Intelicoat Technologies Image Products Matthews Inactive

Filed: 7 Dec 11, 12:00am

Filed pursuant to Rule 424(b)(3)

Registration No. 333-178048

PROSPECTUS

EXOPACK HOLDING CORP.

Offer to exchange $235,000,000 aggregate principal amount of

10% Senior Notes due 2018

which have been registered under the Securities Act

for

$235,000,000 aggregate principal amount of

10% Senior Notes due 2018

which have not been registered under the Securities Act

The exchange offer will expire at 5:00 p.m., New York City

time, on January 10, 2012, unless we extend it.

Key Terms of The Exchange Offer

| • | We are offering to exchange registered 10% Senior Notes due 2018 (“new notes”) for all of our old unregistered 10% Senior Notes due 2018 (“old notes”). The old notes and the new notes are collectively referred to herein as the “notes.” The new notes will be guaranteed on a senior unsecured basis by all of our existing and future domestic restricted subsidiaries. All references to the notes include references to the related guarantees. |

| • | The terms of the new notes to be issued in this exchange offer will be identical in all material respects to the terms of the old notes, except that the registration rights and related liquidated damages provisions, and the transfer restrictions applicable to the old notes, will not be applicable to the new notes. |

| • | The Bank of New York Mellon Trust Company, N.A. is serving as the exchange agent. If you wish to tender your old notes, you must complete, execute and deliver, among other things, a letter of transmittal to the exchange agent no later than 5:00 p.m., New York City time, on the expiration date. |

| • | You may withdraw tendered old notes at any time prior to the expiration of the exchange offer. |

| • | Any old notes not validly tendered will remain subject to existing transfer restrictions. |

| • | The exchange of the old notes for the new notes pursuant to the exchange offer will not be a taxable event for United States federal income tax purposes. See “United States Federal Income Tax Considerations.” |

| • | We will not receive any proceeds from the exchange offer. |

| • | The new notes will not be listed on any securities exchange or included in any automated quotation system. |

See “Risk Factors” on page 21 of this prospectus for a discussion of risks that you should consider before participating in the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or the accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is December 6, 2011

| PAGE | ||||

| 1 | ||||

| 3 | ||||

| 21 | ||||

| 34 | ||||

| 42 | ||||

| 42 | ||||

| 43 | ||||

| 47 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 50 | |||

| 70 | ||||

| 71 | ||||

| 87 | ||||

| 90 | ||||

| 105 | ||||

| 105 | ||||

| 107 | ||||

| 110 | ||||

| 151 | ||||

| 152 | ||||

| 152 | ||||

| 152 | ||||

| 153 | ||||

| F-1 | ||||

Each broker-dealer that receives new notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of the new notes it receives. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act of 1933, as amended (the “Securities Act”). This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of new notes received in exchange for old notes where such old notes were acquired by the broker-dealer as a result of market-making activities or other trading activities. We have agreed that we will promptly provide each broker-dealer holding old notes with such number of copies of this prospectus, in conformity in all material respects with the requirements of the Securities Act and the Trust Indenture Act of 1939, as amended, and the rules and regulations thereunder, as such broker-dealer may request prior to the expiration of the period beginning when new notes are first issued in this exchange offer and ending upon the earlier of the expiration of the 180th day after this exchange offer has been completed or such time as such broker-dealers no longer own any notes.

i

This prospectus may contain forward-looking statements. These statements include, but are not limited to, any statement that may predict, forecast, indicate or imply future results, performance, achievements or events. These forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or will be important factors that could cause our actual results to differ materially from those indicated in these statements. We believe that these factors include but are not limited to the following:

| • | intense competition in the flexible packaging markets may adversely affect our operating results; |

| • | the profitability of our business depends on the price and availability of polyethylene resin and paper, two of our principal raw materials, and our ability to pass on polyethylene resin and paper price increases to customers; |

| • | our business is affected by global economic factors including risks associated with a recession and our customers’ access to credit; |

| • | we are subject to the risk of loss resulting from nonpayment or nonperformance by our customers; |

| • | financial difficulties and related problems at our vendors, suppliers and other business partners could result in a disruption to our operations and have a material adverse effect on our business; |

| • | fluctuations in the equity market may adversely affect our pension plan assets and our future cash flows; |

| • | energy price increases could adversely affect the results of our operations; |

| • | we may be unable to adapt to technological advances in the packaging industry; |

| • | we may be unable to protect our proprietary technology from infringement; |

| • | our operations could expose us to substantial environmental costs and liabilities; |

| • | we may not be able to obtain additional funding, if needed; |

| • | we may, from time to time, experience problems in our labor relations; |

| • | we are subject to risks related to our internal operations; |

| • | loss of third-party transportation providers upon whom we depend or increases in fuel prices could increase our costs or cause a disruption in our operations; |

| • | unexpected equipment failures may lead to production curtailments or shutdowns; |

| • | an affiliate of Sun Capital controls us and may have conflicts of interest with us in the future; |

| • | we are required to comply with Section 404 of the Sarbanes-Oxley Act, and there can be no assurance that we will be able to establish, maintain and apply effective internal control over financial reporting under applicable SEC rules promulgated under Section 404; |

| • | we may be adversely affected by interest rate changes; |

| • | numerous other factors over which we may have limited or no control may affect our performance and profitability; |

| • | our substantial indebtedness could adversely affect our financial health and prevent us from fulfilling our obligations under the notes and New Term Loan Facility (as defined below), obtaining financing in the future and reacting to changes in our business; |

| • | despite current indebtedness levels, we and our subsidiaries may still be able to incur substantially more debt and this could further exacerbate the risks described above; |

| • | to service our indebtedness, we will require a significant amount of cash and our ability to generate cash depends on many factors beyond our control; |

1

| • | the indenture governing the notes and the credit agreements governing our Senior Credit Facility (as defined below) and New Term Loan Facility will restrict our operations; |

| • | we may not successfully complete the integration of Exopack Meat, Cheese and Specialty (“EMCS”); |

| • | we may be unable to realize the expected cost savings and other synergies from the EMCS acquisition into our business and operations; |

| • | we may be unable to successfully or timely complete the transition of equipment and business related to the EMCS acquisition to our existing facilities; |

| • | it is uncertain when our search for a new chief executive officer and chief financial officer will be completed, and a prolonged search for these positions, or the loss of other key individuals could disrupt our operations and harm our business; and |

| • | we are conducting a search for a new chief executive officer and a new chief financial officer, and until these positions are filled there may be an adverse effect on the performance of these functions. |

You can often identify these and other forward-looking statements by the use of the words such as “may,” “will,” “could,” “would,” “should,” “expects,” “plans,” “anticipates,” “estimates,” “intends,” “potential,” “projected,” “continue,” or the negative of such terms, or other comparable terminology. Forward-looking statements also include the assumptions underlying or relating to any of the foregoing statements.

These statements are based on current expectations and assumptions regarding future events and business performance and involve known and unknown risks, uncertainties and other factors that may cause industry trends or our actual results, level of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these statements.

The foregoing factors should not be construed as exhaustive and should be read in conjunction with the other cautionary statements that are included in this prospectus. For a more detailed discussion of the principal factors that could cause actual results to be materially different, you should read our risk factors included below under “Risk Factors.”

Although we believe that expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. We will assume no obligation to update any of the forward-looking statements after the date of this prospectus to conform these statements to actual results or changes in our expectations, except as required by law. You should not place undue reliance on these forward-looking statements, which apply only as of the date of this prospectus.

2

The following summary highlights the information contained elsewhere in this prospectus. Because this is only a summary, it does not contain all of the information that may be important to you. For a more complete understanding of this exchange offer, we encourage you to read this entire prospectus and the documents to which we refer you. You should read the following summary together with the more detailed information and consolidated financial statements and the notes to those statements included elsewhere in this prospectus.

In this prospectus, “EHC,” “Company,” “we,” “our,” and “us” refer to Exopack Holding Corp. With respect to descriptions of our business contained in this prospectus, such terms refer to Exopack Holding Corp. and our subsidiaries.

Our Company

We are a provider of flexible packaging, film products, and specialty substrates based in North America and Europe. We design, manufacture and supply plastic and paper-based flexible packaging, film products and precision coated substrates to approximately 1,200 customers in a variety of industries, including the food, medical, pet food, chemicals, beverages, personal care and hygiene, lawn and garden and building materials industries, among others. We have 18 manufacturing facilities in the United States, Canada and the United Kingdom and one distribution warehouse in China. We provide packaging and films products for many of the world’s most well-known brands. Our primary strategy is to use a technologically advanced manufacturing platform coupled with excellent customer service in order to help our customers distinguish their brands and improve product shelf life.

The many products that we produce can be divided into four separate segments: (i) pet food and specialty packaging, (ii) consumer food and specialty packaging, (iii) performance packaging and (iv) coated products. Typically, customers decide whether to use paper or plastic packaging on the basis of end-use application, presentation considerations and the demands of particular filling processes. Such decisions may also be influenced by the relative importance of package size, sealability, shelf-appeal, durability, functionality and printability. Our pet food and specialty packaging segment produces products used in applications such as pet food, lawn and garden, charcoal, and popcorn packaging. The consumer food and specialty packaging segment produces products used in applications such as fresh meat, natural cheese and dairy products, beverage, frozen foods, confectionary, breakfast foods, personal care and unprinted films. The performance packaging segment produces products used in applications such as building materials, chemicals, agricultural products and food ingredient packaging. The coated products segment produces precision-coated films, foils, fabrics and other substrates for imaging, electronics, medical and optical technologies.

We offer our diverse array of paper and plastic packaging products and precision-coated substrates, including multi-wall bags, printed and laminated roll stock, stand-up pouches and coated films, in the following end markets, among others:

| • | Food |

| • | Medical |

| • | Pet Food |

| • | Personal Care and Hygiene |

| • | Chemicals |

| • | Beverages |

| • | Cheese and Dairy |

3

| • | Fresh Meat |

| • | Lawn & Garden Products |

| • | Building Materials |

| • | Electronics |

Industry Overview

The flexible packaging and coating industry manufactures a broad range of consumer and industrial packaging for use in diverse end markets. Multi-layer flexible polymer/paper structures and barrier laminates are used for food, medical, agricultural and personal care products, as well as other consumer and industrial uses, and are used in a variety of products that generally include plastic film, paper or a combination of the two.

Plastic films, which account for the largest share of market demand in the industry, have been increasingly popular in recent years and offer strong barrier performance, re-closeability and outstanding print characteristics. Plastic has been used to reduce packaging weight when switching from rigid packaging applications. Paper products are versatile and support vibrant graphics and color schemes, while offering both durability and freshness retention. Moreover, paper products are increasingly appealing to consumers who place emphasis on environmental concerns and value the ability to use renewable resources and the option to recycle such products.

According to the Flexible Packaging Association (“FPA”), the domestic flexible packaging market accounted for an estimated $25.5 billion in sales in 2010, and the market is expected to experience annual growth rates of approximately 3%. The flexible packaging industry is highly fragmented, as demonstrated by the number of flexible packaging manufacturers operating in North America, currently estimated at over 400.

Our Strategy

We intend to enhance our market position and operating results by leveraging our customer relationships, efficiently managing our procurement cost structure, maintaining our commitment to state-of-the-art production facilities and technologies, capitalizing on opportunities to realize operating efficiencies and selectively pursuing strategic acquisitions.

Leveraging Our Customer Relationships. We enjoy long-standing relationships with many of our customers. One of our top priorities has been to integrate our product offerings into our customers’ operations by providing high quality, cost-effective products that are tailored to our customers’ specific needs. We seek to offer enhanced service and support, anticipating customer needs and providing value-added solutions to customer problems. We have undertaken joint product development efforts with many of our customers, allowing us to manage our research and development expenditures and increase incentives for customers to remain loyal to us over the long term. Our formation through the consolidation of Cello-Foil Products, Inc., The Packaging Group and Exopack, LLC and subsequent acquisitions have provided us with additional opportunities to cross-sell our products to our customer base.

Efficiently Managing Our Procurement Cost Structure. We have multiple supply sources for paper, plastics and films and have maintained the majority of those relationships for over a decade. As one of the largest flexible packaging converters in the United States, we believe we are often able to use our increased size to secure volume pricing from our suppliers and expand our procurement reach.

We are currently focusing on efficiently managing the costs of raw materials, packaging and freight. To further these objectives, we are working to develop highly efficient procurement functions and innovative approaches to raw materials sourcing, including global sourcing arrangements. We continue to leverage purchasing across our organization and standardize the use of raw materials across facilities.

4

Continuing to Focus on Enhancing Our Product Mix Through State-of-the-Art Technology. Our production facilities have allowed us to improve our production flexibility and dependability. We use high-performance machinery and a broad range of state-of-the-art technologies. Recent investments include printing presses that can print up to ten colors, high efficiency pasted valve machines, co-extruded blown film extruders, heat sealable paper bag line and stand-up re-sealable pouch machines. We believe that a key factor that differentiates our services from those of our competitors is the state-of-the-art graphics and technical capabilities of our Customer Resource Center, located at our Spartanburg, South Carolina headquarters. In addition, to enhance the convenience that we strive to provide to our customers, we have continued to add features such as handles and advanced package re-closure systems.

We view our array of facilities and ongoing commitment to state-of-the-art technology as key drivers in our ability to provide an exceptional combination of service, performance and value. Strategically, we plan to grow our revenue base by providing customized packaging solutions and benefiting from an overall trend toward flexible, rather than rigid, packaging.

Realizing Operational Efficiencies and Synergies. We strive to cultivate safe, efficient manufacturing by focusing on quality and operational practices. Our efficiency initiatives include establishing common operating and reporting procedures, streamlining production, optimizing asset utilization, rationalizing product mix and making strategic capital expenditures.

Selectively Pursue Strategic Acquisition Opportunities. In addition to the growth in revenue, earnings and cash flow we are targeting through organic volume growth and cost-structure management, we believe that we are well positioned as a platform for additional acquisition opportunities. We believe that we have demonstrated the ability to successfully integrate acquisitions and achieve operating efficiencies. We intend to pursue a selective and disciplined acquisition strategy that will broaden our customer base and strengthen our end-market penetration, provide opportunities for manufacturing and corporate overhead cost savings, allow us to leverage our existing procurement platform and enhance our production and technological capabilities.

Our Strengths

We believe we have the following competitive strengths:

Established Relationships with Blue Chip Customers. We maintain strong relationships with a diverse base of customers in a wide array of businesses. We have approximately 1,200 customers, and even with recent market consolidations, most of our customers individually represent less than 5% of our net sales. No customer exceeded 10% of our net sales for 2010.

Cost Savings Opportunities. Part of our strategy consists of combining the functions shared by our acquired businesses and extracting synergies. We believe that we can achieve cost savings by in-sourcing manufacturing of certain films and other materials, improving procurement (through increased purchasing volume and efficiencies of scale in freight), and eliminating operational redundancies (through reducing headcount, restructuring certain facilities and consolidating information technology programs). For example, in 2008, we moved the Exopack Advanced Coatings (“EAC”) business operations conducted at Intelicoat’s South Hadley, Massachusetts facility to the EAC facility we acquired in Matthews, North Carolina. Similarly, we integrated the Whitby, Canada plant we purchased from DuPont into the Exopack business. The integration of the Whitby facility allowed us to produce certain films that we previously purchased from outside vendors. We also now process certain print jobs that were outsourced by the Exopack Performance Films (“EPF”) business.

5

Position within the Industry. According to the FPA, the size of the domestic flexible packaging industry was estimated to be approximately $25.5 billion in annual sales in 2010, of which “value-added” products accounted for an estimated $19.7 billion in sales. The “value-added” segment does not include retail shopping bags, consumer storage bags and wraps, or trash bags.

The flexible packaging market is highly fragmented, with over 400 manufacturers operating in North America. A significant number of these manufacturers are relatively small, with the average flexible packaging converter generating annual sales of approximately $60.0 million to $65.0 million in 2009, according to the FPA. We believe that, as a result of customer consolidation, certain sectors and customers are underserved by smaller manufacturers. We believe we can take advantage of this market opportunity.

We believe there are several key drivers in the industry, including: the growing importance of convenience, functionality and shelf-appeal; technological developments; a trend toward flexible rather than rigid packaging; globalization; raw material cost volatility; the impact of sustainable packaging; and pressures to consolidate. We believe we are well positioned to compete and expand our business due to our broad product mix, substrate expertise, customer service, award winning printing technology, global presence and technologically advanced manufacturing capabilities. Our global presence and capabilities are supported by Global Packaging Linx (“GPL”).

GPL is a strategic initiative we developed to leverage relationships with global packaging manufacturers. We believe GPL is a unique initiative in our industry. The goal of GPL is to procure flexible packaging solutions from a select network of global packaging manufacturers when it provides value to our customers or potential customers. We aim to take advantage of GPL while maintaining our standards for quality, service and innovation. Through GPL, we believe we will be able to further identify and develop opportunities within our multinational customer base that will allow us to provide value through our own mix of domestic converted packaging solutions, as well as through offshore packaging technologies provided by our global alliance partners.

As part of the GPL initiative, we signed a joint venture agreement with Lebanon-based packaging manufacturer INDEVCO Group (“INDEVCO”) to manufacture co-extruded polyethylene film in the Middle East under the name CEDEX Plastics Flexible Packaging (“CEDEX”). The joint venture represents the strengthening of a long-term relationship between Exopack and INDEVCO to support global customers. During 2010, the joint venture brought the first cost-effective films from the Middle East to customers in North America. We intend to expand our relationship with INDEVCO to take advantage of the new polymer manufacturing capacity coming on line in the Middle East, which is primarily due to the increased economic advantage of ethylene production in this region of the world. The CEDEX film is distributed by us as part of our family of film products.

Highly Experienced Management Team. We have an experienced management team with an average of more than 20 years of industry experience. Tom Vale, our President and Chief Operating Officer, who is also currently serving as our Interim Chief Executive Officer, has over 15 years of management experience, during which he served as President and Chief Executive Officer of Deluxe Media Services, and Executive Vice President and Chief Financial Officer of Resorts USA. Mr. Vale has served as our Chief Operating Officer since he joined our Company in 2008. We also benefit from highly-motivated and experienced managers in key functional areas, including sales and marketing, operations, procurement and accounting and finance. Each of our key business unit managers has significant experience in the packaging and related industries.

Ability to Pass Through Raw Material Price Increases Within a Short Period of Time. Although most of our customers have contracts that prevent us from passing through raw material price increases immediately, historically, we have been able to pass through raw material price increases to our customers within a relatively short period of time, maintaining a relatively stable spread between selling price and raw material purchase price. More than 75% of our sales volume generated is under agreements that typically allow us to pass through raw material price increases/decreases every 30 to 90 days to customers that purchase plastic-based packaging

6

products and every 90 to 180 days to customers that purchase paper-based packaging products. The remainder of our business is transactional, which permits us to pass through price increases/decreases to customers on an order-by-order basis.

Diversified Raw Material Supplier Base. We have relationships with multiple vendors in our pet food and specialty, consumer food and specialty, performance and coated products segments. We currently purchase our raw materials from more than 10 paper suppliers, more than 12 plastics suppliers, and more than 15 suppliers to our coated products segment. We are generally able to switch suppliers without sacrificing quality. We do not believe we are dependent on any single supplier to operate efficiently and profitably.

Diverse Mix of Paper Packaging, Plastic Packaging and Coated Products. We offer a diverse array of plastic packaging, paper packaging, films and coated products. We believe that we are well positioned to meet customer needs in these three principal sectors. We believe we offer a high quality and diversified product line. Typically, our flexible packaging products are customized to fit particular customer specifications. We believe the multi-wall construction capabilities of our paper packaging segment are among the best in the industry. Our paper packaging products include a wide range of weights, run volumes and end-use applications, such as pinch bags, two- and three-ply pasted valve bags, sewn-open-mouth bags, self-opening sacks and specialty bags, among other products. Our plastic packaging and film products consist of a variety of film structures, printing, EB treatments and a number of converting styles. Our plastic packaging and films products include barrier films, high-clarity printed shrink films, shipping sacks, quad seal bags, stand-up pouches and laminated roll stock with a wide variety of printing options. Our coated products consist of a variety of laminations, coatings and other treatments. Our coated products include optical films, microfilm, medical products, conductive films and foils, ink jet receptive products and phototool products.

Proprietary Brands, Products and Processes. We believe we have established a reputation for developing innovative products, improving the shelf-appeal of our customers’ products and enhancing product performance. For example, we have developed our RAVE™ brand of plastic-laminated and converted plastic bags with easy to open and reclose features for the pet food and lawn and garden markets, specialty packaging for feminine care products, eXpress pv™ two-ply cement bags for our cement and packaged concrete customers and paper bags with reclosable zippers for popular pet food brands. The acquisition of the EMCS facilities has added recognizable brands such as Clearshield®, Maraflex®, and Halo® for the meat and cheese market segments. We also hold numerous patents, have other patent applications pending, and possess a number of proprietary constructions, compositions and manufacturing processes. In addition to our expertise in developing innovative products, our in-house graphics center has earned several industry awards for print quality and innovation.

Recent Developments

New Senior Secured Credit Facilities

New Term Loan Facility

In connection with the offering of the old notes, we entered into a new $350.0 million six-year secured term loan facility (the “New Term Loan Facility”). The New Term Loan Facility is secured by substantially all of our assets, and the old notes and the related guarantees are effectively subordinated to the borrowings under the New Term Loan Facility to the extent of the assets securing such debt. See “Description of Certain Indebtedness—New Term Loan Facility.”

Senior Credit Facility

In connection with the offering of the old notes, we refinanced our existing $125.0 million senior secured revolving credit facility (the “Senior Credit Facility”) with the proceeds from the old notes and borrowings under the New Term Loan Facility. We amended the credit agreement governing the Senior Credit Facility to, among

7

other things, extend the maturity of the Senior Credit Facility to 2016 and decrease availability under the Senior Credit Facility from $125.0 million to $75.0 million. In addition, the amendment permitted us to (i) issue and guarantee the old notes, (ii) incur additional indebtedness in connection with the New Term Loan Facility, and (iii) make a cash dividend to our stockholders of $150.0 million. See “Description of Certain Indebtedness—Senior Credit Facility.”

Resignation of Certain Officers and Directors

On August 4, 2011, Jack E. Knott informed us of his decision to resign from his position as Chief Executive Officer and Secretary of our Company, effective September 1, 2011. Mr. Knott accepted an appointment as a Managing Director of Sun Capital Partners, Inc. (“Sun Capital”), an affiliate of our Company. Mr. Knott continues to serve as our Chairman of the Board of Directors. Tom Vale, our President and Chief Operating Officer, is currently serving as our Interim Chief Executive Officer. We are conducting a search for a new Chief Executive Officer.

Mr. Vale, 49, has served as our Chief Operating Officer since February 2008 and has served as our President since September 30, 2010. Mr. Vale also served as our Interim Chief Financial Officer from September 30, 2010 to April 14, 2011. Mr. Vale has an undergraduate degree from Valparaiso University in Accounting and Economics and received his MBA in Finance from DePaul University. After working in public accounting for 10 years, Mr. Vale joined McDonalds Corporation where he worked for five years in Accounting and Business Development. In 1998, he joined Resorts USA as Executive Vice President and Chief Financial Officer. In 2000, he moved to Deluxe Media Services as Executive Vice President and Chief Financial Officer. He served in those capacities until August 2004, when he was promoted to President and Chief Executive Officer. Mr. Vale served in those capacities until May 2007. He subsequently opened a consulting practice, TMV Consulting, which he maintained until he joined our Company as Chief Operating Officer in 2008.

Effective September 6, 2011, Clarence E. Terry resigned from his position as a member of the Board of Directors of our Company. The Company intends to leave Mr. Terry’s position on the Board of Directors vacant for the immediate future.

Effective October 12, 2011, Robert H. Arvanites, Senior Vice President and General Manager of our Company, separated from our Company.

On November 4, 2011, Eric M. Lynch informed us of his decision to resign as Chief Financial Officer of our Company effective November 18, 2011. We are conducting a search for a new Chief Financial Officer.

8

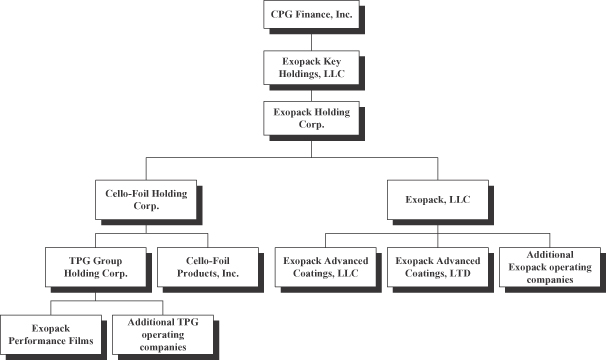

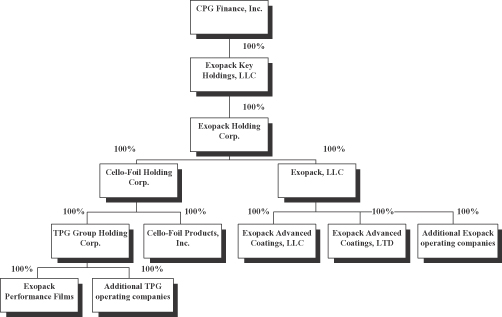

Corporate Structure

CPG Finance, Inc. is a subsidiary of an affiliate of Sun Capital. Exopack Key Holdings, LLC is a wholly-owned subsidiary of CPG Finance, Inc., and is the parent company of Exopack Holding Corp., the issuer of the old notes. Exopack Holding Corp. is a holding company that conducts substantially all of its operations through Exopack, LLC, Cello-Foil Holding Corp. and their respective subsidiaries. The diagram below illustrates our basic corporate and principal debt structure. Each subsidiary is wholly owned by its direct parent.

Our Sponsor

Sun Capital is a leading private investment firm focused on leveraged buyouts, equity, debt and other investments in market-leading companies. Sun Capital affiliates have invested in more than 260 companies worldwide with combined sales in excess of $40 billion since Sun Capital’s inception in 1995. Sun Capital currently has approximately $8 billion of equity capital under management. Sun Capital has offices in Boca Raton, Los Angeles and New York, as well as affiliates with offices in London, Paris, Frankfurt, Shanghai and Shenzhen. Sun Capital has experience in the paper and packaging industry, including investments in the Britton Group, Polestar UK Print, PACCOR, Albéa, Betts, Reuther Verpackung, PaperWorks Industries, Veriplast Solutions and InteliCoat Technologies.

Our Principal Executive Offices

EHC is incorporated in the state of Delaware. Our principal executive office is at 3070 Southport Road, Spartanburg, SC 29302, and our telephone number is (864) 596-7140. Our website address is www.exopack.com. The information on our website does not constitute a part of this prospectus, and the reference to our website address is intended as an inactive textual reference only.

9

Summary of the Terms of the Exchange Offer

On May 31, 2011, we completed an offering of 10% senior notes due 2018 (the “old notes”) in a private transaction exempt from the registration requirements of the Securities Act pursuant to Section 4(2) of the Securities Act and in compliance with Rule 144A and Regulation S promulgated thereunder. The old notes were sold for an aggregate purchase price of $235,000,000. The notes:

| • | are guaranteed on a senior basis by certain of our existing and future domestic restricted subsidiaries, and |

| • | are effectively subordinated to all of our and the guarantors’ secured indebtedness, including the Senior Credit Facility, to the extent of the value of the assets securing that indebtedness. |

We entered into an exchange and registration rights agreement with the initial purchaser of the old notes, in which we agreed to complete this exchange offer. This exchange offer gives you the opportunity to exchange your old notes for notes with substantially identical terms that are registered for issuance under the Securities Act (the “new notes”). You should read the discussion under the heading “The Exchange Offer” beginning on page 34 and “Description of the Notes” beginning on page 110 for further information about the new notes.

Securities Offered | $235.0 million aggregate principal amount of 10% senior notes due 2018. The terms of the new notes offered in the exchange offer are substantially identical to those of the old notes, except that certain transfer restrictions, registration rights and liquidated damages provisions relating to the old notes do not apply to the new registered notes. |

The Exchange Offer | We are offering to issue new notes in exchange for a like principal amount and like denomination of our old notes. We are offering to issue these registered notes to satisfy our obligations under an exchange and registration rights agreement that we entered into with the initial purchasers of the old notes when we sold them in a transaction that was exempt from the registration requirements of the Securities Act. You may tender your old notes for exchange by following the procedures described under the heading “The Exchange Offer.” |

Registration Rights Agreement | Under the exchange and registration rights agreement, we have agreed to use our commercially reasonable efforts to, among other things, (i) cause the registration statement of which this prospectus forms a part to become effective under the Securities Act as promptly as practicable, but in any event no later than 270 days after the date of the exchange and registration rights agreement, (ii) commence and complete the exchange offer promptly (but no later than sixty days) following such effective time, (iii) hold the exchange offer open for at least 30 days and (iv) exchange new notes for all old notes that have been properly tendered and not withdrawn promptly following expiration of the exchange offer. |

| In addition, we have agreed, in some circumstances, to file a “shelf registration statement” that would allow some or all of the old notes to be offered to the public. |

10

| If we do not comply with the foregoing obligations under the registration rights agreement, we will be required to pay special interest and liquidated damages to the holders of the old notes, including special interest of 0.25% per annum during the first 90 days following our failure to comply, 0.50% per annum during the second 90 days, 0.75% per annum during the third 90 days, and 1.00% thereafter. See “Exchange Offer—Registration Rights; Liquidated Damages.” |

Resales | We believe the new notes may be offered for resale, resold and otherwise transferred by you without compliance with the registration and prospectus delivery provisions of the Securities Act provided that you: |

| • | acquire the new notes issued in the exchange offer in the ordinary course of your business, |

| • | are not participating, do not intend to participate, and have no arrangement or understanding with anyone to participate, in the distribution of the new notes issued to you in the exchange offer, and |

| • | are not an “affiliate” of our Company as defined in Rule 405 of the Securities Act. |

| If any of these conditions are not satisfied and you transfer any new notes issued to you in the exchange offer without delivering a proper prospectus or without qualifying for a registration exemption, you may incur liability under the Securities Act. We will not be responsible for, or indemnify you against, any liability you may incur. |

| In connection with the exchange offer, you will be required to acknowledge that you are not engaged in, and do not intend to engage in, the distribution of the new notes. In addition, any broker-dealer that acquires new notes in the exchange offer for its own account in exchange for old notes which it acquired through market-making or other trading activities may be an “underwriter” within the meaning of the Securities Act and must acknowledge that it will deliver a prospectus when it resells or transfers any new notes. See “Plan of Distribution” for a description of the prospectus delivery obligations of broker-dealers in the exchange offer. |

Expiration Date | The exchange offer will expire at 5:00 p.m., New York City time, January 10, 2012, unless we decide to extend the expiration date. If we extend the exchange offer, the longest we could keep the offer open without incurring liquidated damages under the registration rights agreement in the form of increased interest payable on the old notes would be until 60 business days after the date the registration statement of which this prospectus forms a part is declared effective. |

11

Conditions to the Exchange Offer | The exchange offer is not subject to any condition other than that the exchange offer does not violate law or any interpretation of the staff of the Securities and Exchange Commission, or the SEC, and the other conditions expressly described under “The Exchange Offer.” |

Procedure for Tendering Old Notes Held in the Form of Book-Entry Interests | If you are a holder of a note held in the form of a book-entry interest through The Depository Trust Company, or DTC, and you wish to tender your book-entry interest for exchange in the exchange offer, you must transmit to The Bank of New York Mellon Trust Company, N.A., as exchange agent, before the expiration date of the exchange offer: |

| either |

| • | a properly completed and executed letter of transmittal, which accompanies this prospectus, or a facsimile of the letter of transmittal, including all other documents required by the letter of transmittal, to the exchange agent at the address on the cover page of the letter of transmittal; |

| or |

| • | a computer-generated message (an “agent’s message”) transmitted by means of DTC’s Automated Tender Offer Program system and received by the exchange agent and forming a part of a confirmation of book-entry transfer in which you acknowledge and agree to be bound by the terms of the letter of transmittal; |

| and, either |

| • | a timely confirmation of book-entry transfer of your old notes into the exchange agent’s account at DTC, according to the procedure for book-entry transfers described in this prospectus under the heading “The Exchange Offer—Book-Entry Transfer” beginning on page 39, which must be received by the exchange agent on or prior to the expiration date; |

| or |

| • | the documents necessary for compliance with the guaranteed delivery procedures described below. |

Procedures for Tendering Certificated Notes | If you are a holder of a beneficial interest in the old notes, you are entitled to receive, in exchange for your beneficial interest, certificated notes in equal principal amounts to your beneficial interest. As of the date of this prospectus, however, no certificated notes were issued and outstanding. If you acquire certificated notes before the expiration date of the exchange offer, you must tender your notes under the procedures described in this prospectus under the heading “The Exchange Offer—Procedure for Tendering Old Notes” beginning on page 36. |

12

Special Procedures for Beneficial Owners | If you are the owner of a beneficial interest and your name does not appear on a security position listing of DTC as the holder of that interest or if you are a beneficial owner of certificated notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee and you wish to tender that interest or certificated notes in the exchange offer, you should contact the person in whose name your interest or certificated notes are registered promptly and instruct such person to tender on your behalf. |

Guaranteed Delivery Procedures | If you wish to tender your notes and time will not permit your required documents to reach the exchange agent by the expiration date of the exchange offer, or the procedure for book-entry transfer cannot be completed on time or certificates for your notes cannot be delivered on time, you may tender your notes according to the procedures described in this prospectus under the heading “The Exchange Offer—Guaranteed Delivery Procedures” beginning on page 39. |

Withdrawal Rights | You may withdraw the tender of your notes at any time prior to the time of expiration. We will return to you any old notes not accepted for exchange for any reason without expense to you promptly after withdrawal, rejection of tender or termination of the exchange offer. See “The Exchange Offer—Withdrawal Rights” beginning on page 39 for a more complete description of the withdrawal provisions. |

Regulatory Approvals | Other than pursuant to the federal securities laws, there are no federal or state regulatory requirements that we must comply with, or approvals that we must obtain, in connection with the exchange offer. |

Appraisal Rights | You will not have dissenters’ rights or appraisal rights in connection with the exchange offer. See “The Exchange Offer—Appraisal Rights” on page 41. |

U.S. Federal Income Tax Consequences | The exchange of notes will not be a taxable exchange for U.S. federal income tax purposes. You will not recognize any taxable gain or loss or any interest income as a result of the exchange. |

Exchange Agent | The Bank of New York Mellon Trust Company, N.A. is serving as exchange agent for the exchange offer. |

Consequences of Failure to Exchange | Notes that are not tendered or that are tendered but not accepted will continue to be subject to the restrictions on transfer that are described in the legend on those notes. In general, you may offer or sell your notes only if they are registered under, or offered or sold under an exemption from, the Securities Act and applicable state securities laws. We, however, will have no further obligation to register the notes. If you do not participate in the exchange offer, the liquidity of your notes could be adversely affected. |

13

Summary of the Terms of the New Notes

The terms of the new notes will be identical in all material respects to the terms of the old notes, except that the registration rights and related liquidated damages provisions, and the transfer restrictions applicable to the old notes, are not applicable to the new notes, and the new notes will be registered under the Securities Act. The new notes will evidence the same debt as the old notes. The new notes and the old notes will be governed by the same indenture. For more complete information about the new notes, see the “Description of the Notes” section of this prospectus.

Issuer | Exopack Holding Corp. (“EHC”) |

Aggregate Amount | $235.0 million aggregate principal amount of 10% senior notes due 2018. |

Interest | Interest will accrue on the notes from June 1, 2011 at the rate of 10% per annum. Interest on the notes will be payable semi-annually in arrears on each June 1 and December 1, commencing on December 1, 2011. |

Maturity Date | June 1, 2018. |

Ranking, Guarantees | The notes and the guarantees will be our and our guarantors’ senior unsecured obligations. The notes and the guarantees will rank senior to all of our and our guarantors’ existing and future subordinated indebtedness. |

| The notes and the guarantees will be effectively subordinated to all of our and the guarantors’ secured indebtedness, including the Senior Credit Facility and New Term Loan Facility, to the extent of the value of the assets securing that indebtedness. See “Description of Certain Indebtedness.” |

| As of September 30, 2011, after giving effect to the offering of the old notes and borrowings under the New Term Loan Facility and the application of the net proceeds therefrom, we and the subsidiary guarantors had $599.9 million of senior debt outstanding, consisting of $235.0 million of indebtedness represented by the old notes, $349.1 million of borrowings under the New Term Loan Facility, $2.5 million of borrowings under the Senior Credit Facility and $13.3 million of capital lease obligations, and we had $68.7 million available for borrowings under the Senior Credit Facility. |

Optional Redemption | Before June 1, 2014, we may redeem some or all of the notes at a price equal to 100% of the principal amount of the notes redeemed, plus accrued and unpaid interest, if any, to the redemption date and a “make-whole premium” as described in this prospectus. See “Description of the Notes—Optional Redemption.” |

14

| In addition, at any time (which may be more than once) before June 1, 2014, we may redeem up to 35% of the aggregate principal amount of notes issued with the net proceeds that we raise in one or more equity offerings, as long as: |

| • | we pay 110% of the principal amount of the notes, plus accrued and unpaid interest to the date of redemption; |

| • | we redeem the notes within 90 days of completing the equity offering; and |

| • | at least 65% of the aggregate principal amount of notes issued remains outstanding afterwards. |

| On and after June 1, 2014, we may redeem some or all of the notes at the redemption prices listed under “Description of the Notes—Optional Redemption,” plus accrued and unpaid interest to the redemption date |

Change of Control | If we experience a change of control, we may be required to offer to purchase the notes at a purchase price equal to 101% of the principal amount, plus accrued and unpaid interest to the date of redemption. We may not be able to pay you the required price for notes you present us at the time of a change of control because the Senior Credit Facility or New Term Loan Facility or other indebtedness may prohibit payment or we may not have sufficient funds at such time. |

Asset Sale Proceeds | If we or our subsidiaries sell assets under certain circumstances, we generally must invest the net cash proceeds from such asset sales in our business within a period of time, prepay certain secured senior debt or make an offer to purchase a principal amount of the notes equal to the excess net cash proceeds. The purchase price of the notes will be 100% of their principal amount, plus accrued and unpaid interest. See “Description of the Notes—Repurchase at the Option of Holders—Asset Sales.” |

Certain Covenants | The indenture governing the notes contains covenants that limit our ability to, among other things: |

| • | incur additional indebtedness or issue preferred stock; |

| • | pay dividends or make other distributions or repurchase or redeem our stock or subordinated indebtedness; |

| • | make investments; |

| • | sell assets and issue capital stock of restricted subsidiaries; |

| • | incur liens; |

| • | enter into agreements restricting our subsidiaries’ ability to pay dividends; |

| • | enter into transactions with affiliates; and |

| • | consolidate, merge or sell all or substantially all of our assets. |

15

| These covenants are subject to important exceptions and qualifications, which are described under the heading “Description of the Notes—Certain Covenants” in this prospectus. |

Use of Proceeds | We will not receive any proceeds from the exchange offer. For a description of the use of proceeds from the offering of the old notes, see “Use of Proceeds.” |

Form of the New Notes | The new notes will be represented by one or more permanent global securities in registered form deposited with The Bank of New York Mellon Trust Company, N.A., as custodian, for the benefit of The Depository Trust Company. You will not receive notes in registered form unless one of the events set forth under the heading “Description of the Notes—Book-Entry, Delivery and Form” occurs. Instead, beneficial interests in the new notes will be shown on, and transfers of these interests will be effected only through, records maintained in book-entry form by The Depository Trust Company with respect to its participants. |

Absence of a Public Market for the New Notes | There has been no public market for the old notes, and no active market for the new notes is currently anticipated. We do not intend to apply for a listing of the new notes on any securities exchange or inclusion in any automated quotation system. We cannot make any assurances regarding the liquidity of the market for the new notes, the ability of holders to sell their new notes or the price at which holders may sell their new notes. See “Plan of Distribution.” |

Trustee | The Bank of New York Mellon Trust Company, N.A. is serving as the trustee under the Indenture. |

Risk Factors

As a holder of our old notes, your investment is subject to various risks and uncertainties, including those described under “Risk Factors,” beginning on page 21, and your investment will remain subject to those risks and uncertainties if you exchange your old notes for new notes.

16

Summary Consolidated Financial Data

The following tables set forth summary consolidated financial data as of and for the nine months ended September 30, 2011 and 2010, as of and for the fiscal years ended December 31, 2010, 2009, 2008, 2007 and 2006. We derived the historical statement of operations data, the cash flow data and the other data for the years ended December 31, 2010, 2009 and 2008, and the historical balance sheet data as of December 31, 2010 and 2009, presented below from our audited consolidated financial statements included elsewhere in this prospectus, and such data are qualified in their entirety by reference to, and should be read in conjunction with, such audited consolidated financial statements. We derived the historical statement of operations data, the cash flow data and the other data for the years ended December 31, 2007 and 2006, and the historical balance sheet data as of December 31, 2008, December 31, 2007 and December 31, 2006, presented below from our audited consolidated financial statements which are not included in this prospectus. The historical statement of operations data, the cash flow data and the other data for the nine months ended September 30, 2011 and 2010, and the historical balance sheet data as of September 30, 2011, were derived from our unaudited condensed consolidated financial statements included elsewhere in this prospectus. The unaudited balance sheet data as of September 30, 2010 was derived from our September 30, 2010 unaudited condensed consolidated balance sheet which is not included in this prospectus. In the opinion of management, the interim financial information provided herein reflects all adjustments (consisting of normal and recurring adjustments) necessary for a fair statement of the data for the periods presented. Interim results are not necessarily indicative of the results to be expected for any other interim period, for the entire fiscal year or for any future period.

On July 13, 2010, we completed the acquisition of EMCS. Therefore, investors should note that our results of operations for the nine month period ended September 30, 2011 and the fiscal year ended December 31, 2010 are not directly comparable to our results of operations for the corresponding prior periods.

The summary pro forma consolidated financial data for the year ended December 31, 2010 and the nine months ended September 30, 2010 gives effect to the acquisition of EMCS and the associated financing transaction as if they had occurred on January 1, 2010. The summary pro forma consolidated financial data is based on our historical financial statements and EMCS’s historical financial statements, adjusted to give pro forma effect to the acquisition of EMCS. The summary pro forma consolidated financial data is based on estimates and assumptions that management believes are reasonable. The summary pro forma consolidated financial data is for information purposes only and does not purport to represent what our actual results of operations would have been if the acquisition of EMCS had been completed as of January 1, 2010 or that may be achieved in the future. The information in the following table should be read in conjunction with EMCS’s historical financial statements and related notes thereto and our historical financial statements and notes related thereto appearing in this prospectus.

17

You should read the following summary financial data together with “Capitalization,” “Pro Forma Consolidated Financial Information (Unaudited),” “Selected Historical Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the notes thereto included elsewhere in this prospectus.

| Year Ended December 31, | Pro Forma (1) Year Ended December 31, | Nine Months Ended September 30, | Pro Forma (1) Nine Months Ended September 30, | |||||||||||||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | 2010 | 2010 | 2011 | 2010 | ||||||||||||||||||||||||||||

| (unaudited) | (unaudited) | (unaudited) | ||||||||||||||||||||||||||||||||||

| (dollars in millions) | ||||||||||||||||||||||||||||||||||||

Statement of Operations Data: | ||||||||||||||||||||||||||||||||||||

Net sales | $ | 655.4 | $ | 676.1 | $ | 781.7 | $ | 673.7 | $ | 785.1 | $ | 859.0 | $ | 569.2 | $ | 663.9 | $ | 643.1 | ||||||||||||||||||

Cost of sales | 583.3 | 603.7 | 699.5 | 596.7 | 684.2 | 743.6 | 498.8 | 574.3 | 558.2 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Gross Profit | 72.1 | 72.4 | 82.2 | 77.0 | 100.9 | 115.4 | 70.4 | 89.6 | 84.9 | |||||||||||||||||||||||||||

Operating expenses (2) | 48.0 | 49.5 | 57.2 | 55.9 | 66.5 | 67.0 | 48.9 | 56.6 | 49.5 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Operating income | 24.1 | 22.9 | 25.0 | 21.1 | 34.4 | 48.4 | 21.5 | 33.0 | 35.4 | |||||||||||||||||||||||||||

Other expenses: | ||||||||||||||||||||||||||||||||||||

Interest expense | 27.3 | 28.9 | 31.0 | 28.6 | 36.4 | 44.4 | 25.1 | 36.6 | 33.1 | |||||||||||||||||||||||||||

Loss on early extinguishment of debt (3) | 4.0 | — | — | — | — | — | — | 22.1 | — | |||||||||||||||||||||||||||

Other expense (income), net (4) | — | (1.6 | ) | 1.3 | (0.5 | ) | (1.1 | ) | (1.1 | ) | (0.9 | ) | (0.2 | ) | (0.9 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Net other expense | 31.3 | 27.3 | 32.3 | 28.1 | 35.3 | 43.3 | 24.2 | 58.5 | 32.2 | |||||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Income (loss) before income taxes | (7.2 | ) | (4.4 | ) | (7.3 | ) | (7.0 | ) | (0.9 | ) | 5.1 | (2.7 | ) | (25.5 | ) | 3.2 | ||||||||||||||||||||

Provision for (benefit from) income taxes | (2.3 | ) | (0.5 | ) | (1.2 | ) | (1.1 | ) | 1.9 | 4.2 | 0.7 | (9.4 | ) | 3.0 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

Net (loss) income | $ | (4.9 | ) | $ | (3.9 | ) | $ | (6.1 | ) | $ | (5.9 | ) | $ | (2.8 | ) | $ | 0.9 | $ | (3.4 | ) | $ | (16.1 | ) | $ | 0.2 | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||||

| Year Ended December 31, | Nine Months Ended September 30, | |||||||||||||||||||||||||||

| 2006 | 2007 | 2008 | 2009 | 2010 | 2010 | 2011 | ||||||||||||||||||||||

| (unaudited) | ||||||||||||||||||||||||||||

| (dollars in millions) | ||||||||||||||||||||||||||||

Balance Sheet Data (at period end): | ||||||||||||||||||||||||||||

Cash | $ | 0.5 | $ | 1.3 | $ | 1.7 | $ | 0.6 | $ | 2.5 | $ | 1.5 | $ | 1.3 | ||||||||||||||

Working capital (5) | $ | 51.4 | $ | 5.9 | $ | 4.6 | $ | 1.3 | $ | 21.3 | $ | 16.7 | $ | 92.2 | ||||||||||||||

Property, plant and equipment, net | $ | 145.8 | $ | 186.4 | $ | 173.8 | $ | 174.1 | $ | 214.3 | $ | 214.8 | $ | 221.4 | ||||||||||||||

Total assets (6) | $ | 451.1 | $ | 519.1 | $ | 498.6 | $ | 481.5 | $ | 609.8 | $ | 612.1 | $ | 628.6 | ||||||||||||||

Long term debt, less current portion (7) | $ | 220.2 | $ | 220.1 | $ | 220.1 | $ | 220.0 | $ | 330.5 | $ | 320.0 | $ | 580.6 | ||||||||||||||

Total debt (7) | $ | 230.2 | $ | 291.1 | $ | 294.6 | $ | 288.6 | $ | 389.3 | $ | 402.6 | $ | 599.9 | ||||||||||||||

Stockholder’s equity (deficit) | $ | 66.0 | $ | 65.0 | $ | 42.7 | $ | 44.5 | $ | 40.0 | $ | 41.7 | $ | (126.7 | ) | |||||||||||||

Other Data: | ||||||||||||||||||||||||||||

Ratio of earnings to fixed charges (8) | — | — | — | — | — | — | — | |||||||||||||||||||||

Cash Flow Data: | ||||||||||||||||||||||||||||

Net cash provided by (used in): | ||||||||||||||||||||||||||||

Operating activities (9) | $ | 9.7 | $ | 12.8 | $ | 13.0 | $ | 26.0 | $ | 29.6 | $ | 7.4 | $ | (8.2 | ) | |||||||||||||

Investing activities (10) | $ | (17.5 | ) | $ | (71.8 | ) | $ | (19.0 | ) | $ | (19.7 | ) | $ | (100.3 | ) | $ | (93.7 | ) | $ | (33.3 | ) | |||||||

Financing activities (11) | $ | (0.7 | ) | $ | 59.4 | $ | 5.1 | $ | (6.9 | ) | $ | 72.7 | $ | 87.2 | $ | 40.4 | ||||||||||||

Capital expenditures | $ | 17.5 | $ | 23.2 | $ | 19.1 | $ | 26.4 | $ | 25.0 | $ | 18.4 | $ | 34.8 | ||||||||||||||

| (1) | For a reconciliation of the historical statement of operations data for the year ended December 31, 2010 and the nine months ended September 30, 2010 to the pro forma statement of operations data for the year ended December 31, 2010 and the nine months ended September 30, 2010, see “Pro Forma Consolidated Financial Information (Unaudited).” |

| (2) | Operating expenses for the nine months ended September 30, 2011 included approximately $4.3 million related to costs to complete the Recapitalization Transactions, $3.0 million in management fees, $2.1 million in costs related to the integration of EMCS, $2.0 million in process improvement consulting fees and $1.1 million in severance costs. Operating expenses for the nine months ended September 30, 2010 included $4.5 million in acquisition costs related to EMCS, $2.6 million in process improvement consulting fees, $2.5 million in severance costs and $1.3 million in management fees. Operating expenses for the year ended December 31, 2010 included $6.0 million in expenses related to acquisition costs and the start-up and integration of EMCS operations into our business, $5.0 million in other selling, general and administrative costs acquired with the EMCS |

18

| acquisition, $3.5 million in professional services related to process improvement consulting, $2.7 million in severance costs, and $2.5 million in incentive bonus related to our management incentive plan bonus (“MIP”). Operating expenses for the year ended December 31, 2009 included $3.3 million in incentive bonus related to our MIP, $3.1 million in severance costs, $1.7 million in professional services related to process improvement consulting, and approximately $831,000 related to the closure of one of our Canadian facilities. Operating expenses for the year ended December 31, 2008 included $3.4 million in start-up and transition costs related to the EEF and EPF Acquisitions, $8.5 million in other selling, general and administrative expenses due to a full year of EEF and EPF operations in 2008, $2.0 million in severance costs, and approximately $567,000 related to a lease obligation to consolidate operations at one of our Canadian facilities. Operating expenses for the year ended December 31, 2007 included $1.3 million of accelerated amortization related to the reduction of the useful life of the Cello-Foil trademark and trade name, $1.3 million (excluding certain severance charges included in severance costs below) related to costs associated with continued efforts to combine and streamline certain operations of our consumer food and specialty packaging Canadian facilities, $2.0 million in severance costs, $1.5 million in start-up and transition expenses related to the EEF and EPF Acquisitions and $2.6 million in other selling, general and administrative costs related to the EEF and EPF Acquisitions. |

| (3) | Loss on early extinguishment of debt for the nine months ended September 30, 2011 represented a charge to earnings to write-off deferred financing costs of approximately $11.9 million and a recognition of approximately $10.2 million in early redemption and consent costs related to the early extinguishment of our former 11.25% senior notes. Loss on early extinguishment of debt for the year ended December 31, 2006 represented a charge to earnings during the year ended December 31, 2006 to write-off the deferred financing costs related to our former senior credit facility and subordinated term loans. This debt was refinanced in January 2006. |

| (4) | Other income for the nine months ended September 30, 2010 and the year ended December 31, 2010 was primarily related to insurance proceeds of approximately $1.0 million received in 2010 related to a press fire at one of our consumer food and specialty packaging facilities in the third quarter of 2009. Other income from the year ended December 31, 2009 includes primarily $432,000 in exchange gains related to an intercompany note with our United Kingdom operations as a result of the strengthening of the British pound against the U.S. dollar. Other income for the year ended December 31, 2008 includes primarily $1.7 million in exchange loss related to an intercompany note with our United Kingdom operations as a result of the weakening of the British pound against the U.S. dollar. Other income for the year ended December 31, 2007 includes primarily $1.8 million in proceeds received from the settlement of a business interruption insurance claim related to the 2005 hurricane season. |

| (5) | Working capital reflects current assets less current liabilities, including the current portion of long term debt and the Senior Credit Facility. The significant increase at September 30, 2011 is due to the repayment of the Senior Credit Facility during 2011 with proceeds from the Recapitalization Transaction. The significant increase in 2010 is primarily the result of the EMCS acquisition. The significant decrease in 2007 primarily the result of borrowings under our Senior Credit Facility to fund the 2007 acquisitions. |

| (6) | Total assets increased in 2010 primarily as a result of the EMCS acquisition. Total assets decreased in 2009 due to reductions in accounts receivables and inventory, primarily as a result of reduced sales volume. Total assets of our foreign subsidiaries were reported at lower amounts at December 31, 2008 due to the weakening of the British pound and Canadian dollar relative to the U.S. dollar. Total assets increased significantly in 2007 due to the 2007 acquisitions. |

| (7) | Long term and total debt increased in 2011 primarily due to the $350.0 million New Term Loan Facility and a new capital lease obligation in the amount of $2.3 million. Long-term and total debt increased in 2010 primarily due to issuance of $100.0 million in Former Additional Notes (as defined in “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Cash Flows for the Year Ended December 31, 2010”) to finance the EMCS acquisition and $10.5 million in capital lease obligations. |

| (8) | Income (loss) used in computing the ratio of earnings to fixed charges consists of income (loss) before income taxes plus fixed charges. Fixed charges consist of interest expense on debt, the amortization of deferred financing costs, and the portion of rental expense that management believes is representative of the interest component of rental expense. For the nine months ended September 30, 2011, our earnings were insufficient to cover our fixed charges by $25.5 million, and for the years ended December 31, 2010, 2009, 2008, 2007 and 2006, our earnings were insufficient to cover our fixed charges by $0.9 million, $7.0 million, $7.3 million, $4.4 million and $7.2 million, respectively. |

| (9) | Includes primarily an increase in receivables and inventory and a decrease in accounts payable and accrued liabilities for the nine months ended September 30, 2011. Includes primarily an increase in receivables, inventory, and accounts payable and accrued liabilities as a result of the EMCS acquisition for the year ended December 31, 2010. Includes primarily a decrease in receivables and inventory, partially offset by a decrease in accounts payable and accrued liabilities for the year ended December 31, 2009. |

| (10) | Includes primarily $34.8 million related to the purchase of property, plant and equipment during the nine months ended September 30, 2011. Includes primarily $82.1 million related to the acquisition of EMCS and $25.0 million related to the purchase of property, plant and equipment partially offset by $7.2 million in proceeds from sales of property, plant and equipment for the year ended December 31, 2010. Includes primarily $26.4 million related to the purchase of property, plant and equipment partially offset by $7.1 million in proceeds from sales of property, plant and equipment for the year ended December 31, 2009. Includes primarily $19.1 million related to the purchase of property, plant and equipment for the year ended December 31, 2008. Includes primarily the acquisition costs of EAC and EPF, totaling $48.9 million and $23.2 million related to the purchase of property, plant and equipment for the year ended December 31, 2007. During the year ended December 31, 2006, an additional $346,000 of acquisition costs was paid related to the 2005 acquisition of Cello-Foil, TPG and Exopack, an additional $6.2 million had been estimated to be payable to the former stockholders of Exopack under tax-related provisions contained in the Exopack purchase agreement, and the amount estimated to be payable to the former stockholders of Cello-Foil under tax-related provisions contained in the Cello-Foil purchase agreement was reduced by $163,000, resulting in a total cost of the acquired companies of $312.6 million. |

19

| (11) | Includes activity related to the Recapitalization Transactions for 2011 consisting of the issuance of the $350.0 million New Term Loan Facility, the issuance of $235.0 million related to the 10.0% senior notes, the repayment of $320.0 million related to the former 11.25% senior notes, net repayments of $54.5 million related to the Senior Credit Facility, a dividend of $150.0 million paid to an affiliate, deferred loan costs paid of $17.7 million and repayment of capital lease obligations of $1.4 million. Includes approximately $100.0 million related to issuance of Former Additional Notes, $12.9 million in deferred financing costs related to the Former Additional Notes and the re-negotiation of the Senior Credit Facility and $11.9 million in net repayments under our Senior Credit Facility for the year ended December 31, 2010 (excluding the impact of foreign currency fluctuations). Includes approximately $6.9 million related to net repayments under our Senior Credit Facility for the year ended December 31, 2009 (excluding the impact of foreign currency fluctuations). Includes approximately $5.4 million related to net borrowings under our Senior Credit Facility for the year ended December 31, 2008 (excluding the impact of foreign currency fluctuations). Includes approximately $48.9 million related to borrowings under our Senior Credit Facility to fund the 2007 acquisitions for the year ended December 31, 2007. |

20

The new notes, like the old notes, entail risk. In deciding whether to participate in the exchange offer, you should consider the risks associated with the nature of our industry, the nature of our business and the risk factors relating to the exchange offer in addition to the other information contained in this prospectus. You should carefully consider the following factors before making a decision to exchange your old notes for new notes.

Risk Factors Related to the Notes

Our substantial indebtedness could adversely affect our financial health and prevent us from fulfilling our obligations under the notes, obtaining financing in the future and reacting to changes in our business.

We have a substantial amount of debt, which requires significant payments. As of September 30, 2011, we had $599.9 million of debt outstanding. We had $68.7 million of undrawn availability, subject to a borrowing base limitation, under our Senior Credit Facility after giving effect to the amendment thereof.

Our substantial indebtedness could have important consequences to you. For example, it could:

| • | make it more difficult for us to satisfy our obligations with respect to the notes; |

| • | make it more difficult for us to meet all of our obligations to creditors, who could then require us, among other things, to restructure our indebtedness, sell assets or raise additional debt or equity capital; |

| • | increase our vulnerability to adverse economic and general industry conditions, including interest rate fluctuations, because a portion of our borrowings are and will continue to be at variable rates of interest; |

| • | limit our flexibility in planning for, and reacting to, changes in our business and industry; |

| • | require us to dedicate a substantial portion of our cash flows from operations to payments on our indebtedness, which will reduce the availability of our cash flows to fund acquisitions, working capital, capital expenditures, research and development efforts and other general corporate purposes; |

| • | limit our ability to borrow additional amounts for working capital, capital expenditures, debt service requirements, execution of our growth strategy or general corporate purposes; |

| • | place us at a competitive disadvantage compared to our competitors that may have less debt; |

| • | increase our cost of borrowing; and |

| • | limit our ability to make future acquisitions. |

The instruments governing the notes and the credit agreements governing our Senior Credit Facility and New Term Loan Facility contain, and the instruments governing any indebtedness we may incur in the future may contain, restrictive covenants that limit our ability to engage in activities that may be in our long-term best interests. Our failure to comply with these covenants could result in an event of default which, if not cured or waived, could result in the acceleration of all or a portion of our outstanding indebtedness.

Despite current indebtedness levels, we and our subsidiaries may still be able to incur substantially more debt. This could further exacerbate the risks described above.

We and our subsidiaries may be able to incur substantial additional indebtedness, including additional secured indebtedness, in the future. The terms of the indenture governing the notes and the credit agreements governing our Senior Credit Facility and New Term Loan Facility will restrict, but will not prohibit, us or our subsidiaries from doing so. At September 30, 2011, we had $68.7 million of undrawn availability under our Senior Credit Facility, subject to borrowing base limitations. If new debt is added to our and our subsidiaries’

21

current debt levels, the related risks that we now face could intensify. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Liquidity and Capital Outlook.”

To service our indebtedness, we will require a significant amount of cash. Our ability to generate cash depends on many factors beyond our control.

Our ability to make scheduled payments on and to refinance our indebtedness, including the notes, and to fund capital expenditures, acquisitions and research and development efforts, will depend on our ability to generate cash. A number of factors that affect our ability to generate cash are beyond our control. These factors include economic, financial, competitive, legislative, regulatory and other factors, such as changes in packaging designs, adverse weather conditions and acts of God, all of which are beyond our control.

We may also be required to obtain the consent of the lenders under our Senior Credit Facility or New Term Loan Facility and to refinance material portions of our indebtedness, including the notes. We cannot assure you that we will maintain a level of cash flows from operating activities sufficient to permit us to pay the principal, premium, if any, and interest on our indebtedness, including the notes.

If our cash flows and capital resources are insufficient to fund our debt service obligations, we may be forced to reduce or delay investments and capital expenditures, or to sell assets, seek additional capital or restructure or refinance our indebtedness, including the notes. These alternative measures may not be successful and may not permit us to meet our scheduled debt service obligations. If our operating results and available cash are insufficient to meet our debt service obligations, we could face substantial liquidity problems and might be required to dispose of material assets or operations to meet our debt service and other obligations. We may not be able to consummate those dispositions or to obtain the proceeds that we could realize from them, and these proceeds may not be adequate to meet any debt service obligations then due. Additionally, the credit agreements governing our Senior Credit Facility and New Term Loan Facility and the indenture governing the notes will limit the use of the proceeds from any disposition; as a result, we may not be allowed, under these documents, to use proceeds from such dispositions to satisfy all current debt service obligations.

Your right to receive payments on the notes is effectively subordinated to the rights of our existing and future secured creditors.