Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A

(Rule 14a-101)

PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE

SECURITIES EXCHANGE ACT OF 1934

(AMENDMENT NO. )

Filed by the Registrant x Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement | |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) | |

| x | Definitive Proxy Statement | |

| ¨ | Definitive Additional Materials | |

| ¨ | Soliciting Material Pursuant to §240.14a-12 | |

GLOBAL INDEMNITY plc

(Name of Registrant as Specified In Its Charter)

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| x | No fee required. | |||

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. | |||

| (1) | Title of each class of securities to which transaction applies:

| |||

| (2) | Aggregate number of securities to which transaction applies:

| |||

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11 (set forth the amount on which the filing fee is calculated and state how it was determined):

| |||

| (4) | Proposed maximum aggregate value of transaction:

| |||

| (5) | Total fee paid:

| |||

| ¨ | Fee previously paid with preliminary materials. | |||

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. | |||

| (1) | Amount Previously Paid:

| |||

| (2) | Form, Schedule or Registration Statement No.

| |||

| (3) | Filing Party:

| |||

| (4) | Date Filed:

| |||

Table of Contents

GLOBAL INDEMNITYPLC

SPECIAL SCHEME MEETING AND EXTRAORDINARY GENERAL MEETING OF HOLDERS

OF ORDINARY SHARES TO BE HELD ON SEPTEMBER 14, 2016

July 15, 2016

To the Holders of A ordinary shares and B Ordinary Shares of Global Indemnity plc (“GI Ireland”):

On September 14, 2016, commencing at 10:00 a.m., local time, we will hold two special meetings of holders of our ordinary shares at our registered office located at 25/28 North Wall Quay, Dublin 1 Ireland.

At these meetings, you will be asked to vote on a number of proposals, including proposals for a “scheme of arrangement” under Irish law that would change the ultimate holding company of the Global Indemnity group of companies from an entity incorporated in Ireland to an entity incorporated in the Cayman Islands (“Cayman”).

Our Board of Directors has determined that replacing the current holding company of the Global Indemnity group of companies, an entity incorporated in Ireland, with an entity incorporated in Cayman and the other proposals referenced below are in the interests of GI Ireland, its operations and its shareholders. In summary, our Board of Directors believes that simplifying our corporate and tax structure by reverting to a structure where the holding company of the Global Indemnity group of companies is an entity incorporated in the Cayman Islands would be in the best interest of GI Ireland and its shareholders, that the Cayman Islands has a business friendly regulatory environment and a predictable legal framework that simultaneously provides both corporate certainty and shareholder protections, and that the Cayman Islands presents a flexible and stable legal and corporate governance framework, which allows a company’s board of directors latitude to exercise its judgment in what it deems to be in the best interests of the company, particularly with respect to extraordinary transactions. The reasons for the transaction and the other proposals are discussed in further detail in the accompanying proxy statement.

Completion of the proposed scheme of arrangement will result in the cancellation of your A ordinary shares and/or B ordinary shares (together, the A ordinary shares and B ordinary shares, the “GI Ireland ordinary shares”) in GI Ireland, and the replacement of those shares with an equal number of A ordinary shares and/or B ordinary shares, respectively, issued by Global Indemnity Limited, a Cayman exempted company (“GI Cayman”).

Following completion of the transaction, the A ordinary shares of our ultimate parent company will be listed on the Nasdaq Global Select Market (“Nasdaq”) under the ticker symbol “GBLI” and will be registered with the U.S. Securities and Exchange Commission (the “SEC”) under the Securities Exchange Act of 1934, as amended, and be subject to the same SEC reporting requirements, the mandates of the Sarbanes-Oxley Act of 2002 and the applicable corporate governance rules of Nasdaq. We will continue to report our financial results in U.S. dollars and under U.S. generally accepted accounting principles. GI Cayman will no longer be required to provide you with our Irish Statutory Accounts prepared in accordance with Irish law, but we will in the ordinary course provide you with customary financial information in accordance with our established historical practices.

Table of Contents

In addition to the proposals relating to the scheme of arrangement, we are also asking you to approve the following additional proposals at the extraordinary general meeting (as more fully described in the accompanying “scheme circular” and set out in the Notice Of Extraordinary General Meeting at Annex E):

| • | To approve a reduction of our capital under Sections 84 and 85 of the Irish Companies Act 2014 in order to effect a cancellation of our outstanding GI Ireland ordinary shares, other than any shares held by GI Cayman and, for the avoidance of doubt, the Deferred Shares of €1 each in the Capital of GI Ireland (“Deferred Share”) and any shares in the capital of GI Ireland held as treasury shares within the meaning of Section 106 of the Companies Act 2014 of Ireland (“Treasury Shares”), in connection with the scheme of arrangement. |

| • | To approve the terms of the acquisition of a GI Ireland ordinary share by GI Cayman prior to the scheme of arrangement, in connection with the scheme of arrangement. |

| • | To approve the authorization of the directors of GI Ireland to allot ordinary shares in GI Ireland to GI Cayman up to an amount equal to the nominal value of the ordinary shares in GI Ireland which are to be cancelled in connection with the scheme of arrangement. |

| • | To approve the application by GI Ireland of a reserve credit, arising on its books of account as a result of the cancellation of GI Ireland ordinary shares in connection with the scheme of arrangement, to pay up in full at par the ordinary shares allotted to GI Cayman in connection with the scheme of arrangement. |

| • | To approve an amendment to the memorandum of association of GI Ireland to grant GI Ireland a new object enabling it to enter into the scheme of arrangement. |

| • | To approve an amendment to the articles of association of GI Ireland to (i) provide that the allotment or issue of all ordinary shares in GI Ireland on or after the amendment to the articles of association and before the capital of GI Ireland is reduced by the cancellation of the GI Ireland ordinary shares, (other than any shares held by GI Cayman, and for the avoidance of doubt the Deferred Shares and any Treasury Shares) in issue before 5:00 p.m. (Eastern Standard Time) and 10:00 p.m. (Irish time) on the day before the hearing at which the Scheme of Arrangement is sanctioned (the“Cancellation Record Time”) will be subject to the Scheme of Arrangement; (ii) allow GI Cayman to transfer to itself, or to any person on its behalf, any ordinary shares in GI Ireland allotted or issued to any person on or after the Cancellation Record Time, or otherwise issued after the amendment to the articles of association of GI Ireland that are not subject to the Scheme of Arrangement; (iii) allow GI Ireland to appoint an attorney to enter into any transfers required in respect of the transfer referred to at (ii) above; and GI Cayman to appoint an attorney to exercise rights attached to those shares and (iv) disapply rights of pre-emption to ordinary shares in GI Ireland allotted and issued pursuant to the Scheme of Arrangement. |

| • | To approve motions to adjourn each meeting to a later date to solicit additional proxies, in the discretion of the chairman of the meeting, if there are insufficient proxies to approve the meeting proposals at the time of each applicable shareholder meeting. |

The accompanying proxy statement provides important information about the meeting proposals described above. We encourage you to read the entire document carefully, including the “Risk Factors” section beginning on page 28 of the accompanying proxy statement, before voting. You are entitled to vote by attending the meetings or by appointing a proxy. It is not necessary that the proxy appointed by you be a shareholder of GI Ireland.

Your vote is very important. Your Board of Directors unanimously recommends that you vote “FOR” all of the above proposals.

To ensure that your GI Ireland ordinary shares are voted in accordance with your wishes, please mark, date, sign and return both the accompanying proxy cards (one blue for the scheme meeting, and one white for the extraordinary general meeting) in the enclosed, postage-paid envelope as promptly as possible. In order for your

Table of Contents

proxies to be voted we must receive your proxy cards at P.O. Box2094, Jersey City, New Jersey 07303-9874, not later than 9:00 a.m. (Eastern time) on September 7, 2016 or at the registered office of GI Ireland, at 25/28 North Wall Quay, Dublin 1, Ireland (ref. MJW/JGG), at least forty eight hours prior to the commencement of the relevant meeting.

If you hold your GI Ireland ordinary shares in “street name” through a bank, broker, trustee, custodian or other nominee (which we generally refer to as “brokers” or “nominees”), please follow the voting instructions provided by your broker, which may include an option to instruct the broker or nominee by telephone on how to vote.

Please note that holders of GI Ireland ordinary shares through brokers or nominees may be required to submit voting instructions to their applicable broker or nominee at or prior to the deadline applicable to registered holders of GI Ireland ordinary shares and such holders should therefore follow the separate instructions that will be provided by their applicable broker or nominee.

If you have any questions about the meetings or require assistance, please call Georgeson LLC, our proxy solicitor, at (866) 767-8989 (toll-free within the United States) or at (781) 575-2137 (outside the United States).

On behalf of GI Ireland’s Board of Directors, thank you for your continued support.

Sincerely,

|

| |

| Cynthia Y. Valko | Saul A. Fox | |

| Chief Executive Officer | Chairman of the Board of Directors |

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued in the contemplated scheme of arrangement or determined if the accompanying proxy statement is truthful or complete. Any representation to the contrary is a criminal offense.

The accompanying proxy statement related to the GI Ireland ordinary shares is dated July 15, 2016 and is first being mailed to the holders of GI Ireland’s ordinary shares on or about July 18, 2016.

Table of Contents

SUMMARY OF NOTICES OF THE SPECIAL SCHEME MEETING

AND THE EXTRAORDINARY GENERAL

MEETING OF THE HOLDERS OF GLOBAL INDEMNITY PLC A ORDINARY SHARES AND B

ORDINARY SHARES

TO BE HELD ON SEPTEMBER 14, 2016

To the Holders of A ordinary shares and B ordinary shares of Global Indemnity plc (together the A ordinary shares and B ordinary shares, the “GI Ireland ordinary shares”):

On September 14, 2016, Global Indemnity plc, a public limited company organized under the laws of Ireland (“GI Ireland”), will hold a special meeting (the “scheme meeting”) of the holders of GI Ireland A ordinary shares and B ordinary shares (the “shareholders”), which will commence at 10:00 a.m., local time, and an extraordinary general meeting (the “extraordinary general meeting”) of shareholders, which will commence at 10:15 a.m., local time (or as soon thereafter as the scheme meeting concludes or is adjourned), in order to approve certain proposals, including a proposal related to a scheme of arrangement under Irish law. We sometimes refer to these meetings together as the “shareholder meetings.” The shareholder meetings will be held at our office at 25/28 North Wall Quay, Dublin 1, Ireland. Shareholders are being asked to vote on the following matters:

At the scheme meeting:

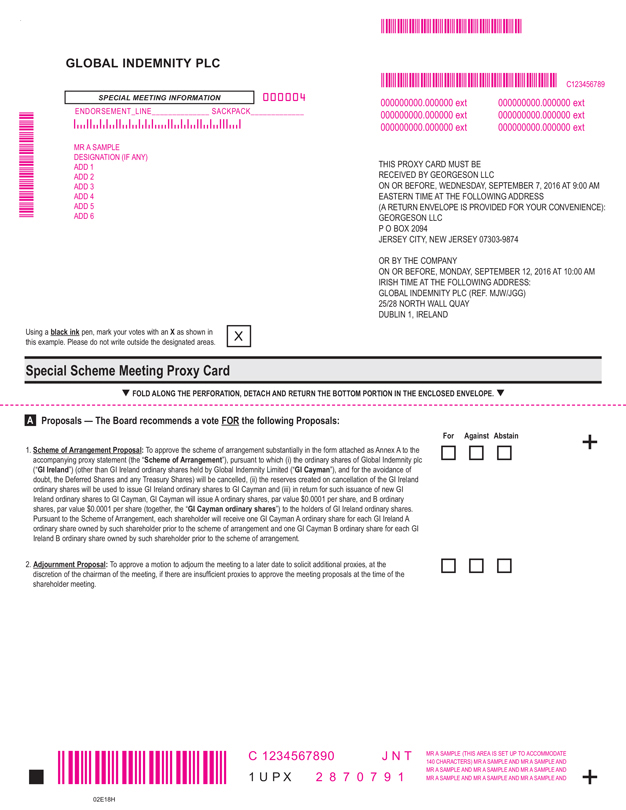

| • | To approve the scheme of arrangement substantially in the form attached as Annex A to the accompanying proxy statement (the “Scheme of Arrangement”), pursuant to which (i) GI Ireland ordinary shares (other than GI Ireland ordinary shares held by Global Indemnity Limited (“GI Cayman”), and for the avoidance of doubt, the Deferred Shares and any Treasury Shares) will be cancelled, (ii) the reserve created on cancellation of the GI Ireland ordinary shares will be used to issue GI Ireland ordinary shares to GI Cayman and (iii) in return for such issuance of new GI Ireland ordinary shares to GI Cayman, GI Cayman will issue A ordinary shares, par value $0.0001 per share, and B ordinary shares, par value $0.0001 per share (together, the “GI Cayman ordinary shares”) to the holders of GI Ireland ordinary shares. Pursuant to the Scheme of Arrangement, each shareholder will receive one GI Cayman A ordinary share for each GI Ireland A ordinary share owned by such shareholder prior to the scheme of arrangement and one GI Cayman B ordinary share for each GI Ireland B ordinary share owned by such shareholder prior to the scheme of arrangement. |

We refer to this proposal (Proposal Number One) as the “Scheme of Arrangement Proposal.”

At the extraordinary general meeting:

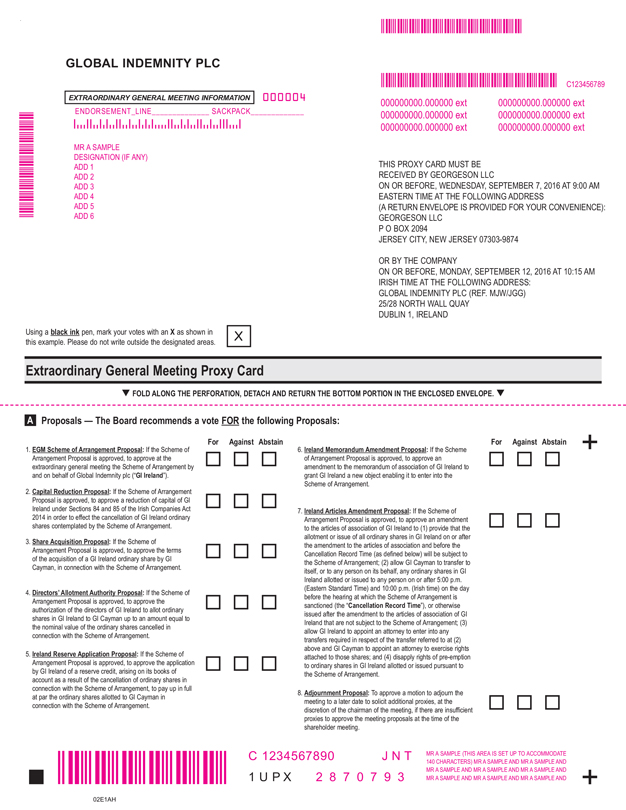

| • | If the Scheme of Arrangement Proposal is approved, to approve the Scheme of Arrangement by and on behalf of GI Ireland. |

We refer to this proposal (Proposal Number Two) as the “EGM Scheme of Arrangement Proposal.”

| • | If the Scheme of Arrangement Proposal is approved, to approve a reduction of capital of GI Ireland under Sections 84 and 85 of the Irish Companies Act 2014 in order to effect the cancellation of GI Ireland ordinary shares contemplated by the Scheme of Arrangement. |

We refer to this proposal (Proposal Number Three) as the “Capital Reduction Proposal.”

| • | If the Scheme of Arrangement Proposal is approved, to approve the terms of the acquisition of a GI Ireland ordinary share by GI Cayman in connection with the Scheme of Arrangement. |

We refer to this proposal (Proposal Number Four) as the “Share Acquisition Proposal.”

| • | If the Scheme of Arrangement Proposal is approved, to approve the authorization of the directors of GI Ireland to allot ordinary shares in GI Ireland to GI Cayman up to an amount equal to the nominal value of the ordinary shares cancelled in connection with the Scheme of Arrangement. |

Table of Contents

We refer to this proposal (Proposal Number Five) as the “Directors’ Allotment Authority Proposal.”

| • | If the Scheme of Arrangement Proposal is approved, to approve the application by GI Ireland of a reserve credit, arising on its books of account as a result of the cancellation of ordinary shares in connection with the Scheme of Arrangement, to pay up in full at par the ordinary shares allotted to GI Cayman in connection with the Scheme of Arrangement. |

We refer to this proposal (Proposal Number Six) as the “Ireland Reserve Application Proposal.”

| • | If the Scheme of Arrangement Proposal is approved, to approve an amendment to the memorandum of association of GI Ireland to grant GI Ireland a new object enabling it to enter into the Scheme of Arrangement. |

We refer to this proposal (Proposal Number Seven) as the “Ireland Memorandum Amendment Proposal.”

| • | If the Scheme of Arrangement Proposal is approved, to approve an amendment to the articles of association of GI Ireland to (i) provide that the allotment or issue of all ordinary shares in GI Ireland on or after the amendment to the articles of association and before the Cancellation Record Time (as defined below) will be subject to the Scheme of Arrangement; (ii) allow GI Cayman to transfer to itself, or to any person on its behalf, any ordinary shares in GI Ireland allotted or issued to any person on or after 5:00 p.m. (Eastern Standard Time) and 10:00 p.m. (Irish time) on the day before the hearing at which the Scheme of Arrangement is sanctioned (the “Cancellation Record Time”), or otherwise issued after the amendment to the articles of association of GI Ireland that are not subject to the Scheme of Arrangement; (iii) allow GI Ireland to appoint an attorney to enter into any transfers required in respect of the transfer referred to at (ii) above and GI Cayman to appoint an attorney to exercise rights attached to those shares; and (iv) disapply rights of pre-emption to ordinary shares in GI Ireland allotted or issued pursuant to the Scheme of Arrangement. |

We refer to this proposal (Proposal Number Eight) as the “Ireland Articles Amendment Proposal.”

At both shareholder meetings:

| • | To approve motions to adjourn each meeting to a later date to solicit additional proxies, in the discretion of the chairman of the meeting, if there are insufficient proxies to approve the meeting proposals at the time of each applicable shareholder meeting. |

We refer to such proposals as the “Adjournment Proposals.”

The proposals contemplated by this proxy statement, including the Scheme of Arrangement Proposal, the EGM Scheme of Arrangement Proposal, the Capital Reduction Proposal, the Share Acquisition Proposal, the Director’s Allotment Authority Proposal, the Ireland Reserve Application Proposal, the Ireland Memorandum Amendment Proposal, the Ireland Articles Amendment Proposal, and the Adjournment Proposals, are sometimes referred to herein as the “meeting proposals.”

The transactions contemplated by the Scheme of Arrangement, including the Scheme of Arrangement Proposal, the EGM Scheme of Arrangement Proposal, the Capital Reduction Proposal, the Directors’ Allotment Authority Proposal, the Ireland Reserve Application Proposal, the Ireland Memorandum Amendment Proposal and the Ireland Articles Amendment Proposal and, if approved, the Share Acquisition Proposal, are sometimes referred to herein as the “Transaction.”

Approval of each of the Scheme of Arrangement Proposal, the EGM Scheme of Arrangement Proposal, the Capital Reduction Proposal, the Directors’ Allotment Authority Proposal, the Ireland Reserve Application Proposal, the Ireland Memorandum Amendment Proposal and the Ireland Articles Amendment Proposal by our shareholders is a condition to the Scheme of Arrangement becoming effective.

The formal notices of the scheme meeting and the extraordinary general meeting are provided as attachments to the accompanying proxy statement as Annexes D and E, respectively, and should be read closely. This summary does not constitute the formal notice in respect of either of those meetings.

Table of Contents

If any other matters properly come before either of the shareholder meetings or any adjournments of either of such shareholder meetings, the persons named in the proxy card will have the authority to vote the GI Ireland ordinary shares represented by all properly executed proxies in their discretion. The Board of Directors of GI Ireland currently does not know of any matters to be raised at the shareholder meetings other than the meeting proposals contained in this proxy statement.

The GI Ireland Board of Directors has set July 12, 2016 as the record date for the scheme meeting and for the extraordinary general meeting. This means that only those persons who were holders of GI Ireland ordinary shares at the close of business on the record date will be entitled to attend and vote at the shareholder meetings and any adjournments thereof.

The scheme meeting is being convened by the directors of GI Ireland. If the GI Ireland shareholders approve each of the Scheme of Arrangement Proposal, the EGM Scheme of Arrangement Proposal, the Capital Reduction Proposal, the Directors’ Allotment Authority Proposal, the Ireland Reserve Application Proposal, the Ireland Memorandum Amendment Proposal and the Ireland Articles Amendment Proposal and the other conditions to the Scheme of Arrangement have been satisfied or waived (and we do not abandon the Scheme of Arrangement), we will proceed to seek the sanction of the High Court of Ireland (the “Irish High Court”) in respect of the Scheme of Arrangement and the Capital Reduction Proposal. Our Irish counsel has advised us that the Irish High Court is unlikely to sanction the Scheme of Arrangement until all conditions to the Transaction have been satisfied or waived. Sanction of the Irish High Court must be obtained as a condition to the Scheme of Arrangement becoming effective. We expect the hearing before the Irish High Court regarding sanction of the Scheme of Arrangement (the “Sanction Hearing”) to be held on a date falling on or around October 21, 2016, further details of which will be advertised by the company on its website and in The Wall Street Journal and certain Irish newspapers. If you are a GI Ireland shareholder who wishes to appear in person or by counsel at the Sanction Hearing and present evidence or arguments in support of or opposition to the Scheme of Arrangement, you may do so by giving proper written notice to A&L Goodbody Solicitors (Reference MJW/JGG), North Wall Quay, IFSC, Dublin 1 as Irish legal advisers to GI Ireland not less than two weeks before the date of such hearing. GI Ireland will not object to the participation in the Sanction Hearing by any person who holds shares through a broker or any other person with a legitimate interest in the proceedings and all such persons will have a right to participate.

The accompanying proxy statement and proxy cards (one blue for the scheme meeting, and one white for the extraordinary general meeting) are first being sent to GI Ireland shareholders on or about July 18, 2016 and contain additional information on how to attend the shareholder meetings and vote any ordinary shares you own in person at the shareholder meetings.

Proof of ownership of GI Ireland ordinary shares as of the record date, as well as a form of personal photo identification, must be presented to be admitted to the shareholder meetings.

If you hold your GI Ireland ordinary shares in the name of a bank, broker, trustee, custodian or other nominee (which we generally refer to as “brokers” or “nominees”), and you plan to attend the shareholder meetings, you must present proof of your ownership of those shares as of the record date, such as a bank or brokerage account statement or letter from your broker or other nominee, together with a form of personal photo identification, to be admitted to the shareholder meetings. In addition, you may not vote your GI Ireland ordinary shares in person at the shareholder meetings unless you obtain an “instrument of proxy” from the broker or nominee that holds your GI Ireland ordinary shares. You will need to follow the instructions of your broker or nominee in order to obtain such an “instrument of proxy”.

YOUR VOTE IS IMPORTANT. WHETHER OR NOT YOU EXPECT TO ATTEND THE SHAREHOLDER MEETINGS, PLEASE TAKE THE NECESSARY STEPS TO VOTE AT THE MEETING.

IF YOU ARE A REGISTERED SHAREHOLDER, YOU SHOULD MARK, DATE, SIGN AND RETURN BOTH ACCOMPANYING PROXY CARDS (ONE BLUE FOR THE SCHEME MEETING, AND ONE WHITE FOR THE EXTRAORDINARY GENERAL MEETING) IN THE ENCLOSED, POSTAGE-PAID ENVELOPE AS PROMPTLY AS POSSIBLE.

Table of Contents

IN ORDER FOR YOUR PROXIES TO BE VOTED WE MUST RECEIVE YOUR PROXY CARDS AT P.O. BOX 2094, JERSEY CITY, NEW JERSEY 07303-9874, NOT LATER THAN 9:00 A.M. (EASTERN TIME) ON SEPTEMBER 7, 2016 OR AT THE REGISTERED OFFICE OF GI IRELAND, AT 25/28 NORTH WALL QUAY, DUBLIN 1, IRELAND (REF. MJW/JGG), AT LEAST FORTY EIGHT HOURS PRIOR TO THE COMMENCEMENT OF THE RELEVANT MEETING.

IF YOU HOLD YOUR GI IRELAND ORDINARY SHARES IN “STREET NAME” THROUGH A BROKER OR NOMINEE, PLEASE FOLLOW THE VOTING INSTRUCTIONS PROVIDED TO YOU BY SUCH BROKER OR NOMINEE, WHICH MAY INCLUDE AN OPTION TO INSTRUCT THE BROKER OR NOMINEE BY TELEPHONE ON HOW TO VOTE.

PLEASE NOTE THAT HOLDERS OF GI IRELAND ORDINARY SHARES THROUGH A BROKER OR NOMINEE MAY BE REQUIRED TO SUBMIT VOTING INSTRUCTIONS TO THEIR APPLICABLE BROKER OR NOMINEE AT OR PRIOR TO THE DEADLINE APPLICABLE FOR THE SUBMISSION BY GI IRELAND SHAREHOLDERS AND SUCH HOLDERS SHOULD THEREFORE FOLLOW THE SEPARATE INSTRUCTIONS THAT WILL BE PROVIDED BY SUCH NOMINEE.

The accompanying proxy statement incorporates documents by reference. Please see “Where You Can Find More Information” beginning on page 134 of the accompanying proxy statement for a listing of documents incorporated by reference. These documents are available to any person, including any beneficial owner, upon request by contacting us at:

Global Indemnity plc

Investor Relations

25/28 North Wall Quay

Dublin 1, Ireland (ref. MJW/JGG)

Telephone: +353 (0) 49 4891407

Email: info@globalindemnity.ie

To ensure timely delivery of these documents, any request should be made no later than September 7, 2016. The exhibits to these documents will generally not be made available unless such exhibits are specifically incorporated by reference in the accompanying proxy statement.

Table of Contents

| Page | ||||

| 3 | ||||

QUESTIONS AND ANSWERS ABOUT THE TRANSACTION AND THE OTHER PROPOSALS | 6 | |||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 14 | ||||

| 15 | ||||

| 16 | ||||

| 17 | ||||

| 17 | ||||

| 17 | ||||

| 17 | ||||

| 18 | ||||

| 18 | ||||

| 18 | ||||

| 19 | ||||

Proposal Number Five: The Directors’ Allotment Authority Proposal | 19 | |||

Proposal Number Six: The Ireland Reserve Application Proposal | 19 | |||

Proposal Number Seven: The Ireland Memorandum Amendment Proposal | 20 | |||

Proposal Number Eight: The Ireland Articles Amendment Proposal | 20 | |||

| 20 | ||||

| 20 | ||||

| 21 | ||||

| 23 | ||||

| 23 | ||||

| 25 | ||||

| 27 | ||||

| 28 | ||||

| 31 | ||||

| 32 | ||||

| 32 | ||||

| 33 | ||||

| 34 | ||||

| 35 | ||||

| 35 | ||||

| 36 | ||||

| 36 | ||||

| 37 | ||||

| 37 | ||||

| 38 | ||||

| 38 | ||||

| 38 | ||||

| 38 | ||||

Table of Contents

| Page | ||||

| 39 | ||||

| 39 | ||||

Outstanding Debt and Effect on Access to Capital and Credit Markets | 39 | |||

| 39 | ||||

| 39 | ||||

| 40 | ||||

Effect of the Transaction on Potential Future Status as a Foreign Private Issuer | 40 | |||

| 40 | ||||

| 40 | ||||

| 40 | ||||

| 41 | ||||

| 41 | ||||

| 41 | ||||

| 41 | ||||

| 41 | ||||

| 42 | ||||

| 42 | ||||

| 42 | ||||

| 42 | ||||

| 42 | ||||

| 43 | ||||

| 43 | ||||

| 43 | ||||

| 43 | ||||

| 43 | ||||

PROPOSAL NUMBER FIVE: THE DIRECTORS’ ALLOTMENT AUTHORITY PROPOSAL | 44 | |||

| 44 | ||||

| 44 | ||||

| 44 | ||||

| 44 | ||||

PROPOSAL NUMBER SIX: THE IRELAND RESERVE APPLICATION PROPOSAL | 45 | |||

| 45 | ||||

| 45 | ||||

| 45 | ||||

| 45 | ||||

PROPOSAL NUMBER SEVEN: THE IRELAND MEMORANDUM AMENDMENT PROPOSAL | 46 | |||

| 46 | ||||

| 46 | ||||

| 46 | ||||

| 46 | ||||

PROPOSAL NUMBER EIGHT: THE IRELAND ARTICLES AMENDMENT PROPOSAL | 47 | |||

| 47 | ||||

| 47 | ||||

| 47 | ||||

| 47 | ||||

| 49 | ||||

| 49 | ||||

| 59 | ||||

Table of Contents

| Page | ||||

| 59 | ||||

| 60 | ||||

| 65 | ||||

| 65 | ||||

| 65 | ||||

| 65 | ||||

| 66 | ||||

| 67 | ||||

| 67 | ||||

| 67 | ||||

| 67 | ||||

| 68 | ||||

| 68 | ||||

| 69 | ||||

| 69 | ||||

| 70 | ||||

| 70 | ||||

| 70 | ||||

| 71 | ||||

| 71 | ||||

| 71 | ||||

| 71 | ||||

| 71 | ||||

COMPARISON OF RIGHTS OF SHAREHOLDERS AND POWERS OF THE BOARD OF DIRECTORS | 73 | |||

| 118 | ||||

| 118 | ||||

| 118 | ||||

| 119 | ||||

| 119 | ||||

| 119 | ||||

| 120 | ||||

| 122 | ||||

| 122 | ||||

| 123 | ||||

| 124 | ||||

| 127 | ||||

| 129 | ||||

| 130 | ||||

| 131 | ||||

| 132 | ||||

| 133 | ||||

| 134 | ||||

| A-1 | ||||

ANNEX B: FORM OF MEMORANDUM AND ARTICLES OF ASSOCIATION OF GLOBAL INDEMNITY LIMITED | B-1 | |||

| C-1 | ||||

Table of Contents

| Page | ||||

| D-1 | ||||

| E-1 | ||||

ANNEX F: LIST OF RELEVANT TERRITORIES FOR THE PURPOSES OF IRISH DIVIDEND WITHHOLDING TAX | F-1 | |||

| G-1 | ||||

Table of Contents

GLOBAL INDEMNITY PLC

PROXY STATEMENT

For the Special Scheme Meeting and the Extraordinary General Meeting

of the Holders of Global Indemnity plc A Ordinary Shares and B Ordinary Shares

to be held on September 14, 2016

This proxy statement, which also constitutes the “scheme circular” required to be sent to shareholders under Section 452 of the Companies Act 2014 of Ireland, is furnished to the holders of A ordinary shares and B ordinary shares (the “shareholders”) of Global Indemnity plc, a public limited company organized under the laws of Ireland (“GI Ireland”), in connection with the solicitation of proxies on behalf of the board of directors of GI Ireland (the “Board”) to be voted at the special scheme meeting of shareholders (the “scheme meeting”) and the extraordinary general meeting of shareholders (the “extraordinary general meeting”) to be held on September 14, 2016, and any adjournments thereof, at the times and place and for the purposes set forth in the accompanying notices of the scheme meeting and the extraordinary general meeting. We sometimes refer to these meetings together as the “shareholder meetings.” This proxy statement and the accompanying proxy cards (one blue proxy card for the scheme meeting, and one white proxy card for the extraordinary general meeting) are first being sent to shareholders on or about July 18, 2016. Pleasemark, date, sign and return both enclosed proxy cards (one blue for the scheme meeting, and one white for the extraordinary general meeting)to ensure that all of your GI Ireland A ordinary shares, par value $0.0001 per share and B ordinary shares, par value $0.0001 per share (together, the “GI Ireland ordinary shares”), are represented at the shareholder meetings.

GI Ireland ordinary shares represented by valid proxies will be voted in accordance with instructions contained therein or, in the absence of such instructions, “FOR” each of the meeting proposals set forth in this proxy statement. You may revoke your proxy at any time before it is exercised at the shareholder meetings by timely delivery of a properly executed, later-dated proxy with respect to the shareholder meetings to GI Ireland. You may also notify our Secretary in writing before the shareholder meetings that you are revoking your proxy with respect to the shareholder meetings.

GI Ireland has set July 12, 2016 as the record date (the “record date”) for the scheme meeting and for the extraordinary general meeting. This means that only those persons who were holders of GI Ireland ordinary shares at the close of business on July 12, 2016 will be entitled to attend and vote at the shareholder meetings and any adjournments thereof. As of the record date, 13,455,659 GI Ireland A ordinary shares and 4,133,366 GI Ireland B ordinary shares were issued and outstanding.

Only holders of GI Ireland ordinary shares as of the record date are invited to attend the shareholder meetings. For registered shareholders we have enclosed two proxy cards – one blue proxy card for the scheme meeting, and one white proxy card for the extraordinary general meeting. Please complete, sign and return both proxy cards.

Proof of ownership of GI Ireland ordinary shares as of the record date, as well as a form of personal photo identification, must be presented to be admitted to the shareholder meetings.

If you hold your GI Ireland ordinary shares in “street name” beneficially though a bank, broker, trustee, custodian or other nominee (which we generally refer to as “brokers” or “nominees”), you must follow the procedures required by your broker or nominee to appoint or revoke a proxy with respect to the shareholder meetings. You should contact your broker or nominee directly for more information on these procedures.

Table of Contents

In addition, if you wish to attend the special meetings in person and you hold your GI Ireland ordinary shares in “street name” beneficially though either a broker or nominee, you must present proof of your ownership of those shares as of the record date, such as a bank or brokerage account statement or letter from your bank, broker or other nominee, together with a form of personal photo identification, to be admitted to the shareholder meetings. In addition, you may not vote your GI Ireland ordinary shares in person at the shareholder meetings unless you obtain an “instrument of proxy” from the broker or nominee that holds your GI Ireland ordinary shares. You will need to follow the instructions of your broker or nominee in order to obtain such an “instrument of proxy”.

-2-

Table of Contents

In Proposal Number One (the “Scheme of Arrangement Proposal”), we are seeking your approval at the scheme meeting with respect to a scheme of arrangement under Sections 449 to 455 of the Irish Companies Act 2014, substantially in the form attached as Annex A to this proxy statement (the “Scheme of Arrangement”), that, once it becomes effective, will result in you owning ordinary shares of Global Indemnity Limited, a Cayman Islands exempted company (“GI Cayman”), instead of GI Ireland ordinary shares.

In Proposal Number Two (the “EGM Scheme of Arrangement Proposal”), we are seeking your approval at the extraordinary general meeting with respect to the Scheme of Arrangement. This second approval at the extraordinary general meeting is being sought to fulfill a requirement of Irish law.

In Proposal Number Three (the “Capital Reduction Proposal”), we are seeking your approval at the extraordinary general meeting of a capital reduction under Sections 84 and 85 of the Irish Companies Act 2014 in order to effect the cancellation of GI Ireland ordinary shares contemplated by the Scheme of Arrangement.

In Proposal Number Four (the “Share Acquisition Proposal”), we are seeking your approval at the extraordinary general meeting of the terms of the acquisition of a GI Ireland ordinary share by GI Cayman prior to the Scheme of Arrangement, in connection with the Scheme of Arrangement. This is to avoid any doubt on the validity of that acquisition under Irish company law.

In Proposal Number Five (the “Directors’ Allotment Authority Proposal”), we are seeking your approval at the extraordinary general meeting of the authorization of the directors of GI Ireland to allot ordinary shares in GI Ireland to GI Cayman up to an amount equal to the nominal value of the ordinary shares cancelled in connection with the Scheme of Arrangement.

In Proposal Number Six (the “Ireland Reserve Application Proposal”), we are seeking your approval at the extraordinary general meeting of the application by GI Ireland of a reserve credit, arising on its books of account as a result of the cancellation of GI Ireland ordinary shares in connection with the Scheme of Arrangement, to pay up in full at par the GI Ireland ordinary shares allotted to GI Cayman in connection with the Scheme of Arrangement.

In Proposal Number Seven (the “Ireland Memorandum Amendment Proposal”), we are seeking your approval at the extraordinary general meeting of the application by GI Ireland of an amendment to the memorandum of association of GI Ireland to grant GI Ireland a new object enabling it to enter into the Scheme of Arrangement.

In Proposal Number Eight (the “Ireland Articles Amendment Proposal”), we are seeking your approval at the extraordinary general meeting of an amendment to the articles of association of GI Ireland to (1) provide that the allotment or issue of all ordinary shares in GI Ireland on or after the amendment to the articles of association and before 5:00 p.m. (Eastern Standard Time) and 10:00 p.m. (Irish time) on the day before the hearing at which the Scheme of Arrangement is sanctioned (the “Cancellation Record Time”) will be subject to the Scheme of Arrangement; (2) allow GI Cayman to transfer to itself, or to any person on its behalf, any ordinary shares in GI Ireland allotted or issued to any person on or after the Cancellation Record Time, or otherwise issued after the amendment to the articles of association of GI Ireland that are not subject to the Scheme of Arrangement; (3) allow GI Ireland to appoint an attorney to enter into any transfers required in respect of the transfer referred to at (2) above and GI Cayman to appoint an attorney to exercise rights attached to those shares; and (4) disapply rights of pre-emption to ordinary shares in GI Ireland allotted or issued pursuant to the Scheme of Arrangement.

GI Cayman proposes to acquire shares of GI Ireland. If the Scheme of Arrangement becomes effective, (i) all of the existing ordinary shares of GI Ireland will be cancelled, other than the GI Ireland ordinary share

-3-

Table of Contents

held by GI Cayman and for the avoidance of doubt, the Deferred Shares of €1 each in the Capital of GI Ireland (“Deferred Shares”) and any shares in the capital of GI Ireland held as treasury shares within the meaning of Section 106 of the Companies Act 2014 of Ireland (“Treasury Shares”), (ii) GI Ireland will issue shares to GI Cayman equal to the number of shares cancelled pursuant to (i) above using the reserve created by the cancellation of the GI Ireland ordinary shares, and (iv) in return for such issuance of GI Ireland ordinary shares to GI Cayman, GI Cayman will issue A ordinary shares and B ordinary shares of GI Cayman, par value $0.0001 per share (together, the “GI Cayman ordinary shares”), to existing GI Ireland shareholders whose shares were cancelled pursuant to (i) above. As a result of the Scheme of Arrangement, each shareholder of GI Ireland will receive one GI Cayman ordinary share for each GI Ireland ordinary share owned by such shareholder, except GI Cayman which will retain its initial shares in GI Ireland.

Several steps are required in order for us to effect the Scheme of Arrangement, including holding the scheme meeting. We will hold the scheme meeting to approve the Scheme of Arrangement on September 14, 2016. If each of the Scheme of Arrangement Proposal, the EGM Scheme of Arrangement Proposal, the Capital Reduction Proposal, the Directors’ Allotment Authority Proposal, the Ireland Reserve Application Proposal, the Ireland Memorandum Amendment Proposal and the Ireland Articles Amendment Proposal are approved by the shareholders and the other conditions to the Scheme of Arrangement have been satisfied or waived (and we do not abandon the Scheme of Arrangement), we will seek the sanction of the High Court of Ireland (the “Irish High Court”) of the Scheme of Arrangement and the Capital Reduction Proposal at the Sanction Hearing.

If we obtain the requisite approvals from our shareholders and the Irish High Court and if all of the other conditions to the Scheme of Arrangement are satisfied or, if allowed by law, waived, we intend to file the court order authorizing the Scheme of Arrangement with the Irish Companies Registration Office within 21 days. Registration of that order by the Registrar of Companies will cause the Scheme of Arrangement to become effective before the opening of trading of the GI Ireland A ordinary shares on the Nasdaq Global Select Market (“Nasdaq”) on the date of such registration (the “Effective Time”). The Effective Time will depend on factors such as any postponement or adjournment of the Sanction Hearing.

At the Effective Time, the following steps will occur effectively simultaneously in the following order:

| 1. | all of the existing ordinary shares of GI Ireland will be cancelled, other than the GI Ireland ordinary share held by GI Cayman, and for the avoidance of doubt, the Deferred Shares and any Treasury Shares; |

| 2. | GI Ireland will issue shares to GI Cayman equal to the number and categories of shares cancelled pursuant to step 1 above using the reserve created by the cancellation of the GI Ireland ordinary shares; and |

| 3. | in return for such issuance of GI Ireland ordinary shares to GI Cayman, GI Cayman will issue GI Cayman ordinary shares to existing GI Ireland shareholders whose shares were cancelled pursuant to step 1 above. Each shareholder other than GI Cayman will receive one GI Cayman A ordinary share for each GI Ireland A ordinary share held and one GI Cayman B ordinary share for each GI Ireland B ordinary share held. |

As a result of the Scheme of Arrangement, the holders of GI Ireland ordinary shares will become holders of GI Cayman ordinary shares and GI Cayman will own all of the outstanding GI Ireland ordinary shares. The members of the Board then in office will become the members of the Board of Directors of GI Cayman at the Effective Time.

After the Effective Time, you will continue to own an interest in the ultimate holding company of the Global Indemnity group of companies, which will conduct the same business operations through its subsidiaries as are conducted by GI Ireland through its subsidiaries before the Effective Time. The number and classes of GI Cayman ordinary shares you will own will be the same as the number and classes of GI Ireland ordinary shares you owned prior to the Effective Time, and your relative ownership interest in Global Indemnity will remain

-4-

Table of Contents

unchanged other than a non-material concentration of value as the GI Ireland ordinary shares held by GI Cayman will not be cancelled and therefore, no equivalent GI Cayman ordinary shares will be issued.

At July 12, 2016, 13,455,659 GI Ireland A ordinary shares and 4,133,366 GI Ireland B ordinary shares were issued and outstanding.

The transactions contemplated by the Scheme of Arrangement, including the Scheme of Arrangement Proposal, the EGM Scheme of Arrangement Proposal, the Capital Reduction Proposal, the Directors’ Allotment Authority Proposal, the Ireland Reserve Application Proposal, the Ireland Memorandum Amendment Proposal and the Ireland Articles Amendment Proposal and, if approved, the Share Acquisition Proposal, are sometimes referred to herein as the “Transaction.”

If, and only if, the Transaction is consummated, GI Ireland will be liquidated and following the effectiveness of such liquidation, GI Ireland’s direct, wholly owned subsidiary United America Indemnity, Ltd. will become a direct, wholly owned subsidiary of GI Cayman. If the Transaction is consummated, the liquidation of GI Ireland is expected to begin before the end of 2016.

We use the terms “GI,” “we,” “our company,” “the company,” “our” and “us” in this proxy statement to refer to Global Indemnity plc and its subsidiaries prior to the Scheme of Arrangement and to refer to Global Indemnity Limited and its subsidiaries after the Scheme of Arrangement.

-5-

Table of Contents

QUESTIONS AND ANSWERS ABOUT THE TRANSACTION AND THE OTHER PROPOSALS

| 1. | Q: What am I being asked to vote on at the shareholder meetings? |

| A: | Shareholders are being asked to vote on the following matters: |

At the scheme meeting:

| • | To approve the Scheme of Arrangement, pursuant to which: (i) all of the existing ordinary shares of GI Ireland will be cancelled, other than the GI Ireland ordinary share held by GI Cayman, and for the avoidance of doubt the Deferred Shares and any Treasury Shares; (ii) GI Ireland will issue shares to GI Cayman equal to the number of shares cancelled pursuant to (i) above using the reserve created by the cancellation of the GI Ireland ordinary shares; and (iii) in return for such issuance of GI Ireland ordinary shares to GI Cayman, GI Cayman will issue GI Cayman ordinary shares to existing GI Ireland shareholders whose shares were cancelled pursuant to (i) above. Pursuant to the Scheme of Arrangement, each shareholder of GI Ireland will receive one GI Cayman A ordinary share for each GI Ireland A ordinary share owned by such shareholder and will receive one GI Cayman B ordinary share for each GI Ireland B ordinary share held by such shareholder, except GI Cayman which will retain its initial share in GI Ireland. |

At the extraordinary general meeting:

| • | If the Scheme of Arrangement Proposal is approved, to approve the Scheme of Arrangement by and on behalf of GI Ireland. |

| • | If the Scheme of Arrangement Proposal is approved, to approve a reduction of capital of GI Ireland under Sections 84 and 85 of the Irish Companies Act 2014 in order to effect the cancellation of GI Ireland ordinary shares contemplated by the Scheme of Arrangement. |

| • | If the Scheme of Arrangement Proposal is approved, to approve the terms of the acquisition of a GI Ireland ordinary share by GI Cayman, in connection with the Scheme of Arrangement. This is to avoid any doubt on the validity of that acquisition under Irish company law. |

| • | If the Scheme of Arrangement Proposal is approved, to approve the authorization of the directors of GI Ireland to allot ordinary shares in GI Ireland to GI Cayman up to an amount equal to the nominal value of the ordinary shares cancelled in connection with the Scheme of Arrangement. |

| • | If the Scheme of Arrangement Proposal is approved, to approve the application by GI Ireland of a reserve credit, arising on its books of account as a result of the cancellation of ordinary shares in connection with the Scheme of Arrangement, to pay up in full at par the ordinary shares allotted to GI Cayman in connection with the Scheme of Arrangement. |

| • | If the Scheme of Arrangement Proposal is approved, to approve an amendment to the memorandum of association of GI Ireland to grant GI Ireland a new object enabling it to enter into the Scheme of Arrangement. |

| • | If the Scheme of Arrangement Proposal is approved, to approve an amendment to the articles of association of GI Ireland to (i) provide that the allotment or issue of all ordinary shares in GI Ireland on or after the amendment to the articles of association and before the Cancellation Record Time will be subject to the Scheme of Arrangement; (ii) allow GI Cayman to transfer to itself, or to any person on its behalf, any ordinary shares in GI Ireland allotted or issued to any person on or after the Cancellation Record Time, or otherwise issued after the amendment to the articles of association of GI Ireland that are not subject to the Scheme of Arrangement; (iii) allow GI Ireland to appoint an attorney to enter into any transfers required in respect of the transfer referred to at (ii) above and GI Cayman to appoint an attorney to exercise the rights attached to those shares; and (iv) disapply rights of pre-emption to ordinary shares in GI Ireland allotted or issued pursuant to the Scheme of Arrangement. |

-6-

Table of Contents

At both of the shareholder meetings:

| • | To approve motions to adjourn each meeting to a later date to solicit additional proxies, in the discretion of the chairman of the meeting, if there are insufficient proxies to approve the meeting proposals at the time of each applicable shareholder meeting. |

We refer to such proposals as the “Adjournment Proposals”. The proposals contemplated by this proxy statement, including the Scheme of Arrangement Proposal, the EGM Scheme of Arrangement Proposal, the Capital Reduction Proposal, the Share Acquisition Proposal, the Directors’ Allotment Authority Proposal, the Ireland Reserve Application Proposal, the Ireland Memorandum Amendment Proposal, the Ireland Articles Amendment Proposal, and the Adjournment Proposals, are sometimes referred to herein as the “meeting proposals”.

Please see “Proposal Number One: The Scheme of Arrangement Proposal”, “Proposal Number Two: The EGM Scheme of Arrangement Proposal”, “Proposal Number Three: The Capital Reduction Proposal”, “Proposal Number Four: The Share Acquisition Proposal”, “Proposal Number Five: The Directors’ Allotment Authority Proposal”, “Proposal Number Six: The Ireland Reserve Application Proposal”, “Proposal Number Seven: The Ireland Memorandum Amendment Proposal”, and “Proposal Number Eight: The Ireland Articles Amendment Proposal.”

| 2. | Q: Why is Global Indemnity proposing the Scheme of Arrangement and related transactions? |

| A: | The Board determined that replacing the current holding company of the Global Indemnity group of companies with a company incorporated in Cayman would be in the interests of GI Ireland and its shareholders for, among others, the following reasons: |

| • | The Cayman Islands has a business friendly regulatory environment and a predictable legal framework that simultaneously provides both corporate certainty and shareholder protections; |

| • | GI Ireland evaluated the reasons for leaving the Cayman Islands in 2010 and determined that developments in the laws and business environments in the Cayman Islands no longer present the same risks as may have been the case prior to 2010; |

| • | The Cayman Islands presents a flexible and stable legal and corporate governance framework, which allows a company’s board of directors latitude to exercise its judgment in what it deems to be in the best interests of the company, particularly with respect to extraordinary transactions; |

| • | The Cayman Islands is a leading international financial center, attracts a high volume of non-resident financial activity from the United States, Europe and other countries with substantial capital to invest and is a significant hub for institutional investment; |

| • | The Cayman Islands has an impeccable reputation for economic and political stability and compliance with international standards; |

| • | The Cayman Islands offers a beneficial tax regime: it is a tax-neutral jurisdiction that has no system of direct corporate taxation, and, like Irish law, permits dividends to be paid in U.S. dollars and upon the approval of the Board without the need for shareholder approval; |

| • | The Cayman Islands, like Ireland, is a common law jurisdiction. In addition, both jurisdictions are subject to companies acts that have their source in English companies law. Therefore, despite certain differences between the two corporate legal systems, we believe that the rights of GI Ireland shareholders and GI Cayman shareholders will be substantially similar; |

| • | The Cayman Islands has an Aa3 sovereign risk rating due to its prudent economic policies and a strong financial services sector; and |

| • | The Cayman Islands is a British overseas territory and has a history of stable government. |

Please see “Proposal Number One: The Scheme of Arrangement Proposal—Reasons for the Transaction.”

-7-

Table of Contents

| 3. | Q: How does the Board of Directors recommend that I vote? |

| A: | Our Board unanimously recommends that our shareholders vote “FOR” each of the meeting proposals set forth in this proxy statement. |

| 4. | Q: Who can vote at the shareholder meetings? |

| A: | All persons who were registered holders of GI Ireland ordinary shares at the close of business on July 12, 2016, the record date for the shareholder meetings, are shareholders of record for the purposes of the shareholder meetings and will be entitled to attend and vote, in person or by proxy, at the shareholder meetings and any adjournments thereof. At the scheme meeting, each shareholder of record will be entitled to one vote per GI Ireland A ordinary share and B ordinary share held by such shareholder. At the extraordinary general meeting, shareholders of record who hold GI Ireland A ordinary shares shall be entitled to one vote per GI Ireland A ordinary share held and shareholders of record who hold GI Ireland B ordinary shares shall be entitled to ten votes per GI Ireland B ordinary share held. |

If you hold your GI Ireland ordinary shares in “street name” beneficially though a broker or nominee, you must follow the procedures required by your broker or nominee to appoint or revoke a proxy with respect to the shareholder meetings. You should contact your broker or nominee directly for more information on these procedures.

Please see “The Shareholder Meetings—Record Date; Voting Rights.”

| 5. | Q: How do I vote if I am a registered shareholder? |

| A: | You may vote your GI Ireland ordinary shares either by voting in person at the shareholder meetings or by submitting a completed proxy. We have enclosed two proxy cards (one blue proxy card for the scheme meeting, and one white proxy card for the extraordinary general meeting). By submitting your proxy, you are legally authorizing another person to vote your GI Ireland ordinary shares by proxy in accordance with your instructions. You may appoint any person as your proxy and it is not a requirement that this person be a shareholder of GI Ireland. The enclosed proxy card designates Stephen W. Ries or, failing him, Thomas M. McGeehan to vote your GI Ireland ordinary shares in accordance with the voting instructions you indicate in your proxy at each of the shareholder meetings. If you wish to appoint another person as your proxy, you can strike out the name of Stephen W. Ries or Thomas M. McGeehan and replace it with the name of such other person. |

In addition, if any other matters (other than the meeting proposals contained in this proxy statement) properly come before either of the shareholder meetings or any adjournments of those meetings, the persons named in the proxy card will have the authority to vote your GI Ireland ordinary shares on those matters in their discretion. The Board currently does not know of any matters to be raised at the shareholder meetings other than the meeting proposals contained in this proxy statement.

You may submit your proxy either by mail, courier or hand delivery. Please let us know whether you plan to attend each of the shareholder meetings by marking the appropriate box on your proxy card. In order for your proxy to be validly submitted and for your GI Ireland ordinary shares to be voted in accordance with your proxy, Georgeson LLC must receive your mailed proxy at P.O. Box2094, Jersey City, New Jersey 07303-9874, not later than 9:00 a.m. (Eastern time) on September 7, 2016, or you may send it to our registered office, at 25/28 North Wall Quay, Dublin 1, Ireland (ref. MJW/JGG) where it must be received at least forty eight hours prior to the commencement of the relevant meeting.

If you do not wish to vote all of your GI Ireland ordinary shares in the same manner on any particular proposal(s), you may specify your vote by clearly hand-marking the proxy card to indicate how you want to vote your GI Ireland ordinary shares.

If you do not specify on the enclosed proxy cards that are submitted how you want to vote your GI Ireland ordinary shares, the proxy holders will vote such unspecified shares “FOR” each of the meeting proposals set forth in this proxy statement.

-8-

Table of Contents

Please see “The Shareholder Meetings—Proxies” and “The Shareholder Meetings—How You Can Vote.”

| 6. | Q: How can I vote if I hold my shares in “street name”? |

| A: | Shareholders who hold their shares in “street name” beneficially though a broker or nominee must vote their GI Ireland ordinary shares by following the procedures established by their broker or nominee. |

Under Nasdaq Rule 2251, absent instructions, brokers and nominees who hold GI Ireland ordinary shares on behalf of customers will not have the authority to vote on any of the matters to be considered at the shareholder meetings, other than the Adjournment Proposals. If you do not instruct your broker or nominee on how to vote your GI Ireland ordinary shares prior to the shareholder meetings, your GI Ireland ordinary shares will not be voted at the shareholder meetings and such GI Ireland ordinary shares will not be considered when determining whether any applicable proposal has received the required approval. However, if your broker or nominee attends or appoints a proxy to attend a meeting, they will be counted as present in person or by proxy for purposes of the relevant quorum requirement.

If you hold GI Ireland ordinary shares through a broker or nominee, we recommend that you contact your broker or nominee directly for more information on the procedures by which your GI Ireland ordinary shares can be voted. Your broker or nominee will not be able to vote your GI Ireland ordinary shares unless it receives appropriate instructions from you.

In addition, you may not vote your GI Ireland ordinary shares in person at the shareholder meetings unless you obtain an “instrument of proxy” from your broker or nominee that holds your GI Ireland ordinary shares. You will need to follow the instructions of your broker or nominee in order to obtain such an “instrument of proxy.”

Please see “The Shareholder Meetings—How You Can Vote.” Please also see “The Shareholder Meetings—Votes of Shareholders Required for Approval” for further information on how shares held in the “street name” of a broker will be considered for purposes of the “majority in number” approval requirement.

| 7. | Q: What vote of GI Ireland shareholders is required to approve the meeting proposals? |

| A: | The Scheme of Arrangement Proposal requires approval by the affirmative vote of (i) a majority in number of the registered holders of GI Ireland ordinary shares attending the scheme meeting, in person or by proxy and (ii) not less than 75% of the GI Ireland ordinary shares voted at the scheme meeting, in person or by proxy. |

The EGM Scheme of Arrangement Proposal requires the affirmative vote of not less than 75% of the votes cast in respect of all GI Ireland ordinary shares voted, at the extraordinary general meeting, in person or by proxy. Approval of the EGM Scheme of Arrangement Proposal by our shareholders is a condition to the effectiveness of the Scheme of Arrangement.

The Capital Reduction Proposal requires the affirmative vote of not less than 75% of the votes cast in respect of all GI Ireland ordinary shares voted, at the extraordinary general meeting, in person or by proxy. Approval of the Capital Reduction Proposal by our shareholders is a condition to the effectiveness of the Scheme of Arrangement.

The Share Acquisition Proposal requires the affirmative vote of not less than 75% of the votes cast in respect of all GI Ireland ordinary shares voted, at the extraordinary general meeting, in person or by proxy.

The Directors’ Allotment Authority Proposal requires the affirmative vote of more than 50% of the votes cast in respect of all GI Ireland ordinary shares voted at the extraordinary general meeting, in person or by proxy. Approval of the Directors’ Allotment Authority Proposal by our shareholders is a condition to the effectiveness of the Scheme of Arrangement.

-9-

Table of Contents

The Ireland Reserve Application Proposal requires the affirmative vote of more than 50% of the votes cast in respect of all GI Ireland ordinary shares voted at the extraordinary general meeting, in person or by proxy. Approval of the Ireland Reserve Application Proposal by our shareholders is a condition to the effectiveness of the Scheme of Arrangement.

The Ireland Memorandum Amendment Proposal requires the affirmative vote of not less than 75% of the votes cast in respect of all GI Ireland ordinary shares voted at the extraordinary general meeting, in person or by proxy. Approval of the Ireland Memorandum Amendment Proposal by our shareholders is a condition to the effectiveness of the Scheme of Arrangement.

The Ireland Articles Amendment Proposal requires the affirmative vote of not less than 75% of the votes cast in respect of all GI Ireland ordinary shares voted at the extraordinary general meeting, in person or by proxy. Approval of the Ireland Articles Amendment Proposal by our shareholders is a condition to the effectiveness of the Scheme of Arrangement.

The Adjournment Proposals require the affirmative vote of GI Ireland’s ordinary shares representing more than 50% of the votes cast in respect of all GI Ireland ordinary shares voted, in person or by proxy, at the relevant meeting.

At the scheme meeting, each shareholder of record will be entitled to one vote per GI Ireland A ordinary share and B ordinary share held by such shareholder. At the extraordinary general meeting, shareholders of record who hold GI Ireland A ordinary shares shall be entitled to one vote per GI Ireland A ordinary share held and shareholders of record who hold GI Ireland B ordinary shares shall be entitled to ten votes per GI Ireland B ordinary share held.

Please see “The Shareholder Meetings—Votes of Shareholders Required for Approval.”

| 8. | Q: What quorum is required for action at the shareholder meetings? |

| A: | At the scheme meeting to approve the Scheme of Arrangement Proposal, one or more shareholders holding GI Ireland ordinary shares having at least a majority of the votes eligible to be cast at the meeting, must be present in person or by proxy. |

At the extraordinary general meeting, one or more shareholders holding GI ordinary shares having at least a majority of the votes eligible to be cast at the meeting, must be present in person or by proxy.

An adjournment of either meeting can be approved by a quorum of at least one shareholder holding shares having a majority of votes eligible to be cast at that meeting.

For purposes of determining a quorum, abstentions and broker non-votes present in person or by proxy are counted as represented.

At the record date there were 13,455,659 A ordinary shares and 4,133,366 B ordinary shares issued and outstanding.

Please see “The Shareholder Meetings—Quorum.”

| 9. | Q: When do you expect the Transaction to be consummated? |

| A: | We currently expect to complete the Scheme of Arrangement, if approved and sanctioned, in the fourth quarter of 2016. The Transaction may be delayed or abandoned by the Board for any reason prior to obtaining the sanction of the Irish High Court, even if the Transaction has been approved by the requisite vote of the GI Ireland shareholders. The Board may determine not to proceed with the Transaction for any reason. |

Please see “Proposal Number One: The Scheme of Arrangement Proposal—Effective Time of the Transaction” and “Proposal Number One: The Scheme of Arrangement Proposal—Amendment, Termination or Delay.”

-10-

Table of Contents

| 10. | Q: If all required approvals are obtained and conditions are satisfied or waived, is the Transaction required to be consummated? |

| A: | The Transaction may be delayed or abandoned by the Board for any reason prior to obtaining the sanction of the Irish High Court, even if the Transaction has been approved by the requisite vote of the GI Ireland shareholders. However, the Board will not have any statutory discretion under Irish law to refuse to consummate the Scheme of Arrangement if the Scheme of Arrangement is sanctioned by the Irish High Court. |

Please see “Proposal Number One: The Scheme of Arrangement Proposal—Amendment, Termination or Delay.”

| 11. | Q: Will the Transaction affect Global Indemnity’s future operations? |

| A: | We believe that the Transaction and the contemplated liquidation of GI Ireland will have no material impact on how we conduct our day-to-day operations. The location of our future operations will depend on the needs of our business, independent of our legal domicile. |

| 12. | Q: Will the Transaction dilute my economic interest? |

| A: | No, your relative economic ownership in Global Indemnity will not be diluted. |

| 13. | Q: How will the Transaction affect Global Indemnity’s financial reporting and the information Global Indemnity provides to its shareholders? |

| A: | Upon completion of the Transaction, we will remain subject to the U.S. Securities and Exchange Commission (the “SEC”) reporting requirements, the mandates of the Sarbanes-Oxley Act and the applicable corporate governance rules of Nasdaq, and we will continue to report our consolidated financial results in U.S. dollars and in accordance with U.S. generally accepted accounting principles (“U.S. GAAP”). We will continue to file reports on Forms10-K,10-Q and 8-K with the SEC, as we currently do. We will no longer be required to provide you with our Irish Statutory Accounts prepared in accordance with Irish law, but we will in the ordinary course provide you with customary financial information in accordance with our established historical practices. |

| 14. | Q: How will GI Cayman ordinary shares differ from GI Ireland ordinary shares? |

| A: | GI Cayman ordinary shares will be similar to your existing GI Ireland ordinary shares. However, there are differences between what your rights as a shareholder will be under Cayman law and what they currently are as a shareholder under Irish law. In addition, there are differences between the organizational documents of GI Cayman and GI Ireland. |

We discuss these and other differences in detail under “Description of Global Indemnity Limited Share Capital” and “Comparison of Rights of Shareholders and Powers of the Board of Directors.” GI Cayman’s memorandum and articles of association will be substantially in the form attached to this proxy statement as Annex B.

| 15. | Q: What are the material tax consequences of the Transaction? |

| A: | The Transaction should not be a taxable transaction for GI Ireland or GI Cayman for either Irish, Cayman or U.S. federal income tax purposes. Further, under U.S. federal income tax law, holders of GI Ireland ordinary shares generally will not recognize gain or loss in the Transaction. |

For Irish tax law purposes, holders of GI Ireland ordinary shares who are neither resident nor ordinarily resident in Ireland and who do not have some connection with Ireland other than holding GI Ireland

-11-

Table of Contents

ordinary shares should not be within the charge to Irish capital gains tax or corporation tax on chargeable gains on the cancellation of their GI Ireland ordinary shares in connection with the Scheme of Arrangement.

For a discussion of certain material U.S. federal, Cayman, and Irish tax consequences of the Transaction to Global Indemnity’s shareholders and Global Indemnity, please see “Summary—Proposal Number One: The Scheme of Arrangement Proposal—Tax Considerations of the Transaction” and “Material Tax Considerations Relating to the Transaction.” All holders of GI Ireland ordinary shares should consult their own tax advisors regarding the particular tax consequences of the Transaction and the ownership and disposition of the GI Cayman ordinary shares to them in light of their particular situations.

| 16. | Q: If the Scheme of Arrangement is approved and consummated, do I have to take any action to participate in the Scheme of Arrangement? |

| A: | Not if your GI Ireland ordinary shares are held in book-entry form or by your broker. GI Ireland ordinary shares so held will automatically be cancelled at the Effective Time and, as part of the Scheme of Arrangement, new GI Cayman ordinary shares will be issued to you or your broker without any action on your part. Please see “Proposal Number One: The Scheme of Arrangement Proposal—Cancellation and Issuance of Shares.” If you hold your GI Ireland ordinary shares in certificated form, please see the next question. |

| 17. | Q: What happens if I hold share certificates? |

| A: | If you hold your GI Ireland ordinary shares in certificated form, and the Scheme of Arrangement is consummated, your GI Ireland ordinary shares will automatically be cancelled at the Effective Time and cease to be valid and your ownership of GI Cayman ordinary shares will be evidenced through an electronic book-entry in your name on GI Cayman’s shareholder records. Upon completion of the Transaction, our transfer agent will mail you a letter of transmittal for you to complete and return along with your old certificates and, once returned and validated, will send to you a statement documenting your ownership of GI Cayman ordinary shares in registered form.You should not return your GI Ireland ordinary share certificates with the enclosed proxy cards. |

Please see “Proposal Number One: The Scheme of Arrangement Proposal—Cancellation and Issuance of Shares.” Please also see “Summary—Proposal Number One: The Scheme of Arrangement Proposal—Tax Considerations of the Transaction” and “Material Tax Considerations Relating to the Transaction—Cayman Tax Considerations” for further information.

| 18. | Q: May I revoke my proxy? |

| A: | Any proxy is revocable. |

| • | If you hold your GI Ireland ordinary shares in “street name” beneficially though a broker or nominee, you must follow the procedures required by your broker or nominee to revoke your proxy or change your vote. You should contact your broker or nominee if you have any questions with respect to these procedures. |

| • | For registered holders of GI Ireland ordinary shares: |

| • | After you have submitted a proxy, you may revoke it by mail, courier, or hand delivery before the shareholder meetings by sending a written notice to our Secretary at Global Indemnity plc, 25/28 North Wall Quay, Dublin 1, Ireland (Reference: MJW/JGG) or at our administrative headquarters. Your written notice must be received at least one hour (and, in the case of revocation by electronic means, at least twenty four hours) prior to the start of the applicable shareholder meeting. |

-12-

Table of Contents

| • | If you wish to revoke your submitted proxy and submit new voting instructions by mail, courier or hand delivery, then you must sign, date and mail, courier or hand-deliver a proxy card with your new voting instructions for the shareholder meetings, which we must receive at either of the locations specified above at least one hour (and, in the case of revocation by electronic means, at least twenty four hours) prior to the start of the applicable shareholder meeting. |

| • | You also may revoke your proxy in person by completing a written ballot (but only if you are the registered owner of the GI Ireland ordinary shares as of the record date or if you obtain a “form of proxy” from the registered owner of the GI Ireland ordinary shares as of the record date) and vote your GI Ireland ordinary shares at the shareholder meetings. |

| • | Attending the shareholder meetings without taking one of the actions above will not revoke your proxy. |

Please see “The Shareholder Meetings—Revoking Your Proxy.”

| 19. | Q: How do I attend the shareholder meetings? |

| A: | All holders of GI Ireland ordinary shares as of the record date are invited to attend the scheme meeting at Global Indemnity’s registered office, located at 25/28 North Wall Quay, Dublin 1, Ireland, which will commence at 10:00 a.m., local time, on September 14, 2016. All holders of GI Ireland ordinary shares are also invited to attend the extraordinary general meeting at Global Indemnity’s registered office, which will commence at 10:15 a.m., local time, on September 14, 2016 (or as soon thereafter as the scheme meeting concludes or is adjourned). Proof of ownership of GI Ireland ordinary shares as of the record date, as well as a form of personal photo identification, must be presented to be admitted to either of the shareholder meetings. |

If you are not a registered holder of GI Ireland ordinary shares – in other words, if you hold GI Ireland ordinary shares in “street name” through a broker or nominee– then your name will not appear in GI Ireland’s register of shareholders. In such circumstances, GI Ireland ordinary shares are held in your broker’s name or the name of the nominee through which your broker holds the shares, on your behalf, and your broker or nominee will be entitled to vote your GI Ireland ordinary shares in accordance with your instructions. To attend the shareholder meetings, you must present proof of your ownership of your shares as of the record date, such as a bank or brokerage account statement or letter from your bank, broker or other nominee, together with a form of personal photo identification, to be admitted to the shareholder meetings. Note that, if you are not a registered holder of your GI Ireland ordinary shares, even if you attend the shareholder meetings, you cannot vote the GI Ireland ordinary shares that are held by your broker or nominee unless you obtain an “instrument of proxy” from the broker or nominee that holds your GI Ireland ordinary shares. You will need to follow the procedures required by your broker or nominee in order to obtain such an “instrument of proxy.” You should contact your broker or nominee if you have any questions with respect to these procedures.

Please see “The Shareholder Meetings—How You Can Vote”.

| 20. | Q: Whom should I call if I have questions about the shareholder meetings or the meeting proposals in this proxy statement? |

| A: | You should contact our proxy solicitor: |

Georgeson LLC

480 Washington Blvd., 26th Floor

Jersey City, NJ 07310

Toll-free within the United States: (866) 767-8989

Outside the United States: (781) 575-2137

-13-

Table of Contents

This summary highlights selected information from this proxy statement. It does not contain all of the information that is important to you. To understand the Transaction and the meeting proposals more fully, and for a more complete legal description of the Transaction, you should read carefully the entire proxy statement, including the Annexes. The Scheme of Arrangement, substantially in the form attached as Annex A to this proxy statement, is the legal document that governs the Transaction. The memorandum and articles of association of GI Cayman, substantially in the form attached to this proxy statement as Annex B, will govern GI Cayman after the completion of the Scheme of Arrangement.

Proposal Number One: The Scheme of Arrangement Proposal

Global Indemnity plc. Global Indemnity plc (which we refer to as “GI Ireland”), one of the leading specialty property and casualty insurers and reinsurers in the industry, provides its insurance products across a distribution network that includes binding authority, program, brokerage, and reinsurance. The registered office of GI Ireland is located at 25/28 North Wall Quay, Dublin 1, Ireland, and Global Indemnity plc’s telephone number is +353 (0) 49 4891407.

Global Indemnity Limited. Global Indemnity Limited (which we refer to as “GI Cayman”), was formed in February 2016. If the Scheme of Arrangement is consummated, GI Cayman will become the ultimate holding company of the Global Indemnity group of companies. Prior to the Transaction, GI Cayman will not engage in any business or other activities other than in connection with the Transaction. Following the Effective Time, the holders of GI Ireland ordinary shares will own GI Cayman ordinary shares. The registered office of GI Cayman will be located at Walkers Corporate Limited, Cayman Corporate Centre, 27 Hospital Road, George Town, Grand Cayman KY1-9008, Cayman Islands and GI Cayman’s telephone number will be +1345 814 7600.

Prior to the Scheme of Arrangement, GI Cayman, will acquire a GI Ireland ordinary share. If the Scheme of Arrangement becomes effective, (i) all of the existing ordinary shares of GI Ireland will be cancelled, other than the GI Ireland ordinary share held by GI Cayman, and for the avoidance of doubt, the Deferred Shares and any Treasury Shares, (ii) GI Ireland will issue shares to GI Cayman equal to the number of shares cancelled pursuant to (i) above using the reserve created by the cancellation of the GI Ireland ordinary shares, and (iii) in return for such issuance of GI Ireland ordinary shares to GI Cayman, GI Cayman will issue GI Cayman ordinary shares to existing GI Ireland shareholders whose shares were cancelled pursuant to (i) above. As a result of the Scheme of Arrangement, each shareholder of GI Ireland will receive one GI Cayman A ordinary share for each GI Ireland A ordinary share owned by such shareholder and one GI Cayman B ordinary share for each GI Ireland B ordinary share held by such shareholder, except GI Cayman which will retain its initial shares in GI Ireland.

Several steps are required in order for us to effect the Scheme of Arrangement, including holding the scheme meeting. The scheme meeting is being convened at the direction of the Board. We will hold the scheme meeting to approve the Scheme of Arrangement on September 14, 2016. If each of the Scheme of Arrangement Proposal, the EGM Scheme of Arrangement Proposal, the Capital Reduction Proposal, the Directors’ Allotment Authority Proposal, the Ireland Reserve Application Proposal, the Ireland Memorandum Amendment Proposal and the Ireland Articles Amendment Proposal are approved by the shareholders and the other conditions to the Scheme of Arrangement have been satisfied or waived (and we do not abandon the Scheme of Arrangement), we will seek the Irish High Court’s sanction of the Scheme of Arrangement and the Capital Reduction Proposal.