SELECTED CONSOLIDATED FINANCIAL DATA

The summary information presented below under “Selected Balance Sheet Data” and “Selected Operations Data” for, and as of the end of, each of the years ended September 30 is derived from our audited consolidated financial statements. The following information is only a summary and you should read it in conjunction with our consolidated financial statements and notes beginning on page 50. All share information prior to the second step conversion and stock offering completed in December 2010 (“the corporate reorganization”) has been revised to reflect the 2.2637 exchange ratio.

| | | | | | | | | | | | | | | |

| | September 30, |

| | 2012 | | 2011 | | 2010 | | 2009 | | 2008 |

| | | (Dollars in thousands, except per share amounts) |

Selected Balance Sheet Data: | | | | | | | | | | | | | | | |

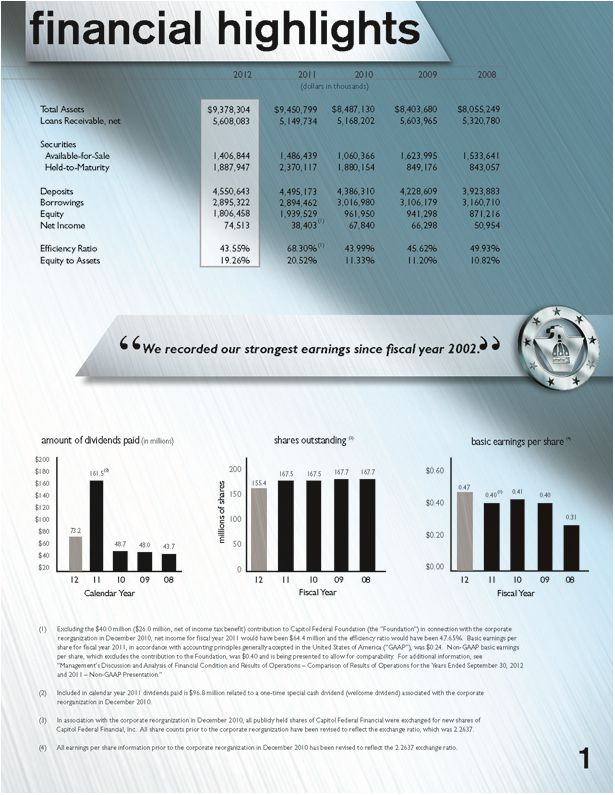

Total assets | | $ | 9,378,304 | | $ | 9,450,799 | | $ | 8,487,130 | | $ | 8,403,680 | | $ | 8,055,249 |

Loans receivable, net | | | 5,608,083 | | | 5,149,734 | | | 5,168,202 | | | 5,603,965 | | | 5,320,780 |

Securities: | | | | | | | | | | | | | | | |

Available-for-sale (“AFS”) | | | 1,406,844 | | | 1,486,439 | | | 1,060,366 | | | 1,623,995 | | | 1,533,641 |

Held-to-maturity (“HTM”) | | | 1,887,947 | | | 2,370,117 | | | 1,880,154 | | | 849,176 | | | 843,057 |

Capital stock of Federal Home Loan Bank (“FHLB”) | | | 132,971 | | | 126,877 | | | 120,866 | | | 133,064 | | | 124,406 |

Deposits | | | 4,550,643 | | | 4,495,173 | | | 4,386,310 | | | 4,228,609 | | | 3,923,883 |

Advances from FHLB | | | 2,530,322 | | | 2,379,462 | | | 2,348,371 | | | 2,392,570 | | | 2,447,129 |

Other borrowings | | | 365,000 | | | 515,000 | | | 668,609 | | | 713,609 | | | 713,581 |

Stockholders’ equity | | | 1,806,458 | | | 1,939,529 | | | 961,950 | | | 941,298 | | | 871,216 |

| | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | |

| | For the Year Ended September 30, |

| | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 |

| | | (Dollars and counts in thousands, except per share amounts) |

Selected Operations Data: | | | | | | | | | | | | | | | |

Total interest and dividend income | | $ | 328,051 | | $ | 346,865 | | $ | 374,051 | | $ | 412,786 | | $ | 410,806 |

Total interest expense | | | 143,170 | | | 178,131 | | | 204,486 | | | 236,144 | | | 276,638 |

Net interest and dividend income | | | 184,881 | | | 168,734 | | | 169,565 | | | 176,642 | | | 134,168 |

Provision for credit losses | | | 2,040 | | | 4,060 | | | 8,881 | | | 6,391 | | | 2,051 |

Net interest and dividend income after provision | | | | | | | | | | | | | | | |

for credit losses | | | 182,841 | | | 164,674 | | | 160,684 | | | 170,251 | | | 132,117 |

Retail fees and charges | | | 15,915 | | | 15,509 | | | 17,789 | | | 18,023 | | | 17,805 |

Other income | | | 8,318 | | | 9,486 | | | 16,622 | | | 10,571 | | | 12,222 |

Total other income | | | 24,233 | | | 24,995 | | | 34,411 | | | 28,594 | | | 30,027 |

Total other expenses | | | 91,075 | | | 132,317 | | | 89,730 | | | 93,621 | | | 81,989 |

Income before income tax expense | | | 115,999 | | | 57,352 | | | 105,365 | | | 105,224 | | | 80,155 |

Income tax expense | | | 41,486 | | | 18,949 | | | 37,525 | | | 38,926 | | | 29,201 |

Net income | | | 74,513 | | | 38,403 | | | 67,840 | | | 66,298 | | | 50,954 |

| | | | | | | | | | | | | | | |

Basic earnings per share | | $ | 0.47 | | $ | 0.24 | (1) | $ | 0.41 | | $ | 0.40 | | $ | 0.31 |

Average basic shares outstanding | | | 157,913 | | | 162,625 | | | 165,862 | | | 165,576 | | | 165,112 |

Diluted earnings per share | | $ | 0.47 | | $ | 0.24 | (1) | $ | 0.41 | | $ | 0.40 | | $ | 0.31 |

Average diluted shares outstanding | | | 157,916 | | | 162,633 | | | 165,899 | | | 165,721 | | | 165,279 |

| | | | | | | | | | | | | | | | | | | | |

| | 2012 | | 2011 | | 2010 | | 2009 | | 2008 |

Selected Performance and Financial Ratios | | | | | | | | | | | | | | | | | | | | |

and Other Data: | | | | | | | | | | | | | | | | | | | | |

Performance Ratios: | | | | | | | | | | | | | | | | | | | | |

Return on average assets | | | 0.79 | % | | | 0.41 | %(1) | | | 0.80 | % | | | 0.81 | % | | | 0.65 | % |

Return on average equity | | | 3.93 | | | | 2.20 | (1) | | | 7.09 | | | | 7.27 | | | | 5.86 | |

Dividends paid per share(2) | | $ | 0.40 | | | $ | 1.63 | | | $ | 2.29 | | | $ | 2.11 | | | $ | 2.00 | |

Dividend payout ratio | | | 85.58 | % | | | 390.88 | % | | | 71.34 | % | | | 66.47 | % | | | 81.30 | % |

Ratio of operating expense to | | | | | | | | | | | | | | | | | | | | |

average total assets | | | 0.97 | | | | 1.40 | (1) | | | 1.06 | | | | 1.14 | | | | 1.04 | |

Efficiency ratio | | | 43.55 | | | | 68.30 | (1) | | | 43.99 | | | | 45.62 | | | | 49.93 | |

Ratio of average interest-earning assets | | | | | | | | | | | | | | | | | | | | |

to average interest-bearing liabilities | | | 1.24 | x | | | 1.22 | x | | | 1.11 | x | | | 1.12 | x | | | 1.12 | x |

Interest rate spread information: | | | | | | | | | | | | | | | | | | | | |

Average during period | | | 1.64 | % | | | 1.42 | % | | | 1.78 | % | | | 1.86 | % | | | 1.35 | % |

End of period | | | 1.68 | | | | 1.60 | | | | 1.76 | | | | 1.89 | | | | 1.70 | |

Net interest margin | | | 2.01 | | | | 1.84 | | | | 2.06 | | | | 2.20 | | | | 1.75 | |

Asset Quality Ratios: | | | | | | | | | | | | | | | | | | | | |

Non-performing assets to total assets | | | 0.43 | (3) | | | 0.40 | | | | 0.49 | | | | 0.46 | | | | 0.23 | |

Non-performing loans to total loans | | | 0.57 | (3) | | | 0.51 | | | | 0.62 | | | | 0.55 | | | | 0.26 | |

Allowance for credit losses ("ACL") to | | | | | | | | | | | | | | | | | | | | |

non-performing loans | | | 34.88 | (3) | | | 58.34 | | | | 46.60 | | | | 32.83 | | | | 42.37 | |

ACL to loans receivable, net | | | 0.20 | | | | 0.30 | | | | 0.29 | | | | 0.18 | | | | 0.11 | |

Capital Ratios: | | | | | | | | | | | | | | | | | | | | |

Equity to total assets at end of period | | | 19.26 | | | | 20.52 | | | | 11.33 | | | | 11.20 | | | | 10.82 | |

Average equity to average assets | | | 20.11 | | | | 18.50 | | | | 11.30 | | | | 11.08 | | | | 11.05 | |

| | | | | | | | | | | | | | | | | | | | |

Regulatory Capital Ratios of Bank: | | | | | | | | | | | | | | | | | | | | |

Tier 1 leverage ratio | | | 14.6 | | | | 15.1 | | | | 9.8 | | | | 10.0 | | | | 10.0 | |

Tier 1 risk-based capital | | | 36.4 | | | | 37.9 | | | | 23.5 | | | | 23.2 | | | | 23.1 | |

Total risk-based capital | | | 36.7 | | | | 38.3 | | | | 23.8 | | | | 23.3 | | | | 23.0 | |

| | | | | | | | | | | | | | | | | | | | |

Other Data: | | | | | | | | | | | | | | | | | | | | |

Number of traditional offices | | | 36 | | | | 35 | | | | 35 | | | | 33 | | | | 30 | |

Number of in-store offices | | | 10 | | | | 10 | | | | 11 | | | | 9 | | | | 9 | |

| (1) | Excluding the $40.0 million ($26.0 million, net of income tax benefit) contribution to the Capitol Federal Foundation (“the Foundation”) in connection with Capitol Federal Financial’s conversion from a mutual holding company form of organization to a stock form of organization, basic and diluted earnings per share would have been $0.40, return on average assets would have been 0.68%, return on average equity would have been 3.69%, ratio of operating expense to average total assets would have been 0.98%, and the efficiency ratio would have been 47.65%. This adjusted financial data is not presented in accordance with accounting principles generally accepted in the United States of America (“GAAP”). See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Comparison of Results of Operations for the Years Ended September 30, 2012 and 2011 – Non-GAAP Presentation.” |

| (2) | For fiscal years 2008 through 2010, Capitol Federal Savings Bank MHC (“MHC”) owned a majority of the outstanding shares of Capitol Federal Financial common stock and waived its right to receive dividends paid on the common stock with the exception of the $0.50 per share dividend paid on 500,000 shares in February 2010. Public shares excluded shares held by MHC, as well as unallocated shares held in the Capitol Federal Financial Employee Stock Ownership Plan (“ESOP”). In December 2010, Capitol Federal Financial completed its conversion from a mutual holding company form of organization to a stock form of organization and all shares owned by MHC were sold in a public offering. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Executive Summary” for additional information. |

| (3) | See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Financial Condition – Loans Receivable” for additional information regarding non-performing loans and non-performing assets. |

MANAGEMENT'S DISCUSSION AND ANALYSIS OF

FINANCIAL CONDITION AND RESULTS OF OPERATIONS

General Overview

Capitol Federal Financial, Inc. (the “Company”) is the holding company and the sole shareholder of Capitol Federal Savings Bank (the “Bank”). The Company’s common stock is traded on the NASDAQ Global Select Market under the symbol “CFFN.”

Private Securities Litigation Reform Act—Safe Harbor Statement

We may from time to time make written or oral “forward‑looking statements”, including statements contained in our filings with the Securities and Exchange Commission (“SEC”). These forward-looking statements may be included in this annual report to stockholders and in other communications by the Company, which are made in good faith by us pursuant to the “safe harbor” provisions of the Private Securities Litigation Reform Act of 1995.

These forward-looking statements include statements about our beliefs, plans, objectives, goals, expectations, anticipations, estimates and intentions that are subject to significant risks and uncertainties, and are subject to change based on various factors, some of which are beyond our control. The words “may”, “could”, “should”, “would”, “believe”, “anticipate”, “estimate”, “expect”, “intend”, “plan” and similar expressions are intended to identify forward-looking statements. The following factors, among others, could cause our future results to differ materially from the plans, objectives, goals, expectations, anticipations, estimates and intentions expressed in the forward-looking statements:

| · | our ability to continue to maintain overhead costs at reasonable levels; |

| · | our ability to continue to originate a significant volume of one- to four-family mortgage loans in our market areas or to purchase loans through correspondents; |

| · | our ability to acquire funds from or invest funds in wholesale or secondary markets at favorable yields as compared to the related funding source; |

| · | our ability to access cost-effective funding; |

| · | the future earnings and capital levels of the Bank and the continued non-objection by our primary federal banking regulators, to the extent required, to distribute capital from the Bank to the Company, which could affect the ability of the Company to pay dividends in accordance with its dividend policies; |

| · | fluctuations in deposit flows, loan demand, and/or real estate values, as well as unemployment levels, which may adversely affect our business; |

| · | the credit risks of lending and investing activities, including changes in the level and direction of loan delinquencies and write-offs, changes in property values, and changes in estimates of the adequacy of the ACL; |

| · | results of examinations of the Bank and the Company by their respective primary federal banking regulators, including the possibility that the regulators may, among other things, require us to increase our ACL; |

| · | the strength of the U.S. economy in general and the strength of the local economies in which we conduct operations; |

| · | the effects of, and changes in, trade, fiscal policies and laws, and monetary and interest rate policies of the Board of Governors of the Federal Reserve System (“FRB”); |

| · | the effects of, and changes in, foreign and military policies of the United States government; |

| · | inflation, interest rate, market and monetary fluctuations; |

| · | the timely development and acceptance of our new products and services and the perceived overall value of these products and services by users, including the features, pricing and quality compared to competitors’ products and services; |

| · | the willingness of users to substitute competitors’ products and services for our products and services; |

| · | our success in gaining regulatory approval of our products and services and branching locations, when required; |

| · | the impact of changes in financial services laws and regulations, including laws concerning taxes, banking, securities and insurance and the impact of other governmental initiatives affecting the financial services industry; |

| · | implementing business initiatives may be more difficult or expensive than anticipated; |

| · | acquisitions and dispositions; |

| · | changes in consumer spending and saving habits; and |

| · | our success at managing the risks involved in our business. |

This list of important factors is not exclusive. We do not undertake to update any forward-looking statement, whether written or oral, that may be made from time to time by or on behalf of the Company or the Bank.

The following discussion is intended to assist in understanding the financial condition and results of operations of the Company. The Bank comprises almost all of the consolidated assets and liabilities of the Company and the Company is dependent primarily upon the performance of the Bank for the results of its operations. Because of this relationship, references to management actions, strategies and results of actions apply to both the Bank and the Company.

Executive Summary

The following summary should be read in conjunction with our Management’s Discussion and Analysis of Financial Condition and Results of Operations in its entirety.

In December 2010, Capitol Federal Financial completed its conversion from a mutual holding company form of organization to a stock form of organization. Capitol Federal Financial, which owned 100% of the Bank, was succeeded by Capitol Federal Financial, Inc., a new Maryland corporation. As part of the corporate reorganization, MHC’s ownership interest of Capitol Federal Financial was sold in a public stock offering. Capitol Federal Financial, Inc. sold 118,150,000 shares of common stock at $10.00 per share in the stock offering. The publicly held shares of Capitol Federal Financial were exchanged for new shares of common stock of Capitol Federal Financial, Inc. The exchange ratio was 2.2637 and ensured that immediately after the corporate reorganization the public stockholders of Capitol Federal Financial owned the same aggregate percentage of Capitol Federal Financial, Inc. common stock that they owned of Capitol Federal Financial common stock immediately prior to that time. In lieu of fractional shares, Capitol Federal Financial stockholders were paid in cash. Gross proceeds from the offering were $1.18 billion and related offering expenses were $46.7 million. The net proceeds from the stock offering were $1.13 billion, of which 50%, or $567.4 million, was contributed to the Bank as a capital contribution, as required by the Office of Thrift Supervision (the “OTS”) regulations. The other 50%, or $567.4 million, remained at Capitol Federal Financial, Inc., of which $40.0 million was contributed to the Bank’s charitable foundation, Capitol Federal Foundation, and $47.3 million was loaned to the ESOP for its purchase of Capitol Federal Financial, Inc. shares in the stock offering. In April 2011, the Company redeemed the outstanding Junior Subordinated Deferrable Interest Debentures (the “Debentures”) of $53.6 million using a portion of the offering proceeds from the corporate reorganization.

On July 21, 2010, the Dodd-Frank Wall Street Reform and Consumer Protection Act (the “Dodd-Frank Act”) was signed into law. The Dodd-Frank Act, among other things, required the OTS to be merged into the Office of the Comptroller of the Currency (the “OCC”). On July 21, 2011, the OCC assumed all functions and authority from the OTS relating to federally charted savings banks, and the FRB assumed all functions and authority from the OTS relating to savings and loan holding companies. Accordingly, effective July 21, 2011, the Bank became regulated by the OCC and the Company became regulated by the FRB. Prior to that date, the Bank and Company were regulated by the OTS. All references to the OTS in this document on or after that date will refer to the successor regulator (i.e., the OCC for the Bank and the FRB for the Company), as appropriate.

We have been, and intend to continue to be, a community-oriented financial institution offering a variety of financial services to meet the needs of the communities we serve. We attract retail deposits from the general public and invest those funds primarily in permanent loans secured by first mortgages on owner-occupied, one- to four-family residences. To a lesser extent, we also originate consumer loans, loans secured by first mortgages on non-owner-occupied one- to four-family residences, multi-family and commercial real estate loans, and construction loans. While our primary business is the origination of one- to four-family mortgage loans funded through retail deposits, we also purchase whole one- to four-family mortgage loans from correspondent and nationwide lenders, and invest in certain investment securities and mortgage-backed securities (“MBS”) using funding from retail deposits, advances from FHLB, and repurchase agreements. The Company is significantly affected by prevailing economic conditions including federal monetary and fiscal policies and federal regulation of financial institutions. Retail deposit balances are influenced by a number of factors including interest rates paid on competing personal investment products, the level of personal income, and the personal rate of savings within our market areas. Lending activities are influenced by the demand for housing and other loans, changing loan underwriting guidelines, as well as interest rate pricing competition from other lending institutions. The primary sources of funds for lending activities include deposits, loan repayments, investment income, borrowings, and funds provided from operations.

The Company’s results of operations are primarily dependent on net interest income, which is the difference between the interest earned on loans, MBS, investment securities, and cash, and the interest paid on deposits and borrowings. On a weekly basis, management reviews deposit flows, loan demand, cash levels, and changes in several market rates to assess all pricing strategies. The Bank generally prices its first mortgage loan products based on secondary market and competitor pricing. Generally, deposit pricing is based upon a survey of competitors in the Bank’s market areas, and the need to attract funding and retain maturing deposits. The majority of our loans are fixed-rate products with maturities up to 30 years, while the majority of our deposits have maturity or repricing dates of less than two years.

The Federal Open Market Committee of the Federal Reserve (the “FOMC”) noted in their October 2012 statement that the economy continues to expand at a moderate pace. Growth in employment has been slow, and the level of unemployment remains elevated. The FOMC noted that household spending has advanced a bit more quickly in recent months; however, business fixed investment has waned. The housing sector has shown signs of improvement, albeit from a depressed level, and inflation has recently picked up somewhat reflecting higher energy

prices. The FOMC decided to continue, through the end of the year, its program to extend the average maturity of its holdings of Treasury securities, as announced in September 2011, by purchasing Treasury securities with remaining maturities of six to 30 years and maintain its existing policy of reinvesting principal payments from its holdings of agency debt and agency MBS in agency MBS. Additionally, the FOMC stated that they will continue their program, announced in September 2012, of purchasing agency MBS at a pace of $40 billion per month. There is no definitive end date to this program. The FOMC believes these actions will put downward pressure on longer-term interest rates, support mortgage markets, and help to make broader financial conditions more accommodative. The FOMC also decided to maintain the overnight lending rate at zero to 0.25% and it believes the low rates will be warranted through at least mid-2015.

Economic conditions in the Bank’s local market areas have a significant impact on the ability of borrowers to repay loans and the value of the collateral securing these loans. As of September 2012, the unemployment rate was 5.9% for Kansas and 6.9% for Missouri, compared to the national average of 7.8%. The unemployment rate remains relatively low in our market areas, compared to the national average, due to diversified industries within our market areas, primarily in the Kansas City metropolitan statistical area, but it is higher than the historical average. Our Kansas City market area, which comprises the largest segment of our loan portfolio and deposit base, has an average household income of approximately $79 thousand per annum, based on 2012 estimates from the American Community Survey, which is a statistical survey by the U.S. Census Bureau. The average household income in our combined market areas is approximately $68 thousand per annum, with 92% of the population at or above the poverty level, also based on the 2012 estimates from the American Community Survey. The Federal Housing Finance Agency (“FHFA”) price index for Kansas and Missouri has not experienced significant fluctuations during the past 10 years, unlike several other segments of the United States, which indicates relative stability in property values in our local market areas.

Total assets decreased $72.5 million, from $9.45 billion at September 30, 2011 to $9.38 billion at September 30, 2012, due primarily to a $561.8 million decrease in the securities portfolio, partially offset by an increase of $458.3 million in loans receivable, net, and an increase in cash and cash equivalents of $20.6 million. The decrease in securities was due primarily to called and matured investment securities not being fully replaced, including $300.0 million at Capitol Federal Financial, Inc., at the holding company level. The increase in loans receivable was due primarily to an increase in one- to four-family loans resulting largely from $630.2 million of bulk and correspondent loan purchases during the current fiscal year.

The performance of our loan portfolio continues to improve as evidenced by a decline in delinquent loan balances and the level of loan charge-offs. Loans 30 to 89 days delinquent decreased $3.5 million from $26.8 million at September 30, 2011 to $23.3 million at September 30, 2012. Loans more than 90 days delinquent or in foreclosure decreased $7.0 million from $26.5 million at September 30, 2011 to $19.5 million at September 30, 2012. Additionally, net loan charge-offs during the current fiscal year were $2.9 million, excluding the $3.5 million of specific valuation allowances (“SVAs”) charged-off during the year as the OCC Call Report requirements do not permit the use of SVAs, compared to $3.5 million of net loan charge-offs during the prior fiscal year.

Total liabilities increased $60.6 million, from $7.51 billion at September 30, 2011 to $7.57 billion at September 30, 2012. The increase was due primarily to a $55.5 million increase in deposits. The increase in the deposit portfolio was due primarily to a $54.9 million increase in the checking portfolio and a $44.9 million increase in the money market portfolio, partially offset by a $52.0 million decrease in the certificate of deposit portfolio.

Stockholders’ equity decreased $133.1 million, from $1.94 billion at September 30, 2011 to $1.81 billion at September 30, 2012. The decrease was due primarily to the repurchase of $149.0 million of common stock and the payment of $63.8 million of dividends, partially offset by net income of $74.5 million.

Net income for fiscal year 2012 was $74.5 million, compared to $38.4 million for fiscal year 2011. The $36.1 million, or 94.0%, increase for the current year was due primarily to the prior year including a $40.0 million ($26.0 million, net of income tax benefit) contribution to the Foundation in connection with the corporate reorganization. Additionally, net interest income increased $16.2 million, or 9.6%, from $168.7 million for the prior year to $184.9 million for the current year. The increase in net interest income was due primarily to a decrease in interest expense of $34.9 million, or 19.6%, partially offset by a decrease in interest income of $18.8 million, or 5.4%. The net interest margin increased 17 basis points to 2.01% for the current year, up from 1.84% for the prior year. The increase was largely due to a decrease in the cost of the certificate of deposit portfolio, along with a decrease in costs on FHLB advances and other borrowings, partially offset by a decrease in interest income on loans receivable.

The Bank currently expects to open one branch in calendar year 2013. The branch will be located in our Kansas City market area. Management continues to consider expansion opportunities in all of our market areas.

Critical Accounting Policies

Our most critical accounting policies are the methodologies used to determine the ACL and fair value measurements. These policies are important to the presentation of our financial condition and results of operations, involve a high degree of complexity, and require management to make difficult and subjective judgments that may require assumptions or estimates about highly uncertain matters. The use of different judgments, assumptions, and estimates could cause reported results to differ materially. These critical accounting policies and their application are reviewed at least annually by our audit committee. The following is a description of our critical accounting policies and an explanation of the methods and assumptions underlying their application.

Allowance for Credit Losses. The Company maintains an ACL to absorb inherent losses in the loan portfolio based upon ongoing quarterly assessments of the loan portfolio. The ACL is maintained through provisions for credit losses which are charged to income. The methodology for determining the ACL is considered a critical accounting policy by management because of the high degree of judgment involved, the subjectivity of the assumptions used, and the potential for changes in the economic environment that could result in changes to the amount of the recorded ACL. Additionally, bank regulators have the ability to require the Bank, as they can require all banks, to increase the ACL or recognize additional charge-offs based upon their judgments, which may differ from management’s judgments. Although management believes that the Bank has established and maintained the ACL at appropriate levels, additions may be necessary if economic and other conditions continue or worsen substantially from the current operating environment, and/or if bank regulators require the Bank to increase the ACL and/or recognize additional charge-offs.

Our primary lending emphasis is the origination and purchase of one- to four-family mortgage loans on residential properties, and, to a lesser extent, home equity and second mortgages on one- to four-family residential properties, resulting in a loan concentration in residential first mortgage loans. As a result of our lending practices, we also have a concentration of loans secured by real property located in Kansas and Missouri. At September 30, 2012, approximately 70% and 15% of the Bank’s loans were secured by real property located in Kansas and Missouri, respectively. We believe the primary risks inherent in our one- to four-family and consumer portfolios are the continued weakened economic conditions, continued high levels of unemployment or underemployment, and a continuing decline in home real estate values. Any one or a combination of these events may adversely affect borrowers’ ability or desire to repay their loans, resulting in increased delinquencies, non-performing assets, loan losses, and future loan loss provisions. Although the multi-family and commercial loan portfolio also shares the risk of continued weakened economic conditions, the primary risks for the portfolio include the ability of the borrower to sustain sufficient cash flows from leases and to control expenses to satisfy their contractual debt payments, or the ability to utilize personal and/or business resources to pay their contractual debt payments if the cash flows are not sufficient.

Generally, when a one- to four-family secured loan is 180 days delinquent, new collateral values are obtained through appraisals. If the estimated fair value of the collateral, less estimated costs to sell, is less than the current loan balance, the difference is charged-off. Anticipated private mortgage insurance (“PMI”) proceeds are taken into consideration when calculating the amount of the charge-off. An updated appraisal is requested, at a minimum, every six months thereafter that a purchased loan remains a classified asset and every 12 months thereafter that an originated loan remains 180 days or more delinquent. If the Bank holds the first and second mortgage, both loans are combined when evaluating whether there is a potential loss on the loan. However, charge-offs for real estate-secured loans may also occur at any time if we have knowledge of the existence of a potential loss. For all other real estate loans that are not secured by one- to four-family property, losses are charged-off when we believe the collection of such amounts is unlikely. When a non-real estate secured loan is 120 days delinquent, any identified losses are charged-off.

Each quarter, we prepare a formula analysis which segregates our loan portfolio into categories based on certain risk characteristics such as loan type (one- to four-family, multi-family, etc.), interest payments (fixed-rate, adjustable-rate), loan source (originated or bulk purchased), loan-to-value (“LTV”) ratios, borrower’s credit score and payment status (i.e. current or number of days delinquent). Consumer loans, such as second mortgages and home equity lines of credit, with the same underlying collateral as a one- to four-family loan are combined with the one- to four-family loan in the formula analysis to calculate a combined LTV ratio. All loans that are not individually evaluated for impairment are included in the formula analysis. Quantitative loss factors are applied to each loan category in the formula analysis based on the historical net loss experience for each respective loan category. Additionally, qualitative loss factors that management believes impact the collectability of the loan portfolio as of the evaluation date are applied to certain loan categories. Such qualitative factors include changes in collateral values, unemployment rates, credit scores and delinquent loan trends. Loss factors increase as loans are classified or become delinquent. Additionally, troubled debt restructurings (“TDRs”) that have not been partially charged-off are included in a category within the formula analysis model with an overall higher qualitative loss factor than corresponding performing loans, for the life of the loan.

The factors applied in the formula analysis are reviewed quarterly by management to assess whether the factors adequately cover probable and estimable losses inherent in the loan portfolio. Our ACL methodology permits modifications to the formula analysis in the event that, in management’s judgment, significant factors which affect the collectability of the portfolio or any category of the loan portfolio, as of the evaluation date, have changed from the current formula analysis. Management’s evaluation of the qualitative factors with respect to these conditions is subject to a higher degree of uncertainty because they are not identified with a specific problem loan or portfolio segment.

Management utilizes the formula analysis, along with several other factors, when evaluating the adequacy of the ACL. Such factors include the trend and composition of delinquent loans, results of foreclosed property and short sale transactions, the current status and trends of local and national economies, particularly levels of unemployment, trends and current conditions in the real estate and housing markets, and loan portfolio growth and concentrations. Since our loan portfolio is primarily concentrated in one- to four-family real estate, we monitor one- to four-family real estate market value trends in our local market areas and geographic sections of the U.S. by reference to various industry and market reports, economic releases and surveys, and our general and specific knowledge of the real estate markets in which we lend, in order to determine what impact, if any, such trends may have on the level of our ACL. We seek to apply ACL methodology in a consistent manner; however, the methodology can be modified in response to changing conditions. In addition, the adequacy of the Company’s ACL is reviewed during bank regulatory examinations. We consider any comments from our regulator when assessing the appropriateness of our ACL. Reviewing these quantitative and qualitative factors assists management in evaluating the overall reasonableness of the ACL and whether changes need to be made to our assumptions.

Fair Value Measurements. The Company uses fair value measurements to record fair value adjustments to certain assets and to determine fair value disclosures, per the provisions of Accounting Standards Codification (“ASC”) 820, Fair Value Measurements and Disclosures. In accordance with ASC 820, the Company groups its assets at fair value in three levels, based on the markets in which the assets are traded and the reliability of the underlying assumptions used to determine fair value, with Level 1 (quoted prices for identical assets in an active market) being considered the most reliable, and Level 3 having the most unobservable inputs and therefore being considered the least reliable. The Company bases its fair values on the price that would be received to sell an asset in an orderly transaction between market participants at the measurement date. As required by ASC 820, the Company maximizes the use of observable inputs and minimizes the use of unobservable inputs when measuring fair value. The Company did not have any liabilities that were measured at fair value at September 30, 2012.

The Company’s AFS securities are its most significant assets measured at fair value on a recurring basis. Changes in the fair value of AFS securities are recorded, net of tax, in accumulated other comprehensive income (“AOCI”) which is a component of stockholders’ equity. As part of determining fair value, the Company obtains fair values for all AFS securities from independent nationally recognized pricing services. Various modeling techniques are used to determine pricing for the Company’s securities, including option pricing and discounted cash flow models. The inputs to these models may include benchmark yields, reported trades, broker/dealer quotes, issuer spreads, benchmark securities, bids, offers and reference data. There is a security in the AFS portfolio that has significant unobservable inputs requiring the independent pricing services to use some judgment in pricing the related securities. This AFS security is classified as Level 3. All other AFS securities are classified as Level 2.

Loans receivable individually evaluated for impairment and other real estate owned (“OREO”) are the Company’s significant assets measured at fair value on a non-recurring basis. These non-recurring fair value adjustments involve the application of lower-of-cost-or-fair value accounting or write-downs of individual assets. Fair value for these assets is estimated using current appraisals or listing prices. Fair values may be adjusted by management to reflect current economic and market conditions and, as such, are classified as Level 3.

Recent Accounting Pronouncements. For a discussion of Recent Accounting Pronouncements, see “Notes to Financial Statements - Note 1 - Summary of Significant Accounting Policies.”

Management Strategy

We are a retail-oriented financial institution dedicated to serving the needs of customers in our market areas. Our commitment is to provide qualified borrowers the broadest possible access to home ownership through our mortgage lending programs and to offer a complete set of personal banking products and services to our customers. We strive to enhance stockholder value while maintaining a strong capital position. To achieve these goals, we focus on the following strategies:

| · | Residential Portfolio Lending. We are one of the leading originators of one- to four-family loans in the state of Kansas. We originate these loans primarily for our own portfolio, and we service the loans we originate. We also purchase one- to four-family loans from correspondent and nationwide lenders. We offer both fixed- and adjustable-rate products with various terms to maturity and pricing options. We also offer government-sponsored programs directed towards first time home buyers, low or moderate income borrowers, or borrowers with certain credit risk concerns. We maintain strong relationships with local real estate agents to attract mortgage loan business. We rely on our marketing efforts and reputation to attract mortgage business from walk-in customers, customers that apply online, and existing customers. |

| · | Retail Financial Services. We offer a wide array of deposit products and retail services for our customers. These products include checking, savings, money market, certificates of deposit, and retirement accounts. These products and services are provided through a branch network of 46 locations, including traditional branches and retail in-store locations, our call center which operates on extended hours, mobile banking, telephone banking and bill payment services, and online banking and bill payment services. |

| · | Cost Control. We generally are very effective at controlling our costs of operations. By using technology, we are able to centralize our lending and deposit support functions for efficient processing. We have located our branches to serve a broad range of customers through relatively few branch locations. Our average deposit base per traditional branch at September 30, 2012 was approximately $112.8 million. This large average deposit base per branch helps to control costs. Our one- to four-family lending strategy and our effective management of credit risk allows us to service a large portfolio of loans at efficient levels because it costs less to service a portfolio of performing loans. |

| · | Asset Quality. We utilize underwriting standards for our lending products that are designed to limit our exposure to credit risk. We require complete documentation for both originated and purchased loans, and make credit decisions based on our assessment of the borrower’s ability to repay the loan in accordance with its terms. See additional discussion of asset quality in Part I, Item 1 of the Annual Report on Form 10-K. |

| · | Capital Position. Our policy has always been to protect the safety and soundness of the Bank through credit and operational risk management, balance sheet strength, and sound operations. The end result of these activities has been a capital ratio in excess of the well-capitalized standards set by the OCC. We believe that maintaining a strong capital position safeguards the long-term interests of the Bank, the Company and our stockholders. |

| · | Stockholder Value. We strive to enhance stockholder value while maintaining a strong capital position. One way that we continue to provide returns to stockholders is through our dividend payments. Total dividends declared and paid during fiscal year 2012 were $63.8 million. The Company’s cash dividend payout policy is reviewed quarterly by management and the Board of Directors, and the ability to pay dividends under the policy depends upon a number of factors, including the Company’s financial condition and results of operations, the Bank’s regulatory capital requirements, regulatory limitations on the Bank’s ability to make capital distributions to the Company, and the amount of cash at the holding company. It is the Board of Directors’ intentions to continue to pay regular quarterly and special cash dividends each year. For fiscal year 2013, it is the intent of the Board of Directors and management to continue with the payout of 100% of the Company’s earnings to its stockholders. |

| · | Interest Rate Risk Management. Changes in interest rates are our primary market risk as our balance sheet is almost entirely comprised of interest-earning assets and interest-bearing liabilities. As such, fluctuations in interest rates have a significant impact not only upon our net income but also upon the cash flows related to those assets and liabilities and the market value of our assets and liabilities. In order to maintain acceptable levels of net interest income in varying interest rate environments, we actively manage our interest rate risk and assume a moderate amount of interest rate risk consistent with board policies. |

Quantitative and Qualitative Disclosure about Market Risk

Asset and Liability Management and Market Risk

The risk associated with changes in interest rates on the earnings of the Bank and the market value of its financial assets and liabilities is known as interest rate risk. Interest rate risk is our most significant market risk and our ability to adapt to changes in interest rates is known as interest rate risk management. The rates of interest the Bank earns on assets and pays on liabilities generally are established contractually for a period of time. Fluctuations in interest rates have a significant impact not only upon our net income, but also upon the cash flows of those assets and liabilities and the market value of our assets and liabilities. Our results of operations, like those of other financial institutions, are impacted by these changes in interest rates and the interest rate sensitivity of our interest-earning assets and interest-bearing liabilities. The analysis presented in the tables below reflects the level of market risk at the Bank and does not include the assets of the Company. The inclusion of assets at the holding company would not materially change the results of the analysis provided.

The general objective of our interest rate risk management program is to determine and manage an appropriate level of interest rate risk while maximizing net interest income in a manner consistent with our policy to reduce, to the extent possible, the exposure of our net interest income to changes in market interest rates. The Asset and Liability Committee (“ALCO”) regularly reviews the interest rate risk exposure of the Bank by forecasting the impact of hypothetical, alternative interest rate environments on net interest income and market value of portfolio equity (“MVPE”) at various dates. The MVPE is defined as the net of the present value of the cash flows of existing assets, liabilities and off-balance sheet instruments. The present values are determined based upon market conditions as of the date of the analysis as well as in alternative interest rate environments providing potential changes in MVPE under those alternative interest rate environments. Net interest income is projected in the same alternative interest rate environments as well, both with a static balance sheet and with management strategies considered. MVPE and net interest income analyses are also conducted to estimate our sensitivity to rates for future time horizons based upon market conditions as of the date of the analysis. In addition to the interest rate environments presented below, management also reviews the impact of non-parallel rate shock scenarios on a quarterly basis. These scenarios consist of flattening and steepening the yield curve by changing short-term and long-term interest rates independent of each other, and simulating cash flows and valuations as a result of the simulated changes in rates. This analysis helps management quantify the Bank’s exposure to changes in the shape of the yield curve.

Based upon management’s recommendations, the Board of Directors sets the asset and liability management policies of the Bank. These policies are implemented by ALCO. The purpose of ALCO is to communicate, coordinate and control asset and liability management consistent with board-approved policies. ALCO’s objectives are to manage assets and funding sources to produce the highest profitability balanced against liquidity, capital adequacy and risk management objectives. At each monthly meeting, ALCO recommends appropriate strategy changes. The Chief Financial Officer, or his designee, is responsible for executing, reviewing and reporting on the results of the policy recommendations and strategies to the Board of Directors, generally on a monthly basis.

The ability to maximize net interest income is dependent largely upon the achievement of a positive interest rate spread that can be sustained despite fluctuations in prevailing interest rates. The asset and liability repricing gap is a measure of the difference between the amount of interest-earning assets and interest-bearing liabilities which either reprice or mature within a given period of time. The difference provides an indication of the extent to which an institution's interest rate spread will be affected by changes in interest rates. A gap is considered positive when the amount of interest-earning assets exceeds the amount of interest-bearing liabilities maturing or repricing during the same period. A gap is considered negative when the amount of interest-bearing liabilities exceeds the amount of interest-earning assets maturing or repricing during the same period. Generally, during a period of rising interest rates, a negative gap within shorter repricing periods adversely affects net interest income, while a positive gap within shorter repricing periods results in an increase in net interest income. During a period of falling interest rates, the opposite would generally be true.

Management recognizes that dramatic changes in interest rates within a short period of time can cause an increase in our interest rate risk relative to the balance sheet. At times, ALCO may recommend increasing our interest rate risk exposure in an effort to increase our net interest margin, while maintaining compliance with established board limits for interest rate risk sensitivity. Management believes that maintaining and improving earnings is the best way to preserve a strong capital position. Management recognizes the need, in certain interest rate environments, to limit the Bank's exposure to changing interest rates and may implement strategies to reduce our interest rate risk which could, as a result, reduce earnings in the short-term. To minimize the potential for adverse effects of material and prolonged changes in interest rates on our results of operations, we have adopted asset and liability management policies to better balance the maturities and repricing terms of our interest-earning assets and interest-bearing liabilities based on existing local and national interest rates.

During periods of economic uncertainty, rising interest rates, or extreme competition for loans, the Bank’s ability to originate or purchase loans may be adversely affected. In such situations, the Bank alternatively may invest its funds into investment securities or MBS. These investments may have rates of interest lower than rates we could receive on loans, if we were able to originate or purchase them, potentially reducing the Bank’s interest income.

At September 30, 2012, the Bank’s one-year gap between interest-earning assets and interest-bearing liabilities was $2.13 billion, or 22.82% of total assets. Interest-earning assets repricing to lower rates at a faster pace than interest-bearing liabilities will generally result in net interest margin compression. Should interest rates rise, the amount of interest-earning assets that are expected to reprice will likely decrease as borrowers and agency debt issuers will have less economic incentive or ability to lower their cost. The amount of interest-bearing liabilities expected to reprice in a given period, however, is not usually impacted by changes in market interest rates because the maturities within the Bank’s borrowings and certificate of deposit portfolios are contractual and generally cannot be terminated early without penalty. If rates were to increase 200 basis points, the Bank’s one-year gap would be $241.9 million, or 2.6% of total assets. The majority of interest-earning assets anticipated to reprice in fiscal year 2013 are mortgages and MBS, both of which may prepay and/or be refinanced or endorsed. As interest rates decrease, borrowers have an economic incentive to refinance or endorse loans to lower market interest rates. This significantly increases the amount of cash flows anticipated to reprice to lower market interest rates during fiscal year 2013, as evidenced by the volume of mortgages that were endorsed and refinanced during fiscal year 2012 as a result of the decrease in market interest rates. In addition, cash flows from the Bank’s callable investment securities are anticipated to remain elevated during fiscal year 2013 as the issuers of these securities will likely continue to exercise their option to call the securities in order to issue new debt securities at lower market rates. Any decrease in the net interest margin due to interest-earning assets repricing will likely be at least partially offset by a decrease in our cost of funds.

The shape of the yield curve also has an impact on our net interest income and, therefore, the Bank’s net interest margin. Historically, the Bank has benefited from a steeper yield curve as the Bank’s mortgage loans are generally priced off of long-term rates while deposits are priced off of short-term rates. A steeper yield curve (one with a greater difference between short-term rates and long-term rates) allows the Bank to receive a higher rate of interest on its mortgage-related assets relative to the rate paid for the funding of those assets, which generally results in a higher net interest margin. As the yield curve flattens, the spread between rates received on assets and paid on liabilities becomes compressed, which generally leads to a decrease in net interest margin.

We manage the reinvestment risk of loan prepayments through our interest rate risk and asset management strategies. In recent periods, principal repayments in excess of loan originations and purchases have been reinvested in shorter-term MBS and investment securities at lower market rates than our loan portfolio, which reduces our interest rate spread. If, however, market rates were to rise, the shorter-term nature of the securities provides management with the opportunity to reinvest the maturing funds at the higher rates.

General assumptions used by management to evaluate the sensitivity of our financial performance to changes in interest rates presented in the tables below are utilized in, and set forth under, the gap table and related notes. Although management finds these assumptions reasonable given the constraints described above, the interest rate sensitivity of our assets and liabilities and the estimated effects of changes in interest rates on our net interest income and MVPE indicated in the below tables could vary substantially if different assumptions were used or actual experience differs from these assumptions. To illustrate this point, the projected cumulative excess (deficiency) of interest-earning assets over interest-bearing liabilities within the three to 12 months category as a percent of total assets (“one-year gap”) is also provided for an up 200 basis point scenario, as of September 30, 2012.

Qualitative Disclosure about Market Risk

Percentage Change in Net Interest Income. For each period presented in the following table, the estimated percentage change in the Bank’s net interest income based on the indicated instantaneous, parallel and permanent change in interest rates is presented. The percentage change in each interest rate environment represents the difference between estimated net interest income in a 0 basis point interest rate environment (“base case”, assumes the forward market and product interest rates implied by the yield curve are realized) and estimated net interest income in alternative interest rate environments (assumes market and product interest rates have a parallel shift in rates across all maturities by the indicated change in rates). Estimations of net interest income used in preparing the table below are based upon the assumptions that the total composition of interest-earning assets and interest-bearing liabilities does not change materially and that any repricing of assets or liabilities occurs at anticipated product and market rates for the alternative rate environments as of the dates presented. The estimation of net interest income does not include any projected gains or losses related to the sale of loans or securities, or income derived from non-interest income sources, but does include the use of different prepayment assumptions in the alternative interest rate environments. It is important to consider that the estimated changes in net interest income are for a cumulative four-quarter period. These do not reflect the earnings expectations of management.

| | | | | |

Change | | Percentage Change in Net Interest Income | |

(in Basis Points) | | At September 30, | |

in Interest Rates(1) | | 2012 | | 2011 | |

-100 bp | | N/A | | N/A | |

000 bp | | -- | | -- | |

+100 bp | | 5.00 | % | 4.46 | % |

+200 bp | | 3.79 | % | 3.75 | % |

+300 bp | | 1.54 | % | (0.33) | % |

(1)Assumes an instantaneous, permanent and parallel change in interest rates at all maturities.

The projected percentage change in the net interest income was higher at September 30, 2012 than September 30, 2011 due primarily to an increase in mortgage-related assets projected to reprice in the next 12 months, as compared to the prior year. Mortgage rates were lower at September 30, 2012 than at September 30, 2011; therefore, borrowers’ economic incentive to refinance or endorse their mortgage to a lower interest rate was higher at September 30, 2012, resulting in more asset cash flows. Additionally, a bulk purchase of $342.5 million of ARM loans during the fourth quarter of fiscal year 2012 increased the amount of assets repricing within the next 12 months as a portion of the funds used to purchase the loans would have been used to buy securities with longer repricing characteristics than the loans purchased.

The Bank’s net interest income projections are directly correlated to the amount of assets and liabilities that are expected to reprice over the next year. Repricing can occur as a result of variable interest rate characteristics of the Bank’s assets or liabilities, or as a result of cash flows that are received on assets or due on liabilities and are replaced at current market interest rates. The Bank’s liabilities generally have stated maturities and the related cash flows do not generally fluctuate as a result of changes in interest rates. Conversely, on the asset side, cash flows from mortgage-related assets and callable agency debentures can vary significantly as a result of changes in interest rates. As interest rates decrease, borrowers have an economic incentive to lower their cost of debt by refinancing or endorsing their mortgage to a lower interest rate. Similarly, agency debt issuers are more likely to exercise embedded call options for agency securities and issue new securities at a lower interest rate. As of September 30, 2011 and 2012, interest rates were at historically low levels, which resulted in a greater amount of cash flows from assets projected to reprice compared to liabilities. As interest rates rise, assets reprice to a higher interest rate at a faster pace than liabilities, thus increasing net interest income projections compared to the base case. However, the further interest rates rise, the less economic incentive and ability borrowers and agency debt issuers have to modify their cost of debt; thus, cash flows become significantly reduced. The benefit of rising interest rates to net interest income diminishes due to lower asset cash flow projections as interest rates rise. At September 30, 2012, in the +300 basis point interest rate environment, cash flows related to assets diminished such that the benefit of reinvesting cash flows at higher yields was more than offset by the cash flows from liabilities repricing to higher levels. See the Gap analysis discussion below for additional information.

Percentage Change in MVPE. The following table sets forth the estimated percentage change in the MVPE at each period presented based on the indicated instantaneous, parallel and permanent change in interest rates. The percentage change in each interest rate environment represents the difference between MVPE in the base case and MVPE in each alternative interest rate environment. The estimations of MVPE used in preparing the table below are based upon the assumptions that the total composition of interest-earning assets and interest-bearing liabilities does not change, that any repricing of assets or liabilities occurs at current product or market rates for the alternative rate environments as of the dates presented, and that different prepayment rates are used in each alternative interest rate environment. The estimated MVPE results from the valuation of cash flows from financial assets and liabilities over the anticipated lives of each for each interest rate environment. The table below presents the effects of the change in interest rates on our assets and liabilities as they mature, repay, or reprice, as shown by the change in the MVPE in changing interest rate environments.

| | | | | |

Change | | Percentage Change in MVPE | |

(in Basis Points) | | At September 30, | |

in Interest Rates(1) | | 2012 | | 2011 | |

-100 bp | | N/A | | N/A | |

000 bp | | -- | | -- | |

+100 bp | | 3.09 | % | 0.61 | % |

+200 bp | | (3.72) | % | (5.69) | % |

+300 bp | | (13.79) | % | (14.91) | % |

(1)Assumes an instantaneous, permanent and parallel change in interest rates at all maturities.

Changes in the estimated market values of our financial assets and liabilities drive changes in estimates of MVPE. The market value of an asset or liability reflects the present value of all the projected cash flows over its remaining life, discounted at current market interest rates. As interest rates rise, the market value for both assets and liabilities decrease. The opposite is generally true as interest rates fall. The MVPE represents the theoretical market value of capital that is calculated by netting the market value of assets and liabilities. If the market values of assets increase at a faster pace than the market values of liabilities, or if the market values of liabilities decrease at a faster pace than the market values of assets, the MVPE will increase. The magnitude of the changes in the Bank’s MVPE represents the Bank’s interest rate risk. The market value of shorter term-to-maturity financial instruments are less sensitive to changes in interest rates than are longer term-to-maturity financial instruments. Because of this, our certificates of deposit (which generally have relatively short average lives) tend to display less sensitivity to changes in interest rates than do our mortgage-related assets (which generally have relatively long average lives). The average life expected on our mortgage-related assets varies under different interest rate environments because borrowers have the ability to prepay their mortgage loans. Therefore, as interest rates decrease, the average life of mortgage-related assets decrease as well. As interest rates increase, the average life would be expected to increase as well.

At September 30, 2012, the average life of the Bank’s mortgage-related assets were shorter than the average life of the Bank’s long-term borrowings and core deposits due to the historical low level of interest rates. Because the level of interest rates at both September 30, 2012 and 2011 were at historical lows, prepayment projections for mortgage-related assets and call projections for callable agency debentures were high, thereby significantly reducing the average life for these assets. As interest rates rise, the market values of the Bank’s liabilities decrease at a faster pace than that of its assets. As a result, the Bank’s MVPE increases in the +100 basis point interest rate environment.

As interest rates move higher in the +200 and +300 basis point interest rate environments, prepayment projections for mortgage-related assets, in general, are expected to decrease significantly. As interest rates rise to these levels, projected prepayments would likely only be realized through normal changes in borrowers’ lives, such as divorce, death, job-related relocations, or other life changing events, resulting in an increase in the average life of these assets. Call projections for the Bank’s callable agency debentures would also decrease significantly as interest rates rise to these levels, which would result in the cash flows for these assets to move to their contractual maturity. The longer expected average lives of these assets, relative to the assumptions in the base case environment, increases their sensitivity to changes in interest rates. As a result, the Bank’s sensitivity to rising interest rates increases to such a point that the expected decrease in the market value of the Bank’s assets more than offsets the decrease in the market value of liabilities, resulting in a decrease in the MVPE in these interest rate environments.

The sensitivity of the MVPE improved in all interest rate environments from September 30, 2011 to September 30, 2012. This was due to the decrease in interest rates between periods, primarily mortgage rates. This decrease resulted in a decrease in the weighted average life (“WAL”) of all mortgage-related assets compared to the prior fiscal year. This resulted in a decrease in the price sensitivity of all mortgage-related assets, and, as a result, of interest-earning assets as a whole. Since the price sensitivity of all assets is reduced in the base case, the adverse impact to rising interest rates is thereby reduced in all interest rate environments presented.

Gap Table. The gap table summarizes the anticipated maturities or repricing of the Bank’s interest-earning assets and interest-bearing liabilities as of September 30, 2012, based on the information and assumptions set forth in the notes below.

| | | | | | | | | | | | | | | | | |

| Within | | Three to | | More Than | | More Than | | | | |

| Three | | Twelve | | One Year to | | Three Years | | Over | | |

| Months | | Months | | Three Years | | to Five Years | | Five Years | | Total |

Interest-earning assets: | | (Dollars in thousands) |

Loans receivable: (1) | | | | | | | | | | | | | | | | | |

Mortgage loans: | | | | | | | | | | | | | | | | | |

Fixed | $ | 389,435 | | $ | 1,216,094 | | $ | 1,288,642 | | $ | 485,581 | | $ | 902,174 | | $ | 4,281,926 |

Adjustable | | 97,009 | | | 732,781 | | | 281,560 | | | 58,419 | | | 15,570 | | | 1,185,339 |

Other loans | | 118,945 | | | 14,101 | | | 13,474 | | | 4,502 | | | 4,320 | | | 155,342 |

Investment securities (2) | | 271,424 | | | 267,067 | | | 248,312 | | | 109,605 | | | 1,585 | | | 897,993 |

MBS (3) | | 299,250 | | | 882,746 | | | 630,745 | | | 230,397 | | | 254,667 | | | 2,297,805 |

Other interest-earning assets | | 117,483 | | | -- | | | -- | | | -- | | | -- | | | 117,483 |

Total interest-earning assets | | 1,293,546 | | | 3,112,789 | | | 2,462,733 | | | 888,504 | | | 1,178,316 | | | 8,935,888 |

| | | | | | | | | | | | | | | | | |

Interest-bearing liabilities: | | | | | | | | | | | | | | | | | |

Deposits: | | | | | | | | | | | | | | | | | |

Checking (4) | | 95,417 | | | 44,422 | | | 95,327 | | | 76,633 | | | 294,705 | | | 606,504 |

Savings (4) | | 80,711 | | | 12,010 | | | 27,692 | | | 21,478 | | | 119,042 | | | 260,933 |

Money market (4) | | 62,379 | | | 241,973 | | | 364,922 | | | 180,345 | | | 569,991 | | | 1,419,610 |

Certificates | | 379,267 | | | 890,522 | | | 1,011,563 | | | 289,020 | | | 1,872 | | | 2,572,244 |

Borrowings (5) | | 100,000 | | | 372,827 | | | 1,170,000 | | | 975,000 | | | 347,260 | | | 2,965,087 |

Total interest-bearing liabilities | | 717,774 | | | 1,561,754 | | | 2,669,504 | | | 1,542,476 | | | 1,332,870 | | | 7,824,378 |

| | | | | | | | | | | | | | | | | |

Excess (deficiency) of interest-earning assets over | | | | | | | | | | | | | | | | | |

interest-bearing liabilities | $ | 575,772 | | $ | 1,551,035 | | $ | (206,771) | | $ | (653,972) | | $ | (154,554) | | $ | 1,111,510 |

| | | | | | | | | | | | | | | | | |

Cumulative excess of interest-earning | | | | | | | | | | | | | | | | | |

assets over interest-bearing liabilities | $ | 575,772 | | $ | 2,126,807 | | $ | 1,920,036 | | $ | 1,266,064 | | $ | 1,111,510 | | | |

| | | | | | | | | | | | | | | | | |

Cumulative excess of interest-earning | | | | | | | | | | | | | | | | | |

assets over interest-bearing liabilities as a | | | | | | | | | | | | | | | | | |

percent of total assets (one-year gap) at September 30, 2012 | | 6.18% | | | 22.82% | | | 20.61% | | | 13.59% | | | 11.93% | | | |

| | | | | | | | | | | | | | | | | |

Cumulative one-year gap - interest rates +200 bp | | | | | | | | | | | | | | | | | |

at September 30, 2012 | | | | | 2.60% | | | | | | | | | | | | |

Cumulative one-year gap at September 30, 2011 | | | | | 18.60% | | | | | | | | | | | | |

Cumulative one-year gap at September 30, 2010 | | | | | 20.69% | | | | | | | | | | | | |

| (1) | Adjustable-rate mortgage (“ARM”) loans are included in the period in which the rate is next scheduled to adjust or in the period in which repayments are expected to occur, or prepayments are expected to be received, prior to their next rate adjustment, rather than in the period in which the loans are due. Fixed-rate loans are included in the periods in which they are scheduled to be repaid, based on scheduled amortization and prepayment assumptions. Balances have been reduced for loans 90 or more days delinquent or in foreclosure, which totaled $19.5 million at September 30, 2012. |

| (2) | Based on contractual maturities, term to call dates or pre-refunding dates as of September 30, 2012, and excludes the unrealized gain adjustment of $3.7 million on AFS investment securities. |

| (3) | Reflects estimated prepayments of MBS in our portfolio, and excludes the unrealized gain adjustment of $35.1 million on AFS MBS. |

| (4) | Although the Bank’s checking, savings and money market accounts are subject to immediate withdrawal, management considers a substantial amount of these accounts to be core deposits having significantly longer effective maturities. The decay rates (the assumed rate at which the balance of existing accounts would decline) used on these accounts are based on assumptions developed from our actual experience with these accounts. If all of the Bank’s checking, savings and money market accounts had been assumed to be subject to repricing within one year, interest-bearing assets which were estimated to mature or reprice within one year would have exceeded interest-earning liabilities with comparable characteristics by $376.7 million, for a cumulative one-year gap of 4.0% of total assets. |

| (5) | Borrowings exclude $20.0 million of deferred prepayment penalty costs and $274 thousand of deferred gain on the terminated interest rate swap agreements. |

Cash flow projections for mortgage loans and MBS are calculated based on current interest rates. Prepayment projections are subjective in nature, involve uncertainties and assumptions and, therefore, cannot be determined with a high degree of accuracy. Although certain assets and liabilities may have similar maturities or periods to repricing, they may react differently to changes in market interest rates. Assumptions may not reflect how actual yields and costs respond to market changes. The interest rates on certain types of assets and liabilities may fluctuate in advance of changes in market interest rates, while interest rates on other types of assets and liabilities may lag behind changes in market interest rates. Certain assets, such as ARM loans, have features that restrict changes in interest rates on a short-term basis and over the life of the asset. In the event of a change in interest rates, prepayment and early withdrawal levels would likely deviate significantly from those assumed in calculating the gap table. For additional information regarding the impact of changes in interest rates, see the “Percentage Change in Net Interest Income” and “Percentage Change in MVPE” discussion and tables within this section.

The increase in the one-year gap to 22.82% at September 30, 2012, from 18.60% at September 30, 2011, was due primarily to an increase in the amount of assets expected to reprice in fiscal year 2013 as compared to fiscal year 2012. The increase was due primarily to a decrease in mortgage rates at September 30, 2012 as compared to September 30, 2011. The decrease in mortgage rates increased prepayment expectations and thus increased the amount of assets expected to reprice in fiscal year 2013, as compared to fiscal year 2012. Additionally, a $342.5 million bulk loan ARM purchase during the fourth quarter of fiscal year 2012 increased the amount of assets repricing within the next 12 months as a portion the funds used to purchase these loans would have been used to purchase securities with longer repricing characteristics.

As noted above, changes in interest rates have a material impact on the amount of cash flows expected to reprice in a given period, primarily on the asset side of the balance sheet. In the +200 basis point interest rate environment, the cash flows from mortgage-related assets and callable agency debentures decreased significantly as borrowers and issuers no longer have an economic incentive to refinance their mortgages or debentures. In this interest rate environment, the Bank’s assets would reprice at a significantly slower pace than the base case environment.

Financial Condition

Assets. Total assets decreased $72.5 million, from $9.45 billion at September 30, 2011 to $9.38 billion at September 30, 2012, due primarily to a $561.8 million decrease in the securities portfolio, partially offset by an increase of $458.3 million in loans receivable, net and an increase in cash and cash equivalents of $20.6 million.

Loans Receivable. The net loans receivable portfolio increased $458.3 million, or 8.9%, to $5.61 billion at September 30, 2012, from $5.15 billion at September 30, 2011. The increase in the portfolio was due primarily to an increase in one- to four-family loans resulting largely from $630.2 million of bulk and correspondent loan purchases during the current fiscal year. Included in the $630.2 million of total purchases was $342.5 million related to one bulk loan purchase in the fourth quarter of the current fiscal year. The purchase was funded with cash flows from the Bank’s securities portfolio, using the FHLB line-of-credit to temporarily fund the purchase due to the timing of those cash flows. The FHLB line-of-credit was repaid before September 30, 2012. The loans are ARM loans that reprice annually at various times throughout the year. The weighted average rate of the loans was 2.48% at the time of purchase, which was higher than the yield available on similar duration securities. The seller of the loans has guaranteed, and has the ability, to repurchase or replace delinquent loans.

The following table presents characteristics of our loan portfolio as of September 30, 2012 and September 30, 2011. The weighted average rate of the loan portfolio decreased 54 basis points from 4.69% at September 30, 2011 to 4.15% at September 30, 2012. The decrease in the weighted average portfolio rate was due primarily to the endorsement of loans at current market rates, as well as the purchase and origination of loans during the year with rates less than the average rate of the existing portfolio. Within the one- to four-family loan portfolio at September 30, 2012, 70% of the loans had a balance at origination of less than $417 thousand.

| | | | | | | | | | | | |

| September 30, 2012 | | September 30, 2011 |

| | | Average | | | | | Average |

| Amount | | Rate | | | Amount | | Rate |

| (Dollars in thousands) |

Real Estate Loans: | | | | | | | | | | | | |

One-to four-family: | | | | | | | | | | | | |

Originated | $ | 4,032,581 | | 4.34 | % | | | $ | 3,986,957 | | 4.82 | % |

Correspondent purchased | | 575,502 | | 4.04 | | | | | 396,063 | | 4.75 | |

Bulk purchased | | 784,346 | | 2.94 | | | | | 535,758 | | 3.37 | |

Multi-family and commercial | | 48,623 | | 5.64 | | | | | 57,965 | | 6.13 | |

Construction | | 52,254 | | 4.08 | | | | | 47,368 | | 4.27 | |

Total real estate loans | | 5,493,306 | | 4.11 | | | | | 5,024,111 | | 4.66 | |

| | | | | | | | | | | | |

Consumer Loans: | | | | | | | | | | | | |

Home equity | | 149,321 | | 5.42 | | | | | 164,541 | | 5.48 | |

Other | | 6,529 | | 4.77 | | | | | 7,224 | | 5.10 | |

Total consumer loans | | 155,850 | | 5.39 | | | | | 171,765 | | 5.46 | |

| | | | | | | | | | | | |

Total loans receivable | | 5,649,156 | | 4.15 | % | | | | 5,195,876 | | 4.69 | % |

| | | | | | | | | | | | |

Less: | | | | | | | | | | | | |

Undisbursed loan funds | | 22,874 | | | | | | | 22,531 | | | |

ACL | | 11,100 | | | | | | | 15,465 | | | |

Discounts/unearned loan fees | | 21,468 | | | | | | | 19,093 | | | |

Premiums/deferred costs | | (14,369) | | | | | | | (10,947) | | | |

Total loans receivable, net | $ | 5,608,083 | | | | | | $ | 5,149,734 | | | |

Included in the loan portfolio at September 30, 2012 were $136.2 million, or 2.4% of the total loan portfolio, of ARM loans that were originated as interest-only. Of these interest-only loans, $113.6 million were purchased in bulk loan packages from nationwide lenders, primarily during fiscal year 2005. Interest-only ARM loans do not typically require principal payments during their initial term, and have initial interest-only terms of either five or 10 years. The $113.6 million of purchased interest-only ARM loans held as of September 30, 2012, had a weighted average credit score of 724 and a weighted average LTV ratio of 71% at September 30, 2012. At September 30, 2012, $67.0 million, or 49%, of the interest-only loans were still in their interest-only payment term. At September 30, 2012, $6.2 million, or 19% of non-performing loans, were interest-only ARMs.

The following tables present the weighted average credit score, LTV ratio, and average unpaid principal balance for our one- to four-family loans as of the dates presented. Credit scores were updated in September of each year presented and obtained from a nationally recognized consumer rating agency. The LTV ratios were based on the current loan balance and either the lesser of the purchase price or original appraisal, the most recent bank appraisal or broker price opinion (“BPO”). In most cases, the most recent appraisal was obtained at the time of origination.

| | | | | | | | | | | | | | | |

| September 30, 2012 | | September 30, 2011 |

| Credit | | | | | Average | | Credit | | | | | Average |

| Score | | LTV | | Balance | | Score | | LTV | | Balance |

| (Dollars in thousands) |

Originated | 763 | | 65 | % | | $ | 124 | | 763 | | 66 | % | | $ | 123 |

Correspondent purchased | 761 | | 65 | | | | 326 | | 759 | | 64 | | | | 290 |

Bulk purchased | 749 | | 67 | | | | 316 | | 740 | | 60 | | | | 252 |

| 761 | | 65 | % | | $ | 147 | | 760 | | 65 | % | | $ | 137 |

The following table presents the rates and WAL in years, which reflects prepayment assumptions, of our loan portfolio as of September 30, 2012. The terms listed under fixed-rate one- to four-family loans represent original terms-to-maturity and the terms listed under adjustable-rate one- to four-family loans represent initial terms-to-repricing.

| | | | | | | |

| September 30, 2012 |

| Amount | | Rate | | WAL |

| (Dollars in thousands) |

Fixed-rate one- to four-family: | | | | | | | |

<= 15 years | $ | 1,059,416 | | 4.00 | % | | 2.6 |

> 15 years | | 3,157,909 | | 4.53 | | | 3.6 |

Adjustable-rate one- to four-family: | | | | | | | |

<= 36 months | | 460,444 | | 2.73 | | | 3.6 |

> 36 months | | 714,660 | | 3.26 | | | 2.7 |

All other loans | | 256,727 | | 5.17 | | | 1.4 |

Total loans receivable | $ | 5,649,156 | | 4.15 | % | | 3.2 |

The Bank generally prices its one- to four-family loan products based upon prices available in the secondary market and competitor pricing. During fiscal year 2012, the average daily spread between the Bank’s 30-year fixed-rate one- to four-family loan offer rate, with no points paid by the borrower, and the 10-year Treasury rate was approximately 210 basis points, while the average daily spread between the Bank’s 15-year fixed-rate one- to four-family loan offer rate and the 10-year Treasury rate was approximately 130 basis points.