As filed with the Securities and Exchange Commission on July 30, 2010

Registration No. 333-166998

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 2

TO

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

| | | | |

| BUMBLE BEE CAPITAL CORP. | | BUMBLE BEE FOODS, LLC | | CONNORS BROS. CLOVER LEAF SEAFOODS COMPANY |

(Exact name of registrant

as specified in its charter) | | (Exact name of registrant as

specified in its organizational document) | | (Exact name of registrant as specified in its organizational document) |

| DELAWARE | | DELAWARE | | NOVA SCOTIA, CANADA |

(State or other jurisdiction of incorporation or organization) | | (State or other jurisdiction of incorporation or organization) | | (State or other jurisdiction of incorporation or organization) |

| 2000 | | 2000 | | 2000 |

(Primary Standard Industrial Classification Code Number) | | (Primary Standard Industrial Classification Code Number) | | (Primary Standard Industrial Classification Code Number) |

| 01-0937816 | | 45-0510146 | | Not applicable |

(IRS Employer Identification No.) 9655 Granite Ridge Drive, Suite 100 San Diego, CA 92123 (858) 715-4000 | | (IRS Employer Identification No.) 9655 Granite Ridge Drive, Suite 100 San Diego, CA 92123 (858) 715-4000 | | (IRS Employer Identification No.) 80 Tiverton Court Suite 600 Markham , ON L3R 0G4 (905) 474-0608 |

| | |

| | |

| | |

| (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) | | (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) | | (Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices) |

Jill Irvin, Esq.

9655 Granite Ridge Drive, Suite 100

San Diego, CA 92123

(858) 715-4000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Mark E. Thierfelder, Esq.

Dechert LLP

1095 Avenue of the Americas

New York, NY 10036-6797

(212) 698-3500

Approximate date of commencement of proposed sale of the securities to the public: As soon as practicable after this registration statement becomes effective.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

| | | | |

Large accelerated filer ¨ | | Accelerated filer | | ¨ |

Non-accelerated filer x (Do not check if a smaller reporting company) | | Smaller reporting company | | ¨ |

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

|

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) ¨ |

Exchange Act Rule 14d-1(d) (Cross-Border Third-Party Tender Offer) ¨ |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

TABLE OF ADDITIONAL REGISTRANTS

| | | | | | | | |

Exact Name of Registrant Guarantor as Specified in its Organizational Document | | State or Other

Jurisdiction of

Incorporation or

Organization | | Primary Standard

Industrial Classification

Code Number | | IRS Employer

Identification No. | | Address, including Zip Code,

and Telephone Number,

including Area Code, of

Registrant Guarantor’s Principal

Executive Offices |

6162410 Canada Limited | | Canada | | 2000 | | N/A | | 669 Main Street, Blacks Harbour, NB E5H 1K1 |

| | | | |

BB Acquisition (PR), L.P. | | Delaware | | 2000 | | 83-0359228 | | 3075 Carr 64, 00682-6031, Mayaguez, Puerto Rico |

| | | | |

Bumble Bee Holdings, Inc. | | Georgia | | 2000 | | 58-1931051 | | 9655 Granite Ridge Drive, Suite 100, San Diego, CA 92123 |

| | | | |

Bumble Bee International (PR), Inc. | | Cayman Islands | | 2000 | | N/A | | Post Office Box 309GT, Ugland House, South Church Street, George Town, Grand Cayman Island |

| | | | |

Clover Leaf Dutch

Holdings, LLC | | Delaware | | 2000 | | 74-3219267 | | c/o Centre Partners Management LLC, 30 Rockefeller Plaza, 50th Floor, New York, NY 10020 |

| | | | |

Clover Leaf Holdings Company | | Nova Scotia,

Canada | | 2000 | | N/A | | 80 Tiverton Court Suite 600 Markham, ON L3R 0G4 |

| | | | |

Clover Leaf Seafood 2 B.V. | | The Netherlands | | 2000 | | N/A | | Strawinskylaan 3105 Atrium, 1077 ZX Amsterdam, the Netherlands |

| | | | |

Clover Leaf Seafood B.V. | | The Netherlands | | 2000 | | N/A | | Strawinskylaan 3105 Atrium, 1077 ZX Amsterdam, the Netherlands |

| | | | |

Clover Leaf Seafood Coöperatief U.A. | | The Netherlands | | 2000 | | N/A | | Strawinskylaan 3105 Atrium, 1077 ZX Amsterdam, the Netherlands |

| | | | |

Connors Bros. Holdings, L.P. | | Delaware | | 2000 | | N/A | | c/o Centre Partners Management, LLC, 30 Rockefeller Plaza, 50th Floor, New York, NY 10020 |

| | | | |

K.C.R. Fisheries Ltd. | | New Brunswick,

Canada | | 2000 | | N/A | | 669 Main Street, Blacks Harbour, NB E5H 1K1 |

| | | | |

Stinson Seafood (2001), Inc. | | Delaware | | 2000 | | 04-3625659 | | 200 Main Street, P.O. Box 69, Prospect Harbor, ME 04669 |

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 30, 2010

PRELIMINARY PROSPECTUS

Bumble Bee Foods, LLC

Connors Bros. Clover Leaf Seafoods Company

Bumble Bee Capital Corp.

Exchange Offer for $220,000,000

7.75% Senior Secured Notes due 2015

THE NOTES

| | • | | We are offering to issue $220,000,000 of our 7.75% Senior Secured Notes due 2015, whose issuance is registered under the Securities Act of 1933, as amended (the “Securities Act”), which we refer to as the exchange notes, in exchange for a like aggregate principal amount of 7.75% Senior Secured Notes due 2015, which were issued on December 17, 2009 and which we refer to as the initial notes. The exchange notes will be issued under the existing indenture, dated as of December 17, 2009. |

| | • | | Interest on the exchange notes will accrue at a rate per annum equal to 7.75% and will be payable semi-annually in cash in arrears on each June 15 and December 15, beginning on June 15, 2010. The exchange notes will mature on December 15, 2015. |

| | • | | The exchange notes will be guaranteed on a senior secured basis by Connors Bros. Holdings, L.P. (“Parent Guarantor”) and each of Parent Guarantor’s existing subsidiaries and certain future subsidiaries that guarantee our senior credit facilities. |

| | • | | The exchange notes and the guarantees will be our and the guarantors’ senior obligations. The exchange notes will rank equally in right of payment with all of our existing and future senior obligations and senior in right of payment to all of our existing and future subordinated obligations. The guarantees will rank equally in right of payment with the guarantors’ existing and future senior obligations and senior in right of payment to their future subordinated obligations. |

| | • | | The exchange notes and the guarantees will be secured by a third-priority lien on substantially all of our assets and the assets of the guarantors that secure our obligations under our senior credit facilities as described herein. The exchange notes and the guarantees will be effectively subordinated to our secured debt that is secured by a lien ranking prior to the lien on the collateral for the exchange notes and the guarantees, including obligations under our senior credit facilities, to the extent of the value of the assets securing such debt, and any obligations that are secured by any of our assets that are not part of the collateral for the exchange notes and guarantees, to the extent of the value of assets securing such obligations. See “Description of Notes—Security.” |

THE TERMS OF THE EXCHANGE OFFER

| | • | | It will expire at 5:00 p.m., New York City time, on , 2010, unless we extend it. |

| | • | | If all the conditions to the exchange offer are satisfied, we will exchange all of our initial notes that are validly tendered and not withdrawn for the exchange notes. |

| | • | | You may withdraw your tender of initial notes at any time before the expiration of the exchange offer. We will exchange all of the outstanding initial notes that are validly tendered and not withdrawn. |

| | • | | We believe that the exchange of the initial notes will not be a taxable event for U.S. federal income tax purposes, but you should see “Certain U.S. Federal Income Tax Considerations” on page164 of this prospectus for more information. |

| | • | | We will not receive any proceeds from the exchange offer. |

| | • | | The exchange notes that we will issue to you in exchange for your initial notes will be substantially identical to your initial notes except that, unlike your initial notes, the exchange notes will have no transfer restrictions or registration rights. We are making the exchange offer to satisfy your registration rights, as a holder of the initial notes. |

| | • | | The exchange notes that we will issue to you in exchange for your initial notes are new securities with no established market for trading. We do not intend to list the exchange notes on any national securities exchange or quotation system. |

| | • | | Broker-dealers who receive exchange notes pursuant to the exchange offer must acknowledge that they will deliver a prospectus in connection with any resale of such exchange notes. |

| | • | | Broker-dealers who acquired the initial notes as a result of market-making or other trading activities may use this prospectus for the exchange offer, as supplemented or amended, in connection with resales of the exchange notes. |

You should see theRisk Factors beginning on page 15 of this prospectus for a discussion of business and financial risks that you should consider carefully prior to participating in the exchange offer.

Neither the Securities and Exchange Commission (the “SEC”) nor any state or other domestic or foreign securities commission or regulatory authority has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2010

TABLE OF CONTENTS

We have not authorized anyone to give any information or represent anything to you other than the information contained in this prospectus. You must not rely on any unauthorized information or representations.

INCORPORATED INFORMATION

This prospectus incorporates important business and financial information that is not included or delivered with this prospectus. This information is available free of charge to noteholders upon written or oral request to:

Connors Bros. Holdings, L.P.

9655 Granite Ridge Drive

San Diego, CA 92123

Attention: General Counsel

(858) 715-4000

To ensure timely delivery, you should request any information no later than five business days prior to the expiration of the exchange offer.

PRESENTATION OF FINANCIAL INFORMATION

The historical financial data presented in this prospectus for the fiscal years ended December 31, 2009 and December 31, 2008, the three months ended April 3, 2010 and the three months ended April 4, 2009 represents that of Connors Bros. Holdings, L.P. (“CBH” or “Parent Guarantor”) and Bumble Bee Foods, L.P. (f/k/a Connors Bros., L.P.) (“BBFLP”) (both referred to herein as the “Successor”). Effective December 17, 2009, BBFLP is no longer included in our consolidated financial statements. The historical financial data presented in this prospectus for the fiscal year ended December 31, 2008 has been derived by combining the historical financial data of Connors Bros. Income Fund (the “Predecessor”) for the period from January 1, 2008 to November 22, 2008, and the Successor for the period from November 23, 2008 (inception) to December 31, 2008. The historical financial data presented in this prospectus for the fiscal years ended December 31, 2007, December 31, 2006 and December 31, 2005 represents that of the Predecessor. We report results of operations on a calendar year basis with fiscal quarters of approximately 13 weeks or three months’ duration.

On December 1, 2009, BBFLP formed CBH as a wholly owned subsidiary for the purpose of holding all of its subsidiary ownership interests that were transferred from BBFLP to Parent Guarantor (the “Transfer of Investments”) concurrently with the closing of the sale of the initial notes. Upon completion of the Transfer of Investments, CBH became the ultimate parent company for reporting purposes of the consolidated group of companies comprising the issuers. BBFLP historically has had, on a stand-alone basis, immaterial interest income and immaterial operating expenses. The preferred partnership units of BBFLP, the general and limited partnership equity of BBFLP, and the accumulated deficit of BBFLP has been, effective with the Transfer of Investments on December 17, 2009, excluded from the consolidated balance sheet of Successor. As such, our consolidated statement of partnership equity for the year ended December 31, 2009 reflects the exit of BBFLP as the top consolidating entity and the issuance of partnership equity by CBH. Our consolidated balance sheet as of December 31, 2009 no longer includes related party notes and receivables, redeemable preferred partnership units, the general partnership unit, class A common partnership units and accumulated deficit of BBFLP.

ENFORCEABILITY OF CIVIL LIABILITIES

Connors Bros. Clover Leaf Seafoods Company and certain of the guarantors of the notes are corporations incorporated or other entities organized under the laws of Nova Scotia, Canada, the Netherlands, the Cayman Islands and other non-U.S. jurisdictions. Two of our directors and officers named in this prospectus are residents of jurisdictions outside of the U.S., and a significant portion of our assets are located outside the U.S. These non-U.S. entities have agreed, in accordance with the terms of the indenture under which the initial notes were issued, to accept service of process in any suit, action or proceeding with respect to the indenture or the notes brought in any federal or state court located in New York City by an agent designated for such purpose, and to submit to the jurisdiction of such courts in connection with such suits, actions or proceedings. However, it may be difficult for holders of the notes to effect service within the U.S. upon directors and officers who are not residents of the U.S. or to realize in the U.S. upon judgments of courts of the U.S. predicated upon civil liability under U.S. federal or state securities laws. We have been advised by Torys LLP, our Canadian counsel, that there is doubt as to the enforceability in Canada against these non-U.S. entities or our directors and officers who are not residents of the U.S., in original actions or in actions for enforcement of judgments of courts of the U.S., of liabilities predicated solely upon U.S. federal or state securities laws.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements that are based on our management’s beliefs and assumptions and on information currently available to us. The use of any words such as “anticipate,” “continue,” “estimate,” “expect,” “may,” “might,” “will,” “project,” “should,” “believe,” “intend,” “continue,” “could,” “plan,” “predict” and negatives of these words and similar expressions are intended to identify forward-looking

ii

statements. In particular, statements about our expectations, beliefs, plans, objectives, assumptions or future events or performance contained in this prospectus are forward- looking statements. These statements are based on, but not limited to, management’s assessment of such factors as expected consumer demand, resource supply and competitive environment. These assessments could prove inaccurate.

We have based these forward-looking statements on our current expectations, assumptions, estimates and projections. While we believe these expectations, assumptions, estimates and projections are reasonable, such forward-looking statements are only predictions and involve known and unknown risks and uncertainties, many of which are beyond our ability to control. These and other important factors, including those discussed in this prospectus under the headings “Prospectus Summary,” “Risk Factors,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business,” may cause our actual results, performance or achievements to differ materially from any future results, performance or achievements expressed or implied by these forward-looking statements. Some of the key factors that could cause actual results to differ from our expectations include:

| | • | | fluctuations in commodity prices, including wholesale tuna and energy costs; |

| | • | | the competitive environment in the shelf-stable seafood industry; |

| | • | | continued consolidation of our retail customers or the loss of a significant customer; |

| | • | | the decline in the supply of tuna or biomass of wild fish stocks in the fisheries in which we operate or disruption in our ability to procure such biomass; |

| | • | | reduction in revenue due to declining consumption trends; |

| | • | | certain hazards and liability risks associated with canned food products, including the impact of recalls; |

| | • | | uninsured and underinsured losses; |

| | • | | pension plans that are not fully funded; |

| | • | | our exposure to changes in foreign currency exchange rates and variations in interest rates; |

| | • | | changes in U.S. government trade policy; |

| | • | | our exposure to product liability and product safety-related claims; |

| | • | | changes in the laws, rules, regulations and policies with respect to the production, processing, preparation, distribution, packaging and labeling of food products; |

| | • | | our failure to comply with, or adverse changes to, environmental, health and safety regulations; |

| | • | | the actual or perceived health risks posed by methylmercury in seafood products, including tuna; |

| | • | | employment disputes, deterioration of labor relations and our inability to attract and retain qualified employees; |

| | • | | changes in import and export duties, wage rates and political or economic climates in the countries in which we operate; |

| | • | | failure by a supplier or co-packer to fulfill its obligations to supply us with certain products; |

| | • | | general risks of the food industry; |

| | • | | our breach of any of the covenants or other provisions in our debt agreements; |

| | • | | the success of our marketplace initiatives and acceptance by consumers of our products; |

| | • | | risks related to our substantial indebtedness; |

| | • | | downgrades in our credit ratings; |

| | • | | the loss or dilution of important intellectual property rights; |

iii

| | • | | our inability to improve productivity and control or reduce costs; |

| | • | | departure of members of senior management; |

| | • | | the control of our operation by Centre Partners V L.P.; |

| | • | | impact of severe weather, natural disasters and climate change; and |

| | • | | other risks and uncertainties detailed elsewhere in this prospectus, including those listed under the caption “Risk Factors.” |

Given these risks and uncertainties, you are cautioned not to place undue reliance on such forward-looking statements. The forward-looking statements included in this prospectus are made only as of the date hereof. We do not undertake and specifically decline any obligation to update any such statements or to publicly announce the results of any revisions to any such statements to reflect future events or developments.

MARKETS, RANKING AND OTHER DATA

The data included in this prospectus regarding categories, segments and ranking, including the position of us and our competitors within these categories, are based on independent industry publications or databases, reports of government agencies or other published industry sources, including the National Marine Fisheries Service, the National Fisheries Institute and The Nielsen Company, and our estimates based on our management’s knowledge and experience in the categories and segments in which we operate. Industry publications and surveys generally state that they have obtained information from sources believed to be reliable, but do not guarantee the accuracy and completeness of such information. Unless noted otherwise, where reference is made to category or segment share, or ranking within a category or segment, such data is derived from The Nielsen Company’s All-Channel dollar sales data for the 52 weeks ending December 26, 2009 for U.S. data and December 19, 2009 for Canadian data. The “All-Channel” data is licensed to Bumble Bee Foods, LLC in the form of a database customized to Bumble Bee specifications; the “All-Channel” data is derived from consumption data provided to Nielsen by samples of consumers as well as samples of retail stores in the U.S. and the Canadian market. The “All-Channel” data represents Nielsen’s estimate of consumption in all classes of retail trade including grocery, drugstores, mass merchandisers and club stores. While we believe that each of these studies and publications is reliable, we have not independently verified such data and do not make any representation as to the accuracy or completeness of such information. Similarly, our internal research, which includes certain consumer surveys and studies, is based upon our understanding of industry conditions and we believe it to be reliable but it has not been verified by any independent sources.

TRADEMARKS

In this prospectus, we refer (without the ownership notation after the initial use) to several registered trademarks that we own, includingBumble Bee®,Clover Leaf®,Brunswick®,Beach Cliff®,Snow’s® andSweet Sue®. All brand names or other trademarks appearing in this prospectus are the property of their respective owners.

iv

PROSPECTUS SUMMARY

The following summary should be read in connection with, and is qualified in its entirety by, the more detailed information and financial statements (including the accompanying notes) appearing elsewhere in this prospectus. See “Risk Factors” for a discussion of certain factors that should be considered in connection with the exchange offer.

In this prospectus, unless the context otherwise requires, the “Company,” “we,” “us,” or “our” refers to Parent Guarantor and its subsidiaries, and the “issuers” refers to Bumble Bee Foods, LLC, Connors Bros. Clover Leaf Seafoods Company and Bumble Bee Capital Corp., collectively. When we use the term “notes” in this prospectus, the term includes the initial notes and the exchange notes.

OUR COMPANY

We are the largest producer and marketer of shelf-stable seafood in North America and maintain a leading share in virtually all segments of the U.S. and Canadian shelf-stable seafood categories. We operate in the United States as Bumble Bee Foods, LLC (“Bumble Bee”) and in Canada as Connors Bros. Clover Leaf Seafoods Company (“Clover Leaf”). Clover Leaf also conducts our business outside of North America. Headquartered in San Diego, California, we have grown since our inception in 1897 from a salmon canning cooperative in Astoria, Oregon into a leading producer and provider of shelf-stable tuna, salmon, sardines, clams and other specialty products. Our top three brands,Bumble Bee,Clover LeafandBrunswick, each have nearly 100 year histories and maintain strong consumer awareness, with ourBumble Bee andClover Leafbrands both enjoying nearly 90% consumer awareness levels in the U.S. and Canada, respectively. We strategically focus on higher-margin seafood products such as albacore tuna, sockeye salmon and certain specialty items, while incorporating an array of lower-margin products such as lightmeat tuna and pink salmon to leverage our infrastructure and meet our customers’ preference for single-source suppliers. In the U.S., we are #1 in shelf-stable seafood, holding a #1 or #2 share position in nearly every product segment in which we compete. In the U.S., we hold the #1 share position in albacore tuna, canned salmon, sardines and clams, and the #2 share position in the overall U.S. shelf-stable tuna category. In Canada, we are #1 in shelf-stable seafood, holding the #1 share position for albacore tuna, lightmeat tuna, salmon and specialty seafood, including sardines and herring. We sell to a diversified customer base consisting of almost every major U.S. and Canadian food retailer and food distributor, including supermarkets, mass merchandisers, drug stores, warehouse clubs, dollar stores and independent grocers.

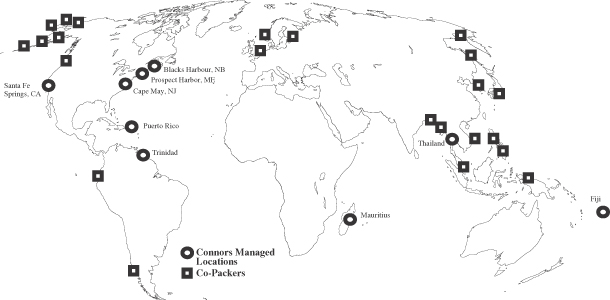

We maintain a global sourcing matrix, which allows us to selectively purchase raw materials from each of the world’s major oceans. Our established processing network provides us with the flexibility to take advantage of higher catches and lower prices in any of the world’s significant fisheries. Our processing facilities are strategically located adjacent to supply sources to enable direct access to fish, reduced labor costs and preferential duty status for certain items. As a result of our strategically located facilities, and our status as one of the world’s largest purchasers of tuna, tuna loins and canned seafood, we believe that we are a low cost operator in the shelf-stable seafood industry. We process approximately 60% of our own shelf-stable seafood requirements, with the balance co-packed by third-party suppliers. We operate tuna canning facilities in Puerto Rico and California, have exclusive supply contracts with tuna loin processing factories in Fiji, Mauritius and Trinidad, and have a joint venture partnership in a tuna processing facility in Thailand. Additionally, we own and operate a sardine canning facility in New Brunswick, Canada, as well as a clam canning facility in Cape May, New Jersey.

For the three months ended April 3, 2010, we generated revenues of $256.6 million, net income of $14.4 million and net cash provided by operating activities of $22.7 million. For the twelve months ended December 31, 2009, we generated revenues of $944.0 million, net income of $12.9 million and net cash provided by operating activities of $74.2 million. As of April 3, 2010 and December 31, 2009, our total assets were $799.0 million and $806.3 million, respectively. See “Summary Historical Consolidated Financial Data.”

1

Industry Overview

The shelf-stable seafood industry is generally divided into three significant categories:

| | • | | Tuna (including the higher-margin albacore tuna segment and lower-margin lightmeat tuna segment); |

| | • | | Salmon (including the higher-margin sockeye salmon segment and lower-margin pink salmon segment); and |

| | • | | Specialty seafood, which encompasses a wide variety of segments such as sardines, clams, crab, oysters, shrimp and other canned seafood. |

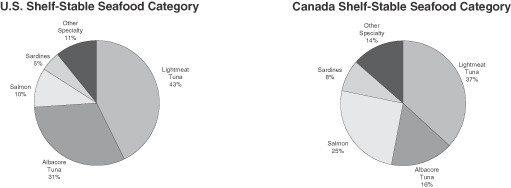

The total category size for U.S. shelf-stable seafood was approximately $2.4 billion for the 52 week period ended December 26, 2009, with tuna representing approximately $1.8 billion, or 74%, of the total U.S. shelf-stable seafood category. In the U.S., canned tuna is the second most consumed seafood behind shrimp (including frozen, fresh and canned), with nearly three pounds of canned tuna consumed per person each year. Additionally, canned tuna had a household penetration rate of approximately 68% as of 2008 according to Nielsen Household Panel Data and has been a staple of the U.S. diet for decades. The total tuna category can be further divided into albacore and lightmeat tuna. Albacore sales represented approximately 42% of total tuna dollar sales, but only 33% of tuna case volume, which reflects albacore tuna’s higher price point.

Salmon represented approximately $241.0 million, or 10%, of the total U.S. shelf-stable seafood category for the 52 week period ended December 26, 2009. The salmon category is comprised of pink and red (or sockeye) salmon.

The shelf-stable specialty seafood category is comprised of a wide variety of segments, including sardines, clams, crab, oysters, shrimp and other products, and represented approximately $380.0 million, or 16%, of the total U.S. shelf-stable seafood categoryfor the 52 week period ended December 26, 2009. The largest single segment in the specialty seafood category is sardines, which represented approximately $121.0 million, or 5% of the categoryfor such period.

In Canada, the shelf-stable seafood category was approximately C$394.0 million for the 52 week period ended December 19, 2009. The tuna category represented approximately C$209.0 million, or 53%, of the total Canadian shelf-stable seafood category for such period. Similar to the U.S., the tuna category in Canada is divided into lightmeat and albacore tuna. Salmon and specialty seafood have a much higher household penetration in Canada, as Canadian consumers include a much broader range of seafood in their diets. The salmon category in Canada was approximately C$99.0 million, or 25% of the total shelf-stable seafood category, versus 10% in the U.S. for the 52 week period ended December 26, 2009. Sardines and other specialty seafood represented C$32.0 million or 8% and C$53.0 million, or 14% of the total Canadian category for such period, respectively.

Our management team, led by industry veteran Chris Lischewski, has an average of 20 years of industry experience and over 250 years of collective experience. Our management team has demonstrated its ability to successfully improve operations and profitability, and to anticipate and respond effectively to industry trends and dynamics.

2

CENTRE PARTNERS RELATIONSHIP

We are currently controlled by affiliates of Centre Partners Management LLC, or Centre Partners. Centre Partners is a leading private equity firm focused on investments in the North American middle market. For more than two decades since its founding in 1986, the firm has maintained a disciplined and value-oriented investment philosophy. Centre Partners seeks to generate returns on equity investments by leveraging its long-standing relationships and its “Centre Resource Model” to develop exclusive and proprietary deal flow, to enhance the transaction review process, and to add value throughout the life of an investment. Centre Partners’ principals have invested over $3.2 billion in more than 100 companies in partnership with management teams across a broad spectrum of industries. Centre Partners has deep investment expertise covering consumer, healthcare, industrial products and services, financial services, energy, media, restaurants, retail and aviation services. The firm has an experienced investment team of 16 professionals located in New York and Los Angeles.

In November 2008, Centre Partners completed the acquisition of our company for approximately $650 million. Pursuant to the terms of a business acquisition agreement dated September 25, 2008, as amended on October 15, 2008, Bumble Bee Foods, L.P. (f/k/a Connors Bros., L.P.), through a newly created organizational structure, acquired shares in entities holding, directly or indirectly, all or substantially all of the assets of Connors Bros. Income Fund (the “Acquisition”). Bumble Bee Foods, L.P. is a limited partnership formed under the laws of Delaware on September 12, 2008 under the name Connors Bros., L.P. and is the sole limited partner and sole member of the general partner of CBH. The name of the limited partnership was changed on June 23, 2010.

CREDIT AGREEMENT AMENDMENTS

We entered into certain amendments (the “Credit Agreement Amendments”) to our existing senior revolving credit facility and senior term loan facility to, among other things, permit the completion of the note offering, the repayment of our existing senior subordinated loans, which we refer to as the senior subordinated notes, and other related transactions, which became effective contemporaneously with the December 17, 2009 note offering. The amendments to the senior revolving credit facility provide for, among other things, the addition of additional guarantors and changes in certain baskets, caps and thresholds. The amendments to the senior term loan facility also provide for, among other things, the reduction in the applicable LIBOR rate margin, LIBOR rate, base rate margin and base rate. See “Description of Other Indebtedness.”

RECENT DEVELOPMENTS

Engagement Letter

On July 30, 2010, Bumble Bee Foods, L.P., our ultimate parent, entered into an agreement with J.P. Morgan Securities Inc. to serve as its financial advisor to explore various strategic alternatives available to it and/or its direct and indirect subsidiaries. Strategic alternatives may include, but are not limited to, a sale of all or substantially all of its business and/or its direct and indirect subsidiaries, a merger or other business combination or a sale of all or substantially all of its assets.

Redemption of Notes

In accordance with Section 3.7(d) of the Indenture, we intend to redeem 10% of the original aggregate principal amount of the Notes prior to or contemporaneously with the completion of the exchange offer. The total redemption payment, excluding accrued interest, will be approximately $22.7 million, which includes principal of $22.0 million and a call premium of approximately $0.7 million. In the event we determine to proceed with the redemption, notice of the optional redemption will be delivered to each holder of the Notes in accordance with the relevant terms of the Indenture prior to or on the date of this prospectus.

3

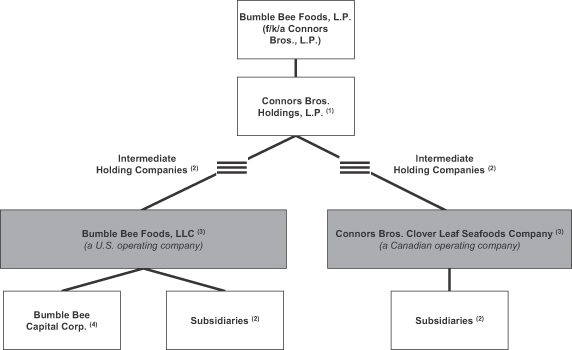

SUMMARY ISSUER STRUCTURE

The following chart summarizes our structure.

| (1) | Parent Guarantor of the notes and our senior credit facilities. |

| (2) | Guarantors of the notes and our senior credit facilities. |

| (3) | Co-issuer of the notes and co-borrower under our senior credit facilities. |

| (4) | Co-issuer formed to facilitate the note offering, which has no assets and conducts no operations. |

4

Summary of the Exchange Offer

The summary below describes selected terms of the exchange offer. Certain of the terms and conditions described below are subject to important limitations and exceptions. The section in this prospectus entitled “The Exchange Offer” contains a more detailed description of the terms and conditions of the exchange offer.

Note Offering | We sold $220.0 million of the initial notes on December 17, 2009 to Wells Fargo Securities, LLC, Jefferies & Company, Inc. and Barclays Capital Inc. We refer to these parties collectively in this prospectus as the “initial purchasers.” The initial purchasers subsequently resold $220.0 million of the initial notes: (i) to qualified institutional buyers pursuant to Rule 144A; or (ii) outside the United States in compliance with Regulation S, each as promulgated under the Securities Act. |

Registration Rights Agreement | On the date the initial notes were issued, we entered into an agreement with the initial purchasers, for the benefit of holders of the initial notes, in which we agreed to (1) use our reasonable best efforts to consummate the exchange offer within 270 calendar days after the issue date of the initial notes and (2) file a shelf registration statement for the resale of the initial notes if we cannot effect an exchange offer within the time period provided. |

The Exchange Offer | We will exchange up to $220.0 million aggregate principal amount at maturity of our exchange notes for a like aggregate principal amount at maturity of our initial notes. |

Expiration Date | 5:00 p.m., New York City time, on �� , 2010, unless we extend the expiration date. The expiration date of the exchange offer will be at least 20 business days after the commencement of the exchange offer in accordance with Rule 14e-1(a) under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). |

Conditions to the Exchange Offer | The exchange offer is subject to certain customary conditions, which we may waive in our sole discretion. For more information, see the section in this prospectus entitled “The Exchange Offer—Conditions to the Exchange Offer.” The exchange offer is not conditioned upon the exchange of any minimum principal amount of the initial notes. |

Procedures for Tendering Initial Notes | To participate in the exchange offer, you must complete, sign and date the letter of transmittal or its facsimile and transmit it, together with your initial notes to be exchanged and all other documents required by the letter of transmittal, to Deutsche Bank Trust Company Americas, as exchange agent, at its address indicated under “The Exchange Offer—Exchange Agent.” In the alternative, you can tender your initial notes by bookentry delivery following the procedures described in this prospectus. For more information on tendering your initial notes, please refer to the section in this prospectus entitled “The Exchange Offer—Procedures for Tendering Initial Notes.” |

5

Special Procedures for Beneficial Owners | If you are a beneficial owner of initial notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee and you wish to tender your initial notes in the exchange offer, you should contact the registered holder promptly and instruct that person to tender on your behalf. If you wish to tender in the exchange offer on your own behalf, you must, prior to completing and executing the letter of transmittal and delivering your initial notes, either make appropriate arrangements to register ownership of your initial notes in your name or obtain a properly completed bond power from the person or entity in whose name your initial notes are registered. The transfer of registered ownership may take considerable time. For more information, see the section in this prospectus entitled “The Exchange Offer—Procedures for Tendering Initial Notes.” |

Guaranteed Delivery Procedures | If you wish to tender your initial notes and you cannot get the required documents to the exchange agent on time, you may tender your initial notes by using the guaranteed delivery procedures described under the section in this prospectus entitled “The Exchange Offer—Procedures for Tendering Initial Notes—Guaranteed Delivery Procedure.” |

Withdrawal Rights | You may withdraw the tender of your initial notes at any time before 5:00 p.m., New York City time, on the expiration date of the exchange offer. To withdraw, you must send a written or facsimile transmission notice of withdrawal to the exchange agent at its address indicated under “The Exchange Offer—Exchange Agent” before 5:00 p.m., New York City time, on the expiration date of the exchange offer. |

Acceptance of Initial Notes and Delivery of Exchange Notes | If all the conditions to the completion of the exchange offer are satisfied, we will accept any and all initial notes that are tendered in the exchange offer in accordance with the procedures set forth below under “The Exchange Offer—Procedures for Tendering Initial Notes” on or before 5:00 p.m., New York City time, on the expiration date. We will return any initial note that we do not accept for exchange to you without expense promptly after the expiration date. We will deliver the exchange notes to you promptly after the expiration date. Please refer to the section in this prospectus entitled “The Exchange Offer—Acceptance of Initial Notes for Exchange; Delivery of Exchange Notes.” |

U.S. Federal Income Tax Considerations Relating to the Exchange Offer | We believe that exchanging your initial notes for exchange notes will generally not be a taxable event to you for United States federal income tax purposes. Please refer to the section in this prospectus entitled “Certain U.S. Federal Income Tax Considerations.” |

Exchange Agent | Deutsche Bank Trust Company Americas is serving as exchange agent in the exchange offer. For the address, telephone number and facsimile number of the exchange agent, please refer to the section in this prospectus entitled “The Exchange Offer—Exchange Agent.” |

6

Fees and Expenses | We will pay all expenses related to the exchange offer. Please refer to the section in this prospectus entitled “The Exchange Offer—Fees and Expenses.” |

Use of Proceeds | We will not receive any proceeds from the issuance of the exchange notes. We are making the exchange offer solely to satisfy certain of our obligations under our registration rights agreement entered into in connection with the note offering. |

Consequences to Noteholders Who Do Not Participate in the Exchange Offer | In general, if you do not participate in the exchange offer (i) except as set forth below, you will not necessarily be able to require us to register your initial notes under the Securities Act; (ii) you will not be able to resell, offer to resell or otherwise transfer your initial notes unless they are registered under the Securities Act or unless you resell, offer to resell or otherwise transfer them under an exemption from the registration requirements of, or in a transaction not subject to, the Securities Act; and (iii) the trading market for your initial notes will become more limited to the extent other holders of initial notes participate in the exchange offer. In addition, if you do not participate in the exchange offer, you will not be able to require us to register your initial notes under the Securities Act unless: |

| | • | | the exchange offer is not permitted by applicable law or SEC policy; |

| | • | | the exchange offer is not consummated within 270 days after the closing date of the note offering; |

| | • | | you are prohibited by applicable law or SEC policy from participating in the exchange offer; |

| | • | | you may not resell the exchange notes you acquire in the exchange offer to the public without delivering a prospectus and that the prospectus contained in the exchange offer registration statement is not appropriate or available for such resales by you; or |

| | • | | you are a broker-dealer and hold initial notes acquired directly from us or one of our affiliates. |

In these cases, the registration rights agreement requires us to file a registration statement for a continuous offering in accordance with Rule 415 under the Securities Act for the benefit of the holders of the initial notes described in this paragraph. We do not currently anticipate that we will register under the Securities Act any notes that remain outstanding after completion of the exchange offer. Please refer to the section in this prospectus entitled “The Exchange Offer—Your Failure to Participate in the Exchange Offer Will Have Adverse Consequences.”

Resales | Based on interpretations by the staff of the SEC, as set forth in no-action letters issued to third parties, we believe that it may be possible for you to resell the notes issued in the exchange offer |

7

| | without compliance with the registration and prospectus delivery provisions of the Securities Act, subject to the conditions described under “—Obligations of Broker-Dealers” below. |

To tender your initial notes in the exchange offer and resell the exchange notes without compliance with the registration and prospectus delivery requirements of the Securities Act, you must make the following representations:

| | • | | you are authorized to tender the initial notes and to acquire exchange notes, and that we will acquire good and unencumbered title to those initial notes; |

| | • | | the exchange notes acquired by you are being acquired in the ordinary course of business; |

| | • | | you have no arrangement or understanding with any person to participate in a distribution of the exchange notes and are not participating in, and do not intend to participate in, the distribution of such exchange notes; |

| | • | | you are not an “affiliate,” as defined in Rule 405 promulgated under the Securities Act, of ours; |

| | • | | if you are not a broker-dealer, you are not engaging in, and do not intend to engage in, a distribution of exchange notes; |

| | • | | if you are a broker-dealer, initial notes to be exchanged were acquired by you as a result of market-making or other trading activities and you will deliver a prospectus in connection with any resale, offer to resell or other transfer of such exchange notes; and |

| | • | | you are not acting on behalf of any person who could not truthfully make the foregoing representations. |

Please refer to the sections in this prospectus entitled “The Exchange Offer—Procedure for Tendering Initial Notes—Proper Execution and Delivery of Letters of Transmittal,” “Risk Factors—Risks Related to the Exchange Offer—Some persons who participate in the exchange offer must deliver a prospectus in connection with resales of the exchange notes” and “Plan of Distribution.”

Obligations of Broker-Dealers | If you are a broker-dealer that receives exchange notes, you must acknowledge that you will deliver a prospectus in connection with any resales of the exchange notes. If you are a broker-dealer who acquired the initial notes as a result of market-making or other trading activities, you may use the exchange offer prospectus as supplemented or amended, in connection with resales of the exchanges notes. If you are a broker-dealer who acquired the initial notes directly from the issuers in the note offering and not as a result of market-making and trading activities, you must, in the absence of an exemption, comply with the registration and prospectus delivery requirements of the Securities Act in connection with resales of the exchange notes. |

8

Summary of Terms of the Exchange Notes

The exchange notes will be governed by the indenture, dated as of December 17, 2009, by and among Bumble Bee Foods, LLC, Connors Bros. Clover Leaf Seafoods Company, Bumble Bee Capital Corp., the guarantors named therein and Deutsche Bank Trust Company Americas, as trustee and collateral agent. The terms of the exchange notes and those of the outstanding initial notes are substantially identical, except that the transfer restrictions and registration rights relating to the initial notes do not apply to the exchange notes. The following is a summary of certain terms of the indenture and the notes and is qualified in its entirety by the more detailed information contained under the heading “Description of Notes” elsewhere in this prospectus.

Issuers | Bumble Bee Foods, LLC, Connors Bros. Clover Leaf Seafoods Company and Bumble Bee Capital Corp. |

Notes Offered | $220,000,000 aggregate principal amount of 7.75% Senior Secured Notes due 2015. |

Maturity Date | December 15, 2015. |

Interest | Interest on the notes will accrue at a rate per annum equal to 7.75%. |

Guarantees | The notes will be guaranteed on a senior secured basis by Parent Guarantor and each of Parent Guarantor’s existing subsidiaries and certain future subsidiaries that guarantee our senior credit facilities. |

Interest Payment Dates | Every June 15 and December 15, beginning June 15, 2010. |

Ranking | The notes and guarantees will be our senior obligations and will rank equal in right of payment to our existing and future senior obligations and senior in right of payment to all of our existing and future subordinated obligations. The notes and guarantees will be effectively subordinated to our secured debt that is secured by a lien ranking prior to the lien on the collateral for the notes and the guarantees, including obligations under our credit facilities and other senior lien obligations, to the extent of the value of the assets securing such obligations, and will be structurally subordinated to all obligations of any of our subsidiaries that is not a guarantor of the notes. The notes and guarantees will be effectively senior to all existing and future senior unsecured debt to the extent of the value of the collateral after giving effect to senior lien obligations. As of April 3, 2010, we had approximately $163.7 million of senior secured first and second lien debt outstanding and $39.9 million of available borrowing capacity under our senior credit facilities (after giving effect to $3.6 million in outstanding letters of credit), all of which would effectively rank senior to the notes. |

Collateral | The notes and guarantees will be secured by a third-priority security interest in substantially all of the collateral securing the senior credit facilities with certain exceptions, and will be junior in priority to the liens securing the senior credit facilities and to all other senior lien obligations and permitted prior liens, including liens securing certain hedging obligations and cash management obligations. The liens securing first and second-priority lien obligations will continue to be held by the collateral agents under the senior credit facilities. |

9

The collateral securing the notes will consist of substantially all of the issuers’ and the guarantors’ property and assets that secure the senior credit facilities, which will exclude: (i) any rights or interest in certain contracts covering real or personal property, (ii) certain intent-to-use trademark or service mark applications, (iii) any leasehold interest in real property, (iv) any deposit account that is used exclusively for payroll, payroll taxes and other employee wage and benefit payments to or for employees and (v) certain other limited exclusions. In addition, pledges of capital stock or other securities will be limited to the extent Rule 3-16 of Regulation S-X would require the filing of separate financial statements with the SEC for that subsidiary. See “Description of Notes—Security.”

The value of collateral at any time will depend on market and other economic conditions, including the availability of suitable buyers for the collateral. The liens on the collateral may be released without the consent of the holders of notes if collateral is disposed of in a transaction that complies with the indenture and related security documents or in accordance with the provisions of the intercreditor agreement. See “Risk Factors—Risks Related to the Notes” and “Description of Notes—Security” and “—Intercreditor Agreement” below.

Intercreditor Agreement | The trustee and the collateral agent under the indenture governing the notes and the administrative agents and the collateral agents under the senior credit facilities have entered into an intercreditor agreement as to the relative priorities of their respective security interests in the assets securing the notes and borrowings under the senior credit facilities and certain other matters relating to the administration of security interests. See “Description of Notes—Intercreditor Agreement.” |

Optional Redemption | We may redeem some or all of the notes at any time prior to December 15, 2012 at a price equal to 100% of the principal amount of the notes to be redeemed, plus a make-whole premium and accrued and unpaid interest to the redemption date. Thereafter, we may redeem some or all of the notes at the redemption prices listed under “Description of Notes—Optional Redemption” plus accrued and unpaid interest on the notes to the date of redemption. Prior to December 15, 2012, we may also redeem up to 10% per year of the notes at any time and from time to time at a redemption price equal to 103% of the principal amount thereof plus accrued and unpaid interest on the notes to the applicable redemption date. In addition, at any time prior to December 15, 2012, we may redeem up to 35% of the notes from the proceeds of certain sales of our equity securities at 107.75% of the principal amount, plus accrued and unpaid interest to the date of redemption. We may make that redemption only if, after the redemption, at least 65% of the aggregate principal amount of the notes remains outstanding and the redemption occurs within 90 days of the closing of an equity offering. See “Description of Notes—Optional Redemption.” |

10

Change of Control | Upon the occurrence of a change of control (as described under “Description of Notes—Change of Control”), we must offer to repurchase the notes at 101% of the principal amount of the notes, plus accrued and unpaid interest to the date of repurchase. We will comply, to the extent applicable with the requirements of Section 14(e) of the Exchange Act, and any other securities laws or regulations in connection with the repurchase of notes in the event of a change of control. See “Description of Notes—Change of control.” |

Basic Covenants of the Indenture | The indenture governing the notes contains certain covenants limiting our ability and the ability of our restricted subsidiaries to, under certain circumstances: |

| | • | | pay dividends or make other distributions on, redeem or repurchase, capital stock; |

| | • | | make investments or other restricted payments; |

| | • | | enter into transactions with affiliates; |

| | • | | engage in sale and leaseback transactions; |

| | • | | sell all, or substantially all, of our assets; |

| | • | | create liens on assets to secure debt; or |

| | • | | effect a consolidation or merger. |

These covenants are subject to important exceptions and qualifications as described in this prospectus under the caption “Description of Notes—Certain Covenants.”

Use of Proceeds | We will not receive any proceeds from the issuance of the exchange notes in exchange for the outstanding initial notes. We are making this exchange solely to satisfy our obligations under the registration rights agreement entered into in connection with the note offering. |

Absence of a Public Market for the Exchange Notes | The exchange notes are new securities with no established market for them. We cannot assure you that a market for these exchange notes will develop or that this market will be liquid. Please refer to the section in this prospectus entitled “Risk Factors—Risks Relating to the Exchange Offer—If an active trading market for the notes does not develop, the liquidity and value of the notes could be harmed.” |

Risk Factors

You should carefully consider all of the information in this prospectus. In particular, you should evaluate the specific risk factors set forth under the caption “Risk Factors” in this prospectus.

11

Summary Historical Consolidated Financial Data

Set forth below is summary historical consolidated financial data and other operating information for the periods indicated. The summary historical consolidated financial data presented below for the fiscal year ended December 31, 2007 represents that of the Predecessor and has been derived from, and should be read together with, the audited consolidated financial statements and accompanying notes of the Predecessor included elsewhere in this prospectus. The summary balance sheet data as of December 31, 2007 has been derived from the audited financial statements of the Predecessor not included in this prospectus.

The summary historical consolidated financial data presented below for the period from January 1, 2008 to November 22, 2008 represents that of the Predecessor and has been derived from, and should be read together with, the audited consolidated financial statements and accompanying notes of the Predecessor included elsewhere in this prospectus. The summary historical consolidated financial data presented below for the period from November 23, 2008 (inception) to December 31, 2008 represents that of the Successor and has been derived from, and should be read together with, the audited consolidated financial statements and accompanying notes of the Successor included elsewhere in this prospectus. The summary balance sheet data as of November 22, 2008 has been derived from the unaudited consolidated financial statements of the Predecessor not included in this prospectus.

The summary historical consolidated financial data presented below for the fiscal year ended December 31, 2009 represents that of the Successor and has been derived from, and should be read together with the audited consolidated financial statements and accompanying notes of the Successor included elsewhere in this prospectus.

The summary historical consolidated financial data presented below as of and for the three months ended April 3, 2010 and April 4, 2009 has been derived from and should be read together with the unaudited consolidated financial statements and accompanying notes of the Successor included elsewhere in this prospectus. In the opinion of management, such unaudited financial data contains all adjustments, consisting of normal recurring adjustments, necessary for fair presentation of such unaudited consolidated financial data. The results of operations for these interim periods are not necessarily indicative of the results to be expected for a full year or any future periods.

12

The following summary historical consolidated financial data should be read in conjunction with “Selected Historical Consolidated Financial Data,” “Use of Proceeds,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and the consolidated financial statements and accompanying notes thereto included elsewhere in this prospectus.

| | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Predecessor | | | | | Successor | |

| | Years Ended

December 31, | | | January 1,

2008 to

November 22,

2008 | | | | November 23,

2008

(inception) to

December 31,

2008 | | | Year Ended

December 31,

2009 | | | Three Months Ended | |

| | 2007 | | | | | | | April 4,

2009 | | | April 3,

2010 | |

| | (in thousands, except ratios) | |

Statement of Operations Data: | | | | | | | | | | | | | | | | | | | | | | | | | | |

Revenue | | $ | 916,356 | | | $ | 896,389 | | | | | $ | 95,603 | | | $ | 944,013 | | | $ | 251,004 | | | $ | 256,560 | |

Cost of sales | | | 787,969 | | | | 743,611 | | | | | | 79,340 | | | | 757,459 | | | | 208,606 | | | | 200,650 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Gross profit | | | 128,387 | | | | 152,778 | | | | | | 16,263 | | | | 186,554 | | | | 42,398 | | | | 55,910 | |

Selling, general and administrative expenses | | | 90,258 | | | | 89,294 | | | | | | 8,740 | | | | 103,833 | | | | 27,720 | | | | 28,251 | |

Asset impairment charges | | | 81,946 | | | | — | | | | | | — | | | | — | | | | — | | | | — | |

Product recall expenses | | | 10,574 | | | | — | | | | | | — | | | | — | | | | — | | | | — | |

Restructuring and other transition costs, net | | | — | | | | 1,000 | | | | | | — | | | | — | | | | — | | | | 2,314 | |

Gain on divested brands | | | (2,487 | ) | | | — | | | | | | — | | | | — | | | | — | | | | — | |

Loss on the sale of meat assets and plant closure | | | — | | | | 16,760 | | | | | | — | | | | — | | | | — | | | | — | |

Loss on settlement of hedging instruments | | | — | | | | 8,112 | | | | | | — | | | | — | | | | — | | | | — | |

Accelerated vesting of LTIP compensation | | | — | | | | 6,582 | | | | | | — | | | | — | | | | — | | | | — | |

Gain on insurance claim | | | (3,076 | ) | | | — | | | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating income (loss) | | | (48,828 | ) | | | 31,030 | | | | | | 7,523 | | | | 82,721 | | | | 14,678 | | | | 25,345 | |

Interest expense, net | | | 18,339 | | | | 15,825 | | | | | | 5,059 | | | | 46,707 | | | | 12,534 | | | | 7,904 | |

Loss on extinguishment of debt | | | — | | | | — | | | | | | — | | | | 25,750 | | | | — | | | | 573 | |

Cost of hedging purchase price consideration | | | — | | | | — | | | | | | 7,561 | | | | — | | | | — | | | | — | |

Other (income) expenses, net | | | (1,967 | ) | | | 2,732 | | | | | | (1,424 | ) | | | (6,100 | ) | | | 563 | | | | (2,347 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Income (loss) before income taxes | | | (65,200 | ) | | | 12,473 | | | | | | (3,673 | ) | | | 16,364 | | | | 1,581 | | | | 19,215 | |

Income taxes | | | 7,962 | | | | 5,072 | | | | | | 1,051 | | | | 3,429 | | | | 377 | | | | 4,780 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income (loss) | | $ | (73,162 | ) | | $ | 7,401 | | | | | $ | (4,724 | ) | | $ | 12,935 | | | $ | 1,204 | | | $ | 14,435 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

Statement of Cash Flows Data: | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net cash provided by (used in): | | | | | | | | | | | | | | | | | | | | | | | | | | |

Operating activities | | $ | 58,123 | | | $ | 75,928 | | | | | $ | (22,031 | ) | | $ | 74,154 | | | $ | 21,979 | | | $ | 22,659 | |

Investing activities(1) | | | (21,329 | ) | | | (19,998 | ) | | | | | (611,865 | ) | | | (13,720 | ) | | | (3,657 | ) | | | (1,025 | ) |

Financing activities(1) | | | (33,373 | ) | | | (59,088 | ) | | | | | 638,548 | | | | (60,887 | ) | | | (21,025 | ) | | | (24,645 | ) |

| | | | | | | |

Balance Sheet Data (at period end): | | | | | | | | | | | | | | | | | | | | | | | | | | |

Cash and cash equivalents | | $ | 6,458 | | | $ | 3,248 | | | | | $ | 4,695 | | | $ | 4,491 | | | $ | 1,961 | | | $ | 1,440 | |

Total assets | | | 878,497 | | | | 795,927 | | | | | | 804,479 | | | | 806,329 | | | | 778,856 | | | | 798,962 | |

Total debt | | | 274,176 | | | | 404,954 | | | | | | 426,407 | | | | 399,924 | | | | 407,456 | | | | 377,392 | |

Redeemable preferred partnership units | | | — | | | | 40,807 | | | | | | 41,509 | | | | — | | | | 42,570 | | | | — | |

Total equity | | | 447,183 | | | | 180,273 | | | | | | 190,317 | | | | 264,966 | | | | 189,019 | | | | 286,423 | |

| | | | | | | |

Other Financial Data: | | | | | | | | | | | | | | | | | | | | | | | | | | |

Capital expenditures | | $ | 23,507 | | | $ | 22,931 | | | | | $ | 2,524 | | | $ | 14,226 | | | $ | 2,869 | | | $ | 1,235 | |

| | | | | | | |

Other Operating Information: | | | | | | | | | | | | | | | | | | | | | | | | | | |

Ratio of earnings to fixed charges(2) | | | (2.6 | ) | | | 1.8 | | | | | | 0.3 | | | | 1.4 | | | | 1.1 | | | | 3.4 | |

13

| (1) | Represents the impact of the Acquisition in 2008. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Cash Flows, Liquidity and Capital Resources.” |

| (2) | For the year ended December 31, 2007, the ratio of earnings to fixed charges reflects a deficiency. In 2007, the Predecessor incurred losses as a result of a product recall. For the year ended December 31, 2007, the amount of the deficiency was $65.2 million, and the amount of pre-tax charges related to the product recall totaled $120.5 million. For the period from November 23, 2008 (inception) to December 31, 2008, the ratio of earnings to fixed charges reflects a deficiency. In 2008, the Successor incurred losses as a result of non-cash inventory “step-up” charges and the cost of hedging purchase price consideration. For the period from November 23, 2008 (inception) to December 31, 2008, the amount of the deficiency was $3.7 million, and the amounts of the non-cash inventory “step-up” charges and cost of hedging purchase price consideration were $3.6 million and $7.6 million, respectively. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” |

14

RISK FACTORS

Your decision whether to acquire the exchange notes will involve risk. You should carefully consider the following risks, as well as the other information contained in this prospectus, before deciding whether to participate in the exchange offer. Any of the following risks could materially and adversely affect our business, financial condition or results of operations. The risks described below are not the only risks facing us. Additional risks and uncertainties not currently known to us or those we currently view to be immaterial may also materially and adversely affect our business, financial condition or results of operations. In such a case, you may lose all or part of your original investment.

Risks Related to the Notes

Our substantial indebtedness could adversely affect our financial condition.

As a result of our substantial indebtedness, a significant portion of our cash flow will be required to pay interest and principal on our outstanding indebtedness, and we may not generate sufficient cash flow from operations, or have future borrowings available under our senior credit facilities, to enable us to repay our indebtedness, including the notes, or to fund other liquidity needs. As of April 3, 2010, we had total indebtedness of approximately $383.7 million (including approximately $158.9 million of debt under our senior credit facilities, approximately $4.8 million of capital leases and installment notes and approximately $220.0 million of debt under the initial notes).

Our substantial indebtedness could have important consequences to you. For example, it could:

| | • | | make it more difficult for us to satisfy our obligations with respect to the notes and our other debt; |

| | • | | increase our vulnerability to general adverse economic and industry conditions; |

| | • | | require us to dedicate a substantial portion of our cash flow from operations to payments on our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures and other general corporate purposes; |

| | • | | limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

| | • | | increase our cost of borrowing; |

| | • | | place us at a competitive disadvantage compared to our competitors that may have less debt; and |

| | • | | limit our ability to obtain additional financing for working capital, capital expenditures, acquisitions or general corporate purposes. |

We expect to use cash flow from operations to meet our current and future financial obligations, including funding our operations, debt service and capital expenditures. Our ability to make these payments depends on our future performance, which will be affected by financial, business, economic and other factors, many of which we cannot control. Our business may not generate sufficient cash flow from operations in the future, which could result in our being unable to repay indebtedness, or to fund other liquidity needs. If we do not have enough money, we may be forced to reduce or delay our business activities and capital expenditures, sell assets, obtain additional debt or equity capital or restructure or refinance all or a portion of our debt, including our senior credit facilities and the notes, on or before maturity. We cannot make any assurances that we will be able to accomplish any of these alternatives on terms acceptable to us, or at all. In addition, the terms of existing or future indebtedness, including the agreements for our senior revolving credit facility and our senior term loan facility, respectively, may limit our ability to pursue any of these alternatives.

15

Our senior credit facilities are secured by substantially all the assets of the issuers and the guarantors and will be senior to the notes to the extent of the value of the collateral.

Obligations under our senior revolving credit facility are secured by a first-priority lien on all of the borrowers’ and guarantors’ accounts receivable and inventory and a second-priority lien on the borrowers’ and guarantors’ other tangible and intangible assets. Obligations under our senior term loan facility are secured by a second-priority lien on all of the borrowers’ and guarantors’ accounts receivable and inventory and a first-priority lien on the borrowers’ and guarantors’ other tangible and intangible assets. The notes and the related guarantees will be secured by a third-priority lien in substantially all of the collateral securing indebtedness under our senior credit facilities, with certain exceptions. As of April 3, 2010, we had approximately $163.7 million of senior secured first and second lien indebtedness outstanding and $39.9 million of available borrowing capacity under our senior credit facilities (after giving effect to $3.6 million in outstanding letters of credit) ranking ahead of the notes and related guarantees. Any rights to payment and claims by the holders of the notes will, therefore, be effectively junior to any rights to payment or claims by our creditors under our senior credit facilities with respect to distributions of such collateral. Only when our obligations under our senior credit facilities are satisfied in full will the proceeds of the collateral securing indebtedness under our senior credit facilities, subject to other permitted liens, be available to satisfy the obligations under the notes and guarantees. In addition, the indenture permits us under certain circumstances to incur additional indebtedness secured by a lien that ranks senior to or equally with the notes. Any such indebtedness may further limit the recovery from the realization of the value of such collateral available to satisfy holders of the notes. As a result, if there is a default, the value of such collateral may not be sufficient to repay the first-priority and second-priority lien creditors, the holders of the notes and the guarantees andpari passu indebtedness.

Despite current indebtedness levels and restrictive covenants, we may still be able to incur more debt or make certain restricted payments, which could further exacerbate the risks described above.

We and our subsidiaries may be able to incur additional debt in the future. Although our senior credit facilities contain, and the indenture governing the notes contains, restrictions on our ability to incur indebtedness, those restrictions are subject to a number of exceptions. In addition, if we are able to designate some of our restricted subsidiaries under the indenture governing the notes as unrestricted subsidiaries, those unrestricted subsidiaries would be permitted to borrow beyond the limitations specified in the indenture and engage in other activities in which restricted subsidiaries may not engage. We may also consider investments in joint ventures or acquisitions, which may increase our indebtedness. Moreover, although our senior credit facilities contain, and the indenture governing the notes contains, restrictions on our ability to make restricted payments, including the declaration and payment of dividends, we are able to make such restricted payments under certain circumstances. Adding new debt to current debt levels or making restricted payments could intensify the related risks that we and our subsidiaries now face. See “Capitalization” and “Description of Other Indebtedness.”

The agreements governing our debt agreements restrict our ability to engage in some business and financial transactions.

Our debt agreements, such as the indenture governing the notes and the agreements governing our senior credit facilities, restrict our ability in certain circumstances to, among other things:

| | • | | pay dividends and make other distributions on, redeem or repurchase, capital stock; |

| | • | | make investments or other restricted payments; |

| | • | | enter into transactions with affiliates; |

| | • | | engage in sale and leaseback transactions; |

| | • | | sell all, or substantially all, of our assets; |

| | • | | create liens on assets to secure debt; or |

| | • | | effect a consolidation or merger. |

16

These covenants limit our operational flexibility and could prevent us from taking advantage of business opportunities as they arise, growing our business or competing effectively. In addition, our senior credit facilities require us to maintain specified financial ratios and satisfy other financial condition tests. Our ability to meet these financial ratios and tests can be affected by events beyond our control, and we cannot assure you that we will meet these tests.

A breach of any of these covenants or other provisions in our debt agreements could result in an event of default, which if not cured or waived, could result in such debt becoming immediately due and payable. This, in turn, could cause our other debt to become due and payable as a result of cross-acceleration provisions contained in the agreements governing such other debt. In the event that some or all of our debt is accelerated and becomes immediately due and payable, we may not have the funds to repay, or the ability to refinance, such debt. In addition, in the event that the notes become immediately due and payable, the holders of the notes would not be entitled to receive any payment in respect of the notes until all of our senior debt has been paid in full.

Our ability to make payments on the notes depends in part on our ability to receive dividends and other distributions from our subsidiaries.

We depend in part on dividends and other payments from our subsidiaries to generate the funds necessary to meet our financial obligations, including the payment of principal of and interest on their outstanding debt. Our subsidiaries are legally distinct from us. Payment to us by our subsidiaries will be contingent upon our subsidiaries’ earnings and other business considerations. The ability of our subsidiaries and joint ventures to pay dividends, make distributions, provide loans or make other payments to us may be restricted by applicable state and foreign laws, potentially adverse tax consequences and their agreements, including agreements governing their debt. In addition, the equity interests of our joint venture partners or other shareholders in our non-wholly owned subsidiaries in any dividend or other distribution made by these entities would need to be satisfied on a proportionate basis with us. As a result, we may not be able to access their cash flow to service our debt, including the notes, and we cannot assure you that the amount of cash and cash flow reflected on our financial statements will be fully available to us.

The notes will be structurally subordinated to all liabilities of our future subsidiaries that are not guarantors of the notes.

Not all of our future subsidiaries will guarantee the notes. The notes are structurally subordinated to the indebtedness and other liabilities of our future subsidiaries that do not guarantee the notes. These future non-guarantor subsidiaries are separate and distinct legal entities and will have no obligation, contingent or otherwise, to pay any amounts due pursuant to the notes, or to make any funds available therefor, whether by dividends, loans, distributions or other payments. Any right that we or the subsidiary guarantors have to receive any assets of any of the non-guarantor subsidiaries upon the liquidation or reorganization of those subsidiaries, and the consequent rights of holders of the notes to realize proceeds from the sale of any of those subsidiaries’ assets, will be effectively subordinated to the claims of those subsidiaries’ creditors, including trade creditors and holders of preferred equity interests of those subsidiaries. Accordingly, in the event of a bankruptcy, liquidation or reorganization of any of our future non-guarantor subsidiaries, absent a decision of the court, such as in the case of substantive consolidation, these future non-guarantor subsidiaries will pay the holders of their debts, holders of preferred equity interests and their trade creditors before they will be able to distribute any of their assets to us.

The note guarantee of a subsidiary guarantor may be released if such subsidiary guarantor no longer guarantees or is otherwise no longer an obligor of indebtedness under our senior credit facilities.

Any subsidiary guarantee of the notes may be released without action by, or consent of, any holder of the notes or the trustee under the indenture if the subsidiary guarantor is no longer a guarantor or an obligor of our senior credit facilities. The lenders under our senior credit facilities have the discretion to release the subsidiary guarantees under the senior credit facilities in certain circumstances. You will not have a claim as a creditor against any subsidiary that is no longer a subsidiary guarantor of the notes, and the indebtedness and other liabilities, including trade payables, whether secured or unsecured, of those subsidiaries will effectively be senior to your claims.

17