As filed with the Securities and Exchange Commission on January 7, 2011

Registration No. 333-168803

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

PRE-EFFECTIVE

AMENDMENT NO. 2 TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

JINTAI MINING GROUP, INC.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 1031 | 27-2987974 | ||

| (State or other jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer | ||

| incorporation or organization) | Classification Code Number) | Identification Number) |

No. 48 Qiaodong Road, Sien Town,

Huanjiang County Hechi City,

Guangxi Province, China 547100

Tel: + (86 778) 220-5911

(Address, including zip code and telephone number, including area code,

of registrant’s principal executive offices)

National Corporate Research, Ltd.

615 S. Dupont Highway

Dover, DE 19901

(Name, address, including zip code and telephone number, including area code,

of agent for service)

Copies to:

| Arthur Marcus, Esq. | Yvan-Claude Pierre, Esq. | |

| Cheryll J. Calaguio, Esq. | Daniel I. Goldberg, Esq. | |

| Yuan Sun, Esq. | Matthew D. Adler, Esq. | |

| Gersten Savage LLP | DLA Piper LLP (US) | |

600 Lexington Avenue, 9 th Floor | 1251 Avenue of the Americas | |

| New York, NY 10022 | New York, NY 10020 | |

| Tel: (212) 752-9700 | Tel: (212) 335-4500 | |

| Fax: (212) 980-5192 | Fax: (212) 335-4501 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the

effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. þ

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer ¨ | Accelerated Filer ¨ |

Non-accelerated Filer ¨ (Do not check if a smaller reporting company) | Smaller reporting company þ |

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities to be Registered | Amount to be Registered | Proposed Maximum Offering Price per Share(1) | Proposed Maximum Aggregate Offering Price | Amount of Registration Fee(2) | ||||||||||

| Common stock, par value $.0001 per share(3) | 6,900,000 | $ | 6.00 | 41,400,000 | $ | 2,951.82 | ||||||||

| Common stock issuable upon the conversion of the Convertible Notes issued to the Selling Stockholders(4) | 4,000,000 | $ | 6.00 | 24,000,000 | $ | 1,711.20 | ||||||||

| Common stock issuable upon exercise of warrants issued to the Selling Stockholders(5) | 800,000 | $ | 6.60 | 5,280,000 | $ | 376.46 | ||||||||

| Total | 11,700,000 | 70,680,000 | $ | 5,039.49 | (6) | |||||||||

| The registration fee for securities to be offered by the Registrant is based on an estimate of the Proposed Maximum Aggregate Offering Price of the securities, and such estimate is solely for the purpose of calculating the registration fee pursuant to Rule 457(o). Includes shares which the underwriter has the option to purchase to cover over-allotments. |

| (2) | Calculated pursuant to Rule 457(o) based on an estimate of the proposed Maximum Aggregate Offering Price. |

| (3) | Includes 900,000 shares of the Registrant’s common stock subject to an option granted to the underwriter solely to cover over-allotments if any. |

| (4) | Represents shares of the Registrant’s common stock that will be acquired upon the conversion of the Convertible Notes issued to the Selling Stockholders that are being registered for resale. |

| (5) | Pursuant to Rule 416, this registration statement also covers such number of additional shares to prevent dilution resulting from stock splits, stock dividends and similar transactions. |

| (6) | Previously paid. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 (the “Securities Act”) or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to Section 8(a), may determine.

EXPLANATORY NOTE

This registration statement contains two forms of prospectus, as set forth below:

| · | Public Offering Prospectus. A prospectus to be used for the direct public offering by the registrant of up to 6,000,000 shares of common stock (in addition, up to 900,000 shares of the Registrant's common stock may be sold upon exercise of the underwriter' over-allotment option) (the “Public Offering Prospectus”). |

| · | Selling Stockholder Prospectus. A prospectus to be used in connection with the potential resale by the selling stockholders of (i) 4,000,000 shares of our common stock issuable upon conversion of convertible promissory notes (the “Convertible Notes”) sold to Ms. Liwen Hu and Mr. Haibin Zhong (the “Selling Stockholders”) in a private offering in August and November 2010; (ii) 800,000 shares of common stock issuable upon exercise of warrants (the “Selling Stockholders’ Warrants”) issued to Ms. Liwen Hu and Mr. Haibin Zhong in the private offering in August and November 2010 (the “Selling Stockholder Prospectus”). |

The Public Offering Prospectus and the Selling Stockholder Prospectus will be identical in all respects except for the following principal points:

| · | they contain different front covers; |

| · | they contain different Use of Proceeds sections; |

| · | they contain different Underwriting/Plan of Distribution sections; |

| · | a Shares Registered for Resale section is included in the Selling Stockholder Prospectus; |

| · | a Selling Stockholders section is included in the Selling Stockholder Prospectus; and |

| · | they contain different back covers. |

The registrant has included in this registration statement, after the financial statements, a set of alternate pages to reflect the foregoing differences between the Public Offering Prospectus and the Selling Stockholder Prospectus.

Investors who receive the public offering prospectus from the Company or the underwriter will all be potential investors in the public offering. The purpose of the alternative prospectus in connection with the resale offering is that the selling stockholders, whose shares are being registered in the resale offering prospectus, will be responsible for delivering the alternative prospectus in connection with the sales made by such selling stockholders.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | SUBJECT TO COMPLETION, DATED JANUARY 7, 2011 |

JINTAI MINING GROUP, INC.

6,000,000 SHARES

OF

COMMON STOCK

We are offering 6,000,000 shares of our common stock. We expect the initial public offering price of the shares to be between $4.00 and $6.00 per share. Currently, no public market exists for our common stock. We intend to apply for the listing of the shares on the NYSE Amex Equities under the symbol “JTI”, however no assurance can be given that our application will be approved. If the application is not approved, we will not complete this offering.

Investing in our common stock involves a high degree of risk. Please see the section entitled "Risk Factors" starting on page 6 of this prospectus to read about risks that you should consider carefully before buying shares of our common stock.

Per Share (1) | Total (2) | |||||||

| Initial public offering price | $ | $ | ||||||

| Underwriting discount and commissions | $ | $ | ||||||

| Proceeds, before expenses, to Jintai Mining Group, Inc. | $ | $ | ||||||

(1)Based on the mid-point price for this offering.

(2)Does not include a corporate finance fee equal to 1% of the gross proceeds, or $0.05 per share, payable to the underwriter, Maxim Group, LLC, of which $25,000 has been paid by the Company to the underwriter.

We have granted the underwriter a 45-day option to purchase up to an additional 900,000 shares of our common stock at the public offering price, less the underwriting discount, to cover any over-allotments.

The underwriter expects to deliver the shares against payment in New York, New York, on or about ____, 2011.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Maxim Group, LLC

The date of this prospectus is ___, 2011

TABLE OF CONTENTS

| PROSPECTUS SUMMARY | 1 | |

| THE OFFERING | 4 | |

| RISK FACTORS | 11 | |

| SPECIAL NOTE REGARDING FORWARD LOOKING STATEMENTS | 32 | |

| USE OF PROCEEDS | 33 | |

| DIVIDEND POLICY | 34 | |

| CAPITALIZATION | 35 | |

| DILUTION | 36 | |

| EXCHANGE RATE INFORMATION | 37 | |

| MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION | 38 | |

| CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE | 49 | |

| INDUSTRY OVERVIEW | 49 | |

| DESCRIPTION OF BUSINESS | 56 | |

| OUR HISTORY AND CORPORATE STRUCTURE | 52 | |

| DESCRIPTION OF PROPERTY | 80 | |

| DIRECTORS AND EXECUTIVE OFFICERS | 88 | |

| EXECUTIVE COMPENSATION | 92 | |

| SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 94 | |

| CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS | 94 | |

| DESCRIPTION OF SECURITIES | 96 | |

| TRANSFER AGENT | ||

| SHARES ELIGIBLE FOR FUTURE SALE | 97 |

| UNDERWRITING | 99 | |

| LEGAL MATTERS | 103 | |

| EXPERTS | 103 | |

| INTERESTS OF NAMED EXPERTS AND COUNSEL | 103 | |

| DISCLOSURE OF COMMISSION POSITION OF INDEMNIFICATION FOR SECURITIES ACT LIABILITIES | 103 | |

| SERVICE OF PROCESS AND ENFORCEMENT OF JUDGEMENT | 104 | |

| WHERE YOU CAN FIND ADDITIONAL INFORMATION | 104 | |

| INDEX TO FINANCIAL STATEMENTS |

YOU SHOULD RELY ONLY ON THE INFORMATION CONTAINED IN THIS DOCUMENT OR TO WHICH WE HAVE REFERRED YOU. WE HAVE NOT, AND THE UNDERWRITER HAS NOT, AUTHORIZED ANYONE TO PROVIDE YOU WITH INFORMATION THAT IS DIFFERENT. THIS DOCUMENT MAY ONLY BE USED WHERE IT IS LEGAL TO SELL THESE SECURITIES. THE INFORMATION IN THIS DOCUMENT MAY ONLY BE ACCURATE ON THE DATE OF THIS DOCUMENT.

PROSPECTUS SUMMARY

This summary contains basic information about us and our securities. The reader should read the entire prospectus carefully, especially the risks of investing in our common stock discussed under “Risk Factors.” Some of the statements contained in this prospectus, including statements under “Summary” and “Risk Factors” are forward-looking statements and may involve a number of risks and uncertainties. We note that our actual results and future events may differ significantly based upon a number of factors. The reader should not put undue reliance on the forward-looking statements in this document, which speak only as of the date on the cover of this prospectus.

As used in this Prospectus, references to “ Jintai,” the “ Company,” “ we,” “ our,” “ ours” and “ us” refer to Jintai Mining Group, Inc., a Delaware corporation, including its consolidated subsidiaries and variable interest entities (“ VIE” ), unless the context otherwise requires. Unless otherwise indicated, the term “ common stock” refers to shares of the Company ’ s common stock, par value $0.0001.

The following summary highlights some of the information in this prospectus. It may not contain all of the information that is important to you. To understand this offering fully, you should read the entire prospectus carefully, including the risk factors and our financial statements and the notes accompanying the financial statements appearing elsewhere in this prospectus.

THE COMPANY

Our Company

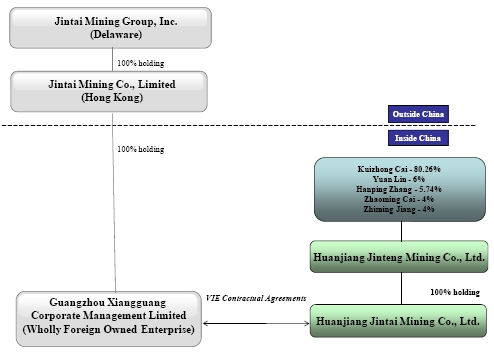

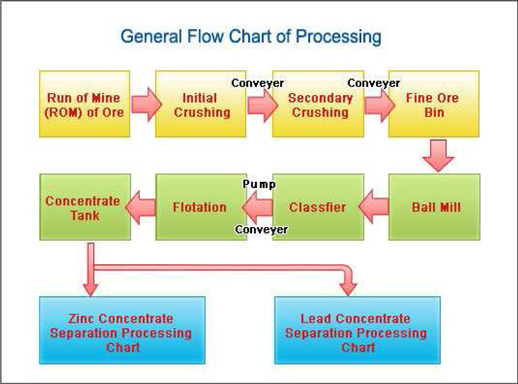

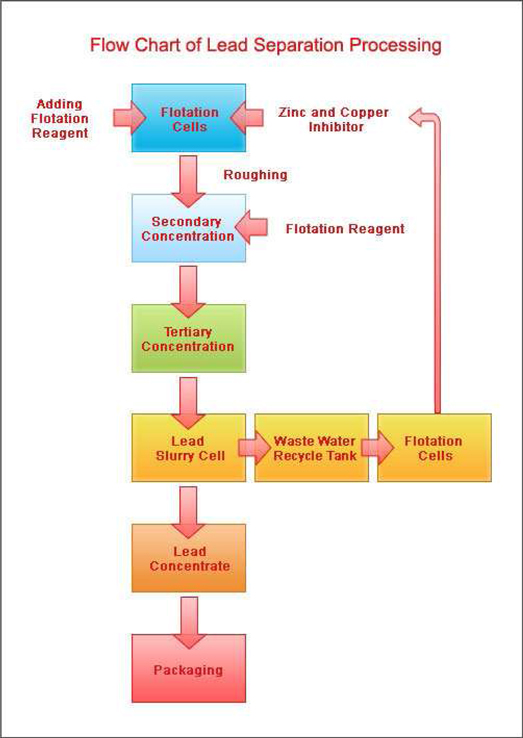

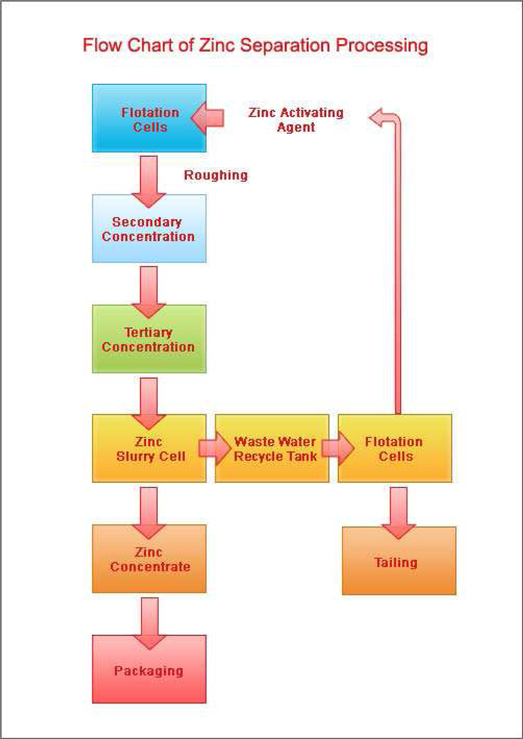

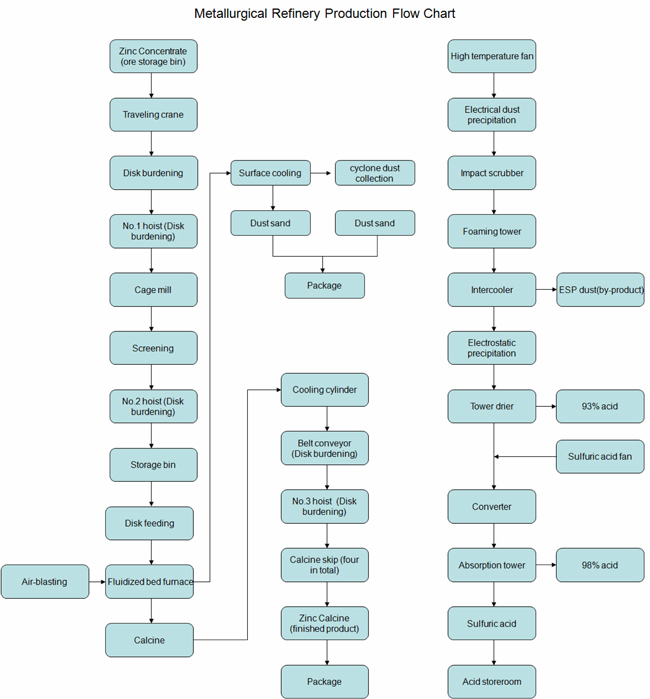

We are an emerging vertically integrated mining company operating in the Guangxi Province of the People’s Republic of China (“PRC”); however we are incorporated in the State of Delaware, the United States of America. We are engaged in exploration, mining, leaching, smelting and other processing operations of primarily zinc and lead. Through our wholly-owned subsidiary, Jintai Mining Co., Limited (“Jintai HK”), a Hong Kong limited liability company, we own another subsidiary, Guangzhou Xiangguang Corporate Management Co. Ltd (“Xiangguang”), which controls Huanjiang Jintai Mining Company Limited (“Huanjiang Jintai”) through a series of VIE contractual arrangements. Huanjiang Jintai owns and operates an ore mine in an area measuring approximately 2.83 square kilometers (“the Ore Mine”) and owns the exploration rights to an additional 21.58 square kilometers (the “Exploration Right Properties”) of very limited production or non-producing properties. Huanjiang Jintai sells the refined zinc and lead based products such as zinc concentrate, lead concentrate, zinc calcine, zinc dust and sand, sulfuric acid and other variations of zinc and lead. It also sells by-products such as “tailings” that are produced after the concentration process of zinc-lead ores. For a more detailed discussed on the Company’s business and the products we sell, please see the sections entitled “Description of Business” beginning on page 56, and the sub-section entitled “ Description of Business - Our Products” beginning on page 68 hereof.

Our Industry

Based on a report issued by ResearchInChina issued in 2009, the proven zinc resources and reserves worldwide are approximately 1.9 billion tons, most of which is found in Australia, China, Peru, the United States and Kazakhstan. Together, the collective reserves of these five countries account for 70.9% of the global reserves.

Due to its vast zinc and lead resources, a significant number of zinc and lead mines and processing plants have developed in China. While zinc-lead resources may be found throughout the country, a majority of these resources are concentrated within the western and middle areas of China. In 2008, it was reported by ResearchInChina that there were 27 provinces and areas within China wherein zinc-lead ores were explored. However, only 6 of the 27 provinces contained zinc and lead reserves of more than 8 million tons: (i) Yunnan Province- 26.6 million tons; (ii) Inner Mongolia - 16.1 million tons; (iii) Gansu Province - 11.2 million tons (iv) Guangdong Province- 10.8 million tons; (v) Hunan Province - 8.9 million tons; and (vi) Guangxi Province - 8.8 million tons. Based on these figures, the 6 provinces accounted for 82.4 million tons of zinc and lead reserves, or 64% of China’s total reserves of 129.6 million tons.

Further, a study of the locations of zinc-lead mines within China show that there are five main locations for mining, dressing and smelting and production bases within the country, namely, (i) Northeast; (ii) Hunan; (iii) Guangdong and Guangxi; (iv) Yunnan and Sichuan; and (v) Northwest. In total, the mines and production plants located in these areas have collectively produced more than 95% of the nation’s total zinc production and 85% of its total lead production in 2008.

The production of zinc ore and refined zinc within China accounts for one-third of the world’s total production. In 2007, China produced approximately 3,748,600 tons of refined zinc and 2,604,000 tons of zinc ore.

While the 2008 global financial crisis had the effect of reducing the overall demand for zinc and its by-products worldwide, China still increased its overall production to 3,910,000 tons of refined zinc and 3,126,600 tons of zinc ore during the year 2008. Such level of production continues to be consistent from year-to-year and it is estimated that between January and October of 2009, China produced approximately 3,520,000 tons of refined zinc. However, due to the declining price in zinc internationally, the production of zinc ore decreased to 2,440,000 tons between January and October 2009.

China has also become the leading producer of refined lead and lead ore. In 2007, China produced approximately 2,717,500 tons of refined lead and 917,600 tons of lead ore. Between 2006 and 2008, the refined lead production in China continued to grow. However, production of lead ore was far behind the production of refined lead and there was a relatively large gap between the production of refined lead and lead ore during such years.

During the 2008 global financial crisis, China increased its production of both refined lead and lead ore. Between the months of January and October of 2009, China produced approximately 3,160,000 tons of refined lead and 1,260,000 tons of lead ore.

According to statistics, China’s zinc consumption in 2008 was roughly 3.7 million tons. Of this amount, consumption by the zinc plating industry accounted for approximately 47%, while die casting alloy is accountable for approximately 22%, brass-15% and oxide-14%.

China’s consumption of lead is driven mostly by the lead acid storage battery, lead oxide, and lead alloy industries. China’s lead production growth is mostly attributable to the lead acid storage battery industry, as it consumes roughly 75% of the lead produced throughout China. Lead oxide, on the other hand, accounts for 13%, while lead alloy accounts for 6%.

1

Competitive Strength

We believe that the following strengths give us a competitive edge over our competitors:

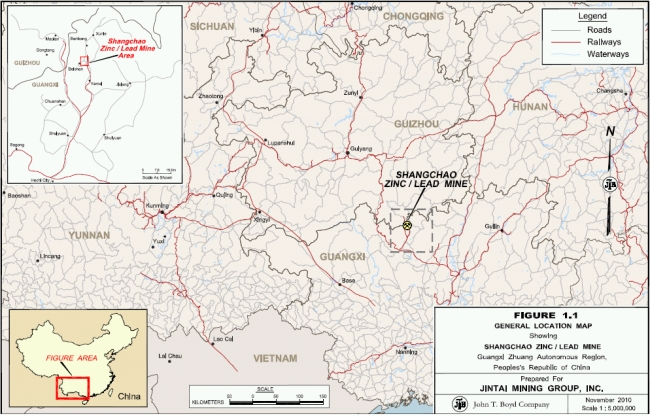

| o | Unique Exploration Environment - Guangxi is located in the south western part of China. Hechi is located in the north part of Guangxi. Guangxi is rich in zinc and lead reserves, ranked as the fifth largest zinc reserve in China and the sixth in the category of lead reserve in China. Hechi City of Guangxi Province is well regarded for its non-ferrous metal resources. |

| o | High Grade Ore Reserve - Based on a report provided by JT Boyd coupled with the opinion of our management based on their previous experience in the mining industry, we believe that we own one of the highest quality zinc-lead mines in the region which contains high purity zinc-lead ore and good extracting conditions. |

| o | Low Cost Producer - We believe that our low cost position is a result of many strategic initiatives including, our access to abundant and low-cost labor resources, our sharing best practices across all exploitation and production facilities, and our cost control measures. We are the only company in the Guangxi Province that owns and operates our own mine, concentrators and smelters. Based on our management’s opinion, the implementation of this vertically integrated business model results in lower production costs compared to other mining companies in the region. |

| o | Government support - Based on management’s assessment, we believe that our relationship with local government and the provincial government is strong and mutually beneficial. Due to this good relationship, the local government gives us strong incentives to continue with our mining operations. Further, regional human resources and specialized professional mining teams are available to us at a low cost. |

Business Strategy

We will seek to implement numerous strategies to expand the size of our Company and continue efficient operating advantages. Our strategies include:

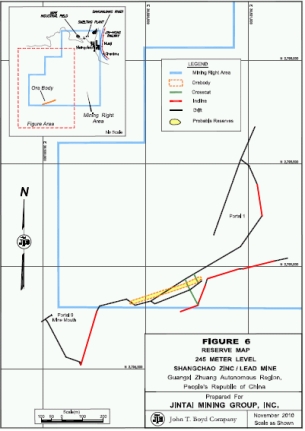

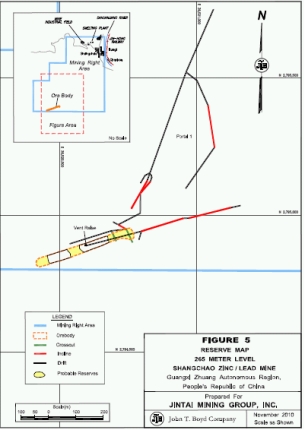

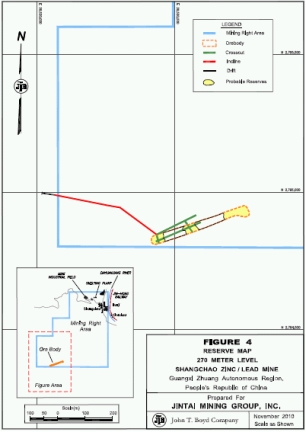

Expanding the Existing Ore Mine - Our strategy is aimed at efficiently increasing production of our existing mine through the upgrading and improvement of up to four (4) transportation channels or tunnels into the Ore Mine. At present, the Ore Mine has widely scattered working sites or portals and therefore it has not reached maximum production capacity.

Survey and develop additional mines in our Exploration Rights Properties - We have mapped out a systematic approach to acquire sufficient geological and assay data to have a reasonable estimate of resources in our Exploration Rights Properties, particularly, the Shangchao-Gangshan lead ore deposit, Shangchao lead ore deposit, and Dongjiang zinc ore deposit.

Increase vertical integration of our value chain to include zinc-oxide and facility expansion – Our current annual output capacity of 25,000 metric tons of refined zinc products can be doubled to 50,000 metric tons by upgrading and expanding the Jintai Duchuan Smelter facility to include zinc-oxide production lines. It is anticipated that the increased output will be used to produce zinc-oxide, which has greater margins than zinc calcine. Lastly, we intend to further improve our margins by adding a new concentrator to increase ore output to an annual capacity of 450,000 tons of run-of-mine ore, which is raw ore extracted from the ore body.

Acquisition Opportunities - We also intend to customarily review other potential development and production oriented acquisitions in the similar geographic concentration as our existing properties. By leveraging our expertise and knowledge of certain markets, increased facility expansion plans, and improved capital structure, we intend to grow our market share in the Chinese market. To a lesser extent, we may seek other properties outside the zinc-lead campaign. At this time, we have no agreements to acquire any entities or properties.

Based on management’s assessment, we believe that our relationship with local government and provincial government is strong and mutually beneficial. We are not aware of any current problems and are not aware of any reason why this strong relationship would not continue over the foreseeable future.

We believe that the funding from our anticipated initial public offering could accelerate the execution of our business strategy. While current cash flow from internally generated sources is capable of supporting our growth plans, it would take a significant amount of time for us to reach our objectives if we were to rely on current cash flow alone in order to undertake our planned activities. As such, additional funds are sought through this offering in order to accelerate the execution of our business plan and we anticipate that our corporate planning and business initiatives will be achieved within 18 to 24 months from the completion of this offering. Our goal is to evolve from an emerging diversified mining company to a leading fully integrated mining entity. A more detailed description of our business and strategy can be found in the section of this prospectus entitled the “Description of Business”.

2

Corporate Structure

We are a vertically integrated mining company operating in the Guangxi Province of the PRC. We were incorporated in the State of Delaware on June 14, 2010 under the name Jintai Mining Group, Inc. We are focused on exploration, mining, leaching, smelting and other processing operations of primarily zinc and lead. Through our wholly-owned subsidiary, Jintai HK, we own Xiangguang, which controls Huanjiang Jintai through a series of variable interest entity (VIE) contractual arrangements. The VIE contracts grant us, through Xiangguang, the right to manage and control Huanjiang Jintai and further entitle us to receive the revenue and control the assets of Huanjiang Jintai. Other than these interests in these contractual arrangements, we, Jintai HK and Xiangguang have no equity interests in Huanjiang Jintai. A more detailed description of these contractual arrangements is provided in the section of this Prospectus entitled “Description of Business - Contractual Arrangements.”

Huanjiang Jintai owns and operates our Ore Mine and owns the Exploration Right Properties and sells the refined zinc and lead based products such as zinc concentrate, lead concentrate, zinc calcine, zinc dust and sand, sulfuric acid and other variations of zinc and lead. We also sell by-products such as “tailings” that are produced after the concentration process of zinc-lead ores.

Under the structure above, we believe that we do not need to obtain approval from Ministry of Commerce (“MOFCOM”) or the China Securities Regulatory Commission (the “CSRC”) prior to publicly listing our securities, even if our operations and assets are concentrated in Huanjiang Jintai, a PRC company. For a discussion of the risks and uncertainties arising from these PRC rules and regulations, see section entitled “Risk Factors — Risks Related to Our Corporate Structure” beginning on page 16 hereof.

The following diagram illustrates our shareholding and corporate structure as of the date of this prospectus:

Risks Associated With Our Business

Investing in our common stock involves a high degree of risk. Please see the section entitled “Risk Factors” starting on page 11 of this prospectus to read about risks that you should consider carefully before buying shares of our common stock.

Company Information

Our principal executive offices are located at No. 48 Qiaodong Road, Sien Town, Huanjiang County Hechi City; Guangxi Province, China. Our correspondence address is Room 1708, B2 Nan Fung Tower, Des Voeux Road, Central Hong Kong. Our telephone number is (86-0778) 220-5911. Our website address is www.jintaimining.com. The information on our website is not a part of this prospectus.

3

THE OFFERING

| Securities Being Offered: | 6,000,000 shares of our common stock, with an over-allotment option for additional 900,000 shares granted to our underwriter. | |

| Initial Offering Price: | The purchase price for the shares is between $4.00 to $6.00 per share. | |

| Common Stock Issued and Outstanding Before the Offering: | 32,000,000 shares of our common stock are issued and outstanding as of the date of this prospectus. | |

| Common Stock Issued and Outstanding After the Offering: | 42,000,000 shares of our common stock will be issued and outstanding after this offering is completed. (1) | |

| Use of Proceeds: | Assuming that all shares offered herein are sold at a price of $5.00 per share, we will use the estimated net proceeds of $26,000,000 as follows: (a) $2,000,000 for existing mine safety improvements, expansion and rehabilitation. We shall rehabilitate up to four (4) tunnels in the Ore Mine and improve current ventilation, drainage and slagging shaft. It is anticipated that these activities will improve our working environment and increase our operating efficiencies; (b) $6,000,000 to explore and develop our existing Exploration Rights Properties. Our goal is to become a leading fully integrated developer and operator in our province. This capital injection should accelerate our initiatives into meeting this objective; and (c) $17,000,000 for plant expansion and new construction. $7,000,000 of this $17,000,000 shall immediately be utilized to expand production capacity and construct a new concentrator to include additional ores and the remaining $10,000,000 is designated to construct a state-of-the-art zinc oxide production line in the Duchuan Smelter with an estimated annual output of 50,000 metric tons. $1,000,000 will be placed in an escrow account to be used for payment of certain expenses incurred by us related to us being a public company. Please see “Use of Proceeds” on page 27. | |

| Proposed NYSE Amex Equities Symbol: | “JTI” | |

| Lock-Up | Our directors and executive officers of the Company have agreed, through contractual lock-up agreements, that for a period of twelve (12) months following the date of this prospectus, they will not offer, issue, sell or contract to sell, encumber, grant any option for the sale or otherwise dispose of any securities of the Company. Pursuant to such lock-up agreements, the 32,000,000 shares of common stock currently held by the directors and officers of the Company will not be sold, encumbered or otherwise disposed for a period of twelve (12) months from the date of this prospectus. For a more detailed description of the contractual lock-ups, please see “Underwriting” on page 99 hereof. |

4

| Concurrent Offering: | The registration statement of which this prospectus forms a part includes 4,000,000 shares of common stock issuable upon the conversion of the Convertible Notes and 800,000 shares issuable upon the exercise of warrants issued to the Selling Stockholders*. | |

| Risk Factors: | See “Risk Factors” and other information included in this prospectus for a discussion of the factors you should carefully consider before deciding to invest in our shares of common stock. |

(1) The number of shares of common stock to be outstanding immediately after this offering is based on 32,000,000 shares of common stock outstanding as of January 6, 2011, and includes 4,000,000 shares issuable upon the automatic conversion of the Convertible Notes upon the closing of this offering and excludes (i) 800,000 shares of our common stock issuable upon the exercise of warrants issued pursuant to the Subscription Agreement between Jintai Mining Group, Inc. and Ms. Liwen Hu and Mr. Haibin Zhong dated August 2010 and November 2010; and (ii) 900,000 shares underlying an over-allotment option granted to our underwriter;

* Unless otherwise indicated, the number of shares of common stock issuable to the Selling Stockholders upon the conversion of the Convertible Notes assumes that the offering price for our shares pursuant to this offering will be $5.00 per share.

5

SUMMARY FINANCIAL AND OPERATING DATA

The following summary financial data for the six months ended September 30, 2010 and 2009, and the years ended March 31, 2010 and 2009 are derived from our audited financial statements that are included elsewhere in this prospectus. The historical results presented below are not necessarily indicative of financial results to be achieved in future periods.

Jintai Mining Co., Limited (“Jintai HK”) was established in Hong Kong on April 28, 2010. Jintai Mining Group, Inc. was incorporated in Delaware on June 14, 2010. By the execution of a share exchange agreement on August 3, 2010, Jintai HK became a wholly-owned subsidiary of Jintai Mining Group, Inc. We founded our wholly-owned foreign entity, Xiangguang, on August 24, 2010. Therefore, the financial statements for the six months ended September 30, 2010 presents the financial operations of all four legal entities, Jintai Mining Group, Inc., Jintai HK, Xiangguang and Huanjiang Jintai Mining Co. Ltd. on a consolidated basis.

For the six months ended September 30, 2009, as well as the years ended March 31, 2010 and 2009, as none of Jintai Mining Group, Inc., Jintai HK and Xiangguang was yet established, only the financial operations of Huanjiang Jintai Mining Co. Ltd is presented.

Prospective investors should read these summary consolidated financial data together with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes included elsewhere in this Prospectus.

For the six months ended September 30, 2010 and 2009:

6

Jintai Mining Group, Inc. and subsidiaries

Consolidated Statements of Operations

(Expressed in USD Dollars)

| Six months ended September 30 | ||||||||

| 2009 | ||||||||

| 2010 (unaudited) | (unaudited) | |||||||

| Revenues | ||||||||

| Sales | $ | 20,701,541 | $ | 15,249,704 | ||||

| Cost of sales | (7,280,171 | ) | (8,373,775 | ) | ||||

| Gross profits | $ | 13,421,370 | $ | 6,875,929 | ||||

| Operating expenses | ||||||||

| Selling and marketing | (71,264 | ) | (145,796 | ) | ||||

| General and administrative | (1,723,389 | ) | (452,317 | ) | ||||

| Total Operating Expenses | $ | (1,794,653 | ) | $ | (598,113 | ) | ||

| Other operating income | ||||||||

| Income (Loss) from continuing operations | 11,626,717 | 6,277,816 | ||||||

| Other income (expenses | ||||||||

| Other Income | 11,711 | |||||||

| Other expenses | (7,827 | ) | (343 | ) | ||||

| Total other income (loss) | (7,827 | ) | 11,368 | |||||

| Income (loss) before income tax provision | 11,618,890 | 6,289,184 | ||||||

| Income taxes | (2,410,050 | ) | (866,586 | ) | ||||

| Net Income | 9,208,840 | 5,422,598 | ||||||

| Other comprehensive income (loss) | ||||||||

| Foreign currency translation gain (loss) | 735,008 | 58,946 | ||||||

| Comprehensive income (loss) | $ | 9,943,848 | $ | 5,481,544 | ||||

| Earnings per common share | ||||||||

| Basic | $ | 0.29 | $ | 0.17 | ||||

| Diluted | $ | 0.28 | $ | 0.17 | ||||

| Weighted average common shares outstanding | ||||||||

| Basic | 32,000,000 | 32,000,000 | ||||||

| Diluted | 32,400,000 | 32,000,000 | ||||||

7

For the fiscal years ended March 31, 2010 and 2009:

8

Huanjiang Jintai Mining Co. Ltd.

Audited Statement of Operations

For the Years Ended March 31, 2010 and 2009

| (Expressed in USD Dollars) |

Year Ended March 31, | ||||||||

| 2010 | 2009 | |||||||

| Revenues | ||||||||

| Sales | $ | 35,027,568 | $ | 23,765,415 | ||||

| Cost of sales | 18,430,646 | 15,273,882 | ||||||

| Gross profit | 16,596,922 | 8,491,533 | ||||||

| Operating expenses | ||||||||

| Selling and marketing | 274,965 | 232,602 | ||||||

| General and administrative | 1,258,262 | 1,111,620 | ||||||

| Total Operating Expenses | 1,533,227 | 1,344,222 | ||||||

| Other operating income | - | 14,563 | ||||||

| Income (Loss) from continuing operations | 15,063,694 | 7,161,874 | ||||||

| Other income (expenses) | ||||||||

| Other Income | 11,715 | 254 | ||||||

| Other expenses | (343 | ) | (72,060 | ) | ||||

| Total other income (loss) | 11,372 | (71,806 | ) | |||||

| Income (loss) before income tax provision | 15,075,067 | 7,090,068 | ||||||

| Provision for income taxes | 2,283,890 | 579,412 | ||||||

| Net Income | 12,791,177 | 6,510,656 | ||||||

| Other comprehensive income (loss) | ||||||||

| Foreign currency translation gain (loss) | 34,697 | 415,676 | ||||||

| . | . | |||||||

| Comprehensive income (loss) | $ | 12,825,874 | $ | 6,926,332 | ||||

9

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below and the other information contained in this prospectus before deciding to invest in our common stock. Our business, financial condition or results of operations could be materially adversely affected by any of these risks. The trading price of our securities could decline due to any of these risks, and you may lose all or part of your investment.

Risks Relating to our Business Operations

We are subject to numerous risks and hazards associated with the mining industry.

Our mining operations are subject to a number of risks and hazards including:

| · | industrial accidents; |

| · | unusual or unexpected geologic formations; |

| · | explosive rock failures; and |

| · | flooding and periodic interruptions due to inclement or hazardous weather conditions. |

Such risks could result in a variety of issues that could affect our operations, such as damage to or destruction of mineral properties or production facilities, environmental damage, delays in our mining operations, personal injury or death, monetary losses and possible legal liability. No assurance can be given that we will be able to avoid any or all of the hazards discussed above and any such occurrence may substantially affect our business and financial operations.

Our mining operations currently have material safety concerns which may result in accidents and in turn negatively affect our revenue.

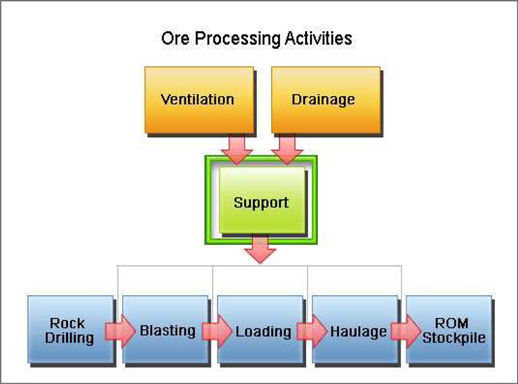

We have identified certain safety concerns in our Ore Mine, including overly large unsupported openings along the main tunnels on some levels, enlarged opening size at a number of the draw points, poorly conditioned wooden supports along some of the main arteries that are in poor condition, historic mined-out stopes that may trigger massive roof failure, inadequate natural ventilation and high likelihood of flooding in the tunnels. Accidents and employee’s injury arising from the safety issues described above may cause suspension or discontinuance of our mining operation and thus negatively affect our revenue.

Mining operations are highly susceptible to hazardous weather conditions and seasonal weather conditions.

Certain weather conditions may affect underground mining operations. The Ore Mine is located in a region with a typical subtropical climate characterized mainly by high precipitation and high evaporation and humid conditions. The rainy season occurs from May to August of each year and based on past occurrences, some of the portals to our Ore Mine become inaccessible or unusable during such rainy season due to flooding caused by insufficient drainage and pumping facilities necessary to release the excess water that has accumulated into our portals. During the last rainy season, which was a particularly rainy season marked by much flooding in China, the mines had only five of the nine portals that were accessible. As such, our mining operation may be interrupted due to inclement or hazardous weather conditions experienced during such rainy season.

11

Mining is inherently dangerous and subject to conditions or events beyond our control, and any operating hazards could have a material adverse effect on our business.

During the course of mining activities, we use dangerous materials and there is no assurance that accidents will not occur. Should we be held liable for any such accident, we may be subject to penalties, and possible criminal proceedings may be brought against us by our employees, which could have a material adverse effect on our business.

Mineral exploration and development and mining activities are subject to extensive environmental regulations, which may prevent or delay the commencement or continuance of our operations.

Mineral exploration and development, as well as our current mining activities and our future mineral mining operations are, and may continue to be, subject to stringent state, provincial and local laws and regulations relating to environmental quality, production, labor standards, occupational health, waste disposal, protection and remediation of the environment, mine safety, toxic substances and other matters. Mineral mining is also subject to risks and liabilities associated with pollution of the environment and disposal of waste products occurring as a result of mineral production. Compliance with these laws and regulations will impose substantial costs on us and may subject us to significant potential liabilities. Further, any changes to these regulations may increase our operating costs and may adversely affect our results of operations. A more detailed discussion of the applicable environmental regulations and safety procedures can be found in the section entitled “ Our Business - Applicable Environmental Protection Regulations and our Environmental Protection Measures ” ..

We may suffer losses resulting from unexpected accidents.

Like other mining companies, our operations may suffer from structural issues such as unusual or unexpected geologic formations or explosive rock failures that may result in accidents that cause property damage and possible personal injuries. We can give no assurance that industry-related accidents will not occur in the future. We do not maintain flood or other property insurance covering our properties, equipment or inventories. Any losses and/or liabilities we incur due to unexpected property damage or personal injury could have a material adverse effect on our financial condition and results of operations.

Our mining exploitation activities are labor intensive and employ low levels of mechanization which may result in inefficiency and impose greater safety and health hazards concern.

We have used rudimentary mining methods and low levels of mechanization since the beginning of our mining operation. The labor-intensive and low-mechanization mining method we use in our mining operations results in inefficient operation. The relatively large number of mining workers exposed to dust, noise, heat and vibration caused by our mining methods may increase the possibility of accidents and health hazards.

The actual output at our Ore Mine exceeds the annual capacity allowed by the relevant PRC government authorities and we may face fines or even possible revocation of mining licenses, which could have a material adverse affect on our business.

The mining license we currently hold authorizes us to produce up to 30,000 tons of zinc lead ores per year, but we currently have an annual output of 400,000 tons per year. However, due to this overcapacity, Huanjiang Jintai has paid an aggregate amount of $277,185 for fiscal years 2008, 2009 and 2010 as resource fees to the relevant PRC authorities for its total output, including the excessive output. The Company accounts for the payment of the resource fees on the accrual basis. Furthermore, the PRC government currently has not issued any definitive rule or interpretation specifically relating to excessive output of zinc lead ores such as Huanjiang Jintai is involved in shall be subject to any judicial or administrative discipline such as suspension or revocation of its mining license.

12

Although we believe that this situation of excess output has been remedied by the payment of a fee to the authorities and the lack of a current definitive law or regulation governing this situation, we cannot assure you that the PRC government would agree, and that excess output would not be found in violation of any current or future Chinese laws or regulations. We cannot predict the effect of the interpretation of existing or new Chinese laws or regulations on excess output of zinc lead ores. According to the regulations concerning the mineral resources exploration and mining, where the company fails to comply with the plan for the mineral resource exploitation, relevant government agencies may order one or more of the following: reduction of its output to authorized output levels, payment for additional mining licenses to cover the amount in excess of the allowed total capacity, payment of fines, and possible revocation of the mining license of the company in the most serious instance. Any of these or similar actions could significantly disrupt our business operations or restrict us from conducting a substantial portion of our business operations, which could materially and adversely affect our business, financial condition and results of operations.

Our mining operations are inherently subject to changing conditions that can affect our profitability.

Our operations are subject to changing conditions that may increase our production costs for varying lengths of time. We are exposed to price risks related to the sale of zinc and lead based products and by-products. In addition, weather and natural disasters (such as earthquakes, landslides, flooding, and other similar occurrences), unexpected maintenance problems, key equipment failures, fires, amounts of overburden, variations in rock and other natural materials and variations in geological conditions can be expected to have a significant impact on our future operating results. Prolonged disruption in our production at the Ore Mine could result in a material decrease in our revenues and profitability.

Our future success may partly depend on our ability to successfully upgrade, expand and operate the Jintai Duchuan Smelter with zinc-oxide processing facilities.

In the first fiscal quarter of 2011, we began to upgrade and expand our Jintai Duchuan Smelter with zinc-oxide processing facilities. Total processing capability will increase from 1,100 ton/day to 2,600 ton/day. While we believe the successful upgrading and expansion of this facility will result in increased profitability, no assurance can be given that we will be able to complete the same or that if completed, that we will be able to operate the upgraded facilities profitably.

Any acquisitions made by us may disrupt our operations or have a negative impact on our business.

As a part of our long term strategy, we plan to start mining operations on the Exploration Rights Properties and to acquire additional mining operations. Such additional operating activities will require us to employ additional personnel, and we may have difficulty integrating such new personnel or may experience difficulty in integrating the operations of the mining companies we acquire with that of our own. We cannot predict the effect that any intended expansion may have on our business. Further, any acquisition may disrupt our ongoing business, divert the attention of our management and employees or may result in an increase in our operating expenses. In addition, acquisitions are accompanied by a number of inherent risks, including, without limitation, the following:

| · | delays and waiting periods associated with required safety inspections, as well as government licensing or permitting procedures; |

| · | the difficulty of incorporating acquired resources, facilities, operations or products into the existing business; |

| · | difficulties in disposing of the excess or idle facilities of an acquired company or business and expenses in maintaining such facilities; |

13

| · | difficulties in maintaining uniform standards, controls, procedures and policies; |

| · | the potential impairment of relationships with employees and customers as a result of any integration of new management personnel; and |

| · | potential unknown liabilities associated with acquired businesses and the associated operations, or the need to spend significant amounts to retool, reposition or modify the existing operations. |

No assurance can be given that any of the above risks will be sufficiently addressed or that such will not have a negative effect on our business operations.

We may not be able to effectively control and manage our growth.

As part of our current business strategy, we intend to acquire other local mining operations. As our business grows, it will be necessary for us to finance and manage expansion in an orderly fashion. We may face challenges in identifying attractive mining sites and/or additional mining rights and/or complementary mining businesses. Such eventualities will increase demands on our existing management, workforce and facilities. Failure to satisfy such increased demands could interrupt or adversely affect our operations and cause administrative inefficiencies that may have a negative impact on our financial operations.

The working sites in our Ore Mine are scattered, which results in an inefficient exploitation.

At present our Ore Mine is accessible through nine (9) main portals/adits for a total extraction area of 2.83 square kilometers. The relatively small number of accessible portals/adits results in an inefficient exploitation and as such, we are unable to maximize our ore production. Increased production can be attained through the rehabilitation of connecting tunnels or through the construction of additional tunnels into the Ore Mine which will grant access into the Ore Mine for our workers. However, we do not, at present, have the necessary capital to undertake such rehabilitation and construction in the immediate future. Our continued failure to maximize our production may result in lower revenue, which could affect the value of your investment.

We engage independent contractors for the transportation of our zinc and lead ores to our processing facilities and any dispute with such contractors could result in a disruption in our operations.

We engage local independent contractors to transport the ores mined from our Ore Mine to our processing facilities and no assurance can be given that the current good business relationship with such contractors will be maintained. Any dispute with such contractors could result in a disruption in our business operations and consequently, may negatively affect our financial operations.

A large portion of our revenue is derived from two major customers.

Two of our major customers, Huanjiang Mao Nan Autonomous County Nanping Concentrator Co. Ltd. and Jingyi Liu accounted for 57% and 30%, respectively of our total revenue for the fiscal year ended March 31, 2010 and 29% and 21%, respectively, of our total revenue for the fiscal year ended March 31, 2009. For the six months ended September 30, 2010, Huanjiang Mao Nan Autonomous County Nanping Concentrator Co. Ltd. and Shaoguan Futong Trading Co., Ltd. accounted for 24% and 23% of our total revenue, respectively. Non-renewal or/and termination of such relationship may have a material adverse effect on our revenue. No assurance can be given that we will be able to maintain such a relationship. Additionally, no assurance can be given that our business will not remain largely dependent on a limited number of customers accounting for a substantial part of our revenue.

14

Our revenue and, therefore, our profitability, may be affected by metal price volatility.

The majority of our revenue is derived from the sale of zinc and lead based products and by-products. As a consequence, our revenue is directly related to the price of zinc and lead metal. The fact that we do not conduct any hedging exposes us to increased price volatility. However, prices for zinc have historically fluctuated widely due to numerous factors beyond our control, including the overall demand and supply of zinc, production costs in major producing regions, the availability and prices of competing commodities, inventory levels maintained by customers, as well as international economic and political conditions. Changes in the prices of zinc and lead may adversely affect our operating results. It is difficult to predict whether zinc prices will rise or fall in the future and a decline in prices could have an adverse impact on our future results of operations and financial condition.

We may not be able to successfully compete for mineral rights with companies having greater financial resources than we have.

All mines have limited resources and as such, we intend to acquire additional mining operations, as part of our long term strategy. As there is a limited supply of desirable mineral deposits in the PRC, in particular, in the Guangxi Province, we face strong competition for promising acquisition targets from other mining companies, some of which have greater financial resources than us. We may be unable to compete with such other mining companies in making acquisition that we deem to be complementary to our business, or to acquire such on terms that are acceptable to us.

Our ability to operate effectively could be impaired if we lose key personnel or if we fail to attract qualified personnel.

We manage our business through a number of key personnel, including Mr. Kuizhong Cai, our President, Mr. Yuan Lin, our Chief Executive Officer and Mr. Danny T.N. Ho, our Chief Operating Officer. The loss of any of these key officers could have a material adverse effect on our operations. In addition, as business develops and expands, we believe that our future success will depend greatly on our continued ability to attract and retain highly skilled and qualified personnel. No assurance can be given that key personnel will continue to be employed by us or that we will be able to attract and retain qualified personnel in the future. Accordingly, if we are not able to retain these officers and/or personnel, or effectively fill vacancies created by departing key persons, our business may be impaired. The lack of key man insurance on any of these important personnel will also have an adverse effect on our financial conditions in case of the death of any of these important key personnel.

All but one member of our current management team have no experience in managing and operating a public company and are not well versed on the federal securities laws, rules and regulations that will apply to us upon becoming a public company. Any failure to comply or adequately comply with federal securities laws, rules or regulations could subject us to fines or regulatory actions, which may materially adversely affect our business, results of operations and financial condition.

None of the members of our current management team, other than Mr. Danny T. Ho, have experience managing and operating a public company and they rely in many instances on the professional experience and advice of third parties, including our attorneys and accountants. While we are obligated to hire a qualified chief financial officer to enable us to meet our ongoing reporting obligations as a U.S. public company, qualified individuals are often difficult to find, or may not have all of the qualifications that we require. Failure to comply or adequately comply with any laws, rules, or regulations applicable to our business may result in fines or regulatory actions, which may materially adversely affect our business, results of operation, or financial condition and could result in delays in achieving either the effectiveness of a registration statement relating to the shares being sold in this offering or the development of an active and liquid trading market for our common stock. To the extent that the market place perceives that we do not have a strong financial staff and financial controls, the market for, and price of, our stock may be impaired.

15

Risks Related to Our Corporate Structure

We conduct our business through Huanjiang Jintai by means of the VIE contractual arrangements. If the Chinese government determines that these contractual arrangements do not comply with applicable regulations, our business could be adversely affected. If the PRC regulatory bodies determine that the agreements that establish the structure for operating our business in China do not comply with PRC regulatory restrictions on foreign investment, we could be subject to severe penalties. In addition, changes in such Chinese laws and regulations may materially and adversely affect our business.

There are uncertainties regarding the interpretation and application of PRC laws, rules and regulations, including but not limited to the laws, rules and regulations governing the validity and enforcement of the contractual arrangements between Xiangguang and Huanjiang Jintai (Please see section entitled “Description of Business-Contractual Arrangements”). Although we have been advised by our PRC counsel, that based on their understanding of the current PRC laws, rules and regulations, the structure for operating our business in China (including our corporate structure and contractual arrangements with Huanjiang Jintai and its owner) comply with all applicable PRC laws, rules and regulations, and do not violate, breach, contravene or otherwise conflict with any applicable PRC laws, rules or regulations, we cannot assure you that the PRC regulatory authorities will not determine that our corporate structure, established through contractual arrangements, do not violate PRC laws, rules or regulations. If the PRC regulatory authorities determine that our contractual arrangements are in violation of applicable PRC laws, rules or regulations, our contractual arrangements will become invalid or unenforceable which will substantially affect our operations and the value of an investment in our common stock. Further, under the PRC Property Rights Law that became effective on October 1, 2007, we are required to register with the relevant government authority the security interests on the equity interests in Huanjiang Jintai granted to us under the equity pledge agreements that are part of the contractual arrangements and the Certificate of Registration was issued on October 20, 2010. In addition, new PRC laws, rules and regulations may be introduced from time to time to impose additional requirements that may be applicable to our contractual arrangements.

Regarding our contractual arrangements, the Chinese government has broad discretion in dealing with violations of laws and regulations, including levying fines, revoking business and other licenses and requiring actions necessary for compliance. In particular, licenses and permits issued or granted to us by relevant governmental bodies may be revoked at a later time by higher regulatory bodies. We cannot predict the effect of the interpretation of existing or new Chinese laws or regulations on our businesses. We cannot assure you that our current ownership and operating structure would not be found in violation of any current or future Chinese laws or regulations. As a result, we may be subject to sanctions, including fines, and could be required to restructure our operations or cease to provide certain services. Any of these or similar actions could significantly disrupt our business operations or restrict us from conducting a substantial portion of our business operations, which could materially and adversely affect our business, financial condition and results of operations.

If Xiangguang or Huanjiang Jintai is determined to be in violation of any existing or future PRC laws, rules or regulations or fail to obtain or maintain any of the required governmental permits or approvals, the relevant PRC regulatory authorities would have broad discretion in dealing with such violations, including:

· | revoking the business and operating licenses of our PRC consolidated entities; |

· | discontinuing or restricting the operations of our PRC consolidated entities; |

| · | imposing conditions or requirements with which we or our PRC consolidated entities may not be able to comply; |

16

| · | requiring us or our PRC consolidated entities to restructure the relevant ownership structure or operations; |

| · | restricting or prohibiting our use of the proceeds from our initial public offering to finance our business and operations in China; or |

| · | imposing fines. |

The imposition of any of these penalties would severely disrupt our ability to conduct business and have a material adverse effect on our financial condition, results of operations and prospects.

Our contractual arrangements with Huanjiang Jintai may not be effective in providing control over Huanjiang Jintai.

All of our revenue and net income is derived from Huanjiang Jintai. Current PRC laws restrict foreign equity ownership in companies engaged in certain non-ferrous metal smelting and rolling processing business in China, including zinc and lead, and as such, we do not have equity ownership interest in Huanjiang Jintai but rely on contractual arrangements with Huanjiang Jintai to control and operate its business. However, these contractual arrangements may not be effective in providing us with the necessary control over Huanjiang Jintai and its operations. Any deficiency in these contractual arrangements may result in our loss of control over the management and operations of Huanjiang Jintai, which will result in a significant loss in the value of our common stock.

In addition, we rely on contractual rights to effect control and management of Huanjiang Jintai, which exposes us to the risk of potential breach of contract by the shareholder of Huanjiang Jintai. The shareholder of Huanjiang Jintai may breach, or cause Huanjiang Jintai to breach, the contracts for a number of reasons. For example, its interests as shareholder of Huanjiang Jintai and the interests of our company may conflict, and we may fail to resolve such conflicts; the shareholder may believe that breaching the contracts will lead to greater economic benefit for it; or the shareholder may otherwise act in bad faith. If any of the foregoing were to happen, we may have to rely on legal or arbitral proceedings to enforce our contractual rights, including claims for damages, specific performance or injunctive relief. Such arbitral and legal proceedings may result in the disruption of our business, and may be financially burdensome and may divert the attention of our management, any of which may have a negative impact on our financial operations.

In addition, as all of these contractual arrangements are governed by the PRC laws and as such, would be interpreted in accordance with PRC law and any disputes relating to such would be resolved in accordance with PRC legal procedures. Uncertainties in the PRC legal system could limit our ability to enforce these contractual arrangements. Furthermore, these contracts may not be enforceable in China if PRC government authorities or courts take a view that such contracts contravene PRC laws and regulations or are otherwise unenforceable for public policy reasons. In the event we are unable to enforce these contractual arrangements, we may not be able to exert effective control over Huanjiang Jintai, and our ability to conduct our business will be materially and adversely affected.

17

Huanjiang Jintai may terminate the Consulting Services Agreement and fail to fulfill its obligations under the same agreement, which may trigger an auction or sale of Huanjiang Jinteng Mining Co., Ltd’s(“HJM”)interest in HuanjiangJintai pursuant to the Equity Pledge Agreement, resulting in Xiangguang having the priority in receiving payments of proceeds from such an auction or sale.

Under Section 7.2 of the Consulting Services Agreement, Huanjiang Jintai may terminate the Consulting Services Agreement prior to the expiration of its term. If the Consulting Services Agreement is to be terminated pursuant to Section 7.2, Section 7.3 of the Consulting Services Agreement provides that all amounts then due and payable and accrued but not yet paid to Xiangguang shall become due and payable by Huanjiang Jintai. If Huanjiang Jintai fails to perform this payment obligation, it would still be subject to the Equity Pledge Agreement pursuant to Section 3.1 thereof. Under Section 3.2 of the Equity Pledge Agreement, Xiangguang is entitled to control, sell, or dispose of the equity interest of Huanjiang Jintai. Pursuant to Section 2 of the Equity Pledge Agreement, Xiangguang has the priority in receiving payments of proceeds from the auction or sale of HJM’s one hundred percent (100%) equity interest in Huanjiang Jintai. As Xiangguang, a PRC company, is subject to restrictions on paying dividends and making other payments to us, we may experience difficulties in completing the necessary administrative procedure to obtain payments from such a sale.

The failure to comply with PRC regulations relating to mergers and acquisitions of domestic enterprises by offshore special purpose vehicles may subject us to severe fines or penalties and create other regulatory uncertainties regarding our corporate structure.

On August 8, 2006, MOFCOM, joined by the CSRC, the State-owned Assets Supervision and Administration Commission of the State Council (the “SASAC”), the State Administration of Taxation (the “SAT”), the State Administration for Industry and Commerce (the “SAIC”), and the State Administration of Foreign Exchange (“SAFE”), jointly promulgated regulations entitled the Provisions Regarding Mergers and Acquisitions of Domestic Enterprises by Foreign Investors (the "M&A Rules"), which took effect as of September 8, 2006. Among other things, the M&A Rules contain certain provisions that require offshore special purpose vehicles (“SPVs”) that are controlled directly or indirectly by PRC individuals and companies and which were formed overseas listing purposes to obtain the approval of MOFCOM prior to engaging in such acquisitions and to obtain the approval of the CSRC prior to publicly listing their securities on an overseas stock market.

The application of the M&A Rules with respect to our corporate structure and to this offering remains unclear, with no current consensus existing among leading PRC law firms regarding the scope and applicability of the M&A Rules. As such, we cannot be certain that the relevant PRC government agencies, including the CSRC and MOFCOM, would reach the conclusion that the M&A Rules do not apply to us or our corporate structure, or that this offering is not subject to the M&A Rules and as such, does not require the prior approval of MOFCOM or CSRC. Further, we cannot rule out the possibility that the relevant PRC government agencies, including MOFCOM, would deem that the M&A Rules required us or our entities in China to obtain approval from MOFCOM or other PRC regulatory agencies in connection with Xiangguang’s control of Huanjiang Jintai through contractual arrangements.

If the CSRC, MOFCOM, or another PRC regulatory agency subsequently determines that CSRC, MOFCOM or other approval was required for the share exchange transaction and/or the VIE arrangements between Xiangguang and Huanjiang Jintai, or if prior CSRC approval for this offering is required and not obtained, we may face severe regulatory actions or other sanctions from MOFCOM, the CSRC or other PRC regulatory agencies. In such event, these regulatory agencies may impose fines or other penalties on us, limit our operating privileges in the PRC, delay or restrict the repatriation of the proceeds from this offering into the PRC, restrict or prohibit payment or remittance of dividends to us or take other actions that could have a material adverse effect on our business, financial condition, results of operations, reputation and prospects, as well as the trading price of our common stock. The CSRC or other PRC regulatory agencies may also take actions requiring us, or making it advisable for us, to delay or cancel this offering, to restructure our current corporate structure, or to seek regulatory approvals that may be difficult or costly to obtain.

Further, the M&A Rules, along with certain foreign exchange regulations discussed below, will also be interpreted or implemented by the relevant government authorities in connection with any of our future offshore financings or acquisitions, and we cannot predict how they will affect our acquisition strategy. For example, our operating companies' ability to remit dividends to us, or to engage in foreign-currency-denominated borrowings, may be conditioned upon compliance with the SAFE registration requirements by such Chinese domestic residents, over whom we may have no control.

18

SAFE regulations relating to offshore investment activities by PRC residents may increase our administrative burdens and restrict our overseas and cross-border investment activity. If our shareholders and beneficial owners who are PRC residents fail to make any required applications, registrations and filings under such regulations, we may be unable to distribute profits and may become subject to liability under PRC laws.

SAFE has promulgated several regulations, including Notice on Relevant Issues Concerning Foreign Exchange Administration for PRC Residents to Engage in Financing and Inbound Investment via Oversea Special Purpose Vehicles, or “Circular No. 75”, issued on October 21, 2005 and effective as of November 1, 2005 and certain implementation rules issued in recent years, requiring registrations with, and approvals from, PRC government authorities in connection with direct or indirect offshore investment activities by PRC residents and PRC corporate entities. These regulations apply to our shareholders and beneficial owners who are PRC residents, and may affect any offshore acquisitions that we make in the future.

SAFE Circular No. 75 requires PRC residents, including both PRC legal person residents and/or natural person residents to register with the local SAFE branch before establishing or controlling any company outside of China for the purpose of equity financing with assets or equities of PRC companies, referred to in the notice as an “offshore special purpose company”. In addition, any PRC resident who is a direct or indirect shareholder of an offshore company is required to update his registration with the relevant SAFE branches, with respect to that offshore company, in connection with any material change involving an increase or decrease of capital, transfer or swap of shares, merger, division, equity or debt investment or creation of any security interest. Moreover, the PRC subsidiaries of that offshore company are required to coordinate and supervise the filing of SAFE registrations by the offshore company's shareholders who are PRC residents in a timely manner. If a PRC shareholder with a direct or indirect stake in an offshore parent company fails to make the required SAFE registration, the PRC subsidiaries of such offshore parent company may be prohibited from making distributions of profit to the offshore parent and from paying the offshore parent proceeds from any reduction in capital, share transfer or liquidation in respect of the PRC subsidiaries, and the offshore parent company may also be prohibited from injecting additional capital into its PRC subsidiaries. Furthermore, failure to comply with the various SAFE registration requirements described above may result in liability for the PRC shareholders and the PRC subsidiaries under PRC law for foreign exchange registration evasion.

Although we have requested our PRC shareholders to complete the SAFE Circular No. 75 registration, there is no assurance that all of our PRC resident beneficial owners will be able to comply with the requirements imposed by Circular 75. The failure or inability of our PRC shareholders to receive any required approvals or make any required registrations may subject us to fines and legal sanctions, restrict our overseas or cross-border investment activities, limit our PRC subsidiaries' ability to make distributions or pay dividends or affect our ownership structure, as a result of which our acquisition strategy and business operations and our ability to distribute profits to you could be materially and adversely affected.

Under Operating Rules on the Foreign Exchange Administration of the Involvement of Domestic Individuals in the Employee Stock Ownership Plans and Share Option Schemes of Overseas Listed Companies, issued and effective as of March 28, 2007 by the State Administration of Foreign Exchange, or “SAFE Circular No. 78”, PRC residents who are granted shares or share options by an overseas listed company according to its employee share option plan or share incentive plan are required to obtain approval from and register with the SAFE or its local branches and complete certain other procedures related to the share option or other share incentive plan through the PRC subsidiary of such overseas listed company or any other qualified PRC agent before such grants are made. We intend to grant our PRC employees stock options pursuant to an employee stock option plan. We believe that all of our PRC employees who will be granted share options are subject to SAFE Circular No. 78. We will request our PRC management, personnel, directors and employees who are to be granted stock options to register them with local SAFE branches pursuant to Circular No. 78. However, we cannot assure you that each of these individuals will successfully comply with all the required procedures above. If we or our PRC security holders fail to comply with these regulations, we or our PRC security holders may be subject to fines and legal sanctions. Further, failure to comply with the various SAFE registration requirements described above could result in liability under PRC law for foreign exchange evasion and we may become subject to a more stringent review and approval process with respect to our foreign exchange activities.

19

Our agreements with Huanjiang Jintai are governed by the laws of the PRC and we may have difficulty in enforcing any rights we may have under these contractual arrangements.

Our contractual arrangements with Huanjiang Jintai are governed by PRC law and any disputes would be adjudicated by arbitration through the China International Economic and Trade Arbitration Commission (“CIETAC”) Shanghai Branch in accordance with CIETAC arbitration rules. If Huanjiang Jintai and its shareholder fail to perform their obligations under these agreements, we may incur substantial costs to enforce such arrangements and will have to rely on legal remedies provided under PRC law. However, uncertainties in the Chinese legal system could limit our ability to enforce these contractual arrangements. In the event that we are unable to enforce these contractual arrangements, our business, financial condition and results of operations would be materially and adversely affected.

Mr. Kuizhong Cai, as the majority beneficial owner of Huanjiang Jintai, has a potential conflict of interest with our shareholders.

As of the date of this prospectus, our Chairman of the Board and President, Mr. Kuizhong Cai owns 80.26% of the equity interest of Huanjiang Jinteng Mining Co., Ltd. (“HJM”), the entity which owns 100% of the equity interest in Huanjiang Jintai. In addition, Mr. Kuizhong Cai owns a 75% equity interest in our Company, which controls 100% of Jintai HK, which, in turn, owns 100% of the equity interest of Xiangguang, the entity which entered into the contractual arrangements with Huanjiang Jintai. As a result, Mr. Kuizhong Cai may ultimately have control over Huanjiang Jintai through both equity ownership and contractual arrangements. Mr. Kuizhong Cai also will hold 54.6% of our outstanding common stock after the offering on a fully-diluted base and currently serves as the Chairman of our Board of Directors. As such, there may be a potential conflict of interest between his dual roles as a beneficial majority owner of Huanjiang Jintai and our majority shareholder and Chairman of our Board of Directors. We cannot assure you that when conflicts of interest arise, Mr. Cai will act in our best interests or that conflicts of interest will be resolved in our favor or in favor of our shareholders. In addition, Huanjiang Jintai, which is under Mr. Cai’s control, may breach or refuse to renew the existing contractual arrangements that allow us to receive economic benefits from Huanjiang Jintai. If we cannot resolve any conflicts of interest or disputes between us and Mr. Cai, we would have to rely on legal proceedings, which would be a burden to our resources and could result in disruption of our business and substantial uncertainty as to the outcome of any such legal proceedings.

Risks Related to Doing Business in China

We depend upon the acquisition and maintenance of licenses to conduct our business in the PRC.

In order to conduct business, especially mining and exploration activities in the PRC, we are required to maintain various licenses from the appropriate government authorities, including general business licenses and licenses and/or permits specific to our mining operations. We are required to maintain valid mining licenses, exploration licenses, pollutant emission licenses, safety production licenses and other relevant licenses and permits to conduct our mining extraction and exploration activities. Our mining license is subject to periodic renewal. An application for renewal needs to be submitted at least 30 days before the expiration date and the extension will be approved if the applicant satisfies all applicable requirements and pays the appropriate resource fee. Ten, twenty and thirty years are the maximum periods of time for mining licenses for small, medium and large deposits of ore mines, respectively. We have a nine year mining license as our Ore Mine is regarded to have a medium-scale deposit of ore. On the other hand, the relevant Land and Resources Law of PRC1 allows for two-year extensions of an exploration rights license. As per the Regulations for Administration of Mineral Resources of Guangxi Zhuang Autonomous Region, the granting of an extension of an exploration rights license is dependent upon the exploration stage a company is at. At the first two stages (reconnaissance and prospecting), no extensions are allowed. However, once a company enters the third stage (general exploration) and/or the fourth stage (detailed exploration), it is permitted to extend its license up to two times, each for two year periods. As an alternative to an application for an extension, a company may instead apply for a license reservation, but such is conditioned on the mining company having reached the general exploration stage. A company is permitted to apply for a license reservation for up to two times, each for a two-year period. 2 Following the expiration of such reservation periods, we could apply for mining licenses by submitting geological exploration reports and related documents. In pursuant to the “Implementing Rules of Mineral Resources Law” and related regulations, companies with exploration rights should be given the preference in applying mining rights in the exploration area.

2 Ibid Article 21.

20