MANAGEMENT’S DISCUSSION AND ANALYSIS

For the three and nine months ended September 30, 2013

Tables are expressed in USD $000’s except share and per share amounts

The following provides management’s discussion and analysis (‘‘MD&A’’) of IMRIS Inc.’s consolidated results of operations and financial condition for the three and nine months ended September 30, 2013. In this MD&A, “IMRIS”, the “Company”, “we”, “our” and “us” are used to refer to IMRIS Inc.

This MD&A is dated as of November 4, 2013 and should be read in conjunction with the interim unaudited consolidated financial statements and the notes thereto for the three and nine months ended September 30, 2013 and with the audited consolidated financial statements and notes thereto for the year ended December 31, 2012.

This MD&A contains forward-looking statements about future events or future performance and reflects management’s expectations and assumptions regarding our growth, results of operations, performance and business prospects and opportunities. Such forward-looking statements reflect management’s current beliefs and are based on information currently available to us. In some cases, forward-looking statements can be identified by terminology such as “may”, “would”, “could”, “will”, “should”, “expect”, “plan”, “intend”, “anticipate”, “believe”, “estimate”, “predict”, “potential”, “continue” or the negative of these terms or other similar expressions concerning matters that are not historical facts. In particular, statements regarding our future operating results, economic performance and product development efforts are or involve forward-looking statements.

A number of factors could cause actual events, performance or results, including those in respect of the foregoing items, to differ materially from the events, performance and results discussed in the forward-looking statements. Factors which could cause future outcomes to differ materially from those set forth in the forward-looking statements include, but are not limited to: [i] timing and amount of revenue recognition of order backlog and the Company’s expectation of sales and margin growth [ii] obtaining sufficient and suitable financing to support operations and commercialization of products, [iii] adequately protecting proprietary information and technology from competitors, [iv] obtaining regulatory approvals and successfully completing new product launches, [v] successfully competing in the targeted markets, and [vi] maintaining third party relationships, including key personnel, and key suppliers. In evaluating these forward-looking statements, readers should specifically consider various factors, including the risks outlined under “Risks and Uncertainties”, which may cause actual events, performance or results to differ materially from any forward-looking statement.

Readers are cautioned that our expectation, beliefs, projections and assumptions used in preparation of such information, although considered reasonable at the time of preparation, may prove to be wrong, and as such, undue reliance should not be placed on forward-looking statements. By their nature, forward-looking statements are subject to numerous known and unknown risks and uncertainties so as a result, we can give no assurance that any of the actual events, performance, results, or expectations will occur or be realized. These forward-looking statements are expressly qualified by this cautionary statement as of the date of this MD&A and we do not intend, and do not assume any obligation, to update or revise them to reflect new or future events or circumstances.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 1 of 28 |

OVERVIEW

IMRIS designs, manufactures and marketsImage Guided Therapy Systems that enhance the effectiveness of therapy delivery. Our Image Guided Therapy Systems are a combination of real time visualization products and therapy delivery products that are designed to improve patient outcomes and reduce the cost of patient care. We accomplish this by combining our visualization technology products with therapy delivery products in a single integrated system that has the ability to provide timely information to clinicians to properly assess the treatment plan at the point of therapy delivery. We believe this approach to patient care not only improves patient outcomes, but also contributes to reduced cost of care for those patients. Our goal is to continuously deliver products that improve therapy delivery for an increasing number of medical procedures while at the same time are supported by peer reviewed published measurement of improved outcomes and reduced cost of care.

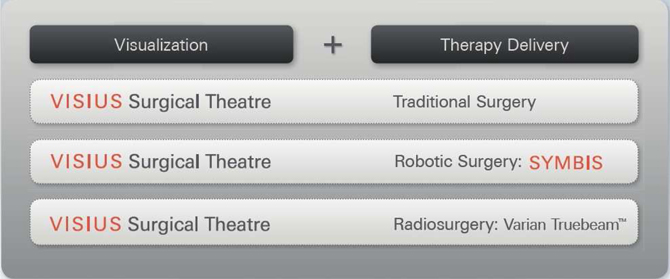

Visualization and Therapy Delivery

In 2005 at the founding of the company, we created a visualization platform based on a single Magnetic Resonance (MR) Imaging product. Since then we have introduced a variety of next generation imaging capabilities into our visualization products. These include multiple field strength MR systems, X-Ray Fluoroscopy (AX) systems, and Computed Tomography (CT) systems, all designed to provide imaging capabilities for different therapy delivery products. All of these imaging capabilities are marketed as theVISIUS Surgical Theatre.

Our goal is to design visualization products that have the ability to be used in a large number of surgical and interventional procedures and to become a foundational investment in every hospital. To do this the system must be flexible enough to meet current and evolving procedural requirements while at the same time improving patient care and reducing costs to the hospital. The VISIUS Surgical Theatre can incorporate multiple configurations and imaging modalities while reducing patient risk and delivering real-time information to clinicians while preserving optimal surgical access and techniques.

Our visualization product, the VISIUS Surgical Theatre, is used in combination with multiple therapy delivery systems including traditional surgery, Surgeon directed robotic surgery, and Radio-surgery. It is our goal to provide a means for clinicians to improve therapy delivery by moving towards a minimally invasive surgical (MIS) procedure whenever possible. The transition to an MIS procedure is expected to contribute to improved outcomes and reduced costs of care versus traditional surgical methods.

We sell our VISIUS Surgical Theatre globally to hospitals that deliver clinical services to patients in the neurosurgical, spinal, cerebrovascular, and cardiovascular markets. Historically our products have enabled therapy delivery through traditional surgical techniques, primarily for neurosurgical applications. We believe that the VISIUS Surgical Theatre, in combination with therapy delivery, has the ability to continue to expand across a large number of clinical procedures. As we continue to work with clinicians to promote and identify potential new areas of clinical application, new high value procedures are expected, resulting in increased utilization and further adoption of the products.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 2 of 28 |

Value Proposition

We believe that the combination of the VISIUS Surgical Theatre with therapy delivery benefits patients, physicians and hospitals:

Patients

| · | Improved Outcomes: Peer reviewed published research has shown significant improvements in patient outcomes when the intraoperative MRI available in the VISIUS Surgical Theatre is used in a procedure. |

| · | Risk Reduction: The risk of requiring a repeat operation because of incomplete procedures is significantly reduced due to improved levels of complete resection in the case of brain tumors as a result of the intraoperative visualization. |

Clinicians

| · | Enhanced Efficiency and Effectiveness for Clinicians: High resolution imaging information is captured rapidly and presented in a manner designed to enhance clinician efficiency and effectiveness. |

| · | Enhanced Workflow for Clinicians: The patient can be maintained in the optimal surgical position throughout the procedure and the MRI or CT imaging system is removed from the surgical or interventional theatre when not required resulting in unrestricted access to the patient by the surgical team. |

Hospitals

| · | Greater Utilization of the VISIUS Surgical Theatre:The VISIUS Surgical Theatre permits greater utilization of the imaging equipment as the MR or CT scanner can be shared by multiple operating rooms and a diagnostic imaging suite allowing for a single asset to be used by numerous clinicians. |

| · | Increased Patient Volumes: Improved patient outcomes may result in higher patient volumes and revenue for hospitals. |

| · | Technology Attracts Clinicians: Access to technologies such as the VISIUS Surgical Theatre can assist in both the recruitment and retention of clinicians. |

PRODUCT PORTFOLIO

The VISIUS Surgical Theatre is the foundational technology of our Company and continues to evolve in its utilization across numerous surgical and interventional applications. We have invested in research and development to further broaden our product portfolio by introducing new procedures into the VISIUS Surgical Theatre as well as combining it with new therapy products.

Our product portfolio consists of three therapy delivery systems made up of the VISIUS Surgical Theatre in combination with:

| 1: | Traditional surgical techniques, |

| 2: | The SYMBIS Surgical System, a surgeon controlled surgical robot, and |

| 3: | The TrueBeamTM radiation therapy product from Varian Medical Systems, Inc. (Varian). |

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 3 of 28 |

(The SYMBIS surgical system and the Radiosurgery product with the TrueBeamTM system are both works in progress and not available for commercial sale)

All of these Image Guided Therapy systems include our proprietary VISIUS Surgical Theatre in combination with therapy delivery systems that are integrated with multiple proprietary supporting products and technologies. These include patient handling systems, data management and information presentation systems, surgical devices, imaging and system control software platforms, and safety and remote management products. These are proprietary products that underlay the VISIUS Surgical Theatre’s ability to be integrated with each therapy delivery product.

| I. | VISIUS Surgical Theatre and Traditional Surgical Procedures |

The VISIUS Surgical Theatrecan be configured to support the delivery of a wide rangeof neurosurgical, cardiovascular and cerebrovascular procedures using traditional surgical techniques. The VISIUS Surgical Theatre can be equipped with intraoperative imaging utilizing MRI, x-ray angiography and computed tomography, alone or in multimodality combinations.

The VISIUS Surgical Theatre provides a fully integrated surgical environment with the availability of high-resolution images for use in a number of surgical procedures. These procedures include neurological tumor resection, epilepsy foci resection, arteriovenous malformation, aneurysm, upper C-spine and frame-based stereotaxy. Due to the invasive nature of brain surgery and the importance of minimizing disturbance to healthy brain tissue, neurosurgical procedures may particularly benefit from an MRI's unique ability to distinguish between diseased and healthy brain tissue. The VISIUS Surgical Theatre provides visualization information to allow clinicians to make adjustments to the procedure while the procedure is in progress, which may lead to improved patient outcomes and reduce the likelihood that repeat surgeries will be needed.

When equipped with an MR scanner and integrated x-ray angiography system, the VISIUS Surgical Theatre provides clinicians with timely and accurate images for visualizing the patient anatomy before, during and after interventions for the treatment of a wide variety of cardiovascular and cerebrovascular conditions, such as atrial fibrillation, certain structural heart disorders and stroke. With seamless transitions between MR and x-ray angiography systems, the VISIUS Surgical Theatre enables surgical and catheter-based treatments and real-time assessment of therapy in a single integrated suite. The single integrated system in a VISIUS Surgical Theatre eliminates patient transport between imaging modalities and streamlines workflow. After MR scanning, the patient can be transitioned to image-guided intervention on the angiography system without moving the patient from the table. During and immediately after the procedure, new MR images can be taken to assess treatment and to determine if further intervention is required.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 4 of 28 |

We have recently developed a ceiling mounted CT based version of the VISIUS Surgical Theatre leveraging our know-how from our existing VISIUS Surgical Theatre offering in MR systems for use in certain cranial and spine procedures. This system has the ability to move over top of a stationary patient, and provide intraoperative images of diagnostic quality, without the additional risk of moving the patient, while still preserving optimal surgical access and techniques. This system has the ability to move between multiple operating rooms, offering significant benefits over the previously offered floor mounted system. This product received regulatory clearance by the FDA in July 2013 and got its CE Mark for the European Union in August 2013.

| II. | VISIUS Surgical Theatre and the SYMBIS Surgical System |

In February 2010, we acquired NeuroArm Surgical Ltd and all of its intellectual property. Since then we have been developing the SYMBIS Surgical System, a surgeon controlled surgical robot designed to enable minimally invasive procedures that are currently performed in a more invasive manner. This system consists of a MR compatible robot and surgical control console integrated together with the VISIUS Surgical Theatre. We believe that the combination of optical and MR or CT imaging integrated with a surgical robot may have the ability to transform a number of surgical procedures to MIS procedures. The robot has been designed to operate in the bore of a high field MR system and a CT gantry that can provide unprecedented visualization of the surgical site by providing both optical and MR views of the surgical target. The SYMBIS Surgical System is a micro-surgical system that has all of the traditional attributes of a robotic system such as accuracy, repeatability, and control, but also has integrated MR, CT and optical imaging, along with haptic feedback to the clinician. The haptic feedback or “sense of touch” may enable surgeons to complete procedures in a way never before possible. The SYMBIS Surgical System is designed to be installed in both existing VISIUS Surgical Theatre systems, and in new installations.

We are developing surgical instruments for the SYMBIS that are procedure specific and are designed to enable greater precision and flexibility for the surgeon. We believe that the SYMBIS Surgical System will be applicable for a large number of high volume surgical procedures with the potential to be clinically meaningful and thereby further adoption of the system.

As part of our clinical strategy, we have recently engaged a Medical Advisory Board consisting of key clinical thought leaders in the field of robotics. The advisory board will help define clinical strategy and future products as we develop surgical applications for the SYMBIS Surgical System.

| III. | VISIUS Surgical Theatre and the TrueBeamTMSystem for Radiosurgery |

On October 5, 2010 we announced our agreement with Varian to integrate the capabilities of the VISIUS Surgical Theatre together with the therapy capability of Varian’s TrueBeamTMradiotherapy system. This product has the potential to provide a number of high value capabilities to radiation oncology centres that are hospital based or standalone clinics. This system is designed to provide a radiation oncology centre with the ability to deliver MR guided radiation therapy, MR simulation, and MR guided brachytherapy from a single integrated system. The system consists of three connected rooms that provide radiosurgery, simulation, and brachytherapy all with a common MR imaging platform.

MR simulation is a planning and imaging procedure that is done in conjunction with a patient’s preparation for radiation therapy delivery. Our system allows for a high field MR to be used in a diagnostic simulation suite and then, on demand, be available for use in MR guided radiosurgery, or MR guided brachy therapy. This may provide a significant economic advantage over other means of completing the same procedure.

For MR guided radiation therapy, the patient is located in the radiation therapy bunker and a high field MR moves into the bunker over top of a stationary patient. The MR image is acquired, the MR moves out of the room, and the therapy treatment plan is developed and delivered to the TrueBeamTM radiosurgery system which executes the treatment. The ability to image soft tissue lesions with MR, immediately before the application of radiation therapy may allow for more accurate targeting of the lesion, resulting in a reduction in the radiation delivered to adjacent healthy tissue. This improved targeting may also result in the ability to increase the energy delivered at a treatment session, which may result in fewer treatment sessions for the patient. This new approach to treatment delivery is expected to provide improved patient outcomes versus existing radiosurgery technology systems and have the opportunity to reduce the cost of care.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 5 of 28 |

We believe that the ability to deliver MR guided brachytherapy in a single suite may have compelling advantages over other means of delivering brachytherapy to patients. Brachytherapy is the deposition of high dose radiation seeds into target tissue for the delivery of radiation. It requires the ability to image, target, and deliver the seeds with precision and confidence. Our system is designed to enhance the workflow and provide improved procedural outcomes. This product is currently under development with regulatory clearance anticipated in mid-2014.

Technology and Product Development

Underlying all of our image guided therapy solutions is advanced proprietary technology and intellectual property that we have developed as part of our unique solutions. The protection of these products, our processes and know-how is integral to our business. We currently have 52 patents either issued or pending. As we develop our technologies, we will continue to seek patent protection to contribute to our competitive advantage. We have patents in place in the United States, Canada and other countries, where available, to protect our core patent family and we have filed a number of additional patent applications that are directed to specific aspects of our technology.

Innovation and the creation of high value novel products is a cornerstone of IMRIS’s development activities. To grow the Company and remain competitive, we are continuously engaged in new product development and enhancement and each year we invest significantly in research and development to drive continuing innovations that support our competitive position.

As we move forward our product development efforts will be focused on enhancing the capabilities of the VISIUS Surgical Theatre so that we are increasing the number and quantity of traditional procedures that can be completed in our theatres. Following commercialization of our products that combine robotics and radiosurgery with the VISIUS Surgical Theatre, we expect to continue to expand the capabilities of these systems to continue to grow their value proposition.

Regulatory

IMRIS is a global company serving global markets. We have registered our core MR VISIUS Surgical Theatre in the United States, Canada, European Union, Australia, Japan, China, Singapore and South Korea. We continue to maintain our facility and product registrations to serve these globalmarkets. We successfully completed re-certification to ISO-13485 in September 2012, and certified our new Minnetonka, Minnesota facility in August 2013, which is a requirement for many of our global markets. During this period, IMRIS cleared the industry’s first MRI wireless coil and ceiling-mounted iCT system.

IMRIS maintains a proven network of global regulatory partners and will seek product registrations based on market demand and product launch strategy as the new products and technologies are developed.

Market and Sales Cycle

Wesell our VISIUS Surgical Theatres globally to hospitals that deliver clinical services to patients in the neurosurgical, spinal, cerebrovascular and cardiovascular markets. We believe that the primary market for our iMRI product portfolio is comprised of those hospitals having relatively large neurosurgical, cerebrovascular or cardiovascular practices. The VISIUS iCT serves this group as well, but extends into orthopedic and neurosurgical spine practices in hospitals and surgery centers alike. Clinical appreciation for the benefits of VISIUS Surgical Theatres for neurosurgical and orthopedic applications is growing supported by repeat purchases from hospitals and market penetration within regions in which our product is being sold.

We have a direct sales force in theUnited States, Canada, China, Singapore, Japan and Europe, excluding Italy and Eastern European countries. Our recent investment in sales management in Singapore during 2013 is the result of the market opportunities we foresee in the Asia Pacific region. In all other markets where we have a presence, we utilize distributors.

Our sales force is focusing its efforts on hospitals with the greatest ability to benefit from neurosurgical and spinal applications. They are aggressively working our sales pipeline and we are increasing our marketing efforts. As a result, we expect that market interest will develop for new applications of the product and the new products being developed, which can be utilized within our Theatres.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 6 of 28 |

The purchase and installation of a VISIUS Surgical Theatre for traditional surgical procedures represents a significant capital project for our customers that can range in price from approximately $1.5 million to $12 million depending on the product solution, the configuration of the VISIUS Surgical Theatre layout and system options selected. In addition to the capital equipment sale, most of our customers enter into equipment service contracts that are generally 4-5 years in duration. These contracts begin after the typical one-year warranty period and are on average equal to approximately 5 percent of the original equipment purchase price per year in revenues. In addition to our equipment and services, customers may require further capital expenditures for construction and ancillary equipment. The sales cycle for our VISIUS Surgical Theatres is both complex and lengthy and can be more than 12 months from initial customer engagement to receipt of a purchase order, though we expect we can significantly shorten the sales cycle with the introduction of the iCT system.

Following the receipt of a customer purchase order, the delivery and installation cycle for one of our VISIUS Surgical Theatres typically ranges from 8 months to 18 months or more the larger scale iMRI products depending on the configuration of our system and the amount of additional construction work that may be required to be completed by the customer. The VISIUS Surgical Theatre using CT installation cycles are expected to be significantly shorter ranging from as little as 3 months to 9 months depending on the availability of the customer site. We invoice customers for a VISIUS Surgical Theatre in installments spread over a number of milestones, which typically include a deposit at the time of order and a percentage of the remaining total price upon delivery of the equipment, completion of installation and final acceptance. Due to the project nature of our VISIUS Surgical Theatre sales, we recognize revenues and related cost of sales on a percentage-of-completion basis as the VISIUS Surgical Theatre is installed.

As our newer products are commercialized, we believe we can leverage our significant customer relationships to accelerate new product introductions. Moreover, our VISIUS Surgical Theatres equipped with the SYMBIS Surgical System are being designed to have shorter installation timeframes. These factors together are expected to result in significantly shorter sales and installation cycles for our Company.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 7 of 28 |

Overall Performance

Highlights from the third quarter of 2013 include:

| · | Quarterly revenues were $17.8 million, an increase of 54 percent over the prior year; |

| · | Net loss in the third quarter improved to $3.8 million, or $0.07 per diluted share, compared with a prior-year net loss of $8.5 million, or $0.19 per diluted share; |

| · | Quarterly gross margins of 38.2 percent of sales, a 14.4 percent of sales improvement from the prior year; |

| · | New order bookings of $14.5 million resulted in an ending backlog of $101.4 million; |

| · | Entered into a secured loan facility agreement for $25 million with Deerfield Management Company L.P., a healthcare investment firm with $3.5 billion of assets under management; |

| · | Established a new agreement in October 2013 with Siemens Healthcare to incorporate Siemens CT technology into the VISIUS technology platform; |

| · | The spinal surgery team at Duke University Medical Center in Durham, NC, completed the first surgical cases using VISIUS iCT in October 2013. |

SUMMARY OF SELECTED FINANCIAL INFORMATION

Quarterly Results

The following table sets forth selected financial information for the dates and periods indicated:

Selected Financial Information

(Thousands of US dollars, except per share amounts)

(Unaudited)

| | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Sales | | $ | 17,765 | | | $ | 11,569 | | | | 53.6 | % | | $ | 36,057 | | | $ | 32,297 | | | | 11.6 | % |

| Gross profit | | $ | 6,781 | | | $ | 2,751 | | | | 146.5 | % | | $ | 12,910 | | | $ | 10,803 | | | | 19.5 | % |

| Gross profit % | | | 38.2 | % | | | 23.8 | % | | | | | | | 35.8 | % | | | 33.4 | % | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Operating expenses | | $ | 10,771 | | | $ | 11,341 | | | | -5.0 | % | | $ | 32,381 | | | $ | 32,011 | | | | 1.2 | % |

| Operating loss | | $ | (3,990 | ) | | $ | (8,590 | ) | | | -53.6 | % | | $ | (19,471 | ) | | $ | (21,208 | ) | | | -8.2 | % |

| | | | | | | | | | | | | | | | | | | | 18 | | | | | |

| Income taxes | | $ | 6 | | | $ | 48 | | | | -87.5 | % | | $ | 32 | | | $ | 66 | | | | -51.5 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net loss | | $ | (3,804 | ) | | $ | (8,520 | ) | | | -55.4 | % | | $ | (20,385 | ) | | $ | (21,152 | ) | | | -3.6 | % |

| Basic and diluted loss per share | | $ | (0.07 | ) | | $ | (0.19 | ) | | | -63.2 | % | | $ | (0.41 | ) | | $ | (0.46 | ) | | | -10.9 | % |

| Balance Sheet Data | | As of

September 30,

2013 | | | As of

December 31,

2012 | |

| | | | | | | |

| Cash and restricted cash | | $ | 28,399 | | | $ | 20,980 | |

| Total assets | | | 106,122 | | | | 81,985 | |

| Deferred revenue | | | 10,174 | | | | 10,182 | |

| Total liabilities | | | 50,341 | | | | 31,398 | |

| Shareholders' equity | | | 55,781 | | | | 50,587 | |

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 8 of 28 |

Revenues

Revenues by sales classification

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| VISIUS Surgical Theatres | | $ | 15,017 | | | $ | 10,247 | | | | 46.6 | % | | $ | 29,327 | | | $ | 28,742 | | | | 2.0 | % |

| Extended maintenance contracts | | | 2,748 | | | | 1,322 | | | | 107.9 | % | | | 6,730 | | | | 3,555 | | | | 89.3 | % |

| Total revenues | | $ | 17,765 | | | $ | 11,569 | | | | 53.6 | % | | $ | 36,057 | | | $ | 32,297 | | | | 11.6 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| VISIUS Surgical Theatres as a percentage of total revenues | | | 84.5 | % | | | 88.6 | % | | | | | | | 81.3 | % | | | 89.0 | % | | | | |

| Extended maintenance contracts as a percentage of total revenues | | | 15.5 | % | | | 11.4 | % | | | | | | | 18.7 | % | | | 11.0 | % | | | | |

Revenues by region

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| North America | | $ | 10,386 | | | $ | 7,939 | | | | 30.8 | % | | $ | 19,621 | | | $ | 23,270 | | | | -15.7 | % |

| Europe and Middle East | | | 6,681 | | | | 65 | | | | 10178.5 | % | | | 10,308 | | | | 306 | | | | 3268.6 | % |

| Asia Pacfic | | | 698 | | | | 3,565 | | | | -80.4 | % | | | 6,128 | | | | 8,721 | | | | -29.7 | % |

| | | $ | 17,765 | | | $ | 11,569 | | | | 53.6 | % | | $ | 36,057 | | | $ | 32,297 | | | | 11.6 | % |

Revenue for the three months ended September 30, 2013 increased $6.2 million or 54 percent, compared with the same period last year. Revenue from VISIUS Surgical Theaters was $4.8 million higher during the three months ended September 30, 2013 compared with the same period in last year due to an increase in scheduled major system component deliveries and a favorable increase in the average sales price per project. Extended maintenance contract revenue was $1.4 million higher during the three months ended September 30, 2013 compared with the same period last year due to additional extended maintenance contracts as a result of a higher installation base of VISIUS Surgical Theatres which have transitioned off warranty to chargeable service programs.

Revenue for the nine months ended September 30, 2013 increased $3.8 million, compared with the same period last year. Revenue from VISIUS Surgical Theaters was $0.6 million higher during the nine months ended September 30, 2013 compared with the same period in last year due to higher average sales prices per project in 2013 partially offset by increased project activity in 2012 that were at varying stages of installation activity that generated lower project revenues. Extended maintenance contract revenue was $3.2 million higher during the nine months ended September 30, 2013 compared with the same period last year due to additional extended maintenance contracts as a result of a higher installation base of VISIUS Surgical Theatres which have transitioned off warranty to chargeable service programs.

Revenues from the North America region for the three months ended September 30, 2013 increased compared with the same period last year due to increased VISIUS Surgical Theatre equipment component deliveries, as well as higher extended maintenance revenue, all primarily in the United States. Revenues from the Europe and Middle East region for the three months ended September 30, 2013 increased compared with the same period last year primarily due to significant imaging equipment deliveries in the Middle East. Revenues from the Asia Pacific region decreased compared to the same period last year due to limited project activity in 2013, compared to 2012 which had one large component equipment delivery in Japan and two project installations in China.

Revenues from the North America region for the nine months ended September 30, 2013 decreased compared with the same period last year due to decreased product deliveries, partially offset by higher extended maintenance revenue, particularly in the United States. Revenues from the Europe and Middle East region for the nine months ended September 30, 2013 increased compared with the same period last year due to a large project installation in the Middle East. Revenues from the Asia Pacific region decreased compared to the same period last year, primarily as a result of more delivery and installation activity in 2012.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 9 of 28 |

Gross Profit

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Gross profit | | $ | 6,781 | | | $ | 2,751 | | | | 146.5 | % | | $ | 12,910 | | | $ | 10,803 | | | | 19.5 | % |

| As a percentage of sales | | | 38.2 | % | | | 23.8 | % | | | | | | | 35.8 | % | | | 33.4 | % | | | | |

Gross profit for the three months ended September 30, 2013 increased $4.0 million compared with the same period last year primarily due to additional scheduled equipment deliveries, significantly improved project margins, and increased gross profit earned on additional extended maintenance contracts.

Gross profit as a percentage of sales was 38.2 percent for the three months ended September 30, 2013 compared with 23.8 percent in the same period last year. Gross profit as a percentage of sales from VISIUS Surgical Theatres was 37.1 percent for the three months ended September 30, 2013 compared to 22.3 percent in the same period last year. Gross profit as a percentage of sales increased due to a significantly more favorable project margin profile compared with the same period last year which included a low margin project for the Company’s first installation in Japan. Extended maintenance contract gross profit as a percentage of sales for the three months ended September 30, 2013 was 61.2 percent compared to 52.9 percent in the same period last year as a result of an improved service experience on the installed customer base in the period.

Gross profit for the nine months ended September 30, 2013 increased $2.1 million, compared with the same period last year due to increased gross profit earned on additional extended maintenance contracts that commenced in 2013 and a reduction of warranty costs from the prior year period.

Gross profit as a percentage of sales was 35.8 percent for the nine months ended September 30, 2013, up from 33.4 percent during the same period last year. Gross profit as a percentage of sales from VISIUS Surgical Theatres was 34.9 percent for the nine months ended September 30, 2013 compared to 35.5 percent in the same period last year. The decrease was primarily due to unanticipated cost overruns in 2013 for certain research programs. Gross profit as a percentage of sales from extended maintenance contracts for the nine months ended September 30, 2013 was 53.0 percent compared with 50.8 percent the same period last year as a result of improved service experience on the installed customer base in the period.

Operating Expenses

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Operating expenses | | $ | 10,771 | | | $ | 11,341 | | | | -5.0 | % | | $ | 32,381 | | | $ | 32,011 | | | | 1.2 | % |

Operating expenses for the three months ended September 30, 2013 were $10.8 million, a decrease of $0.6 million or 5.0 percent compared with the same period last year. The decrease in operating expenses is primarily due to lower research and development costs of $2.0 million for robotics, MRgRT and other ancillary research projects as these are nearing completion. These reductions were partially offset by one-time costs related to the relocation of the Company’s operations to Minnesota of $0.8 million, additional rent and utilities expense of $0.4 million at the new facility in Minnesota and higher employee-related costs of $0.3 million.

Operating expenses for the nine months ended September 30, 2013 were $32.4 million, an increase of $0.4 million compared with the same period last year. The increase is primarily due to additional one-time costs related to the relocation of the Company’ operations to Minnesota of $2.3 million, additional employee related costs of $2.2 million, and additional rent and utilities expense of $0.7 million at the new facility in Minnesota, partially offset by lower research and development costs of $5.0 million related to robotics, MR-guided radiation therapy and other ancillary research programs as those projects near completion, along with lower amortization of $0.2 million due to assets becoming fully depreciated. The relocation costs consist of recruiting of $0.9 million, retention and severance costs of $0.2 million, other employee benefits of $0.3 million, business and travel fees and other expenses of $0.3 million, professional services of $0.2 million, and other expenses of $0.4 million.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 10 of 28 |

Administrative

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Administrative | | $ | 2,280 | | | $ | 2,000 | | | | 14.0 | % | | $ | 7,523 | | | $ | 5,560 | | | | 35.0 | % |

Administrative expense for the three months ended September 30, 2013 increased $0.3 million compared with the same period last year, including $0.1 million of relocation costs. The remainder of the increase is primarily related to additional rent and utilities expenses of $0.3 million mostly related to the additional facility in Minnesota, partially offset by lower business travel of $0.1 million. The relocation costs consist primarily of recruiting and staff retention and severance.

Administrative expense for the nine months ended September 30, 2013 increased $2.0 million compared with the same period last year, including $0.7 million of costs related to the relocation. The relocation costs consist of professional services fees and other expenses of $0.2 million, recruiting expenses of $0.3 million, staff retention and severance costs of $0.1 million, and other expenses of $0.1 million. The remainder of the increase is primarily related to additional rent and utilities expenses of $0.6 million mostly related to the additional facility in Minnesota, additional professional fees of $0.2 million, and additional salaries, benefits and stock option expense of $0.6 million, partially offset by lower business travel of $0.1 million. The increased salaries, benefits and stock option expense of $0.6 million are due primarily to the addition of the Company’s Chief Operating Officer and other new hires.

Sales and marketing

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Sales and marketing | | $ | 2,300 | | | $ | 2,427 | | | | -5.2 | % | | $ | 7,081 | | | $ | 7,014 | | | | 1.0 | % |

Sales and marketing expense for the three months ended September 30, 2013 decreased $0.1 million compared with the same period last year. Commissions expense increased $0.3 million due to the timing of equipment deliveries and installation activities, offset by lower recruiting expense of $0.2 million as a result of lower hiring activity in 2013.

Sales and marketing expense for the nine months ended September 30, 2013 was consistent compared with the same period last year. Staff related expenses increased $0.5 million due to higher commissions expense as a result of the timing of equipment deliveries and installation activities, and higher salaries and employee benefits due to additional headcount. These costs were offset by lower recruiting expense of $0.2 million as a result of lower hiring activity in 2013 and lower professional services of $0.3 million.

Customer support and operations

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Customer support and operations | | $ | 2,889 | | | $ | 2,007 | | | | 43.9 | % | | $ | 8,309 | | | $ | 5,584 | | | | 48.8 | % |

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 11 of 28 |

Customer support and operations expense for the three months ended September 30, 2013 increased $0.9 million compared with the same period last year, including relocation related costs of $0.2 million. The remainder of the increase is primarily related to increased headcount within customer support including the appointment of two senior executives in Operations and Customer Service, resulting in higher salaries and benefits and stock option expense of $0.3 million, as well as due to higher rent and utilities expense of $0.2 million related to the additional facility in Minnesota, along with other expenses of $0.2 million. The relocation related costs consist primarily of recruiting expenses of $0.1 million other expenses of $0.1 million.

Customer support and operations expense for the nine months ended September 30, 2013 increased $2.7 million compared with the same period last year, including relocation related costs of $0.8 million. The remainder of the increase is primarily related to increased headcount within customer support including the appointment of two senior executives in Operations and Customer Service, resulting in higher salaries and benefits and stock option expense of $1.2 million, as well as due to higher rent and utilities expense of $0.4 million related to the additional facility in Minnesota and travel and other costs of $0.3 million. The relocation related costs consist of recruiting expenses of $0.3 million and staff retention and severance expenses of $0.2 million and other expenses of $0.3 million.

Research and development

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Research and development | | $ | 2,339 | | | $ | 3,840 | | | | -39.1 | % | | $ | 6,612 | | | $ | 10,827 | | | | -38.9 | % |

Research and development expense for the three months ended September 30, 2013 decreased $1.5 million compared with the same period last year. The decrease is primarily related to reduced spending on technical development associated with image-guided surgical robotics, MR guided radiation therapy development, and other ongoing development programs as those project near completion and lower equipment maintenance costs as a result of periodic repairs to capital. This was partially offset by higher relocation related costs of $0.5 million, consisting of recruiting costs of $0.2 million, business travel of $0.2 million, and $0.1 million of other expenses.

Research and development expense for the nine months ended September 30, 2013 decreased $4.2 million compared with the same period last year. The decrease is primarily related to reduced spending on technical development associated with image-guided surgical robotics, MR guided radiation therapy development, and other ongoing development programs, as well as lower equipment maintenance costs as a result of periodic repairs to capital equipment. This decrease was partially offset by higher relocation related costs of $0.8 million, consisting of staff recruiting costs of $0.4 million, business travel expenses of $0.2 million, legal costs of $0.1 million, and other expenses of $0.1 million.

Amortization

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Amortization | | $ | 963 | | | $ | 1,067 | | | | -9.7 | % | | $ | 2,856 | | | $ | 3,026 | | | | -5.6 | % |

Amortization expense for the three and nine months ended September 30, 2013, respectively, decreased due to certain assets becoming fully depreciated.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 12 of 28 |

Foreign exchange

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Foreign exchange income/(loss) | | $ | 387 | | | $ | 118 | | | | 228.0 | % | | $ | (651 | ) | | $ | 107 | | | | -708.4 | % |

Foreign exchange income/(loss) for the three and nine month periods ended September 30, 2013 increased $0.3 million and decreased $0.8 million respectively resulting in income of $0.4 million and loss of $0.7 million for the three and nine month periods of 2013, respectively, compared with the same periods last year. The change for the three and nine month periods ended September 30, 2013 is due to a weakening and strengthening of the U.S. dollar against the Company’s higher net foreign denominated monetary assets compared to the same period in 2012, which resulted in income and loss, respectively, on revaluation.

Interest and other

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Interest and other (expense)/income | | $ | (195 | ) | | $ | - | | | | nm | | | $ | (231 | ) | | $ | 15 | | | | nm | |

nm – Not meaningful

Interest and other (expense)/income consists primarily of interest expense on outstanding debt, amortization of the related deferred debt acquisition costs, warrant discount amortization, and other interest income and expense and bank fees. On September 16, 2013, Imris entered into a secured loan facility agreement for $25 million, and received net proceeds of $24.5 million following execution of the agreement. The outstanding principal amount of the loan at any time will accrue interest at a rate of 9 percent per annum. In connection with the loan, the lender received warrants to purchase 6.1 million shares of IMRIS common stock at an exercise price of $1.94 per share.

Interest and other (expense)/income for the three and nine months ended September 30, 2013 includes interest expense of $88 thousand, debt discount amortization of $49 thousand, and debt issuance cost amortization of $17 thousand. The remainder is other net interest income/expense and banking fees. Interest expense, warrant discount amortization, and debt issuance cost amortization are recognized on an effective interest rate method over 5 years.

Income taxes

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Income taxes | | $ | 6 | | | $ | 48 | | | | -87.5 | % | | $ | 32 | | | $ | 66 | | | | -51.5 | % |

The Company generates taxable income in several of its foreign subsidiaries due to transfer pricing policies used in those foreign jurisdictions. As a result of activities in these foreign subsidiaries, the Company has recognized tax expense during the three and nine month periods ended September 30, 2013. The change in income tax expense compared with the same periods last year is primarily due to changes in taxable income in those foreign jurisdictions.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 13 of 28 |

Operating Loss and Net Loss

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Operating Loss | | $ | (3,990 | ) | | $ | (8,590 | ) | | | -53.6 | % | | $ | (19,471 | ) | | $ | (21,208 | ) | | | -8.2 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Net loss | | $ | (3,804 | ) | | $ | (8,520 | ) | | | -55.4 | % | | $ | (20,385 | ) | | $ | (21,152 | ) | | | -3.6 | % |

Operating loss for the three months ended September 30, 2013 decreased $4.6 million compared with the same period last year. The decrease in the operating loss is primarily due to higher gross profit of $4.0 million and lower operating expenses of $0.6 million, offset by one-time relocation costs of $0.8 million. The relocation costs were recorded within the affected functional area, including administrative ($0.1 million), customer support and operations ($0.2 million) and research and development ($0.5 million). Additional rent and utilities expense and employee related costs in administration and customer support and operations was largely offset by lower research and development cost of $1.5 million, each as described above.

Operating loss for the nine months ended September 30, 2013 decreased $1.7 million compared with the same period last year. The decrease in the operating loss is primarily due to higher gross profit of $2.1 million partially offset by higher operating expenses of $0.4 million, including one-time relocation costs of $2.3 million. The relocation costs were recorded within the affected functional area, including administrative ($0.7 million), customer support and operations ($0.8 million) and research and development ($0.8 million). Additional employee related costs in administration and customer support and operations was largely offset by lower research and development cost of $4.2 million, each as described above.

Net loss for the three months ended September 30, 2013 decreased $4.7 million compared with the same period last year. The decrease in net loss was primarily due to higher gross profit of $4.0 million, lower operating expenses of $0.6 million, and higher foreign exchange income of $0.3 million, partially offset by higher interest expense of $0.2 million. Changes in gross profit and foreign exchange were the result of factors noted above.

Net loss for the nine months ended September 30, 2013 decreased $0.8 million compared with the same period last year. The decrease in net loss was primarily due to higher gross profit of $2.1 million, partially offset by higher operating expenses of $0.4 million, higher foreign exchange loss of $0.8 million during the period and higher interest expense of $0.2 million. Changes in gross profit, operating expenses and foreign exchange were the result of factors noted above.

Adjusted EBITDA

| (Thousands of US dollars) | | Three months ended | | | | | | Nine months ended | | | | |

| | | September 30 | | | % | | | September 30 | | | % | |

| | | 2013 | | | 2012 | | | Change | | | 2013 | | | 2012 | | | Change | |

| | | | | | | | | | | | | | | | | | | |

| Adjusted EBITDA | | $ | (2,535 | ) | | $ | (7,128 | ) | | | -64.4 | % | | $ | (15,167 | ) | | $ | (17,078 | ) | | | -11.2 | % |

The Company uses the non-GAAP measure Adjusted EBITDA to measure aspects of our financial performance (see “Non-GAAP Financial Measures” for a reconciliation of adjusted EBITDA to GAAP measures). The Company defines Adjusted EBITDA as earnings (loss) before stock based compensation, interest income (expense) and other, foreign exchange gain (loss), embedded derivatives gain (loss), income taxes and amortization.

Adjusted EBITDA for the three months ended September 30, 2013 was negative $2.5 million, compared with negative $7.1 million for the same period last year. Adjusted EBITDA for the 2013 third quarter reflects higher gross profit of $4.0 million, lower operating expenses of $0.6 million, higher foreign exchange income of $0.3 million, and higher interest expense of $0.2 million.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 14 of 28 |

Adjusted EBITDA for the nine months ended September 30, 2013 was negative $15.2 million, compared with negative $17.1 million for the same period last year. The decrease in negative Adjusted EBITDA stemmed primarily from higher gross profit of $2.1 million, partially offset by higher operating expenses of $0.4 million.

SUMMARY OF QUARTERLY RESULTS

The following table is a summary of our financial results for the past eight quarters:

| (Thousands of US dollars) | | Q3 | | | Q2 | | | Q1 | | | Q4 | | | Q3 | | | Q2 | | | Q1 | | | Q4 | |

| | | 2013 | | | 2013 | | | 2013 | | | 2102 | | | 2012 | | | 2012 | | | 2012 | | | 2011 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | $ | 17,765 | | | $ | 10,226 | | | $ | 8,066 | | | $ | 20,095 | | | $ | 11,569 | | | $ | 17,235 | | | $ | 3,493 | | | $ | 14,677 | |

| Cost of sales | | | 10,984 | | | | 7,117 | | | | 5,046 | | | | 13,100 | | | | 8,818 | | | | 10,577 | | | | 2,099 | | | | 9,855 | |

| Gross profit | | | 6,781 | | | | 3,109 | | | | 3,020 | | | | 6,995 | | | | 2,751 | | | | 6,658 | | | | 1,394 | | | | 4,822 | |

| As a percentage of sales | | | 38.2 | % | | | 30.4 | % | | | 37.4 | % | | | 34.8 | % | | | 23.8 | % | | | 38.6 | % | | | 39.9 | % | | | 32.9 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Operating expenses | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Administration | | | 2,280 | | | | 2,833 | | | | 2,410 | | | | 2,664 | | | | 2,000 | | | | 1,887 | | | | 1,673 | | | | 2,037 | |

| Sales and marketing | | | 2,300 | | | | 2,522 | | | | 2,259 | | | | 2,785 | | | | 2,427 | | | | 2,536 | | | | 2,051 | | | | 2,941 | |

| Customer support and operations | | | 2,889 | | | | 2,984 | | | | 2,436 | | | | 3,062 | | | | 2,007 | | | | 1,907 | | | | 1,670 | | | | 1,805 | |

| Research and development | | | 2,339 | | | | 1,534 | | | | 2,739 | | | | 3,729 | | | | 3,840 | | | | 3,411 | | | | 3,576 | | | | 2,433 | |

| Amortization | | | 963 | | | | 943 | | | | 950 | | | | 1,071 | | | | 1,067 | | | | 990 | | | | 969 | | | | 908 | |

| | | | 10,771 | | | | 10,816 | | | | 10,794 | | | | 13,311 | | | | 11,341 | | | | 10,731 | | | | 9,939 | | | | 10,124 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Operating loss before the following: | | | (3,990 | ) | | | (7,707 | ) | | | (7,774 | ) | | | (6,316 | ) | | | (8,590 | ) | | | (4,073 | ) | | | (8,545 | ) | | | (5,302 | ) |

| Foreign exchange | | | 387 | | | | (483 | ) | | | (555 | ) | | | (232 | ) | | | 118 | | | | (207 | ) | | | 196 | | | | 710 | |

| Interest | | | (195 | ) | | | (3 | ) | | | (33 | ) | | | (55 | ) | | | - | | | | (2 | ) | | | 17 | | | | (1 | ) |

| Gain on sale of asset disposal | | | | | | | - | | | | - | | | | 19 | | | | | | | | | | | | | | | | | |

| Loss before taxes | | $ | (3,798 | ) | | $ | (8,193 | ) | | $ | (8,362 | ) | | $ | (6,584 | ) | | $ | (8,472 | ) | | $ | (4,282 | ) | | $ | (8,332 | ) | | $ | (4,593 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Income taxes | | | 6 | | | | 10 | | | | 16 | | | | 20 | | | | 48 | | | | - | | | | 18 | | | | 366 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Net loss for the quarter | | $ | (3,804 | ) | | $ | (8,203 | ) | | $ | (8,378 | ) | | $ | (6,604 | ) | | $ | (8,520 | ) | | $ | (4,282 | ) | | $ | (8,350 | ) | | $ | (4,959 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Loss per share | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Basic | | $ | (0.07 | ) | | $ | (0.16 | ) | | $ | (0.18 | ) | | $ | (0.14 | ) | | $ | (0.19 | ) | | $ | (0.09 | ) | | $ | (0.18 | ) | | $ | (0.11 | ) |

| Diluted | | $ | (0.07 | ) | | $ | (0.16 | ) | | $ | (0.18 | ) | | $ | (0.14 | ) | | $ | (0.19 | ) | | $ | (0.09 | ) | | $ | (0.18 | ) | | $ | (0.11 | ) |

The financial results for the eight most recent quarters reflect the progression of an early stage Company with a limited operating history. Factors that have caused our results to vary are described below.

| Ø | As a result of the limited number of VISIUS Surgical Theatres sold and installed to date and the high dollar value associated with each sale, our revenues recorded from quarter to quarter have varied depending on the number and stage of active projects in any given quarter. |

| Ø | Gross margins for the VISIUS Surgical Theatre are largely dependent on whether a particular product application has achieved acceptance amongst clinical thought leaders. Given the maturity and clinical data surrounding the neurosurgical application of the VISIUS Surgical Theatre, margins for these products have generally been stronger than other newer clinical applications. |

| Ø | The decrease in gross profit percentage in the latter stages of 2011 is primarily tied to market penetration pricing for the introduction of the VISIUS Surgical Theatre for cerebrovascular and cardiovascular applications, as well as the provision of certain equipment for research purposes to a third party customer. The decrease in gross margins in 2012 is mainly due to higher installation costs with third quarter margins being further impacted by the provision of certain equipment for research purposes and lower margins for the Company’s first customer installation in Japan. Margins in Q2 2013 were lower than anticipated due to cost overruns for certain research installations for the MR guided radiation therapy pre-clinical site as well as the initial iCT installations and the Company’s first commercial version of its MR compatible surgical robot. |

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 15 of 28 |

| Ø | Net losses generally vary depending on the timing of when specific projects were installed and the pricing associated with the respective projects. Net losses in 2013, 2012 and 2011 have largely been the result of lower product installations and planned increases in research and development activity for the Company’s MR guided radiation therapy program and the image-guided robotics program. |

| Ø | Operating expenses began to increase in 2011 because of planned research and development activities for robotics, MR-guided radiation therapy and other ancillary research projects, increased employee costs, and professional fees as a result of additional reporting requirements as a NASDAQ registrant. Operating expenses during the first part of 2012, in areas outside of research and development, are lower as a result of cost management measures undertaken by management. Increases in the second half of 2012 and the first half of 2013 reflect additional efforts to recruit qualified personnel and severance as well as retention costs recorded in the fourth quarter of 2012 and the first three quarters of 2013 related to the relocation of operations from Winnipeg, Canada to Minnesota, U.S.A. |

| Ø | Although the majority of the Company’s sales are denominated in U.S. dollars, the Company sells its VISIUS Surgical Theatres in a variety of foreign currencies. As well, a significant portion of the Company’s operating costs are in Canadian dollars. This gives rise to foreign exchange gains or losses each quarter depending on the change in value of the U.S. dollar versus the Canadian dollar and other currencies in each quarter. |

| Ø | The Company generated taxable income in several of its foreign subsidiaries in 2013, 2012 and 2011 because of our transfer pricing methodology. As a result, the Company began recognizing tax expense in the 4th quarter of 2011 related to these subsidiaries. |

Backlog

In the third quarter of 2013, total order bookings were $14.5 million, consisting of product bookings totaling $8.1 million and new service contracts of $6.4 million. We converted $17.8 million of backlog into revenues and changes due to foreign exchange were insignificant in the period. We evaluate our backlog and individual order conversion on a regular basis and our experience is that orders typically convert into revenues over 12 to 18 months but can often vary depending on customer site conditions. As a result of certain budget constraints with two separate customers, one customer converted their order from a full integrated offering to a multi-source project and one customer has cancelled their existing service contract. The net result to our existing backlog was a reduction of $6.3 million; $5.2 million reduction for the change to a multi-source project and $1.1 million for the cancellation of the remaining four years of a five year service contract.

The table below provides the Company’s backlog on a segmented basis, as of September 30, 2013 and its comparable periods for each of the last three years as of December 31:

| | | December 31, | | | March 31, | | | June 30, | | | September 30, | |

| | | 2010 | | | 2011 | | | 2012 | | | 2013 | | | 2013 | | | 2013 | |

| VISIUS Surgical Theatres | | $ | 86,505 | | | $ | 58,583 | | | $ | 69,213 | | | $ | 63,141 | | | $ | 59,278 | | | $ | 47,172 | |

| Service contracts | | | 30,619 | | | | 36,430 | | | | 53,326 | | | | 52,337 | | | | 51,720 | | | | 54,227 | |

| Total backlog | | $ | 117,124 | | | $ | 95,013 | | | $ | 122,539 | | | $ | 115,478 | | | $ | 110,998 | | | $ | 101,399 | |

As of September 30, 2013, we have sold 60 systems, of which 46 are installed and 14 are in the delivery phase. Of those sold, 39 are in the United States, 7 are in Canada, 10 are in Asia Pacific and 4 are in Europe and the Middle East.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 16 of 28 |

We use the non-GAAP measure “backlog” to measure aspects of our financial performance. Backlog is defined as the unrecognized portion of (i) revenues anticipated to be recorded from VISIUS Surgical Theatre orders, including confirmed orders and orders subject to the completion of formal documentation and (ii) service contracts with a term of four to five years and which commence at the conclusion of the warranty period on our VISIUS Surgical Theatres. The term of our service contracts generally ranges from 4 to 5 years commencing at the conclusion of the warranty period on our VISIUS Surgical Theatres, which are typically 1 year in length. Service contract revenue is recognized ratably over the term of the contract.

OUTLOOK

We are very encouraged that the VISIUS Surgical Theatre is gaining clinical traction and generating a lot of interest in the marketplace When we assess the opportunity today for our existing products, we continue to have a significant number of customers that remain actively engaged with us that are in the mid-to-later stages of the order process but the procurement cycle has lengthened in a number of cases due to the cost to acquire the system. In response to this particular circumstance, we launched a multi-source delivery approach, where a customer can directly procure certain components of our iMRI system from our original equipment manufacturing partners. This approach can enable a customer to purchase our base model iMRI system for under $3 million in some cases. We have begun to evaluate this new model with customers who had delayed their purchasing process due to the cost of our system, and found the approach is gaining traction, including one instance where we recently implemented this model for an existing customer. We continue to grow our sales funnel, particularly with the recent approval of the iCT, and while not all of these customers move to purchase order we believe that most will convert over time.

In looking forward from a regional perspective, we anticipate that North America will continue to be the strongest contributor to overall bookings performance, with approximately half of all system bookings coming from this region. We are also well positioned in China and have a solid position from which to continue to expand our installed base. Asia Pacific, and specifically Japan, is also an area of focus for our company. We believe that the Japanese market potential is substantial and with our second order in the most recent quarter we are positioning ourselves to better serve that market. In Europe and the Middle East we will be focused on advancing a select number of opportunities this year. While the market is not robust across all of Europe, there are many centers that are proceeding with the procurement of systems, and we intend to ensure we are positioned to take advantage of those opportunities.

New Product Development

We received FDA regulatory clearance in July 2013 for our VISIUS Surgical Theatre equipped with a ceiling mounted CT scanner, and got the CE Mark for the European Union in August 2013. This product addresses the demand for radiological quality imaging during spinal and other procedures and we believe that the combination of enhanced work flow, ceiling mounted technology and radiological quality imaging will be a compelling value for many centers.

Completion of our MR Guided Radiation Therapy system is scheduled for 2014 as part of our collaboration with Varian Medical. This innovative new product is designed to deliver MR guided radiation therapy, MR simulation, and MR guided brachytherapy from a single integrated system. We believe that our MR guided brachy therapy solution has the ability to improve workflow and also reduce the cost of care. The MR Guided radiotherapy portion of the system is expected to be completed in the third quarter and soon after begin acceptance testing with the goal of completion by the end of the year coinciding with the expected completion of the pre-clinical MR guided radiation therapy project at Princess Margaret Hospital in Toronto Canada.

Our third major product development initiative is the SYMBIS Surgical System — the world's first MR compatible surgical robot. Version 1 of the system is has been in clinical use as part of a single site clinical trial and has provided highly valuable experience in the development of our first commercial version of the product. This fall, we expect to commence production of this second generation in our facility in Minnetonka for delivery to clinical sites for a multi-user study necessary to obtain regulatory approval. We continue to work with the FDA to address the study requirements including end points and patient volumes required. We have established a Medical Advisory Board, recruiting key thought leaders in surgical robotics to utilize their experience in directing and designing the study, and collaborating on future developments product applications. We expect we will be able conclude our discussions with the FDA in late 2013 or early 2014 where we can determine the scope and size of the additional patient data that will satisfy the needs of the evaluators and provide us with clarity and a timeline to completion.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 17 of 28 |

Financial Outlook

Revenues

Our ability to complete installations and recognize revenue on a timely basis is directly influenced by the circumstances of each hospital and schedules can shift because of unique customer specific requirements. The delivery cycle and installation process for a VISIUS Surgical Theatre is lengthy and installation times can be further lengthened depending on additional site-specific construction work that may be required to be completed by the customer.

Given the delay in expected customer bookings, including the later than anticipated approval of the iCT by the FDA, and construction delays in certain customer sites, 2013 revenues are expected to be in the range of $47 million to $49 million and include revenues from the conversion of both system and service backlog. Included in this forecast are revenues associated with three new VISIUS Surgical Theatre equipped with a ceiling mounted CT.

IMRIS’s quarterly revenue profile varies depending on the underlying system installations in each period. We anticipate that Q4 2013 revenues will be lower than originally expected in the $11 million to 13 million range, as certain customer sites have been delayed and therefore impact our ability to deliver and install in the period.

Gross Profit

Gross profit for 2013 is expected to be consistent with the prior year on an annual basis; despite additional costs incurred for research related projects attributed to MR guided radiation therapy and initial iCT project installations. Gross profit as a percentage of sales was 38.2 percent in our most recent quarter, as higher sales volumes and the delivery of systems at more historical gross margins had a favorable impact over the gross margin performance realized in the prior two quarter. Quarterly gross profit as a percentage of sales will vary depending on the underlying system installations in the respective quarters. Gross profit as a percentage of sales is forecast to be in the range of 35 percent for the fourth quarter as installation activity is projected to be lower in the period resulting in full year 2013 gross profit guidance of 35 percent. As we look in 2014, we expect annual gross profit as a percentage of sales to return back to the 40 percent range as many of the research related projects noted above that had a negative impact on margin will be largely completed in 2013.

Operating Expenses

Carefully managing expenses is a priority for our Company and in 2013 we continue to expect our departmental cash operating expenses to decrease approximately $3 million from 2012 levels to approximately $35 million. Not included in this amount are one-time cash costs of $4 million associated with the relocation of the Company’s facility from Winnipeg to Minneapolis and a charge of approximately $8 million to research and development costs which is described further below. The total cost of the Company’s relocation is forecast to be $5.4 million including $1.4 million incurred in 2012 and approximately $4.0 million in 2013.

Total research and development expenses are anticipated to be approximately $17 million, including an exceptional research and development charge of approximately $8 million arising from the expected completion in the fourth quarter of 2013 of the collaborative arrangement we entered into with Princess Margaret Hospital in October 2011 for their clinical MR-guided radiation therapy system. The MR-guided radiation therapy system will be used to conduct research at the hospital in order to clinically validate the system and develop a commercially viable version of the platform. The approximate $8 million charge includes approximately $5 million of deferred costs incurred in prior year periods as part of the development of the clinical site and has been recorded in prepaid expenses and other assets. These costs will be deferred until the installation is complete and then charged as research and development when clinical validation can begin.

Research and development will continue to be a priority in 2013 in support of commercializing our MR-guided radiation therapy system and SYMBIS Surgical System as well as enhancements for the VISIUS Surgical Theatre and traditional surgical procedures, including the addition of a ceiling mounted CT to the VISIUS Surgical Theatre.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 18 of 28 |

Taken together, total cash and non-cash operating expenses in 2013 are expected to be approximately $53 million, as summarized in the table below:

| 2013 Forecast | | $ Millions | |

| Cash operating expenses | | $ | 35.0 | |

| Minneapolis relocation costs | | | 4.0 | |

| Research & development charge | | | 3.0 | |

| Total | | | 42.0 | |

| Research & development charge (non-cash) | | | 5.0 | |

| Depreciation (non-cash) | | | 4.0 | |

| Stock based compensation (non-cash) | | | 2.0 | |

| Total operating expenses | | | 53.0 | |

Liquidity and Capital Resources

With cash, restricted cash and accounts receivable at September 30, 2013 of $43.2 million and order backlog of $101.4 million we have a strong base from which to continue to fund our operations and product development projects.

Our cash requirements in 2013 include funding for operations, capital investments related to robotics, iCT and MRgRT test labs, the costs related to the U.S. relocation and prepaid development costs associated with our collaborative arrangements. Our total capital expenditures for the fourth quarter of 2013 are expected to be in the range of $0.8 million to $0.9 million.

LIQUIDITY AND CAPITAL RESOURCES

Our principal capital needs are for funding scientific research and development programs, supporting our sales and marketing activities and funding capital expenditures and working capital. The Company is still in the early stages of its adoption and development of its products and has financed its cash requirements primarily through long-term debt, issuances of securities and advanced customer deposits from new orders.

Our primary objective over the last few years when managing capital is to ensure we have sufficient funds available to carry out meeting our customer commitments as well and funding our research, development and commercialization programs based, in part, on continuous monitoring of our progress.

Cash

We had cash and restricted cash of $28.4 million as of September 30, 2013, an increase of $7.4 million from December 31, 2012. The increase primarily resulted from financing activities which included proceeds from the issuance of share capital during the nine months ended September 30, 2013 of $18.9 million and net proceeds from long-term debt of $24.5 million. This was partially offset by cash used to fund operating activities, which included an operating loss for the nine months ended September 30, 2013 (excluding non-cash related items) of $15.4 million and cash used for working capital of $11.9 million. In addition, we invested $13.4 million in capital spending of $7.6 million and $5.6 million of additional restricted cash. These uses of cash were offset by a foreign exchange translation adjustment of $0.3 million.

Long-Term Debt

On September 16, 2013, we entered into a secured loan facility agreement for $25 million, and received the net proceeds of $24.5 million following execution of the agreement. The loan matures five years from the date of the Agreement and may be prepaid subject to certain restrictions. The principal amount of the loan is payable in three equal annual installments on the third, fourth and fifth anniversaries of the date of the disbursement, except that, if IMRIS achieves certain revenue targets, the principal payment due on the third anniversary can be deferred for up to two years and the payment due on the fourth anniversary can be deferred for one year. The outstanding principal amount of the loan at any time will accrue interest at a rate of 9 percent per annum. In connection with the loan, the lender received warrants to purchase 6.1 million shares of our common stock at an exercise price of $1.94 per share. Interest and other for the three and nine months ended September 30, 2013 includes interest expense of $88 thousand, debt discount amortization of $49 thousand and debt issuance cost amortization of $17 thousand. Interest expense, warrant discount amortization, and debt issuance cost amortization are recognized on an effective interest rate method over 5 years.

IMRIS Inc.

Management’s Discussion and Analysis – November 4, 2013

Page 19 of 28 |

Liquidity

The following table sets forth the summary statement of cash flows for the dates and periods indicated:

| | | Nine months ended | |

| | | September 30 | |

| | | 2013 | | | 2012 | | | Change | |

| Cash flows: | | | | | | | | | | | | |

| Used in Operating Activities | | $ | (27,281 | ) | | $ | (8,605 | ) | | $ | (18,676 | ) |

| From Financing Activities | | | 42,093 | | | | 2,346 | | | | 39,747 | |

| Used in Investing Activities | | | (13,352 | ) | | | (5,866 | ) | | | (7,486 | ) |

| Foreign exchange translation adjustment | | | 379 | | | | 83 | | | | 296 | |

| Net decrease | | | 1,839 | | | | (12,042 | ) | | | 13,881 | |

| | | | | | | | | | | | | |

| Cash and cash equivalents, opening | | | 19,060 | | | | 40,425 | | | | | |

| Cash and cash equivalents, closing | | $ | 20,899 | | | $ | 28,383 | | | $ | (7,484 | ) |

Operating Activities