UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| (Mark One) | |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the fiscal year ended December 31, 2012 OR | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| For the transition period from ____ to ____ | |

Commission file number 001-35009

Fortegra Financial Corporation

(Exact name of Registrant as specified in its charter)

| Delaware | 58-1461399 | |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 10151 Deerwood Park Boulevard, Building 100, Suite 330, Jacksonville, FL | 32256 | |

| (Address of principal executive offices) | (Zip Code) | |

| Registrant's telephone number, including area code: | (866)-961-9529 | |

| Securities registered pursuant to Section 12(b) of the Act: | ||

| Title of each class | Name of each exchange on which registered | |

| Common Stock, $0.01 par value per share | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None | ||

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No x

Note - Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Exchange Act from their obligations under those Sections.

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of Registrant's knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o

Non-accelerated filer x (Do not check if a smaller reporting company) Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The aggregate market value of the voting common equity held by non-affiliates of the registrant was $53,422,712 at June 29, 2012 (last day of the registrant's most recently completed second quarter) based on the closing sale price of $8.00 per share for the common stock on such date as traded on the New York Stock Exchange.

The number of outstanding shares of the registrant's Common Stock, $0.01 par value, outstanding as of March 14, 2013 was 19,831,697.

Documents Incorporated by Reference

Certain specifically designated portions of Fortegra Financial Corporation's definitive proxy statement for its 2013 Annual meeting of Stockholders (the "Proxy Statement"), which will be filed on or prior to 120 days following the end of Fortegra Financial Corporation's fiscal year ended December 31, 2012, are incorporated by reference into Parts III and IV of this Form 10-K.

FORTEGRA FINANCIAL CORPORATION

ANNUAL REPORT ON FORM 10-K

DECEMBER 31, 2012

TABLE OF CONTENTS

| Page Number | ||

| Item 1. | ||

| Item 1A. | ||

| Item 1B. | ||

| Item 2. | ||

| Item 3. | ||

| Item 4. | Mine Safety Disclosures | |

| Executive Officers of the Registrant | ||

| Item 5. | ||

| Item 6. | ||

| Item 7. | ||

| Item 7A. | ||

| Item 8. | ||

| Item 9. | ||

| Item 9A. | ||

| Item 9B. | ||

| Item 10. | ||

| Item 11. | ||

| Item 12. | ||

| Item 13. | ||

| Item 14. | ||

| Item 15. | ||

1

EXPLANATORY STATEMENT REGARDING RESTATEMENT

In this Annual Report on Form 10-K ("Form 10-K"), the terms "Fortegra Financial," "Fortegra," "we," "us," "our," "the Company" or similar terms refer to Fortegra Financial Corporation and its subsidiaries unless the context requires otherwise.

This Form 10-K is for our year ended December 31, 2012, and restates the following previously issued Consolidated Financial Statements, data and related disclosures:

| 1. | Our Consolidated Balance Sheet as of December 31, 2011, and the related Consolidated Statements of Income, Comprehensive Income, Stockholders' Equity and Cash Flows for the years ended December 31, 2011 and 2010, located in Part II, Item 8 of this Form 10-K; |

| 2. | Our selected financial data as of and for the years ended December 31, 2011, and 2010, located in Part II, Item 6 of this Form 10-K; |

| 3. | Our management's discussion and analysis of financial condition and results of operations as of and for the years ended December 31, 2011 and 2010, located in Part II, Item 7 of this Form 10-K; |

| 4. | Our unaudited quarterly financial information for the quarterly periods ended March, 31 2012, June 30, 2012 and September 30, 2012 and for the quarterly periods ended March 31, June 30, September 30, and December 31, 2011 and 2010, respectively, located in the Note, "Summarized Quarterly Information (Unaudited)," the Note, " Quarterly Information - Restated (Unaudited)" and the Note, "Quarterly Segment Results - Restated (Unaudited)," of the Notes to Consolidated Financial Statements in Part II, Item 8 of this Form 10-K; and |

| 5. | Our management's discussion and analysis of financial condition and results of operations for the quarterly periods ended March 31, June 30, and September 30, 2010, 2011 and 2012, respectively, located in Part II, Item 7 of this Form 10-K. |

We are restating the previously issued Consolidated Financial Statements, data and related disclosures described above to correct the presentation of revenues and expenses of the Motor Clubs division in our Payment Protection segment. As discussed in the Note, "Restatement of the Consolidated Financial Statements," the Company performed an analysis and determined that, under the guidance in Accounting Standards Codification 605, "Revenue Recognition," our revenues for service and administrative fees generated by the Motor Clubs division should be reported on a gross basis with the corresponding gross reporting of member benefit claims and commission expenses. Historically, these revenues and expenses were presented on a combined net basis in service and administrative fees on the Consolidated Statements of Income. The effect of this correction does not impact our net income, basic or diluted earnings per share amounts, comprehensive income or loss, net cash provided by operating activities or stockholders' equity for the affected periods. We also corrected immaterial errors in revenue recognition, purchase accounting and cash flows, as also discussed in the Note, "Restatement of the Consolidated Financial Statements".

The financial information for the periods indicated above that are included in the Company's Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and earnings, press releases and similar communications issued prior to the filing of this Form 10-K should not be relied on and are superseded by this Form 10-K.

2

PART I

Unless the context requires otherwise, references in this Annual Report on Form 10-K ("Form 10-K") to "Fortegra Financial," "Fortegra," "we," "us," "the Company" or similar terms refer to Fortegra Financial Corporation and its subsidiaries.

FORWARD-LOOKING STATEMENTS

This Form 10-K contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended (the "Securities Act"), and Section 21E of the Securities Exchange Act of 1934, as amended (the "Exchange Act"), which are made in reliance upon the protection provided by such act for forward-looking statements. Such statements are subject to risks and uncertainties. All statements other than statements of historical fact included in this Form 10-K are forward-looking statements. Forward-looking statements give our current expectations and projections relating to our financial condition, results of operations, plans, objectives, future performance and business. You can identify forward-looking statements by the fact that they do not relate strictly to historical or current facts. These statements may include words such as "anticipate," "estimate," "expect," "project,'' "plan," "intend," "believe," "may," "should," "can have," "will," "likely" and other words and terms of similar meaning in connection with any discussion of the timing or nature of future operating results or financial performance or other events.

The forward-looking statements contained in this Form 10-K are based on assumptions that we have made in light of our industry experience and our perceptions of historical trends, current conditions, expected future developments and other factors we believe are appropriate under the circumstances. As you read this Form 10-K, you should understand that these statements are not guarantees of performance or results. They involve risks, uncertainties (some of which are beyond our control) and assumptions. Although we believe that these forward-looking statements are based on reasonable assumptions, you should be aware that many factors could affect our actual financial results and cause them to differ materially from those anticipated in the forward-looking statements. We believe these factors include, but are not limited to, those described under PART I, ITEM 1A. RISK FACTORS and PART II, ITEM 7. MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS. Should one or more of these risks or uncertainties materialize, or should any of these assumptions prove incorrect, our actual results may vary materially from those projected in these forward-looking statements.

Any forward-looking statement made by us in this Form 10-K speaks only as of the date on which we make it. Factors or events that could cause our actual results to differ may emerge from time to time, and it is not possible for us to predict all of them. We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future developments or otherwise, except as may be required by law.

ITEM 1. BUSINESS

Corporate Overview

Fortegra Financial Corporation is an insurance services company that provides distribution and administration services to insurance companies, insurance brokers and agents and other financial services companies primarily in the United States. We were incorporated in 1981 in the State of Georgia and in 2010 we re-incorporated in the State of Delaware. We sell our services and products principally through clients rather than directly to consumers. We initially provided credit life and disability insurance for financial institutions, primarily small community banks in Georgia, and their customers under our Life of the South brand. In 2008, we changed our name from Life of the South Corporation to Fortegra Financial Corporation. Most of our business is generated through networks of small to mid-sized community and regional banks, small loan companies and automobile dealerships. Our majority-owned and controlled subsidiaries, are as follows:

| • | LOTS Intermediate Co. ("LOTS IM") |

| • | Bliss and Glennon, Inc. ("B&G") |

| • | CRC Reassurance Company, Ltd. ("CRC") |

| • | Insurance Company of the South ("ICOTS") |

| • | Life of the South Insurance Company ("LOTS") and its subsidiary, Bankers Life of Louisiana ("Bankers Life") |

| • | LOTS Reassurance Company ("LOTS RE") |

| • | LOTSolutions, Inc. |

| • | Lyndon Southern Insurance Company ("Lyndon Southern") |

| • | Southern Financial Life Insurance Company ("SFLAC"), 85% owned |

| • | South Bay Acceptance Corporation ("South Bay") |

| • | Continental Car Club, Inc. ("Continental") |

| • | United Motor Club of America, Inc. ("United") |

| • | Auto Knight Motor Club, Inc. ("Auto Knight") |

| • | eReinsure.com, Inc. ("eReinsure") |

| • | Pacific Benefits Group Northwest, LLC ("PBG") |

| • | Magna Insurance Company ("Magna") |

3

| • | Digital Leash, LLC, d/b/a ProtectCELL ("ProtectCELL"), 62.4% owned |

| • | 4Warranty Corporation ("4Warranty") |

In June 2007, entities affiliated with Summit Partners, a growth equity investment firm, acquired 91.2% of our capital stock. The acquisition was financed through (i) $20.0 million of subordinated debentures maturing in 2013 issued to affiliates of Summit Partners, (ii) $35.0 million of preferred trust securities maturing in 2037 and (iii) an equity investment of $43.1 million by affiliates of Summit Partners. In connection with the acquisition, all of our $11.5 million of redeemable preferred stock outstanding prior to the acquisition remained outstanding and certain stockholders prior to the acquisition continued to hold such shares after the acquisition. In addition to acquiring our capital stock in the acquisition, the proceeds from the equity and debt financings were used to repay pre-transaction indebtedness of $10.1 million and pay transaction costs of $5.8 million. We refer to the foregoing transactions collectively as the "Summit Partners Transactions." In April 2009, in connection with our acquisition of Bliss and Glennon, Inc., affiliates of Summit Partners acquired additional shares of our common stock for $6.0 million.

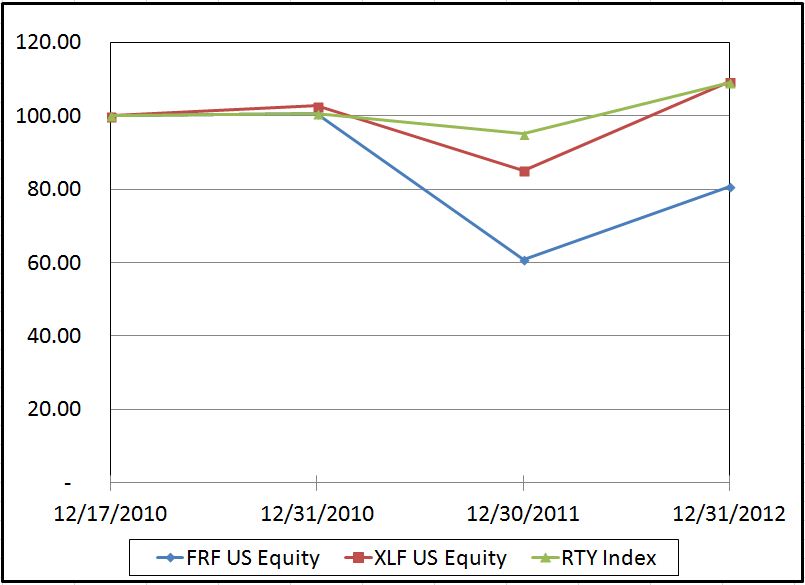

On December 17, 2010, we completed our initial public offering (the "IPO") and began trading on the New York Stock Exchange ("NYSE") under the symbol "FRF". In conjunction with our IPO we issued 6,000,000 shares of common stock at an IPO price of $11.00 per share, of which 4,265,637 shares were sold by us and 1,734,363 shares were sold by selling stockholders. In connection with the IPO, Summit Partners sold 1,548,675 common shares of stock. At December 31, 2012, affiliates of Summit Partners beneficially owned approximately 63.2% of our common stock. At December 31, 2012, we had 20,710,370 shares of common stock outstanding.

Business Overview

We began over 30 years ago as a provider of credit insurance products and, through our transformational efforts, have evolved into a diversified insurance services company. From 1994 to 2003, through a series of strategic acquisitions and organic growth, we expanded our payment protection client (or producer) base to include consumer finance companies, retailers, automobile dealers, credit card issuers, credit unions and regional and community banks throughout the United States. During this period, we expanded our product and service offerings to include credit property, debt cancellation and warranty products.

We now leverage our proprietary technology infrastructure, internally developed best practices and access to specialty insurance markets to provide our clients with distribution and administration services and insurance-related products. Our services and products complement consumer credit offerings, provide outsourcing solutions designed to reduce the costs associated with the administration of insurance and other financial products and facilitate the distribution of excess and surplus lines insurance products through insurance companies, brokers and agents. These services and products are designed to increase revenues, improve customer value and loyalty and reduce costs for our clients.

We generally target market segments that are niche and specialty in nature, which we believe are underserved by competitors and have high barriers to entry. We focus on building quality client relationships and emphasizing customer service. This focus, along with our ability to help clients enhance revenue and reduce costs, has enabled us to develop and maintain numerous long-term client relationships. Over 80% of our clients have been with us for more than five years.

Our fee-driven revenue model is focused on delivering a high volume of recurring transactions through our clients and producing attractive profit margins and operating cash flows. Historically, our business has grown both organically and through acquisitions of complementary businesses. For the year ended December 31, 2012, our total revenues increased 3.6% or $10.1 million to $291.6 million from $281.6 million, for the year ended December 31, 2011, which includes the impact of the restatement and the immaterial correction of a prior period error as discussed in the Note, "Restatement of the Consolidated Financial Statements," of the Notes to Consolidated Financial Statements. Our net income was $15.2 million for the year ended December 31, 2012 compared to $13.5 million for the year ended December 31, 2011. Our adjusted earnings before interest expense, taxes, non-controlling interest, depreciation and amortization ("Adjusted EBITDA") totaled $40.6 million and $39.3 million for the years ended December 31, 2012 and 2011, respectively. See the section titled "Results of Operations - Segments" included in Item 7 of this Annual Report for more information and a Reconciliation of Adjusted EBITDA.

Financial Information About Our Business Segments

Financial information with respect to our business segments, including revenue, and operating income or loss with respect to our operations outside the United States, is contained in the Note, "Segment Results" in the Notes to Consolidated Financial Statements and is incorporated herein by reference.

Our Business Segments

Fortegra operates in three business segments: (i) Payment Protection, (ii) Business Process Outsourcing ("BPO") and (iii) Brokerage. Payment Protection specializes in protecting lenders and their consumers from death, disability or other events that could otherwise impair their ability to repay a debt and also offers warranty and service contracts for mobile handsets, furniture and major appliances, and motor club solutions to consumers. BPO provides an assortment of administrative services tailored to insurance and other financial services companies through a virtual insurance company platform. Brokerage uses a pure wholesale sell-through model to sell specialty

4

casualty and surplus lines insurance and also provides web-hosted applications used by insurers, reinsurers and reinsurance brokers for the global reinsurance market.

In each segment, we deliver services and products that generate incremental revenues and utilize technology to reduce operating costs. Our businesses benefit from efficiencies by sharing accounting, compliance, legal, technology, human resources and administrative services. Please see the Note, "Segment Results," in the Notes to the Consolidated Financial Statements included in Item 8 of this Form 10-K for additional information.

Payment Protection

Our Payment Protection segment, marketed under our Life of the South, ProtectCELL, 4Warranty, Continental Car Club, United Motor Club and Auto Knight Motor Club brands, delivers credit insurance, debt protection, warranty and service contracts, motor club solutions and membership plans to consumer finance companies, regional banks, community banks, retailers, small loan companies, warranty administrators, automobile dealers, vacation ownership developers, credit unions and independent wireless retailers. Our clients then offer these products to their customers in conjunction with consumer transactions.

We own and operate insurance company subsidiaries to facilitate, on behalf of our Payment Protection clients, the distribution of credit insurance and payment protection services and products. This allows our clients to sell these services and products to their customers without having to establish their own insurance companies, which saves our clients the cost and time of undertaking and complying with substantial regulatory and licensing requirements. Our clients typically retain underwriting risk related to such products either through retrospective commission arrangements or fully-collateralized reinsurance companies owned by them, which we administer on their behalf. While the majority of our Payment Protection revenue is fee-based, we assume insurance underwriting risk in select instances to meet clients' needs and to enhance our profitability. In addition, our insurance company's subsidiaries issue contractual liability policies to warranty companies and service providers in relation to warranty and service contracts.

Our Payment Protection business generates service and administrative fees for distributing and administering payment protection products on behalf of our clients. We also earn ceding commissions in our Payment Protection business for credit insurance that we cede to reinsurers through coinsurance arrangements. We elect to cede to reinsurers a significant portion of the credit insurance that we distribute to participate in the underwriting profits of these products and to maximize our return on capital. Our Payment Protection business also generates net investment income from our invested assets portfolio.

BPO

Our BPO segment, marketed under the Consecta and Pacific Benefits Group Northwest, LLC brands, provides a broad range of administrative services tailored to insurance and other financial services companies. Our BPO business is one of our most technology-driven segments. Through our operating platform, which utilizes our proprietary technology, we provide sales and marketing, electronic underwriting, premium billing and collections, policy administration, claims adjudication and call center management services on behalf of our clients. In addition our BPO segment markets and sells health, accident, critical illness and life insurance policies to customers in the U.S.

Our proprietary administrative technology platform allows our clients to outsource the fixed costs and complexity associated with internal development and ongoing administration of insurance products at a lower cost than if our client performs these functions on its own. In addition, the scalability of our operating platform allows us to add new clients or additional services for clients without incurring significant incremental costs.

Our BPO business generates service and administrative fees and other income under per-unit priced contracts. Service and administrative fees for our BPO business are based on the complexity and volume of business that we manage on behalf of our clients. We do not take any insurance underwriting risk in our BPO business.

Brokerage

Our Brokerage segment is marketed under our Bliss & Glennon, eReinsure.com, Inc. and South Bay Acceptance Corporation brands. We acquired eReinsure in March 2011, which allows us to broaden our relationships with major insurers, reinsurers and brokers worldwide who use the eReinsure system to assist in the management of facultative reinsurance transactions. Bliss & Glennon, acquired in April 2009, is one of the largest surplus lines brokers in California according to the Surplus Line Association of California, and ranked in the top 10 wholesale brokers in the United States in 2012 by premium volume according to Business Insurance, an industry publication.

The Brokerage segment uses a wholesale model to sell specialty property and casualty ("P&C") and surplus lines insurance through retail insurance brokers and agents and insurance companies, as well as the placement of reinsurance risks on reinsurers. We believe that our emphasis on customer service, rapid responsiveness to submissions and underwriting integrity in this segment has resulted in high customer satisfaction among retail insurance brokers and agents and insurance companies.

5

Our Brokerage business provides retail insurance brokers and agents and insurance companies the ability to obtain various types of commercial insurance coverages outside of their core areas of focus, broader access to insurance markets and the expertise to place complex risks. We also provide underwriting services for ancillary or niche insurance products as a managing general agent ("MGA") for specialized insurance carriers. We believe that insurance carriers value their relationship with us because we provide them with access to new markets without the need for costly distribution infrastructure. Our Brokerage business also utilizes our technology platform to provide its clients with administrative services, including policy underwriting, premium and claim administration and actuarial analysis. Through South Bay we finance premiums on insurance and insurance-related products.

Our Brokerage business earns wholesale brokerage commissions and fees for the placement of specialty insurance products. We also earn profit commissions which we receive from carriers based upon the ultimate profitability of the insurance policies that we place with those carriers. We do not take any insurance underwriting risk in our Brokerage business. Our Brokerage segment also derives fees from master license agreements to use the eReinsure system together with fees for the transactions completed through its platform.

Recent Business Acquisitions and Dispositions

One of the main drivers of our success has been growth from business acquisitions. Our 2012 and 2011 acquisitions are detailed below:

Acquisitions in 2012

On December 31, 2012, we acquired a 62.4% ownership interest in Digital Leash, LLC, d/b/a ProtectCELL and an option to purchase the remaining 37.6% ownership interest in ProtectCELL after 2014. ProtectCELL provides membership plans that afford protection for mobile wireless devices and other benefits including data management and identity theft protection. ProtectCELL is one of the leaders in mobile device protection plans and will spearhead Fortegra's efforts to expand its warranty and service contract business in the mobile and wireless device space.

On December 31, 2012, we acquired 100% of the outstanding stock ownership of 4Warranty Corporation, a leading warranty and extended service contract administrator with extensive expertise in furniture, electronics, appliance, lawn and garden, and fitness equipment extended service contracts. 4Warranty complements the Company's rapidly expanding warranty business within its Payment Protection segment.

On April 24, 2012, we acquired a 100% ownership interest in MHA & Associates LLC, for $0.3 million, obtaining the renewal rights of the business and hiring the prior owner to maintain and increase the block of business.

Acquisitions in 2011

In January 2011, the Company acquired 100% of the outstanding stock ownership of Auto Knight Motor Club, Inc., of Palm Springs, CA. Auto Knight provides motor club memberships, vehicle service plans and tire and wheel programs, which are offered by automobile and truck dealerships and retailers in the United States and Canada. The acquisition expands the Company's geographic reach to Canada, where Auto Knight offers its products through retailers as a subscription benefit.

In March 2011, the Company acquired 100% of the outstanding stock ownership of eReinsure.com, Inc.. eReinsure provides web-hosted applications for the reinsurance market by leveraging Internet technologies in application architecture, network communication and information delivery to facilitate reinsurance transactions.

In October 2011, the Company acquired Pacific Benefits Group Northwest, LLC, a leading U.S. independent insurance agency. PBG markets and sells health, accident, critical illness and life insurance policies. PBG is headquartered in Beaverton, OR and is licensed as an agent in 42 states.

Effective December 1, 2011, the Company's Payment Protection subsidiary, Life of the South Insurance Co., entered into an assumption reinsurance transaction with Magna Insurance Company in which LOTS assumed all the outstanding liabilities for insurance policies underwritten by Magna, including its credit, annuity and mortgage life policies. The value of the insurance liabilities assumed, net of reinsurance was approximately $11.3 million. These policies are running off and no new policies are being underwritten.

Effective December 29, 2011, the Company acquired Magna from Hancock Holding Company. Magna does not have any ongoing insurance business, but does have twelve State Certificates of Authority, which are redundant with certificates held by other Fortegra subsidiaries.

We historically have used a combination of borrowings under our credit facilities and cash on hand to pay the purchase price of our acquisitions. The following table summarizes our acquisition activity for the year ended:

6

| (in thousands, except number of acquisitions closed) | December 31, 2012 | ||

| Number of acquisitions closed | 3 | ||

| Total cash consideration | $ | 23,166 | |

Market Opportunity

We operate in the insurance, consumer finance and commercial finance industries principally in the United States, offering our services and products through the brands and distribution bases of our clients. We believe that we are well positioned to capitalize on the following key industry trends:

Financial Performance of Financial Services Companies and Retailers. Financial services companies and retailers offer complementary services and products, including payment protection and insurance-related services and products, which we believe increase their revenues, enhance customer value and loyalty and improve their profitability.

Growth of Outsourcing in the Insurance Industry. By outsourcing business functions that can be more efficiently and cost effectively provided by specialized service providers, we believe that insurance companies can increase productivity, focus on core competencies and reduce operating costs.

Growth of the Specialty P&C Insurance Market. We believe the market for specialty P&C insurance products has grown as a result of increased acceptance of these products by insured parties and the development of new risk management products by insurance carriers. Insurance carriers operating in the surplus lines market generally distribute their products through wholesale insurance brokers, such as Bliss & Glennon.

Our Competitive Strengths

We believe the following to be the key strengths of our business model:

Strong Value Proposition for Our Clients and Their Customers. Our solutions manage the essential aspects of insurance distribution and administration, providing low-cost access to complex, often highly-regulated markets, which we believe enables our clients to generate high-margin, incremental revenues, enter new markets, mitigate risk, improve operating efficiencies and enhance customer loyalty.

Proprietary Technology and Low-Cost Operating Platform. Our proprietary technology delivers low-cost, highly automated services to our clients without significant up-front investments and enables us to automate core business processes and reduce our clients' operating costs.

Scalability. We believe that our scalable and flexible technology infrastructure, together with our highly trained and knowledgeable information technology personnel and consultants, enables us to add new clients and launch new services and products and expand our transaction volume quickly and easily without significant incremental expense.

High Barriers to Entry. We believe that each of our businesses would be time consuming and expensive for new market participants to replicate due to the barriers to entry provided by our long-term relationships with clients and other market participants and substantial experience in the markets that we serve.

Experienced Management Team. We have an experienced management team with extensive operating and industry experience in the markets that we serve. Our management team has successfully developed profitable new services and products and completed the acquisition of thirteen complementary businesses since January 1, 2008.

While we believe these strengths will enable us to compete effectively, there are various risk factors that could materially and adversely affect our competitive position. See ITEM 1A. RISK FACTORS, for a discussion on these factors.

Key Attributes of Our Business Model

We believe the following are the key attributes of our business model:

Recurring Revenue Generation. Our business model, which includes the deployment of our technology with many of our clients, has historically generated substantial recurring revenues, high profit margins and significant operating cash flows.

Long-Term Relationships. By delivering value-added services and products to our clients' customers, and offering fixed-term contracts, we become an important part of our clients' businesses and develop long-term relationships.

Wholesale Distribution. We provide most of our services and products to businesses on a wholesale basis enabling our clients to enhance their customer relationships and allowing us to take advantage of economies of scale.

7

Business Diversification. Our businesses and results of operations are highly diversified within the financial services industry and among retailers, which positions us to take better advantage of emerging industry trends and to better manage business and insurance cycles than companies that operate in only one sector of the financial services industry.

Our Growth Strategy

We believe the following are the key contributors to our growth strategy:

Provide High Value Solutions. We continue to enhance our technologies and processes and focus on integrating our operations with those of our clients in order to provide our clients with services and products that will allow them to generate incremental revenues while reducing the costs of providing insurance and other financial products.

Increase Revenue from Our Existing Clients. We will seek to leverage our long-standing relationships with our existing clients by providing them with additional services and products, introducing new services and products for them to market to their customers and establishing volume-based fee arrangements.

Expand Client Base in Existing Markets. We intend to take advantage of business opportunities to develop new client relationships through our direct sales force, from referrals from existing clients and business partners, by responding to requests for proposals and through our participation in industry events.

Enter New Geographic Markets. We will look to expand our market presence in new geographic markets in the United States and internationally by broadening the jurisdictions in which we operate, hiring new employees, opening new offices, seeking additional licenses and regulatory approvals and pursuing acquisition opportunities.

Pursue Strategic Acquisitions. We plan to continue pursuing acquisitions of complementary businesses to expand our service offerings, access new markets and expand our client base.

Competition

Our businesses focus on niche segments within broader insurance markets. While we face competition in each of our businesses, we believe that no single competitor competes against us in all of our segments and the markets in which we operate are generally characterized by a limited number of competitors. Competition in our operating segments is based on many factors, including price, industry knowledge, quality of client service, the effectiveness of our sales force, technology platforms and processes, the security and integrity of our information systems, the financial strength ratings of our insurance subsidiaries, office locations, breadth of products and services and brand recognition and reputation. Some competitors may offer a broader array of services and products, may have a greater diversity of distribution resources, may have a better brand recognition, may have lower cost structures or, with respect to insurers, may have higher financial strength or claims paying ratings. Some competitors also have larger client bases than we do. In addition, new competitors could enter our markets in the future. The relative importance of these factors varies by product and market. The competitive landscape for each of our business segments is described below.

In our Payment Protection business, we compete with insurance companies, financial institutions and other insurance service providers. The principal competitors for our Payment Protection business include the payment protection groups of The Warranty Group, Assurant, Inc., Asurion Corporation and smaller regional companies. As a result of state and federal regulatory developments and changes in prior years, certain financial institutions are able to offer debt cancellation plans and are also able to affiliate with other insurance companies in order to offer services similar to those in our Payment Protection business. As financial institutions gain experience with payment protection programs, their reliance on our services and products may diminish. ProtectCELL principally serves independent wireless retailers. Competitors offering similar products and services to ProtectCELL include eSecuritel Holdings, LLC, Asurion, LLC and Global Warranty Group, LLC.

Our BPO business competes with a variety of companies, including large multinational firms that provide consulting, technology and/or business process services, off-shore business process service providers in low-cost locations like India, and in-house captive insurance companies of potential clients. Our principal business process outsourcing competitors include Aon Corporation, Computer Sciences Corporation, Direct Response Insurance Administrative Services, Inc., Marsh & McLennan Companies, Inc., Dell Services and Unisys Corporation. The trend toward outsourcing and technological changes may also result in new and different competitors entering our markets. There could also be newer competitors with strong competitive positions as a result of strategic consolidation of smaller competitors or of companies that each provide different services or serve different industries. In addition, a client or potential client may choose not to outsource its business, including by setting up captive outsourcing operations or by performing formerly outsourced services themselves.

Our Brokerage business competes with numerous firms for retail insurance clients, including AmWINS Group, Inc., Arthur J. Gallagher & Co., Brown & Brown, Inc. and The Swett & Crawford Group, Inc. Many of our Brokerage competitors have relationships with insurance companies or have a significant presence in niche insurance markets that may give them an advantage over us. Because relationships between insurance intermediaries and insurance companies or clients are often local or regional in nature, this potential competitive disadvantage is particularly pronounced outside of California. This could also impact our ability to compete effectively

8

in any new states or regions that we enter. A number of standard market insurance companies are engaged in the sale of products that compete with those products we offer. These carriers sell their products directly through retail agents and brokers, without the involvement of a wholesale broker, which may yield higher commissions to retail agents and brokers and may impact our ability to compete. In addition, the Internet continues to evolve as a source for direct placement of personal lines insurance business. Although we are uniquely positioned in the Facultative Reinsurance marketplace with no comparable companies currently providing similar services, systems such as Aon's FAConnect, the LexisNexis Insurance Exchange and the Lloyd's Exchange have technology platforms that could provide solutions which could directly compete with us in the future.

In addition, the Gramm-Leach-Bliley Financial Services Modernization Act of 1999 and regulations enacted thereunder permit banks, securities firms and insurance companies to affiliate. As a result, the financial services industry has experienced and may continue to experience consolidation, which in turn has resulted and could continue to result in increased competition from diversified financial institutions, including competition for acquisition prospects.

Regulation

We are subject to the reporting requirements of the Exchange Act, and its rules and regulations, which requires us to file reports, proxy statements and other information with the Securities and Exchange Commission ("SEC").

Our Payment Protection, BPO and Brokerage businesses are subject to extensive regulation and supervision, including at the federal, state, local and foreign level. We cannot predict the impact of future changes to such laws or regulations on our business. Future laws and regulations, or the interpretation thereof, may have a material adverse effect on our results of operations, financial condition and cash flows.

Regulation - Payment Protection Segment

State Regulation

Our insurance operations and subsidiaries are subject to regulation in the various states and jurisdictions in which they transact business. State insurance laws and regulations regulate most aspects of our insurance businesses, and our insurance subsidiaries are regulated by the insurance departments of the states in which they are domiciled and licensed. Our non-U.S. insurance operations are principally regulated by insurance regulatory authorities in the jurisdictions in which they are domiciled (i.e., Turks and Caicos). Our insurance products and thus our businesses also are affected by U.S. federal, state and local tax laws, and the tax laws of non-U.S. jurisdictions.

The extent of U.S. state insurance regulation varies, but generally derives from statutes that delegate regulatory, supervisory and administrative authority to a department of insurance in each state. The purpose of the laws and regulation affecting our insurance operations is primarily to protect the policyholders and not our stockholders or our agents (i.e., the financial institutions that sell our products to their customers). The regulation, supervision and administration by state departments of insurance relate, among other things, to: standards of solvency that must be met and maintained; the payment of dividends; changes in control of insurance companies; the licensing of insurers and their agents and other producers; the types of insurance that may be written; privacy practices; the ability to enter and exit certain insurance markets; the nature of and limitations on investments and premium rates, or restrictions on the size of risks that may be insured under a single policy; reserves and provisions for unearned premiums, losses and other obligations; deposits of securities for the benefit of policyholders; payment of sales compensation to third parties; approval of policy forms; and the regulation of market conduct, including underwriting and claims practices.

Insurance Holding Company Statutes. As a holding company, we are not regulated as an insurance company, but because we own capital stock in insurance subsidiaries, we are subject to the state insurance holding company statutes, as well as certain other laws of each of the states of domicile of our insurance subsidiaries. All holding company statutes, as well as other laws, require disclosure and in many instances, prior regulatory approval of material transactions between an insurance company and an affiliate. The holding company statutes, as well as other laws, also require, among other things, prior regulatory approval of an acquisition of control of a domestic insurer, certain transactions between affiliates and payments of extraordinary dividends or distributions. Transactions within the holding company system affecting insurers must be fair and reasonable, and each insurer's policyholder surplus following any such transaction must be both reasonable in relation to its outstanding liabilities and adequate for its needs.

Dividends Limitations. We are a holding company and have limited direct operations. Our holding company assets consist primarily of the capital stock of our subsidiaries. Accordingly, our future cash flows depend upon the availability of dividends and other payments from our subsidiaries, including statutorily permissible payments from our insurance company subsidiaries, as well as payments under our tax allocation agreement and management agreements with our subsidiaries. The ability of our insurance company subsidiaries to pay such dividends and to make such other payments will be limited by applicable laws and regulations of the states in which our subsidiaries are domiciled and in which our subsidiaries operate, which vary from state to state and by type of insurance provided by the applicable subsidiary. These laws and regulations require, among other things, our insurance subsidiaries to maintain minimum solvency requirements and limit the amount of dividends these subsidiaries can pay to the holding company. Along with solvency regulations, the primary factor in determining the amount of capital available for potential dividends is the level of capital needed to maintain desired financial strength ratings from A.M. Best for our insurance company subsidiaries. Given recent economic events that

9

have affected the insurance industry, both regulators and rating agencies could become more conservative in their methodology and criteria, including increasing capital requirements for our insurance subsidiaries which, in turn, could negatively affect our capital resources. The following table sets forth the dividends paid to us by our insurance company subsidiaries for the following periods:

| For the Years Ended December 31, | |||||||||||

| (in thousands) | 2012 | 2011 | 2010 | ||||||||

| Ordinary dividends | $ | 2,783 | $ | 6,956 | $ | 7,572 | |||||

| Extraordinary dividends | — | 830 | 2,474 | ||||||||

| Total dividends | $ | 2,783 | $ | 7,786 | $ | 10,046 | |||||

Regulation of Investments. Our insurance company subsidiaries must comply with their respective state of domicile's laws regulating insurance company investments. These laws prescribe the kind, quality and concentration of investments and while unique to each state, the laws are modeled on the standards promulgated by the National Association of Insurance Commissioners ("NAIC"). Such investment laws are generally permissive with respect to federal, state and municipal obligations, and more restrictive with respect to corporate obligations, particularly non-investment grade obligations, foreign investment, equity securities and real estate investments. Each insurance company is therefore limited by the investment laws of its state of domicile from making excessive investments in any given security (such as single issuer limitations) or in certain classes or riskier investments (such as aggregate limitation in non-investment grade bonds). The diversification requirements are broadly consistent with our investment strategies. Failure to comply with these laws and regulations would cause investments exceeding regulatory limitations to be treated as non-admitted assets for the purpose of measuring surplus, and, in some instances, would require divestiture of such non-complying investments. We believe the investments made by our insurance subsidiaries comply with these laws and regulations.

Risk-Based Capital Requirements. The NAIC has adopted a model act with risk-based capital ("RBC") formulas to be applied to insurance companies. RBC is a method of measuring the amount of capital appropriate for an insurance company to support its overall business operations in light of its size and risk profile. RBC standards are used by state insurance regulators to determine appropriate regulatory actions relating to insurers that show signs of weak or deteriorating conditions. The domiciliary states of our insurance subsidiaries have adopted laws substantially similar to the NAIC's RBC model act. RBC requirements determine minimum capital requirements and are intended to raise the level of protection for policyholder obligations. RBC levels are not intended as a measure to rank insurers generally, and the insurance laws in the domiciliary states of our subsidiaries generally restrict the public dissemination of insurers' RBC levels. Under laws adopted by individual states, insurers having total adjusted capital less than that required by the RBC calculation will be subject to varying degrees of regulatory action, depending on the level of capital inadequacy.

Federal Regulation

Dodd-Frank Wall Street Reform and Consumer Protection Act. In July 2010, President Obama signed into law the Dodd-Frank Wall Street Reform and Consumer Protection Act (the "Dodd-Frank Act"), which implements comprehensive changes to the regulatory landscape of financial services in the U.S. Many aspects of the Dodd-Frank Act are subject to rule-making and will take effect over several years, making it difficult to anticipate the overall financial impact on our business, our customers or the insurance and financial services industries.

In addition, Congress created the Consumer Financial Protection Bureau (the "CFPB"). While the CFPB does not have direct jurisdiction over insurance products, it is possible that regulations promulgated by the CFPB may extend its authority to cover these products and thereby potentially affecting the Company's business or the clients that we serve.

Gramm-Leach-Bliley Act. On November 12, 1999, the Gramm-Leach-Bliley Act of 1999 became law, implementing fundamental changes in the regulation of the financial services industry in the United States. The Gramm-Leach-Bliley Act permits the transformation of the already converging banking, insurance and securities industries by permitting mergers that combine commercial banks, insurers and securities firms under one holding company. Under the Gramm-Leach-Bliley Act, community banks retain their existing ability to sell insurance products in some circumstances. Privacy provisions of the Gramm-Leach-Bliley Act became fully effective in 2001. These provisions established consumer protections regarding the security and confidentiality of nonpublic personal information and, as implemented through state insurance laws and regulations, require us to make full disclosure of our privacy policies to customers.

Health Insurance Portability and Accountability Act of 1996 ("HIPAA"). Through HIPAA, the Department of Health and Human Services imposes obligations for issuers of health and dental insurance coverage and health and dental benefit plan sponsors. HIPAA established requirements for maintaining the confidentiality and security of individually identifiable health information and new standards for electronic health care transactions. The Department of Health and Human Services promulgated final HIPAA regulations in 2002. The privacy regulations required compliance by April 2003, the electronic transactions regulations by October 2003 and the security regulations by April 2005. Recently, parts of HIPAA were amended under the HITECH Act, and pursuant to these amendments, new regulations have been issued requiring notification of government agencies and consumers in the event of certain security breaches involving personal health information.

10

HIPAA is far-reaching and complex and proper interpretation and practice under the law continue to evolve. Consequently, our efforts to measure, monitor and adjust our business practices to comply with HIPAA are ongoing. Failure to comply could result in regulatory fines and civil lawsuits. Knowing and intentional violations of these rules may also result in federal criminal penalties.

Foreign Jurisdictions. A portion of our business is ceded to our reinsurance subsidiaries domiciled in Turks and Caicos. Those subsidiaries must satisfy local regulatory requirements, such as filing annual financial statements, filing annual certificates of compliance and paying annual fees. If we fail to maintain compliance with applicable laws, rules and regulations, the licenses issued by the regulatory authority in Turks and Caicos could be subject to modification or revocation, and our subsidiaries could be prevented from conducting business.

Regulation - BPO Segment

We are subject to federal and state laws and regulations, particularly related to our administration of insurance products on behalf of other insurers. In order for us to process and administer insurance products of other companies, we are required to maintain licenses of a third party administrator in the states where those insurance companies operate. With regard to our third party administration operations, we also must comply with the related federal and state privacy laws that similarly apply to our insurance operations.

We are also subject to laws and regulations on direct marketing, such as the Telemarketing Consumer Fraud and Abuse Prevention Act and the Telemarketing Sales Rule, the Telephone Consumer Protection Act, the Do-Not-Call Implementation Act and rules promulgated by the Federal Communications Commission and the Federal Trade Commission and the CAN-SPAM Act. Failure to comply with the provisions of such acts and rules could result in fines and penalties.

As a business process outsourcer for insurers and financial institutions, we are subject to data protection and privacy laws, such as the Gramm-Leach-Bliley Act as well as HIPAA and certain state data privacy laws. In addition, the terms of our contracts typically require us to comply with applicable laws and regulations. If we fail to comply with any applicable laws or regulations, we may be restricted in our ability to provide services and may also be subject to civil or criminal penalties, litigation as well as contract termination.

Regulation - Brokerage Segment

Our Brokerage and premium finance operations are subject to regulation at the federal, state and local levels. B&G and our designated employees must be licensed to act as agents, brokers, producers and/or agencies by state regulatory authorities in the states where we conduct business. Regulations and licensing laws vary by state and are often complex and subject to interpretation and enforcement by the relevant departments of insurance.

Laws and regulations vary from state to state and are always subject to amendment or interpretation by regulatory authorities. These authorities have substantial discretion as to the decision to grant, renew and revoke licenses and approvals. Our continuing ability to do business in the states in which we currently operate depends on the validity of and continued good standing under the licenses and approvals pursuant to which we operate. More restrictive laws, rules or regulations may be adopted in the future that could make compliance more difficult and expensive or adversely affect our business. For further information, see "Item 1A. Risk Factors" of this Annual Report under "Risks Related to Regulatory and Legal Matters - We are subject to extensive governmental laws and regulations, which increase our costs and could restrict the conduct of our business."

Seasonality

Our financial results may be affected by seasonal variations. Revenues in our Payment Protection business may fluctuate seasonally based on consumer spending trends, where consumer spending has historically been higher in September and December, corresponding to back-to-school and the holiday season. Accordingly, our Payment Protection revenues may reflect higher third and fourth quarters than in the first half of the year.

Revenues in our Brokerage business may fluctuate seasonally based on policy renewal dates, which are typically concentrated in July and December, the months during our third and fourth quarters. In addition, our quarterly revenues may be affected by new placements, cancellations or non-renewals of large policies because commission revenues are earned on the effective date as opposed to ratably over the year. Our quarterly Brokerage revenues may also be affected by the amount of profit commissions received from insurance carriers, since profit commissions are primarily received in the first and second quarters of each year.

Employees

At December 31, 2012, we employed approximately 700 people, which includes the employees from the December 31, 2012 acquisitions of ProtectCELL and 4Warranty, on a full or part-time basis. None of our employees are represented by unions or trade organizations. We believe that our relations with our employees are satisfactory.

Intellectual Property

We own or license a number of trademarks, patents, trade names, copyrights, service marks, trade secrets and other intellectual property rights that relate to our services and products. Although we believe that these intellectual property rights are, in the aggregate, of

11

material importance to our businesses, we believe that none of our businesses are materially dependent upon any particular trademark, trade name, copyright, service mark, license or other intellectual property right. U.S. trademark and service mark registrations are generally for a term of 10 years, renewable every 10 years as long as the trademark or service mark is used in the regular course of trade. We have entered into confidentiality agreements with our clients. These agreements impose restrictions on such clients' use of our proprietary software and other intellectual property rights.

Web Site Access to Fortegra's Filings with the SEC

We maintain an Internet website at www.fortegra.com. The information that appears on our website is not part of, and is not incorporated into, this Annual Report. We will make available free of charge on our website our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act and the rules promulgated thereunder, as soon as reasonably practicable after electronically filing or furnishing such material to the SEC. All filings with the SEC are posted to our website in the "Investor Relations" tab under the section "Financial Information." Upon written request of any stockholder of record on December 31, 2012, Fortegra will provide, without charge, a printed copy of its 2012 Annual Report as required to be filed with the SEC. To obtain a copy of the 2012 Annual Report, Contact: Investor Relations, Fortegra Financial Corporation, 10151 Deerwood Park Boulevard, Building 100, Suite 330, Jacksonville, FL, 32256, or call (866)-961-9529.

Copies of all of Fortegra's filings and other information may also be obtained electronically from the SEC's website at www.sec.gov. or may be read and copied at the: SEC Public Reference Room, 100 F Street, NE, Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling the SEC at 1-800-SEC-0330.

ITEM 1A. RISK FACTORS

The following are certain risks that management believes are specific to our business. This should not be viewed as an all-inclusive list of risks or presenting the risk factors listed in any particular order. You should carefully consider the risks described below, together with the other information contained in this report and in our other filings with the SEC when evaluating our Company. Should any of the events discussed in the risk factors below occur, our business, results of operations or financial condition could be materially affected. Additional risks unknown at this time, or risks we currently deem immaterial, may also impact our financial condition or results of operations.

Risks Related to our Business and Industries

General economic and financial market conditions may have a material adverse effect on the business, results of operations, cash flows and financial condition of all of our business segments.

General economic and financial market conditions, including the availability and cost of credit, the loss of consumer confidence, reduction in consumer or business spending, inflation, unemployment, energy costs and geopolitical issues, have contributed to increased uncertainty and volatility as well as diminished expectations for the U.S. economy and the financial markets. These conditions could materially and adversely affect each of our businesses. Adverse economic and financial market conditions could result in:

| • | a reduction in the demand for, and availability of, consumer credit, which could result in reduced demand by consumers for our Payment Protection products and our Payment Protection clients opting to no longer make such products available; |

| • | higher than anticipated loss ratios on our Payment Protection products due to rising unemployment or disability claims; |

| • | higher risk of increased fraudulent insurance claims; |

| • | individuals terminating loans or canceling credit insurance policies, thereby reducing our revenues; |

| • | A reduction in the demand for consumer warranty products, service contract offerings, and motor club memberships; |

| • | individuals terminating warranty products, service contract or motor club memberships, thereby reducing our revenues; |

| • | businesses reducing the amount of coverage under surplus lines and specialty admitted insurance policies or allowing such policies to lapse thereby reducing our premium or commission income in our Brokerage business; |

| • | a reduction in demand for new surplus lines and specialty insurance policies from retail insurance brokers and agents or retail insurance brokers and agents and insurance companies ceasing to offer our surplus lines and specialty insurance products and related services from our Brokerage business; |

| • | a contraction in the reinsurance market caused by reduced demand by major insurers, reduced supply by reinsurers or other factors or reduced reinsurance demand by our insurance customers due to market conditions; |

| • | our clients being more likely to experience financial distress or declare bankruptcy or liquidation, which could have an adverse impact on demand for our services and products and the remittance of premiums from such customers, as well as the collection of receivables from such clients for items such as unearned premiums, commissions or BPO-related accounts receivable, which could make the collection of receivables from our clients more difficult; |

| • | increased pricing sensitivity or reduced demand for our services and products; |

| • | increased costs associated with, or the inability to obtain, debt financing to fund acquisitions or the expansion of our businesses; and |

| • | defaults in our fixed income investment portfolio or lower than anticipated rates of return as a result of low interest rate environments. |

12

If we are unable to successfully anticipate changing economic or financial market conditions, we may be unable to effectively plan for or respond to such changes, and our business, results of operations and financial condition could be materially and adversely affected.

We face significant competitive pressures in each of our businesses, which could materially and adversely affect our business, results of operations and financial condition.

We face significant competition in each of our businesses. Competition in our businesses is based on many factors, including price, industry knowledge, quality of client service, the effectiveness of our sales force, technology platforms and processes, the security and integrity of our information systems, the financial strength ratings of our insurance subsidiaries, office locations, breadth of services and products and brand recognition and reputation. Some competitors may offer a broader array of services and products, may have a greater diversity of distribution resources, may have better brand recognition, may have lower cost structures or, with respect to insurers, may have higher financial strength or claims paying ratings. Some competitors also have larger client bases than we do. In addition, new competitors could enter our markets in the future, and existing competitors may gain strength by forging new business relationships. The competitive landscape for each of our businesses is described below.

| • | Payment Protection - In our Payment Protection business, we compete with insurance companies, financial institutions, extended service plan providers, membership plan providers and other insurance and warranty service providers. The principal competitors for our Payment Protection business include The Warranty Group, Assurant, Inc., Asurion Corporation, eSecuritel Holdings, LLC, Asurion, LLC, Global Warranty Group, LLC and smaller regional companies. As a result of state and federal regulatory developments and changes in prior years, certain financial institutions are able to offer debt cancellation plans and are also able to affiliate with other insurance companies in order to offer services similar to those in our Payment Protection business. This has resulted in new competitors, some of whom have significant financial resources, entering some of our markets. As financial institutions gain experience with payment protection and warranty programs, their reliance on our services and products may diminish. |

| • | BPO - Our BPO business competes with a variety of companies, including large multinational firms that provide consulting, technology and/or business process services, off-shore business process service providers in low-cost locations like India, and in-house captive insurance companies of potential clients. Our principal business process outsourcing competitors include Aon Corporation, Computer Sciences Corporation, Direct Response Insurance Administrative Services, Inc., Marsh & McLennan Companies, Inc., Dell Services and Unisys Corporation. The trend toward outsourcing and technological changes may also result in new and different competitors entering our markets. There could also be newer competitors with strong competitive positions as a result of consolidation of smaller competitors or of companies that each provide different services or serve different industries. |

| • | Brokerage - Our Brokerage business competes for retail insurance clients with numerous firms, including AmWINS Group, Inc., Arthur J. Gallagher & Co., Brown & Brown, Inc. and The Swett & Crawford Group, Inc. Many of our Brokerage competitors have relationships with insurance companies or have a significant presence in niche insurance markets that may give them an advantage over us. Because relationships between insurance intermediaries and insurance companies or clients are often local or regional in nature, this potential competitive disadvantage is particularly pronounced outside of California. This could also impact our ability to compete effectively in any new states or regions that we enter. A number of standard market insurance companies are engaged in the sale of products that compete with those products we offer. These carriers sell their products directly through retail agents and brokers without the involvement of a wholesale broker, which may yield higher commissions to retail agents and brokers and may impact our ability to compete. Although we are uniquely positioned in the Facultative Reinsurance marketplace with no comparable companies currently providing similar services. Systems such as Aon's FAConnect, the LexisNexis Insurance Exchange and the Lloyd's Exchange have technology platforms that could provide solutions which could directly compete with us in the future. |

We expect competition to intensify in each of our businesses. Increased competition may result in lower prices and volumes, higher personnel and sales and marketing costs, increased technology expenditures and lower profitability. We may not be able to supply clients with services or products that they deem superior and at competitive prices and we may lose business to our competitors. If we are unable to compete effectively in any of our business segments, it would have a material adverse effect on our business, results of operations and financial condition.

Our results of operations may fluctuate significantly, which makes our future results of operations difficult to predict. If our results of operations fall below expectations, the price of our common stock could decline.

Our annual and quarterly results of operations have fluctuated in the past and may fluctuate significantly in the future due to a variety of factors, many of which are beyond our control. In addition, our expenses as a percentage of revenues may be significantly different than our historical rates. As a result, comparing our results of operations on a period-to-period basis may not be meaningful. Factors that may cause our results of operations to fluctuate from period-to-period include:

| • | demand for our services and products; |

| • | the length of our sales cycle; |

| • | the amount of sales to new clients: |

| • | the timing of implementations of our services and products with new clients; |

| • | pricing and availability of surplus lines and other specialty insurance products coverages; |

13

| • | seasonality; |

| • | the timing of acquisitions; |

| • | competitive factors; |

| • | prevailing interest rates; |

| • | pricing changes by us or our competitors; |

| • | transaction volumes in our clients' businesses; |

| • | the introduction of new services and products by us and our competitors; |

| • | changes in strategic partnerships; |

| • | changes in regulatory and accounting standards; and |

| • | our ability to control costs. |

In addition, our Payment Protection revenues can vary depending on the level of consumer activity and the success of our clients in selling products. In our Brokerage business, our commission and fee income can vary due to the timing of policy renewals, as well as the timing and amount of the receipt of profit commission payments and fees and the net effect of new and lost business production. We do not control the factors that cause these variations. Specifically, third party customers' demand for insurance products can influence the timing of renewals, new business, lost business (which includes policies that are not renewed) and cancellations. In addition, we rely on retail insurance brokers and agents and insurance companies for the payment of certain commissions. Because these payments are processed internally by these companies, we may not receive a payment that is otherwise expected from a particular firm in one period until after the end of that period, which can adversely affect our ability to budget for such period.

Our results of operations could be materially and adversely affected if we fail to retain our existing clients, cannot sell additional services and products to our existing clients, do not introduce new or enhanced services and products or are not able to attract and retain new clients.

Our revenue and revenue growth are dependent on our ability to retain clients, to sell those clients additional services and products, to introduce new services and products and to attract new clients in each of our businesses. Our ability to increase revenues will depend on a variety of factors, including:

| • | the quality and perceived value of our product and service offerings by existing and new clients; |

| • | the effectiveness of our sales and marketing efforts; |

| • | the speed with which our Brokerage business can respond to requests for price quotes from retail insurance agents and brokers, and the availability of competitive services and products from our carriers; |

| • | the successful installation and implementation of our services and products for new and existing Payment Protection and BPO clients; |

| • | availability of capital to complete investments in new or complementary products, services and technologies; |

| • | the availability of adequate reinsurance for us and our clients, including the ability of our clients to form, capitalize and operate captive reinsurance companies; |

| • | our ability to find suitable acquisition candidates, successfully complete such acquisitions and effectively integrate such acquisitions; |

| • | our ability to integrate technology into our services and products to avoid obsolescence and provide scalability; |

| • | the reliability, execution and accuracy of our services, particularly our BPO services; and |

| • | client willingness to accept any price increases for our services and products. |

In addition, we are subject to risks of losing clients due to consolidation in each of the markets we serve. Our inability to retain existing clients, sell additional services and products, or successfully develop and implement new and enhanced services and products and attract new clients and, accordingly, increase our revenues could have a material adverse effect on our results of operations.

We typically face a long selling cycle to secure new clients in each of our businesses as well as long implementation periods that require significant resource commitments, which result in a long lead time before we receive revenues from new client relationships.

The industries in which we compete generally consist of mature businesses and markets and the companies that participate in these industries have well-established business operations, systems and relationships. Accordingly, each of our businesses typically faces a long selling cycle to secure a new client. Even if we are successful in obtaining a new client engagement, it is generally followed by a long implementation period in which the services are planned in detail and we demonstrate to the client that we can successfully integrate our processes and resources with their operations. We also typically negotiate and enter into a contractual relationship with the new client during this period. There is then a long implementation period in order to commence providing the services.

We typically incur significant business development expenses during the selling cycle. We may not succeed in winning a new client's business, in which case we receive no revenues and may receive no reimbursement for such expenses. Even if we succeed in developing a relationship with a potential client and begin to plan the services in detail, such potential client may choose a competitor or decide to retain the work in-house prior to the time a final contract is signed. If we enter into a contract with a client, we will typically receive no revenues until implementation actually begins. In addition, a significant portion of our revenue is based upon the success of our clients' marketing programs, which may not generate the transaction volume we anticipate. Our clients may also experience delays in obtaining internal approvals or delays associated with technology or system implementations, thereby further lengthening the implementation cycle. If we are not successful in obtaining contractual commitments after the selling cycle, in maintaining contractual

14

commitments after the implementation cycle or in maintaining or reducing the duration of unprofitable initial periods in our contracts, it may have a material adverse effect on our business, results of operations and financial condition. Furthermore, the time and effort required to complete the implementation phases of new contracts makes it difficult to accurately predict the timing of revenues from new clients as well as our costs.

Acquisitions are a significant part of our growth strategy and we may not be successful in identifying suitable acquisition candidates, completing such acquisitions or integrating the acquired businesses, which could have a material adverse effect on our business, results of operations, financial condition or growth.

Historically, acquisitions have played a significant role in our expansion into new businesses and in the growth of some of our businesses. Acquiring complementary businesses is a significant component of our growth strategy. Accordingly, we frequently evaluate possible acquisition transactions for our business. However, we may not be able to identify suitable acquisitions, and such transactions may not be financed and completed on acceptable terms. We may incur significant expenses in evaluating such acquisitions. Furthermore, any future acquisitions may not be successful. In addition, we may be competing with larger competitors with substantially greater resources for acquisition targets. Any deficiencies in the process of integrating companies we may acquire could have a material adverse effect on our results of operations and financial condition. Acquisitions entail a number of risks including, among other things:

| • | failure to achieve anticipated revenues, earnings or cash flow; |

| • | increased expenses; |

| • | diversion of management time and attention; |

| • | failure to retain the acquired business' customers or personnel; |

| • | difficulties in realizing projected efficiencies; |

| • | ability to realize synergies and cost savings; |

| • | difficulties in integrating systems and personnel; and |

| • | inaccurate assessment of liabilities. |