ZODIAC EXPLORATION INC.

MANAGEMENT’S DISCUSSION & ANALYSIS

The following is Management’s Discussion and Analysis (“MD&A”) of the performance, financial condition and future prospects of Zodiac Exploration Inc. (“Zodiac” or “the Company”). This document should be read in conjunction with the audited annual consolidated financial statements of the Company for the year ended September 30, 2012 and September 30, 2013, and notes thereto. With its head office based in Calgary, Alberta, Canada, Zodiac is primarily engaged in the exploration for, and development of, oil and gas interests in California, USA. Common shares of the Company are listed on the TSX-Venture under the symbol “ZEX”.

The financial information in this MD&A is derived from the Company’s audited consolidated financial statements. All amounts are expressed in Canadian $000’s unless otherwise indicated, except for per share amounts and are prepared in accordance with US generally accepted accounting principles (“US GAAP”).

Additional information about Zodiac and its business activities is available on SEDAR athttp://www.sedar.com, EDGAR http://www.sec.gov/edgar, and at http://www.zodiacexploration.ca

Forward Looking Statements

Certain information contained herein may constitute forward-looking statements under applicable securities laws. Forward-looking statements look into the future and provide an opinion as to the effect of certain events and trends on the business. Forward-looking statements are based on the estimates and opinions of the Company’s management at the time the statements were made. Readers are cautioned not to place undue reliance on these statements as the Company’s actual results, performance or achievements may differ materially from any future results, performance or achievements expressed or implied by such forward-looking statements if known or unknown risks, uncertainties or other factors affect the Company’s business, or if the Company’s estimates or assumptions prove inaccurate. Therefore, the Company cannot provide any assurance that forward-looking statements will materialize.

The Company assumes no obligation to update forward-looking statements should circumstances or management’s estimates change.

The material assumptions that were applied in making the forward-looking statements in this MD&A include: execution of the Company’s existing plans for each of its projects, which may change due to changes in the views of the Company or if new information arises which makes it prudent to change such plans; and execution of the Company’s plans to seek out additional opportunities in the natural resource sector, which are dependent in part on global economic conditions and upon the prices of commodities and natural resources.

Readers are urged to carefully review and consider the various disclosures made by us in this report and in our other reports filed with the Securities and Exchange Commission.

Highlights

During the year ended September 30, 2013, Zodiac:

| · | Signed a definitive farmout agreement with Aera Energy LLC, a large California operator, whereby Aera acquired the right to earn a 50% interest in approximately 19,600 net acres of Zodiac lands located in Kings County, California. |

| o | Drilled the initial Phase 1 vertical earning well reaching TD in April 2013. The well remains on tight hole status while Aera continues to evaluate the results of the well. |

| · | Initiated a formal process aimed at seeking out partners to jointly develop Zodiac’s extensive inventory of land or monetization of the properties. |

| · | Continued to develop its land base which currently sits at approximately 72,000 net acres, including a program of lease extensions. |

| · | Ended the year with $13,923 in cash and $13,914 in working capital. |

Subsequent to year end

Subsequent to year end Zodiac announced that it had entered into a definitive agreement (the "Acquisition Agreement") with Muskwa Resources Ltd. ("Muskwa") whereby Zodiac has agreed, subject to certain conditions, to acquire all of the issued and outstanding common shares ("Muskwa Shares") of Muskwa (the "Acquisition"). Muskwa is a private oil and gas company incorporated in 2008 with approximately 54,240 acres of land in central Alberta, primarily in the Duvernay and Nordegg formations, and 9,000 net acres in Montana acquired from Jackfish Exploration Inc. ("Jackfish") and subject to certain earning conditions. Muskwa has a pending assets acquisition in Montana from Tanglewood Energy Inc. ("Tanglewood") that will add up to approximately 15,000 net acres of land upon satisfaction of certain conditions under the agreement. At this moment, the Tanglewood asset acquisition by Muskwa remains outstanding and there is no certainty that it will be completed.

The Acquisition is expected to be completed by way of an amalgamation and is subject to customary approvals, including approval by Muskwa shareholders and the approval of the TSX Venture Exchange. Closing of the Acquisition is expected to occur during December, 2013.

Transaction Highlights:

Alberta Assets of Muskwa:

| · | Muskwa is a top holder of Duvernay rights in Alberta with a total of 54,240 acres of land in central Alberta, primarily in the Duvernay and Nordegg formations (49,760 contiguous 100% working interest acres in the Duvernay light oil resource window) plus an option to acquire up to an additional 6,880 acres |

| · | Muskwa's land position has significant stacked resource potential in the Duvernay, Nordegg, Montney and Beaverhill Lake formations |

| · | GLJ Petroleum Consultants Ltd. ("GLJ") has provided Muskwa with an evaluation (the "GLJ Report") dated October 25, 2012 and effective as of June 30, 2012 in accordance with the requirements of National Instrument 51-101 –Standards of Disclosure for Oil and Gas Activities ("NI 51-101") on the undiscovered petroleum initially-in-place on the 39,680 acres of lands held by Muskwa at such time. Using the same methodology as GLJ utilized in the preparation of the GLJ Report, a member of Muskwa's management team, who is a qualified reserves evaluator for the purposes of NI 51-101, has provided an estimate of the undiscovered petroleum initially-in place effective as of December 31, 2012 for the additional 11,520 acres acquired by Muskwa since the date of the GLJ Report, which estimates are set forth as follows: |

Undiscovered Petroleum Initially-in-Place(1) |

| Formation | Estimate | GLJ Report (STB '000)(4) | Muskwa Internal Estimate(3) (STB '000) (4) | Total (STB '000) (4) |

| Duvernay | Low Estimate(5) | 434,116 | 142,132 | 576,248 |

| | Best Estimate(5) | 868,232 | 284,275 | 1,152,507 |

| | High Estimate(5) | 1,519,407 | 497,473 | 2,016,880 |

| | | | | |

| Middle Nordegg | Low Estimate(5) | 120,401 | 70,713 | 191,114 |

| | Best Estimate(5) | 229,941 | 122,412 | 352,362 |

| | High Estimate(5) | 344,912 | 183,635 | 528,547 |

| | | | | |

| Lower Nordegg | Low Estimate(5) | 192,076 | 117,311 | 309,387 |

| | Best Estimate(5) | 320,126 | 195,517 | 515,643 |

| | High Estimate(5) | 512,212 | 312,828 | 825,030 |

Notes:

| 1. | Undiscovered Petroleum Initially-in-Place is that quantity of petroleum that is estimated, on a given date, to be contained in accumulations yet to be discovered. There is no certainty that any portion of the resources will be discovered. If discovered, there is no certainty that it will be commercially viable to produce any portion of the resources. Further sub-categorization of the reported resources volumes was not possible at the time the foregoing estimates were made as a recovery project could not be defined for such resource volumes. See "Cautionary Statements" below. |

| 2. | The GLJ Report is dated October 25, 2012 and effective as of June 30, 2012. |

| 3. | The Muskwa internal estimate was prepared on January 15, 2013 with an effective date as of December 31, 2012 and was prepared by a member of management who is a qualified reserves evaluator for the purposes of NI 51-101, using the same methodology as utilized by GLJ in its preparation of the GLJ Report. |

| 4. | STB = stock tank barrels. Figures reported in thousands of stock tank barrels of oil. |

| 5. | See "Cautionary Statements" below for further information in respect of the definitions of "low estimate", "best estimate" and "high estimate". |

| · | Industry has spent over $6 billion on land, corporate acquisitions and wells on the Duvernay play |

| · | Significant interest and activity exists in the area in which Muskwa holds land with over 90 wells drilled by large producers actively proving up the Duvernay light oil window with commercial results and there have been several recent commercial discoveries in the Duvernay light oil window to the south of Muskwa's land position |

Jackfish Assets (Montana)

| · | Muskwa entered into a definitive purchase and sale agreement dated October 3, 2013 with Jackfish whereby Muskwa would acquire, prior to closing of the Acquisition and subject to customary closing conditions, the entire interest of Jackfish under a farm-in agreement to which Jackfish is currently a party (the "Jackfish Farm-in Agreement") whereby Muskwa will have the right to farm-in on approximately 12,000 gross acres (9,000 net acres after earning is completed under the farm-in agreement) located in southern Montana, USA which management of Zodiac and Muskwa believe are prospective for light oil in the Grey Bull (Cretaceous) formation. The Jackfish acquisition was completed on October 11, 2013. |

| · | Zodiac has reviewed the 2D seismic results for the channel play in the Grey Bull formation at a depth of approximately 1,500 meters and is encouraged by these results |

| · | Assuming completion of the Muskwa transaction, Zodiac plans to shoot a 3D seismic program and drill two evaluation wells by June 30, 2014 and will be required to do so in order to fulfil the earning requirements under the Jackfish Farm-in Agreement |

| · | Management of Muskwa and Zodiac believe that the acquisition of the Jackfish assets is a low cost exploration opportunity (approximately US$600 to drill, test, complete and equip wells on the lands comprising the Jackfish assets) |

Tanglewood Assets (Montana)

| · | Muskwa has entered into a definitive purchase and sale agreement dated October 7, 2013 with Tanglewood whereby it is proposed that Muskwa will acquire, prior to closing of the Acquisition and subject to customary closing conditions, approximately 30,000 gross acres (15,000 net acres) located in northern Montana. As at the date of this MD&A the Tanglewood transaction has not been completed and there is no certainty that this will be achieved. |

| · | Zodiac has reviewed the 3D seismic results for a Nisku play at approximately 1,500 meters and is encouraged by these results |

| · | Management of Muskwa and Zodiac believe that the acquisition of the Tanglewood assets is a low cost exploration opportunity (approximately US$600 to drill, test, complete and equip wells on the lands comprising the Tanglewood assets) adjacent to existing production in the prospective Devonian horizons |

Pro-forma Highlights

| · | Large conventional and unconventional light oil asset base across several regions of North America provides excellent diversification |

| · | Conventional light oil assets offer potential for near term light oil production and cash flow to maintain financial flexibility |

| · | Based on the GLJ Report and the management resource estimates set forth above, Muskwa and its assets provide a multi-billion barrel original oil in place, unconventional light oil resource opportunity in North America's prolific shale regions |

| · | Drill-ready prospects in Montana provide potential near-term production catalysts |

| · | Addition of proven technical and management team members to assist in the growth of Zodiac |

Operations

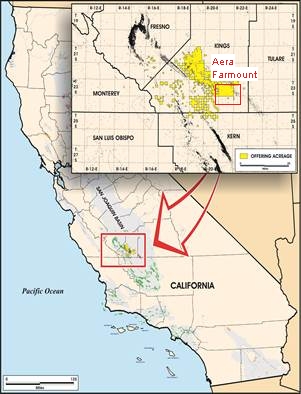

Overview of Californian Operations

Zodiac’s operations are focused in the San Joaquin Basin – principally Kings County, California.

Fig 1: Zodiac Acreage in Kings County

Summary of Operations to date

Since 2010, the Company has drilled three wells on its properties in Kings County, either as operator or non-operated partner.

Aera – Mortgage 881D-15 Well

Under terms of the farmout agreement between Zodiac and Aera Energy LLC (the "Farmout Agreement"), Aera has acquired the right to earn up to 50% of Zodiac's interest in approximately 19,600 acres of the Mortgage block, located in Kings County, California by the drilling of two vertical and two horizontal earning wells on or adjacent to the farmout lands in two earning phases. Each phase comprises one vertical and one horizontal well and upon fulfillment of the drilling commitment under each phase, Aera will earn a 50% interest in approximately 9,800 acres of each phase respectively.

On February 5, 2013, Aera spudded the first well under the terms of the Farmout Agreement. The well reached its final vertical depth of 15,362 feet on April 29, 2013 and the well was temporarily suspended and remains on tight-hole status pending evaluation and further drilling decisions.

The well was designed to penetrate and evaluate the thick, regional Monterey and Kreyenhagen formations, both of which, from previous wells drilled in the vicinity, have demonstrated the potential to contain very large accumulations of oil in these established source rocks.

4-9 and 1-10 Wells

During 2010 through 2012, Zodiac drilled two operated wells, the 4-9 and 1-10 and while the production from these wells was not commercially viable, the data has proven the existence of a number of oil charged formations. In many of these large resource type plays, the initial wells in the ‘learning curve’ often do not result in commercial producing wells but rather they provide the information needed for further development. This is the case here. The 4-9 well is shut-in. The 1-10 well and the lease associated with this well have been turned back to the lessor as it has not as yet been proven to be capable of commercial production. The scientific and drilling/completion data and learnings gained from these wells have nevertheless been substantial.

These wells have provided the Company with a comprehensive data set over several prospective light oil targets within the Monterey, Allison/Whepley, Vaqueros and Tumey /Kreyenhagen Formations.

Kreyenhagen Formation

The Kreyenhagen formation is one of the primary source rocks in the San Joaquin Basin and these source rocks have been estimated by the United States Geological Service (“USGS”) to have generated over 100 Billion barrels of crude oil.1 USGS PP 1713

The 4-9 well reached total depth after intersecting 650 feet of Kreyenhagen silts and organic source shales. In the area of the wellbore, data from drilling and coring operations conducted by Zodiac indicate that the Kreyenhagen formation is approximately 800 feet thick and reaches thicknesses exceeding 1,500 feet further south on Zodiac acreage.

Zodiac completed and tested a 30 foot silty interval in the upper part of the Kreyenhagen, known as the Tumey Formation. This upper interval flowed 29° API oil at an average rate of 24 barrels per day (“bbls/day”) over a nine day flow test period. The pressure transient analysis (“PTA”) indicated significant formation damage. The well test analysis demonstrated that a rate of 120 bbls per day could be achieved by removing the formation damage.

The production testing, the coring and the log analyses have shown that the Kreyenhagen formation has similarities to the Bakken in that organic rich shales are feeding oil into siltier units.

The major difference between the Bakken and the Kreyenhagen interval is the thickness. The Kreyenhagen is approximately 800 to 1,500 feet thick across Zodiac’s land base while the Bakken ranges from 40 to 100 feet.

Detailed geologic mapping of the Upper Kreyenhagen or ‘Tumey” Formation indicates that this zone is present on much of Zodiacs acreage.

Lower Vaqueros Formation

The entire Vaqueros formation is over 650 feet thick, with the first test comprising 30 feet within the lowermost 200 feet of the Vaqueros formation. Oil-bearing sandstones above the tested zone have been identified in core and on well logs but down-hole equipment limitations did not allow the Company to test these zones in the 4-9 well.

Allison/Whepley Formation

A 30 foot interval was completed in the Allison/Whepley formation. This zone flowed 33° API oil at a stabilized an average rate of 13 bbls/day over a 9 day flow period. The well was then shut-in and the pressure transient analysis indicated significant formation damage. A reservoir pressure of 11,100 psia was extrapolated from the PTA and this equates to a gradient of 0.8 psi per foot.

The test results achieved in the Allison/Whepley formation were very encouraging to the Company, particularly as the interval completed was mostly shale rather than a siltstone or sandstone sequence inter-bedded in the shale. Optimal perforation placement was not achieved due to poor cement bond over the primary target. Over 50 feet of potential siltstone reservoir remains to be adequately tested in future operations.

The results from drilling to date have been very encouraging and Zodiac continues to seek partners to help drill requisite wells into these promising plays to help unlock the potential of Zodiacs lands

Land Holdings

The Company continued to evaluate its land base in 2013. During the year, the Company elected not to exercise its option to drill its first earning well on the Panther block and as a result it reassigned approximately 8,000 non-contiguous and non-core lands back to its farmout partner. Furthermore, Zodiac held an option to earn lands on a prospect designated as the Hawk acreage (7,000 Gross, 3,900 Net acres) and Zodiac determined that these lands were not sufficiently prospective and accordingly elected not to drill to earn, thereby relinquishing its option too earn an interest in those lands. These events accounted for much of the decrease in the Company’s overall land base during the year. The Company commenced a lease renewal program targeting 2014 and 2015 expiries. At year end the Company is maintaining a total land base of approximately 72,000 net acres.

| Land Holdings | Acres | Sections |

| Gross | 104,000 | 163 |

| Net | 72,000 | 112 |

| Net revenue interest | 57,000 | 89 |

| | | | |

Strategy and Outlook

Zodiac plans to continue its process in California to identify additional joint venture (“JV”) partners to assist the Company in assessing and ultimately exploiting the potential within its acquired land base. That process is currently on-going.

Zodiac’s strategy also includes the evaluation of oil and gas opportunities both in North America and Internationally. Zodiac recently announced the acquisition of Muskwa Resources Ltd, with properties in the Duvernay and Nordegg plays in Alberta and a cretaceous channel play in Montana, USA.

The Company expects to focus its resources both on advancing its Californian properties and on developing a systematic plan to both achieve commerciality and appraise the array of resource and conventional plays on its lands in Alberta and Montana.

The pace at which this is executed will depend on the resources that the Company has at its disposal.

Corporate History and Background

Zodiac is in the pre-production stages of its oil and gas exploration and development program on its land holdings in California, USA (San Joaquin Valley, California). The Company holds varying working interests in approximately 72,000 net acres in the San Joaquin Basin in California. The primary target formations in the Jaguar prospect area are characterized as naturally fractured, low permeability sandstone, siltstone and shale contained in the Whepley, Vaqueros and Kreyenhagen formations. Management believes that this acreage position contains a major accumulation of light oil and further believes that through the application of established oilfield drilling, completion and production technologies and methodologies that Zodiac will be able to ultimately prove the commercial productivity of these lands.

On August 19, 2010, Zodiac Exploration Corp. (“Old Zodiac”) entered into an Arrangement Agreement with Peninsula Resources Ltd. (“Peninsula”), and a wholly-owned subsidiary of Peninsula, 1543081 Alberta Ltd., to effect a reverse takeover transaction (“RTO”). Under the Agreement, Old Zodiac amalgamated with 1543081 Alberta Ltd (the continuing corporate entity post-amalgamation was named Zodiac Exploration Corp.). Peninsula was renamed Zodiac Exploration Inc. (TSX-V:ZEX). This transaction was successfully completed on September 28, 2010 and shares of ZEX began trading on October 6, 2010.

Upon completion of the RTO, Old Zodiac shareholders exchanged their shares in Old Zodiac for shares in Zodiac Exploration Inc. on a 1:1.45 basis. Pre-existing warrants, performance warrants and stock options of Old Zodiac remain outstanding until they are exercised, expired, forfeited, or cancelled. Upon exercise of the warrants, performance warrants, or options they will be exchanged at the 1:1.45 ratio for Zodiac Exploration Inc. shares.

On October 9, 2013 Zodiac entered into a definitive agreement to acquire all the issued and outstanding shares of Muskwa Resources Ltd., a private oil and gas company based in Alberta. The exchange ratio for the Muskwa shares was one common share of Zodiac for each Muskwa share. The acquisition is to be completed by way of amalgamation and is expected to close during December 2013.

SELECTED ANNUAL FINANCIAL INFORMATION

At September 30, 2013, the Company has not yet achieved profitable operations, has accumulated a deficit of $50,323 (September 30, 2012 - $46,012, September 30, 2011 - $18,381) since inception and expects to incur further losses in the development of its business, which is typical of an oil and gas exploration company in the early stages of development. As at September 30, 2013, the Company’s cash balance was $13,923 (September 30, 2012 - $20,381, September 30, 2011 - $40,532) primarily resulting from warrant exercises during the year ended September 30, 2011.

To date, the Company has no oil and gas revenues and is considered to be in the development stage as defined by the Financial Accounting Standards Board (“FASB”) Accounting Standard’s Codification (“ASC”) 915.

SELECTED ANNUAL FINANCIAL HIGHLIGHTS

| | FINANCIAL HIGHLIGHTS |

| | Year ended September 30, 2013 $ | Year ended September 30, 2012 $ | Year ended September 30, 2011 $ |

| Interest income | 169 | 194 | 215 |

| Total assets | 71,726 | 76,180 | 109,198 |

| Cash flows used in operating activities | (4,349) | (4,162) | (3,785) |

| Net loss | (4,511) | (27,631) | (13,761) |

| Per share (basic and diluted) | (0.01) | (0.08) | (0.04) |

| Capital expenditures | 2,487 | 13,548 | 46,402 |

| General & administrative expenses | 4,408 | 3,629 | 3,824 |

Interest income was generated from interest received on cash held in bank deposits and term deposits obtained throughout the period.

Total assets at September 30, 2013 were $71,726 (September 30, 2012 - $76,180, September 30, 2011 - $109,198). The decrease in assets in 2013 was primarily the result of cash used in operating activities. Assets are comprised mainly of cash of $13,923 and property, plant and equipment of $56,636.

During the year ended September 30, 2013, funds used in operating activities increased to $4,349, from usage of $4,162 during the year ended September 30, 2012 and $3,785 during the year ended September 30, 2011. This increase in 2013 compared to 2012 is due to the increase in G&A expense resulting from severance payments made to previous management totaling $1,150 and payment of fees totaling $500 for services provided in relation to a campaign to find a joint venture partner. This resulted in the farm-out agreement with Aera Energy LLC. These increased expenditures were partly offset by lower overall G&A (mainly payroll costs) due to reduced activity and personnel during the year. G&A excluding the severance payments and fees was $2,758 compared with $3,629 in 2012. The net loss for the year ended September 30, 2013 was $4,511 or $(0.01) per share, compared to a loss of $27,631 or $(0.08) per share for the year ended September 30, 2012, and a loss of $13,761 or $(0.04) per share for the year ended September 30, 2011. The net loss incurred in 2013 was the result of continued G&A expenses for the Calgary and Bakersfield, CA offices. The loss in 2012 was primarily the result of a $23.2 million impairment writedown related to the 1-10 well and associated lease in California. The loss in 2011 was primarily the result of the $8.5 million impairment writedown related to the Company’s Nova Scotia properties. For the year ended September 30, 2013, Zodiac expensed $4,408 in general and administrative expenses (September 30, 2012 - $3,629, September 30, 2011 - $3,824), net of capitalized G&A of $26 (September 30, 2012 - $107, September 30, 2011 - $1,510). The amounts capitalized are directly related to costs associated with drilling permit applications.

Zodiac uses the Canadian dollar as its functional and reporting currency. The Company’s US operations are considered integrated. Accordingly, the Company uses the temporal method of accounting for the foreign currency transactions of its US subsidiaries.

ANNUAL RESULTS OF OPERATIONS

| | RESULTS OF OPERATIONS |

| | Year ended September 30, 2013 $ | Year ended September 30, 2012 $ | Year ended September 30, 2011 $ |

| Interest income | 169 | 194 | 215 |

| General and administrative expenses | 4,408 | 3,629 | 3,824 |

| Foreign exchange (gain)/loss | (174) | 195 | 64 |

| Stock based compensation | 236 | 499 | 1,546 |

| Depletion, depreciation and accretion | 39 | 340 | 45 |

| Asset impairment charge | 171 | 23,162 | 8,497 |

| Net loss | 4,511 | 27,631 | 13,761 |

Stock based compensation during the period ended September 30, 2013 was $236 (September 30, 2012 - $499, September 30, 2011 - $1,546). Included in the current year, the Company recognized $13 (September 30, 2012 - $73, September 30, 2011 - $265) of performance warrant compensation expense resulting from the issuance of 10,150,000 performance warrants to officers of the Company during the year ended September 30, 2011. During the 2012, 2,900,000 performance warrants held by a former officer were cancelled along with the remaining 7,250,000 during the year ended September 30, 2013. The balance of stock based compensation is related to stock options.

Depreciation and accretion (“D&A”) expenses during the period ended September 30, 2013 was $39 (September 30, 2012 - $340, September 30, 2011 - $45). These expenses relate to depreciation on fixed assets and accretion on the asset retirement obligation (“ARO”). As the Company’s petroleum and natural gas assets have not yet commenced production, no depletion has been recorded.

CAPITAL EXPENDITURES

The Company’s intention is to fund the acquisition of mineral and surface rights, the initiation of exploration activities including acquisition of seismic data, and the drilling, completion and tie-in of oil and gas wells through equity issues, operating cash flow and eventually borrowing base loans. A summary of the Company’s Property, Plant and Equipment additions to date are summarized below:

| | September 30, 2013 $ | September 30, 2012 $ | September 30, 2011 $ |

Beginning Property, Plant and Equipment balance | 54,465 | 64,477 | 21,037 |

| Land and lease rentals additions | 2,409 | 3,830 | 13,487 |

| Geology and seismic additions | 32 | 73 | 2,167 |

| Drilling and completions additions | 46 | 9,425 | 36,104 |

| Asset retirement obligation additions | (25) | (177) | 163 |

| Other fixed assets additions/(disposals) | (24) | 24 | 36 |

| Impairment expense | (264) | (23,162) | (8,472) |

Accumulated depreciation removed on disposal of fixed assets | 11 | - | - |

| Depreciation and accretion | (14) | (28) | (45) |

| Total | 56,636 | 54,465 | 64,477 |

During the year the Company’s capital focus was on maintaining and renewing mineral leases on property considered prospective to the company. At the same time the Company directed its efforts to farming out its lands, so that the capital cost of exploration could be borne by the Farmor.

In 2012 the Company’s capital focus was on finishing the drilling and completion of the 1-10 well. The Company performed a ten stage completion operation on the well using a water based fluid and a ball drop system. Despite equipment limitations during the stimulation and testing phases, the well flowed with no artificial lift. However, analysis of the flowing pressures and data from a very brief shut-in during the month of January 2012 indicated possible damage to the reservoir and hydraulic fractures with very limited effectiveness. In an attempt to offset the damage, the Company performed a small acid stimulation that had a negligible impact.In late April 2012, the Company shut-in the well to perform an extended build up test to further evaluate the reservoir and possible remedial actions to improve well results. The mineral lease upon which the 1-10 horizontal well was drilled contained continuous drilling obligations that required Zodiac to spud a new well by June 4, 2012. It was determined that additional expenditures on this lease and wellbore would not be in the Company’s best interest and accordingly, an impairment writedown of $23,162 was recognized.

In 2011 the Company’s primary focus was the drilling of the 4-9 well and initiation of the 1-10 well in the San Joaquin Basin along with the acquisition of the Panther prospect. Throughout the period discussed above there has been constant acquisition of additional lands in the Company’s operational area of focus in the San Joaquin basin, lease rental costs to maintain our rights in our land holdings, and acquisition of additional 3-D seismic data.

The Company’s initial entry into California occurred on June 8, 2009,when the Company acquired the rights, through farm-in, to drill for petroleum and natural gas on approximately 19,700 gross acres (15,750 net) (the “Jaguar Prospect”), of principally contiguous land in the San Joaquin Basin in California (“California Transaction”). The Company paid US$2,500 (CDN $2,800), issued 2 million Zodiac common shares, committed to pay 100% of a seismic program and drill the initial well on the Jaguar prospect, and agreed to pay 100% of the land lease rentals until the initial well is drilled to earn an 80% interest in these lands. With the completion of the drilling of the 4-9 well on the Jaguar prospect the Company has satisfied its earning requirements on the Jaguar prospect.

The California Transaction also had a secondary component, the Hawk prospect, which is characterized as a conventional prospect. The Company received an option to drill and pay for 100% of the first exploratory well on the Hawk prospect (to be spud by May 31, 2013) to earn an 80% interest in an approximate additional 4,800 gross acres (3,860 net). During 2013, Zodiac elected not to fulfill its drilling obligation on the Hawk lands and the option terminated and leases assigned back to the optionor.

On November 3, 2010, the Corporation entered into the Panther Acquisition Agreement whereby Zodiac would acquire, through farm-in, a 74.5% working interest in the Panther Assets. Total consideration paid by Zodiac for the Panther Assets was approximately US $8.4 million which was comprised of US $5.6 million in cash, US $1.9 million in Common Shares and a US $0.9 million credit in respect of future cash calls to be made by Zodiac to the seller. In addition, as part of the earning arrangements of the farm-in agreement, Zodiac was required to pay approximately 92% of the costs to drill two wells to test the Monterey and Kreyenhagen formations. Closing of the acquisition of the Panther Assets occurred January 31, 2011.The first well under the Panther acquisition agreement was due to be drilled by January 1, 2013. The Company elected not to exercise its option to drill its first earning well on the Panther block and as a result it reassigned approximately 8,000 non-contiguous and non-core lands back to its farmout partner.

During 2013 and 2012 reclamation activities continued in relation to its interests in Nova Scotia. During the year ended September 30, 2011, the Company took a full impairment charge of $8.5 million on its Nova Scotia assets upon assessing certain factors including (among others): intent to drill by the operator of the Windsor Basin project; remaining lease term; geological and geophysical evaluations; and drilling results. Given that the operator was no longer allocating meaningful resources to continued evaluation, lack of proved reserves attributable to the property and no success to date in finding a joint venture partner to fund a drilling program the Company felt that a full impairment charge was both reasonable and warranted.

LIQUIDITY & CAPITAL RESOURCES

As of September 30, 2013 the Company had positive working capital of $13,914 (September 30, 2012 - $20,420, September 30, 2011 - $37,731) and a cash balance of $13,923 (September 30, 2012 - $20,381).The reduction in working capital was primarily the result of expenditure on general and administrative costs and on the company’s land rental obligations. Zodiac’s revenue is incidental to its operations and is comprised entirely of interest earned on cash and cash equivalent balances and short-term investments. Zodiac’s short-term investments are held with a major Canadian financial institution. Zodiac has no outstanding bank debt or other interest-bearing indebtedness as at September 30, 2013.

In view of current financial market conditions and management’s need to preserve cash the Company initiated a joint-venture campaign on its lands in California in 2012. During the year ended September 30, 2013, the Company entered into the Farmout Agreement whereby Aera Energy LLC (“Aera”) has acquired the right to earn a 50% interest in approximately 19,600 net acres of Zodiac lands located in Kings County, California. The Farmout Agreement is comprised of two phases whereby Aera is required to pay 100% of the costs of drilling a vertical well and a horizontal well in each phase. Upon fulfillment of the drilling commitments in Phase 1, Aera will earn a 50% interest in approximately 9,800 acres and upon fulfillment of the drilling commitments in Phase 2, Aera will earn a 50% interest in approximately 9,800 acres. As a result, the Company does not anticipate spending its own capital resources on drilling on these lands during the current fiscal year. Therefore, its capital resource requirements have been reduced in 2013. Aera, spudded the first vertical well under the farm-out agreement on February 5, 2013 and has until June 1, 2014 to have complied with its drilling obligations under the Farmout Agreement. Failure to complete the terms of the farm out agreement result in damages payable to Zodiac of up to $3 million. On June 17, 2013 the Company entered into an engagement agreement with Meagher Energy Advisors and Western Energy Production to further its strategy of monetizing its Californian asset base through joint ventures, farm outs and dispositions, which if successful, would be expected to further reduce the demands on the Company’s capital resources.

The Company holds an operating lease agreement for office space in Calgary, Alberta commencing on March 1, 2012 and ending on February 28, 2017. The annual, average, basic rent obligation is $110 payable in monthly installments of $9. In addition to the basic rent, additional costs are payable monthly, and includes the Company’s proportionate share of all building operating costs and taxes of approximately $9,000 per month. As of August 1, 2013, a portion of the space was subleased to a third party reducing the annual average basic rent obligation to $28, payable in monthly installments of $2 for the remaining term and approximately $2 per month for the Company’s share of building operating costs and taxes. The Company is currently seeking to sublet the remainder of this space.

The Company holds an operating lease agreement for office space in Calgary, Alberta commencing on November 1, 2013 and ending on October 31, 2016. The annual average basic rent obligation is $132, payable in monthly installments of $11. In addition to the basic rent, additional rent is payable monthly, and includes the Company’s proportionate share of all operating costs and taxes. The Company holds an operating lease agreement for office space in Bakersfield, California commencing July 1, 2012 and ending on June 30, 2017. The annual average basic rent obligation is US$77 per annum, payable in average monthly installments of USD$6. In addition to the basic rent, additional rent is payable monthly, and includes the Company’s proportionate share of all operating costs and taxes.

The Company holds a five-year lease for its office space in Bakersfield, California commencing July 1, 2012. The annual, average, basic rent obligation will be US$77 per annum, payable in average monthly installments of USD$6. In addition, to the basic rent, additional costs are payable monthly, and includes the Company’s proportionate share of all building operating costs and taxes of approximately $1 per month. The Company is currently seeking to sublease part of these premises to further reduce rent and operating costs.

Zodiac assesses its financing requirements and its ability to access equity or debt markets on an ongoing basis. This assessment considers: the stage and success of the Company’s evaluation activities to date; the continued participation of the Company’s partners in evaluation activities; and financial market conditions.

Zodiac intends to continue to maintain financial flexibility and monitor its financing requirements along with its ability to access the equity markets. It is possible that future economic events and global conditions may result in further volatility in the financial markets, which could negatively impact Zodiac’s ability to access equity or debt markets in the future. Any inability to access equity or debt markets for sufficient capital, at acceptable terms, and within required timeframes, could have a material adverse effect on Zodiac’s financial condition, results of operations and prospects. Further discussion of these risks may be found in the “Business Risks and Uncertainties” section of this MD&A.

SUBSEQUENT EVENTS

ACQUISITION OF MUSKWA RESOURCES LTD.

On October 9, 2013, Zodiac entered into a definitive agreement (the "Acquisition Agreement") with Muskwa Resources Ltd. ("Muskwa"), a private oil and gas company, whereby Zodiac has agreed, subject to certain conditions, to acquire all of the issued and outstanding common shares of Muskwa as part of a business combination. The exchange ratio for the Muskwa Shares shall be one (1) common share of Zodiac for each issued and outstanding Muskwa Share at the price of $0.10 per share, for a total consideration paid of $8,500.

Pursuant to the terms of the Acquisition Agreement, Zodiac has agreed to provide Muskwa with a bridge loan exploration activities as well as certain of its general and administrative expenses. The bridge loan has a term of 180 days, an interest rate of 6% per annum and is secured against all of the present and after acquired property of Muskwa.

The Acquisition is expected to be completed by way of an amalgamation and is subject to customary approvals, including approval by Muskwa shareholders and the approval of the TSX Venture Exchange. Closing of the Acquisition is expected to occur during December, 2013.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

The discussion and analysis of our financial condition and results of operations are based upon the consolidated financial statements, which have been prepared in accordance with accounting principles generally accepted in the Unites States of America. The preparation of these financial statements requires us to make estimates and assumptions that affect the reported amounts of assets, liabilities, revenues and expenses, related disclosure of contingent assets and liabilities and oil and gas properties. Certain accounting policies involve judgments and uncertainties to such an extent that there is reasonable likelihood that materially different amounts could have been reported under different conditions, or if different assumptions had been used. We evaluate our estimates and assumptions on a regular basis. We base our estimates on historical experience and various other assumptions that are believed to be reasonable under the circumstances, the results of which form the basis for making judgments about the carrying values of assets and liabilities that are not readily apparent from other sources. Actual results may differ from these estimates and assumptions used in preparation of our financial statements. Below, we have provided expanded discussion of our more significant accounting policies, estimates and judgments for our financial statements. We believe these accounting policies reflect the more significant estimates and assumptions used in preparation of the financial statements.

The Company views the following estimates as critical:

Income Tax

Income taxes are accounted for using the liability method of income tax allocation. Under the liability method, future income tax assets and liabilities are recorded to recognize future income tax inflows and outflows arising from the settlement or recovery of assets and liabilities at their carrying values. Future income tax assets are also recognized for the benefits from tax losses and deductions that cannot be identified with particular assets or liabilities, provided those benefits are more likely than not to be realized. Future income tax assets and liabilities are determined based on the substantively enacted tax laws and rates that are anticipated to apply in the period of realization.

Oil and Gas Properties

The Company follows the full cost method of accounting whereby all costs related to the acquisition are initially capitalized. Costs capitalized include land acquisition costs, geological and geophysical expenditures, lease rentals on undeveloped properties, costs of drilling productive and non-productive wells, together with overhead and interest directly related to exploration and development activities, and lease and well equipment.

Costs capitalized are to be depleted and amortized on a cost centre basis using the unit-of-production method based on estimated proved petroleum and natural gas reserves before royalties as determined by independent engineers. In determining its depletion base, the Company includes estimated future capital costs to be incurred in developing proved reserves and excludes the cost of significant unproved properties until it is determined whether proved reserves are attributable to the unproved properties or impairment has occurred. Unproved properties are evaluated separately for impairment based on management’s assessment of future drilling and exploration activities. The Company’s decision to withhold costs from amortization and the timing of the transfer of those costs into the depreciating asset base involve significant judgment and may be subject to changes over time based on several factors, including drilling plans, availability of capital, project economics and results of drilling on adjacent acreage. During the period there has been nil production, and a depletion expense was not recognized.

Costs capitalized are periodically assessed for impairment after considering geological data and other information. A loss is recognized at the time of impairment by providing an impairment allowance.

As at September 30, 2013, the Company had oil and gas properties with a net book value of $56,636 (September 30, 2012 - $54,398, September 30, 2011 - $64,406) included in Property, Plant and Equipment on the balance sheet.

Future Development and Abandonment Costs

The Company recognizes the fair value of an asset retirement obligation (“ARO”) in the period in which a well or related asset is drilled, constructed or acquired and when a reasonable estimate of the fair value can be made. The fair value of the estimated ARO is recorded as a long-term liability, and equals the present value of estimated future cash flows, discounted using a risk-free interest rate adjusted for the Company’s credit standing. The liability accretes until the date of expected settlement of the retirement obligations or the asset is sold and is recorded as an accretion expense. Asset retirement costs are capitalized as part of the carrying value of the related assets. The capitalized amount is amortized to earnings on a basis consistent with depreciation and depletion of the underlying assets. Actual restoration expenditures are charged to the accumulated obligation as incurred. Any settlements are charged to income in the period of settlement. Holding all other factors constant, if our estimate of future abandonment and development costs is revised upward, earnings would decrease due to higher depletion, depreciation & accretion expense. Conversely, should these estimates be revised downwards, earnings would increase.

The Company develops estimates of these costs on a location by location basis, and as these costs typically extend many years into the future, estimating these future costs is difficult and requires management to make judgments that are subject to future revisions based upon numerous factors, including changing technology and the political and regulatory environment. We review our assumptions and estimates of future development and future abandonment costs on an annual basis.

Revenue Recognition

Revenue from the sale of petroleum and natural gas is recorded on a gross basis when title passes to an external party and is recognized based on volumes delivered to customers at contractual delivery points and when the significant risks and rewards of ownership have been transferred to the buyer and collectability is reasonably assured.

As at September 30, 2013, the Company has not recognized revenue from the sale of petroleum and natural gas as production has not yet occurred, other than incidental production from testing net against capital costs.

Stock-based Compensation

The Company records compensation expense in the consolidated financial statements for stock options granted to employees, consultants and directors using the fair value method. Fair values are determined using the Black-Scholes option pricing model, which is sensitive to the estimate of stock price volatility and the options’ expected life.

Financial Instruments

The fair values of financial instruments, which include cash and cash equivalents, other receivables, accounts payable and accrued liabilities approximate their carrying values due to the relatively short maturity of these instruments.

RECENT ACCOUNTING PRONOUNCEMENTS

The Company successfully completed efforts to raise additional equity capital in conjunction with the plan to combine with Peninsula (note 4). Post RTO, U.S. based investors form a substantial minority of the Company’s shareholder base. Should trading of the Company’s shares shift the balance to majority ownership by U.S. investors, it was anticipated, given the Company’s focus on the properties located in California, that the Company will eventually become a Domestic Issuer from a Securities Exchange Commission ("SEC") perspective. As a result, the Company would then be obligated to prepare and file U.S. GAAP based financial statements and regulatory filings to comply with U.S. regulations and the Company could avail itself of the option to use its U.S. GAAP statements for all financial disclosure requirements both in Canada and the U.S. Alternatively, should shareholdings shift towards a greater allocation to Canadian and international investors or stay static, International Financial Reporting Standards (“IFRS”) would have needed to be adopted for the fiscal year beginning October 1, 2011. In order to eliminate the uncertainty regarding an inevitable accounting conversion, to either IFRS or U.S. GAAP, the Company filed a form 40 F registration statement with the SEC during the quarter ended June 30, 2011. The Company intends to continue to avail itself of the option to use its U.S. GAAP statements for all financial disclosure requirements both in Canada and the U.S. which it began doing for fiscal 2011.

The following recently issued accounting developments have been applied or may impact the Company in future periods.

In January 2013, the FASB issued Accounting Standards Update No. 2013-01, Balance Sheet (Topic 210): Clarifying the Scope of Disclosures about Offsetting Assets and Liabilities (ASU 2013-01). The main objective in developing this update is to address implementation issues about the scope of Accounting Standards Update No. 2011-11, Balance Sheet (Topic 210): Disclosures about Offsetting Assets and Liabilities. The update requires entities to disclose information about offsetting and related arrangements of financial instruments and derivative instruments. ASU 2013-01 is effective for our first quarter of fiscal 2014. The pronouncement did not have a material effect on the Company’s financial position, results of operations or cash flows.

In February 2013, the FASB issued Accounting Standards Update (“ASU”) 2013-02, Reporting of Amounts Reclassified out of Accumulated Other Comprehensive Income, an amendment to FASB ASC Topic 220. The update requires disclosure of amounts reclassified out of accumulated other comprehensive income by component. In addition, an entity is required to present either on the face of the statement of operations or in the notes, significant amounts reclassified out of accumulated other comprehensive income by the respective line items of net income but only if the amount reclassified is required to be reclassified to net income in its entirety in the same reporting period. For amounts not reclassified in their entirety to net income, an entity is required to cross-reference to other disclosures that provide additional detail about those amounts. This ASU is effective prospectively for the Company’s fiscal years, and interim periods within those years, beginning after December 15, 2012. The pronouncement did not have a material effect on the Company’s financial position, results of operations or cash flows.

In February 2013, the Financial Accounting Standards Board, or FASB, issued ASU No. 2013-04, “Liabilities (Topic 405): Obligations Resulting from Joint and Several Liability Arrangements for which the Total Amount of the Obligation Is Fixed at the Reporting Date.” This ASU addresses the recognition, measurement, and disclosure of certain obligations resulting from joint and several arrangements including debt arrangements, other contractual obligations, and settled litigation and judicial rulings. The ASU is effective for public entities for fiscal years, and interim periods within those years, beginning after December 15, 2013. Management does not expect the pronouncement to have a material effect on the Company’s financial position, results of operations or cash flows.

In March 2013, the FASB issued ASU No. 2013-05, “Foreign Currency Matters (Topic 830): Parent’s Accounting for the Cumulative Translation Adjustment upon Derecognition of Certain Subsidiaries or Groups of Assets within a Foreign Entity or of an Investment in a Foreign Entity.” This ASU addresses the accounting for the cumulative translation adjustment when a parent either sells a part or all of its investment in a foreign entity or no longer holds a controlling financial interest in a subsidiary or group of assets that is a nonprofit activity or a business within a foreign entity. The guidance outlines the events when cumulative translation adjustments should be released into net income and is intended by the FASB to eliminate some disparity in current accounting practice. This ASU is effective prospectively for fiscal years, and interim periods within those years, beginning after December 15, 2013. Management does not expect the pronouncement to have a material effect on the Company’s financial position, results of operations or cash flows.

In March 2013, the FASB issued ASU 2013-07, “Presentation of Financial Statements (Topic 205): Liquidation Basis of Accounting.” The amendments require an entity to prepare its financial statements using the liquidation basis of accounting when liquidation is imminent. Liquidation is imminent when the likelihood is remote that the entity will return from liquidation and either (a) a plan for liquidation is approved by the person or persons with the authority to make such a plan effective and the likelihood is remote that the execution of the plan will be blocked by other parties or (b) a plan for liquidation is being imposed by other forces (for example, involuntary bankruptcy). If a plan for liquidation was specified in the entity’s governing documents from the entity’s inception (for example, limited-life entities), the entity should apply the liquidation basis of accounting only if the approved plan for liquidation differs from the plan for liquidation that was specified at the entity’s inception. The amendments require financial statements prepared using the liquidation basis of accounting to present relevant information about an entity’s expected resources in liquidation by measuring and presenting assets at the amount of the expected cash proceeds from liquidation. The entity should include in its presentation of assets any items it had not previously recognized under U.S. GAAP but that it expects to either sell in liquidation or use in settling liabilities (for example, trademarks). The amendments are effective for entities that determine liquidation is imminent during annual reporting periods beginning after December 15, 2013, and interim reporting periods therein. Entities should apply the requirements prospectively from the day that liquidation becomes imminent. Early adoption is permitted. Management does not expect the pronouncement to have a material effect on the Company’s financial position, results of operations or cash flows.

In July 2013, the FASB issued ASU No. 2013-11, Income Taxes (Topic 740): Presentation of an Unrecognized Tax Benefit When a Net Operating Loss Carryforward, a Similar Tax Loss, or a Tax Credit Carryforward Exists. The update provides that an unrecognized tax benefit, or a portion of an unrecognized tax benefit, should be presented in the financial statements as a reduction to a deferred tax asset for a net operating loss carryforward, a similar tax loss, or a tax credit carryforward, except as follows. To the extent a net operating loss carryforward, a similar tax loss, or a tax credit carryforward is not available at the reporting date under the tax law of the applicable jurisdiction to settle any additional income taxes that would result from the disallowance of a tax position or the tax law of the applicable jurisdiction does not require the entity to use, and the entity does not intend to use, the deferred tax asset for such purpose, the unrecognized tax benefit should be presented in the financial statements as a liability and should not be combined with deferred tax assets. The assessment of whether a deferred tax asset is available is based on the unrecognized tax benefit and deferred tax asset that exist at the reporting date and should be made presuming disallowance of the tax position at the reporting date. The amendments in this update do not require new recurring disclosures. The amendments are effective prospectively for reporting periods beginning after December 15, 2013. Management does not expect the pronouncement to have a material effect on the Company’s financial position, results of operations or cash flows.

OFF BALANCE SHEET ARRANGEMENTS

The Company has not entered into any off-balance sheet arrangements such as guarantee contracts, contingent interests in assets transferred to unconsolidated entities, derivative financial obligations, or with respect to any obligation under a variable interest equity arrangement.

OUTSTANDING SHARE DATA

Authorized capital:

Unlimited number of common shares with voting rights.

Unlimited number of preferred shares, issuable in series.

Issued and outstanding:

| - | 359,635,408 common shares as at September 30, 2013. |

Warrants outstanding:

| - | 24,445,706 with an exercise price of $0.414. 12,325,008 expire on March 17, 2015, 11,088,539 expire on April 1, 2015 and 1,032,159 expire on April 9, 2015. |

RELATED PARTIES

During the year ended September 30, 2013, aggregate legal fees of $179, were charged by a law firm in which the corporate secretary of the Company is a partner of, and were expensed as general and administrative expenses (September 30, 2012 - $139).

As at September 30, 2013 the Company owed $28 (September 30, 2012 - $50) to the law firm.

BUSINESS RISKS AND UNCERTAINTIES

The Company is subject to various risks and uncertainties, including, but not limited to, those listed below:

Oil and Gas Exploration and Development

The oil and gas industry is extremely competitive in all aspects including the acquisition of oil and gas interests, the marketing of oil and natural gas, and acquiring or gaining access to necessary drilling equipment, services and supplies. Zodiac competes with numerous other companies in the search for and acquisition of prospective oil and gas plays.

Zodiac is subject to all risks and hazards inherent in the business involved in the exploration for, and the acquisition, development, production and marketing of oil and natural gas. Many of these inherent risks cannot be compensated for, even with the combination of experience, knowledge and careful planning of an experienced technical team. The risks and hazards typically associated with oil and gas operations include equipment failure, fire, explosion, blowouts, sour gas releases, pipeline ruptures and oil spills, each of which could result in substantial damage to oil and gas wells, production facilities, other property, the environment or personal injury.

Capital Requirements

To finance future operations, Zodiac may require financing from external sources including, but not limited to, issuance of common or preferred shares, issuance of debt or implementation of working interest farm-out agreements. There can be no assurance that such financing will be offered on acceptable terms or that it will be available at all to the Company. If additional financing is raised through the issuance of equity or convertible debt securities, control of the Company may change and the interests of shareholders in the net assets of Zodiac may be diluted. If unable to secure financing on acceptable terms, Zodiac may have to cancel or postpone certain of its planned exploration and development activities which may ultimately lead to Zodiac’s inability to fulfill the minimum work obligations under various farm-in agreements and potentially to the forfeiture of existing land holdings. Availability of capital will also directly impact the Company’s ability to take advantage of additional farm-in and acquisition opportunities.

Operations

Zodiac’s largest land position relates to the oil and gas projects located in Kings County, California, USA, which is currently its primary focus. Uncertainties include, but are not limited to: a change in the general regulatory environment; a change in environmental protection policies; or a change in taxation policies. These uncertainties, all of which are beyond the Company’s control, could have a material adverse effect on Zodiac’s business, prospects and results of operations. Zodiac will require licenses or permits from various governmental authorities to carry out future exploration, development and production activities. There can be no assurance that Zodiac will be able to obtain all necessary licenses and permits when required.

Uncertainty of Title

Although Zodiac conducts a thorough title review prior to acquiring additional acreage in its areas of interest, such reviews do not guarantee that an unforeseen defect in the chain of title will not arise that may call into question Zodiac’s interest in its land holdings. Any uncertainty with respect to one or more of Zodiac’s leasehold interests could have a material adverse effect on the Company’s business, prospects and results of operations.

Foreign Operations

Zodiac operates in the United States and consequently, if legal disputes arise related to oil and gas leases acquired by Zodiac, these disputes would likely be subject to the jurisdiction of courts other than those of Canada.

Operational Uncertainties

In carrying out its planned exploration program, Zodiac is subject to various risks including, but not limited to: the availability of equipment, manpower and supplies; the effects of weather on drilling and production; and operating in an environmentally responsible fashion.

The Company mitigates these business risks by: working with qualified operators and/or operating the majority of properties to control the amount and timing of capital expenditures; restricting operations to areas where locations are accessible, operating and capital costs are reasonable and on-stream times are shorter; drilling wells in areas with multiple high deliverability zone potential; striving to maintain cost-effective operations; using current technology to maximize production and recoveries and reduce operating costs and environmental impacts; and maintainingmemberships in industry organizations.

Dependence on Management

The Company strongly depends on the technical and business expertise of its management team and there is little possibility that this dependence will decrease in the near term. The unexpected loss of any member of the management team may have a material adverse impact on the operations of the Company.

DATE

This MD&A is dated December 3, 2013