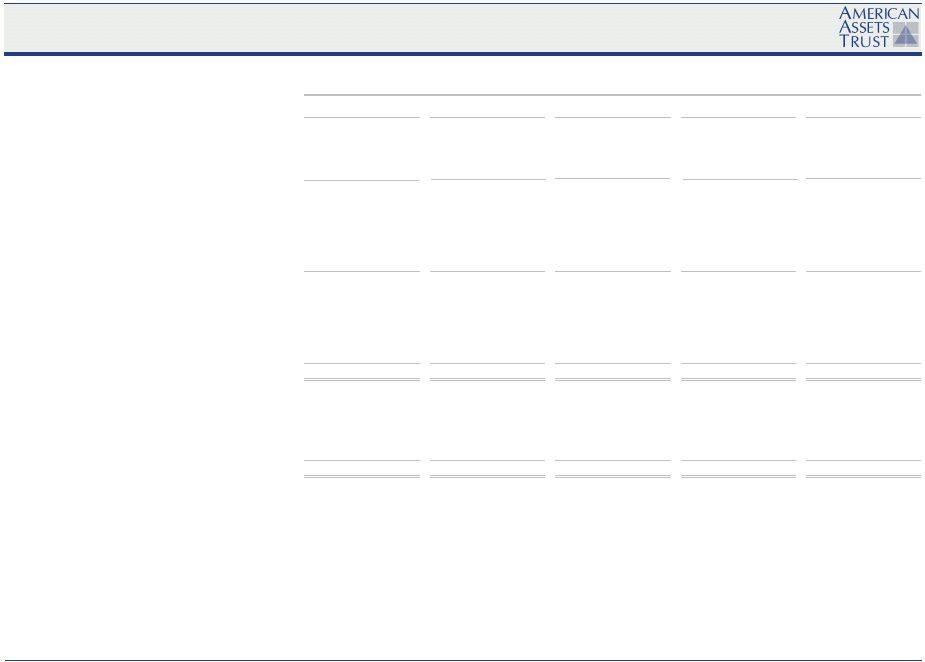

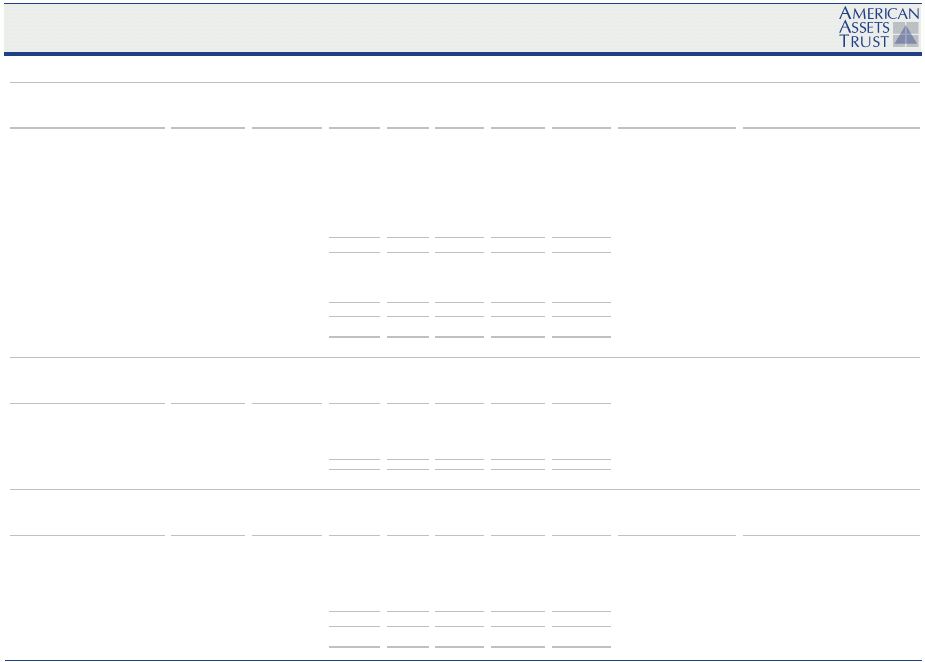

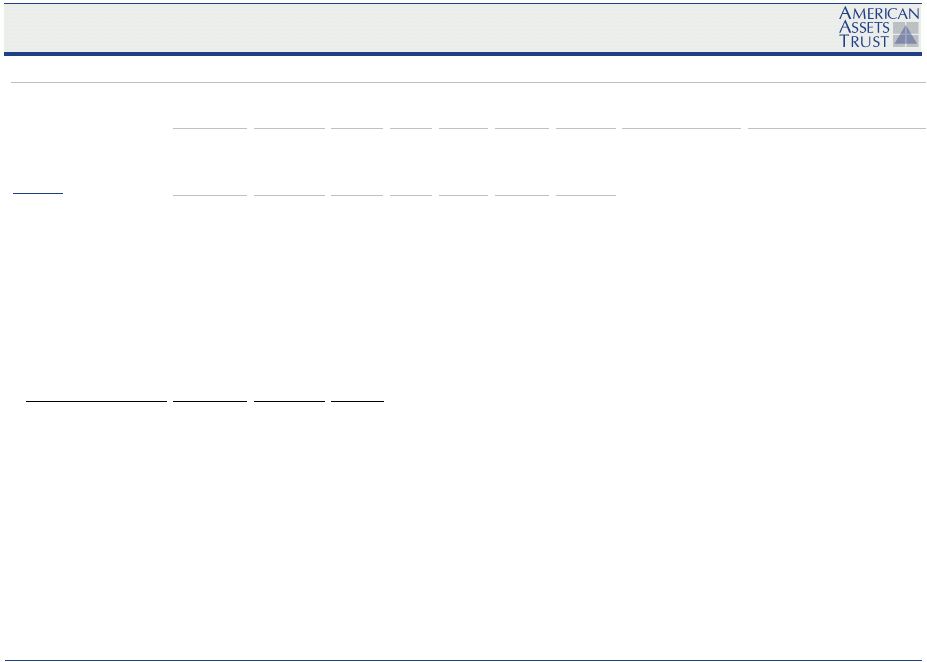

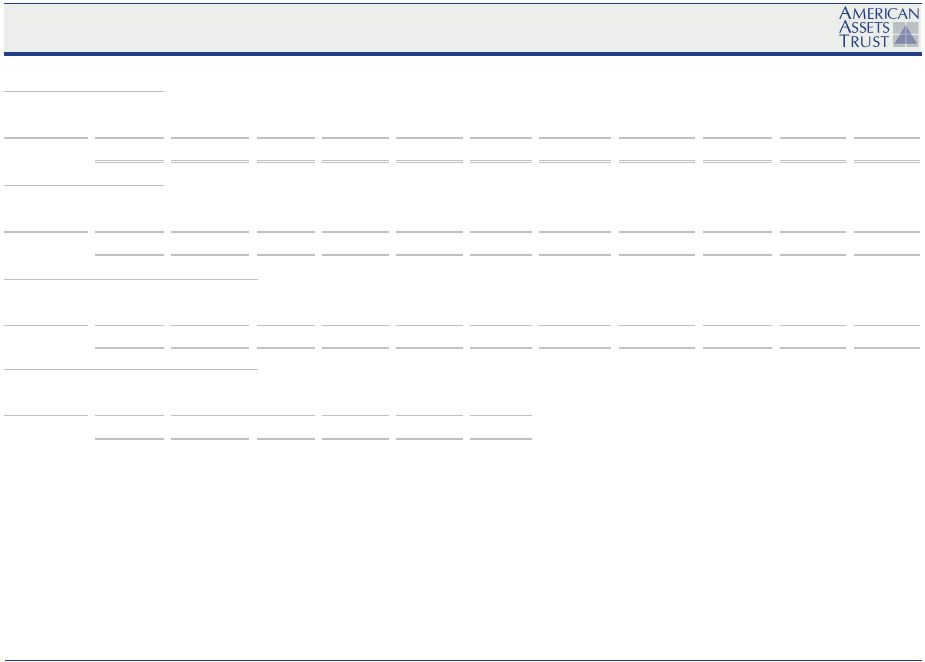

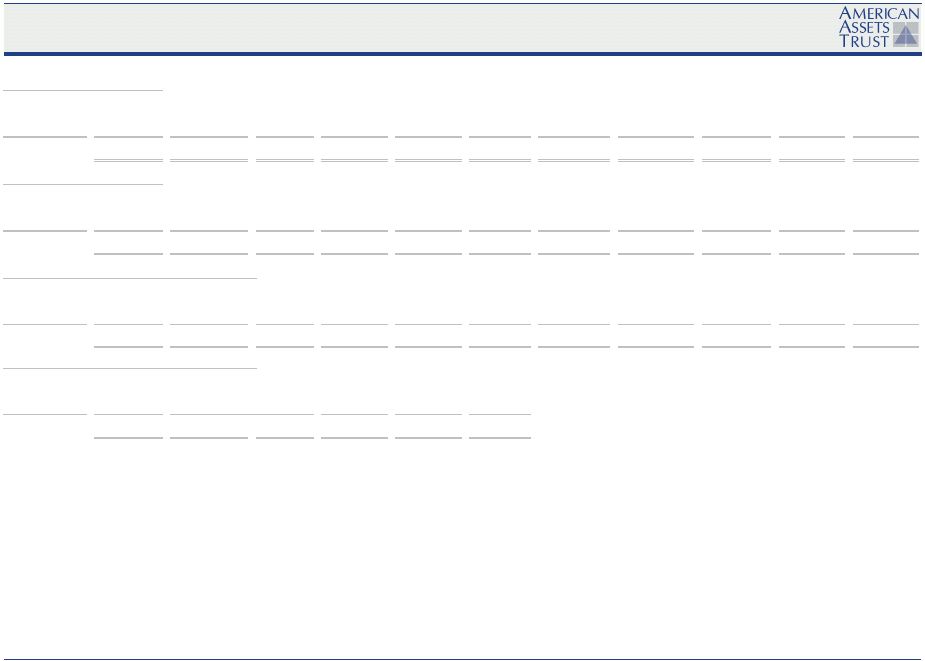

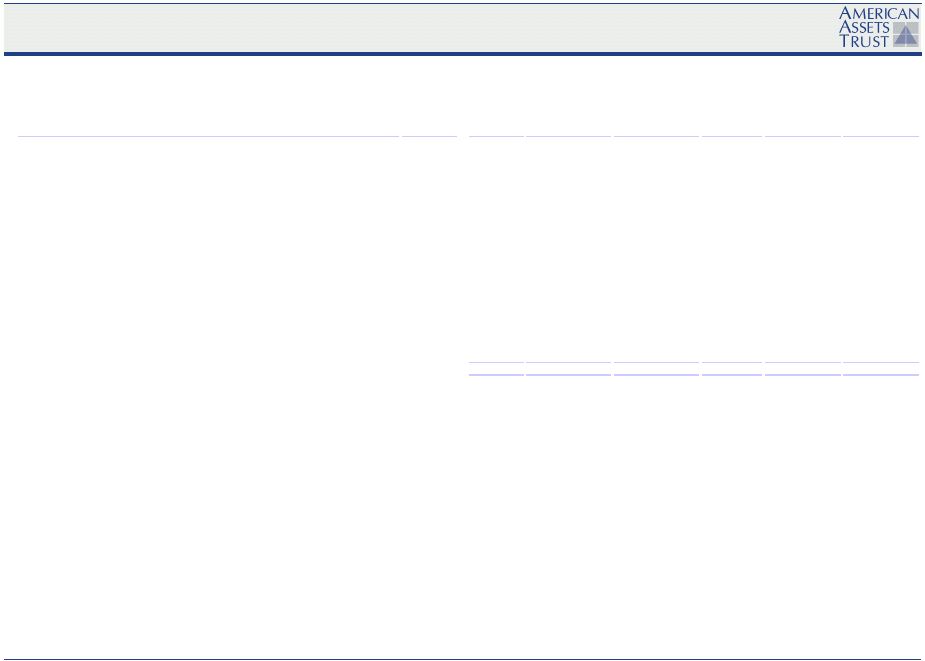

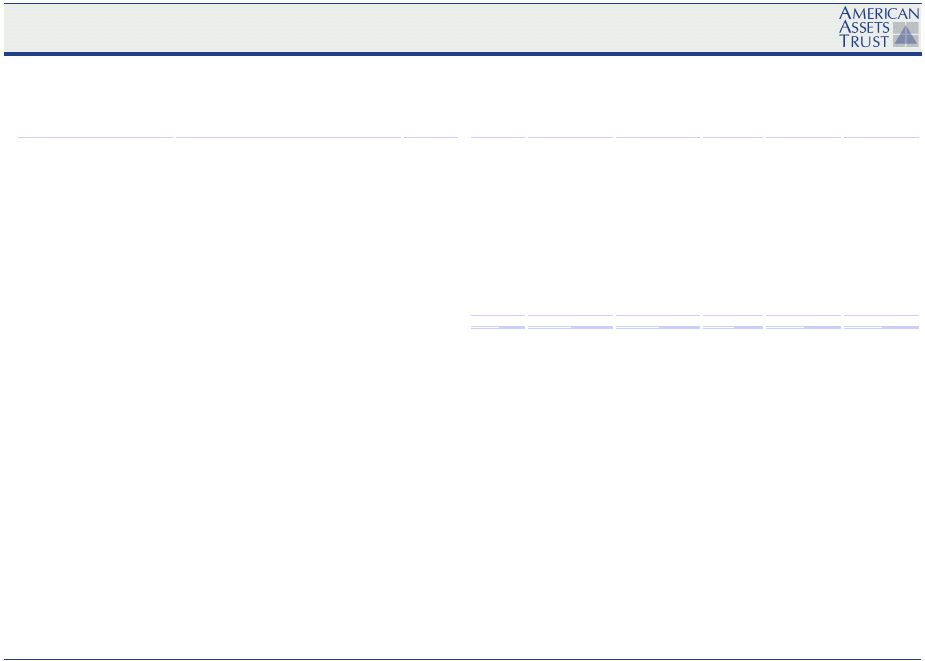

First Quarter 2011 Supplemental Information Page 18 PROPERTY REPORT As of March 31, 2011 Net Annualized Number Rentable Base Rent Year Built/ of Square Percentage Annualized per Leased Location Renovated Buildings Feet (1) Leased (2) Base Rent (3) Square Foot (4) Retail Properties Carmel Country Plaza San Diego, CA 1991 9 77,813 100.0% $3,473,151 $44.63 Sharp Healthcare, Frazee Industries Inc. Carmel Mountain (7) San Diego, CA 1994 13 520,228 82.6 8,915,956 20.75 Sears Sports Authority, Reading Cinemas South Bay Marketplace (7) San Diego, CA 1997 9 132,873 100.0 2,036,884 15.33 Office Depot Inc., Ross Dress for Less Rancho Carmel Plaza San Diego, CA 1993 3 30,421 74.5 733,521 32.37 Oggi's Pizza & Brewing Co., Sprint PCS Assets Lomas Santa Fe Plaza Solana Beach, CA 1972/1997 9 209,569 96.6 5,115,486 25.27 Vons, Ross Dress for Less Del Monte Center (7) Monterey, CA 1967/1984/2006 16 674,224 97.3 8,804,402 13.42 Macy's Century Theatres, Macy's Furniture Gallery The Shops at Kalakaua Honolulu, HI 1971/2006 3 11,671 100.0 1,535,028 131.52 Whalers General Store, Diesel U.S.A. Inc. Waikele Center Waipahu, HI 1993/2008 9 538,024 94.8 16,930,680 33.19 Lowe's, Kmart, Sports Authority, Foodland Super Market Old Navy, Officemax Alamo Quarry Market (7) San Antonio, TX 1997/1999 16 589,479 97.5 11,959,469 20.81 Regal Cinemas Bed Bath & Beyond, Whole Foods Market Subtotal/Weighted Average Retail Portfolio 87 2,784,302 94.3% $59,504,577 $22.66 Office Properties Torrey Reserve Campus San Diego, CA 1996-2000 9 456,801 92.7% $14,773,127 $34.89 Valencia Corporate Center Santa Clarita, CA 1999-2007 3 194,268 80.9 4,493,081 28.59 160 King Street San Francisco, CA 2002 1 167,986 95.2 5,463,637 34.16 Subtotal/Weighted Average Office Portfolio 13 819,055 90.4% $24,729,845 $33.40 Total/Weighted Average Retail and Office Portfolio 100 3,603,357 93.2% $84,234,422 $25.08 Average Number Monthly Year Built/ of Percentage Annualized Base Rent per Location Renovated Buildings Units Leased (2) Base Rent (3) Leased Unit (4) Loma Palisades San Diego, CA 1958/2001-2008 80 548 94.7% $9,285,516 $1,491 Imperial Beach Gardens Imperial Beach, CA 1959/2008-present 26 160 88.8 2,255,172 1,323 Mariner's Point Imperial Beach, CA 1986 8 88 97.7 1,087,104 1,054 Santa Fe Park RV Resort (8) San Diego, CA 1971/2007-2008 1 126 81.0 801,120 654 Total/Weighted Average Multifamily Portfolio 115 922 92.1% $13,428,912 $1,318 Net Annualized Number Rentable Base Rent Year Built/ of Square Percentage Annualized per Leased Location Renovated Buildings Feet (1) Leased (2) Base Rent (3) Square Foot (4) Retail Property Solana Beach Towne Centre Solana Beach, CA 1973/2000/2004 12 246,730 97.7% $5,300,689 $21.99 Dixieline Probuild, Marshalls Office Properties Solana Beach Corporate Centre Solana Beach, CA 1982/2005 4 211,971 87.6% $5,829,266 $31.39 The Landmark at One Market (9) San Francisco, CA 1917/2000 1 421,934 100.0 23,442,652 55.56 First & Main Portland, OR 2010 1 363,701 95.9 10,548,509 30.24 Subtotal/Weighted Average Office Portfolio 6 997,606 95.9% $39,820,427 $41.62 Total/Weighted Average Retail and Office Portfolio 18 1,244,336 96.2% $45,121,116 $37.69 Other Principal Retail Tenant(s) (6) Same-Store Retail and Office Portfolios Property Same-Store Multifamily Portfolio Retail Anchor Tenant(s) (5) Non-Same Store Retail and Office Portfolios Retail Anchor Tenant(s) (5) Other Principal Retail Tenant(s) (6) Property Property |