October 1, 2020

Via EDGAR Correspondence

Ms. Deborah O’Neal

Senior Counsel

Division of Investment Management

U.S. Securities and Exchange Commission

100 F Street, N.E.

Washington, DC 20549-0505

Re: JANUS DETROIT STREET TRUST (“Registrant”)

Registration Statement on Form N-1A (the “Registration Statement”)

1933 Act File No. 333-207814

1940 Act File No. 811-23112

Post-Effective Amendment No. 35

Dear Ms. O’Neal:

This letter responds to the comments to Post-Effective Amendment No. 35 to the Registrant’s registration statement on Form N-1A that were provided via electronic mail on August 19, 2020 and by telephone on September 3, 2020 by the staff of the Securities and Exchange Commission (the “Staff”) with respect to Janus Henderson AAA CLO ETF (the “Fund”). The Staff’s comments, as we understand them, and the Registrant’s responses are below.

Prospectus

| 1. | Staff Comment: It appears that the fund “will seek to maintain a minimum of 80% of its portfolio in AAA-rated CLOs.” Given the liquidity profile of these investments, please explain in detail how the fund determined that its investment strategy is appropriate for the open-end structure. Your response should include general market data on the liquidity of AAA-rated CLOs and information concerning the relevant factors referenced in the release adopting rule 22e-4 under the Investment Company Act of 1940. You should also explain whether the fund has had discussions with authorized participants concerning their ability to help the fund trade at or near its net asset value. Please also discuss any experience the adviser and its portfolio managers have in trading AAA-rated CLOs and how this factors into your determination that the strategy is appropriate for an open-end fund. See Investment Company Liquidity Risk Management Programs, Investment Company Act Release No. 32315 (Oct. 13, 2016) at pp. 154-155. |

Response: The Registrant’s investment adviser (the “Adviser”) engaged in a thorough examination of the liquidity of AAA rated CLO debt as an asset class and considered the appropriateness of holding this asset class in an ETF structure. This review included a thorough vetting of the Fund’s potential compliance with both Rule

22e-4 and the Registrant’s existing Liquidity Risk Management Program that was adopted as required by Rule 22e-4. In reviewing the Fund’s potential investments in AAA CLO debt, the Adviser considered a variety of factors in accordance with its Liquidity Risk Management Program, including among other things: the existence of an active market for AAA CLO debt, including the number, diversity, and quality of market participants; the frequency of trades or quotes for AAA CLO debt and average daily trading volume of the asset class; volatility of trading prices for the asset class; anticipated bid-ask spreads for the asset class; a consideration of the structure of AAA CLO debt; the range of maturities and date of issuance of AAA CLO debt; the ability to trade the asset class and any potential restrictions on trading or limitations on transfer of AAA CLO debt; the anticipated size of the Fund’s position in AAA CLO debt relative to the asset class’s historic trading volume. The Adviser also took into account the likelihood of authorized participants’ ability and willingness to maintain a market in the Fund’s shares. The Registrant also took into account the Adviser’s significant experience in trading the asset class.

For the reasons set forth above and as further supported by the materials provided to the Staff via e-mail on August 25, 2020, the Registrant confirms that the Fund’s proposed investment objective and principal investment strategies are appropriate for an open-end fund structure in view of the requirements of Rule 22e-4, under the Investment Company Act of 1940, as amended. These materials are again attached herewith for the Staff’s convenience as Appendix A, and the Registrant specifically directs the Staff’s attention to slides 4, and 8-12 as responsive to the above comment.

| 2. | Staff Comment: Please provide the Staff with a completed fee table and expense examples for the Fund at least one week before the effective date of the registration statement. |

Response: The form-of the Fund’s completed fee table and expense examples are attached hereto, in Appendix B to this letter.

| 3. | Staff Comment: Footnote 1 to the Fund’s Annual Fund Operating Expenses table, which describes the Fund’s unitary fee structure in detail, is not required by Form N-1A. Please consider removing this footnote. |

Response: The Registrant acknowledges the Staff’s comment, but respectfully declines to make the requested change at this time, in order to ensure consistency in presentation for each series of the Registrant. However, the Registrant confirms that, at its next annual prospectus update, the Registrant will consider removing this footnote for each of its series (including the Fund).

| 4. | Staff Comment: In its Principal Investment Strategy, the Fund discloses that it “may temporarily deviate from the 80% policy [(to maintain a minimum of 80% of its portfolio in AAA-rated CLOs)] while deploying new capital as the result of cash creation or redemption activity, or during highly unusual market conditions, such as a downgrade in the rating of one or more securities.” Please confirm that this |

disclosure complies with the requirements of Instruction 6 to Item 9(b) of Form N-1A, and clarify when such circumstances may arise. |

Response: The Registrant confirms that the Fund’s disclosure, which discusses two specific circumstances in which the Fund may temporarily deviate from its stated 80- and 90-percent policies, complies with the requirements of Instruction 6 to Item 9(b) of Form N-1A. In particular, the Registrant notes that during times of significant creations in cash, the portfolio managers may need to take additional time to select investments that are consistent with the Fund’s investment policies and how they seek to implement the Fund’s investment strategy. In addition, in highly unusual circumstances where the universe of AAA-rated CLOs has been reduced, it may take additional time for the portfolio managers to select investments that are suitable and consistent with the Fund’s investment policies. Consequently, the Registrant believes that the Fund’s existing disclosure appropriately discloses the effect of taking such a temporary defensive position.

| 5. | Staff Comment: Please confirm whether derivatives used by the Fund as described in the Fund’s Principal Investment Strategy will be included or excluded for purposes of calculating the Fund’s 80- and 90-percent policies with respect to investing in AAA-rated CLOs. Second, if included, please confirm that these derivatives will be marked to market for purposes of calculating the Fund’s 80- and 90-percent policies with respect to investing in AAA-rated CLOs. |

Response: The Registrant confirms that these derivative instruments will be included for purposes of calculating the Fund’s 80- and 90-percent policies with respect to investing in AAA-rated CLOs, and notes that a statement to that effect is included in the registration statement. The Registrant also confirms that these derivatives will be marked to market for purposes of these calculations.

| 6. | Staff Comment: Within Principal Investment Risk – Fluctuation of NAV please include disclosure indicating that, in times of market stress, market makers and authorized participants may cease to perform these functions for the Fund which, in turn, may lead to variance between market price and the underlying value of the Fund’s shares. |

Response: In response to the Staff’s comment, the Registrant has made the following changes to disclosure (additions underlined, deletionsstricken):

“Fluctuation of NAV. The NAV of the Fund shares will generally fluctuate with changes in the market value of the Fund’s securities holdings. The market prices of shares will generally fluctuate in accordance with changes in the Fund’s NAV and supply and demand of shares on the [NYSE Arca]. An absence of trading in shares of the Fund, or a high volume of trading in the Fund, may result in trading prices that differ significantly from the Fund’s NAV. Additionally, in times of market volatility, market makers and authorized participants may cease to perform these functions on behalf of the

Fund, which may result in an increase in the variance between market price and the Fund’s NAV. It cannot be predicted whether Fund shares will trade below, at or above the Fund’s NAV….”

| 7. | Staff Comment: Supplementally, please confirm whether the Fund’s anticipated portfolio holdings are expected to trade outside of a collateralized settlement system. Secondly, if so, please disclose: (i) that there are a limited number of financial institutions that may act as authorized participants that post collateral for certain trades on an agency basis (i.e., on behalf of other market participants); (ii) that, to the extent that those authorized participants exit the business or are unable to process creation and/or redemption orders and no other authorized participant is able to step forward to do so, there may be a significantly diminished trading market for the Funds’ shares; and (iii) that this could in turn lead to differences between the market price of the Funds’ shares and the underlying value of those shares. |

Response: Supplementally, the Registrant confirms that the Fund expects its portfolio holdings to trade within collateralized settlement systems. However, in response to the Staff’s comment, the Registrant has implemented the following changes to disclosure (additions underlined, deletionsstricken):

Authorized Participant Risk. The Fund may have a limited number of financial institutions that may act as Authorized Participants (“APs”). Only APs who have entered into agreements with the Fund’s distributor may engage in creation or redemption transactions directly with the Fund. These APs have no obligation to submit creation or redemption orders and, as a result, there is no assurance that an active trading market for the Fund’s shares will be established or maintained. This risk may be heightened to the extent that the securities underlying the Fund are traded outside of a collateralized settlement system. In that case, APs may be required to post collateral on certain trades on an agency basis (i.e., on behalf of other market participants), which only a limited number of APs may be willing or able to do. Additionally,Tto the extent that those APs exit the business or are unable to process creation and/or redemption orders, and no other AP is able to step forward to create and redeem in either of these cases, shares may trade like closed-end fund shares at a premium or a discount to NAV and possibly face delisting.

| 8. | Staff Comment: If applicable, please include disclosure in the Purchasing and Selling Shares – Share Prices section of the Fund’s prospectus indicating that when current pricing is not available for certain portfolio securities, the intra-day indicative value may not accurately reflect the current market value of the Fund’s shares. |

Response: The Fund will rely upon Rule 6c-11, under the Investment Company Act of 1940, as amended (“ETF Rule”), at the time of launch. Additionally, the Fund will rely (on both an initial and ongoing basis) on the listing requirements set forth in NYSE Arca Rule 5.2-E(j)(8) (“Listing Standards”). Neither the ETF Rule nor the Listing Standards require publication of an intra-day indicative value. Accordingly, the Registrant has determined not to publish an intra-day indicative value with respect to the Fund. As a result, the Registrant has removed all references to the intra-day indicative value (and/or “iNAV”) from the Fund’s registration statement.

Statement of Additional Information

| 1. | Staff Comment: In the “Investment Policies and Restrictions Applicable to the Fund” section of the Fund’s Statement of Additional Information, please disclose that the Fund will consider the underlying holdings of investment companies in which it invests for purposes of determining compliance with the Fund’s fundamental concentration policy. |

Response: The Registrant acknowledges the comment, but respectfully declines to amend its disclosure at this time. Supplementally, the Registrant confirms that, where sufficient information is reasonably available, it will endeavor to evaluate the types of securities in which underlying investment companies invest in determining compliance with the Fund’s fundamental investment policy relating to its concentration of assets.

Please call me at (303) 336-5065 with any questions or comments.

Respectfully, |

| /s/ James D. Kerr |

| James D. Kerr |

| Assistant Secretary |

Enclosures (via EDGAR only) |

cc: |

Byron Hittle, Esq. |

Eric Purple, Esq. |

Appendix A

Proposed Janus Henderson AAA CLO ETF (JAAA)

August, 2020 |  | |

|

Key Product Attributes

| Product: | Janus Henderson AAA CLO ETF | |||

| Ticker: | JAAA | |||

| Investment Objective: | Seeks capital preservation and current income by seeking to deliver floating-rate exposure to high | |||

quality AAA-rated collateralized loan obligations (CLOs) | ||||

| Principal Investment Strategy: | The Fund pursues its investment objective by investing, under normal circumstances, at least 90% of its net assets (plus any borrowings made for investment purposes) in collateralized loan obligations (“CLOs”) of any maturity that are rated AAA (or equivalent by a NRSRO) at the time of purchase, or if unrated, determined to be of comparable credit quality by Janus Capital | |||

| Investment Limits / Restrictions | Under normal circumstances:

• Minimum 90% AAA on purchase. Nothing below A-

• Seeks to maintain a minimum of 80% in AAA-rated CLOs

• Maximum 15% exposure per CLO manager | |||

Portfolio Managers: | John P. Kerschner, Nick Childs | |||

| Benchmark: | JP Morgan Collateralized Loan Obligation Index (“CLOIE”) | |||

| Fees: | To be determined; but expected to be similar to the existing series of the Janus Detroit Street Trust. | |||

| Regulatory & Exchange Listing | The Fund will launch in reliance upon Rule 6c-11, under the Investment Company Act of 1940, as amended, and will list in reliance upon the NYSE’s Rule 5.2-E(j)(8). | |||

1

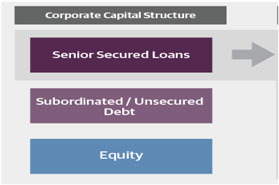

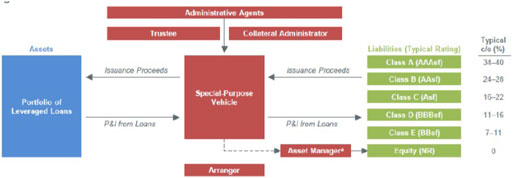

Collateralized Loan Obligations (CLOs) – Overview

CLOs are structured securities collateralized predominantly by broadly syndicated corporate loans rated below investment grade (bank loans). The CLO manager purchases a portfolio of bank loans, and holds them in a special purpose vehicle which issues different tranches which are ranked in priority and credit quality based on their claim to proceeds from the pool. CLOs are generally quoted as spread to LIBOR1 and, therefore, are typically floating-rate instruments.

|  |

CLOs are missing from most major indices and many investors have little CLO exposure. Higher-rated CLOs in particular are primarily held by large institutional investors looking for yield enhancement.

1 Janus Capital Management will continue to monitor developments with respect to the sunset of LIBOR as a benchmark rate within the industry, including development of replacement reference rates. | | 2 |

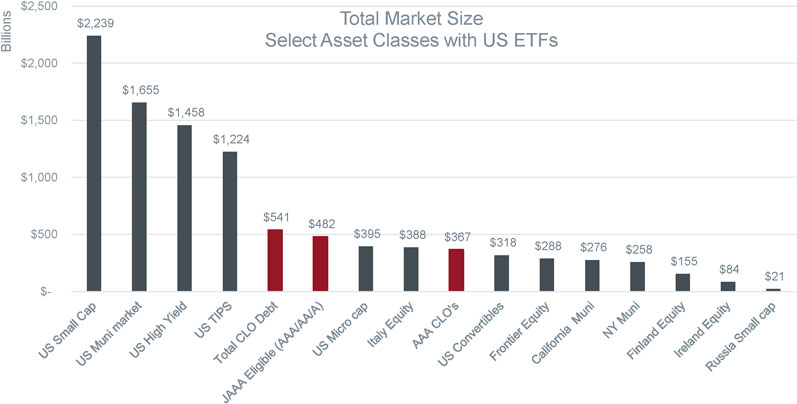

Total Market Size vs Outstanding US ETF Asset Classes

CLOs are a significant asset class; however, are currently under-represented in the ETF market.

| Source: Bloomberg, Janus Henderson | | 3 |

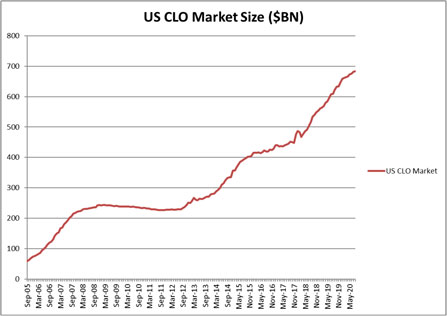

CLO Issuance and Liquidity Have Significantly Improved

CLO issuance and liquidity have substantially increased since 2005, with issuance currently averaging $10-20 billion per month, and secondary trading (bid wanted in competition, (“BWIC“)) averaging $4-5 billion per month. Single A and higher typically represent 40-50% of secondary volumes.

With most major banks providing liquidity, we believe that the market can now support a daily-liquidity, open-end AAA-rated CLO product, particularly with an ETF structure utilizing in-kind transactions.

With this liquidity, and based upon our observations of the market as well as confirmed interest from the Authorized Participant community in supporting this product and asset class, we believe that the arbitrage mechanism for JAAA will function effectively.

Source: Janus Henderson, Citi, JPM, Bloomberg as of 8/1//20.

| 4 |

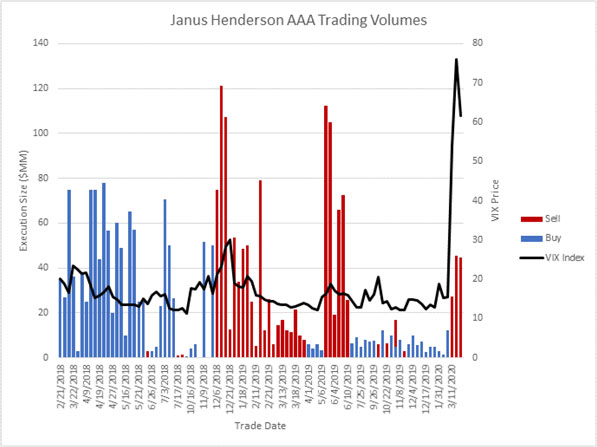

Recent Crisis Stress Tested the CLO Market

Like most areas of the fixed income market, the COVID crisis stressed the CLO market. However, the CLO market actually hit record trading volumes in March 2020, with AAA tranches comprising the majority of the month’s trading. AAA primary market spreads to LIBOR were at 139bps to start the year, peaked at 262bps in April and were trading around 180bps at the end of July. Secondary market spreads to LIBOR were briefly as high as 408bps for AAA tranches, but levels converged in under a month.

Source: Janus Henderson, Citi, JPM, Bloomberg as of 7/31/20.

| 5 |

Recent Crisis Stress Tested the CLO Market

YTD CLO Spreads versus IG Corporates

| • | AAA- to A-rated CLO spread recovery from March volatility is in line with comparable fixed income asset classes, including Investment Grade Corporates |

Source: Janus Henderson, JPMorgan Research as of 8/24/20.

| 6 |

Recent Crisis Stress Tested the CLO Market

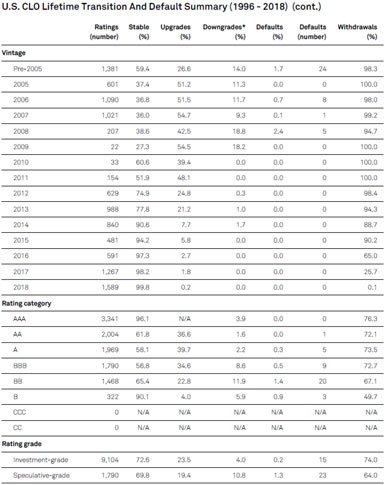

*Including defaults, Securities with ratings that migrated to ‘NR’ over the period are classified based on the rating prior to ‘NR’ when determining stable, upgrade downgrade, and default rates. N/A –Not applicable. Source: S&P Global Fixed Income Research.

On average, 80% of the underlying collateral would have to default and continue to default over the life of the CLO in order to result in a write-down (reduction in payments) to the AAA tranche. (See table below)

| Constant Default Rate Required for Principal Write-down | ||||

| Tranche | Mean | Median | ||

AAA | 79.5 | 80.8 | ||

AA | 37.3 | 41.3 | ||

A | 24.4 | 27.1 | ||

BBB | 15.2 | 17.8 | ||

BBB | 9.2 | 11.5 | ||

BBB | 7.2 | 10.2 | ||

For this reason, highly rated CLOs have had historically very low default rates, and the current crisis has seen very little impact to credit ratings. No AAA-rated CLO has ever defaulted, including during the great recession. (See table to the left)

Source: S&P, Morgan Stanley Research

| 7 |

The Fund’s Strategy is Appropriate for an Open-End Fund

Rule 22e-4 Liquidity Risk Assessment: Conclusions

| • | We believe that JAAA’s strategy to invest in high-quality investment grade CLOs does not raise concerns regarding the Fund’s ability to meet the requirements under SEC rule 22e-4. |

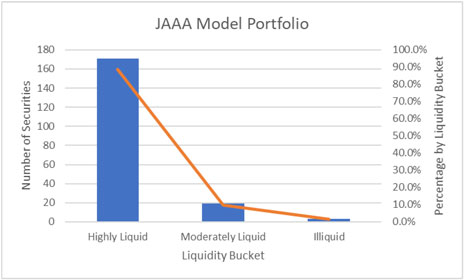

| • | A model portfolio1 provided by the investment team included up to 193 different securities and, on balance, the majority of the assets, 88.6%, are considered Highly Liquid. This percentage is well above the Liquidity Risk Management Program’s primarily highly liquid threshold of 60%. As a result, we expect the Fund to be considered “primarily highly liquid.” |

| • | The remaining CLOs in the model portfolio that are not considered highly liquid are either moderately liquid (9.8%) or illiquid (1.6%). Given that the Fund intends to invest primarily in high quality investment grade CLOs, it is not anticipated that the Fund would exceed the 15% limit on illiquid assets. |

| • | The JAAA strategy is considered appropriate for an open-ended fund as the Fund is expected to be a primarily highly liquid fund, and recent COVID related market volatility indicate Funds that hold CLOs did not see a significant impact to the Fund’s liquidity profile. |

| • | The Fund’s published basket will be monitored to determine whether the percentage of cash-in-lieu exceeds 10%, requiring the Liquidity Risk Management Program Administrator to rescind the “in-kind ETF” determination. |

1 The individual CLO securities used to compile the model portfolio are eligible for purchase by JAAA based upon the criteria established in the 485APOS filing with the SEC on July 29, 2020 and do not necessarily represent the securities that will comprise the Fund’s portfolio at the time of launch.

| 8 |

Rule 22e-4 Liquidity Risk Assessment

Model Portfolio Analysis & Results

| • | A model portfolio for JAAA was evaluated using the third party liquidity risk tool, ICE Vantage, used by the Liquidity Risk Management Program Administrator to monitor Funds’ liquidity under the requirements of SEC Rule 22e-4 |

| • | The majority of CLOs included in the model are classified as highly liquid, 88.6%. Of the remaining CLOs in the model portfolio, 9.8% were considered moderately liquid, and 1.6% illiquid |

| • | The Fund may invest non-US CLOs and to the extent it does, it will hedge the foreign currency exposure. In each case, the sample non-US CLOs reviewed were classified as highly liquid |

Market Stress Considerations

• During the COVID related market volatility, Funds that held CLOs did not see a material change in their liquidity profile

• Additionally, the Liquidity Risk Management Program Administrator reviewed the classifications for certain security types including asset backed securities (e.g., CLOs) and re-confirmed the liquidity buckets determined by the third party liquidity risk tool |  |

| 9 |

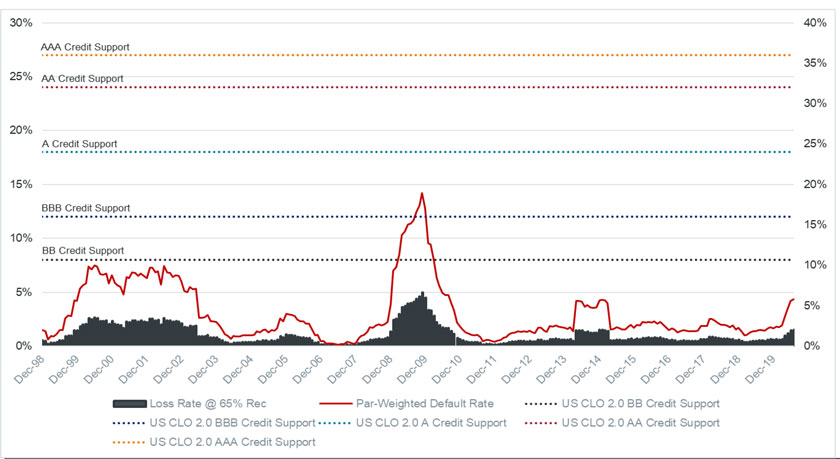

Recent Crisis Stress Tested the CLO Market

Historical bank loan default and loss rates have never come close to the credit support levels of senior CLOs.

Source: Janus Henderson, JPMorgan, S&P/LCD as of 7/31/20.

| 10 |

The Fund’s Adviser is an Experienced CLO Investor

| • | Over the previous two years across its global products and strategies, Janus Henderson Investors has traded over $4.3 billion in CLO securities, $2.7 billion of which was in the Secondary market and $1.7 billion of which represented AAA-rated CLOs. |

| Source: Janus Henderson |

| 11 |

Biographies – Investment Team

John Kerschner, CFA

Portfolio Manager | Head of U.S. SecuritizedProducts

John Kerschner is Head of U.S. Securitized Products at Janus Henderson Investors and a Portfolio Manager of the Multi-Sector Income strategy and Mortgage-Backed Securities ETF. He also has co-managed the fixed income portion of the Perkins Value Plus Income strategy since 2018. In his role as Head of U.S. Securitized Products, Mr. Kerschner primarily focuses on mortgage-backed securities and other structured products.

Prior to joining Janus in 2010, Mr. Kerschner was director of portfolio management at BBW Capital Advisors. Before that, he worked for Woodbourne Investment Management, where he was global head of credit investing. Mr. Kerschner began his career at Smith Breeden Associates as an assistant portfolio manager and was promoted several times over 12 years, becoming a principal, senior portfolio manager and director of the ABS-CDO group.

Mr. Kerschner received his bachelor of arts degree in biology from Yale University, graduating cum laude. He earned his MBA from Duke University, Fuqua School of Business, where he was designated a Fuqua Scholar. Mr. Kerschner holds the Chartered Financial Analyst designation and has 30 years of financial industry experience.

Nick Childs, CFA

Portfolio Manager | Securitized ProductsAnalyst

Nick Childs is a Portfolio Manager at Janus Henderson Investors, a position he has held since 2018. He is responsible for managing the Mortgage-Backed Securities ETF, with a primary focus on valuing opportunities and managing exposure of mortgage-backed securities (MBS). Additionally, he is a Securitized Products Analyst. Prior to joining Janus in 2017 as a securitized products analyst, he was a portfolio manager from 2012 to 2016 at Proprietary Capital, LLC, where he managed alternative fixed income strategies specializing in MBS, absolute return investing. His work with Proprietary Capital included managing all major U.S. interest rate and MBS risks, modeling borrower behavior and MBS deal structure, and advancing market-neutral hedging strategies. Before that, he was vice president at Barclays Capital in their capital markets division, where he focused on securitized products from 2007 until 2012. Prior to joining Barclays, he was vice president at Lehman Brothers. He began his career at State Street Global Advisors in 2003.

Mr. Childs received his bachelor of science degree in finance with a minor in economics from the University of Denver. He holds the Chartered Financial Analyst designation and has 17 years of financial industry experience.

Jessica Shill

Assistant Portfolio Manager | SecuritizedProducts Analyst

Jessica Shill is a Securitized Products Analyst at Janus Henderson Investors, a position she has held since joining the firm in 2019. Prior to this, she was an intern and an analyst for the Wells Fargo Investment Portfolio. Ms. Shill received her bachelor of arts degree in economics from Bryn Mawr College, where she graduated cum laude. She has 4 years of financial industry experience.

| 12 |

Appendix B: Form-of Completed Fee Table

FEES AND EXPENSES OF THE FUND |

This table describes the fees and expenses that you may pay if you buy, hold and sell shares of the Fund. Investors may pay brokerage commissions on their purchases and sales of Fund shares, which are not reflected in the table or in the example below.

| ANNUAL FUND OPERATING EXPENSES | ||

| (expenses that you pay each year as a percentage of the value of your investment) | ||

Management Fees (1) | 0.25% | |

Other Expenses(2) | 0.00% | |

Total Annual Fund Operating Expenses | 0.25% | |

(1) | The Fund’s Management Fee is a “unitary” fee that is designed to pay substantially all operating expenses, except for distribution fees (if any), brokerage expenses or commissions, interest, dividends taxes, litigation expenses, acquired fund fees and expenses (if any), and other extraordinary expenses not incurred in the ordinary course of the Fund’s business. | |

(2) | Other Expenses are based on the estimated expenses that the Fund expects to incur. |

EXAMPLE:

The Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then sell all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | |||

| $26 | $80 |