UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2015

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number: 000-54685

CNL Healthcare Properties, Inc.

(Exact name of registrant as specified in its charter)

Maryland | | 27-2876363 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

| | |

CNL Center at City Commons 450 South Orange Avenue Orlando, Florida | | 32801 |

(Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code (407) 650-1000

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | o | Accelerated filer | o |

| | | |

Non-accelerated filer | x (Do not check if a smaller reporting company) | Smaller reporting company | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

The number of shares of common stock of the registrant outstanding as of November 11, 2015 was 173,657,093.

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

INDEX

Item 1. Financial Statements

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED BALANCE SHEETS (UNAUDITED)

(in thousands, except per share data)

| | September 30, | | | December 31, | |

| | 2015 | | | 2014 | |

ASSETS | | | | | | | | |

Real estate assets: | | | | | | | | |

Real estate investment properties, net (including VIEs $192,663 and $174,449, respectively) | | $ | 2,251,200 | | | $ | 1,657,500 | |

Real estate under development, including land (including VIEs $67,350 and $47,153, respectively) | | | 69,478 | | | | 47,153 | |

Total real estate assets, net | | | 2,320,678 | | | | 1,704,653 | |

Intangibles, net (including VIEs $24,426 and $25,519, respectively) | | | 163,538 | | | | 140,264 | |

Cash (including VIEs $1,462 and $6,280, respectively) | | | 51,185 | | | | 91,355 | |

Other assets (including VIEs $862 and $511, respectively) | | | 22,024 | | | | 19,738 | |

Deferred rent and lease incentives (including VIEs $6,330 and $2,978, respectively) | | | 21,244 | | | | 8,240 | |

Loan costs, net (including VIEs $2,497 and $2,300, respectively) | | | 12,604 | | | | 14,012 | |

Restricted cash (including VIEs $2,053 and $5,304, respectively) | | | 8,816 | | | | 10,753 | |

Total assets | | $ | 2,600,089 | | | $ | 1,989,015 | |

LIABILITIES AND EQUITY | | | | | | | | |

Liabilities: | | | | | | | | |

Mortgages and other notes payable, net (including VIEs $172,537 and $137,754, respectively) | | $ | 865,263 | | | $ | 853,561 | |

Credit facilities | | | 390,000 | | | | 206,403 | |

Accounts payable and accrued liabilities (including VIEs $10,351 and $10,268, respectively) | | | 39,862 | | | | 26,444 | |

Other liabilities (including VIEs $4,551 and $4,949, respectively) | | | 37,880 | | | | 27,448 | |

Due to related parties (including VIEs $171 and $219, respectively) | | | 5,620 | | | | 2,999 | |

Total liabilities | | | 1,338,625 | | | | 1,116,855 | |

Commitments and contingencies (Note 14) | | | | | | | | |

Redeemable noncontrolling interest | | | 568 | | | | 568 | |

Stockholders' equity: | | | | | | | | |

Preferred stock, $0.01 par value per share, 200,000 shares authorized; none issued or outstanding | | ― | | | ― | |

Excess shares, $0.01 par value per share, 300,000 shares authorized; none issued or outstanding | | ― | | | ― | |

Common stock, $0.01 par value per share, 1,120,000 shares authorized, 172,682 and 116,672 shares issued, and 171,575 and 116,256 shares outstanding, respectively | | | 1,715 | | | | 1,163 | |

Capital in excess of par value | | | 1,501,420 | | | | 1,007,326 | |

Accumulated loss | | | (133,725 | ) | | | (83,091 | ) |

Accumulated distributions | | | (94,233 | ) | | | (49,342 | ) |

Accumulated other comprehensive loss | | | (14,649 | ) | | | (4,864 | ) |

Total stockholders' equity | | | 1,260,528 | | | | 871,192 | |

Noncontrolling interest | | | 368 | | | | 400 | |

Total equity | | | 1,261,464 | | | | 872,160 | |

Total liabilities and equity | | $ | 2,600,089 | | | $ | 1,989,015 | |

The abbreviation VIEs above means variable interest entities. | | | | | | | | |

See accompanying notes to condensed consolidated financial statements

2

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS (UNAUDITED)

(in thousands, except per share data)

| | Quarter Ended | | | Nine Months Ended | |

| | September 30, | | | September 30, | |

| | 2015 | | | 2014 | | | 2015 | | | 2014 | |

Revenues: | | | | | | | | | | | | | | | | |

Rental income from operating leases | | $ | 28,435 | | | $ | 13,393 | | | $ | 72,306 | | | $ | 33,478 | |

Resident fees and services | | | 47,505 | | | | 34,162 | | | | 129,262 | | | | 86,636 | |

Tenant reimbursement income | | | 3,964 | | | | 1,957 | | | | 10,845 | | | | 4,787 | |

Interest income on note receivable from related party | | ― | | | | 148 | | | ― | | | | 498 | |

Total revenues | | | 79,904 | | | | 49,660 | | | | 212,413 | | | | 125,399 | |

Operating expenses: | | | | | | | | | | | | | | | | |

Property operating expenses | | | 39,923 | | | | 25,716 | | | | 105,088 | | | | 64,703 | |

General and administrative | | | 2,239 | | | | 1,997 | | | | 6,823 | | | | 5,689 | |

Acquisition fees and expenses | | | 9,073 | | | | 3,729 | | | | 15,939 | | | | 15,726 | |

Asset management fees | | | 5,085 | | | | 2,753 | | | | 13,426 | | | | 5,572 | |

Property management fees | | | 3,923 | | | | 2,358 | | | | 10,539 | | | | 6,118 | |

Contingent purchase price consideration adjustment | | | (268 | ) | | | 1,800 | | | | (589 | ) | | | 479 | |

Impairment provision | | ― | | | ― | | | | 4,661 | | | ― | |

Loss on lease terminations | | ― | | | ― | | | | 863 | | | ― | |

Depreciation and amortization | | | 27,854 | | | | 17,550 | | | | 75,147 | | | | 44,111 | |

Total operating expenses | | | 87,829 | | | | 55,903 | | | | 231,897 | | | | 142,398 | |

Operating loss | | | (7,925 | ) | | | (6,243 | ) | | | (19,484 | ) | | | (16,999 | ) |

Other income (expense): | | | | | | | | | | | | | | | | |

Interest and other income | | | 28 | | | | 7 | | | | 138 | | | | 27 | |

Interest expense and loan cost amortization | | | (10,990 | ) | | | (8,549 | ) | | | (30,369 | ) | | | (21,654 | ) |

Equity in loss of unconsolidated entities | | | (151 | ) | | | (180 | ) | | | (656 | ) | | | (1,193 | ) |

Gain on purchase of controlling interest of investment in unconsolidated entity | | ― | | | | 2,798 | | | ― | | | | 2,798 | |

Total other expense | | | (11,113 | ) | | | (5,924 | ) | | | (30,887 | ) | | | (20,022 | ) |

Loss before income taxes | | | (19,038 | ) | | | (12,167 | ) | | | (50,371 | ) | | | (37,021 | ) |

Income tax expense | | | (193 | ) | | | (37 | ) | | | (279 | ) | | | (9 | ) |

Net loss | | | (19,231 | ) | | | (12,204 | ) | | | (50,650 | ) | | | (37,030 | ) |

Less: Net loss attributable to noncontrolling interest | | | (6 | ) | | ― | | | | (16 | ) | | ― | |

Net loss attributable to common stockholders | | $ | (19,225 | ) | | $ | (12,204 | ) | | $ | (50,634 | ) | | $ | (37,030 | ) |

Net loss per share of common stock (basic and diluted) | | $ | (0.12 | ) | | $ | (0.14 | ) | | $ | (0.34 | ) | | $ | (0.47 | ) |

Weighted average number of shares of common stock outstanding (basic and diluted) | | | 162,730 | | | | 89,597 | | | | 147,075 | | | | 78,296 | |

See accompanying notes to condensed consolidated financial statements.

3

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE LOSS (UNAUDITED)

(in thousands)

| | Quarter Ended | | | Nine Months Ended | |

| | September 30, | | | September 30, | |

| | 2015 | | | 2014 | | | 2015 | | | 2014 | |

Net loss attributable to common stockholders | | $ | (19,225 | ) | | $ | (12,204 | ) | | $ | (50,634 | ) | | $ | (37,030 | ) |

Other comprehensive income (loss): | | | | | | | | | | | | | | | | |

Unrealized income (loss) on derivative financial instruments, net | | | (6,435 | ) | | | 224 | | | | (10,060 | ) | | | (872 | ) |

Reclassification of cash flow hedges upon derecognition | | | — | | | | — | | | | 236 | | | | — | |

Reclassification of cash flow hedges due to ineffectiveness | | | 48 | | | | — | | | | 48 | | | | — | |

Unrealized income (loss) on derivative financial instruments of equity method investments | | | (1 | ) | | | (2 | ) | | | (9 | ) | | | 21 | |

Total other comprehensive income (loss) | | | (6,388 | ) | | | 222 | | | | (9,785 | ) | | | (851 | ) |

Comprehensive loss | | | (25,613 | ) | | | (11,982 | ) | | | (60,419 | ) | | | (37,881 | ) |

Less: Comprehensive loss attributable to noncontrolling interest | | | — | | | | — | | | | — | | | | — | |

Comprehensive loss attributable to common stockholders | | $ | (25,613 | ) | | $ | (11,982 | ) | | $ | (60,419 | ) | | $ | (37,881 | ) |

See accompanying notes to condensed consolidated financial statements.

4

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF STOCKHOLDERS’ EQUITY AND REDEEMABLE NONCONTROLLING INTEREST

Nine Months Ended September 30, 2015 (Unaudited) and the Year Ended December 31, 2014

(in thousands, except per share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | Accumulated | | | | | | | | | | | | | |

| | Redeemable | | | Common Stock | | | Capital in | | | | | | | | | | | Other | | | Total | | | Non- | | | | | |

| | Noncontrolling | | | Number | | | Par | | | Excess of | | | Accumulated | | | Accumulated | | | Comprehensive | | | Stockholders' | | | controlling | | | Total | |

| | Interest | | | of Shares | | | Value | | | Par Value | | | Loss | | | Distributions | | | Loss | | | Equity | | | Interest | | | Equity | |

Balance at December 31, 2013 | | $ | — | | | | 58,218 | | | $ | 582 | | | $ | 500,361 | | | $ | (30,580 | ) | | $ | (17,423 | ) | | $ | (959 | ) | | $ | 451,981 | | | $ | — | | | $ | 451,981 | |

Subscriptions received for common stock through public offering and reinvestment plan | | | — | | | | 56,006 | | | | 560 | | | | 571,764 | | | | — | | | | — | | | | — | | | | 572,324 | | | | — | | | | 572,324 | |

Stock distributions | | | — | | | | 2,356 | | | | 24 | | | | (24 | ) | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

Redemptions of common stock | | | — | | | | (324 | ) | | | (3 | ) | | | (2,993 | ) | | | — | | | | — | | | | — | | | | (2,996 | ) | | | — | | | | (2,996 | ) |

Stock issuance and offering costs | | | — | | | | — | | | | — | | | | (59,782 | ) | | | — | | | | — | | | | — | | | | (59,782 | ) | | | — | | | | (59,782 | ) |

Net loss | | | — | | | | — | | | | — | | | | — | | | | (52,511 | ) | | | — | | | | — | | | | (52,511 | ) | | | — | | | | (52,511 | ) |

Other comprehensive loss | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | (3,905 | ) | | | (3,905 | ) | | | — | | | | (3,905 | ) |

Distribution to holder of promoted interest | | | — | | | | — | | | | — | | | | (2,000 | ) | | | — | | | | — | | | | — | | | | (2,000 | ) | | | — | | | | (2,000 | ) |

Cash distributions declared and paid or reinvested ($0.4071 per share) | | | — | | | | — | | | | — | | | | — | | | | — | | | | (31,919 | ) | | | — | | | | (31,919 | ) | | | — | | | | (31,919 | ) |

Contribution from noncontrolling interests | | | 568 | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | ― | | | | 400 | | | | 968 | |

Balance at December 31, 2014 | | | 568 | | | | 116,256 | | | | 1,163 | | | | 1,007,326 | | | | (83,091 | ) | | | (49,342 | ) | | | (4,864 | ) | | | 871,192 | | | | 400 | | | | 872,160 | |

Subscriptions received for common stock through public offering and reinvestment plan | | | — | | | | 52,815 | | | | 528 | | | | 555,629 | | | | — | | | | — | | | | — | | | | 556,157 | | | | — | | | | 556,157 | |

Stock distributions | | | — | | | | 3,196 | | | | 31 | | | | (31 | ) | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | |

Redemptions of common stock | | | — | | | | (692 | ) | | | (7 | ) | | | (6,627 | ) | | | — | | | | — | | | | — | | | | (6,634 | ) | | | — | | | | (6,634 | ) |

Stock issuance and offering costs | | | — | | | | — | | | | — | | | | (54,877 | ) | | | — | | | | — | | | | — | | | | (54,877 | ) | | | — | | | | (54,877 | ) |

Net loss | | | — | | | | — | | | | — | | | | — | | | | (50,634 | ) | | | — | | | | — | | | | (50,634 | ) | | | (16 | ) | | | (50,650 | ) |

Other comprehensive loss | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | (9,785 | ) | | | (9,785 | ) | | | — | | | | (9,785 | ) |

Distribution to holder of noncontrolling interest | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | (16 | ) | | | (16 | ) |

Cash distributions declared and paid or reinvested ($0.3177 per share) | | | — | | | | — | | | | — | | | | — | | | | — | | | | (44,891 | ) | | | — | | | | (44,891 | ) | | | | | | | (44,891 | ) |

Balance at September 30, 2015 | | $ | 568 | | | | 171,575 | | | $ | 1,715 | | | $ | 1,501,420 | | | $ | (133,725 | ) | | $ | (94,233 | ) | | $ | (14,649 | ) | | $ | 1,260,528 | | | $ | 368 | | | $ | 1,261,464 | |

See accompanying notes to condensed consolidated financial statements.

5

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

(in thousands)

| | Nine Months Ended | |

| | September 30, | |

| | 2015 | | | 2014 | |

Operating activities: | | | | | | | | |

Net cash flows provided by operating activities | | $ | 32,393 | | | $ | 18,673 | |

Investing activities: | | | | | | | | |

Acquisition of properties | | | (647,538 | ) | | | (524,654 | ) |

Development of properties | | | (54,411 | ) | | | (32,893 | ) |

Capital expenditures | | | (5,840 | ) | | | (2,570 | ) |

Issuance of note receivable to related party | | ― | | | | (2,065 | ) |

Collection of note receivable from related party | | ― | | | | 5,591 | |

Distribution from unconsolidated entities | | ― | | | | 2,206 | |

Purchase of controlling interest in unconsolidated entity | | ― | | | | (1,584 | ) |

Investment in unconsolidated entities | | ― | | | | (220 | ) |

Changes in restricted cash | | | 1,937 | | | | (3,539 | ) |

Payment of tenant improvements | | ― | | | | (797 | ) |

Payment of leasing costs | | | (1,904 | ) | | | (324 | ) |

Deposits on real estate | | | (1,900 | ) | | | (2,950 | ) |

Net cash used in investing activities | | | (709,656 | ) | | | (563,799 | ) |

Financing activities: | | | | | | | | |

Subscriptions received for common stock through public offering | | | 530,083 | | | | 333,960 | |

Payment of stock issuance and offering costs | | | (55,626 | ) | | | (36,575 | ) |

Distributions to stockholders, net of distribution reinvestments | | | (18,816 | ) | | | (9,782 | ) |

Distribution to holder of promoted interest | | ― | | | | (2,000 | ) |

Contribution from redeemable noncontrolling interest | | ― | | | | 568 | |

Distributions to holder of noncontrolling interest | | | (16 | ) | | ― | |

Redemptions of common stock | | | (4,725 | ) | | | (1,068 | ) |

Draws under revolving credit facility | | | 215,000 | | | | 112,115 | |

Repayment on revolving credit facility | | | (31,403 | ) | | | (30,000 | ) |

Proceeds from mortgage and other notes payable | | | 84,888 | | | | 245,587 | |

Principal payments on mortgage and other notes payable | | | (80,270 | ) | | | (24,096 | ) |

Lender deposits | | | (36 | ) | | | (335 | ) |

Payment of loan costs | | | (1,986 | ) | | | (3,974 | ) |

Net cash flows provided by financing activities | | | 637,093 | | | | 584,400 | |

Net increase (decrease) in cash | | | (40,170 | ) | | | 39,274 | |

Cash at beginning of period | | | 91,355 | | | | 44,209 | |

Cash at end of period | | $ | 51,185 | | | $ | 83,483 | |

Supplemental disclosure of non-cash investing and financing activities: | | | | | | | | |

Amounts incurred but not paid (including amounts due to related parties): | | | | | | | | |

Accrued development costs | | $ | 9,100 | | | $ | 4,683 | |

Redemptions payable | | $ | 2,781 | | | $ | 1,178 | |

Contingent purchase price consideration | | $ | 3,000 | | | $ | — | |

Unrealized loss on derivative financial instruments, net | | $ | 14,699 | | | $ | 1,798 | |

Assumption of liabilities on acquisition of property | | $ | 2,502 | | | $ | — | |

Assumption of mortgage note payable on acquisition of property | | $ | 7,128 | | | $ | 27,657 | |

See accompanying notes to condensed consolidated financial statements.

6

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

CNL Healthcare Properties, Inc. (“Company”) is a Maryland corporation incorporated on June 8, 2010 that elected to be taxed as a real estate investment trust (“REIT”) for U.S. federal income tax purposes beginning with the year ended December 31, 2012. The Company is externally advised by CNL Healthcare Corp. (“Advisor”) and its property manager is CNL Healthcare Manager Corp. (“Property Manager”), each of which is a Florida corporation and a wholly owned subsidiary of CNL Financial Group, LLC (“Sponsor”). The Sponsor is an affiliate of CNL Financial Group, Inc. (“CNL”) and CNL Securities Corp., the managing dealer of the Offerings and a wholly owned subsidiary of CNL (“Managing Dealer”). The Advisor is responsible for managing the Company’s affairs on a day-to-day basis and for identifying and making acquisitions and investments on behalf of the Company pursuant to an advisory agreement among the Company, the operating partnership and the Advisor. Substantially all of the Company’s acquisition, operating, administrative and certain property management services are provided by affiliates of the Advisor and the Property Manager. In addition, third-party sub-property managers have been engaged to provide certain property management services.

The Company conducts substantially all of its operations either directly or indirectly through: (1) an operating partnership, CHP Partners, LP, in which the Company is the sole limited partner and its wholly owned subsidiary, CHP GP, LLC, is the sole general partner; (2) a wholly owned taxable REIT subsidiary (“TRS”), CHP TRS Holding, Inc.; (3) property owner subsidiaries and lender subsidiaries, which are single purpose entities; and (4) investments in joint ventures.

On June 27, 2011, the Company commenced its initial public offering (“Initial Offering”), including shares being offered through its distribution reinvestment plan (“Reinvestment Plan”), pursuant to a registration statement on Form S-11 under the Securities Act of 1933 with the Securities and Exchange Commission (“SEC”). In addition, the Company filed a follow-on registration statement on Form S-11 under the Securities Act of 1933 with the SEC in connection with the proposed offering of up to $1 billion in shares of common stock (“Follow-On Offering”), which was declared effective on February 2, 2015. Accordingly, the Company closed its Initial Offering and commenced its Follow-On Offering (collectively, the “Offerings”). The Company closed its Follow-On Offering on September 30, 2015 and discontinued its stock distributions concurrently.

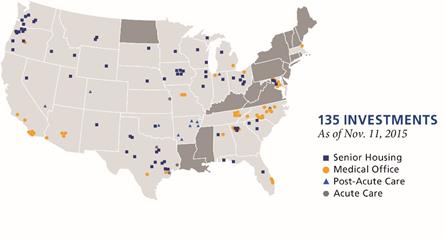

The Company’s investment focus is on acquiring a diversified portfolio of healthcare real estate or real estate-related assets, primarily in the United States, within the seniors housing, medical office, post-acute care and acute care asset classes. The types of seniors housing that the Company may acquire include active adult communities (age-restricted and age-targeted housing), independent and assisted living facilities, continuing care retirement communities, and Alzheimer’s / memory care facilities. The types of medical offices that the Company may acquire include medical office buildings, specialty medical and diagnostic service facilities, surgery centers, outpatient rehabilitation facilities, and other facilities designed for clinical services. The types of post-acute care facilities that the Company may acquire include skilled nursing facilities, long-term acute care hospitals and inpatient rehabilitative hospitals. The types of acute care facilities that the Company may acquire include general acute care hospitals and specialty surgical hospitals. The Company views, manages and evaluates its portfolio homogeneously as one collection of healthcare assets with a common goal of maximizing revenues and property income regardless of the asset class or asset type.

The Company is committed to investing the remaining proceeds of its Offerings through strategic investment types aimed to maximize stockholder value by generating sustainable cash flow growth and increasing the value of its healthcare assets. The Company expects to primarily lease its seniors housing properties to wholly owned TRS entities and engage independent third-party managers under management agreements to operate the properties under REIT Investment Diversification and Empowerment Act of 2007 (“RIDEA”) structures; however, the Company may also lease its properties to third-party tenants under triple-net or similar lease structures, where the tenant bears all or substantially all of the costs (including cost increases, for real estate taxes, utilities, insurance and ordinary repairs). Medical office, post-acute care and acute care properties will be leased on a triple-net, net or modified gross basis to third-party tenants. In addition, the Company expects most investments will be wholly owned, although, it has and may continue to invest through partnerships with other entities where it is believed to be appropriate and beneficial.

The Company has and may continue to invest in new property developments or properties that have not reached full stabilization. Finally, the Company also may invest in and originate mortgage, bridge or mezzanine loans or in entities that make investments similar to the foregoing investment types. The Company generally makes loans to the owners of properties to enable them to acquire land, buildings, or to develop property. In exchange, the owner generally grants the Company a first lien or collateralized interest in a participating mortgage collateralized by the property or by interests in the entity that owns the property.

7

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

2. | Summary of Significant Accounting Policies |

Basis of Presentation and Consolidation — The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with the instructions to Form 10-Q and do not include all of the information and note disclosures required by generally accepted accounting principles in the United States (“GAAP”). The unaudited condensed consolidated financial statements reflect all normal recurring adjustments, which, in the opinion of management, are necessary for the fair statement of the Company’s results for the interim period presented. Operating results for the quarter and nine months ended September 30, 2015 may not be indicative of the results that may be expected for the year ending December 31, 2015. Amounts as of December 31, 2014 included in the unaudited condensed consolidated financial statements have been derived from audited consolidated financial statements as of that date but do not include all disclosures required by GAAP. These unaudited condensed consolidated financial statements should be read in conjunction with the audited consolidated financial statements and notes thereto included in the Company’s Annual Report on Form 10-K for the year ended December 31, 2014.

The accompanying unaudited condensed consolidated financial statements include the Company’s accounts and the accounts of its wholly owned subsidiaries or subsidiaries for which the Company has a controlling financial interest, including the accounts of variable interest entities (“VIEs”) in which the Company is the primary beneficiary. All material intercompany accounts and transactions have been eliminated in consolidation.

In accordance with the guidance for the consolidation of VIEs, the Company analyzes its variable interests, including loans, leases, guarantees, and equity investments, to determine if the entity in which it has a variable interest is a variable interest entity (“VIE”). The Company’s analysis includes both quantitative and qualitative reviews. The Company bases its quantitative analysis on the forecasted cash flows of the entity, and its qualitative analysis on its review of the design of the entity, its organizational structure including decision-making ability and financial agreements. The Company also uses its quantitative and qualitative analyses to determine if it is the primary beneficiary of the VIE, and if such determination is made, it includes the accounts of the VIE in its consolidated financial statements.

Use of Estimates — The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities as of the date of the financial statements, the reported amounts of revenues and expenses during the reporting periods and the disclosure of contingent liabilities. For example, significant assumptions are made in the allocation of purchase price, the analysis of real estate impairments, the valuation of contingent assets and liabilities, and the valuation of restricted stock shares issued. Accordingly, actual results could differ from those estimates.

Adopted Accounting Pronouncements — In April 2014, the Financial Accounting Standards Board (“FASB”) issued Accounting Standard Update (“ASU”) No. 2014-08, “Presentation of Financial Statements (Topic 205) and Property, Plant, and Equipment (Topic 360): Reporting Discontinued Operations and Disclosures of Disposals of Components of an Entity.” This update changes the criteria for reporting discontinued operations where only disposals representing a strategic shift that has (or will have) a major effect on an entity’s operations and financial results, such as a major line of business or geographical area, should be presented as a discontinued operation. This ASU is effective prospectively for all disposals (or classifications as held for sale) of components of an entity that occur within annual periods beginning on or after December 15, 2014 with early adoption permitted. The Company has determined that the amendments will impact the Company’s determinations of which future property disposals, if any, qualify as discontinued operations and will require additional disclosure about discontinued operations for future property disposals, if any.

Recent Accounting Pronouncements — In May 2014, the FASB issued ASU No. 2014-09, “Revenue from Contracts with Customers,” as a new Accounting Standard Concept (“ASC”) topic (Topic 606). The core principle of this amendment is that an entity should recognize revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which the entity expects to be entitled in exchange for those goods or services. The standard further provides guidance for any entity that either enters into contracts with customers to transfer goods or services or enters into contracts for the transfer of nonfinancial assets, unless those contracts are within the scope of other standards (for example, lease contracts). The FASB subsequently issued ASU 2015-14 to defer the effective date of ASU 2014-09 until annual reporting periods beginning after December 15, 2017, including interim periods within that reporting period, with earlier adoption permitted. ASU 2014-09 can be adopted using one of two retrospective transition methods: 1) retrospectively to each prior reporting period presented or 2) as a cumulative-effect adjustment as of the date of adoption. The Company has not yet selected a transition method and is currently evaluating the impact of ASU 2014-09; however, its adoption could potentially have a significant effect on the Company’s consolidated financial position, results of operations or cash flows.

8

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

2. | Summary of Significant Accounting Policies (continued) |

In February 2015, the FASB issued ASU 2015-02, “Consolidation (Topic 810): Amendments to the Consolidation Analysis,” which requires amendments to both the variable interest entity and voting models. The amendments (i) modify the identification of variable interests (fees paid to a decision maker or service provider), the VIE characteristics for a limited partnership or similar entity and primary beneficiary determination under the VIE model, and (ii) eliminate the presumption within the current voting model that a general partner controls a limited partnership or similar entity. The new guidance is effective for annual reporting periods, and interim periods within those annual periods, beginning after December 15, 2015 with early adoption permitted. The amendments may be applied using either a modified retrospective or full retrospective approach. The Company has determined that it will not early adopt this ASU and is currently evaluating the effect the guidance will have on its consolidated financial position, results of operations or cash flows.

In April 2015, the FASB issued ASU 2015-03, “Interest-Imputation of Interest (Subtopic 835-30): Simplifying the Presentation of Debt Issuance Costs,” which requires that loan costs related to a recognized debt liability be presented in the balance sheet as a direct deduction from the carrying amount of that debt liability, consistent with debt discounts or premiums. The new guidance is effective for annual reporting periods, and interim periods within those annual periods, beginning after December 15, 2015 with early adoption permitted. The ASU is to be applied retrospectively for each period presented. Upon adoption, an entity is required to comply with the applicable disclosures for a change in an accounting principle. The FASB subsequently issued ASU 2015-15, “Presentation and Subsequent Measurement of Debt Issuance Costs Associated with Line-of-Credit Arrangements,” which clarifies that, given the absence of authoritative guidance in ASU 2015-03 regarding presentation and subsequent measurement of loan costs related to line-of-credit arrangements, the SEC Staff would not object to an entity deferring and presenting loan costs as an asset and subsequently amortizing the loan costs ratably over the term of the line-of-credit arrangement, regardless of whether there are any outstanding borrowings on the line-of-credit arrangement. The Company has determined that it will not early adopt this ASU and that the amendments will materially impact the presentation of the Company’s consolidated financial position but will not have a material impact on the Company’s consolidated results of operations or cash flows.

In September 2015, the FASB issued ASU 2015-16, “Business Combinations (Topic 805): Simplifying the Accounting for Measurement-Period Adjustments,” which requires an acquirer to recognize provisional amounts that are identified during the measurement period in the reporting period in which the adjustment amounts are determined. The amendments require that the acquirer record, in the same period’s financial statements, the effect on earnings of changes in depreciation, amortization, or other income effects, if any, as a result of the change to the provisional amounts, calculated as if the accounting had been completed at the acquisition date. The new guidance is effective for annual reporting periods, and interim periods within those annual periods, beginning after December 15, 2015 with early adoption permitted. The Company has determined that it will not early adopt this ASU and does not expect that adopting this guidance will have a material impact on its consolidated financial position, results of operations or cash flows.

9

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

Real Estate Investment Properties — During the nine months ended September 30, 2015, the Company acquired the following 30 properties, which were comprised of one acute care hospital, 17 medical office buildings (“MOB”) and 12 seniors housing communities:

| | | | | | Purchase Price | |

Name and Location | | Structure | | Date Acquired | | (in thousands) | |

Acute care | | | | | | | | |

Triangle Orthopaedic | | | | | | | | |

North Carolina Specialty Hospital | | Modified Lease | | 6/29/2015 | | $ | 31,830 | |

Durham, NC | | | | | | | | |

Medical Office | | | | | | | | |

Novi Orthopaedic Center | | Modified Lease | | 2/13/2015 | | | 30,500 | (1) |

Novi, MI | | | | | | | | |

Southeast Medical Office Properties | | | | | | | | |

UT Cancer Institute | | Modified Lease | | 2/20/2015 | | | 33,660 | |

Knoxville, TN | | | | | | | | |

Bend Memorial Clinic Medical Office Building | | Modified Lease | | 5/11/2015 | | | 34,612 | (1) |

Bend, OR | | | | | | | | |

Stoneterra Medical Plaza | | Modified Lease | | 5/29/2015 | | | 15,050 | (1) |

San Antonio, TX | | | | | | | | |

Triangle Orthopaedic | | | | | | | | |

Triangle Orthopaedic Durham | | Modified Lease | | 6/29/2015 | | | 21,275 | |

Durham, NC | | | | | | | | |

Triangle Orthopaedic Oxford | | Modified Lease | | 6/29/2015 | | | 4,728 | |

Oxford, NC | | | | | | | | |

Triangle Orthopaedic Chapel Hill | | Modified Lease | | 6/29/2015 | | | 3,257 | |

Chapel Hill, NC | | | | | | | | |

Triangle Orthopaedic Roxboro | | Modified Lease | | 6/29/2015 | | | 2,067 | |

Roxboro, NC | | | | | | | | |

Doctor's Park | | | | | | | | |

Doctor's Park Building B | | Modified Lease | | 6/30/2015 | | | 5,000 | (1) |

Chula Vista, CA ("San Diego") | | | | | | | | |

Doctor's Park Building C | | Modified Lease | | 6/30/2015 | | | 10,000 | (1) |

Chula Vista, CA ("San Diego") | | | | | | | | |

540 New Waverly Place | | Modified Lease | | 7/20/2015 | | | 15,000 | (1) |

Cary, NC ("Raleigh") | | | | | | | | |

MedHelp | | Modified Lease | | 7/31/2015 | | | 14,076 | (1) |

Birmingham, AL | | | | | | | | |

Maryland MOBs | | | | | | | | |

Patriot Professional Center | | Modified Lease | | 7/31/2015 | | | 16,900 | (1) |

Frederick, MD ("Baltimore") | | | | | | | | |

Liberty Professional Center | | Modified Lease | | 7/31/2015 | | | 7,350 | (1) |

Frederick, MD ("Baltimore") | | | | | | | | |

Columbia MOBs | | | | | | | | |

Broadway Medical Plaza 1 | | Modified Lease | | 8/21/2015 | | | 10,619 | (1) |

Columbia, MO | | | | | | | | |

Broadway Medical Plaza 2 | | Modified Lease | | 8/21/2015 | | | 13,014 | (1) |

Columbia, MO | | | | | | | | |

Broadway Medical Plaza 4 | | Modified Lease | | 8/21/2015 | | | 14,091 | (1) |

Columbia, MO | | | | | | | | |

10

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

3. | Acquisitions (continued) |

| | | | | | Purchase Price | |

Name and Location | | Structure | | Date Acquired | | (in thousands) | |

Seniors Housing | | | | | | | | |

Fieldstone Memory Care (2) | | Managed | | 3/31/2015 | | | 12,400 | (1) |

Yakima, WA | | | | | | | | |

Primrose III Communities | | | | | | | | |

Primrose Retirement Community of Anderson | | Triple-net Lease | | 5/29/2015 | | | 21,086 | |

Anderson, IN ("Muncie") | | | | | | | | |

Primrose Retirement Community of Lancaster | | Triple-net Lease | | 5/29/2015 | | | 25,657 | |

Lancaster, OH ("Columbus") | | | | | | | | |

Primrose Retirement Community of Wausau | | Triple-net Lease | | 5/29/2015 | | | 20,307 | |

Wausau, WI ("Green Bay") | | | | | | | | |

Superior Residences of Panama City | | Managed | | 7/15/2015 | | | 20,000 | (1) |

Panama City Beach, FL | | | | | | | | |

Southeast Seniors Housing Communities | | | | | | | | |

Parc at Duluth | | Triple-net Lease | | 7/31/2015 | | | 52,800 | |

Duluth, GA ("Atlanta") | | | | | | | | |

Parc at Piedmont | | Triple-net Lease | | 7/31/2015 | | | 50,800 | |

Marietta, GA ("Atlanta") | | | | | | | | |

The Pavilion at Great Hills | | Managed | | 7/31/2015 | | | 35,000 | |

Austin, TX | | | | | | | | |

The Hampton at Meadows Place | | Managed | | 7/31/2015 | | | 28,400 | |

Fort Bend, TX ("Houston") | | | | | | | | |

The Beacon at Gulf Breeze | | Managed | | 7/31/2015 | | | 28,000 | |

Gulf Breeze, FL ("Pensacola") | | | | | | | | |

Palmilla Senior Living | | Managed | | 9/30/2015 | | | 47,600 | |

Albuquerque, NM | | | | | | | | |

Cedar Lake Assisted Living and Memory Care | | Managed | | 9/30/2015 | | | 30,000 | |

Lake Zurich, IL ("Chicago") | | | | | | | | |

| | | | | | $ | 655,079 | |

FOOTNOTES:

(1) | This represents a single property or portfolio acquisition that is not considered material to the Company and as such no pro forma financial information has been included related to this property or portfolio. |

(2) | This property was purchased from a related party of the Company’s Sponsor; refer to Note 11. “Related Party Arrangements” for additional information. |

11

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

3. | Acquisitions (continued) |

During the nine months ended September 30, 2014, the Company acquired the following 22 properties, which were comprised of three acute care hospitals, three MOBs, three post-acute care hospitals and, 13 seniors housing communities:

| | | | | | Purchase Price | |

Name and Location | | Structure | | Date Acquired | | (in thousands) | |

Acute Care | | | | | | | | |

Memorial Hermann Orthopedic & Spine Hospital ("MHOSH") | | Triple-net Lease | | 6/2/2014 | | $ | 49,000 | |

Bellaire, TX ("Houston") | | | | | | | | |

Medical Portfolio II Properties | | | | | | | | |

Hurst Specialty Hospital | | Modified Lease | | 8/15/2014 | | | 29,465 | |

Hurst, TX ("Dallas/Fort Worth") | | | | | | | | |

Beaumont Specialty Hospital | | Modified Lease | | 8/15/2014 | | | 33,600 | |

Beaumont, TX ("Houston") | | | | | | | | |

Medical Office | | | | | | | | |

Chula Vista Medical Arts Center - Plaza I | | Modified Lease | | 1/21/2014 | | | 17,863 | (1) |

Chula Vista, CA ("San Diego") | | | | | | | | |

MHOSH Medical Office Building | | Modified Lease | | 6/2/2014 | | | 27,000 | |

Bellaire, TX ("Houston") | | | | | | | | |

Lee Hughes Medical Building | | Modified Lease | | 9/29/2014 | | | 29,870 | (1) |

Glendale, CA ("Los Angeles") | | | | | | | | |

Post-Acute Care | | | | | | | | |

Medical Portfolio II Properties | | | | | | | | |

Oklahoma City Inpatient Rehabilitation Hospital | | Modified Lease | | 7/15/2014 | | | 25,504 | |

Oklahoma City, OK | | | | | | | | |

Las Vegas Inpatient Rehabilitation Hospital | | Modified Lease | | 7/15/2014 | | | 22,292 | |

Las Vegas, NV | | | | | | | | |

South Bend Inpatient Rehabilitation Hospital | | Modified Lease | | 7/15/2014 | | | 20,240 | |

Mishawaka, IN ("South Bend") | | | | | | | | |

Seniors Housing | | | | | | | | |

Pacific Northwest II Communities | | | | | | | | |

Prestige Senior Living Auburn Meadows | | Managed | | 2/3/2014 | | | 21,930 | |

Auburn, WA ("Seattle") | | | | | | | | |

Prestige Senior Living Bridgewood | | Managed | | 2/3/2014 | | | 22,096 | |

Vancouver, WA ("Portland") | | | | | | | | |

Prestige Senior Living Monticello Park | | Managed | | 2/3/2014 | | | 27,360 | |

Longview, WA | | | | | | | | |

Prestige Senior Living Rosemont | | Managed | | 2/3/2014 | | | 16,877 | |

Yelm, WA | | | | | | | | |

Prestige Senior Living West Hills | | Managed | | 3/3/2014 | | | 14,986 | |

Corvallis, OR | | | | | | | | |

12

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

3. | Acquisitions (continued) |

| | | | | | Purchase Price | |

Name and Location | | Structure | | Date Acquired | | (in thousands) | |

South Bay II Communities | | | | | | | | |

Isle at Cedar Ridge | | Managed | | 2/28/2014 | | | 21,630 | |

Cedar Park, TX ("Austin") | | | | | | | | |

HarborChase of Plainfield | | Managed | | 3/28/2014 | | | 26,500 | |

Plainfield, IL | | | | | | | | |

Legacy Ranch Alzheimer’s Special Care Center | | Managed | | 3/28/2014 | | | 11,960 | |

Midland, TX | | | | | | | | |

The Springs Alzheimer’s Special Care Center | | Managed | | 3/28/2014 | | | 10,920 | |

San Angelo, TX | | | | | | | | |

Isle at Watercrest – Bryan | | Managed | | 4/21/2014 | | | 22,050 | |

Bryan, TX | | | | | | | | |

Watercrest at Bryan | | Managed | | 4/21/2014 | | | 28,035 | |

Bryan, TX | | | | | | | | |

Isle at Watercrest – Mansfield | | Managed | | 5/5/2014 | | | 31,300 | |

Mansfield, TX ("Dallas/Fort Worth") | | | | | | | | |

Watercrest at Mansfield | | Managed | | 6/30/2014 | | | 49,000 | |

Mansfield, TX ("Dallas/Fort Worth") | | | | | | | | |

| | | | | | $ | 559,478 | |

FOOTNOTE:

(1) | This represents a single property acquisition that is not considered material to the Company and as such no pro forma financial information has been included related to this property. |

The following summarizes the purchase price allocation for the above properties, and the estimated fair values of the assets acquired and liabilities assumed (in thousands):

| September 30, | |

| 2015 | | | 2014 | |

Land and land improvements | $ | 66,583 | | | $ | 46,064 | |

Buildings and building improvements | | 523,103 | | | | 442,887 | |

Furniture, fixtures and equipment | | 9,469 | | | | 10,014 | |

Intangibles (1) | | 65,126 | | | | 67,431 | |

Other liabilities | | (3,765 | ) | | | (8,718 | ) |

Liabilities assumed | | (2,589 | ) | | ― | |

Assumed mortgage note payable (2) | | (6,976 | ) | | | (27,657 | ) |

Net assets acquired | | 650,951 | | | | 530,021 | |

Contingent purchase price consideration | | (3,000 | ) | | | (12,395 | ) |

Total purchase price consideration | $ | 647,951 | | | $ | 517,626 | |

FOOTNOTE:

(1) | At the acquisition date, the weighted-average amortization period on the acquired lease intangibles for the nine months ended September 30, 2015 and 2014 was approximately 7.9 years and 7.1 years, respectively. The acquired lease intangibles during the nine months ended September 30, 2015 were comprised of approximately $60.7 million and $4.4 million of in-place lease intangibles and other lease intangibles, respectively, and the acquired lease intangibles during the nine months ended September 30, 2014 were comprised of approximately $61.4 million and $6.0 million of in-place lease intangibles and other lease intangibles, respectively. |

(2) | At the acquisition date, the fair value of the mortgage note payable assumed reflects an approximate $0.2 million discount on the below-market mortgage note payable assumed. |

13

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

3. | Acquisitions (continued) |

The revenues and net loss (including deductions for acquisition fees and expenses, and depreciation and amortization expense) attributable to the acquired properties considered to be material were approximately $7.1 million and $4.7 million, respectively, and $8.6 million and $7.6 million, respectively, for the quarter and nine months ended September 30, 2015; and approximately $19.8 million and $4.7 million, respectively, and $36.5 million and $15.3 million, respectively, for the quarter and nine months ended September 30, 2014.

The following table presents the unaudited pro forma results of operations for the Company as if the 2015 acquisitions noted as material in Note 3. “Acquisitions” above were acquired as of January 1, 2014 and the unaudited pro forma results of operations for the Company assuming the 2014 acquisitions noted as material in Note 3. “Acquisitions” above were acquired as of January 1, 2013 (in thousands except per share data):

| | (Unaudited) | | | (Unaudited) | |

| | Quarter Ended September 30, | | | Nine Months Ended September 30, | |

| | 2015 | | | 2014 | | | 2015 | | | 2014 | |

Revenues | | $ | 86,793 | | | $ | 64,136 | | | $ | 245,650 | | | $ | 187,170 | |

Net income (loss) (1) | | $ | (16,244 | ) | | $ | (11,332 | ) | | $ | (48,601 | ) | | $ | (45,370 | ) |

Loss per share of common stock (basic and diluted) | | $ | (0.09 | ) | | $ | (0.10 | ) | | $ | (0.29 | ) | | $ | (0.46 | ) |

Weighted average number of shares of common stock outstanding (basic and diluted) (2) | | | 171,102 | | | | 109,212 | | | | 165,408 | | | | 97,911 | |

FOOTNOTES:

(1) | The unaudited pro forma results for the quarter and nine months ended September 30, 2015, were adjusted to exclude approximately $6.1 million and $9.8 million, respectively, of acquisition related expenses directly attributable to the properties acquired during the quarter and nine months ended September 30, 2015. The unaudited pro forma results for the nine months ended September 30, 2014 were adjusted to include approximately $9.8 million of acquisition related expenses, as if the properties had been acquired on January 1, 2014. The unaudited pro forma results for the quarter and nine months ended September 30, 2014 were adjusted to exclude approximately $3.1 million and $13.8 million, respectively, of acquisition related expenses directly attributable to the properties acquired during the quarter and nine months ended September 30, 2014, as if the properties had been acquired on January 1, 2013. |

(2) | As a result of the acquired properties being treated as operational since January 1, 2014, the Company assumed approximately 19.0 million shares were issued as of January 1, 2014. Consequently the weighted average shares outstanding was adjusted to reflect this amount of shares being issued on January 1, 2014 instead of actual dates on which the shares were issued, and such shares were treated as outstanding as of the beginning of the period presented. |

Real Estate Under Development — In August 2015, the Company acquired a tract of land in Greenville, South Carolina for $2.3 million (“Waterstone at Greenville”). In connection with the acquisition, the Company entered into a development agreement with a third-party developer for the construction and development of an assisted living and memory care community with a maximum development budget of approximately $27.0 million, including the allocated purchase price of the land. The Company determined that Waterstone at Greenville is a VIE because it believes there is insufficient equity at risk due to the development nature of the property. The Company is the primary beneficiary while the developer or its affiliates manage the development, construction and certain day-to-day operations of the property subject to the Company’s oversight. Under a promoted interest agreement with the developer, certain net operating income targets have been established which, upon meeting such targets, result in the developer being entitled to additional payments based on enumerated percentages of the assumed net proceeds of a deemed sale, subject to achievement of an established internal rate of return on the Company’s investment in the development.

In September 2015, the Company acquired a tract of land in Grand Junction, Colorado for $1.1 million (“Wellbrook Senior Living Grand Junction”). In connection with the acquisition, the Company entered into a development agreement with a third-party developer for the construction and development of a transitional rehabilitation facility with a maximum development budget of approximately $13.1 million, including the allocated purchase price of the land. The Company determined that Wellbrook Senior Living Grand Junction is not a VIE because the Company’s equity investment is sufficient to finance the activities of the entity without a construction loan and the Company will receive substantially all expected residual returns.

14

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

3. | Acquisitions (continued) |

In September 2015, the Company acquired a tract of land in Lexington, South Carolina for $2.3 million (“Wellmore of Lexington”), which is a suburb of Columbia, South Carolina. In connection with the acquisition, the Company entered into a development agreement with a third-party developer for the construction and development of a continuing care retirement facility with a maximum development budget of approximately $53.9 million, including the allocated purchase price of the land. The Company determined that Wellmore of Lexington is a VIE because it believes there is insufficient equity at risk due to the development nature of the property. The Company is the primary beneficiary while the developer or its affiliates manage the development, construction and certain day-to-day operations of the property subject to the Company’s oversight. Under a promoted interest agreement with the developer, certain net operating income targets have been established which, upon meeting such targets, result in the developer being entitled to additional payments based on enumerated percentages of the assumed net proceeds of a deemed sale, subject to achievement of an established internal rate of return on the Company’s investment in the development.

Purchase of Controlling Interest in Montecito Joint Venture — In January 2013, the Company acquired a 90% membership interest in a two-story MOB in Claremont, California for approximately $7.0 million in equity through a joint venture (“Montecito Joint Venture”) formed by the Company and its co-venture partner, an unrelated party, that initially held the remaining 10% interest. The Montecito Joint Venture was previously recorded under the equity method of accounting because the decisions that significantly impacted the entity were shared between the Company and its co-venture partner.

In August 2014, the Company acquired its co-venture partner’s 10% interest in the Montecito Joint Venture for approximately $1.6 million. As a result of this transaction, the Company owns 100% of the Montecito Joint Venture, and began consolidating all of the assets, liabilities and results of operations in the Company’s consolidated financial statements upon acquisition. Accordingly, the Company recorded a step up from its carrying value of the investment in the Montecito Joint Venture to the estimated fair value of the net assets acquired and liabilities assumed. The following summarizes the allocation of the purchase price, and the estimated fair values of the assets acquired and liabilities assumed as of the acquisition date (in thousands):

Land and land improvements | | $ | 6,324 | |

Buildings and building improvements | | | 13,533 | |

Intangibles (1) | | | 2,691 | |

Working capital, net | | | 87 | |

Other liabilities | | | (175 | ) |

Mortgage note payable assumed (2) | | | (12,331 | ) |

Net assets acquired | | $ | 10,129 | |

FOOTNOTES:

(1) | At the acquisition date, the weighted-average amortization period on the acquired lease intangibles was approximately 5.1 years and was comprised of approximately $1.9 million and $0.8 million of in-place lease intangibles and other lease intangibles, respectively. |

(2) | At the acquisition date, the fair value of the mortgage note payable assumed reflects an approximate $0.6 million discount on the below-market mortgage note payable assumed. |

The fair value of the Company’s equity interest in the Montecito Joint Venture immediately before the acquisition date was approximately $5.7 million. The Company recorded a gain of approximately $2.8 million based on the acquisition-date fair value of its equity interest in the Montecito Joint Venture. The following summarizes the gain that resulted from the change of control in the equity method investment for the quarter and nine months ended September 30, 2014 (in thousands):

Fair value of net assets acquired | $ | 10,129 | |

Less: Previous investment in Montecito Joint Venture | | (5,747 | ) |

Less: Cash paid to acquire co-venture partner's interest | | (1,584 | ) |

Gain on purchase of controlling interest of investment in unconsolidated entity | $ | 2,798 | |

15

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

4. | Real Estate Assets, net |

The gross carrying amount and accumulated depreciation of the Company’s real estate assets as of September 30, 2015 and December 31, 2014 are as follows (in thousands):

| | September 30, | | | December 31, | |

| | 2015 | | | 2014 | |

Land and land improvements | | $ | 200,763 | | | $ | 128,662 | |

Building and building improvements | | | 2,094,128 | | | | 1,545,614 | |

Furniture, fixtures and equipment | | | 54,284 | | | | 36,319 | |

Less: accumulated depreciation | | | (97,975 | ) | | | (53,095 | ) |

Real estate investment properties, net | | | 2,251,200 | | | | 1,657,500 | |

Real estate under development, including land | | | 69,478 | | | | 47,153 | |

Total real estate assets, net | | $ | 2,320,678 | | | $ | 1,704,653 | |

Depreciation expense on the Company’s real estate investment properties, net was approximately $16.9 million and $44.8 million for the quarter and nine months ended September 30, 2015, respectively, and approximately $10.8 million and $27.4 million for the quarter and nine months ended September 30, 2014, respectively.

In June 2015, the Company completed the construction and development of a seniors housing community in Tega Cay, South Carolina (“Wellmore of Tega Cay”), which is a suburb of Charlotte, North Carolina. Wellmore of Tega Cay opened to residents beginning in July 2015 and was considered placed into service as of June 30, 2015. As such, the asset values related to Tega Cay are included in real estate investment properties, net in the accompanying condensed consolidated balance sheet as of September 30, 2015.

As of September 30, 2015, six of the Company’s properties have real estate under development with third-party developers as follows (in thousands):

Property Name (and Location) | | Developer | | Real Estate Development Costs Incurred (1) | | | Remaining Development Budget (2) | |

HarborChase of Shorewood (Shorewood, WI) | | Harbor Shorewood Development, LLC | | $ | 22,034 | | | $ | 5,776 | |

Raider Ranch (Lubbock, TX) | | South Bay Partners, Ltd | | | 13,464 | | | | 3,460 | |

Watercrest at Katy (Katy, TX) (3) | | South Bay Partners, Ltd | | | 20,049 | | | | 22,342 | |

Welbrook Senior Living Grand Junction (Grand Junction, CO) | | Embree Asset Group, Inc. | | | 2,128 | | | | 11,473 | |

Waterstone at Greenville (Greenville, SC) | | The Balance Group, Inc. | | | 5,298 | | | | 22,401 | |

Wellmore of Lexington (Lexington, SC) | | Maxwell Group, Inc. | | | 6,505 | | | | 48,698 | |

| | | | $ | 69,478 | | | $ | 114,150 | |

FOOTNOTES:

(1) | This amount represents land and total capitalized costs for GAAP purposes for the acquisition, development and construction of the seniors housing or post-acute care communities as of September 30, 2015. Amounts include investment services fees, asset management fees, interest expense and other costs capitalized during the development period. |

(2) | This amount includes preleasing and marketing costs which will be expensed as incurred. |

(3) | This property is owned through a joint venture in which the Company’s initial ownership interest is 95%. |

The development budgets include the cost of the land, construction costs, development fees, financing costs, start-up costs and initial operating deficits of the respective properties. An affiliate of the developer of the respective community coordinates and supervises the management and administration of the development and construction. Each developer is responsible for any cost overruns beyond the approved development budget for the applicable project pursuant to a cost overrun guarantee. Some of these developments were deemed to be VIEs; refer to Note 7. “Variable Interest Entities” for additional information.

16

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

The gross carrying amount and accumulated amortization of the Company’s intangible assets and liabilities as of September 30, 2015 and December 31, 2014 are as follows (in thousands):

| | September 30, | | | December 31, | |

| | 2015 | | | 2014 | |

In-place lease intangibles | | $ | 199,815 | | | $ | 148,880 | |

Above-market lease intangibles | | | 13,586 | | | | 11,320 | |

Below-market ground lease intangibles | | | 12,470 | | | | 10,314 | |

Less: accumulated amortization | | | (62,333 | ) | | | (30,250 | ) |

Intangible assets, net | | $ | 163,538 | | | $ | 140,264 | |

Below-market lease intangibles | | $ | (10,685 | ) | | $ | (13,243 | ) |

Above-market ground lease intangibles | | | (3,488 | ) | | | (2,273 | ) |

Less: accumulated amortization | | | 2,177 | | | | 1,014 | |

Intangible liabilities, net (1) | | $ | (11,996 | ) | | $ | (14,502 | ) |

FOOTNOTE:

(1) | Intangible liabilities, net are included in other liabilities in the accompanying condensed consolidated balance sheets. |

Amortization on the Company’s intangible assets was approximately $11.6 million and $32.1 million for the quarter and nine months ended September 30, 2015, of which approximately $0.6 million and $1.5 million, respectively, were treated as a reduction of rental income from operating leases, approximately $0.08 million and $0.2 million, respectively, were treated as an increase of property operating expenses and approximately $10.9 million and $30.3 million, respectively, were included in depreciation and amortization. Amortization on the Company’s intangible assets was approximately $7.1 million and $17.4 million for the quarter and nine months ended September 30, 2014, of which approximately $0.3 million and $0.7 million, respectively, were treated as a reduction of rental income from operating leases, approximately $0.02 million and $0.1 million, respectively, were treated as an increase of property operating expenses and approximately $6.7 million and $16.7 million, respectively, were included in depreciation and amortization.

Amortization on the Company’s intangible liabilities was approximately $0.4 million and $1.2 million for the quarter and nine months ended September 30, 2015, of which approximately $0.4 million and $1.1 million, respectively, were treated as an increase of rental income from operating leases and approximately $0.02 million and $0.06 million, respectively, were treated as a reduction of property operating expenses. For the quarter and nine months ended September 30, 2014, amortization on the Company’s intangible liabilities was approximately $0.3 million and $0.5 million, of which approximately $0.3 million and $0.5 million, respectively, were treated as an increase of rental income from operating leases and approximately two thousand and six thousand dollars, respectively, was treated as a reduction of property operating expenses.

During the nine months ended September 30, 2015, due to the uncertainty of a tenant’s ability to meet its future obligations under the leases at two of the Company’s specialty hospitals, the Company recorded an impairment provision of approximately $4.7 million related to the lease intangibles as it was determined that the carrying value of these assets would more than likely not be recoverable. In September 2015, the Company signed an amended and restated lease agreement with a new tenant at one of the specialty hospitals, which included similar economic terms and the collection of approximately $1.0 million in rents owed under the lease. In addition, the Company assessed the underlying real estate assets on the second specialty hospital for impairment and concluded that no adjustment to the carrying value was necessary based on the Company’s expected holding period and the estimated undiscounted cash flows and estimated net sales proceeds that could be generated by the property.

17

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

5. | Intangibles, net (continued) |

The estimated future amortization on the Company’s intangibles for the remainder of 2015, each of the next four years and thereafter, in the aggregate, as of September 30, 2015 is as follows (in thousands):

| | In-place Lease Intangibles | | | Above- market Leases | | | Below- market Ground Leases | | | Total Assets | | | Below- market Leases | | | Above- market Ground Leases | | | Total Liabilities | |

2015 | | $ | 11,859 | | | | 524 | | | | 80 | | | $ | 12,463 | | | $ | (379 | ) | | | (22 | ) | | $ | (401 | ) |

2016 | | | 38,280 | | | | 1,797 | | | | 320 | | | | 40,397 | | | | (1,449 | ) | | | (89 | ) | | | (1,538 | ) |

2017 | | | 24,845 | | | | 1,636 | | | | 320 | | | | 26,801 | | | | (1,299 | ) | | | (89 | ) | | | (1,388 | ) |

2018 | | | 14,685 | | | | 1,469 | | | | 320 | | | | 16,474 | | | | (1,146 | ) | | | (89 | ) | | | (1,235 | ) |

2019 | | | 10,537 | | | | 1,168 | | | | 320 | | | | 12,025 | | | | (982 | ) | | | (89 | ) | | | (1,071 | ) |

Thereafter | | | 40,374 | | | | 4,282 | | | | 10,722 | | | | 55,378 | | | | (3,321 | ) | | | (3,042 | ) | | | (6,363 | ) |

| | $ | 140,580 | | | | 10,876 | | | | 12,082 | | | $ | 163,538 | | | $ | (8,576 | ) | | | (3,420 | ) | | $ | (11,996 | ) |

Weighted average remaining useful life as of September 30, 2015 (in years):

| | In-place Lease Intangibles | | | Above- market Leases | | | Below- market Ground Leases | | | Below- market Leases | | | Above- market Ground Leases | |

| | | 4.6 | | | | 6.2 | | | | 37.8 | | | | 4.9 | | | | 38.3 | |

As of September 30, 2015, the Company owned 78 properties that were leased to tenants on a triple-net, net or modified gross basis, and accounted for as operating leases; of which, 37 are single-tenant properties that are 100% leased under operating leases and the remaining 41 are multi-tenant properties that are leased under operating leases. The Company’s leases had a weighted average remaining lease term of 7.5 years based on annualized base rents expiring between 2015 and 2038, subject to the tenants’ options to extend the lease periods ranging from two to 10 years. In addition, certain tenants hold options to extend their leases for multiple periods.

Under the terms of the Company’s triple-net lease agreements, each tenant is responsible for the payment of property taxes, general liability insurance, utilities, and repairs and maintenance, including structural and roof maintenance expenses. Each tenant is expected to pay real estate taxes directly to taxing authorities. However, if the tenant does not pay, the Company will be liable. The total annualized property tax assessed on these properties is approximately $2.8 million.

Under the terms of the multi-tenant lease agreements that have third-party property managers, each tenant is responsible for the payment of their proportionate share of property taxes, general liability insurance, utilities, repairs and common area maintenance. These amounts are billed monthly and recorded as tenant reimbursement income in the accompanying condensed consolidated statements of operations.

The following are future minimum lease payments to be received under non-cancellable operating leases for the remainder of 2015, each of the next four years and thereafter, as of September 30, 2015 (in thousands):

2015 | | $ | 26,253 | |

2016 | | | 103,139 | |

2017 | | | 97,240 | |

2018 | | | 89,806 | |

2019 | | | 81,268 | |

Thereafter | | | 442,941 | |

| | $ | 840,647 | |

The above future minimum lease payments to be received excludes tenant reimbursements, straight-line rent adjustments, amortization of above- and below-market lease intangibles and base rent attributable to any renewal options exercised by the tenants in the future. In addition, future minimum lease payments related to one of the two specialty hospitals discussed in Note 5. “Intangibles, net” have been excluded.

18

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

7. | Variable Interest Entities |

Consolidated VIEs – As of September 30, 2015, the Company has 15 subsidiaries, which are VIEs due to the following factors and circumstances:

| (1) | Two of these subsidiaries are single property entities, designed to own and lease their respective properties to single tenants, for which buy-out options are held by the respective tenants that are formula based. |

| (2) | Four of these subsidiaries are single property entities, designed to own and lease their respective properties to multiple tenants, which are subject to either a ground lease or an air rights lease that include buy-out and put options held by either the tenant or landlord under the applicable lease. |

| (3) | Seven of these subsidiaries are entities with real estate under development or completed developments in which the third-party developers have an opportunity to earn promoted interest payments after certain net operating income targets and internal rate of return targets have been met. |

| (4) | One of these subsidiaries is a joint venture with real estate under development in which the third-party developer has an opportunity to earn promoted interest payments after certain net operating income targets and internal rate of return targets have been met. |

| (5) | One of these subsidiaries is a joint venture with equity interest that consists of non-substantive voting rights. |

The Company determined it is the primary beneficiary and holds a controlling financial interest in each of the aforementioned property and development entities due to its power to direct the activities that most significantly impact the economic performance of the entities, as well as its obligation to absorb the losses and its right to receive benefits from these entities that could potentially be significant to these entities. As such, the transactions and accounts of these VIEs are included in the accompanying condensed consolidated financial statements.

The aggregate carrying amount and major classifications of the consolidated assets that can be used to settle obligations of the VIEs and liabilities of the consolidated VIEs that are non-recourse to the Company as of September 30, 2015 and December 31, 2014 are as follows (in thousands):

| | September 30, | | | December 31, | |

| | 2015 | | | 2014 | |

Assets: | | | | | | | | |

Real estate investment properties, net | | $ | 192,663 | | | $ | 174,449 | |

Real estate under development, including land | | $ | 67,350 | | | $ | 47,153 | |

Intangibles, net | | $ | 24,426 | | | $ | 25,519 | |

Cash | | $ | 1,462 | | | $ | 6,280 | |

Other assets | | $ | 862 | | | $ | 511 | |

Deferred rent and lease incentives | | $ | 6,330 | | | $ | 2,978 | |

Loan costs, net | | $ | 2,497 | | | $ | 2,300 | |

Restricted cash | | $ | 2,053 | | | $ | 5,304 | |

Liabilities: | | | | | | | | |

Mortgages and other notes payable | | $ | 172,537 | | | $ | 137,754 | |

Accounts payable and accrued liabilities | | $ | 1,497 | | | $ | 2,317 | |

Accrued development costs | | $ | 8,854 | | | $ | 7,951 | |

Due to related parties | | $ | 171 | | | $ | 219 | |

Other liabilities | | $ | 4,551 | | | $ | 4,949 | |

The Company’s maximum exposure to loss as a result of its involvement with these VIEs is limited to its net investment in these entities which totaled approximately $109.0 million as of September 30, 2015. The Company’s exposure is limited because of the non-recourse nature of the borrowings of the VIEs.

19

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

8. | Ground and Air Rights Leases |

During the nine months ended September 30, 2015, in conjunction with the Novi Orthopaedic Center, UT Cancer Institute, and Columbia MOBs detailed in Note 3. “Acquisitions,” the Company acquired interests in five additional ground leases. The Novi Orthopaedic Center, UT Cancer Institute, and Columbia MOBs ground leases represent operating leases with scheduled payments over the life of the respective lease expiring in 2045 to 2076.

Overall, under the terms of its ground and air rights lease agreements, the Company is responsible for the monthly rental payments. These amounts are billed monthly and recorded as property operating expenses in the accompanying condensed consolidated statements of operations. In some cases, the Company is able to pass this expense through to its tenants as tenant reimbursement income. For the quarter and nine months ended September 30, 2015, the Company incurred approximately $0.7 million and $1.8 million, respectively, in ground and air rights lease expense, including any straight-line rent adjustments. For the quarter and nine months ended September 30, 2014, the Company incurred approximately $0.04 million and $0.1 million, respectively, in ground and air rights lease expense, including any straight-line rent adjustments.

The following is a schedule of future minimum lease payments to be paid under the ground and air rights leases for the remainder of 2015, each of the next four years and thereafter, in the aggregate, as of September 30, 2015 (in thousands):

2015 | | $ | 484 | |

2016 | | | 1,957 | |

2017 | | | 1,984 | |

2018 | | | 2,016 | |

2019 | | | 2,041 | |

Thereafter | | | 115,515 | |

| | $ | 123,997 | |

9. | Contingent Purchase Price Consideration |

Capital Health Communities

In connection with the acquisition of the Capital Health Communities in 2012, the Company required that approximately $7.0 million of the purchase price be placed in an escrow account as the seller guaranteed the Company an annual return of at least $6.9 million, $7.0 million, and $7.1 million of net operating income on the acquired properties during 2013, 2014 and 2015, respectively (“Yield Guaranty”). As of September 30, 2015, the Company determined the fair value of the Yield Guaranty to be $1.8 million, which was recorded as other assets in the accompanying condensed consolidated balance sheet. The following table provides a roll-forward of the fair value of the contingent purchase price consideration related to the Yield Guaranty on the Capital Health Communities for the quarter and nine months ended September 30, 2015 and 2014 (in thousands):

| | Quarter ended | | | Nine Months Ended | |

| | September 30, | | | September 30, | |

| | 2015 | | | 2014 | | | 2015 | | | 2014 | |

Beginning balance | | $ | 1,820 | | | $ | 3,509 | | | $ | 4,078 | | | $ | 4,488 | |

Yield Guaranty payment received from seller | | | — | | | | (301 | ) | | | (2,579 | ) | | | (2,601 | ) |

Change in fair value | | | — | | | | — | | | | 321 | | | | 1,321 | |

Ending balance | | $ | 1,820 | | | $ | 3,208 | | | $ | 1,820 | | | $ | 3,208 | |

20

CNL HEALTHCARE PROPERTIES, INC. AND SUBSIDIARIES

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

NINE MONTHS ENDED SEPTEMBER 30, 2015 (UNAUDITED)

9. | Contingent Purchase Price Consideration (continued) |

Medical Portfolio I

During 2013, in conjunction with the acquisition of Medical Portfolio I, the Company entered into an earn-out agreement with the seller related to Cleveland Clinic, the tenant at Chestnut Commons, whereby the tenant maintains an exercisable right to expand the leased space by an additional 10,000 square feet within 24 months of the property acquisition closing (“Chestnut Commons Earn-Out”). The Chestnut Commons Earn-Out fee was equal to (a) the base rent due for the first full year of the lease applicable to the expansion space divided by 8% minus (b) the costs incurred by the Company in connection with the exercise by Cleveland Clinic of its option for the expansion space, including tenant improvement costs, multiplied by 50%. The Chestnut Commons Earn-Out expired in August 2015. The following table provides a roll-forward of the fair value of the contingent purchase price consideration related to the Chestnut Commons Earn-Out for the quarter and nine months ended September 30, 2015 and 2014 (in thousands):

| | Quarter Ended | | | Nine Months Ended | |

| | September 30, | | | September 30, | |

| | 2015 | | | 2014 | | | 2015 | | | 2014 | |

Beginning balance | | $ | (268 | ) | | $ | (507 | ) | | $ | (268 | ) | | $ | (507 | ) |

Contingent consideration in connection with acquisition | | | — | | | | — | | | | — | | | | — | |

Change in fair value | | | 268 | | | | — | | | | 268 | | | | — | |

Ending balance | | $ | — | | | $ | (507 | ) | | $ | — | | | $ | (507 | ) |

South Bay II Communities

In conjunction with the acquisition of the South Bay II Communities, the Company entered into an agreement with the sellers whereby the purchase price is adjusted in the event that certain net operating income targets are met. The additional consideration was determined within three months of the acquisition date and is equal to (a) the baseline net operating income divided by the baseline capitalization rates (as defined in the purchase and sale agreement) less (b) the purchase price paid at closing. The following table provides a roll-forward of the fair value of the estimated contingent purchase price consideration related to the South Bay II Communities for the quarter and nine months ended September 30, 2015 and 2014 (in thousands):

| | Quarter ended | | | Nine Months Ended | |

| | September 30, | | | September 30, | |

| | 2015 | | | 2014 | | | 2015 | | | 2014 | |

Beginning balance | | $ | — | | | $ | (8,500 | ) | | $ | — | | | $ | — | |

Contingent consideration in connection with acquisition | | | — | | | | — | | | | — | | | | (12,395 | ) |

Contingent consideration payment | | | — | | | | 10,300 | | | | — | | | | 14,195 | |

Change in fair value | | | — | | | | (1,800 | ) | | | — | | | | (1,800 | ) |

Ending balance | | $ | — | | | $ | — | | | $ | — | | | $ | — | |

Superior Residences of Panama City

In connection with the purchase of Superior Residences of Panama City, the Company entered into an earn-out agreement with the seller whereby additional consideration is owed in the event that certain performance targets are met (“Panama City Earn-Out”). Under the earn-out agreement, the seller has an opportunity of earning up to $4.0 million in additional purchase price consideration during the immediate 36 months post-closing. At the acquisition date and as of September 30, 2015, the Company determined the fair value of the Panama City Earn-Out to be $3.0 million, which was recorded as other liabilities in the accompanying condensed consolidated balance sheet.

Fair Value Measurements