UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(a) OF THE

SECURITIES EXCHANGE ACT OF 1934

(Amendment No. )

Filed by the Registrant¨

Filed by a Party other than the Registrantx

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| ¨ | Definitive Proxy Statement |

| x | Definitive Additional Materials |

| ¨ | Soliciting Material under § 240.14a-12 |

SURGE COMPONENTS, INC.

(Name of Registrant as Specified In Its Charter)

Bradley P. Rexroad

Michael D. Tofias

(Name of Person(s) Filing Proxy Statement, if other than the Registrant)

Payment of Filing Fee (Check the appropriate box):

| ¨ | Fee computed on table below per Exchange Act Rules 14a-6(i)(4) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate number of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11

(Set forth the amount on which the filing fee is calculated and state how it was determined): |

| (4) | Proposed maximum aggregate value of transaction: |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the Form or Schedule and the date of its filing. |

| (1) | Amount Previously Paid: |

| (2) | Form, Schedule or Registration Statement No.: |

Concerned Stockholders Make Case for Change at Surge Components, Inc.

—Highlight History of Underperformance—

—Question Poor Governance Practices—

New York, NY—November 7, 2016—The Concerned Stockholders of Surge Components, Inc., long-term stockholders of Surge Components, Inc. (OTCPK: SPRS) (“Surge”) who beneficially own approximately 22% of Surge, today announced that they sent a letter to their fellow stockholders. Among other things, the Concerned Stockholders highlighted Surge’s sustained, long-term poor performance; history of poor capital management; outsized executive compensation and dilutive equity issuances; and poor corporate governance. The Confirmed Stockholders, who would be highly qualified, independent voices at Surge, confirmed that they will work tirelessly to improve Surge for the benefit of all stockholders.

The full text of the letter follows:

Concerned Stockholders of Surge Components

concernedsurgestockholders@gmail.com

+1-507-86SURGE (507-867-8743)

November 7, 2016

Dear Fellow Stockholder of Surge Components, Inc.:

HELP US FIX SURGE—VOTE THEWHITE PROXY CARD

We are Brad Rexroad and Mike Tofias. Both of us are long-term stockholders of Surge Components, Inc. (“Surge”), with Mike owning shares for over 12 years and Brad owning shares for almost four years. Together, we own approximately 22% of the outstanding common stock. As major stockholders,our interests are completely aligned with yours.

Like you, we have been frustrated by Surge’s poor performance. We patiently waited for things to improve. We suggested strategies and alternates to management, all of which fell on deaf ears. Things are not improving, andit is time for a change.

As recently as a few days ago, Surge offered to buy our shares to make us “go away.” Surge has made that offer to us in the past, and we have turned them down each time. We have no intention of selling our shares unless Surge offers the same deal to ALL stockholders.

WE BELIEVE THAT THERE IS SIGNIFICANT ROOM FOR IMPROVEMENT AT SURGE. That is why we nominated ourselves to serve on the Board of Directors (the “Board”). We have also made three proposals for consideration at the upcoming annual meeting that we believe will be helpful in improving Surge’s corporate governance, which we believe to be shockingly poor. We are both spending tens of thousands of dollars and hours of our time in support of improving Surgefor the benefit of all stockholders. We would both be highly qualified,independent voices on the Board and able to offer the perspective of significant, independent stockholders. We will look at all decisions with a fresh perspective and open minds, and we have no preconceived notions about the “right” future direction for Surge.

HELP US IMPROVE SURGE! Please sign, date and return the enclosed WHITE proxy card to cast your vote in favor of electing new directors at Surge. |

SUSTAINED, LONG-TERM POOR PERFORMANCE

Surge’s record of underperformance could not be clearer:

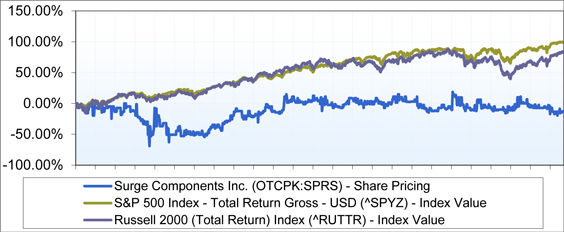

| · | Over the five years preceding August 26, 2016 (when we first went public with our concerns), Surge’s stock pricedeclined by 17%, while the S&P 500 and Russell 2000 indices have produced returns of 105% and 92%, respectively. |

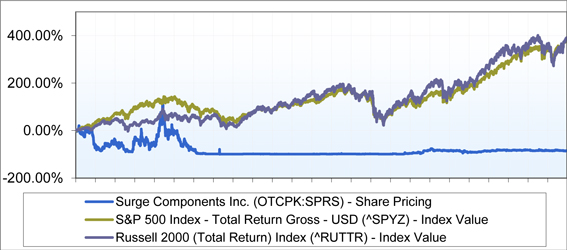

| · | Over the 20 years prior to August 26, 2016, Surge’s stock pricedropped by 85%, while the S&P 500 returned 375% and the Russell 2000 returned 387%. |

| · | As of August 1996, shortly after Surge’s initial public offering, its book value per share was $1.28. Twenty years later, as of August 2016, its book value per share haddeclined to $1.22. |

Stockholders should not tolerate more years of poor performance and squandered opportunities.

POOR CAPITAL MANAGEMENT

| · | We have repeatedly urged the Board to use its surplus cash—all of which isyour money—to repurchase a large amount of stock through a tender offer. |

| · | Given Surge’s thin trading volume, we believe that a tender offer is the most efficient and effective way to meaningfully return capital to stockholders. |

| · | The $500,000 repurchase plan that Surge announced in November 2015 has been woefully mismanaged, as Surge hasrepurchased only $23,000 worth of stock through August 2016. |

| · | Surge’s actions support our belief that management and the Board do not ever intend to meaningfully return the approximately $7 million of cash—almost 70 cents a share!—that Surge has been hoarding. |

MANAGEMENT AND THE BOARD HAVE BEEN RICHLY REWARDED

IN CASH AND DILUTIVE EQUITY FOR THEIR POOR PERFORMANCE

Over and over, Surge has richly rewarded its senior management team for its dismal performance:

| · | For the fiscal year ended November 30, 2015, Chief Executive Officer Ira Levy and Vice President Steven Lubman received aggregate non-equity compensation of $818,763, while Surge’s earnings were just $857,785. |

| · | Over the 20 years ended August 2016, Messrs. Levy and Lubman received aggregate non-equity compensation in excess of $10 million, in addition to significant equity compensation. During that same period, Surge lost a cumulative $11 million. And that is just the compensation that Surge had to report publicly. For fiscal years 2004 to 2007, Surge did not publicly report its executive compensation amounts. |

And the Board has continued to dilute you:

| · | For the two years between October 2014 and September 2016, Surge’s shares outstanding increased by 11%,with 75% of that increase attributable to management and the Board granting themselves stock and exercising stock options. |

| · | Since 2010, the Board has granted itself and management options and stock amounting to roughly 12% of Surge. |

| · | What have you received in return for this dilution, other than stock performance that has meaningfully lagged the S&P 500 and Russell 2000? |

SHOCKINGLY POOR CORPORATE GOVERNANCE

Surge’s corporate governance is, in our opinion, shockingly poor. Consider:

| · | Surge maintains a classified board of directors under whichdirectors stand for election only once every three years. We believe that it is self-evident that each director—your representatives on the Board—should stand for election each year. |

| · | Surge has refused to provide us with customary information that would allow us to communicate with our fellow stockholders.We believe that Surge is legally required to provide us with this information. We have been forced to sue Surge to get it. Why does Surge not want us to communicate with you? |

| · | Just after we announced our proxy contest, the Board adopted a poison pill with a low 4.99% triggering threshold. The Board claims it is to protect Surge’s net operating losses (“NOLs”). If these NOLs are so valuable, why did Surge and the Board wait until just after we nominated ourselves to the Board to protect them? Why not do this a decade ago when the value of the NOLs was even greater? Furthermore, all of Surge’s NOLs expire over the next four years, and we believe that it ishighly unlikely that all of the NOLs will be utilized. |

| · | To add insult to injury, Mr. Lubman made several well-timed purchases around the time that the poison pill was being adopted. Just days before adoption, Mr. Lubman made five open market purchases for 38,140 shares.We believe that these are the first open market purchases of Surge’s common stock that Mr. Lubman has ever made, and they were completed days before the poison pill was adopted! None of these purchases would have been permissible had they occurred after the adoption of the poison pill. |

| · | Surge and its Board are entangled in numerous related-party relationships and transactions. |

| o | Surge rents its corporate headquarters fromGreat American Realty of Jeffryn Blvd., LLC, an entity owned by Messrs. Levy and Lubman and Marc Siegel, Mr. Levy’s former brother-in-law. |

| o | Director Martin Novick is a partner atGreat American Realty. |

| o | Director Lawrence Chariton is a consultant toGreat American Jewelry. |

| o | Mr. Levy’s former father-in-law, David Siegel, was one of the founders ofGreat American Electronics. |

| o | What is the relationship between all of these Great American entities? |

| · | The Board continues to employ an “independent” auditor that also performs personal tax work for Messrs. Lubman and Chariton, as well as a company owned by Mr. Chariton’s wife. We believe that this is a blatant conflict of interest. |

WE WILL WORK TIRELESSLY TO IMPROVE SURGE

| · | We will both be highly qualified,independent voices on the Board. As the owners of approximately 22% of Surge,our interests are completely aligned with yours. |

| · | We will bring a sense of urgency to the Board and are dedicated to enhancing stockholder value, whatever path that may take. |

| · | We believe that Surge should evaluate whether there is a value-maximizing transaction available for stockholders, such as through a sale of Surge to a third party. We intend to advocate that the Board fully inform itself on the available options. |

| · | If elected to the Board, we will join with no preconceived notions about the “right” future direction for Surge. Rather, we will take a fresh look at everything with the goal ofmaximizing stockholder value.We have no intention of pursuing a “fire sale” of Surge, and for Surge to state otherwise is reckless.As the owners of approximately 22% of Surge, we have a vested interest in maximizing the value of our investment, not taking the first offer that comes along. We have been patient, long-term stockholders and that will not change. |

| · | If elected to the Board, we will each waive any compensation payable to us as directors. Just like you, we will only make money if the stock appreciates in value. |

HELP US FIX SURGE—VOTE THEWHITE PROXY CARD

As two of the largest stockholders in Surge, we are investing significant amounts of our time and tens of thousands of dollars of our own money to bring you a choice at this year’s annual meeting.

As recently as a few days ago, Surge offered to buy our shares to make us “go away.” Surge has made that offer to us in the past, and we have turned them down each time. We have no intention of selling our shares unless Surge offers the same deal to ALL stockholders.

We believe in Surge. But we have lost confidence in the current Board as the proper stewards for our company. For too long, the Board has tolerated management’s continued underperformance while rewarding management and the directors with generous cash and equity compensation. The Board has also tolerated unacceptable conflicts of interest, such as renting Surge’s corporate headquarters from an entity owned by Messrs. Levy and Lubman.It is time for a change on the Board.

Protect the value of your investment in Surge

by signing, dating and returning the enclosedWHITE proxy card. DO NOT VOTE THE GOLD PROXY CARD

FROM SURGE, EVEN AS A PROTEST VOTE. |

| Very truly yours, | |

| | |

| /s/ Brad Rexroad | /s/ Mike Tofias |

| | |

| Brad Rexroad | Mike Tofias |

Contact:

For Concerned Stockholders of Surge Components, Inc.

Bradley Rexroad, +1-507-86SURGE (507-867-8743)

concernedsurgestockholders@gmail.com