ capital contribution or shareholding therein. The capital contributing parties may specify their profit and risk sharing ratio only and may or may not specify their shareholdings in the CJV. One party may make capital contribution by way of non-monetary assets such as rights in lands, factories and machineries etc. while the other party may make capital contribution by way of cash.

In an EJV, the shareholders contribute capital and operate business jointly, and share profits, risks and losses in proportion to their equity contributions. Foreign investor’s capital contribution shall not be less than 25 percent of the total registered capital.

The Company engages in projects based on consulting and service agreements (as described under “Consulting and Services Agreements” below), whereby the Company can choose whether the cooperation shall continue under a consulting and service agreement or be acquired by the Company.

Consulting and Services Agreement

Consulting and service (“C&S”) agreements are important for the operation of the Company’s subsidiaries and partners. Only the Company’s subsidiaries SJAP and HSA do not and have not operated under C&S agreements.

19According to the official documents of the Company’s Chinese subsidiary JHMC, the registered capital of such subsidiary is USD 2 million that was paid in full by year ended 31 December 2014. As of the date of this Annual Report, MEIJI, a subsidiary of the Company, has contributed USD 400,000 of the subscribed capital, whereas USD 1.6 million of the subscribed capital has not been paid. Moreover, according to the official documents of the Company’s Chinese subsidiary HSA, the registered capital of such subsidiary is USD 2.5 million and shall be paid in full no later than 18 July 2013. As of the date of this Annual Report, MEIJI, a subsidiary of the Company, has contributed USD 865,000 of the subscribed capital, whereas USD 234,500 of the subscribed capital has not been paid by the Chinese owner. The aforementioned deadlines can be re-arranged by all the promoters. If no new deadline is agreed upon, failure by MEIJI to make full payment may lead to the other promoters making full payment of the capital contribution on MEIJI’s behalf and requesting MEIJI to compensate for their payment and losses.

Initially, agriculture and aquaculture investors invite the Company to act as a developer and project manager of an agribusiness or food-related project. If the management of the Company sees the proposal as interesting, the Company carries out an in-depth study of the target company including legal due diligence, business plan, budget and projected financial information. The Company makes the decision through a resolution of the Board of Directors. If the Company determines to proceed, the Chinese investor forms a private Chinese company dedicated to the project and the parties sign a C&S agreement.

The Company acts as the project manager providing turnkey services to the Chinese developer of the project, meaning that the Company builds the project using its technology, systems, know-how, and management expertise and systems. As such, the Company’s expenditure in the project includes the Company’s own administration and operational expenses provided for and incurred in the project (charged and recorded under the Company’s general and administrative operation expenses), which are billed to the Chinese developer. All other development expenditures (inclusive of the Company’s subcontractors’ and sub-suppliers’ costs and the Company’s marked up profits) are billed to the Chinese developer who will pay accordingly.

When the C&S Project Company initiates production the Company acts as the sole marketer of food products and as the supplier for the C&S Project Company under the terms and conditions of the C&S agreement. The Company acts as the selling supplier and buying wholesaler to the company supplying items such as feed, young cattle, and RAS technological components and buys mature prawns, sleepy cod, eels and live cattle. The Company earns a gross profit of between 10-15% based on the C&S Project Company’s revenue on this exclusivity.

The C&S Project Company will remain wholly-owned by the Chinese developer until the Company exercises the acquisition option and subsequently converts the company into an SFJVC where the Chinese investor remains as a minority shareholder. The acquisition price is normally determined in accordance with the book value of the Chinese company as of the acquisition date. Consideration will normally consist partly of cash and partly of project loans owed by the Chinese investor, which offset and decrease the purchase proceeds in the corresponding amount. Generally, the agreements that the Company has entered into governing the formation of the unincorporated companies into SFJVCs do not regulate the maturity date for the formation of SFJVC. The date for the formation of the SFJVC is generally left to the discretion of the Company, based on the development and profitability of the relevant project.

As of the date of this Annual Report, the Company has entered into ten C&S agreements. A portion of the C&S agreements contain an acquisition premium clause, in which the accumulated C&S project development fees billed by the Company will be paid in addition to the equity book value at the time of acquisition. In the event that either of the investors decides to sell all or part of its equity in the SFJVC to any third party, a portion of the agreements require the selling investor to obtain prior consent of the other investor before such sale and to grant the right of first refusal to the other investor on the like terms for the intended sale.

As of October 1, 2016, when Tri-way became the developer and operator of all fishery C&S Projects formerly under SIAF, CA’s new role is one of turnkey operator appointed by and working on behalf of Tri-way.

Land leases

Private ownership of land is not permitted in China. Therefore, the Company leases land that is either collectively owned land or state owned land, through land use rights. Corporate entities and individuals may own the property (buildings) erected on the land.

Land use rights may be transferred, but they are based on agricultural contracts and cannot be changed arbitrarily to non-agricultural purposes. The lease term varies from 27 to 60 years. There are certain uncertainties (e.g., lease term may not exceed 30 years and all transfers have not yet been registered correctly) in respect of certain leased land due to the fact that not all requirements have been fulfilled or not yet registered. However, the Company believes it is protected against these uncertainties through its agreements with the relevant local Chinese partners and relevant registration processes have been initiated. The Company’s subsidiary HSA has acquired land use rights for state owned land located in OuChi Village, FengHuo Town, LinLi County, Hunan Province. However, HSA has not obtained a land use right certificate for such land, which therefore, for the time being, cannot be lawfully mortgaged or transferred. Moreover, the Company’s subsidiary CA has entered into a Rural Land Management Rights Sub-Sales Agreement for the acquisition of the contractual operating and use rights of 202 mu of collective owned land located in Da San Dui Wei You Nan Village, Shenwan Town, Zhongshan City for a period of 30 years. However, the transfer procedures for the land in question have not been completed. CA is not an enterprise registered in mainland China and therefore, according to Chinese law, cannot acquire the contractual operating and use rights of collective owned land. The Company is currently negotiating with Beijing Hengxintianyi Investment Guarantee Co. Ltd. to designate a subsidiary of the Company in China for the purpose of entering into a new Rural Land Management Rights Sub-Sales Agreement.

License Rights

Through the past 10 years (from 2007 to present) the Company has improved and modified the Recirculating Aquaculture System (“RAS”) originally pioneered in Germany into a unique system designed for indoor systems referred to as A Power Module (“APM indoor”) and an outdoor module called open dam RAS (“ODRAS”). We provide two types of licenses under this technology namely, a Developer License permitting a fishery project license to utilize the technology in its design of the APM indoor or ODRAS farms, and an Operator license permitting the use of APM-indoor or ODRAS technology at their respective farms. Each license is granted a 50-year term per assigned module unit for a one-time fee of $50,000 per license, that is a $50,000 fee for rights to the Developer license and a $50,000 fee for rights to the Operator license for 50 years per developed module.

On November 12, 2008, the Company’s subsidiary TRW entered into an agreement with the inventor of a patent, Mr. Shan Dezhang, concerning the sale and purchase of the master license rights of a patent registered in China with patent number ZL200510063039.9.

On May 15, 2009, Tri-way (as licensor) entered into a sub-license agreement with SJAP (as licensee) concerning the sub-licensing of the above-mentioned patent (ZL200510063039.9). For further information on the aforementioned agreements, please refer to the section entitled “Intellectual Property Rights” above.

Regulation of M&A and Overseas Listings

On August 8, 2006, six PRC regulatory agencies, including the Ministry of Commerce (the “MOFCOM”), the State Assets Supervision and Administration Commission, the State Administration of Taxation (“SAT”), the State Administration of Industry and Commerce (the “SAIC”), the China Securities Regulatory Commission (“CSRC”), and the State Administration of Foreign Exchange (the “SAFE”), jointly issued the Regulations on Mergers and Acquisitions of Domestic Enterprises by Foreign Investors (the “M&A Rules”), which became effective on September 8, 2006 and was amended on June 22, 2009. The M&A Rules include provisions that purport to require that an offshore special purpose vehicle formed for purposes of the overseas listing of equity interests in PRC companies and controlled directly or indirectly by PRC companies or individuals obtain the approval of the CSRC prior to the listing and trading of such special purpose vehicle’s securities on an overseas stock exchange.

On September 21, 2006, the CSRC published on its official Website procedures regarding its approval of overseas listings by special purpose vehicles. The CSRC approval procedures require the filing of a number of documents with the CSRC. The application of this new PRC regulation remains unclear, with no consensus currently existing among leading PRC law firms regarding the scope of the applicability of the CSRC approval requirement.

The M&A Rules also establish procedures and requirements that could make some acquisitions of Chinese companies by foreign investors more time-consuming and complex, including requirements in some instances that the MOFCOM be notified in advance of any change-of-control transaction in which a foreign investor takes control of a Chinese domestic enterprise.

In February 2011, the General Office of the State Council promulgated a Notice on Establishing the Security Review System for Mergers and Acquisitions of Domestic Enterprises by Foreign Investors (“Circular 6”), which established a security review system for mergers and acquisitions of domestic enterprises by foreign investors. Under Circular 6, a security review is required for mergers and acquisitions by foreign investors having “national defense and security” concerns and mergers and acquisitions by which foreign investors may acquire “de facto control” of domestic enterprises with “national security” concerns. In August 2011, the MOFCOM promulgated the Rules on Implementation of Security Review System (the “MOFCOM Security Review Rules”), to replace the Interim Provisions of the Ministry of Commerce on Matters Relating to the Implementation of the Security Review System for Mergers and Acquisitions of Domestic Enterprises by Foreign Investors promulgated by the MOFCOM in March 2011. The MOFCOM Security Review Rules, which came into effect on September 1, 2011, provide that the MOFCOM will look into the substance and actual impact of a transaction and prohibit foreign investors from bypassing the security review requirement by structuring transactions through proxies, trusts, indirect investments, leases, loans, control through contractual arrangements or offshore transactions.

On October 23, 2019, the SAFE issued the Notice of the State Administration of Foreign Exchange to Further the Facilitation of Cross-border Trade and Investment, which cancelled restrictions on the use by foreign-invested companies that are not investment companies of their capital funds for equity investments.

Regulation of Foreign Currency Exchange and Dividend Distribution