Exhibit 99.3

izea company overview

1

Confidential All persons who receive this Confidential Company Overview agree that they will hold the contents of this Company Overview and all enclosures and related documents in the strictest confidence. Recipients of this Company Overview agree that they will not copy, reproduce or distribute to others this Company Overview or enclosures or related documents in whole or in part, or utilize the contents hereof or thereof for any purpose other than to evaluate the transaction described herein, and will return this Company Overview and any enclosures and related documents promptly at the request of the undersigned. To the extent the Overview is delivered in hard copy form, the recipient agrees by accepting receipt of same to return the Overview promptly if such recipient determines not to purchase any securities or if otherwise requested to do so by the Company.

2

DISCLAIMER This presentation is for discussion purposes only. All timelines, prices and rates referenced herein are indicative and subject to market conditions. The material is based upon information that we consider reliable, but we do not represent that it is accurate or complete, and it should not be relied upon as such. This presentation may contain forward-looking statements that are based on current expectations and assumptions that are subject to risks and uncertainties. In some cases, you can identify these statements by forward-looking words such as “may”, “might”, “will”, “should”, “expect”, “plan”, “anticipate”, “believe”, “estimate”, “predict”, “optimistic”, “potential”, “future” or “continue”, the negative of these terms and other comparable terminology. All of such assumptions are inherently subject to significant economic and competitive uncertainties and contingencies beyond our control and upon assumptions with respect to the future business decisions which are subject to change. Accordingly, there can be no assurance that actual results will meet expectations and actual results could differ materially because of factors such as: • Execution and competitive risks IZEA's ability to attract and retain clients IZEA's ability to successfully implement its current long-term growth strategy Delays in website & application development as well as technical issues and server issues beyond IZEA's control Reliance on the third-party platforms on which IZEA builds its applications, which platforms and access to the functionality thereof are controlled solely by such third parties. Improper collection and disclosure of personal data could result in liability and harm to IZEA's reputation Risks inherent in IZEA's business as well as potential legal disputes arising from IZEA's operations IZEA, Inc.’s (“IZEA” or “Company”) actual results, performance and achievements may differ materially from any future results, performance, or achievements expressed or implied by such forward-looking statements. We do not assume responsibility for the accuracy or completeness of any forward-looking statement and you should not rely on forward-looking statements as predictions of future events. We are under no duty to update any of these forward-looking statements to conform them to actual results or revised expectations.

3

izea snapshot Focus Operates multiple marketplaces that facilitate transactions between social media publishers and online advertisers Leader in “Social Media Sponsorships”1 Founded 2006 in Orlando, Florida Employees 30 full time employees On-line Properties Five different online marketplaces including: SocialSpark.com, SponsoredTweets.com, WeReward.com, PayPerPost.com, InPostLinks.com Customers Wide range of small businesses, large businesses and agencies a Has executed campaigns for Fortune 500 brands Network Reach 500,000+ registered social media creators and 50,000+ registered advertisers on IZEA platforms Company has completed nearly 1.5 million social media sponsorship transactions Business Model Business Model Scalable transaction-based model on robust software platforms Financial Profile Strong revenue potential with attractive 52% gross margin on transactions $3.8M in revenues in 2010. 37% Y/Y growth from 2009 Currently burning $175k per month, devoting spend to new mobile platform WeReward

4

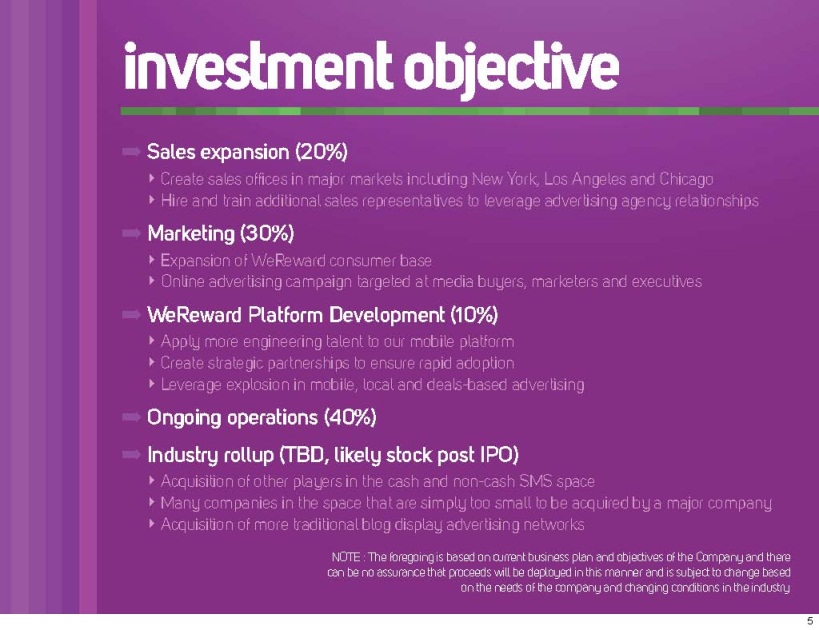

investment objective Sales expansion (20%) Create sales offices in major markets including New York, Los Angeles and Chicago Hire and train additional sales representatives to leverage advertising agency relationships Marketing (30%) Expansion of WeReward consumer base Online advertising campaign targeted at media buyers, marketers and executives WeReward Platform Development (10%) Apply more engineering talent to our mobile platform Create strategic partnerships to ensure rapid adoption Leverage explosion in mobile, local and deals-based advertising Ongoing operations (40%) Industry rollup (TBD, likely stock post IPO) Acquisition of other players in the cash and non-cash SMS space Many companies in the space that are simply too small to be acquired by a major company Acquisition of more traditional blog display advertising networks NOTE : The foregoing is based on current business plan and objectives of the Company and there can be no assurance that proceeds will be deployed in this manner and is subject to change based

5

financial overview 2008 Audited 2009 Audited 2010 Unaudited Preliminary Numbers in Millions Bookings (Unaudited) $ 3.8 $ 3.3 $ 4.1 Revenue $ 3.8 $ 2.8 $ 3.7

COS $ 2.6 $ 1.3 $ 1.8 Gross Profit $ 1.1 $ 1.4 $ 1.9 31% 52% 52% OPEX $ 5.4 $ 3.7 $ 4.0 EBITDA $ (4.2) $ (2.2) $ (2.1) EBITDA - (earnings before interest, taxes, depreciation and amortization) is calculated by subtracting total expenses, including cost of sales and operating expenses with the exception of interest, taxes, depreciation and amortization from total income. 2010 results are internally prepared and unaudited. Final audited numbers may differ from results presented.from results presented.

6

balance sheet 2008 Audited 2009 Audited 2010 Unaudited Preliminary Numbers in Millions Cash and cash equivalents $ 1.9 $ 0.5 $ 1.5 Accounts receivable $ 0.2 $ 0.3 $ 0.5 Other assets $ 0.6 $ 0.2 $ 0.2 Total assets $ 2.6 $ 1.0 $ 2.2 Accounts payable and accrued expenses $ 0.3 $ 0.5 $ 0.7 Unearned revenue * $ 0.8 $ 1.1 $ 1.2 Notes payable $ 1.0 $ 0.7 $ 0.3 Convertible notes payable - $ 0.8 - Total liabilities $ 2.0 $ 3.1 $ 2.2 Stockholders equity $ 0.6 $ (2.0) $ 0.0 * Unearned revenue is defined as deposits made to IZEA from advertisers in the form of cash or credit to be used in future campaigns. Cash deposits are non-refundable after 30 days.

7

company

8

investment highlights IZEA is a first mover and pioneer in a rapidly growing market IZEA founder Ted Murphy pioneered the cash Social Media Sponsorship (SMS) space 1 IZEA had a 28% market share of world wide cash SMS spending in 2010 1 SMS is increasingly seen as a powerful marketing tool by advertisers Total SMS spending is projected to rise at a 28.5% CAGR during the 2009-2014 period, reaching $161.2 million in 2014 1 Multiple social media marketing marketplaces, diversified income Five distinct online marketplaces connecting advertisers and social media publishers Superior aggregation capabilities enable efficient clearing with higher margins 500k+ registered social media publishers, 50k+ registered advertisers on IZEA platforms Platform delivers measurable ROI to advertisers Reports traffic and conversions delivered to a client’s destination site Advertisers can use CPC, CPA or Cost Per Post (CPP) options based on their target ROI Revenue focused management team with scalable business model Low incremental costs as network, transactions and revenue increase High margins allow for attractive partnership opportunities (1) SOURCE : PQ MEDIA Social Media Sponsorships Forecast 2010-2014

9

WHAT WE DO We pay bloggers, tweeters and other social media publishers to create and distribute advertiser content through their social networks. This is called a Social Media Sponsorship or SMS. We execute campaigns through our marketplaces. Think of us like an eBay that brings together buyers and sellers. Our buyers are advertisers. Our sellers are anyone who publishes social media content.

10

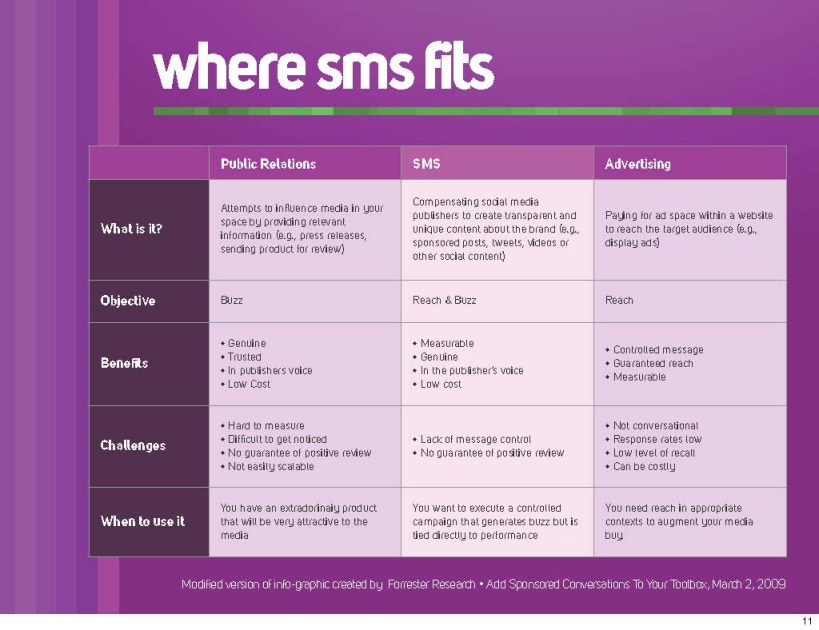

where sms fits Public Relations SMS Advertising What is it? Attempts to influence media in your space by providing relevant information (e.g., press releases, sending product for review) Compensating social media publishers to create transparent and unique content about the brand (e.g., sponsored posts, tweets, videos or other social content) Paying for ad space within a website to reach the target audience (e.g., display ads) Objective Buzz Reach & Buzz Reach Benefits Genuine Trusted In publishers voice Low Cost Measurable Genuine In the publisher’s voice Low cost Controlled message Guaranteed reach Measurable Challenges Hard to measure Difficult to get noticed No guarantee of positive review Not easily scalable Lack of message control No guarantee of positive review Not conversational Response rates low Low level of recall Can be costly When to use it You have an extradorinaiy product that will be very attractive to the media You want to execute a controlled campaign that generates buzz but is tied directly to performance You need reach in appropriate contexts to augment your media buy. Modified version of info-graphic created by Forrester Research • Add Sponsored Conversations To Your Toolbox, March 2, 2009

11

integrated sms campaigns IZEA Platforms Advertisers Publishers Distribution Mobile Platforms

12

sample blog post

13

leveraging the long tail Publishers Following @kimkardashian TV Star @chrispirillo Web Celeb @pensieverobin Mother Our network includes celebrities like Kim Kardashian, Diddy and Bob Villa, along with hundreds of thousands of everyday people and professional publishers. WE CONNECT OUR PUBLISHERS WITH GREAT BRANDS AT SCALE

14

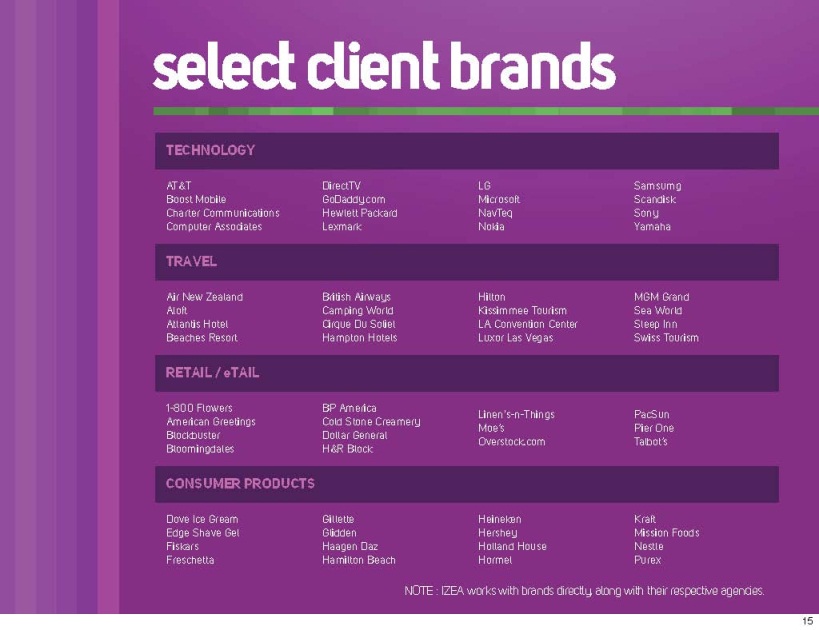

select client brands TECHNOLOGY AT&T Boost Mobile Charter Communications Computer Associates DirectTV GoDaddy.com Hewlett Packard Lexmark LG Microsoft NavTeq Nokia Samsumg Scandisk Sony Yamaha TRAVEL Air New Zealand Aloft Atlantis Hotel Beaches Resort British Airways Camping World Cirque Du Soliel Hampton Hotels Hilton Kissimmee Tourism LA Convention Center Luxor Las Vegas MGM Grand Sea World Sleep Inn Swiss Tourism RETAIL / eTAIL 1-800 Flowers American Greetings Blockbuster Bloomingdales BP America Cold Stone Creamery Dollar General H&R Block Linen's-n-Things Moe’s Overstock.com PacSun Pier One Talbot’s CONSUMER PRODUCTS Dove Ice Gream Edge Shave Gel Fiskars Freschetta Gillette Glidden Haagen Daz Hamilton Beach Heineken Hershey Holland House Hormel Kraft Mission Foods Nestle Purex NOTE : IZEA works with brands directly, along with their respective agencies.

15

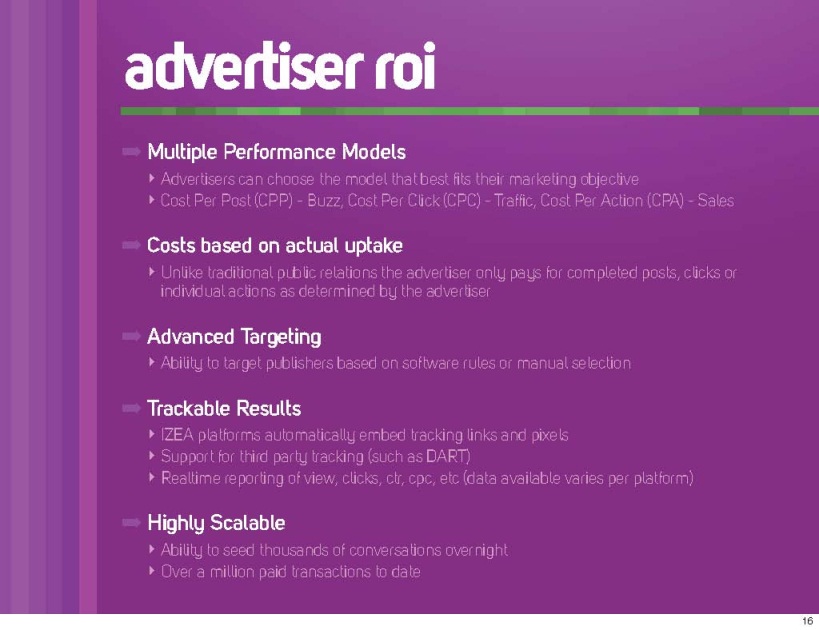

advertiser roi Multiple Performance Models Advertisers can choose the model that best fits their marketing objective Cost Per Post (CPP) - Buzz, Cost Per Click (CPC) - Traffic, Cost Per Action (CPA) - Sales Costs based on actual uptake Unlike traditional public relations the advertiser only pays for completed posts, clicks or individual actions as determined by the advertiser Advanced Targeting Ability to target publishers based on software rules or manual selection Trackable Results IZEA platforms automatically embed tracking links and pixels Support for third party tracking (such as DART) Realtime reporting of view, clicks, ctr, cpc, etc (data available varies per platform) Highly Scalable Ability to seed thousands of conversations overnight Over a million paid transactions to date

16

completed transactions Cumulative Paid Transactions on all IZEA Platforms SOURCE: IZEA Platform data

17

publisher growth Cumulative Registered IZEA Publisher Accounts 2006-2010 SOURCE: IZEA Platform data. May include publishers registered in multiple platforms.

18

advertiser growth Cumulative Registered IZEA Advertiser Accounts 2006-2010 SOURCE: IZEA Platform data. May include advertisers registered in multiple platforms.

19

platform milestones 2006 Launch of PayPerPost.com v1.0 2007 Launch of SocialSpark.com v1.0, PayPerPost v2.0 2008 Launch of PayPerPost.com v3.0 2009 Launch of SponsoredTweets.com v1.0, PayPerPost.com v4.0, InPostLinks v1.0

2010 Launch of SponsoredTweets.com v1.5, SocialSpark v2.0, WeReward v1.0 IZEA has launched five marketplaces in five years. Innovation is at our core.

20

leadership team Ted Murphy, Founder/CEO Successful serial entrepreneur, founding 6 companies since 1995 15 year marketing technology veteran Donna Mackenzie, CFO, CPA President of Central Florida Chapter of Financial Executives International Previously CFO at Channel Intelligence, Cytura Jerry Biuso, VP of Sales 25 years of sales experience, Certified Sales Coach Previously with Banco Popular, Prudential Home Mortgage Peter Scott, VP of Business Development, APR, MBA President of Public Relations Society of America, Orlando Chapter 15 Years experience in marketing, PR, social media and mobile

21

market

22

online ad spending Growth of US Online Ad Spending 2009 2010 2011 2012 2013 2014 $22.7B $25.8B $28.5B $32.6B $35.0B $40.5B

23

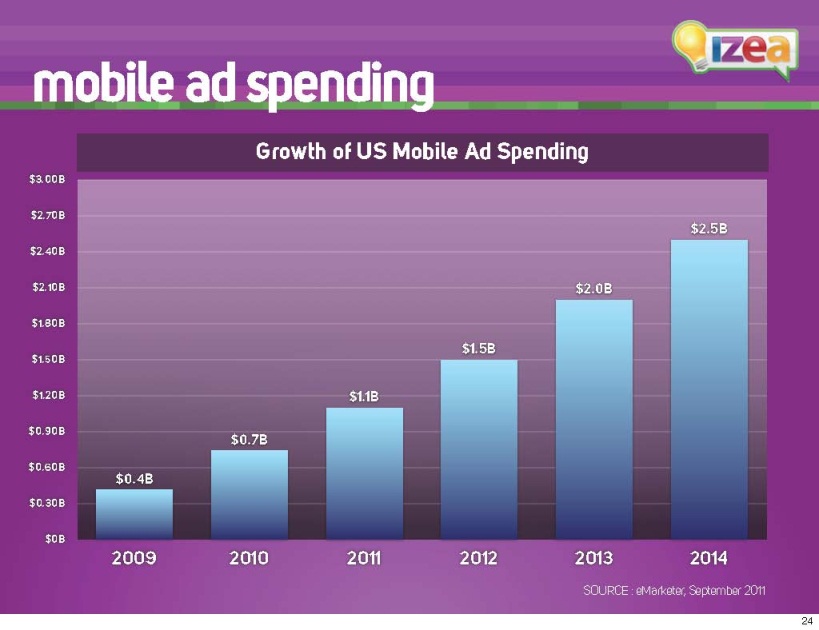

mobile ad spending Growth of US Mobile Ad Spending 2009 2010 2011 2012 2013 2014 $0.4B $0.7B $1.1B $1.5B $2.0B $2.5B

24

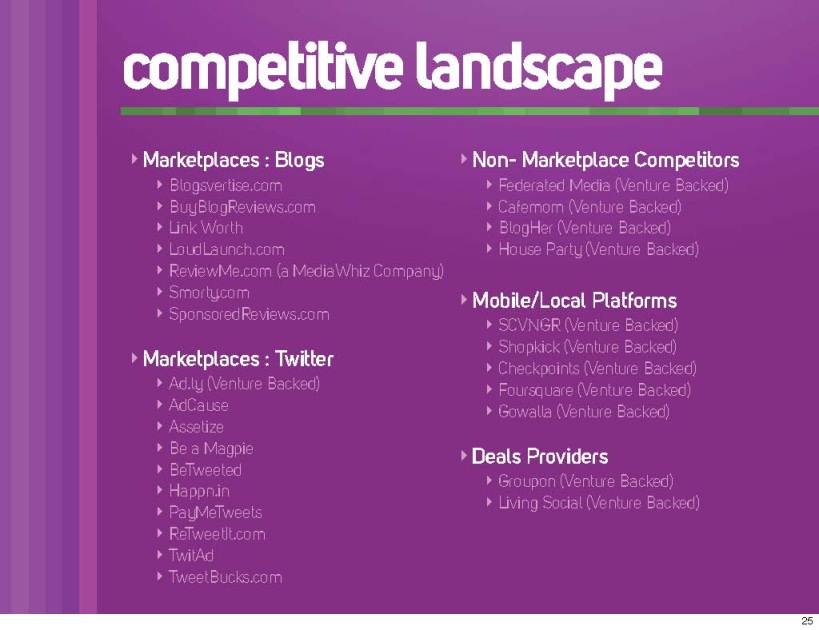

competitive landscape Marketplaces : Blogs Blogsvertise.com BuyBlogReviews.com Link Worth LoudLaunch.com ReviewMe.com (a MediaWhiz Company) Smorty.com SponsoredReviews.com Marketplaces : Twitter Ad.ly (Venture Backed) AdCause Assetize Be a Magpie BeTweeted Happn.in PayMeTweets ReTweetIt.com TwitAd TweetBucks.com Non- Marketplace Competitors Federated Media (Venture Backed) Cafemom (Venture Backed) BlogHer (Venture Backed) House Party (Venture Backed) Mobile/Local Platforms SCVNGR (Venture Backed) Shopkick (Venture Backed) Checkpoints (Venture Backed) Foursquare (Venture Backed) Gowalla (Venture Backed) Deals Providers Groupon (Venture Backed) Living Social (Venture Backed)

25

growth of social media US Bloggers 2008-2013 US Adult Twitter Users 2008 2009 2010 2011 2012 2013 2008 2009 2010 25.1 27.9 30.8 33.7 35.6 37.6 6.0 17.0 26.0 Source: eMarketer, September 2009

26

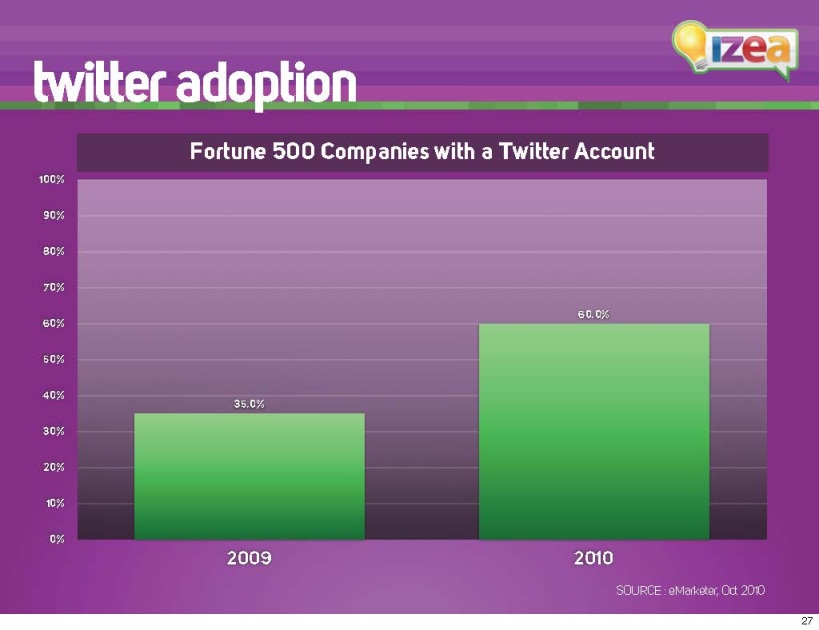

twitter adoption Fortune 500 Companies with a Twitter Account 2009 2010 35.0% 60.0%

27

Do you directly monetize your social media activities through advertisement, sponsorship or affiliate programs? monetizing social media SOURCE : IZEA Q2, 2010 SMS Survey 11.6% 32.1% 56.2% Yes I Would like to I Don’t want to SOCIAL MEDIA PUBLISHERS

28

Community/Social Media Tools that US Online Retailer Currently Use or Plan to Use Today Next 12 Months Beyond 1 Year No Plans Facebook Fan Page 86% 10% 3% 1% Twitter Publishing 65% 19% 7% 9% Customer Reviews 55% 26% 13% 6% Blogs 55% 25% 12% 8% Viral Videos 50% 22% 13% 15% Facebook Connect 43% 31% 10% 16% Social Listening 36% 31% 19% 14% Questions and Answers 29% 20% 25% 26% Community Forums 27% 18% 23% 32% Product Suggestion Box 19% 26% 20% 35% Source: the e-tailing group and PowerReviews, "Community and Social Media Study' September 9, 2009

29

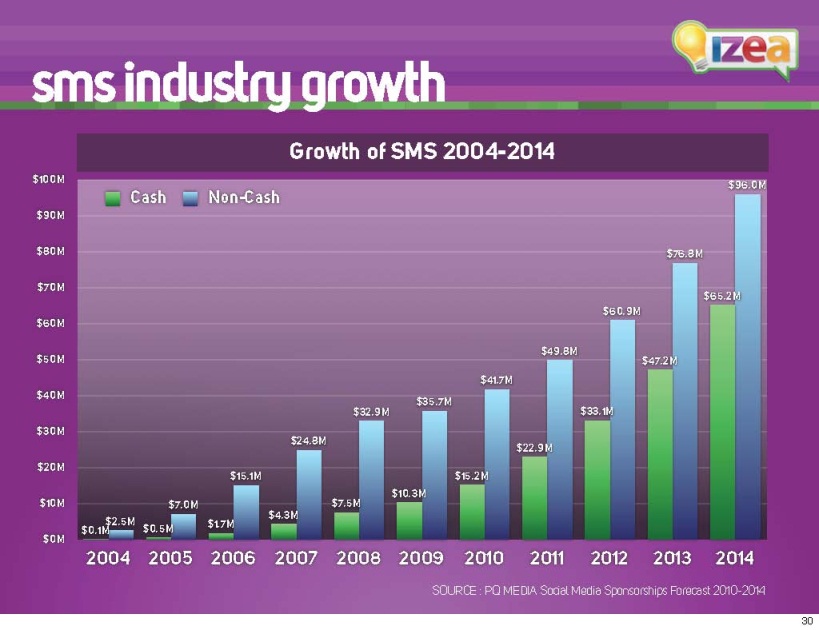

sms industry growth SOURCE : PQ MEDIA Social Media Sponsorships Forecast 2010-2014 Growth of SMS 2004-2014 $0M $10M $20M $30M $40M $50M $60M $70M $80M $90M $100M 2004 2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 $96.0M $76.8M $60.9M $49.8M $41.7M $35.7M $32.9M $24.8M $15.1M $7.0M $2.5M $65.2M $47.2M $33.1M $22.9M $15.2M $10.3M $7.5M $4.3M $0.1M $0.5M $1.7M Cash Non-Cash

30

market opportunity Social media is the fastest growing segment of the Internet1 69% of US Adults participate in social media2 Total SMS spending is projected to rise at a 28.5% CAGR during the 2009-2014 period,

reaching $161.2 million in 20143 Effect on advertisers Social media takes time away from traditional media, effecting businesses large and small Negative impact on television, radio, print and even large online publishers Advertisers can’t cost effectively execute large scale SMS campaigns on their own New FTC guidelines make manual outreach more time consuming and complex Effect on social media publishers Not enough traffic to warrant attention from advertisers by themselves Unable to capitalize on the small but loyal following they have developed IZEA’s solutions Aggregate social media publishers into online marketplaces creating scale and targeting Provide self service platforms that service all business types and sizes Automation of FTC disclosure, compliance and monitoring tools (1) SOURCE : Click: What Millions of People Are Doing Online and Why it Matters by Bill Tancer (2) SOURCE : PQ MEDIA Social Media Sponsorships Forecast 2010-2014 (3) SOURCE : Forrester Research - North American Social Technograhics Online Survey, Q2 2007 & Q2 2008

31

comparables Source: CapitalIQ as of 03/14/11 ($mm, except per share data) % of 52 TEV/ TEV/ LTM yoy Close Week Market LTM LTM LTM LTM EBITDA Revenue Company Name Price High Cap TEV Revenue EBITDA Revenue EBITDA Margin Growth Augme Technologies, Inc. (AUGT) $3.92 82.2% $244.6 $244.0 $2.0 ($9.0) 119.1x NM NM NM Constant Contact, Inc. (CTCT) 30.40 93.9% 894.2 769.8 174.2 14.4 4.4x 53.4x 8.3% 35.0% CrowdGather, Inc. (CRWG)1.37 72.1% 63.6 62.3 1.0 (2.2) 62.8x NM NM 412.7% Demand Media, Inc. (DMD) 20.75 78.4% 1,719.2 2,060.9 252.9 50.9 8.1x 40.5x 20.1% 27.5% Velti Plc (AIM:VEL) $12.41 86.9% $630.4 $679.3 $124.6 $36.5 5.3x 19.6x 29.3% 183.3% Mean 40.0x 37.9x 19.2% 164.6% Median 8.1x 40.5x 20.1% 109.1%

32

press

33

34

35

36

37

38

39

thank you

40