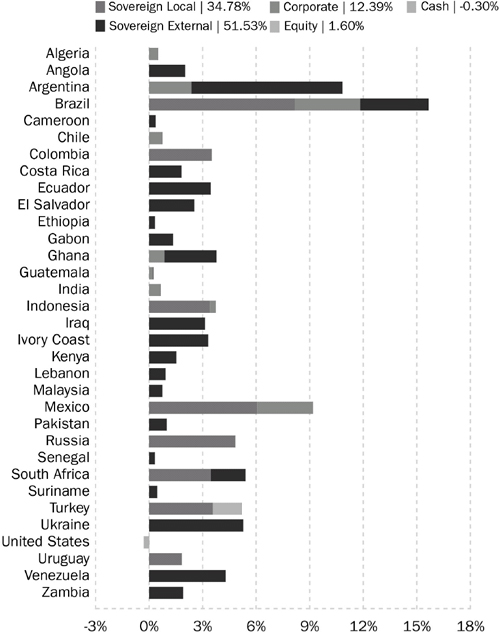

Sector Allocation(2) | |

| Sovereign Local | 34.78% |

| Sovereign External | 51.53% |

| Corporate | 12.39% |

| Equity | 1.60% |

| Cash & Equivalents/U.S. Treasuries | ‐0.30% |

Regional Breakdown(2) | |

| Latin America | 54.36% |

| Africa | 20.13% |

| Europe | 15.24% |

| Asia | 6.06% |

| Middle East | 4.51% |

| Cash & Equivalents/ U.S. Treasuries | ‐0.30% |

Sovereign Local Currency Breakdown(2) | |

| Brazilian Real | 8.15% |

| Mexican Peso | 6.06% |

| Russian Ruble | 4.82% |

| Turkish New Lira | 3.56% |

| Colombian Peso | 3.49% |

| South African Rand | 3.45% |

| Indonesian Rupiah | 3.41% |

| Uruguayan Peso | 1.84% |

| Total | 34.78% |

(1) | Current Distribution Rate is based on the Fund’s current annualized monthly distribution divided by the Fund’s current market price. The Fund’s monthly distributions to its shareholders may be comprised of ordinary income, net realized capital gains and return of capital in order to maintain a level distribution. |

(2) | Based on managed assets and investment manager’s sector classifications including derivative exposure. For purposes of this example, managed assets include total net assets plus any borrowings attributed to the use of reverse repurchase agreements and the notional values of interest rate swaps as described on page 12. |

(3) | Country refers to country of primary risk exposure, as determined by Stone Harbor. In certain instances, a security’s country of incorporation may be different from its country of risk. |

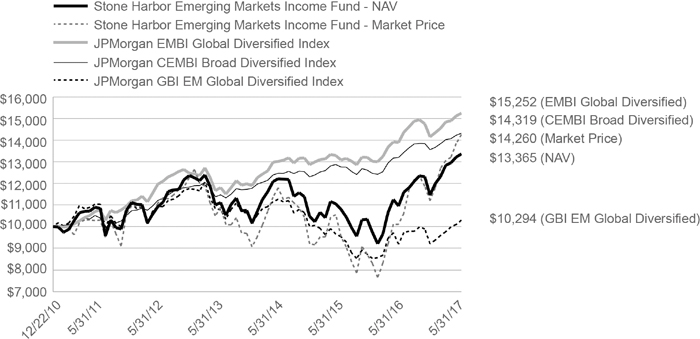

| Stone Harbor Emerging Markets Income Fund | Growth of $10,000 Investment |

Comparison of Change in Value of $10,000 Investment in Stone Harbor Emerging Markets Income Fund and the JPMorgan Emerging Markets Bond Indices: EMBI Global Diversified, CEMBI Broad Diversified, and GBI EM Global Diversified (Please refer to the Additional Information section for detailed benchmark descriptions).

Total Returns as of May 31, 2017 (Inception Date December 22, 2010)

| | | Average Annual Return |

| | 6 Month | One Year | Three Year | Five Year | Since Inception |

| Stone Harbor Emerging Markets Income Fund – NAV | 16.71% | 22.08% | 3.43% | 5.64% | 4.61% |

| Stone Harbor Emerging Markets Income Fund – Market Price | 27.32% | 41.16% | 7.89% | 6.88% | 5.67% |

| JPMorgan CEMBI Broad Diversified Index | 5.61% | 8.50% | 4.96% | 5.90% | 5.73% |

| JPMorgan EMBI Global Diversified Index | 7.76% | 9.77% | 5.55% | 6.48% | 6.78% |

| JPMorgan GBI EM Global Diversified Index | 11.91% | 12.17% | ‐2.63% | 0.32% | 0.45% |

Past performance is no guarantee of future results. Current performance may be lower or higher than the performance shown. Total return is calculated by determining the percentage change in NAV or market price (as applicable) in the specified period. The calculation assumes that all income dividends, capital gain and return of capital distributions, if any, have been reinvested and includes all fee waivers and expense reimbursements. Total return does not reflect the deduction of taxes that a shareholder would pay on Fund distributions or broker commissions or sales charges in connection with the purchase or sale of Fund shares. Investment return and principal value will vary, and shares, when sold, may be worth more or less than their original cost. Total returns for a period of less than one year are not annualized. Index returns do not include the effects of sales charges or management fees. It is not possible to invest directly in an index.

Performance at market price will differ from its results at NAV. Although market price returns typically reflect investment results over time, during shorter periods returns at market price can also be influenced by factors such as changing views about the Fund, market conditions, supply and demand for the Fund’s shares, or changes in Fund dividends.

An investment in the Fund involves risk, including the loss of principal. Total return, market price, market price yield and NAV will fluctuate with changes in market conditions. This data is provided for information purposes only and is not intended for trading purposes. Closed‐end funds, unlike open‐end funds, are not continuously offered. There is a onetime public offering and once issued, shares of closed‐end funds are traded in the open market through a stock exchange. NAV is equal to total assets attributable to common shareholders less total liabilities divided by the number of common shares outstanding. Holdings are subject to change daily.

| Semi-Annual Report | May 31, 2017 | 5 |

| Stone Harbor Emerging Markets Income Fund | Statement of Investments |

May 31, 2017 (Unaudited)

| | | Reference Rate | | Currency | | Rate | | Maturity Date | | Principal Amount/Shares* | | Value Expressed (in USD) | |

| | | | | | | | | | | | | | |

| SOVEREIGN DEBT OBLIGATIONS - 105.36% | | | | | | | | | | | |

| Angola - 2.93% | | | | | | | | | | | | | |

| Republic of Angola: | | | | | | | | | | | | | |

| | | | | USD | | | 9.50 | % | 11/12/25 | | | 2,689,000 | | $ | 2,887,314 | (1)(2) |

| | | | | USD | | | 9.50 | % | 11/12/25 | | | 3,798,000 | | | 4,078,102 | (2)(3) |

| | | | | | | | | | | | | | | | 6,965,416 | |

| | | | | | | | | | | | | | | | | |

| Argentina - 12.94% | | | | | | | | | | | | | | | | |

| Provincia del Chaco | | | | USD | | | 9.38 | % | 08/18/24 | | | 2,360,000 | | | 2,365,900 | (2)(3) |

| Republic of Argentina: | | | | | | | | | | | | | | | | |

| | | | | EUR | | | 7.82 | % | 12/31/33 | | | 3,283,422 | | | 3,960,456 | |

| | | | | EUR | | | 7.82 | % | 12/31/33 | | | 6,447,712 | | | 7,686,677 | |

| | | | | USD | | | 8.28 | % | 12/31/33 | | | 13,007,618 | | | 14,275,861 | (2) |

| | | | | EUR | | | 0.00 | % | 12/15/35 | | | 20,140,897 | | | 2,132,434 | (4) |

| | | | | EUR | | | 2.26 | % | 12/31/38 | | | 509,052 | | | 359,690 | (5) |

| | | | | | | | | | | | | | | | 30,781,018 | |

| | | | | | | | | | | | | | | | | |

| Brazil - 16.33% | | | | | | | | | | | | | | | | |

| Brazil Minas SPE via State of Minas Gerais | | | | USD | | | 5.33 | % | 02/15/28 | | | 11,827,000 | | | 11,472,190 | (2)(3) |

| Nota Do Tesouro Nacional: | | | | | | | | | | | | | | | | |

| | | | | BRL | | | 10.00 | % | 01/01/21 | | | 49,200,000 | | | 15,121,437 | |

| | | | | BRL | | | 10.00 | % | 01/01/23 | | | 40,500,000 | | | 12,251,028 | |

| | | | | | | | | | | | | | | | 38,844,655 | |

| | | | | | | | | | | | | | | | | |

| Cameroon - 0.52% | | | | | | | | | | | | | | | | |

| Republic of Cameroon | | | | USD | | | 9.50 | % | 11/19/25 | | | 1,030,000 | | | 1,226,987 | (1) |

| | | | | | | | | | | | | | | | | |

| Colombia - 4.52% | | | | | | | | | | | | | | | | |

| Bogota Distrio Capital | | | | COP | | | 9.75 | % | 07/26/28 | | | 8,000,000,000 | | | 2,911,809 | (3) |

| Republic of Colombia | | | | COP | | | 7.50 | % | 08/26/26 | | | 21,000,000,000 | | | 7,830,896 | |

| | | | | | | | | | | | | | | | 10,742,705 | |

| | | | | | | | | | | | | | | | | |

| Costa Rica - 2.61% | | | | | | | | | | | | | | | | |

| Republic of Costa Rica: | | | | | | | | | | | | | | | | |

| | | | | USD | | | 7.00 | % | 04/04/44 | | | 1,485,000 | | | 1,546,256 | (3) |

| | | | | USD | | | 7.00 | % | 04/04/44 | | | 2,853,000 | | | 2,970,686 | (1)(2) |

| | | | | USD | | | 7.16 | % | 03/12/45 | | | 1,602,000 | | | 1,684,103 | (2)(3) |

| | | | | | | | | | | | | | | | 6,201,045 | |

| | | | | | | | | | | | | | | | | |

| Ecuador - 1.37% | | | | | | | | | | | | | | | | |

| Republic of Ecuador: | | | | | | | | | | | | | | | | |

| | | | | USD | | | 7.95 | % | 06/20/24 | | | 1,300,000 | | | 1,238,250 | (3) |

| | | | | USD | | | 9.65 | % | 12/13/26 | | | 1,998,000 | | | 2,027,970 | (1)(2) |

| | | | | | | | | | | | | | | | 3,266,220 | |

| | | | | | | | | | | | | | | | | |

| El Salvador - 3.62% | | | | | | | | | | | | | | | | |

| Republic of El Salvador: | | | | | | | | | | | | | | | | |

| | | | | USD | | | 7.75 | % | 01/24/23 | | | 357,000 | | | 362,801 | (3) |

| | | | | USD | | | 8.25 | % | 04/10/32 | | | 4,108,000 | | | 4,077,190 | (2)(3) |

| | | | | USD | | | 7.65 | % | 06/15/35 | | | 3,735,000 | | | 3,482,888 | (2)(3) |

| | | | | USD | | | 7.63 | % | 02/01/41 | | | 750,000 | | | 690,000 | (3) |

| | | | | | | | | | | | | | | | 8,612,879 | |

See Notes to Financial Statements.

| Stone Harbor Emerging Markets Income Fund | Statement of Investments |

May 31, 2017 (Unaudited)

| | | Reference Rate | | Currency | | Rate | | Maturity Date | | Principal Amount/Shares* | | Value Expressed (in USD) | |

| Ethiopia - 0.44% | | | | | | | | | | | | | |

| Federal Democratic Republic of Ethiopia | | | | USD | | | 6.63 | % | 12/11/24 | | | 1,028,000 | | $ | 1,036,995 | (1) |

| | | | | | | | | | | | | | | | | |

| Gabon - 1.90% | | | | | | | | | | | | | | | | |

| Republic of Gabon: | | | | | | | | | | | | | | | | |

| | | | | USD | | | 6.38 | % | 12/12/24 | | | 1,709,000 | | | 1,702,591 | (1) |

| | | | | USD | | | 6.95 | % | 06/16/25 | | | 2,775,000 | | | 2,816,625 | (1)(2) |

| | | | | | | | | | | | | | | | 4,519,216 | |

| | | | | | | | | | | | | | | | | |

| Ghana - 4.20% | | | | | | | | | | | | | | | | |

| Republic of Ghana: | | | | | | | | | | | | | | | | |

| | | | | USD | | | 9.25 | % | 09/15/22 | | | 5,525,000 | | | 5,994,625 | (1)(2) |

| | | | | USD | | | 7.88 | % | 08/07/23 | | | 2,244,000 | | | 2,288,880 | (2)(3) |

| | | | | USD | | | 10.75 | % | 10/14/30 | | | 1,366,000 | | | 1,704,085 | (1)(2) |

| | | | | | | | | | | | | | | | 9,987,590 | |

| | | | | | | | | | | | | | | | | |

| Indonesia - 4.91% | | | | | | | | | | | | | | | | |

| Republic of Indonesia: | | | | | | | | | | | | | | | | |

| | | | | IDR | | | 8.25 | % | 07/15/21 | | | 75,881,000,000 | | | 6,015,791 | |

| | | | | IDR | | | 8.38 | % | 09/15/26 | | | 68,900,000,000 | | | 5,664,077 | |

| | | | | | | | | | | | | | | | 11,679,868 | |

| | | | | | | | | | | | | | | | | |

| Iraq - 1.33% | | | | | | | | | | | | | | | | |

| Republic of Iraq | | | | USD | | | 5.80 | % | 01/15/28 | | | 3,440,000 | | | 3,156,200 | (2)(3) |

| | | | | | | | | | | | | | | | | |

| Ivory Coast - 4.73% | | | | | | | | | | | | | | | | |

| Ivory Coast Government | | | | USD | | | 5.75 | % | 12/31/32 | | | 11,567,920 | | | 11,249,802 | (2)(3)(5) |

| | | | | | | | | | | | | | | | | |

| Kenya - 2.14% | | | | | | | | | | | | | | | | |

| Republic of Kenya: | | | | | | | | | | | | | | | | |

| | | | | USD | | | 6.88 | % | 06/24/24 | | | 2,350,000 | | | 2,420,500 | (2)(3) |

| | | | | USD | | | 6.88 | % | 06/24/24 | | | 2,596,000 | | | 2,673,880 | (1)(2) |

| | | | | | | | | | | | | | | | 5,094,380 | |

| | | | | | | | | | | | | | | | | |

| Lebanon - 1.32% | | | | | | | | | | | | | | | | |

| Lebanese Republic: | | | | | | | | | | | | | | | | |

| | | | | USD | | | 6.25 | % | 11/04/24 | | | 712,000 | | | 712,890 | |

| | | | | USD | | | 6.75 | % | 11/29/27 | | | 2,400,000 | | | 2,427,600 | (2) |

| | | | | | | | | | | | | | | | 3,140,490 | |

| | | | | | | | | | | | | | | | | |

| Malaysia - 1.05% | | | | | | | | | | | | | | | | |

| 1MDB Global Investments Ltd. | | | | USD | | | 4.40 | % | 03/09/23 | | | 2,700,000 | | | 2,511,000 | (2)(3) |

| | | | | | | | | | | | | | | | | |

| Mexico - 4.91% | | | | | | | | | | | | | | | | |

| Mexican Bonos: | | | | | | | | | | | | | | | | |

| | | | | MXN | | | 8.50 | % | 12/13/18 | | | 52,440,000 | | | 2,865,265 | |

| | | | | MXN | | | 6.50 | % | 06/10/21 | | | 129,500,000 | | | 6,758,857 | |

| | | | | MXN | | | 5.75 | % | 03/05/26 | | | 42,480,000 | | | 2,047,474 | |

| | | | | | | | | | | | | | | | 11,671,596 | |

| | | | | | | | | | | | | | | | | |

| Pakistan - 1.42% | | | | | | | | | | | | | | | | |

| Republic of Pakistan | | | | USD | | | 8.25 | % | 09/30/25 | | | 3,000,000 | | | 3,388,125 | (2)(3) |

| | | | | | | | | | | | | | | | | |

| Russia - 6.91% | | | | | | | | | | | | | | | | |

| Russian Federation | | | | RUB | | | 7.40 | % | 12/07/22 | | | 947,000,000 | | | 16,445,610 | |

| | | | | | | | | | | | | | | | | |

| Senegal - 0.43% | | | | | | | | | | | | | | | | |

| Republic of Senegal | | | | USD | | | 6.25 | % | 05/23/33 | | | 1,024,000 | | | 1,036,298 | (1) |

See Notes to Financial Statements.

| Semi-Annual Report | May 31, 2017 | 7 |

| Stone Harbor Emerging Markets Income Fund | Statement of Investments |

May 31, 2017 (Unaudited)

| | | Reference Rate | | Currency | | Rate | | Maturity Date | | Principal Amount/Shares* | | Value Expressed (in USD) | |

| South Africa - 4.77% | | | | | | | | | | | | | |

| Republic of South Africa | | | | ZAR | | | 10.50 | % | 12/21/26 | | | 132,440,000 | | $ | 11,341,493 | |

| | | | | | | | | | | | | | | | | |

| Suriname - 0.62% | | | | | | | | | | | | | | | | |

| Republic of Suriname | | | | USD | | | 9.25 | % | 10/26/26 | | | 1,438,000 | | | 1,477,545 | (1) |

| | | | | | | | | | | | | | | | | |

| Turkey - 5.05% | | | | | | | | | | | | | | | | |

| Republic of Turkey: | | | | | | | | | | | | | | | | |

| | | | | TRY | | | 10.50 | % | 01/15/20 | | | 24,520,000 | | | 6,948,573 | |

| | | | | TRY | | | 9.00 | % | 07/24/24 | | | 19,000,000 | | | 5,057,116 | |

| | | | | | | | | | | | | | | | 12,005,689 | |

| | | | | | | | | | | | | | | | | |

| Ukraine - 7.20% | | | | | | | | | | | | | | | | |

| Ukraine Government: | | | | | | | | | | | | | | | | |

| | | | | USD | | | 7.75 | % | 09/01/19 | | | 51,000 | | | 52,453 | (1) |

| | | | | USD | | | 7.75 | % | 09/01/20 | | | 2,966,000 | | | 3,022,354 | (1)(2) |

| | | | | USD | | | 7.75 | % | 09/01/21 | | | 7,216,000 | | | 7,327,848 | (1)(2) |

| | | | | USD | | | 7.75 | % | 09/01/22 | | | 1,886,000 | | | 1,897,316 | (3) |

| | | | | USD | | | 7.75 | % | 09/01/23 | | | 1,427,000 | | | 1,424,146 | (1) |

| | | | | USD | | | 7.75 | % | 09/01/23 | | | 2,458,000 | | | 2,453,084 | (2)(3) |

| | | | | USD | | | 7.75 | % | 09/01/25 | | | 972,000 | | | 957,420 | (1) |

| | | | | | | | | | | | | | | | 17,134,621 | |

| | | | | | | | | | | | | | | | | |

| Uruguay - 2.63% | | | | | | | | | | | | | | | | |

| Oriental Republic of Uruguay | | | | UYU | | | 4.38 | % | 12/15/28 | | | 95,742,550 | | | 3,620,002 | |

| Uruguay Notas del Tesoro | | | | UYU | | | 13.90 | % | 07/29/20 | | | 69,000,000 | | | 2,642,419 | |

| | | | | | | | | | | | | | | | 6,262,421 | |

| | | | | | | | | | | | | | | | | |

| Venezuela - 1.82% | | | | | | | | | | | | | | | | |

| Republic of Venezuela: | | | | | | | | | | | | | | | | |

| | | | | USD | | | 13.63 | % | 08/15/18 | | | 518,000 | | | 409,867 | (3) |

| | | | | USD | | | 7.75 | % | 10/13/19 | | | 7,059,200 | | | 3,926,680 | (2) |

| | | | | | | | | | | | | | | | 4,336,547 | |

| | | | | | | | | | | | | | | | | |

| Zambia - 2.74% | | | | | | | | | | | | | | | | |

| Republic of Zambia: | | | | | | | | | | | | | | | | |

| | | | | USD | | | 5.38 | % | 09/20/22 | | | 204,000 | | | 195,075 | (3) |

| | | | | USD | | | 8.50 | % | 04/14/24 | | | 1,169,000 | | | 1,249,369 | (3) |

| | | | | USD | | | 8.50 | % | 04/14/24 | | | 2,280,000 | | | 2,436,750 | (1)(2) |

| | | | | USD | | | 8.97 | % | 07/30/27 | | | 2,435,000 | | | 2,631,322 | (2)(3) |

| | | | | | | | | | | | | | | | 6,512,516 | |

| | | | | | | | | | | | | | | | | |

| TOTAL SOVEREIGN DEBT OBLIGATIONS | | | | | | | | | | | | | 250,628,927 | |

| (Cost $243,382,265) | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| BANK LOANS - 0.69% | | | | | | | | | | | | | | | | |

| Brazil - 0.69% | | | | | | | | | | | | | | | | |

| Banco de Investimentos Credit Suisse Brasil SA - Brazil Loan Tranche A | | | | USD | | | 6.25 | % | 01/10/18 | | | 500,000 | | | 503,325 | (6) |

| Banco de Investimentos Credit Suisse Brasil SA - Brazil Loan Tranche B | | | | USD | | | 6.25 | % | 01/10/18 | | | 1,125,000 | | | 1,132,482 | (6) |

| | | | | | | | | | | | | | | | 1,635,807 | |

| | | | | | | | | | | | | | | | | |

Indonesia - 0.00%(7) | | | | | | | | | | | | | | | | |

| PT Bakrie & Brothers TBK | | | | USD | | | 0.00 | % | 11/25/14 | | | 2,515,676 | | | 252 | (6)(8) |

| | | | | | | | | | | | | | | | | |

| TOTAL BANK LOANS | | | | | | | | | | | | | | | 1,636,059 | |

| (Cost $2,631,271) | | | | | | | | | | | | | | | | |

See Notes to Financial Statements.

| Stone Harbor Emerging Markets Income Fund | Statement of Investments |

May 31, 2017 (Unaudited)

| | | Reference Rate | | Currency | | Rate | | Maturity Date | | Principal Amount/Shares* | | | Value Expressed (in USD) | |

| CORPORATE BONDS - 32.40% | | | | | | | | | | | | | | |

| Algeria - 0.72% | | | | | | | | | | | | | | |

| GTH Finance BV | | | | USD | | | 7.25 | % | 04/26/23 | | | 1,534,000 | | | $ | 1,706,575 | (1) |

| | | | | | | | | | | | | | | | | | |

| Argentina - 2.53% | | | | | | | | | | | | | | | | | |

| Pampa Energia SA | | | | USD | | | 7.50 | % | 01/24/27 | | | 2,500,000 | | | | 2,646,250 | (1)(2) |

| Petrobras Argentina SA | | | | USD | | | 7.38 | % | 07/21/23 | | | 1,000,000 | | | | 1,060,000 | (1) |

| YPF SA | | | | USD | | | 8.75 | % | 04/04/24 | | | 2,003,000 | | | | 2,311,963 | (1)(2) |

| | | | | | | | | | | | | | | | | 6,018,213 | |

| | | | | | | | | | | | | | | | | | |

| Brazil - 5.32% | | | | | | | | | | | | | | | | | |

| Cosan Luxembourg SA | | | | USD | | | 7.00 | % | 01/20/27 | | | 1,000,000 | | | | 1,040,000 | (1) |

| ESAL GmbH | | | | USD | | | 6.25 | % | 02/05/23 | | | 2,145,000 | | | | 1,966,697 | (1) |

| GTL Trade Finance Inc. | | | | USD | | | 7.25 | % | 04/16/44 | | | 1,000,000 | | | | 981,000 | (1) |

| MARB BondCo PLC | | | | USD | | | 7.00 | % | 03/15/24 | | | 655,000 | | | | 647,631 | (1) |

| Marfrig Holdings Europe BV | | | | USD | | | 8.00 | % | 06/08/23 | | | 2,000,000 | | | | 2,079,000 | (1) |

| Minerva Luxembourg SA | | | | USD | | | 6.50 | % | 09/20/26 | | | 2,000,000 | | | | 1,990,000 | (1) |

| Petrobras Global Finance BV | | | | USD | | | 8.75 | % | 05/23/26 | | | 2,252,000 | | | | 2,626,395 | |

| Rumo Luxembourg Sarl | | | | USD | | | 7.38 | % | 02/09/24 | | | 750,000 | | | | 775,313 | (1) |

| Votorantim Cimentos SA | | | | USD | | | 7.25 | % | 04/05/41 | | | 550,000 | | | | 542,850 | (1) |

| | | | | | | | | | | | | | | | | 12,648,886 | |

| | | | | | | | | | | | | | | | | | |

| Chile - 1.04% | | | | | | | | | | | | | | | | | |

| GeoPark Latin America Ltd. Agencia en Chile | | | | USD | | | 7.50 | % | 02/11/20 | | | 855,000 | | | | 863,550 | (1) |

| VTR Finance BV | | | | USD | | | 6.88 | % | 01/15/24 | | | 1,500,000 | | | | 1,599,375 | (1) |

| | | | | | | | | | | | | | | | | 2,462,925 | |

| | | | | | | | | | | | | | | | | | |

| Colombia - 0.36% | | | | | | | | | | | | | | | | | |

| Emgesa SA ESP | | | | COP | | | 8.75 | % | 01/25/21 | | | 911,000,000 | | | | 324,694 | (1) |

| Empresas Publicas de Medellin ESP: | | | | | | | | | | | | | | | | | |

| | | | | COP | | | 8.38 | % | 02/01/21 | | | 500,000,000 | | | | 176,524 | (3) |

| | | | | COP | | | 8.38 | % | 02/01/21 | | | 1,030,000,000 | | | | 363,640 | (1) |

| | | | | | | | | | | | | | | | | 864,858 | |

| | | | | | | | | | | | | | | | | | |

| Ecuador - 3.57% | | | | | | | | | | | | | | | | | |

| EP PetroEcuador via Noble Sovereign Funding I Ltd. | | | | USD | | | 6.78 | % | 09/24/19 | | | 6,250,000 | | | | 6,312,500 | (2)(4) |

| Petroamazonas EP | | | | USD | | | 4.63 | % | 02/16/20 | | | 2,338,000 | | | | 2,179,519 | (1)(2) |

| | | | | | | | | | | | | | | | | 8,492,019 | |

| | | | | | | | | | | | | | | | | | |

| Ghana - 1.25% | | | | | | | | | | | | | | | | | |

| Tullow Oil PLC: | | | | | | | | | | | | | | | | | |

| | | | | USD | | | 6.00 | % | 11/01/20 | | | 1,218,000 | | | | 1,184,505 | (3) |

| | | | | USD | | | 6.25 | % | 04/15/22 | | | 1,883,000 | | | | 1,784,142 | (3) |

| | | | | | | | | | | | | | | | | 2,968,647 | |

| | | | | | | | | | | | | | | | | | |

| Guatemala - 0.34% | | | | | | | | | | | | | | | | | |

| Comcel Trust via Comunicaciones Celulares SA | | | | USD | | | 6.88 | % | 02/06/24 | | | 750,000 | | | | 802,425 | (1) |

| | | | | | | | | | | | | | | | | | |

| India - 0.90% | | | | | | | | | | | | | | | | | |

| Vedanta Resources PLC: | | | | | | | | | | | | | | | | | |

| | | | | USD | | | 8.25 | % | 06/07/21 | | | 347,000 | | | | 371,290 | (1) |

| | | | | USD | | | 6.38 | % | 07/30/22 | | | 1,562,000 | | | | 1,562,000 | (1) |

| | | | | USD | | | 7.13 | % | 05/31/23 | | | 210,000 | | | | 216,038 | (1) |

| | | | | | | | | | | | | | | | | 2,149,328 | |

See Notes to Financial Statements.

| Semi-Annual Report | May 31, 2017 | 9 |

| Stone Harbor Emerging Markets Income Fund | Statement of Investments |

May 31, 2017 (Unaudited)

| | | Reference Rate | | Currency | | Rate | | Maturity Date | | Principal Amount/Shares* | | | Value Expressed (in USD) | |

| Indonesia - 0.44% | | | | | | | | | | | | | |

| Indika Energy Capital II Pte Ltd. | | | | USD | | | 6.88 | % | 04/10/22 | | | 1,078,000 | | | $ | 1,053,745 | (1) |

| | | | | | | | | | | | | | | | | | |

| Mexico - 8.40% | | | | | | | | | | | | | | | | | |

| Cemex SAB de CV | | | | USD | | | 7.75 | % | 04/16/26 | | | 2,000,000 | | | | 2,276,000 | (1)(2) |

| Metalsa SA de CV | | | | USD | | | 4.90 | % | 04/24/23 | | | 468,000 | | | | 469,170 | (1) |

| Mexichem SAB de CV: | | | | | | | | | | | | | | | | | |

| | | | | USD | | | 6.75 | % | 09/19/42 | | | 2,181,000 | | | | 2,355,589 | (1)(2) |

| | | | | USD | | | 5.88 | % | 09/17/44 | | | 500,000 | | | | 498,750 | (1) |

| Petroleos Mexicanos: | | | | | | | | | | | | | | | | | |

| | | | | MXN | | | 7.65 | % | 11/24/21 | | | 87,000,000 | | | | 4,418,868 | (3) |

| | | | | MXN | | | 7.47 | % | 11/12/26 | | | 98,000,000 | | | | 4,564,364 | |

| | | | | USD | | | 5.50 | % | 06/27/44 | | | 281,000 | | | | 253,153 | |

| Sixsigma Networks Mexico SA de CV | | | | USD | | | 8.25 | % | 11/07/21 | | | 2,305,000 | | | | 2,309,149 | (1)(2) |

| Southern Copper Corp. | | | | USD | | | 6.75 | % | 04/16/40 | | | 2,500,000 | | | | 2,846,875 | (2) |

| | | | | | | | | | | | | | | | | 19,991,918 | |

| | | | | | | | | | | | | | | | | | |

| South Africa - 2.77% | | | | | | | | | | | | | | | | | |

| Eskom Holdings SOC Ltd. | | | | USD | | | 7.13 | % | 02/11/25 | | | 6,258,000 | | | | 6,591,238 | (1)(2) |

| | | | | | | | | | | | | | | | | | |

| Ukraine - 0.37% | | | | | | | | | | | | | | | | | |

| Oschadbank Via SSB #1 PLC | | | | USD | | | 9.63 | % | 03/20/25 | | | 872,000 | | | | 891,402 | (3)(5) |

| | | | | | | | | | | | | | | | | | |

| Venezuela - 4.39% | | | | | | | | | | | | | | | | | |

| Petroleos de Venezuela | | | | USD | | | 6.00 | % | 05/16/24 | | | 26,445,227 | | | | 10,443,220 | (2)(3) |

| | | | | | | | | | | | | | | | | | |

| TOTAL CORPORATE BONDS | | | | | | | | | | | | | | | | 77,085,399 | |

| (Cost $75,281,536) | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| CREDIT LINKED NOTES - 3.17% | | | | | | | | | | | | | | | | | |

| Iraq - 3.17% | | | | | | | | | | | | | | | | | |

| Republic of Iraq (Counterparty: Bank of America - Merrill Lynch) | | | | JPY | | | 2.86 | % | 01/01/28 | | | 1,084,960,540 | | | | 7,541,333 | (4)(6) |

| | | | | | | | | | | | | | | | | | |

| TOTAL CREDIT LINKED NOTES | | | | | | | | | | | | | | | | 7,541,333 | |

| (Cost $10,228,133) | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

EXCHANGE TRADED FUNDS ‐ 2.35% | | | | | | | | | | | | | | | | | |

iShares® MSCI Turkey ETF | | | | USD | | | N/A | | N/A | | | 135,893 | | | | 5,598,792 | |

| | | | | | | | | | | | | | | | | | |

| TOTAL EXCHANGE TRADED FUNDS | | | | | | | | | | | | | | | | 5,598,792 | |

| (Cost $6,401,702) | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| SHORT TERM INVESTMENTS - 0.18% | | | | | | | | | | | | | | | | | |

| Money Market Mutual Funds - 0.18% | | | | | | | | | | | | | | | | | |

| State Street Institutional Liquid Reserves Fund (7-Day Yield) | | | | USD | | | 0.94 | % | N/A | | | 428,041 | | | | 428,083 | |

| | | | | | | | | | | | | | | | | | |

| TOTAL SHORT TERM INVESTMENTS | | | | | | | | | | | | | | | | 428,083 | |

| (Cost $428,083) | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

| Total Investments - 144.15% | | | | | | | | | | | | | | | | 342,918,593 | |

| (Cost $338,352,990) | | | | | | | | | | | | | | | | | |

| Liabilities in Excess of Other Assets - (44.15)% | | | | | | | | | | | | | | (105,035,728 | )(9) |

| | | | | | | | | | | | | | | | | | |

| Net Assets - 100.00% | | | | | | | | | | | | | | | $ | 237,882,865 | |

See Notes to Financial Statements.

| Stone Harbor Emerging Markets Income Fund | Statement of Investments |

May 31, 2017 (Unaudited)

| * | The principal amount/shares of each security is stated in the currency in which the security is denominated. |

| Currency Abbreviations: |

| ARS | - | Argentine Peso |

| BRL | - | Brazilian Real |

| COP | - | Colombian Peso |

| EUR | - | Euro Currency |

| IDR | - | Indonesian Rupiah |

| JPY | - | Japanese Yen |

| MXN | - | Mexican Peso |

| RUB | - | Russian Ruble |

| TRY | - | New Turkish Lira |

| USD | - | United States Dollar |

| UYU | - | Uruguayan Peso |

| ZAR | - | South African Rand |

(1) | Security exempt from registration under Rule 144A of the Securities Act of 1933. Such securities may normally be sold to qualified institutional buyers in transactions exempt from registration. Total market value of Rule 144A securities amounts to $84,360,023, which represents approximately 35.46% of net assets as of May 31, 2017. |

(2) | On May 31, 2017, securities valued at $146,437,665 were pledged as collateral for reverse repurchase agreements. |

(3) | Securities were originally issued pursuant to Regulation S under the Securities Act of 1933, which exempts securities offered and sold outside of the United States from registration. Such securities cannot be sold in the United States without either an effective registration statement filed pursuant to the Securities Act of 1933, or pursuant to an exemption from registration. As of May 31, 2017, the aggregate market value of those securities was $86,658,690, which represents approximately 36.43% of net assets. |

(4) | Floating or variable rate security. Interest rate disclosed is that which is in effect as of May 31, 2017. |

(5) | Step bond. Coupon changes periodically based upon a predetermined schedule. Interest rate disclosed is that which is in effect as of May 31, 2017. |

(6) | The level 3 assets were a result of unavailable quoted prices from an active market or the unavailability of other significant observable inputs. |

(7) | Amount represents less than 0.005% of net assets. |

(8) | Security is in default and therefore is non-income producing. |

(9) | Includes cash which is being held as collateral for derivatives. |

See Notes to Financial Statements.

| Semi-Annual Report | May 31, 2017 | 11 |

| Stone Harbor Emerging Markets Income Fund | Statement of Investments |

May 31, 2017 (Unaudited)

OUTSTANDING FORWARD FOREIGN CURRENCY CONTRACTS

| Counterparty | Foreign Currency | | Contracted Amount** | | Purchase/Sale Contract | Settlement Date | | Current Value | | | Unrealized Appreciation/ (Depreciation) | |

| J.P. Morgan Chase & Co. | ARS | | | 65,072,000 | | Sale | 06/01/17 | | $ | 4,039,021 | | | $ | 129,589 | |

| J.P. Morgan Chase & Co. | EUR | | | 12,849,600 | | Purchase | 06/09/17 | | | 14,441,853 | | | | 16,898 | |

| J.P. Morgan Chase & Co. | JPY | | | 834,862,200 | | Sale | 07/10/17 | | | 7,551,963 | | | | 9,975 | |

| | | | | | | | | | | | | | $ | 156,462 | |

| J.P. Morgan Chase & Co. | ARS | | | 65,072,000 | | Purchase | 06/01/17 | | $ | 4,039,021 | | | $ | (5,230 | ) |

| J.P. Morgan Chase & Co. | EUR | | | 12,849,600 | | Sale | 06/09/17 | | | 14,441,853 | | | | (374,381 | ) |

| J.P. Morgan Chase & Co. | EUR | | | 12,768,700 | | Sale | 07/10/17 | | | 14,374,505 | | | | (15,502 | ) |

| J.P. Morgan Chase & Co. | JPY | | | 812,430,400 | | Sale | 06/09/17 | | | 7,338,806 | | | | (37,485 | ) |

| J.P. Morgan Chase & Co. | JPY | | | 812,430,400 | | Purchase | 06/09/17 | | | 7,338,806 | | | | (9,043 | ) |

| | | | | | | | | | | | | | $ | (441,641 | ) |

| ** | The contracted amount is stated in the currency in which the contract is denominated. |

REVERSE REPURCHASE AGREEMENTS

| Counterparty | | Interest Rate | | Acquisition Date | | Amount | |

| Credit Suisse First Boston | | | 1.750 | % | 03/17/2017 | | $ | 24,999,480 | |

| Credit Suisse First Boston | | | 2.000 | % | 03/17/2017 | | | 2,273,620 | |

| Credit Suisse First Boston | | | 1.750 | % | 03/20/2017 | | | 13,826,821 | |

| Credit Suisse First Boston | | | 2.000 | % | 03/20/2017 | | | 11,381,821 | |

| Credit Suisse First Boston | | | 1.750 | % | 03/21/2017 | | | 1,676,261 | |

| Credit Suisse First Boston | | | 2.000 | % | 03/21/2017 | | | 9,751,132 | |

| Credit Suisse First Boston | | | 1.750 | % | 03/31/2017 | | | 7,920,000 | |

| Credit Suisse First Boston | | | 1.750 | % | 04/20/2017 | | | 2,641,061 | |

| Credit Suisse First Boston | | | 2.000 | % | 04/27/2017 | | | 1,510,000 | |

| Credit Suisse First Boston | | | 1.750 | % | 05/12/2017 | | | 1,897,078 | |

| Credit Suisse First Boston | | | 1.750 | % | 05/25/2017 | | | 2,157,923 | |

| Credit Suisse First Boston | | | 2.000 | % | 05/25/2017 | | | 5,467,492 | |

| J.P. Morgan Chase & Co. | | | 1.800 | % | 02/02/2017 | | | 1,821,889 | |

| J.P. Morgan Chase & Co. | | | 1.000 | % | 03/17/2017 | | | 1,276,145 | |

| J.P. Morgan Chase & Co. | | | 1.950 | % | 04/17/2017 | | | 3,599,252 | |

| J.P. Morgan Chase & Co. | | | 1.850 | % | 04/20/2017 | | | 4,661,736 | |

| J.P. Morgan Chase & Co. | | | 1.650 | % | 04/25/2017 | | | 7,940,376 | |

| J.P. Morgan Chase & Co. | | | 1.650 | % | 05/03/2017 | | | 5,631,463 | |

| | | | | | | | $ | 110,433,550 | |

All agreements can be terminated by either party on demand at value plus accrued interest.

INTEREST RATE SWAP CONTRACTS

| Pay/Receive Floating Rate | | Clearing House | | Floating Rate | | Expiration Date | | Notional Amount | | | Fixed Rate | | | Value | | | Unrealized Appreciation/(Depreciation) | |

| Receive | | Chicago Mercantile Exchange | | 3 month LIBOR | | 02/06/2025 | | $ | 26,600,000 | | | | 1.975 | % | | $ | 114,686 | | | $ | 114,686 | |

| | | | | | | | | | | | | | | | | $ | 114,686 | | | $ | 114,686 | |

| Receive | | Chicago Mercantile Exchange | | 3 month LIBOR | | 02/01/2027 | | $ | 20,400,000 | | | | 2.427 | % | | $ | (504,694 | ) | | $ | (504,694 | ) |

| Receive | | Chicago Mercantile Exchange | | 3 month LIBOR | | 02/21/2022 | | | 27,000,000 | | | | 2.051 | % | | | (293,851 | ) | | | (293,851 | ) |

| Receive | | Chicago Mercantile Exchange | | 3 month LIBOR | | 02/21/2027 | | | 13,500,000 | | | | 2.427 | % | | | (332,936 | ) | | | (332,936 | ) |

| | | | | | | | | | | | | | | | | $ | (1,131,481 | ) | | $ | (1,131,481 | ) |

See Notes to Financial Statements.

| Stone Harbor Emerging Markets Income Fund | Statement of Assets & Liabilities |

May 31, 2017 (Unaudited)

| ASSETS: | | | |

Investments, at value(1) | | $ | 342,918,593 | |

| Cash | | | 374,993 | |

| Foreign currency, at value (Cost $186,501) | | | 198,487 | |

| Unrealized appreciation on forward foreign currency contracts | | | 156,462 | |

| Deposits with brokers for interest rate swap contracts | | | 2,112,672 | |

| Deposits with brokers for forward foreign currency contracts | | | 270,000 | |

| Interest receivable | | | 8,081,494 | |

| Prepaid and other assets | | | 28,736 | |

| Total Assets | | | 354,141,437 | |

| | | | | |

| LIABILITIES: | | | | |

| Payable for reverse repurchase agreements | | | 110,433,550 | |

| Interest payable on reverse repurchase agreements | | | 319,923 | |

| Payable due to brokers for reverse repurchase agreements collateral | | | 3,060,000 | |

| Payable for investments purchased | | | 1,421,233 | |

| Unrealized depreciation on forward foreign currency contracts | | | 441,641 | |

| Variation margin payable on interest rate swap contracts | | | 94,946 | |

| Payable to adviser | | | 290,645 | |

| Payable to administrator | | | 88,333 | |

| Other payables | | | 108,301 | |

| Total Liabilities | | | 116,258,572 | |

| Net Assets | | $ | 237,882,865 | |

| | | | | |

| NET ASSETS CONSIST OF: | | | | |

| Paid‐in capital | | $ | 316,019,627 | |

| Distribution in excess of net investment income | | | (9,244,075 | ) |

| Accumulated net realized loss | | | (72,204,910 | ) |

| Net unrealized appreciation | | | 3,312,223 | |

| Net Assets | | $ | 237,882,865 | |

| | | | | |

| PRICING OF SHARES: | | | | |

| Net Assets | | $ | 237,882,865 | |

| Shares of beneficial interest outstanding (unlimited number of shares, par value of $0.001 per share authorized) | | | 15,907,664 | |

| Net assets value, offering and redemption price per share | | $ | 14.95 | |

| | | | | |

(1) Cost of Investments | | $ | 338,352,990 | |

See Notes to Financial Statements.

| Semi-Annual Report | May 31, 2017 | 13 |

| Stone Harbor Emerging Markets Income Fund | Statement of Operations |

For the Six Months Ended May 31, 2017 (Unaudited)

| INVESTMENT INCOME: | | | |

| Interest (net of foreign withholding tax of $167,519) | | $ | 13,799,445 | |

| Dividends | | | 41,398 | |

| Total Investment Income | | | 13,840,843 | |

| | | | | |

| EXPENSES: | | | | |

| Investment advisory fees | | | 1,648,547 | |

| Interest on reverse repurchase agreements | | | 830,252 | |

| Administration fees | | | 253,695 | |

| Custodian fees | | | 49,921 | |

| Professional fees | | | 82,594 | |

| Printing fees | | | 45,089 | |

| Trustee fees | | | 13,813 | |

| Transfer agent fees | | | 10,559 | |

| Insurance fees | | | 12,943 | |

| Other | | | 29,091 | |

| Total Expenses | | | 2,976,504 | |

| Net Investment Income | | | 10,864,339 | |

| | | | | |

| REALIZED AND UNREALIZED GAIN/(LOSS) ON INVESTMENTS: | | | | |

| Net realized gain/(loss) on: | | | | |

| Investments | | | 2,091,647 | |

| Credit default swap contracts | | | 1,092,128 | |

| Interest rate swap contracts | | | (340,308 | ) |

| Forward foreign currency contracts | | | 439,795 | |

| Foreign currency transactions | | | 28,463 | |

| Net realized gain | | | 3,311,725 | |

| Net change in unrealized appreciation/(depreciation) on: | | | | |

| Investments | | | 25,754,758 | |

| Credit default swap contracts | | | (1,474,561 | ) |

| Interest rate swap contracts | | | (1,315,573 | ) |

| Forward foreign currency contracts | | | (1,196,458 | ) |

| Translation of assets and liabilities denominated in foreign currencies | | | 170,789 | |

| Net change in unrealized appreciation | | | 21,938,955 | |

| Net Realized and Unrealized Gain on Investments | | | 25,250,680 | |

| Net Increase in Net Assets Resulting from Operations | | $ | 36,115,019 | |

See Notes to Financial Statements.

| Stone Harbor Emerging Markets Income Fund | Statements of Changes in Net Assets |

| | | For the Six Months Ended May 31, 2017 (Unaudited) | | | For the Year Ended November 30, 2016 | |

| OPERATIONS: | | | | | | |

| Net investment income | | $ | 10,864,339 | | | $ | 22,481,383 | |

| Net realized gain/(loss) | | | 3,311,725 | | | | (27,570,340 | ) |

| Net change in unrealized appreciation | | | 21,938,955 | | | | 26,652,520 | |

| Net increase in net assets resulting from operations | | | 36,115,019 | | | | 21,563,563 | |

| | | | | | | | | |

| DISTRIBUTIONS TO SHAREHOLDERS: | | | | | | | | |

| From net investment income | | | (17,139,852 | ) | | | (5,518,170 | ) |

| From tax return of capital | | | – | | | | (28,610,475 | ) |

| Net decrease in net assets from distributions to shareholders | | | (17,139,852 | ) | | | (34,128,645 | ) |

| | | | | | | | | |

| Net asset value of common shares issued to stockholders from reinvestment of dividends | | | 959,633 | | | | 770,031 | |

| Net increase in net assets from capital share transactions | | | 959,633 | | | | 770,031 | |

| | | | | | | | | |

| Net Increase/(Decrease) in Net Assets | | | 19,934,800 | | | | (11,795,051 | ) |

| | | | | | | | | |

| NET ASSETS: | | | | | | | | |

| Beginning of period | | | 217,948,065 | | | | 229,743,116 | |

| End of period (including distribution in excess of net investment income of $(9,244,075) and $(2,968,562)) | | $ | 237,882,865 | | | $ | 217,948,065 | |

| | | | | | | | | |

| OTHER INFORMATION: | | | | | | | | |

| Share Transactions: | | | | | | | | |

| Beginning shares | | | 15,843,749 | | | | 15,791,688 | |

| Shares issued as reinvestment of dividends | | | 63,915 | | | | 52,061 | |

| Shares outstanding ‐ end of period | | | 15,907,664 | | | | 15,843,749 | |

See Notes to Financial Statements.

| Semi-Annual Report | May 31, 2017 | 15 |

| Stone Harbor Emerging Markets Income Fund | Statement of Cash Flows |

For the Six Months Ended May 31, 2017 (Unaudited)

| CASH FLOWS FROM OPERATING ACTIVITIES: | | | |

| Net increase in net assets from operations | | $ | 36,115,019 | |

| Purchase of investment securities | | | (192,783,391 | ) |

| Proceeds from disposition of investment securities | | | 189,184,607 | |

| Net purchase of short‐term investment securities | | | (428,104 | ) |

| Net amortization of discounts and accretion of premiums | | | (1,512,598 | ) |

| Net realized (gain)/loss on: | | | | |

| Investments | | | (2,091,647 | ) |

| Net change in unrealized (appreciation)/depreciation on: | | | | |

| Investments | | | (25,754,758 | ) |

| Credit default swap contracts | | | 1,474,561 | |

| Forward foreign currency contracts | | | 1,196,458 | |

| Decrease in deposits with brokers for credit default swap contracts, interest rate swap contracts, reverse repurchase agreements | | | 897,088 | |

| Increase in interest receivable | | | (1,529,620 | ) |

| Decrease in receivable on credit default swap contracts | | | 40,000 | |

| Decrease in variation margin receivable | | | 122,624 | |

| Increase in prepaid and other assets | | | (8,511 | ) |

| Increase in payable due to brokers for reverse repurchase agreements, credit default swaps and forward foreign currency contracts | | | 2,080,000 | |

| Increase in variation margin payable on interest rate swap contracts | | | 94,946 | |

| Increase in payable to adviser | | | 25,240 | |

| Increase in payable to administrator | | | 41,680 | |

| Decrease in other payables | | | (42,774 | ) |

| Decrease in interest due on reverse repurchase agreements | | | (203,873 | ) |

| Decrease in premiums received for credit default swap contracts | | | (1,004,672 | ) |

| Net cash provided by operating activities | | | 5,912,275 | |

| | | | | |

| CASH FLOWS FROM FINANCING ACTIVITIES: | | | | |

| Cash payments for reverse repurchase agreements | | | (261,248,573 | ) |

| Cash payments from reverse repurchase agreements | | | 270,841,137 | |

| Cash distributions paid | | | (16,180,219 | ) |

| Net cash used in financing activities | | | (6,587,655 | ) |

| | | | | |

| Effect of exchange rates on cash | | | 11,190 | |

| | | | | |

| Net decrease in cash | | | (664,190 | ) |

| Cash, beginning balance | | | 1,237,670 | |

| Cash, ending balance | | $ | 573,480 | |

| | | | | |

| SUPPLEMENTAL DISCLOSURE OF CASH FLOW INFORMATION: | | | | |

| Cash paid during the period for interest expense on reverse repurchase agreements: | | $ | 1,034,125 | |

| Non‐cash financing activities not included herein consist of reinvestment of dividends and distributions of: | | $ | 959,633 | |

See Notes to Financial Statements.

| Stone Harbor Emerging Markets Income Fund | Financial Highlights |

For a share outstanding throughout the periods presented.

| | | For the Six Months Ended May 31, 2017 (Unaudited) | | | For the Year Ended November 30, 2016 | | | For the Year Ended November 30, 2015 | | | For the Year Ended November 30, 2014 | | | For the Year Ended November 30, 2013 | | | For the Year Ended November 30, 2012 | |

| Net asset value ‐ beginning of period | | $ | 13.76 | | | $ | 14.55 | | | $ | 18.56 | | | $ | 19.60 | | | $ | 23.61 | | | $ | 22.03 | |

| Income/(loss) from investment operations: | | | | | | | | | | | | | | | | | | | | | | | | |

Net investment income(1) | | | 0.68 | | | | 1.42 | | | | 2.24 | | | | 2.05 | | | | 1.67 | | | | 2.20 | |

| Net realized and unrealized gain/(loss) on investments | | | 1.59 | | | | (0.05 | ) | | | (4.09 | ) | | | (0.93 | ) | | | (3.52 | ) | | | 1.54 | |

| Total income/(loss) from investment operations | | | 2.27 | | | | 1.37 | | | | (1.85 | ) | | | 1.12 | | | | (1.85 | ) | | | 3.74 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Less distributions to common shareholders: | | | | | | | | | | | | | | | | | | | | | | | | |

| From net investment income | | | (1.08 | ) | | | (0.35 | ) | | | (0.33 | ) | | | (1.90 | ) | | | (1.90 | ) | | | (2.16 | ) |

| From net realized gains | | | – | | | | – | | | | – | | | | – | | | | (0.26 | ) | | | – | |

| From tax return of capital | | | – | | | | (1.81 | ) | | | (1.83 | ) | | | (0.26 | ) | | | – | | | | – | |

| Total distributions | | | (1.08 | ) | | | (2.16 | ) | | | (2.16 | ) | | | (2.16 | ) | | | (2.16 | ) | | | (2.16 | ) |

| Net Increase/(Decrease) in Net Asset Value | | | 1.19 | | | | (0.79 | ) | | | (4.01 | ) | | | (1.04 | ) | | | (4.01 | ) | | | 1.58 | |

| Net asset value ‐ end of period | | $ | 14.95 | | | $ | 13.76 | | | $ | 14.55 | | | $ | 18.56 | | | $ | 19.60 | | | $ | 23.61 | |

| Market price ‐ end of period | | $ | 16.70 | | | $ | 14.09 | | | $ | 12.86 | | | $ | 17.80 | | | $ | 18.55 | | | $ | 24.70 | |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Total Return - Net Asset

Value(2) | | | 16.71 | % | | | 10.87 | % | | | (9.27 | %) | | | 6.03 | % | | | (8.37 | %) | | | 17.71 | % |

Total Return - Market Price(2) | | | 27.32 | % | | | 28.45 | % | | | (16.38 | %) | | | 7.45 | % | | | (17.10 | %) | | | 21.22 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Ratios/Supplemental Data: | | | | | | | | | | | | | | | | | | | | | | | | |

| Net assets, end of period (in millions) | | $ | 238 | | | $ | 218 | | | $ | 230 | | | $ | 293 | | | $ | 309 | | | $ | 371 | |

| Ratio of expenses to average net assets | | | 2.58 | %(3)(4) | | | 2.18 | %(4) | | | 2.13 | %(4) | | | 2.07 | % | | | 1.88 | % | | | 1.83 | % |

| Ratio of net investment income to average net assets | | | 9.40 | %(3) | | | 10.03 | % | | | 14.08 | % | | | 10.42 | % | | | 7.43 | % | | | 9.59 | % |

Ratio of expenses to average managed assets(5) | | | 1.81 | %(3)(4) | | | 1.62 | %(4) | | | 1.46 | %(4) | | | 1.44 | % | | | 1.42 | % | | | 1.40 | % |

| Portfolio turnover rate | | | 55 | % | | | 105 | % | | | 89 | % | | | 97 | % | | | 157 | % | | | 122 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | |

| Borrowings at End of Period | | | | | | | | | | | | | | | | | | | | | | | | |

| Aggregate Amount Outstanding (in millions) | | $ | 110 | | | $ | 101 | | | $ | 90 | | | $ | 137 | | | $ | 120 | | | $ | 134 | |

| Asset Coverage (000s) | | $ | 3 | | | $ | 3 | | | $ | 4 | | | $ | 3 | | | $ | 4 | | | $ | 4 | |

(1) | Calculated using average shares throughout the period. |

(2) | Total investment return is calculated assuming a purchase of common share at the opening on the first day and a sale at closing on the last day of each period reported. Dividends and distributions, if any, are assumed for purposes of this calculation to be reinvested at prices obtained under the Fund’s dividend reinvestment plan. Total investment returns do not reflect brokerage commissions, if any. |

(4) | For the six months ended 2017 and years ended 2016 and 2015, includes borrowing costs of 0.72%, 0.41% and 0.30% to average net assets and 0.51%, 0.30% and 0.21% to average managed assets, respectively. |

(5) | Average managed assets represent average net assets applicable to common shares plus average amount of borrowings during the period. |

See Notes to Financial Statements.

| Semi-Annual Report | May 31, 2017 | 17 |

| Stone Harbor Emerging Markets Income Fund | Notes to Financial Statements |

May 31, 2017 (Unaudited)

1. ORGANIZATION

Stone Harbor Emerging Markets Income Fund (the “Fund”) is a closed‐end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Fund is organized as a Massachusetts business trust pursuant to an Agreement and Declaration of Trust governed by the laws of The Commonwealth of Massachusetts (the “Declaration of Trust”). The Fund’s inception date is December 22, 2010. Prior to that, the Fund had no operations other than matters relating to its organization and the sale and issuance of 4,188 shares of beneficial interest (“Common Shares”) in the Fund to the Stone Harbor Investment Partners LP (the “Adviser” or “Stone Harbor”) at a price of $23.88 per share. The Fund’s common shares are listed on the New York Stock Exchange (the “Exchange”) and trade under the ticker symbol “EDF”.

The Fund’s investment objective is to maximize total return, which consists of income on its investments and capital appreciation. The Fund will normally invest at least 80% of its net assets (plus any borrowings made for investment purposes) in emerging markets securities. Emerging markets securities include fixed income securities and other instruments (including derivatives) that are economically tied to emerging market countries, which are denominated in the predominant currency of the local market of an emerging market country or whose performance is linked to those countries’ markets, currencies, economies or ability to repay loans. A security or instrument is economically tied to an emerging market country if it is principally traded on the country’s securities markets or if the issuer is organized or principally operates in the country, derives a majority of its income from its operations within the country or has a majority of its assets within the country.

The Fund is classified as “non‐diversified” under the 1940 Act. As a result, it can invest a greater portion of its assets in obligations of a single issuer than a “diversified” fund. The Fund may therefore be more susceptible than a diversified fund to being adversely affected by any single corporate, economic, political or regulatory occurrence.

2. SIGNIFICANT ACCOUNTING POLICIES AND RISK DISCLOSURES

The following is a summary of significant accounting policies consistently followed by the Fund in the preparation of its financial statements. The Fund is considered an investment company for financial reporting purposes under generally accepted accounting principles in the United States of America (“GAAP”). The policies are in conformity with GAAP. The preparation of the financial statements in accordance with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities at the date of the financial statements and the reported amounts of income and expenses during the reporting period. Actual results could differ from those estimates.

Investment Valuation: Sovereign debt obligations, corporate bonds, and convertible corporate bonds, are generally valued at the mean between the closing bid and asked prices provided by an independent pricing service. The pricing service generally uses market models that consider trade data, yields, spreads, quotations from dealers and active market makers, credit worthiness, market information on comparable securities, and other relevant security specific information. Bank Loans are primarily valued by a loan pricing provider using a composite loan price at the mean of the bid and ask prices from one or more brokers of dealers. Credit Linked securities are generally valued using quotations from the broker through which the Fund executed the transaction. The broker’s quotation considers cash flows, default and recovery rates, and other security specific information. Equity securities for which market quotations are available are generally valued at the last sale price or official closing price on the primary market or exchange on which they trade. If on a given day, a closing price is not available on the exchange, the equity security is valued at the mean between the closing bid and ask prices, as such prices are provided by a pricing service. Publicly traded foreign government debt securities are typically traded internationally in the over the counter market and are valued at the mean between the bid and asked prices as of the close of business of that market. When prices are not readily available, or are determined not to reflect fair value, such as when the value of a security has been significantly affected by events after the close of the exchange or market on which the security is principally traded, but before the Fund calculates its net asset value, the Fund may value these investments at fair value as determined in accordance with the procedures approved by the Fund’s Board of Trustees (the “Board”). Short term obligations with maturities of 60 days or less are valued at amortized cost, which approximates market value. Exchange Traded Funds (“ETFs”) are valued at the close price on the exchange it is listed. Money market mutual funds are valued at their net asset value. Over the counter traded derivatives (primarily swaps and foreign currency options) are generally priced by an independent pricing service. OTC traded credit default swaps are valued by the independent pricing source using a mid price that is calculated based on data an independent pricing source receives from dealers. OTC traded foreign currency options are valued by an independent pricing source using mid foreign exchange rates against USD for all currencies at 4:00 p.m. EST. Derivatives which are cleared by an exchange are priced by using the last price on such exchange. Foreign currency positions including forward currency contracts are priced at the mean between the closing bid and asked prices at 4:00 p.m. Eastern time.

A three-tier hierarchy has been established to measure fair value based on the extent of use of “observable inputs” as compared to “unobservable inputs” for disclosure purposes and requires additional disclosures about these valuations measurements. Inputs refer broadly to the assumptions that market participants would use in pricing a security. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the security developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the reporting entity’s own assumptions about the assumptions market participants would use in pricing the security developed based on the best information available in the circumstances.

| Stone Harbor Emerging Markets Income Fund | Notes to Financial Statements |

May 31, 2017 (Unaudited)

The three‐tier hierarchy is summarized as follows:

| Level 1 | Unadjusted quoted prices in active markets for identical assets or liabilities that the Fund has the ability to access. |

| Level 2 | Observable inputs other than quoted prices included in Level 1 that are observable for the asset or liability, either directly or indirectly. These inputs may include quoted prices for the identical instrument on an inactive market, prices for similar instruments, interest rates, prepayment speeds, credit risk, yield curves, default rates and similar data. |

| Level 3 | Unobservable inputs for the asset or liability, to the extent relevant observable inputs are not available, representing the Fund’s own assumptions about the assumptions a market participant would use in valuing the asset or liability and would be based on the best information available. |

The following is a summary of the Fund’s investment and financial instruments based on the three‐tier hierarchy as of May 31, 2017:

Investments in Securities at Value* | | Level 1 | | | Level 2 | | | Level 3 | | | Total | |

| Sovereign Debt Obligations | | $ | – | | | $ | 250,628,927 | | | $ | – | | | $ | 250,628,927 | |

| Bank Loans | | | – | | | | – | | | | 1,636,059 | | | | 1,636,059 | |

| Corporate Bonds | | | – | | | | 77,085,399 | | | | – | | | | 77,085,399 | |

| Credit Linked Notes | | | – | | | | – | | | | 7,541,333 | | | | 7,541,333 | |

| Exchange Traded Funds | | | 5,598,792 | | | | – | | | | – | | | | 5,598,792 | |

| Short Term Investments | | | 428,083 | | | | – | | | | – | | | | 428,083 | |

| Total | | $ | 6,026,875 | | | $ | 327,714,326 | | | $ | 9,177,392 | | | $ | 342,918,593 | |

| | | | | | | | | | | | | | | | | |

Other Financial Instruments** | | | | | | | | | | | | | | | | |

| Assets | | | | | | | | | | | | | | | | |

| Forward Foreign Currency Contracts | | $ | – | | | $ | 156,462 | | | $ | – | | | $ | 156,462 | |

| Interest Rate Swap Contracts | | | – | | | | 114,686 | | | | – | | | | 114,686 | |

| | | | | | | | | | | | | | | | | |

| Liabilities | | | | | | | | | | | | | | | | |

| Forward Foreign Currency Contracts | | | – | | | | (441,641 | ) | | | – | | | | (441,641 | ) |

| Interest Rate Swap Contracts | | | – | | | | (1,131,481 | ) | | | – | | | | (1,131,481 | ) |

| Total | | $ | – | | | $ | (1,301,974 | ) | | $ | – | | | $ | (1,301,974 | ) |

| * | For detailed country descriptions, see accompanying Statement of Investments. |

| ** | Other financial instruments are derivative instruments reflected in the Statement of Investments. The derivatives shown in this table are reported at their unrealized appreciation/(depreciation) at measurement date, which represents the change in the contract's value from trade date. |

There were no transfers in or out of Levels 1 and 2 during the period ended May 31, 2017. It is the Fund’s policy to recognize transfers into and out of all levels at the end of the reporting period.

| Semi-Annual Report | May 31, 2017 | 19 |

| Stone Harbor Emerging Markets Income Fund | Notes to Financial Statements |

May 31, 2017 (Unaudited)

The following is a reconciliation of assets in which significant unobservable inputs (Level 3) were used in determining fair value:

| Investments in Securities | | Balance as of November 30, 2016 | | | Accrued discount/ premium | | | Realized Gain/ (Loss) | | | Change in Unrealized Appreciation/ (Depreciation) | | | Purchases | | | Sales Proceeds | | | Balance as of May 31, 2017 | | | Net change in unrealized appreciation/ (depreciation) included in the Statements of Operations at May 31, 2017 | |

| Bank Loans | | $ | 3,662,236 | | | $ | – | | | $ | – | | | $ | (401,177 | ) | | $ | – | | | $ | (1,625,000 | ) | | $ | 1,636,059 | | | $ | (401,177 | ) |

| Credit Linked | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Notes | | | 6,846,248 | | | | 67,809 | | | | (32,249 | ) | | | 1,091,726 | | | | – | | | | (432,201 | ) | | | 7,541,333 | | | | 1,091,726 | |

| Total | | $ | 10,508,484 | | | $ | 67,809 | | | $ | (32,249 | ) | | $ | 690,549 | | | $ | – | | | $ | (2,057,201 | ) | | $ | 9,177,392 | | | $ | 690,549 | |

All level 3 investments have values determined utilizing third‐party pricing information without adjustment.

The inputs or methodology used for valuing securities are not necessarily an indication of the risk associated with investing in those securities.

In the event a Board approved independent pricing service is unable to provide an evaluated price for a security or the Adviser believes the price provided is not reliable, securities of the Fund may be valued at fair value as described above. In these instances the Adviser may seek to find an alternative independent source, such as a broker/dealer to provide a price quote, or use evaluated pricing models similar to the techniques and models used by the independent pricing service. These fair value measurement techniques may utilize unobservable inputs (Level 3).

On at least a quarterly basis, the Adviser presents the factors considered in determining the fair value measurements and presents that information to the Board which meets at least quarterly.

Security Transactions and Investment Income: Security transactions are accounted for on a trade date basis. Interest income, adjusted for amortization of premium and accretion of discount, is recorded on the accrual basis. Dividend income is recorded on the ex‐dividend date. Foreign dividend income is recorded on the ex‐dividend date or as soon as practical after the Fund determines the existence of a dividend declaration after exercising reasonable due diligence. If applicable, any foreign capital gains taxes are accrued, net of unrealized gains, and are payable upon the sale of such investments. The cost of investments sold is determined by use of the specific identification method. To the extent any issuer defaults on an expected interest payment, the Fund’s policy is to generally halt any additional interest income accruals and consider the realizability of interest accrued up to the date of default.

Foreign Currency Translation: The books and records of the Fund are maintained in U.S. dollars. Investment valuations and other assets and liabilities initially expressed in foreign currencies are converted each business day into U.S. dollars based upon current exchange rates. Prevailing foreign exchange rates may generally be obtained at the close of the NYSE (normally 4:00 p.m. Eastern time).

The portion of realized and unrealized gains or losses on investments due to fluctuations in foreign currency exchange rates is not separately disclosed and is included in realized and unrealized gains or losses on investments, when applicable.

Foreign Securities: The Fund may directly purchase securities of foreign issuers. Investing in securities of foreign issuers involves special risks not typically associated with investing in securities of U.S. issuers. The risks include possible revaluation of currencies, the ability to repatriate funds, less complete financial information about companies and possible future adverse political and economic developments. Moreover, securities of many foreign issuers and their markets may be less liquid and their prices more volatile than those of securities of comparable U.S. issuers.

Credit Linked Notes: The Fund may invest in credit linked notes to obtain economic exposure to high yield, emerging markets or other securities. Investments in a credit linked note typically provide the holder with a return based on the return of an underlying reference instrument, such as an emerging market bond. Like an investment in a bond, investments in credit linked securities represent the right to receive periodic income payments (in the form of distributions) and payment of principal at the end of the term of the security. In addition to the risks associated with the underlying reference instrument, an investment in a credit linked note is also subject to liquidity risk, market risk, interest rate risk and the risk that the counterparty will be unwilling or unable to meet its obligations under the note.

| Stone Harbor Emerging Markets Income Fund | Notes to Financial Statements |

May 31, 2017 (Unaudited)

Loan Participations and Assignments: The Fund may invest in loans arranged through private negotiation between one or more financial institutions. The Fund’s investment in any such loan may be in the form of a participation in or an assignment of the loan. In connection with purchasing participations, the Fund generally will have no right to enforce compliance by the borrower with the terms of the loan agreement relating to the loan, or any rights of set‐off against the borrower, and the Fund may not benefit directly from any collateral supporting the loan in which it has purchased the participation.

While some loans are collateralized and senior to an issuer’s other debt securities, other loans may be unsecured and/or subordinated to other securities. Some senior loans, such as bank loans, may be illiquid and generally tend to be less liquid than many other debt securities.

The Fund assumes the credit risk of the borrower, the lender that is selling the participation and any other persons interpositioned between the Fund and the borrower. In the event of the insolvency of the lender selling the participation, the Fund may be treated as a general creditor of the lender and may not benefit from any set‐off between the lender and the borrower. Loans may not be considered “securities”, and purchasers, such as the Fund, therefore may not be entitled to rely on the anti‐fraud protections of the federal securities laws.

Segregation and Collateralization: In cases in which the 1940 Act and the interpretive positions of the U.S. Securities and Exchange Commission (“SEC”) require that the Fund either delivers collateral or segregates assets in connection with certain investments (e.g., foreign currency exchange contracts, securities with extended settlement periods, and swaps) or certain borrowings (e.g., reverse repurchase agreements), the Fund will segregate collateral or designate on its books and record cash or other liquid securities having a value at least equal to the amount that is required to be physically segregated for the benefit of the counterparty. Furthermore, based on requirements and agreements with certain exchanges and third party broker‐dealers, each party has requirements to deliver/deposit cash or securities as collateral for certain investments. Cash collateral that has been pledged to cover obligations of the Fund and cash collateral received from the counterparty, if any, is reported separately on the Statement of Assets and Liabilities as “Deposits with brokers” or “Payable due to brokers”, respectively. Securities collateral pledged for the same purpose is noted on the Statement of Investments.

Leverage: The Fund may borrow from banks and other financial institutions and may also borrow additional funds by entering into reverse repurchase agreements or the issuance of debt securities (collectively, “Borrowings”) in an amount that does not exceed 33 1/3% of the Fund’s Managed Assets (defined in Note 4) immediately after such transactions. It is possible that following such Borrowings, the assets of the Fund will decline due to market conditions such that this 33 1/3% limit will be exceeded. In that case, the leverage risk to Common Shareholders will increase.

In a reverse repurchase agreement, the Fund delivers a security in exchange for cash to a financial institution, the counterparty, with a simultaneous agreement to repurchase the same or substantially the same security at an agreed upon price and date. The Fund is entitled to receive principal and interest payments, if any, made on the security delivered to the counterparty during the term of the agreement. Cash received in exchange for securities delivered plus accrued interest payments to be made by the Fund to counterparties are reflected as a liability on the Statement of Assets and Liabilities. Interest payments made by the Fund to counterparties are recorded as a component of interest expense on the Statement of Operations. In periods of increased demand for the security, the Fund may receive a fee for use of the security by the counterparty, which may result in interest income to the Fund. The Fund will segregate assets determined to be liquid to cover its obligations under reverse repurchase agreements. As all agreements can be terminated by either party on demand, face value approximates fair value at May 31, 2017. This fair value is based on Level 2 inputs under the three‐tier fair valuation hierarchy described above. For the period ended May 31, 2017, the average amount of reverse repurchase agreements outstanding was $98,841,050, at a weighted average interest rate of 1.68%.

Emerging Market Risk: Emerging market countries often experience instability in their political and economic structures. Government actions could have a great effect on the economic conditions in these countries, which can affect the value and liquidity of the assets of a Fund. Specific risks that could decrease a Fund’s return include seizure of a company’s assets, restrictions imposed on payments as a result of blockages on foreign currency exchanges, expropriation, confiscatory taxation and unanticipated social or political occurrences. In addition, the ability of an emerging market government to make timely payments on its debt obligations will depend on the extent of its reserves, interest rate fluctuations and access to international credit and investments. A country with non‐diversified exports or that relies on specific imports will be subject to a greater extent to fluctuations in the pricing of those commodities. Failure to generate adequate earnings from foreign trade would make it difficult for an emerging market country to service foreign debt. Disruptions resulting from social and political factors may cause the securities markets of emerging market countries to close. If this were to occur, the liquidity and value of a Fund’s assets invested in corporate debt obligations of emerging market companies would decline. Foreign investment in debt securities of emerging market countries may be restricted or controlled to varying degrees. These restrictions can limit or preclude foreign investment in debt securities of certain emerging market countries. In addition, certain emerging market countries may also restrict investment opportunities in issuers in industries deemed important to national interests.

Interest Rate Risk: Changes in interest rates will affect the value of the Fund’s investments. In general, as interest rates rise, bond prices fall, and as interest rates fall, bond prices rise. Interest rate risk is generally greater for funds that invest a significant portion of their assets in high yield securities. However, funds that generally invest a significant portion of their assets in higher‐rated fixed income securities are also subject to this risk. The Fund also faces increased interest rate risk if it invests in fixed income securities paying no current interest (such as zero coupon securities and principal‐only securities), interest‐only securities and fixed income securities paying non‐cash interest in the form of other securities.

| Semi-Annual Report | May 31, 2017 | 21 |

| Stone Harbor Emerging Markets Income Fund | Notes to Financial Statements |

May 31, 2017 (Unaudited)

Liquidity Risk: Liquidity risk exists when particular investments are difficult to purchase or sell at the time that the Fund would like or at the price that the Fund believes such investments are currently worth. Certain of the Fund’s investments may be illiquid. Illiquid securities may become harder to value, especially in changing markets. The Fund’s investments in illiquid securities may reduce the returns of the Fund because it may be unable to sell the illiquid securities at an advantageous time or price or possibly require the Fund to dispose of other investments at unfavorable times or prices in order to satisfy its obligations, which could prevent the Fund from taking advantage of other investment opportunities. Additionally, the market for certain investments may become illiquid under adverse market or economic conditions independent of any specific adverse changes in the conditions of a particular issuer. Derivatives, securities that involve substantial interest rate or credit risk and bank loans tend to involve greater liquidity risk. In addition, liquidity risk tends to increase to the extent the Fund invests in securities whose sale may be restricted by law or by contract, such as Rule 144A and Regulation S securities.

Foreign Investment Risk: The securities markets of many foreign countries are relatively small, with a limited number of companies representing a small number of industries. Additionally, issuers of foreign (non‐U.S.) securities are usually not subject to the same degree of regulation as U.S. issuers. Reporting, accounting, auditing and custody standards of foreign countries differ, in some cases significantly, from U.S. standards. Global economies and financial markets are becoming increasingly interconnected, and conditions and events in one country, region or financial market may adversely impact issuers in a different country, region or financial market. Also, nationalization, expropriation or confiscatory taxation, currency blockage, political changes or diplomatic developments could adversely affect the Fund’s investments in a foreign country. In the event of nationalization, expropriation or other confiscation, the Fund could lose its entire investment in foreign (non‐U.S.) securities. Adverse conditions in a certain region can adversely affect securities of other countries whose economies appear to be unrelated. Foreign (non‐U.S.) securities may also be less liquid and more difficult to value than securities of U.S. issuers.

Leverage Risk: Leverage creates risks for Common Shareholders, including the likelihood of greater volatility of NAV per share and market price of, and dividends paid on, the Common Shares. There is a risk that fluctuations in the interest rates on any Borrowings held by the Fund may adversely affect the return to the Common Shareholders. If the income from the securities purchased with the proceeds of leverage is not sufficient to cover the cost of leverage, the return on the Fund will be less than if leverage had not been used, and therefore the amount available for distribution to the Common Shareholders as dividends and other distributions will be reduced.

The Fund may choose not to use leverage at all times. The amount and composition of leverage used may vary depending upon a number of factors, including economic and market conditions in the relevant emerging market countries, the availability of relatively attractive investment opportunities not requiring leverage and the costs and risks that the Fund would incur as a result of leverage.

Credit and Market Risk: The Fund invests in high yield and emerging market instruments that are subject to certain credit and market risks. The yields of high yield and emerging market debt obligations reflect, among other things, perceived credit and market risks. The Fund’s investment in securities rated below investment grade typically involves risks not associated with higher rated securities including, among others, greater risk related to timely and ultimate payment of interest and principal, greater market price volatility and less liquid secondary market trading. The consequences of political, social, economic or diplomatic changes may have disruptive effects on the market prices of investments held by the Fund. The Fund’s investment in non‐dollar denominated securities may also result in foreign currency losses caused by devaluations and exchange rate fluctuations. Investments in derivatives are also subject to credit and market risks.

ETFs and Other Investment Companies Risk: The Fund may invest in an ETF or other investment company. The Fund will be subject to the risks of the underlying securities in which the other investment company invests. In addition, as a shareholder in an ETF or other investment company, the Fund will bear its ratable share of that investment company's expenses, and would remain subject to payment of the Fund's investment management fees with respect to the assets so invested. Common Shareholders would therefore be subject to duplicative expenses to the extent the Fund invests in other investment companies. In addition, these other investment companies may use leverage, in which case an investment would subject the Fund to additional risks associated with leverage. The Fund may invest in other investment companies for which the Adviser or an affiliate serves as investment manager or with which the Adviser is otherwise affiliated. The relationship between the Adviser and any such other investment company could create a conflict of interest between the Adviser and the Fund.

In addition to the risks related to investing in investment companies generally, investments in ETFs involve the risk that the ETF's performance may not track the performance of the index or markets the ETF is designed to track. In addition, ETFs often use derivatives to track the performance of the relevant index and, therefore, investments in those ETFs are subject to the same derivatives risks discussed below.

Distributions to Shareholders: The Fund intends to make a level dividend distribution each month to Common Shareholders. The level dividend rate may be modified by the Board of Trustees from time to time. Any net capital gains earned by the Fund are distributed at least annually. Income and capital gain distributions are determined in accordance with federal income tax regulations, which may differ from GAAP. Distributions to shareholders are recorded by the Fund on the ex‐dividend date. A portion of the Fund’s distributions made for a taxable year may be recharacterized as a return of capital to shareholders. This may occur, for example, if the Fund’s distributions exceed its “earnings and profits” for the taxable year or because certain foreign currency losses may reduce the Fund’s income. This recharacterization may be retroactive. A return of capital will generally not be taxable, but will reduce a shareholder’s basis in his or her Fund shares and therefore result in a higher gain or lower loss when the shareholder sells the shares.

| Stone Harbor Emerging Markets Income Fund | Notes to Financial Statements |

May 31, 2017 (Unaudited)

Federal and Other Taxes: No provision for income taxes is included in the accompanying financial statements, as the Fund intends to distribute to shareholders all taxable investment income and realized gains and otherwise comply with Subchapter M of the Code applicable to regulated investment companies.

The Fund evaluates tax positions taken (or expected to be taken) in the course of preparing the Fund’s tax returns to determine whether these positions meet a “more‐likely‐than‐not” standard that, based on the technical merits, have more than a 50 percent likelihood of being sustained by a taxing authority upon examination. A tax position that meets the “more‐likely‐than‐not” recognition threshold is measured to determine the amount of benefit to recognize in the financial statements.

As of and during the year ended November 30, 2016, the Fund did not have a liability for any unrecognized tax benefits. The Fund files U.S. federal, state, and local tax returns as required. The Fund’s tax returns are subject to examination by the relevant tax authorities until expiration of the applicable statute of limitations which is generally three years after the filing of the tax return for federal purposes and four years for most state returns. Tax returns for open years have incorporated no uncertain tax positions that require a provision for income taxes.

3. DERIVATIVE INSTRUMENTS

Risk Exposure and the Use of Derivative Instruments: The Fund’s investment objectives not only permit the Fund to purchase investment securities, they also allow the Fund to enter in various types of derivatives contracts. In doing so, the Fund will employ strategies in differing combinations to permit it to increase, decrease or change the level or types of exposure to market factors. Central to those strategies are features inherent to derivatives that may make them more attractive for this purpose than equity or debt securities: they require little or no initial cash investment; they can focus exposure on only certain selected risk factors; and they may not require the ultimate receipt or delivery of the underlying security (or securities) to the contract. This may allow the Fund to pursue its objectives more quickly and efficiently than if the Fund were to make direct purchases or sales of securities capable of effecting a similar response to market factors.

The Fund’s use of derivatives can result in losses due to unanticipated changes in the risk factors described in Note 2 and the overall market. In instances where the Fund is using derivatives to decrease, or hedge, exposures to market risk factors for securities held by the Fund, there are also risks that those derivatives may not perform as expected resulting in losses for the combined or hedged positions.