Exhibit 99.1

October 2022 New Orleans Investment Conference Corporate Update Plans for 2022-2024 Exhibit 99.1

FORWARD LOOKING STATEMENT The Feasibility Study (“FS”) referenced herein that relates to Peak Gold, LLC (“Peak Gold”), was prepared by Kinross Gold Corporation (“Kinross”), which controls the Manager of Peak Gold and holds 70% of its outstanding membership interests, in accordance with Canadian National Instrument 43-101 (NI 43-101). CORE owns the remaining 30% membership interest in Peak Gold, and must rely on Kinross and its affiliates for the FS and related information. Further, CORE is not subject to regulation by Canadian regulatory authorities and no Canadian regulatory authority has reviewed the FS or passed upon its accuracy or compliance with NI43-101. The terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” as used in the resource estimate, the FS and this presentation are Canadian mining terms as defined in accordance with NI 43-101. Mining disclosure in the United States was previously required to comply with SEC Industry Guide 7 (“SEC Industry Guide 7”) under the United States Securities Exchange Act of 1934, as amended. The U.S. Securities and Exchange Commission (the “SEC”) adopted final rules to replace SEC Industry Guide 7 with new mining disclosure rules under sub-part 1300 of Regulation S-K of the U.S. Securities Act (“Regulation S-K 1300”) which became mandatory for U.S. reporting companies beginning with the first fiscal year commencing on or after January 1, 2021. Under Regulation S-K 1300, the SEC now recognizes estimates of “Measured Mineral Resources”, “Indicated Mineral Resources” and “Inferred Mineral Resources”. In addition, the SEC has amended its definitions of “Proven Mineral Reserves” and “Probable Mineral Reserves” to be substantially similar to international standards. CORE is in the process of preparing a Regulation S-K 1300 compliant feasibility study. Investors are cautioned that while the above terms are “substantially similar” to the NI 43-101 definitions, there are differences in the definitions under Regulation S-K 1300 and NI 43-101. Accordingly, there is no assurance any mineral reserves or mineral resources that CORE may report as “probable mineral reserves”, “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources” under NI 43-101 would be the same had CORE prepared the mineral reserve or mineral resource estimates under the standards adopted under Regulation S-K 1300. U.S. investors are also cautioned that while the SEC recognizes “measured mineral resources”, “indicated mineral resources” and “inferred mineral resources” under Regulation S-K 1300, investors should not assume that any part or all of the mineralization in these categories will ever be converted into a higher category of mineral resources or into mineral reserves. Mineralization described using these terms has a greater degree of uncertainty as to its existence and feasibility than mineralization that has been characterized as reserves. Accordingly, investors are cautioned not to assume that any measured mineral resources, indicated mineral resources or inferred mineral resources that CORE's reports are or will be economically or legally mineable. Please see the CORE's press release dated July 28, 2022 and Kinross' press release dated July 26, 2022 for more detail regarding the FS. 2

The Preliminary Economic Assessment (“PEA”) referenced herein was prepared in accordance with Canadian National Instrument 43-101 (NI 43-101). CORE is not subject to regulation by Canadian regulatory authorities and no Canadian regulatory authority has reviewed the PEA or passed upon its accuracy or compliance with NI43-101. The terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” as used in the resource estimate, the PEA and this presentation are Canadian mining terms as defined in accordance with NI 43-101; however, these terms are not defined terms under the U.S. Securities and Exchange Commission’s (“SEC’s”) Industry Guide 7 and are normally not permitted to be used in reports and registration statements filed with the SEC. The estimation of measured resources and indicated resources involves greater uncertainty as to their existence and the legal and economic feasibility of extraction than the estimation of proven and probable reserves. Conversion of mineral resources to proven and probable mineral reserves generally requires a further economic study, such as a preliminary feasibility study. The PEA is not a preliminary feasibility study and does not support an estimate of proven and probable mineral reserves. Investors are cautioned not to assume that all or any part of an inferred mineral resource exists or is economically or legally mineable. Investors are also cautioned not to assume that all or any part of measured or indicated resources will ever be converted into mineral reserves. In addition, the SEC normally only permits issuers to report mineralization that does not constitute mineral reserves as in-place tonnage of mineralized material and grade without reference to unit amounts of metal. Please see the Company’s press release dated September 24, 2018 for more detail regarding the PEA. 3 CAUTIONARY NOTE REGARDING ESTIMATES OF MEASURED, INDICATED AND INFERRED RESOURCES

Developing Alaska’s Next Gold Mines Manh Choh – Development Stage Project under construction in partnership with Kinross (70%) and the Alaska Native Tetlin Tribe (Royalty) 100% Owned Lucky Shot Mine – Exploring historic high-grade gold mine Three Early-Stage Exploration Projects: Shamrock Eagle-Hona Triple Z 4

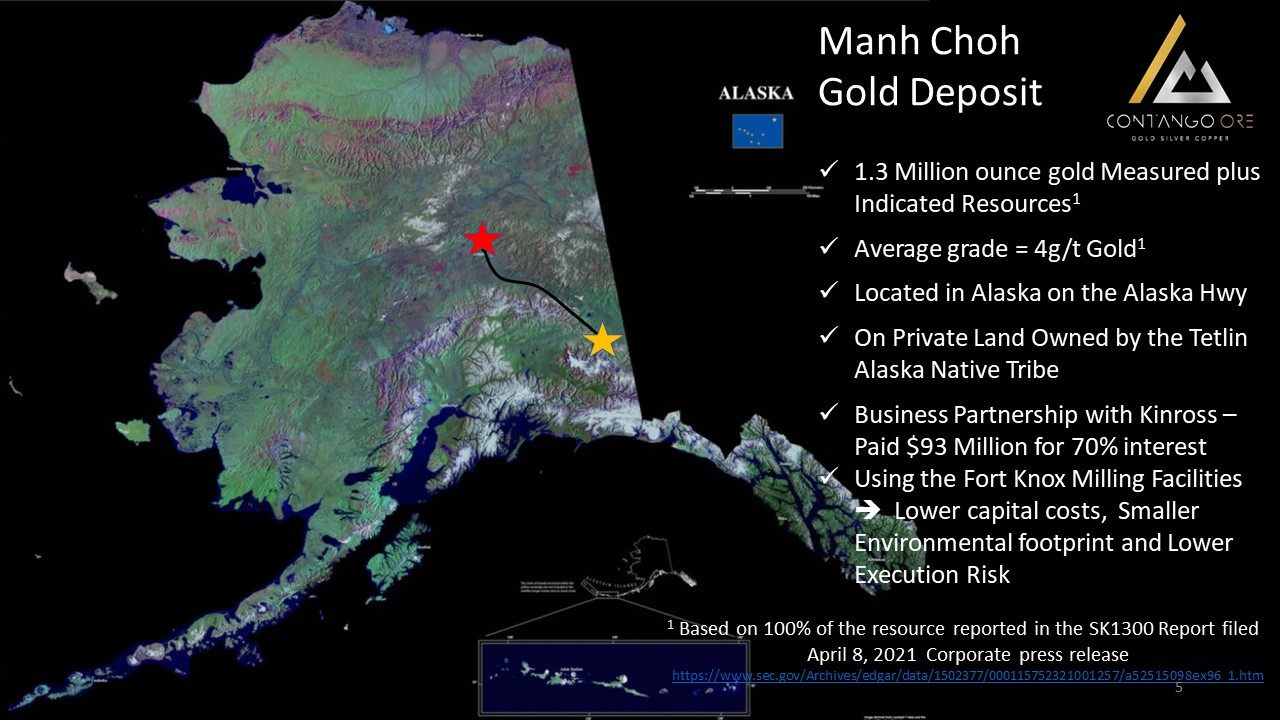

Manh Choh Gold Deposit 1.3 Million ounce gold Measured plus Indicated Resources1 Average grade = 4g/t Gold1 Located in Alaska on the Alaska Hwy On Private Land Owned by the Tetlin Alaska Native Tribe Business Partnership with Kinross – Paid $93 Million for 70% interest Using the Fort Knox Milling Facilities Lower capital costs, Smaller Environmental footprint and Lower Execution Risk 1 Based on 100% of the resource reported in the SK1300 Report filed April 8, 2021 Corporate press release https://www.sec.gov/Archives/edgar/data/1502377/000115752321001257/a52515098ex96_1.htm 5

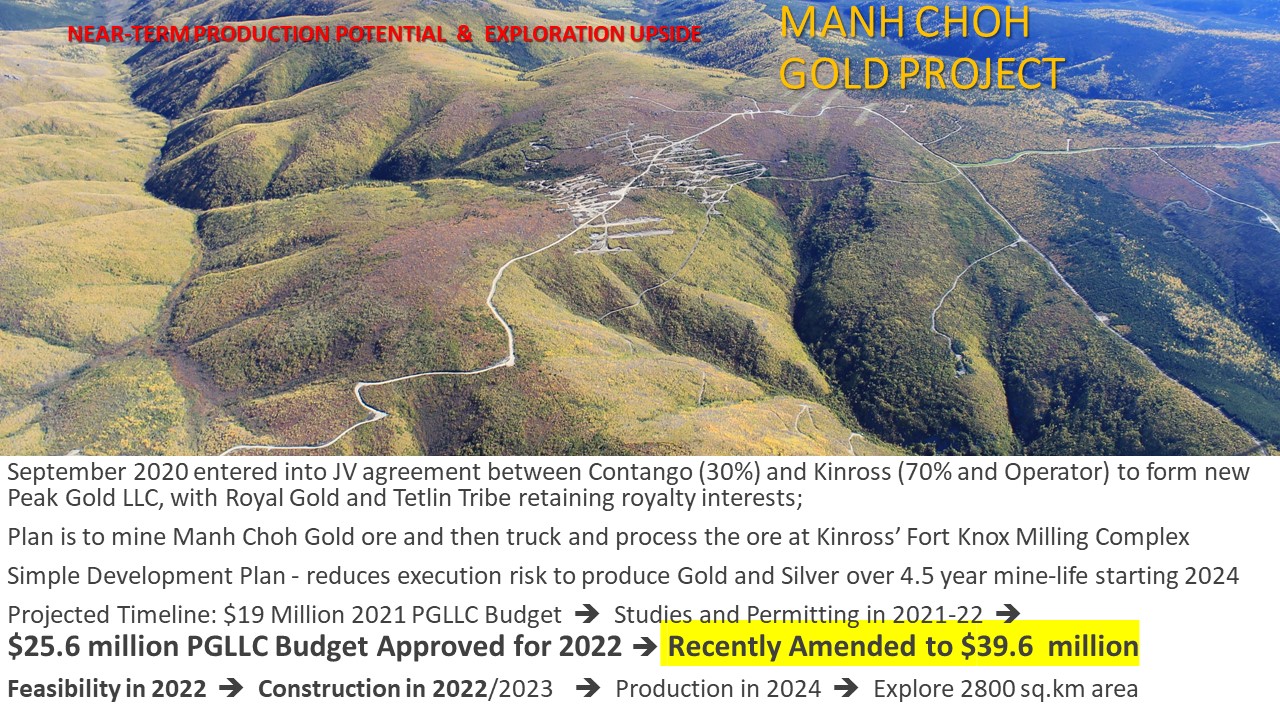

NEAR-TERM PRODUCTION POTENTIAL & EXPLORATION UPSIDE 6 MANH CHOH GOLD PROJECT NYSE-A:CTGO September 2020 entered into JV agreement between Contango (30%) and Kinross (70% and Operator) to form new Peak Gold LLC, with Royal Gold and Tetlin Tribe retaining royalty interests; Plan is to mine Manh Choh Gold ore and then truck and process the ore at Kinross’ Fort Knox Milling Complex Simple Development Plan - reduces execution risk to produce Gold and Silver over 4.5 year mine-life starting 2024 Projected Timeline: $19 Million 2021 PGLLC Budget Studies and Permitting in 2021-22 $25.6 million PGLLC Budget Approved for 2022 Recently Amended to $39.6 million Feasibility in 2022 Construction in 2022/2023 Production in 2024 Explore 2800 sq.km area

MANH CHOH GOLD PROJECT: Anticipated Economics Using existing infrastructure at Fort Knox, Peak Gold LLC is planning on a 2024 start date Kinross estimates 914,000 GEO production over a 4.5-years equating to roughly 225,000 GEO per annum (30% to Contango Ore = 67,500 GEO/Yr)1 Using elevated cut-off grade - Average processed grades expected to be ~8 g/t Au Capital Costs - Existing infrastructure expected to reduce start-up capital requirements $182 million (including $21M Contingency) based on Q2 2022 Feasibility Study1 Manager has recommended an additional contingency of $18 million to cover potential inflationary pressures – Contango’s Share $60 million Operating Costs - Kinross estimates AISC of ~US$900/GEO1 Contango AISC pending analysis 7 Model Assumptions: per Kinross Disclosure1 1 Based on Kinross Gold Corporation “Q2 Corporate Update ” presentation dated July 27, 2022; Initial capex reflects the feasibility study completed in 2022; The optimization for the mineral reserve estimate assumed a $1,300 per ounce gold price; the $182 Million estimate reflects remaining funds to be expended between 2022 and 2024; there will be additional capital required at Fort Knox to accommodate Manh Choh ore; and there will be a Toll Milling charge to the Peak Gold JV; "All-in sustaining cost (AISC) per equivalent ounce sold“ is a non-GAAP ratio. see Appendix for disclaimers regarding reconciliation. “GEO” refers to Gold Equivalent Ounces.

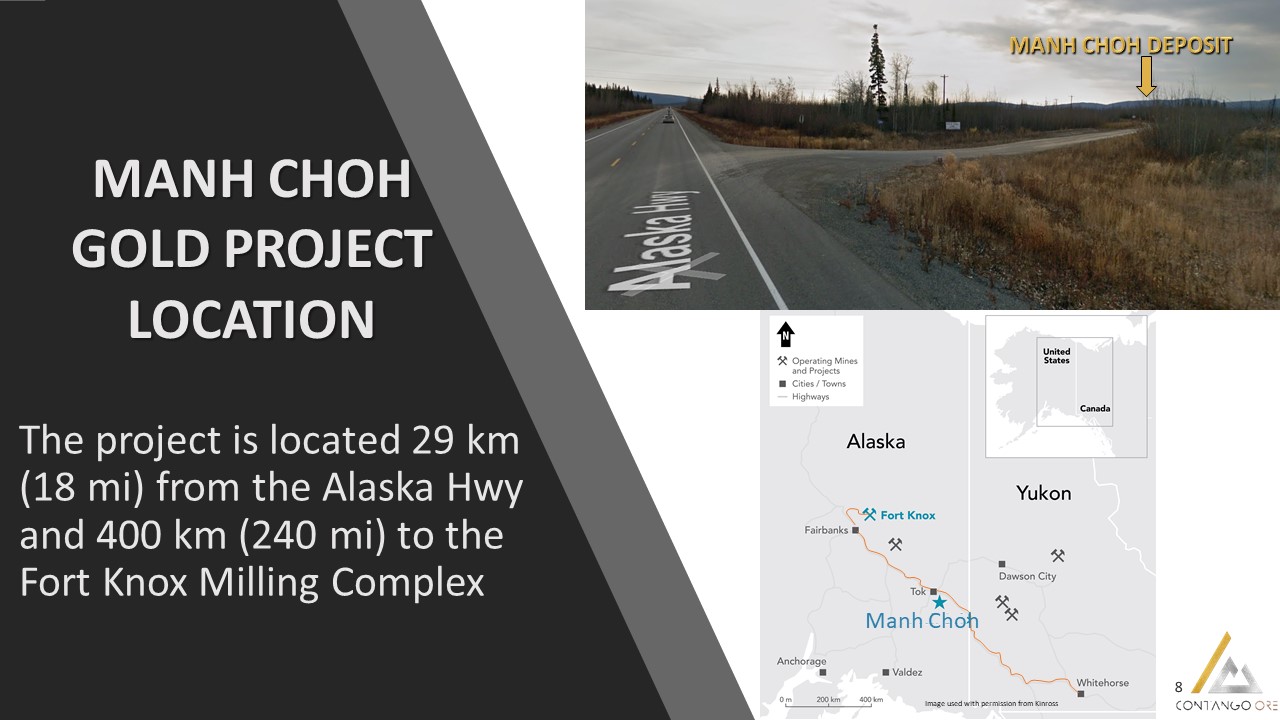

The project is located 29 km (18 mi) from the Alaska Hwy and 400 km (240 mi) to the Fort Knox Milling Complex 8 MANH CHOH GOLD PROJECT LOCATION MANH CHOH DEPOSIT Image used with permission from Kinross Manh Choh

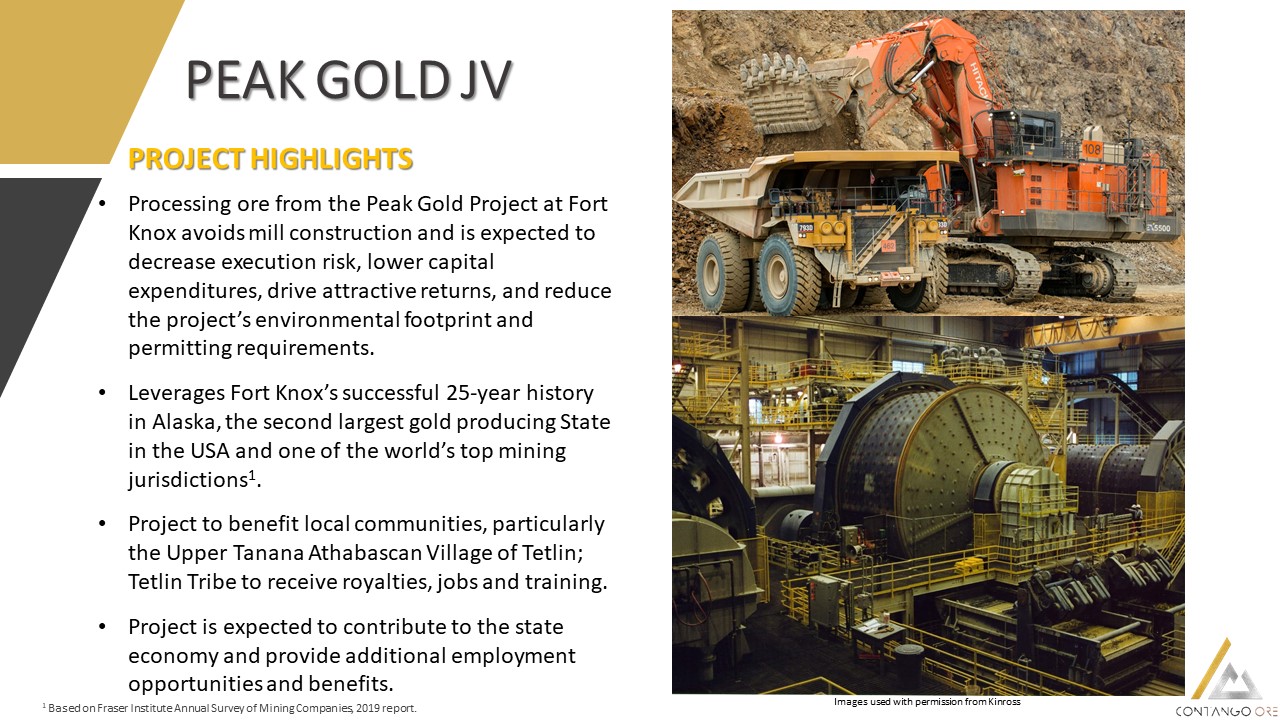

PEAK GOLD JV 9 Processing ore from the Peak Gold Project at Fort Knox avoids mill construction and is expected to decrease execution risk, lower capital expenditures, drive attractive returns, and reduce the project’s environmental footprint and permitting requirements. Leverages Fort Knox’s successful 25-year history in Alaska, the second largest gold producing State in the USA and one of the world’s top mining jurisdictions1. Project to benefit local communities, particularly the Upper Tanana Athabascan Village of Tetlin; Tetlin Tribe to receive royalties, jobs and training. Project is expected to contribute to the state economy and provide additional employment opportunities and benefits. PROJECT HIGHLIGHTS 1 Based on Fraser Institute Annual Survey of Mining Companies, 2019 report. Images used with permission from Kinross

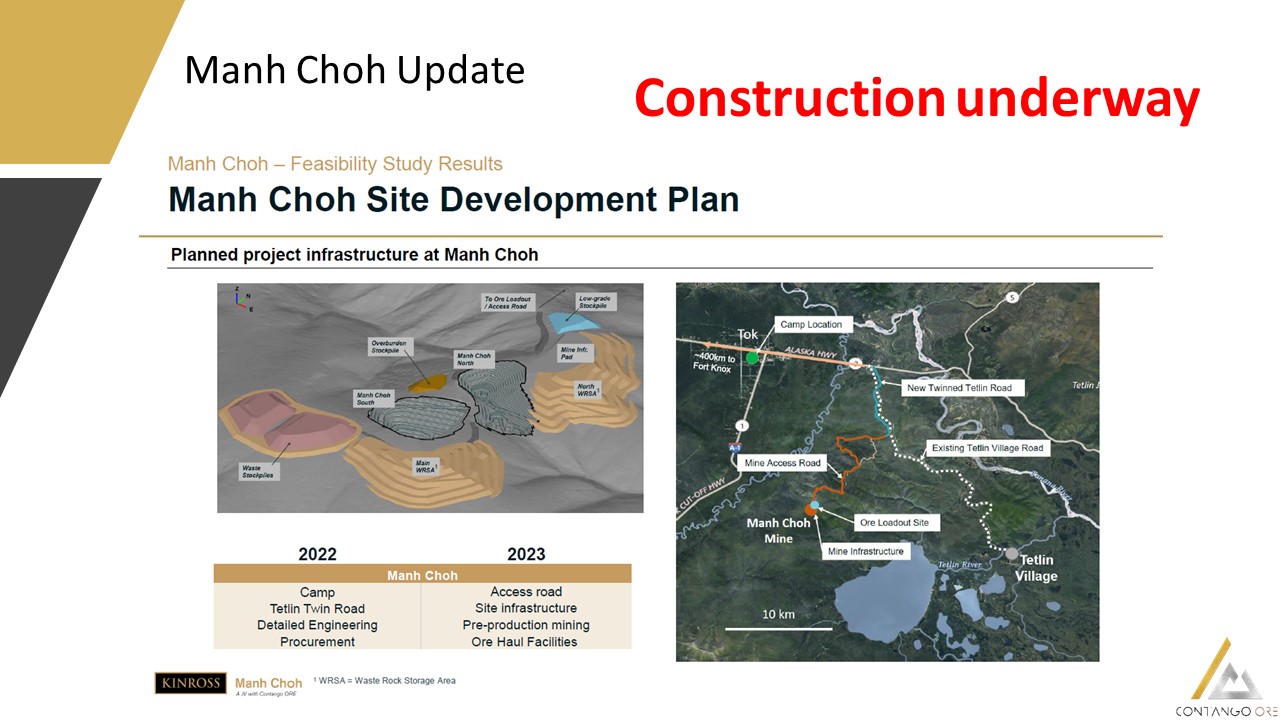

10 Manh Choh Update Construction underway

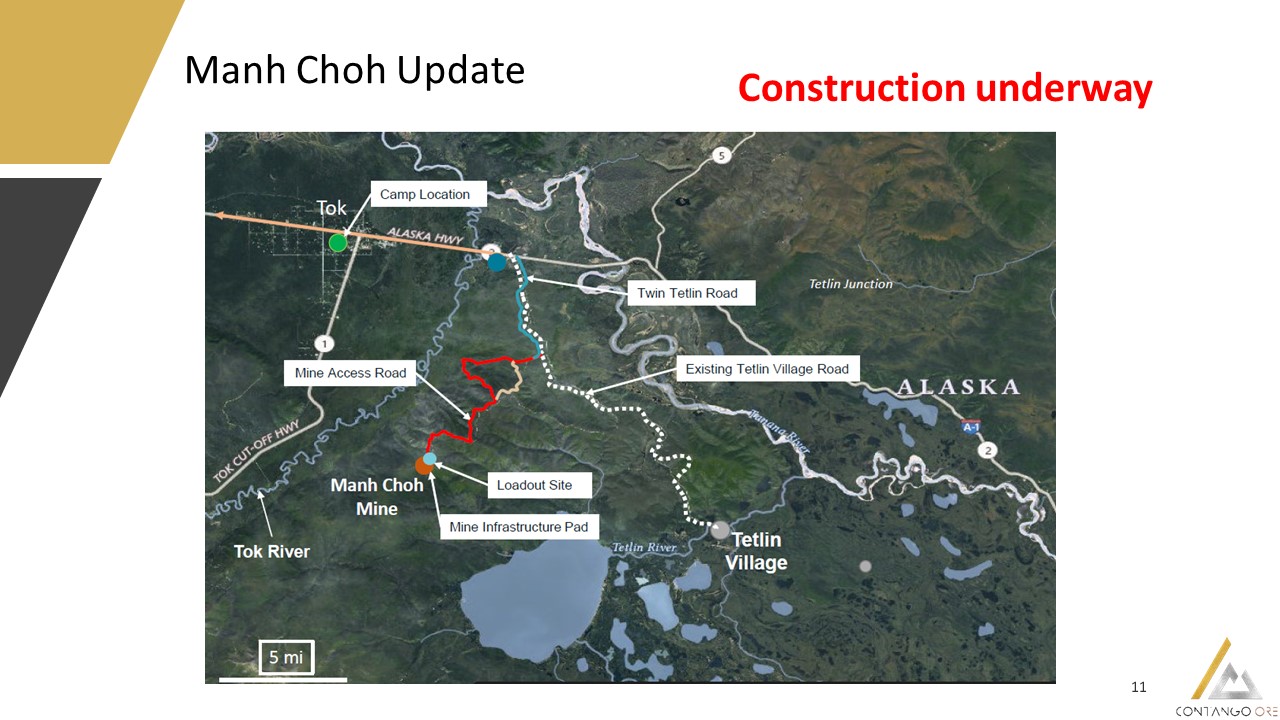

11 Manh Choh Update Construction underway

12 Manh Choh Update - Construction underway

13 Manh Choh Update - Construction underway

14 Manh Choh Update - Construction underway

15 Manh Choh Update – Camp Construction underway

16 Manh Choh Update – Camp Construction underway

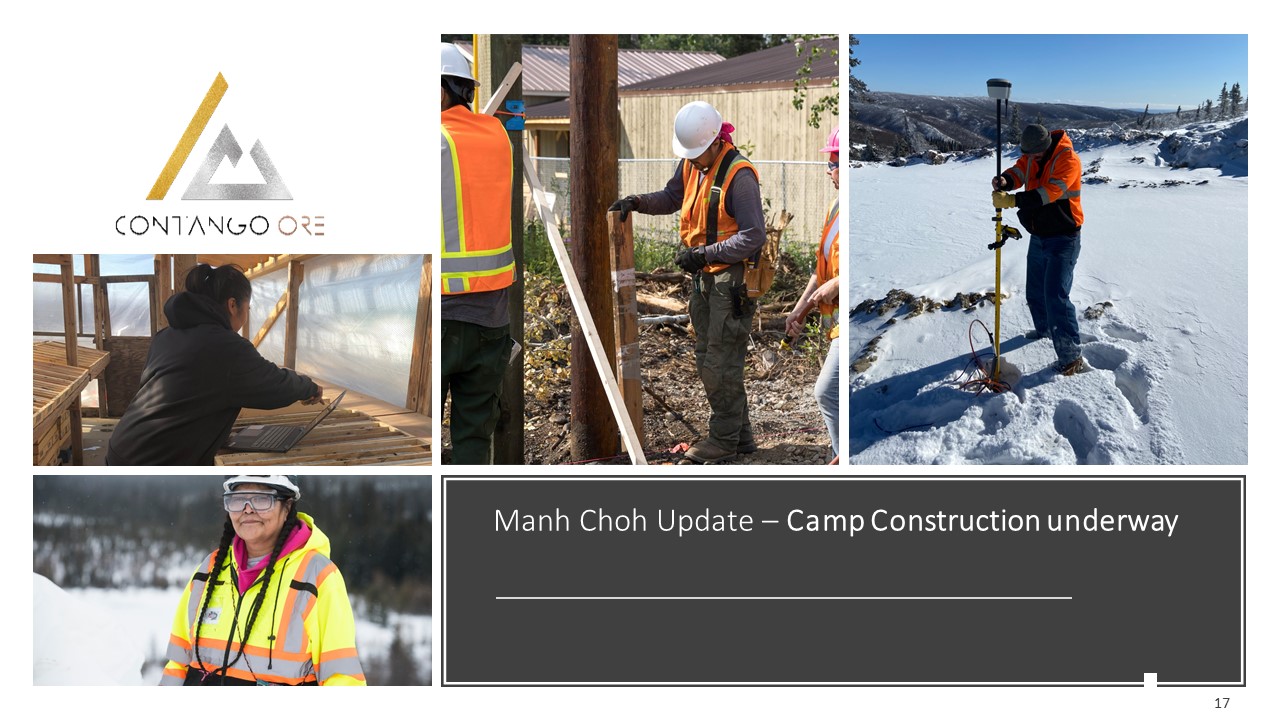

Manh Choh Update – Camp Construction underway 17

18 Manh Choh Update – Community Engagement

19 MANH CHOH GOLD PROJECT Benefits to Alaska Residents and Businesses with smaller Environmental Footprint McKinley Research confirms jobs, economic boost to Tok, road and infrastructure enhancements, and taxes: • 250 to 300 new Construction jobs • 400 to 600 direct Mine and Trucking jobs plus indirect and induced jobs (2X) • The average annual wage estimated at $130,000 + benefits • Once in production, Manh Choh will be the second largest private employer in SE Fairbanks area • Manh Choh plans to purchase +$500 Million of goods and services in Alaska over 4.5 year mine life • The Native Village of Tetlin will earn royalties • Construction of a new cellular tower to support mine operations will benefit local communities • Manh Choh is expected to donate several million dollars to local community benefits, such as investment in training, education, scholarships, or sponsorships

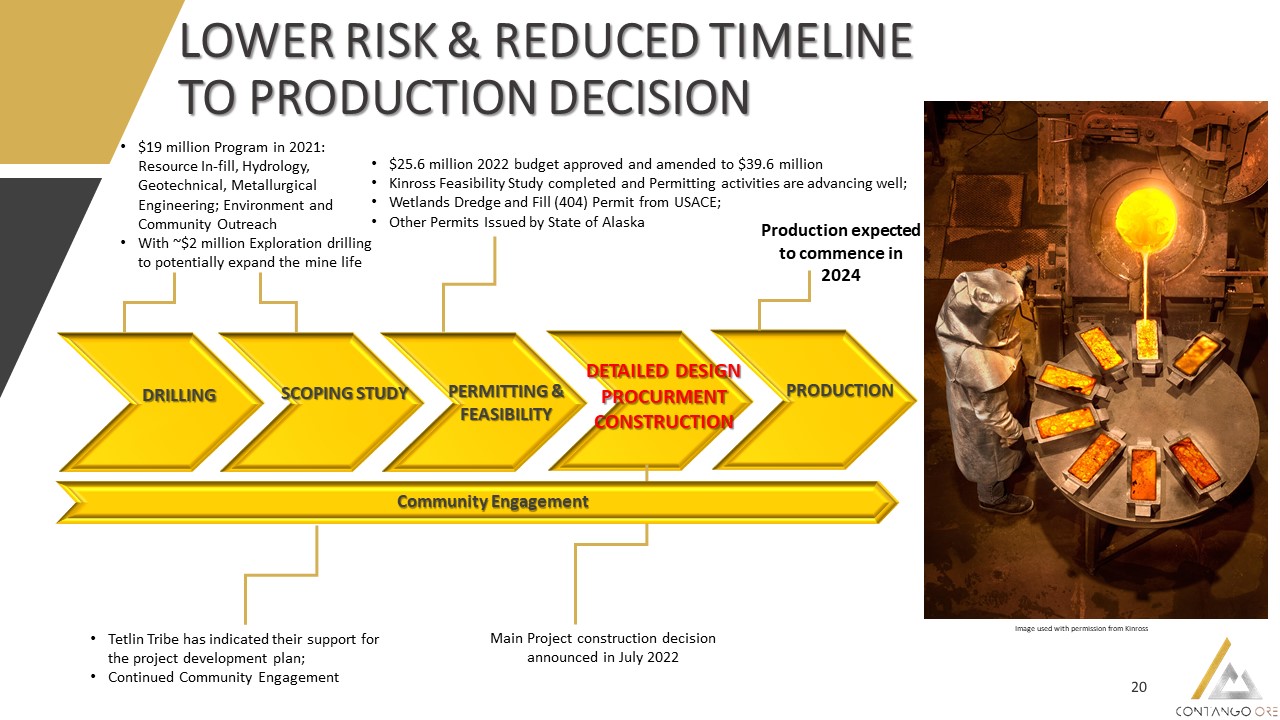

20 LOWER RISK & REDUCED TIMELINE TO PRODUCTION DECISION DRILLING SCOPING STUDY PERMITTING & FEASIBILITY PRODUCTION DETAILED DESIGN PROCURMENT CONSTRUCTION $19 million Program in 2021: Resource In-fill, Hydrology, Geotechnical, Metallurgical Engineering; Environment and Community Outreach With ~$2 million Exploration drilling to potentially expand the mine life Tetlin Tribe has indicated their support for the project development plan; Continued Community Engagement $25.6 million 2022 budget approved and amended to $39.6 million Kinross Feasibility Study completed and Permitting activities are advancing well; Wetlands Dredge and Fill (404) Permit from USACE; Other Permits Issued by State of Alaska Main Project construction decision announced in July 2022 Production expected to commence in 2024 Image used with permission from Kinross Community Engagement

PEAK GOLD LLC 21 Exploration Highlights Completed ~$3.0 million exploration program Q4 2020 primarily directed at metallurgical and geotechnical drilling, and on-going environmental studies to advance feasibility and permitting Completed ~$3 million in 2021 exploration program and conducted resource in-fill and condemnation drilling, hydrology, geotechnical metallurgy studies along with engineering and environmental studies to support completion of a feasibility and permitting. 528 Core and RC holes in the database with 394 drill holes used for modeling is including 69,574 m (228,260 ft) of assays. Approved $3 million exploration program to complete regional stream sediment and pan concentrate sample, geologic reconnaissance with 1,348 samples collected (607 stream sediment, 518 soils, and 223 rocks) and approximately 8500 ft (2600 meter) drill program on Chief Danny area targets OPEN

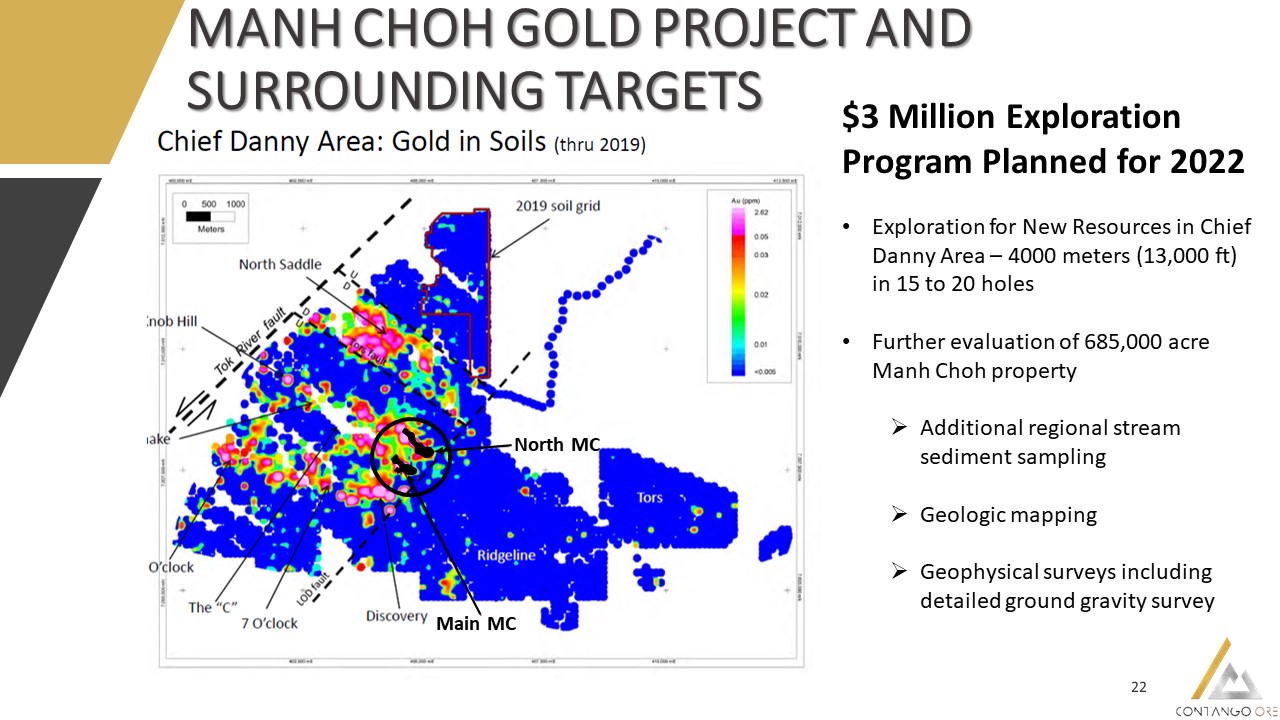

22 MANH CHOH GOLD PROJECT AND SURROUNDING TARGETS Main MC North MC $3 Million Exploration Program Planned for 2022 Exploration for New Resources in Chief Danny Area – 4000 meters (13,000 ft) in 15 to 20 holes Further evaluation of 685,000 acre Manh Choh property Additional regional stream sediment sampling Geologic mapping Geophysical surveys including detailed ground gravity survey

ASSET SUMMARY 23 Peak Gold Project ~(675,000 Acres) State Claims (~160,000 Acres) The Manh Choh project consists of a ~685,000 acres land package including ~13,423 acres of State Mining Claims Roughly the size of Rhode Island Contango is also the 100% owner of the Alaska state claims exploration land package (~160,000 acres) Peak Gold JV 70% 30% 100% State Mining Claims Part of PGLLC 100% Contango ORE

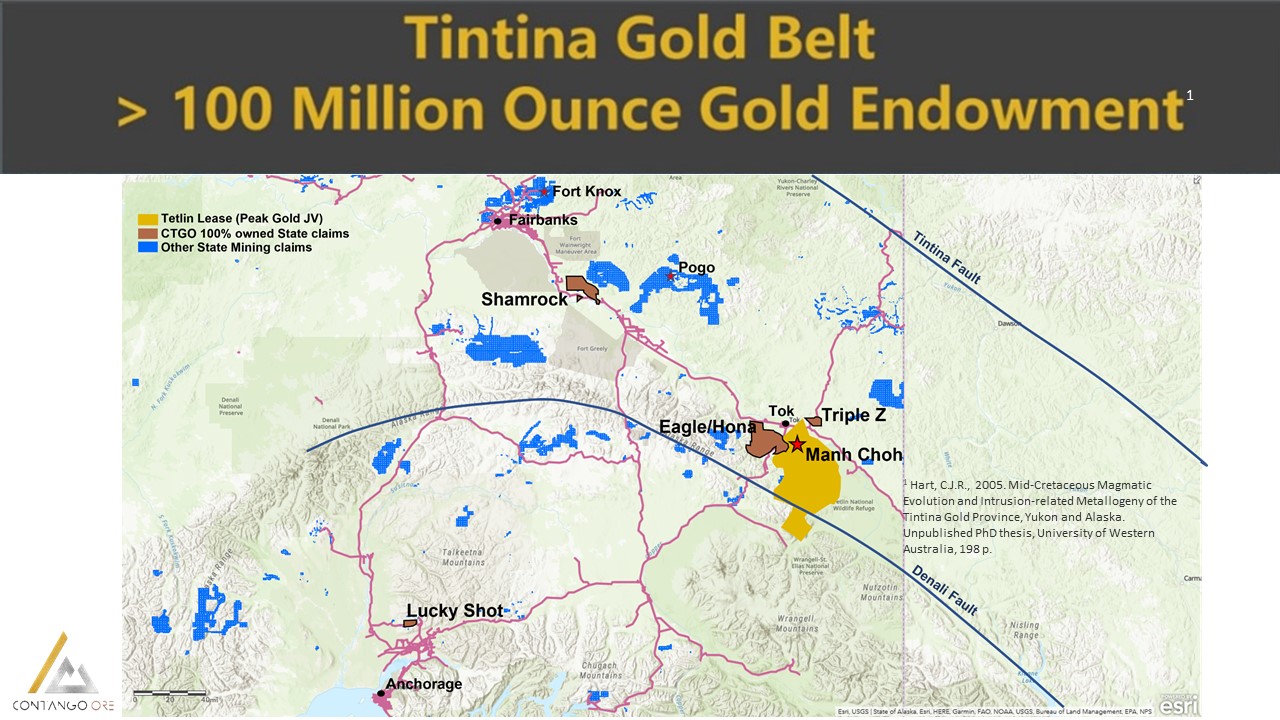

24 1 Hart, C.J.R., 2005. Mid-Cretaceous Magmatic Evolution and Intrusion-related Metallogeny of the Tintina Gold Province, Yukon and Alaska. Unpublished PhD thesis, University of Western Australia, 198 p. 1

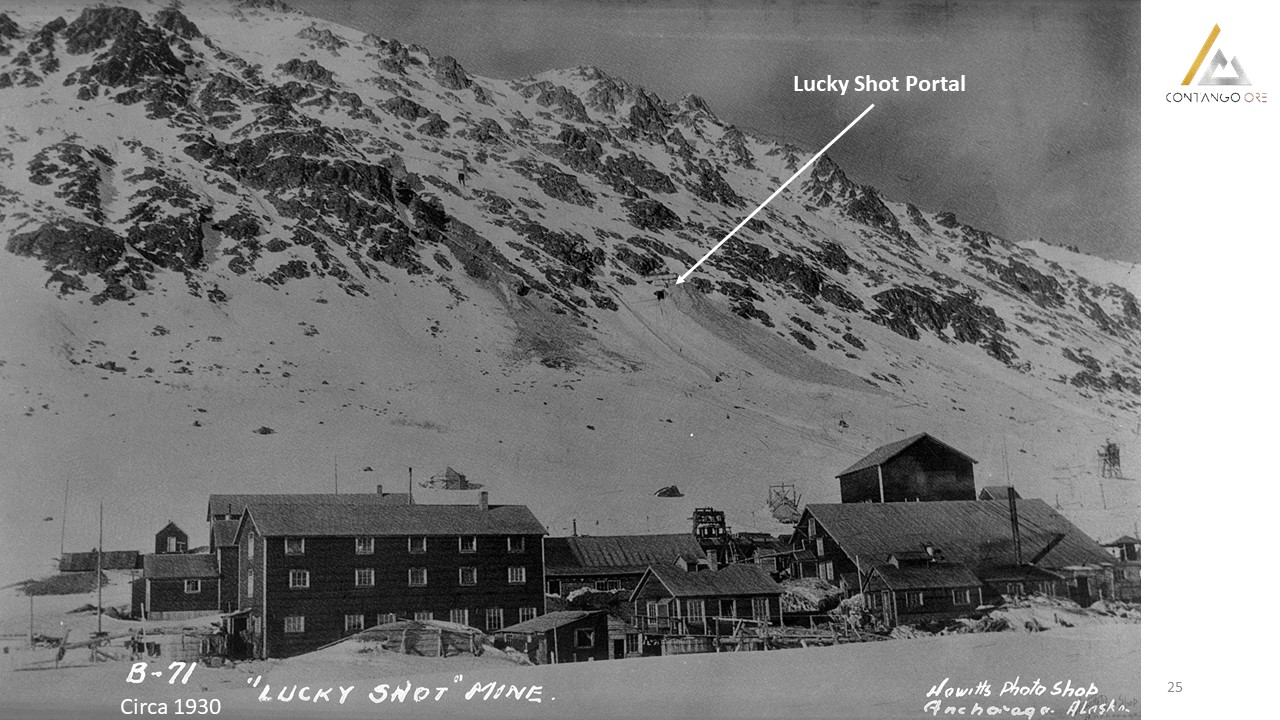

Lucky Shot Portal Circa 1930 25

Lucky Shot Portal Circa 1930 26

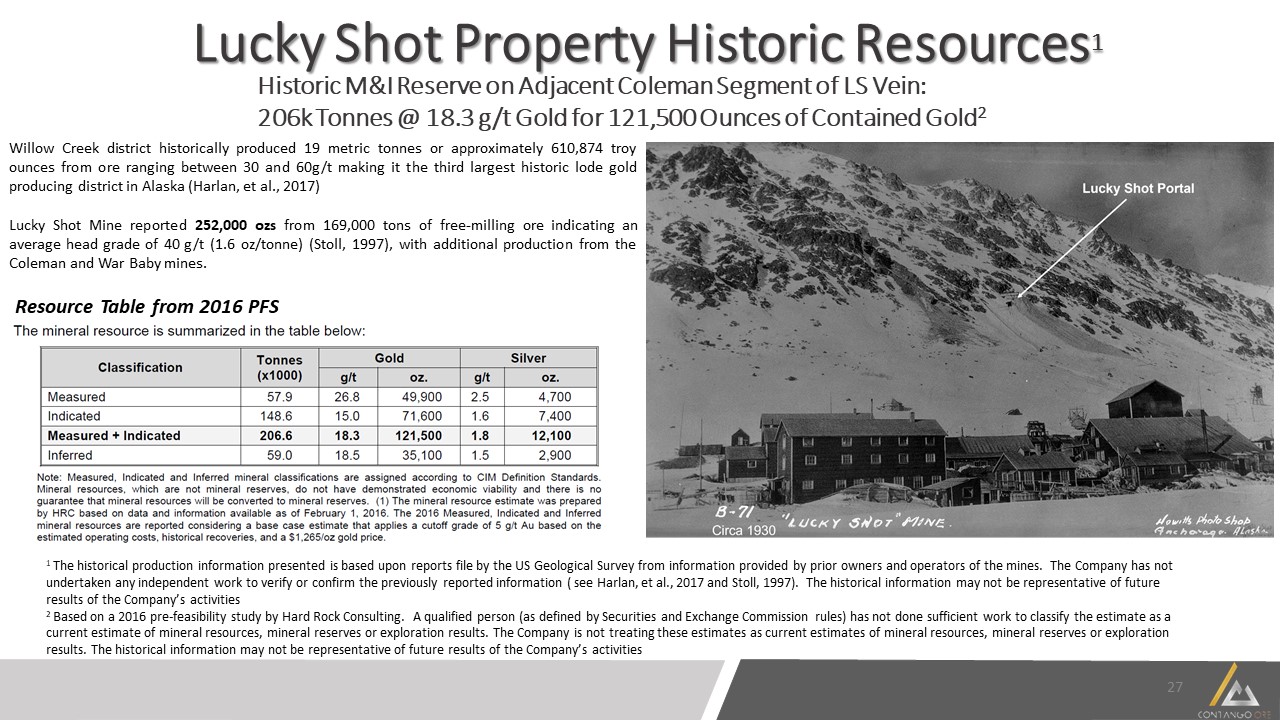

Lucky Shot Property Historic Resources1 Historic M&I Reserve on Adjacent Coleman Segment of LS Vein: 206k Tonnes @ 18.3 g/t Gold for 121,500 Ounces of Contained Gold2 1 The historical production information presented is based upon reports file by the US Geological Survey from information provided by prior owners and operators of the mines. The Company has not undertaken any independent work to verify or confirm the previously reported information ( see Harlan, et al., 2017 and Stoll, 1997). The historical information may not be representative of future results of the Company’s activities 2 Based on a 2016 pre-feasibility study by Hard Rock Consulting. A qualified person (as defined by Securities and Exchange Commission rules) has not done sufficient work to classify the estimate as a current estimate of mineral resources, mineral reserves or exploration results. The Company is not treating these estimates as current estimates of mineral resources, mineral reserves or exploration results. The historical information may not be representative of future results of the Company’s activities Willow Creek district historically produced 19 metric tonnes or approximately 610,874 troy ounces from ore ranging between 30 and 60g/t making it the third largest historic lode gold producing district in Alaska (Harlan, et al., 2017) Lucky Shot Mine reported 252,000 ozs from 169,000 tons of free-milling ore indicating an average head grade of 40 g/t (1.6 oz/tonne) (Stoll, 1997), with additional production from the Coleman and War Baby mines. Resource Table from 2016 PFS 27

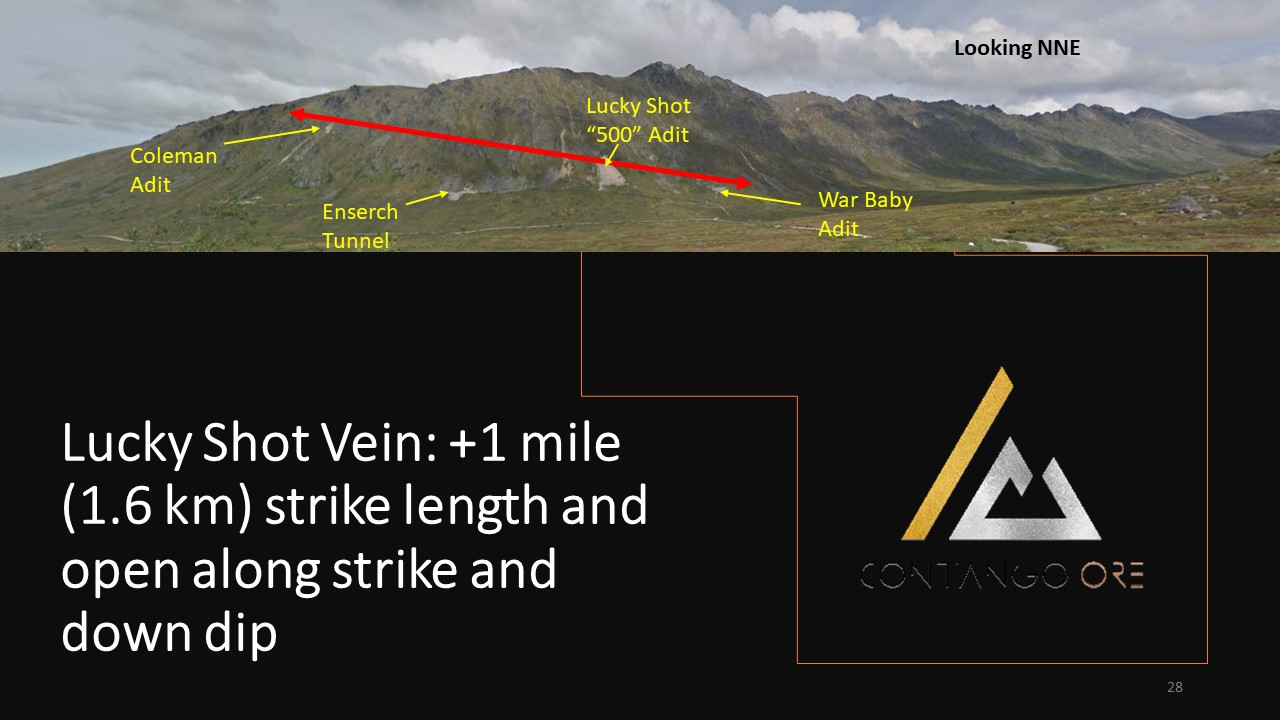

Lucky Shot Vein: +1 mile (1.6 km) strike length and open along strike and down dip 28 Coleman Adit Lucky Shot “500” Adit War Baby Adit Looking NNE Enserch Tunnel

29

30

31

Lucky Shot Update - Safety First Approach 32

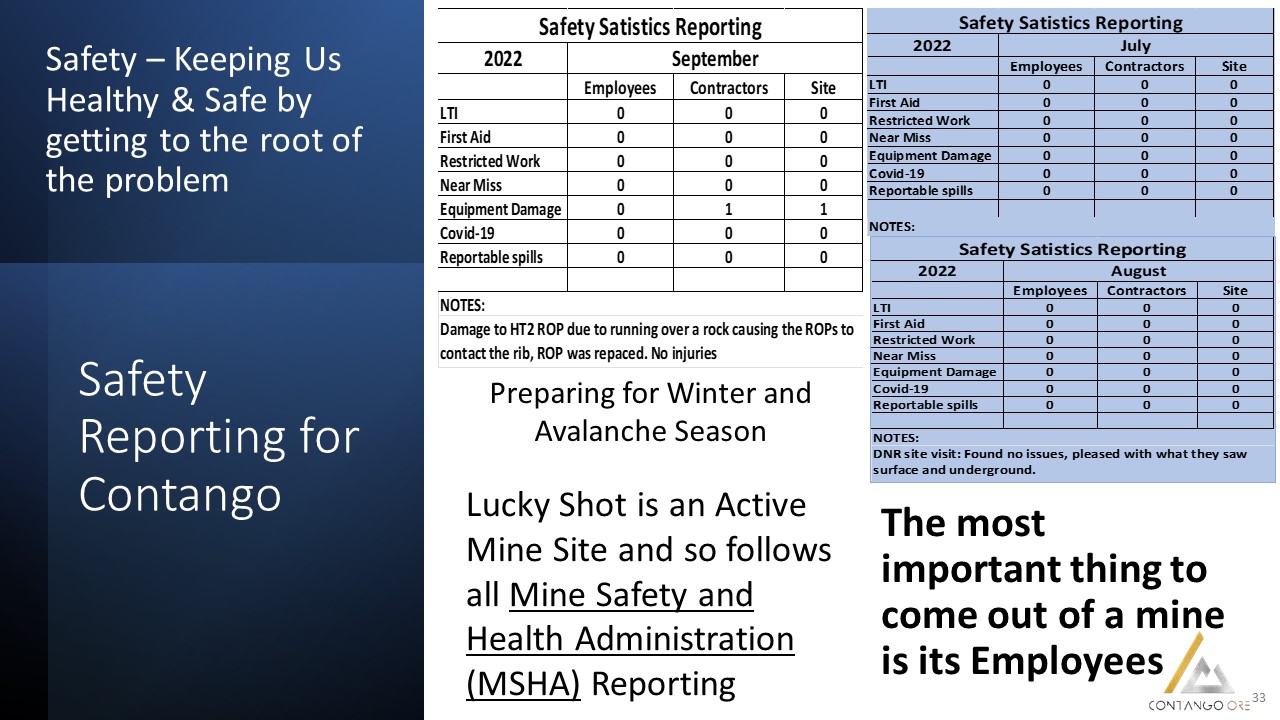

Safety Reporting for Contango Safety – Keeping Us Healthy & Safe by getting to the root of the problem 33 Lucky Shot is an Active Mine Site and so follows all Mine Safety and Health Administration (MSHA) Reporting Preparing for Winter and Avalanche Season The most important thing to come out of a mine is its Employees

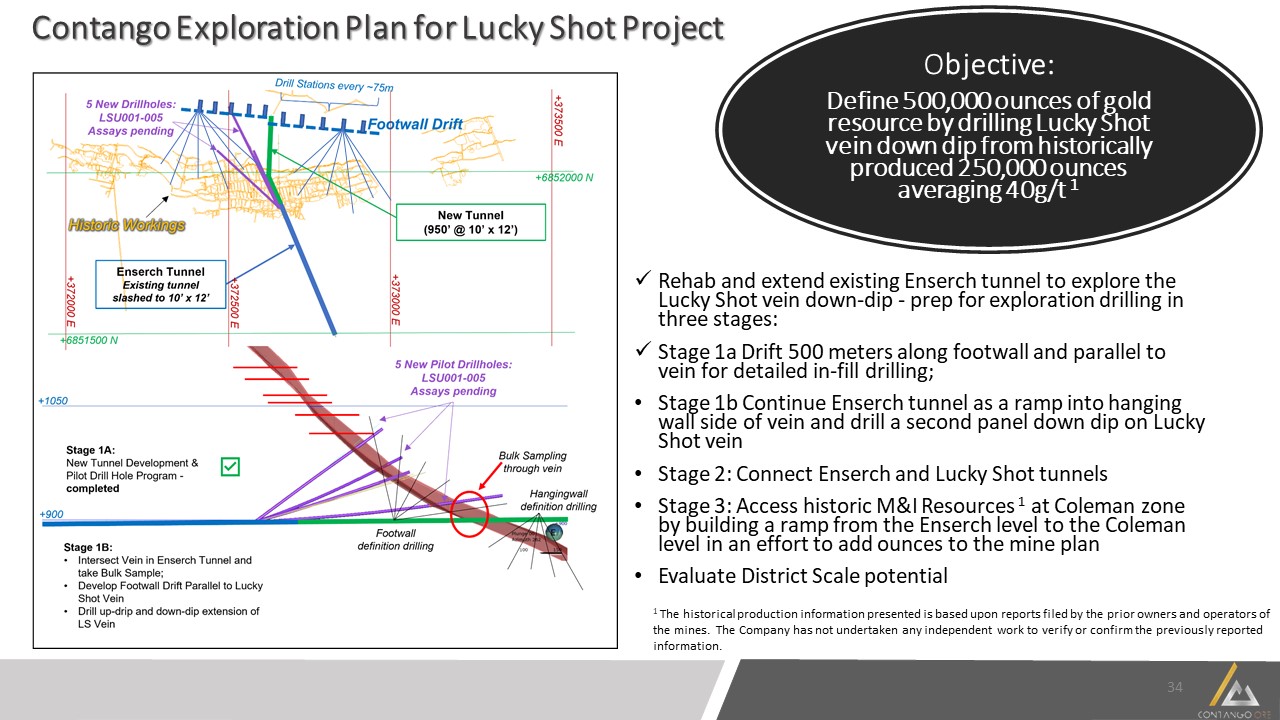

Contango Exploration Plan for Lucky Shot Project Rehab and extend existing Enserch tunnel to explore the Lucky Shot vein down-dip - prep for exploration drilling in three stages: Stage 1a Drift 500 meters along footwall and parallel to vein for detailed in-fill drilling; Stage 1b Continue Enserch tunnel as a ramp into hanging wall side of vein and drill a second panel down dip on Lucky Shot vein Stage 2: Connect Enserch and Lucky Shot tunnels Stage 3: Access historic M&I Resources 1 at Coleman zone by building a ramp from the Enserch level to the Coleman level in an effort to add ounces to the mine plan Evaluate District Scale potential Objective: Define 500,000 ounces of gold resource by drilling Lucky Shot vein down dip from historically produced 250,000 ounces averaging 40g/t 1 34 1 The historical production information presented is based upon reports filed by the prior owners and operators of the mines. The Company has not undertaken any independent work to verify or confirm the previously reported information.

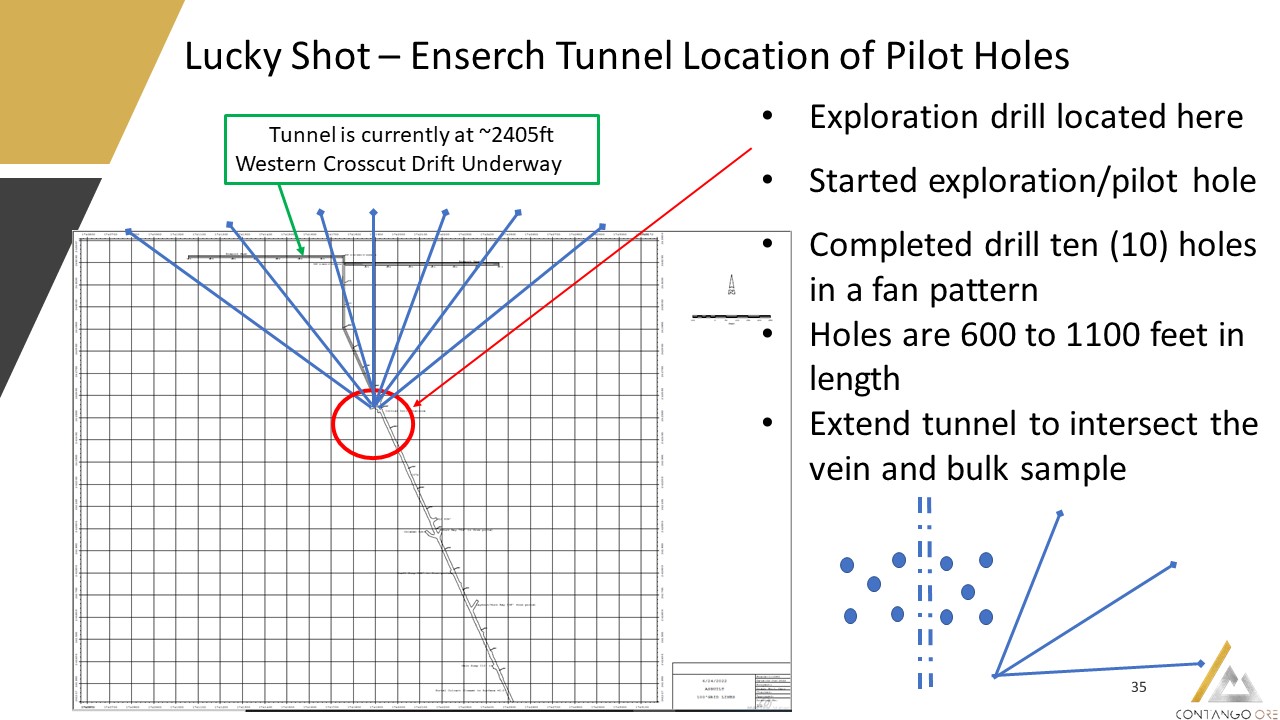

35 Lucky Shot – Enserch Tunnel Location of Pilot Holes Exploration drill located here Started exploration/pilot hole Completed drill ten (10) holes in a fan pattern Holes are 600 to 1100 feet in length Extend tunnel to intersect the vein and bulk sample Tunnel is currently at ~2405ft Western Crosscut Drift Underway

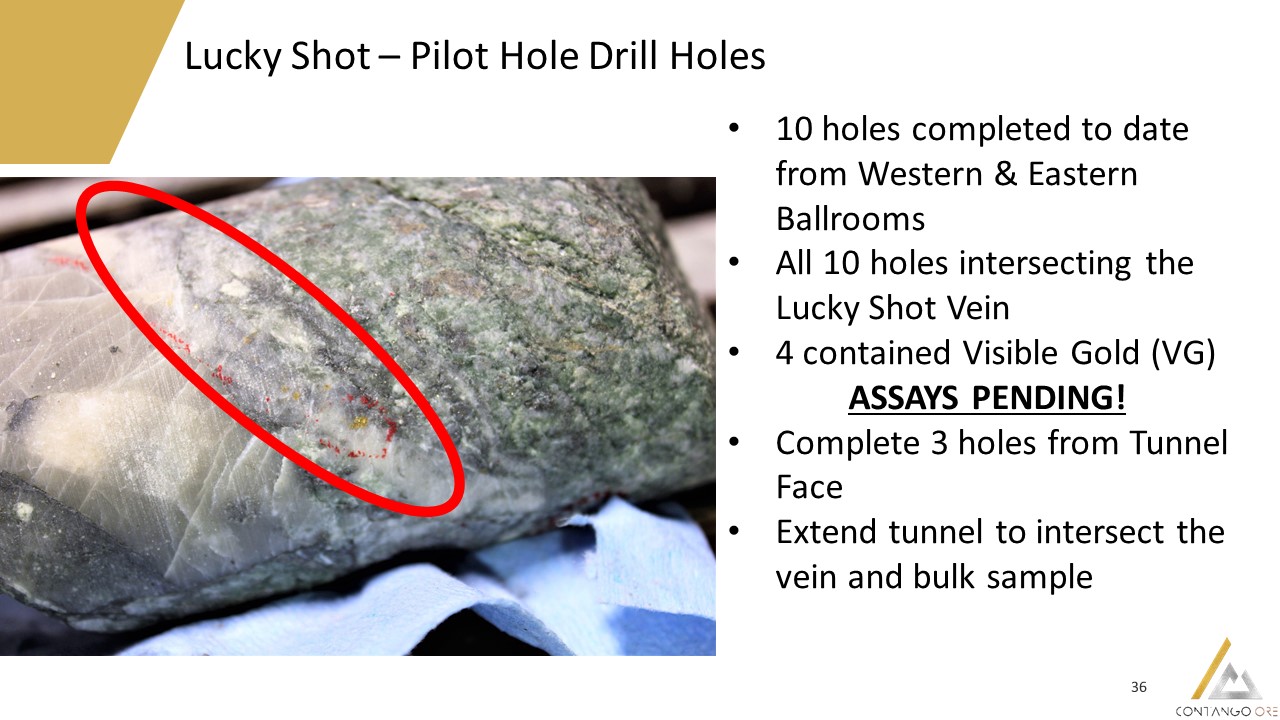

36 Lucky Shot – Pilot Hole Drill Holes 10 holes completed to date from Western & Eastern Ballrooms All 10 holes intersecting the Lucky Shot Vein 4 contained Visible Gold (VG) ASSAYS PENDING! Complete 3 holes from Tunnel Face Extend tunnel to intersect the vein and bulk sample

Fault Lucky Shot vein VG VG VG VG

38 Partnered with Proven Operator Plan to truck ore to Fort Knox mill simplifies permitting and execution Kinross has proven operating experience in Alaska further reducing risk The plan lowers the required capital and shortens timelines to production by leveraging existing infrastructure High grade open pit production expected to result in strong free cash flows Creating Shareholder Value Strong management that has created significant value for shareholders Planned listing on NYSE American Exchange Clear path to production decision Uniquely positioned for growth Growth with Exploration Success Significant exploration potential on the Peak Gold JV lands as well as the 100% owned State of Alaska mining claims adjacent to the future operation DEVELOPING ALASKA’S NEXT GOLD MINES IN PARTNERSHIP WITH KINROSS AND THE TETLIN ALASKA NATIVE TRIBE WITH CONTINUED EXPLORATION TO EXPAND RESOURCES

39 THANK YOU

Lucky Shot – Underground Development to support 2022 Exploration Program and Year-Round Operations 41

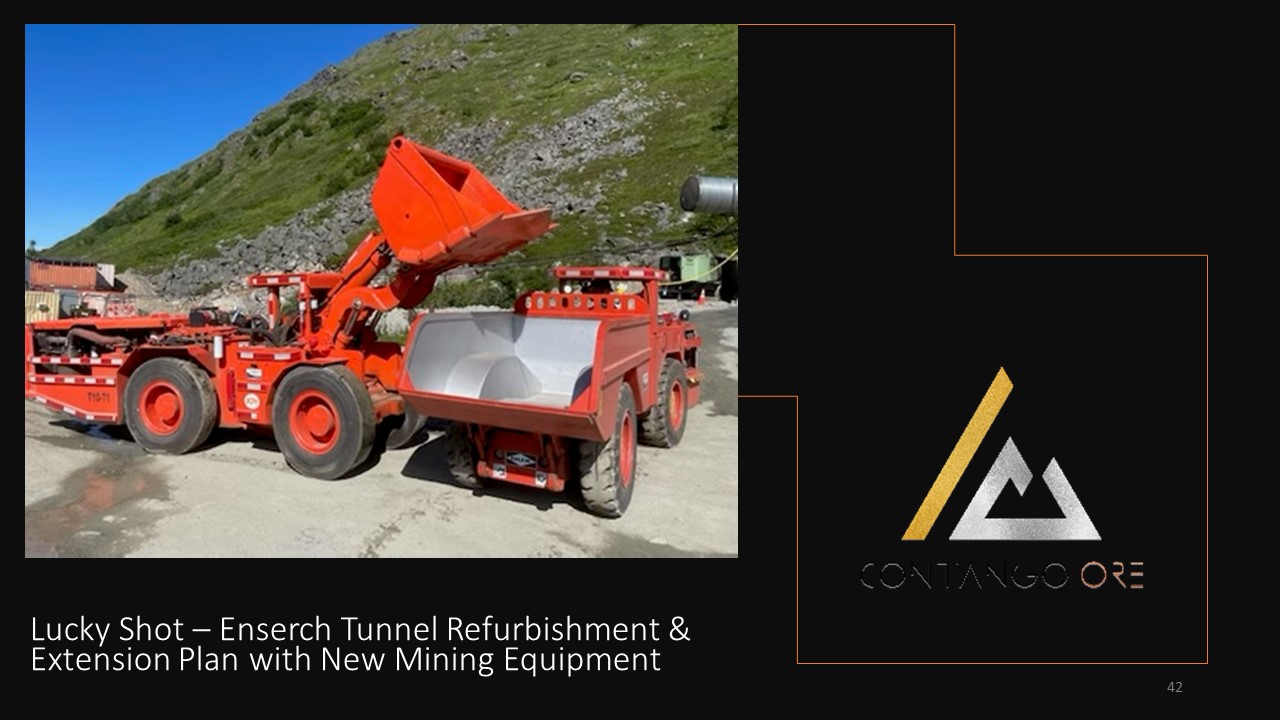

Lucky Shot – Enserch Tunnel Refurbishment & Extension Plan with New Mining Equipment 42

43 Lucky Shot – Currently Advancing Towards Drift Parallel and in Footwall to Lucky Shot Vein – Exploration Drilling to Start in June

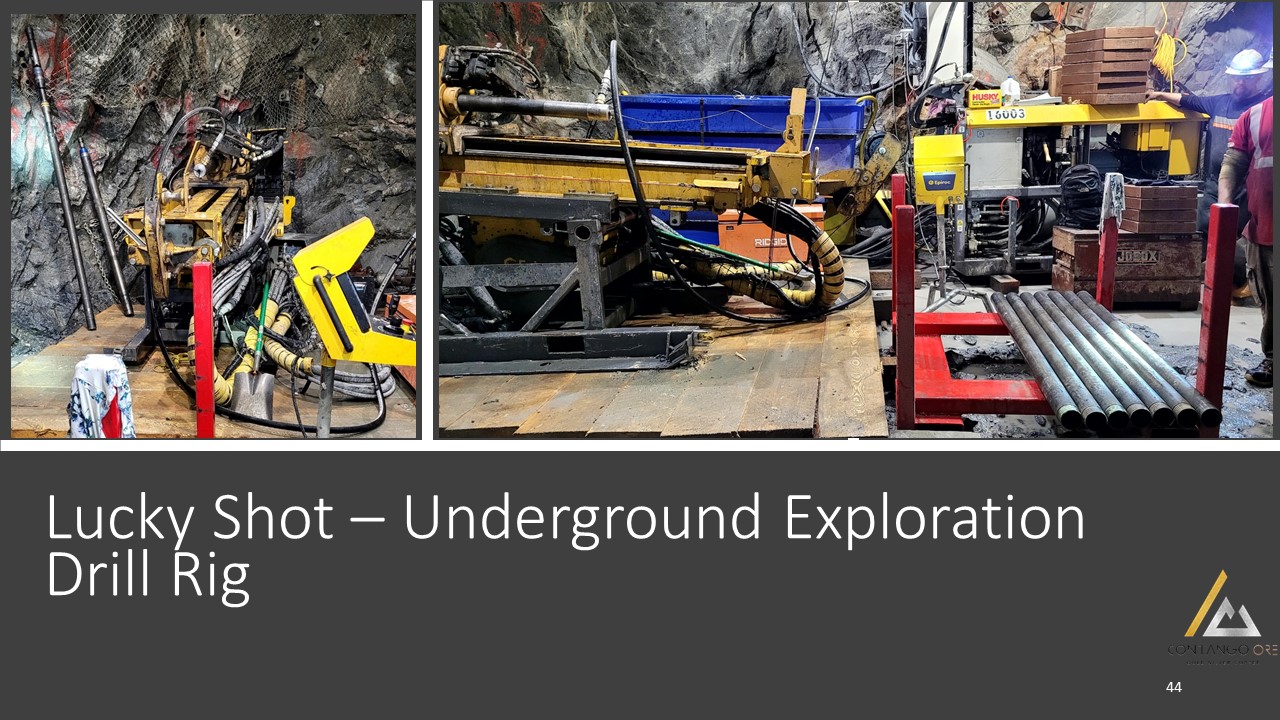

44 Lucky Shot – Underground Exploration Drill Rig

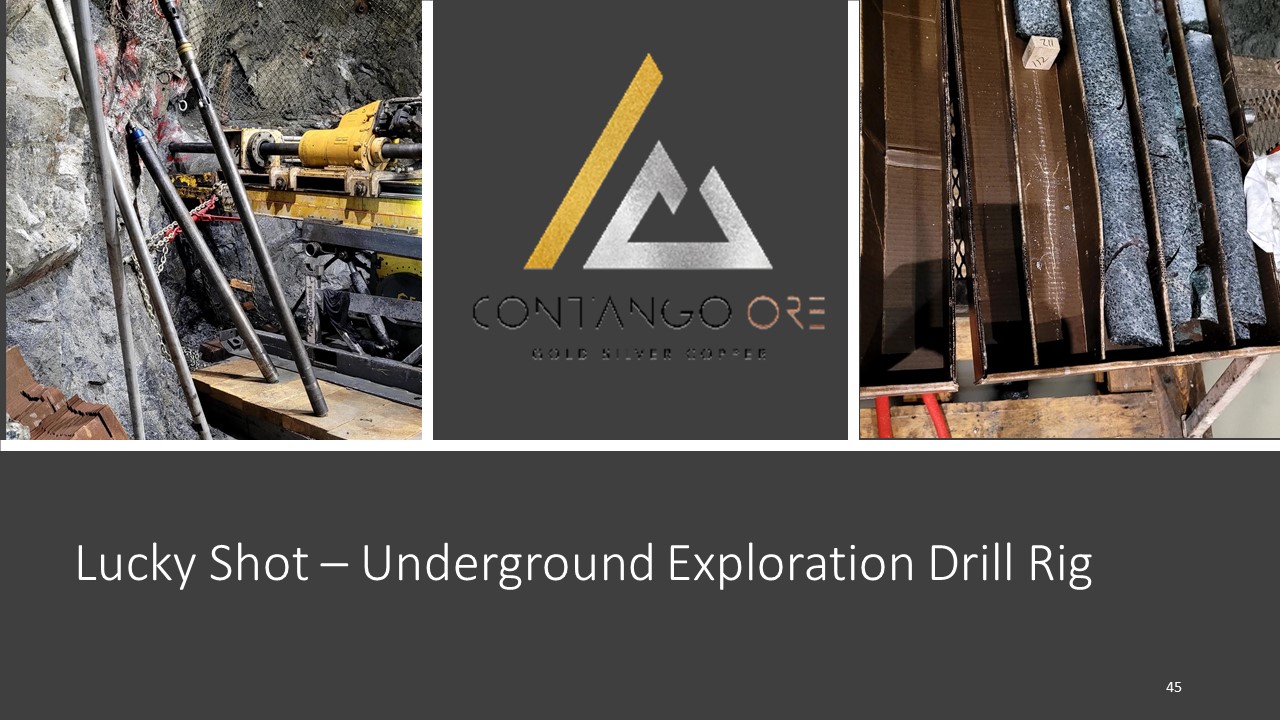

Lucky Shot – Underground Exploration Drill Rig 45

Corporate Inquires:info@contangoore.com+1-778-386-6227www.contangoore.com NYSE American: CTGO Twitter: @orecontangoLinkedIn: Contango OREInstagram: ContangoOREFacebook: Contango ORE

This presentation contains forward looking estimates of all-in sustaining cost (“AISC”), resources and EBITDA, which are a financial measure not determined in accordance with United States generally accepted accounting principles (“GAAP”). We cannot provide a reconciliation of estimated AISC, resources, EBITDA and cash flow to estimated costs of goods sold, assets and net income, which are the GAAP financial measures most directly comparable to such non-GAAP measures, without unreasonable efforts due to the inherent difficulty and impracticality of quantifying certain amounts that would be required to calculate projected AISC, resources, EBITDA. In addition, the estimates of AISC, resources and EBITDA have been prepared by Kinross and are based on IFRS accounting standards and detailed information to which the Company has not had access to at this time. These amounts that would require unreasonable effort to quantify could be significant, such that the amount of projected GAAP cost of goods sold, assets and net income would vary substantially from the amount of projected AISC, resources and EBITDA. 47 NON-GAAP RECONCILIATION DISCLAIMER APPENDIX