UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

Commission File Number: 000-54191

SINO AGRO FOOD, INC.

(Exact Name of Registrant as Specified in its Charter)

| Nevada | 33-1219070 |

| (State or Other Jurisdiction of Incorporation) | (IRS Employer Identification Number) |

Room 3801, Block A, China Shine Plaza

No. 9 Lin He Xi Road

Tianhe District, Guangzhou City, P.R.C. 510610

(Address of principal executive offices, including zip code)

Registrant’s Telephone Number, including area code:(860) 20 22057860

Copies to:

Marc Ross, Esq.

Henry Nisser, Esq.

Sichenzia Ross Friedman Ference LLP

61 Broadway, 32ndFloor

New York, New York 10006

Telephone: (212) 930-9700

Securities registered pursuant to Section 12(b) of the Exchange Act: None

Securities registered pursuant to Section 12(g) of the Exchange Act: Common Stock, $0.001 par value per share

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| Large Accelerated Filer¨ | Accelerated Filerx |

| Non-Accelerated Filer¨ | Smaller Reporting Companyx |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

The aggregate market value of the voting stock held by non-affiliates of the issuer on June 30, 2015, based upon the $13.49 per share closing price of such stock on that date, was approximately $220,405,596.

There were 20,133,757 shares of common stock outstanding as of December 31, 2015.

Documents incorporated by reference: None

FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K (the “Annual Report”) contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, and Section 21E of the Securities Exchange Act of 1934, as amended. These statements relate to future events or our future financial performance. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,” “expects,” “can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predict,” “should” or “will” or the negative of these terms or other comparable terminology. These statements are only predictions; uncertainties and other factors may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels or activity, performance or achievements expressed or implied by these forward-looking statements. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Our expectations are as of the date this Annual Report is filed, and we do not intend to update any of the forward-looking statements after the date this Annual Report is filed to confirm these statements to actual results, unless required by law.

This Annual Report also contains estimates and other statistical data made by independent parties and by us relating to market size and growth and other industry data. This data involves a number of assumptions and limitations, and you are cautioned not to give undue weight to such estimates. We have not independently verified the statistical and other industry data generated by independent parties and contained in this Annual Report and, accordingly, we cannot guarantee their accuracy or completeness, though we do generally believe the data to be reliable. In addition, projections, assumptions and estimates of our future performance and the future performance of the industries in which we operate are necessarily subject to a high degree of uncertainty and risk due to a variety of factors, including those described in “Risk Factors” and elsewhere in this Annual Report. These and other factors could cause results to differ materially from those expressed in the estimates made by the independent parties and by us.

PART I

| ITEM 1. | DESCRIPTION OF BUSINESS |

In this Annual Report, unless the context requires otherwise, references to the “Company,” “Sino Agro,” “SIAF,” “we,” “our company” and “us” refer to Sino Agro Food, Inc., a Nevada corporation together with its subsidiaries.

Sino Agro Food, Inc.

SIAF is an agriculture technology and natural food holding company with principal operations in the People’s Republic of China. The Company acquires and maintains equity stakes in a cohesive portfolio of companies that SIAF forms according to its core mission to produce, distribute, market and sell natural, sustainable protein food and produce, primarily seafood and cattle, to the rapidly growing middle class in China. SIAF provides financial oversight and strategic direction for each company, and for the interoperation between companies, stressing vertical integration between the levels of the Company’s subsidiary food chain. The Company owns or licenses patents, proprietary methods, and other intellectual properties in its areas of expertise. SIAF provides technology consulting and services to joint venture partners to construct and operate food businesses, primarily producing wholesale fish and cattle. Further joint ventures market and distribute the wholesale products as part of an overall “farm to plate” concept and business strategy.

Revenues by division were as follows (in millions of U.S. dollars):

| Division (on Sales of Goods) | | 2015 | | | 2014 | |

| Fisheries (CA) | | $ | 85.4 | | | $ | 105.8 | |

| Organic Fertilizer (HSA & SJAP) | | | 164.6 | | | | 122.0 | |

| Cattle (MEIJI) | | | 35.3 | | | | 32.9 | |

| Plantation (JHST) | | | 13.7 | | | | 11.1 | |

| Corporate, Marketing & Trading (SIAF) | | | 37.9 | | | | 50.9 | |

| Total Revenues derived on sales of goods | | $ | 336.9 | | | $ | 322.7 | |

| Division (on consulting & services) | | 2015 | | | 2014 | |

| CA (Fishery related developments) | | $ | 88.5 | | | $ | 76.8 | |

| MEIJI (Cattle farm developments) | | | 0 | | | | 0 | |

| SIAF (Other developments) | | | 3.8 | | | | 4.9 | |

| Total Revenues derived on consulting & services | | $ | 92.3 | | | $ | 81.7 | |

History

The Company, which was formerly known as Volcanic Gold, Inc. and A Power Agro Agriculture Development, Inc., was incorporated on October 1, 1974 in the State of Nevada. The Company was formerly engaged in the mining and exploration business but ceased the mining and exploring business in 2005. On 24 August 2007, the Company entered into a merger and acquisition agreement with CA, a Belize corporation and its subsidiaries CS and CH. Effective of the same date, CA completed a reverse merger transaction with the Company.

For two years after its introduction in China, the Company operated in the dairy segment, but sold the dairy business in December of 2009 and began to implement its five year plan to develop its vertically integrated business operations consisting of (i) cattle fattening and production of beef products and (ii) cultivation of fish and prawn and related products. The Company now operates as an engineering, technology and consulting company specializing in building and operating agriculture and aquaculture farms in China.

Our principal executive office is located at Room 3801, 38th Floor, Block A, China Shine Plaza, No. 9 Lin He Xi Road, Tianhe District, Guangzhou City, Guangdong Province, PRC, 510610.

The table below provides an overview of key events in the development of the business of the Company.

| Year | | Event |

| 2006 | | · | Initiates agriculture and aquaculture consulting activities in China. |

| 2007 | | · | Changes name from A Power Agro Agriculture Development, Inc. to Sino Agro Food, Inc. |

| | | · | Acquires the Belize holding company Capital Award. Today, Capital Award is Sino Agro Food’s subsidiary operating many of the Company’s aquaculture activities. |

| | | · | Acquires the dairy operations through a 78 percent ownership stake in ZhongXing Agriculture and Husbandry. |

| | | · | Acquires the HU Plantation through a 75 percent ownership stake in Jiang Men City Heng Sheng Tai Agriculture Development. |

| 2009 | | · | Conducts a strategic review and divests the dairy business in December due to poor industry fundamentals with control of the industry concentrated in a few very large value-added manufacturers. |

| | | · | Founds Qinghai Sanjiang A Power Agriculture (“SJAP”). SJAP manufactures bioorganic fertilizer, livestock feed and develops other agriculture projects in the County of Huangyuan, in the vicinity of Xining City, Qinghai Province. |

| 2010 | | · | Creates a five-year plan to develop vertically integrated businesses in primary production, distribution and marketing of beef cattle, beef products and seafood through proprietary recirculating aquaculture systems. |

| | | · | Begins construction of the Company’s first fish farm, Fish Farm 1, with targeted capacity of 1,000 metric tons per year. |

| 2011 | | · | Begins construction of Prawn Farm 1 & 2, Cattle Farm 1 and Fish Farm 2. |

| | | · | Becomes a fully reporting SEC company on the OTCQB (as defined below). |

| 2012 | | · | Acquires a 75 percent ownership in Fish Farm 1 and Cattle Farm 1. Advances construction of Cattle Farm 2 and Wholesale Center 1 in Guangzhou. |

| | | · | Produces 1,800 MT of seafood and raises 6,000 head of cattle. |

| 2013 | | · | Closes the Zhongshan Prawn Farm agreement, targeting production of 10,000 MT of prawn p.a. in 2016/2017 and 100,000 MT in 2024. |

| | | · | SJAP awarded Dragon Head Enterprise status by the Qinghai provincial government. |

| | | · | Mr. George Yap and Mr. Nils-Erik Sandberg join SIAF’s Board of Directors, as independent directors. |

| | | · | Produces 4,700 MT of seafood and raises 15,000 head of cattle. |

| 2014 | | · | SJAP’s abattoir and meat processing facilities commence operations. SJAP signs supplier and concession agreements with Tesco, PLC China for packaged meat products. |

| | | · | Advances construction of a wholesale and distribution center in Shanghai, targeting ultimate capacity of 12,000 MT of meat and 6,000 MT of seafood per annum. |

| | | · | Mr. Anthony Soh and Mr. Dan Ritchey join SIAF’s Board of Directors as independent directors. |

| | | · | Ms. Olivia Lai is hired as Chief Financial Officer. |

| | | · | Produces 5,600 MT of Seafood and raises 26,000 head of cattle during 2014. |

| 2015 | | · | Sino Agro Food announces a long-term vision to become a leading sustainable aquaculture company focused on organically farmed fish and prawns. |

| | | · | Wholesale Center 2 in Shanghai initiates operations |

| | | · | Mr. Bertil Tiusanen is hired as Chief Financial Officer. Ms. Lai becomes the Company’s Chief Corporate Affairs Officer. |

| | | · | Sino Agro Food announces contemplated plan to divest its aquaculture operations and seek a separate listing on the Oslo Stock Exchange. |

| 2016 | | · | Sino Agro Food was admitted to the Merkur market in Oslo. |

| | | · | The Company upgraded to OTCQX Premier from the OTCQB®Venture Market. |

| | | · | Mr. Bertil Tiusanen resigned as Chief Financial Officer and was appointed as SVP Business Development, New Ventures Europe |

| | | · | Mr. Dan Ritchey was appointed as Chief Financial Officer. |

| | | | |

In all of its development projects, the Company has been contracted as Turnkey Contractor to the owners and developers of the C&S Project Companies and acted as the master engineer, pioneering the construction and building of farms, from raw land into fully operational facilities. The Company completes the construction and building of infrastructure including staff quarters, offices, processing facilities, storage, and all related production facilities. The Company’s management teams are responsible for developing all business activities into effective and efficient operations.

In just a few years, Sino Agro Food has matured into a company dedicated to the agriculture and aquaculture industry in China. The Company currently maintains operation of its HU Plantation (see description in section 4.10 below) as well as its services in engineering consulting, specializing in the development of two major products, namely meat derived from the rearing of beef cattle and seafood derived from the growth of fish, prawns, eel and other marine species.

Background

After successfully developing many aquaculture fishery farms, cattle farms and related business operations (along with sales and marketing of produce and products) in Australia and Malaysia since 1998, SIAF’s management team introduced our business activities in China in 2006. We are an engineering and consulting company that specializes in building and operating agriculture and aquaculture farms.

To accomplish this, we use our expertise and know how in specific agriculture and aquaculture technologies. Our “A Power Re-circulating Aquaculture System,” sometimes referred to herein as APRAS, is a patented and proven technology for indoor fish farming. We have developed modern techniques and technologies to grow, feed and house both fish and cattle. These are engineered into the designs of, and the management systems for, indoor and outdoor fishery and cattle farms. Our experience managing crops, and employing technologies, including hydroponic, to work within climate and growing conditions optimizes production of organic, green and natural agricultural produce.

In all of our developments we have acted as the master engineer, pioneering the construction and building of farms, from raw land into fully operational facilities. We complete the construction and building of infrastructure including staff quarters, offices, processing facilities, storage, and all related production facilities. Our management teams are responsible for developing all business activities into effective and efficient operations.

In just a few years, SIAF has matured into a company dedicated to the agriculture and aquaculture industry in China. We currently maintain operation of our HU Plantation as well as our services in engineering consulting, specializing in the development of two major products, namely meat derived from the rearing of beef cattle and seafood derived from the growth of fish, prawns, eel and other marine species.

Revenues are generated from activities that we divide into five stand-alone business divisions or units: (1) Fishery, (2) Cattle & Beef, (3) Organic Fertilizer, (4) HU Plantation, and (5) Marketing and Trading. This fifth and newest division, “Marketing and Trading” represents our strongest push to vertically integrate the Company’s operations, furthering the Company’s overall “farm to plate” concept.

Corporate Acquisitions

On September 5, 2007, we acquired two businesses in the People’s Republic of China (“PRC”):

(a) Tri-Way Industries Ltd., Hong Kong (“TRW”) (formerly known as Tri-way Industries Limited), a company incorporated in Hong Kong; and

(b) Macau EIJI Co. Ltd., Macau (“MEIJI”) (formerly known as Macau Eiji Company Limited), a company incorporated in Macau, and the owner of 75% equity interest in Enping City Juntang Town Hang Sing Tai Agriculture Co. Ltd. (“HST”), a PRC corporate Sino Foreign joint venture.

On November 27, 2007, MEIJI and HST established a corporate Sino Foreign joint venture, Jiangmen City Heng Sheng Tai Agriculture Development Co. Ltd, China (“JHST”) (formerly known as Jiang Men City Heng Sheng Tai Agriculture Development Co. Ltd.), a company incorporated in the PRC with MEIJI owning a 75% interest and HST owning a 25% interest. HST was dissolved in 2010.

In September 2009, we formed a 100% owned subsidiary in Macau, A Power Agriculture Development (Macau) Ltd., China (“APWAM”) (formerly known as A Power Agro Agriculture Development (Macau) Limited). APWAM presently owns 45% of a corporate Sino Foreign joint venture, Qinghai Sanjiang A Power Agriculture Co. Ltd. (“SJAP”). SJAP is engaged in the business of manufacturing bioorganic fertilizer, livestock feed and development of other agriculture projects in the County of Huangyuan, in the vicinity of the Xining City, Qinghai Province, PRC.

On February 28, 2011, TRW applied to form a corporate joint venture, Enping City A Power Prawn Culture Development Co. Ltd., China (“EBAPCD”) (formerly known as Enping City Bi Tao A Power Fishery Development Co., Limited), which is incorporated in the PRC. TRW initially owned a 25% equity interest in EBAPFD. On November 17, 2011, TRW formed Jiangmen City A Power Fishery Development Co. Ltd, China (“JFD”) (formerly known as Jiang Men City A Power Fishery Development Co., Limited) in which it acquired a 25% equity interest, while withdrawing its 25% equity interest in EBAPFD. As of December 31, 2011, we had invested $1,258,607 in JFD. JFD operates an indoor fish farm. On January 1, 2012, we acquired an additional 25% equity interest in JFD for total cash consideration of $1,662,365. On April 1, 2012, we acquired an additional 25% equity interest in JFD for the amount of $1,702,580. We presently own a 75% equity interest in JFD and control its board of directors. As of September 30, 2012, we had consolidated the assets and operations of JFD.

On April 15, 2011, MEIJI applied to form Enping City A Power Beef Cattle Farm 2 Co. Ltd., China (“EAPBCF”) (formerly known as Enping City A Power Cattle Farm Co., Limited), all of which we would indirectly own a 25% equity interest in as of November 17, 2011. On September 13, 2012 MEIJI formed Jiangmen City Hang Mei Cattle Farm Development Co. Ltd., a company incorporated in the PRC (“JHMC”) (formerly known as Jiang Men City Hang Mei Cattle Farm Development Co., Limited) in which it owns 75% equity interest with an investment of $3,636,326, while withdrawing its 25% equity interest in ECF. As of September 30, 2012, we had consolidated the assets and operations of JHMC.

Cross-Listing on the Merkur Market

On January 13, 2016, securities representing beneficial interests in the shares of common stock on the Company, referred to as VPS Shares, began to be traded on the Oslo Børs’ Merkur Market under the symbol “SIAF-ME.” The Company’s common shares continued to trade on the OTCQB under the symbol “SIAF.”

The Merkur Market is a multilateral trading facility operated by Oslo Børs ASA. The Merkur Market is subject to the rules in the Norwegian Securities Trading Act and the Securities Trading Regulations that apply to such marketplaces. These rules apply to companies admitted to trading on the Merkur Market, as do the marketplace’s own rules, which are less comprehensive than the rules and regulations that apply to companies listed on Oslo Børs and Oslo Axess. The Merkur Market is not a regulated market, and is therefore not subject to the Norwegian Stock Exchange Act or to the Stock Exchange Regulations. Investors should take this into account when making investment decisions.

Up listing to the OTC QX Premier

On January 19, 2016, the Company’s shares of common stock began to be traded on the OTCQX® Best Market in the U.S. under its existing ticker symbol “SIAF.” The Company upgraded to OTCQX Premier from the OTCQB®Venture Market.

The OTCQX® Market is the top tier of the U.S. over-the-counter markets operated by OTC Markets Company. It is reserved for established investor-focused companies meeting high financial and governance standards, and sponsored by professional third party advisors. SIAF has qualified to trade on OTCQX U.S. Premier, for which eligibility standards are higher still. For comparison, as of December 31, 2015, there were 942 companies traded on the OTCQB, 425 companies traded on the OTCQX and 98 companies traded on OTCQX U.S. Premier, of which only 17 are non-bank companies.

With OTCQX admission, OTC Market Company’s Blue Sky Monitoring Service provides the Company with a customized daily audit of its compliance status in all 50 states. Blue Sky complianceis mandatory for broker-dealers and registered investment advisors to solicit or recommend a security to investors.

U.S. investors can find current financial disclosure and Real-Time Level 2 quotes for the Company onwww.otcmarkets.com.

Emerging Growth Company

We are an “emerging growth company,” as defined in the Jumpstart Our Business Startups Act of 2012. We will remain an emerging growth company until the earlier of (1) the last day of the fiscal year (a) in which we have total annual gross revenue of at least $1.0 billion or (b) in which we are deemed to be a large accelerated filer, which means the market value of our common stock that is held by non-affiliates exceeded $700.0 million as of the prior June 30, and (2) the date on which we have issued more than $1.0 billion in non-convertible debt during the prior three-year period. We refer to the Jumpstart Our Business Startups Act of 2012 herein as the “JOBS Act” and references herein to “emerging growth company” shall have the meaning associated with it in the JOBS Act.

As an emerging growth company, we may take advantage of specified reduced disclosure and other requirements that are otherwise applicable generally to public companies. These provisions include:

| · | only two years of audited consolidated financial statements in addition to any required unaudited interim financial statements with correspondingly reduced “Management’s Discussion and Analysis of Financial Conditions and Results of Operations” disclosure; |

| · | reduced disclosure about our executive compensation arrangements; |

| · | no requirement that we hold non-binding advisory notes on executive compensation or golden parachute arrangements; and |

| · | exemption from the auditor attestation requirement in the assessment of our internal control over financial reporting. |

We have taken advantage of some of these reduced burdens, and thus the information we provide stockholders may be different from what you might receive from other public companies in which you hold shares.

In addition, Section 107 of the JOBS Act also provides that an emerging growth company can take advantage of the extended transition period provided in Section 7(a)(2)(B) of the Securities Act for complying with new or revised accounting standards. In other words, an emerging growth company can delay the adoption of certain accounting standards until those standards would otherwise apply to private companies. However, we are choosing to “opt out” of such extended transition period, and as a result, we will comply with new or revised accounting standards on the relevant dates on which adoption of such standards is required for non-emerging growth companies. Section 107 of the JOBS Act provides that our decision to opt out of the extended transition period for complying with new or revised accounting standards is irrevocable.

Reverse Split

On November 10, 2014, the board of directors of Sino Agro Food, Inc. approved an amendment to our Articles of Incorporation to effectuate a reverse stock split (the “Reverse Split”) of our common stock, par value $.001 per share, affecting both the authorized and issued and outstanding number of such shares by a ratio of 1 for 9.9. The Reverse Split became effective in the State of Nevada on December 16, 2014. The Market Effective Date of the Reverse Split was December 16, 2014, having been approved by the Financial Industry Regulatory Authority, Inc. (“FINRA”) on December 15, 2014. As a result of the Reverse Split, each 9.9 shares of common stock authorized as well as each such share issued and outstanding prior to the Reverse Split has been converted into 1 share of common stock, and all options, warrants, and any other similar instruments convertible into, or exchangeable or exercisable for, shares of common stock have been proportionally adjusted. All references to common stock have been retroactively restated.

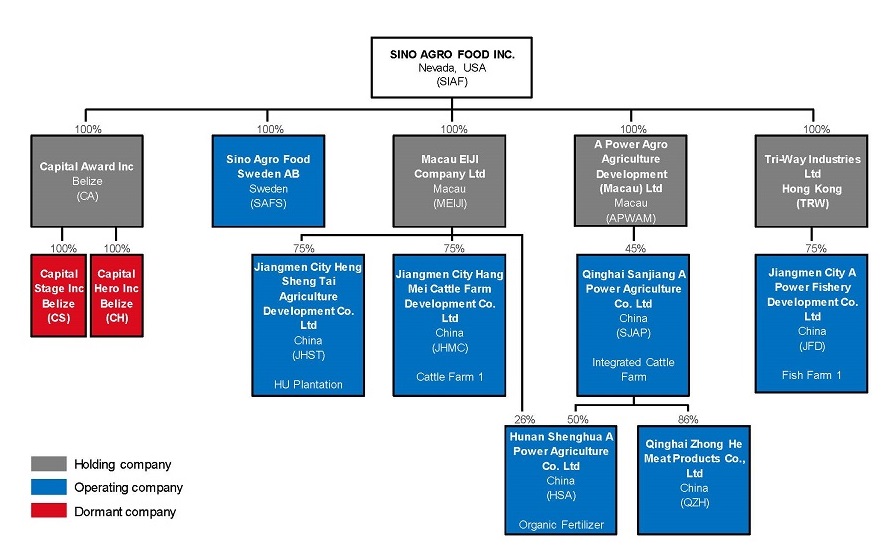

Legal structure

The Company is primarily a holding company whose operations are carried out through its subsidiaries.

The following table sets out information about the entities in which the Company, as of the date of this Annual Report, holds (directly or indirectly) more than 10 percent of the outstanding capital and votes.

The table below sets out a brief description of the companies within the Company as well as the Company’s respective holdings within such companies and their domiciles.

| Company | | Country of

incorporation | | Field of activity | | % Holding |

| Sino Agro Food, Inc. | | US | | Engineering consulting (general types of developments), business management, trading, sales and marketing | | |

| Capital Award Inc. (CA) | | Belize | | Engineering consulting (mainly in development of fishery), management of fishery operation, marketing and sales of fishery produces and products | | 100 |

| Tri-way Industries Limited (TRW) | | Hong Kong | | Holding company and holder of technology licenses | | 100 |

| Macau Eiji Company Limited (MEIJI) | | Macau | | Engineering consulting (mainly in cattle farming and vegetable farming), management service and marketing and sales of cattle and related products | | 100 |

| A Power Agro Agriculture Development (Macau) Limited (APWAM) | | Macau | | Holding company | | 100 |

| Sino Agro Food Sweden AB (publ) (SAFS) | | Sweden | | Various support and service to parent company, asset management, finance, consulting and provision of services in agriculture and aquaculture, marketing and sale of agricultural products, consultancy for business development in China, and related business | | 100 |

| Capital Stage Inc. (CS) | | Belize | | Dormant | | 100 |

| Capital Hero Inc. (CH) | | Belize | | Dormant | | 100 |

| Jiangmen City A Power Fishery Development Co. Ltd. (JFD or Fish Farm 1) | | China | | Growing of fish (sleepy cod species), eels (flower pattern species) and prawns | | 75 |

| Jiangmen City Hang Mei Cattle Farm Development Co. Ltd. (JHMC or Cattle Farm 1) | | China | | A demonstration farm for growing cattle in a semi-tropical climate | | 75 |

| Jiangmen City Heng Sheng Tai Agriculture Development Co. Ltd. (JHST) | | China | | HU plantation, immortal vegetable planning, processing and sales of produces and products | | 75 |

| Hunan Shenghua A Power Agriculture Co. Ltd. (HSA) | | China | | Existing activities: manufacturing of organic fertilizer, 100% pure organic mixed fertilizer and lake fish farming organic fertilizer. Cattle rearing. | | 76 |

| Qinghai Sanjiang A Power Agriculture Co. Ltd. (SJAP) | | China | | Existing activities: manufacturing of organic fertilizer (permits valid until December 2016), bulk and concentrated livestock feed, and rearing of cattle and cooperative farming. Slaughter and deboning of cattle and value added processing of beef products. | | 45 |

| Qinghai Zhong He Meat Products Co. Ltd. (QZH) | | China | | Cattle slaughter and deboning | | 86% |

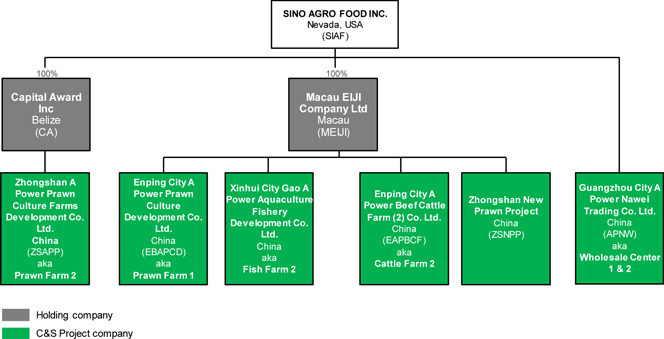

In addition to the legal entities included in the chart and table above, the Company is providing technology know-how with consulting service and turnkey contracting services (“C&S”) to various Chinese owned Project Companies (“C&S Project Company”) which mainly are private companies formed in China with Chinese citizens acting as legal representatives. Sino Agro Food does not have any ownership in these C&S Project Companies. However, in consideration of the Company’s right to protect its technology and know-how granted to the C&S Project Companies, the Company has an option to acquire equity stakes in the future SFJVC at an agreed value equivalent to the project’s development cost. The chart below sets out the various C&S Project Companies in which the Company is currently involved. The maximum equity stake, which may be obtained in any C&S Project Company is 75%.

On October 25, 2015, both QZH and new stockholder, Qinghai Quanwang Investment Management Co., Ltd (“QQI”) contributed additional capital of $4,157,682 and $769,941, respectively. As of result, SJAP decreased its equity interest from 100% to 85% and QQI owned a 14% equity interest. In addition, regarding the investment agreement between QZH and QQI, (i) QQI enjoyed 6% annual interest on its capital contribution, but not any profit distribution; (ii) investment period was 3 years, and (iii) SJAP shared 100% (2014: 100%) on profit or loss after 6% interest payment to QQI and enjoyed 100% (2014: 100%) voting rights of QZH’s board and stockholders meetings.

| Company | | Field of activity |

“EAPBCF” or “Cattle Farm 2” Enping City A Power Beef Cattle Farm 2 Co. Ltd. | | Cattle rearing |

“Fish & Eel Farm 2” XinHui City Gao A Power Aquaculture Fishery Development Co. Ltd. | | Growing fish, eels and prawns. Production started in 2014, although construction is on-going. |

“EBAPCD” or “Prawn Farm 1” Enping City A Power Prawn Culture Development Co. Ltd. | | Grow-out of mainly prawns, production started in Q3 2013. Additional production commenced from 10 additional APM tanks in Q2 2015. |

“ZSAPP” or “Prawn Farm 2” Zhongshan A Power Prawn Culture Farms Development Co. Ltd. | | Hatchery and Nursery operation of prawns, production started from Q2 2012. Growing of prawns using open-dams applying re-circulating filtration systems, with production started from Q3 2013, with construction still being in progress. |

“ZSNPP” or “Zhongshan New Prawn Project” (Guangzhou City A Power NaWei Trading Co. Ltd.) | | Grow-out of prawns and other seafood. Hatchery and Nursery operation of prawns and hydroponics to be commenced in the future. Trails for stocking of fingerling at its Phase (1) Stage (1) farms started from late February 2016. |

“APNW” or “Wholesale Center 1&2” (Guangzhou City A Power NaWei Trading Co. Ltd.) | | Marketing, sales and distribution of seafood and meats and related products |

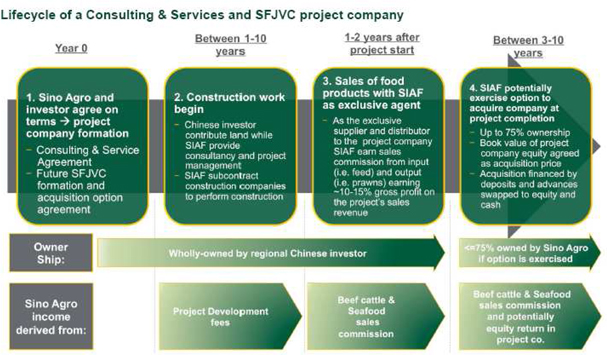

Business model

The Company works with Chinese investors to form operating companies, in which Sino Agro Food retains the option to acquire equity interest. After a certain period of time and successful operating results, the Company and the Chinese investor may form a Sino Foreign Joint Venture Company (“SFJVC”). Prior to the formal naming, registration, and incorporation of an anticipated SFJVC, the Company prepays a deposit toward the consideration of its future SFJVC stake as a percentage of the assets of the fully developed farm. Upon conversion, the prepayments become equity capital.

The Company oversees financing and provides interoperating strategies, encouraging vertically integrated growth. China has problems with quality assurance in primary production, distribution and poor origin traceability, as well as low food quality. This has created a market where consumers pay significant price premiums for organic food with brands guaranteeing quality and consistency.

A vertically integrated operation in a fragmented and poorly regulated environment such as in China is the strategy that will yield the most success for the Company. Our presence in retailing and wholesale markets generates market power and provides potential for both margin maintenance and expansion.

Integration into fertilizer and feed production for rearing of beef cattle together with breeding of prawn brood stock decreases primary production operational risks as well as the price volatility in production input goods.

Sino Agro Food uses expertise and know-how in specific agriculture and aquaculture technologies. The Company’s “A Power Re-circulating Aquaculture System” (the “APRAS”) is a proven recirculating aquaculture system (“RAS”) technology for indoor fish farming. Sino Agro Food has developed modern techniques and technologies to grow, feed and house both fish and cattle. These are engineered into the designs of, and the management systems for, indoor and outdoor fishery and cattle farms. Today Sino Agro Food is the world’s largest operator of RAS aquaculture for prawns. In all developments Sino Agro Food acts as the master engineer, pioneering the construction and building of farms, from raw land into fully operational facilities. Sino Agro Food builds the infrastructure including staff quarters, offices, processing facilities, storage, and all related production facilities; then, manages developing of all business activities into effective and efficient operations. Sino Agro Food’s largest customer represents a Company of thirty separate live seafood wholesalers at the Guangzhou wholesale markets.

The Company holds licenses for fertilizer formulas and for indoor fish farm techniques, including a “master license” in China for “A Power Technology” (“APT”), a modular land based fish growing system and technology utilizing RAS.

Sino Agro Food partners with Chinese investors in food projects as a turnkey project manager

The Company engages in projects as a technological and engineering expert, partnering with local and regional investors in food related projects. Sino Agro Food generally has exclusive marketing, sales and distribution rights for each project company. For example, CA purchases all marketable fish and prawns from the farms and distributes them to wholesale markets. CA also supplies the farms with fingerling, baby or adult fish or prawns and stock feed. MEIJI operates similarly with the cattle that are grown by Cattle Farm 1.

Generally, Sino Agro Food exercises an option to acquire a majority equity stake in the project company once development of the operating company has matured and successful operating results are demonstrated. Prior to acquisition, Sino Agro Food prepays a deposit toward the acquisition consideration of the project company. Upon acquisition and conversion into a SFJVC, the pre-payments together with a cash consideration become equity capital, with Sino Agro Food becoming a majority shareholder.

Acquired project companies are operated and managed by the management team and the Chinese investor, and overseen by Sino Agro Food.

Land ownership in China

In China, nearly all land is owned by the Central Government or local village collectives, which grant “usufructuary” rights (i.e., the right to use and enjoy the derived benefits for a period of time) in the form of land use rights. This is similar to “leasehold” land rights in the United States. Corporate entities and individuals may own the property (buildings) erected on Government land. Land use rights may be transferred, but they are based on agricultural contracts, and cannot be changed arbitrarily to non-agricultural purposes.

Business overview

Introduction

Sino Agro Food is an agriculture technology and natural food holding company with principal operations in China participating in the ongoing transformation of China’s fragmented agrarian sector into a modern food production industry using sustainable and profitable methods. Sino Agro Food focuses on seafood and beef production with integrated wholesale distribution. The Company acquires and maintains equity stakes in a cohesive portfolio of companies that Sino Agro Food forms according to its core mission to produce, distribute, market and sell natural, sustainable protein food and produce, primarily seafood and cattle, to the rapidly growing middle class in China.

Sino Agro Food employs a strategy of vertical integration from primary production through processing, distribution and marketing of high quality, organic food products in the food value chain. China’s fast growing middle class is creating rapidly rising demand for gourmet and high-quality protein food. The Company’s core products are live prawns, live eels, whole beef cattle and packaged beef meat.

The Company’s operations and strategy are executed through a number of subsidiaries located in China, and the Company contributes financial oversight and strategic direction to otherwise independent management teams which employ the Company’s intellectual property and proprietary methods within aquaculture, beef cattle rearing and production of organic fertilizer.

Sino Agro Food has enjoyed strong growth since the Company initiated its business activities in China in 2006. During the fiscal year of 2015, the Company’s consolidated revenues amounted to USD 429 million. The four principal factors that have enabled the growth are:

| · | Joint venture investment models with existing local Chinese investors in agriculture and aquaculture; |

| · | Technological competitive advantages in recirculating aquaculture, beef rearing and livestock slaughter; |

| · | Strong growth in Chinese consumers’ demand for quality protein food; and |

| · | The Chinese Government’s policy to consolidate the agrarian sector and increase the efficiency of China’s food production industry. |

Sino Agro Food provides consulting and services to a number of private Chinese third party companies to construct and operate primary production facilities for fish, prawn and beef cattle, as well as wholesale marketing and distribution centers. As part of its consulting and service agreements, Sino Agro Food has the option to acquire these operations in order to expand Sino Agro Food’s proprietary production and wholesaling capacity.

Revenues are generated from activities that are divided into five stand-alone business divisions:

| (i) | Aquaculture (CA: inclusive Technology engineering consulting & services (Project Development division) and sales of goods) |

| (ii) | Integrated Cattle Farm (SJAP & QZH) and Organic Fertilizer (HSA) |

| (iii) | Cattle Farm (MEIJI: sales of goods) |

| (v) | Seafood & Meat Trading (SIAF GZ: inclusive Technology engineering consulting & services (Project Development division) and sales of goods and corporate affairs) |

Aquaculture division

Operated by CA, the Aquaculture division is the business unit of Sino Agro Food active in sale of seafood. Revenue for fiscal year ended December 31, 2015 was USD 85.4 million, or 25.6 percent of the Company’s total sales of goods’ revenue of USD 336.8 million in the same period. Gross profit for the Aquaculture division for the fiscal year ended December 31st 2015 was USD18.3 million, or 24.0 percent of the Company’s total gross profit on sales of goods of USD 75.9 million in the same period. The table below lists aquaculture project companies with status and schedule for each.

CA has entered into several CSC’s. Their information and status are shown in the table below:

| Name of the Developments | | Fish Farm 1 | | Prawn Farm 1 | | Fish Farm 2:

The Fish & Eel Farm | | Prawn Farm 2:

Hatchery, Nursery & Grow-out

Farm |

| | | | | | | | | |

| Abbreviation of company Name | | JFD | | EBAPCD | | Fish & Eel Farm 2 | | ZSAPP |

| | | | | | | | | |

| Location | | Enping | | Enping City | | Xin Hui District, Jiang Men | | San Jiao Town, Zhong San City |

| | | | | | | | | |

| Annual capacity (as designed) | | 1,200 MT | | 2013=400MT 2014=800MT 2015=1200 MT | | 2014=800 MT 2015= 1600 MT 2016=2000MT | | 2013: 1.6 Billion Fingerlings and 400MT Prawns increasing yearly. By 2015:3.2 billion Fingerlings and 1200 MT Prawns |

| | | | | | | | | |

| Land area or built up area | | 9,900 m2 | | 23,100 m2 | | 165,000 m2 | | 120,000 m2 |

| | | | | | | | | |

| Current phase and stage | | Fully operational | | 2 phases and road work | | 4 phases | | 3 phases |

| | | | | | | | | |

| Date development commenced | | July 2010 | | Phase 1: June 2011 Phase 2.1 + 2.2 Road Work: August 2012 | | Phase 1: January 2012 Bridge & Road Oct. 2012 Phase 3: 2013 Phase 4: 2014 | | Phases 1 and 2: May 2012 Phase 3 2014 |

| | | | | | | | | |

| Contractual amount (in millions of U.S. Dollars) | | $5.3M | | Phase 1: $11.6M Phase 2: $6.39M Road Work: $2.94M Phase 3:$ 3.5 M Phase 4:$ 2.7 M | | Phase 1: $8.73M Bridge & Road $2.48M Phase 3 $4.38M Phase 4 $10.63M | | Phase 1 $9.26M Phase 2 $8.42 M Phase 3 $11.5M Phase 4: $12 M |

| | | | | | | | | |

| % complete as at March 28 2015 | | Fully Operational | | Phase (1) In operation Phase 2 : Production started Q2 2015 Road work: completed Phase 2 additional 10 APMs completed and operational | | Phase 1 completed Bridge & Road completed Phase 3 Completed Phase 4 not started Pending on owners’ decision for further work to be commenced. | | Phase 1 fully operational Phase 2 in operation Phase 3 85% completed but production started. Phase 4 started and 30% work has been done |

CA is the sole marketing, sales and distribution agent of the APRAS fishery and prawn farms. CA purchases all marketable fish and prawn from the farms, and then sells them to wholesale markets. CA also supplies the farms with fingerlings, baby or adult fish or prawns, and stock feed. CA generates revenue from the sale of seafood bought from farms that are Company subsidiaries or C&S Project Companies, as well as from contracted growers as further described below.

Jiangmen City A Power Fishery Development Co. Ltd. (JFD or Fish Farm 1): The Company owns a 75 percent equity interest in JFD, the owner and operator of Fish Farm 1, growing fish (sleepy cod species), eels and prawns. Fish Farm 1 is located in the Guangdong Province in China.

Built on a block of land measuring 9,900m2, Fish Farm 1 contains staff quarters that provide accommodation for up to 15 workers, a self-contained office, a laboratory, external live bait holding tanks, all season red worms nurturing tanks, dry and cold storage, workshops, processing facilities, a heating room, 500 Metric Tons (“MT”) of water holding tanks, landscape gardens, standby generator rooms, all related underground and above ground infrastructure, and a 4,000m2 fish grow-out farm.

This farm supports 16 RAS (or APM) tanks, each measuring 10m x 10m x 3m in depth and holding up to 240,000 liters (or 240 MT of water. Each tank has production capacity to grow up to 80 MT of aquatic animals per year depending on stocking cycles (frequency of stocking of fish), and initial size of the fish in each cycle. In other words, if the initial stocked fingerling is around 30-40 mm per fish, then it will take over 12 months to grow the fish into a marketable fish (averaging over 500 gram per fish) such that its annual production is only up to 30-35 MT per tank; however if the initial fish being stocked are at an average of 200 to 300 grams each then its stocking and harvesting cycle is four times per year, enhancing annual production capacity to up to 80 MT per tank.

Xinhui Gao A Power Fishery Development Co. Ltd. (Fish & Eel Farm 2):

Growing fish, eels and prawns. Production started in 2014, although construction is on-going.

CA was appointed exclusive wholesale distributor and marketing agent for the products produced by Fish & Eel Farm 2 for a period of three years from 1 September 2015. Under the terms of the relevant agreement, the off-take prices for the products shall be determined and fixed at the latest prices for Guangdong Province, Guangzhou City, Huangsha Wholesale Fish Market’s daily sales prices (as published on the web page of the National Agricultural Products Commercial Information).

Enping City Bi Tao A Power Prawn Culture Development Co. Ltd. (EBAPCD or Prawn Farm 1): The proposed name of the Company’s future SFJVC is subject to approval by relevant Chinese authorities under its application for SFJVC status. EBAPCD was established to own and operate Prawn Farm 1. EBAPCD commenced to generate revenue during Q3 2013. CA recognizes income (booked in the Aquaculture Division’s sales of goods) by receiving a distribution fee on the seafood sold by Prawn Farm 1 to the wholesale markets.

On 22 April 2013, the Company placed the first 500,000 Mexican White prawn fingerlings in Prawn Farm 1, and has noted that prawns are meeting growth benchmarks with low mortality, and reaching around 15 cm per prawn in size. The Mexican White shrimp are known in the west as “Western White Shrimp,” or by their genus species “Penaeus Vannamei.”

By Mid-year 2015, an additional of 10 RAS (or APM) tanks were built in Prawn Farm 1 as such the farm is now in operation with a total 14 RAS (APM) tanks.

CA was appointed exclusive wholesale distributor and marketing agent for the products produced by EBAPCD for a period of three years from August 31, 2015. Under the terms of the relevant agreement, the off-take prices for the products shall be determined and fixed at the latest prices for Guangdong Province, Guangzhou City, Huangsha Wholesale Fish Market’s daily sales prices (as published on the web page of the National Agricultural Products Commercial Information).

Zhongshan A Power Prawn Culture Farms Development Co. Ltd. (ZSAPP or Prawn Farm 2): Subject to approval by relevant Chinese authorities under application for SFJVC status, the proposed name of the future SFJVC is ZSAPP. Prior to the said official formation of the SFJVC, CA acts as Prawn Farm 2’s sole marketing agent and recognizes income from the following: (i) management fees and commission fees charged to Prawn Farm 2 based on RMB 20 per 10,000 pieces of White leg shrimp post-larvae and RMB 40 per 10,000 pieces of Giant River Prawn post-larvae and (ii) the purchases of prawns and fishes from Prawn Farm 2 and sale to the wholesale markets.

CA was appointed exclusive wholesale distributor and marketing agent for the products produced by ZSAPP for a period of three years from 7 September 2015. Under the terms of the relevant agreement, the off-take prices for the products shall be determined and fixed at the latest prices for Guangdong Province, Guangzhou City, Huangsha Wholesale Fish Market’s daily sales prices (as published on the web page of the National Agricultural Products Commercial Information).

Zhongshan New Prawn Project (“ZSNPP”): In March of 2014, Sino Agro Food announced that CA was granted a contract to build an 8,000 MU prawn and agriculture center in Zhongshan City. CA has been engaged to provide construction and development services, as well as consulting support in the form of management, supervision, and training. The contract price for Phase 1 of the project is stipulated at USD 180 million +/- 15 %. If project costs exceed this number, there are no provisions in the agreement providing for extra compensation. However, under Chinese law, CA is entitled to be compensated if the Chinese party has asked for work in excess of what the estimation in the current contract has been based on. The fees payable to CA are presently estimated to total approximately USD 149.6M, consisting of USD 104.3M from construction and development, and USD 45.3M from consulting, including USD 8.5M in license fees for up to 350 A-Power Modules that the licenses that are valid for 50 years. CA anticipates being designated as the marketer and distributor of the project’s end product prawns, eels, fish and produce.

To date, the Company has completed or is just about to complete the following:

| (i) | A complex of office space, staff quarters, staff canteen, storage, parking areas and landscaping encompassing a total of 2,000 square meters on 15,000 square meters of land (about 23 MU or about four acres). These facilities are sufficient to house the staff personnel and working areas to administer Phase 1 of the project. |

| (ii) | Two out of three buildings in Phase (1) development, with each building occupies 8,560 m2 of floor area, houses 48 standard units of APM filters (with each standard APM filter controls and situated in between two APM tanks that collectively act as one unit has the capacity to contain up to 400 MT of water within its dimension of 12 m x 12 m x 3m in depth) are 95% completed with initial trials for stocking of prawn fingerling commenced in late February 2016; as of the date of this Annual Report, said prawn fingerling have been grown to an average size of 2 cm prawns that were transferred into 2nd stage grow-out tanks for their 2nd stage grow-out. |

| (iii) | A 3.5 Km coastal boundary road and over 5 Km of internal roads. |

| (iv) | Basic infrastructure in landfills and leveling, electricity and water supplies, underground drainages and pipes and cables have been laid and connected covering total areas measured up to 132 acres within the project property of 635 acres. |

| (v) | A demonstration model consists of 4 opened (RAS or APM) dams is 80% completed on a 10 acre block of land. |

| (vi) | 60% of construction work has been completed for the development of salt water, fresh water and wastewater holding dams with inbuilt filters (using the RAS or APM technology) on a 12 acre block of land. |

The Phase (1) model targets production capacity of 10,000 metric tons of prawns within said 3 buildings, with trials having commenced at the end of February 2016 and commercial operations of the Phase (1) Stage (1) built farms in said Building (1 & 2) scheduled to begin in July 2016.

Integrated Cattle Farm division (SJAP)

Operated by SJAP, the Integrated Cattle Farm division is the business unit of Sino Agro Food active in beef cattle rearing and value added processing of domestic and imported beef meat. Revenue for fiscal year ended December 31, 2015 was USD 144.6 million or 42.9 percent of the Company’s total sales of goods revenue of USD 336.8 million in the same period. Gross profit for SJAP in the fiscal year ended December 31, 2015 was USD 33.3 million, or 43.9 percent of the Company’s total gross profit in sales of goods of USD 75.9 million in the same period.

Within the beef cattle farm division, the Company applies a co-operative farming model creating an intermediary supply pipeline to ramp up production at lower marginal cost to its operations.

The cattle grown by the Company are primarily Simmental, Charolais, and Angus. In general, local farmers buy 12 to 15 month old cattle from the Company’s cattle agents, and the Company commits to repurchasing the cattle between 21 months to 24 months old.

SJAP now has twelve cattle houses, with its smaller buildings housing a minimum of 200 head and larger cattle houses accommodating up to 350 head.

Within the Chinese agriculture market, small farmers lack commercial scale and expertise and therefore benefit from a strategic alliance. The Company works with the local government, soliciting their help to introduce and initiate a farmers’ co-operative, such as in the Huangyuan County, Xining City. This concept of strategic alliance with smallholder farmers under a co-operative farming model was originated and has been based on the following key characteristics and value enablers:

| · | The Company assesses the ability of the regional farmers to grow crops and pastures as its nominated contractors, using the Company’s land that is leased to the Company free of rent by the local government or using the farmer’s own land. The regional farmers use the Company’s plant and equipment for their planting and harvesting. The Company provides the farmers with supervision and associated services, seeds and organic fertilizer on credit terms, and also purchases crops and pastures from them. |

| · | The Company also uses this regional farmers’ concept when growing cattle. The farmers are the Company’s contractors using the Company’s bulk livestock feed and concentrated livestock feed on credit terms. The Company buys the mature cattle, which the regional farmers raised on the Company’s livestock feed. |

| · | Ultimately, the Company is aiming to obtain cattle that will be qualified as “organically raised cattle,” in order to produce organic beef products on a commercial scale. |

The key features of the co-operative farming model are set out in the illustration below:

As of the date of this report, SJAP has established 22 farmer co-operatives that have the capacity to fatten up to 20,000 head of cattle per year based on a 3-month turn-around program. The cost of rearing cattle is expected to be lower as a result of concentrating efforts on manufacturing and/or selling livestock feed. The regional farmers are contracted to grow crops and pasture for the Company using the Company’s land that has been provided lease-free by the local Government or by using their own land, the Company’s equipment operated by its workers for planting and harvesting, and the Company’s supervision and associated services, as well as seed and organic fertilizer. These items are provided to them on credit, which are then charged against their account when the Company purchases the crops and pasture grass from them in return. Regional farmers also raise cattle for the Company using its bulk and concentrated livestock feed under the same credit terms and conditions described above. That is, when the Company purchases the mature cattle from the regional farmers, their accounts are charged for the feed against the amount paid.

| 2. | The Organic Chain: (Organic Beef Product and Supply Chain) |

The Company prepares its agricultural wastes into bioorganic fertilizer.1 Also the livestock feed2 is prepared into bioorganic livestock feed. Bioorganic fertilizer and the bio-organic livestock feed is sold to farmers that work on the Company’s land-use rights, which is owned by the government and leased with a subsidy or rent free, due to the many benefits for the community. Fertilizer and livestock feedis are prepared based on the Company’s patented enzyme. The use of the enzyme is synergistic, as the production of fertilizer and livestock feed is permissible all 12 months of the year, which is a competitive advantage.

The farmers use the bioorganic fertilizer on the soil and feed the grain to the cows together with the livestock feed. Government tests show:

| · | Additional average weight gain per head of fattening cattle; |

| · | Additional fresh milk is produced; |

1 Through the environmental friendly “Bacterial and Bio-organic Fertilizer Manufacturing Technology”

2 Consists of raw material consisting of crop wastes as well as locally grown and available wild wheat plus wild wheat sterns, wild peas with sterns and leaves, and selective pastures grown in the wild. These raw materials will be finely cut and put through a number of aging and fermentation processes by adopting a technology and method called “Stock Feed Manufacturing Technology,” duly licensed by TRW, a 100 percent owned subsidiary of the Company, and catalyzed by the enzyme developed by SJAP. Thereafter, the end materials will be packed and sealed in airtight and weatherproof packaging ready for storage.

| · | All feeds are much easier to digest resulting in much cleaner environment in the cattle yards and houses; |

| · | No ill effects were recorded due to the Company’s feed; |

| · | All cattle preferred to eat the Company’s feed and were reluctant to revert back to the consumption of their old feed after they had consumed the Company’s feed during the period. |

Through an acquired patent,3 the fat content of a 15 month-old cattle can be decreased from 15 kg to 5 kg, which improves the quality of the meat and its yield. The inventor of the patent is now an equity partner in SJAP.

On February 28, 2013, SJAP completed its development of the Concentrated Livestock Feed (“CLF”) manufacturing factory, and started the production and sales of CLF. This CLF complements SJAP’s bulk livestock feed to provide the local cattle and sheep farming industry with a completed feed formula that can cater to the rearing of cattle and sheep at various growing cycles (e.g., specially formulated mixes with efficient nutrients for dairy cows and sheep, weaning, fattening and mature cattle and sheep). The advantage of the formulated feed combination is that the cattle and sheep growers will realize cost savings in production knowing precisely the amount of concentrated feed that will be needed by their livestock, thus avoiding wasted excess concentrated feed due to over feeding, which results in worthless excess fat in mature animals. In this respect, the Chinese central government has placed an order with SJAP to reserve up to 5,000 MT of CLF annually as part of the country’s annual reserve emergency livestock feed inventory. Thus, since March 2013 onward, SJAP has generated additional revenue generated from the sales of CLF.

SJAP sells its organic fertilizer and bulk livestock feed mainly to its cooperative and regional farmers in addition to using it to rear its own grown cattle, but because its geographic location is so far away from other major provinces there are high costs associated with selling its fertilizer, bulk livestock feed and live cattle other than to local purchasers. Conversely, equivalent imports from other provinces must be purchased at a higher cost, providing SJAP with a competitive edge. Furthermore, Qinghai Province is a region rearing millions of cattle and sheep per year, providing an ample market for SJAP’s fertilizer and livestock feed.

In the longer term, the Company believes that wholesale prices of SJAP’s livestock feed will maintain a steady growth rate of 5% to 10% per annum influenced mainly by rising labor cost of the country.

| 4. | Value Added Processing and distribution |

In 2014 the Company initiated operations in slaughter and deboning services to farmers at its abattoir and deboning facilities. SJAP received a business permit from the Chinese authorities on April 17, 2013, and construction commenced on April 21, 2013 on the abattoir, deboning factory, and related packaging facility. Since it is rare and difficult to obtain a permit for an abattoir facility in China, having this facility is expected to become a very valuable asset for the Company. To date, SJAP’s abattoir, deboning factory and packaging facilities are fully operational.

Before the abattoir and related facilities were operational, the Company sold mostly live cattle to or through various cattle wholesalers to existing wholesale and distribution markets that did not require much marketing efforts and networking.

In China, beef is customarily distributed through various tiers of established wholesalers and distributors that source their beef from various slaughter and deboning houses located across many districts in China. Most of these wholesalers sell multiple types of frozen or freshly chilled meats (including pork and poultry, etc.), and some slaughterhouses specialize in and solely supply beef. These wholesalers and distributors supply beef to regional supermarket chain stores, retailing wet and frozen food markets, the catering industry, etc. Therefore, after having established its own slaughterhouse and deboning factory, SJAP is expected to automatically become the primary supplier of beef. As such, many existing wholesalers and distributors will source their beef supplies directly from the Company. With the current ever increasing demands of quality beef meats due to the increase of middle class consumers, the Government’s enforcement of food safety regulation, and of anti-smuggling and illegal imports of beef, the right opportunity exists for SJAP to market its high-quality beef product. Therefore, the Company is confident it will successfully sell its beef meats in domestic markets. Also, a portion was exported to South Asian countries (i.e., Malaysia, Singapore, Hong Kong, Middle East countries and Thailand etc.) in 2014, as the Local Government encourages the Company to do.

The following table shows the current average mark-up margin for most of the sellers and operators in the beef trade in China:

| Type of wholesalers, distributors or retailers | | Mark-up Margin in Localities (Low / High) |

| | | Tier 1 Cities | | Tier 2 and Tier 3 Cities | | Tier 4, Tier 5 & Lower Cities |

| Slaughter cum deboning houses | | 30% / 35% | | 33% / 38% | | 39% / 42% |

| 1st tier wholesalers and distributors | | 10% / 12% | | 12% / 15% | | 15% / 20% |

| 2nd and 3rd tier wholesalers and distributors | | 15% / 20% | | 18% / 25% | | 20% / 30% |

| 1st tier retailers (i.e. supermarket chains) | | 22% to 35% | | 22% / 35% | | 22% / 35% |

3T1 Enzyme Technology (T1), Patent number ZL2005 10063039.9.

The Company’s marketing strategy to sell its beef meats and beef products targets the middle class consumers through the following developments:

| Development Items and Marketing Channels | | Estimated Annual Beef Production in Metric Tons (MT) | | | Share of Sales | |

| | | 2014 | | | 2015 | | | 2016 | | | 2014 | | | 2015 | | | 2016 | |

| | | | 6,000 | | | | 9,000 | | | | 18,000 | | | | | | | | | | | | | |

| Develop up to five sales and distribution outlets in Guangzhou, Beijing, Tianjin, Chongqing and Shanghai City | | | | | | | | | | | | | | | | | | | | | | | | |

| (A) Existing localized 1st, 2nd and 3rd tier wholesalers and distributors in these cities | | | | | | | | | | | | | | | 60 | % | | | 45 | % | | | 35 | % |

| (B) Own sales and distribution outlets* | | | | | | | | | | | | | | | 40 | % | | | 30 | % | | | 30 | % |

| Develop up to five sales and distribution outlets in Fuzhou, Changsha, Suzhou, Shenzhen and Xiamen City | | | | | | | | | | | | | | | | | | | | | | | | |

| (A) Existing localized 1st, 2nd and 3rd tier wholesalers and distributors in these cities | | | | | | | | | | | | | | | | | | | 15 | % | | | 20 | % |

| (B) Own sales and distribution outlets * | | | | | | | | | | | | | | | | | | | 10 | % | | | 15 | % |

*The Company’s own sales distribution outlets will include the development and operation of the following:

| · | 1st and 2nd Tier Wholesale and Distribution Network directly competing with, and supplying to, existing local wholesalers. |

| · | Distribution and service networking into supermarket chains, restaurant chains and domestic distributors. |

| · | Franchising of “Bull” Restaurants that will sell the Company’s own beef and beef products |

Currently the Company’s “Bull” restaurant serves as a demonstration model. Converted from an old cattle house, and situated next to the renovated cattle houses at SJAP’s complex, the “Bull” restaurant seats over 130 and uses on average one head of cattle every three days.

The Company assumes that in big cities, compared to the small community of Huangyuan where the demonstration restaurant is located, a similar restaurant must have the capacity to use up to at least two head of cattle per day, equal to 730 head per year. Therefore, if and when the Company develops additional “Bull” restaurants, it is anticipated realizing sales of up to 36,500 head of cattle in a year, which is more than SJAP targets to slaughter in 2016 (i.e., 30,000 head).

The table below lists some of the biggest wholesale frozen food (including beef) markets in Tier 1 cities (i.e., Beijing, Shanghai and Guangzhou City) from which there are many established logistic services to channel frozen goods to other Tier 2 and Tier 3 cities, where many existing localized wholesalers and distributors are situated and operating:

| City | | Name of Wholesale (cold storage) Markets | | Address |

| Beijing | | XinFa Di Wholesale Market of Agricultural Produce | | XinFa Di Bridge, Jingkai Highway, Fengtai District, Beijing |

| | | Jing Hua Jin Niu Qing Zhen Wholesale Market of Meat and Aquatic Produce | | No.6 Nanding Road, Fengtai District, Beijing |

| | | YueGeZhuang wholesale Market | | No.34 Fengtai Road, Beijing |

| | | Jin Xiu Da Di Wholesale Market of Meat | | No.69 Fushi Road, Haidian District, Beijing |

| Shanghai | | Shanghai City Beef and Mutton Wholesale Trade Market | | No.178 Nanda Road, Baoshan District, Shanghai |

| | | Cao An Hu Tai Agricultural Wholesale Market | | Mei Ling North Road, Putuo District, Shanghai |

| | | Shanghai Agricultural Produce Wholesale Market Centre | | Hunan Road, Pudong District, Shanghai |

| | | Shanghai Qi Bao Agricultural and Sideline Products Integrated Trading Market | | Laiting North Road, Minxing District, Shanghai |

| | | Shanghai Jiang Yang Agricultural Produce Wholesale Market | | Jiang Yang North, Baoshan District, Shanghai |

| | | HuiFeng Frozen Produce Market | | No. 5 Shui Chang Road, Huang Shi Xi Road, Guangzhou |

| | | Zi You Ma Frozen Produce Wholesale Market | | No.1 Huang Shi Xi Road, Guangzhou |

| | | Da Luo Tang International Frozen Produce Centre | | Qiao Xing Avenue, Panyu District, Guangzhou |

Note: the Company intends to acquire an existing wholesale establishment in each of these Tier 1, Tier 2, and Tier 3 Cities to be its main sales and distribution outlets, and as its main regional sales administration centers.

With the slaughterhouse, deboning and value added processing facilities (“VAF”) operational since Q1 2014, the Company expects rapid growth of revenue and profits for SJAP, thereafter.

The combined operation of SJAP achieved sales revenues of USD144.6 million in 2015 compared to USD102.04 million in 2014, representing a growth rate of 41.7 %.

Overall, SJAP expects that revenues from operations will multiply and increase rapidly as a result of the addition of further herds, and of comprehensive value added processing and marketing facilities.

In this respect, SJAP’s fully owned subsidiary Qinghai Zhong He Meat Company (or QZH, the company that operates the VAF) increased sales revenue by USD 44.3 million or 336% from 2014’s USD13.2 million to 2015’s USD 57.6 million and generated gross profit of USD15.1 million in 2015 compared to USD3.9 million in 2014.

In 2014, the Company expected a trend of continuous increases in beef and cattle prices given the increase in demand for quality beef and beef products (including value-added products) in tandem with the rise of living standards in China, the short supply of quality breeding stock that will be required to produce enough cattle to satisfy the increased demand. However, this prediction turned out to be wrong because the Chinese government changed its beef import policy during the 2nd quarter of 2015 relaxing the restriction on beef imports from eleven countries (e.g., New Zealand, Brazil, Australia, etc.), which started to affect the local cattle and beef industry primarily due to the drop of local cattle and beef prices from June 2016 as supplies were increasing rapidly while the growth rate of China’s middle-class did not keep pace in such a short space of time; (i.e., early months 2015 averaged wholesale prices for live weight cattle was at about RMB32 / Kg and it went as low as to RMB20 / Kg by December 2015).

In this respect, SJAP’s overall cattle division (excluding QZH) achieved sales revenue of USD86.97 million in 2015 compared to 2014’s USD88.8 million (representing a negative growth rate of -1.86%) and gross profit dropped to USD18.25 million from 2014’s USD26.95 million (representing a drop of 32.3%).

In order that the impact of said governmental change of policy affecting the local cattle and beef industry could be minimized, the Company decided to implement the following business plan and direction ( the “Program”):

| • | Increase its VAP activities by importing more beef from other countries (Australia and Brazil, etc.); |

| • | Upgrade its cattle herd by 2018 aiming at annual production thereon at rates of 3,000 head of Wagyu cattle, 2,500 head of 500-day grain fed angus and 2,500 head of pure organically grown angus, thus reducing its current cattle herd makeup gradually down to zero by 2018 starting from last quarter of 2015; |

| • | To add more value added processing lines of activities (i.e. canning division etc.) to gain more export sales apart from its domestic sales; |

| • | To expand its marketing network to cover major cities of nearby provinces that collectively have more than 350 million in population; and |

| • | To train and to recruit suitable human resources effectively and efficiently. |

The Program will involve additional capital expenditure and working capital over a 3-year period; as such, the Company may divest SJAP and list it as a stand-alone entity on a Chinese Stock Exchange such that it will be able to raise capital to finance the development needs of the Program. There can be no assurance that the Company will ultimately pursue this plan or, if it does, when such a spin-off would occur.

Organic Fertilizer (HSA) division

The business division Organic Fertilizer refers to the operations of the subsidiary HSA in Linli District, Hunan Province. Revenue for the fiscal year ended December 31, 2015 was USD 20 million, or 5.9 percent of the Company’s total sales of goods revenue of USD 336.8 million in the same period. Gross profit for the Organic Fertilizer division for the fiscal year ended December 31, 2015 was USD8.5 million, or 11.2 percent of the Company’s total gross profit for sales of goods of USD 75.9 million in the same period.

The operation in Linli District, Hunan Province, is run by HSA, a 76% owned Chinese subsidiary. HSA conducts the following business activities, both of which are in the development stage:

| · | manufacturing and sales of organic and mixed fertilizer, |

| · | cultivation of pastures and crops in preparation for the establishment of beef cattle farms, and |

By January 2013, the first organic fertilizer production plant was established and started its production of organic fertilizer. On March 5, 2013, HSA secured the rights to use an enzyme developed by a Hong Kong company some twenty years ago that has been utilized by global manufacturers of organic fertilizer. The advantage of this particular enzyme is that when it is applied to the organic fertilizer it has the ability to convert part of the organic raw materials into potash and phosphate without having to add in chemically formulated potash and phosphate, such that the Company’s end fertilizer can be qualified as pure organic fertilizer made with 100% natural organic raw materials. With this pure organic fertilizer, HSA is in a position to fully explore the potential market for fish in farm lakes and thereby to attempt to align itself with the government’s policy of encouraging lake fish farmers to use pure organic fertilizer instead of chemical fertilizers. In addition, cost savings from avoiding the use of chemical potash and phosphate will, in management’s belief, result in a better profit margin for the Company. Sales of pure organic fertilizer commenced at the end of Q1 2013.

Currently, chemical fertilizers in the region are sold at wholesale between RMB 3,000 to 3,600 per MT depending upon their chemical composition, compared to organic fertilizer from HSA selling at an average of RMB 1,200 to RMB 1,300 per MT. The Company’s new 100% pure organic fertilizer with up to 8% potash is currently being marketed between RMB 2,000 to RMB 2,200 per MT targeting to reach an average up to RMB2,600 per MT such that its prices will be at the mid-range between organic and chemical fertilizer.

HSA produced 50,000 MT of organic fertilizer and organic mixed fertilizer in 2014 under its newly completed production plant and facilities, and aims to ultimately increase its capacity to about 90,000 MT per year in stages. The main hardship related to selling fertilizer is the requirement to provide longer credit terms (sometimes up to 180 days) to the Company’s end buyers because these end users normally can afford to pay for them only after they sell their products. Therefore, the Company must assess creditworthiness of its prospective customers, and only consider the farmers who can be deemed creditworthy, and who follow the Company’s requirements for planting their fields and harvesting crops each year.

Development of HSA in Linli District, Hunan Province, follows SJAP’s business model. HSA is situated in a much better growing environment than SJAP, a farming rich province in central China. Thus, HSA benefits from cheaper logistics costs, close proximity to large markets, and a more favorable climate (milder winters and longer summers versus SJAP’s long bitterly cold winters and short summers). However, financial support from the Government is more difficult to obtain in the Hunan Province because more entities share the Government’s support provisions.

HSA endures both higher development costs and longer time to construct its facilities when compared to SJAP, whose property had 40 older (yet salvageable) buildings, which it has renovated to meet its needs.

Hunan Province is one of the biggest primary producing provinces of China with over four million primary producers that grow rice, tea, tobacco, grapes, citrus, cotton, seedlings, sunflowers, herb plants and many varieties of cash crops. Hunan also has a long-standing history in lake aquaculture producing millions of tons of fish and other seafood annually (e.g., total primary production is over RMB 450 Billion, or about USD 75 Billion, recorded in 2011 as announced by Hunan Province Agriculture Department).

At the Company’s newly built fertilizer factory, the 100% pure organic mixed fertilizer (“POMF”) is generating stable income and revenues reached targets in 2015 of over 13,037 MT of Organic Fertilizer, 36,232 MT of Organic Mixed Fertilizer and 180 MT of retailed packed fertilizer, collectively amounting to just under 50,000 MT.

Construction work to develop HSA’s cattle station that began in March 2012 with preparation work on its general layout is now, as of December 2015, a 2,000 head capacity cattle farm built and ready for operation. The Company cultivated 75 acres of its land, situated below the fertilizer factory, and planted crops and pasture.

The Company’s plan for HSA is to process cattle waste from its own cattle farm to be used as raw materials for the manufacturing of fertilizer, thus there will be substantial saving in its cost of fertilizer manufacturing (estimated at over USD2.5 million per year based on current sales), and with such cost of saving, HSA will be able to self-finance the development of its Yellow Cattle Program designed to eventually produce the Yellow Cattle into one of the top quality beef cattle in Asia, aiming to reach meat quality on par with Japanese Wagyu Cattle.

Therefore the Company’s plan is to merge Cattle Farm (1) & (2) with HSA sometime in 2016 or 2017, at the latest, such that CF (1 & 2) will be the breeding station to supply yearlings for HSA to grow into full grown cattle (up to 3 years old) that will be sold in the Chinese market. The Yellow Cattle is very similar in body size and weight and quality to the Japanese Wagyu cattle and has distinct meat texture, flavor and quality that are in high demand in China.

Cattle farms (MEIJI) division

The business division Cattle Farms, or MEIJI, refers to SIAF’s cattle rearing operations in Jiangmen, Guangdong Province. Revenue for fiscal year ended December 31, 2015 was USD 35.3 million, or 10.5 percent, of the Company’s total sales of goods revenue of USD 336.8 million in the same period. Gross profit for the Cattle Farm (MEIJI) division for the 12 months ended December 31, 2015 was USD 1.9 million, or 2.5 percent of the Company’s total gross profit on sales of goods of USD 75.9 million in the same period.

Currently there are two operations in this segment, Cattle Farm 1 and Cattle Farm 2. Sales for 2015 amounted to 14,947 head of cattle.

Cattle Farm 1: Cattle Farm 1 was built as a demonstration farm to show that cattle can be raised in a semi-tropical climate using the Company’s semi-grazing and housing method. Using the Company’s semi-free growing management system, the cattle are allowed to graze in the field during the early morning and kept indoors and out of the sun during the hot summer days. This method has proven reliable, with the growth rate of the cattle measuring slightly higher than the cattle at SJAP (i.e., averaging around 0.28 kg per day per cattle more).

Cattle Farm 2:Cattle Farm 2 is a beef cattle farm situated in Guangdong Province, Guangzhou City. Cattle Farm 2 is operated by a private company formed in China with Chinese citizens acting as its legal representative as required by Chinese law. EAPBCF will become a Sino Agro Food subsidiary when its SFJVC is officially formed. This is expected to occur during 2016 or 2017 pending availability of free cash flow of the Company; however, no guarantee can be made that the SFJVC will be formed.

Cattle Farm 2 is complementary to Cattle Farm 1, having an additional 76 acres of land suitable for growing the Company’s type of pasture (a cross between elephant grass and yellow grass) that has a very high yield rate of over 35 MT per 1/6 acre per year, and containing an average of over 9 percent protein that is very suitable for consumption by cattle. Between the two farms, under normal seasons, they have a capacity to produce up to 30,000 MT of pasture/year collectively that is capable to feed up to 5,000 head of cattle/year based on the consumption rate on average of 6 MT/head.