Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

| x | REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ¨ | SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number

BRASILAGRO – COMPANHIA BRASILEIRA DE PROPRIEDADES AGRÍCOLAS

(Exact name of Registrant as specified in its charter)

BrasilAgro – Brazilian Agricultural Real Estate Company

(Translation of issuer’s name into English)

The Federative Republic of Brazil

(Jurisdiction of incorporation or organization)

1309 Av. Brigadeiro Faria Lima, 5th floor, São Paulo, São Paulo 01452-002, Brazil

(Address of principal executive offices)

Julio Cesar de Toledo Piza Neto,

Chief Executive Officer and Investor Relations Officer,

Tel. +55 11 3035 5350, Fax +55 11 3035 5366, ri@brasil-agro.com

1309 Av. Brigadeiro Faria Lima, 5th floor

São Paulo, São Paulo 01452-002, Brazil

(Name, Telephone, E-mail and/or Facsimile number and Address of Company Contact Person)

Securities registered or to be registered pursuant to Section 12(b) of the Act:

| Title of each class | Name of each exchange on which registered | |||

American Depositary Shares, each representing one ordinary share, no par value | New York Stock Exchange | |||

| * | Not for trading but only in connection with the registration of American Depositary Shares. |

Securities registered or to be registered pursuant to Section 12(g) of the Act: None

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act: None

Indicate number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close of the period covered by the annual report.

| Ordinary shares, no par value | 58,422,400 |

BrasilAgro – Brazilian Agricultural Real Estate Company is an emerging growth company as defined in Section 3(a) of the Securities Exchange Act of 1934.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ¨ No ¨

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes ¨ No ¨ (Note: None required of the registrant)

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act (check one):

Large accelerated filer ¨ Accelerated filer ¨ Non-accelerated filer x Smaller reporting company ¨

Indicate by check mark which basis of accounting the registrant has used to prepare the financial statements included in this filing:

U.S. GAAP ¨ | International Financial Reporting Standards as issued by the International Accounting Standards Board x | Other ¨ |

If “Other” has been checked in response to the previous question, indicate by check mark which financial statement item the registrant has elected to follow. Item 17 ¨ Item 18 ¨

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ¨

Table of Contents

| Page | ||||

| ii | ||||

| ii | ||||

| v | ||||

| 1 | ||||

ITEM 1—IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS | 1 | |||

| 3 | ||||

| 3 | ||||

| 24 | ||||

| 38 | ||||

| 38 | ||||

| 55 | ||||

| 64 | ||||

| 69 | ||||

| 75 | ||||

| 80 | ||||

ITEM 11—QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK | 114 | |||

ITEM 12—DESCRIPTION OF SECURITIES OTHER THAN EQUITY SECURITIES | 115 | |||

| 123 | ||||

| 123 | ||||

ITEM 14—MATERIAL MODIFICATIONS TO THE RIGHTS OF SECURITY HOLDERS AND USE OF PROCEEDS | 123 | |||

| 123 | ||||

| 123 | ||||

| 123 | ||||

| 123 | ||||

ITEM 16D—EXEMPTIONS FROM THE LISTING STANDARDS FOR AUDIT COMMITTEES | 123 | |||

ITEM 16E—PURCHASES OF EQUITY SECURITIES BY THE ISSUER AND AFFILIATED PURCHASERS | 123 | |||

| 123 | ||||

| 124 | ||||

| 124 | ||||

| 124 | ||||

| 125 | ||||

| 125 | ||||

| F-1 | ||||

i

Table of Contents

Unless the context otherwise requires, the terms “Brazil” and the “Brazilian Government” refer to the Federative Republic of Brazil; the term “BrasilAgro” refers to BrasilAgro – Companhia Brasileira de Propriedades Agrícolas and its consolidated subsidiaries; and unless indicated otherwise, the terms “we,” “our” or “us” refer to BrasilAgro.

PRESENTATION OF FINANCIAL INFORMATION

All references herein to “real,” “reais” or “R$” are to the Brazilian real, the official currency of Brazil. All references to “U.S. dollars,” “dollars” or “US$” are to U.S. dollars.

On June 30, 2012, the year-end of our fiscal year, the exchange rate for reais into U.S. dollars was R$2.0213 to US$1.00, based on the selling rate as reported by the Central Bank of Brazil (Banco Central do Brasil), or the Central Bank. On June 30, 2011, the selling rate was R$1.5611 to US$1.00. The selling rate was R$1.8015 to US$1.00 at June 30, 2010, R$1.9516 to US$1.00 at June 30, 2009, and R$1.5919 to US$1.00 at June 30, 2008, in each case, as reported by the Central Bank. The real/U.S. dollar exchange rate fluctuates widely, and the selling rate at June 30, 2012 may not be indicative of future exchange rates. See “Item 3—Key Information—Exchange Rates” for information regarding exchange rates for the real since January 1, 2006.

Solely for the convenience of the reader, we have translated certain amounts included in “Item 3—Key Information—Selected Financial Information” in this registration statement from reais into U.S. dollars, unless otherwise indicated, using the selling rate as reported by the Central Bank at June 30, 2012 of R$2.0213 to US$1.00. These translations should not be considered representations that any such amounts have been, could have been or could be converted into U.S. dollars at that or at any other exchange rate.

Financial Statements

We maintain our books and records in reais. Our fiscal year is from July 1 of each year to June 30 of the following year. Our consolidated financial statements as of June 30, 2012, June 30, 2011 and 2010 and for the years ended June 30, 2012, 2011 and 2010 have been audited, as stated in the report annexed hereto.

We prepared our annual consolidated financial information included herein in compliance with International Financial Reporting Standards, or IFRS, as issued by the International Accounting Standards Board, or the IASB. Our consolidated financial statements as of and for the year ended June 30, 2011 are our first annual consolidated financial statements to be prepared in compliance with IFRS. IFRS 1, “First-time Adoption of International Reporting Standards,” has been applied in preparing these consolidated financial statements.

Until June 30, 2010, we prepared our annual consolidated financial statements in accordance with accounting practices adopted in Brazil in effect on and prior to June 30, 2010, or Brazilian GAAP, which were based on:

| • | Brazilian Law No. 6,404/76, as amended by Brazilian Law No. 9,457/97, Brazilian Law No. 10,303/01, and Brazilian Law No. 11,638/07, which we refer to collectively as Brazilian corporate law; |

| • | the rules and regulations of the Brazilian Securities Commission (Comissão de Valores Mobiliários), or the CVM, the accounting standards issued by the Brazilian Institute of Independent Accountants (Instituto dos Auditores Independentes do Brasil), or Ibracon, and the Brazilian Federal Accounting Council (Conselho Federal de Contabilidade), or CFC; and |

| • | the accounting standards issued by the Brazilian Accounting Standards Committee (Comitê de Pronunciamentos Contábeis), or the CPC, and applicable on and prior to June 30, 2010. |

ii

Table of Contents

Brazilian GAAP as previously in effect during our fiscal year ended June 30, 2011 has been modified through the adoption of several standards issued by the CPC, which are equivalent to the corresponding standards issued by the IASB, and which resulted in Brazilian GAAP as currently required for consolidated financial statements being in compliance with IFRS as issued by the IASB.

In preparing our consolidated financial statements as of and for the year ended June 30, 2011, all comparative figures have been restated to reflect the effects of the transition from Brazilian GAAP to IFRS.

As required under Brazilian corporate law, we also prepare parent-company financial statements, in accordance with Brazilian GAAP. Our parent-company financial statements are statutorily required for certain purposes, including for calculation of dividends. Brazilian GAAP, as applied in the preparation of our parent-company financial statements, differs from IFRS as issued by the IASB in that (1) Brazilian GAAP requires presentation of a value added statement, and (2) Brazilian GAAP requires the application of the equity method of accounting in investments in associates and subsidiaries while under IFRS as issued by the IASB these are recorded either at their cost or fair value. The parent-company financial statements under Brazilian GAAP are not presented herein.

Crop Year, Harvest and Planting Season

Our agricultural production is based on the crop year, which varies according to each crop. The crop year for sugarcane is from January 1 to December 31 of the same year, and the crop year for grains is from July 1 to June 30 of the following year. We also make reference to the planting season and the harvest season, or harvest period. In Brazil, the planting season for grains is from September to December, and the planting season for sugarcane is from February to May. The harvesting period in Brazil for grains is from February to May, and such period for sugarcane is from April to November.

Market Information

The market information included herein concerning the Brazilian economy and the domestic and international agriculture industry was obtained from market research, publicly available information and industry publications from established public sources, such as the Brazilian Central Bank, the Brazilian Institute of Geography and Statistics (Instituto Brasileiro de Geografia e Estatística), or the IBGE, the Brazilian Food Supply Company (Companhia Nacional de Abastecimento), or Conab, a state-owned company, the Brazilian Ministry of Agriculture, Livestock and Food Supply (Ministério da Agricultura, Pecuária e Abastecimento), or MAPA, the U.S. Department of Agriculture, or USDA, the U.S. Food and Agriculture Organization, or FAO, the United Nations, and the Organization for Economic Cooperation and Development, or OECD, as well as from other public institutions and independent sources as indicated throughout this registration statement. We believe that such information is true and accurate as of the date of this registration statement.

Rounding

Some percentages and amounts included herein have been rounded for ease of presentation. Accordingly, figures shown as totals in certain tables may not be arithmetic aggregations of the figures that precede them.

Emerging Growth Company Status

We are an “emerging growth company,” as defined in Section 3(a) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, as modified by the Jumpstart Our Business Startups Act of 2012, or the JOBS Act. As such, we are eligible to take advantage of certain exemptions from various reporting requirements that are applicable to other public companies that are not “emerging growth companies” including, but not limited to, not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, or the Sarbanes-Oxley Act, or any Public Company Accounting Oversight Board, or “PCAOB” rules, including mandatory audit firm rotation and auditor discussion and analysis rules and any future audit rule promulgated by the PCAOB (unless the SEC determines otherwise). We have not made a decision whether to take advantage of any or all of these exemptions. If we do take advantage of any of these exemptions, we do not know if some investors will find our common stock less attractive as a result. The result may be a less active trading market for our common stock and our stock price may be more volatile.

iii

Table of Contents

We could remain an “emerging growth company” until the earliest of (a) the last day of the first fiscal year in which our annual gross revenues exceed $1 billion, (b) the last day of our fiscal year following the fifth anniversary of the date of our first sale of our common equity securities pursuant to an effective registration statement under the Securities Act, (c) the date on which we have issued more than $1 billion in non-convertible debt during the preceding three-year period, or (d) the date that we become a “large accelerated filer” as defined in Rule 12b-2 under the Exchange Act, which would occur if the market value of our common stock that is held by non-affiliates exceeds $700 million as of the last business day of our most recently completed second fiscal quarter.

iv

Table of Contents

This registration statement includes, and future public filings and oral and written statements by our management may include, statements that constitute forward-looking statements. These statements are based on the beliefs and assumptions of our management and on information available to management at the time such statements were made. Forward-looking statements include, but are not limited to: (a) information concerning possible or assumed future results of our operations, earnings, industry conditions, demand and pricing for our services and other aspects of our business under “Item 4—Information on the Company,” “Item 5—Operating and Financial Review and Prospects” and “Item 11—Quantitative and Qualitative Disclosures About Market Risk”; and (b) statements that are preceded by, followed by or include the words “believes,” “expects,” “anticipates,” “intends,” “is confident,” “plans,” “estimates,” “may,” “might,” “could,” “would,” the negatives of such terms or similar expressions.

Forward-looking statements are not guarantees of future performance. They involve risks, uncertainties and assumptions. Although we make such statements based on assumptions that we believe to be reasonable, there can be no assurance that actual results will not differ materially from our expectations. Many of the factors that will determine these results are beyond our ability to control or predict. We do not intend to review or revise any particular forward-looking statements referenced in this registration statement in light of future events or to provide reasons why actual results may differ therefrom. Investors are cautioned not to put undue reliance on any forward-looking statements.

Any of the following important factors, and those described elsewhere in this or in other of our filings with the U.S. Securities and Exchange Commission, or the SEC, among other things, could cause our results to differ from any results that might be projected, forecasted or estimated by us in any such forward-looking statements:

| • | the economic, political and business situation in Brazil; |

| • | inflation, depreciation or appreciation of the real against foreign currencies and interest rate fluctuations; |

| • | changes in prices in the Brazilian agricultural real estate sector; |

| • | developments in, or changes to, Brazilian legislation and regulation governing our business and products or failure to comply with them, including environmental and sanitary liabilities and accounting developments; |

| • | governmental intervention impacting the economy, taxes or tariffs; |

| • | loss of investment grade ratings for Brazil as issued by any of the international rating agencies; |

| • | conditions of transportation infrastructure and logistics in Brazil; |

| • | our ability to execute our business strategy, including our ability to finance our operations at reasonable terms and conditions, if necessary; |

| • | our level of debt and other obligations; |

| • | changes in the domestic and international agricultural commodity markets; |

| • | availability and changes in prices of raw materials, skilled labor, oil and oil products, fertilizers, lime, machinery and other agricultural inputs; |

| • | outbreaks of diseases affecting our farms and crops; |

| • | our ability to obtain and maintain environmental permits for our existing or new areas of operations; |

v

Table of Contents

| • | supply and demand for our products; |

| • | weather conditions in our areas of operations; |

| • | the interests of our controlling shareholder, Cresud; |

| • | other factors that may affect our financial condition, liquidity and operating result, and |

| • | other risks discussed under “Item 3—Key Information—Risk Factors.” |

vi

Table of Contents

ITEM 1—IDENTITY OF DIRECTORS, SENIOR MANAGEMENT AND ADVISERS

Board of Directors

Our board of directors is responsible for establishing our overall business plan, guidelines and policies, including our long term strategy, and for overseeing our performance. Our board of directors is also responsible for the supervision of our executive officers.

Pursuant to our bylaws, our board of directors consists of a minimum of five and a maximum of nine members. Election of our directors is made at our annual shareholders’ meetings. The members of our board are elected for a term of approximately two years, with reelection permitted. A director must remain in office until replaced by a successor. However, any director may be removed by the shareholders before the end of such director’s term.

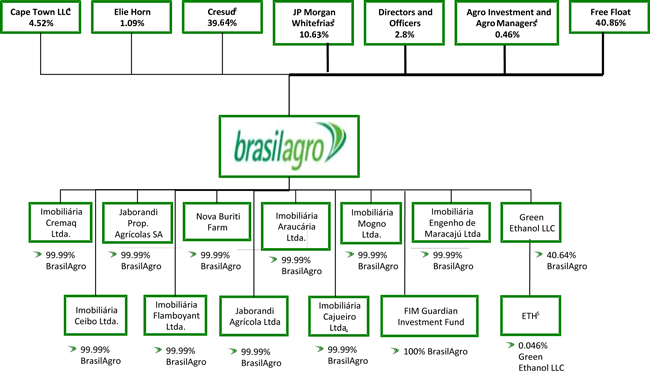

Our controlling shareholder is Cresud, who, at the date of this registration statement, holds 39.64% of our common shares. Cresud was organized in December 1936 under the laws of Argentina. Cresud’s principal operating activities consist of the acquisition, development and sale of agricultural properties in Argentina, and the production of agricultural products. Its shares are listed on the Buenos Aires Stock Exchange (Bolsa de Comércio de Buenos Aires) and on the Nasdaq (under the symbol CRESY). At the date of this registration statement, four members of our board of directors, namely Eduardo Elsztain, Saul Zang, Alejandro G. Elsztain and Gabriel Pablo Blasi, were nominated by Cresud.

In addition to our bylaws, the Novo Mercado rules also subject us to additional corporate governance requirements. The Novo Mercado is a stock market segment of the BM&FBOVESPA intended for companies meeting certain requirements and agreeing to adhere to heightened corporate governance rules, which are summarized in further detail under “Item 9—The Offer and Listing—The Novo Mercado Segment.” Under Novo Mercado regulations as well as our bylaws, a minimum of 20% of the members of our board of directors must be independent. However, in the case that our board consists of nine members, three of such directors must be independent. Prior to taking office, our board members are required to sign an agreement requiring them to comply with Novo Mercado regulations.

Our board of directors holds mandatory meetings six times per year, and may hold other meetings, as necessary. Meetings of our board of directors are convened only if a majority of the directors are present; and all board decisions are taken by a two-thirds or three-fourths majority, or by simple majority, depending on the nature of the matters under discussion.

Brazilian Corporate Law and CVM Regulation No. 282 of June 26, 1998 allow the adoption of a cumulative vote process by the request of a number of our shareholders representing a minimum of 5% of our capital stock. Such request by our shareholders may be made on a meeting by-meeting-basis. Brazilian Corporate Law allows minority shareholders that, individually or as a group, hold at least 15% of our common shares to appoint one director, by means of a separate vote. Brazilian Corporate Law does not allow for the election to our board of directors of any person that is an employee or senior officer of one of our competitors or has an interest that conflicts with ours, although this rule may be waived by our shareholders.

Our board of directors is currently made up of seven members, all of whom were elected at the general shareholders’ meeting held on October 27, 2011 and whose terms expire at our annual shareholders’ meeting in 2013.

1

Table of Contents

The table below sets forth the name, title, date of election and date of the end of the term of each current member of our board of directors:

Directors | Title | Date of election | Age | |||

Eduardo S. Elsztain | Chairman | October 27, 2011 | 52 | |||

Robert Charles Gibbins | Vice-Chairman and Independent Director | October 27, 2011 | 43 | |||

Alejandro G. Elsztain | Director | October 27, 2011 | 46 | |||

Saul Zang | Director | October 27, 2011 | 66 | |||

Isaac Selim Sutton | Independent Director | October 27, 2011 | 51 | |||

Gabriel Pablo Blasi | Director | October 27, 2011 | 51 | |||

João de Almeida Sampaio Filho | Independent Director | October 27, 2011 | 45 |

The business address of each member of our board of directors is 1309 Av. Brigadeiro Faria Lima, 5th floor, São Paulo, São Paulo, 0145-002, Brazil.

Board of Executive Officers

Our board of executive officers may be composed of two to six officers who may or may not be shareholders but who must all be residents of Brazil. Our board of executive officers is nominated by our board of directors. Currently, we have four executive officers. Our executive officers are nominated for a one year term with reelection permitted, and are required to remain in office until the installation of their successors. Under Novo Mercado rules, our executive officers are required to sign an agreement to comply with the rules of the Novo Mercado prior to taking office.

Our executive officers are our legal representatives and are responsible for our day to day management, implementation of the policies and directives set by our board of directors and other duties assigned to them under applicable law and our bylaws. Our executive officers are authorized to take all actions required for the operation of our business, unless applicable law or our bylaws specifically delegate such authority to the shareholders’ meeting or our board of directors.

The table below indicates the name, title, date of election and term of office of each current member of our board of executive officers:

Executive officers | Title | Date of election | End of term of office | Age | ||||

Julio César de Toledo Piza Neto | Chief executive officer and investor relations officer | December 13, 2011 | November, 2012* | 40 | ||||

Gustavo Javier Lopez | Chief administrative officer | December 13, 2011 | November, 2012* | 43 | ||||

André Guillaumon | Chief operating officer | December 13, 2011 | November, 2012* | 36 | ||||

Mario Aguirre | Agricultural technical officer | December 13, 2011 | November, 2012* | 45 |

| * | The officers shall remain in office until the Directors’ Meeting to be held promptly after the General Shareholders’ Meeting at which the 2012 financial results will be considered for approval. |

The address of our executive officers is 1309 Av. Brigadeiro Faria Lima, 5th floor, São Paulo, São Paulo, 0145-002, Brazil.

Advisers

Our legal adviser in Brazil is Mattos Filho, Veiga Filho, Marrey Jr. e Quiroga Advogados, the business address of which is Al. Joaquim Eugênio Lima, 447, Sao Paulo, SP, 01403-001, Brazil. Our legal adviser in the U.S. is Simpson Thacher & Bartlett LLP, the business address of which is 425 Lexington Avenue, New York NY 10017, USA. Our auditor for the preceding three years is PricewaterhouseCoopers Auditores Independentes, the business address of which is Avenida Francisco Matarazzo, 1400, Torre Torino, São Paulo, SP 05001-100, Brazil.

2

Table of Contents

ITEM 2—OFFER STATISTICS AND EXPECTED TIMETABLE

We are not required to provide the information called for by Item 2.

Selected Consolidated Financial Data

The information set forth below is qualified by reference to, and should be read in conjunction with, our audited financial statements and the notes thereto and also “Item 5—Operating and Financial Review and Prospects” included in this registration statement.

The selected financial data has been derived from our audited consolidated financial statements as of June 30, 2012, 2011 and 2010 and for the years ended June 30, 2012, 2011 and 2010 prepared in compliance with IFRS as issued by the IASB.

We have included information with respect to dividends and/or interest attributable to shareholders’ equity paid to holders of our common shares and preferred shares since June 30, 2008 in reais and in U.S. dollars translated from reais at the commercial market selling rate in effect as of the payment date under the caption “Item 8—Financial Information—Dividends and Dividend Policy—Recent Dividend Payments.”

| Year ended June 30, | ||||||||||||||||

| 2012 | 2012 | 2011 | 2010 | |||||||||||||

| (US$ thousand) | (R$ thousand) | |||||||||||||||

CONSOLIDATED STATEMENT OF OPERATIONS | ||||||||||||||||

Revenue | 72,339 | 146,218 | 79,544 | 36,745 | ||||||||||||

Gain on farm sale | 6,425 | 12,987 | ||||||||||||||

Gain (loss) in fair value of biological assets and agricultural product | (206 | ) | (417 | ) | 22,761 | (25,076 | ) | |||||||||

Impairment to net realizable value of agricultural produce after harvest | (1,317 | ) | (2,663 | ) | (986 | ) | (2,059 | ) | ||||||||

Cost of sales | (67,505 | ) | (136,447 | ) | (61,500 | ) | (30,310 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Gross profit (loss) | 9,735 | 19,678 | 39,819 | (20,700 | ) | |||||||||||

Selling expenses | (1,986 | ) | (4,015 | ) | (2,991 | ) | (2,175 | ) | ||||||||

General and administrative expenses | (14,294 | ) | (28,892 | ) | (26,330 | ) | (22,916 | ) | ||||||||

Other gains | 5 | 10 | 73 | 416 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Operating profit (loss) | (6,540 | ) | (13,219 | ) | 10,571 | (45,375 | ) | |||||||||

Financial income | 18,836 | 38,073 | 25,738 | 24,147 | ||||||||||||

Financial expenses | (21,916 | ) | (44,299 | ) | (16,460 | ) | (8,368 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

Profit (loss) before income tax and social contribution | (9,620 | ) | (19,445 | ) | 19,849 | (29,596 | ) | |||||||||

Income tax and social contribution | 6,355 | 12,845 | (5,186 | ) | 10,108 | |||||||||||

|

|

|

|

|

|

|

| |||||||||

Profit (loss) for the year and comprehensive income (loss) for the year | (3,265 | ) | (6,600 | ) | 14,663 | (19,488 | ) | |||||||||

|

|

|

|

|

|

|

| |||||||||

Profit (loss) attributed to: | ||||||||||||||||

Owners of the parent | (2,757 | ) | (5,572 | ) | 14,743 | (18,434 | ) | |||||||||

Non-controlling interests | (509 | ) | (1,028 | ) | (80 | ) | (1,054 | ) | ||||||||

Outstanding shares at the year end | 58,422,400 | 58,422,400 | 58,422,400 | 58,422,400 | ||||||||||||

Basic earnings (loss) per share | (0.05 | ) | (0.10 | ) | 0.25 | (0.32 | ) | |||||||||

Diluted earnings (loss) per share | (0.05 | ) | (0.10 | ) | 0.25 | (0.32 | ) | |||||||||

3

Table of Contents

| Year ended June 30, | ||||||||||||||||

| 2012 | 2012 | 2011 | 2010 | |||||||||||||

| (US$ thousand) | (R$ thousand) | |||||||||||||||

CONSOLIDATED CASH FLOW | ||||||||||||||||

Net cash used in operating activities | (5,289 | ) | (10,691 | ) | (32,633 | ) | (38,962 | ) | ||||||||

Net cash used in investment activities | (12,059 | ) | (24,375 | ) | (33,998 | ) | (60,733 | ) | ||||||||

Net cash generated from (used in) financing activities | (16,368 | ) | (33,085 | ) | (3,954 | ) | 41,525 | |||||||||

|

|

|

|

|

|

|

| |||||||||

Net change in cash and cash equivalents | (33,716 | ) | (68,151 | ) | (70,585 | ) | (58,170 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

4

Table of Contents

| As of June 30, | ||||||||||||||||

| 2012 | 2012 | 2011 | 2010 | |||||||||||||

| (US$ thousand) | (R$ thousand) | |||||||||||||||

CONSOLIDATED BALANCE SHEET | ||||||||||||||||

Assets | ||||||||||||||||

Current assets | ||||||||||||||||

Cash and cash equivalents | 33,377 | 67,464 | 135,615 | 206,200 | ||||||||||||

Trade receivable | 30,008 | 60,655 | 25,971 | 17,773 | ||||||||||||

Inventories | 36,897 | 72,558 | 77,479 | 16,032 | ||||||||||||

Biological assets | 2,034 | 4,111 | 1,335 | 1,001 | ||||||||||||

Tax credits | 4,616 | 9,331 | 4,307 | 3,358 | ||||||||||||

Derivative financial instruments | 2,141 | 4,327 | 5,386 | 1,180 | ||||||||||||

Prepaid expenses | 223 | 450 | 343 | 415 | ||||||||||||

Other assets | 129 | 260 | 578 | 15 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total current assets | 108,423 | 219,156 | 251,014 | 245,974 | ||||||||||||

Non current assets | ||||||||||||||||

Biological assets | 15,797 | 31,931 | 40,334 | 38,696 | ||||||||||||

Time deposits | 11,476 | 23,197 | 21,262 | 26,562 | ||||||||||||

Loans to related parties | — | — | 7,118 | 6,060 | ||||||||||||

Tax credits | 11,281 | 22,803 | 25,784 | 17,655 | ||||||||||||

Deferred taxes | 7,401 | 14,960 | 3,120 | 3,370 | ||||||||||||

Receivable from the sale of farms | 6,312 | 12,759 | 2,936 | 4,293 | ||||||||||||

Investment properties | 193,889 | 391,907 | 383,687 | 357,473 | ||||||||||||

Other assets | 133 | 268 | 94 | 24 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| 246,290 | 497,825 | 484,335 | 454,133 | |||||||||||||

Investments in unquoted equity instruments (at cost less impairment) | 203 | 410 | 410 | 410 | ||||||||||||

Property, plant and equipment | 7,799 | 15,764 | 12,900 | 7,216 | ||||||||||||

Intangible assets | 1,290 | 2,607 | 2,612 | 2,288 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total non-current assets | 255,581 | 516,606 | 500,257 | 464,047 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total assets | 364,004 | 735,762 | 751,271 | 710,021 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Liabilities | ||||||||||||||||

Current liabilities | ||||||||||||||||

Trade and other payables | 2,054 | 4,151 | 2,435 | 1,803 | ||||||||||||

Loans and financings | 21,307 | 43,067 | 37,899 | 28,689 | ||||||||||||

Labor obligations | 3,679 | 7,436 | 4,801 | 4,143 | ||||||||||||

Taxes payable | 1,225 | 2,476 | 767 | 614 | ||||||||||||

Dividends payable | 1 | 2 | 2 | 2 | ||||||||||||

Derivative financial instruments | 4110 | 8,307 | 2,918 | 60 | ||||||||||||

Payable for purchase of farms | 20,214 | 40,858 | 57,521 | 61,420 | ||||||||||||

Advance from customers | 2,221 | 4,490 | 5,909 | 178 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total current liabilities | 54,810 | 110,787 | 112,252 | 96,909 | ||||||||||||

Non-current liabilities | ||||||||||||||||

Loans and financings | 25,377 | 51,294 | 55,436 | 49,299 | ||||||||||||

Deferred taxes | 1,643 | 3,321 | 6,168 | 2,203 | ||||||||||||

Derivative financial instruments | 5,051 | 10,209 | — | — | ||||||||||||

Other liabilities | 585 | 1,183 | 492 | 782 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total non-current liabilities | 32,656 | 66,007 | 62,096 | 52,284 | ||||||||||||

Equity capital attributed to owners of the parent | ||||||||||||||||

Equity: | ||||||||||||||||

Share capital | 289,034 | 584,224 | 584,224 | 584,224 | ||||||||||||

Capital reserves | 1,056 | 2,134 | 996 | — | ||||||||||||

Other reserves | (3,424 | ) | (6,920 | ) | — | — | ||||||||||

Accumulated losses | (10,127 | ) | (20,470 | ) | (14,898 | ) | (29,641 | ) | ||||||||

|

|

|

|

|

|

|

| |||||||||

| 276,539 | 558,968 | 570,322 | 554,583 | |||||||||||||

Non-controlling interest | — | — | 6,601 | 6,245 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

| 276,539 | 558,968 | 576,923 | 560,828 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||

Total liabilities and equity | 364,004 | 735,762 | 751,271 | 710,021 | ||||||||||||

|

|

|

|

|

|

|

| |||||||||

Exchange Rates

Our dividends, when paid in cash, are denominated in reais. As a result, exchange rate fluctuations have affected and will affect the U.S. dollar amounts received by holders of ADSs on conversion of such dividends by The Bank of New York, as the ADS depositary. The Bank of New York converts dividends it receives in foreign currency into U.S. dollars upon receipt, by sale or such other manner as it has determined and distributes such U.S. dollars to holders of ADSs, net of The Bank of New York’s expenses of conversion, any applicable taxes and other governmental charges. Exchange rate fluctuations may also affect the U.S. dollar price of the ADSs if they become listed on a stock exchange in the United States.

5

Table of Contents

The Brazilian government may impose temporary restrictions on the conversion of reais into foreign currencies and on the remittance to foreign investors of proceeds from their investments in Brazil. Brazilian law permits the government to impose these restrictions whenever it determines there is an imbalance in Brazil’s balance of payments or reason to expect that one will occur.

The following tables show, for the periods and dates indicated, certain information regarding the real/U.S. dollar exchange rate. On June 30, 2012, the real/U.S. dollar exchange rate was R$2.0213 per US$1.00. On October 30, 2012, 2012 the real/U.S. dollar exchange rate was R$2.03 per US$1.00. The information below is based on the noon buying rate in the City of New York for cable transfers in Brazilian reais as certified for U.S. customs purposes by the Federal Reserve Bank of New York.

| Fiscal year ended June 30, | Average Rate(1) | |||

| (R$ per US$1.00) | ||||

2008 | 1.836 | |||

2009 | 1.996 | |||

2010 | 1.759 | |||

2011 | 1.677 | |||

2012 | 1.792 | |||

| (1) | The average rate is calculated as the average of the noon buying rates on the last day of each month during the period. |

| Period | High | Low | ||||||

| (R$ per US$1.00) | ||||||||

March 2012 | 1.827 | 1.714 | ||||||

April 2012 | 1.908 | 1.818 | ||||||

May 2012 | 2.091 | 1.908 | ||||||

June 2012 | 2.078 | 2.009 | ||||||

July 2012 | 2.057 | 1.985 | ||||||

August 2012 | 2.050 | 2.013 | ||||||

September 2012 | 2.042 | 2.012 | ||||||

October 2012 (through October 30, 2012) | 2.038 | 2.022 | ||||||

6

Table of Contents

Capitalization and Indebtedness

The table below sets forth our total consolidated loans, total current accounts payable for the acquisition of farms and consolidated shareholders’ equity as of June 30, 2012.

| As of June 30, 2012 | ||||||||

| (US$ thousand)(1) | (R$ thousand) | |||||||

Current loans and financing | 21,307 | 43,067 | ||||||

|

|

|

| |||||

Guaranteed | — | — | ||||||

Unguaranteed | — | — | ||||||

Secured | 14,158 | 28,618 | ||||||

Unsecured | 7,148 | 14,449 | ||||||

Non-current loans and financing | 25,377 | 51,294 | ||||||

Guaranteed | — | — | ||||||

Unguaranteed | — | — | ||||||

Secured | 21,769 | 44,002 | ||||||

Unsecured | 3,508 | 7,292 | ||||||

Current accounts payable for the acquisition of farms | 20,214 | 40,858 | ||||||

|

|

|

| |||||

Guaranteed | ||||||||

Unguaranteed | ||||||||

Secured | ||||||||

Unsecured | 20,214 | 40,858 | ||||||

Total equity | 276,539 | 558,968 | ||||||

|

|

|

| |||||

Total capitalization | 343,436 | 694,187 | ||||||

|

|

|

| |||||

| (1) | Translated for convenience only using the exchange rate as reported by the Central Bank on June 30, 2012 for exchanging reais into U.S. dollars of R$2.0213 to US$1.00. |

Risk Factors

Risks Relating to our Business and Industry

We commenced operations in May 2006 and, as a result, have a limited operating history.

Our operating track record, financial statements and business history date to May of 2006 and therefore may not be representative of our business prospects or the future value of our common shares. Since 2006, we have begun implementing our initial strategy, which remains subject to potentially significant alterations in the future. Our strategy may not be successful, and if so, we may not be able to make the necessary changes to our strategy on a timely basis. Substantial uncertainties remain with respect to the geographic regions and agricultural sectors in which we currently invest and will invest in the future, when we might make such investments and what price we might pay for such investments. We are still in the initial investment phase in certain agricultural sectors that are important to our overall strategy. We cannot assure you that we will manage to implement our strategy successfully and, as a result, your investment in our common shares is subject to a high degree of risk. Prior to investing in our common shares you should understand that there is a possibility of loss of your entire investment.

Our ability to implement our business strategy successfully may be adversely affected by numerous factors beyond our control, which may materially and adversely affect our business, financial condition, and results of operations.

Our business strategy depends on our ability to acquire, develop, operate and sell our agricultural properties on a profitable basis. Our strategy is premised on our ability to acquire agricultural properties at attractive prices, develop them into efficient and profitable operations and sell them at a profit in the medium and long term. These factors are essential for our prospects of success, but are subject to significant uncertainties, contingencies and risks within our economic, competitive, regulatory and operational environment, many of which are beyond our control. Our ability to execute our business strategy successfully is uncertain and may be adversely affected by any one or more of the following:

| • | failure to acquire and sell agricultural properties at attractive prices; |

7

Table of Contents

| • | changes in market conditions or our failure to anticipate and adapt to new trends in Brazil’s rapidly evolving agricultural real estate sector; |

| • | inability to overcome certain limitations on the acquisition of land in Brazil by foreigners, as provided in a recent opinion of the Attorney General of the federal government; |

| • | failure to expand our operations within the originally proposed time frame; |

| • | inability to develop infrastructure and attract personnel in a timely and effective manner; |

| • | inability to identify service providers for our agricultural properties and projects; |

| • | increased competition for suitable land from other agricultural real estate owners or developers which increases our costs and adversely affects our margins; |

| • | inability to develop and operate our agricultural properties profitably that may result from inaccurate estimates regarding the cost of infrastructure, other investments or operating costs; |

| • | failure, delays or difficulties in obtaining necessary environmental and regulatory permits; |

| • | the failure of purchasers of our properties to comply with their payment obligations to us; |

| • | increased operating costs, including the need for improvements to fixed assets, insurance premiums and property and utility taxes and fees that affect our profit margins; |

| • | global climate conditions, such as global warming, which may contribute to the frequency of unpredictable and previously rare meteorological phenomena such as hurricanes and typhoons, as well as unpredictable and unusual patterns of rainfall, among others; |

| • | unfavorable climate conditions in Brazil, particularly in the regions where we will carry out our activities; |

| • | the economic, political and business environment in Brazil, and specifically in the geographical regions where we will invest; |

| • | inflation, devaluation of the real and fluctuating interest rates; |

| • | disputes and litigation relating to our agricultural properties; and |

| • | labor, environmental, civil and pension liabilities. |

We may not be able to continue acquiring suitable agricultural properties on attractive terms.

In recent years, investments in Brazil’s agriculture sector have increased substantially. As a result, demand and valuations for the kind of properties we seek to acquire have escalated significantly. We believe that prices for such properties are likely to continue to increase, perhaps significantly as demand is expected to remain high. We compete with local and foreign investors, many of whom are larger and have greater financial resources than we do. Such investors may be able to incur operating losses for a sustained period, retain their real estate investments for a longer period than we can or accept lower returns on such investments. As a result, such investors may be willing to pay substantially higher prices for agricultural properties than we are able or willing to do, depriving us of opportunities to acquire the best agricultural properties and/or increasing our acquisition costs. As a result of the foregoing, we cannot assure you that we will be able to locate and acquire suitable investments on reasonable terms, and our inability to do so would have a material adverse effect on us.

8

Table of Contents

The imposition of restrictions on acquisitions of agricultural properties by non-Brazilian nationals may materially restrict the development of our business.

In August 2010, the president of Brazil approved the opinion of the Attorney General of the federal government affirming the constitutionality of Brazilian Law No. 5,709/71 which imposes important limitations on the acquisition and lease of land in Brazil by foreigners and by Brazilian companies controlled by foreigners. Under this legislation, companies that are majority-owned by foreigners may not acquire agricultural properties in excess of 100 indefinite exploration modules, or MEI (which are measurement units adopted by the National Institute of Agrarian Development (Instituto Nacional de Colonização e Reforma Agrária) or INCRA, within different Brazilian regions, and which range from five to 100 hectares) absent the prior approval of the Brazilian Congress, while the acquisition of areas measuring less than 100 MEIs by such companies requires the prior approval of INCRA. In addition, agricultural areas that are owned by foreigners or companies controlled by foreigners may not exceed 25% of the surface area of the relevant municipality, of which area up to 40% may not belong to foreigners or companies controlled by foreigners of the same nationality, meaning that the sum of agricultural areas that belong to foreigners or companies controlled by foreigners of the same nationality may not exceed 10% of the surface area of the relevant municipality. In addition, INCRA will also verify if the agricultural, cattle-raising, industrial or colonization projects to be developed in such areas were previously approved by the relevant authorities. After that analysis INCRA will issue a certificate allowing the acquisition or lease of the property. The purchase and/or lease of agricultural properties that do not respect the requirements above, need to be authorized by the Brazilian Congress. In both cases, it is not possible to determine an estimated time frame for the approval procedure, since at the date of this registration statement, there are no known cases of certificates having been granted.

At June 30, 2012, 87.5% of our common shares were held by foreigners and, accordingly, the implementation of Law no. 5,709/71 is likely to impose on us additional procedures and approvals in connection with our future acquisitions of land, which may result in material delays and/or our inability to obtain needed approvals. In addition, we may need to modify our business strategy and intended practices in order to be able to acquire agricultural properties. For example, we currently have control over the properties we own, and we would need to acquire properties in partnership with local companies in which we relinquish our right to exercise control over the entities acquiring such properties. This might have the effect increase the number of transactions we must complete, which would add transaction costs. It might also require the execution of joint ventures or shareholder agreements, which increases the complexity and risk associated with such transactions. Any regulatory limitations and restrictions could materially limit our ability to acquire agricultural properties, increase the investments, transaction costs or complexity of such transactions, or complicate the regulatory procedures required, any of which could materially and adversely affect us and our ability to successfully implement our business strategy.

A substantial portion of our assets consist of agricultural properties which are illiquid.

Our business strategy is premised on the appreciation of the capital invested in our agricultural properties and the liquidity of those investments. We cannot assure you that the value of our agricultural properties will increase in the short-, medium- or long-term or that we will be able to monetize our agricultural investments successfully. Agricultural real estate assets are generally illiquid and have volatile values, and agricultural properties in Brazil are especially illiquid and volatile, partially as a result of foreign ownership restrictions that limit the aggregate pool of available purchasers. As a result, it may be difficult for us to promptly adjust our portfolio of properties in response to changes in economic or business conditions, and we may be unable to find purchasers willing to acquire our agricultural properties at prices favorable to us. Lack of liquidity and volatility in local market conditions would adversely affect our ability to execute property dispositions on a timely and profitable basis which would have a material adverse effect on us.

We may not be profitable or our cash flow may not be positive for a number of years.

We expect to incur significant capital and operating expenses for several years on account of our continuing development activities. Due to the capital intensive and long-term nature of our real estate development activities, many of our properties will not generate immediate cash flows or provide a short-term return on investment. Therefore, we may not achieve positive cash flows or profitability for a number of years, and even if we do, we cannot assure you that such positive cash flows or profitability will be sustained in the future. Should we fail to achieve and sustain profitability, our business, financial condition, and results of operations and the market value of our common shares would be adversely affected.

9

Table of Contents

Fluctuation in market prices for our agricultural products could adversely affect us.

We are not able to obtain hedging protection or minimum price guarantees for the entirety of our production and therefore we are exposed to significant risks associated with the level and volatility of crop prices. The prices we are able to obtain for our agricultural products from time to time will depend on many factors beyond our control, including:

| • | global commodity prices, which historically have been subject to significant fluctuations over relatively short periods of time, depending on worldwide supply and demand as well as speculation; |

| • | weather conditions, or natural disasters in areas where agricultural products are cultivated; |

| • | worldwide inventory levels (i.e., supply or stock of commodities carried over from year to year); |

| • | the business strategies adopted by other major companies operating in the agricultural and agribusiness sectors; |

| • | changes in agriculture subsidies with regard to certain important producers (mainly in the United States and the European Economic Community), trade barriers with regard to certain important consumer markets and the adoption of other government policies affecting market conditions and prices; |

| • | available transportation methods and infrastructure development in the regions where we operate or in remote areas serving local markets and which affect the local prices of our crops; and |

| • | supply of and demand for competing commodities and substitutes. |

In addition, we believe there is a close relationship between the value of our agricultural properties and market prices of the commodities we produce which are affected by global economic and other conditions. A decline in the prices of grains, sugar or related by-products below their current levels for a sustained period would significantly reduce the value of our land holdings and materially and adversely affect our business, financial condition, and results of operations.

We are dependent on third-party service providers.

In addition to our own personnel, we are highly dependent on third-party contractors to develop and cultivate our agricultural properties, and to provide the machinery and equipment needed for such purpose. As a result, our future success depends on the skill, experience, knowledge and efforts of our third-party service providers. We cannot assure you that we will be able to hire the desired third-party service providers for our agricultural properties or that such providers will have the ability to ensure quality agricultural production in an efficient manner, and at competitive prices. Our failure to hire the desired service providers for our agricultural properties, or the failure of our providers to provide quality services, or the revocation or termination or our failure to renew our service contracts or negotiate new contracts with other service providers at comparable prices and terms, would adversely affect us.

Our dependence on third-party contractors also subjects us to the risk of labor lawsuits alleging that an employment relationship exists between us and our contractors’ personnel, and that as a result we have joint and several or secondary liability for our contractors’ labor and social security payment obligations, lease payments or other obligations. Such lawsuits could be brought independently by such third-party employees, or could arise as a result of inspections by governmental authorities. The Brazilian Supreme Labor Court (Tribunal Superior do Trabalho) has held that outsourcing is legally permissible with respect to specialized services not related to the outsourcing company’s core business, such that an employment relationship is not formed between the outsourcer and the workers providing the non-core services. In addition, pursuant to the court’s decision, companies hiring

10

Table of Contents

third-party contractors in violation of such standard will be held secondarily liable for labor and social security contingent liabilities of the employees of such third-party contractors. If we are forced to recognize an employment relationship between us and the employees of our third-party service providers, we may be required to change our strategy with regard to the use of third-party service providers, which could have an adverse effect on our business, financial condition, and results of operations.

Moreover, pursuant to Brazilian environmental law we are jointly and severally liable, together with our contractors, for all environmental damages caused by our third-party contractors, irrespective of our fault for such damages. Such obligations or our costs for defending against any such allegations are potentially significant and could have a material adverse effect on us if we were deemed responsible for their payment.

Changes in government policies may adversely affect our business, financial condition, and results of operations.

Government policies for encouraging biofuels as a response to environmental concerns have shown, and are likely to continue to show an impact on grain prices. The nature and scope of future legislation and regulations affecting our markets are unpredictable, and we cannot assure you that current concessions, prices or market protections involving biofuels will be maintained in their current form for any finite period. Any reduction in the support for biofuels on the part of the United States government or any other government may result in stagnation or decline in the market prices of certain agricultural commodities, and consequently on the price of our agricultural properties, which may adversely affect our business, financial condition, and results of operations.

We are subject to extensive environmental regulation.

Our business activities in Brazil are subject to extensive federal, state and municipal laws and regulations concerning environmental protection, which impose on us various environmental obligations, such as environmental licensing requirements, minimum standards for the release of effluents, use of agrochemicals, management of solid waste, protection of certain areas (legal reserve and permanent preservation areas), and the need for a special authorization to use water, among others. The failure to comply with such laws and regulations may subject the violator to administrative fines, mandatory interruption of activities and criminal sanctions, in addition to the obligation to cure and pay environmental and third-party damage compensation, without any caps. In addition, Brazilian environmental law adopts a joint and several and strict liability system for environmental damages, which makes the polluter liable even in cases where it is not negligent and would make us jointly and severally liable for the obligations of our producers or off-takers. If we become subject to environmental liabilities, any costs we may incur to rectify possible environmental damage would lead to a reduction in the financial resources which would otherwise remain at our disposal for current or future strategic investment, thus causing an adverse impact on us.

As environmental laws and their enforcement become increasingly stringent, our expenses for complying with environmental requirements are likely to increase in the future. Furthermore, the possible implementation of new regulations, changes in existing regulations or the adoption of other measures could cause the amount and frequency of our expenditures on environmental preservation to vary significantly compared to present estimates or historical costs. Any unplanned future expenses could force us to reduce or forego strategic investments and as a result could materially and adversely affect us.

If we fail to innovate and utilize modern agricultural technologies and techniques to enhance production and yields of our acquired agricultural properties, we may be adversely affected.

Our business model is focused on our acquiring underdeveloped or underutilized agricultural properties and improving them by applying evolving agricultural technologies and techniques. Therefore, our strategy depends to a large extent on our ability to obtain and apply modern agricultural techniques and technologies to enhance the value of the properties we acquire. If we are unable to apply in a timely manner the most advanced technologies and farming techniques required to add value to our agricultural properties and make our products competitive and attractive to local and international investors, we would be adversely affected.

11

Table of Contents

We may experience difficulties implementing our investment projects, which may affect our growth.

Part of our strategy with regard to our agricultural properties consists of investing in support infrastructure in order to increase the value of such agricultural properties. In implementing our investment projects, we may face a number of challenges, including: (i) failures or delays in acquiring necessary equipment or services: (ii) higher costs than those originally estimated; (iii) difficulties securing the necessary environmental and government licenses; (iv) changes in market conditions, which could render the projects less profitable than originally estimated; (v) impossibility or delays in acquiring land at attractive prices, or an increase in the land prices on account of growing demand for land by our competitors; (vi) impossibility of, and delay in identifying and acquiring land that is in compliance with Brazilian real estate property laws; (vii) lack of capacity to develop infrastructure and attract qualified labor on a timely and efficient basis; (viii) disputes and litigation relating to the land we acquire; (ix) cultural challenges deriving from the integration of new management and employees in our organization; and (x) the need to update accounting systems, administrative data and human resources. Our inability to manage these risks would adversely affect us.

Property values in Brazil could decline significantly.

Property values in Brazil are influenced by a wide variety of factors beyond our control, and therefore we cannot assure you that property values will continue to increase or that property values will not decline. A significant decline in property values in Brazil would adversely affect us.

Our growth depends on our ability to attract and retain qualified personnel.

We are highly dependent on the services of our technical and administrative staff. If we lose any of our senior management, or require additional management personnel, we will have to attract similarly qualified administrative and technical personnel. There is significant demand for high-level, technical personnel with the skills and know-how required to operate our business, and we compete for this talent in the context of a global market. The availability of attractive opportunities in Brazil and other countries may adversely affect our ability to hire or retain highly-qualified personnel. If we fail to attract and retain the professionals we need to expand and manage our operations, we may not be able to manage our business effectively and we may be materially and adversely affected.

Unpredictable weather conditions may have an adverse impact on our agricultural properties and products.

The occurrence of severe weather conditions, including droughts, floods, heavy rainfall, hail, frost or extremely high temperatures is unpredictable and has had and could have in the future a potentially devastating impact on our agricultural properties or production. Adverse weather conditions may be exacerbated by the effects of climate change. In recent years, different regions in Brazil have been affected by extreme weather conditions, and the regions where our properties are located have also experienced high temperatures, high humidity and heavy rainfall in recent years. Higher than average temperatures and rainfall can contribute to an increased presence of insects that are harmful to agriculture or the spread of crop disease. For instance, an increase in Asian rust (ferrugem asiática) affecting soy crops was reported in 2011 in the state of Mato Grosso in Brazil, as a result of high humidity and extensive rainfall. The effect of severe weather conditions may materially reduce the productivity of our farms, impairing our revenue and cash flow, and requiring higher levels of investment or significant increases in our operating costs, any of which could have a material and adverse impact on us.

Diseases may affect our crops, potentially destroying all or part of our production.

The occurrence and effect of diseases can be unpredictable and devastating on crops, potentially rendering useless all or a significant portion of the affected crops. The cost of preventing and treating crop disease tends to be high. For example, the spread of Asian soybean rust (ferrugem asiática), has resulted in lower crop yields and higher operating costs. Currently, Asian soybean rust can only be controlled, not eliminated. The origination and spread of diseases may occur for many reasons beyond our control, including the failure of other agricultural producers to comply with applicable health and environmental regulations. The appearance of new diseases or the mutation or proliferation of existing diseases could damage or completely destroy our crops which would materially and adversely affect us.

12

Table of Contents

Fires and other accidents may affect our agricultural properties and adversely affect us.

Our operations will be subject to various risks affecting our agricultural properties and agricultural installations, including destruction of farms and crops by fire and other natural disasters or events, and theft or other unexpected loss of grains or fertilizers and supplies. We could be materially and adversely affected if any of these risks were to occur.

Widespread uncertainties and fraud involving ownership of real estate in Brazil may adversely affect us.

Under Brazilian law, ownership of real estate is conveyed only through registration of deeds at the applicable land registry. Land registry recording errors, including duplicate or fraudulent entries, and legal challenges to deeds occur frequently. Real estate title litigation is prevalent in Brazil, and as a result there is a risk that such errors, fraud or challenges could adversely affect us, causing the loss of all or substantially all our agricultural properties.

We depend on international trade, and economic and other conditions in our key export markets.

Brazil’s current agricultural production capacity is greater than the consumption requirement of its domestic agricultural market. Agriculture exports account for an increasingly significant portion of our revenue, especially as our rehabilitated farm properties gain crop production capabilities and increased yield. As a result, our results of operations will increasingly depend on political, economic and regulatory conditions in our principal export markets. The ability of our products to compete effectively in these export markets may be adversely affected by a number of factors beyond our control including the deterioration of macroeconomic conditions, the volatility of exchange rates, the imposition of tariffs or other trade barriers or other factors in those markets such as regulations relating to the chemical content of agricultural products and safety and health regulations.

Due to the growing market share of Brazilian agricultural and beef products in the international markets, Brazilian exporters are increasingly being affected by tariffs and other barriers imposed by importing countries to, among other things, protect local producers, limiting access of Brazilian companies to their markets. For example, the European Union currently charges protective tariffs designed to mitigate the effects of Brazil’s lower production costs on local European producers. Developed countries also sometimes use direct and indirect subsidies to enhance the competitiveness of their producers in other markets. The adoption of measures by a given country or region, such as restrictions, import quotas or suspension of imports could substantially affect the export volume of agricultural products and, consequently, our volume of exports and results of operations. If the competitiveness of our products in one or more of our significant markets were to be affected by any one of these events, we may not be able to reallocate our products to other markets on comparable terms, and we could be adversely affected.

Fluctuations in the value of the real in relation to the U.S. dollar could adversely affect us.

Foreign exchange fluctuations, particularly of the Brazilian real against the U.S. dollar, may significantly affect our results of operations given that: (1) our products and the basic supplies used in our production are traded internationally; (2) soybean prices are defined based on prices prevalent on the Chicago Board of Trade, or CBOT; and (3) most markets are served by several suppliers from different countries and competitiveness of farm products abroad may increase in relation to ours in light of the appreciation of the Brazilian currency in relation to the U.S. dollar. Fluctuations in the value of the real in relation to the U.S. dollar could impact our export revenue, our sales in U.S. dollars in the Brazilian market and our financial expenses and operating costs, which may adversely affect us.

We also hold derivative financial instruments to hedge risks relating to foreign currencies on our revenue from exports and operating costs. If we fail to manage these instruments properly we may be adversely affected by our exposure to these risks, which may have a material adverse effect on us.

13

Table of Contents

Our business is seasonal, and our revenue may fluctuate significantly depending on the growing cycle of our crops.

Agribusiness operations are predominantly seasonal in nature. In Brazil the harvest of soybean, corn and rice generally occurs from July to June of the following year. The annual sugarcane harvesting period in Brazil begins in January and ends in December. As a result, our results of operations are likely to continue to fluctuate significantly between the planting and harvesting periods of each crop which cause fluctuations in our cash flows as a result of disparities between our revenue stream and our fixed expenses. In addition, seasonality creates limited windows of opportunity for our producers to complete required tasks at each stage of crop cultivation. Should events such as adverse weather conditions (including deluges of rain as has recently been the case throughout Brazil) or transportation interruptions occur during these seasonal windows, we may be faced with the possibility of reduced revenue without an opportunity to recover until the following crop’s planting. Finally, because of the effects of seasonality, our quarterly results may not be indicative of our annual result.

Our growth will require additional capital which may not be available or may not be available on terms and conditions acceptable to us.

Our operations require a significant amount of capital. It will be necessary for us to seek additional capital by issuing shares or debt securities, or by incurring indebtedness. Our ability to raise capital will depend on our future profitability, which is currently uncertain, and on political and economic conditions in Brazil and the international agricultural and real estate markets. Depending on these and other factors, many of which are beyond our control, additional capital may not be available or, if available, may not be available on conditions that are favorable or acceptable to us. If we are required to finance our activities through indebtedness, it is likely that the terms of that debt will impose upon us obligations or covenants, financial or otherwise, that could restrict our operational flexibility. Should we fail to raise additional capital under conditions that are acceptable to us, we could be adversely affected.

We plan to continue to use financial derivative instruments which may cause substantial losses.

We plan to continue to use derivative financial instruments, principally commodity hedge derivatives, foreign exchange derivatives and exchange rate swaps. If we enter into such hedging agreements and future prices of the underlying commodities differ from our expectations, we may incur substantial losses which could have an adverse effect on us.

Furthermore, our hedging strategies may not properly take account of the effects of foreign exchange or commodity variations on our financial position. On entering into forward exchange and commodity agreements, we will be subject to the risk that our counterparties could fail to fulfill the conditions of the respective agreement. We may not be able to receive compensation for losses and damages from any defaulting counterparty through legal remedies, on account of laws protecting against bankruptcy or other similar protections for insolvent debtors, foreign laws restricting cross-border legal remedies, or for other reasons, which may adversely affect our business, financial condition, and results of operations.

We may not be successful in our future partnerships and strategic relationships.

We may enter into strategic partnerships and alliances in order to benefit from certain business opportunities. We cannot predict if and when such strategic partnerships and alliances will occur. Our ability to expand our business successfully through strategic partnerships and alliances depends on various factors, including our ability to negotiate favorable conditions for such partnerships and alliances, in addition to factors beyond our control, such as our partners’ compliance with obligations arising from the partnership. Furthermore, our expectations regarding the benefits of these partnerships may not materialize. If we are unable to develop successful strategic partnerships and alliances we could be adversely affected.

14

Table of Contents

Cresud, our controlling shareholder, and certain members of our board of directors may have interests that differ from those of our other shareholders.

As of the date of this registration statement, Cresud holds 39.64% of our common shares. Cresud has numerous other investments and may have other priorities that may conflict with those of our other shareholders, and as a result significant conflicts of interest may arise between Cresud and our other shareholders. In addition, four of our seven directors have been nominated by Cresud and therefore are affiliated with such company. In addition, certain members of our management, including our chief administrative officer and our agricultural technical officer, were previously employed by, and as of the date of this registration statement are no longer employed by, Cresud. This situation may give rise to real or apparent conflicts of interest as such directors and officers may have fiduciary duties or other interests owed to both us and Cresud or any of its affiliates. It may also limit the ability of such directors and officers to participate in certain matters. It is impossible to predict whether the outcome of decisions by the members of the board will be favorable to us or to our other shareholders.

In addition, as a result of Cresud’s ownership interest in us, conflicts of interest could arise with respect to transactions involving our ongoing business activities, and the resolution of these conflicts may not be favorable to us. Specifically, business opportunities, including but not limited to potential targets for rural property acquisitions may be attractive to both Cresud and us. We may not be able to resolve any potential conflicts and, even if we do so, the resolution may be less favorable to us than if we were dealing with an unaffiliated party.

Substantially all of our revenue is derived from a small number of clients.

We currently sell a substantial portion of our total crop production to a small number of clients who have substantial bargaining power. For instance, during the year ended June 30, 2012, our three largest customers accounted for 60% of our total revenue. Furthermore, we have entered into a supply contract with ETH Bioenergia S.A., (previously Brenco and hereinafter ETH Bioenergia), pursuant to which we currently supply 100% of our sugarcane production from our Alto Taquari and Araucaria farms to ETH Bioenergia. The term of this supply contract covers two full crop cycles, which consists of six crop years and five harvests, and therefore is scheduled to expire in crop year 2021/2022. As a result, the strong competition between a relatively fragmented sector of agricultural producers in the internal and external markets further increases the bargaining power of our highly concentrated client base. Thus, we may not be able to maintain or form new relationships with customers, which could have a material adverse effect on us.

Concentration among our client base also increases the consequences that would result should we lose any of our clients or if any of our clients default on their obligations to us, either in the form of non-payment or through a breach of any contractual provision or obligation, such as failure to ship a product purchased or delays in shipment. Noncompliance with the time of shipment of our products could directly affect the planning of our harvest, which could generate losses and result in additional costs.

Increases in the price of raw materials and oil may adversely affect us.

Our agricultural properties are located in Brazil’s savannah region where the soil is generally acidic and not very fertile, requiring the use of lime and fertilizers. Our operations require other raw materials such as pesticides and seeds which we acquire from local and international suppliers. We do not have long-term supply contracts for these raw materials and therefore are exposed to the risk of cost increases. A significant increase in the price of lime, fertilizers or other raw materials we use would likely reduce our profitability or otherwise adversely affect our business operations as these are not costs that can readily be passed on to our customers. In addition, certain of our production costs, including fertilizers and the cost of leasing agricultural machinery, are linked to the international price of oil and its derivatives. Therefore, if the price of oil increases significantly, we could be adversely affected.

Delays or failures in the delivery of raw materials used by us and our suppliers could have an adverse affect on us.

We depend on suppliers to provide us with fertilizers, seeds, other raw materials and machinery services. Possible delays in the delivery of such items may delay our planting efforts until we are able to establish agreements with other suppliers, or may delay our harvest in the case of the delay in delivery of machinery. Accordingly, any delays, failures or defects in the delivery of raw materials or inputs or with regard to the provision of services to us by our suppliers could adversely affect our business and our results of operations.

15

Table of Contents

Some of our agricultural products contain genetically modified organisms (GMOs), and risks associated with GMOs remain uncertain.

Approximately 65% of our products, including soybean and corn, contain genetically modified organisms, or GMOs, in varying proportions, depending on the crop year. Production and consumption of GMOs remain controversial, and adverse publicity and consumer resistance has led to adoption of certain governmental regulations limiting sales of GMO products in important markets including the European Union. If GMOs were determined to present risks to human health or to the environment, demand for our GMO products could collapse, and we could face potentially significant liability for harm caused by such products, all of which could materially and adversely affect our business, financial condition, and results of operations.

Lack of transportation, storage and processing infrastructure in Brazil represents an important challenge for the Brazilian agricultural and agricultural real estate sectors.