Issuer Free Writing Prospectus

Filed Pursuant to Rule 433

Registration No: 333-166225

September 6, 2011

Attached is the presentation by management during the Annual Meeting of Shareholders of Customers Bank on September 6, 2011.

Annual Shareholders Meeting

September 6, 2011

Forward-Looking Statements

This presentation includes forward-looking statements, including statements about future results. These

statements are subject to uncertainties and risks, including but not limited to our ability to integrate the

business and operations of companies and banks that we may acquire in the future, and do so in a cost-

efficient manner; the failure to effectively implement our growth strategy; inability to generate sufficient

deposits or obtain other sources of liquidity; changes in the level of non-performing assets, classified

assets and charge-offs; the loss of key personnel; potential customer loss, deposit attrition and business

disruption as a result of companies and banks that we may acquire in the future; the failure to achieve

expected gains, revenue growth, and/or expense savings from companies and banks that we may acquire

in the future; our need and our ability to incur additional debt or equity financing; the strength of the

United States economy in general and the strength of the local economies in which we conduct

operations; the accuracy of our financial statement estimates and assumptions, including the sufficiency

of our loan loss reserves; the effects of inflation, interest rate, market and monetary fluctuations; the

effects of our lack of a diversified loan portfolio, including the risks of geographic and industry

concentrations; the frequency and magnitude of foreclosure of our loans; effect of changes in the stock

market and other capital markets; legislative or regulatory changes; our ability to comply with the

extensive laws and regulations to which we are subject; the willingness of customers to accept third-party

products and services rather than our products and services and vice versa; changes in the securities and

real estate markets; increased competition and its effect on pricing; technological changes; changes in

monetary and fiscal policies of the U.S. Government; the effects of security breaches and computer

viruses that may affect our computer systems; changes in consumer spending and saving habits; growth

and profitability of our non-interest income; changes in accounting principles, policies, practices or

guidelines; anti-takeover provisions under Federal and state law as well as our Articles of Association and

our bylaws; and our ability to manage the risks involved in the foregoing.

statements are subject to uncertainties and risks, including but not limited to our ability to integrate the

business and operations of companies and banks that we may acquire in the future, and do so in a cost-

efficient manner; the failure to effectively implement our growth strategy; inability to generate sufficient

deposits or obtain other sources of liquidity; changes in the level of non-performing assets, classified

assets and charge-offs; the loss of key personnel; potential customer loss, deposit attrition and business

disruption as a result of companies and banks that we may acquire in the future; the failure to achieve

expected gains, revenue growth, and/or expense savings from companies and banks that we may acquire

in the future; our need and our ability to incur additional debt or equity financing; the strength of the

United States economy in general and the strength of the local economies in which we conduct

operations; the accuracy of our financial statement estimates and assumptions, including the sufficiency

of our loan loss reserves; the effects of inflation, interest rate, market and monetary fluctuations; the

effects of our lack of a diversified loan portfolio, including the risks of geographic and industry

concentrations; the frequency and magnitude of foreclosure of our loans; effect of changes in the stock

market and other capital markets; legislative or regulatory changes; our ability to comply with the

extensive laws and regulations to which we are subject; the willingness of customers to accept third-party

products and services rather than our products and services and vice versa; changes in the securities and

real estate markets; increased competition and its effect on pricing; technological changes; changes in

monetary and fiscal policies of the U.S. Government; the effects of security breaches and computer

viruses that may affect our computer systems; changes in consumer spending and saving habits; growth

and profitability of our non-interest income; changes in accounting principles, policies, practices or

guidelines; anti-takeover provisions under Federal and state law as well as our Articles of Association and

our bylaws; and our ability to manage the risks involved in the foregoing.

2

Forward-Looking Statements updated

This presentation as well as other written or oral communications made from time to time by us, may contain certain

forward-looking information within the meaning of the Securities Act of 1933, as amended, and the Securities

Exchange Act of 1934, as amended. These statements relate to future events or future predictions, including events

or predictions relating to our future financial performance, and are generally identifiable by the use of forward-looking

terminology such as “believes,” “expects,” “may,” “will,” “should,” “plan,” “intend,” or “anticipates” or the negative

thereof or comparable terminology, or by discussion of strategy that involve risks and uncertainties. These forward-

looking statements are only predictions and estimates regarding future events and circumstances and involve known

and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance

or achievements to be materially different from any future results, levels of activity, performance or achievements

expressed or implied by such forward-looking statements. This information is based on various assumptions by us

that may not prove to be correct.

forward-looking information within the meaning of the Securities Act of 1933, as amended, and the Securities

Exchange Act of 1934, as amended. These statements relate to future events or future predictions, including events

or predictions relating to our future financial performance, and are generally identifiable by the use of forward-looking

terminology such as “believes,” “expects,” “may,” “will,” “should,” “plan,” “intend,” or “anticipates” or the negative

thereof or comparable terminology, or by discussion of strategy that involve risks and uncertainties. These forward-

looking statements are only predictions and estimates regarding future events and circumstances and involve known

and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance

or achievements to be materially different from any future results, levels of activity, performance or achievements

expressed or implied by such forward-looking statements. This information is based on various assumptions by us

that may not prove to be correct.

Important factors to consider and evaluate in such forward-looking statements include:

· changes in the external competitive market factors that might impact our results of operations;

· changes in laws and regulations, including without limitation changes in capital requirements under the federal

prompt corrective action regulations;

prompt corrective action regulations;

· changes in our business strategy or an inability to execute our strategy due to the occurrence of unanticipated

events;

events;

· our ability to identify potential candidates for, and consummate, acquisition or investment transactions;

· the timing of acquisition or investment transactions;

· constraints on our ability to consummate an attractive acquisition or investment transaction because of

significant competition for these opportunities;

significant competition for these opportunities;

· the failure of the Bank to complete any or all of the transactions described herein on the terms currently

contemplated;

contemplated;

· local, regional and national economic conditions and events and the impact they may have on us and our

customers;

customers;

· ability to attract deposits and other sources of liquidity;

· changes in the financial performance and/or condition of our borrowers;

· changes in the level of non-performing and classified assets and charge-offs;

3

Forward-Looking Statements updated

· changes in estimates of future loan loss reserve requirements based upon the periodic review thereof under

relevant regulatory and accounting requirements;

relevant regulatory and accounting requirements;

· the integration of the Bank’s recent FDIC-assisted acquisitions may present unforeseen challenges;

· inflation, interest rate, securities market and monetary fluctuations;

· the timely development and acceptance of new banking products and services and perceived overall value of

these products and services by users;

these products and services by users;

· changes in consumer spending, borrowing and saving habits;

· technological changes;

· the ability to increase market share and control expenses;

· continued volatility in the credit and equity markets and its effect on the general economy; and

· the effect of changes in accounting policies and practices, as may be adopted by the regulatory agencies, as

well as the Public Company Accounting Oversight Board, the Financial Accounting Standards Board and other

accounting standard setters;

well as the Public Company Accounting Oversight Board, the Financial Accounting Standards Board and other

accounting standard setters;

· the businesses of the Bank and any acquisition targets or merger partners and subsidiaries not integrating

successfully or such integration being more difficult, time-consuming or costly than expected;

successfully or such integration being more difficult, time-consuming or costly than expected;

· material differences in the actual financial results of merger and acquisition activities compared with

expectations, such as with respect to the full realization of anticipated cost savings and revenue enhancements

within the expected time frame;

expectations, such as with respect to the full realization of anticipated cost savings and revenue enhancements

within the expected time frame;

· revenues following any merger being lower than expected; and

· deposit attrition, operating costs, customer loss and business disruption following the merger, including, without

limitation, difficulties in maintaining relationships with employees being greater than expected.

limitation, difficulties in maintaining relationships with employees being greater than expected.

These forward-looking statements are subject to significant uncertainties and contingencies, many of which are

beyond our control. Although we believe that the expectations reflected in the forward-looking statements are

reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Accordingly, there

can be no assurance that actual results will meet expectations or will not be materially lower than the results

contemplated in this presentation. You are cautioned not to place undue reliance on these forward-looking

statements, which speak only as of the date of this document or, in the case of documents referred to or incorporated

by reference, the dates of those documents. We do not undertake any obligation to release publicly any revisions to

these forward-looking statements to reflect events or circumstances after the date of this document or to reflect the

occurrence of unanticipated events, except as may be required under applicable law.

beyond our control. Although we believe that the expectations reflected in the forward-looking statements are

reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Accordingly, there

can be no assurance that actual results will meet expectations or will not be materially lower than the results

contemplated in this presentation. You are cautioned not to place undue reliance on these forward-looking

statements, which speak only as of the date of this document or, in the case of documents referred to or incorporated

by reference, the dates of those documents. We do not undertake any obligation to release publicly any revisions to

these forward-looking statements to reflect events or circumstances after the date of this document or to reflect the

occurrence of unanticipated events, except as may be required under applicable law.

4

Where We Stand Today

§ Well-capitalized bank headquartered in Wyomissing, PA with over $1.7

billion in assets, 11 branches in suburban Philadelphia, Hamilton, NJ and

Port Chester, NY

billion in assets, 11 branches in suburban Philadelphia, Hamilton, NJ and

Port Chester, NY

§ Ranked #1 Top Performing Bank in Pennsylvania and #4 among America’s

top performing banks with assets under $3 billion by American Banking

Journal in 2010

top performing banks with assets under $3 billion by American Banking

Journal in 2010

§ Raised $93 million of common equity ($16 million in 2011, $60 million in

2010, $17 million in 2009)

2010, $17 million in 2009)

§ Management team with extensive community banking and M&A

experience

experience

§ 19th largest bank in PA in terms of assets

§ Total deposits now over $1.4 billion with average branch size is over

$120 million

$120 million

§ Significant board and management ownership (23.6%)

5

Directors

Directors

6

Experienced Management Team

§ Highly experienced and cohesive management team with an average tenure of 30 years leadership experience

§ Management interests aligned with shareholders

7

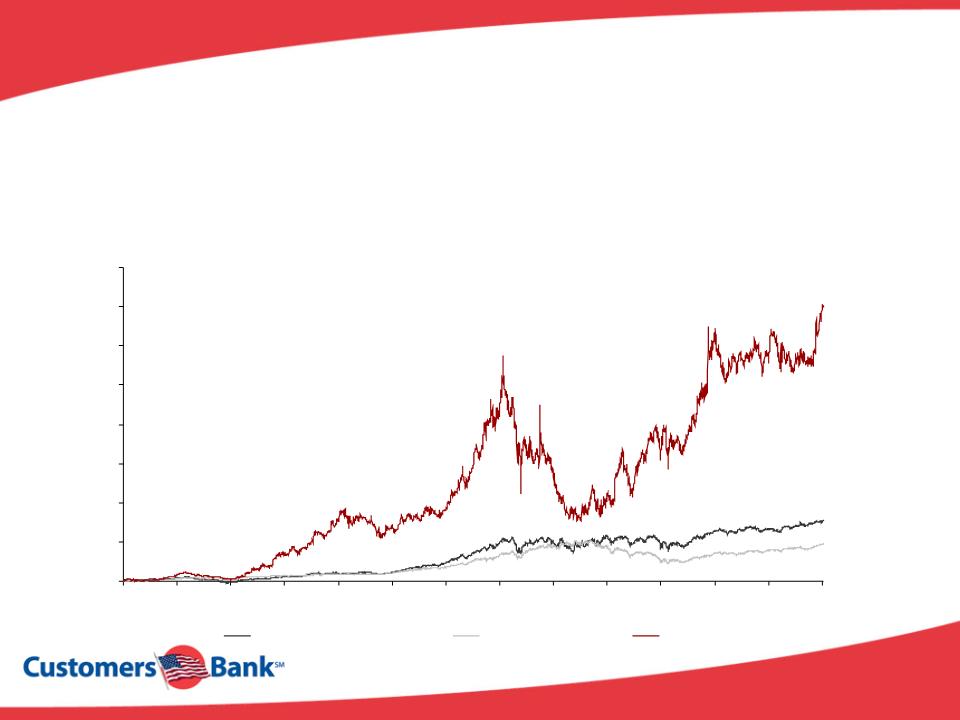

Management Team Track

Record

§ Jay Sidhu, Customers Bank Chairman and CEO, served at Sovereign from 1986 to 2006

§ As CEO, Mr. Sidhu oversaw the growth from a $500 million asset financially-challenged thrift to a

$90 billion financial institution

$90 billion financial institution

§ Sovereign had more than 785 branch locations spanning from Maryland to New Hampshire

100%

600%

1100%

1600%

2100%

2600%

3100%

3600%

4100%

Dec-87

Jun-89

Nov-90

May-92

Oct-93

Apr-95

Sep-96

Mar-98

Aug-99

Feb-01

Jul-02

Jan-04

Jun-05

Dec-06

SNL Bank Index

S&P 500

SOV

8

Investment Highlights

Proven

Management

Team

Management

Team

§ Experience in building community banks into a multi-billion dollar depository franchise

§ Worked together for more than 15 years delivering above average shareholder value

§ Successfully executed and integrated 30 acquisitions and delivered on organic growth

strategies

strategies

Existing Bank

Platform

Platform

§ Well-capitalized, scalable and reserves for legacy credit issues

§ Achieved stand-alone profitability organically

§ Strong risk management culture and strategy in place

§ New management and board members significantly invested

Unique Organic

Growth Strategy

Growth Strategy

§ Small bank acquisitions

§ Branch divestitures

§ Positioned as a partner of choice

§ FDIC-assisted transactions (regulatory approval required)

§ “High tech, high touch” strategy that brings the bank to the customer

§ Targeting approximately 25% annual organic deposit growth rate

§ Unique branch expansion model

Substantial

M&A

Opportunities

M&A

Opportunities

9

Strategic Initiatives

§ “High tech, high touch” model designed to take the bank to the customer

§ Capture market share from larger bank competitors by employing high

producing team members, providing superior service, and leveraging

technological infrastructure

producing team members, providing superior service, and leveraging

technological infrastructure

§ Long-term goal, add 4 - 6 branches annually in core franchise market through

cost-efficient branching strategy (1 branches in 2011)

cost-efficient branching strategy (1 branches in 2011)

§ Lending initiatives focused on small-business, multi-family, mortgage banking,

home equity, warehouse, and manufactured housing

home equity, warehouse, and manufactured housing

§ Expand fee-based services and products including mortgage banking, small

business cash management, and online/mobile banking

business cash management, and online/mobile banking

§ Maintain strong risk management culture

10

Deposit Strategy

§ Capture market share from larger competitors by providing customers with a “high tech, high

touch” customer experience

touch” customer experience

Concierge Banking

§ Brings banker to

customer, 12 hours a

day, 7 days a week

customer, 12 hours a

day, 7 days a week

§ Appointment banking

approach

approach

§ Customer has access to

senior level

management

senior level

management

§ Most convenient bank

for customers

for customers

Pricing

§ Low cost banking model

allows for more pricing

flexibility

allows for more pricing

flexibility

§ Significantly lower

overhead costs vs. a

traditional branch

overhead costs vs. a

traditional branch

§ Pricing/profitability

measured across

relationship

measured across

relationship

Technology

§ Implementation of new

technology suite allows for

unique product offerings:

technology suite allows for

unique product offerings:

§ Remote account opening

§ Remote deposit capture

§ Internet/mobile banking

§ Online switch kits

§ ATM Deployment

§ Partnered with Intuit

technology suite

technology suite

§ Provides customer with

an enhanced online

banking experience

an enhanced online

banking experience

Sales Force

§ Top producers

§ Bankers own a

portfolio of

customers

portfolio of

customers

§ Business

development

officers

compensation

aligned with the

Bank’s interests

development

officers

compensation

aligned with the

Bank’s interests

§ Deposit pricing and

growth strongly

incentivized

growth strongly

incentivized

11

Lending Strategy

§ Capitalize on management’s in-market experience with a focus on commercial lending

Small Business

§ Target companies

with less than $5.0

million in annual

revenue

with less than $5.0

million in annual

revenue

§ Loans (incl. SBA

loans) originated

by branch network

and specialist small

business

relationship

managers

loans) originated

by branch network

and specialist small

business

relationship

managers

Specialty Lending

§ Capitalize on recent

market disruption

market disruption

§ Diversify earning assets

§ Focus on lower risk lines

of business

of business

§ Warehouse lending

§ Manufactured

Housing (with credit

enhancement)

Housing (with credit

enhancement)

§ Mortgage Banking

§ Multifamily Lending

Consumer Lending

§ Focus on real estate-

secured lending

secured lending

§ Conservative

underwriting standards

(>700 FICO score)

underwriting standards

(>700 FICO score)

§ Establish long-term

customer relationship

customer relationship

Commercial Banking

Business Banking

§ Target companies with

$5.0 to $20.0 million in

annual revenue

$5.0 to $20.0 million in

annual revenue

§ Business driven by

dedicated relationship

managers

dedicated relationship

managers

§ Loan offices operate

on a mobile basis

on a mobile basis

12

Target Franchise Market

Target Markets

Existing Markets

Berks County, PA

Bucks County, PA

Chester County, PA

Delaware County, PA

Mercer County, NJ

Westchester County, NY

Selected Attractive Counties

Lackawanna County, PA

Montgomery County, PA

Northampton County, PA

Schuylkill County, PA

Middlesex County, NJ

Monmouth County, NJ

Ocean County, NJ

Greenwich, CT

All counties in MD

Customer Bank branches

13

Key Financial Targets

§ Return on Equity = 10% to 12%

§ Return on Assets = 1.00% to 1.10%

§ Tier 1 Leverage Ratio = 8% to 10%

§ Total-Risk Based Capital Ratio = 12% plus

§ Loan-to-Deposit Ratio = 70% to 90%

§ Investments / Assets < = 25%

§ Borrowings / Assets < = 15%

§ Fee Revenue / Total Revenue = 15% to 25%

§ Net Interest Margin > = 3.00%

§ Efficiency Ratio < = 50%

§ Deposit Mix = 40% or less CD

§ Loan Mix = 50% Commercial / 50% Consumer

§ Specialty Lending = 25% or less capital at risk per specialty business

14

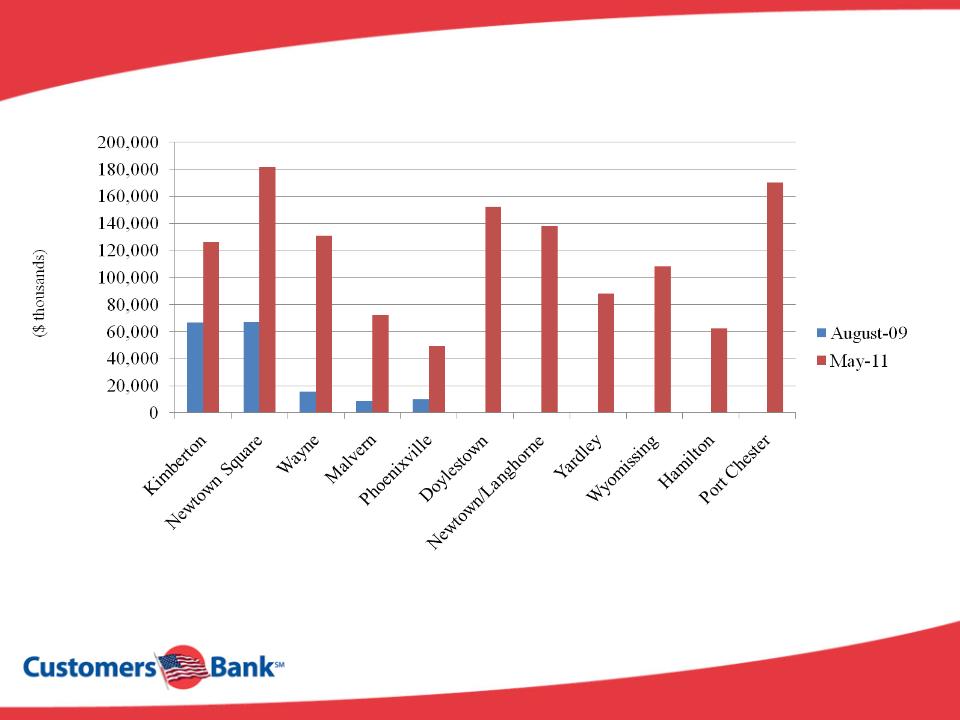

Deposit Growth

15

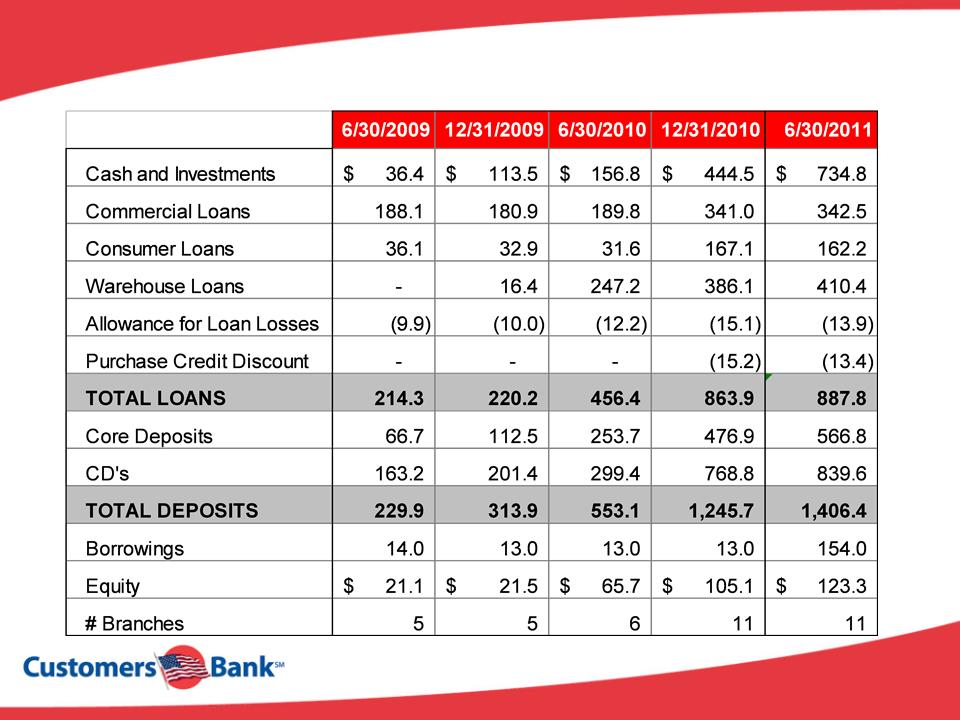

Financial Highlights

16

USA Bank Acquisition

§ 1 Branch bank headquartered in Port Chester, NY

§ Acquired $196 million of assets and $202 million of liabilities

§ All loans have 80% loss sharing protection from the FDIC

§ Branch is near very affluent areas including Greenwich, Stamford, CT,

White Plains, NY, etc.

White Plains, NY, etc.

§ Goal is to build $500 million franchise in 3 to 5 years

§ Bargain purchase gain is over $20 million after tax

§ No capital raise needed for this deal as the book value per share

accretion was 30%

accretion was 30%

§ Closed in July 2010

§ System conversion completed

17

ISN Bank Acquisition

§ 1 Branch bank headquartered in Cherry Hill, NJ

§ Acquired $78 million of assets and $76 million of liabilities

§ All loans have 80% loss sharing protection from the FDIC

§ Bargain purchase gain is over $8.2 million after tax

§ No capital raise needed for this deal as the book value per share

accretion was 8%

accretion was 8%

§ Closed in September 2010

§ System conversion completed

18

Berkshire Bank Acquisition

§ 5 Branch bank headquartered in Wyomissing, PA

§ $140 million bank with $125 million of deposits and $107 million of

loans

loans

§ Purchase price is book value; price adjusts lower if book value drops

with a price floor; if non-performing assets increase 20% between now

and close we can walk away

with a price floor; if non-performing assets increase 20% between now

and close we can walk away

§ Mildly accretive to earnings per share and modest book value dilution

§ Goals is to create a $500 million franchise in Berks County making $5 to

$7.5 million per year in net income; this deal accelerates expansion in a

more cost effective way versus de novo expansion

$7.5 million per year in net income; this deal accelerates expansion in a

more cost effective way versus de novo expansion

§ Expected to close this month

§ System conversion scheduled for September 17th, 2011

19

Conclusion

§ Unique bank platform; current banking dislocation provides significant

opportunity for M&A growth that is supported by a strong organic business

model

opportunity for M&A growth that is supported by a strong organic business

model

§ Management team with proven capability of integrating acquisitions and

delivering above average shareholder returns

delivering above average shareholder returns

§ Considerable opportunities for traditional M&A

§ Strive to create above average shareholder returns over the long term

20

21

Annual Shareholders Meeting

September 6, 2011

Customers Bank filed a registration statement on Form S-1 (File no. 333-166225) with the U.S.

Securities and Exchange Commission (“SEC”) which included the prospectus for the offer and sale

of securities of a bank holding company (the “Holding Company”) to shareholders of the Bank in

connection with a proposed reorganization of the Bank to a bank holding company structure and

a proposed merger of Berkshire Bancorp, Inc. (“Berkshire”) with an into the Holding Company

(collectively, the “proposed transaction”). The combined prospectus and proxy statement,

together with other documents filed by the Holding Company with the SEC, contained important

information about the Bank, the Holding Company and the proposed transaction. We urge

investors, Bank shareholders and Berkshire shareholders to read carefully the combined

prospectus and proxy statement and other documents filed with the SEC, including any

amendments or supplements also filed with the SEC. Bank Investors and shareholders may

obtain a free copy of the combined prospectus and proxy statement at the SEC's website at

http://www.sec.gov. Copies of the combined prospectus and proxy statement can also be

obtained free of charge by directing a request to Customers Bank, Corporate Secretary, 99 Bridge

Street, Phoenixville, PA 19460, or calling (484) 923-2164.

Securities and Exchange Commission (“SEC”) which included the prospectus for the offer and sale

of securities of a bank holding company (the “Holding Company”) to shareholders of the Bank in

connection with a proposed reorganization of the Bank to a bank holding company structure and

a proposed merger of Berkshire Bancorp, Inc. (“Berkshire”) with an into the Holding Company

(collectively, the “proposed transaction”). The combined prospectus and proxy statement,

together with other documents filed by the Holding Company with the SEC, contained important

information about the Bank, the Holding Company and the proposed transaction. We urge

investors, Bank shareholders and Berkshire shareholders to read carefully the combined

prospectus and proxy statement and other documents filed with the SEC, including any

amendments or supplements also filed with the SEC. Bank Investors and shareholders may

obtain a free copy of the combined prospectus and proxy statement at the SEC's website at

http://www.sec.gov. Copies of the combined prospectus and proxy statement can also be

obtained free of charge by directing a request to Customers Bank, Corporate Secretary, 99 Bridge

Street, Phoenixville, PA 19460, or calling (484) 923-2164.

The Bank, the Holding Company and certain of their directors and executive officers may, under

the rules of the SEC, be deemed to be “participants” in the solicitation of proxies from

shareholders in connection with the proposed transaction. Information concerning the interests

of directors and executive officers is set forth in the combined prospectus and proxy statement

relating to the proposed transaction.

the rules of the SEC, be deemed to be “participants” in the solicitation of proxies from

shareholders in connection with the proposed transaction. Information concerning the interests

of directors and executive officers is set forth in the combined prospectus and proxy statement

relating to the proposed transaction.

This communication shall not constitute an offer to sell or the solicitation of an offer to buy any

securities nor shall there be any sale of securities in any jurisdiction in which the offer,

solicitation, or sale is unlawful before registration or qualification of the securities under the

securities laws of the jurisdiction. No offer of securities shall be made except by means of a

prospectus satisfying the requirements of Section 10 of the Securities Act of 1933, as amended.

securities nor shall there be any sale of securities in any jurisdiction in which the offer,

solicitation, or sale is unlawful before registration or qualification of the securities under the

securities laws of the jurisdiction. No offer of securities shall be made except by means of a

prospectus satisfying the requirements of Section 10 of the Securities Act of 1933, as amended.