Table of Contents

As filed with the Securities and Exchange Commission on August 10, 2010

Registration Statement No. 333-165999

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 6

to

FORM S-11

FOR REGISTRATION

UNDER

THE SECURITIES ACT OF 1933

OF CERTAIN REAL ESTATE COMPANIES

DLC Realty Trust, Inc.

(Exact name of registrant as specified in its governing instruments)

580 White Plains Road

Tarrytown, New York 10591

(914) 631-3131

(Address, including Zip Code, and Telephone Number, including Area Code, of Registrant’s Principal Executive Offices)

Adam Ifshin

Chief Executive Officer and President

c/o DLC Realty Trust, Inc.

580 White Plains Road

Tarrytown, New York 10591

(914) 631-3131

(Name, Address, including Zip Code, and Telephone Number, including Area Code, of Agent for Service)

Copies to:

| Larry P. Medvinsky, Esq. | Ettore A. Santucci, Esq. | |

| Jason D. Myers, Esq. | Daniel P. Adams, Esq. | |

| Clifford Chance US LLP | Goodwin Procter LLP | |

| 31 West 52nd Street | Exchange Place, 53 State Street | |

| New York, New York 10019 | Boston, Massachusetts 02109 | |

| Tel: (212) 878-8000 | Tel: (617) 570-1000 | |

| Fax: (212) 878-8375 | Fax: (617) 523-1231 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If any of the Securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box: ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check One):

| Large accelerated filer ¨ | Accelerated filer ¨ | Non-accelerated filer x | Smaller Reporting Company ¨ | |||

| (Do not check if a smaller reporting company) |

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price(1) (2) | Amount of Registration Fee(1) | ||

Common Stock, par value $0.01 per share | $598,000,000 | $42,637.40(3) | ||

| (1) | Estimated solely for purposes of calculating the registration fee in accordance with Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | Includes the offering price of common stock that may be purchased by the underwriters upon the exercise of their option. |

| (3) | Includes $40,997.50 previously paid. |

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is declared effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion

Preliminary Prospectus, dated August 10, 2010

P R O S P E C T U S

40,000,000 Shares

DLC Realty Trust, Inc.

Common Stock

DLC Realty Trust, Inc. is a Maryland corporation organized to qualify as a real estate investment trust that acquires, manages, leases, repositions and redevelops grocery and value-retail anchored shopping centers primarily in the Southeast, Northeast, Midwest and Mid-Atlantic United States.

This is our initial public offering and no public market currently exists for our common stock. We are offering 40,000,000 shares of our common stock as described in this prospectus. All of the shares of common stock offered by this prospectus are being sold by us. We currently expect the initial public offering price to be between $12.00 and $13.00 per share. Our common stock has been approved for listing on the New York Stock Exchange under the symbol “DLC,” subject to official notice of issuance.

Shares of our common stock are subject to ownership limitations that are intended to assist us in qualifying and maintaining our qualification as a real estate investment trust. Our charter contains certain restrictions relating to the ownership and transfer of our common stock, including, subject to certain exceptions, a 9.0% ownership limit for all stockholders, generally, and a 13.8% ownership limit for Adam Ifshin, our chief executive officer and president, together with his family. See “Description of Securities—Restrictions on Ownership and Transfer” beginning on page 144 of this prospectus.

Investing in our common stock involves risks. See “Risk Factors” beginning on page 20 of this prospectus for a discussion of these risks.

| Per Share | Total | |||||

Public offering price | $ | $ | ||||

Underwriting discounts and commissions | $ | $ | ||||

Proceeds, before expenses, to us | $ | $ | ||||

We have granted the underwriters the option to purchase an additional 6,000,000 shares of our common stock on the same terms and conditions set forth above if the underwriters sell more than 40,000,000 shares of common stock in this offering.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed on the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The underwriters expect to deliver the shares of our common stock on or about , 2010.

Joint Book-Running Managers

| BofA Merrill Lynch | Barclays Capital |

Senior Co-Managers

| Deutsche Bank Securities | Raymond James | RBC Capital Markets |

Co-Managers

| Piper Jaffray | PNC Capital Markets LLC |

The date of this prospectus is , 2010.

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Page | ||

| 1 | ||

| 1 | ||

| 2 | ||

| 3 | ||

| 4 | ||

| 5 | ||

| 7 | ||

New Senior Secured Revolving Credit Facility and Debt Capitalization | 8 | |

| 8 | ||

Consequences of This Offering and the Formation Transactions | 10 | |

| 11 | ||

| 12 | ||

| 13 | ||

| 14 | ||

| 14 | ||

| 14 | ||

| 15 | ||

| 15 | ||

| 16 | ||

Summary Historical and Unaudited Pro Forma Financial and Operating Data | 17 | |

| 20 | ||

| 20 | ||

| 31 | ||

| 34 | ||

| 37 | ||

| 42 | ||

| 44 | ||

| 47 | ||

| 50 | ||

| 51 | ||

| 53 | ||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 56 | |

| 56 | ||

| 57 | ||

| 58 | ||

| 60 |

| Page | ||

| 63 | ||

| 64 | ||

| 65 | ||

| 69 | ||

| 71 | ||

Consolidated Indebtedness to be Outstanding After This Offering | 72 | |

| 74 | ||

| 75 | ||

| 75 | ||

| 75 | ||

| 76 | ||

| 78 | ||

| 78 | ||

| 79 | ||

| 79 | ||

| 80 | ||

| 80 | ||

| 80 | ||

| 82 | ||

| 82 | ||

| 83 | ||

| 83 | ||

| 84 | ||

| 86 | ||

| 89 | ||

| 94 | ||

| 94 | ||

| 95 | ||

| 96 | ||

| 96 | ||

| 97 | ||

| 97 | ||

| 98 | ||

| 99 | ||

| 99 | ||

| 101 | ||

| 101 | ||

| 101 | ||

| 102 |

i

Table of Contents

| Page | ||

| 102 | ||

| 103 | ||

| 103 | ||

| 103 | ||

| 104 | ||

| 104 | ||

| 105 | ||

| 105 | ||

| 109 | ||

| 110 | ||

| 110 | ||

| 110 | ||

| 112 | ||

| 112 | ||

| 112 | ||

| 114 | ||

| 119 | ||

| 120 | ||

| 120 | ||

| 121 | ||

| 122 | ||

| 122 | ||

| 122 | ||

| 123 | ||

| 124 | ||

| 124 | ||

| 125 | ||

| 125 | ||

| 125 | ||

| 125 | ||

| 127 | ||

| 127 | ||

| 127 | ||

Consequences of This Offering and the Formation Transactions | 130 | |

| 131 | ||

Benefits of This Offering and the Formation Transactions to Certain Parties | 132 | |

| 133 | ||

| 134 | ||

| 134 |

| Page | ||

| 135 | ||

| 135 | ||

| 136 | ||

| 137 | ||

| 137 | ||

DESCRIPTION OF THE PARTNERSHIP AGREEMENT OF DLC REALTY, L.P. | 138 | |

| 138 | ||

| 138 | ||

| 138 | ||

| 139 | ||

| 139 | ||

| 139 | ||

| 140 | ||

Transferability of Operating Partnership Units; Extraordinary Transactions | 140 | |

| 141 | ||

| 141 | ||

| 141 | ||

| 142 | ||

| 143 | ||

| 143 | ||

| 143 | ||

| 144 | ||

| 144 | ||

| 144 | ||

| 148 | ||

CERTAIN PROVISIONS OF THE MARYLAND GENERAL CORPORATION LAW AND OUR CHARTER AND BYLAWS | 149 | |

| 149 | ||

| 149 | ||

| 149 | ||

| 150 | ||

| 151 | ||

| 151 | ||

| 151 | ||

| 152 |

ii

Table of Contents

| Page | ||

| 152 | ||

Anti-Takeover Effect of Certain Provisions of Maryland Law and of Our Charter and Bylaws | 152 | |

| 153 | ||

Indemnification and Limitation of Directors’ and Officers’ Liability | 153 | |

| 154 | ||

| 155 | ||

| 155 | ||

| 155 | ||

| 156 | ||

| 156 | ||

| 156 | ||

Lock-up Agreements and Other Contractual Restrictions on Resale | 156 | |

| 158 | ||

| 159 | ||

| 162 | ||

| 171 | ||

| 173 |

| Page | ||

| 173 | ||

| 179 | ||

| 180 | ||

| 181 | ||

| 181 | ||

| 182 | ||

| 182 | ||

| 182 | ||

| 182 | ||

| 183 | ||

| 184 | ||

| 184 | ||

| 184 | ||

| 185 | ||

Notice to Prospective Investors in the Dubai International Financial Centre | 186 | |

| 187 | ||

| 187 | ||

| 187 | ||

| F-1 |

You should rely only on the information contained in this prospectus or in any free writing prospectus prepared by us or information to which we have referred you. We have not, and the underwriters have not, authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume that the information appearing in this prospectus and any free writing prospectus prepared by us is accurate only as of their respective dates or on the date or dates which are specified in these documents. Our business, financial condition, liquidity, results of operations and prospects may have changed since those dates.

We use market data throughout this prospectus. We have obtained certain market data from publicly available information and industry publications. These sources generally state that the information they provide has been obtained from sources believed to be reliable. Forecasts are based on industry surveys and the preparer’s expertise in the industry and there is no assurance that any of the projected amounts will be achieved. We believe this data others have compiled are reliable, but we have not independently verified this information.

iii

Table of Contents

The term “our predecessor” means (i) DLC Management Corporation, which we refer to as “our management company,” (ii) Delphi Commercial Properties, Inc., a full service commercial real estate brokerage, which we refer to as “Delphi,” and (iii) the limited liability companies or partnerships that currently own, directly or indirectly and either through a fee interest or a ground lease interest, the 86 grocery and value-retail anchored shopping centers that we will own after the formation transactions described in this prospectus, which we refer to as the “existing entities.” Interests in our operating partnership are denominated in units of limited partnership, which we call operating partnership units. LTIP units are a special class of operating partnership units that may be awarded under our equity incentive plan. Operating partnership units are redeemable for cash, or at our election, shares of our common stock on a one-for-one basis. LTIP units will be similarly redeemable upon the satisfaction of certain conditions. As used herein, when we refer to our ownership interest in our operating partnership, we mean the percentage of all operating partnership units, including LTIP units, that are expected to be held by us. The term “fully diluted basis” means all outstanding shares of our common stock at such time plus all outstanding shares of restricted stock and shares of common stock issuable upon the exchange of operating partnership units and LTIP units for shares of our common stock on a one-for-one basis, which is not the same as the meaning of “fully diluted” under generally accepted accounting principles in the United States of America, or GAAP. The term “vertically integrated” means that we are able to provide a full spectrum of real estate services, including asset and property management, leasing, construction and financing, to support our existing portfolio. The term “grocery and value-retail anchored shopping centers” means shopping centers whose largest tenants, which drive customer traffic, are grocery stores and value-oriented retailers whose products are generally necessity-based items. The term “percentage rent” means the specified percentage of a tenant’s sales made at the rented premises that the tenant is obligated to pay its landlord, in addition to any fixed rental payments.

iv

Table of Contents

You should read the following summary together with the more detailed information regarding our company, including under the caption “Risk Factors,” as well as the historical and unaudited pro forma financial statements, including the related notes, appearing elsewhere in this prospectus. Unless the context otherwise requires or indicates, references in this prospectus to “we,” “our,” “us” and “our company” refer to (i) DLC Realty Trust, Inc., a Maryland corporation, together with its consolidated subsidiaries, including DLC Realty, L.P., a Delaware limited partnership, which we refer to in this prospectus as “our operating partnership,” after giving effect to the formation transactions described in this prospectus and (ii) our predecessor before giving effect to the formation transactions described in this prospectus. Unless the context otherwise requires or indicates, the information contained in this prospectus assumes (i) the formation transactions, as described under the caption “Structure and Formation of Our Company” beginning on page 127, have been completed, (ii) the 40,000,000 shares of common stock to be sold in this offering are sold at $12.50 per share, which is the mid-point of the range of prices set forth on the front cover of this prospectus, (iii) no exercise by the underwriters of their option to purchase up to an additional 6,000,000 shares of our common stock solely to cover over-allotments, (iv) the operating partnership units to be issued in the formation transactions are valued at $12.50 per unit and (v) all property information is as of March 31, 2010.

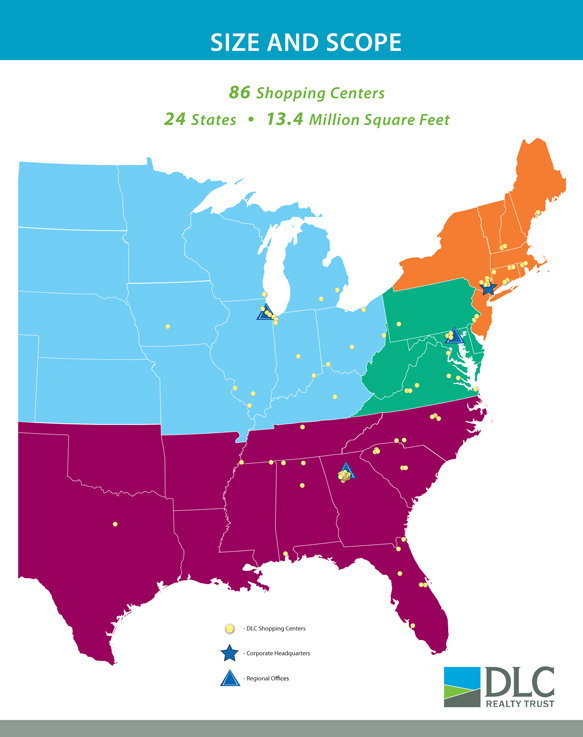

We are a vertically integrated, self-administered and self-managed real estate investment trust, or REIT, that acquires, manages, leases, repositions and redevelops grocery and value-retail anchored shopping centers primarily in the Southeast, Northeast, Midwest and Mid-Atlantic United States. As of March 31, 2010, our portfolio consisted of 86 shopping centers totaling approximately 13.4 million square feet of gross leasable area, or GLA, located in 24 states. The shopping centers in our portfolio typically are tenanted by retailers that focus on value and necessity items and services, with approximately 66% of our annualized base rent derived from grocery-anchored shopping centers. We believe such retail shopping centers generate reliable customer traffic, which will provide us with more consistent property cash flows to support our ability to sustain our distributions through all economic cycles.

Since the founding of our predecessor entity in 1991, we have acquired over 100 retail shopping centers representing an aggregate transaction value of approximately $1.5 billion in 60 transactions totaling more than 16.8 million square feet in GLA, creating the 13th largest private owner of shopping centers in the United States as of December 2009, according to Retail Traffic magazine. We are vertically integrated across all critical real estate operations and have more than 90 professionals who pro-actively and entrepreneurially manage our shopping centers with a long-term, hands-on approach that emphasizes the aggressive leasing of vacant spaces, attentive asset management and rigorous expense control.

Our primary business objectives are to increase cash flow from operations, achieve sustainable long-term growth and maximize stockholder value through stable dividends and stock appreciation. We seek to accomplish these objectives by improving the overall performance and positioning of our assets by utilizing our strong tenant relationships and leasing expertise to increase occupancy and rental rates and our hands-on asset and property management experience to reduce property operating expenses. We target acquisitions that offer what we believe to be returns that will increase our funds from operations, or FFO, per share and operating partnership unit, or accretive returns, and significant upside through one or more of the following: vacant space for immediate lease-up, below-market rents in the existing tenancy, expansion opportunities, reducible cost structures, economies of scale and/or repositioning or redevelopment opportunities. We believe our focus differentiates us from many of our competitors, who frequently target core, stabilized properties. We also seek to acquire assets in opportunistic off-market transactions through our extensive relationships across the real estate and retail industries and through opportunities arising from our third-party asset management business. We do not intend to engage in any ground-up development activity.

1

Table of Contents

Our portfolio was approximately 88.3% leased as of March 31, 2010, with approximately 1.6 million square feet of GLA available for leasing. The occupancy of our portfolio reflects our strategic focus on acquiring properties that have relatively lower occupancy and rental rates, where we believe we can significantly improve operations and cash flow. During the three months ended March 31, 2010 and the year ended December 31, 2009, despite a very difficult economic environment for retail tenants, we leased approximately 432,916 square feet and 1.3 million square feet of GLA, respectively, including new leases totaling approximately 177,609 square feet and 360,000 square feet and renewals totaling approximately 255,307 square feet and 935,721 square feet. In addition, we executed new leases and lease renewals in the three months ended June 30, 2010 and the period from July 1, 2010 through July 23, 2010 and accepted non-binding letters of intent for new leases and lease renewals that remained outstanding as of July 23, 2010 as follows:

| April 1 – June 30, 2010 | July 1 – July 23, 2010 | |||||||||||||

| No. of Leases | Total GLA | Average Base Rent per Square Foot(1) | No. of Leases | Total GLA | Average Base Rent per Square Foot(1)(2) | |||||||||

New leases signed | 33 | 169,600 | $ | 12.94 | 2 | 6,058 | $ | 12.49 | ||||||

Renewal leases signed | 49 | 293,289 | 9.55 | 14 | 131,025 | 8.36 | ||||||||

New lease LOIs(2) | — | — | — | 10 | 49,647 | 12.44 | ||||||||

Renewal lease LOIs(2) | — | — | — | 9 | 41,663 | 13.34 | ||||||||

| (1) | Based upon GLA of signed leases for the period presented. |

| (2) | LOIs represent accepted non-binding letters of intent with prospective tenants with which we have entered into lease negotiations. All letters of intent outstanding as of July 23, 2010 are presented in the period from July 1, 2010 through July 23, 2010 regardless of when they were accepted. |

We are a Maryland corporation that was formed on March 8, 2010. We conduct all of our business activities through our operating partnership, of which we are the sole general partner and expect to hold a 68.6% ownership interest upon completion of this offering. Our principal executive offices are located at 580 White Plains Road, Tarrytown, New York 10591. In addition, we have regional leasing and property management offices in Atlanta, Georgia; Chicago, Illinois; and Towson, Maryland. Our telephone number is (914) 631-3131. Our website address is www.dlcreit.com. The information on, or otherwise accessible through, our website does not constitute a part of this prospectus. We intend to qualify as a REIT for U.S. federal income tax purposes commencing with our taxable year ending December 31, 2010.

The following business strengths serve as the foundation of our business:

| • | Established, Diversified Portfolio of Grocery and Value-Retail Anchored Shopping Centers. As of March 31, 2010, our portfolio consisted of 86 shopping centers totaling approximately 13.4 million square feet of GLA located in 24 states. Approximately 66% of our annualized base rent is generated from grocery-anchored shopping centers, and our portfolio is comprised predominantly of shopping centers with value-focused tenants that provide necessity items and services, which we believe to be advantageous throughout all economic cycles. Our four largest tenants represent four of the five largest grocery store chains in the United States as of March 31, 2010. No single tenant represents more than 5.0% of our annualized base rent in aggregate and our top ten tenants represent less than 30% of our annualized base rent in aggregate. |

| • | Significant Internal Growth Potential. As of March 31, 2010, our portfolio was 88.3% leased. The occupancy of our portfolio reflects our strategic focus on acquiring properties with relatively lower occupancy and rental rates, where we believe we can significantly improve operations and cash flow. Our approximately 1.6 million square feet of GLA available for leasing as of March 31, 2010 offers |

2

Table of Contents

immediate opportunity for incremental cash flow generation with what we believe to be modest lease-up investments. |

| • | Significant External Growth Potential. We believe that, as a result of the continued disruption in the real estate market, there will be opportunities over the next several years to acquire assets that are under-leased or have below-market rents, and to acquire over-leveraged and under-capitalized shopping centers for redevelopment and repositioning. We believe we have established an extensive network of relationships that will enable us to continue to source new acquisition and redevelopment opportunities. |

| • | Entrepreneurial Investment Focus. We believe we have an entrepreneurial corporate culture, and approach the retail real estate business with a different perspective than many of our peers. We seek to acquire assets where we believe we can generate accretive returns by employing our human capital and expertise, rather than focusing on the acquisition of low vacancy, stabilized assets where we see limited upside. |

| • | Experienced and Committed Management Team. Our senior management team, which is led by Adam Ifshin, has been in place since 2005 and has an average of more than 20 years of real estate industry experience through several real estate, credit and retail cycles. In addition, upon consummation of this offering and the formation transactions, our senior management team will collectively own approximately 11.7% of our outstanding common stock on a fully diluted basis. As a result of their significant ownership interest, our senior management team’s interests are aligned with those of our stockholders and they are highly incentivized to maximize returns for our stockholders. |

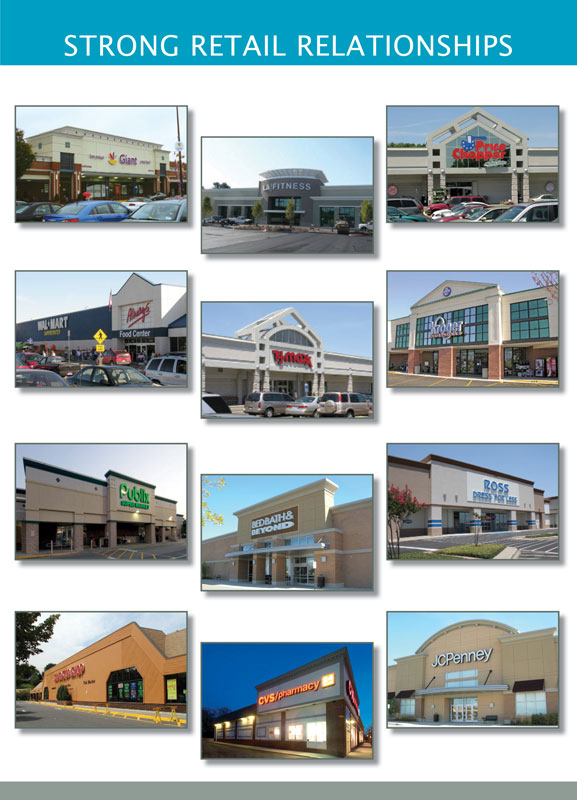

| • | Strong Relationships with a Diverse Group of Nationally Recognized Retailers. We have strong relationships and completed multiple transactions with many leading retailers including Ahold USA Inc. (the parent company of the Stop & Shop Supermarket Company and Giant Food Stores, LLC), CVS Caremark Corp., Dollar Tree, Inc., Family Dollar Stores, Inc., The Kroger Co., LA Fitness International, LLC, Publix Super Markets, Inc., Ross Stores, Inc., Sears Holdings Corporation, Supervalu Inc., The TJX Companies, Inc., Walgreen Co. and Wal-Mart Stores, Inc. We believe our strong retailer relationships create new leasing opportunities as these retailers expand while also supporting our tenant retention rate and reducing our marketing, leasing and tenant improvement costs that would otherwise result from having to re-lease space. |

| • | Flexible Capital Structure Enables Us to Take Advantage of Acquisition Opportunities. Upon consummation of this offering and the formation transactions, our aggregate indebtedness (other than under our senior secured revolving credit facility) will consist almost entirely of fixed rate debt, which will have staggered maturities with a weighted average maturity of approximately 5.4 years and a weighted average interest rate of 5.7% per annum. None of our indebtedness will mature until 2012 and approximately $62.3 million (or approximately 9.2% of our total indebtedness upon completion of this offering and the formation transactions) will mature prior to 2014. We have entered into an agreement with affiliates of certain of the underwriters of this offering to provide us with a three-year, $200.0 million senior secured revolving credit facility to fund acquisitions, redevelopment activities, tenant improvements, general corporate matters and working capital. The agreement will become effective upon the pricing of this offering and we intend to close the facility concurrently with the closing of this offering. The closing of the facility is contingent on the satisfaction of customary conditions. |

Business and Growth Strategies

Our primary business objectives are to increase cash flow from operations, achieve sustainable long-term growth and maximize stockholder value through stable dividends and stock appreciation. The strategies we intend to execute to achieve these goals include:

| • | Focus on Grocery and Value-Retail Anchored Shopping Center Ownership, Acquisition and Repositioning in Our Primary Markets. We intend to continue to pursue a broad mix of national, |

3

Table of Contents

regional and local value-focused tenants, such as grocery stores, drugstores and discounters, as we believe these retailers are less reliant on sales of discretionary goods. We believe these retailers generate more consistent customer traffic and sales over time than retailers that rely on higher-end consumers and high levels of disposable income. Our acquisition strategy will focus primarily on shopping centers with what we believe to be longer-term growth potential as opposed to fully stabilized assets that provide more limited opportunities to grow cash flow. |

| • | Maximize Cash Flow from Existing Properties. We aggressively seek to lease vacant space through our national retailer relationships and local, on-the-ground canvassing, while providing for an appropriate tenant mix for the local market. We believe our continued focus on reducing operating expenses enables us to generate additional cash flow and makes our properties more competitive by reducing our tenants’ total cost of occupancy. Further, we expect to take advantage of what we believe will be a period of increasing retail demand combined with limited new supply of shopping centers to lease the approximately 1.6 million square feet of GLA available for leasing in our portfolio, as of March 31, 2010. |

| • | Exploit Existing Internal Growth Opportunities. We have historically pursued an investment strategy focused on acquiring properties that have relatively lower occupancy and rental rates where we believe we can improve the performance of these properties. We have significant real estate management, leasing, property management, and construction and redevelopment management expertise that we employ to improve operations and increase cash flows at these properties. As a result of these embedded internal growth opportunities, we believe we are not dependent solely upon new acquisitions to grow our business. |

| • | Achieve External Growth Through Disciplined Acquisition Strategy. We target grocery and value-retail anchored shopping centers that offer what we believe to be significant upside through one or more of the following: vacant space for immediate lease-up, below-market rents in the existing tenancy, expansion opportunities, reducible cost structures, economies of scale and/or repositioning or redevelopment opportunities. We underwrite each acquisition to generate accretive returns and then seek to increase these returns over time by improving occupancy and cash flow at our properties. We believe our unique strategy of acquiring non-core, unstabilized or distressed properties offers greater growth opportunities than acquiring stabilized properties. |

| • | Leverage Our Vertically Integrated Infrastructure. We are vertically integrated across all critical real estate operations, with more than 90 professionals who have significant expertise in real estate asset management, leasing, property management, acquisitions, dispositions, financial structuring, construction and redevelopment management and related legal and environmental matters. We have built an extensive infrastructure of personnel, policies and procedures that we believe enables us to manage and lease a large property portfolio with a diverse group of retail tenants. |

We have obtained certain market data included herein from publicly available information and other industry sources. These sources generally state that the information they provide has been obtained from sources believed to be reliable. Forecasts are based on data (including third-party data), models and experience of these sources, and are based on various assumptions, all of which are subject to change without notice. There is no assurance any of the projected amounts will be achieved. We believe the data others have compiled are reliable, but we have not independently verified this information.

Our business focuses primarily on neighborhood shopping centers (30,000 – 150,000 square feet in size) and community shopping centers (100,000 – 350,000 square feet in size) that provide consumers with convenience and necessity goods such as food, drugs and services. We believe over the next several years the performance of

4

Table of Contents

neighborhood and community shopping centers will benefit from the limited completion and delivery of new developments, improving macroeconomic conditions and a renewed focus on non-discretionary goods and services by retailers and consumers alike.

Retail sales of goods typically sold at shopping centers totaled $2.22 trillion in 2009 and have grown at an annual compounded rate of 4.1% per year since 1992. We expect the current economic environment will lead to increased customer traffic at shopping centers like ours with value-driven and discount retailers as consumers redirect their purchases away from higher-cost and discretionary retailers.

We believe grocery- and drug-store anchored neighborhood and community shopping centers generally are more resilient during economic downturns relative to retail centers that are more dependent upon discretionary spending. According to figures published by the U.S. Census Bureau in the Monthly Retail Trade Report, total grocery store sales were in excess of $526 billion in 2009 and have grown at an average rate of 3.5% per year for each of the last five years. According to the International Council of Shopping Centers, or the ICSC, supermarkets draw local customers an average of two-and-a-half times a week, generating reliable and repeat customer traffic.

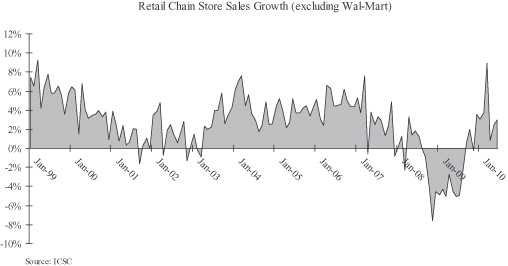

After an extended period of positive growth, retail chain store sales growth, as measured by the ICSC, fell off sharply beginning in September 2008. However, in September 2009, retail chain store sales growth once again turned positive. Our belief that macroeconomic fundamentals are now recovering is further evidenced by labor market improvements and a return to positive growth in Gross Domestic Product, or GDP. According to figures published by the Bureau of Labor Statistics, following a period of sustained job loss throughout 2008 and 2009, the U.S. economy experienced five consecutive months of positive job growth from January through May 2010. Additionally, GDP has also resumed a positive growth trend with the Department of Commerce registering increases of 2.2%, 5.6% and 2.7% in the third and fourth quarters of 2009 and first quarter of 2010, respectively.

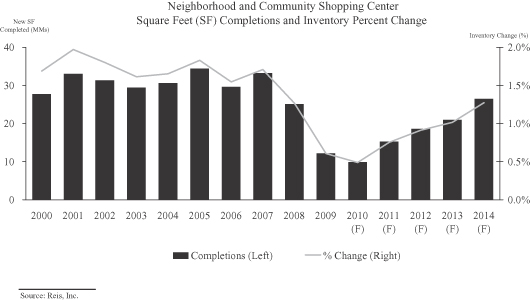

According to data published by Reis, Inc., an independent industry research provider, the total new supply of neighborhood and community shopping center space entering the market in 2009 was the lowest on record since the company began tracking the metric more than a decade ago. Additionally, forecasts of new community and neighborhood center space to be completed over the next five years are well below historical levels and should serve to benefit existing property owners through decreased competition for tenants.

Investing in our common stock involves a high degree of risk. You should carefully consider the following risk factors, together with all the other information contained in this prospectus, before making an investment decision to purchase our common stock. The occurrence of any of the following risks could materially and adversely affect our business, prospects, financial condition, results of operations and our ability to make cash distributions to our stockholders, which could cause you to lose all or a significant part of your investment in our common stock.

| • | We have not obtained as part of the formation transactions recent appraisals of the properties we will own upon completion of this offering and the formation transactions and the value of these properties was not negotiated at arm’s length and the consideration given by us in exchange for them may exceed their fair market value. |

| • | Our performance and value are subject to risks associated with real estate assets and with the real estate industry. |

| • | Our dependence on rental income may adversely affect our profitability, our ability to meet our debt obligations and our ability to make distributions to our stockholders; failure by any major tenant with leases in multiple locations to make rental payments to us could seriously harm our performance. |

5

Table of Contents

| • | Our outstanding indebtedness upon completion of this offering reduces cash available for distribution and may expose us to the risk of default under our debt obligations. |

| • | Our results of operations will be significantly influenced by the economies of the markets in which we operate, and the market for retail space generally. |

| • | Our growth depends on external sources of capital that are outside of our control, which may affect our ability to seize strategic opportunities, satisfy debt obligations and make distributions to our stockholders. |

| • | We may be unable to renew leases, lease vacant space or re-lease space as leases expire, which could adversely affect our financial condition, results of operations, cash flow and trading price of our common stock. |

| • | We may assume unknown liabilities in connection with the formation transactions, which, if significant, could adversely affect our business. |

| • | We have no experience operating as a REIT or as a public company, which may affect our ability to successfully operate our business or generate sufficient cash flows to make or sustain distributions to our stockholders. |

| • | Our success depends on key personnel whose continued service is not guaranteed. |

| • | Certain members of our senior management team have outside business interests that could take their time and attention away from us. |

| • | Certain provisions of our charter and Maryland law could inhibit changes in control of us, which could lower the value of our shares. |

| • | There has been no public market for our common stock prior to this offering and an active trading market may not develop or be sustained following this offering. |

| • | Our ability to pay our estimated initial annual distribution, which represents approximately 107.5% of our estimated cash available for distribution for the twelve months ending March 31, 2011, depends on our actual operating results, and we may be required to borrow funds to pay this distribution, which could slow our growth. |

| • | Differences between the book value of the assets we will own following the formation transactions and the price paid for our common stock will result in an immediate and material dilution of the book value of our common stock that investors will own upon completion of this offering and the formation transactions. |

| • | Our predecessor has experienced historical losses and accumulated deficits and we may experience future losses. |

| • | Our failure to qualify or remain qualified as a REIT would subject us to U.S. federal income tax and applicable state and local taxes, which would reduce the amount of cash available for distribution to our stockholders. |

| • | REIT distribution requirements could require us to borrow funds during unfavorable market conditions or subject us to tax which would reduce the cash available for distribution to our stockholders. |

6

Table of Contents

As of March 31, 2010, our portfolio consisted of 86 shopping centers totaling approximately 13.4 million square feet of GLA and was approximately 88.3% leased. The occupancy of our portfolio reflects our strategic focus on acquiring properties that have relatively lower occupancy and rental rates, where we believe we can significantly improve operations and cash flow. The table below presents an overview of our portfolio as of March 31, 2010:

Region / State | Number of Properties | Total GLA(1) | Leased GLA(1) | Percent of Total GLA | Percent Leased(2) | Annualized Base Rent(2)(3) | Percent of Annualized Base Rent | Annualized Base Rent Per Leased Square Foot(4) | |||||||||||||

| (in thousands) | |||||||||||||||||||||

Southeast | |||||||||||||||||||||

Georgia | 14 | 1,550,828 | 1,362,442 | 11.5 | % | 87.9 | % | $ | 13,861 | 11.2 | % | $ | 10.15 | ||||||||

Florida | 6 | 774,234 | 709,883 | 5.8 | % | 91.7 | % | 7,742 | 6.3 | % | 10.12 | ||||||||||

North Carolina | 5 | 602,364 | 538,466 | 4.5 | % | 89.4 | % | 4,898 | 4.0 | % | 8.88 | ||||||||||

Alabama | 4 | 548,059 | 399,304 | 4.1 | % | 72.9 | % | 3,396 | 2.8 | % | 8.50 | ||||||||||

Tennessee | 2 | 537,918 | 451,826 | 4.0 | % | 84.0 | % | 3,150 | 2.6 | % | 6.97 | ||||||||||

South Carolina | 5 | 317,181 | 301,204 | 2.4 | % | 95.0 | % | 2,962 | 2.4 | % | 9.56 | ||||||||||

Texas | 1 | 173,376 | 127,518 | 1.3 | % | 73.5 | % | 1,128 | 0.9 | % | 8.48 | ||||||||||

Mississippi | 1 | 179,905 | 171,985 | 1.3 | % | 95.6 | % | 956 | 0.8 | % | 5.56 | ||||||||||

Subtotal: Southeast | 38 | 4,683,865 | 4,062,628 | 34.9 | % | 86.7 | % | $ | 38,093 | 30.9 | % | $ | 9.17 | ||||||||

Northeast | |||||||||||||||||||||

New York | 6 | 1,002,749 | 918,163 | 7.5 | % | 91.6 | % | $ | 13,600 | 11.0 | % | $ | 14.64 | ||||||||

Connecticut | 5 | 968,789 | 930,467 | 7.2 | % | 96.0 | % | 11,952 | 9.7 | % | 12.77 | ||||||||||

New Hampshire | 2 | 301,570 | 289,632 | 2.2 | % | 96.0 | % | 2,754 | 2.2 | % | 9.51 | ||||||||||

Maine | 1 | 101,124 | 89,249 | 0.8 | % | 88.3 | % | 1,593 | 1.3 | % | 17.85 | ||||||||||

Rhode Island | 1 | 121,660 | 97,497 | 0.9 | % | 80.1 | % | 1,432 | 1.2 | % | 14.69 | ||||||||||

Massachusetts | 1 | 101,782 | 82,788 | 0.8 | % | 81.3 | % | 750 | 0.6 | % | 9.06 | ||||||||||

Subtotal: Northeast | 16 | 2,597,674 | 2,407,796 | 19.3 | % | 92.7 | % | $ | 32,081 | 26.0 | % | $ | 13.23 | ||||||||

Midwest | |||||||||||||||||||||

Ohio | 4 | 1,450,520 | 1,241,493 | 10.8 | % | 85.6 | % | $ | 10,894 | 8.8 | % | $ | 8.68 | ||||||||

Illinois | 6 | 989,836 | 836,079 | 7.4 | % | 84.5 | % | 8,346 | 6.8 | % | 9.68 | ||||||||||

Indiana | 4 | 692,865 | 620,362 | 5.2 | % | 89.5 | % | 5,316 | 4.3 | % | 8.37 | ||||||||||

Michigan | 2 | 401,403 | 386,726 | 3.0 | % | 96.3 | % | 2,546 | 2.1 | % | 6.58 | ||||||||||

Kentucky | 1 | 104,892 | 104,892 | 0.8 | % | 100.0 | % | 1,671 | 1.4 | % | 12.93 | ||||||||||

Wisconsin | 1 | 260,664 | 231,339 | 1.9 | % | 88.7 | % | 1,539 | 1.2 | % | 6.65 | ||||||||||

Iowa | 1 | 109,434 | 91,762 | 0.8 | % | 83.9 | % | 1,177 | 1.0 | % | 12.82 | ||||||||||

Subtotal: Midwest | 19 | 4,009,614 | 3,512,653 | 29.8 | % | 87.6 | % | $ | 31,489 | 25.5 | % | $ | 8.74 | ||||||||

Mid-Atlantic | |||||||||||||||||||||

Maryland | 4 | 788,843 | 699,636 | 5.9 | % | 88.7 | % | $ | 9,497 | 7.7 | % | $ | 13.37 | ||||||||

Pennsylvania | 3 | 653,112 | 602,935 | 4.9 | % | 92.3 | % | 6,597 | 5.3 | % | 10.94 | ||||||||||

Virginia | 6 | 705,043 | 579,043 | 5.2 | % | 82.1 | % | 5,554 | 4.5 | % | 9.55 | ||||||||||

Subtotal: Mid-Atlantic | 13 | 2,146,998 | 1,881,614 | 16.0 | % | 87.6 | % | $ | 21,648 | 17.6 | % | $ | 11.42 | ||||||||

Total / Average | 86 | 13,438,151 | 11,864,691 | 100.0 | % | 88.3 | % | $ | 123,311 | 100.0 | % | $ | 10.22 | ||||||||

| (1) | GLA represents all square footage owned. |

| (2) | Includes leases signed but not commenced as of March 31, 2010 representing 327,216 square feet of GLA and $3.7 million of Annualized Base Rent. |

| (3) | Annualized Base Rent represents annualized monthly base rent under leases signed as of March 31, 2010 excluding tenant reimbursements and including Annualized Base Rent attributable to ground leases of approximately $2.0 million. Our leases generally do not provide for abatements or free rent discounts. Annualized base rent data for our shopping centers is as of March 31, 2010 and does not reflect scheduled lease expirations for the 12 months ending March 31, 2011. Calculating total annualized base rent to reflect the impact of scheduled lease expirations for the 12 months ending March 31, 2011 (by including in annualized base rent, for leases with a term of less than one year, only amounts through the expiration of the lease) would reduce total annualized base rent by approximately $7.1 million to approximately $116.2 million. For lease expiration data, see “Business and Properties—Lease Expirations.” |

| (4) | Annualized Base Rent Per Leased Square Foot equals Annualized Base Rent less Annualized Base Rent attributable to ground leases (approximately $2.0 million) divided by Leased GLA. |

7

Table of Contents

New Senior Secured Revolving Credit Facility and Debt Capitalization

We have entered into an agreement with affiliates of certain of the underwriters of this offering to provide us with a three-year, $200.0 million senior secured revolving credit facility. The agreement will become effective upon the pricing of this offering and we intend to close the facility concurrently with the closing of this offering. The closing of the facility is contingent on the satisfaction of customary conditions. We intend to use this facility to, among other things, fund acquisitions, general corporate matters and working capital. We expect to have approximately $685.1 million of total consolidated indebtedness outstanding upon consummation of this offering and the formation transactions (based on March 31, 2010 pro forma outstanding balances). Our overall leverage will depend on our mix of investments and the cost of leverage. Our charter does not restrict the amount of leverage that we may use. For more information see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Consolidated Indebtedness to be Outstanding After This Offering.”

Structure and Formation of Our Company

| • | We currently operate our business through our predecessor. Prior to or concurrently with the completion of this offering, we will engage in a series of mergers and other transactions, which we refer to as the formation transactions, that are designed to: |

| • | consolidate the ownership of our portfolio of shopping centers and the management company into our operating partnership; |

| • | facilitate this offering; |

| • | enable us to raise the necessary capital to repay existing indebtedness related to certain properties in our portfolio and other obligations; |

| • | enable us to qualify as a REIT for federal income tax purposes commencing with the taxable year ending December 31, 2010; |

| • | defer the recognition of taxable gain by certain continuing investors (as defined below); and |

| • | enable continuing investors to obtain liquidity (after the expiration of applicable lock-ups) for their investments. |

| • | Pursuant to the formation transactions, the following have occurred or will occur prior to or concurrently with the completion of this offering (all amounts are based on the mid-point of the range of prices set forth on the front cover of this prospectus): |

| • | We were formed as a Maryland corporation on March 8, 2010. |

| • | Our operating partnership was formed as a Delaware limited partnership on March 9, 2010. We are the sole general partner of our operating partnership. |

| • | Part of the formation transactions includes a consolidation transaction, pursuant to which, prior to or concurrently with the completion of this offering, certain holders of interests in our predecessor will exchange, through a series of mergers and other transactions, their equity interests in our predecessor for operating partnership units and/or shares of our common stock. We refer to holders of interests in our predecessor that will own operating partnership units and/or shares of our common stock following consummation of the formation transactions as continuing investors. Certain other holders of interests in the existing entities that are non-accredited investors (none of which consist of members of our senior management team or directors) will exchange their equity interests in the existing entities for cash. The agreements relating to the consolidation transaction are subject to customary closing conditions, including the closing of this offering. As part of the formation transactions, our predecessor will declare final distributions to the continuing investors, |

8

Table of Contents

including certain members of our senior management team and certain of our directors, in the amount of approximately $19.0 million in the aggregate, which will be paid shortly following consummation of this offering. |

| • | As part of the consolidation transaction, our operating partnership will enter into agreements with Messrs. Adam Ifshin and Stephen Ifshin (with respect to clause (i) below) and certain of the continuing investors, including Adam Ifshin and Stephen Ifshin (with respect to clause (ii) below), pursuant to which the operating partnership will indemnify these continuing investors against certain tax liabilities intended to be deferred in the consolidation transaction (i) if those tax liabilities result from the operating partnership’s sale, transfer, conveyance or other disposition of 25 specified properties acquired by the operating partnership in the consolidation transaction representing approximately 41.1% of our annualized base rent as of March 31, 2010, or (ii) if the operating partnership fails to offer these continuing investors the opportunity to guarantee, or otherwise bear the risk of loss of, $75.0 million of indebtedness in the aggregate for U.S. federal income tax purposes. |

| • | While the relative valuation of our predecessor was fixed prior to the initial filing of the registration statement of which this prospectus is a part, the final valuation will be determined based on the actual public offering price of shares of our common stock in this offering. In consideration for the acquisition of our predecessor, we expect to issue an aggregate of 18,713,015 operating partnership units and 2,375,000 shares of our common stock, which include an aggregate of 4,122,729 operating partnership units and 2,375,000 shares of our common stock to members of our senior management team, and pay approximately $196,690 in cash from the net proceeds of this offering. Based on the mid-point of the range of prices set forth on the front cover of this prospectus, the aggregate value of the consideration to be issued and paid by us in the consolidation transaction will be approximately $263.8 million, including approximately $81.2 million to members of our senior management team. An increase in the actual public offering price will result in an increase in the value of the consideration paid to continuing investors, including members of our senior management team. Likewise, a decrease in the actual public offering price will result in a decrease in the value of the consideration paid to continuing investors, including members of our senior management team. |

| • | In connection with the formation transactions, we will assume approximately $680.1 million of total debt (based on March 31, 2010 outstanding balances), excluding amounts outstanding under our senior secured revolving credit facility. |

| • | We will sell 40,000,000 shares of our common stock in this offering and an additional 6,000,000 shares if the underwriters exercise their option to purchase additional shares in full solely to cover over-allotments. We will contribute the net proceeds from this offering to our operating partnership in exchange for 40,000,000 operating partnership units (or 46,000,000 operating partnership units if the underwriters exercise their option to purchase up to an additional 6,000,000 shares in full solely to cover over-allotments). |

| • | We expect to use a portion of the net proceeds from this offering to repay approximately $441.0 million of our outstanding indebtedness (based on March 31, 2010 outstanding balances) and to pay approximately $8.0 million in prepayment penalties, exit fees, swap breakage costs and defeasance costs related to such indebtedness. |

| • | We have entered into an agreement with affiliates of certain of the underwriters of this offering to provide us with a three-year, $200.0 million senior secured revolving credit facility. The agreement will become effective upon the pricing of this offering and we intend to close the facility concurrently with the closing of this offering. The closing of the facility is contingent on the satisfaction of customary conditions. |

9

Table of Contents

| • | Effective upon completion of this offering, we will grant to our executive officers a total of 732,269 long-term incentive units in our operating partnership, or LTIP units, and grant 26,000 restricted shares of our common stock to our independent directors, that are subject to certain vesting requirements. |

| • | We will enter into management agreements with the entities that own the excluded properties, or the excluded entities, on what we believe to be market terms. See “Certain Relationships and Related Transactions—Excluded Properties and Businesses.” |

| • | We expect to enter into management agreements with subsidiaries of Infill Development, LLC, pursuant to which, we expect to be designated as the exclusive property manager for all properties owned by Infill Development, LLC and will provide construction management and leasing services to Infill Development, LLC on what we believe to be market terms. |

Consequences of This Offering and the Formation Transactions

Upon completion of this offering and the formation transactions (all amounts are based on the mid-point of the range of prices set forth on the front cover of this prospectus):

| • | Our operating partnership will directly or indirectly own the assets of our management company and the fee simple or other interests in all of our properties that were previously owned by the existing entities. |

| • | Purchasers of shares of our common stock in this offering are expected to own 94.3% of our outstanding common stock, or 64.7% on a fully diluted basis. If the underwriters exercise their option to purchase an additional 6,000,000 shares in full solely to cover over-allotments, purchasers of shares of our common stock in this offering are expected to own 95.0% of our outstanding common stock, or 67.8% on a fully diluted basis. |

| • | We are the sole general partner of our operating partnership. We are expected to own 68.6% of the operating partnership units and the continuing investors, including certain members of our senior management team, will own 31.4%. If the underwriters exercise their option to purchase an additional 6,000,000 shares in full solely to cover over-allotments, we are expected to own 71.3% of the operating partnership units and the continuing investors, including certain members of our senior management team, are expected to own 28.7%. |

| • | Substantially all of the current employees of our management company will become our employees. |

| • | We expect to have total consolidated indebtedness of approximately $685.1 million (based on March 31, 2010 pro forma outstanding balances). |

10

Table of Contents

The following diagram depicts our ownership structure upon completion of this offering and the formation transactions, based on the mid-point of the range of prices set forth on the front cover of this prospectus.(1)

| (1) | If the underwriters exercise their option to purchase an additional 6,000,000 shares of our common stock in full solely to cover over-allotments, our public stockholders, senior management team and directors and other continuing investors are expected to own 95.0%, 5.0% and 0.0%, respectively, of our outstanding common stock, and we, our senior management team and directors and all other continuing investors are expected to own 71.3%, 7.3% and 21.4% of the outstanding operating partnership units, respectively. |

| (2) | On a fully diluted basis, our public stockholders are expected to own 64.7% of our outstanding common stock, our senior management team and directors are expected to own 11.8% of our outstanding common stock, and all other continuing investors as a group are expected to own 23.5% of our outstanding common stock. |

| (3) | If the underwriters exercise their option to purchase an additional 6,000,000 shares of our common stock in full solely to cover over-allotments, on a fully diluted basis, our public stockholders are expected to own 67.8% of our outstanding common stock, our senior management team and directors are expected to own 10.8% of our outstanding common stock, and all other continuing investors as a group are expected to own 21.4% of our outstanding common stock. |

| (4) | Our operating partnership will own various properties directly, or indirectly through limited liability companies and/or limited partnerships, the structure of which may be based upon the tax treatment of such an entity in the state in which the property is located or dictated by the financing that is placed on the property. |

11

Table of Contents

Upon completion of this offering or in connection with the formation transactions, our senior management team, our directors and our continuing investors will receive material benefits, including the following (all amounts are based on the mid-point of the range of prices set forth on the front cover of this prospectus):

| • | In the case of Adam Ifshin, our Chairman, Chief Executive Officer and President, he is expected to own 5.6% of our outstanding common stock, or 7.6% on a fully diluted basis, with a total value of $59.1 million represented by 2,375,000 shares of common stock, 2,222,818 operating partnership units and 131,837 LTIP units. |

| • | In the case of Stephen Ifshin, our Vice Chairman, he is expected to own 2.8% of our outstanding common stock on a fully diluted basis, with a total value of $21.4 million, represented by 1,542,827 operating partnership units and 167,115 LTIP units. |

| • | In the case of Daniel Taub, our Chief Operating Officer, he is expected to own 0.3% of our outstanding common stock on a fully diluted basis, with a total value of $2.7 million, represented by 103,748 operating partnership units and 110,767 LTIP units. |

| • | In the case of William Comeau, our Chief Financial Officer, he is expected to own 0.2% of our outstanding common stock on a fully diluted basis, with a total value of $1.3 million, represented by 2,094 operating partnership units and 100,952 LTIP units. |

| • | In the case of Jonathan Wigser, our Chief Investment Officer and Secretary, he is expected to own 0.3% of our outstanding common stock on a fully diluted basis, with a total value of $2.2 million, represented by 63,268 operating partnership units and 110,801 LTIP units. |

| • | In the case of Michael Cohen, our Executive Vice President of Leasing, he is expected to own 0.5% of our outstanding common stock on a fully diluted basis, with a total value of $3.7 million, represented by 187,974 operating partnership units and 110,797 LTIP units. |

| • | In the case of Catherine Paglia, one of our independent directors, she is expected to own 0.1% of our outstanding common stock on a fully diluted basis, with a total value of $0.9 million, represented by 68,569 operating partnership units and 5,200 restricted shares of common stock. |

| • | Employment agreements for Mr. Adam Ifshin, Mr. Stephen Ifshin, Mr. Taub, Mr. Comeau, Mr. Wigser and Mr. Cohen, providing for salary, bonus and other benefits, including severance upon a termination of employment under certain circumstances as described under “Management—Employment Agreements.” |

| • | Indemnification by us for certain liabilities and expenses incurred as a result of actions brought, or threatened to be brought, against our senior management team and directors of our management company who will become members of our senior management team and/or directors, in their capacities as such. |

| • | Indemnification by us against adverse tax consequences to Messrs. Adam Ifshin and Stephen Ifshin in the event that we sell in a taxable transaction 25 of our properties until the eighth anniversary of the closing of the formation transactions. |

| • | Our commitment to use commercially reasonable efforts to make $75.0 million of indebtedness available for guarantee, or otherwise bear the risk of loss, by certain continuing investors, including Messrs. Adam Ifshin and Stephen Ifshin, which will, among other things, allow them to defer the recognition of gain in connection with the formation transactions. |

| • | The benefit of (i) the property management, construction management and leasing services provided by us to Infill Development, LLC, an entity that Messrs. Adam Ifshin and Stephen Ifshin control and |

12

Table of Contents

(ii) the management, leasing and redevelopment services provided by us to each of the excluded entities that own the excluded properties under management agreements, each of which we believe contains fair market terms and conditions. |

| • | The repayment of approximately $6.5 million of indebtedness to our management company under an existing secured revolving credit facility. |

| • | The release of guarantees to repay personally approximately $18.4 million of indebtedness that will be repaid with the proceeds of this offering and/or assumed upon the closing of this offering. |

| • | A release by us with respect to all claims, liabilities, damages and obligations against (i) Mr. Adam Ifshin, related to his ownership of our management company and Delphi and (ii) our senior management team related to their ownership in the existing entities and their employment with our management company that exist at the closing of the formation transactions, other than breaches by them or entities related to them, as applicable, of the employment and non-competition agreement and the exchange and subscription agreements entered into by them and these entities in connection with the formation transactions. |

| • | Effective upon completion of this offering, we will grant 131,837, 167,115, 110,767, 100,952, 110,801 and 110,797 LTIP units, to each of Mr. Adam Ifshin, Mr. Stephen Ifshin, Mr. Taub, Mr. Comeau, Mr. Wigser and Mr. Cohen, respectively, that are subject to certain vesting requirements. |

| • | Effective upon completion of this offering, we will grant an aggregate of 26,000 restricted shares of our common stock to our independent directors. |

| • | Our predecessor will declare final distributions to the continuing investors, including members of our senior management team and certain of our directors, in the amount of approximately $19.0 million in the aggregate, which will be paid shortly following consummation of this offering. |

Persons holding shares of our common stock and operating partnership units as a result of the formation transactions will have rights (i) beginning one year after the completion of this offering, to cause our operating partnership to redeem any or all of their operating partnership units for a cash amount equal to the then-current market value of one share of our common stock per operating partnership unit, or, at our election, to exchange each of such operating partnership unit for which a redemption notice has been received for shares of our common stock on a one-for-one basis and (ii) beginning 14 months after completion of this offering, (a) to cause us to register shares of our common stock that may be issued in exchange for operating partnership units and LTIP units upon issuance or for resale under the Securities Act and (b) to cause us to register such shares of common stock for resale under the Securities Act.

Under the operating partnership agreement, holders of operating partnership units do not have redemption or exchange rights and may not otherwise transfer their operating partnership units, except under certain limited circumstances, for a period of one year after consummation of this offering. In addition, each continuing investor, including the members of our senior management team and one of our independent directors, will be required to execute a lock-up agreement in connection with the consolidation transaction that prohibits such continuing investor, for one year following completion of this offering, without the written consent of the representatives of the underwriters to directly or indirectly, offer for sale, sell, pledge, or otherwise dispose of (or enter into any transaction or agreement which is designed to, or could be expected to have any such result) any operating partnership units or shares of our common stock. In addition, our company and certain of our independent directors have agreed with the representatives of the underwriters, subject to certain exceptions, not to sell or otherwise transfer or encumber any shares of our common stock or securities convertible or exchangeable into common stock (including operating partnership units) owned by them at the completion of this offering for a period of 180 days after the date of this prospectus without the consent of the representatives.

13

Table of Contents

Restrictions on Ownership of Our Capital Stock

To assist us in complying with the limitations on the concentration of ownership of a REIT imposed by the Internal Revenue Code of 1986, as amended, or the Code, among other purposes, our charter generally prohibits, with certain exceptions, any stockholder from beneficially or constructively owning, applying certain attribution rules under the Code, more than 9.0% by value or number of shares, whichever is more restrictive, of the outstanding shares of our common stock, or 9.0% by value or number of shares, whichever is more restrictive, of the outstanding shares of our capital stock. As an exception to this general prohibition, our charter permits Adam Ifshin, our chief executive officer and president, together with his family, to own up to 13.8% by value or number of shares, whichever is more restrictive, of our outstanding shares of common stock or capital stock. Our board of directors may, in its sole discretion, waive (prospectively or retroactively) the 9.0% ownership limits with respect to a particular stockholder if it receives certain representations and undertakings required by our charter and is presented with evidence satisfactory to it that such ownership will not then or in the future cause it to fail to qualify as a REIT.

Excluded Properties and Businesses

Mr. Adam Ifshin and certain other members of our senior management team own interests in seven additional shopping centers and one office building that will not be contributed to us in the formation transactions, which we refer to collectively as the excluded properties. In addition, Mr. Adam Ifshin is the sole stockholder of First Man Investment Securities Corp. an entity that is a registered placement agent. Messrs. Adam Ifshin and Stephen Ifshin also control Infill Development, LLC, primarily a stand-alone development business, that may continue to develop primarily single tenant stand-alone properties for Walgreens. Messrs. Adam Ifshin and Stephen Ifshin each own 50% of the membership interests in UrbanCore Development, LLC, a commercial real estate consulting and development company focused on mixed-use commercial sites in urban markets. Each of these businesses will not be contributed to us in the formation transactions and we refer to them as the excluded businesses. Pursuant to our management agreements with subsidiaries of Infill Development, LLC, we have been designated as the exclusive property manager for all properties owned by Infill Development, LLC, and will provide construction management and leasing services to Infill Development, LLC on what we believe to be market terms. Pursuant to management agreements between our company and the excluded entities, we have been designated as the exclusive property and redevelopment manager and leasing agent for the excluded properties on what we believe to be market terms.

Following the completion of this offering, there will be conflicts of interest with respect to certain transactions between the holders of operating partnership units and our stockholders. In particular, the consummation of certain business combinations, the sale of any properties or a reduction of indebtedness could have adverse tax consequences to holders of operating partnership units, which would make those transactions less desirable to them. Our senior management team will hold operating partnership units and shares of our common stock upon completion of this offering and the formation transactions.

We did not conduct arm’s length negotiations with the parties involved regarding the terms of the formation transactions. In the course of structuring the formation transactions, certain members of our senior management team and other contributors had the ability to influence the type and level of benefits that they will receive from us. In addition, we have not obtained as part of the formation transactions any recent third-party appraisals of the properties and other assets we will own upon completion of this offering and the formation transactions, or any other independent third-party valuations or fairness opinions in connection with the formation transactions. As a result, the consideration to be given by us for our properties and other assets in the formation transactions may exceed their fair market value.

14

Table of Contents

We have adopted policies designed to eliminate or minimize certain potential conflicts of interest, and the limited partners of our operating partnership have agreed that in the event of a conflict in the duties owed by us to our stockholders and the fiduciary duties owed by us, in our capacity as general partner of our operating partnership, to such limited partners, we will fulfill our fiduciary duties to such limited partners by acting in the best interests of our stockholders. See “Policies with Respect to Certain Activities—Conflict of Interest Policies” and “Description of the Partnership Agreement of DLC Realty, L.P.—Fiduciary Responsibilities.”

We intend to make regular quarterly distributions to holders of shares of our common stock. We intend to pay a pro rata initial distribution with respect to the period commencing on the completion of this offering and ending September 30, 2010, based on $0.15 per share for a full quarter. On an annualized basis, this would be $0.60 per share, or an annual distribution rate of approximately 4.8% based on the mid-point of the range of prices set forth on the front cover of this prospectus. We estimate that this initial annual distribution will represent approximately 107.5% of our estimated cash available for distribution to our common stockholders for the twelve months ending March 31, 2011. Although we have not previously paid distributions, we intend to maintain our initial distribution rate for the twelve-month period following completion of this offering unless actual results of operations, economic conditions or other factors differ materially from the assumptions used in our estimate. We may be required to fund distributions from working capital or borrow to provide funds for such distribution or we may make a portion of the required distributions in the form of a taxable stock dividend. However, we have no intention to use the net proceeds from this offering to make distributions nor do we intend to make distributions using shares of our common stock. Distributions declared by us will be authorized by our board of directors in its sole discretion out of funds legally available therefor and will be dependent upon a number of factors, including restrictions under applicable law, the capital requirements of our company and meeting the distribution requirements necessary to maintain our qualification as a REIT. Actual distributions may be significantly different from the expected distributions. We do not intend to reduce the expected distribution per share if the underwriters exercise their option to purchase up to 6,000,000 additional shares solely to cover over-allotments.

We intend to elect and qualify as a REIT commencing with our taxable year ending December 31, 2010. We believe we have been organized in conformity with the requirements for qualification and taxation as a REIT under the Code, and that our intended manner of operation will enable us to meet the requirements for qualification and taxation as a REIT. So long as we qualify as a REIT, we generally will not be subject to U.S. federal income tax on our taxable income that we distribute currently to our stockholders. If we fail to qualify as a REIT in any taxable year and do not qualify for certain statutory relief provisions, we will be subject to U.S. federal income tax at regular corporate rates and may be precluded from qualifying as a REIT for the subsequent four taxable years following the year during which we lost our REIT qualification. Even if we qualify for taxation as a REIT, we may be subject to certain U.S. federal, state and local taxes on our income or property. See “U.S. Federal Income Tax Considerations.”

15

Table of Contents

Common stock offered by us | 40,000,000 shares |

Common stock to be outstanding after this offering | 42,401,000 shares (1) |

Common stock and operating partnership units to be outstanding after this offering | 61,846,284 shares / units(2) |

Use of proceeds | We intend to use the net proceeds of this offering to: |

| • | repay or defease existing indebtedness, including prepayment penalties, exit fees, swap breakage costs and defeasance costs related to such indebtedness; |

| • | pay fees associated with the senior secured revolving credit facility; |

| • | pay fees in connection the assumption of indebtedness, including assumption fees; |

| • | pay expenses incurred in connection with this offering and the formation transactions; |

| • | pay certain holders of interests in the existing entities that are non-accredited investors for their equity interests in certain of the existing entities; and |

| • | for general working capital purposes and to fund potential future acquisitions and redevelopment activities. |

Proposed New York Stock Exchange symbol | “DLC” |

| (1) | Includes 26,000 restricted shares of our common stock to be granted by us concurrently with this offering to our independent directors and 2,375,000 shares of our common stock to be issued in connection with the formation transactions. Assumes no exercise by the underwriters of their option to purchase up to an additional 6,000,000 shares of our common stock solely to cover over-allotments, excludes 5,350,533 shares available for future issuance under our 2010 equity incentive plan and 732,269 LTIP units to be granted by us concurrently with this offering to our executive officers under our 2010 equity incentive plan. |

| (2) | Includes 18,713,015 operating partnership units and 732,269 LTIP units not owned by us expected to be outstanding following the consummation of the formation transactions. The operating partnership units may, subject to the limits in the operating partnership agreement, be exchanged for cash or, at our option, shares of our common stock on a one-for-one basis generally commencing one year after the date of this prospectus. |

16

Table of Contents

Summary Historical and Unaudited Pro Forma Financial and Operating Data

The following table sets forth summary financial and operating data on (i) a pro forma basis for our company giving effect to this offering and the formation transactions the use of proceeds thereof and the other adjustments described in the unaudited pro forma financial information beginning on page F-2 and (ii) a combined historical basis for our predecessor beginning on page F-15. We have not presented historical information for DLC Realty Trust, Inc. because we have not had any corporate activity since our formation other than the issuance of shares of common stock in connection with the initial capitalization of our company and because we believe a discussion of the results of our company would not be meaningful.

Our predecessor’s combined historical financial information includes:

| • | our management company, including its asset and property management, leasing and real estate redevelopment operations; |

| • | the commercial real estate brokerage operations of Delphi; and |

| • | the real estate operations for the existing entities. |

You should read the following summary financial data in conjunction with our combined historical and unaudited pro forma condensed consolidated financial statements and the related notes and with “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

The summary historical combined balance sheet information as of December 31, 2009 and 2008 of our predecessor and summary combined statements of operations information for the years ended December 31, 2009, 2008 and 2007 of our predecessor have been derived from the audited historical combined financial statements of our predecessor. Ernst & Young LLP, our independent auditors whose report with respect thereto is included elsewhere in this prospectus with the combined balance sheets as of December 31, 2009 and 2008 and the related combined statements of operations and cash flows for the years ended December 31, 2009, 2008 and 2007, and the related notes thereto. The historical combined balance sheet information as of March 31, 2010 and combined statements of operations for the three months ended March 31, 2010 and 2009 have been derived from the unaudited combined financial statements of our predecessor. The summary historical combined balance sheet information as of December 31, 2007, 2006 and 2005 and summary combined statements of operations information for the years ended December 31, 2006 and December 31, 2005 have been derived from the unaudited combined financial statements of our predecessor. Our results of operations for the interim period ended March 31, 2010 are not necessarily indicative of the results that will be obtained for the full fiscal year.