Exhibit 99.1

Anchorage Economic Development Corporation Presentation August 11, 2021

FORWARD LOOKING STATEMENT This presentation contains forward-looking statements regarding CORE that are intended to be covered by the safe harbor "forward-looking statements" provided by the Private Securities Litigation Reform Act of 1995, based on CORE’s current expectations and includes statements regarding future results of operations, quality and nature of the asset base, the assumptions upon which estimates are based and other expectations, beliefs, plans, objectives, assumptions, strategies or statements about future events or performance (often, but not always, using words such as "expects", “projects”, "anticipates", "plans", "estimates", "potential", "possible", "probable", or "intends", or stating that certain actions, events or results "may", "will", "should", or "could" be taken, occur or be achieved). Forward- looking statements are based on current expectations, estimates and projections that involve a number of risks and uncertainties, which could cause actual results to differ materially from those reflected in the statements. These risks include, but are not limited to: the risks of the exploration and the mining industry (for example, operational risks in exploring for, developing mineral reserves; risks and uncertainties involving geology; the speculative nature of the mining industry; the uncertainty of estimates and projections relating to future production, costs and expenses; the volatility of natural resources prices, including prices of gold and associated minerals; the existence and extent of commercially exploitable minerals in properties acquired by CORE or the Joint Venture Company; ability to realize the anticipated benefits of the recent transactions with Kinross; disruption from the transactions and transition of the Joint Venture Company’s management to Kinross, including as it relates to maintenance of business and operational relationships; potential delays or changes in plans with respect to exploration or development projects or capital expenditures; the interpretation of exploration results and the estimation of mineral resources; the loss of key employees or consultants; health, safety and environmental risks and risks related to weather and other natural disasters); uncertainties as to the availability and cost of financing; inability to realize expected value from acquisitions; inability of our management team to execute its plans to meet its goals; extent of disruptions caused by the COVID-19 pandemic; and the possibility that government policies may change or governmental approvals may be delayed or withheld, including the inability to obtain any mining permits. Additional information on these and other factors which could affect CORE’s exploration program or financial results are included in CORE’s other reports on file with the Securities and Exchange Commission. Investors are cautioned that any forward-looking statements are not guarantees of future performance and actual results or developments may differ materially from the projections in the forward-looking statements. Forward-looking statements are based on the estimates and opinions of management at the time the statements are made. CORE does not assume any obligation to update forward-looking statements should circumstances or management's estimates or opinions change. 2

NON-GAAP MEASURES The Preliminary Economic Assessment (“PEA”) referenced herein was prepared in accordance with Canadian National Instrument 43-101 (NI 43-101). CORE is not subject to regulation by Canadian regulatory authorities and no Canadian regulatory authority has reviewed the PEA or passed upon its accuracy or compliance with NI43-101. The terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” as used in the resource estimate, the PEA and this presentation are Canadian mining terms as defined in accordance with NI 43-101; however, these terms are not defined terms under the U.S. Securities and Exchange Commission’s (“SEC’s”) Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC. The estimation of measured resources and indicated resources involves greater uncertainty as to their existence and the legal and economic feasibility of extraction than the estimation of proven and probable reserves. Conversion of mineral resources to proven and probable mineral reserves generally requires a further economic study, such as a preliminary feasibility study. The PEA is not a preliminary feasibility study and does not support an estimate of proven and probable mineral reserves. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Investors are also cautioned not to assume that all or any part of measured or indicated resources will ever be converted into mineral reserves. In addition, the SEC normally only permits issuers to report mineralization that does not constitute mineral reserves as in-place tonnage of mineralized material and grade without reference to unit amounts of metal. Please see the Company’s press release dated September 24, 2018 for more detail regarding the PEA. 3 CAUTIONARY NOTE REGARDING ESTIMATES OF MEASURED, INDICATED AND INFERRED RESOURCES This presentation contains certain non-GAAP financial measures. A reconciliation of each such measure to the most comparable GAAP measure is presented in the Appendix hereto. Preliminary all-in sustaining cost estimates included in this presentation exclude corporate overhead costs. This measure is not a measure of financial performance under GAAP. We strongly advise investors to review our financial statements and publicly filed reports in their entirety and not rely on any single financial measure. See the Appendix for a reconciliation to GAAP.

4 6 large scale mines6 Advanced Development Stage ProjectsOver 50 ACTIVE Exploration Stage Projects>$500,000 in 2021Over 150 active placer miners producing ~ 50,000 ounces in 2020Numerous Sand and Gravels operations around the State to support construction and road projects Mining and Minerals Exploration in Alaska Large Mine Development Stage Exploration Stage

5 Red Dog MineUsibelliFort KnoxPogoKensingtonGreens Creek Large Scale Mining in Alaska

6 Donlin Gold – 40 Million OunceBarrick Gold – NovaGold JVAmbler Metals Feasibility Study on Arctic Copper-Zinc-Lead-Gold-Silver depositLarge district being explored by South32-Trilogy JV and Valhalla Metals (Private)Manh Choh Gold-Silver - +1 Million OunceKinross-ContangoOre JV on Tetlin Tribal LandsPebble Copper-Gold-Silver-MolybdenumHuge but controversial Copper ResourceGraphite One World class graphite deposit currently completing a Pre-feasibility StudyLivengood Gold - +10 Million Ounce resource currently re-doing a PFS 6 Development Stage Projects in Alaska

7 Over 50 Exploration Stage projects ACTIVE in Alaska searching for: Copper, Lead, Zinc, Gold, Silver, Tin, Graphite, Rare Earths$160 Million Projected Expenditures in 2021 Exploration Stage Projects in Alaska

8 Over 50 Exploration Stage projects ACTIVE in Alaska searching for: Copper, Lead, Zinc, Gold, Silver, Tin, Graphite, Rare Earths$160 Million Projected Expenditures in 2021 Exploration Stage Projects in Alaska

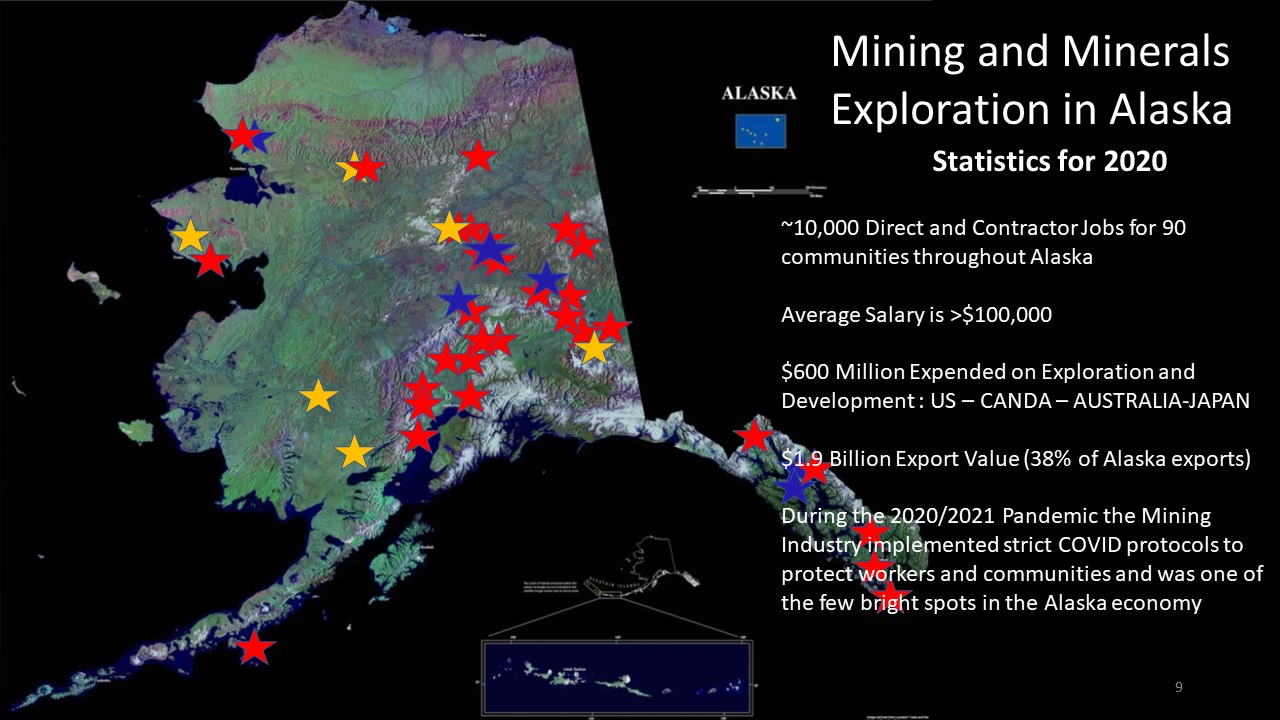

9 Mining and Minerals Exploration in Alaska Statistics for 2020 ~10,000 Direct and Contractor Jobs for 90 communities throughout AlaskaAverage Salary is >$100,000$600 Million Expended on Exploration and Development : US – CANDA – AUSTRALIA-JAPAN$1.9 Billion Export Value (38% of Alaska exports)During the 2020/2021 Pandemic the Mining Industry implemented strict COVID protocols to protect workers and communities and was one of the few bright spots in the Alaska economy

Manh Choh Gold Deposit1.3 Moz Gold – Measured plus Indicated Resources1Average grade = 4g/t Gold*Located in Alaska on the Alaska HwyOn Private Land Owned by the Tetlin Alaska Native TribeBusiness Partnership with Kinross - Using the Fort Knox Milling Facilities Lower capital costs, Smaller Environmental footprint and Lower execution risk 1 Based on SK1300 Report filed April 8, 2021 Corporate press release

CORPORATE OVERVIEW Traded on OTCQB – Pursuing listing on NYSE American6.67 Million Shares Outstanding6.77 Million Shares Fully Diluted100,000 OptionsNo Warrants and No Debt~ $US36 Million Cash Contango Owns 30% of Peak JV; Kinross Owns 70% and is OperatorContango Owns 100% on adjacent 160,000 acres 11 $10M Strategic Investment by Alaska Future FundSufficient cash to meet projected 2 year construction decisionPlanned 2021 budget expected to be ~US$10M for Contango OREStrong Cash Position and Tight Share StructureContango ORE is expecting strong cash flow per share (CFPS) starting in 2024 assuming Manh Choh construction decision made CAPITAL STRUCTURE Institutional Retail / Others Directors & Officers (Insiders)

12 MANH CHOH GOLD PROJECT Well EstablishedTetlin Relationship and Project Facilities

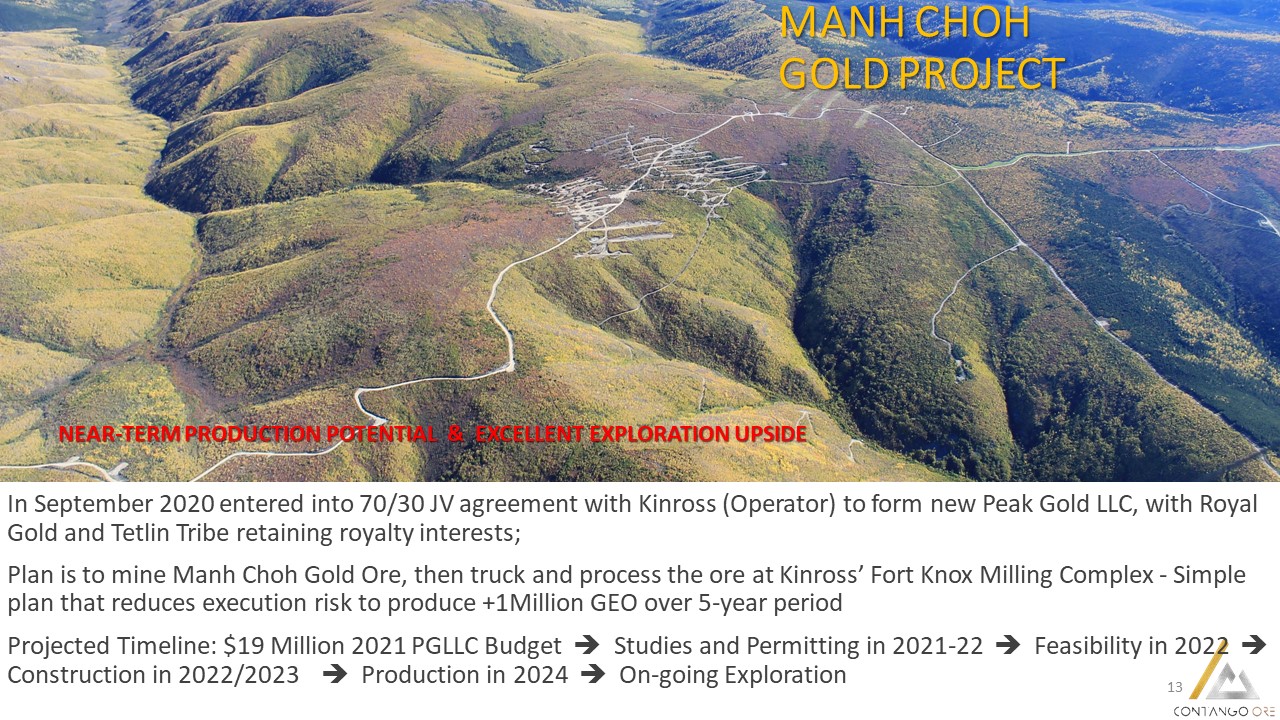

NEAR-TERM PRODUCTION POTENTIAL & EXCELLENT EXPLORATION UPSIDE 13 MANH CHOH GOLD PROJECT OTCQB:CTGO In September 2020 entered into 70/30 JV agreement with Kinross (Operator) to form new Peak Gold LLC, with Royal Gold and Tetlin Tribe retaining royalty interests;Plan is to mine Manh Choh Gold Ore, then truck and process the ore at Kinross’ Fort Knox Milling Complex - Simple plan that reduces execution risk to produce +1Million GEO over 5-year periodProjected Timeline: $19 Million 2021 PGLLC Budget Studies and Permitting in 2021-22 Feasibility in 2022 Construction in 2022/2023 Production in 2024 On-going Exploration

MANH CHOH GOLD PROJECT: Anticipated Economics Using existing infrastructure, the Peak Gold LLC is planning on a a 2024 start dateCapital Costs - Existing infrastructure expected to reduce total capital requirements to ~US$110 million – Recently revised to a range of $105 to $130 million based on recent internal scoping study completed by Kinross2Kinross estimates 1 million oz gold equivalent production over a 4.5-year period equating to roughly 220,000 oz GEO per annum (30% to Contango Ore = 66,000 GEO/Yr)1Average processed grades of approximately of ~6 g/t Au equivalentOperating Costs - Kinross estimates AISC of ~US$750/GEO – Expect operating cost to increase – will be updated with Feasibility study planned for late 2022 14 Model Assumptions: 2 Based on the news releases issued by Kinross Gold Corporation dated September 29, 2020 and then updated after an internal scoping study discussed in a Kinross Corporate update July 28, 2021. The $105 to $130 Million estimate reflects remaining funds to be expended between 2022 and 2024; there may be additional capital required at Fort Knox to accommodate Manh Choh ore that will be charged as a Toll Milling charge to the Peak Gold JV. Non-GAAP financial measure; see Appendix for disclaimers regarding reconciliation. GEO – Gold Equivalent Ounces

15 Health and Safety Manh Choh ProjectZero LTIs

Hiring and Training Local Residents 16

Community Meetings - Tetlin Village TokTanacrossNorthwayMentasta LakeDelta JunctionFairbanks Fox Tanana Chiefs ConferenceDoyon Alaska Chamber & AMA

The project is located 15 km (10 mi) from the Alaska Hwy and 400 km (250 mi) to the Fort Knox Milling Complex 18 MANH CHOH GOLD PROJECT LOCATION PEAK DEPOSIT Image used with permission from Kinross

PEAK GOLD JV 19 Processing ore from the Peak Gold Project at Fort Knox avoids mill construction and is expected to decrease execution risk, lower capital expenditures, drive attractive returns, and reduce the project’s environmental footprint and permitting requirements.Leverages Fort Knox’s successful 25-year history in Alaska, the second largest gold producing State in the USA and one of the world’s top mining jurisdictions3.Project to benefit local communities, particularly the Upper Tanana Athabascan Village of Tetlin; Tetlin Tribe to receive royalties, jobs and training.Project is expected to contribute to the state economy and provide additional employment opportunities and benefits. PROJECT HIGHLIGHTS 3 Based on Fraser Institute Annual Survey of Mining Companies, 2019 report. Images used with permission from Kinross

MANH CHOH GOLD PROJECT Winter Drilling 20

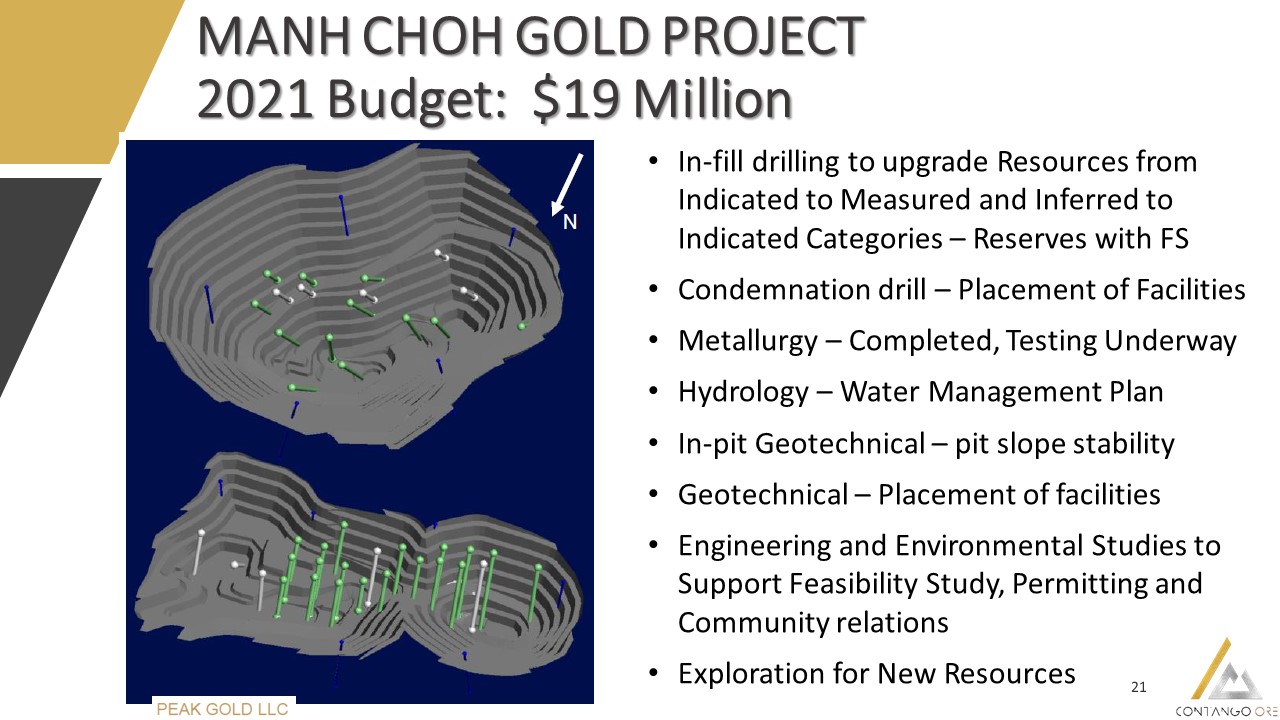

21 MANH CHOH GOLD PROJECT 2021 Budget: $19 Million In-fill drilling to upgrade Resources from Indicated to Measured and Inferred to Indicated Categories – Reserves with FSCondemnation drill – Placement of FacilitiesMetallurgy – Completed, Testing UnderwayHydrology – Water Management PlanIn-pit Geotechnical – pit slope stabilityGeotechnical – Placement of facilitiesEngineering and Environmental Studies to Support Feasibility Study, Permitting and Community relationsExploration for New Resources

22 MANH CHOH GOLD PROJECT Simple Development Plan Two Open Pits with Development Rock /Waste materials adjacent to pitsNo Mill No Tailings FacilityEngineering and Environmental Studies to Support Feasibility Study and Permitting are UnderwayTarget early construction to start in the summer of 2022 and completed by end of 2023Followed by Ramp Up and Full Production in 2024 Preliminary - Under Review

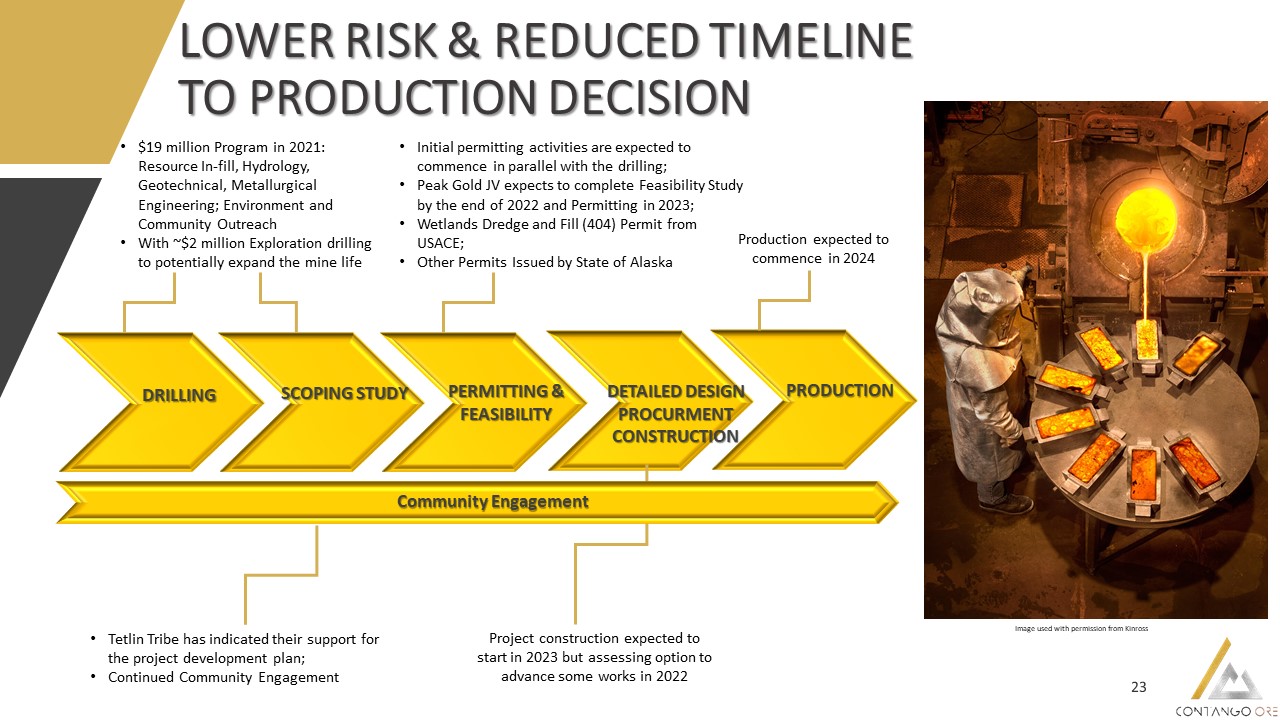

23 LOWER RISK & REDUCED TIMELINE TO PRODUCTION DECISION DRILLING SCOPING STUDY PERMITTING & FEASIBILITY PRODUCTION DETAILED DESIGN PROCURMENTCONSTRUCTION $19 million Program in 2021: Resource In-fill, Hydrology, Geotechnical, Metallurgical Engineering; Environment and Community OutreachWith ~$2 million Exploration drilling to potentially expand the mine life Tetlin Tribe has indicated their support for the project development plan;Continued Community Engagement Initial permitting activities are expected to commence in parallel with the drilling; Peak Gold JV expects to complete Feasibility Study by the end of 2022 and Permitting in 2023;Wetlands Dredge and Fill (404) Permit from USACE; Other Permits Issued by State of Alaska Project construction expected to start in 2023 but assessing option to advance some works in 2022 Production expected to commence in 2024 Image used with permission from Kinross Community Engagement

24 Shamrock 100% Owned SHAMROCK PROPERTY

ASSET SUMMARY 25 Peak Gold Project~(675,000 Acres) State Claims(~160,000 Acres) Contango is a 30% owner of the Peak Gold JV with Kinross owning the remaining 70% and acting as project operatorThe Manh Choh project consists of a ~675,000 acres land package and ~13,423 acres of State Mining ClaimsContango is also the 100% owner of the Alaska state claims exploration land package (~160,000 acres) Peak Gold JV 70% 30% 100% State Mining Claims Part of PGLLC 100% Contango ORE

26 Partnered with Proven OperatorPlan to truck ore to Fort Knox mill simplifies permitting and executionKinross has proven operating experience in Alaska further reducing riskThe plan lowers the required capital and shortens timelines to production by leveraging existing infrastructureHigh grade open pit production expected to result in strong free cash flows Creating Shareholder ValueStrong management that has created significant value for shareholdersPlanned listing on NYSE American Exchange Clear path to production decisionUniquely positioned for growth Growth with Exploration SuccessSignificant exploration potential on the Peak Gold JV lands as well as the 100% owned State of Alaska mining claims adjacent to the future operation DEVELOPING ALASKA’S NEXT GOLD MINE IN PARTNERSHIP WITH KINROSS AND THE TETLIN ALASKA NATIVE TRIBEWITH CONTINUED EXPLORATION TO EXPAND RESOURCES

27 THANK YOU

Corporate Inquires:info@contangoore.com+1-778-386-6227www.contangoore.com OTCQB:CTGO Twitter: @orecontangoLinkedIn: Contango OREInstagram: ContangoOREFacebook: Contango ORE

This presentation contains forward looking estimates of all-in sustaining cost (“AISC”), resources and EBITDA, which are a financial measure not determined in accordance with United States generally accepted accounting principles (“GAAP”). We cannot provide a reconciliation of estimated AISC, resources, EBITDA and cash flow to estimated costs of goods sold, assets and net income, which are the GAAP financial measures most directly comparable to such non-GAAP measures, without unreasonable efforts due to the inherent difficulty and impracticality of quantifying certain amounts that would be required to calculate projected AISC, resources, EBITDA. In addition, the estimates of AISC, resources and EBITDA have been prepared by Kinross and are based on IFRS accounting standards and detailed information to which the Company has not had access to at this time. These amounts that would require unreasonable effort to quantify could be significant, such that the amount of projected GAAP cost of goods sold, assets and net income would vary substantially from the amount of projected AISC, resources and EBITDA. 29 NON-GAAP RECONCILIATION DISCLAIMER APPENDIX