UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

Investment Company Act file number | | 811-22482 |

Nuveen Energy MLP Total Return Fund

(Exact name of registrant as specified in charter)

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Address of principal executive offices) (Zip code)

Gifford R. Zimmerman

Nuveen Investments

333 West Wacker Drive

Chicago, IL 60606

(Name and address of agent for service)

Registrant’s telephone number, including area code: (312) 917-7700

Date of fiscal year end: November 30

Date of reporting period: November 30, 2017

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. ss. 3507.

ITEM 1. REPORTS TO STOCKHOLDERS.

| | |

| | |  |

| Closed-End Funds | |

| | | | | | |

| | | | | | | Annual Report November 30, 2017 |

| | | |

| | | | | | |

| | | | | | | |

| JMF | | | | | | |

| Nuveen Energy MLP Total Return Fund | | |

| | | | | | | |

| JMLP | | | | | | |

| Nuveen All Cap Energy MLP Opportunities Fund | | |

| | | | | | | |

| | | | | | | | | | | | |

| | | | | | |

| | | | |

| | | | | | | | |

| |

| | Life is Complex |

| |

| | Nuveen makes things e-simple. It only takes a minute to sign up for e-Reports. Once enrolled, you’ll receive an e-mail as soon as your Nuveen Fund information is ready – no more waiting for delivery by regular mail. Just click on the link within the e-mail to see the report and save it on your computer if you wish. |

| | |

| | Free e-Reports right to your e-mail! |

| |

| | www.investordelivery.com If you receive your Nuveen Fund dividends and statements from your financial advisor or brokerage account. |

| |

| or | | www.nuveen.com/accountaccess If you receive your Nuveen Fund dividends and statements directly from Nuveen. |

Table

of Contents

Chairman’s Letter

to Shareholders

Dear Shareholders,

Asset prices steadily climbed during 2017, propelled by a “Goldilocks” economic scenario that enabled markets to sidestep geopolitical tensions, natural disasters, terrorism events and political noise. The U.S. economy continued to run not too hot, not too cold, with steady growth and low levels of unemployment, inflation and interest rates. Corporate earnings have been healthy and recession risk appeared low. At the same time, growth across the rest of the world has improved as well, leading to upward revisions in global growth projections.

Yet, a global synchronized recovery also brings the prospect of higher inflation. Central banks have to manage the delicate balance between too-loose financial conditions, which risks economies overheating, and too-tight conditions, which could trigger recession. The nomination of Jerome Powell for Chairman of the U.S. Federal Reserve (Fed) is largely expected to maintain the course set by Chair Janet Yellen after her term expires in February 2018, and the much anticipated tax overhaul, passed at the end of December, may likely boost economic growth but could complicate the Fed’s job of managing interest rates in the years ahead.

Negotiations surrounding the budget showdown are in the forefront, as Congress debates the U.S. debt ceiling limit and spending related to the military, disaster relief, the Children’s Health Insurance Program and immigration policy. In addition, the ongoing “Brexit” negotiations and the North American Free Trade Agreement (NAFTA) talks may impact key trade and political partnerships. Tensions with North Korea may continue to flare.

The magnitude of the market’s bullishness during 2017 has been somewhat surprising, but gains may not be so easy in the coming years. Nobody can predict market shifts, and that is why Nuveen encourages you to talk to your financial advisor to ensure your investment portfolio is appropriately diversified for your objectives, time horizon and risk tolerance. On behalf of the other members of the Nuveen Fund Board, we look forward to continuing to earn your trust in the months and years ahead.

Sincerely,

William J. Schneider

Chairman of the Board

January 22, 2018

Portfolio Managers’

Comments

Nuveen Energy MLP Total Return Fund (JMF)

Nuveen All Cap Energy MLP Opportunities Fund (JMLP)

The Funds’ investment adviser is Nuveen Fund Advisors, LLC (NFAL), an affiliate of Nuveen, LLC. These Funds feature portfolio management by the MLP & Energy Infrastructure team of Advisory Research, Inc., which is a wholly-owned subsidiary of Piper Jaffray Companies. James J. Cunnane Jr., CFA, Managing Director and Chief Investment Officer for the MLP & Energy Infrastructure team and Quinn T. Kiley, Managing Director and Senior Portfolio Manager, manage the Funds.

Here they discuss economic and market conditions, their investment strategies and the performance of the Funds for the twelve-month reporting period ended November 30, 2017.

What factors affected the U.S. economy and financial markets during the twelve-month reporting period ended November 30, 2017?

The U.S. economy continued to expand at a below-trend pace in the reporting period overall but did mark two consecutive quarters of above 3% growth in the second and third quarters of 2017. The Bureau of Economic Analysis reported its “third” estimate of third-quarter gross domestic product (GDP) at an annualized rate of 3.2%, an increase from 3.1% in the second quarter, alleviating concerns that Hurricanes Harvey, Irma and Maria depressed the nation’s output. GDP is the value of goods and services produced by the nation’s economy less the value of the goods and services used up in production, adjusted for price changes. Despite some softening in shopping and dining out activity due to the hurricanes, consumer spending remained the main driver of demand in the economy. Business investment had been muted for most of the recovery but has accelerated in 2017, with the “hard” data now falling more in line with the highly optimistic business sentiment levels, or “soft” data, seen after President Trump won the election.

Elsewhere in the economy, the labor market continued to tighten, with unemployment staying below 5% over the course of the reporting period. As reported by the Bureau of Labor Statistics, the unemployment rate fell to 4.1% in November 2017 from 4.6% in November 2016 and job gains averaged around 172,000 per month for the past twelve months. Higher energy prices, especially gasoline, helped drive a steady increase in inflation over this reporting period. The Consumer Price Index (CPI) increased 2.2% over the twelve-month reporting period ended November 30, 2017 on a seasonally adjusted basis, as reported by the Bureau of Labor Statistics. The core CPI (which excludes food and energy) increased 1.7% during the same period, slightly below the Federal Reserve’s (Fed) unofficial longer term inflation objective of 2.0%. The housing market also continued to improve, with historically low mortgage rates and low inventory driving home prices higher. The S&P CoreLogic Case-Shiller U.S. National Home Price Index, which covers all nine U.S. census divisions, recorded a 6.2% annual gain in October 2017 (most recent data available at the time this report was prepared). The 10-City and 20-City Composites reported year-over-year increases of 6.0% and 6.4, respectively.

This material is not intended to be a recommendation or investment advice, does not constitute a solicitation to buy or sell securities, and is not provided in a fiduciary capacity. The information provided does not take into account the specific objectives or circumstances of any particular investor, or suggest any specific course of action. Investment decisions should be made based on an investor’s objectives and circumstances and in consultation with his or her advisors.

Certain statements in this report are forward-looking statements. Discussions of specific investments are for illustration only and are not intended as recommendations of individual investments. The forward-looking statements and other views expressed herein are those of the portfolio managers as of the date of this report. Actual future results or occurrences may differ significantly from those anticipated in any forward-looking statements and the views expressed herein are subject to change at any time, due to numerous market and other factors. The Funds disclaim any obligation to update publicly or revise any forward-looking statements or views expressed herein.

Refer to the Glossary of Terms Used in this report for further definition of the terms used within this section.

Portfolio Managers’ Comments (continued)

With the U.S. economy delivering a sustainable growth rate and employment strengthening, the Fed’s policy making committee raised its main benchmark interest rate in December 2016, March 2017, June 2017 and December 2017. These moves were widely expected by the markets, as were the Fed’s decisions to leave rates unchanged at the July, September and October/November 2017 meetings. (There was no August meeting.) The Fed also announced it would begin reducing its balance sheet in October 2017 by allowing a small amount of maturing Treasury and mortgage securities to roll off without reinvestment. The market expects the pace to remain moderate and predictable, with minimal market disruption.

While the markets remained comfortable with the course of monetary policy during this reporting period, the political environment was frequently a source of uncertainty. Markets were initially highly optimistic about pricing in the new administration’s “pro-growth” fiscal agenda after Donald Trump won the election. However, several attempts at health care reform were unable to pass in Congress, which weakened the outlook for the remainder of President Trump’s agenda. In the final months of 2017, legislators refocused their efforts on tax reform, ultimately passing a bill at the end of December (subsequent to the close of this reporting period) while postponing what are expected to be contentious budget talks into 2018. While the new tax law changes are widely considered stimulative to the economy, there are some concerns that it could pose challenges to the Fed’s ability to manage interest rates in the future. Although Fed Chairman nominee Jerome Powell is expected to maintain the course established by outgoing Chair Janet Yellen, after her term expires in February 2018, markets may deem this as another source of uncertainty. Geopolitical risks also remained prominent throughout the reporting period, with the ongoing renegotiation of the North American Free Trade Agreement (NAFTA); the start of “Brexit” talks between the U.K. and European Union; closely watched elections in the Netherlands, France and Germany; and escalating tensions between the U.S. and North Korea.

Strong economic activity drove prices for West Texas Intermediate (WTI) crude oil up 16.1% for the reporting period. Energy equities did not follow suit, with energy equities in the S&P 500® Index falling 4.2% and the Alerian MLP Index losing 6.8% over the same period. A closely watched indicator of the health of the energy industry is the active rig count which was up 36% and 44% for natural gas and crude oil, respectively. This disconnect between improving fundamentals and equity prices reflects investor exhaustion with the energy industry. As companies in the space recalibrate what exactly investors want, either growth in oil and gas production or for companies to live within cash flows, those investors were content to sit on the sideline (further discussion may be found on page seven of this report). Although early in the reporting period, we saw some flows into active master limited partnerships (MLP) products, as crude oil set an annual low in June 2017 those in-flows turned into out-flows as the reporting period progressed. Overall flows into MLP products, including passive vehicles, were down.

As the energy industry recovered from the 2016 bottom, many market participants expected to see consolidation among the group. These types of transactions are typically more difficult for MLPs because of their governance structure. The control of an MLP is typically not at the MLP itself; instead it is held at another entity that owns the general partner. These consolidated transactions between related entities are intended to simplify the MLP structure, and though control doesn’t actually change hands, the result is a form of consolidation. During the reporting period there were over $120 billion of these types of transactions; $77 billion were simplifying corporate restructuring deals and $44 billion were change of control, arms-length transactions. Both Funds were exposed to these transactions through their existing holdings and JMLP owned Arc Logistics Partners and Penntex Midstream Partners, which were outright purchases with premiums paid by the acquirers. We tendered our shares of Penntex Midstream Partners at zero commission in June 2017 and sold Arc Logistics Partners in October 2017.

How did the Funds perform during this twelve-month reporting period ended November 30, 2017?

The tables in each Fund’s Performance Overview and Holding Summaries section of this report provide total returns for the one-year, five-year and since inception periods, where applicable, ended November 30, 2017. Each Fund’s total returns at net asset value (NAV) are compared with the performance of a corresponding market index. JMF’s total return at NAV underperformed both the Alerian MLP Index (“Index”) and the S&P 500® Index during the twelve-month

reporting period, while JMLP’s total return at NAV outperformed the Index and underperformed the S&P 500® Index for the twelve-month reporting period.

The Funds are taxed as “C” corporations, and unlike most other investment companies, they pay taxes on their own income. Consequently, as explained more fully later in the report, the Funds’ adjustments to their assets and liabilities to reflect the Funds’ projected tax payments can significantly impact Fund share performance. In the most recent twelve-month reporting period, those tax adjustments had a positive impact on the share performance of JMF and no impact on the share performance of JMLP.

The Funds employ leverage. In the most recent twelve-month reporting period, this leverage had a negative impact on the Funds’ total return. You should consider the Funds’ tax adjustments and leverage when comparing each Fund’s performance to the Index and S&P 500® Index, as neither index is leveraged nor affected by the tax treatment of gains or losses. As a result, the Funds’ total return performance could differ significantly from the actual returns of its portfolio and that of the indexes, even if the pre-tax adjustment performance of the Funds’ portfolio assets and the performance of the indexes were similar. We will divide the discussion of the various strategies used by and features of the Funds, and how each of them impacted the performance of the Funds’ shares during the twelve-month reporting period ended November 30, 2017, into the following sub-sections:

| | • | | Impact of portfolio management strategies on Fund share performance |

| | • | | Impact of tax adjustments on Fund share performance |

| | • | | Impact of leverage on Fund share performance |

Impact of the Funds’ primary portfolio investment strategies on Fund share performance.

Both Funds continue to invest primarily in publicly traded MLPs operating in the energy sector with the main objective of providing a tax-advantaged total return.

During the reporting period, the Funds were primarily invested in midstream MLPs that own pipelines and other infrastructure facilities. These assets provide an essential service to our economy: procuring, processing, storing and transporting the commodities and products that fuel every aspect of our lives.

As mentioned earlier, fundamentals for MLPs improved during the reporting period. Nevertheless, while fundamentals improved, the reporting period was a frustrating one for investors as MLPs and energy infrastructure equities did not follow suit. Meager flows into the asset class were not sufficient to meet the equity needs of the companies in the space. Fund flows were approximately $4.3 billion for the reporting period, compared to new equity issuance of $15.8 billion. This over supply of equity resulted in many dedicated MLP investors selling one portion of their portfolios to buy these offerings, which can create negative price pressure. Furthermore, several management teams took the decision to change their company’s distribution policy during the reporting period. There remains a large portion of MLP investors, closed-end fund managers included, that view a higher yield as an attractive aspect of MLP securities. When distributions are reduced with the goal of funding growth in the future, there is typically some turnover in the unit holder base.

Conversely, there is a group of MLP investors who are drawn not just to the yield provided by distributions but the growth in that distribution over time. When a management team reduces the growth trajectory of the distribution to fund cash flow growth in the future, these growth-oriented investors may step away as well. Both of these sets of actions and reactions create selling pressure. Perhaps more importantly, these changes create confusion and that keeps opportunistic investors who might move into the asset class at these lower valuations on the sideline until they can better understand the distribution strategy these companies will employ. With regard to Fund flows, we think this scenario is the proximate cause of weak flows in the second half of the reporting period, despite crude oil rallying from June 2017 lows to new 52-week highs.

Portfolio Managers’ Comments (continued)

JMF’s portfolio performance underperformed the Index for the twelve-month reporting period ended November 30, 2017. The Fund’s allocation towards higher yielding MLPs, and away from faster growing MLPs, detracted from performance as the market favored growth during the reporting period. This is a reversal of what we saw in 2016 when yield meaningfully outperformed growth. The preference for growth was not that strong of a trend as the highest yielding MLPs also outperformed. Security selection among large-caps also added to underperformance. The Fund was underweight Enterprise Products Partners, the largest Index constituent, which posted gains in an otherwise negative environment. During the reporting period the Index provider capped positions at 10% weightings. While still concentrated among large-caps, the Index will present less single name risk going forward. Several MLPs have changed their distribution policies during the reporting period. Specifically, three surprised the market by implementing distribution cuts. Enbridge Energy Partners LP, Plains All American Pipeline LP, and Genesis Energy LP reduced their distribution and as a result were among the largest detractors from performance during the reporting period. The Fund held overweight positions in these names and that accounted for the majority of underperformance during the reporting period. All three of these names continue to pay attractive yields, have defensive distribution payout ratios, and will have minimal reliance on the capital markets to fund growth. Adding to relative performance for the Fund was overweight exposure to those MLPs with gathering and processing assets. These entities benefit when oil & gas production is growing and when the relative value of crude oil is much higher than the price of natural gas. That scenario played out during the reporting period and overweight positions in DCP Midstream LP, Williams Partners LP, and EnLink Midstream Partners LP were among the largest contributors to relative performance.

JMLP’s portfolio performance outperformed the Index for the twelve-month reporting period ended November 30, 2017. JMLP’s strategy is differentiated from JMF in the following ways: 1) JMLP will not own the top ten constituents in the Index, and 2) JMLP will not purchase securities in the bottom 30% of the universe, as defined by the sub-adviser’s “Quality Scorecard” process, which ranks each constituent of the investable MLP universe according to fundamental metrics. JMLP’s strategy worked with the investable universe outperforming the Index. Avoiding the top ten holdings in the Index was helpful in that the Fund avoided owning Plains All American Pipeline and Enbridge Energy Partners, both of which surprised the market with distribution cuts. The quality screen was helpful as well in that the MLPs we avoided underperformed the Index. The smaller capitalization of the Fund’s portfolio contributed to performance as this group posted gains in an otherwise down year. Similar to JMF, avoiding Enterprise Products Partners was a detractor from performance. The largest detractor from performance was Teekay Offshore Partners LP, which continues to struggle in the market due to confusion around its business model and a previous distribution cut. We sold our holding in Teekay Offshore Partners, LP during July through September 2017.

Impact of tax adjustments on the Funds’ share performance

Each Fund is treated as a “C” Corporation for U.S. federal income tax purposes and therefore is a taxable entity, meaning that in addition to recording a current tax expense on current year earnings and realized gains, they also record either a net deferred tax liability representing the future taxes projected to be payable on unrealized portfolio gains, or a net deferred tax asset representing the tax benefit projected to be associated with realized and unrealized portfolio losses. These tax adjustment entries on the Funds’ accounting records are intended to ensure that the Funds’ NAVs take into account the future income tax that the Funds may be liable for based on unrealized appreciation as well as the tax benefit of losses that may be used to offset future earnings. Such entries will often have a “moderating impact” on the total returns of investment of the Funds’ shares during a particular measurement period. An increase in the value of a Fund’s portfolio investments will typically trigger an increase to the deferred tax liability or a reduction to the deferred tax asset that would partially offset the portfolio value increases; in contrast, a decrease in value of the Fund’s portfolio investments will typically trigger a reduction in a deferred tax liability and/or an increase to the deferred tax asset, which again would tend to partially offset such portfolio value decreases.

During the reporting period for JMF, the projected future tax liability of the Fund decreased, resulting in a positive contribution to NAV performance.

To the extent that a Fund has a deferred tax asset, consideration is given to whether or not a valuation allowance is required that would offset the tax asset. Accounting principles dictate that the determination of such a valuation allowance is based on whether there is a more-likely-than-not probability that some portion or all of the deferred tax asset will not be realized.

At November 30, 2016, JMLP had a valuation allowance to offset the deferred tax asset. This allowance still existed at November 30, 2017. As a result, there was no impact to NAV performance associated with the deferred tax asset or liability.

Event subsequent to the close of this reporting period

In light of the passage and signing into law on December 22, 2017 of the Tax Cuts and Jobs Act of 2017, JMF made adjustments on that day to the Fund’s estimate of its deferred tax liability balance. The Fund’s deferred tax liability and/or asset balances are determined using estimates of effective tax rates expected to apply to taxable income in the years such balances are realized. The Tax Cuts and Jobs Act of 2017 reduced the statutory federal income tax rate applicable to corporations, such as JMF and JMLP, from 35% to 21%. JMF reduced the estimate of its net deferred tax liability balance to reflect this reduction in the corporate federal income tax rate; this reduced its net deferred tax liability balance as of December 22, 2017 from an amount that would have been somewhat in excess of $35 million to approximately $22 million. That adjustment in turn caused JMF’s net asset value to increase by $0.33 per common share.

JMLP, on the other hand, had a net deferred tax asset immediately prior to December 22, 2017, but that asset had a fully offsetting valuation allowance. The amount of JMLP’s net deferred tax asset decreased on December 22, 2017 due to the reduction in the income tax rate, but the valuation allowance was also reduced by the same amount, resulting in no impact to the net asset value of that Fund.

Further modifications of the Funds’ estimates or assumptions regarding its deferred tax liability and/or asset balances and any applicable valuation allowance could result in increases or decreases in the Fund’s net asset value per share, which could be material.

Impact of the Funds’ leverage strategies on performance

One important factor impacting the returns of the Funds relative to their comparative benchmarks was the Funds’ use of leverage through bank borrowings. The Funds use leverage because our research has shown that, over time, leveraging provides opportunities for additional income and total return for shareholders. However, use of leverage also can expose shareholders to additional volatility. For example, as the prices of securities held by a Fund decline, the negative impact of these valuation changes on NAV and total return is magnified by the use of leverage. Conversely, leverage may enhance returns during periods when the prices of securities held by a Fund generally are rising. For the twelve-month reporting period ended November 30, 2017, leverage had a negative impact on performance for both Funds.

The Funds employ regulatory leverage through the use of bank borrowings. As of November 30, 2017, the Funds had outstanding bank borrowings as shown in the accompanying table.

| | | | | | | | |

| | | JMF | | | JMLP | |

Bank Borrowings | | $ | 175,000,000 | | | $ | 41,500,000 | |

Portfolio Managers’ Comments (continued)

As of November 30, 2017, the Funds’ leverage, expressed as a percentage of total managed assets, were as shown in the accompanying table.

| | | | | | | | |

| | | JMF | | | JMLP | |

Effective Leverage* | | | 28.59 | % | | | 27.74 | % |

Regulatory Leverage* | | | 28.59 | % | | | 27.74 | % |

| * | Effective Leverage is a Fund’s effective economic leverage, and includes both regulatory leverage and the leverage effects of certain derivative and other investments in a Fund’s portfolio that increase the Fund’s investment exposure. Regulatory leverage consists of preferred shares issued or borrowings of a Fund. Both of these are part of a Fund’s capital structure. A Fund, however, may from time to time borrow on a typically transient basis in connection with its day-to-day operations, primarily in connection with the need to settle portfolio trades. Such incidental borrowings are excluded from the calculation of a Fund’s effective leverage ratio. Regulatory leverage is subject to asset coverage limits set forth in the Investment Company Act of 1940. |

Bank Borrowings

As noted above, the Funds employ leverage through the use of bank borrowings.

The Funds operate under established leverage guidelines. During the current reporting period, volatility in the MLP market caused the Funds to periodically reduce and increase the amount of their outstanding borrowings in order to maintain levels consistent with these guidelines. The Funds’ bank borrowing activities are as shown in the accompanying table.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Current Reporting Period | | | | | | Subsequent to the Close of

the Reporting Period | |

| Fund | | December 1, 2016 | | | Draws | | | Paydowns | | | November 30, 2017 | | | Average Balance

Outstanding | | | | | | Draws | | | Paydowns | | | January 24, 2018 | |

JMF | | $ | 185,550,000 | | | $ | 6,450,000 | | | $ | (17,000,000 | ) | | $ | 175,000,000 | | | $ | 185,808,767 | | | | | | | $ | — | | | $ | — | | | $ | 175,000,000 | |

JMLP | | $ | 39,000,000 | | | $ | 6,000,000 | | | $ | (3,500,000 | ) | | $ | 41,500,000 | | | $ | 42,890,137 | | | | | | | $ | — | | | $ | — | | | $ | 41,500,000 | |

Refer to Notes to Financial Statements, Note 7 – Borrowing Arrangements for further details.

During the reporting period, JMF continued to utilize forward interest rate swap contracts and JMLP entered into forward interest rate swap contracts to hedge the future interest expense of its leverage. During the reporting period, these swaps had a marginally positive impact on the Funds’ overall performance.

Share

Information

DISTRIBUTION INFORMATION

The following information regarding the Funds’ distributions is current as of November 30, 2017, the Funds’ fiscal and tax year end, and may differ from previously issued distribution notifications.

The Funds have a cash flow-based distribution program. Under this program, each Fund seeks to maintain an attractive and stable regular distribution based on the Fund’s net cash flow received from its portfolio investments. Fund distributions are not intended to include expected portfolio appreciation; however, each Fund invests in securities that make payments which ultimately may be fully or partially treated as gains or return of capital for tax purposes. This tax treatment will generally “flow through” to the Fund’s distributions, but the specific tax treatment is often not known with certainty until after the end of the Fund’s tax year. As a result, regular distributions throughout the year are likely to be re-characterized for tax purposes as either long-term gains (both realized and unrealized), or as a non-taxable return of capital.

The figures in the table below provide the sources (for tax purposes) of each Fund’s distributions as of November 30, 2017. These sources include amounts attributable to realized gains and/or returns of capital. The Funds attribute these non-income sources equally to each regular distribution throughout the fiscal year. The information shown below is for the distributions paid on common shares for all prior months in the current fiscal year. These amounts should not be used for tax reporting purposes, and the distribution sources may differ for financial reporting than for tax reporting. The final determination of the tax characteristics of all distributions paid in 2017 will be made in early 2018 and reported to you on Form 1099-DIV. More details about the tax characteristics of each Fund’s distributions are available on www.nuveen.com/CEFdistributions.

Data as of November 30, 2017

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Fiscal YTD | | | Fiscal YTD | |

| | | Percentage of the Distribution | | | Per Share Amounts | |

| Fund | | Net

Investment

Income(1) | | | Realized

Gains | | | Return of

Capital(2) | | | Total

Distributions | | | Net

Investment

Income(1) | | | Realized

Gains | | | Return of

Capital(2) | |

JMF (FYE 11/30) | | | 13.30 | % | | | 0.00 | % | | | 86.70 | % | | $ | 1.3480 | | | $ | 0.1793 | | | $ | 0.0000 | | | $ | 1.1687 | |

JMLP (FYE 11/30) | | | 0.00 | % | | | 0.00 | % | | | 100 | % | | $ | 0.9840 | | | $ | 0.0000 | | | $ | 0.0000 | | | $ | 0.9840 | |

| (1) | The Funds may have current fiscal year earnings and profits, and if so, a portion or all of the distributions may be treated as ordinary dividend income. |

| (2) | Return of Capital may represent unrealized gains, return of shareholders’ principal, or both. |

The following table provides information regarding fund distributions and total return performance over various time periods. This information is intended to help you better understand whether fund returns for the specified time periods were sufficient to meet fund distributions.

Data as of November 30, 2017

| | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | Annualized | | | Cumulative | |

| Fund | | Inception

Date | | | Latest

Quarterly

Per Share

Distribution | | | Current

Distribution

on

NAV | | | 1-Year

Return on

NAV | | | Since Inception

Return on

NAV | | | Calendar YTD

Distributions

on

NAV | | | Calendar

YTD

Return

on NAV | |

JMF (FYE 11/30) | | | 2/23/2011 | | | $ | 0.3370 | | | | 12.37 | % | | | (9.44 | )% | | | (0.18 | )% | | | 12.37 | % | | | (13.38 | )% |

JMLP (FYE 11/30) | | | 3/26/2014 | | | $ | 0.2460 | | | | 11.99 | % | | | (4.22 | )% | | | (11.37 | )% | | | 11.99 | % | | | (12.39 | )% |

Share Information (continued)

EQUITY SHELF PROGRAM

During the current reporting period, the Funds were authorized by the Securities and Exchange Commission (SEC) to issue additional shares through an equity shelf program (Shelf Offering). Under these programs, the Funds, subject to market conditions, may raise additional capital from time to time in varying amounts and offering methods at a net price at or above each Fund’s NAV per share. Under the Shelf Offerings, each Fund is authorized to issue additional shares as shown in the accompanying table:

| | | | | | | | |

| | | JMF | | | JMLP | |

Additional authorized shares | | | 9,800,000 | * | | | 3,100,000 | ** |

| * | Represents additional shares for the period October 17, 2017 through November 30, 2017. |

| ** | Represents additional shares for the period July 12, 2017 through Novemner 30, 2017. |

During the current reporting period, the Funds sold shares through their Shelf Offering at a weighted average premium to their NAV per share as shown in the accompanying table.

| | | | | | | | |

| | | JMF | | | JMLP | |

Shares sold through Shelf Offering | | | 450,848 | | | | 399,500 | |

Weighted average premium to NAV per share sold | | | 1.54 | % | | | 1.65 | % |

Refer to Notes to Financial Statements, Note 4 – Fund Shares, Shares Equity Shelf Programs and Offering Costs for further details of Shelf Offerings and each Fund’s respective transactions.

SHARE REPURCHASES

During August 2017, the Funds’ Board of Trustees reauthorized an open-market share repurchase program, allowing each Fund to repurchase an aggregate of up to approximately 10% of its outstanding shares.

As of November 30, 2017, and since the inception of the Funds’ repurchase programs, the Funds have cumulatively repurchased and retired their outstanding shares as shown in the accompanying table.

| | | | | | | | |

| | | JMF | | | JMLP | |

Shares cumulatively repurchased and retired | | | 0 | | | | 0 | |

Shares authorized for repurchase | | | 3,955,000 | | | | 1,285,000 | |

OTHER SHARE INFORMATION

As of November 30, 2017, and during the current reporting period, the Funds’ share prices were trading at a premium/(discount) to their NAVs as shown in the accompanying table.

| | | | | | | | |

| | | JMF | | | JMLP | |

NAV | | $ | 10.90 | | | $ | 8.21 | |

Share price | | $ | 10.57 | | | $ | 8.02 | |

Premium/(Discount) to NAV | | | (3.03 | )% | | | (2.31 | )% |

12-month average premium/(discount) to NAV | | | 1.11 | % | | | 0.95 | % |

Risk

Considerations

Fund shares are not guaranteed or endorsed by any bank or other insured depository institution, and are not federally insured by the Federal Deposit Insurance Corporation.

Nuveen Energy MLP Total Return Fund (JMF)

Investing in closed-end funds involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. Closed-end fund shares may frequently trade at a discount or premium to their net asset value. MLP Units are subject to energy sector concentration risk, limited voting rights, and heightened tax risk. Common stock returns often have experienced significant volatility. Leverage increases return volatility and magnifies the Fund’s potential return and its risks; there is no guarantee a fund’s leverage strategy will be successful. For these and other risks such as tax risk, please see the Fund’s web page at www.nuveen.com/JMF.

Nuveen All Cap Energy MLP Opportunities Fund (JMLP)

Investing in closed-end funds involves risk; principal loss is possible. There is no guarantee the Fund’s investment objectives will be achieved. Closed-end fund shares may frequently trade at a discount or premium to their net asset value. MLP Units are subject to energy sector concentration risk, limited voting rights, and heightened tax risk. Common stock returns often have experienced significant volatility. Leverage increases return volatility and magnifies the Fund’s potential return and its risks; there is no guarantee a fund’s leverage strategy will be successful. For these and other risks, including tax risk and small capitalization risk, please see the Fund’s web page at www.nuveen.com/JMLP.

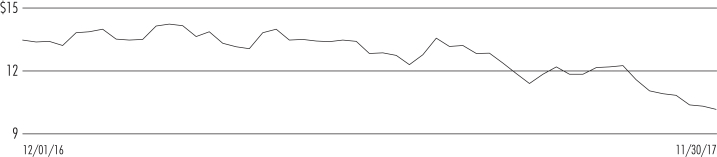

JMF

Nuveen Energy MLP Total Return Fund

Performance Overview and Holding Summaries as of November 30, 2017

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of November 30, 2017

| | | | | | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | 5-Year | | | Since

Inception | |

| JMF at NAV | | | (9.44)% | | | | (1.29)% | | | | (0.18)% | |

| JMF at Share Price | | | (11.44)% | | | | (1.91)% | | | | (0.87)% | |

| Alerian MLP Index | | | (6.83)% | | | | (1.61)% | | | | 1.23% | |

| S&P 500® Index | | | 22.87% | | | | 15.74% | | | | 13.38% | |

Since inception returns are from 2/23/11. Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Share Price Performance — Weekly Closing Price

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

Fund Allocation

(% of net assets)

| | | | |

| Master Limited Partnerships & MLP Affiliates | | | 146.0% | |

| Repurchase Agreements | | | 0.3% | |

| Other Assets Less Liabilities | | | (0.1)% | |

| Net Assets Plus Borrowings and Deferred Tax Liability, net | | | 146.2% | |

| Borrowings | | | (40.0)% | |

| Deferred Tax Liability, net | | | (6.2)% | |

Net Assets | | | 100% | |

Portfolio Composition

(% of total investments)

| | | | |

| Oil, Gas & Consumable Fuels | | | 98.7% | |

| Energy Equipment & Services | | | 1.1% | |

| Repurchase Agreements | | | 0.2% | |

| Total | | | 100% | |

Top Ten Issuers

(% of total long-term

investments)

| | | | |

DCP Midstream LP | | | 9.1% | |

EnLink Midstream Partners LP | | | 8.7% | |

Williams Partners LP | | | 8.1% | |

Energy Transfer Partners LP | | | 6.2% | |

Buckeye Partners LP | | | 6.1% | |

MPLX LP | | | 4.8% | |

Enbridge Energy Partners LP | | | 4.3% | |

Enable Midstream Partners LP | | | 4.3% | |

Plains All American Pipeline LP | | | 3.9% | |

TC PipeLines LP | | | 3.9% | |

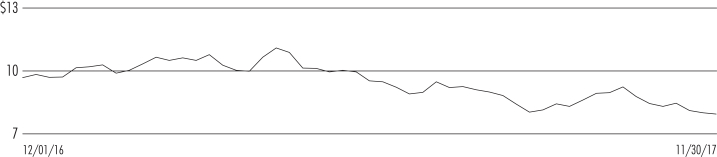

JMLP

Nuveen All Cap Energy MLP Opportunities Fund

Performance Overview and Holding Summaries as of

November 30, 2017

Refer to the Glossary of Terms Used in this Report for further definition of the terms used within this section.

Average Annual Total Returns as of November 30, 2017

| | | | | | | | |

| | | Average Annual | |

| | | 1-Year | | | Since

Inception | |

| JMLP at NAV | | | (4.22)% | | | | (11.37)% | |

| JMLP at Share Price | | | (8.91)% | | | | (12.97)% | |

| Alerian MLP Index | | | (6.83)% | | | | (7.69)% | |

| S&P 500® Index | | | 22.87% | | | | 12.52% | |

Since inception returns are from 3/26/14. Past performance is not predictive of future results. Current performance may be higher or lower than the data shown. Returns do not reflect the deduction of taxes that shareholders may have to pay on Fund distributions or upon the sale of Fund shares. Returns at NAV are net of Fund expenses, and assume reinvestment of distributions. Comparative index return information is provided for the Fund’s shares at NAV only. Indexes are not available for direct investment.

Share Price Performance — Weekly Closing Price

This data relates to the securities held in the Fund’s portfolio of investments as of the end of the reporting period. It should not be construed as a measure of performance for the Fund itself. Holdings are subject to change.

Fund Allocation

(% of net assets)

| | | | |

| Master Limited Partnerships & MLP Affiliates | | | 136.8% | |

| Repurchase Agreements | | | 1.5% | |

| Other Assets Less Liabilities | | | 0.1% | |

Net Assets Plus Borrowings | | | 138.4% | |

| Borrowings | | | (38.4)% | |

| Net Assets | | | 100% | |

Portfolio Composition

(% of total investments)

| | | | |

| Oil, Gas & Consumable Fuels | | | 93.2% | |

| Energy Equipment & Services | | | 3.2% | |

| Gas Utilities | | | 2.5% | |

| Repurchase Agreements | | | 1.1% | |

| Total | | | 100% | |

Top Ten Issuers

(% of total long-term investments)

| | | | |

Enable Midstream Partners LP | | | 9.6% | |

EnLink Midstream Partners LP | | | 8.2% | |

DCP Midstream LP | | | 8.1% | |

American Midstream Partners LP | | | 5.8% | |

KNOT Offshore Partners LP | | | 5.6% | |

NGL Energy Partners LP | | | 4.8% | |

Summit Midstream Partners LP | | | 4.8% | |

Crestwood Equity Partners LP | | | 4.6% | |

Golar LNG Partners LP | | | 4.3% | |

GasLog Partners LP | | | 4.2% | |

Report of

Independent Registered Public Accounting Firm

To the Board of Trustees and Shareholders of

Nuveen Energy MLP Total Return Fund

Nuveen All Cap Energy MLP Opportunities Fund:

In our opinion, the accompanying statements of assets and liabilities, including the portfolios of investments, and the related statements of operations, of changes in net assets, and of cash flows and the financial highlights present fairly, in all material respects, the financial position of Nuveen Energy MLP Total Return Fund and Nuveen All Cap Energy MLP Opportunities Fund (hereafter referred to as the “Funds”) as of November 30, 2017, the results of each of their operations and their cash flows for the year then ended, the changes in each of their net assets for each of the two years in the period then ended and the financial highlights for each of the periods indicated therein, in conformity with accounting principles generally accepted in the United States of America. These financial statements and financial highlights (hereafter referred to as “financial statements”) are the responsibility of the Funds’ management. Our responsibility is to express an opinion on these financial statements based on our audits. We conducted our audits of these financial statements in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements are free of material misstatement. An audit includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. We believe that our audits, which included confirmation of securities as of November 30, 2017 by correspondence with the custodian and brokers, provide a reasonable basis for our opinion.

PricewaterhouseCoopers LLP

Chicago, IL

January 24, 2018

JMF

| | |

Nuveen Energy MLP Total Return Fund | | |

Portfolio of Investments | | November 30, 2017 |

| | | | | | | | | | | | | | | | |

| Shares/Units | | | Description (1) | | | | | | | | Value | |

| | | | |

| | | | LONG-TERM INVESTMENTS – 146.0% (99.8% of Total Investments) | | | | | | | | | | | | |

| | | |

| | | | MASTER LIMITED PARTNERSHIPS & MLP AFFILIATES – 146.0% (99.8% of Total Investments) | | | | | | | | | |

| | | | |

| | | | Energy Equipment & Services – 1.6% (1.1% of Total Investments) | | | | | | | | | |

| | | | |

| | 640,836 | | | Archrock Partners LP | | | | | | | | | | $ | 7,017,154 | |

| | | | |

| | | | Oil, Gas & Consumable Fuels – 144.4% (98.7% of Total Investments) | | | | | | | | | |

| | | | |

| | 491,568 | | | American Midstream Partners LP | | | | | | | | | | | 5,874,238 | |

| | 482,362 | | | Andeavor Logistics LP | | | | | | | | | | | 21,590,523 | |

| | 850,210 | | | Buckeye Partners LP | | | | | | | | | | | 39,050,145 | |

| | 825,434 | | | Crestwood Equity Partners LP | | | | | | | | | | | 19,769,144 | |

| | 1,651,790 | | | DCP Midstream LP | | | | | | | | | | | 58,043,901 | |

| | 474,653 | | | Delek Logistics Partners LP | | | | | | | | | | | 13,883,600 | |

| | 1,819,800 | | | Enable Midstream Partners LP | | | | | | | | | | | 27,260,604 | |

| | 941,747 | | | Enbridge Energy Management LLC, (2) | | | | | | | | | | | 12,713,585 | |

| | 1,888,940 | | | Enbridge Energy Partners LP | | | | | | | | | | | 27,616,303 | |

| | 2,394,876 | | | Energy Transfer Partners LP | | | | | | | | | | | 39,778,890 | |

| | 3,456,765 | | | EnLink Midstream Partners LP | | | | | | | | | | | 55,273,672 | |

| | 818,834 | | | Enterprise Products Partners LP | | | | | | | | | | | 20,167,881 | |

| | 781,827 | | | Genesis Energy, LP | | | | | | | | | | | 16,785,826 | |

| | 395,180 | | | Golar LNG Partners LP, (3) | | | | | | | | | | | 7,899,648 | |

| | 560,000 | | | KNOT Offshore Partners LP, (3) | | | | | | | | | | | 11,312,000 | |

| | 224,025 | | | Martin Midstream Partners LP | | | | | | | | | | | 3,013,136 | |

| | 863,415 | | | MPLX LP | | | | | | | | | | | 30,962,062 | |

| | 679,895 | | | Navios Maritime Midstream Partners LP, (3) | | | | | | | | | | | 5,500,351 | |

| | 1,541,550 | | | NGL Energy Partners LP | | | | | | | | | | | 19,269,375 | |

| | 43,085 | | | NuStar Energy LP | | | | | | | | | | | 1,252,050 | |

| | 389,473 | | | ONEOK, Inc. | | | | | | | | | | | 20,213,649 | |

| | 407,200 | | | PBF Logistics LP | | | | | | | | | | | 8,021,840 | |

| | 1,270,678 | | | Plains All American Pipeline LP | | | | | | | | | | | 24,778,221 | |

| | 958,122 | | | Summit Midstream Partners LP | | | | | | | | | | | 18,156,412 | |

| | 132,855 | | | Sunoco LP | | | | | | | | | | | 3,900,623 | |

| | 162,550 | | | Tallgrass Energy Partners LP | | | | | | | | | | | 7,139,196 | |

| | 479,635 | | | Targa Resources Corp. | | | | | | | | | | | 20,816,159 | |

| | 486,045 | | | TC PipeLines LP | | | | | | | | | | | 24,695,946 | |

| | 91,535 | | | The Williams Companies Inc., (3) | | | | | | | | | | | 2,659,092 | |

| | 980,540 | | | USD Partners LP | | | | | | | | | | | 9,952,481 | |

| | 50,000 | | | Western Gas Partners, LP | | | | | | | | | | | 2,241,000 | |

| | 1,413,385 | | | Williams Partners LP | | | | | | | | | | | 51,871,230 | |

| | | | Total Oil, Gas & Consumable Fuels | | | | | | | | | | | 631,462,783 | |

| | | | Total Long-Term Investments (cost $592,023,150) | | | | | | | | | | | 638,479,937 | |

| | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Value | |

| | | | |

| | | | SHORT-TERM INVESTMENTS – 0.3% (0.2% of Total Investments) | | | | | | | | | | | | |

| | | | |

| | | | REPURCHASE AGREEMENTS – 0.3% (0.2% of Total Investments) | | | | | | | | | |

| | | | |

| $ | 1,178 | | | Repurchase Agreement with Fixed Income Clearing Corporation, dated 11/30/17,

repurchase price $1,178,426, collateralized by $1,130,000 U.S. Treasury Notes,

3.625%, due 2/15/21, value $1,202,294 | | | 0.120% | | | | 12/01/17 | | | $ | 1,178,422 | |

| | | | Total Short-Term Investments (cost $1,178,422) | | | | | | | | | | | 1,178,422 | |

| | | | Total Investments (cost $593,201,572) – 146.3% | | | | | | | | | | | 639,658,359 | |

| | | | Borrowings – (40.0)% (4), (5) | | | | | | | | | | | (175,000,000 | ) |

| | | | Deferred Tax Liability, net – (6.2)% | | | | | | | | | | | (26,943,912 | ) |

| | | | Other Assets Less Liabilities – (0.1)% (6) | | | | | | | | | | | (562,485 | ) |

| | | | Net Assets – 100% | | | | | | | | | | $ | 437,151,962 | |

| | | | |

| JMF | | Nuveen Energy MLP Total Return Fund | | |

| | Portfolio of Investments (continued) | | November 30, 2017 |

Investments in Derivatives as of November 30, 2017

Interest Rate Swaps – OTC Uncleared

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Counterparty | | Notional

Amount | | | Fund

Pay/Receive

Floating Rate | | | Floating Rate Index | | | Fixed Rate

(Annualized) | | | Fixed Rate

Payment

Frequency | | | Effective

Date (7) | | | Optional

Termination

Date | | | Maturity

Date | | | Value | | | Unrealized

Appreciation

(Depreciation) | |

JPMorgan Chase Bank, N.A. | | $ | 94,500,000 | | | | Receive | | | | 1-Month LIBOR | | | | 1.969 | % | | | Monthly | | | | 6/01/18 | | | | 7/01/25 | | | | 7/01/27 | | | $ | 1,130,986 | | | $ | 1,130,986 | |

For Fund portfolio compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications into sectors for reporting ease.

| (1) | All percentages shown in the Portfolio of Investments are based on net assets unless otherwise noted. |

| (2) | Payment-in-kind (“PIK”) security. Depending on the terms of the security, distributions may be received in the form of cash, securities, or a combination of both. |

| (3) | Distribution designated as ordinary income which is recognized as “Dividends” on the Statement of Operations. |

| (4) | Borrowings as a percentage of Total Investments is 27.4%. |

| (5) | The Fund segregates 100% of its eligible investments (excluding any investments separately pledged as collateral for specific investments in derivatives, when applicable) in the Portfolio of Investments as collateral for borrowings. As of the end of the reporting period, investments with a value of $479,638,302 have been pledged as collateral for borrowings. |

| (6) | Other assets less liabilities includes the unrealized appreciation (depreciation) of certain over-the-counter (“OTC”) derivatives as presented on the Statement of Assets and Liabilities, when applicable. The unrealized appreciation (depreciation) of OTC cleared and exchange-traded derivatives is recognized as part of the cash collateral at brokers and/or the receivable or payable for variation margin as presented on the Statement of Assets and Liabilities, when applicable. |

| (7) | Effective date represents the date on which both the Fund and counterparty commence interest payment accruals on each contract. |

| LIBOR | London Inter-Bank Offered Rate |

See accompanying notes to financial statements.

JMLP

| | |

Nuveen All Cap Energy MLP Opportunities Fund | | |

Portfolio of Investments | | November 30, 2017 |

| | | | | | | | | | | | | | | | |

| Shares/Units | | | Description (1) | | | | | | | | Value | |

| | | | |

| | | | LONG-TERM INVESTMENTS – 136.8% (98.9% of Total Investments) | | | | | | | | | | | | |

| | | |

| | | | MASTER LIMITED PARTNERSHIPS & MLP AFFILIATES – 136.8% (98.9% of Total Investments) | | | | | | | | | |

| | | | |

| | | | Energy Equipment & Services – 4.4% (3.2% of Total Investments) | | | | | | | | | |

| | | | |

| | 431,902 | | | Archrock Partners LP | | | | | | | | | | $ | 4,729,327 | |

| | | | |

| | | | Gas Utilities – 3.5% (2.5% of Total Investments) | | | | | | | | | |

| | | | |

| | 84,049 | | | AmeriGas Partners, LP | | | | | | | | | | | 3,772,960 | |

| | | | |

| | | | Oil, Gas & Consumable Fuels – 128.9% (93.2% of Total Investments) | | | | | | | | | |

| | | | |

| | 719,495 | | | American Midstream Partners LP | | | | | | | | | | | 8,597,965 | |

| | 285,129 | | | Crestwood Equity Partners LP | | | | | | | | | | | 6,828,840 | |

| | 343,048 | | | DCP Midstream LP | | | | | | | | | | | 12,054,706 | |

| | 153,650 | | | Delek Logistics Partners LP | | | | | | | | | | | 4,494,263 | |

| | 951,490 | | | Enable Midstream Partners LP | | | | | | | | | | | 14,253,319 | |

| | 319,521 | | | Enbridge Energy Management LLC, (2) | | | | | | | | | | | 4,313,534 | |

| | 368,305 | | | Enbridge Energy Partners LP | | | | | | | | | | | 5,384,619 | |

| | 760,630 | | | EnLink Midstream Partners LP | | | | | | | | | | | 12,162,473 | |

| | 279,685 | | | GasLog Partners LP, (3) | | | | | | | | | | | 6,181,039 | |

| | 176,840 | | | Genesis Energy, LP | | | | | | | | | | | 3,796,755 | |

| | 187,215 | | | Global Partners LP | | | | | | | | | | | 3,257,541 | |

| | 315,640 | | | Golar LNG Partners LP, (3) | | | | | | | | | | | 6,309,644 | |

| | 227,270 | | | Hoegh LNG Partners LP | | | | | | | | | | | 3,977,225 | |

| | 154,535 | | | Holly Energy Partners LP | | | | | | | | | | | 5,116,654 | |

| | 410,190 | | | KNOT Offshore Partners LP, (3) | | | | | | | | | | | 8,285,837 | |

| | 102,170 | | | Martin Midstream Partners LP | | | | | | | | | | | 1,374,187 | |

| | 238,485 | | | Navios Maritime Midstream Partners LP, (3) | | | | | | | | | | | 1,929,344 | |

| | 565,613 | | | NGL Energy Partners LP | | | | | | | | | | | 7,070,163 | |

| | 200,000 | | | Oasis Midstream Partners LP | | | | | | | | | | | 3,624,000 | |

| | 110,525 | | | PBF Logistics LP | | | | | | | | | | | 2,177,343 | |

| | 372,815 | | | Summit Midstream Partners LP | | | | | | | | | | | 7,064,844 | |

| | 28,915 | | | Sunoco LP | | | | | | | | | | | 848,944 | |

| | 102,095 | | | Tallgrass Energy Partners LP | | | | | | | | | | | 4,484,012 | |

| | 52,473 | | | TC PipeLines LP | | | | | | | | | | | 2,666,153 | |

| | 314,902 | | | USD Partners LP | | | | | | | | | | | 3,196,255 | |

| | | | Total Oil, Gas & Consumable Fuels | | | | | | | | | | | 139,449,659 | |

| | | | Total Long-Term Investments (cost $152,881,236) | | | | | | | | | | | 147,951,946 | |

| | | | |

Principal

Amount (000) | | | Description (1) | | Coupon | | | Maturity | | | Value | |

| | | | |

| | | | SHORT-TERM INVESTMENTS – 1.5% (1.1% of Total Investments) | | | | | | | | | | | | |

| | | | |

| | | | REPURCHASE AGREEMENTS – 1.5% (1.1% of Total Investments) | | | | | | | | | |

| | | | |

| $ | 1,611 | | | Repurchase Agreement with Fixed Income Clearing Corporation, dated 11/30/17,

repurchase price $1,610,867, collateralized by $1,665,000 U.S. Treasury Notes,

1.375%, due 1/31/21, value $1,645,408 | | | 0.120% | | | | 12/01/17 | | | $ | 1,610,862 | |

| | | | Total Short-Term Investments (cost $1,610,862) | | | | | | | | | | | 1,610,862 | |

| | | | Total Investments (cost $154,492,098) – 138.3% | | | | | | | | | | | 149,562,808 | |

| | | | Borrowings – (38.4)% (4), (5) | | | | | | | | | | | (41,500,000 | ) |

| | | | Other Assets Less Liabilities – 0.1% (6) | | | | | | | | | | | 65,753 | |

| | | | Net Assets – 100% | | | | | | | | | | $ | 108,128,561 | |

| | | | |

| JMLP | | Nuveen All Cap Energy MLP Opportunities Fund |

| | Portfolio of Investments (continued) | | November 30, 2017 |

Investments in Derivatives as of November 30, 2017

Interest Rate Swaps – OTC Uncleared

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Counterparty | | Notional

Amount | | | Fund

Pay/Receive

Floating Rate | | | Floating Rate Index | | | Fixed Rate

(Annualized) | | | Fixed Rate

Payment

Frequency | | | Effective

Date (7) | | | Optional

Termination

Date | | | Maturity

Date | | | Value | | | Unrealized

Appreciation

(Depreciation) | |

Morgan Stanley Capital Services LLC | | $ | 21,000,000 | | | | Receive | | | | 1-Month LIBOR | | | | 2.042 | % | | | Monthly | | | | 6/01/18 | | | | 7/01/25 | | | | 7/01/27 | | | $ | 141,632 | | | $ | 141,632 | |

For Fund portfolio compliance purposes, the Fund’s industry classifications refer to any one or more of the industry sub-classifications used by one or more widely recognized market indexes or ratings group indexes, and/or as defined by Fund management. This definition may not apply for purposes of this report, which may combine industry sub-classifications into sectors for reporting ease.

| (1) | All percentages shown in the Portfolio of Investments are based on net assets unless otherwise noted. |

| (2) | Payment-in-kind (‘PIK”) security. Depending on the terms of the security, distributions may be received in the form of cash, securities, or a combination of both. |

| (3) | Distribution designated as ordinary income which is recognized as “Dividends” on the Statement of Operations. |

| (4) | Borrowings as a percentage of Total Investments is 27.7%. |

��

| (5) | The Fund segregates 100% of its eligible investments (excluding any investments separately pledged as collateral for specific investments in derivatives, when applicable) in the Portfolio of Investments as collateral for borrowings. As of the end of the reporting period, investments with a value of $95,704,459 have been pledged as collateral for borrowings. |

| (6) | Other assets less liabilities includes the unrealized appreciation (depreciation) of certain over-the-counter (“OTC”) derivatives as presented on the Statement of Assets and Liabilities, when applicable. The unrealized appreciation (depreciation) of OTC cleared and exchange-traded derivatives is recognized as part of the cash collateral at brokers and/or the receivable or payable for variation margin as presented on the Statement of Assets and Liabilities, when applicable. |

| (7) | Effective date represents the date on which both the Fund and counterparty commence interest payment accruals on each contract. |

| LIBOR | London Inter-Bank Offered Rate |

See accompanying notes to financial statements.

| | | | | | |

Statement of Assets and Liabilities | | November 30, 2017 |

| | | | | | | | |

| | | JMF | | | JMLP | |

Assets | | | | | | | | |

Long-term investments, at value (cost $592,023,150 and $152,881,236, respectively) | | $ | 638,479,937 | | | $ | 147,951,946 | |

Short-term investments, at value (cost approximates value) | | | 1,178,422 | | | | 1,610,862 | |

Unrealized appreciation on interest rate swaps | | | 1,130,986 | | | | 141,632 | |

Receivable for shares sold | | | — | | | | 53,202 | |

Deferred offering costs | | | — | | | | 181,085 | |

Other assets | | | 61,771 | | | | 10,141 | |

Total assets | | | 640,851,116 | | | | 149,948,868 | |

Liabilities | | | | | | | | |

Borrowings | | | 175,000,000 | | | | 41,500,000 | |

Cash overdraft | | | 1,686 | | | | 1,633 | |

Payable for: | | | | | | | | |

Interest | | | 308,532 | | | | 57,264 | |

Interest rate swaps purchased | | | 210,079 | | | | — | |

State income tax | | | 258,505 | | | | 8,989 | |

Deferred tax liability, net | | | 26,943,912 | | | | — | |

Accrued expenses: | | | | | | | | |

State franchise tax | | | 41,009 | | | | 6,236 | |

Management fees | | | 528,809 | | | | 130,957 | |

Trustees fees | | | 61,382 | | | | 9,107 | |

Other | | | 345,240 | | | | 106,121 | |

Total Liabilities | | | 203,699,154 | | | | 41,820,307 | |

Net assets | | $ | 437,151,962 | | | $ | 108,128,561 | |

Shares outstanding | | | 40,097,949 | | | | 13,162,721 | |

Net asset value (“NAV”) per share outstanding | | $ | 10.90 | | | $ | 8.21 | |

Net assets consist of: | | | | | | | | |

Shares, $0.01 par value per share | | $ | 400,979 | | | $ | 131,627 | |

Paid-in surplus | | | 386,537,516 | | | | 193,329,754 | |

Accumulated net investment income (loss), net of tax | | | (83,163,451 | ) | | | (9,161,203 | ) |

Accumulated net realized gain (loss), net of tax | | | 58,622,830 | | | | (71,383,959 | ) |

Net unrealized appreciation (depreciation), net of tax | | | 74,754,088 | | | | (4,787,658 | ) |

Net assets | | $ | 437,151,962 | | | $ | 108,128,561 | |

Authorized shares | | | Unlimited | | | | Unlimited | |

See accompanying notes to financial statements.

| | | | | | |

Statement of Operations | | Year Ended November 30, 2017 |

| | | | | | | | |

| | | JMF | | | JMLP | |

Investment Income | | | | | | | | |

Distributions from Master Limited Partnerships (“MLPs”) | | $ | 57,311,108 | | | $ | 12,210,678 | |

Less: Return of capital on distributions from MLPs | | | (57,311,108 | ) | | | (12,210,678 | ) |

Dividends | | | 2,784,123 | | | | 1,870,071 | |

Interest | | | 10,395 | | | | 5,753 | |

Total investment income | | | 2,794,518 | | | | 1,875,824 | |

Expenses | | | | | | | | |

Management fees | | | (7,237,602 | ) | | | (1,730,436 | ) |

Interest expense on borrowings | | | (3,399,419 | ) | | | (747,759 | ) |

Custodian fees | | | (70,736 | ) | | | (23,417 | ) |

Trustees fees | | | (30,225 | ) | | | (7,102 | ) |

Professional fees | | | (121,992 | ) | | | (98,208 | ) |

Shareholder reporting expenses | | | (61,577 | ) | | | (21,673 | ) |

Shareholder servicing agent fees | | | (297 | ) | | | (143 | ) |

Stock exchange listing fees | | | (11,383 | ) | | | (7,042 | ) |

Investor relations expenses | | | (143,256 | ) | | | (41,435 | ) |

Franchise tax expenses | | | (28,675 | ) | | | (26,895 | ) |

Other | | | (67,095 | ) | | | (93,927 | ) |

Total expenses | | | (11,172,257 | ) | | | (2,798,037 | ) |

Net investment income (loss) before taxes | | | (8,377,739 | ) | | | (922,213 | ) |

Deferred tax benefit | | | 3,199,288 | | | | — | |

Current tax (expense)/benefit | | | (80,152 | ) | | | (6,775 | ) |

Net investment income (loss) | | | (5,258,603 | ) | | | (928,988 | ) |

Realized and Unrealized Gain (Loss) | | | | | | | | |

Net realized gain (loss) from: | | | | | | | | |

Investments before taxes | | | 20,321,577 | | | | (11,465,552 | ) |

Swaps before taxes | | | (7,220,235 | ) | | | — | |

Deferred tax (expense)/benefit | | | (5,003,135 | ) | | | — | |

Net realized gain (loss) from investments | | | 8,098,207 | | | | (11,465,552 | ) |

Change in net unrealized appreciation (depreciation) of: | | | | | | | | |

Investments before taxes | | | (88,780,203 | ) | | | 7,700,171 | |

Swaps before taxes | | | 9,413,579 | | | | 141,632 | |

Deferred tax (expense)/benefit | | | 30,308,490 | | | | — | |

Change in net unrealized appreciation (depreciation) of investments | | | (49,058,134 | ) | | | 7,841,803 | |

Net realized and unrealized gain (loss) | | | (40,959,927 | ) | | | (3,623,749 | ) |

Net increase (decrease) in net assets from operations | | $ | (46,218,530 | ) | | $ | (4,552,737 | ) |

See accompanying notes to financial statements.

| | | | | | |

Statement of Changes in Net Assets | | |

| | | | | | | | | | | | | | | | |

| | | JMF | | | JMLP | |

| | | Year

Ended

11/30/17 | | | Year

Ended

11/30/16 | | | Year

Ended

11/30/17 | | | Year

Ended

11/30/16 | |

Operations | | | | | | | | | | | | | | | | |

Net investment income (loss) | | $ | (5,258,603 | ) | | $ | (4,900,707 | ) | | $ | (928,988 | ) | | $ | (587,082 | ) |

Net realized gain (loss) from: | | | | | | | | | | | | | | | | |

Investments | | | 15,318,442 | | | | (53,597,931 | ) | | | (11,465,552 | ) | | | (43,674,877 | ) |

Swaps | | | (7,220,235 | ) | | | — | | | | — | | | | — | |

Change in net unrealized appreciation (depreciation) of: | | | | | | | | | | | | | | | | |

Investments | | | (58,471,713 | ) | | | 111,267,003 | | | | 7,700,171 | | | | 65,167,980 | |

Swaps | | | 9,413,579 | | | | (750,605 | ) | | | 141,632 | | | | — | |

Net increase (decrease) in net assets from operations | | | (46,218,530 | ) | | | 52,017,760 | | | | (4,552,737 | ) | | | 20,906,021 | |

Distributions to Shareholders | | | | | | | | | | | | | | | | |

From net investment income | | | (7,093,871 | ) | | | — | | | | — | | | | — | |

Return of capital | | | (46,224,336 | ) | | | (53,172,869 | ) | | | (12,646,074 | ) | | | (13,115,564 | ) |

Decrease in net assets from distributions to shareholders | | | (53,318,207 | ) | | | (53,172,869 | ) | | | (12,646,074 | ) | | | (13,115,564 | ) |

Fund Share Transactions | | | | | | | | | | | | | | | | |

Proceeds from shelf offering, net of offering costs | | | 4,819,170 | | | | — | | | | 3,479,922 | | | | — | |

Proceeds from shares issued to shareholders due to reinvestment of distributions | | | 1,737,280 | | | | 762,380 | | | | 24,162 | | | | 28,658 | |

Net increase (decrease) in net assets from Fund share transactions | | | 6,556,450 | | | | 762,380 | | | | 3,504,084 | | | | 28,658 | |

Net increase (decrease) in net assets | | | (92,980,287 | ) | | | (392,729 | ) | | | (13,694,727 | ) | | | 7,819,115 | |

Net assets at the beginning of period | | | 530,132,249 | | | | 530,524,978 | | | | 121,823,288 | | | | 114,004,173 | |

Net assets at the end of period | | $ | 437,151,962 | | | $ | 530,132,249 | | | $ | 108,128,561 | | | $ | 121,823,288 | |

Accumulated net investment income (loss), net of tax at the end of period | | $ | (83,163,451 | ) | | $ | (70,810,977 | ) | | $ | (9,161,203 | ) | | $ | (8,232,215 | ) |

See accompanying notes to financial statements.

| | | | | | |

Statement of Cash Flows | | Year Ended November 30, 2017 |

| | | | | | | | |

| | | JMF | | | JMLP | |

Cash Flows from Operating Activities: | | | | | | | | |

Net Increase (Decrease) in Net Assets from Operations | | $ | (46,218,530 | ) | | $ | (4,552,737 | ) |

Adjustments to reconcile the net increase (decrease) in net assets from operations to net cash provided by (used in) operating activities: | | | | | | | | |

Purchases of investments | | | (85,288,273 | ) | | | (44,871,272 | ) |

Proceeds from sales of investments | | | 98,643,395 | | | | 37,871,742 | |

Proceeds from (Purchases of) short-term investments, net | | | (467,756 | ) | | | 2,566,560 | |

Proceeds from (Payments for) swap contracts, net | | | (7,220,235 | ) | | | — | |

Premiums received (paid) for interest rate swaps | | | 2,996,828 | | | | — | |

Return of capital distributions from MLPs | | | 57,311,108 | | | | 12,210,678 | |

(Increase) Decrease in: | | | | | | | | |

Receivable for income tax refund | | | — | | | | 18,189 | |

Receivable for investments sold | | | 5,008,045 | | | | 6,869,003 | |

Other assets | | | (12,518 | ) | | | (2,996 | ) |

Increase (Decrease) in: | | | | | | | | |

Deferred tax liability, net | | | (28,504,644 | ) | | | — | |

Payable for interest | | | 105,716 | | | | 16,260 | |

Payable for interest rate swaps purchased | | | 210,079 | | | | — | |

Payable for federal income tax | | | (465,450 | ) | | | — | |

Payable for state income tax | | | (3,993 | ) | | | 1,023 | |

Accrued state franchise tax expense | | | (9,171 | ) | | | (8,527 | ) |

Accrued management fees | | | (74,203 | ) | | | (5,321 | ) |

Accrued Trustees fees | | | 6,417 | | | | 1,138 | |

Accrued other expenses | | | 37,636 | | | | 7,854 | |

Net realized (gain) loss from: | | | | | | | | |

Investments before taxes | | | (20,321,577 | ) | | | 11,465,552 | |

Swaps before taxes | | | 7,220,235 | | | | — | |

Change in net unrealized appreciation (depreciation) of: | | | | | | | | |

Investments before taxes | | | 88,780,203 | | | | (7,700,171 | ) |

Swaps before taxes | | | (9,413,579 | ) | | | (141,632 | ) |

Net cash provided by (used in) operating activities | | | 62,319,733 | | | | 13,745,343 | |

Cash Flows from Financing Activities | | | | | | | | |

Proceeds from borrowings | | | 6,450,000 | | | | 6,000,000 | |

Repayments of borrowings | | | (17,000,000 | ) | | | (3,500,000 | ) |

Proceeds from shelf offering, net of offering costs | | | 4,819,170 | | | | 3,426,720 | |

Increase (Decrease) in cash overdraft | | | (5,007,976 | ) | | | (6,869,066 | ) |

Cash distributions paid to shareholders | | | (51,580,927 | ) | | | (12,621,912 | ) |

(Payments for) deferred offering costs | | | — | | | | (181,085 | ) |

Net cash provided by (used in) financing activities | | | (62,319,733 | ) | | | (13,745,343 | ) |

Net Increase (Decrease) in Cash | | | — | | | | — | |

Cash at the beginning of period | | | — | | | | — | |

Cash at the end of period | | $ | — | | | $ | — | |

| | |

| Supplemental Disclosures of Cash Flow Information | | JMF | | | JMLP | |

Cash paid for interest on borrowings (excluding borrowing costs) | | $ | 3,293,703 | | | $ | 731,499 | |

Net cash paid (received) for taxes | | | 595,829 | | | | 40,682 | |

See accompanying notes to financial statements.

THIS PAGE INTENTIONALLY LEFT BLANK

Financial

Highlights

Selected data for a share outstanding throughout each period:

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | |

| | | | | | Investment Operations | | | Less Distributions | | | | | | | | | | | | | |

| | | Beginning

NAV | | | Net

Investment

Income

(Loss)(a) | | | Net

Realized/

Unrealized

Gain (Loss) | | | Total | | | From

Net

Investment

Income | | | Return

of

Capital | | | Total | | | Offering

Costs | | | Premium

from

Shares

Sold

through

Shelf

Offering | | | Ending

NAV | | | Ending

Share

Price | |

|

JMF | |

Year Ended 11/30: | |

2017 | | $ | 13.42 | | | $ | (0.13 | ) | | $ | (1.04 | ) | | $ | (1.17 | ) | | $ | (0.18 | ) | | $ | (1.17 | ) | | $ | (1.35 | ) | | $ | — | | | $ | — | ** | | $ | 10.90 | | | $ | 10.57 | |

2016 | | | 13.45 | | | | (0.12 | ) | | | 1.44 | | | | 1.32 | | | | — | | | | (1.35 | ) | | | (1.35 | ) | | | — | | | | — | | | | 13.42 | | | | 13.32 | |

2015 | | | 22.10 | | | | (0.08 | ) | | | (7.23 | ) | | | (7.31 | ) | | | — | | | | (1.34 | ) | | | (1.34 | ) | | | — | | | | — | | | | 13.45 | | | | 11.91 | |

2014 | | | 20.22 | | | | (0.32 | ) | | | 3.48 | | | | 3.16 | | | | (0.12 | ) | | | (1.16 | ) | | | (1.28 | ) | | | — | | | | — | | | | 22.10 | | | | 20.72 | |

2013 | | | 17.73 | | | | (0.29 | ) | | | 4.04 | | | | 3.75 | | | | (1.14 | ) | | | (0.12 | ) | | | (1.26 | ) | | | — | | | | — | | | | 20.22 | | | | 19.40 | |

|

JMLP | |

Year Ended 11/30: | |

2017 | | | 9.55 | | | | (0.07 | ) | | | (0.29 | ) | | | (0.36 | ) | | | — | | | | (0.98 | ) | | | (0.98 | ) | | | — | | | | — | ** | | | 8.21 | | | | 8.02 | |

2016 | | | 8.94 | | | | (0.05 | ) | | | 1.69 | | | | 1.64 | | | | — | | | | (1.03 | ) | | | (1.03 | ) | | | — | | | | — | | | | 9.55 | | | | 9.80 | |

2015 | | | 18.52 | | | | (0.12 | ) | | | (8.09 | ) | | | (8.21 | ) | | | — | | | | (1.37 | ) | | | (1.37 | ) | | | — | | | | — | | | | 8.94 | | | | 8.35 | |

2014(g) | | | 19.10 | | | | (0.27 | ) | | | 0.73 | | | | 0.46 | | | | (0.21 | ) | | | (0.79 | ) | | | (1.00 | ) | | | (0.04 | ) | | | — | | | | 18.52 | | | | 16.35 | |

| | | | | | | | |

| | | Borrowings at the End of Period | |

| | | Aggregate

Amount

Outstanding

(000) | | | Asset

Coverage

Per $1,000 | |

|

JMF | |

Year Ended 11/30: | |

2017 | | $ | 175,000 | | | $ | 3,498 | |

2016 | | | 185,550 | | | | 3,857 | |

2015 | | | 199,000 | | | | 3,666 | |

2014 | | | 315,000 | | | | 3,768 | |

2013 | | | 283,000 | | | | 3,818 | |

|

JMLP | |

Year Ended 11/30: | |

2017 | | | 41,500 | | | | 3,606 | |

2016 | | | 39,000 | | | | 4,124 | |

2015 | | | 41,800 | | | | 3,727 | |

2014(g) | | | 85,000 | | | | 3,780 | |

| (a) | Per share Net Investment Income (Loss) is calculated using the average daily shares method. |

| (b) | Total Return Based on NAV is the combination of changes in NAV, reinvested dividend income at NAV and reinvested capital gains distributions at NAV, if any. The last dividend declared in the period, which is typically paid on the first business day of the following month, is assumed to be reinvested at the ending NAV. The actual reinvest price for the last dividend declared in the period may often be based on the Fund’s market price (and not its NAV), and therefore may be different from the price used in the calculation. Total returns are not annualized. |

Total Return Based on Share Price is the combination of changes in the market price per share and the effect of reinvested dividend income and reinvested capital gains distributions, if any, at the average price paid per share at the time of reinvestment. The last dividend declared in the period, which is typically paid on the first business day of the following month, is assumed to be reinvested at the ending market price. The actual reinvestment for the last dividend declared in the period may take place over several days, and in some instances may not be based on the market price, so the actual reinvestment price may be different from the price used in the calculation. Total returns are not annualized.

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | Ratios/Supplemental Data | |

| Total Returns | | | | | | Ratios to Average Net Assets

Before Reimbursement/

Income Taxes/

Tax Benefit (Expense)(e) | | | Ratios to Average Net Assets

After Reimbursement/

Income Taxes/

Tax Benefit (Expense)(d)(e) | | | Ratios

to Average

Net Assets | | | | |

| | | | | | | | |

Based

on

NAV(b) | | | Based

on

Share

Price(b) | | | Ending

Net

Assets

(000) | | | Expenses | | | Net

Investment

Income (Loss) | | | Expenses | | | Net

Investment

Income (Loss) | | | Current and

Deferred Tax

Benefit

(Expense) | | | Portfolio

Turnover

Rate(f) | |

| | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | (9.44 | )% | | | (11.44 | )% | | $ | 437,152 | | | | (2.23 | )% | | | (1.67 | )% | | | 3.45 | % | | | (1.05 | )% | | | 5.68 | % | | | 12 | % |

| | 12.27 | | | | 27.51 | | | | 530,132 | | | | (1.99 | ) | | | (1.46 | ) | | | (8.10 | ) | | | (1.05 | ) | | | (6.11 | ) | | | 28 | |

| | (34.43 | ) | | | (37.51 | ) | | | 530,525 | | | | (1.95 | ) | | | (0.68 | ) | | | 22.29 | (c) | | | (0.42 | )(c) | | | 24.23 | | | | 18 | |

| | 15.67 | | | | 13.67 | | | | 871,905 | | | | (1.84 | ) | | | (1.45 | ) | | | (10.38 | ) | | | (1.47 | ) | | | (8.54 | ) | | | 6 | |

| | 21.51 | | | | 13.20 | | | | 797,625 | | | | (1.98 | ) | | | (1.97 | ) | | | (13.22 | ) | | | (1.48 | ) | | | (11.25 | ) | | | 39 | |

| | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | (4.22 | ) | | | (8.91 | ) | | | 108,129 | | | | (2.32 | ) | | | (0.76 | ) | | | (2.33 | ) | | | (0.77 | ) | | | (0.01 | ) | | | 24 | |

| | 22.62 | | | | 34.48 | | | | 121,823 | | | | (2.15 | ) | | | (0.59 | ) | | | (2.14 | ) | | | (0.58 | ) | | | 0.01 | | | | 37 | |

| | (46.47 | ) | | | (43.24 | ) | | | 114,004 | | | | (2.02 | ) | | | (1.42 | ) | | | (0.16 | ) | | | (0.85 | ) | | | 1.86 | | | | 37 | |