|

| | |

| | |

| | P.O. Box 29243 - Phoenix, Arizona 85038-9243 |

| | 2200 S. 75th Avenue - Phoenix, Arizona 85043 |

| | (602) 269-9700 |

| | |

April 27, 2015

Dear Fellow Stockholders of Swift Transportation Company (NYSE: SWFT),

A summary of our key results for the three months ended March 31st is shown below:

|

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 | | 2013 |

| | Unaudited |

| | ($ in millions, except per share data) |

| Operating Revenue | $ | 1,015.1 |

| | $ | 1,008.4 |

| | $ | 981.6 |

|

Revenue xFSR(1) | $ | 894.9 |

| | $ | 817.0 |

| | $ | 784.6 |

|

| | | | | | |

| Operating Ratio | 92.6 | % | | 95.4 | % | | 92.9 | % |

Adjusted Operating Ratio(2) | 91.2 | % | | 93.9 | % | | 90.6 | % |

| | | | | | |

EBITDA(2) | $ | 135.3 |

| | $ | 104.5 |

| | $ | 130.4 |

|

Adjusted EBITDA(2) | $ | 138.2 |

| | $ | 108.5 |

| | $ | 136.0 |

|

| | | | | | |

| Diluted EPS | $ | 0.26 |

| | $ | 0.09 |

| | $ | 0.21 |

|

Adjusted EPS(2) | $ | 0.29 |

| | $ | 0.12 |

| | $ | 0.24 |

|

| | | | | | |

1Revenue xFSR is operating revenue, excluding fuel surcharge revenue |

2 See GAAP to Non-GAAP reconciliation in the schedules following this letter |

Key Highlights for the First Quarter 2015 as compared to the First Quarter 2014:

(discussed in more detail below, including GAAP to non-GAAP reconciliations)

Consolidated

| |

• | Adjusted EPS increased 141.7% to $0.29, compared to $0.12 |

| |

| • | Consolidated Revenue xFSR grew 9.5% |

| |

| • | Consolidated Average Operational Truck Count increased 766 trucks, or 4.5% across our various reporting segments |

| |

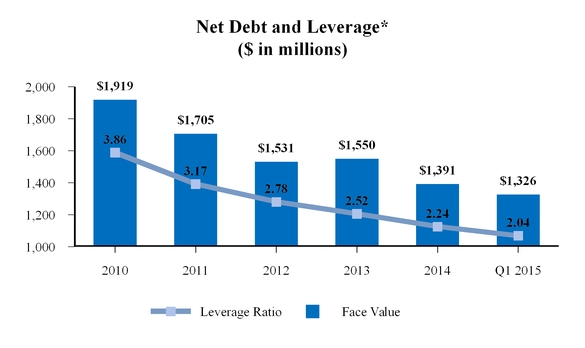

| • | Net Debt was reduced by $65.4 million to $1,325.5 million during the quarter and our net leverage ratio dropped to 2.04 as of March 31, 2015 |

Truckload

| |

| • | Truckload Adjusted Operating Ratio improved 490 basis points to 87.9% |

| |

| • | Truckload utilization, as measured by loaded miles per tractor per week, improved 1.1% |

| |

| • | Truckload pricing increases continued to gain momentum, resulting in a 6.0% increase in Revenue xFSR per loaded mile |

Dedicated

| |

| • | Dedicated Revenue xFSR grew 24.8% driven by the addition of multiple new customer contracts over the last 12 months |

| |

| • | Adjusted Operating Ratio remains flat as operational improvements help offset driver pay increases |

Central Refrigerated Services ("CRS")

| |

| • | CRS Adjusted Operating Ratio improved 300 basis points to 94.1% |

| |

| • | CRS weekly revenue xFSR per tractor increased 5.3% |

| |

| • | Terminated contract with a significant specialty dedicated account, after not attaining profitability targets |

Intermodal

| |

| • | Intermodal Revenue xFSR grew 5.9% on Container on Flat Car growth of 16.1%, partially offset by a reduction in Trailer on Flat Car loads |

| |

| • | Container turns increased 10.6% and dray efficiencies improved |

| |

| • | Intermodal margins were challenged by the West Coast port labor negotiations and related slowdown in freight volumes |

We are pleased with our team's ability to once again deliver positive operating results in the first quarter of 2015, as described in the highlights above. We are encouraged by these trends, specifically as they relate to revenue growth and profitability improvement within our Truckload and CRS segments. CRS first quarter profitability improved, both year over year and sequentially, as both the Adjusted Operating Ratio, as well as Operating Income reached their strongest levels since the acquisition. Consolidated Average Operational Truck Count increased in the first quarter of 2015, on both a year over year and sequential basis, with the majority of the sequential increase occurring within our largest and most profitable segment, Truckload. As we discussed last quarter, we are targeting 2015 enterprise-wide fleet growth of 700-1,100 tractors from the beginning to the end of 2015, 218 of which occurred in the first quarter. Improvements in both driver retention and recruiting have enabled this growth and were made possible by the ongoing effects of the various driver-friendly initiatives we implemented in 2014. In order to ensure continued progress on this front, we have announced plans to enact a material, targeted wage increase for drivers and pay increase for owner-operators on May 1st. This will have a short-term effect on the second quarter earnings, but we believe the investment in our drivers will yield returns over the long run through improved operational metrics. Safety trends continued to improve as our initiatives to reduce accident frequency and severity take hold. Year over year, improvements in insurance and claims expense as a percentage of Revenue xFSR allowed our Dedicated segment to offset driver pay increases while maintaining profitability.

The accumulation of these various positive trends leaves us comfortable in affirming our previously provided Adjusted EPS range for 2015 of $1.64 - $1.74.

First Quarter Results by Reportable Segment

Truckload Segment

Our Truckload segment consists of one-way movements over irregular routes throughout the United States, Mexico and Canada. This service uses both company and owner-operator tractors with dry van, flatbed and other specialized trailing equipment.

|

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 | | 2013 |

| | Unaudited |

Operating Revenue (1) | $ | 538.3 |

| | $ | 553.1 |

| | $ | 559.6 |

|

Revenue xFSR(1)(2)(3) | $ | 468.8 |

| | $ | 441.4 |

| | $ | 441.3 |

|

| | | | | | |

| Operating Ratio | 89.4 | % | | 94.2 | % | | 92.4 | % |

Adjusted Operating Ratio(3) | 87.9 | % | | 92.8 | % | | 90.4 | % |

| | | | | | |

| Weekly Revenue xFSR per Tractor | $ | 3,461 |

| | $ | 3,225 |

| | $ | 3,182 |

|

Total Loaded Miles(4) | 254,926 |

| | 254,426 |

| | 261,850 |

|

| | | | | | |

| Average Operational Truck Count | 10,535 |

| | 10,635 |

| | 10,785 |

|

| Deadhead Percentage | 11.8 | % | | 11.7 | % | | 11.2 | % |

| | | | | | |

1 In millions |

2 Revenue xFSR is operating revenue, excluding fuel surcharge revenue |

3 See GAAP to Non-GAAP reconciliation in the schedules following this letter |

4 Total Loaded Miles presented in thousands |

Our Truckload Revenue xFSR for the first quarter of 2015 increased $27.4 million, or 6.2%, over the same quarter in 2014. This revenue growth was the result of a 6.0% year over year increase in Revenue xFSR per loaded mile and a 1.1% increase in loaded miles per tractor per week, partially offset by the 0.9% decrease in Average Operational Truck Count. Our Revenue xFSR per loaded mile increase was driven primarily by contractual rate increases and freight mix. Although down slightly year over year, the first quarter Average Operational Truck Count increased 202 trucks when compared to the fourth quarter of 2014 which is in line with our expectations for our Truckload segment.

Our Adjusted Operating Ratio improved 490 basis points to 87.9% compared to 92.8% from the prior year. This improvement was driven by the increases in pricing and utilization discussed above, as well as a reduction in fuel expense reflecting a combination of declining diesel prices, better fuel efficiency, and reduced engine idle time; partially offset by increased driver wages and owner-operator pay. As discussed above, we have announced a driver pay increase for May 1st for the majority of the drivers in the Truckload segment. This increase is expected to negatively impact the Truckload operating ratio in second quarter, but as we continue to work with our customers for rate increases and seek to achieve other operational improvements with better driver retention, we believe the pay increase will yield returns longer term.

Dedicated Segment

Through our Dedicated segment, we devote equipment and offer tailored solutions under long-term contracts with customers. This dedicated business utilizes refrigerated, dry van, flatbed and other specialized trailing equipment.

Dedicated Revenue xFSR grew a notable 24.8% to $196.1 million in the first quarter of 2015 compared to the first quarter of 2014. This growth was driven by the various new contracts awarded over the last twelve months, which also drove the 23.6% increase in our Average Operational Truck Count year over year. Weekly Revenue xFSR per

Tractor increased 1.0% to $3,204 due to improved operational fundamentals, including pricing, utilization and deadhead for the respective contracts.

|

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 | | 2013 |

| | Unaudited |

Operating Revenue (1) | $ | 217.8 |

| | $ | 193.7 |

| | $ | 179.2 |

|

Revenue xFSR(1)(2)(3) | $ | 196.1 |

| | $ | 157.1 |

| | $ | 144.8 |

|

| | | | | | |

| Operating Ratio | 93.4 | % | | 94.0 | % | | 89.4 | % |

Adjusted Operating Ratio(3) | 92.7 | % | | 92.7 | % | | 86.9 | % |

| | | | | | |

| Weekly Revenue xFSR per Tractor | $ | 3,204 |

| | $ | 3,173 |

| | $ | 3,385 |

|

| Average Operational Truck Count | 4,761 |

| | 3,852 |

| | 3,327 |

|

| | | | | | |

1 In millions |

2 Revenue xFSR is operating revenue, excluding fuel surcharge revenue |

3 See GAAP to Non-GAAP reconciliation in the schedules following this letter |

For the first quarter of 2015 the Adjusted Operating Ratio in our Dedicated segment remained flat at 92.7%, compared to the first quarter of 2014. Several of the recently implemented safety initiatives have been effective, and have resulted in a reduction in our insurance and claims expense as a percentage of Revenue xFSR within the Dedicated segment. These safety improvements along with the truck count growth and Weekly Revenue xFSR per Tractor improvement discussed above, helped offset driver wage and owner-operator pay increases. With regard to fuel, many of our Dedicated contracts have unique fuel recovery characteristics, which drive more consistent net fuel expense compared to our over-the-road Truckload contracts. Therefore, the fuel benefit from declining fuel prices in Dedicated was limited.

CRS Segment

Our CRS segment represents shipments for customers that require temperature-controlled trailers. These shipments include one-way movements over irregular routes and dedicated truck operations.

CRS Revenue xFSR for the first quarter of 2015 decreased 3.0% to $81.1 million compared to $83.6 million for the same quarter in 2014, despite experiencing a 8.0% reduction in Average Operational Truck Count year over year. Weekly Revenue xFSR per Tractor increased 5.3% to $3,405, primarily due to a 6.4% improvement in loaded miles per tractor per week partially offset by a 0.9% reduction in Revenue xFSR per loaded mile.

As previously disclosed, a large CRS dedicated customer account was added in June of 2013 that had a much lower average length of haul, higher deadhead, and a much higher Revenue xFSR per loaded mile. Due to the unique requirements of this account and lack of attaining profitability targets, we made the decision to discontinue servicing this account effective January 31, 2015. Excluding the impact of this dedicated account, Revenue xFSR per loaded mile for the first quarter of 2015 increased 4.7% year over year. Further impact to these metrics is expected in the second quarter of 2015.

|

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 | | 2013 |

| | Unaudited |

Operating Revenue (1) | $ | 95.6 |

| | $ | 106.8 |

| | $ | 106.4 |

|

Revenue xFSR(1)(2)(3) | $ | 81.1 |

| | $ | 83.6 |

| | $ | 81.6 |

|

| | | | | | |

| Operating Ratio | 95.0 | % | | 97.7 | % | | 95.6 | % |

Adjusted Operating Ratio(3) | 94.1 | % | | 97.1 | % | | 94.2 | % |

| | | | | | |

| Weekly Revenue xFSR per Tractor | $ | 3,405 |

| | $ | 3,235 |

| | $ | 3,330 |

|

| Average Operational Truck Count | 1,852 |

| | 2,012 |

| | 1,905 |

|

| Deadhead Percentage | 14.0 | % | | 14.0 | % | | 12.1 | % |

| | | | | | |

1 In millions |

2 Revenue xFSR is operating revenue, excluding fuel surcharge revenue |

3 See GAAP to Non-GAAP reconciliation in the schedules following this letter |

The Adjusted Operating Ratio in our CRS segment improved 300 basis points to 94.1% in the first quarter of 2015 from 97.1% in the first quarter of 2014. This improvement was driven by increased loaded miles per tractor per week and lower fuel prices, partially offset by increased insurance and claims expense. Our driver-based initiatives and other structural changes discussed in recent quarters continue to gain momentum, as driver recruiting and retention continues to improve. In order to ensure continued progress on this front, similar to the Truckload segment, we have announced plans to enact a meaningful, targeted driver pay increase for drivers in our CRS segment on May 1st. This will have a short-term effect on the second quarter earnings for this segment, but we believe will yield returns over the long-run as we are able to attract and retain drivers, which will have a direct impact on our operational metrics.

Intermodal Segment

Our Intermodal segment includes revenue generated by freight moving over the rail in our containers and other trailing equipment, combined with revenue for drayage to transport loads between the railheads and customer locations.

Intermodal Revenue xFSR grew by 5.9% in the first quarter of 2015 compared to the same period in the prior year, driven by an 8.6% increase in Load Counts. Container on Flat Car (COFC) loads increased 16.1%, while Trailer on Flat Car (TOFC) loads decreased 59.0% primarily due to the elimination of the refrigerated TOFC business as discussed in 2014. Revenue xFSR per load decreased 2.5% in the first quarter of 2015 from the same period of 2014 due to the mix shift to COFC from TOFC and the slowdown of West Coast volumes resulting from the port labor disruptions. This caused a larger portion of our volume to occur in the east reducing our average length of haul and thus our average revenue per load.

Intermodal Adjusted Operating Ratio increased 30 basis points to 101.6% in the first quarter of 2015 compared to 101.3% during the same period last year. The West Coast port issues resulted in an increased usage of lower priced spot business off the West Coast in an effort to keep our container network balanced. Based upon the size of this impact relative to our fleet size, the port situation significantly impacted profitability, but was partially offset by a 10.6% improvement in container turns, as well as improvements in dray efficiencies and improved safety trends.

|

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 | | 2013 |

| | Unaudited |

Operating Revenue (1) | $ | 90.4 |

| | $ | 91.3 |

| | $ | 83.3 |

|

Revenue xFSR(1)(2)(3) | $ | 77.3 |

| | $ | 72.9 |

| | $ | 65.3 |

|

| | | | | | |

| Operating Ratio | 101.4 | % | | 101.0 | % | | 101.9 | % |

Adjusted Operating Ratio(3) | 101.6 | % | | 101.3 | % | | 102.5 | % |

| | | | | | |

| Load Counts | 41,940 | | 38,603 | | 35,639 |

| Average Container Counts | 9,150 | | 8,717 | | 8,717 |

| | | | | | |

1 In millions |

2 Revenue xFSR is operating revenue, excluding fuel surcharge revenue |

3 See GAAP to Non-GAAP reconciliation in the schedules following this letter |

Other Non-Reportable Segments

Our other non-reportable segments include our logistics and brokerage services, and our subsidiaries offering support services to customers and owner-operators, including shop maintenance, equipment leasing and insurance. Also captured here is the intangible asset amortization related to the 2007 going-private transaction.

In the first quarter of 2015, combined revenues from the aforementioned services, before eliminations, increased $16.0 million compared to the same period of 2014 due to 69.0% growth in our logistics business and increased services to owner-operators.

First Quarter Consolidated Operating Expenses

The table below highlights some of our cost categories for the first quarter of 2015, compared to the first quarter of 2014 and the fourth quarter of 2014, showing each as a percent of Revenue xFSR. Fuel surcharge revenue can be volatile and is primarily dependent upon the cost of fuel and not specifically related to our non-fuel operational expenses. Therefore, we believe that Revenue xFSR is a better measure for analyzing our expenses and operating metrics.

Salaries, wages and benefits increased $32.3 million to $261.7 million during the first quarter of 2015, compared to $229.4 million for the first quarter of 2014 due primarily to increases in total miles driven by company drivers within the period and driver pay rate increases.

First quarter 2015 operating supplies and expenses increased $13.4 million year over year due to increases in recruiting and training expenses, equipment maintenance expenses, and toll expenses.

As a percentage of Revenue xFSR, insurance and claims expense decreased to 5.0% in the first quarter of 2015 compared to 5.2% in the first quarter of 2014, but remained elevated due to higher frequency trends related to severe weather conditions in the first quarter of 2015. With the various safety campaigns and new technology we are implementing in 2015, we expect our experience to improve and our insurance and claims expense to taper as a percent of Revenue xFSR going forward.

|

| | | | | | | | | | | | | | | | | | | | |

| | | | | YOY | | | | | | QOQ |

| Q1'15 | | Q1'14 | | Variance1 | ($ in millions) | Q1'15 | | Q4'14 | | Variance1 |

| Unaudited | | Unaudited |

| $ | 1,015.1 |

| | $ | 1,008.4 |

| | 0.7 | % | Operating Revenue | $ | 1,015.1 |

| | $ | 1,139.5 |

| | -10.9 | % |

| $ | (120.3 | ) | | $ | (191.4 | ) | | -37.1 | % | Less: Fuel Surcharge Revenue | $ | (120.3 | ) | | $ | (179.3 | ) | | -32.9 | % |

| $ | 894.8 |

| | $ | 817.0 |

| | 9.5 | % | Revenue xFSR | $ | 894.8 |

| | $ | 960.2 |

| | -6.8 | % |

| | | | | | | | | | | |

| $ | 261.7 |

| | $ | 229.4 |

| | -14.1 | % | Salaries, Wages & Benefits | $ | 261.7 |

| | $ | 263.2 |

| | 0.6 | % |

| 29.2 | % | | 28.1 | % | | -110 bps |

| % of Revenue xFSR | 29.2 | % | | 27.4 | % | | -180 bps |

|

| | | | | | | | | | | |

| $ | 94.2 |

| | $ | 80.8 |

| | -16.6 | % | Operating Supplies & Expenses | $ | 94.2 |

| | $ | 88.7 |

| | -6.2 | % |

| 10.5 | % | | 9.9 | % | | -60 bps |

| % of Revenue xFSR | 10.5 | % | | 9.2 | % | | -130 bps |

|

| | | | | | | | | | | |

| $ | 44.3 |

| | $ | 42.4 |

| | -4.5 | % | Insurance & Claims | $ | 44.3 |

| | $ | 45.8 |

| | 3.3 | % |

| 5.0 | % | | 5.2 | % | | 20 bps |

| % of Revenue xFSR | 5.0 | % | | 4.8 | % | | -20 bps |

|

| | | | | | | | | | | |

| $ | 7.5 |

| | $ | 7.2 |

| | -4.2 | % | Communications & Utilities | $ | 7.5 |

| | $ | 7.7 |

| | 2.6 | % |

| 0.8 | % | | 0.9 | % | | 10 bps |

| % of Revenue xFSR | 0.8 | % | | 0.8 | % | | 0 bps |

|

| | | | | | | | | | | |

| $ | 17.6 |

| | $ | 18.3 |

| | 3.8 | % | Operating Taxes & Licenses | $ | 17.6 |

| | $ | 17.7 |

| | 0.6 | % |

| 2.0 | % | | 2.2 | % | | 20 bps |

| % of Revenue xFSR | 2.0 | % | | 1.8 | % | | -20 bps |

|

| | | | | | | | | | | |

1 Positive numbers represent favorable variances, negative numbers represent unfavorable variances |

Fuel Expense

|

| | | | | | | | | | | | | | |

| Q1'15 | | Q1'14 | ($ in millions) | Q1'15 | | Q4'14 |

| Unaudited | | Unaudited |

| $ | 106.9 |

| | $ | 156.0 |

| Fuel Expense | $ | 106.9 |

| | $ | 133.1 |

|

| 10.5 | % | | 15.5 | % | % of Operating Revenue | 10.5 | % | | 11.7 | % |

Fuel expense for the first quarter of 2015 was $106.9 million, representing a decrease of $49.1 million or 31.5% from the first quarter of 2014. The decrease was a result of lower fuel price, and improved fuel efficiency, partially offset by an increase in the number of miles driven by company drivers.

Purchased Transportation

Purchased transportation includes payments to owner-operators, railroads and other third parties we use for intermodal drayage and other brokered business.

Purchased transportation decreased $30.4 million year over year, primarily due to a reduction in fuel reimbursed to owner-operators and other third parties as a result of declining fuel price, and fewer miles driven by owner-operators. These reductions were partially offset by an increase in owner-operator contracted pay rates and growth in our logistics and intermodal businesses.

|

| | | | | | | | | | | | | | |

| Q1'15 | | Q1'14 | ($ in millions) | Q1'15 | | Q4'14 |

| Unaudited | | Unaudited |

| $ | 288.8 |

| | $ | 319.2 |

| Purchased Transportation | $ | 288.8 |

| | $ | 333.7 |

|

| 28.5 | % | | 31.6 | % | % of Operating Revenue | 28.5 | % | | 29.3 | % |

Sequentially, purchased transportation decreased $44.9 million primarily due to a reduction in fuel reimbursed to owner-operators and other third parties as a result of declining fuel price, lower seasonal freight volumes, and fewer miles driven by owner-operators.

Similar to the driver wage increase discussed above, we have announced plans to enact a meaningful, targeted owner-operator contracted pay rate increase on May 1st, which will have an impact on purchased transportation as a percent of Operating Revenue.

Rental Expense and Depreciation & Amortization of Property and Equipment

Due to fluctuations in the number of tractors leased versus owned, we combine our rental expense with depreciation and amortization of property and equipment for analytical purposes.

|

| | | | | | | | | | | | | | |

| Q1'15 | | Q1'14 | ($ in millions) | Q1'15 | | Q4'14 |

| Unaudited | | Unaudited |

| $ | 62.0 |

| | $ | 51.7 |

| Rental Expense | $ | 62.0 |

| | $ | 61.8 |

|

| 6.9 | % | | 6.3 | % | % of Revenue xFSR | 6.9 | % | | 6.4 | % |

| | | | | | | |

| $ | 56.9 |

| | $ | 56.2 |

| Depreciation & Amortization of Property and Equipment | $ | 56.9 |

| | $ | 55.8 |

|

| 6.4 | % | | 6.9 | % | % of Revenue xFSR | 6.4 | % | | 5.8 | % |

| | | | | | | |

| $ | 118.9 |

| | $ | 107.9 |

| Combined Rental Expense and Depreciation | $ | 118.9 |

| | $ | 117.6 |

|

| 13.3 | % | | 13.2 | % | % of Revenue xFSR | 13.3 | % | | 12.2 | % |

As noted in the table above, combined rental and depreciation expense in the first quarter of 2015 increased $11.0 million to $118.9 million from the first quarter of 2014. This increase is primarily due to an increase in the number of tractors and trailers in the fleet, higher equipment replacement costs, and an increase in the amount of leased equipment. Sequentially, combined rental and depreciation expense increased $1.3 million during the first quarter of 2015.

Gain on Disposal of Property and Equipment

The gain on disposal of property and equipment in the first quarter of 2015 was $3.9 million, compared to $3.2 million in the first quarter of 2014 and $4.6 million in the fourth quarter of 2014.

Income Taxes

The income tax provision in accordance with GAAP for the first quarter of 2015 was $23.7 million, resulting in an effective tax rate of 38.5%, which is in line with our expectations previously provided. In the first quarter of 2014, our income tax provision was $7.7 million, also resulting in an effective tax rate of 38.5%.

Interest Expense

Interest expense, comprised of debt interest expense, the amortization of deferred financing costs and original issue discount and excluding derivative interest expense on our interest rate swaps, decreased by $12.8 million in the first quarter of 2015 to $10.4 million, compared with $23.2 million for the first quarter of 2014. The decrease was largely due to the call of our remaining 10.0% Senior Secured 2nd Lien Notes in November 2014, lower debt balances, and our June 2014 amended and restated credit facility that contains more favorable interest rates and terms.

Debt Balances

|

| | | | | | | | | | | | | |

| | | December 31, 2014 | | | Q1 2015 | | March 31, 2015 |

| ($ in millions) | | | | | Changes | | |

| | | Unaudited |

| Unrestricted Cash | | $ | 105.1 |

| | | $ | (36.4 | ) | | $ | 68.7 |

|

| | | | | | | | |

| A/R Securitization ($375 mm) | | $ | 334.0 |

| | | $ | (40.0 | ) | | $ | 294.0 |

|

| Revolver ($450mm) | | $ | 57.0 |

| | | $ | (57.0 | ) | | $ | — |

|

| Term Loan A | | $ | 500.0 |

| | | $ | (5.6 | ) | | $ | 494.4 |

|

Term Loan B (a) | | $ | 397.0 |

| | | $ | (1.0 | ) | | $ | 396.0 |

|

| Capital Leases & Other Debt | | $ | 208.0 |

| | | $ | 1.8 |

| | $ | 209.8 |

|

| Total Debt | | $ | 1,496.0 |

| | | $ | (101.8 | ) | | $ | 1,394.2 |

|

| | | | | | | | |

| Net Debt | | $ | 1,390.9 |

| | | $ | (65.4 | ) | | $ | 1,325.5 |

|

| | | | | | | | |

| (a) Amounts presented represent face value |

* Data prior to Q3 2013 does not include Central Refrigerated

Our leverage ratio as of March 31, 2015 improved to 2.04 compared to 2.24 as of December 31, 2014. This improvement was primarily the result of year over year Adjusted EBITDA growth and delays in deliveries of new equipment versus expectations, which combined to help us achieve a $65.4 million reduction in Net Debt for the first quarter of 2015 compared to December 31, 2014. We expect that deliveries of new equipment will increase during the second and third quarters, the funding of which should reduce cash, increase the outstanding balances on our liquidity facilities and increase our outstanding lease liabilities. As a result, we expect our leverage ratio to increase modestly until the fourth quarter of 2015.

Cash Flow and Capital Expenditures

We continue to generate positive cash flows from operations. During the three months ending March 31, 2015, we generated $128.2 million of cash from operations compared with $76.2 million during the same period of 2014. Cash used in investing activities was $56.6 million, of which capital expenditures were $62.0 million, partially offset by proceeds from the sale of property and equipment of $13.4 million. Cash used in financing activities for the three months ending March 31, 2015 was $107.9 million, compared to $64.0 million for the same period in 2014, primarily driven by the voluntary repayments of our debt.

Capital expenditures in the second quarter are anticipated to be in the range of $70 - $80 million, offset by anticipated proceeds from sale of property and equipment of approximately $14 million, bringing total capital expenditures for the year in the range of $350 - $375 million and proceeds from the sale of property and equipment to approximately $45 million.

Summary

We are encouraged by the results our team was able to achieve during the first quarter, and are excited about the road ahead. We would like to thank all of our hard-working employees and our owner-operators, as well as our loyal customers and stockholders, for their continued support of Swift and our endeavor of "Delivering a Better LifeSM".

Conference Call Q&A Session

Swift Transportation's management team will host a Q&A session at 10:00 a.m. Eastern Time on Tuesday, April 28th to answer questions about the Company’s first quarter financial results. Please email your questions to Investor_Relations@swifttrans.com prior to 7:00 p.m. Eastern Time on Monday, April 27th.

Participants may access the call using the following dial-in numbers:

U.S./Canada: (800) 480-8614

International/Local: (706) 501-7951

Conference ID: 19522748

The live webcast, letter to stockholders, transcript of the Q&A, and the replay of the earnings Q&A session can be accessed via our investor relations website at investor.swifttrans.com.

IR Contact:

Jason Bates

Vice President of Finance &

Investor Relations Officer

623.907.7335

Forward Looking Statements

This letter contains statements that may constitute forward-looking statements, which are based on information currently available, usually identified by words such as "anticipates," "believes," "estimates", "plans,'' "projects," "expects," "hopes," "intends," "will," "could," "should," "may," or similar expressions which speak only as of the date the statement was made. Such forward-looking statements are made pursuant to the safe harbor provisions of the Private Securities Litigation Reform Act of 1995. Such statements include, but are not limited to, statements concerning:

| |

| • | trends and expectations relating to our operations, Revenue xFSR, expenses, other revenue, pricing, our effective tax rate, profitability and related metrics; |

| |

| • | our plans to enact driver wage and owner-operator pay increases and the anticipated impacts related thereto; |

| |

| • | expected changes in Net Debt and leverage in the remainder of 2015; |

| |

| • | projected Adjusted EPS for full year 2015, including components thereof; the timing and level of fleet size and equipment and container count; |

| |

| • | expected trends in insurance claims expense as a percentage of Revenue xFSR; |

| |

| • | levels and components of, and expected gains from the disposal of property and equipment in the remainder of 2015; and |

| |

| • | estimated capital expenditures for the remainder of 2015. |

Such forward-looking statements are inherently uncertain, and are based upon the current beliefs, assumptions and expectations of Company management and current market conditions, which are subject to significant risks and uncertainties as set forth in the Risk Factors section of our Annual Report on Form 10-K for the year ended December 31, 2014. As to the Company’s business and financial performance, the following factors, among others, could cause actual results to differ materially from those in forward-looking statements:

| |

| • | economic conditions, including future recessionary economic cycles and downturns in customers’ business cycles, particularly in market segments and industries in which we have a significant concentration of customers; |

| |

| • | increasing competition from trucking, rail, intermodal, and brokerage competitors; |

| |

| • | our ability to execute or integrate any future acquisitions successfully; |

| |

| • | increases in driver compensation to the extent not offset by increases in freight rates and difficulties in driver recruitment and retention; |

| |

| • | our ability to attract and maintain relationships with owner-operators; |

| |

| • | our ability to retain or replace key personnel; |

| |

| • | our dependence on third parties for intermodal and brokerage business; |

| |

| • | potential failure in computer or communications systems; |

| |

| • | seasonal factors such as harsh weather conditions that increase operating costs; |

| |

| • | the regulatory environment in which we operate, including existing regulations and changes in existing regulations, or violations by us of existing or future regulations; |

| |

| • | the possible re-classification of our owner-operators as employees; |

| |

| • | changes in rules or legislation by the National Labor Relations Board or Congress and/or union organizing efforts; |

| |

| • | our Compliance Safety Accountability safety rating; |

| |

| • | risks relating to our captive insurance companies; |

| |

| • | uncertainties and risks associated with our operations in Mexico; |

| |

| • | a significant reduction in, or termination of, our trucking services by a key customer; |

| |

| • | our significant ongoing capital requirements; |

| |

| • | the amount and velocity of changes in fuel prices and our ability to recover fuel prices through our fuel surcharge program; |

| |

| • | volatility in the price or availability of fuel; |

| |

| • | increases in new equipment prices or replacement costs; |

| |

| • | our level of indebtedness and our ability to service our outstanding indebtedness, including compliance with our indebtedness covenants, and the impact such indebtedness may have on the way we operate our business; |

| |

| • | restrictions contained in our debt agreements; |

| |

| • | adverse impacts of insuring risk through our captive insurance companies, including our need to provide restricted cash and similar collateral for anticipated losses; |

| |

| • | potential volatility or decrease in the amount of earnings as a result of our claims exposure through our captive insurance companies; |

| |

| • | the potential impact of the significant number of shares of our common stock that is outstanding; |

| |

| • | our intention to not pay dividends; |

| |

| • | conflicts of interest or potential litigation that may arise from other businesses owned by Jerry Moyes, including pledges of Swift stock and guarantees related to other businesses by Jerry Moyes; |

| |

| • | the significant amount of our stock and related control over the Company by Jerry Moyes; |

| |

| • | related-party transactions between the Company and Jerry Moyes; and |

| |

| • | that our acquisition of Central may be challenged by our stockholders. |

You should understand that many important factors, in addition to those listed above and in our filings with the SEC, could impact us financially. As a result of these and other factors, actual results may differ from those set forth in the forward-looking statements and the prices of the Company's securities may fluctuate dramatically. The Company makes no commitment, and disclaims any duty, to update or revise any forward-looking statements to reflect future events, new information or changes in these expectations.

Use of Non-GAAP Measures

In addition to our GAAP results, this Letter to Stockholders also includes certain non-GAAP financial measures, as defined by the SEC. The terms "Adjusted EBITDA," "Adjusted Operating Ratio," and "Adjusted EPS," as we define them, are not presented in accordance with GAAP. These financial measures supplement our GAAP results in evaluating certain aspects of our business. We believe that using these measures improves comparability in analyzing our performance because they remove the impact of items from our operating results that, in our opinion, do not reflect our core operating performance. Management and the board of directors focus on Adjusted EBITDA, Adjusted Operating Ratio and Adjusted EPS as key measures of our performance, all of which are reconciled to the most comparable GAAP financial measures and further discussed below. We believe our presentation of these non-GAAP financial measures is useful because it provides investors and securities analysts the same information that we use internally for purposes of assessing our core operating performance and compliance with debt covenants.

Adjusted EBITDA, Adjusted Operating Ratio and Adjusted EPS are not substitutes for their comparable GAAP financial measures, such as net income, cash flows from operating activities, operating margin, or other measures prescribed by GAAP. There are limitations to using non-GAAP financial measures. Although we believe that they improve comparability in analyzing our period to period performance, they could limit comparability to other companies in our industry if those companies define these measures differently. Because of these limitations, our non-GAAP financial measures should not be considered measures of income generated by our business or discretionary cash available to us to invest in the growth of our business. Management compensates for these limitations by primarily relying on GAAP results and using non-GAAP financial measures on a supplemental basis.

CONSOLIDATED INCOME STATEMENTS (UNAUDITED)

THREE MONTHS ENDED MARCH 31, 2015 AND 2014

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 |

| | (in thousands, except per share data) |

| Operating revenue: | | | |

| Revenue, excluding fuel surcharge revenue | $ | 894,864 |

| | $ | 816,999 |

|

| Fuel surcharge revenue | 120,280 |

| | 191,447 |

|

| Operating revenue | 1,015,144 |

| | 1,008,446 |

|

| Operating expenses: | | | |

| Salaries, wages and employee benefits | 261,654 |

| | 229,366 |

|

| Operating supplies and expenses | 94,204 |

| | 80,825 |

|

| Fuel | 106,907 |

| | 156,022 |

|

| Purchased transportation | 288,811 |

| | 319,169 |

|

| Rental expense | 61,975 |

| | 51,719 |

|

| Insurance and claims | 44,307 |

| | 42,448 |

|

| Depreciation and amortization of property and equipment | 56,927 |

| | 56,175 |

|

| Amortization of intangibles | 4,204 |

| | 4,204 |

|

| Gain on disposal of property and equipment | (3,932 | ) | | (3,159 | ) |

| Communication and utilities | 7,499 |

| | 7,170 |

|

| Operating taxes and licenses | 17,588 |

| | 18,337 |

|

| Total operating expenses | 940,144 |

| | 962,276 |

|

| Operating income | 75,000 |

| | 46,170 |

|

| Other expenses (income): | | | |

| Interest expense | 10,388 |

| | 23,225 |

|

| Derivative interest expense | 2,793 |

| | 1,653 |

|

| Interest income | (587 | ) | | (766 | ) |

| Loss on debt extinguishment | — |

| | 2,913 |

|

| Non-cash impairments of non-operating assets | 1,480 |

| | — |

|

| Other | (605 | ) | | (864 | ) |

| Total other expenses (income), net | 13,469 |

| | 26,161 |

|

| Income before income taxes | 61,531 |

| | 20,009 |

|

| Income tax expense | 23,691 |

| | 7,704 |

|

| Net income | $ | 37,840 |

| | $ | 12,305 |

|

| Basic earnings per share | $ | 0.27 |

| | $ | 0.09 |

|

| Diluted earnings per share | $ | 0.26 |

| | $ | 0.09 |

|

| Shares used in per share calculations: | | | |

| Basic | 142,199 |

| | 140,981 |

|

| Diluted | 143,955 |

| | 143,018 |

|

NON-GAAP RECONCILIATION:

ADJUSTED EPS (UNAUDITED) (1)

THREE MONTHS ENDED MARCH 31, 2015, 2014 AND 2013

|

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 | | 2013 |

| Diluted earnings per share | $ | 0.26 |

| | $ | 0.09 |

| | $ | 0.21 |

|

| Adjusted for: | | | | | |

| Income tax expense | 0.16 |

| | 0.05 |

| | 0.10 |

|

| Income before income taxes | 0.43 |

| | 0.14 |

| | 0.32 |

|

| Non-cash impairments of non-operating assets (2) | 0.01 |

| | — |

| | — |

|

| Loss on debt extinguishment (3) | — |

| | 0.02 |

| | 0.04 |

|

| Amortization of certain intangibles (4) | 0.03 |

| | 0.03 |

| | 0.03 |

|

| Adjusted income before income taxes | 0.46 |

| | 0.19 |

| | 0.38 |

|

| Provision for income tax expense at effective rate | 0.18 |

| | 0.07 |

| | 0.15 |

|

| Adjusted EPS | $ | 0.29 |

| | $ | 0.12 |

| | $ | 0.24 |

|

(1) Our definition of the non-GAAP measure, Adjusted EPS, starts with (a) income (loss) before income taxes, the most comparable GAAP measure. We add

the following items back to (a) to arrive at (b) adjusted income (loss) before income taxes:

| |

| (i) | amortization of the intangibles from our 2007 going-private transaction, |

| |

| (ii) | non-cash impairments, |

(iii) other special non-cash items,

| |

| (iv) | excludable transaction costs, |

| |

| (v) | mark-to-market adjustments on our interest rate swaps, recognized in the income statement, and |

| |

| (vi) | amortization of previous losses recorded in accumulated other comprehensive income (loss) (“AOCI”) related to the interest rate swaps we terminated upon our IPO and refinancing transactions in December 2010. |

We subtract income taxes, at the GAAP effective tax rate (except for 2013, when we used the GAAP expected effective tax rate), from (b) to arrive at (c) adjusted earnings. Adjusted EPS is equal to (c) divided by weighted average diluted shares outstanding. Since the numbers reflected in the above table are calculated on a per share basis, they may not foot due to rounding.

We believe that excluding the impact of derivatives provides for more transparency and comparability since these transactions have historically been volatile. Additionally, we believe that comparability of our performance is improved by excluding impairments that are unrelated to our core operations, as well as intangibles from the 2007 Transactions and other special items that are non-comparable in nature.

| |

| (2) | In September 2013, the Company agreed to advance up to $2.3 million, pursuant to an unsecured promissory note, to an independent contractor of a fleet that transported freight on Swift's behalf. In March 2015, management became aware that the independent contractor violated various covenants outlined in the unsecured promissory note, which created an event of default that made the principal and accrued interest immediately due and payable. As a result of this event of default, as well as an overall decline in the independent contractor's financial condition, management re-evaluated the fair value of the unsecured promissory note. As of March 31, 2015, management determined that the remaining balance due from the independent contractor to the Company was not collectible, which resulted in a $1.5 million pre-tax adjustment that was recorded in "Non-cash impairments of non-operating assets" in the Company's consolidated income statements. |

| |

| (3) | In March 2014, the Company used cash on hand to repurchase $23.8 million in principal of its Senior Secured Second Priority Notes, priced at 110.70%, in an open market transaction. Including principal, premium and accrued interest, the Company paid $27.1 million. The repurchase of the Senior Secured Second Priority Notes resulted in a loss on debt extinguishment of $2.9 million, representing the write-off of the unamortized original issue discount. |

In March 2013, the Company entered into a Second Amended and Restated Credit Agreement ("2013 Agreement"), which included a first lien Term Loan B-1 tranche and a first lien Term Loan B-2 tranche with face values of $250.0 million and $410.0 million, respectively. The 2013 Agreement replaced the then-existing term loan B-1 and B-2 tranches of the Amended and Restated Credit Agreement ("2012 Agreement"), which had outstanding principal balances at closing of $152.0 million and $508.0 million, respectively. The replacement of the 2012 Agreement resulted in a loss on debt extinguishment of $5.0 million, representing the write-off of the unamortized original issue discount and deferred financing fees associated with the original term loan.

| |

| (4) | For each period presented, amortization of certain intangibles reflects the non-cash amortization expense of $3.9 million, relating to certain intangible assets identified in the 2007 going-private transaction through which Swift Corporation acquired Swift Transportation Co. |

NON-GAAP RECONCILIATION:

ADJUSTED OPERATING INCOME AND OPERATING RATIO (UNAUDITED) (1)

THREE MONTHS ENDED MARCH 31, 2015, 2014 AND 2013

|

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 | | 2013 |

| | (dollar amounts in thousands) |

| Operating revenue | $ | 1,015,144 |

| | $ | 1,008,446 |

| | $ | 981,608 |

|

| Less: Fuel surcharge revenue | 120,280 |

| | 191,447 |

| | 197,057 |

|

| Revenue xFSR | 894,864 |

| | 816,999 |

| | 784,551 |

|

| Operating expense | 940,144 |

| | 962,276 |

| | 911,890 |

|

| Adjusted for: | | | | | |

| Fuel surcharge revenue | (120,280 | ) | | (191,447 | ) | | (197,057 | ) |

| Amortization of certain intangibles (2) | (3,912 | ) | | (3,912 | ) | | (3,912 | ) |

| Adjusted operating expense | 815,952 |

| | 766,917 |

| | 710,921 |

|

| Adjusted operating income | $ | 78,912 |

| | $ | 50,082 |

| | $ | 73,630 |

|

| Operating Ratio | 92.6 | % | | 95.4 | % | | 92.9 | % |

| Adjusted Operating Ratio | 91.2 | % | | 93.9 | % | | 90.6 | % |

| |

| (1) | Our definition of the non-GAAP measure, Adjusted Operating Ratio, starts with (a) operating expense and (b) operating revenue, which are GAAP financial measures. We subtract the following items from (a) to arrive at (c) adjusted operating expense: |

| |

| (i) | fuel surcharge revenue, |

| |

| (ii) | amortization of the intangibles from our 2007 going-private transaction, |

| |

| (iii) | non-cash operating impairment charges, |

| |

| (iv) | other special non-cash items, and |

| |

| (v) | excludable transaction costs. |

We then subtract fuel surcharge revenue from (b) to arrive at (d) Revenue xFSR. Adjusted Operating Ratio is equal to (c) adjusted operating expense as a percentage of (d) Revenue xFSR.

We net fuel surcharge revenue against fuel expense in the calculation of our Adjusted Operating Ratio, thereby excluding fuel surcharge revenue from operating revenue in the denominator. Because fuel surcharge revenue is so volatile, we believe excluding it provides for more transparency and comparability. Additionally, we believe that comparability of our performance is improved by excluding impairments, non-comparable intangibles from the 2007 Transactions and other special items.

| |

| (2) | Includes the items discussed in note (4) to the Non-GAAP Reconciliation: Adjusted EPS. |

NON-GAAP RECONCILIATION:

ADJUSTED EARNINGS BEFORE INTEREST, TAXES, DEPRECIATION

AND AMORTIZATION (UNAUDITED) (1)

THREE MONTHS ENDED MARCH 31, 2015, 2014 AND 2013

|

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 | | 2013 |

| | (in thousands) |

| Net income | $ | 37,840 |

| | $ | 12,305 |

| | $ | 30,292 |

|

| Adjusted for: | | | | | |

| Depreciation and amortization of property and equipment | 56,927 |

| | 56,175 |

| | 54,870 |

|

| Amortization of intangibles | 4,204 |

| | 4,204 |

| | 4,204 |

|

| Interest expense | 10,388 |

| | 23,225 |

| | 26,362 |

|

| Derivative interest expense | 2,793 |

| | 1,653 |

| | 562 |

|

| Interest income | (587 | ) | | (766 | ) | | (591 | ) |

| Income tax expense | 23,691 |

| | 7,704 |

| | 14,687 |

|

| Earnings before interest, taxes, depreciation and amortization (EBITDA) | $ | 135,256 |

| | $ | 104,500 |

| | $ | 130,386 |

|

| Non-cash equity compensation (2) | 1,483 |

| | 1,061 |

| | 605 |

|

| Loss on debt extinguishment (3) | — |

| | 2,913 |

| | 5,044 |

|

| Non-cash impairments of non-operating assets (4) | 1,480 |

| | — |

| | — |

|

| Adjusted earnings before interest, taxes, depreciation and amortization (Adjusted EBITDA) | $ | 138,219 |

| | $ | 108,474 |

| | $ | 136,035 |

|

| |

| (1) | Our definition of the non-GAAP measure, Adjusted EBITDA, starts with (a) net income (loss), the most comparable GAAP measure. We add the following items back to (a) to arrive at Adjusted EBITDA |

| |

| (i) | depreciation and amortization, |

| |

| (ii) | interest and derivative interest expense, including fees and charges associated with indebtedness, net of interest income, |

| |

| (iv) | non-cash equity compensation expense, |

| |

| (vi) | other special non-cash items, and |

| |

| (vii) | excludable transaction costs. |

We believe that Adjusted EBITDA is a relevant measure for estimating the cash generated by our operations that would be available to cover capital expenditures, taxes, interest and other investments and that it enhances an investor’s understanding of our financial performance. We use Adjusted EBITDA for business planning purposes and in measuring our performance relative to that of our competitors. Our method of computing Adjusted EBITDA is consistent with that used in our debt covenants, specifically our leverage ratio, and is also routinely reviewed by management for that purpose.

| |

| (2) | Represents recurring non-cash equity compensation expense, on a pre-tax basis. In accordance with the terms of our senior credit agreement, this expense is added back in the calculation of Adjusted EBITDA for covenant compliance purposes. |

| |

| (3) | Includes the items discussed in note (3) to the Non-GAAP Reconciliation: Adjusted EPS. |

| |

| (4) | Includes the item discussed in note (2) to the Non-GAAP Reconciliation: Adjusted EPS. |

FINANCIAL INFORMATION BY SEGMENT (UNAUDITED) (1)

THREE MONTHS ENDED MARCH 31, 2015, 2014 AND 2013

|

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 | | 2013 |

| | (dollar amounts in thousands) |

Operating Revenue: | | | | | |

| Truckload | $ | 538,341 |

| | $ | 553,057 |

| | $ | 559,595 |

|

| Dedicated | 217,775 |

| | 193,653 |

| | 179,226 |

|

| Central Refrigerated | 95,568 |

| | 106,763 |

| | 106,402 |

|

| Intermodal | 90,354 |

| | 91,313 |

| | 83,264 |

|

| Subtotal | 942,038 |

| | 944,786 |

| | 928,487 |

|

| Non-reportable segment (2) | 91,622 |

| | 75,666 |

| | 72,057 |

|

| Intersegment eliminations | (18,516 | ) | | (12,006 | ) | | (18,936 | ) |

| Consolidated operating revenue | $ | 1,015,144 |

| | $ | 1,008,446 |

| | $ | 981,608 |

|

| | | | | | |

Operating Income (Loss): | | | | | |

| Truckload | $ | 56,854 |

| | $ | 31,907 |

| | $ | 42,403 |

|

| Dedicated | 14,345 |

| | 11,530 |

| | 18,954 |

|

| Central Refrigerated | 4,799 |

| | 2,420 |

| | 4,721 |

|

| Intermodal | (1,243 | ) | | (926 | ) | | (1,604 | ) |

| Subtotal | 74,755 |

| | 44,931 |

| | 64,474 |

|

| Non-reportable segment (2) | 245 |

| | 1,239 |

| | 5,244 |

|

| Consolidated operating income | $ | 75,000 |

| | $ | 46,170 |

| | $ | 69,718 |

|

| | | | | | |

Operating Ratio: | | | | | |

| Truckload | 89.4 | % | | 94.2 | % | | 92.4 | % |

| Dedicated | 93.4 | % | | 94.0 | % | | 89.4 | % |

| Central Refrigerated | 95.0 | % | | 97.7 | % | | 95.6 | % |

| Intermodal | 101.4 | % | | 101.0 | % | | 101.9 | % |

| | | | | | |

| Adjusted Operating Ratio (3): | | | | | |

| Truckload | 87.9 | % | | 92.8 | % | | 90.4 | % |

| Dedicated | 92.7 | % | | 92.7 | % | | 86.9 | % |

| Central Refrigerated | 94.1 | % | | 97.1 | % | | 94.2 | % |

| Intermodal | 101.6 | % | | 101.3 | % | | 102.5 | % |

| |

| (1) | In the first quarter of 2014, the Company reorganized its reportable segments to reflect management’s revised reporting structure of its lines of business, following the acquisition of Central. In connection with the operational reorganization, the operations of Central's Trailer on Flat Car ("TOFC") business are reported within the Company's Intermodal segment. Additionally, the operations of Central's logistics business, third-party leasing, and other services provided to owner-operators are reported in the Company's other non-reportable segment. All prior period historical results related to the above noted segment reorganization have been retrospectively recast. |

| |

| (2) | The other non-reportable segment includes the Company's logistics and freight brokerage services, as well as support services provided by its subsidiaries to customers and owner-operators, including repair and maintenance shop services, equipment leasing, and insurance. Intangible asset amortization related to the 2007 Transaction is also included in this other non-reportable segment. |

| |

| (3) | For more details, refer to the Non-GAAP Reconciliation: Adjusted Operating Income and Operating Ratio by Segment. |

OPERATING STATISTICS BY SEGMENT (UNAUDITED) (1)

THREE MONTHS ENDED MARCH 31, 2015, 2014 AND 2013

|

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 | | 2013 |

| Truckload: | | | | | |

| Weekly revenue xFSR per tractor | $ | 3,461 |

| | $ | 3,225 |

| | $ | 3,182 |

|

| Total loaded miles (2) | 254,926 |

| | 254,426 |

| | 261,850 |

|

| Deadhead miles percentage | 11.8 | % | | 11.7 | % | | 11.2 | % |

| Average operational truck count: | | | | | |

| Company | 7,334 |

| | 7,151 |

| | 7,494 |

|

| Owner-Operator | 3,201 |

| | 3,484 |

| | 3,291 |

|

| Total | 10,535 |

| | 10,635 |

| | 10,785 |

|

| | | | | | |

| Dedicated: | | | | | |

| Weekly revenue xFSR per tractor | $ | 3,204 |

| | $ | 3,173 |

| | $ | 3,385 |

|

| Average operational truck count: | | | | | |

| Company | 3,882 |

| | 3,161 |

| | 2,684 |

|

| Owner-Operator | 879 |

| | 691 |

| | 643 |

|

| Total | 4,761 |

| | 3,852 |

| | 3,327 |

|

| | | | | | |

| Central Refrigerated: | | | | | |

| Weekly revenue xFSR per tractor | $ | 3,405 |

| | $ | 3,235 |

| | $ | 3,330 |

|

| Total loaded miles (2) | 41,880 |

| | 42,757 |

| | 47,100 |

|

| Deadhead miles percentage | 14.0 | % | | 14.0 | % | | 12.1 | % |

| Average operational truck count: | | | | | |

| Company | 1,263 |

| | 1,057 |

| | 998 |

|

| Owner-Operator | 589 |

| | 955 |

| | 907 |

|

| Total | 1,852 |

| | 2,012 |

| | 1,905 |

|

| | | | | | |

| Intermodal: | | | | | |

| Average operational truck count: | | | | | |

| Company | 481 |

| | 378 |

| | 295 |

|

| Owner-Operator | 87 |

| | 73 |

| | 18 |

|

| Total | 568 |

| | 451 |

| | 313 |

|

| Load Count | 41,940 |

| | 38,603 |

| | 35,639 |

|

| Average Container Count | 9,150 |

| | 8,717 |

| | 8,717 |

|

| |

| (1) | See note (1) to the Financial Information by Segment schedule, regarding the operational reorganization in the first quarter of 2014. |

| |

| (2) | Total loaded miles presented in thousands. |

CONSOLIDATED TOTAL EQUIPMENT (UNAUDITED)

AS OF MARCH 31, 2015, DECEMBER 31, 2014 AND MARCH 31, 2014

|

| | | | | | | | |

| | As of |

| | March 31, 2015 | | December 31, 2014 | | March 31, 2014 |

| Tractors: | | | | | |

| Company: | | | | | |

| Owned | 6,476 |

| | 6,083 |

| | 6,464 |

|

| Leased – capital leases | 1,655 |

| | 1,700 |

| | 1,791 |

|

| Leased – operating leases | 6,549 |

| | 6,099 |

| | 5,017 |

|

| Total company tractors | 14,680 |

| | 13,882 |

| | 13,272 |

|

| Owner-operator: | | | | | |

| Financed through the Company | 3,836 |

| | 4,204 |

| | 4,526 |

|

| Other | 1,019 |

| | 750 |

| | 572 |

|

| Total owner-operator tractors | 4,855 |

| | 4,954 |

| | 5,098 |

|

| Total tractors | 19,535 |

| | 18,836 |

| | 18,370 |

|

| Trailers | 61,780 |

| | 61,652 |

| | 58,074 |

|

| Containers | 9,150 |

| | 9,150 |

| | 8,717 |

|

NON-GAAP RECONCILIATION:

ADJUSTED OPERATING INCOME AND OPERATING RATIO

BY SEGMENT (UNAUDITED) (1)

THREE MONTHS ENDED MARCH 31, 2015, 2014 AND 2013

|

| | | | | | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 | | 2013 |

| | (in thousands) |

| Truckload: | | | | | |

| Operating revenue | $ | 538,341 |

| | $ | 553,057 |

| | $ | 559,595 |

|

| Less: Fuel surcharge revenue | 69,561 |

| | 111,648 |

| | 118,339 |

|

| Revenue xFSR | 468,780 |

| | 441,409 |

| | 441,256 |

|

| | | | | | |

| Operating expense | 481,487 |

| | 521,150 |

| | 517,192 |

|

| Adjusted for: Fuel surcharge revenue | (69,561 | ) | | (111,648 | ) | | (118,339 | ) |

| Adjusted operating expense | 411,926 |

| | 409,502 |

| | 398,853 |

|

| Adjusted operating income | $ | 56,854 |

| | $ | 31,907 |

| | $ | 42,403 |

|

| Adjusted Operating Ratio | 87.9 | % | | 92.8 | % | | 90.4 | % |

| Operating Ratio | 89.4 | % | | 94.2 | % | | 92.4 | % |

| | | | | | |

| Dedicated: | | | | | |

| Operating revenue | $ | 217,775 |

| | $ | 193,653 |

| | $ | 179,226 |

|

| Less: Fuel surcharge revenue | 21,642 |

| | 36,534 |

| | 34,433 |

|

| Revenue xFSR | 196,133 |

| | 157,119 |

| | 144,793 |

|

| | | | | | |

| Operating expense | 203,430 |

| | 182,123 |

| | 160,272 |

|

| Adjusted for: Fuel surcharge revenue | (21,642 | ) | | (36,534 | ) | | (34,433 | ) |

| Adjusted operating expense | 181,788 |

| | 145,589 |

| | 125,839 |

|

| Adjusted operating income | $ | 14,345 |

| | $ | 11,530 |

| | $ | 18,954 |

|

| Adjusted Operating Ratio | 92.7 | % | | 92.7 | % | | 86.9 | % |

| Operating Ratio | 93.4 | % | | 94.0 | % | | 89.4 | % |

| | | | | | |

| Central Refrigerated: | | | | | |

| Operating revenue | $ | 95,568 |

| | $ | 106,763 |

| | $ | 106,402 |

|

| Less: Fuel surcharge revenue | 14,468 |

| | 23,177 |

| | 24,850 |

|

| Revenue xFSR | 81,100 |

| | 83,586 |

| | 81,552 |

|

| | | | | | |

| Operating expense | 90,769 |

| | 104,343 |

| | 101,681 |

|

| Adjusted for: Fuel surcharge revenue | (14,468 | ) | | (23,177 | ) | | (24,850 | ) |

| Adjusted operating expense | 76,301 |

| | 81,166 |

| | 76,831 |

|

| Adjusted operating income | $ | 4,799 |

| | $ | 2,420 |

| | $ | 4,721 |

|

| Adjusted Operating Ratio | 94.1 | % | | 97.1 | % | | 94.2 | % |

| Operating Ratio | 95.0 | % | | 97.7 | % | | 95.6 | % |

| | | | | | |

| Intermodal: | | | | | |

| Operating revenue | $ | 90,354 |

| | $ | 91,313 |

| | $ | 83,264 |

|

| Less: Fuel surcharge revenue | 13,090 |

| | 18,364 |

| | 18,011 |

|

| Revenue xFSR | 77,264 |

| | 72,949 |

| | 65,253 |

|

| | | | | | |

| Operating expense | 91,597 |

| | 92,239 |

| | 84,868 |

|

| Adjusted for: Fuel surcharge revenue | (13,090 | ) | | (18,364 | ) | | (18,011 | ) |

| Adjusted operating expense | 78,507 |

| | 73,875 |

| | 66,857 |

|

| Adjusted operating loss | $ | (1,243 | ) | | $ | (926 | ) | | $ | (1,604 | ) |

| Adjusted Operating Ratio | 101.6 | % | | 101.3 | % | | 102.5 | % |

| Operating Ratio | 101.4 | % | | 101.0 | % | | 101.9 | % |

| |

| (1) | See note (1) to the Financial Information by Segment schedule, regarding the operational reorganization in the first quarter of 2014. |

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED)

AS OF MARCH 31, 2015 AND DECEMBER 31, 2014

|

| | | | | | | |

| | March 31, 2015 | | December 31, 2014 |

| | (in thousands) |

| ASSETS | | | |

| Current assets: | | | |

| Cash and cash equivalents | $ | 68,736 |

| | $ | 105,132 |

|

| Restricted cash | 61,692 |

| | 45,621 |

|

| Restricted investments, held to maturity, amortized cost | 18,286 |

| | 24,510 |

|

| Accounts receivable, net | 452,757 |

| | 478,999 |

|

| Equipment sales receivable | 689 |

| | 288 |

|

| Income tax refund receivable | 4,233 |

| | 18,455 |

|

| Inventories and supplies | 18,074 |

| | 18,992 |

|

| Assets held for sale | 3,438 |

| | 2,907 |

|

| Prepaid taxes, licenses, insurance and other | 48,874 |

| | 51,441 |

|

| Deferred income taxes | 35,276 |

| | 44,861 |

|

| Current portion of notes receivable | 8,730 |

| | 9,202 |

|

| Total current assets | 720,785 |

| | 800,408 |

|

| Property and equipment, at cost: | | | |

| Revenue and service equipment | 2,120,927 |

| | 2,061,835 |

|

| Land | 122,835 |

| | 122,835 |

|

| Facilities and improvements | 273,567 |

| | 268,025 |

|

| Furniture and office equipment | 68,927 |

| | 67,740 |

|

| Total property and equipment | 2,586,256 |

| | 2,520,435 |

|

| Less: accumulated depreciation and amortization | 1,017,060 |

| | 978,305 |

|

| Net property and equipment | 1,569,196 |

| | 1,542,130 |

|

| Other assets | 37,957 |

| | 41,855 |

|

| Intangible assets, net | 295,729 |

| | 299,933 |

|

| Goodwill | 253,256 |

| | 253,256 |

|

| Total assets | $ | 2,876,923 |

| | $ | 2,937,582 |

|

| LIABILITIES AND STOCKHOLDERS’ EQUITY | | | |

| Current liabilities: | | | |

| Accounts payable | $ | 162,226 |

| | $ | 160,186 |

|

| Accrued liabilities | 110,947 |

| | 100,329 |

|

| Current portion of claims accruals | 73,429 |

| | 81,251 |

|

| Current portion of long-term debt (1) | 32,581 |

| | 31,445 |

|

| Current portion of capital lease obligations | 45,891 |

| | 42,902 |

|

| Fair value of interest rate swaps | 4,233 |

| | 6,109 |

|

| Total current liabilities | 429,307 |

| | 422,222 |

|

| Revolving line of credit | — |

| | 57,000 |

|

| Long-term debt, less current portion (1) | 867,042 |

| | 871,615 |

|

| Capital lease obligations, less current portion | 153,786 |

| | 158,104 |

|

| Claims accruals, less current portion | 152,732 |

| | 143,693 |

|

| Deferred income taxes | 465,419 |

| | 480,640 |

|

| Securitization of accounts receivable | 294,000 |

| | 334,000 |

|

| Other liabilities | 32 |

| | 14 |

|

| Total liabilities | 2,362,318 |

| | 2,467,288 |

|

| Stockholders' equity: | | | |

| Preferred stock | — |

| | — |

|

| Class A common stock | 914 |

| | 911 |

|

| Class B common stock | 510 |

| | 510 |

|

| Additional paid-in capital | 786,455 |

| | 781,124 |

|

| Accumulated deficit | (272,177 | ) | | (310,017 | ) |

| Accumulated other comprehensive loss | (1,199 | ) | | (2,336 | ) |

| Noncontrolling interest | 102 |

| | 102 |

|

| Total stockholders' equity | 514,605 |

| | 470,294 |

|

| Total liabilities and stockholders' equity | $ | 2,876,923 |

| | $ | 2,937,582 |

|

Note to Condensed Consolidated Balance Sheets:

| |

| (1) | As of March 31, 2015, the Company's total long-term debt had a carrying value of $899.6 million, comprised of: |

•$494.4 million: Term Loan A, due June 2019

•$395.1 million: Term Loan B, due 2021, net of $0.9 million OID

•$10.1 million: Other

As of December 31, 2014, the Company's total long-term debt had a carrying value of $903.1 million, comprised of:

•$500.0 million: Term Loan A, due June 2019

•$396.1 million: Term Loan B, due 2021, net of $0.9 million OID

•$7.0 million: Other

CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

THREE MONTHS ENDED MARCH 31, 2015 AND 2014

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 |

| | (in thousands) |

| Cash flows from operating activities: | |

| Net income | $ | 37,840 |

| | $ | 12,305 |

|

| Adjustments to reconcile net income to net cash provided by operating activities: | | | |

| Depreciation and amortization of property, equipment and intangibles | 61,131 |

| | 60,379 |

|

| Amortization of debt issuance costs, original issue discount, and losses on terminated swaps | 2,606 |

| | 2,515 |

|

| Gain on disposal of property and equipment less write-off of totaled tractors | (3,698 | ) | | (2,958 | ) |

| Impairments | 1,480 |

| | — |

|

| Deferred income taxes | (6,346 | ) | | (7,942 | ) |

| Provision for losses on accounts receivable | 1,913 |

| | 792 |

|

| Non-cash loss on debt extinguishment and write-offs of deferred financing costs and original issue discount | — |

| | 2,913 |

|

| Non-cash equity compensation | 1,483 |

| | 1,061 |

|

| Excess tax benefits from stock-based compensation (1) | (1,172 | ) | | (1,078 | ) |

| Income effect of mark-to-market adjustment of interest rate swaps | (119 | ) | | (32 | ) |

| Increase (decrease) in cash resulting from changes in: | | | |

| Accounts receivable | 24,329 |

| | (37,064 | ) |

| Inventories and supplies | 918 |

| | 653 |

|

| Prepaid expenses and other current assets | 16,789 |

| | 18,446 |

|

| Other assets | 1,450 |

| | 2,871 |

|

| Accounts payable, accrued and other liabilities (1) | (10,447 | ) | | 23,296 |

|

| Net cash provided by operating activities | 128,157 |

| | 76,157 |

|

| Cash flows from investing activities: | | | |

| (Increase) decrease in restricted cash | (16,071 | ) | | 3,821 |

|

| Proceeds from maturities of investments | 14,190 |

| | 9,500 |

|

| Purchases of investments | (8,016 | ) | | (9,664 | ) |

| Proceeds from sale of property and equipment | 13,370 |

| | 28,428 |

|

| Capital expenditures | (62,006 | ) | | (60,058 | ) |

| Payments received on notes receivable | 2,065 |

| | 1,553 |

|

| Expenditures on assets held for sale | (2,313 | ) | | (1,521 | ) |

| Payments received on assets held for sale | 1,815 |

| | 2,269 |

|

| Payments received on equipment sale receivables | 352 |

| | 469 |

|

| Net cash used in investing activities | (56,614 | ) | | (25,203 | ) |

| Cash flows from financing activities: | | | |

| Repayment of long-term debt and capital leases | (19,294 | ) | | (46,526 | ) |

| Proceeds from long-term debt | 4,504 |

| | — |

|

| Net repayments on revolving line of credit | (57,000 | ) | | (17,000 | ) |

| Borrowings under accounts receivable securitization | 10,000 |

| | — |

|

| Repayment of accounts receivable securitization | (50,000 | ) | | (5,000 | ) |

| Proceeds from common stock issued | 2,679 |

| | 3,414 |

|

| Excess tax benefits from stock-based compensation | 1,172 |

| | 1,078 |

|

| Net cash used in financing activities | (107,939 | ) | | (64,034 | ) |

| Net decrease in cash and cash equivalents | (36,396 | ) | | (13,080 | ) |

| Cash and cash equivalents at beginning of period | 105,132 |

| | 59,178 |

|

| Cash and cash equivalents at end of period | $ | 68,736 |

| | $ | 46,098 |

|

Note to Consolidated Statements of Cash Flows:

| |

| (1) | Beginning in 2015, we separately present excess tax benefits from stock-based compensation within "Net cash provided by operating activities." The prior period presentation has been retrospectively adjusted to reclassify the amount out of "Accounts payable, accrued and other liabilities" and into the new line item "Excess tax benefits from stock-based compensation." The change in presentation has no net impact on “Net cash provided by operating activities.” |

CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED) — CONTINUED

|

| | | | | | | |

| | Three Months Ended March 31, |

| | 2015 | | 2014 |

| | (in thousands) |

| Supplemental disclosures of cash flow information: | | | |

| Cash paid during the period for: | | | |

| Interest | $ | 13,912 |

| | $ | 11,854 |

|

| Income taxes | 1,507 |

| | 3,463 |

|

| Non-cash investing activities: | | | |

| Equipment purchase accrual | $ | 59,814 |

| | $ | 59,867 |

|

| Notes receivable from sale of assets | 1,298 |

| | 2,762 |

|

| Equipment sales receivables | 753 |

| | 7,376 |

|

| Non-cash financing activities: | | | |

| Capital lease additions | $ | 9,988 |

| | $ | — |

|