Exhibit 99.2

Supplemental Information

September 30, 2012

(Unaudited)

Disclaimer

Certain statements in this supplement contain "forward-looking" information as that term is defined by the Private Securities Litigation Reform Act of 1995. Examples of forward-looking statements include all statements regarding our expected future financial position, results of operations, business strategy, growth opportunities and potential acquisitions, and plans and objectives for future operations. You can identify some of the forward-looking statements by the use of forward-looking words such as “anticipate,” “believe,” “plan,” “estimate,” “expect,” “intend,” “should,” “may” and other similar expressions, although not all forward-looking statements contain these identifying words.

Our actual results may differ materially from those projected or contemplated by our forward-looking statements as a result of various factors, including, among others, the following: our dependence on Sun Healthcare Group, Inc. (“Sun”) until we are able to further diversify our portfolio; our dependence on the operating success of our tenants; changes in general economic conditions and volatility in financial and credit markets; the dependence of our tenants on reimbursement from governmental and other third-party payors; the significant amount of and our ability to service our indebtedness; covenants in our debt agreements that may restrict our ability to make acquisitions, incur additional indebtedness and refinance indebtedness on favorable terms; increases in market interest rates; our ability to raise capital through equity financings; the relatively illiquid nature of real estate investments; competitive conditions in our industry; the loss of key management personnel or other employees; the impact of litigation and rising insurance costs on the business of our tenants; uninsured or underinsured losses affecting our properties and the possibility of environmental compliance costs and liabilities; our ability to maintain our status as a REIT; compliance with REIT requirements and certain tax matters related to our status as a REIT; and other factors discussed from time to time in our news releases, public statements and/or filings with the Securities and Exchange Commission (the “SEC”), especially the “Risk Factors” sections of our Annual and Quarterly Reports on Forms 10-K and 10-Q. We do not intend, and we undertake no obligation, to update any forward-looking information to reflect events or circumstances after the date of this supplement or to reflect the occurrence of unanticipated events, unless required by law to do so.

Note Regarding Non-GAAP Financial Measures

This supplement includes the following financial measures defined as non-GAAP financial measures by the SEC: EBITDA, funds from operations (“FFO”), adjusted FFO (“AFFO”), normalized AFFO, FFO per diluted share, AFFO per diluted share and normalized AFFO per diluted share. These measures may be different than non-GAAP financial measures used by other companies, and the presentation of these measures is not intended to be considered in isolation or as a substitute for financial information prepared and presented in accordance with U.S. generally accepted accounting principles. Explanations of these non-GAAP financial measures are included under “Reporting Definitions” in this supplement and reconciliations of these non-GAAP financial measures to the GAAP financial measures we consider most comparable are included under “Reconciliations of Net Income to EBITDA, Funds from Operations (FFO), Adjusted Funds from Operations (AFFO) and Normalized AFFO” in this supplement.

Tenant Information

This supplement includes information regarding Sun. Sun is subject to the reporting requirements of the SEC and is required to file with the SEC annual reports containing audited financial information and quarterly reports containing unaudited financial information. Sun's filings with the SEC can be found at www.sec.gov. This supplement also includes information regarding each of our other tenants that lease properties from us. The information related to Sun and our other tenants that is provided in this supplement has been provided by the tenants or, in the case of Sun, derived from Sun's public filings or provided by Sun. We have not independently verified this information. We have no reason to believe that such information is inaccurate in any material respect. We are providing this data for informational purposes only.

Table of Contents

|

| |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| |

| | |

| Real Estate Portfolio Geographic Concentrations | |

| | |

| |

| | |

| Distribution of Licensed Beds/Units | |

| | |

| |

| | |

| Rental Income - Three Months Ended September 30, 2012 | |

| | |

| Rental Income - Nine Months Ended September 30, 2012 | |

| | |

| |

| | |

| |

| | |

| Recent Investment Activity | |

| | |

| |

| | |

| |

| | |

| |

Company Information

Board of Directors

|

| | |

| | | |

Richard K. Matros Chairman of the Board, President and Chief Executive Officer Sabra Health Care REIT, Inc. | | Michael J. Foster Managing Director RFE Management Corp. |

| | |

Milton J. Walters President Tri-River Capital | | Robert A. Ettl Chief Operating Officer Harvard Management Company |

| | |

Craig A. Barbarosh Partner Katten Muchin Rosenman LLP | | |

Senior Management

|

| | |

| | | |

Richard K. Matros Chairman of the Board, President and Chief Executive Officer | | Harold W. Andrews, Jr. Executive Vice President, Chief Financial Officer and Secretary |

| | |

Talya Nevo-Hacohen Executive Vice President, Chief Investment Officer and Treasurer | | |

Other Information

|

| | |

| | | |

Corporate Headquarters 18500 Von Karman Avenue, Suite 550 Irvine, CA 92612 | | Transfer Agent American Stock Transfer and Trust Company 6201 15th Avenue Brooklyn, NY 11219 |

www.sabrahealth.com

The information in this supplemental information package should be read in conjunction with the Company’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other information filed with the SEC. The Reporting Definitions and Reconciliations of Non-GAAP Measures are an integral part of the information presented herein.

On Sabra's website, www.sabrahealth.com, you can access, free of charge, Sabra’s Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Sections 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, as soon as reasonably practicable after such material is filed with, or furnished to, the SEC. The information contained on Sabra’s website is not incorporated by reference into, and should not be considered a part of, this supplemental information package. All material filed with the SEC can also be accessed through their website, www.sec.gov.

For more information, contact Harold W. Andrews, Jr., Executive Vice President, Chief Financial Officer and Secretary at (949) 679-0243.

SABRA HEALTH CARE REIT, INC.

COMPANY FACT SHEET

Company Profile

Sabra Health Care REIT, Inc., a Maryland corporation (“Sabra,” the “Company” or “we”), operates as a self-administered, self-managed real estate investment trust (“REIT”) that, through its subsidiaries, owns and invests in real estate serving the healthcare industry. Sabra primarily generates revenues by leasing properties to tenants and operators throughout the United States.

As of September 30, 2012, Sabra’s portfolio included 105 real estate properties leased to operators/tenants under triple-net lease agreements (consisting of (i) 93 skilled nursing/post-acute facilities, (ii) 11 senior housing facilities, and (iii) one acute care hospital), two mortgage loan investments and one mezzanine loan investment. As of September 30, 2012, Sabra’s real estate properties are located in 26 states and included 11,689 licensed beds.

Objectives and Strategies

Sabra expects to continue to grow its portfolio primarily through the acquisition of senior housing and memory care facilities and with a secondary focus on acquiring skilled nursing facilities. Sabra also expects to opportunistically consider originating financing secured directly or indirectly by healthcare facilities. As Sabra acquires additional properties and expands its portfolio, Sabra expects to further diversify by tenant, asset class and geography within the healthcare sector. Sabra employs a disciplined, opportunistic approach in its healthcare real estate investment strategy by investing in assets that provide attractive opportunities for dividend growth and appreciation of asset values, while maintaining balance sheet strength and liquidity, thereby creating long-term stockholder value.

|

| | | | |

| Market Facts | Portfolio Information (as of September 30, 2012) |

| Stock Information (as of September 30, 2012) | | Investments | |

| Closing Price: | $20.01 | Equity Investments | |

| 52-Week range: | $7.86 - $20.90 | Skilled Nursing/Post-Acute | 93 |

|

| Market Capitalization: | $741.4 million | Senior Housing | 11 |

|

| Enterprise Value: | $1.2 billion | Acute Care Hospital | 1 |

|

| Outstanding Shares: | 37.1 million | | 105 |

|

| Ticker symbol: | SBRA | Debt Investments | 3 |

|

| Stock Exchange: | NASDAQ | Total Investments | 108 |

|

| | | | |

| Credit Ratings | | |

|

|

| Moody's: | B1 (stable) | Bed/Unit Count | |

| S&P: | | Skilled Nursing/Post-Acute | 10,549 |

|

| Corporate Rating | B+ (stable) | Senior Housing | 1,070 |

|

| Senior Notes Rating | BB- | Acute Care Hospital | 70 |

|

| | | | |

| | | Total Beds/Units | 11,689 |

|

| | | | |

|

| | |

| See reporting definitions. | 2 |

SABRA HEALTH CARE REIT, INC.

FINANCIAL HIGHLIGHTS

(dollars in thousands, except per share data) |

| | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Nine Months Ended September 30, |

| | 2012 | | 2011 | | 2012 | | 2011 |

| Revenues | $ | 26,038 |

| | $ | 21,470 |

| | $ | 74,882 |

| | $ | 57,876 |

|

| EBITDA | $ | 22,260 |

| | $ | 16,818 |

| | $ | 63,294 |

| | $ | 47,631 |

|

| Net income | $ | 5,226 |

| | $ | 2,344 |

| | $ | 15,554 |

| | $ | 5,678 |

|

| FFO | $ | 12,722 |

| | $ | 9,194 |

| | $ | 37,910 |

| | $ | 24,905 |

|

| AFFO | $ | 14,868 |

| | $ | 12,525 |

| | $ | 44,528 |

| | $ | 31,884 |

|

| Normalized AFFO | $ | 14,868 |

| | $ | 12,525 |

| | $ | 44,528 |

| | $ | 32,194 |

|

| Per share data: | | | | | | | |

| Diluted EPS | $ | 0.14 |

| | $ | 0.07 |

| | $ | 0.42 |

| | $ | 0.20 |

|

| Diluted FFO | $ | 0.34 |

| | $ | 0.28 |

| | $ | 1.02 |

| | $ | 0.89 |

|

| Diluted AFFO | $ | 0.39 |

| | $ | 0.38 |

| | $ | 1.18 |

| | $ | 1.13 |

|

| Diluted Normalized AFFO | $ | 0.39 |

| | $ | 0.38 |

| | $ | 1.18 |

| | $ | 1.14 |

|

| Weighted-average number of common shares outstanding, diluted: | | | | | | | |

| EPS & FFO | 37,465,114 |

| | 33,049,621 |

| | 37,276,013 |

| | 27,891,690 |

|

| AFFO & Normalized AFFO | 37,748,716 |

| | 33,320,262 |

| | 37,660,657 |

| | 28,142,867 |

|

| | | | | | | | |

| Net cash flow from operations | $ | 23,815 |

| | $ | 16,581 |

| | $ | 47,902 |

| | $ | 34,509 |

|

| | | | | | |

| | September 30, 2012 | | December 31, 2011 | | | | |

| Real Estate Portfolio | | | | | | | |

| Total Equity Investments (#) | 105 |

| | 97 |

| | | | |

| Total Equity Investments, gross ($) | $ | 863,879 |

| | $ | 767,054 |

| | | | |

| Total Licensed Beds/Units | 11,689 |

| | 10,877 |

| | | | |

| Weighted Average Remaining Lease Term (in months) | 135 |

| | 144 |

| | | | |

| Total Debt Investments (#) | 3 |

| | — |

| | | | |

Total Debt Investments, gross ($) (1) | $ | 22,111 |

| | $ | — |

| | | | |

| | | | | | |

| | Three Months Ended September 30, 2012 | | Twelve Months Ended September 30, 2012 | | | | |

EBITDARM Coverage (2) | 1.82x |

| | 1.80x |

| | | | |

EBITDAR Coverage (2) | 1.54x |

| | 1.50x |

| | | | |

| | | | | | | | |

| | September 30, 2012 | | December 31, 2011 | | | | |

| Debt | | | | | | | |

| Book Value | | | | | | | |

| Fixed Rate Debt | $ | 430,112 |

| | $ | 324,239 |

| | | | |

| Variable Rate Debt | 58,262 |

| | 59,159 |

| | | | |

| Total Debt | $ | 488,374 |

| | $ | 383,398 |

| | | | |

| Weighted Average Effective Rate | | | | | | | |

| Fixed Rate Debt | 7.12 | % | | 7.55 | % | | | | |

| Variable Rate Debt | 5.00 | % | | 5.50 | % | | | | |

| Total Debt | 6.87 | % | | 7.24 | % | | | | |

| | | | | | | | |

| % of Total | | | | | | | |

| Fixed Rate Debt | 88.1 | % | | 84.6 | % | | | | |

| Variable Rate Debt | 11.9 | % | | 15.4 | % | | | | |

| Total Debt | 100.0 | % | | 100.0 | % | | | | |

| | | | | | | | |

| Availability Under Credit Facility: | $ | 201,600 |

| | $ | 100,000 |

| | | | |

| Available Liquidity (Unrestricted Cash and Availability Under Credit Facility) | $ | 232,077 |

| | $ | 142,250 |

| | | | |

(1) Total Debt Investments, gross consists of principal of $21.9 million plus capitalized origination fees of $0.2 million.

(2) EBITDARM and EBITDAR and related coverages for facilities with new tenants/operators are only included in periods subsequent to our acquisition of the facilities and exclude the impact of strategic disposition candidates. All facility financial performance data are presented one month in arrears.

|

| | |

| See reporting definitions. | 3 |

SABRA HEALTH CARE REIT, INC.

CONSOLIDATED STATEMENTS OF INCOME

(dollars in thousands, except per share data)

|

| | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Nine Months Ended September 30, |

| | 2012 | | 2011 | | 2012 | | 2011 |

| Revenues: | | | | | | | |

| Rental income | $ | 25,420 |

| | $ | 21,294 |

| | $ | 73,903 |

| | $ | 57,483 |

|

| Interest income | 618 |

| | 176 |

| | 979 |

| | 393 |

|

| | | | | | | | |

| Total revenues | 26,038 |

| | 21,470 |

| | 74,882 |

| | 57,876 |

|

| | | | | | | | |

| | | | | | | | |

| Expenses: | | | | | | | |

| Depreciation and amortization | 7,496 |

| | 6,850 |

| | 22,356 |

| | 19,227 |

|

| Interest | 9,538 |

| | 7,624 |

| | 25,384 |

| | 22,726 |

|

| General and administrative | 3,778 |

| | 4,652 |

| | 11,588 |

| | 10,245 |

|

| | | | | | | | |

| Total expenses | 20,812 |

| | 19,126 |

| | 59,328 |

| | 52,198 |

|

| | | | | | | | |

| Net income | $ | 5,226 |

| | $ | 2,344 |

| | $ | 15,554 |

| | $ | 5,678 |

|

| | | | | | | | |

| Net income per common share, basic | $ | 0.14 |

| | $ | 0.07 |

| | $ | 0.42 |

| | $ | 0.20 |

|

| | | | | | | | |

| Net income per common share, diluted | $ | 0.14 |

| | $ | 0.07 |

| | $ | 0.42 |

| | $ | 0.20 |

|

| | | | | | | | |

| Weighted-average number of common shares outstanding, basic | 37,178,162 |

| | 32,986,657 |

| | 37,121,384 |

| | 27,797,411 |

|

| | | | | | | | |

| Weighted-average number of common shares outstanding, diluted | 37,465,114 |

| | 33,049,621 |

| | 37,276,013 |

| | 27,891,690 |

|

| | | | | | | | |

|

| | |

| See reporting definitions. | 4 |

SABRA HEALTH CARE REIT, INC.

CONSOLIDATED BALANCE SHEETS

(dollars in thousands, except per share data)

|

| | | | | | | |

| | September 30,

2012 | | December 31,

2011 |

| | (unaudited) | | |

| Assets | | | |

| Real estate investments, net of accumulated depreciation of $131,071 and $108,916 as of September 30, 2012 and December 31, 2011, respectively | $ | 733,054 |

| | $ | 658,377 |

|

| Loans receivable, net | 22,092 |

| | — |

|

| Cash and cash equivalents | 30,477 |

| | 42,250 |

|

| Restricted cash | 5,197 |

| | 6,093 |

|

| Deferred tax assets | 25,540 |

| | 25,540 |

|

| Prepaid expenses, deferred financing costs and other assets | 26,651 |

| | 17,390 |

|

| Total assets | $ | 843,011 |

| | $ | 749,650 |

|

| Liabilities and stockholders’ equity | | | |

| Mortgage notes payable | $ | 157,513 |

| | $ | 158,398 |

|

| Senior unsecured notes payable | 330,861 |

| | 225,000 |

|

| Accounts payable and accrued liabilities | 17,778 |

| | 14,139 |

|

| Tax liability | 25,540 |

| | 25,540 |

|

| Total liabilities | 531,692 |

| | 423,077 |

|

| Commitments and contingencies |

| |

|

| Stockholders’ equity | | | |

| Preferred stock, $.01 par value; 10,000,000 shares authorized, zero shares issued and outstanding as of September 30, 2012 and December 31, 2011 | — |

| | — |

|

| Common stock, $.01 par value; 125,000,000 shares authorized, 37,051,242 and 36,891,712 shares issued and outstanding as of September 30, 2012 and December 31, 2011, respectively | 371 |

| | 369 |

|

| Additional paid-in capital | 351,106 |

| | 344,995 |

|

| Cumulative distributions in excess of net income | (40,158 | ) | | (18,791 | ) |

| Total stockholders’ equity | 311,319 |

| | 326,573 |

|

| Total liabilities and stockholders’ equity | $ | 843,011 |

| | $ | 749,650 |

|

|

| | |

| See reporting definitions. | 5 |

SABRA HEALTH CARE REIT, INC.

CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands)

|

| | | | | | | |

| | Nine Months Ended September 30, |

| | 2012 | | 2011 |

| Cash flows from operating activities: |

| | |

| Net income | $ | 15,554 |

| | $ | 5,678 |

|

| Adjustments to reconcile net income to net cash provided by operating activities: |

| | |

| Depreciation and amortization | 22,356 |

| | 19,227 |

|

Non-cash interest income adjustments

| 18 |

| | — |

|

| Amortization of deferred financing costs | 2,620 |

| | 1,507 |

|

| Stock-based compensation expense | 5,749 |

| | 3,249 |

|

| Amortization of premium on notes payable | (12 | ) | | (11 | ) |

| Amortization of premium on senior unsecured notes | (139 | ) | | — |

|

| Straight-line rental income adjustments | (2,857 | ) | | (720 | ) |

| Changes in operating assets and liabilities: |

|

| | |

| Prepaid expenses and other assets | 116 |

| | 556 |

|

| Accounts payable and accrued liabilities | 7,211 |

| | 7,860 |

|

| Restricted cash | (2,714 | ) | | (2,837 | ) |

| | | |

| Net cash provided by operating activities | 47,902 |

| | 34,509 |

|

| | | |

| Cash flows from investing activities: |

| | |

| Acquisitions of real estate | (98,050 | ) | | (187,700 | ) |

| Origination of loans receivable | (22,111 | ) | | — |

|

| Acquisition of note receivable | — |

| | (5,348 | ) |

| Additions to real estate | (1,039 | ) | | (86 | ) |

| | | |

| Net cash used in investing activities | (121,200 | ) | | (193,134 | ) |

| | | |

| Cash flows from financing activities: |

| | |

| Proceeds from secured revolving credit facility | 42,500 |

| | — |

|

| Proceeds from mortgage notes payable | 35,829 |

| | — |

|

| Proceeds from issuance of senior unsecured notes | 106,000 |

| | — |

|

| Payments on secured revolving credit facility | (42,500 | ) | | — |

|

| Principal payments on mortgage notes payable | (36,701 | ) | | (2,249 | ) |

| Payments of deferred financing costs | (7,045 | ) | | (495 | ) |

| Issuance of common stock | 144 |

| | 163,431 |

|

| Dividends paid | (36,702 | ) | | (19,878 | ) |

| | | |

| Net cash provided by financing activities | 61,525 |

| | 140,809 |

|

| | | |

| Net decrease in cash and cash equivalents | (11,773 | ) | | (17,816 | ) |

| Cash and cash equivalents, beginning of period | 42,250 |

| | 74,233 |

|

| | | |

| Cash and cash equivalents, end of period | $ | 30,477 |

| | $ | 56,417 |

|

| | | |

| Supplemental disclosure of cash flow information: |

| | |

| Interest paid | $ | 17,116 |

| | $ | 17,024 |

|

| | | |

|

| | |

| See reporting definitions. | 6 |

SABRA HEALTH CARE REIT, INC.

RECONCILIATIONS OF NET INCOME TO EBITDA, FUNDS FROM OPERATIONS (FFO),

ADJUSTED FUNDS FROM OPERATIONS (AFFO) AND NORMALIZED AFFO

(dollars in thousands, except per share data)

|

| | | | | | | | | | | | | | | |

| | Three Months Ended September 30, | | Nine Months Ended September 30, |

| | 2012 | | 2011 | | 2012 | | 2011 |

| Net income | $ | 5,226 |

| | $ | 2,344 |

| | $ | 15,554 |

| | $ | 5,678 |

|

| Interest expense | 9,538 |

| | 7,624 |

| | 25,384 |

| | 22,726 |

|

| Depreciation and amortization | 7,496 |

| | 6,850 |

| | 22,356 |

| | 19,227 |

|

| | | | | | | | |

| EBITDA | $ | 22,260 |

| | $ | 16,818 |

| | $ | 63,294 |

| | $ | 47,631 |

|

| | | | | | | | |

| Net income | $ | 5,226 |

| | $ | 2,344 |

| | $ | 15,554 |

| | $ | 5,678 |

|

| Add: | | | | | | | |

| Depreciation of real estate assets | 7,496 |

| | 6,850 |

| | 22,356 |

| | 19,227 |

|

| | | | | | | | |

| Funds from Operations (FFO) | $ | 12,722 |

| | $ | 9,194 |

| | $ | 37,910 |

| | $ | 24,905 |

|

| | | | | | | | |

| Acquisition pursuit costs | 367 |

| | 2,643 |

| | 1,239 |

| | 2,954 |

|

| Stock-based compensation expense | 1,907 |

| | 771 |

| | 5,749 |

| | 3,249 |

|

| Straight-line rental income adjustments | (1,167 | ) | | (591 | ) | | (2,857 | ) | | (720 | ) |

| Amortization of deferred financing costs | 1,173 |

| | 512 |

| | 2,620 |

| | 1,507 |

|

| Amortization of debt premium | (143 | ) | | (4 | ) | | (151 | ) | | (11 | ) |

| Non-cash interest income adjustments | 9 |

| | — |

| | 18 |

| | — |

|

| | | | | | | | |

| Adjusted Funds from Operations (AFFO) | $ | 14,868 |

| | $ | 12,525 |

| | $ | 44,528 |

| | $ | 31,884 |

|

| Start-up costs | — |

| | — |

| | — |

| | 310 |

|

| | | | | | | | |

| Normalized AFFO | $ | 14,868 |

| | $ | 12,525 |

| | $ | 44,528 |

| | $ | 32,194 |

|

| | | | | | | | |

| Net income per diluted common share | $ | 0.14 |

| | $ | 0.07 |

| | $ | 0.42 |

| | $ | 0.20 |

|

| | | | | | | | |

| FFO per diluted common share | $ | 0.34 |

| | $ | 0.28 |

| | $ | 1.02 |

| | $ | 0.89 |

|

| | | | | | | | |

| AFFO per diluted common share | $ | 0.39 |

| | $ | 0.38 |

| | $ | 1.18 |

| | $ | 1.13 |

|

| | | | | | | | |

| Normalized AFFO per diluted common share | $ | 0.39 |

| | $ | 0.38 |

| | $ | 1.18 |

| | $ | 1.14 |

|

| | | | | | | | |

| Weighted average number of common shares outstanding, diluted: | | | | | | | |

| Net income and FFO | 37,465,114 |

| | 33,049,621 |

| | 37,276,013 |

| | 27,891,690 |

|

| AFFO and Normalized AFFO | 37,748,716 |

| | 33,320,262 |

| | 37,660,657 |

| | 28,142,867 |

|

| | | | | | | | |

|

| | |

| See reporting definitions. | 7 |

SABRA HEALTH CARE REIT, INC.

CAPITALIZATION

(dollars in thousands, except per share data) |

| | | | | | | |

| Debt | September 30, 2012 | | December 31, 2011 |

| Secured mortgage debt | $ | 157,513 |

| | $ | 158,398 |

|

| Senior unsecured notes | 330,861 |

| | 225,000 |

|

| Revolving credit facility | — |

| | — |

|

| | | | |

| Total debt | $ | 488,374 |

| | $ | 383,398 |

|

|

| | | | | | | |

Book capitalization(1) | | | |

| Total debt | $ | 488,374 |

| | $ | 383,398 |

|

| Total equity | 311,319 |

| | 326,573 |

|

| | | | |

| Book capitalization | 799,693 |

| | 709,971 |

|

| | | | |

| Accumulated depreciation and amortization | 131,071 |

| | 108,916 |

|

| | | | |

| Undepreciated book capitalization | $ | 930,764 |

| | $ | 818,887 |

|

|

| | | | | | | | | | |

| Enterprise Value | | | | | |

| As of September 30, 2012 | Shares Outstanding | | Price | | Value |

| Common stock | 37,051,242 |

| | $ | 20.01 |

| | $ | 741,395 |

|

| Total debt | | | | | 488,374 |

|

| Cash and cash equivalents | | | | | (30,477 | ) |

| | | | | | |

| Total enterprise value | | | | | $ | 1,199,292 |

|

| | | | | | |

| As of December 31, 2011 | Shares

Outstanding | | Price | | Value |

| Common stock | 36,891,712 |

| | $ | 12.09 |

| | $ | 446,021 |

|

| Total debt | | | | | 383,398 |

|

| Cash and cash equivalents | | | | | (42,250 | ) |

| | | | | | |

| Total enterprise value | | | | | $ | 787,169 |

|

| | | | | | |

|

| | | | | | | | | | | | |

| Common Stock and Equivalents | | | | | | | | |

| | | Weighted Avg. Common Shares |

| | | Three Months Ended September 30, 2012 | | Nine Months Ended September 30, 2012 |

| | | EPS & FFO | | AFFO & Normalized AFFO | | EPS & FFO | | AFFO & Normalized AFFO |

| Common stock | | 37,051,242 |

| | 37,051,242 |

| | 37,007,320 |

| | 37,007,320 |

|

| Common equivalents | | 126,920 |

| | 126,920 |

| | 114,064 |

| | 114,064 |

|

| | | | | | | | | |

| Basic common and common equivalents | | 37,178,162 |

| | 37,178,162 |

| | 37,121,384 |

| | 37,121,384 |

|

| Dilutive securities: | | | | | | | | |

| Restricted stock and units | | 277,021 |

| | 547,848 |

| | 146,033 |

| | 530,677 |

|

| Options | | 9,931 |

| | 22,706 |

| | 8,596 |

| | 8,596 |

|

| | | | | | | | | |

| Diluted common and common equivalents | | 37,465,114 |

| | 37,748,716 |

| | 37,276,013 |

| | 37,660,657 |

|

| | | | | | | | | |

(1) Book capitalization is based on the historical carrying value of Sabra’s real estate investments as previously reported by Sabra's former parent company, Sun Healthcare Group, Inc. ("Old Sun"). Therefore, total equity does not reflect any fair market value adjustment for Sabra’s real estate investments as of November 15, 2010 (the date of Old Sun's restructuring), and accumulated depreciation and amortization are for the period from the date of acquisition of the assets by Old Sun to September 30, 2012.

|

| | |

| See reporting definitions. | 8 |

SABRA HEALTH CARE REIT, INC.

INDEBTEDNESS

September 30, 2012

(dollars in thousands)

|

| | | | | | | | | |

| | Principal | | Weighted Average Effective Rate | | % of Total |

| Fixed rate debt | | | | | |

Secured mortgage debt (1) | $ | 99,251 |

| | 5.04 | % | | 20.4 | % |

Unsecured senior notes (2) | 330,861 |

| | 7.75 | % | | 67.7 | % |

| | | | | | |

| Total fixed rate debt | 430,112 |

| | 7.12 | % | | 88.1 | % |

| | | | | | |

| Variable rate debt | | | | | |

Secured mortgage debt(3) | 58,262 |

| | 5.00 | % | | 11.9 | % |

Revolving credit facility (4) | — |

| | 3.46 | % | | — | % |

| | | | | | |

| Total variable rate debt | 58,262 |

| | 5.00 | % | | 11.9 | % |

| | | | | | |

| Total debt | $ | 488,374 |

| | 6.87 | % | | 100.0 | % |

| | | | | |

| Secured debt | | | | | |

| Secured mortgage debt | $ | 157,513 |

| | 5.03 | % | | 32.3 | % |

Revolving credit facility (4) | — |

| | 3.46 | % | | — | % |

| | | | | | |

| Total secured debt | 157,513 |

| | 5.03 | % | | 32.3 | % |

| | | | | | |

| Unsecured debt | | | | | |

Unsecured senior notes (2) | 330,861 |

| | 7.75 | % | | 67.7 | % |

| | | | | | |

| Total unsecured debt | 330,861 |

| | 7.75 | % | | 67.7 | % |

| | | | | | |

| Total debt | $ | 488,374 |

| | 6.87 | % | | 100.0 | % |

(1) Fixed rate secured mortgage debt includes $30.9 million which converts to a variable interest rate based on 90-day LIBOR plus 4.0% (1.00% floor) effective January 2014. This debt matures in August 2015. Fixed rate secured mortgage debt includes $0.5 million of mortgage premium.

(2) Unsecured senior notes includes $5.9 million of notes premium.

(3) Variable rate secured mortgage debt interest is based on 90-day LIBOR plus 4.0% (1.00% floor).

(4) Borrowings under the revolving credit facility bear interest on the outstanding principal amount at a rate equal to, at our option, LIBOR plus 3.00% - 4.00% or a Base Rate plus 2.00% - 3.00%. The actual interest rate within the applicable range is determined based on our then applicable Consolidated Leverage Ratio.

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Maturities |

| | Secured Mortgage Debt | | Unsecured Senior Notes | | Revolving Credit Facility | | Total |

| | Principal | | Rate (5) | | Principal | | Rate (5) | | Principal | | Rate (5) | | Principal | | Rate (5) |

| October 1 through December 31, 2012 | $ | 936 |

| | 5.09 | % | | $ | — |

| | — |

| | $ | — |

| | — |

| | $ | 936 |

| | 5.09 | % |

| 2013 | 3,851 |

| | 5.10 | % | | — |

| | — |

| | — |

| | — |

| | 3,851 |

| | 5.10 | % |

| 2014 | 4,058 |

| | 5.10 | % | | — |

| | — |

| | — |

| | — |

| | 4,058 |

| | 5.10 | % |

| 2015 | 86,442 |

| | 4.83 | % | | — |

| | — |

| | — |

| | 3.46 | % | | 86,442 |

| | 4.83 | % |

| 2016 | 2,065 |

| | 4.28 | % | | — |

| | — |

| | — |

| | — |

| | 2,065 |

| | 4.28 | % |

| 2017 | 2,165 |

| | 4.26 | % | | — |

| | — |

| | — |

| | — |

| | 2,165 |

| | 4.26 | % |

| 2018 | 2,272 |

| | 4.24 | % | | 325,000 |

| | 8.13 | % | | — |

| | — |

| | 327,272 |

| | 8.10 | % |

| 2019 | 2,385 |

| | 4.22 | % | | — |

| | — |

| | — |

| | — |

| | 2,385 |

| | 4.22 | % |

| 2020 | 2,505 |

| | 4.18 | % | | — |

| | — |

| | — |

| | — |

| | 2,505 |

| | 4.18 | % |

| 2021 | 2,636 |

| | 4.13 | % | | — |

| | — |

| | — |

| | — |

| | 2,636 |

| | 4.13 | % |

| Thereafter | 47,710 |

| | 4.21 | % | | — |

| | — |

| | — |

| | — |

| | 47,710 |

| | 4.21 | % |

| | 157,025 |

| | | | 325,000 |

| | | | — |

| | | | 482,025 |

| | |

| Mortgage premium | 488 |

| | | | 5,861 |

| | | | — |

| | | | 6,349 |

| | |

| Total debt | $ | 157,513 |

| | | | $ | 330,861 |

| | | | $ | — |

| | | | $ | 488,374 |

| | |

| Weighted average maturity in years | 12.8 |

| | | | 6.1 |

| | | | 2.4 |

| | | | 8.3 |

| | |

| Weighted average effective interest rate | 5.03 | % | | | | 7.75 | % | | | | 3.46 | % | | | | 6.87 | % | | |

(5) Represents actual contractual interest rates.

|

| | |

| See reporting definitions. | 9 |

SABRA HEALTH CARE REIT, INC.

DEBT COVENANTS

(dollars in millions)

|

| | | | | | | | | | | | | | | |

| | | | | | | | | |

| | Minimum | | Maximum | | December 31, 2011 | | September 30, 2012 | |

| Credit Facility: | | | | | | | | |

| Consolidated Leverage Ratio | | | 5.75x |

| | 4.26x |

| | 4.68x |

| |

| Consolidated Fixed Charge Coverage Ratio | 1.75x |

| | | | 2.87x |

| | 2.63x |

| |

| Consolidated Tangible Net Worth | $ | 342.0 |

| | | | $ | 425.9 |

| | $ | 428.3 |

| |

| | | | | | | | | |

| Unsecured Senior Notes: | | | | | | | | |

| Total Debt/ Asset Value | | | 60 | % | | 39 | % | | 44 | % | |

| Secured Debt/ Asset Value | | | 40 | % | | 16 | % | | 14 | % | |

| Unencumbered Assets/ Unsecured Debt | 150 | % | | | | 227 | % | | 155 | % | |

| Minimum Interest Coverage | 2.00x |

| | | | 3.17x |

| | 2.88x |

| |

Note: All covenants are based on terms defined in the related credit agreement and unsecured senior notes indenture. Asset Value and Unencumbered Assets used for debt covenant calculation purposes include a value for the initial real estate portfolio obtained in the separation from Sun, which is calculated by dividing the total initial annual rental revenue from this portfolio by an assumed 9.75% capitalization rate. This results in an assumed total portfolio value for the initial real estate portfolio of $720 million.

|

| | |

| See reporting definitions. | 10 |

SABRA HEALTH CARE REIT, INC.

PORTFOLIO SUMMARY - ALL INVESTMENTS

September 30, 2012

(dollars in thousands)

|

| | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | Rental Income | | | | Occupancy Percentage |

| | | | | | | Three Months Ended September 30, | | | | Three Months Ended September 30, |

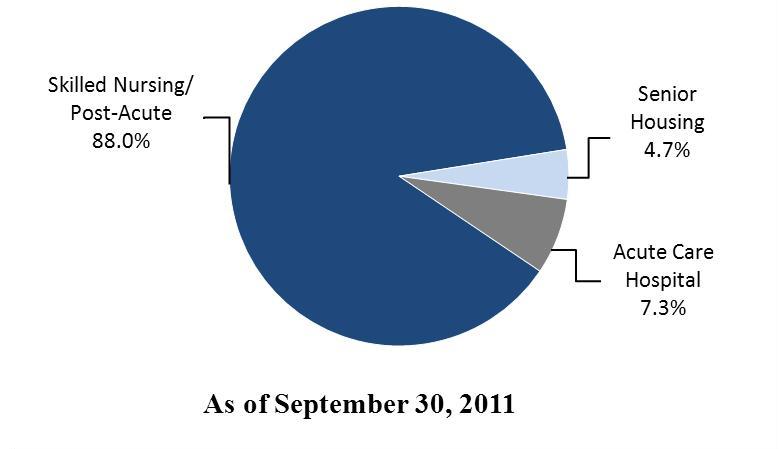

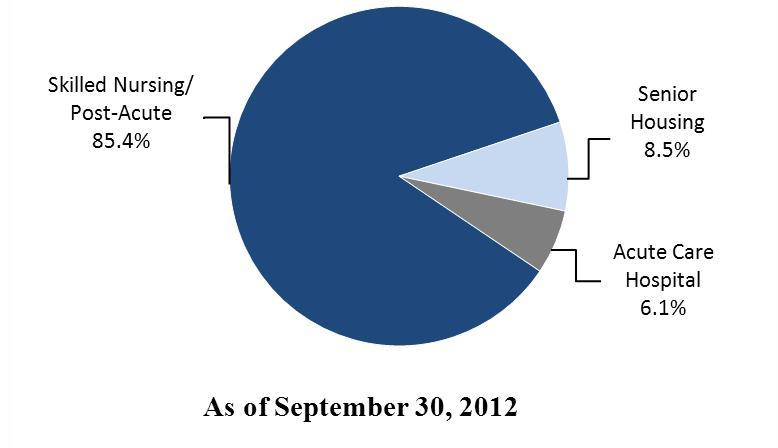

| Facility Type | | Number of Properties | | Investment | | 2012 | | 2011 | | Number of Licensed Beds/Units | | 2012 | | 2011 |

| Skilled Nursing/Post-Acute | | 93 |

| | $ | 712,386 |

| | $ | 22,472 |

| | $ | 18,573 |

| | 10,549 |

| | 89.1 | % | | 88.9 | % |

| Senior Housing | | 11 |

| | 89,853 |

| | 1,300 |

| | 1,073 |

| | 1,070 |

| | 82.3 | % | | 82.4 | % |

| Acute Care Hospital | | 1 |

| | 61,640 |

| | 1,648 |

| | 1,648 |

| | 70 |

| | 66.1 | % | | 68.3 | % |

Total (1) | | 105 |

| | $ | 863,879 |

| | $ | 25,420 |

| | $ | 21,294 |

| | 11,689 |

| | 88.3 | % | | 88.3 | % |

|

| | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, | | Twelve Months Ended September 30, |

| | | 2012 | | 2011 | | 2012 | | 2011 |

| Facility Type | | EBITDARM Coverage | | EBITDAR Coverage | | EBITDARM Coverage | | EBITDAR Coverage | | EBITDARM Coverage | | EBITDAR Coverage | | EBITDARM Coverage | | EBITDAR Coverage |

| Skilled Nursing/Post-Acute | | 1.73x | | 1.43x | | 2.11x | | 1.76x | | 1.75x | | 1.43x | | 2.10x | | 1.76x |

Senior Housing (2) | | 1.43x | | 1.24x | | 1.52x | | 1.77x | | 1.40x | | 1.25x | | 1.63x | | 1.78x |

| Acute Care Hospital | | 3.63x | | 3.59x | | 2.08x | | 2.01x | | 2.96x | | 2.87x | | 2.25x | | 2.15x |

Total (1) | | 1.82x | | 1.54x | | 2.08x | | 1.78x | | 1.80x | | 1.50x | | 2.09x | | 1.79x |

| | | | | | | | | | | | | | | | | |

|

| | | | | | | | | | | | | | | | | | | | | | | | |

| Loan Type | Number of Loans | | Facility Type | | Principal Balance as of September 30, 2012 | | Book Value as of September 30, 2012 | | Contractual Interest Rate | | Annualized Effective Interest Rate | | Interest Income Three Months Ended September 30, 2012 | | Maturity Date |

| Mezzanine | 1 |

| | Skilled Nursing / Assisted Living | | $ | 10,000 |

| | $ | 10,142 |

| | 11.0 | % | | 10.7 | % | | $ | 273 |

| | 3/31/2017 |

| Mortgage | 2 |

| | Skilled Nursing / Assisted Living | | 11,897 |

| | 11,950 |

| | 8.5 | % | | 8.4 | % | | 247 |

| | Various |

| Total | 3 |

| | | | $ | 21,897 |

| | $ | 22,092 |

| | | | | | $ | 520 |

| | |

|

| | | | | | |

| | | Nine Months Ended September 30, |

| Total Revenue | | 2012 | | 2011 |

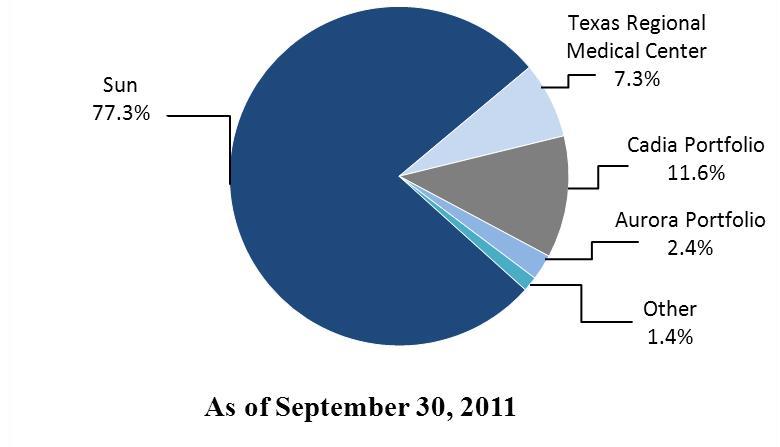

| Sun | | 72.1 | % | | 91.0 | % |

| Cadia Portfolio | | 10.6 |

| | 3.0 |

|

| Texas Regional Medical Center | | 6.7 |

| | 4.7 |

|

| Aurora Portfolio | | 3.3 |

| | — |

|

| Pennsylvania Subacute Portfolio | | 2.3 |

| | — |

|

| Other | | 5.0 |

| | 1.3 |

|

| Total | | 100.0 | % | | 100.0 | % |

(1) Occupancy percentage, EBITDARM and EBITDAR and related coverages are only included in periods subsequent to our acquisition of the facilities for facilities with new tenants/operators and excludes the impact of strategic disposition candidates. All facility financial performance data are presented one month in arrears.

(2) Excluding the impact of Age Well (formerly known as Creekside), which was not stabilized as of September 30, 2012, the three months ended September 30, 2012 EBITDARM Coverage and EBITDAR Coverage for Senior Housing facilities would have been 1.55x and 1.36x, respectively; and for the twelve months ended September 30, 2012, EBITDARM Coverage and EBITDAR Coverage for Senior Housing facilities would have been 1.49x and 1.34x, respectively. See reporting definition for definitions of EBITDARM Coverage and EBITDAR Coverage.

|

| | |

| See reporting definitions. | 11 |

SABRA HEALTH CARE REIT, INC.

PORTFOLIO SUMMARY - SAME STORE (1)

September 30, 2012

(dollars in thousands)

|

| | | | | | | | | | | | | | | | | | | | | | | |

| | | | | Three Months Ended September 30, |

| | | | | Rental Income | | Occupancy Percentage | | Skilled Mix |

| Facility Type | | Number of Properties | | 2012 | | 2011 | | 2012 | | 2011 | | 2012 | | 2011 |

| Skilled Nursing/Post-Acute | | 79 |

| | $ | 17,222 |

| | $ | 16,810 |

| | 88.6 | % | | 88.9 | % | | 37.5 | % | | 41.8 | % |

| Senior Housing | | 8 |

| | 1,099 |

| | 1,073 |

| | 82.7 | % | | 82.4 | % | | NA |

| | NA |

|

| Acute Care Hospital | | 1 |

| | 1,648 |

| | 1,648 |

| | 66.1 | % | | 68.3 | % | | NA |

| | NA |

|

| Total | | 88 |

| | $ | 19,969 |

| | $ | 19,531 |

| | 88.0 | % | | 88.2 | % | | 37.5 | % | | 41.8 | % |

| | | | | | | | | | | | | | | |

|

| | | | | | | | | | | | | | | | |

| | | Three Months Ended September 30, | | Twelve Months Ended September 30, |

| | | 2012 | | 2011 | | 2012 | | 2011 |

| Facility Type | | EBITDARM Coverage | | EBITDAR Coverage | | EBITDARM Coverage | | EBITDAR Coverage | | EBITDARM Coverage | | EBITDAR Coverage | | EBITDARM Coverage | | EBITDAR Coverage |

| Skilled Nursing/Post-Acute | | 1.71x | | 1.45x | | 2.12x | | 1.77x | | 1.75x | | 1.46x | | 2.11x | | 1.77x |

| Senior Housing | | 1.68x | | 1.45x | | 1.52x | | 1.77x | | 1.62x | | 1.46x | | 1.63x | | 1.78x |

| Acute Care Hospital | | 3.63x | | 3.59x | | 2.08x | | 2.01x | | 2.96x | | 2.87x | | 2.25x | | 2.15x |

| Total | | 1.85x | | 1.61x | | 2.08x | | 1.79x | | 1.83x | | 1.56x | | 2.10x | | 1.80x |

| | | | | | | | | | | | | | | | | |

(1) Same Store statistics consist of facilities held or acquired before July 1, 2011 and exclude the impact of strategic disposition candidates.

|

| | |

| See reporting definitions. | 12 |

SABRA HEALTH CARE REIT, INC.

INVESTMENT ACTIVITY

For the Nine Months Ended September 30, 2012

(dollars in thousands)

|

| | | | | | | | | | | | | |

| | | | | | | | | | |

| | Acquisition Date | | Facility Type | | Beds | | Investment Amount | | Initial Cash Yield |

| Real Estate Investments | | | | | | | | | |

| Pennsylvania Subacute Portfolio | 03/30/12 | | Skilled Nursing | | 120 |

| | $ | 29,850 |

| | 9.50 | % |

| Ridgecrest Manor | 05/01/12 | | Skilled Nursing | | 120 |

| | 5,700 |

| | 11.00 |

|

Aurora II Portfolio (1) | 06/01/12 | | Skilled Nursing | | 327 |

| | 20,000 |

| | 10.18 |

|

| New Dawn Memory Care | 09/20/12 | | Senior Housing | | 48 |

| | 16,000 |

| | 8.00 |

|

| Independence Village at Frankenmuth | 09/21/12 | | Senior Housing | | 249 |

| | 26,500 |

| | 8.00 |

|

| Total real estate investments | | | | | 864 |

| | $ | 98,050 |

| | 9.08 | % |

| | | | | | | | | | |

| Debt Investments | | | | | | |

| | |

Meridian Mezzanine Loan (2) | 03/15/12 | | Skilled Nursing/Senior Housing | | | | $ | 10,000 |

| | 11.00 | % |

Onion Creek Mortgage Loan (3) | 06/22/12 | | Skilled Nursing | | | | 11,000 |

| | 8.50 |

|

First Phoenix Mortgage Loan (4) | 08/16/12 | | Senior Housing | | | | 897 |

| | 9.00 |

|

| Total debt investments | | | | | | | $ | 21,897 |

| | 9.66 | % |

| | | | | | | | | | |

| Total Investments | | | | | | | $ | 119,947 |

| | 9.19 | % |

Annualized Revenue Concentration (5)

Annualized Revenue by Asset Class (5)

(1) The total funds paid at closing was $21.8 million, which included $1.8 million in deferred purchase price related to the original Aurora acquisition.

(2) Includes an option to purchase three skilled nursing facilities and one assisted living facility located in Texas.

(3) Includes an option to purchase one skilled nursing facility located in Texas.

(4) Pre-development funding for amount included in pipeline agreement.

(5) September 30, 2011 information excludes interest income on the Hillside Terrace Mortgage Note, which we acquired on March 25, 2011 and was subsequently repaid on December 5, 2011.

|

| | |

| See reporting definitions. | 13 |

SABRA HEALTH CARE REIT, INC.

REAL ESTATE PORTFOLIO GEOGRAPHIC CONCENTRATIONS

September 30, 2012

Property Type

|

| | | | | | | | | | | | | | | |

| State | | Skilled Nursing/Post-Acute | | Senior Housing | | Acute Care Hospital | | Total | | % of Total |

| New Hampshire | | 14 |

| | 2 |

| | — |

| | 16 |

| | 15.2 | % |

| Kentucky | | 13 |

| | 2 |

| | — |

| | 15 |

| | 14.3 |

|

| Connecticut | | 12 |

| | 1 |

| | — |

| | 13 |

| | 12.4 |

|

| Ohio | | 8 |

| | — |

| | — |

| | 8 |

| | 7.6 |

|

| Oklahoma | | 4 |

| | 1 |

| | — |

| | 5 |

| | 4.8 |

|

| Florida | | 5 |

| | — |

| | — |

| | 5 |

| | 4.8 |

|

| Texas | | 3 |

| | — |

| | 1 |

| | 4 |

| | 3.8 |

|

| Delaware | | 4 |

| | — |

| | — |

| | 4 |

| | 3.8 |

|

| Montana | | 4 |

| | — |

| | — |

| | 4 |

| | 3.8 |

|

| Massachusetts | | 3 |

| | — |

| | — |

| | 3 |

| | 2.9 |

|

| Other (16 states) | | 23 |

| | 5 |

| | — |

| | 28 |

| | 26.6 |

|

| | | | | | | | | | | |

| Total | | 93 |

| | 11 |

| | 1 |

| | 105 |

| | 100.0 | % |

| | | | | | | | | | | |

Distribution of Licensed Beds/Units

|

| | | | | | | | | | | | | | | | | | |

| | | Total Number of Properties | | Bed Type | | | |

| State | | | Skilled Nursing/Post-Acute | | Senior Housing | | Acute Care Hospital | | Total | | % of Total |

| Connecticut | | 13 |

| | 1,770 |

| | 49 |

| | — |

| | 1,819 |

| | 15.6 | % |

| New Hampshire | | 16 |

| | 1,464 |

| | 203 |

| | — |

| | 1,667 |

| | 14.3 |

|

| Kentucky | | 15 |

| | 1,020 |

| | 128 |

| | — |

| | 1,148 |

| | 9.8 |

|

| Ohio | | 8 |

| | 897 |

| | — |

| | — |

| | 897 |

| | 7.7 |

|

| Florida | | 5 |

| | 660 |

| | — |

| | — |

| | 660 |

| | 5.6 |

|

| Oklahoma | | 5 |

| | 501 |

| | 83 |

| | — |

| | 584 |

| | 5.0 |

|

| Montana | | 4 |

| | 538 |

| | — |

| | — |

| | 538 |

| | 4.6 |

|

| Delaware | | 4 |

| | 500 |

| | — |

| | — |

| | 500 |

| | 4.3 |

|

| Texas | | 4 |

| | 360 |

| | — |

| | 70 |

| | 430 |

| | 3.7 |

|

| Colorado | | 3 |

| | 362 |

| | 48 |

| | — |

| | 410 |

| | 3.5 |

|

| Other (16 states) | | 28 |

| | 2,477 |

| | 559 |

| | — |

| | 3,036 |

| | 25.9 |

|

| | | | | | | | | | | | | |

| Total | | 105 |

| | 10,549 |

| | 1,070 |

| | 70 |

| | 11,689 |

| | 100.0 | % |

| | | | | | | | | | | | | |

| % of Total beds/units | | | | 90.2 | % | | 9.2 | % | | 0.6 | % | | 100.0 | % | | |

| | | | | | | | | | | | | |

|

| | |

| See reporting definitions. | 14 |

SABRA HEALTH CARE REIT, INC.

REAL ESTATE PORTFOLIO GEOGRAPHIC CONCENTRATIONS

September 30, 2012

(dollars in thousands)

Investment

|

| | | | | | | | | | | | | | | | | | | | | | |

| State | | Total

Number of

Centers | | Skilled Nursing/Post-Acute | | Senior Housing | | Acute Care Hospital | | Total | | % of Total |

| Connecticut | | 13 |

| | $ | 144,470 |

| | $ | 8,008 |

| | $ | — |

| | $ | 152,478 |

| | 17.7 | % |

| Delaware | | 4 |

| | 95,780 |

| | — |

| | — |

| | 95,780 |

| | 11.1 |

|

| New Hampshire | | 16 |

| | 77,895 |

| | 12,997 |

| | — |

| | 90,892 |

| | 10.5 |

|

| Texas | | 4 |

| | 24,959 |

| | — |

| | 61,640 |

| | 86,599 |

| | 10.0 |

|

| Kentucky | | 15 |

| | 60,551 |

| | 10,503 |

| | — |

| | 71,054 |

| | 8.2 |

|

| Colorado | | 3 |

| | 28,920 |

| | 15,702 |

| | — |

| | 44,622 |

| | 5.2 |

|

| Ohio | | 8 |

| | 43,662 |

| | — |

| | — |

| | 43,662 |

| | 5.1 |

|

| Montana | | 4 |

| | 42,809 |

| | — |

| | — |

| | 42,809 |

| | 5.0 |

|

| Florida | | 5 |

| | 31,600 |

| | — |

| | — |

| | 31,600 |

| | 3.7 |

|

| Oklahoma | | 5 |

| | 24,230 |

| | 5,708 |

| | — |

| | 29,938 |

| | 3.5 |

|

| Other (16 states) | | 28 |

| | 137,510 |

| | 36,935 |

| | — |

| | 174,445 |

| | 20.0 |

|

| | | | | | | | | | | | | |

| Total | | 105 |

| | $ | 712,386 |

| | $ | 89,853 |

| | $ | 61,640 |

| | $ | 863,879 |

| | 100.0 | % |

| | | | | | | | | | | | | |

| % of Total Centers | | | | 82.5 | % | | 10.4 | % | | 7.1 | % | | 100.0 | % | | |

| | | | | | | | | | | | | |

|

| | |

| See reporting definitions. | 15 |

SABRA HEALTH CARE REIT, INC.

PORTFOLIO GEOGRAPHIC CONCENTRATIONS

September 30, 2012

(dollars in thousands)

Rental Income - Three Months Ended September 30, 2012

|

| | | | | | | | | | | | | | | | | | | | | | |

| State | | Total

Number of

Centers | | Skilled Nursing/Post-Acute | | Senior Housing | | Acute Care Hospital | | Total | | % of Total |

| Connecticut | | 13 |

| | $ | 3,392 |

| | $ | 74 |

| | $ | — |

| | $ | 3,466 |

| | 13.6 | % |

| New Hampshire | | 16 |

| | 3,026 |

| | 335 |

| | — |

| | 3,361 |

| | 13.2 |

|

| Delaware | | 4 |

| | 2,645 |

| | — |

| | — |

| | 2,645 |

| | 10.4 |

|

| Kentucky | | 15 |

| | 2,364 |

| | 119 |

| | — |

| | 2,483 |

| | 9.8 |

|

| Texas | | 4 |

| | 735 |

| | — |

| | 1,648 |

| | 2,383 |

| | 9.4 |

|

| Florida | | 5 |

| | 1,967 |

| | — |

| | — |

| | 1,967 |

| | 7.7 |

|

| Ohio | | 8 |

| | 1,313 |

| | — |

| | — |

| | 1,313 |

| | 5.2 |

|

| Montana | | 4 |

| | 1,304 |

| | — |

| | — |

| | 1,304 |

| | 5.1 |

|

| Colorado | | 3 |

| | 829 |

| | 45 |

| | — |

| | 874 |

| | 3.4 |

|

| Pennsylvania | | 2 |

| | 847 |

| | — |

| | — |

| | 847 |

| | 3.3 |

|

| Other (16 states) | | 31 |

| | 4,050 |

| | 727 |

| | — |

| | 4,777 |

| | 18.9 |

|

| | | | | | | | | | | | | |

| Total | | 105 |

| | $ | 22,472 |

| | $ | 1,300 |

| | $ | 1,648 |

| | $ | 25,420 |

| | 100.0 | % |

| | | | | | | | | | | | | |

| % of Total centers | | | | 88.4 | % | | 5.1 | % | | 6.5 | % | | 100.0 | % | | |

| | | | | | | | | | | | | |

Rental Income - Nine Months Ended September 30, 2012

|

| | | | | | | | | | | | | | | | | | | | | | |

| State | | Total

Number of

Centers | | Skilled Nursing/Post-Acute | | Senior Housing | | Acute Care Hospital | | Total | | % of Total |

| New Hampshire | | 16 |

| | $ | 8,902 |

| | $ | 1,006 |

| | $ | — |

| | $ | 9,908 |

| | 13.4 | % |

| Connecticut | | 13 |

| | 9,335 |

| | 221 |

| | — |

| | 9,556 |

| | 12.9 |

|

| Delaware | | 4 |

| | 7,934 |

| | — |

| | — |

| | 7,934 |

| | 10.7 |

|

| Kentucky | | 15 |

| | 7,093 |

| | 356 |

| | — |

| | 7,449 |

| | 10.1 |

|

| Texas | | 4 |

| | 2,204 |

| | — |

| | 4,945 |

| | 7,149 |

| | 9.7 |

|

| Florida | | 5 |

| | 5,901 |

| | — |

| | — |

| | 5,901 |

| | 8.0 |

|

| Ohio | | 8 |

| | 3,938 |

| | — |

| | — |

| | 3,938 |

| | 5.3 |

|

| Montana | | 4 |

| | 3,912 |

| | — |

| | — |

| | 3,912 |

| | 5.3 |

|

| Colorado | | 3 |

| | 2,487 |

| | 45 |

| | — |

| | 2,532 |

| | 3.4 |

|

| Idaho | | 3 |

| | 2,169 |

| | — |

| | — |

| | 2,169 |

| | 2.9 |

|

| Other (16 states) | | 30 |

| | 11,446 |

| | 2,009 |

| | — |

| | 13,455 |

| | 18.3 |

|

| | | | | | | | | | | | | |

| Total | | 105 |

| | $ | 65,321 |

| | $ | 3,637 |

| | $ | 4,945 |

| | $ | 73,903 |

| | 100.0 | % |

| | | | | | | | | | | | | |

| % of Total centers | | | | 88.4 | % | | 4.9 | % | | 6.7 | % | | 100.0 | % | | |

| | | | | | | | | | | | | |

|

| | |

| See reporting definitions. | 16 |

SABRA HEALTH CARE REIT, INC.

SKILLED MIX AND OCCUPANCY PERCENTAGE

|

| | | | | | | | | | | | | | | | | | | | |

| | Skilled Mix (1) |

| | Three Months Ended September 30, | | Nine Months Ended September 30, | | Year Ended December 31, |

| | 2012 | | 2011 | | 2012 | | 2011 | | 2011 | | 2010 | | 2009 |

| Skilled Nursing | 36.3 | % | | 42.1 | % | | 37.5 | % | | 42.4 | % | | 41.7 | % | | 39.5 | % | | 39.3 | % |

| | | | | | | | | | | | | | |

| | Occupancy Percentage (1) |

| | Three Months Ended September 30, | | Nine Months Ended September 30, | | Year Ended December 31, |

| | 2012 | | 2011 | | 2012 | | 2011 | | 2011 | | 2010 | | 2009 |

| Skilled Nursing/Post-Acute | 89.1 | % | | 88.9 | % | | 89.4 | % | | 89.2 | % | | 89.1 | % | | 89.0 | % | | 90.4 | % |

| Senior Housing | 82.3 |

| | 82.4 |

| | 88.6 |

| | 82.3 |

| | 82.7 |

| | 84.4 |

| | 88.3 |

|

| Acute Care Hospital | 66.1 |

| | 68.3 |

| | 67.7 |

| | 73.6 |

| | 71.8 |

| | N/A |

| | N/A |

|

| | | | | | | | | | | | | | |

| Weighted Average | 88.3 | % | | 88.3 | % | | 89.2 | % | | 88.6 | % | | 88.5 | % | | 88.6 | % | | 90.2 | % |

(1) Skilled mix and occupancy percentage for facilities with new tenants/operators are only included in periods subsequent to our acquisition of the facilities and exclude the impact of strategic disposition candidates. All facility financial performance data are presented one month in arrears.

|

| | |

| See reporting definitions. | 17 |

SABRA HEALTH CARE REIT, INC.

PORTFOLIO LEASE EXPIRATIONS

September 30, 2012

(dollars in thousands)

|

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | 2012 - 2019 | | 2020 | | 2021 | | 2022 | | 2023 | | 2024 | | 2025 | | Thereafter | | Total |

| Skilled Nursing/Post-Acute | | | | | | | | | | | | | | | | | |

| Properties | — |

| | 29 |

| | 30 |

| | 12 |

| | — |

| | 1 |

| | 6 |

| | 15 |

| | 93 |

|

| Annualized Revenues | $ | — |

| | $ | 24,607 |

| | $ | 27,183 |

| | $ | 8,246 |

| | $ | — |

| | $ | 1,821 |

| | $ | 5,748 |

| | $ | 22,286 |

| | $ | 89,891 |

|

| Senior Housing | | | | | | | | | | | | | | | | | |

| Properties | — |

| | 2 |

| | 3 |

| | 4 |

| | — |

| | — |

| | 2 |

| | — |

| | 11 |

|

| Annualized Revenues | — |

| | 1,762 |

| | 1,368 |

| | 4,371 |

| | — |

| | — |

| | 1,225 |

| | — |

| | 8,726 |

|

| Acute Care Hospital | | | | | | | | | | | | | | | | | |

| Properties | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 1 |

| | 1 |

|

| Annualized Revenues | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | — |

| | 6,593 |

| | 6,593 |

|

| | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| Total Properties | — |

| | 31 |

| | 33 |

| | 16 |

| | — |

| | 1 |

| | 8 |

| | 16 |

| | 105 |

|

| | | | | | | | | | | | | | | | | | |

| Total Annualized Revenues | $ | — |

| | $ | 26,369 |

| | $ | 28,551 |

| | $ | 12,617 |

| | $ | — |

| | $ | 1,821 |

| | $ | 6,973 |

| | $ | 28,879 |

| | $ | 105,210 |

|

| | | | | | | | | | | | | | | | | | |

| % of Revenue | — | % | | 25.2 | % | | 27.1 | % | | 12.0 | % | | — | % | | 1.7 | % | | 6.6 | % | | 27.4 | % | | 100.0 | % |

| | | | | | | | | | | | | | | | | | |

|

| | |

| See reporting definitions. | 18 |

SABRA HEALTH CARE REIT, INC.

RECENT INVESTMENT ACTIVITY

Independence Village at Frankenmuth

|

| | |

| • Acquisition Date: | | September 21, 2012 |

| | | |

| • Purchase Price: | | $26.5 million |

| | | |

| • Investment Type: | | Equity |

| | | |

| • Number of Properties: | | 1 |

| | | |

| • Location: | | Michigan |

| | | |

| • Available Beds: | | 249 |

| | | |

| • Property Type: | | Independent Living Facility |

| | | |

| • Annualized GAAP Rental Income: | | $2.4 million |

| | | |

| • Initial Cash Yield: | | 8.00% |

|

| | |

| See reporting definitions. | 19 |

SABRA HEALTH CARE REIT, INC.

RECENT INVESTMENT ACTIVITY

New Dawn Memory Care

|

| | |

| • Acquisition Date: | | September 20, 2012 |

| | | |

| • Purchase Price: | | $16.0 million |

| | | |

| • Investment Type: | | Equity |

| | | |

| • Number of Properties: | | 1 |

| | | |

| • Location: | | Colorado |

| | | |

| • Available Beds: | | 48 |

| | | |

| • Property Type: | | Assisted Living Facility / Memory Care |

| | | |

| • Annualized GAAP Rental Income: | | $1.5 million |

| | | |

| • Initial Cash Yield: | | 8.00% |

|

| | |

| See reporting definitions. | 20 |

SABRA HEALTH CARE REIT, INC.

RECENT INVESTMENT ACTIVITY

First Phoenix Pipeline Agreement and Mortgage Loan

|

| | |

| | | |

| | | |

| Pipeline Agreement | | |

| | | |

| • Investment Type: | | Pipeline Agreement & RIDEA JV |

| | | |

| • Estimated Investment: | | $150.0 million |

| | | |

| • Property Type: | | Assisted Living & Memory Care |

| | | |

| • Target Markets: | | Minnesota, Wisconsin and Colorado |

| | | |

| • Number of Properties: | | 10 developments identified through 2014 |

| | | |

| • Expected Number of Units: | | 50-72 per facility |

| | | |

| | | |

| Pre-Development Loan Agreement | | |

| | | |

| • Funding Date: | | August 16, 2012 |

| | | |

| • Loan Amount: | | $1.0 million |

| | | |

| • Annualized GAAP Interest Income: | | $0.1 million |

| | | |

| • Initial Cash Yield: | | 9.00% |

|

| | |

| See reporting definitions. | 21 |

SABRA HEALTH CARE REIT, INC.

RECENT INVESTMENT ACTIVITY - PRO FORMA INFORMATION

(dollars in thousands, except per share data)

Note: The following pro forma information assumes the acquisitions of the Pennsylvania Subacute Portfolio, Ridgecrest Manor, Aurora II Portfolio, New Dawn Memory Care, Independence Village at Frankenmuth, the origination of the Meridian Mezzanine loan, Onion Creek Mortgage loan and First Phoenix pre-development loan, the payoff of the revolving credit facility and the additional $100.0 million aggregate principal amount of senior notes issued were completed as of January 1, 2012.

Pro Forma Net Income, FFO, AFFO, and Normalized AFFO

|

| | | | | | |

| | Three Months Ended September 30, 2012 | Nine Months Ended September 30, 2012 |

| Net income | $ | 5,226 |

| $ | 15,554 |

|

| Revenues - real estate and debt investments | 872 |

| 5,722 |

|

| Depreciation and amortization - acquisitions (estimated) | (260 | ) | (1,251 | ) |

| Interest - senior unsecured notes and revolving credit facility (estimated) | (390 | ) | (3,977 | ) |

| Amortization of deferred financing costs - senior unsecured notes (estimated) | (43 | ) | (283 | ) |

| Pro forma net income | $ | 5,405 |

| $ | 15,765 |

|

| | | |

| Pro forma net income | $ | 5,405 |

| $ | 15,765 |

|

| Add: |

| |

| Depreciation of real estate assets (estimated) | 7,756 |

| 23,607 |

|

| Pro forma FFO | $ | 13,161 |

| $ | 39,372 |

|

| Straight-line rental income adjustments | (1,277 | ) | (3,582 | ) |

| Acquisition pursuit costs | 367 |

| 1,239 |

|

| Stock-based compensation expense | 1,907 |

| 5,749 |

|

| Amortization of deferred financing costs (estimated) | 1,216 |

| 2,903 |

|

| Amortization of debt premium (estimated) | (197 | ) | (602 | ) |

| Non-cash interest income adjustments | 9 |

| 18 |

|

| Pro forma AFFO | $ | 15,186 |

| $ | 45,097 |

|

| | | |

| Pro forma net income per diluted common share | $ | 0.14 |

| $ | 0.42 |

|

| | | |

| Pro forma FFO per diluted common share | $ | 0.35 |

| $ | 1.06 |

|

| | | |

| Pro forma AFFO per diluted common share | $ | 0.40 |

| $ | 1.20 |

|

| | | |

| Weighted average number of common shares outstanding, diluted | | |

| Pro forma net income and FFO | 37,465,114 |

| 37,276,013 |

|

| Pro forma AFFO | 37,748,716 |

| 37,660,657 |

|

|

| | |

| See reporting definitions. | 22 |

SABRA HEALTH CARE REIT, INC.

REPORTING DEFINITIONS

Acute Care Hospital. A facility designed to provide extended medical and rehabilitation care for patients who are clinically complex and have multiple acute or chronic conditions.

Annualized Revenues. The annual straight-line rental revenues under leases. Annualized Revenues do not include tenant recoveries or additional rents. The Company uses Annualized Revenues for the purpose of determining tenant concentrations and lease expirations.

Assisted Living Facility (“ALF”). A senior housing facility that predominantly consists of assisted living units is classified by the Company as an ALF.

Continuing Care Retirement Community (“CCRC”). A senior housing facility which provides at least three levels of care (i.e., independent living, assisted living and skilled nursing) is classified by the Company as a CCRC.

EBITDA. The real estate industry uses earnings before interest, taxes, depreciation and amortization (“EBITDA”), a non-GAAP financial measure, as a measure of both operating performance and liquidity. The Company uses EBITDA to measure both its operating performance and liquidity. By excluding interest expense, EBITDA allows investors to measure the Company’s operating performance independent of its capital structure and indebtedness and, therefore, allows for a more meaningful comparison of its operating performance between quarters as well as annual periods and to compare its operating performance to that of other companies, both in the real estate industry and in other industries. As a liquidity measure, the Company believes that EBITDA helps investors analyze the Company’s ability to meet its interest payments on outstanding debt. The Company believes investors should consider EBITDA in conjunction with net income (the primary measure of the Company’s performance) and the other required GAAP measures of its performance and liquidity, to improve their understanding of the Company’s operating results and liquidity, and to make more meaningful comparisons of its performance between periods and against other companies. EBITDA has limitations as an analytical tool and should be used in conjunction with the Company’s required GAAP presentations. EBITDA does not reflect the Company’s historical cash expenditures or future cash requirements for capital expenditures or contractual commitments. While EBITDA is a relevant and widely used measure of operating performance and liquidity, it does not represent net income or cash flow from operations as defined by GAAP and it should not be considered as an alternative to those indicators in evaluating operating performance or liquidity. Further, the Company’s computation of EBITDA may not be comparable to similar measures reported by other companies.

EBITDAR. Earnings before interest, taxes, depreciation, amortization and rent (“EBITDAR”) for a particular facility accruing to the operator/tenant of the property (not the Company) for the period presented plus EBITDAR (excluding one-time adjustments) for the period presented for all other operations of any entities that guarantee the tenants' lease obligations to the Company (if applicable). The Company uses EBITDAR in determining EBITDAR Coverage. EBITDAR has limitations as an analytical tool. EBITDAR does not reflect historical cash expenditures or future cash requirements for facility capital expenditures or contractual commitments. In addition, EBITDAR does not represent a property's net income or cash flow from operations and should not be considered an alternative to those indicators. The Company receives EBITDAR and other information from its operators/tenants and relevant guarantors and utilizes EBITDAR as a supplemental measure of their ability to generate sufficient liquidity to meet related obligations to the Company. All facility and tenant financial performance data is derived solely from information provided by operators/tenants and guarantors without independent verification by the Company and is presented one month in arrears. The Company includes EBITDAR with respect to a property if the property was operated at any time during the period presented subject to a lease with the Company. EBITDAR for facilities with new tenants/operators are only included in periods subsequent to the Company's acquisition of the facilities. EBITDAR excludes the impact of strategic disposition candidates.

EBITDAR Coverage. EBITDAR for the trailing 3 and 12 month periods prior to and including the period presented divided by the same period cash rent for all of our facilities plus rent expense for other operations of any entity that guarantees the tenants' lease obligation to the Company. EBITDAR Coverage is a supplemental measure of an operator/tenant's and relevant guarantor's ability to meet their cash rent and other obligations to the Company. However, its usefulness is limited by, among other things, the same factors that limit the usefulness of EBITDAR. All facility and tenant data are derived solely from information provided by operators/tenants and guarantors without independent verification by the Company. All such data is presented one month in arrears and excludes the impact of strategic disposition candidates.

EBITDARM. Earnings before interest, taxes, depreciation, amortization, rent and management fees ("EBITDARM") for a particular facility accruing to the operator/tenant of the property (not the Company), for the period presented. The Company uses EBITDARM in determining EBITDARM Coverage. The usefulness of EBITDARM is limited by the same factors that limit the usefulness of EBITDAR. Together with EBITDAR, the Company utilizes EBITDARM to evaluate the core operations of the properties by eliminating management fees, which vary based on operator/tenant and its operating structure. All facility financial performance data is derived solely from information provided by operators/tenants without independent verification by the Company. All such data is presented one month in arrears. The Company includes EBITDARM for a property if it was operated at any time during the period presented subject to a lease with the Company. EBITDARM for facilities with new tenants/operators are only included in periods subsequent to our acquisition of the facilities. EBITDARM excludes the impact of strategic disposition candidates.

EBITDARM Coverage. EBITDARM for the trailing 3 and 12 month periods prior to and including the period presented divided by the same period cash rent. EBITDARM coverage is a supplemental measure of a property's ability to generate cash flows for the operator/tenant (not the Company) to meet the operator's/tenant's related cash rent and other obligations to the Company. However, its usefulness is limited by,

SABRA HEALTH CARE REIT, INC.

REPORTING DEFINITIONS

among other things, the same factors that limit the usefulness of EBITDARM. All facility data is derived solely from information provided by operators/tenants without independent verification by the Company. All such data is presented one month in arrears and excludes the impact of strategic disposition candidates.

Enterprise Value. The Company believes Enterprise Value is an important measurement as it is a measure of a company’s value. We calculate Enterprise Value as market equity capitalization plus debt. Market equity capitalization is calculated as the number of shares of common stock multiplied by the closing price of our common stock on the last day of the period presented. Total Enterprise Value includes our market equity capitalization and consolidated debt, less cash and cash equivalents.

Funds From Operations (“FFO”) and Adjusted Funds from Operations (“AFFO”). The Company believes that net income as defined by GAAP is the most appropriate earnings measure. The Company also believes that Funds From Operations, or FFO, as defined in accordance with the definition used by the National Association of Real Estate Investment Trusts (“NAREIT”), and Adjusted Funds from Operations or AFFO (and related per share amounts) are important non-GAAP supplemental measures of operating performance for a real estate investment trust. Because the historical cost accounting convention used for real estate assets requires straight-line depreciation (except on land), such accounting presentation implies that the value of real estate assets diminishes predictably over time. However, since real estate values have historically risen or fallen with market and other conditions, presentations of operating results for a real estate investment trust that uses historical cost accounting for depreciation could be less informative. Thus, NAREIT created FFO as a supplemental measure of operating performance for real estate investment trusts that excludes historical cost depreciation and amortization, among other items, from net income, as defined by GAAP. FFO is defined as net income, computed in accordance with GAAP, excluding gains or losses from real estate dispositions, plus real estate depreciation and amortization. AFFO is defined as FFO excluding non-cash revenues (including straight-line rental income adjustments, amortization of acquired above/below market lease intangibles and non-cash interest income adjustments), non-cash expenses (including stock-based compensation expense, amortization of deferred financing costs and amortization of debt discounts and premiums) and acquisition pursuit costs. The Company believes that the use of FFO and AFFO (and the related per share amounts), combined with the required GAAP presentations, improves the understanding of operating results of real estate investment trusts among investors and makes comparisons of operating results among such companies more meaningful. The Company considers FFO and AFFO to be useful measures for reviewing comparative operating and financial performance because, by excluding gains or losses related to sales of previously depreciated operating real estate assets and real estate depreciation and amortization, and, for AFFO, by excluding non-cash revenues (including straight-line rental income adjustments, amortization of acquired above/below market lease intangibles and non-cash interest income adjustments), non-cash expenses (including stock-based compensation expense, amortization of deferred financing costs and amortization of debt discounts and premiums) and acquisition pursuit costs, FFO and AFFO can help investors compare the operating performance of the Company between periods or as compared to other companies. While FFO and AFFO are relevant and widely used measures of operating performance of real estate investment trusts, they do not represent cash flows from operations or net income as defined by GAAP and should not be considered an alternative to those measures in evaluating the Company’s liquidity or operating performance. FFO and AFFO also do not consider the costs associated with capital expenditures related to the Company’s real estate assets nor do they purport to be indicative of cash available to fund the Company’s future cash requirements. Further, the Company’s computation of FFO and AFFO may not be comparable to FFO and AFFO reported by other real estate investment trusts that do not define FFO in accordance with the current NAREIT definition or that interpret the current NAREIT definition or define AFFO differently from the Company.

Independent Living Facility (“ILF”). A senior housing facility that predominantly consists of independent living units.

Investment. Represents the carrying amount of real estate assets after adding back accumulated depreciation and amortization.

Licensed Beds/Units. Senior housing facilities are measured in units (e.g., studio, one or two bedroom units). Skilled nursing and mental health facilities are measured in licensed bed count. All facility financial performance data were derived solely from information provided by operators/tenants without independent verification by the Company.

Market Capitalization. Total common shares of Sabra outstanding multiplied by the closing price per share as of a given period.

Mental Health Facility. Mental Health Facilities provide a range of inpatient and outpatient behavioral health services for adults and children through specialized treatment programs.

Multi-License Designation. A senior housing facility that provides two levels of care (i.e. skilled nursing and assisted living or assisted living and independent living) is classified by the Company as Multi-License Designation.

Normalized AFFO. Normalized AFFO represents AFFO adjusted for one-time start-up costs and non-recurring income and expenses. The Company considers normalized AFFO to be a useful measure to evaluate the Company’s operating results excluding start-up costs and non-recurring income and expenses. Normalized AFFO can help investors compare the operating performance of the Company between periods or as compared to other companies. Normalized AFFO does not represent cash flows from operations or net income as defined by GAAP and should not be considered an alternative to those measures in evaluating the Company’s liquidity or operating performance. Normalized AFFO also does not consider the costs associated with capital expenditures related to the Company’s real estate assets nor does it purport to be indicative of cash available to fund the Company’s future cash requirements. Further, the Company’s computation of normalized AFFO may not be comparable to normalized AFFO reported by other REITs that do not define FFO in accordance with the current NAREIT definition or that interpret the current NAREIT definition or define AFFO or normalized AFFO differently from the Company.

SABRA HEALTH CARE REIT, INC.

REPORTING DEFINITIONS

Occupancy Percentage. Occupancy Percentage represents the facilities’ average operating occupancy for the period indicated. The percentages are calculated by dividing the actual census from the period presented by the available beds/units for the same period. Occupancy for independent living facilities can be greater than 100% for a given period as multiple residents could occupy a single unit. All facility financial performance data were derived solely from information provided by operators/tenants without independent verification by the Company. All facility financial performance data are presented one month in arrears. The Company includes the occupancy percentage for a property if it was owned by the Company at any time during the period presented and excludes the impact of strategic disposition candidates. Occupancy Percentage for facilities with new tenants/operators are only included in periods subsequent to our acquisition of the facilities.

Senior Housing. Senior housing facilities include independent living, assisted living and continuing care retirement community facilities.

Skilled Mix. Skilled Mix is defined as the total Medicare and non-Medicaid managed care patient revenue at skilled nursing facilities divided by the total revenues at skilled nursing facilities for any given period. All facility financial performance data were derived solely from information provided by the Company's tenants without independent verification by the Company. All facility financial performance data are presented one month in arrears. The Company includes skilled mix for a property if it was owned by the Company at any time during the period presented and excludes the impact of strategic disposition candidates. Skilled Mix for facilities with new tenants/operators are only included in periods subsequent to our acquisition of the facilities.

Skilled Nursing/Post-Acute. Skilled nursing/post-acute facilities include skilled nursing facilities, multi-license designation, and mental health facilities.

Total Debt. The carrying amount of the Company’s secured revolving credit facility, senior unsecured notes, and mortgage indebtedness, as reported in the Company’s consolidated financial statements.

Total Secured Debt. Mortgage and other debt secured by real estate.