Highly Focused, Low Risk, High Growth Bank Holding Company

Investor Presentation

July 2014

NASDAQ: CUBI

Note: All information in this document has been adjusted for the10% stock dividend that was

declared on May 15, 2014 to shareholders of record on May 27th payable on June 30, 2014.

This presentation as well as other written or oral communications made from time to time by us, may contain certain forward-looking information within the meaning of the Securities Act of 1933, as amended, and the Securities Exchange Act of 1934, as amended. These statements relate to future events or future predictions, including events or predictions relating to our future financial performance, and are generally identifiable by the use of forward-looking terminology such as “believes,” “expects,” “may,” “will,” “should,” “plan,” “intend,” “target,” or “anticipates” or the negative thereof or comparable terminology, or by discussion of strategy or goals that involve risks and uncertainties. These forward-looking statements are only predictions and estimates regarding future events and circumstances and involve known and unknown risks, uncertainties and other factors that may cause our actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by such forward-looking statements. This information is based on various assumptions by us that may not prove to be correct.Important factors to consider and evaluate in such forward-looking statements include:changes in the external competitive market factors that might impact our results of operations;changes in laws and regulations, including without limitation changes in capital requirements under the federal prompt corrective action regulations;changes in our business strategy or an inability to execute our strategy due to the occurrence of unanticipated events;our ability to identify potential candidates for, and consummate, acquisition or investment transactions;the timing of acquisition or investment transactions;constraints on our ability to consummate an attractive acquisition or investment transaction because of significant competition for these opportunities;the failure of the Bank to complete any or all of the transactions described herein on the terms currently contemplated;local, regional and national economic conditions and events and the impact they may have on us and our customers;ability to attract deposits and other sources of liquidity;changes in the financial performance and/or condition of our borrowers;changes in the level of non-performing and classified assets and charge-offs;changes in estimates of future loan loss reserve requirements based upon the periodic review thereof under relevant regulatory and accounting requirements;the integration of the Bank’s recent FDIC-assisted acquisitions may present unforeseen challenges;inflation, interest rate, securities market and monetary fluctuations;the timely development and acceptance of new banking products and services and perceived overall value of these products and services by users;changes in consumer spending, borrowing and saving habits;technological changes;

the ability to increase market share and control expenses;continued volatility in the credit and equity markets and its effect on the general economy; andthe effect of changes in accounting policies and practices, as may be adopted by the regulatory agencies, as well as the Public Company Accounting Oversight Board, the Financial Accounting Standards Board and other accounting standard setters;the businesses of the Bank and any acquisition targets or merger partners and subsidiaries not integrating successfully or such integration being more difficult, time-consuming or costly than expected;material differences in the actual financial results of merger and acquisition activities compared with expectations, such as with respect to the full realization of anticipated cost savings and revenue enhancements within the expected time frame; revenues following any merger being lower than expected; anddeposit attrition, operating costs, customer loss and business disruption following the merger, including, without limitation, difficulties in maintaining relationships with employees being greater than expected.These forward-looking statements are subject to significant uncertainties and contingencies, many of which are beyond our control. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Accordingly, there can be no assurance that actual results will meet expectations or will not be materially lower than the results contemplated in this presentation. You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this document or, in the case of documents referred to or incorporated by reference, the dates of those documents. We do not undertake any obligation to release publicly any revisions to these forward-looking statements to reflect events or circumstances after the date of this document or to reflect the occurrence of unanticipated events, except as may be required under applicable law.This presentation is for discussion purposes only, and shall not constitute any offer to sell or the solicitation of an offer to buy any security, nor is it intended to give rise to any legal relationship between Customers Bancorp, Inc. (the “Company”) and you or any other person, nor is it a recommendation to buy any securities or enter into any transaction with the Company. The information contained herein is preliminary and material changes to such information may be made at any time. If any offer of securities is made, it shall be made pursuant to a definitive offering memorandum or prospectus (“Offering Memorandum”) prepared by or on behalf of the Company, which would contain material information not contained herein and which shall supersede, amend and supplement this information in its entirety. Any decision to invest in the Company’s securities should be made after reviewing an Offering Memorandum, conducting such investigations as the investor deems necessary or appropriate, and consulting the investor’s own legal, accounting, tax, and other advisors in order to make an independent determination of the suitability and consequences of an investment in such securities. No offer to purchase securities of the Company will be made or accepted prior to receipt by an investor of an Offering Memorandum and relevant subscription documentation, all of which must be reviewed together with the Company’s then-current financial statements and, with respect to the subscription documentation, completed and returned to the Company in its entirety. Unless purchasing in an offering of securities registered pursuant to the Securities Act of 1933, as amended, all investors must be “accredited investors” as defined in the securities laws of the United States before they can invest in the Company

4

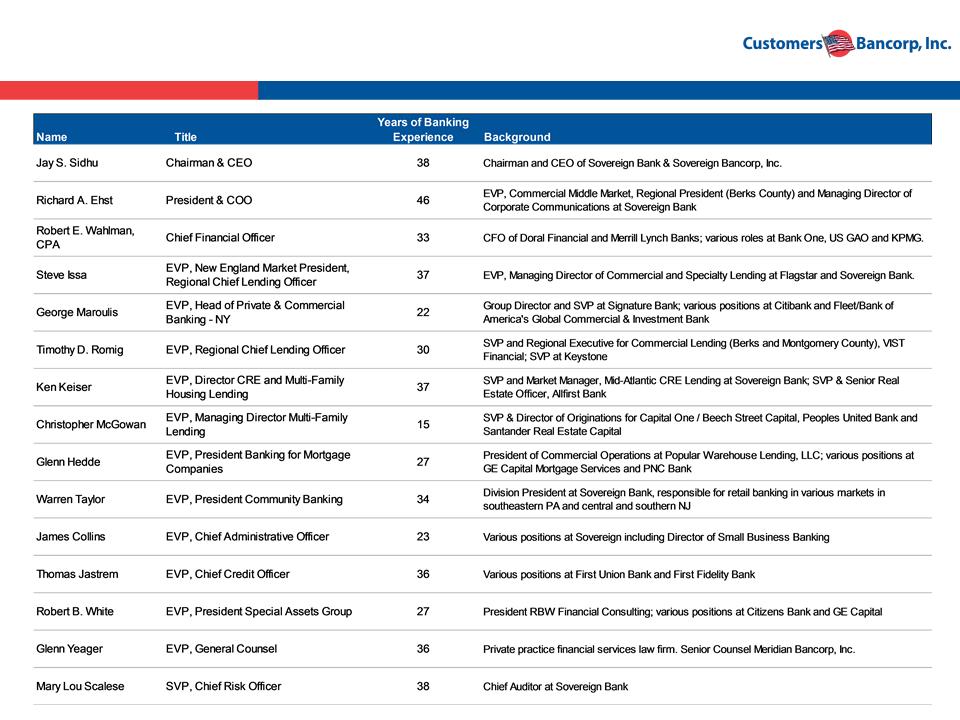

Our Biggest Advantage: A Highly Experienced Management Team

5

Investment Proposition

High Organic Growth, Well Capitalized, Low Risk, Branch Lite Bank

in Attractive Markets

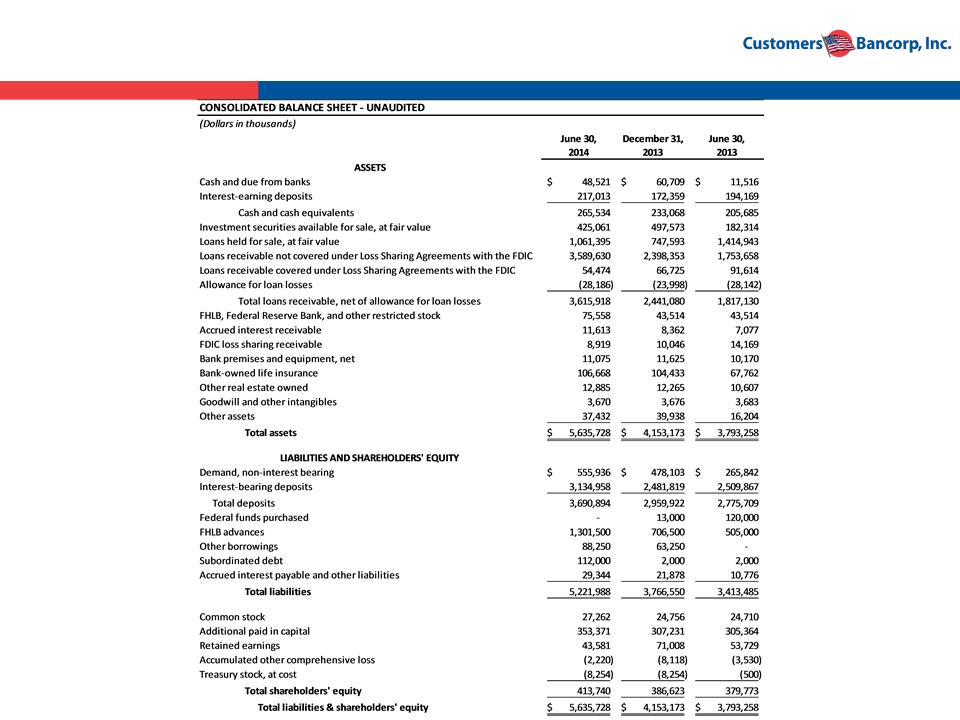

§ $5.6 billion asset bank

§ Well capitalized at 12.8% total risk based capital and 7.8% tier 1 leverage

§ Target market from Boston to Washington D.C. along interstate 95

Strong Profitability & Growth

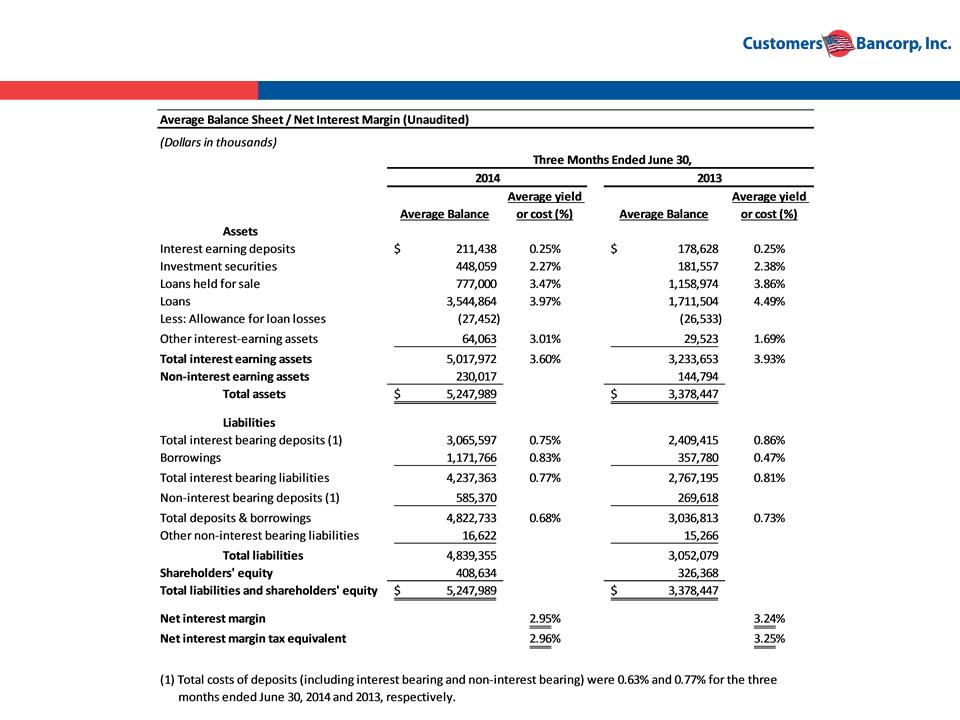

§ Q2 2014 earnings up 24% over 2Q 2013 with an ROE of 10%

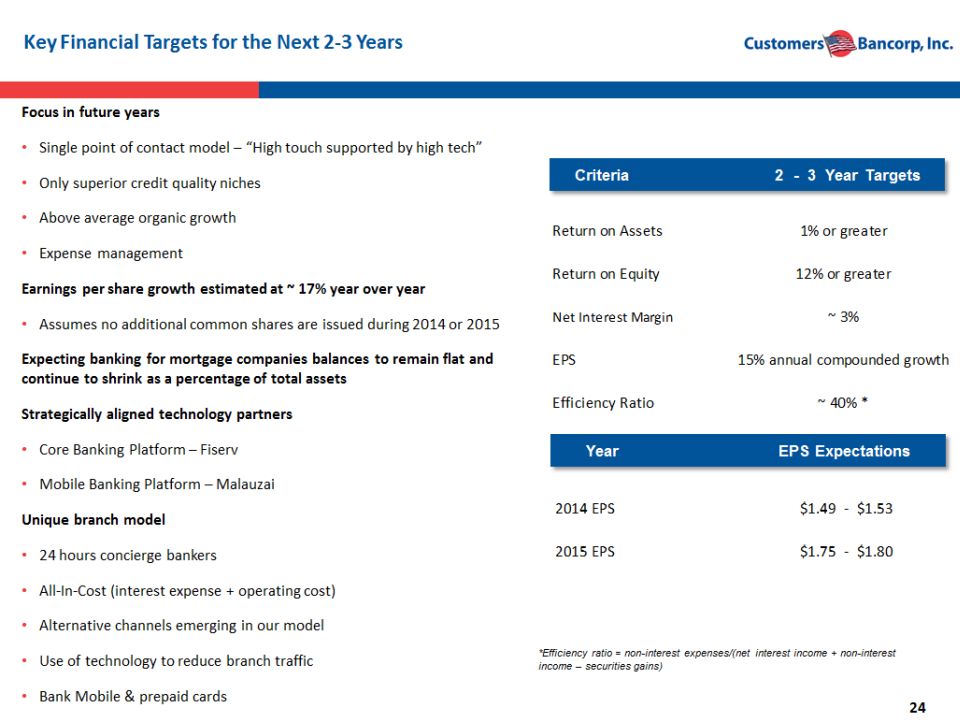

§ ROA goal of 1% + and ROE of 12% + within 2-3 years

§ 3.00% net interest margin goal; Targeting efficiency ratio in the 40’s

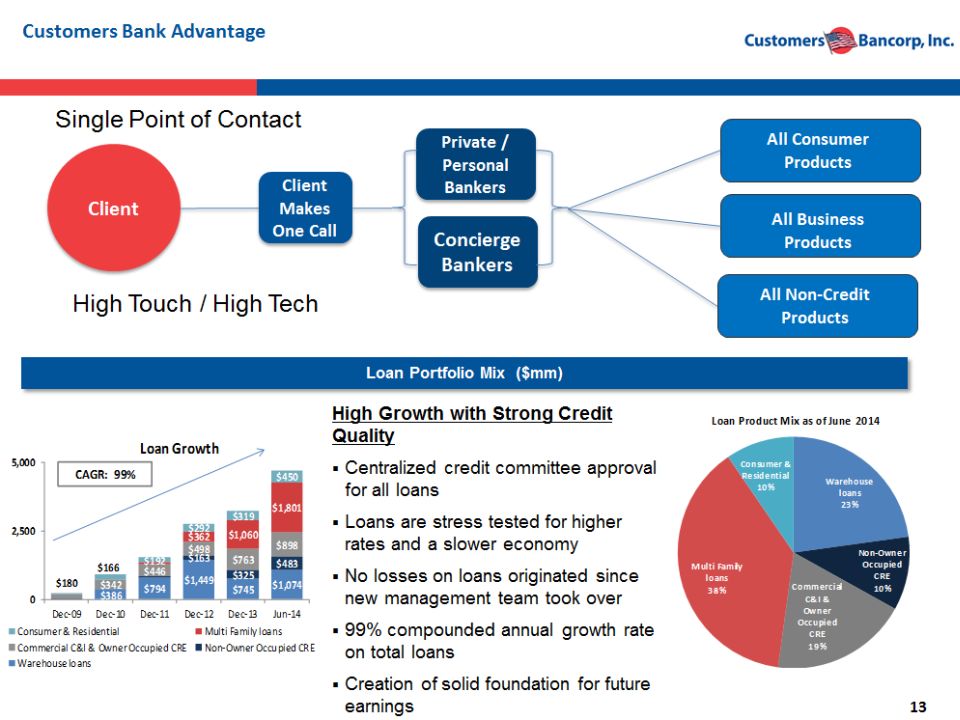

§ 99% compounded annual growth in loans since 2009

§ DDA and total deposits compounded annual growth of 99% and 73%

respectively since 2009

§ 142% compounded annual growth in core earnings since 2011

Strong Credit Quality

§ No charge-offs on loans originated after 2009

§ 0.27% non-performing loans (non-FDIC covered loans)

§ Total reserves to non-performing loans of 184.2%

* Capital ratios are estimates pending final call report

6

Investment Proposition

Low Interest Rate Risk

§ Approximately 40% of the loan portfolio will re-price within one

year (1)

§ 40% of loans have an average life of 3.8 years

§ ~18% of deposits, on average, are non-interest bearing

§ Extending liabilities at this time

§ $150 million in forward starting swaps

§ Neutral to gradually rising rates over next one to two years

Attractive Valuation

§ Current share price ($18.80)(2) is 12.5x estimated 2014 earnings,

and 10.6x estimated 2015 earnings

§ Price/tangible book only at 1.2x and 1.1x for 2014 and 2015

respectively

(1) Includes mortgage warehouse

(2) Share price as of July 17, 2014

7

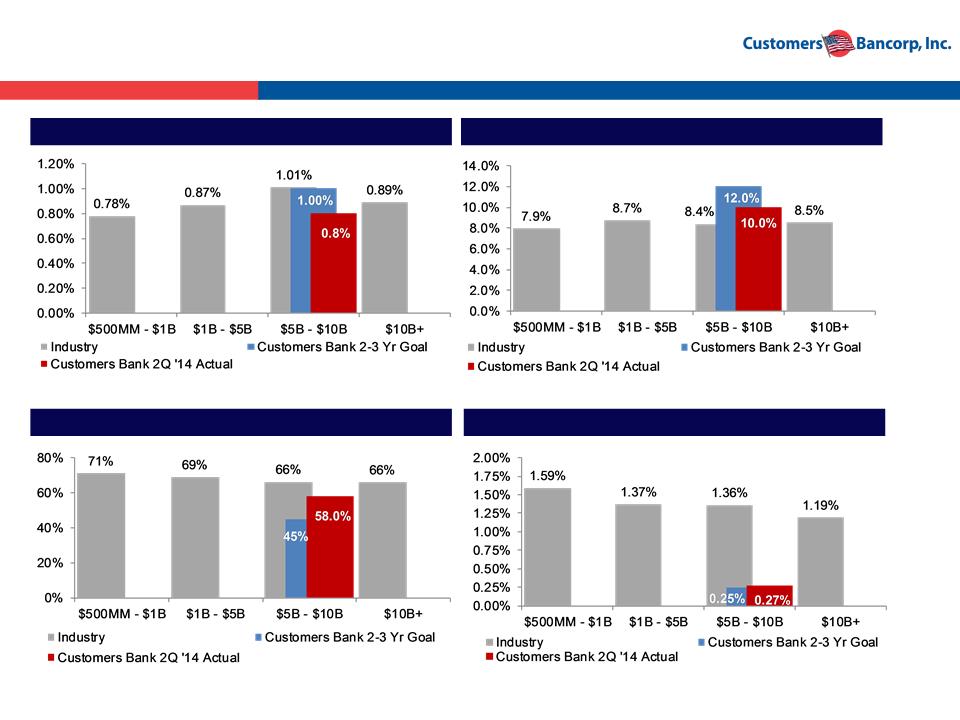

Return on Average Equity

Efficiency Ratio

NPAs

Return on Average Assets

Source: SNL Financial on an LTM basis as of 4Q2013

Customers Bancorp Will Become A Stronger Performer

We invested in and took control of a $270 million asset Customers Bank (FKA New Century Bank)Identified existing credit problems, adequately reserved and recapitalized the bank Actively worked out very extensive loan problems Recruited experienced management team Enhanced credit and risk management Developed infrastructure for organic growth Built out warehouse lending platform and doubled deposit and loan portfolio Completed 3 small acquisitions: ISN Bank (FDIC-assisted) ~ $70 mm USA Bank (FDIC-assisted) ~ $170 mm Berkshire Bancorp (Whole bank) ~ $85 mm Recruited proven lending teams Built out Commercial and Multi-family lending platformsDe Novo expansion;4-6 sales offices or teams added each year Continue to show strong loan and deposit growth Built a “branch lite” high growth Community Bank and model for future growthGoals to ~12%+ ROE; ~1% ROA Single Point of Contact Private Banking model executed – commercial focus Introduce bankmobile – banking of the future for consumers Continue to show strong loan and deposit growth ~12%+ ROE; ~1% ROA expected within 36 months ~$6+ billion asset bank by end of 2014 ~$9 billion asset bank by end of 2019 2009Assets: $350M Equity: $22M 2010-2011 Assets: $2.1B Equity: $148M 2012–2013 Assets: $4.2B Equity: $400M 2Q 2014 Assets: $5.6B Equity: $414M

9

Disciplined Model for Increasing Shareholder Value

§ Strong organic revenue growth + scalable

infrastructure = sustainable double digit EPS growth

and increased shareholder value

§ A clear and simple risk management driven business

strategy

§ Build tangible book value per share each quarter via

earnings

§ Any book value dilution from any acquisitions must

be overcome within 1-2 years

§ Superior execution through proven management

team

Disciplined Model for Superior Shareholder Value Creation

10

Banking Strategy

Business Banking Strategy - ~95% of revenues come from

business

• Loan and deposit business through these segments:

• Banking Privately Held Businesses

• Banking High Net Worth Families

• Banking Mortgage Companies

Consumer Banking Strategy

• Principal focus is getting deposits in a highly efficient and

unique model while meeting the needs of all the

communities in our assessment area

• Introduce Bank Mobile and Prepaid business for Gen Y

and under-banked by late 2014; strategic partnerships for

consumer loan products

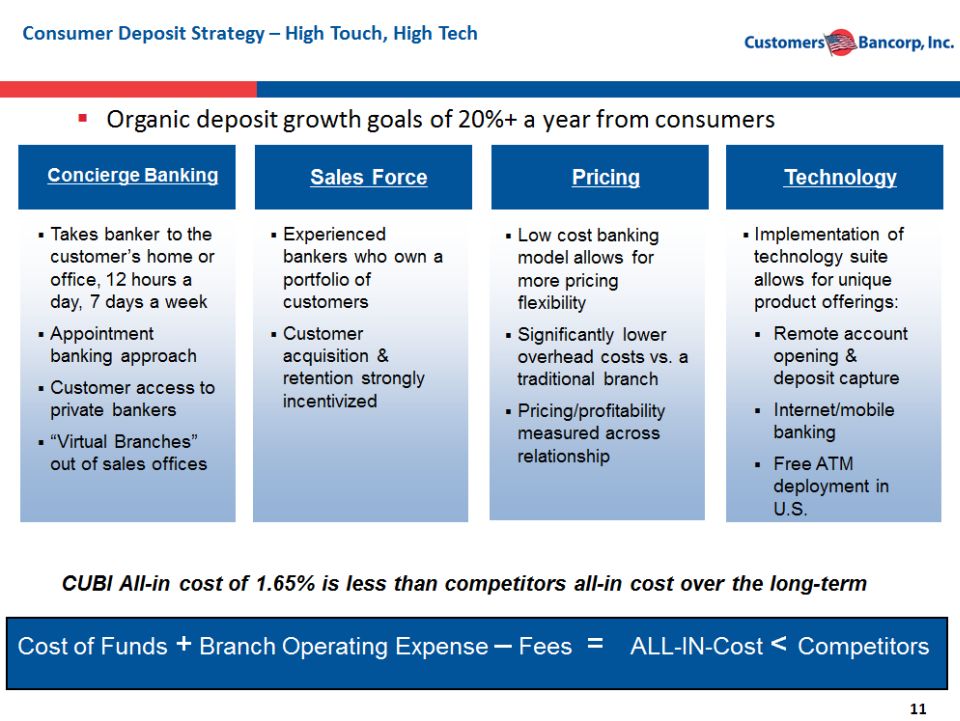

Takes banker to the customer’s home or office, 12 hours a day, 7 days a week Appointment banking approach Customer access to private bankers “Virtual Branches” out of sales offices Experienced bankers who own a portfolio of customers Customer acquisition & retention strongly incentivized Low cost banking model allows for more pricing flexibility Significantly lower overhead costs vs. a traditional branch Pricing/profitability measured across relationship Implementation of technology suite allows for unique product offerings: Remote account opening & deposit capture Internet/mobile banking Free ATM deployment in U.S. CUBI All-in cost of 1.65% is less than competitors all-in cost over the long-term Cost of Funds + Branch Operating Expense – Fees = ALL-IN-Cost < Competitors Organic deposit growth goals of 20%+ a year from consumers Concierge Banking Sales Force Pricing Technology

12

Results of Deposit Growth: Organic Growth With Controlled Costs

Source: Company data.

Total Deposit Growth ($mm)

Average DDA Growth ($mm)

Customers strategies of single point of contact and recruiting known teams in

target markets produce rapid deposit growth with low total cost

High Growth with Strong Credit Quality Centralized credit committee approval for all loans Loans are stress tested for higher rates and a slower economy No losses on loans originated since new management team took over 99% compounded annual growth rate on total loans Creation of solid foundation for future earnings Client Client Makes One Call Private / Personal Bankers Concierge Bankers All Consumer Products All Business Products All Non-Credit Products

14

C&I & Owner Occupied CRE Banking Strategy

Small Business

§Target companies with less than

$5.0 million annual revenue

§Principally SBA loans originated by

small business relationship

managers or branch network

§Current focus PA & NJ markets

Private & Commercial

§Target companies with up to $100

million annual revenues

§Very experienced teams

§Single point of contact

§NE, NY, PA & NJ markets

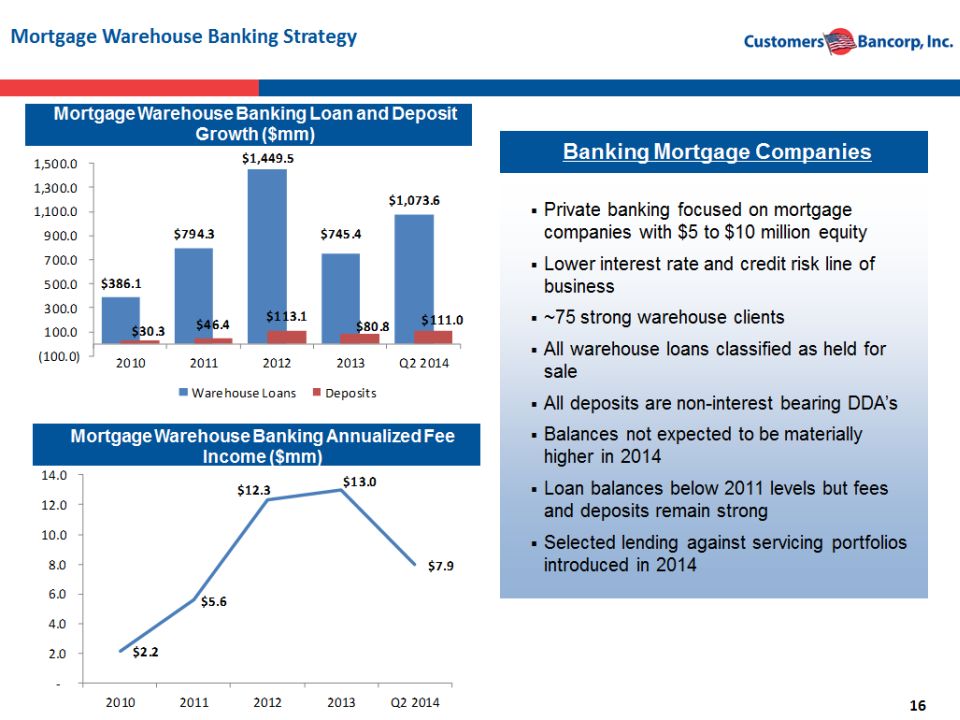

Banking Privately Held Business

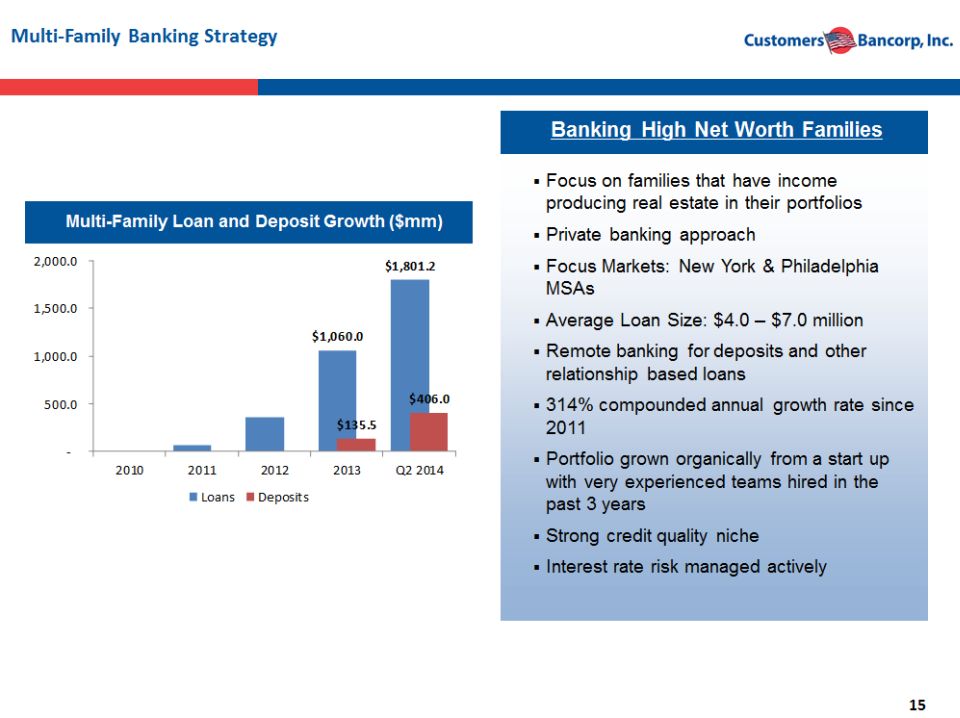

Banking High Net Worth Families Focus on families that have income producing real estate in their portfolios Private banking approach Focus Markets: New York & Philadelphia MSAs Average Loan Size: $4.0 – $7.0 million Remote banking for deposits and other relationship based loans 314% compounded annual growth rate since 2011 Portfolio grown organically from a start up with very experienced teams hired in the past 3 years Strong credit quality niche Interest rate risk managed actively

17

These Deposit and Lending Strategies Results in Disciplined &

Profitable Growth

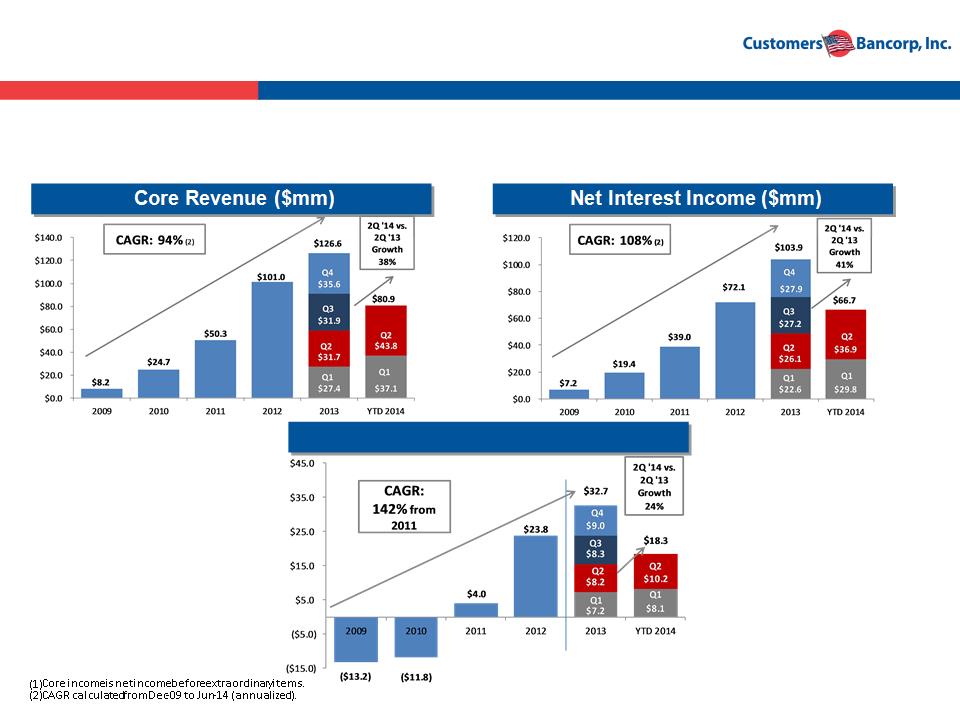

Core Net Income ($mm) (1)

Source: SNL Financial and Company data.

• Strategy execution has produced superior growth in revenues and earnings

18

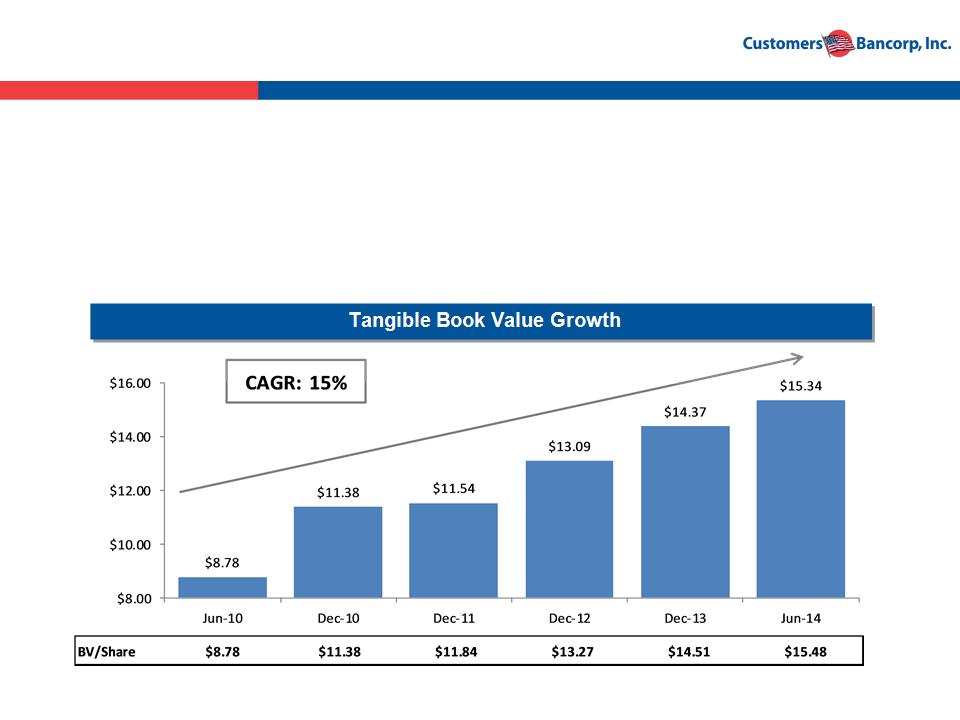

Strong Growth Provides for Shareholder Value Creation

§ Per share tangible book value up 35% since December 2010

§ Focused on continuous growth of TBV aligns executive management

compensation with shareholder value creation

§ Any tangible book value dilution from acquisition must be recovered

within 1 to 2 years

Note: Shares estimated pending final dividend adjustment

Credit Improving – Though Banks Face a Number of Operational Headwinds Capital Accumulation Continues To Create Deployment Challenges ROI Continues to Trend Below 10% Despite Being Modestly Higher Than Pre-Recession1 Critical to Have a Winning Business Model Credit Improving NPAs and NCOs greatly declining across the sector Asset Generation Banks are starved for interest-earning assets and exploring new asset classes, competing on price and looking into specialty finance business / lending NIM Compression Low rate environment for the foreseeable future will continue to compress NIM Several institutions have undergone balance sheet restructuring to alleviate near-term NIM pressure Operational leverage Expense management is top of mind as banks try to improve efficiency in light of revenue pressure and increased regulatory / compliance costs Local dominance Strong credit quality Core deposits Expense management Diversity Cross sell Capital efficiency Higher profitability / consistent earnings Innovator / disruptor Differentiated / Unique model Technology savvy Product dominance

20

Customers Bank Views Itself As An Innovator

That Is Poised To Take Advantage Of

Changes Taking Place In The Industry

• Changes in technology have resulted in the digitization of consumer

and business transactions and automation of the payment system

• Technology dependent consumers and small businesses are not

visiting branches

• Customers are looking for an exceptional experience, no nuisance

fees and very competitive offerings at their fingertips

• Mobile has become the fastest growing channel for financial

services

22

Startling Facts About Banks

§ Banks each year charge $32 billion in overdraft fees -

that’s allowing or creating over 1 billion overdrafts

each year….Why??

§ Payday lenders charge consumers another $7 billion in fees

§ That’s more than 3x what America spends on Breast Cancer

and Lung Cancer combined

§ Combined this is about 50% of all America spends on Food

Stamps

§ Some of banking industries most profitable consumer

customers hate banks

§ Another estimated 25% consumers are unbanked or under

banked

This should not be happening in America

We hope to start, in a small way, a new

revolution to address this problem

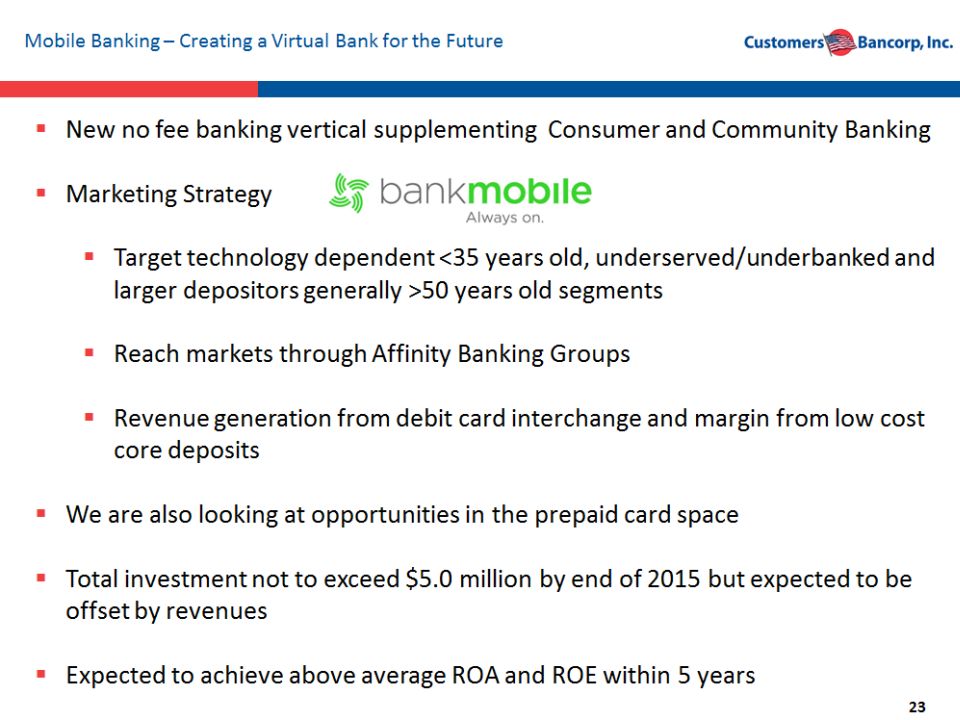

New no fee banking vertical supplementing Consumer and Community Banking Marketing Strategy Target technology dependent <35 years old, underserved/underbanked and larger depositors generally >50 years old segments Reach markets through Affinity Banking Groups Revenue generation from debit card interchange and margin from low cost core deposits We are also looking at opportunities in the prepaid card space Total investment not to exceed $5.0 million by end of 2015 but expected to be offset by revenues Expected to achieve above average ROA and ROE within 5 years Mobile Banking – Creating a Virtual Bank for the Future

25

Summary

§ Strong high performing $5.6 billion bank with significant growth

opportunities

§ Very experienced management team delivers strong results

§ Ranked #1 overall by Bank Director Magazine in the 2012

and 2013 Growth Leader Rankings

§ “High touch, high tech” processes and technologies result in

superior growth, returns and efficiencies

§ Shareholder value results from the combination of increasing

tangible book value with strong and consistent earnings growth

§ Attractive risk-reward: growing several times faster than

industry average but yet trading at a significant discount to

peers

§ Introducing among the 1st mobile banking application for

account opening and complete mobile platform based servicing

in the USA

26

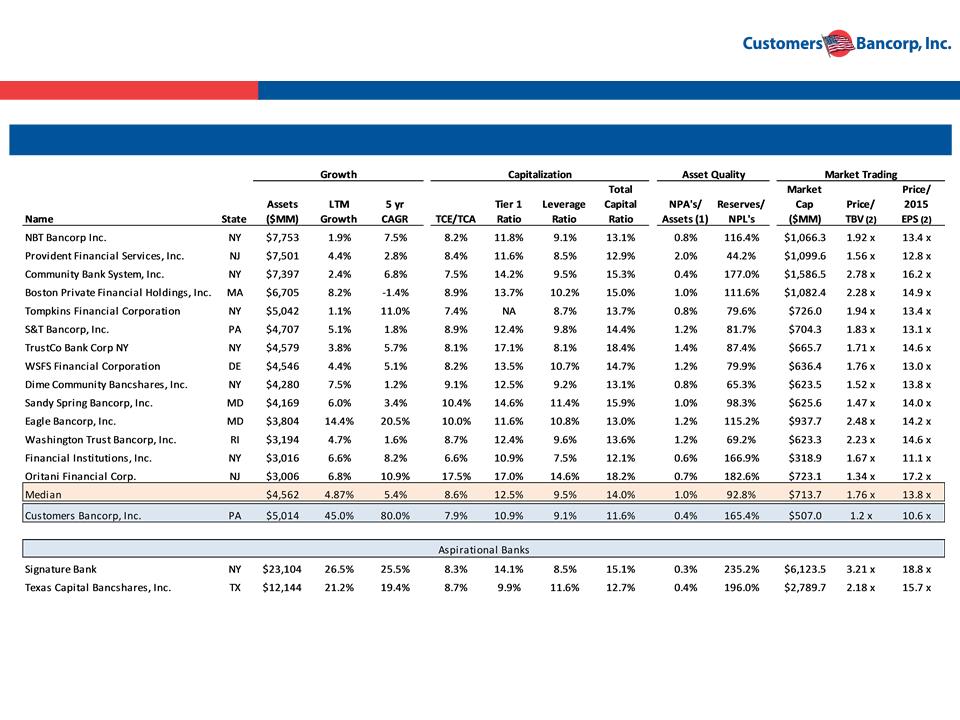

Regional Bank Comparison

High Performance Regional Banks

Source: SNL Financial, Company documents. Market data as of 3/31/2014. Consists of Northeast and Mid-Atlantic banks and thrifts with assets between $3.0 billion and $8.0

billion and most recent quarter core ROAA greater than 90 bps. Excludes merger targets and MHCs.

(1)Customers Bancorp NPAs/Assets calculated as non-covered NPAs divided by total assets. Non-covered NPAs excludes accruing TDRs and loans 90+ days past due and still

accruing.

(2)Customers Bancorp Price/TBV and Price/2015 EPS based on share price as of July 17, 2014.

27

Contacts

Company:

Robert Wahlman, CFO

Tel: 610-743-8074

rwahlman@customersbank.com

www.customersbank.com

Jay Sidhu

Chairman & CEO

Tel: 610-301-6476

jsidhu@customersbank.com

www.customersbank.com

Investor Relations:

Ted Haberfield

President, MZ North America

Tel: 760-755-2716

thaberfield@mzgroup.us

www.mzgroup.us