Other than the adjustment for estimated property-level transaction costs, the Board’s determination of the 2023 NAV was undertaken in accordance with the Company’s valuation policy and the recommendations and methodologies of the Institute for Portfolio Alternatives, a trade association for non-listed direct investment vehicles (“IPA”), as set forth in the Investment Program Association Practice Guideline 2013-01 “Valuations of Publicly Registered Non-Listed REITs” dated April 29, 2013 (“IPA Practice Guideline”).

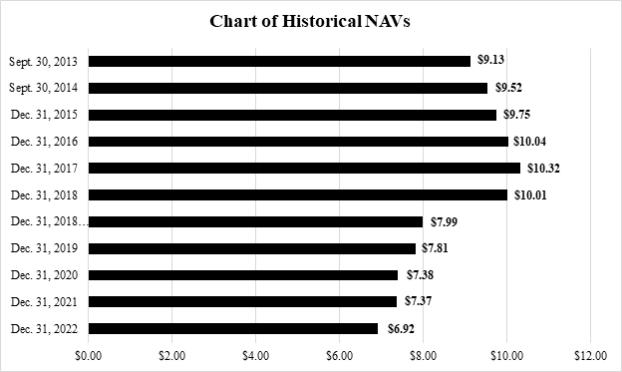

The 2023 NAV represents a snapshot in time as of December 31, 2023, will likely change, and does not represent the amount a stockholder would receive now or in the future for his or her shares of the Company’s common stock. The 2023 NAV is based on a number of assumptions, estimates and data that are inherently imprecise and susceptible to uncertainty and changes in circumstances. Please see “Valuation Methodologies and Major Assumptions,” “Valuation Summary,” and “Additional Information Regarding the Valuation, Limitations of the 2023 NAV and Stanger” in this Current Report, below.

The Company will hold a webinar on March 14, 2024, at 2:30 p.m., Eastern Time, to review the 2023 NAV.

Valuation Methodologies and Major Assumptions

As of the Valuation Date, the Company’s real estate portfolio consisted of interests in 70 properties, including 69 seniors housing communities and one vacant land parcel (the “Appraised Properties” or “Appraised Property”). The Appraised Properties were valued using valuation and appraisal methodologies consistent with real estate industry standards and practices, as described further below.

As of the Valuation Date, the aggregate estimated value of the Appraised Properties was approximately $1.67 billion. To estimate the value of the Appraised Properties, Stanger conducted an appraisal of each asset. In determining the value of each Appraised Property, Stanger utilized all information that it deemed relevant, including information from the Company’s advisor CNL Healthcare Corp. (the “Advisor”) and its own data sources, which data sources included trends in capitalization rates, leasing rates and other economic factors. In conducting its appraisals of the Appraised Properties, and pursuant to its engagement, Stanger utilized the income approach to valuation, which included a discounted cash flow (“DCF”) analysis and/or direct capitalization analysis to determine value (other than the vacant land parcel). Stanger relied solely on DCF analyses in determining the appraised value of 54 RIDEA seniors housing properties and two leased properties. Stanger utilized direct capitalization analyses for 13 leased seniors housing properties and used a sales comparison approach for the land parcels (which includes one vacant land parcel and excess or surplus land) in the 2023 NAV. Stanger also considered macroeconomic factors such as inflation and the lingering impacts of the COVID-19 pandemic (“COVID-19”) on the Appraised Properties.

For properties in which a DCF analysis was utilized, pro forma statements of operations for such properties including revenues, expenses and capital expenditures, were analyzed and projected over a multi-year period (typically ten years). A reversion value is estimated based on pro forma statements of operations after the holding period and then capitalized at an appropriate terminal capitalization rate reflecting the age and anticipated functional and economic obsolescence and competitive position of such properties to determine their reversion value. Net proceeds to owners are determined by deducting appropriate costs of sale in the reversion year. The discount rate selected for the DCF analysis is based upon estimated target rates of return for buyers of similar properties with consideration given to unique property-related factors, lease-up projections, location and age. The discount rate is then applied to the projected cash flows to derive a net present value.

The direct capitalization analysis was performed by applying a market capitalization rate for each applicable Appraised Property to the estimated stabilized forward-year annual net operating income. In selecting each capitalization rate, Stanger considered, among other factors, prevailing capitalization rates in the applicable property sector, the property’s location, age and condition, the property’s operating trends, the anticipated year of stabilization, the lease coverage ratios and other unique property factors.

As applicable, Stanger adjusted the capitalized value of each Appraised Property for any excess land, deferred maintenance or capital needs and lease-up costs to estimate the “as-is” value of each Appraised Property as of the Valuation Date. Stanger then adjusted the “as-is” property values, as appropriate, for the Company’s allocable ownership interest in the Appraised Properties to account for the interest of any third-party investment partners, including any priority distributions.