[Letterhead of Ambow Education Holding Ltd.]

January 31, 2013

Larry Spirgel

Dean Suehiro

Robert Littlepage

Jessica Plowgian

Division of Corporate Finance

Securities and Exchange Commission

100 F Street, NE

Washington, DC 20549-7010

Re: Ambow Education Holding Ltd.

Form 20-F for Fiscal Year Ended December 31, 2011

Filed May 29, 2012

Comment Letter Dated December 21, 2012

File No. 001-34824

Dear Mr. Spirgel, Mr. Suehiro, Mr. Littlepage and Ms. Plowgian:

I refer to your letter to Ms. Jin Huang, dated December 21, 2012, relating to Ambow Education Holding Ltd.’s (“Ambow” or the “Company”) annual report on Form 20-F for the fiscal year ended December 31, 2011, filed with the U.S. Securities and Exchange Commission (the “Commission”) on May 29, 2012 (the “2011 20-F”).

Set forth below are the Company’s responses to the comments contained in the letter dated December 21, 2012 from the staff of the Commission (the “Staff”) (the numbered paragraphs below correspond to the paragraphs of the Staff’s comment letter, which have been retyped below in bold for your ease of reference).

Form 20-F for Fiscal Year Ended December 31, 2011

General

1. Please clarify how many schools and tutoring centers you operate. On pages 21 and 39 you disclose that you have a total of 33 schools (of which three are registered as schools not requiring reasonable returns), while all others are registered as requiring reasonable returns. However, on pages 30 and 39 (and elsewhere) we note your disclosure that as of December 31, you had 150 tutoring centers, five K-12 schools, 25 career enhancement centers, two career enhancement campuses and one college. Please clarify.

The Company respectfully advises the Staff that, under relevant PRC laws, an entity engaged in private education business can be registered either as a private school or as an enterprise (in most cases a tutoring company), provided that those private educational institutions which grant diplomas shall be registered as private schools.

Furthermore, a private school or a tutoring company may have multiple learning centers in one or more cities. For example, Jilin Ambow Clever Training School, a private school established in Jilin province, has 12 tutoring centers in total. On the contrary, two schools, namely Beijing Outbound Training School and Shandong Outbound Training School, do not have any learning centers.

We have two business divisions, “Better Schools” and “Better Jobs,” and four operating segments, i.e. tutoring, K-12 school, career enhancement (including career enhancement centers and career enhancement campuses) and college. The tutoring and K-12 schools segments are within our Better Schools division and the career enhancement and college segments are within our Better Jobs division.

As of December 31, 2011, the Company had across its four operating segments a total of 33 private schools and eight companies conducting private education businesses, comprising of 150 tutoring centers, five K-12 schools, 25 career enhancement centers, two career enhancement campuses and one college.

Of the 33 schools three schools that we continue to own were registered as schools not requiring reasonable returns. In addition, 21st Century School, for which we hold a 15-year operating right, was also registered as a school not requiring reasonable returns. The other 29 schools were registered as schools requiring reasonable returns.

The Company respectfully advises the Staff that its disclosure in the 2011 20-F did not include 21st Century School in the list of schools not requiring reasonable returns and it will correct this omission in our next filing.

Please see below the details of all the learning centers:

Better Jobs

(1) College Segment

Name |

| Nature |

| Number of |

|

Applied Technology College |

| School-1 |

| 1 |

|

Total |

|

|

| 1 |

|

(2) Career Enhancement Segment

Name |

| Nature |

| Number of |

|

Beijing Away Career Enhancement |

| Company-1 |

| 2 career enhancement centers |

|

Beijing IT Career Enhancement |

| Company-2 |

| 2 career enhancement |

|

|

|

|

| centers |

|

Changsha Career Enhancement |

| Company-3 |

| 2 career enhancement centers |

|

Dalian Career Enhancement |

| School-2 |

| 1 career enhancement center |

|

Dalian High Tech Zone Ambow Hope Training School |

| School-3 |

| 1 career enhancement center |

|

Guangzhou ZS Career Enhancement |

| School-4 |

| 1 career enhancement center |

|

Hebei YL Career Enhancement |

| School-5 |

| 1 career enhancement center |

|

Jinan WR Career Enhancement |

| School-6 |

| 1 career enhancement center |

|

Shanghai Hero Further Education Institute |

| School-7 |

| 11 career enhancement centers |

|

Suzhou Career Enhancement |

| School-8 |

| 1 career enhancement center |

|

Chongqing XT Career Enhancement (Chongqing Shapingba Training School and Chongqing Yuzhong Training School) |

| School-9&10 |

| 2 career enhancement centers |

|

Ambow(Dalian) Education and Technology Co., Ltd. |

| Company-4 |

| 1 career enhancement campus |

|

Ambow Kunshan |

| Company-5 |

| 1 career enhancement campus |

|

Total |

|

|

| 27 |

|

Better Schools

(1) K-12 School Segment

Name |

| Nature |

| Number of |

|

Beijing 21st Century International School |

| School-11 |

| 1 |

|

Changsha K-12 Experimental School &Changsha Kindergarten |

| School-12&13 |

| 1 |

|

Shenyang K-12 school |

| School-14 |

| 1 |

|

Shuyang K-12 School |

| School-15 |

| 1 |

|

Zhenjiang Ambow International School |

| School-16 |

| 1 |

|

Total |

|

|

| 5 |

|

(2) Tutoring Segment

Name |

| Nature |

| Number of |

|

Beijing JY Tutoring |

| Company-6 |

| 73 |

|

Beijing XGX Tutoring (Beijing Haidian XGX Training School and Beijing Huairou XGX Training School) |

| School-17&18 |

| 4 |

|

Changsha Tutoring |

| School-19 |

| 6 |

|

Jilin Tutoring |

| School-20 |

| 12 |

|

Shenyang Hanwen Educational Training School |

| School-21 |

| 2 |

|

Shuyang Tutoring |

| School-22 |

| 1 |

|

Tianjin Tutoring&Tianjin Ambow Huaying School |

| School-23&24 |

| 14 |

|

Zhenjiang Ambow Education Training Center |

| School-25 |

| 3 |

|

Zhengzhou Tutoring |

| School-26 |

| 1 |

|

Beijing YZ Tutoring |

| School-27 |

| 6 |

|

Beijing Century Tutoring |

| Company-7 |

| 5 |

|

Beijing JT Tutoring |

| Company-8 |

| 10 |

|

Beijing Aijia Kids English Training School |

| School-28 |

| 1 |

|

Lanzhou Anning Ambow English Training School |

| School-29 |

| 1 |

|

Guangzhou DP Tutoring |

| School-30 |

| 10 |

|

Beijing Haidian SIWA Twenty-one Century Education Training Center |

| School-31 |

| 1 |

|

Total |

|

|

| 150 |

|

*Beijing Outbound Training School and Shandong Outbound Training School, two other schools, which do not have any learning centers, are not illustrated in the table above. They are mainly providing outbound in-house management trainings tailored for employees and management teams.

2. We note that you adopted the VIE structure due to the restrictions on direct foreign ownership of elementary and middle schools for students and businesses that provide content over the internet, as discussed on pages 16 and 46. However, you state on page 39 that direct foreign investment is permitted for your tutoring services, therefore please revise your disclosure to clarify why you use the VIE structure for businesses that appear to be permitted for foreign investment.

In response to the Staff’s comment, the Company will in future filings include the following disclosure under “Item 3. Key Information — D. Risk Factors — Risks Related to Regulation of Our Business and Our Corporate Structure —All aspects of our business are subject to extensive regulation in China, we may not be in full compliance with these regulations and our ability to conduct business is highly dependent on our compliance with this regulatory framework. If the PRC government finds that the agreements that establish the structure for operating our business do not comply with applicable PRC laws and regulations, we could be subject to severe penalties” and “Item 4.B Information on the Company—Business Overview—

Regulations—Foreign investment in education service industry” (changes made to existing disclosure are underlined and in bold for your ease of reference):

“Currently, PRC laws and regulations do not explicitly impose restrictions on foreign investment in the tutoring service sector in China. However, some local government authorities in the PRC have adopted different approaches in granting licenses and permits (particularly, imposing more stringent restrictions on foreign-invested entities) for entities providing tutoring services.”

“We conduct our K-12 school and tutoring business and provide online services in China primarily through contractual arrangements between Ambow Online, our principal operating subsidiary in China, and our VIEs, and their respective shareholders.”

“According to the Foreign Investment Industries Guidance Catalog, or Foreign Investment Catalog, which was amended and promulgated by the National Development and Reform Commission, or NDRC, and the MOFCOM on December 24, 2011 and became effective on January 30, 2012, foreign investment is encouraged to participate in higher education and vocational training services. The foreign investment in higher education has to take the form of a Sino-foreign equity or cooperative joint venture. Senior high school education in grades 10-12 is a restricted industry. The foreign investment in senior high school education has to take the form of a cooperative joint venture. Foreign investment is banned from compulsory education, which means grades 1-9. Foreign investment is allowed to invest in after-school tutoring services which do not grant diplomas. However, many local government authorities in the PRC have adopted different approaches in granting licenses and permits (particularly, imposing more stringent restrictions on foreign-invested entities) for entities providing tutoring services. As of December 31, 2011, we had a total of 183 centers and schools, comprised of 150 tutoring centers, five K-12 schools, 25 career enhancement centers, two career enhancement campuses and one college. We conduct our education business in China primarily through contractual arrangements among our subsidiaries in China and VIEs. Our VIEs and their respective subsidiaries, as PRC domestic entities, hold the requisite licenses and permits necessary to conduct our education business in China and operate our tutoring centers, K-12 schools, career enhancement centers and colleges.”

Risk Factors

3. Please revise your Risk Factors section to include a separate risk factor discussing the potentially limited access by investors and other market participants to corporate records filed with PRC government entities such as SAIC. Include in your discussion what steps must be taken by individuals to gain access to these records, for example, seeking permission from you for SAIC to grant access to this information including, but not limited to, financial reports, shareholder changes and assets transfers.

In response to the Staff’s comment, the Company will include the following risk factor in future filings:

“Public shareholders of China-based, U.S.-listed companies and other market participants may have limited or no access to a wide array of corporate records of such listed companies’ PRC entities filed with industry and commerce administration authorities in China. The inability to access such information may adversely affect overall investor confidence in such companies’ reported results or other disclosures, including those of our Company, and may cause the trading price of our ADSs to decline

All of our PRC corporate entities, including Ambow Online, our VIEs and their subsidiaries, maintain corporate records and filings with industry and commerce administration authorities where such PRC entities are registered. Information contained in such corporate records and filings includes, among others, business address, registered capital, business scope, articles of association, equity interest holders, legal representative, changes to the above information, annual financial reports, matters relating to termination or dissolution, information relating to penalties imposed, and annual inspection records.

There have been regulations promulgated by various government authorities in PRC that govern the public access to corporate records and filings. Pursuant to the Company Law and Regulations of the People’s Republic of China on the Registration Administration of Companies, the company registration authority shall record the registered items of companies in a company recording book for the consultation and reproduction purposes of the public. The general public may apply to the company registration authority for inspection of the registered items of companies. Under the Measures for Accessing Corporate Records and Filings promulgated on December 16, 1996 by the SAIC, or the SAIC Measures, a wide range of basic corporate records, except for such restricted information as business results and financial reports, can be inspected by the public without restrictions. Under these SAIC Measures, a company’s restricted information can only be inspected by authorized government officers and officials from judicial authorities or lawyers involved in pending litigation relating to such company and with court-issued proof of such litigation. In practice, local industry and commerce administration authorities in different cities have adopted various regional regulations which impose more stringent restrictions than the SAIC Measures by expanding the scope of restricted information that the public cannot freely access. Many local industry and commerce administration authorities only allow unrestricted public access to such basic corporate information as name, legal representative, registered capital and business scope of a company. Under these local regulations, access to the other corporate records and filings (many of which are not restricted information under the SAIC Measures) is only granted to authorized government officers and officials from judicial authorities or lawyers involved in pending litigation relating to such company and with court-issued proof of such litigation.

However, neither the SAIC nor the local industry and commerce administration authorities have strictly implemented the restrictions under either the SAIC Measures or the various regional regulations before early 2012. As a result, before early 2012, the public were able to access all or most corporate records and filings of these listed companies’ PRC affiliates maintained with the industry and commerce administration authorities. Such records and filings were reported to have formed important components of research reports on certain China-based, U.S.-listed companies, which were claimed to have uncovered wrongdoings and fraud committed by these companies.

It was reported that, since the first half of 2012, local industry and commerce administration authorities in a number of cities had started strictly implementing the above restrictions and had significantly curtailed public access to corporate records and filings. There have also been reports that only the limited scope of basic corporate records and filings are still accessible by the public, and much of the previously publically accessible information, such as financial reports and changes to equity interests, now can only be accessed by the parties specified in, and in strict accordance with the restrictions under, the various regional regulations. Individuals other than the parties specified in the various regional regulations may get access to the corporate records and filings including, but not limited to, financial reports, shareholder changes and assets transfers with the permission of the PRC subject companies with reference letters issued by the companies. Such reported limitation on the public access to corporate records and filings and the resulting concerns over the loss of, or limit in, an otherwise available source of information to verify and evaluate the soundness of China-based U.S.-listed companies’ business operations in China may have a significant adverse effect on the overall investor confidence in such companies’ reported results or other disclosures, including those of our company, and may cause the trading price of our ADSs to decline.”

“Our VIEs and their respective subsidiaries..,” page 18

4. Please expand your disclosure to indicate the portion of your schools that elect to require reasonable returns.

In response to the Staff’s comment, the Company will include the following disclosure in future filings, as appropriate (changes made to existing disclosure are underlined and in bold for your ease of reference):

“As of December 31, 2011, we had across our four operating segments a total of 33 schools that were registered as private schools as opposed to companies. Of the 33 schools three schools that we continue to own were registered as schools not requiring reasonable returns. In addition 21st Century School, for which we hold a 15-year operating right, was also registered as a school not requiring reasonable returns. The other 29 schools were registered as schools requiring reasonable returns. The total net revenue of the schools requiring reasonable returns accounted for 31.2% of our consolidated total net revenue for the year ended December 31, 2011. The total net revenue of the schools not requiring reasonable returns accounted for 7.0% of our consolidated total net revenue for the year ended December 31, 2011. These schools (those requiring reasonable

returns and those not requiring reasonable returns) reported a net loss position for the period ending December 31, 2011.”

“The regulation of Internet website operators in China…,” page 20

5. Please expand your disclosure to indicate which “competent authorities” your PRC counsel consulted with respect to the whether your activities exceed the scope of Ambow Shida’s ICP license. Please further expand this risk factor to address the risks associated with a finding that your activities have exceeded the scope of the license, including fines, your ability to conduct your business and note the portion of your business attributed to these activities.

In response to the Staff’s comment, the Company respectfully advises the Staff that the “competent authorities” refer to Beijing Municipal Commission of Education. The Company will include such disclosure in future filings, as appropriate.

In addition, the Company will in future filings include the following disclosure under “Item 3.D —Key Information—Risk Factors—Risks related to regulation of our business and our corporate structure—The regulation of Internet website operators in China is subject to interpretation, and our operation of online education programs could be harmed if we are deemed to have violated applicable laws and regulations” (changes made to existing disclosure are underlined and in bold for your ease of reference):

“In 2011, we generated net revenues from our tutoring and career enhancement segments of RMB 778.0 million (US$123.6 million) and RMB 505.2 million (US$80.3 million), respectively. Of these net revenues, 0.6% and 27.8% were related to providing educational materials online from our tutoring and career enhancement segments, respectively. If the provision of these online services is deemed to exceed the scope of Ambow Shida’s license, we may be required to cease providing these online materials, which would harm our net revenues and results of operations. As a foreign enterprise in China, Ambow Shida may also be deemed to have illegally leased its ICP license or provided facilities or other resources to foreign investors. If we are deemed to have violated applicable Chinese Internet regulations, we could be subject to severe penalties, including confiscation of illegal gains, fines ranging from three to five times the illegal gains, suspension of certain types of services provided or orders to shut down the relevant websites.”

“Governmental control of currency conversion may affect the value of your investment…,” page 29

6. Please revise your disclosure in this risk factor to reference any new rules, regulations and circulars, or restrictions by SAFE or other agencies of the PRC (including Circular 45 promulgated November 16, 2011 by SAFE), regarding Renminbi converted from foreign currency capital. Explain how these limitations may affect your ability to finance your PRC subsidiaries.

In response to the Staff’s comment, the Company will in future filings include the following disclosure under “Item 3.D —Key Information—Risk Factors—Risks related to doing business in China—PRC regulation of loans and direct investment by offshore holding companies to PRC entities may delay or prevent us from making loans or additional capital contributions to our PRC operating subsidiaries and affiliated entities, which could harm our liquidity and our ability to fund and expand our business”:

“In addition, SAFE promulgated a circular on November 19, 2010, or Circular 59, which requires the authenticity of settlement of net proceeds from offshore offerings to be closely examined and the net proceeds to be settled in the manner described in the offering documents. Furthermore, SAFE has issued an internal guideline to its local counterparts, referred to as Circular 45, in November 2011. Circular 45 has never been formally announced by SAFE to the public or posted on SAFE’s website. Based on the version of Circular 45 made publicly available by certain local governmental authorities on their websites, we understand that Circular 45 stipulates SAFE’s local counterparts to strengthen the control imposed by Circulars 142 and 59 over the conversion of a foreign-invested company’s capital contributed in foreign currency into RMB. Circular 45 stipulates that a foreign-invested company’s RMB funds, if converted from such company’s capital contributed in foreign currency, may not be used by such company to (i) extend loans (in the form of entrusted loans), (ii) repay borrowings between enterprises, or (iii) repay bank loans it has obtained and lent to third parties.”

Acquisitions and disposals, page 37

7. Please expand your disclosure here and throughout your filing to clarify how you disposed of four tutoring and career enhancement subdivisions and initiated the disposal of Beijing Century College and its schools. Tell us what consideration you received in return for the disposal of such assets. Please clarify how your disposal of four subdivisions assisted you in focusing on organic growth, greater capital efficiency and better asset turnover (as discussed on page 9). Explain whether any of these schools are the same as the school involved in your July 5, 2012 announcement regarding allegations of financial impropriety and wrongful conduct in connection with your acquisition of a training school in 2008.

In response to the Staff’s comment, the Company will include the following disclosure in future filings, as appropriate:

“In the fourth quarter of 2011, we sold to Beijing Tongshengle Investment Co., Ltd. four subdivisions, including three in the tutoring segment and one in the career enhancement segment, for a total consideration of RMB 35 million, which was due to be received by December 31, 2012. In December 2012 the Company received cash payment of RMB 21 million.”

“On December 30, 2011, we entered into a sale and purchase agreement to dispose of Beijing Century College and its 100% owned subsidiary Beijing Siwa Century Facility Management Co. (together “Beijing Century College Group”) and Beijing

21st Century International School (“21st School”) to Xihua Investment Group (“Xihua Group”). At the same time, the Company retained the right to operate the 21st School on behalf of Xihua Group for an additional 15 years, at which point the operating right will revert back to Xihua Group, unless Xihua Group should exercise its option to terminate the operating rights agreement at an earlier date. The total consideration for the disposal of Beijing Century College Group and 21st School of RMB 556 million included RMB 183 million receivable, in cash and shares, a waiver of liabilities of RMB 203 million, and the 15-year operating rights valued at RMB 170 million by an independent valuer.” The receivable made up of cash and shares was due by December 31, 2012.

We draw to the Staff’s attention that by December 31, 2012, the Company had received cash payment of RMB 21 million in respect of the Tongshengle transaction. In the matter of the remaining RMB 14 million, the Company has held discussion regarding the recoverability of this balance and is currently assessing the collectability of the remaining balance and the possible need for a provision for the outstanding balance. We respectfully advise the Staff that we will reassess the level of disclosure required in respect of this transaction when we have finalised our assessment prior to the filing of the 2012 20-F.

We also draw to the Staff’s attention that as of December 31, 2012, the Company had received cash of RMB49.9 million of the RMB183 million receivable in respect of the Xihua transaction. The Company is working with Xihua Group on the collection of the remaining amount owed as well as assessing whether there is a need for a provision for any part of the outstanding balance. We respectfully advise the Staff that we will reassesses the level of disclosure required in respect of this transaction when we have finalized our assessment prior to the filing of the 2012 20-F.

In addition, the Company respectfully advises the Staff that the Company believes these disposals assisted it in focusing on organic growth, greater capital efficiency and better asset turnover because: (i) as to the transaction with Xihua Group, Beijing Century College would not be able to meet the land requirement to continue to be registered as an independent college without significant cost and efforts. Not being registered as an independent college, could greatly restrict its future development. Furthermore, the Company anticipated that to continue to maintain and upgrade 21st School’s buildings it would need to invest a large amount of funds. For example, to incur costs to reinforce its school buildings to protect against earthquakes. These expenditures could adversely affect the Company’s future cash flows and results of operations, (ii) as to disposals of the four subdivisions, all four subdivisions’ market shares were shrinking or not growing in accordance with previous expectations due to intense local competition or certain changes in government policies such as more stringent restrictions on tutoring programs for Mathematical Olympiad at one of these subdivisions. As such, the Company is of the view that these disposals assisted it in consolidating its resources and focusing on the core businesses which in turn resulted in organic growth, greater capital efficiency and better asset turnover.

None of these schools is the same as the school involved in the Company’s July 5, 2012 announcement regarding allegations of financial impropriety and wrongful conduct in connection with the Company’s acquisition of a training school in 2008.

8. Please clarify why you “reverted the operating right” for a portion of the Zhenjiang Ambow International School back to its original owner. Please clarify how you did this. Please tell us whether this is the entity referenced in your July 5, 2012 announcement regarding allegations of financial impropriety and wrongful conduct in connection with your acquisition of a training school in 2008.

The Company respectfully advises the Staff that Zhenjiang International School and Zhenjiang Foreign Language School are public schools in nature, which were established by government funding. Zhenjiang Municipal Education Bureau authorized Zhenjiang Education Development Investment Center (“Investment Center”) to own and operate Zhenjiang International School and Zhenjiang Foreign Language School. As an educational reform measure, Zhenjiang International School and Zhenjiang Foreign Language School were permitted by local government to be operated by private institutions. On August 18, 2008, we concluded a cooperation agreement with Investment Center and both of these two schools, pursuant to which we, through Zhenjiang Ambow International School, a private school we established for this purpose, acquired the right to operate Zhenjiang International School and Zhenjiang Foreign Language School for RMB 50,000,000 for a period of 12 years, from September 2008 to August 2020. Throughout this period, we are entitled to obtain all the economic returns from the operation of these two schools. According to the provisions of the cooperation agreement, in the event that the publicly-funded privately-run nature of Zhenjiang International School or Zhenjiang Foreign Language School should change due to reasons attributable to local government and Investment Center is unable to perform its responsibilities under the cooperation agreement any more, the Investment Center may terminate the Company’s right to operate one or both of the schools provided that Investment Center returns a portion of the consideration paid by the Company for the right to run the schools based on the remaining period of the cooperation agreement.

According to an announcement jointly issued by Jiangsu Provincial Department of Education and Jiangsu Supervision Department on January 27, 2011, Zhenjiang Foreign Language School was to be re-registered as a publicly-funded publicly-run school. This meant that Zhenjiang Foreign Language School had to provide compulsory education to its new students free of charge starting from September 2011. Therefore, the Investment Center asked the Operating Right of Zhenjiang Foreign language School to be reverted back to the original owner. We agreed this with the Investment Center and withdrew from running Zhenjiang Foreign Language School in July 2011.

Zhenjiang Ambow International School is not the entity referenced in the Company’s July 5, 2012 announcement regarding allegations of financial impropriety and wrongful conduct in connection with the Company’s acquisition of a training school in 2008.

Regulation of independent colleges, page 39

9. Please expand your disclosure to address whether management anticipates being able to meet the land requirement applicable to Applied Technology College prior to March 31, 2013.

The Company respectfully advises the Staff that as of December 31, 2012, the land use right of a portion of the land on which Applied Technology College is operating is owned by Taishidian Holding, the holding company of Applied Technology College. Due to the pending technical deadline of March 31, 2013 for transferring the land use rights to Suzhou College, and the costs required to be incurred to process such transfer, the Company has been considering alternatives, including a) initiating discussions with the Ministry of Education requesting an exemption from the technical requirements; and b) outright sale of the Taishidian Holding company, including the underlying land and college. The Company is diligently working with a prospective Buyer to sell and transfer the interests before the March 31, 2013. As of the date of our response to the Staff, the Company has not initiated direct conversations with the Ministry of Education as to a possible exemption from the regulatory provisions.

Accordingly, management does not anticipate that they will meet the land requirement by March 31, 2013.

The 2012-20-F will be updated to reflect the actual results of the Company’s alternative actions before the filing is submitted.

Software copyright registration, page 41

10. We note your statement that you have been issued 67 registration certificates for computer software copyrights. Please clarify how many of these registrations you need for the operation of your business.

In response to the Staff’s comment, the Company respectfully advises the Staff that the Company is currently using 33 out of these 67 registrations for the operation of its business.

Regulations on internet information services, page 41

11. Please clarify whether you believe that your operations are currently in compliance with these regulations.

In response to the Staff’s comment, the Company respectfully advises the Staff that it believes that its operations are currently in compliance with the relevant regulations on Internet information services.

Organizational Structure, page 45

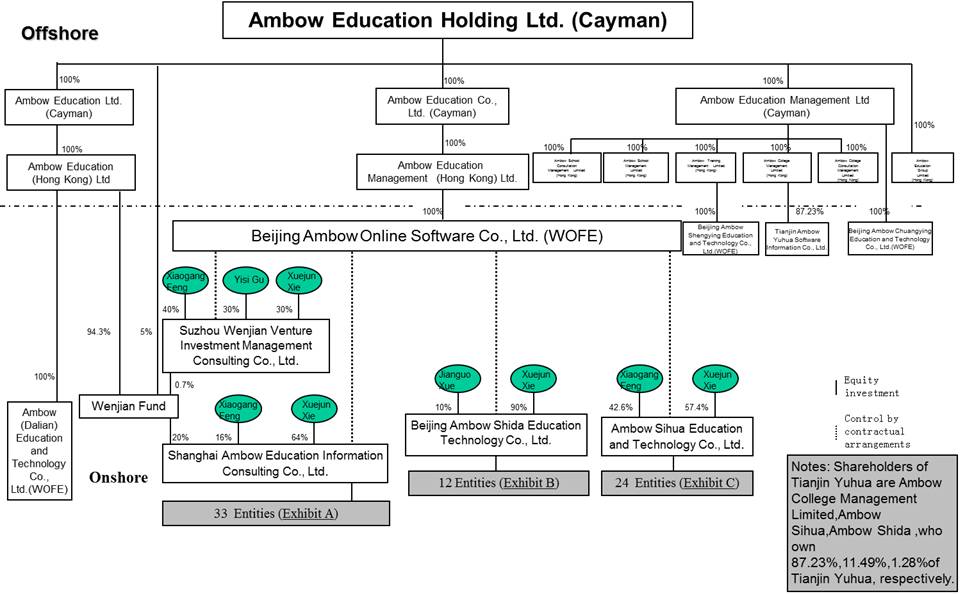

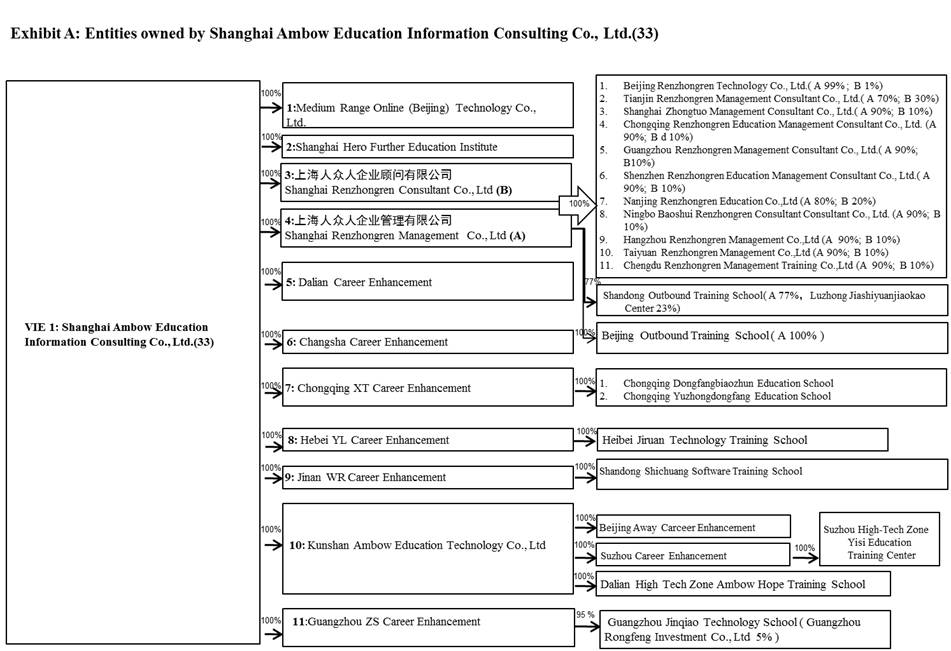

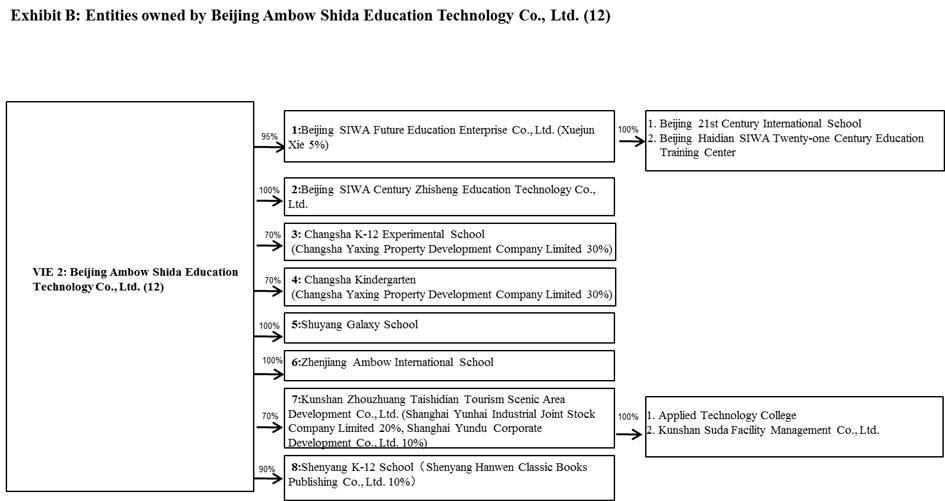

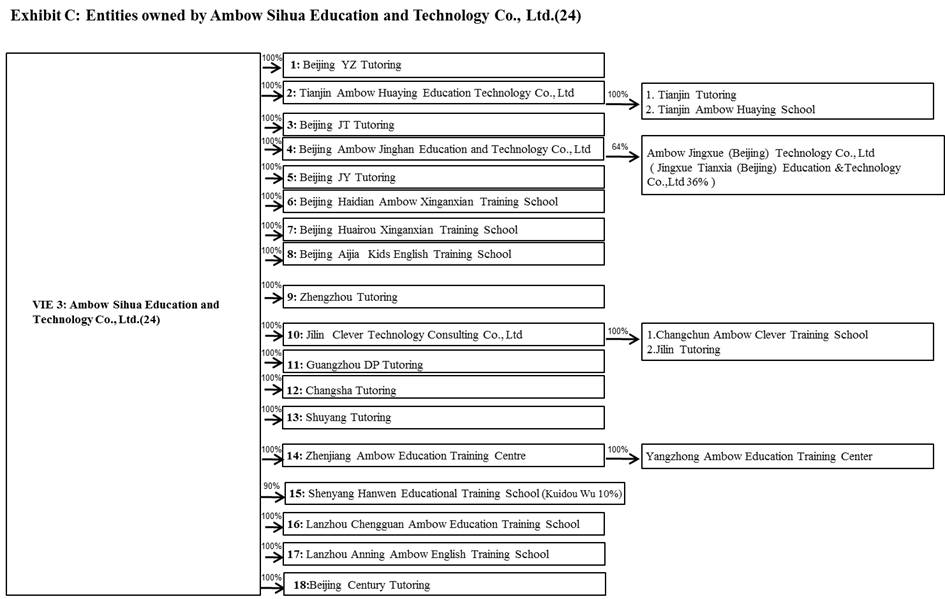

12. Please expand your organizational chart to include the entities owned by the VIEs and other parties. For example, we note your statement on page 48 that Ambow Shida owns 100% equity interest in two of your schools and 70% and 90% equity interest in two other schools.

In response to the Staff’s comment, the Company will include the organizational chart as Annex A attached hereto in future filings, as appropriate.

13. Please revise the last bullet point on page 46 to clarify that the voting power you reference is through a power of attorney.

In response to the Staff’s comment, the Company will include the following disclosure in future filings, as appropriate (changes made to existing disclosure are underlined and in bold for your ease of reference):

“Exercise effective control over our VIEs and their respective subsidiaries by having such VIEs’ shareholders pledge their respective equity interests in these VIEs to Ambow Online and, through powers of attorney, entrust all the rights to exercise their voting power over these VIEs to Ambow Online.”

Schools, page 48

14. Please disclose whether you currently pay any rent or other payments for the use of the land owned by Changsha Yaxing Property Development Company Limited.

In response to the Staff’s comment, the Company respectfully advises the Staff that pursuant to the Lease Agreement, dated August 11, 2009, entered into by and among Chang Yaxing Property Development Company Limited and Changsha Tongsheng Lake Property Development Co., Ltd., as lessors, Hunan Changsha Tongsheng Lake Experimental School and Hunan Changsha Tongsheng Lake Experimental Kindergarten, as lessees, and Beijing Shida Ambow Education Technology Co., Ltd., as guarantor, the land and premises rented by the lessees are free of charge for a period from October 1, 2009 to September 30, 2015. We draw to the Staff’s attention the following: for accounting purposes, we spread the total charges expected to arise from this lease evenly over the entire term of the lease.

In addition, the Company will include the following disclosure in future filings, as appropriate:

“The land and premises are leased to Changsha K-12 Experimental School and Changsha Kindergarten for 20 years, from October 1, 2009 to September 30, 2029, and free of charge for the first six years, i.e. from October 1, 2009 to September 30, 2015.”

Agreements that provide effective control over our VIEs, page 49

15. Please disclose, if true, that you have no agreements that pledge the assets of the VIEs for the benefit of the WFOE.

In response to the Staff’s comment, the Company will include the following disclosure in future filings, as appropriate:

“We have no agreements that pledge the assets of our VIEs for the benefit of Ambow Online.”

16. Please expand your disclosure in this section to include a more detailed summary of the agreements governing your relationship with your VIEs. Your disclosure should include, among other material terms, the term of each such agreement and the respective termination rights of the parties.

In response to the Staff’s comment, the Company will include the following disclosure in future filings, as appropriate (changes made to existing disclosure are underlined and in bold for your ease of reference):

“Agreements that provide effective control over Ambow Shida and its subsidiaries

We have entered into a series of agreements with Ambow Shida and its shareholders. These agreements provide us substantial ability to control Ambow Shida and its shareholders, and we have obtained an option to purchase all of the equity interests of Ambow Shida. These agreements include:

Share Pledge Agreement. Pursuant to the share pledge agreement, dated January 31, 2005, among Ambow Online, Xuejun Xie and Jianguo Xue, each a shareholder of Ambow Shida, as amended by the supplementary agreement dated January 4, 2009 entered into by and among AECL, Ambow Online, Xuejun Xie and Jianguo Xue, each of Xuejun Xie and Jianguo Xue pledged all of her or his equity interest in Ambow Shida to Ambow Online to secure the performance of Ambow Shida under an exclusive cooperation agreement, dated January 31, 2005, between Ambow Online and Ambow Shida as described below. If Ambow Shida fails to fulfil its obligations under the exclusive cooperation agreement, Ambow Online may dispose of the pledged equity in accordance with the provisions of the Security Law of the People’s Republic of China and relevant laws and regulations, and shall have the right to be indemnified for the secured debt and any other relevant expenses out of the proceeds from the disposal of the pledged equity. Each of Xuejun Xie and Jianguo Xue also agreed not to transfer, dispose of or otherwise directly or indirectly create any encumbrance over her or his equity interest in Ambow Shida, or take any actions that may reduce the value of her or his equity interest in Ambow Shida without the prior written consent of Ambow Online. This agreement shall remain in effect until the exclusive cooperation agreement is terminated lawfully and the secured debt is fully repaid pursuant to the terms and conditions under the exclusive cooperation agreement. Without Ambow Online’s prior consent, the pledgors shall not be entitled to grant or assign their rights and obligations under the agreement. Ambow Online may assign at any time all or any of its rights and obligations under the exclusive cooperation agreement and the assets transfer and lease agreement to any person (either a natural person or a legal person) it designates. In such case, the assignee shall assume Ambow Online’s rights and obligations under this agreement. In the event of any change of the pledgee as a result of transfer, the parties shall enter into a new pledge agreement. The parties shall negotiate in good faith to resolve any disputes arising out of or in connection with this agreement. If the parties cannot reach an agreement on the resolution of such disputes, either party shall submit such disputes to China International Economic and Trade Arbitration Commission for arbitration in accordance with its then-effective arbitration rules. The arbitration shall be conducted in Beijing, and the language used in arbitration shall be Chinese. The award of the arbitration shall be final and binding upon the parties.

Call Option Agreement. Pursuant to the call option agreement, dated January 31, 2005, among AECL, Xuejun Xie and Jianguo Xue, each a shareholder of Ambow Shida, as amended by the termination agreement dated April 26, 2007 and further amended by the supplementary agreement dated January 4, 2009 entered into by and among AECL, Ambow Online, Xuejun Xie and Jianguo Xue, AECL or its designee has an option to purchase from each of Xuejun Xie and Jianguo Xue, to the extent permitted under PRC laws, all or part of his or her equity interest in Ambow Shida in one or more installments at an aggregate purchase price of RMB3.0 million unless the applicable laws state otherwise. AECL or its designee shall have sole discretion to decide when to exercise the option, whether in part or in full. Without the written consent of AECL or its designee, Xuejun Xie and/or Jianguo Xue shall not approve or support any equity transfer or capital increase of Ambow Shida, or any resolution approving the capital increase, issuance of additional shares, dilution of the existing shareholdings, or affecting the right of AECL or its designee at any board or shareholders’ meetings, or execute or adopt any resolution approving the distribution of the stock dividends, stock awards or profits at any board or shareholders’ meetings. Xuejun Xie and Jianguo Xue agreed not to dispose of the equity interest or exercise any related rights in any form without AECL or its designee’s written consent. Xuejun Xie and Jianguo Xue agreed that before AECL or its designee exercises the option to obtain all the equity interest and assets, Xuejun Xie and Jianguo Xue shall not engage in and shall not cause Ambow Shida to engage in (i) selling, assigning, mortgaging or otherwise disposing of any assets, lawful income and business revenues of Ambow Shida, or creating security interest on Ambow Shida (other than those made in the ordinary course of business or have been disclosed to and approved by AECL or its designee in writing), (ii) entering into any transactions that may substantially affect Ambow Shida’s assets, liabilities, operations, equity and other legitimate interests (other than those made in the ordinary course of business or have been disclosed to and approved by AECL or its designee in writing), (iii) supplementing, altering or modifying Ambow Shida’s charter documents in any form, which will substantially affect Ambow Shida’s assets, liabilities, operations, equity and other legitimate interests (except the proportional capital increase as required by law), or (iv) appointing any other third party as Ambow Shida’s agent or representative. AECL or its designee may assign the option and any rights and interests under the agreement in its sole discretion. Currently, we do not expect to exercise such option in the foreseeable future. Should we decide to exercise such option, we or our designee would affect such purchase through the cancellation of loans owed to us by Xuejun Xie and/or Jianguo Xue unless the then applicable laws require the purchase price to be determined by a valuation or otherwise provided, in which case the transfer price shall be the minimum amount provided by applicable law and we will effect such purchase through, to the extent necessary, a combination of cash and cancellation of loans owed to us by each of Xuejun Xie and Jianguo Xue. This call option is not subject to any time limit and has been effective upon execution by the parties. This agreement shall not terminate until AECL or its designee exercises the call option and the equity interest has been fully vested in AECL or its designee or upon termination by AECL or its designee in writing. If any dispute arises out of the interpretation or performance of this agreement, the parties shall negotiate in good faith to resolve such dispute; if such dispute cannot be resolved within thirty days of the beginning of such negotiations, either party may submit such dispute to China International Economic and Trade Arbitration Commission in Beijing for arbitration in accordance with its then-effective arbitration rules.

Powers of Attorney. Pursuant to the powers of attorney, each dated April 26, 2007, each of Xuejun Xie and Jianguo Xue irrevocably entrusted all the rights to exercise her or his voting power of Ambow Shida to Ambow Online for an indefinite period of time, including without limitation, proposing to convene a shareholders’ meeting, attending a shareholders’ meeting and exercising the voting rights at a shareholders’ meeting.

Loan Agreements. Pursuant to the loan agreements, each dated January 31, 2005, among AECL, Xuejun Xie and Jianguo Xue, each a shareholder of Ambow Shida, respectively, amended by amendment agreements, dated April 26, 2007, among Ambow Online, AECL and Xuejun Xie and Jianguo Xue, respectively, and further amended by the supplementary agreement dated January 4, 2009 entered into by and among AECL, Ambow Online, Xuejun Xie and Jianguo Xue or renewed by a loan agreement between Ambow Online and Jianguo Xue dated February 1, 2008, as applicable, Ambow Online loaned RMB2.7 million and RMB0.3 million to Xuejun Xie and Jianguo Xue, respectively, to fund the registered capital requirements of Ambow Shida. To the extent permitted by PRC laws, each loan shall be deemed to have been repaid upon the transfer of the equity interest in Ambow Shida held by Xuejun Xie and Jianguo Xue, as applicable, to Ambow Online or its designee. These loan agreements shall remain in effect until the loans thereunder are fully repaid. To the extent permitted by the relevant PRC laws, Ambow Online shall determine at its sole discretion the timing and method of the repayment of the loans thereunder and notify the borrowers in writing of such arrangements seven days in advance. The borrowers shall not repay the loans to Ambow Online early unless Ambow Online notifies the borrowers in writing that the loan thereunder has expired or as otherwise provided therein. Any disputes arising in connection with the interpretation or execution of this agreement shall be resolved by the parties through friendly consultations; if such disputes cannot be resolved within thirty days of the beginning of the consultations, either party may submit such disputes to China International Economic and Trade Arbitration Commission in Beijing for arbitration in accordance with its then-effective arbitration rules.

Agreements that provide effective control over Ambow Shanghai and its subsidiaries

We have entered into a series of agreements with Ambow Shanghai and its shareholders. These agreements provide us substantial ability to control Ambow Shanghai and its shareholders, and we have obtained an exclusive option to purchase all of the equity interests of Ambow Shanghai. These agreements include:

Share Pledge Agreement. Pursuant to the share pledge agreement, dated October 31, 2009, and amended by a supplementary agreement dated January 4, 2010, among Ambow Online, Xuejun Xie and Xiaogang Feng, each a shareholder of Ambow Shanghai, each of Xuejun Xie and Xiaogang Feng pledged all of her or his equity interest in Ambow Shanghai to Ambow Online to secure the performance of Ambow Shanghai or its subsidiaries’ obligations under a technology service agreement between Ambow Online and Ambow Shanghai dated October 31, 2009 as described below. If Ambow Shanghai fails to fulfil its obligations under the technology service agreement, Ambow Online may dispose of the pledged equity in accordance with the provisions of the Security Law of the People’s Republic of China and relevant laws and regulations, and shall have the right to be indemnified for the secured debt and any other relevant expenses out of the proceeds from the disposal of the pledged equity. Without Ambow Online’s prior written consent, each of Xuejun Xie and Xiaogang Feng shall not (i) make a proposal to amend the articles of association of Ambow Shanghai or cause the making of such proposal, or increase or reduce Ambow Shanghai’s registered capital, or otherwise change the structure of its registered capital, (ii) create any further security, encumbrances and any third party’s rights on the pledged equity in addition to the pledge created under the share pledge agreement, (iii)perform any act that may prejudice any rights of Ambow Online under the share pledge agreement, or any act that may materially affect the assets, business and/or operations of Ambow Shanghai, (iv) distribute dividends to the shareholders in any form (however, upon Ambow Online’s request, pledgors shall immediately distribute all of their distributable profits to the shareholders), or (v) transfer or dispose of the pledged equity in any way. The share pledge agreements has been in effect since the date when the authorized representatives of the parties duly execute this agreement and shall remain in effect until the technology service agreement is terminated and the secured debt is fully repaid. The share pledge agreements may be unilaterally terminated by Ambow Online. Neither of Xuejun Xie and Xiaogang Feng is entitled to unilaterally terminate the share pledge agreements. Without Ambow Online’s prior written consent, pledgors shall not transfer any of their rights or obligations under the share pledge agreement to any other party. Ambow Online shall have the right to transfer to any third party any of its rights or obligations under the share pledge agreement and any of its rights or obligations under other agreements contemplated by the share pledge agreement without pledgor’s prior consent. If any dispute arises between the parties in connection with the interpretation and performance of the provisions thereunder, the parties shall resolve such dispute in good faith through discussions. If no agreement can be reached within sixty days after one party receives the notice of the other party requesting the beginning of discussions or as otherwise agreed, either party shall have the right to submit such dispute to China International Economic and Trade Arbitration Commission for arbitration in accordance with its then-effective rules. The arbitration shall be held in Beijing. The award of the arbitration shall be final and binding upon the parties.

Call Option Agreement. Pursuant to the call option agreement, dated October 31, 2009, and amended by a supplementary agreement dated January 4, 2010, among Ambow Online, Xuejun Xie and Xiaogang Feng, each a shareholder of Ambow Shanghai, each of Xuejun Xie and Xiaogang Feng irrevocably granted Ambow Online or its designee an exclusive option to purchase, to the extent permitted under PRC laws, all or part of her or his equity interest in Ambow Shanghai. The exercise price of such option shall be all or part, as applicable, of the initial amount of the registered capital contributed by such shareholder to acquire such equity interest in Ambow Shanghai and may be paid by the cancellation of indebtedness owed by such shareholder to Ambow Online, or the minimum amount of consideration permitted by applicable PRC law at the time when such transfer occurs, in which case we will pay the exercise price through, to the extent necessary, a combination of cash and cancellation of indebtedness owed by such shareholder to Ambow Online. Ambow Online or its designee shall have sole discretion to decide when to exercise the option, whether in part or in full. Currently, we do not expect to exercise such option in the foreseeable future. Without Ambow Online’s written consent, each of Xuejun Xie and Xiaogang Feng shall not (i) transfer the equity interest in Ambow Shanghai to any third party, (ii) supplement, alter or modify the articles of association of Ambow Shanghai in any form, or increase or decrease Ambow Shanghai’s registered capital, or otherwise change the structure of its registered capital, or (iii) incur, assume, guarantee or allow the existence of any debt other than the debt that (x) arises in the normal or routine course of business rather than out of borrowing or (y) has been disclosed to and approved in writing by Ambow Online. This agreement shall remain effective until the termination of the loan agreement. Ambow Online has the right to early terminate this agreement upon twenty days’ prior notice, but neither Xuejun Xie nor Xiaogang Feng may early terminate the agreement. All disputes arising out of or in connection with this agreement shall be settled by the parties through good faith consultations. If no agreement can be reached through consultations within sixty days after one party receives a notice from other party requesting the beginning of such consultations or as otherwise agreed by the parties, either party shall have the right to submit relevant disputes to China International Economic and Trade Arbitration Commission for arbitration in accordance with its then-effective arbitration rules. The arbitration shall be held in Beijing. The award of the arbitration shall be final and binding on both parties.

Powers of Attorney. Pursuant to the powers of attorney, each dated October 31, 2009, each of Xuejun Xie and Xiaogang Feng irrevocably entrusted all the rights to exercise her or his voting power to Ambow Online, including without limitation, the power to sell, transfer or pledge, in whole or in part, such shareholder’s equity interests in Ambow Shanghai and to nominate and appoint the legal representative, directors, supervisors, general managers and other senior management of Ambow Shanghai during the term of the share pledge. The powers of attorney have been in effect since the date of execution. Unless terminated as agreed by the shareholders of Ambow Shanghai and Ambow Online, the powers of attorney shall be irrevocable and remain effective during the term of pledge.

Loan Agreement. Pursuant to the loan agreement, dated October 31, 2009, and amended by a supplementary agreement dated January 4, 2010, among Ambow Online, Xuejun Xie and Xiaogang Feng, Ambow Online loaned RMB0.8 million to Xuejun Xie and RMB0.2 million to Xiaogang Feng to fund the registered capital requirements of Ambow Shanghai. To the extent permitted by PRC laws, each loan shall be deemed to have been repaid upon the transfer of the equity interest in Ambow Shanghai held by each of Xuejun Xie and Xiaogang Feng, as applicable, to Ambow Online or its designee. To the extent permitted by the relevant PRC laws, Ambow Online shall determine at its sole discretion the timing and method of the repayment of the loans under the loan agreement and notify the borrowers in writing of such arrangements seven days in advance. The borrowers shall not repay the loans to Ambow Online early unless Ambow Online notifies the borrowers in writing that the loans have expired or as otherwise provided under the loan agreement. The borrowers shall not assign their rights and obligations under the loan agreement to any third party without Ambow Online’s prior written consent. The loan agreement has been in effect since the date of execution by the parties and shall remain effective until the borrowers fully repay the loans under the agreement. If any dispute arises between the parties in connection with the interpretation and performance of the terms, the parties shall negotiate in good faith to resolve such dispute. If no agreement can be reached, either party may submit such dispute to China International Economic and Trade Arbitration Commission for arbitration in accordance with its then-effective arbitration rules. The arbitration shall be held in Chinese in Beijing. The award of the arbitration shall be final and binding on both parties.

Agreements that provide effective control over Ambow Sihua and its subsidiaries

We have entered into a series of agreements with Ambow Sihua and its shareholders. These agreements provide us substantial ability to control Ambow Sihua and its shareholders, and we have obtained an exclusive option to purchase all of the equity interests of Ambow Sihua. These agreements include:

Share Pledge Agreements. Pursuant to the share pledge agreement, dated October 31, 2009 and further amended by a supplementary agreement dated March 4, 2010, between Ambow Online and Xuejun Xie, a shareholder of Ambow Sihua, and the share pledge agreement, dated March 4, 2010, between Ambow Online and Xiaogang Feng, a shareholder of Ambow Sihua, each of Xuejun Xie and Xiaogang Feng pledged all of her or his equity interest in Ambow Sihua to Ambow Online to secure the performance of Ambow Sihua or its subsidiaries under a technology service agreement between Ambow Online and Ambow Sihua dated October 31, 2009 as described below. If Ambow Sihua fails to fulfil its obligations under the technology service agreement, Ambow Online may dispose of the pledged equity in accordance with the provisions of the Security Law of the People’s Republic of China and relevant laws and regulations, and shall have the right to be

indemnified for the secured debt and any other relevant expenses out of the proceeds from the disposal of the pledged equity. Without Ambow Online’s prior written consent, each of Xuejun Xie and Xiaogang Feng shall not (i) make a proposal to amend the articles of association of Ambow Sihua or cause the making of such proposal, or increase or reduce Ambow Sihua’s registered capital, or otherwise change the structure of its registered capital, (ii) create any further security, encumbrances and any third party’s rights on the pledged equity in addition to the pledge created under the share pledge agreements, (iii) perform any act that may prejudice any rights of Ambow Online under the share pledge agreements, or any act that may materially affect the assets, business and/or operations of Ambow Sihua, (iv) distribute dividends to the shareholders in any form (however, upon Ambow Online’s request, pledgors shall immediately distribute all of their distributable profits to the shareholders), or (v) transfer or dispose of the pledged equity in any way. The share pledge agreements shall remain in effect until the technology service agreement is terminated and the secured debt is fully repaid. The share pledge agreements may be unilaterally terminated by Ambow Online. Neither of Xuejun Xie and Xiaogang Feng is entitled to unilaterally terminate the share pledge agreements. Without Ambow Online’s prior written consent, pledgors shall not transfer any of their rights or obligations under the share pledge agreements to any other party. Ambow Online shall have the right to transfer to any third party any of its rights or obligations under the share pledge agreements and any of its rights or obligations under other agreements contemplated by the share pledge agreements without pledgor’s prior consent. If any dispute arises between the parties in connection with the interpretation and performance of the provisions thereunder, the parties shall resolve such dispute in good faith through discussions. If no agreement can be reached within sixty days after one party receives the notice of the other party requesting the beginning of discussions or as otherwise agreed, either party shall have the right to submit such dispute to the China International Economic and Trade Arbitration Commission for arbitration in accordance with its then-effective rules. The arbitration shall be held in Beijing. The award of the arbitration shall be final and binding upon the parties.

Call Option Agreements. Pursuant to the call option agreement, dated October 31, 2009 and further amended by a supplementary agreement dated March 4, 2010, between Ambow Online and Xuejun Xie, a shareholder of Ambow Sihua, and the call option agreement, dated March 4, 2010, between Ambow Online and Xiaogang Feng, a shareholder of Ambow Sihua, each of Xuejun Xie and Xiaogang Feng irrevocably granted Ambow Online or its designee an exclusive option to purchase, to the extent permitted under PRC laws, all or part of her or his equity interest in Ambow Sihua. The exercise price of such option shall be all or part, as applicable, of the initial amount of the registered capital contributed by such shareholder to acquire such equity interest in Ambow Sihua and may be paid by the cancellation of indebtedness owed by such shareholder to Ambow Online or the minimum amount of consideration permitted by applicable PRC law at the time when such transfer occurs, in which case we will pay the exercise price through, to the extent necessary, a combination of cash and cancellation of indebtedness owed by such shareholder to Ambow Online.

Ambow Online or its designee shall have sole discretion to decide when to exercise the option, whether in part or in full. Currently, we do not expect to exercise such option in the foreseeable future. Without Ambow Online’s written consent, each of Xuejun Xie and Xiaogang Feng shall not (i) transfer the equity interest in Ambow Sihua to any third party, (ii) supplement, alter or modify the articles of association of Ambow Sihua in any form, or increase or decrease Ambow Sihua’s registered capital, or otherwise change the structure of its registered capital, or (iii) incur, assume, guarantee or allow the existence of any debt other than the debt that (x) arises in the normal or routine course of business rather than out of borrowing or (y) has been disclosed to and approved in writing by Ambow Online. Xuejun Xie and Xiaogang Feng represent and warrant that during the term of the call option agreements, Xuejun Xie, Xiaogang Feng and Ambow Sihua have not engaged in and shall not engage in any act or omission that may cause any losses to Ambow Online and may cause any reduction in value of the equity interests in Ambow Sihua held by Xuejun Xie and Xiaogang Feng. This agreement has been in effect as of the date when the authorized representatives of the parties duly execute the agreement, and shall remain effective until the termination of the loan agreement. Unless otherwise provided therein, Ambow Online shall have the right to terminate this agreement early upon twenty days’ prior notice, but neither of Xuejun Xie and Xiaogang Feng shall terminate this agreement early. Ambow Online shall have the right to transfer its rights under the call option agreements and other agreements contemplated by the call option agreements at its sole discretion to any third party without Xuejun Xie and Xiaogang Feng’s consent. All disputes arising out of or in connection with this agreement shall be settled by the parties through good faith consultations. If no agreement can be reached through consultations within sixty days after one party receives a notice from other party requesting the beginning of such consultations or as otherwise agreed by the parties, either party shall have the right to submit relevant disputes to China International Economic and Trade Arbitration Commission for arbitration in accordance with its then-effective arbitration rules. The arbitration shall be held in Beijing. The award of the arbitration shall be final and binding on both parties.

Powers of Attorney. Pursuant to the powers of attorney, dated October 31, 2009 and March 4, 2010, respectively, each of Xuejun Xie and Xiaogang Feng irrevocably entrusted all the rights to exercise her or his voting power to Ambow Online, including without limitation, the power to sell, transfer or pledge, in whole or in part, her or his equity interest in Ambow Sihua and nominate and appoint the legal representative, directors, supervisors, general managers and other senior management of Ambow Sihua during the term of the share pledge. The powers of attorney have been in effect since the date of execution. Unless terminated as agreed by the shareholders of Ambow Sihua and Ambow Online, the powers of attorney shall be irrevocable and remain effective during the term of pledge.

Loan Agreement. Pursuant to the loan agreement between Ambow Online and Xiaogang Feng, dated March 4, 2010, Ambow Online loaned RMB40.0 million to Xiaogang Feng to fund the registered capital requirements of Ambow Sihua. To the extent permitted by PRC laws, such loan shall be deemed to have been repaid upon the transfer of the equity interest in Ambow Sihua held by Xiaogang Feng to Ambow Online or its designee. To the extent permitted by the PRC laws, Ambow Online shall determine at its sole discretion the timing and method of the repayment of the loan under the loan agreement and notify the borrower in writing of such arrangements seven days in advance. The borrower shall not repay the loan early to Ambow Online unless Ambow Online notifies the borrower in writing that the loan has expired or as otherwise provided under the loan agreement. The borrower shall not assign his or her rights and obligations under the loan agreement to any third party without Ambow Online’s prior written consent. The loan agreement has been in effect since the date of execution by the parties and shall remain effective until the borrower fully repays the loan under the agreement. If any dispute arises between the parties in connection with the interpretation and performance of the terms, the parties shall negotiate in good faith to resolve such dispute. If no agreement can be reached, either party may submit such dispute to China International Economic and Trade Arbitration Commission for arbitration in accordance with its then-effective arbitration rules. The arbitration shall be held in Chinese in Beijing. The award of the arbitration shall be final and binding on both parties.

Agreements that provide effective control over Suzhou Wenjian

We have entered into a series of agreements with Suzhou Wenjian and its shareholders. These agreements provide us with the ability to control Suzhou Wenjian and grant us the exclusive option to purchase all of the equity interests of Suzhou Wenjian. These agreements include:

Share Pledge Agreement. Pursuant to the share pledge agreement, dated February 25, 2009, among Ambow Online, Xuejun Xie, Xiaogang Feng and Yisi Gu, each a shareholder of Suzhou Wenjian, each of Xuejun Xie, Xiaogang Feng and Yisi Gu pledged all of his or her equity interest in Suzhou Wenjian to Ambow Online to secure the performance of Suzhou Wenjian under a technology service agreement between Ambow Online and Suzhou Wenjian dated February 25, 2009. If (a) Suzhou Wenjian fails to fulfil its payment obligation or other related obligations to pledgee in accordance with the provisions of technology service agreement, or (b) pledgors breach their duties or obligations thereunder, pledgee shall have the right to exercise the pledge in any manner at any time it deems appropriate to the extent permitted by applicable laws during the term of pledge, including without limitation: (a)to negotiate with pledgors to discharge the secured debt with the pledged equity at a discount rate; (b) to sell off the pledged equity and use the proceeds thereof to discharge the secured debt; (c) to retain a relevant agency to auction all or part of the pledged equity; and/or (d) to otherwise dispose of the pledged equity appropriately to the extent permitted by applicable laws. Each shareholder of Suzhou Wenjian also agreed that, without the prior written consent of Ambow Online, such shareholder shall not transfer, dispose of or otherwise create any encumbrance over his or her equity interest in Suzhou Wenjian. The share pledge will expire three years after all obligations related to the technology service agreement are fully performed. Without Ambow Online’s prior written consent, pledgors shall not transfer any of their rights or obligations under the share pledge agreement to any other party. Ambow Online shall have the right to transfer to any third party any of its rights or obligations under the share pledge agreement and any of its rights or obligations under other agreements contemplated by the share pledge agreement without pledgor’s prior consent. The share pledge agreement shall remain in effect until the secured debt is fully repaid. The share pledge agreement may be unilaterally terminated by Ambow Online. None of Xuejun Xie, Xiaogang Feng and Yisi Gu is entitled to unilaterally terminate the share pledge agreement. If any dispute arises between the parties in connection with the interpretation and performance of the provisions thereunder, the parties shall resolve such dispute in good faith through discussions. If no agreement can be reached within sixty days after one party receives the notice of the other party requesting the beginning of discussions or as otherwise agreed, either party shall have the right to submit such dispute to China International Economic and Trade Arbitration Commission for arbitration in accordance with its then-effective rules. The arbitration shall be held in Beijing. The award of the arbitration shall be final and binding upon the parties.

Call Option Agreement. Pursuant to the call option agreement, dated February 25, 2009, among Ambow Online, Xuejun Xie, Xiaogang Feng and Yisi Gu, each a shareholder of Suzhou Wenjian, each of Xuejun Xie, Xiaogang Feng and Yisi Gu irrevocably granted Ambow Online or its designee an exclusive option to purchase, to the extent permitted under PRC laws, all or part of his or her equity interest in Suzhou Wenjian. The exercise price of such option shall be all or part, as applicable, of the initial amount of the registered capital contributed by such shareholder to acquire such equity interest in Suzhou Wenjian and may be paid by the cancellation of indebtedness owed by such shareholder to Ambow Online, or the minimum amount of consideration permitted by applicable PRC law at the time when such transfer occurs, in which case we will pay the exercise price through, to the extent necessary, a combination of cash and cancellation of indebtedness owed by such shareholder to Ambow Online. Ambow Online or its designee shall have sole discretion to decide when to exercise the option, whether in part or in full. Currently, we do not expect to exercise such option in the foreseeable future. Without Ambow Online’s written consent, each of Xuejun Xie, Xiaogang Feng and Yisi Gu shall not transfer his or her equity interest in Suzhou Wenjian to any third party. Xuejun Xie, Xiaogang Feng and Yisi Gu represent and warrant that (i) except for the pledge granted under the share pledge agreement, they have not created or allowed any option, call option, pledge, or other equity interest or security interest on their equity interests in Suzhou Wenjian, and (ii) during the term of the call option agreement, Xuejun Xie, Xiaogang Feng and Yisi Gu and Suzhou Wenjian have not engaged in and shall not engage in any act or omission that may cause any losses to Ambow Online and may cause any reduction in value of the equity interests in Suzhou Wenjian held by Xuejun Xie, Xiaogang Feng and Yisi Gu. This agreement has been in effect since the date when the authorized representatives of the parties duly execute the agreement, and shall remain effective until the termination of the loan agreement. Unless otherwise provided therein, Ambow Online shall have the right to terminate this agreement early upon twenty days’ prior notice, but Xuejun Xie, Xiaogang Feng and Yisi Gu shall not terminate this agreement early. Ambow Online shall have the right to transfer its rights under the agreement and other agreements contemplated by the agreement at its sole discretion to any third party without Xuejun Xie, Xiaogang Feng and Yisi Gu’s consent. All disputes arising out of or in connection with this agreement shall be settled by the parties through good faith consultations. If no agreement can be reached through consultations within sixty days after one party receives a notice from other party requesting the beginning of such consultations or as otherwise agreed by the parties, either party shall have the right to submit relevant disputes to China International Economic and Trade Arbitration Commission for arbitration in accordance with its then-effective arbitration rules. The arbitration shall be held in Beijing. The award of the arbitration shall be final and binding on both parties.

Powers of Attorney. Under powers of attorney, each dated February 25, 2009, each of Xuejun Xie, Xiaogang Feng and Yisi Gu granted to Ambow Online the power to exercise all of his or her voting rights of Suzhou Wenjian during the term of the share pledge. The powers of attorney shall come into effect upon the date of execution. Unless terminated as agreed by the shareholders of Suzhou Wenjian and Ambow Online, the powers of attorney shall remain effective during the term of pledge.

Loan Agreement. Pursuant to the loan agreement among Ambow Online, Xuejun Xie, Xiaogang Feng and Yisi Gu dated February 25, 2009, Ambow Online loaned RMB0.4 million to Xiaogang Feng, RMB0.3 million to Xuejun Xie and RMB0.3 million to Yisi Gu to fund the registered capital requirements of a domestic PRC company. Ambow later formed Suzhou Wenjian to serve as this domestic PRC company. To the extent permitted by the relevant PRC laws, Ambow Online shall determine at its sole discretion the timing and method of the repayment of the loans and notify borrowers in writing of such arrangements seven days in advance. Borrowers and Ambow Online further agree that borrowers shall not repay the loan to Ambow Online early unless Ambow Online notifies borrowers in writing that the loans thereunder have expired or as otherwise provided therein. To the extent permitted by PRC laws, each loan shall be deemed to have been repaid upon the transfer of the equity interest held by each of Xuejun Xie, Xiaogang Feng and Yisi Gu in Suzhou Wenjian to Ambow Online. This agreement has been in effect since the date of execution by the parties and shall remain effective until the borrowers fully repay the loans under this agreement. If any dispute arises between the parties in connection with the interpretation and performance of the terms thereof, the parties shall negotiate in good faith to resolve such dispute. If no agreement can be reached, either party may submit such dispute to China International Economic and Trade Arbitration Commission for arbitration in accordance with its then-effective arbitration rules. The arbitration shall be conducted in Chinese in Beijing. The award of the arbitration shall be final and binding upon the disputing parties.

Agreements that transfer economic benefits to us

Agreements that transfer economic benefits to us from Ambow Shida and its subsidiaries

Exclusive Cooperation Agreement. Pursuant to the exclusive cooperation agreement, dated January 31, 2005 and revised on May 13, 2010, by and between Ambow Online and Ambow Shida, Ambow Online has the exclusive right to provide to Ambow Shida technical support and marketing consulting services relating to online education for primary and middle school and other related services in exchange for certain service fees, which are equal to Ambow Shida’s pre-tax profit. Without Ambow Online’s written consent, Ambow Shida shall not transfer, pledge or assign to any third party the rights and obligations under this agreement or use such rights and obligations for the benefit of any third party. The initial term of this agreement is twenty years and the term can be renewed upon expiration. The agreement can be terminated by mutual agreement, by written notice from the non-breaching party upon a breaching party’s failure to cure its breach, or by either party’s written notice upon nonperformance of the agreement for 30 days as a result of any force majeure. In the event of any dispute with respect to the interpretation and implementation of this agreement, the parties shall negotiate in good faith to resolve the dispute. In the event the parties fail to reach an agreement on the resolution of such dispute within 30 days after the negotiation begins, either party may submit such dispute to China International Economic and Trade Arbitration Commission for arbitration in accordance with its then-effective arbitration rules. We have not received any payment of service fees contemplated by this agreement.

Ambow Online has the unilateral right to adjust the level of service fee to be charged to Ambow Shida under this exclusive cooperation agreement at any time. At the time this agreement was originally entered into on January 31, 2005, we set the service fee that could be charged at 65% of Ambow Shida’s profits in order to retain sufficient cash in Ambow Shida to fund its operating needs and manage liquidity. We subsequently determined that in the short to medium term we would not charge the service fee available to us in the agreement but on May 13, 2010 we updated the agreement to increase the service fee percentage that could be charged by Ambow Online to Ambow Shida to 100% of profits so as to provide us with more flexibility in the future.

We have not yet received any payment of service fees contemplated by this agreement but retain the flexibility to charge these service fees in the future. In addition to extracting the profits of Ambow Shida through the exclusive cooperation agreement, we also can extract profits from Ambow Shida through dividends to Ambow Online received indirectly through the shareholders of Ambow Shida or through donations directly from Ambow Shida to Ambow Online. The dividends and/or donations can be enacted through the agreements that provide us with effective control over Ambow Shida and its subsidiaries as set out in “Item 7.B —Related Party Transactions — Contractual arrangements with our VIEs and their respective subsidiaries”. These two alternative mechanisms are not currently subject to any legal restrictions or limitations.

As of the date of this report, no distributions have been made to the shareholders of Ambow Shida and so no subsequent distribution has been made to us or Ambow Online. As described above, at our discretion we have decided to retain all of Ambow Shida’s profits to date within Ambow Shida for the purpose of managing its liquidity.

Agreement that transfer economic benefits to us from Ambow Shanghai and its subsidiaries